Chapter-IV Role of Banks, NGO's & MFI in Promoting...

55

13 Chapter-IV Role of Banks, NGO's & MFI in Promoting Micro-finance

Transcript of Chapter-IV Role of Banks, NGO's & MFI in Promoting...

13

Chapter-IV

Role of Banks, NGO's & MFI in Promoting

Micro-finance

CHAPTER-IV

ROLE OF BANKS, NGO'S & MFI IN

PROMOTING MICRO-FINANCE

Non- Government Organization have been part of the historical legacy.

In the context of contemporary social empowerment, self realization and self

initiative it is the base for the formation of self help groups. This logic

motivated NGOs to form SHGs in rural areas to empower them through

developing their inherent skills. Thus, SHG movement among the rural poor

in different parts of the country is emerging as a very reliable and efficient

mode for technology transfer. Chanakya's philosophies statement has

transformed into the SHGs with the help of NGOs and their efforts.

Microfinance is the tool to empower the rural poor and also a tool against

human deprivation. Microfinance is motivating sustainable development

through the support of NGOs.

As a responsible welfare state in the democratic systems, it can be said

that the growth of micro-finance in India has been in response to involvement

of informal credit system, rural credits especially rural cooperatives. This led

to the establishment of microfinance institutions under the guidelines of

NABARD.

Microfinance institutions are highly encouraging. Microfinance

through SHG has become a ladder for the poor to bring them up not only

economically but also socially, mentally and attitudinally. Initially, the SHGs

and microfinance, as an instrument for social and economic empowerment,

are established by the nongovernmental organizations. In the era of 21st

century, NGOs are transforming from non-profit to profit making business

model NGOs. Especially, the success formula of microfinance non profit

model is learned from the PRODEM - Bolivia and Grameen Bank -

Bangladesh. It is proved that committed social development NGOs can

Role of Banks, NGO's & MFI in Promoting Micro-finance 144

develop the society by providing finance accessibility to the poor based on

self help model. Many NGOs (non-government organizations) in India came

forward to promote micro finance. At present more than 1800 NGOs are

implementing micro-finance projects in India.

Some of them are leading MFIs (micro-finance institutions) playing

the role of social intermediation and building better society in rural areas.

These MFIs have adopted different strategies of people's livelihood through

micro-finance delivery.

4.1 Microfinance Institutions

The following are the some of leading microfinance institutions in

India working in the sector for promoting better and sustainable livelihood for

the poor.

Association for Sarva Seva Farms (ASSEFA)

Mitrabharati - The Indian microfinance Information Hub Mysore

Resettlement and Development Agency (MYRADA)

SADHAN - The Association of Community Development Finance

Institutions

SEWA: Self Help Women's Association

SKS India - Swayam Krishi Sangam

Streedhan - Banking with Rural Women

Working Women's Forum, Madras, India

These MFI's are working towards eradication of poverty & hunger,

achieving education universally, promoting Gender equality and women's

empowerment, reducing child mortality, combat diseases and developing

entrepreneurial spirit etc.

Between the 1950s and 1970s, governments and donors focused on

providing agricultural credit to small and marginal farmers, in hopes of

Role of Banks, NGO's & MFI in Promoting Micro-finance 145

raising productivity and incomes. These efforts to expand access to

agricultural credit emphasized supply-led government interventions in the

form of targeted credit through state-owned development finance institutions,

or farmers' cooperatives in some cases, that received concessional loans and

on-lent to customers at below-market interest rates. These subsidized schemes

were rarely successful. Rural development banks suffered massive erosion of

their capital base due to subsidized lending rates and poor repayment

discipline and the funds did not always reach the poor, often ending up

concentrated in the hands of better-off farmers.

Meanwhile, starting in the 1970s, experimental programs in

Bangladesh, Brazil, and a few other countries extended tiny loans to groups of

poor women to invest in micro-businesses. This type of micro enterprise

credit was based on solidarity group lending in which every member of a

group guaranteed the repayment of all members. These "micro enterprise

lending" programs had an almost exclusive focus on credit for income

generating activities (in some cases accompanied by forced savings schemes)

targeting very poor (often women) borrowers.

ACCOIN International, it is a Latin America's one of the prime

microfinance institution working with the poor. In an early pioneer,

ACCION was founded by a law student, Joseph Blatchford, to address

poverty in Latin America's cities. Begun as a student-run volunteer

effort in the shantytowns of Caracas with $90,000 raised from private

companies, ACCION today is one of the premier microfinance

organizations in the world, with a network of lending partners that

spans Latin America, the United States and Africa.

SEWA Bank. In 1972 the Self Employed Women's Association

(SEWA) was registered as a trade union in Gujarat (India), with the

main objective of "strengthening its members' bargaining power to

improve income, employment and access to social security." In 1973,

Role of Banks, NGO's & MFI in Promoting Micro-finance 146

to address their lack of access to financial services, the members of

SEWA decided to found "a bank of their own". Four thousand women

contributed share capital to establish the Mahila SEWA Co-operative

Bank. Since then it has been providing banking services to poor,

illiterate, self-employed women and has become a viable financial

venture with today around 30,000 active clients.

Grameen Bank. In Bangladesh, Professor Muhammad Yunus

addressed the banking problem faced by the poor through a programme

of action-research. With his graduate students in Chittagong University

in 1976, he designed an experimental credit programme to serve them.

It spread rapidly to hundreds of villages. Through a special relationship

with rural banks, he disbursed and recovered thousands of loans, but

the bakers refused to take over the project at the end of the pilot phase.

They feared it was too expensive and risky in spite of his success.

Eventually, through the support of donors, the Grameen Bank was

founded in 1983 and now serves more than 4 million borrowers. The

initial success of Grameen Bank also stimulated the establishment of

several other giant microfinance institutions like BRAC, ASA,

Proshika, etc.

Through the 1980s, the policy of targeted, subsidized rural credit came

under a slow but increasing attack as evidence mounted of the disappointing

performance of directed credit programs, especially poor loan recovery, high

administrative costs, agricultural development bank insolvency, and accrual

of a disproportionate share of the benefits of subsidized credit to larger

farmers.

The basic theme underlying the traditional direct credit approach were

debunked and supplanted by a new school of thought called the "financial

systems approach", which viewed credit not as a productive input necessary

Role of Banks, NGO's & MFI in Promoting Micro-finance 147

for agricultural development but as just one type of financial service that should

be freely priced to guarantee its permanent supply and eliminate rationing. The

financial systems school held that the emphasis on interest rate ceilings and

credit subsidies retarded the development of financial intermediaries,

discouraged intermediation between savers and investors, and benefited larger

scale producers more than small scale and low-income producers.

Micro Credit and Microfinance are closely related terms. Poor people

need micro credit for various and different purposes. It may be to meet the

major household expenses; emergency needs or even basic livelihood support.

There are two main systems of micro credit. One is formal financial

institutions, banks and co-operatives, which provide micro-credit to the poor

people under different schemes for livelihood support or helping them to start

micro-enterprises. The other is informal system comprising traditional

moneylenders, pawnbrokers and trade specific lenders. Both the systems have

their own positive and negative aspects. Micro-Finance, as is being practiced

by the National Credit fund for Women or the Rashtriya Mahila Kosh (RMK),

could be defined as a set of services comprising the following activates:

Micro-credit:

Here, the following activities can be activated such as Small loans;

primarily for income generation activities, but also for consumption and

contingency needs.

Micro-savings:

SHGs micro savings are called as thrift. The thrift is the basic element

for the success of microfinance. Thrift or small savings are from borrowers'

own resources.

Role of Banks, NGO's & MFI in Promoting Micro-finance 148

The main features of the micro-finance

1. It is a tool for empowerment of the poorest women.

2. It is essentially for promoting self-employment; the opportunities of

wage employment are limited in developing countries - micro finance

increases the productivity of self-employment is the informal sector of

the economy - generally used for (a) direct income generation (b)

rearrangement of assets and liabilities for the household to participate

in future opportunities and (c) consumption smoothing.

3. It is not just a financing system, but a tool for social change, specially

for women.

4. Micro credit is aimed at the poorest; micro-finance lending technology

needs to mimic lenders rather than the formal sector lending.

It has to provide for seasonality, allow repayment flexibility, eschew

bureaucratic and legal formalities and also fox a ceiling on loan sizes.

The positive aspects of formal financial system are that under this

system, micro-credit is available at low rate of interest with easy and

periodical repayments and moratorium period. The most important aspect of

this type of credit is that it is available for income generating activities. But at

the same time micro-credit from formal financial system is not easily

available. The system requires collateral or security. It has complex legal and

operational procedures, involving lot of paper work. Since the process of

credit disbursement is time consuming, many times credit is not available

when required. Finally, there is stigma attached to the poor people so that the

bankers do not think them credit-worthy and fell that the recovery rate is

unsatisfactory. But this may not necessarily be always true.

The positive aspects of informal system of micro-credit are that the

credit disbursement is easy and relatively quick. No collateral is required and

there is least paper work. Credit can be given for any activity, especially for

Role of Banks, NGO's & MFI in Promoting Micro-finance 149

consumption and emergency purposes. Credit is generally given for non-

productive purposes as well. But at the same time there is very high interest

rate in informal micro-credit system. Exploitation is also attached with this

system. Moneylender takes repayment at one time only. Based on these two

systems of micro-credit, we can define "micro-credit as the provision wherein

debtor takes money either from formal or informal sources of credit on

unilaterally decided terms by the creditor". If we combine together positive

aspects of both the systems like, low rate of interest, easy and periodical

repayments with moratorium period, credit for income generating activities,

easy process of disbursement, no collateral or security and less paper work

etc., we come closer to understanding the concept of micro-finance. The 'Task

Force on Supportive Policy and Regulatory Framework for Micro-finance'

constituted by NABARD definers "micro-finance as the provision of thrift,

saving, credit and financial services and products of very small amounts to the

poor in rural, semi-urban and urban areas for enabling them to raise their

income levels and improve their standard of living".

The emergence of microfinance's prime objective is to bridge the gap

between demand and supply of funds in the lower rungs of the rural economy,

the formal sector took the initiative to develop a supplementary credit

delivery mechanism by encouraging institutional arrangements outside the

financial system with the launching of NABARD's pilot scheme, microfinance

to cure the illness of rural poverty gained visibility on the India development

landscape.

Services of micro-finance are being provided by various MFIs. In

India, the Task Force mentioned above, has classified these MFIs under the

following categories as below: Not-for-Profit MFIs: These include Societies

registered under Societies Registration Act 1860 or similar State Acts, Public

Trusts registered under the Indian Trust Act 1882 and Non-Profit Companies

Role of Banks, NGO's & MFI in Promoting Micro-finance 150

registered under Section 25 of the Companies Act 1956. Mutual Benefit

MFIs: Such as State Credit Co-operative, National Credit Co-operatives and

Mutually Aided Co-operative Societies (MACS). For-Profit MFIs: Bodies

like Non-Banking Financial Companies (NBFCs) registered under the

Companies Act 1956 and Banks which provide micro finance along with their

other usual banking services could be termed as micro-finance service

providers of this type.

4.2 Some recent examples and innovations in the world's financial

services for the poor are listed as below

1. CCACN (Central de Cooperatives de Ahorroy Credito Financiers

de Nicaragua) is marketing its "Agriculture Salary" savings

product to farmers. The goal of the product is to smoothen the flow

of income from the proceeds of an annual or semi-annual harvest. Each

credit union works with its farmers to identify their individual

expenses and determine a monthly "salary" (portion of harvest

proceeds on deposit combined with an above-market interest rate) to be

withdrawn from the credit union. In its infancy stage, the credit unions

have noted an interest from agriculture-based clients in such a savings

management program.

2. Caja los Andes in Bolivia offers four loan repayment options that fit

the cash flow of various agricultural activities, including an end-of-

term payment for both principal and interest that fits single crop

activities, and unequal payments at irregular intervals for farmers that

have planted several crops with different harvesting periods. Flexibility

is also provided in loan disbursements, and farmers can receive the

sanctioned loan amount in as many as three instalments.

3. PRODEM in Bolivia has introduced a combination of biometric

fingerprint and Smart Cards to deliver financial services to its clients

Role of Banks, NGO's & MFI in Promoting Micro-finance 151

Biometric technology measures an individual's unique physical or

behavioural characteristics, such as fingerprints, facial characteristics,

voice pattern, and gait, to recognize and confirm identity. Although the

technology is still new, growing awareness of the importance of data

security is increasing adoption steadily. Prodem's fingerprint

verification has reduced fraud, error, and repudiation of transactions.

Staff had not had to deal with forgotten PIN numbers or unauthorized

use of cards and accounts so they have more time to provide personal

service and advice to clients.

4. International Remittance Network (IRnet): In late 1999, WOCCU,

in partnership with Vigo, a money transfer firm, launched IRnet. As of

June 2003, 173 credit unions in Central America offer IRnet,

expanding the possibilities for sending remittances through 800 US

credit union points of service. The Central American credit unions

distribute remittances primarily to rural clients. The distributing credit

unions help to integrate remittance recipients into the formal financial

sector through trained stall who cross-sell services. When a non-

Member enters a credit union to pick up a remittance, a staff person

encourages this person to become a credit union member and save a

portion of the remittance in an interest-bearing voluntary savings

account.

5. Unibanka (Latvia): Prior to introducing credit scoring, Unibanka, a

commercial bank, viewed microfinance loans as too costly to deliver.

With the assistance of Bannock Consulting, Unibanka instituted a

credit-scoring system based on qualitative client data because

sufficient quantitative was not available to develop a statistical model.

6. Managed ASCAs: A number of local organisations in the Nyeri

District of Kenya provide management services to group-based loan

funds. The groups operate as Accumulating Savings and Credit

Role of Banks, NGO's & MFI in Promoting Micro-finance 152

Associations (ASCAs) and receive management services provided by

ASCA Management Agencies (AMAs). The AMA model serves a

wider client base than the mainstream donor funded MFIs who tend to

focus their attention on micro and small entrepreneurs. The clientele of

AMAs are also drawn from other socio-economic strata, including

salaried workers such as nurses, teachers and civil servants as well as

subsistence and semi-commercial farmers. Hence their reach into the

rural areas is much greater than the MFIs.

7. ICICI Bank (India): Two banks in India (Cooperation and Canara)

partnered with an NGO to provide salaried low-income workers with

access to savings. The project uses the already established automatic

teller machines (ATMs) in the factories to offer a recurring savings

product, along with education on personal finance.

8. Microenterprise Access to Banking Services (MABS) in the

Philippines nurtures the expanded use of the credit bureau by rural

banks, which was started in 2001 to minimize client over indebtedness

and defaults. MABS has helped to integrate the rural banks'

microenterprise loan clients into an existing national credit bureau, by

creating an e-mail encryption program that allows rural banks to share

information electronically at a low cost.

9. The National Microfinance Bank in Tanzania (NMB) was created to

retain the extensive rural branch network of the National Bank of

Commerce (NBC) when it was privatized in 1997. The key to making it

commercially viable has been rigorous control of costs through drastic

simplification of the business model and tight managerial oversight. Key

initiatives have been correct pricing of products, particularly payments

and remittance services, which had traditionally been cross-subsidized

by other product lines, and the development of microfinance products,

mainly small (average US $400) individual loans.

Role of Banks, NGO's & MFI in Promoting Micro-finance 153

10. ADOPEM (Dominican Republic) thoroughly evaluated its PDA

(Personal Digital Assistants) program and recorded dramatic

improvements. Client retention improved significantly, and the number

of days between application and disbursement dropped from five days

to two days. Expenses for paperwork dropped by 60% and data entry

expenses dropped by 50%.

11. The international NGO Techno serve has developed an inventory

credit scheme in Ghana that enables farmers' groups to obtain higher

value for their crops by providing post-harvest credit through linkage

with a rural financial institution. Instead of selling their entire crop at

harvest - when prices are lowest - in order to meet cash needs, small-

sale farmers in the scheme store their crop in a cooperatively managed

warehouse and receive a loan of about 75-80% of the value of the

stored crop, which serve as collateral. This loan permits them to clear

their accumulated debts and satisfy immediate cash requirements.

Then, when prices have risen in the off-season, the farmers either sell

the stored crop or redeem it for home consumption.

12. Savings-based, Agriculture-oriented Rural Credit Unions-

SICREDI- Brazil specialized in agricultural lending, primarily for the

production of rice, wheat, beef, fodder, fish, vegetables and for

agricultural equipment. Loan approvals are based upon the members'

savings history and credit record, with the size limited to 50 percent of

production costs and dependent upon the potential return of crop sale

at harvest as well as household income and debt obligations. The

borrower makes monthly interest payments and then a balloon

payment of the principal at harvest time. In addition, SICREDI

participates in the PROAGRO national crop insurance, for which a

premium is added on the loan rate. PROAGRO pays 100% of the loan

loss if the crop fails.

Role of Banks, NGO's & MFI in Promoting Micro-finance 154

13. Producer Associations as Clients of a Financial Institution: GAPI

and CLUSA in Mozambique: GAPI offers investment and working

capital loans to fora (federations of associations) of small farmers and

small and micro-enterprises. Loans are secured through a solidarity

group-like guarantee between the participating fora. Each forum on-

lends to its member associations, who collect the produce from their

individual members and other area farmers and deliver it to the forum

in return for the loan. About 80% of the profits from the sale of

produce are handed back to the associations - the remaining 20% of the

profits are kept by the forum as interest payments.

14. Equity Building Society (EBS) in Kenya has emerged as one of

Kenya's leading microfinance institutions, with over 155,000 savings

clients and 41,000 borrowers. Once insolvent, EBS transformed itself

into a profitable financial-service provider by rigorously focusing on

the needs of its clients - in particular, by developing a wide range of

market-based financial products and services, including a mobile

banking service.

The above mentioned experiences shows that effective functioning

with focus group oriented will success in the area of microfinance. At the

global microfinance scenario, most of the institutions are providing loans for

the purpose of agriculture and allied services, micro enterprises and other

rural based micro economic activities.

4.3 Role of Banks and MFI's in the Growth of Micro-Finance Sector

at Global Level

Looking at the historical account of the emergence and growth of

micro finance sector at the global level, the Grameen Bank, Bangladesh, was

started as an experiment in 1976 and accorded a special banking charter in

1983. In 1981 NDF (National Development Foundation), Jamaica, was started

Role of Banks, NGO's & MFI in Promoting Micro-finance 155

with support of Pan American Development Foundation. In 1983 ADEMI

(Association for Development of Micro Enterprises) was established in

Dominican Republic, Santo Domingo with support from ACCION, an

International Agency. In 1984 BRI (Bank Rakayat Indonesia) started micro-

finance in Indonesia. In 1984, K-REP (Kenta Rural Enterprise Programme)

was set up by USAID (United states Agency for International Development)

to develop credit programmes for micro-enterprises through NGOs

intermediation. In 1986 ACEP (Agency de Credit Pour 'L Enterprise Privee)

was established in Senegal with the support of USAID.

In 1986, PRODEM (Foundation for the Promotion and Development

of Micro Enterprises) which was established by USAID and ACCION

International in Bolivia, started micro finance. Later on it was converted into

a bank called Bancosol (Banco Solidario) ion 1992. In 1987 IDH (Instituto de

Desarrollo Hondurando) was started in Honduras with the support of

Opportunity International. In 1992, BANPECO (Banco Nacional del Pequeno

Comercio) that is, National Bank for Small Traders was renamed as BNCI

(Banco Nacional de Comercio Interior), that is National Bank for Domestic

Commerce and started micro-financing in urban areas of Mexico. micro-

Credit Summit (2-4 February, 1997) held at Washington D.C. was organized

to launch a global movement to reach 100 million of the world's poorest

families, especially the women of those families, with credit for self-

employment, by the year 2005.

Mean while the micro credit programs throughout the world improved

upon the original methodologies and defied conventional wisdom about

women, had excellent repayment rates among the better programs, rates that

were better than the formal financial sectors of most developing countries.

Second, the poor were willing and able to pay interest rates that allowed

microfinance institutions (MFIs) to cover their costs. 1990s These two

Role of Banks, NGO's & MFI in Promoting Micro-finance 156

features - high repayment and cost-recovery interest rates - permitted some

MFIs to achieve long-term sustainability and reach large numbers of clients.

Another flagship to the microfinance movement is the village banking

unit system of the bank Rakyat Indonesia (BRI), which is the largest

microfinance institution in developing countries. This state-owned bank

serves about 22 million micro savers with autonomously managed micro

banks. The micro banks of BRI are the product of a successful transformation

by the state of a state-owned agricultural bank during the mid-1980s.

The 1990s saw growing enthusiasm for promoting microfinance as a

strategy for poverty alleviation. The microfinance sector blossomed in many

countries, leading to multiple financial services firms serving the needs of

micro entrepreneurs and poor households. These gains, however, tended to

concentrate in urban and densely populated rural areas.

It was not until the mid- 1990s that the term "micro-credit" began to be

replaced by a new term that included not only credit, but also savings and

other financial services. "Microfinance" emerged as the term of choice to

refer to a range of financial services to the poor, that included not only credit,

but also savings and other services such as insurance and money transfers.

Today, practitioners and donors are increasingly focusing on expanded

financial services to the poor in frontier markets and on the integration of

microfinance in financial systems development. The recent introduction by

some donors of the financial systems approach in microfinance - which

emphasizes favourable policy environment and institution-building - has

improved the overall effectiveness of microfinance interventions. But

numerous challenges remain, especially in rural and agricultural finance and

other frontier markets.

Role of Banks, NGO's & MFI in Promoting Micro-finance 157

Today, the microfinance industry and the international community

share the view that permanent poverty reduction requires addressing the

multiple dimensions of poverty. For the international community, this means

reaching specific Millennium Development Goals (MDGs) in education,

women's empowerment, and health, among others. For microfinance, this

means viewing microfinance as an essential element in any country's financial

system.

4.4 Non-Institutional or Informal Sources of Micro-Credit in India

One can easily conclude that RFIs do not fulfill the credit needs of the

farmers, rural producers and the rural poor in general, resulting in non-

institutional sources of credit. The indirect reason responsible for the growth

of non-institutional sources of credit was also the economic weakness of the

Jajmani System. The non-institutional sources of credit would include big

farmers, big farmer-cum-money-lenders, commission agents, friends/ relatives,

moneylenders, traders, village shopkeepers and others. The All India Rural

Credit Survey Committee, appointed by the RBI in 1951 under the

chairmanship of Gorwala, under took a comprehensive survey of rural credit

and submitted its report in August 1954. The survey revealed that shares of

institutional and non-institutional sources of rural credit were 7.3 per cent and

92.7 per cent respectively.

At present about two-third of the credit need in rural areas is met out

by informal sources. But the moneylenders have yet to disappear. Though

they charge very high rate of interest, varied between 36 per cent to 50 per

cent per annum. There is also need to sensitize the issue of informal rural

banks that they provide timely and adequate credit to the rural poor without

much paperwork and for any purpose, especially for meeting consumption

and other social needs. But physical, economic and social exploitation of the

poor people is attached with this system.

Role of Banks, NGO's & MFI in Promoting Micro-finance 158

Micro finance chronology can be evaluated by the following steps briefly:

Microfinance has been in practice for ages (though informally).

Legal framework for establishing the co-operative movement set up in

1904.

Reserve Bank of India Act, 1934 provided for the establishment of the

Agricultural Credit Department.

Nationalisation of banks in 1969.

Regional Rural Banks created in 1975.

NABARD established as an apex agency for rural finance in 1982.

Passing of Mutually Aided Co-operative Act in AP in 1995.

The Profit of Microfinance in India: The profit of micro finance in India at

present can be traced out in terms of poverty, it is estimated that 350 million

people live Below Poverty Line and this translates to approximately 75

million households with annual credit demand by the poor in the country is

estimated to be about Rs. 60,000 crores.

The following are some of important components of microfinance:

Only about 5% of rural poor have access to microfinance.

While 10% lending to weaker sections is required for commercial

banks, they neither have the network for lending and supervision on a

large scale nor the confidence to offer term loans to big MFIs.

The non poor comprise of 29% of the outreach.

The Status of Microfinance

Considerable gap between demand and supply for all financial services

Majority of poor are excluded from financial services. This is due to,

inter-alia, the following reasons

1) Bankers feel that it is fraught with risks and uncertainties.

2) High transaction costs

Role of Banks, NGO's & MFI in Promoting Micro-finance 159

3) Unfavourable policies like caps on interest rates which

effectively limits the viability of serving the poor.

While MFIs have shown that serving the poor is not an unviable

proposition there are issues that have constrained MFIs while scaling

up. These include

1) Lack of an appropriate legal vehicle

2) Limited access to equity

3) Difficulty in accessing low cost on-lending funds (as of now

they are unable to offer savings services in a legitimate manner.)

4) Limited access to Capacity Building support which is an

important variable in terms of quality of the portfolio, MIS, and

the sustainability of operations.

About 56% of the poor still borrow from informal sources.

70% of the rural poor do not have a deposit account

87% have no access to credit from formal sources.

Less than 15% of the households have any kind of insurance.

Negligible numbers have access to health insurance (0.4%) and crop

insurance (0.2%).

NABARD's bank linkage program has cumulatively reached a total of

9.4 lakh SHGs with about 1.4 crore households.

Related Issues

Designing financially sustainable models

Aim for community participation & ownership

Increase outreach and scale up operations

Demonstrate that banking with the poor is viable

Build professional systems and processes.

Ensure transparency and enhance credibility through disclosures.

Provide support for capacity building initiatives.

Role of Banks, NGO's & MFI in Promoting Micro-finance 160

4.5 Opportunities for Micro-Finance Sector in India

Keeping in view of above mentioned issues relating to how and why

the rural informal credit system is strengthened, NGOs are required to

sensitize the state institutions and NGOs itself has to take initiatives for the

rural banking in micro rural credit system. Moreover, rural population is a

major population segment in India.

According to the 2001 Census of India 72.22 percent of the total

population is rural and dependent on agriculture and allied activities for their

livelihood. Due to the failure of agricultural reforms and not adopting a

farmer-oriented agricultural policy, growth rate of employment in agriculture

sector has declined from 2.32 per cent in 1972-73 to 1.2 per cent in 1983 to

0.65 per cent in 1985. Agriculture contributed only 31.7 percent to GDP in

1993-94 down from 56.5 per cent in 1951. But this is not the complete picture

of the rural economy. The rural economy has a strong base for employment

generation.

Rural economy still accounts nearly 40 per cent of India's GDP

including 10 per cent of RNFS. Share of exports in GDP has increased from

6.2 per cent in 1991-92 to 9.2 per cent in 1994-95. Major contribution to

exports comes from the agricultural and allied sectors such as handloom,

power loom, gem and jewellery, handicrafts, carpets, leather and mineral

products, all of which have at least one primary rural production base.

The rural market share of both consumer durable and non-durable

products exceeds 40-50 per cent for most items and is growing every year.

Pepola (1991) while analysing the trends in rural non-farm employment,

based on the analysis of the data from the quinqennial rounds of the National

Sample Survey during the 1970s and 1980s, reveals that the share of rural

area in total employment has declined from around 82 per cent in 1977-78 to

78 per cent in 1987-88; that the share of the rural non-agricultural employment

Role of Banks, NGO's & MFI in Promoting Micro-finance 161

has increased from around 14 per cent to 17 percent in total employment; and

from 17 per cent to 22 per cent in rural employment.

Rural non-agricultural activities have thus been growing much more

rapidly than the overall employment, agricultural employment and also urban

employment. In fact, the non-agricultural rural employment has grown at an

average rate of about 5 per cent during the ten-year period 1977-78 to 1987-88.

Consequently, there has been a shift from agriculture in which employment

has grown at a rate of only 0.74 per cent, to the non-agricultural activities.

It is because of decrease in self-employment and regular wages/

salaried employment in agriculture and increase in employment in non-

agricultural sector. Micro-enterprises established in RNFS contribute about 40

per cent of the gross industrial turnover and 34 per cent of total exports.

RNFS is the potential sector for employment generation through establishment

of micro-enterprises.

There is a need to match the decline in agriculture sector with the gain

in non-farm activities, to absorb the surplus labour from agriculture. Eighth

Five-Year Plan document (Government of India 1992: 122) states that: "In the

long run, however, it must be recognized that agricultures and other land-

based activities, ever with a reasonably high rate and possible diversification

of growth, will not be able to provide employment to all the rural workers at

adequate levels of incomes.

Indian microfinance continued growing rapidly towards the main

objective of financial inclusion, extending outreach to a growing share of poor

households, and to the approximately 80 percent of the population which has

yet to be reached directly by the banks. The larger of the two main models,

the Self-Help Group (SHG) Bank Linkage Programme (SBLP) covered about

143 million poor households in March 2006 and provided indirect access to

the banking system to another 14 million, including the "borderline poor".

Role of Banks, NGO's & MFI in Promoting Micro-finance 162

Although firm estimates are lacking, the other, Microfinance Institution

(MFI) model served 7.3 million households, of which 3.2 million were poor.

Even allowing for a degree of overlap of borrowers from both models, the

total number of poor households being reached was roughly a fifth of all poor

households, as well as a smaller share of the larger number of non-poor

households who have yet to be reached by the formal financial sector.

Apart from providing financial services to both these segments of the

population, there is widespread evidence that much stronger competition

provided to the informal sector has significantly improved the terms of credit

provided to both segments by the informal sector, which is losing share to

both the formal and (semi-formal) MFI sector.

4.6 SHG Bank Linkage Programme

Of the two major models of microfinance in India, the SHG Bank

Linkage Programme (SBLP) is by far the dominant model in terms of number

of borrowers and loans outstanding. The cumulative number of SHGs linked

has grown almost tenfold in the last five years, to achieve an outreach of

about 31 million families through women's membership in about 2.2 million

SHGs by March 2006. Not all SHGs are currently "linked" in the sense of

having loans outstanding to the banks or federations, and only an estimated

half of their members are poor. However, this still means about 14 million

poor households have been reached so far. Moreover the entire membership is

saving regularly, and has access to a ready source of small emergency and

consumption loans in the form of loans extended out of the group's own funds.

4.7 NGOs Involvement in Micro-Finance and Livelihood Strategies

However, there is no smooth flow of funds from any sources to

provide loans to the rural poor for establishing their micro enterprises in the

RNFS. "Moneylenders rarely provide credit for capital assets acquisition.

They concentrate on lending for consumption needs and social/ medical

Role of Banks, NGO's & MFI in Promoting Micro-finance 163

contingencies while trader lenders provide working capital. Thus, venture

capital for the rural non-farm sector is generally financed from own resources

and supplemented by loans from friends and relatives. The time taken for

getting a loan sanctioned by a bank for the rural non-farm sector can very

from two months to 18 months. Some moneylenders do provide bridge loans

to those rural borrowers who have been sanctioned bank loans but have yet to

receive the funds."

Based on the observations of the failure of development policy and

administration, with a weak role played by the State in supporting the

institutions of development, the importance of developing NGOs as change

agents has been greatly felt. Government of India also realized its failure in

properly implementing development projects and decided to involve NGOs

during the Seventh Five-Year Plan, in executing development projects.

The NGOs strength lies in target group approach, flexibility,

experimentation, innovation, grassroots presence and motivation. By learning

from the example of Grameen Bank, Bangladesh, many NGOs in India, came

forward to provide financial services to the rural poor and RNFS enterprises.

For NGOs, it is also a shift in approach from development to empowerment

wherein they can plan their withdrawal strategy from service delivery projects

and think of their own sustainability by providing financial services. At

present there are almost 800 NGOs involved directly in micro-finance

delivery systems in India. These NGOs have adopted different strategies of

promoting people's livelihood through micro-finance. These strategies are

based on their clientele, approach, focus area, interest rate, savings linkages,

collateral, coverage and organisational/ legal structure. These strategies can

be classified into four broad categories, namely, SHG promotion, MFI, micro-

enterprise development and social development.

Role of Banks, NGO's & MFI in Promoting Micro-finance 164

The SHG promotion approach is based on the premise that the NGO

promotes SHGs and provides them services as financial advisor. This

ultimately leads to build the capacity of SHGs in terms of savings

mobilization, linking them with banks and providing technical support in

starting viable micro enterprises by the members of SHGs members. In this

approach NGO basically is a mediating contact between SHGs and banks.

NGO also examines creditworthiness of the SHGs so that banks can lend

money to the SHGs.

In all this NGO gets some financial support in terms of grant from Apex

Financial Institutions (AFIs) like NABARD and RMK (Rashtriya Makila Kosh).

The examples of such NGOs who are following SHG promotion approach are:

MYRADA in Karnataka, SHARE in Andhra Pradesh, RDO (Rural Development

Organisation) in Manipur, PREM (People's Right and Environment Movement)

in Orissa & Andhra Pradesh, YCO (Youth Charitable Organisation) in Andhra

Pradesh, Anarda (Acil Navsarjan Rural Development Foundation) in Gujarat,

PRADAN (Professional Assistance for Development Action) & RUDSOVAT

(Rural Development Society for Vocational Training) in Rajasthan and

ADITHI in Bihar.

Micro-Finance Institution Strategy

The approach of promoting MFIs is based on the premise that AFIs like

SIDBI (Small Industries Development Bank of India). RMK and other donor

agencies provide bulk lending, soft loan and some grant to such NGOs which

can act as MFIs by on-lending the money to the poor people/SHGs/

Federations/ smaller NGOs. These MFIs stimulate the credit demand of the

poor people. They also provide technical support for the beneficiaries to ensure

proper utilization of loans and repayment. At the same time they meet their cost

of funds, cost of credit management and cost of default through the spread of

interest and generate surplus for the viable operation of micro-finance.

Role of Banks, NGO's & MFI in Promoting Micro-finance 165

The example of such MFIs are Sewa Bank & FWWB in Gujarat,

BASIX in Andhra Pradesh and RGVN (Rashtriya Grameen Vikas Nidhi) in

north-eastern states, Orissa and Bihar. Micro-Enterprise Development

Strategy Entrepreneurship is one of the most important inputs in the economic

development of a country and of the regions within the country. Economic

growth and industrialization are the by-products of entrepreneurship.

NGOs are actively involving in microfinance to make it successful and

effective in terms of identification of place or location, pre-promotional

activities, selection of potential entrepreneurs, entrepreneurial training,

monitoring and follow-up mechanism. NGOs are playing important role as

catalyst in helping the rural unemployed persons to acquire training through

MEDPs (Micro-Enterprise Development Programmes) so that they can also

become job providers instead of job seekers.

Thus, institutionalization of MEDPs through NGOs can be an

alternative approach of rural development in India. The success of any MEDP

in terms of starting the enterprises by the trainees trained under it depends

mainly upon the availability of loan. Micro-finance sector can provide help to

solve this problem. Micro-finance for micro-enterprise development is a

proper approach in India.

Some of the NGOs in India have adopted the approach of micro-

enterprise development through micro-finance. The examples are CDF

(Co-operative Development Foundation) in Andhra Pradesh, LHWRF (Lupin

Human Welfare Research Foundation) in Rajasthan, UPLDC (Uttar Pradesh

Land Development Corporation) in Uttar Pradesh and Group Enterprise

Development Project of EDI (Entrepreneurship Development Institute of

India) in Nagaland.

Social Development Strategy

The social development approach of micro-finance is based on the

premise that people should earn money by investing in viable micro-

Role of Banks, NGO's & MFI in Promoting Micro-finance 166

enterprises. They should earn profit from their enterprises. Major share of the

profit should be reinvested in enterprises for their growth. The other share of

the profit should be spent on social development that is, health, education,

housing, sanitation etc.

By earning profit from the viable micro-enterprises, people will

increase their paying ability for services delivered to them under different

social development projects run by NGO and States/ Central Government. For

the NGOs and Government it can be a process of gradual withdrawal and for

people, decrease dependency on the NGOs and Government. Such projects

have micro-finance as a major component coupled with social service delivery.

These projects have demonstrably positive effects. The examples of

such projects are Indo-Canada Agriculture Extension Project in Uttar Pradesh,

IFFDC (Indian Farm & Forestry Development Corporation) project of farm

and forestry development in Uttar Pradesh and Rajasthan, ICDS (Integrated

Child Development Services) project of RASS (Rayalseema Sewa Samiti) in

Andhra Pradesh and Conversion of ICDS project into Indira Mahila Yojana.

Role of Financial Institutions in Micro-Finance

Especially during 1991-92, NABARD launched projects to provide

micro credits to SHGs by bank linkages. In the same way, NGOs also have

done excellent work in the areas of microfinance. Since the emergence of

micro-finance sector in India, role of AFIs has become significant. NABARD

initiated the process of micro-finance in India through linkage programme of

SHGs under Automatic Refinance Scheme. SIDBI is second important player

in microfinance, providing bulk lending to MFIs. RMK is the third player

providing loans to NGOs for on lending to the women SHGs. These are the

three major AFIs in India. Each has a different approach in micro-finance

sector. The following table shows the achievements under NABARDs SHG

linkage scheme which is the world's largest scheme in the sector.

Role of Banks, NGO's & MFI in Promoting Micro-finance 167

YEAR Amount (Rs. in Crores) Groups (in lakhs)

2008-09 41.90 0.12

2009-10 88.63 0.44

2010-2011 173.38 1.03

2011-2012 255.00 0.75

Source: NABARD

Table 4.1 Achievements under SHG - NABARD linkage scheme

While NABARD's emphasis is entirely on SHGs linkage programme

mobilizing their own savings also, SIBDI is focusing on building and creating

larger MFIs and RMK is lending money to smaller NGOs as well. Taking into

consideration the growth and potential of micro-finance sector in India, other

organizations and international agencies have also made their entry in the

micro-finance sector by providing loans and grants to NGOs for different

income generating projects as well as for incorporating micro-finance

component in the service delivery projects of social development.

4.8 Leading Financial Institutions in promoting microfinance

The important names amount them are HUDCO, NBCFDC (National

Backward Classes Finance Development Corporation), NMFDC (National

Minorities Finance Development Corporation), National Handicrafts

Development Corporation (NHDC), OXFAM (Oxford Committee for Famine &

Relief), NOVIP (Dutch International Development Agency), GTZ

(Gesellschaftfur Techische Zusammenarbeit), CIDA (Canadian International

Development Agency), Action Aid, CARE India, International Fund for

Agriculture Development (IFAD), UNDP, UNIFEM (United Nations

Development Fund for Women), British Department of Foreign and International

Development (DFID) and Consultative Group to Assist the Poorest (CGAP.)

It is seen as an important phenomenon in the process of development,

especially in the context of globalisation and liberalisation wherein subsidy

Role of Banks, NGO's & MFI in Promoting Micro-finance 168

and grant based programmes/ schemes are losing their importance. Micro-

finance sector is seen as the best option based on saving mobilisation of the

poor people and credit linkages. In India, many AFIs have come forward to

lend money to the MFIs. MFIs of different nature (NGO registered under

Societies Registration Act, Trusts under Public Trust Act, Co-operatives

under Co-operative Act, NDFCs under Company Act and LABs under

Banking Act etc.) have also come up with different strategies of promoting

people's livelihood.

4.9 Microfinance support Institutions in the Formal Sector

The following are the major support institutions in India.

• National Bank for Agriculture and Rural Development

• Rashtriya Mahila Kosh

• SIDBI - Small Industries Development Bank of India

• Tamil Nadu Women's Development Corporation

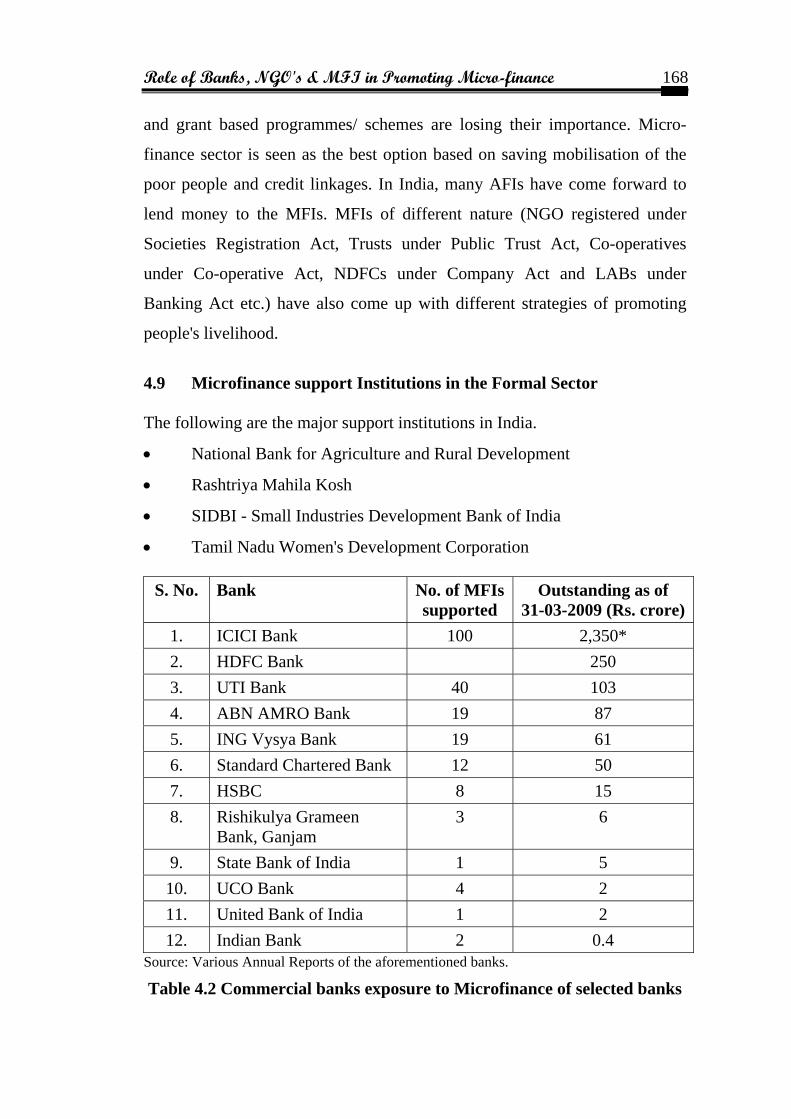

S. No. Bank No. of MFIs supported

Outstanding as of 31-03-2009 (Rs. crore)

1. ICICI Bank 100 2,350* 2. HDFC Bank 250 3. UTI Bank 40 103 4. ABN AMRO Bank 19 87 5. ING Vysya Bank 19 61 6. Standard Chartered Bank 12 50 7. HSBC 8 15 8. Rishikulya Grameen

Bank, Ganjam 3 6

9. State Bank of India 1 5 10. UCO Bank 4 2 11. United Bank of India 1 2 12. Indian Bank 2 0.4

Source: Various Annual Reports of the aforementioned banks.

Table 4.2 Commercial banks exposure to Microfinance of selected banks

Role of Banks, NGO's & MFI in Promoting Micro-finance 169

4.10 Role Models of Micro Finance

There are different models followed by the different microfinance

institutions in India. The following are some successful and established

microfinance institutions and their activates in microfinance:

1) Grameen Bank

Grameen Bank (GB) has reversed conventional banking practice by

removing the need for collateral and created a banking system based on

mutual trust, accountability, participation and creativity. GB provides credit to

the poorest of the poor in rural Bangladesh, without any collateral. Professor

Muhammad Yunus, the founder of "Grameen Bank" The banks has 3.7

million borrowers, 96 percent of whom are women. With 1267 branches, GB

provides services in 46,000 villages, covering more than 68 percent of the

total villages in Bangladesh.

General features of Grameen credit are:

a. It promotes credit as a human right

b. Its mission is to help the poor families to help themselves to overcome

poverty. It is targeted to the poor, particularly poor women.

c. Most distinctive feature of Grameen credit is that it is not based on any

collateral or legally enforceable contracts. It is based on "trust", not on

legal procedures and system.

d. It is offered for creating self-employment for income-generating

activities and housing for the poor.

e. It was initiated as a challenge to the conventional banking which

rejected the poor by classifying them to be "not creditworthy". As a

result it rejected the basic methodology of the conventional banking

and created its own methodology.

f. It provides service at the door-step of the poor based on the principle

that the people should not go to the bank, bank should go to the people.

Role of Banks, NGO's & MFI in Promoting Micro-finance 170

g. In order to obtain loans a borrower must join a group of borrowers.

h. Loans can be received in a continuous sequence. New loan becomes

available to a borrower if her previous loan is repaid.

i. All loans are to be paid back in instalments (weekly, or bi-weekly).

j. Simultaneously more than one loan can be received by a borrower.

k. It comes with both obligatory and voluntary savings programmes for

the borrower.

l. Grameen credits thumb-rule is to keep the interest rate as close to the

market rate, prevailing in the commercial banking sector, as possible,

without sacrificing sustain-ability. Reaching the poor is its non-

negotiable mission. Reaching sustainability is a directional goal. It

must reach sustainability as soon as possible, so that it can expand its

outreach without fund constraints.

Grameen credit gives high priority on building social capital. It is

promoted through formation of groups and centres, developing leadership

quality through annual election of group and centre leaders electing board

members when the institution is owned by the borrowers.

SPANDANA

Institution's Mission

Spandana envision itself as a financially self sustainable Micro Finance

Institution with a diversified ownership. It is committed to strengthening

significantly the socio-economic status of poor women in Rural and Urban

areas by providing technical and financial services on a continued basis for

establishing their identity and self-image

Background and Main Challenges

There are two important challenges ahead. Spandana at present is a non

profit making society and has initiated the prices of transformation into a

regulated Company. Spandana has outperformed the most performing

Role of Banks, NGO's & MFI in Promoting Micro-finance 171

organisations by setting up trends with high level of efficiency, productivity

and thereby profitability levels. Thus the biggest challenges lies in retaining

these levels in the pace of increasing competition.

Products

• Loans • Voluntary Savings • Insurance

Main Funding Sources

• Grants • Loans • Savings

This organization is one of the largest funder of microfinance

The following institutions are the important funders:

ICICI Bank, SIDBI, India Overseas bank, HDFC Bank, IDBI Bank, ABN

AMRO Bank, ING Vysya Bank, HDFC, FWWB, AXIS Bank.

3) Swayam Krishi Sangam (SKS):

Swayam Krishi Sangam (self-cultivation society) is an initiative in

rural India to empower the poorest of the poor to become self-reliant. In June

1998, SKS began operating its main activity, microfinance, which follows the

Grameen Bank model by seeking to eradicate poverty by providing small

loans for income generating activities through a process of collective peer

lending.

SKS established its first women's banking sangams (centers) in the

Narayankhed region. As of July 2005, SKS Microfinance has grown to

include 32 branches in Siz Districts of Telangana and serves over 100,000

clients. Swayam Krishi Sangam began its education activities by

implementing a Preschool (Balwadi) Program in February 2001 in one of the

poorest parts of India-the Narayankhed region of Medak district in Andhra

Pradesh.

Role of Banks, NGO's & MFI in Promoting Micro-finance 172

4) RASHTRIYA MAHILA KOSH - Its Profile, Aims & Objectives,

Roles

It has been felt for some time in India that the credit needs of poor

women, particularly in the unorganized sector, have not been adequately

addressed by the formal financial institutions in the country. The vast gap

between demand for and supply of credit to this sector established the need

for a National Credit Fund for Women.

The National Credit Fund for Women or the Rashtriya Mahila Kosh

(RMK) was set up in March 1993 as an independent registered society by the

Department of Women & Child Development in government of India's

Ministry of Human Resource Development with an initial corpus of Rs.

310,000,000 - not to replace the banking sector but to fill the gap between

what the banking sector offers and what the poor need.

Its main objectives are:

To provide or promote the provision of micro-credit to poor women for

income generation activities or for asset creation.

To adopt a quasi-informal delivery system, which is client friendly,

uses simple and minimal procedures, disburses quickly and repeatedly,

has flexibility of approach, links thrift and savings with credit and has

low transaction costs both for the borrower and for the lender.

To demonstrate and replicate participatory approaches in the

organization of women's group for thrift and savings and effective

utilization of credit.

To use the group concept and the provision of credit as an instrument

of women's empowerment, socio-economic change and development.

To cooperate with and secure the cooperation of the Government of

India, State Governments, Union Territory administrations, credit

institutions, industrial and commercial organizations, NGOs and others

in promoting the objectives of the Kosh.

Role of Banks, NGO's & MFI in Promoting Micro-finance 173

To disseminate information and experience among all these above

agencies in the Government and non-government sectors in the area of

microfinance for poor women.

To receive grants, donations, loans, etc., for the furtherance of the aims

and objectives of the Kosh.

The office of the Kosh is situated in New Delhi. The Kosh does not

have any branch offices. The Executive Director is the chief executive officer

of the Kosh. The executive Director functions under the overall supervision,

direction and control of the Governing Board. The Governing Board

comprises 16 members consisting of senior officers of the Government of

India and State Governments, specialists and representative of NGOs active in

the field of microfinance for women. The Governing Board is chaired by the

Minister in charge of the Department of Women & Child Development in the

Government of India. The General Body of the Kosh consists of all members

of the Board, institutional members and individual members.

RMK- Main Roles:

Wholesaling Role - It acts as a wholesaling apex organization for channelizing

funds from government and donors to retailing intermediate microfinance

organizations (IMOs). [The Kosh has so far received only a one-time grant

from government and has not needed to raise funds from any other sources.

Market Development Role -

It develops the supply side of the micro finance market by offering

institution building support to new and existing-but-inexperienced IMOs by

structures of incentives, transfers of technology, training of staff and other

non-financial services.

The Kosh realizes that it can play a value adding wholesaling role only

when a sufficiently large and well established micro finance sector already

Role of Banks, NGO's & MFI in Promoting Micro-finance 174

exists - this depends on the number of IMOs and the sustainability of IMOs -

subsidized institution building increases the equity of any IMO as much as

grants do - large and premature disbursement of funds to the IMO can reduce

the effectiveness of any institution building effort.

5) Micro finance programmes of CAPART

The Council for Advancement of People's Action and Rural

Technology (CAPART) was set up by the Ministry of Rural Development,

Government of India, to fund voluntary organizations and community based

organizations engaged in serving rural areas. CAPART occupies a significant

space in shaping the development innovations of NGOs and catalyzing

development initiatives to reach the poor.

The main objective of the scheme is:

To fund VOs and CBOs already working with self help groups to

extend their reach to new areas and improve the quality of existing

groups

To extend training support to potential VOs and registered CBOs who

are desirous of working in the areas of micro finance and self help

groups.

To identify and support VOs and registered CBOs having outstanding

experience in formation of SHGs and micro finance who would act as

resource centers. The unit cost for the promotion of group is worked

out to a maximum of Rs. 9,000/- per group, which includes

expenditure for a 3 year project cycle.

To Fund Rs. 10,000/- per SHG without interest, where bank linkages

are not available as revolving fund.

To finance up to Rs. 2.00 lakhs as bridge funds for a federation of over

100 active SHGs.

Role of Banks, NGO's & MFI in Promoting Micro-finance 175

6) SHARE Micro Finance Limited

Introduction

SML started operations in 1989 as a not-for-profit society. It was the

first MFI in India to obtain a NBFC (non-deposit accepting) license and also

the first Indian MFI to carry out a microfinance securitization transaction.

SML has employed a for-profit approach to create social returns by

channelling funds from development institutions and commercial banks as

collateral-free loans to Joint Liability Groups (JLGs). JLGs are the central

element of the Grameen lending methodology adopted by SML.

Vision and mission is to improve the quality of life of the poor by

providing access to financial and support services add to be a viable financial

institution developing sustainable communities, and to mobilize resources to

provide financial and support services to the poor, particularly women, for

viable productive income generation enterprises enabling them to reduce their

poverty

The society has the following main objectives:

To provide financial services predominantly to poor women.

To create opportunities for self- employment for the underprivileged.

To train rural poor in simple skills and enable them to utilize the

available resources and contribute to employment and income

generation in rural areas.

4.11 Banks as Microfinance Providers

The banking sector has been playing an important in providing various

financial services to the poor and the non-poor. Among the three categories of

banks, the cooperative banking institutions, mainly serving in rural areas,

were the first in the formal banking sector to provide micro finance services

to the poor. Later, a few urban cooperative banks also started providing a

Role of Banks, NGO's & MFI in Promoting Micro-finance 176

variety of financial services to the poor and the not-so-poor. Prominent

amount them is the SEWA Bank, Ahmadabad, which focuses on urban poor

women by providing various financial services to them. Traditionally, these

institutions in rural areas were financing only agriculture and allied sectors.

As on 31 March 2009, these cooperative banks had mobilised deposits worth

Rs. 67,700 crore while their advances stood at Rs. 70,770 crore. With the

growing need to finance all forms of enterprises and the felt need for

diversification of business, the cooperative banking institutions have, in the

recent past, diversified their business. Currently, nearly 70% of their credit

portfolio is for agriculture and allied activities. Some of these grassroots level

cooperative banking institutions, both in rural and urban sectors, have been

providing small loans with focus on the poor.

Regional Rural Banks (RRBs) lend mostly to the poor for agriculture

and micro-enterprise sectors. As on 31 March 2009, deposits and advances of

the RRBs stood at Rs. 26,763 crore and Rs. 11,281 crore respectively, with

their advances to the target group accounting for 65% of their total loan

portfolio.

Commercial Banks are required, as per the directions of RBI, to

provide loans to the priority sector comprising agriculture and allied

activities, small, tiny, cottage and village industries, rural artisans, etc., to the

extent of 40 per cent of their credit portfolio. This includes 18 per cent of

lending exclusively to agriculture and allied activities. Further, 10% of their

loan portfolio is required to be provided to weaker section of the society

covering scheduled castes, scheduled tribes, small and marginal farmers,

agricultural labourers, rural artisans, etc. These loans are essentially of the

nature of microfinance.

For banking with the poor, microfinance has been an essential aspect

of the banking policy. Though, in the present scenario, banks are serving a

Role of Banks, NGO's & MFI in Promoting Micro-finance 177

variety of clients and they continue to play an important role in the area of

microfinance. Therefore, it is considered that banks are treated as one of the

major microfinance service providing institutions, though not exclusive

microfinance institutions.

It is observed that there is a growing perception that the gap between

demand and supply of rural credit, especially with regard to weaker sections,

is widening. This credit gap and the felt need for additional systems for

provision of mF and banking with the poor have results in the development of

supplementary and alternative delivery mechanisms as also in the birth and

growth of a number of mFIs.

There is a wide variety of institutions in India catering, with various

degrees of success, to the microfinance needs of poor families. They comprise

mF providers in the formal financial sector comprising commercial banks,

RRBs and cooperative banks and mFIs comprising NGOs, SHGs' federations

and certain non-bank cooperative societies in the non-financial sector. In the

recent past, a few NBFCs have also been established as mFIs. The mFIs can

broadly be sub-divided into three categories of organisational forms as

mentioned earlier in this chapter:

1. Not-for Profit mFIs

Societies registered under Societies Registration Act, 1860 or

similar State Acts

Public Trusts registered under the Indian Trust Act, 1882

Non-profit Companies registered under Section 25 of Companies

Act, 1956

1. Mutual Benefit mFIs

State credit cooperatives

National credit cooperatives

Mutually Aided Cooperative Societies (MACS)

Role of Banks, NGO's & MFI in Promoting Micro-finance 178

1. For Profit mFIs

Non Banking financial Companies (NBFCS), registered under

the Companies Act, 1956

As already indicated in Chapter 1 (Introduction), banks could be called

mF service providers and on the same analogy, NABARD and SIDBI could

be considered as apex level mF service provider institutions, while RMK

could be considered as an apex level mFIs.

A good number of NGOs, besides playing a catalytic role of friend,

philosopher and guide to the SHGs, have also assumed the role of financial

intermediaries either directly or by networking with smaller NGOs or by

promoting SHGs' federations and other outfits like Mutually Aided

Cooperative Societies (MACS).

4.12 SHGs' Federations

SHGs' Federations are generally observed to be formal institutions

registered under societies Registration Act, 1860 or under analogous State

Acts. The Task Force observes that a laudable initiative has been taken by

some of the NGOs in helping the village level SHGs to network in clusters

and the cluster representatives to network at block level federations. This has

at times enabled them to pool the resources of individual SHGs so that even

short term surpluses are used by other resource-deficit SHGs. The federations

facilitate training of SHGs, undertake internal auditing and ensure that the

SHGs and clusters again self-reliance in running their own affairs. SHGs'

Federations, promoted by certain prominent NGOs like MYRADA, DHAN

Foundation, LEAD, Chaitanya and SEWA Bank, are functioning in different

parts of the country as providers of financial services, such as mobilising

thrift and providing credit and other non-financial services like training group

members and extending various support services, viz. input supply, storage,

marketing and legal services. In a few cases, the state governments have also

Role of Banks, NGO's & MFI in Promoting Micro-finance 179

taken initiatives in promoting SHGs by establishing organisations with federal

structures. Notable among them are the Community Development Societies

(CDS) in Kerala and Mahalir Thittam in Tamil Nadu. This approach brings

synergy in integration of community level programmes with SHG approach.

Mutually Aided Cooperative Societies (MACS)

Govt. of Andhra Pradesh has enacted the Mutually Aided Cooperative

Societies (MACS) Act in 1995 for the voluntary formation of cooperative

societies as accountable for competitive, self-reliant, business enterprises

based on thrift, self-help and mutual aid owned, managed and controlled by

members for their socio-economic development. The societies set up under

MACS Act have certain advantages over the existing traditional cooperatives

societies, the most important being the freedom given to their management

from government interference in their affairs, raising of resources, absence of

provision for supersession of the elected board, greater accountability, etc. On

the same token, any society set up under MACS Act may not able to access

funds from the government.

Till the end of December 2010, over 850 societies had been registered

under the Act, of which 319 societies were by way of conversion from

Andhra Pradesh Cooperative Societies Act, 1964 and 539 were newly set up

under MACS Act. Dairy cooperatives (307) and thrift cooperatives (241)

together accounted for 64% of the total societies under the Act. Guntur

district with 302 dairy cooperatives, Warangal district with 72 thrift

cooperatives and 22 marketing cooperatives, ananthapur district with 34

weavers' cooperatives and Kurnool district with a total of 98 societies were in

the forefront in organising societies under the MACS on account of the

proviso that the societies under the new Act cannot accept share capital or

loan from the state government. But, there is a quantum jump in the growth of

these organisations with over 2,000 MACS reportedly registered in the State

in the recent past.

Role of Banks, NGO's & MFI in Promoting Micro-finance 180

Thought there is no specific mention about the type of clientele the

MACS would serve, it is understood that a number of thrift and credit

societies have been set up in seven district of the state of Andhra Pradesh with

focus on poor, some coalitions and networks of the SHGs have

institutionalised themselves under the new enactment. The state government

is keen to use this institutional arrangement to push forward its social agenda

of addressing the problem of poverty and more particularly the women and

thus proposing to have an Apex body of MACS in the state. It proposes to set

up a special fund called 'A.P. Women's Fund' using the MACS route.

4.13 Non-banking Financial Companies

Non-Banking Financial Companies (NBFCs) are companies registered

under the Companies Act, 1956 and regulated by the Reserve Bank of India.

The RBI (Amendment) Act, 1997 has made it obligatory for NBFCs to apply

to the Reserve Bank of India for a certificate of registration. The RBI

introduced a new regulatory framework for the NBFCs in January 1998 with

focus on NBFCs accepting public deposits with a view to safeguarding the

interests of the depositors. Accordingly, NBFCs falling short of the stipulated

minimum NOF were precluded from accepting public deposits. Ceiling on the

quantum of public deposits was related to the level of credit rating given by

the approved credit rating agencies. Net owned funds is defined under the

RBI Act as the aggregate of the paid-up capital and free reserves as per last

balance sheet after deducting there from accumulated losses, deferred revenue

expenditure and other intangible assets, etc. As regards prudential norms,

NBFCs were required to achieve capital adequacy of 12% and to maintain

liquid assets of 15% on public deposits. The interest rate ceiling on public

deposits was fixed at 16% p.a.

Role of Banks, NGO's & MFI in Promoting Micro-finance 181

There are mainly three approaches to provide financial services to the

poor, like:

1. Exclusive focus on mF services: Under this category, NGOs

implementing a variety of mF programmes are the major players. These

NGOs often act as financial poor. These funds may (or, may not) be

added to client savings to form a corpus to the lending. There are a few

cooperative organisations that fall under this category of mFIs. These

are registered under the Central Cooperative Societies Act such as the

Indian Cooperative Network of Women of the Working Women's

Forum and the thrift and credit cooperative societies promoted by the

Cooperative Development Forum in Andhra Pradesh. Also, a few of

the MACS in Andhra Pradesh are engaged in providing mF services

exclusively. Few NBFCs also provide micro financial services.

2. Microfinance services as one of their major objectives: Under this

type, a large number of NGOs that are engaged in various social sector

programmes in health, education and environment also provide mF

services as an "add-on" activity. BASIX, an NBFC, also falls under

this category.

3. Intermediary or apex institutions: Institutions like Rashtriya Mahila

Kosh (RMK), the Friends of WWB, Ahmadabad, Rashtriya Gramin

Vikas Nidhi (RGVN), Guwahati are among the few institutions

providing indirect services in the mF sector by supporting smaller

institutions offering micro financial services. Recently, SIDBI has set

up a Foundation, viz. SIDBI Foundation for Micro Credit (SFMC) for

supporting microcredit provided by mFIs.

Besides, there are a large number of informal SHGs which offer micro

financial services on a limited scale to their members. Though these may not

be considered as mFIs in the strict sense, it is increasingly felt that SHGs

could be recognised as non-formal community-based mFIs.

Role of Banks, NGO's & MFI in Promoting Micro-finance 182

4.14 Experience of Financial Institutions in mF Activities

NABARD and mF

NABARD was set up in 1982 specifically as an organisation for

providing undivided attention, forceful direction and pointed focus to the

credit problems of the rural sector. A series of research studies and action

research projects during the early Eighties to help devise delivery mechanisms

for improving the access of the poor to banking services had led NABARD to

mainstream the SHG-bank linkage strategy, while continuing to look for other

delivery mechanisms and selectively support them.

NABARD started with a limited scale pilot Project to credit-link 500

SHGs across the country, for which detailed guidelines were issued to the

banks in February 1992. These instructions were very comprehensive and

allowed flexibility and discretion to the banks in effecting linking of informal

groups. Stress on compulsory savings, liking of credit with savings, lending

decisions by the SHGs on the basis of collective wisdom, peer-pressure and

group cohesion as collateral substitutes, absence of margin, unit costs, etc.,

were the hallmarks of these operational instruction. In addition to

concessional 100% refinance to the banks, NABARD provides policy

guidance, technical and promotional support mainly for capacity building of