CH03 Solutions DEP - BruceDehning.com

82

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3 3-1 Chapter 3 Adjusting Accounts for Financial Statements Learning Objectives – coverage by question Mini- exercises Exercises Problems Cases LO1 – Identify the major steps in the accounting cycle. LO2 – Review the process of journalizing and posting transactions. 21, 22, 23, 25, 29, 30 33, 35, 36, 38 40, 41, 42, 46, 47, 52, 54 55, 56, 57, 58 LO3 – Describe the adjusting process and illustrate adjusting entries. 23, 24, 25, 29, 30 32, 33, 34, 35, 36, 38 40, 41, 42, 43, 46, 47, 48, 49, 52, 53, 54 55, 56, 57, 58 LO4 – Prepare financial statements from adjusted accounts. 26 39 40, 41, 42, 44, 47, 49, 50, 53, 54 55, 58 LO5 – Describe the process of closing temporary accounts. 27, 28, 30 31, 33, 37, 39 42, 44, 45, 46, 49, 50, 51, 52, 53, 54 55 LO6 – Analyzing changes in balance sheet accounts. 25, 29 32, 34, 35, 36, 38 53 56

Transcript of CH03 Solutions DEP - BruceDehning.com

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-1

Chapter 3

Adjusting Accounts for Financial Statements

Learning Objectives – coverage by question

Mini-exercises

Exercises Problems Cases

LO1 – Identify the major steps in the accounting cycle.

LO2 – Review the process of journalizing and posting transactions.

21, 22, 23, 25,

29, 30 33, 35, 36, 38

40, 41, 42, 46,

47, 52, 54 55, 56, 57, 58

LO3 – Describe the adjusting process and illustrate adjusting entries.

23, 24, 25, 29,

30

32, 33, 34, 35,

36, 38

40, 41, 42, 43,

46, 47, 48, 49,

52, 53, 54

55, 56, 57, 58

LO4 – Prepare financial statements from adjusted accounts.

26 39

40, 41, 42, 44,

47, 49, 50, 53,

54

55, 58

LO5 – Describe the process of closing temporary accounts.

27, 28, 30 31, 33, 37, 39

42, 44, 45, 46,

49, 50, 51, 52,

53, 54

55

LO6 – Analyzing changes in

balance sheet accounts.

25, 29 32, 34, 35, 36,

38 53 56

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-2

QUESTIONS

Q3-1 The five major steps in the accounting cycle are

1. Analyze business activity using transaction analysis based on the related source documents.

2. Record results of the transaction analysis chronologically in the general journal and create a trial balance.

3. Adjust the recorded data to update all accounts for expense and revenue recognition not previously recognized.

4. Report the adjusted financial data in the form of financial statements. 5. Close the books by posting the adjusting and closing entries, which “zero

out” the temporary accounts. Q3-2 The fiscal year is the annual accounting period adopted by a firm. A firm

using a fiscal year ending on December 31 is on a calendar-year basis. Q3-3 Examples of source documents that underlie business transactions are

invoices sent to customers, invoices received from suppliers, bank checks, bank deposit slips, cash receipt forms, and written contracts.

Q3-4 A general journal is a book of original entry that may be used for the initial

recording of any type of transaction. It contains space for dates and for accounts to be debited and credited, columns for the amounts of the debits and credits, and a posting reference column for numbers of the accounts that are posted.

Q3-5 When entries are posted, the page number and identifying initials of the

appropriate journal are placed next to the amounts in the appropriate accounts. The account number is entered beside the related amount posted in the journal's posting reference column. This procedure enables interested users to trace amounts in the ledger back to the originating journal entry and permits us to know which entries have been posted.

Q3-6 A compound journal entry is a journal entry containing more than one debit

entry or one credit entry. Q3-7 A chart of accounts is a list of the accounts appearing in the general ledger,

with the account numbering system indicated. Normally the accounts are classified as asset, liability, owners' equity, revenue, and expense accounts, and often the numbering system identifies the account classification. For example, a coding system might assign the numbers 100–199 to assets, 200–299 to liabilities, and so on.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-3

Q3-8 Many of the transactions reflected in the accounting records through the first two steps of the accounting cycle affect the net income of more than one period. Therefore, adjustments to the account balances are ordinarily necessary at the end of each accounting period to record the proper amount of revenue and to match expenses with revenue properly. This process is also intended to achieve a more accurate picture of financial position by adjusting balance sheet amounts to show unexpired costs, up-to-date amounts of obligations, and so on.

Q3-9 1. Allocating assets to expense to reflect expenses incurred during the

period. Example: Recording supplies used by debiting Supplies Expense and crediting Supplies.

2. Allocating payments received in advance by crediting the revenue account

to reflect revenues earned during the period. Example: Recording service fees earned by debiting Unearned Service Fees and crediting Service Fees Earned.

3. Accruing expenses to reflect expenses incurred during the period that are

not yet paid or recorded. Example: Recording unpaid wages by debiting Wages Expense and crediting Wages Payable.

4. Accruing revenues to reflect revenues earned during the period that are

not yet received or recorded. Example: Recording commissions earned by debiting Commissions Receivable and crediting Commissions Earned.

Q3-10 Jan. 31 Insurance expense (+E, -SE) 78 Prepaid insurance (-A) 78 To record insurance expense for January ($1,872/24 = $78). Q3-11 A contra account is an account that is related to, and deducted from,

another account when financial statements are prepared or when book values are computed. Accumulated depreciation is deducted from the cost of a depreciable asset in computing and portraying the asset's book value.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-4

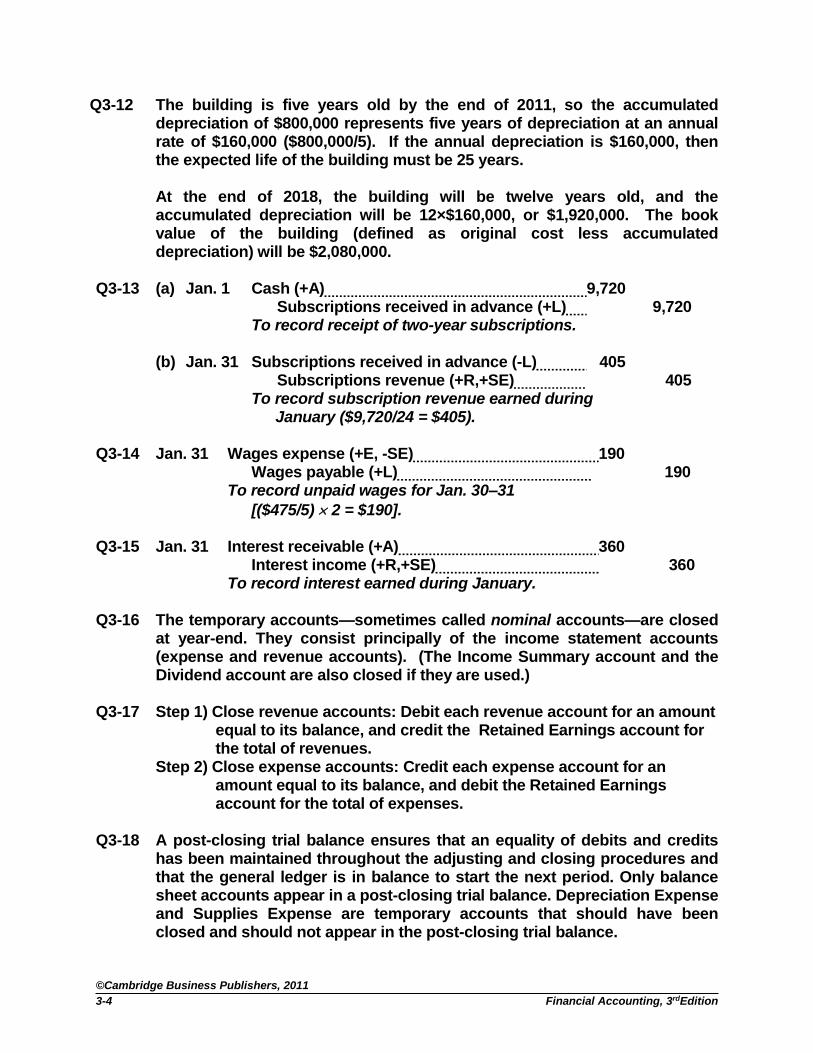

Q3-12 The building is five years old by the end of 2011, so the accumulated depreciation of $800,000 represents five years of depreciation at an annual rate of $160,000 ($800,000/5). If the annual depreciation is $160,000, then the expected life of the building must be 25 years.

At the end of 2018, the building will be twelve years old, and the

accumulated depreciation will be 12×$160,000, or $1,920,000. The book value of the building (defined as original cost less accumulated depreciation) will be $2,080,000.

Q3-13 (a) Jan. 1 Cash (+A) 9,720 Subscriptions received in advance (+L) 9,720 To record receipt of two-year subscriptions. (b) Jan. 31 Subscriptions received in advance (-L) 405 Subscriptions revenue (+R,+SE) 405 To record subscription revenue earned during January ($9,720/24 = $405). Q3-14 Jan. 31 Wages expense (+E, -SE) 190 Wages payable (+L) 190 To record unpaid wages for Jan. 30–31

[($475/5) 2 = $190]. Q3-15 Jan. 31 Interest receivable (+A) 360 Interest income (+R,+SE) 360 To record interest earned during January. Q3-16 The temporary accounts—sometimes called nominal accounts—are closed

at year-end. They consist principally of the income statement accounts (expense and revenue accounts). (The Income Summary account and the Dividend account are also closed if they are used.)

Q3-17 Step 1) Close revenue accounts: Debit each revenue account for an amount

equal to its balance, and credit the Retained Earnings account for the total of revenues.

Step 2) Close expense accounts: Credit each expense account for an amount equal to its balance, and debit the Retained Earnings account for the total of expenses.

Q3-18 A post-closing trial balance ensures that an equality of debits and credits

has been maintained throughout the adjusting and closing procedures and that the general ledger is in balance to start the next period. Only balance sheet accounts appear in a post-closing trial balance. Depreciation Expense and Supplies Expense are temporary accounts that should have been closed and should not appear in the post-closing trial balance.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-5

Q3-19 The cost principle and the matching concept support Dehning's handling of

its catalog costs. Prepaid Catalog Costs is an asset account that is initially recorded at the amount that the catalogs cost Dehning. This is consistent with the cost principle that states that assets are initially recorded at the amounts paid to acquire the assets. The catalogs help Dehning generate sales revenues. The matching concept states that the catalog costs should be matched as expenses with the revenues they help generate. Dehning does this by expensing the catalog costs over their estimated useful lives.

Q3-20

(a) Supplies Expense ($825 + $260 $630 = $455) for the period is omitted from the income statement, overstating net income by $455 (ignoring taxes).

(b) Both Supplies and Owners' Equity are overstated by $455 on the

January 31 balance sheet (again, before considering taxes).

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-6

Mini Exercises M3-21 (45 mintes) a.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

June 1. Invested $12,000 cash.

+12,000 Cash

=

+12,000 Common

Stock

-

=

June 2. Paid $950 cash for June rent.

-950 Cash

=

-950

Retained Earnings

-

+950 Rent

Expense =

-950

June 3. Purchased $6,400 of office equipment on account.

+6,400 Office

Equipment =

+6,400 Accounts Payable

-

=

June 6. Purchased $3,800 of supplies; $1,800 cash, $2,000 on account.

-1,800 Cash

+3,800 Supplies

=

+2,000 Accounts Payable

-

=

June 11. $4,700 billed for services.

+4,700 Accounts

Receivable

=

+4,700 Retained Earnings

+4,700 Service Fees

Earned -

=

+4,700

June 17. Collected $3,250 on accounts.

+3,250 Cash

-3,250 Accounts

Receivable =

-

=

June 19. Paid $3,000 on office equipment account.

-3,000 Cash

=

-3,000 Accounts Payable

-

=

June 25. Paid cash dividend of $900.

-900 Cash

=

-900 Retained Earnings

-

=

June 30. Paid $350 utilities.

-350 Cash

=

-350 Retained Earnings

-

+350 Utilities Expense

= -350

June 30. Paid $2,500 salaries.

-2,500 Cash

=

-2,500 Retained Earnings

-

+2,500 Salaries Expense

= -2,500

TOTALS 5,750 + 11,650 = 5,400 + 12,000 + 0 4,700 - 3,800 = 900

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-7

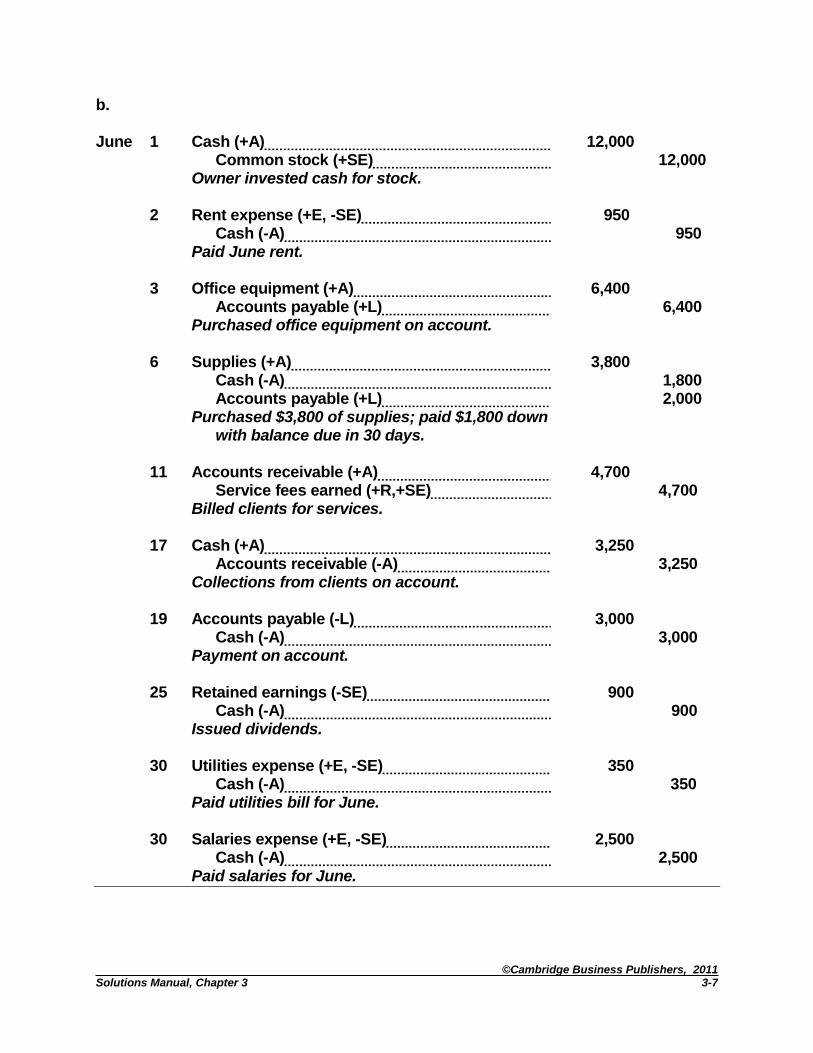

b. June 1 Cash (+A) 12,000 Common stock (+SE) 12,000 Owner invested cash for stock. 2 Rent expense (+E, -SE) 950 Cash (-A) 950 Paid June rent. 3 Office equipment (+A) 6,400 Accounts payable (+L) 6,400 Purchased office equipment on account. 6 Supplies (+A) 3,800 Cash (-A) 1,800 Accounts payable (+L) 2,000 Purchased $3,800 of supplies; paid $1,800 down with balance due in 30 days. 11 Accounts receivable (+A) 4,700 Service fees earned (+R,+SE) 4,700 Billed clients for services. 17 Cash (+A) 3,250 Accounts receivable (-A) 3,250 Collections from clients on account. 19 Accounts payable (-L) 3,000 Cash (-A) 3,000 Payment on account. 25 Retained earnings (-SE) 900 Cash (-A) 900 Issued dividends. 30 Utilities expense (+E, -SE) 350 Cash (-A) 350 Paid utilities bill for June. 30 Salaries expense (+E, -SE) 2,500 Cash (-A) 2,500 Paid salaries for June.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-8

c.

+ Cash (A) - + Supplies (A) -

June 1 12,000 950 June 2 June 6 3,800

17 3,250 1,800 6 3,000 19 900 25

350 30 + Office Equipment (A) -

2,500 30 June 3 6,400

+ Accounts Receivable (A) - - Accounts Payable (L) +

June 11 4,700 3,250 June 17 June 19 3,000 6,400 June 3

2,000 June 6

- Common Stock (SE) + - Retained Earnings (SE) +

12,000 June 1 June 25 900

+ Rent Expense (E) -

June 2 950

- Service Fees Earned (R) + + Utilities Expense (E) -

4,700 June 11 June 30 350

+ Salaries Expense (E) -

June 30 2,500

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-9

M3-22 (45 minutes) a.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income April 1. Invested

$9,000 in cash. +9,000

Cash

=

+9,000 Common

Stock

-

=

April 2. Paid $2,850 cash for lease.

-2,850 Cash

+2,850 Prepaid Van

Lease

=

-

=

April 3. Borrowed $10,000.

+10,000 Cash

=

+10,000 Note

Payable

-

=

April 3. Purchased $5,500 equipment for $2,500 cash with rest on account.

-2,500 Cash

+5,500 Equipment

=

+3,000 Accounts Payable

-

=

April 4. Paid $4,300 cash for supplies.

-4,300 Cash

+4,300 Supplies

=

-

=

April 7. Paid $350 cash for ad.

-350 Cash

=

-350 Retained Earnings

-

+350 Ad.

Expense =

-350

April 21. Billed $3,500 for services

+3,500 Accounts

Receivable =

+3,500 Retained Earnings

+3,500 Cleaning

Fees Earned

-

=

+3,500

April 23. Paid $3,000 cash on account.

-3,000 Cash

=

-3,000 Accounts Payable

-

=

April 28. Collected $2,300 on account.

+2,300 Cash

-2,300 Accounts

Receivable =

-

=

April 29. Paid $1,000 cash dividend.

-1,000 Cash

=

-1,000 Retained Earnings

-

=

April 30. Paid $1,750 cash for wages.

-1,750 Cash

=

-1,750 Retained Earnings

-

+1,750 Wages

Expense =

-1,750

April 30. Paid $995 cash for gas.

-995 Cash

=

-995 Retained Earnings

-

+995 Van Fuel Expense

= -995

TOTALS 4,555 + 13,850 = 10,000 + 9,000 + -595 3,500 - 3,095 = 405

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-10

b. April 1 Cash (+A) 9,000 Common stock (+SE) 9,000 Owner invested cash for stock. 2 Prepaid van lease (+A) 2,850 Cash (-A) 2,850 Paid six months' lease on van. 3 Cash (+A) 10,000 Notes payable (+L) 10,000 Borrowed money from bank for one year at 10% interest. 3 Equipment (+A) 5,500 Cash (-A) 2,500 Accounts payable (+L) 3,000 Purchased $5,500 of equipment; paid $2,500 down with balance due in 30 days. 4 Supplies (+A) 4,300 Cash (-A) 4,300 Purchased supplies for cash. 7 Advertising expense (+E, -SE) 350 Cash (-A) 350 Paid for April advertising. 21 Accounts receivable (+A) 3,500 Cleaning fees earned (+R, +SE) 3,500 Billed customers for services. 23 Accounts payable (-L) 3,000 Cash (-A) 3,000 Payment on account. 28 Cash (+A) 2,300 Accounts receivable (-A) 2,300 Collections from customers on account. 29 Retained earnings (-SE) 1,000 Cash (-A) 1,000 Issued cash dividends.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-11

30 Wages expense (+E, -SE) 1,750 Cash (-A) 1,750 Paid wages for April. 30 Van fuel expense (+E, -SE) 995 Cash (-A) 995 Paid for gasoline used in April.

c.

+ Cash (A) - + Accounts Receivable (A) -

April 1 9,000 2,850 April 2 April 21 3,500 2,300 April 28

3 10,000 2,500 3 28 2,300 4,300 4

350 7 + Prepaid Van Lease (A) -

3,000 23 April 2 2,850

1,000 29

1,750 30 + Equipment (A) -

995 30 April 3 5,500

+ Supplies(A) - - Notes Payable (L) +

April 4 4,300 10,000 April 3

- Accounts Payable (L) + - Retained Earnings (SE) +

April 23 3,000 3,000 April 3 April 29 1,000

- Common Stock (SE) + - Cleaning Fees Earned (R) +

9,000 April 1 3,500 April 21

+ Advertising Expense (E) - + Wages Expense (E) -

April 7 350 April 30 1,750

+ Van Fuel Expense (E) -

April 30 995

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-12

M3-23 (20 minutes) a.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income 1. Received $20,100

in advance for contract work.

+20,100 Cash

=

+20,100Unearned Service

Fees

-

=

Jan. 1 Cash (+A) 20,100 Unearned service fees (+L) 20,100 To record fee received in advance. b.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income 2. Adjusting entry for

work completed by Jan. 31.

=

-3,350 Unearned Service

Fees

+3,350 Retained Earnings

+3,350 Service

Fees -

=

+3,350

Jan. 31 Unearned service fees (-L) 3,350 Service fees (+R, +SE) 3,350 To reflect January service fees earned on contract ($20,100/6 = $3,350). c.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

3. Adjusting entry for fees earned but not billed.

+570 Fees

Receivable =

+570 Retained Earnings

+570 Service

Fees -

=

+570

Jan. 31 Fees receivable (+A) 570 Service fees (+R, +SE) 570 To record unbilled service fees earned at January 31.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-13

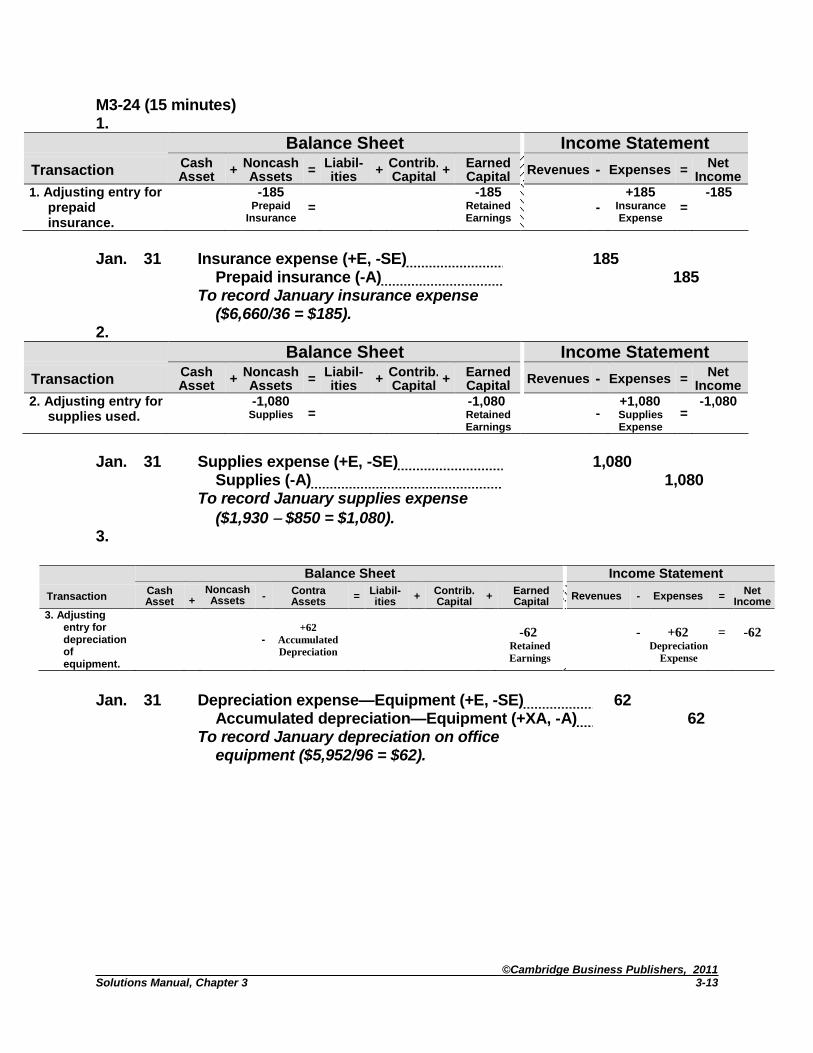

M3-24 (15 minutes) 1.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income 1. Adjusting entry for

prepaid insurance.

-185 Prepaid

Insurance =

-185 Retained Earnings

-

+185 Insurance Expense

= -185

Jan. 31 Insurance expense (+E, -SE) 185 Prepaid insurance (-A) 185 To record January insurance expense ($6,660/36 = $185). 2.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

2. Adjusting entry for supplies used.

-1,080 Supplies =

-1,080 Retained Earnings

-

+1,080 Supplies Expense

= -1,080

Jan. 31 Supplies expense (+E, -SE) 1,080 Supplies (-A) 1,080 To record January supplies expense

($1,930 $850 = $1,080). 3.

Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

3. Adjusting entry for depreciation of equipment.

-

+62

Accumulated

Depreciation

-62 Retained

Earnings

-

+62 Depreciation

Expense

=

-62

Jan. 31 Depreciation expense—Equipment (+E, -SE) 62 Accumulated depreciation—Equipment (+XA, -A) 62 To record January depreciation on office equipment ($5,952/96 = $62).

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-14

4.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income 4. Adjusting entry for

rent.

=

-875 Unearned

Rent Revenue

+875 Retained Earnings

+875 Rent

Revenue -

=

+875

Jan. 31 Unearned rent revenue (-L) 875 Rent revenue (+R, +SE) 875 To record portion of advance rent earned in January. 5.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income 5. Adjusting entry for

accrued salaries.

= +490

Salaries Payable

-490

Retained Earnings

-

+490 Salaries Expense

= -490

Jan. 31 Salaries expense (+E, -SE) 490 Salaries payable (+L) 490 To record accrued salaries at January 31.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-15

M3-25 (10 minutes) (All amounts in $ millions.) a.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income Inventory purchases

(total).

+2,913.49 Inventory

=

+2,913.49 Accounts Payable

-

=

Inventories (+A)……………………….. 2,913.49 Accounts payable (+L)…………….. 2,913.49 To record total purchases made at various dates. b. Beginning AP balance + Purchases – Payments = Ending AP balance, or $2,980.13 = $365.75 + $2,913.49 - $299.11 = Payments. c.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net Income

Adjusting entry for cost of goods sold for 2009.

-2,946.08 Inventory

=

-2,946.08 Retained Earnings

-

+2,946.08

Cost of Goods Sold

=

-2,946.08

* Beginning Inv balance + Purchases – Cost of goods sold = Ending Inv balance, or $2,946.08 = $887.36 + $2,913.49 – $854.77 = COGS

Cost of goods sold (+E, -SE)…………………... 2,946.08 Inventories (-A)………………………………… 2,946.08 To record cost of goods sold for the year ended 1/31/2009. M3-26 (15 minutes)

Architect Services Company Statement of Stockholders’ Equity For Year Ended December 31, 2011

Common Stock

Retained Earnings

Total Stockholders’

Equity

Balance at December 31, 2010 ............ $30,000 $18,000 $48,000

Stock issuance ..................................... 6,000 6,000

Dividends ............................................. (9,700) (9,700)

Net income ........................................... _____ 29,900 29,900

Balance at December 31, 2011 ............ $36,000 $38,200 $74,200

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-16

M3-27 (5 minutes) Ending balance = Beginning balance + Credit from closing revenue – Debit from closing expenses: $137,600 = $99,000 + $347,400 - $308,800 M3-28 (15 minutes) a.

Date 2010 Description Debit Credit Dec. 31 Commissions revenue (-R) 84,900 Retained earnings (+SE) 84,900 To close the revenue account. 31 Retained earnings (-SE) 55,900 Wages expense (-E) 36,000 Insurance expense (-E) 1,900 Utilities expense (-E) 8,200 Depreciation expense (-E) 9,800 To close the expense accounts. Closing the revenue and expense accounts into retained earnings has the effect of increasing the retained earnings balance by an amount equal to net income (revenue minus expenses). The balance of Smith’s Retained Earnings after closing entries are posted is

$101,100 credit ($72,100 + $29,000).

b.

+ Wages Expense (E) - + Utilities Expense (E) -

Bal. 36,000 36,000 (2)Dec. 31 Bal. 8,200 8,200 (2) Dec. 31

Bal. 0 Bal. 0

+ Insurance Expense (E) - - Commissions Revenue (R) +

Bal. 1,900 1,900 (2)Dec. 31 (1)Dec. 31 84,000 84,900 Bal.

Bal. 0 0 Bal.

+ Depreciation Expense (E) - - Retained Earnings (SE) +

Bal. 9,800 9,800 (2)Dec. 31 (2)Dec. 31 55,900 72,100 Bal.

Bal. 0 84,900 (1)Dec.31

101,100 Bal. Dec.31

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-17

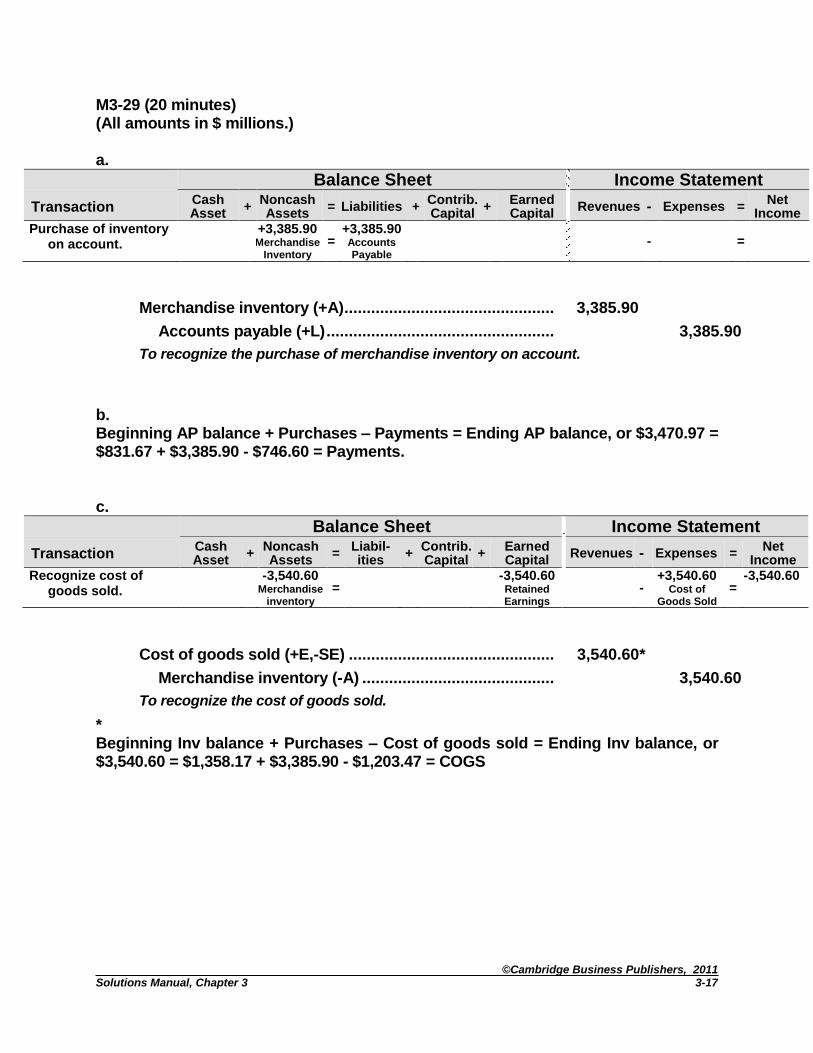

M3-29 (20 minutes) (All amounts in $ millions.) a.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income Purchase of inventory

on account.

+3,385.90 Merchandise

Inventory =

+3,385.90 Accounts Payable

-

=

Merchandise inventory (+A) .................................................. 3,385.90

Accounts payable (+L) ...................................................... 3,385.90

To recognize the purchase of merchandise inventory on account.

b. Beginning AP balance + Purchases – Payments = Ending AP balance, or $3,470.97 = $831.67 + $3,385.90 - $746.60 = Payments. c.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income Recognize cost of

goods sold.

-3,540.60

Merchandise inventory

=

-3,540.60 Retained Earnings

-

+3,540.60 Cost of

Goods Sold =

-3,540.60

Cost of goods sold (+E,-SE) ................................................. 3,540.60*

Merchandise inventory (-A) .............................................. 3,540.60

To recognize the cost of goods sold.

*

Beginning Inv balance + Purchases – Cost of goods sold = Ending Inv balance, or $3,540.60 = $1,358.17 + $3,385.90 - $1,203.47 = COGS

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-18

M3-30 (10 minutes) a.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income a. Dec. 31 Interest

earned.

+600

Interest Receivable

=

+600

Retained Earnings

+600 Interest Income

-

= +600

Dec. 31 Interest receivable (+A) 600 Interest income (+R, +SE) 600 To record accrued interest income. b. Dec. 31 Interest income (-R) 2,400 Retained earnings (+SE) 2,400 To close the Interest Income account. c.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income c. 1/31 Receipt of

$900 interest. +900 Cash

-600 Interest

Receivable =

+ 300 Retained Earnings

+300 Interest Income

-

= +300

2011 Jan. 31 Cash (+A) 900 Interest income (+R, +SE) 300 Interest receivable (-A) 600 To record cash receipt of interest.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-19

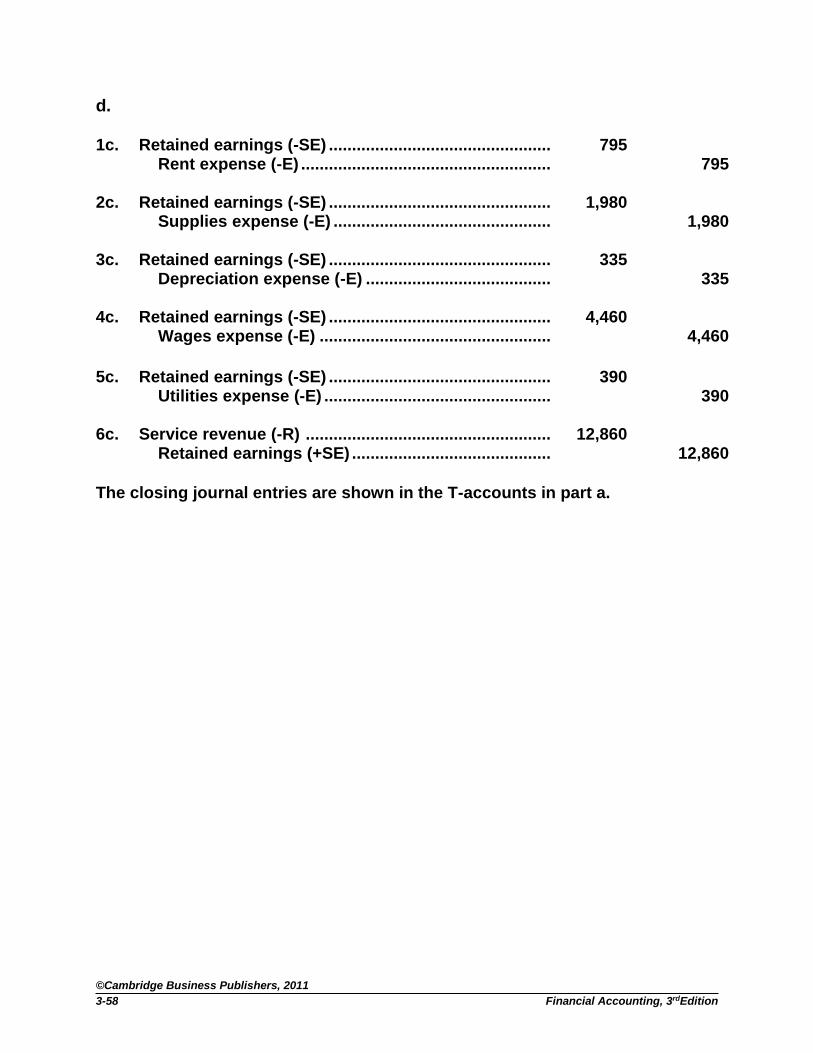

Exercises E3-31 (30 minutes) a. Dec. 31 Service fees earned (-R,-SE) 80,300 Retained earnings (+SE) 80,300 To close the revenue account. 31 Retained earnings (-SE) 82,300 Rent expense (-E) 20,800 Salaries expense (-E) 45,700 Supplies expense (-E) 5,600 Depreciation expense (-E) 10,200 To close the expense accounts.

b.

+ Rent Expense (E) - + Supplies Expense (E) -

Bal. 20,800 20,800 (2) Bal. 5,600 5,600 (2)

Bal. 0 Bal. 0

+ Depreciation Expense (E) -

Bal. 10,200 10,200 (2)

Bal. 0

+ Salaries Expense (E) - - Service Fees Earned (R) +

Bal. 45,700 45,700 (2) (1) 80,300 80,300 Bal.

Bal. 0 0 Bal.

- Retained Earnings (SE) +

(2) 82,300 67,000 Bal. 80,300 (1)

65,000 Bal.

Brooks Consulting earned a loss during the period (expenses exceeded revenues by $2,000), so the ending retained earnings is lower than that beginning retained earnings (even if no dividends were paid).

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-20

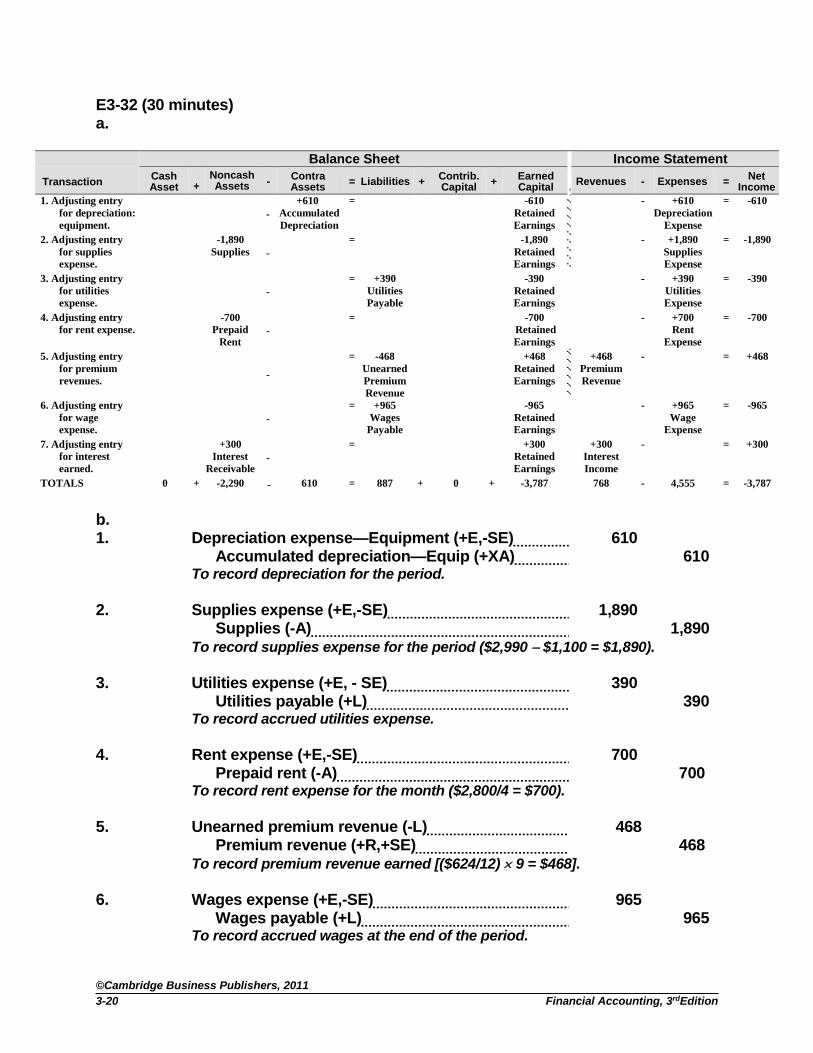

E3-32 (30 minutes) a.

Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

1. Adjusting entry

for depreciation:

equipment.

-

+610

Accumulated

Depreciation

= -610

Retained

Earnings

- +610

Depreciation

Expense

= -610

2. Adjusting entry

for supplies

expense.

-1,890

Supplies -

= -1,890

Retained

Earnings

- +1,890

Supplies

Expense

= -1,890

3. Adjusting entry

for utilities

expense.

-

= +390

Utilities

Payable

-390

Retained

Earnings

- +390

Utilities

Expense

= -390

4. Adjusting entry

for rent expense.

-700

Prepaid

Rent -

= -700

Retained

Earnings

- +700

Rent

Expense

= -700

5. Adjusting entry

for premium

revenues.

-

= -468

Unearned

Premium

Revenue

+468

Retained

Earnings

+468

Premium

Revenue

- = +468

6. Adjusting entry

for wage

expense.

-

= +965

Wages

Payable

-965

Retained

Earnings

- +965

Wage

Expense

= -965

7. Adjusting entry

for interest

earned.

+300

Interest

Receivable -

= +300

Retained

Earnings

+300

Interest

Income

- = +300

TOTALS 0 + -2,290 - 610 = 887 + 0 + -3,787 768 - 4,555 = -3,787

b. 1. Depreciation expense—Equipment (+E,-SE) 610 Accumulated depreciation—Equip (+XA) 610 To record depreciation for the period.

2. Supplies expense (+E,-SE) 1,890 Supplies (-A) 1,890 To record supplies expense for the period ($2,990 $1,100 = $1,890).

3. Utilities expense (+E, - SE) 390 Utilities payable (+L) 390 To record accrued utilities expense. 4. Rent expense (+E,-SE) 700 Prepaid rent (-A) 700 To record rent expense for the month ($2,800/4 = $700).

5. Unearned premium revenue (-L) 468 Premium revenue (+R,+SE) 468 To record premium revenue earned [($624/12) 9 = $468].

6. Wages expense (+E,-SE) 965 Wages payable (+L) 965 To record accrued wages at the end of the period.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-21

7. Interest receivable (+A) 300 Interest income (+R,+SE) 300 To accrue interest earned but not yet received.

E3-33 (15 minutes) a.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

a. Adjusting entry for salaries expense.

=

+4,700 Salaries Payable

-4,700

Retained Earnings

-

+4,700 Salaries Expense

= -4,700

2010 Dec. 31 Salaries expense (+E,-SE) 4,700 Salaries payable (+L) 4,700 To record accrued salaries payable. b. 31 Retained earnings (-RE) 250,000 Salaries expense (-E) 250,000 To close the Salaries Expense account. c.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

c. Paid salaries. -12,000 Cash

=

-4,700 Salaries Payable

-7,300

Retained Earnings

-

+7,300 Salary Expense

= -7,300

2011 Jan. 7 Salaries payable (-L) 4,700 Salaries expense (+E,-SE) 7,300 Cash (-A) 12,000 To record payment of salaries.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-22

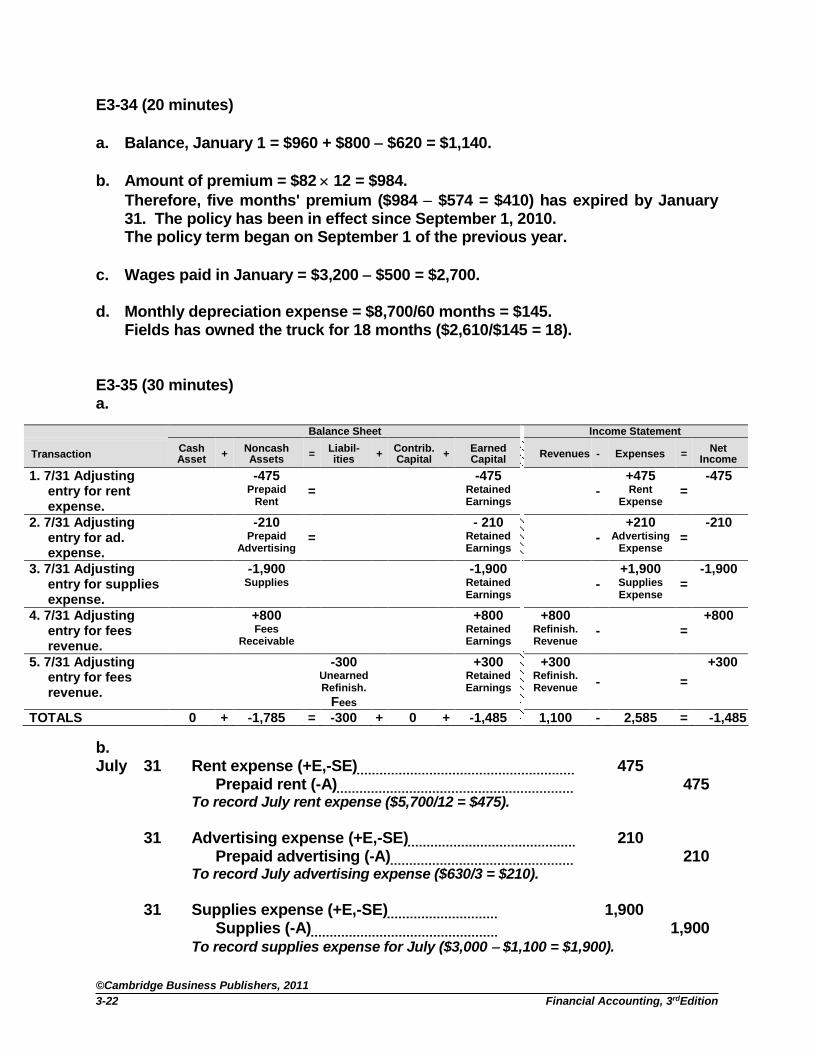

E3-34 (20 minutes)

a. Balance, January 1 = $960 + $800 $620 = $1,140.

b. Amount of premium = $82 12 = $984.

Therefore, five months' premium ($984 $574 = $410) has expired by January 31. The policy has been in effect since September 1, 2010.

The policy term began on September 1 of the previous year.

c. Wages paid in January = $3,200 $500 = $2,700. d. Monthly depreciation expense = $8,700/60 months = $145. Fields has owned the truck for 18 months ($2,610/$145 = 18). E3-35 (30 minutes) a.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil- ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

1. 7/31 Adjusting entry for rent expense.

-475 Prepaid

Rent =

-475 Retained Earnings

-

+475 Rent

Expense =

-475

2. 7/31 Adjusting entry for ad. expense.

-210 Prepaid

Advertising =

- 210 Retained Earnings

-

+210 Advertising

Expense =

-210

3. 7/31 Adjusting entry for supplies expense.

-1,900 Supplies

-1,900 Retained Earnings

-

+1,900 Supplies Expense

= -1,900

4. 7/31 Adjusting entry for fees revenue.

+800 Fees

Receivable

+800 Retained Earnings

+800 Refinish. Revenue

-

= +800

5. 7/31 Adjusting entry for fees revenue.

-300 Unearned Refinish.

Fees

+300 Retained Earnings

+300 Refinish. Revenue -

=

+300

TOTALS 0 + -1,785 = -300 + 0 + -1,485 1,100 - 2,585 = -1,485

b. July 31 Rent expense (+E,-SE) 475 Prepaid rent (-A) 475 To record July rent expense ($5,700/12 = $475). 31 Advertising expense (+E,-SE) 210 Prepaid advertising (-A) 210 To record July advertising expense ($630/3 = $210).

31 Supplies expense (+E,-SE) 1,900 Supplies (-A) 1,900 To record supplies expense for July ($3,000 $1,100 = $1,900).

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-23

31 Fees receivable (+A) 800 Refinishing fees revenue (+R,+SE) 800 To record unbilled revenue earned during July.

31 Unearned refinishing fees (-L) 300 Refinishing fees revenue (+R,+SE) 300 To record portion of advance fees earned in July ($600/2 = $300). c.

+ Prepaid Rent (A) - + Supplies (A) -

Bal. 5,700 475 (1) Bal. 3,000 1,900 (3)

Bal. 5,225 Bal. 1,100

+ Prepaid Advertising (A) - - Unearned Finishing Fees (L) +

Bal. 630 210 (2) (5) 300 600 Bal.

Bal. 420 300 Bal.

+ Fees Receivable (A) - - Refinishing Fees Revenue (R) +

(4) 800 2,500 Bal.

800 (4) 300 (5)

3,600 Bal.

+ Supplies Expense (E) -

(3) 1,900

+ Advertising Expense(E) -

(2) 210

+ Rent Expense (E) -

(1) 475

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-24

E3-36 (15 minutes) (All amounts in $ thousands.) a.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net Income

Recognize cost of

goods sold.

-242,265 Inventory

=

-242,265 Retained Earnings

-

+242,265

Cost of Goods Sold

=

-242,265

Cost of goods sold (+E,-SE) ................................................. 242,265*

Inventory (-A) .................................................................... 242,265

To recognize the cost of goods sold.

*Beginning Inv balance + Cost of acquisition – Cost of goods sold = Ending Inv balance, so $242,265 = $110,596 + $178,519 - $46,850 = COGS

b. Beginning compensation payable + Compensation expense – Compensation

paid = Ending compensation payable, so $10,070 + $40,000 – Payments = $10,204

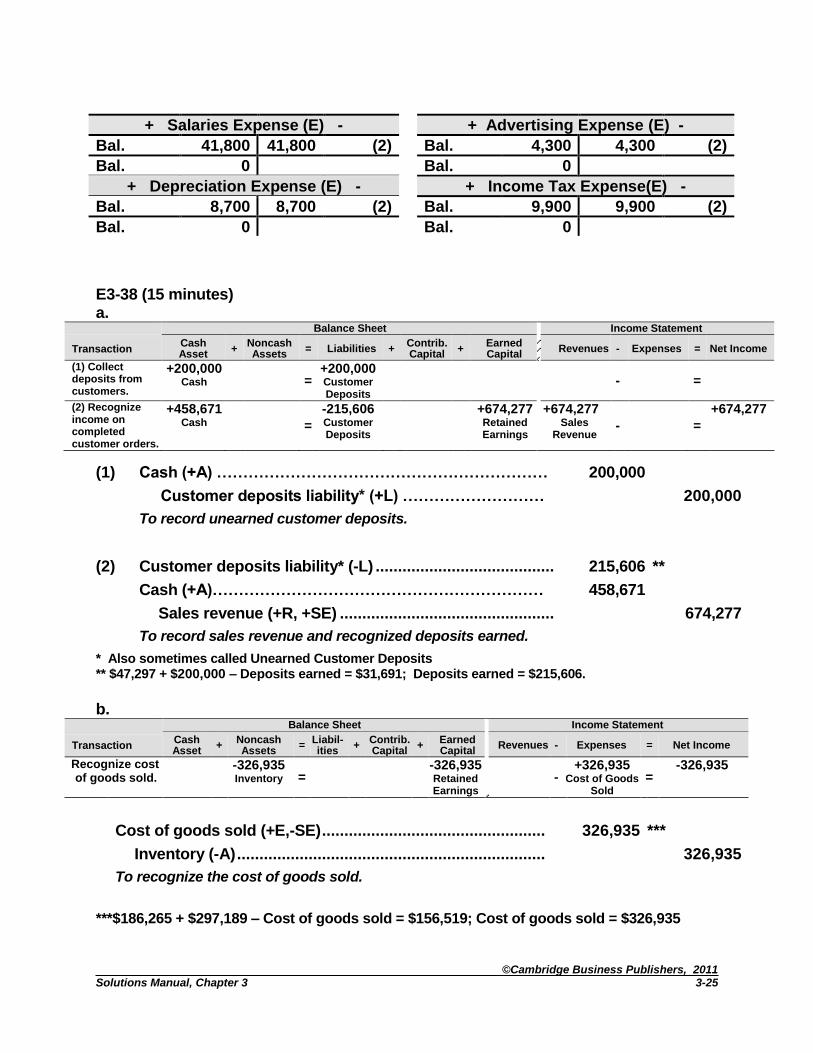

Payments = $39,866 E3-37 (30 minutes) a. Dec. 31 Service fees earned (-R) 92,500 Interest income (-R) 2,200 Retained earnings (+SE) 94,700 To close the revenue accounts. 31 Retained earnings (-SE) 64,700 Salaries expense (-E) 41,800 Advertising expense (-E) 4,300 Depreciation expense (-E) 8,700 Income tax expense (-E) 9,900 To close the expense accounts. b.

- Retained Earnings (SE) + - Service Fees Earned (R) +

(2) 64,700 42,700 Bal. (1) 92,500 92,500 Bal.

94,700 (1) 0 Bal.

72,700 Bal. - Interest Income (R) +

(1) 2,200 2,200 Bal.

0 Bal.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-25

+ Salaries Expense (E) - + Advertising Expense (E) -

Bal. 41,800 41,800 (2) Bal. 4,300 4,300 (2)

Bal. 0 Bal. 0

+ Depreciation Expense (E) - + Income Tax Expense(E) -

Bal. 8,700 8,700 (2) Bal. 9,900 9,900 (2)

Bal. 0 Bal. 0

E3-38 (15 minutes) a.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net Income

(1) Collect deposits from customers.

+200,000 Cash

=

+200,000 Customer Deposits

-

=

(2) Recognize income on completed customer orders.

+458,671 Cash

=

-215,606 Customer Deposits

+674,277 Retained Earnings

+674,277 Sales

Revenue -

=

+674,277

(1) Cash (+A) ……………………………………………………… 200,000

Customer deposits liability* (+L) ……………………… 200,000

To record unearned customer deposits.

(2) Customer deposits liability* (-L) ........................................... 215,606 **

Cash (+A)……………………………………………………… 458,671

Sales revenue (+R, +SE) ................................................... 674,277

To record sales revenue and recognized deposits earned. * Also sometimes called Unearned Customer Deposits ** $47,297 + $200,000 – Deposits earned = $31,691; Deposits earned = $215,606.

b.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net Income

Recognize cost of goods sold.

-326,935 Inventory =

-326,935 Retained Earnings

-

+326,935

Cost of Goods Sold

= -326,935

Cost of goods sold (+E,-SE) .................................................. 326,935 ***

Inventory (-A) ..................................................................... 326,935

To recognize the cost of goods sold.

***$186,265 + $297,189 – Cost of goods sold = $156,519; Cost of goods sold = $326,935

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-26

E3-39 (40 minutes) a.

Solomon Corporation Income Statement

For Year Ended December 31, 2011

Service fees earned .............................................................................. $71,000

Rent expense ........................................................................................ (18,000)

Salaries expense .................................................................................. (37,100)

Depreciation expense…………………………………….. (7,000)

Net income ............................................................................................ $8,900

Solomon Corporation Statement of Stockholders’ Equity For Year Ended December 31, 2011

Common Stock

Retained Earnings

Total Stockholders’

Equity

Balance at December 31, 2010 ............ $43,000 $20,600* $63,600

Stock issuance .....................................

Dividends ............................................. (8,000) (8,000)

Net income ........................................... _____ 8,900 8,900

Balance at December 31, 2011 ............ $43,000 $21,500 $64,500

*12,600 + 8,000 The dividend was paid and debited to retained earnings prior to the end of the period.

Solomon Corporation

Balance Sheet December 31, 2011

Assets Liabilities

Cash $ 4,000 Notes payable $ 10,000

Accounts receivable 6,500 Total Liabilities 10,000

Equipment $ 78,000

Less:Accumulated depreciation

14,000 64,000 Owners’ Equity

Common stock 43,000

Retained earnings 21,500

Total Assets $74,500 Total Liabilities and Owners’ Equity $74,500

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-27

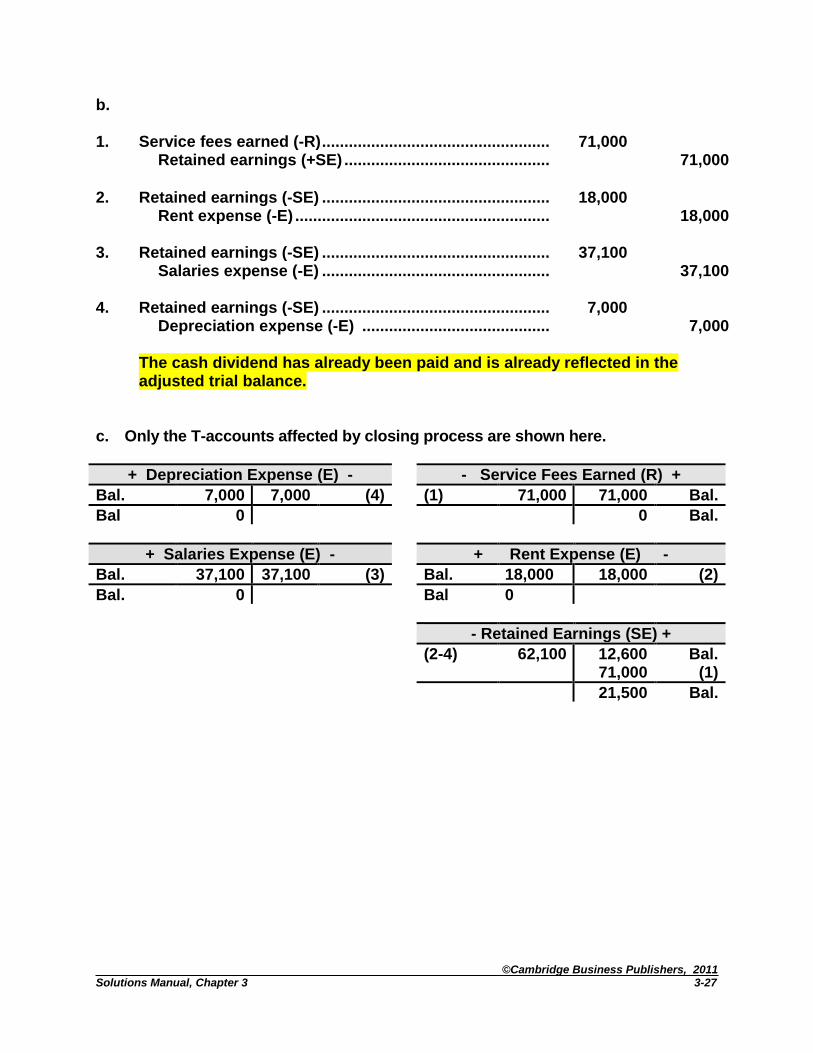

b. 1. Service fees earned (-R) ....................................................... 71,000 Retained earnings (+SE) .................................................. 71,000

2. Retained earnings (-SE) ....................................................... 18,000 Rent expense (-E) ............................................................. 18,000 3. Retained earnings (-SE) ....................................................... 37,100 Salaries expense (-E) ....................................................... 37,100 4. Retained earnings (-SE) ....................................................... 7,000 Depreciation expense (-E) .............................................. 7,000 The cash dividend has already been paid and is already reflected in the

adjusted trial balance. c. Only the T-accounts affected by closing process are shown here.

+ Depreciation Expense (E) - - Service Fees Earned (R) +

Bal. 7,000 7,000 (4) (1) 71,000 71,000 Bal.

Bal 0 0 Bal.

+ Salaries Expense (E) - + Rent Expense (E) -

Bal. 37,100 37,100 (3) Bal. 18,000 18,000 (2)

Bal. 0 Bal 0

- Retained Earnings (SE) +

(2-4) 62,100 12,600 71,000

Bal. (1)

21,500 Bal.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-28

PROBLEMS P3-40 (90 minutes) a.

+ Cash (A) - + Accounts Receivable (A) -

Apr. 1 11,500 2,880 Apr. 1 Apr. 12 5,500 4,900 Apr. 18 5 1,800 6,100 2 30 4,000

18 4,900 1,000 2 Bal. 4,600 675 29

100 30 + Supplies (A) -

2,500 30 Apr. 5 1,200

Bal. 4,945 Unadj. bal. 1,200 800 (d) Apr. 30

Adj. bal. 400

+ Prepaid Insurance (A) -

Apr. 1 2,880 + Trucks (A) -

Unadj. bal. 2,880 120 (d) Apr. 30 Apr. 2 6,100

Adj bal. 2,760 Bal. 6,100

+ Equipment (A) - - Accounts Payable (L) +

Apr. 2 3,100 2,100 Apr. 2

Bal. 3,100 1,200 5

3,300 Bal.

- Roofing Fees Earned (R) + - Unearned Roofing Fees (L) +

5,500 Apr. 12 1,800 Apr. 5

4,000 30 Apr. 30 (d) 450 1,800 Unadj. bal

9,500 Unadj. bal. 1,350 Adj. Bal 450 (d) 30

9,950 Adj. Bal.

+ Supplies Expense (E) - - Common Stock (SE) +

Apr. 30 (d) 800 11,500 Apr. 1

Adj. Bal. 800 11,500 Bal.

+ Advertising Expense (E) - + Fuel Expense (E) -

Apr. 30 100 Apr. 29 675

Bal. 100 Bal. 675

+ Insurance Expense (E) - + Wages Expense (E) -

Apr. 30 (d) 120 Apr. 30 2,500

Adj. Bal. 120 Bal. 2,500

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-29

+ Depreciation Expense – Equip. (E) - - Accumulated Deprec. – Equip. (XA) +

Apr. 30 (d) 35 35 (d) Apr. 30

Adj. Bal. 35 35 Adj. Bal.

+ Depreciation Expense - Trucks (E) - - Accumulated Deprec. – Trucks (XA) +

Apr. 30 (d) 125 125 (d) Apr. 30

Adj. Bal. 125 125 Adj. Bal b.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

Apr. 1. Cash received for stock.

+11,500 Cash

=

+11,500 Common

Stock

-

=

Apr. 1. Purchase liability insurance.

-2,880 Cash

+2,880 Prepaid

Insurance =

-

=

Apr. 2. Purchase truck for cash.

-6,100 Cash

+ 6,100 Truck =

-

=

Apr. 2. Purchase equipment.

-1,000 Cash

+3,100 Equipment =

+2,100 Accounts Payable

-

=

Apr. 5. Purchase supplies on account.

+ 1,200 Supplies =

+1,200 Accounts Payable

-

=

Apr. 5. Cash in advance for roofing repairs.

+1,800 Cash

=

+1,800 Unearned Roofing

Fees

-

=

Apr. 12. Bill customers for services.

+5,500 Accounts

Receivable =

+5,500 Retained Earnings

+5,500 Roofing Fees

Revenue -

=

+5,500

Apr. 18. Collected cash on account.

+4,900 Cash

-4,900 Accounts

Receivable =

-

=

Apr. 29. Paid cash for fuel.

-675 Cash

=

-675 Retained Earnings

-

+675 Fuel

Expense

= -675

Apr. 30. Paid cash for ads.

-100 Cash

=

-100 Retained Earnings

-

+100 Ad. Expense =

-100

Apr. 30. paid cash wages.

-2,500 Cash

=

-2,500 Retained Earnings

-

+2,500 Wages

Expense =

-2,500

Apr. 30. Bill customers for services.

+4,000 Accounts

Receivable =

+4,000 Retained Earnings

+4,000 Roofing fees

Earned -

=

+4,000

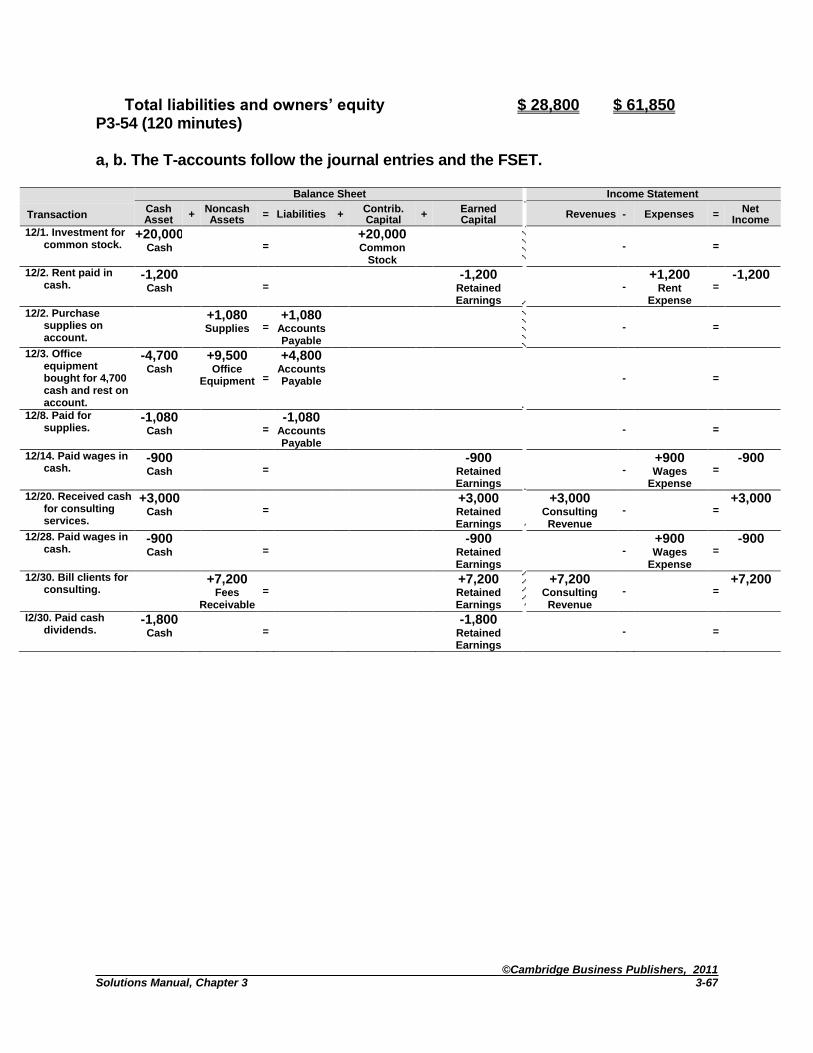

Totals 4,945 + 17,880 = 5,100 + 11,500 + 6,225 9,500 - 3,275 = 6,225

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-30

Date 2010 Description Debit Credit Apr. 1 Cash (+A) 11,500 Common stock (+SE) 11,500 Owner invested cash.

1 Prepaid insurance (+A) 2,880 Cash (-A) 2,880 Paid two-year premium on liability insurance policy.

2 Trucks (+A) 6,100 Cash (-A) 6,100 Purchased used truck for $6,100 cash.

2 Equipment (+A) 3,100 Cash (-A) 1,000 Accounts payable (+L) 2,100 Purchased ladders and other equipment, $1,000 down with $2,100 balance due in 30 days.

5 Supplies (+A) 1,200 Accounts payable (+L) 1,200 Purchased supplies on account.

5 Cash (+A) 1,800 Unearned roofing fees (+L) 1,800 Received advance payment for services.

12 Accounts receivable (+A) 5,500 Roofing fees earned (+R,+SE) 5,500 Billed customers for services.

18 Cash (+A) 4,900 Accounts receivable (-A) 4,900 Collection on account from customers.

29 Fuel expense (+E,-SE) 675 Cash (-A) 675 Paid truck fuel bill for April.

30 Advertising expense (+E,-SE) 100 Cash (-A) 100 Paid for April newspaper advertising.

30 Wages expense (+E, -SE) 2,500 Cash (-A) 2,500 Paid wages.

30 Accounts receivable (+A) 4,000 Roofing fees earned (+R, +SE) 4,000 Billed customeers for services.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-31

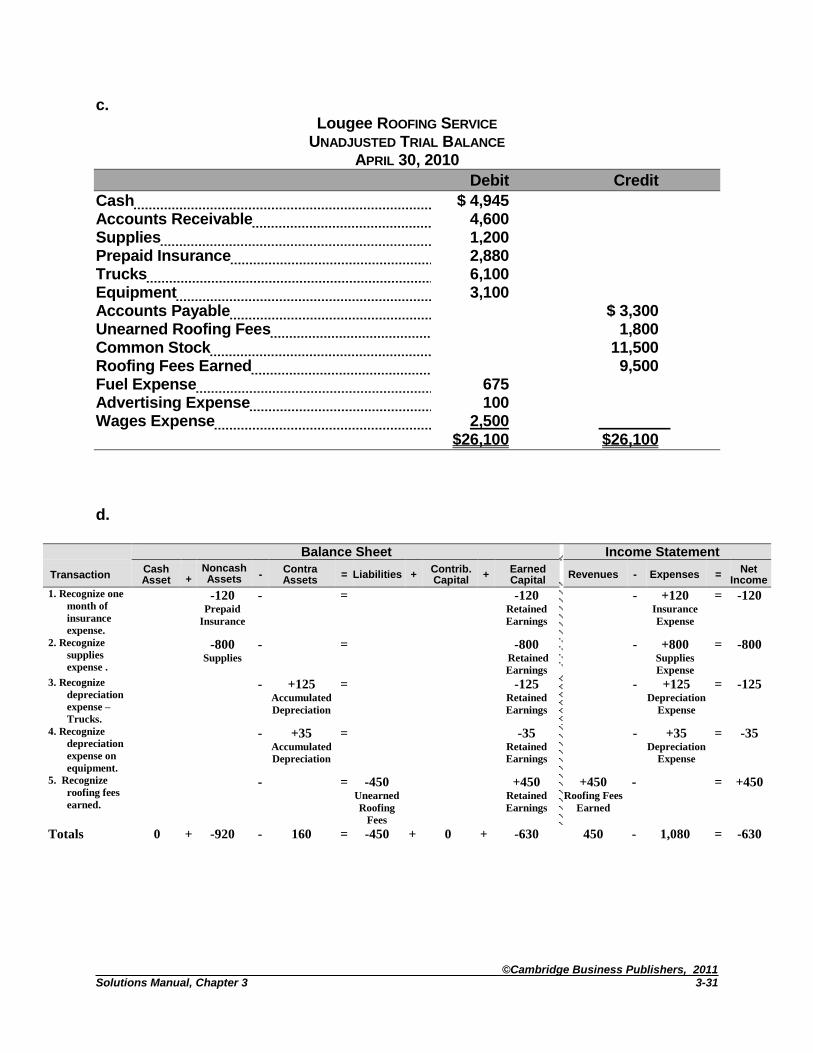

c. Lougee ROOFING SERVICE

UNADJUSTED TRIAL BALANCE APRIL 30, 2010

Debit Credit

Cash $ 4,945 Accounts Receivable 4,600 Supplies 1,200 Prepaid Insurance 2,880 Trucks 6,100 Equipment 3,100 Accounts Payable $ 3,300 Unearned Roofing Fees 1,800 Common Stock 11,500 Roofing Fees Earned 9,500 Fuel Expense 675 Advertising Expense 100 Wages Expense 2,500 $26,100 $26,100

d.

Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

1. Recognize one

month of

insurance

expense.

-120 Prepaid

Insurance

- = -120 Retained

Earnings

- +120 Insurance

Expense

= -120

2. Recognize

supplies

expense .

-800 Supplies

- = -800 Retained

Earnings

- +800 Supplies

Expense

= -800

3. Recognize

depreciation

expense –

Trucks.

- +125 Accumulated

Depreciation

= -125 Retained

Earnings

- +125 Depreciation

Expense

= -125

4. Recognize

depreciation

expense on

equipment.

- +35 Accumulated

Depreciation

= -35 Retained

Earnings

- +35 Depreciation

Expense

= -35

5. Recognize

roofing fees

earned.

- = -450 Unearned

Roofing

Fees

+450 Retained

Earnings

+450 Roofing Fees

Earned

- = +450

Totals 0 + -920 - 160 = -450 + 0 + -630 450 - 1,080 = -630

©Cambridge Business Publishers, 2011

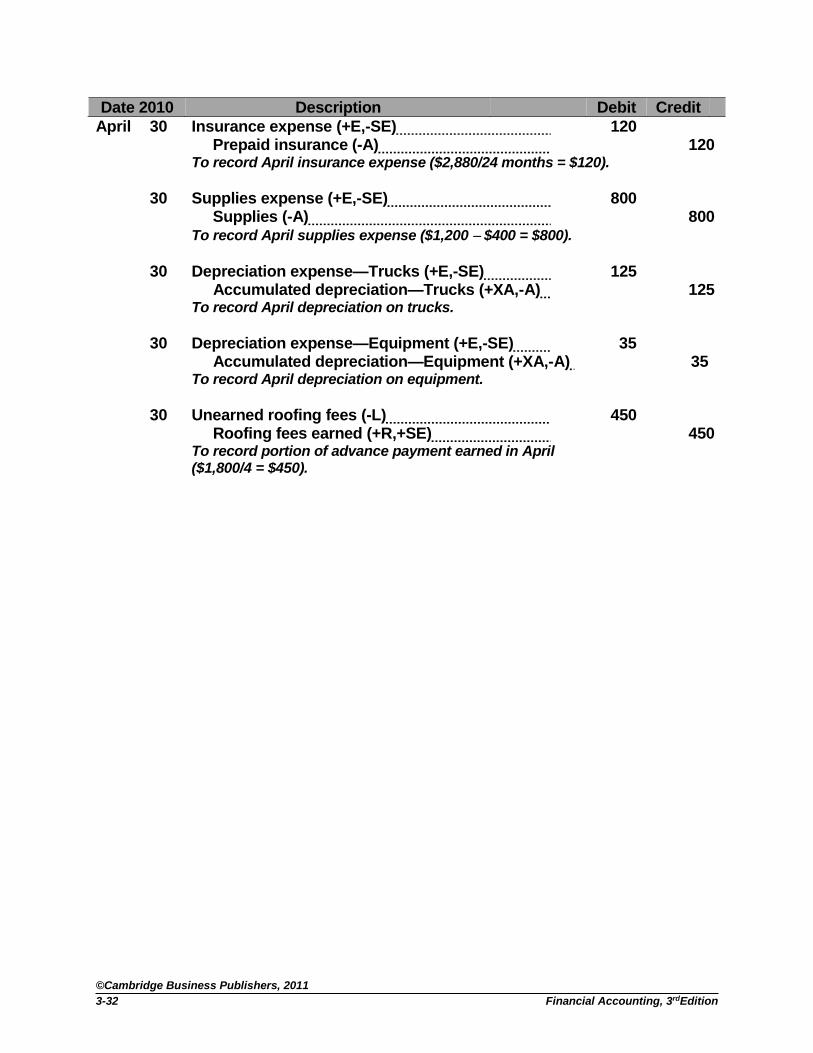

Financial Accounting, 3rdEdition 3-32

Date 2010 Description Debit Credit

April 30 Insurance expense (+E,-SE) 120 Prepaid insurance (-A) 120 To record April insurance expense ($2,880/24 months = $120).

30 Supplies expense (+E,-SE) 800 Supplies (-A) 800 To record April supplies expense ($1,200 $400 = $800).

30 Depreciation expense—Trucks (+E,-SE) 125 Accumulated depreciation—Trucks (+XA,-A) 125 To record April depreciation on trucks. 30 Depreciation expense—Equipment (+E,-SE) 35 Accumulated depreciation—Equipment (+XA,-A) 35 To record April depreciation on equipment. 30 Unearned roofing fees (-L) 450 Roofing fees earned (+R,+SE) 450 To record portion of advance payment earned in April ($1,800/4 = $450).

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-33

P3-41 (40 minutes) SnapShot Company

UNADJUSTED TRIAL BALANCE DECEMBER 31, 2010

a. Debit Credit Cash $2,150 Accounts Receivable 3,800 Prepaid Rent 12,600 Prepaid Insurance 2,970 Supplies 4,250 Equipment 22,800 Accounts Payable $1,910 Unearned Photography Fees 2,600 Common Stock 24,000 Photography Fees Earned 34,480 Wages Expense 11,000 Utilities Expense 3,420 ______ $62,990 $62,990

b.

Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

1. Fees earned

but not

received.

+925 Fees

Receivable

-

=

+925

Retained

Earnings

+925 Photography

Fees Earned

-

= +925

2. Recognize

depreciation

expense for

one year.

-

+2,280

Accumulated

Depreciation =

-2,280 Retained

Earnings

-

+2,280 Depreciation

Expense =

-2,280

3. Recognize

utilities

expense.

-

=

+400 Utilities

Payable

-400 Retained

Earnings

-

+400 Utilities

Expense =

-400

4. Recognize

rent

expense for

year.

-6,300 Prepaid

Rent -

=

-6,300 Retained

Earnings

-

+6,300 Rent

Expense =

-6,300

5. Recognize

photo

revenues.

-

=

-2,600 Unearned

Photo Fees

+2,600 Retained

Earnings

+2,600 Photography

Fee Earned -

=

+2,600

6. Recognize

insurance

expense.

-990 Prepaid

Insurance -

=

-990 Retained

Earnings

-

+990 Insurance

Expense =

-990

7. Recognize

supplies

expense.

-2,730 Supplies -

=

-2,730 Retained

Earnings

-

+2,730 Supplies

Expense =

-2,730

8. Recognize

wages

expense.

-

=

+375 Wages

Payable

-375 Retained

Earnings

-

+375 Wages

Expense =

-375

Totals 0 + -9,095 - 2,280 = -1,825 + 0 + -9,550 3,525 - 13,075 = -9,550

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-34

Date 2010 Description Debit Credit

Dec. 31 Fees receivable (+A) 925 Photography fees earned (+R, +SE) ` 925 To record revenue earned but not billed. 31 Depreciation expense (+E,-SE) 2,280 Accum. depreciation—Equipment (+XA, -A) 2,280 To record depreciation for the year ($22,800/10 years = $2,280). 31 Utilities expense (+E, -SE) 400 Utilities payable (+L) 400 To record estimated December utilities expense. 31 Rent expense (+E, -SE) 6,300 Prepaid rent (-A) 6,300 To record rent expense for the year ($12,600/2 years = $6,300). 31 Unearned photography fees (-L) 2,600 Photography fees earned (+R, +SE) 2,600 To record advance payments earned during the year. 31 Insurance expense (+E, -SE) 990 Prepaid insurance (-A) 990 To record insurance expense for the year ($2,970/3 years = $990). 31 Supplies expense (+E,-SE) 2,730 Supplies (-A) 2,730 To record supplies expense for the year

($4,250 $1,520 = $2,730). 31 Wages expense (+E, -SE) 375 Wages payable(+L) 375 To record unpaid wages at December 31.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-35

c.

+ Cash (A) - - Accounts Payable (L) + Unadj. bal. 2,150 1,910 Unadj. bal.

Adj. bal. 2,150 1,910 Adj. bal.

+ Accounts Receivable (A) - - Unearned Photo Fees (L) + Unadj. bal. 3,800 Dec.31 (5) 2,600 2,600 Unadj. bal.

Adj. bal. 3,800 0 Adj. bal.

+ Fees Receivable (A) - - Utilities Payable (L) +

Dec. 31 (1) 925 400 (3) Dec.31

Adj. bal. 925 400 Adj. bal.

+ Prepaid Rent (A) - - Wages Payable (L) + Unadj. bal. 12,600 6,300 (4) Dec.31 375 (8) Dec.31

Adj. bal. 6,300 375 Adj. bal.

+ Prepaid Insurance (A) - - Common Stock (SE) +

Unadj. bal. 2,970 990 (6) Dec.31 24,000 Unadj. bal.

Adj. bal. 1,980 24,000 Adj. bal.

+ Supplies (A) - - Photo Fees Earned (R) + Unadj. bal. 4,250 2,730 (7) Dec.31 34,480 Unadj. bal

Adj. bal. 1,520 925 (1) Dec.31

2,600 (5) Dec.31

38,005 Adj. bal.

+ Equipment (A) - + Wages Expense (E) - Unadj. bal. 22,800 Unadj. bal. 11,000 Adj. bal. 22,800 Dec.31 (8) 375

Adj. Bal. 11,375

- Accum. Depreciation – Equip. (XA) + + Utilities Expense (E) -

2,280 (2) Dec.31 Unadj. bal. 3,420

2,280 Adj. Bal. Dec.31 (3) 400

Adj. Bal. 3,820

+ Supplies Expense (E) - + Depreciation Expense – Equip. (E) - Dec. 31 (7) 2,730 Dec.31 (2) 2,280 Adj. bal. 2,730 Adj. Bal. 2,280

+ Insurance Expense (E) - + Rent Expense (E) - Dec. 31 (6) 990 Dec.31 (4) 6,300 Adj. bal. 990 Adj. Bal. 6,300

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-36

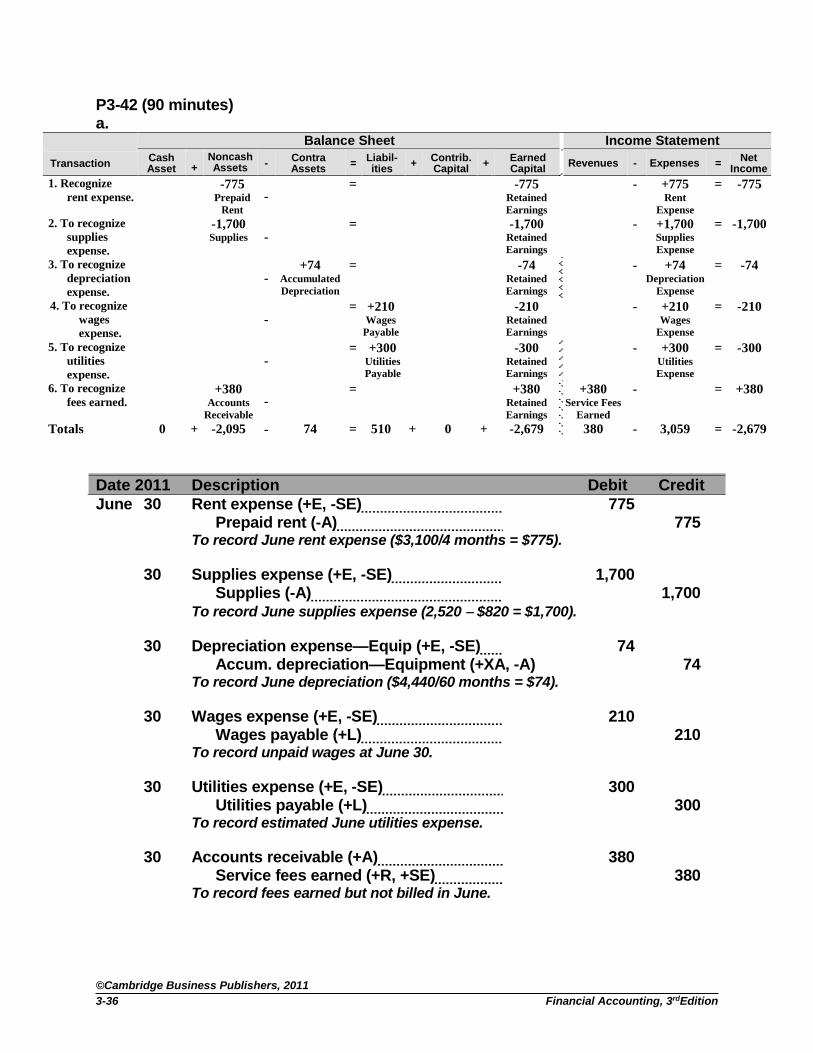

P3-42 (90 minutes) a.

Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

1. Recognize

rent expense. -775

Prepaid

Rent -

= -775 Retained

Earnings

- +775 Rent

Expense

= -775

2. To recognize

supplies

expense.

-1,700 Supplies -

= -1,700 Retained

Earnings

- +1,700 Supplies

Expense

= -1,700

3. To recognize

depreciation

expense.

-

+74

Accumulated

Depreciation

= -74 Retained

Earnings

- +74 Depreciation

Expense

= -74

4. To recognize

wages

expense.

-

= +210 Wages

Payable

-210 Retained

Earnings

- +210 Wages

Expense

= -210

5. To recognize

utilities

expense.

-

= +300 Utilities

Payable

-300 Retained

Earnings

- +300 Utilities

Expense

= -300

6. To recognize

fees earned. +380

Accounts

Receivable -

= +380 Retained

Earnings

+380 Service Fees

Earned

- = +380

Totals 0 + -2,095 - 74 = 510 + 0 + -2,679 380 - 3,059 = -2,679

Date 2011 Description Debit Credit

June 30 Rent expense (+E, -SE) 775 Prepaid rent (-A) 775 To record June rent expense ($3,100/4 months = $775).

30 Supplies expense (+E, -SE) 1,700 Supplies (-A) 1,700 To record June supplies expense (2,520 $820 = $1,700).

30 Depreciation expense—Equip (+E, -SE) 74 Accum. depreciation—Equipment (+XA, -A) 74 To record June depreciation ($4,440/60 months = $74).

30 Wages expense (+E, -SE) 210 Wages payable (+L) 210 To record unpaid wages at June 30.

30 Utilities expense (+E, -SE) 300 Utilities payable (+L) 300 To record estimated June utilities expense.

30 Accounts receivable (+A) 380 Service fees earned (+R, +SE) 380 To record fees earned but not billed in June.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-37

b.

+ Cash (A) - - Accounts Payable (L) + Unadj. bal 1,180 760 Unadj. bal

Adj. bal. 1,180 760 Adj. bal.

+ Accounts Receivable (A) - - Wages Payable (L) + Unadj. bal 450 210 (4) Jun.30

Jun. 30 (6) 380 210 Adj. bal.

Adj. bal. 830

- Utilities Payable (L) +

300 (5) Jun.30

300 Adj. bal.

+ Prepaid Rent (A) - - Retained Earnings (SE) + Unadj. bal 3,100 775 (1) Jun.30 5,300 Unadj. bal.

Adj. bal. 2,325

+ Rent Expense (E) - - Common Stock (SE) +

Jun.30 (1) 775 2,000 Unadj. bal

Adj. bal. 775 2,000 Adj. bal.

+ Supplies (A) - - Service Fees Earned (R) + Unadj. bal 2,520 1,700 (2) Jun.30 4,650 Unadj. bal

Adj. bal. 820 380 (6) Jun.30

5,030 Adj. bal.

+ Equipment (A) - + Wages Expense (E) - Unadj. bal 4,440 Unadj. bal 1,020 Adj. bal. 4,440 Jun.30 (4) 210

Adj. bal. 1,230

- Accum. Depreciation – Equip.(XA) + + Utilities Expense (E) -

74 (3) Jun.30 Jun.30 (5) 300

74 Adj. Bal. Adj. bal. 300

+ Supplies Expense (E) - + Depreciation Expense - EQPT (E) - Jun. 30 (2) 1,700 Jun.30 (3) 74 Adj. bal. 1,700 Adj. bal. 74

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-38

c.

Murdock Carpet Cleaners Income Statement

For Year Ended June 30, 2011

Revenues

Service fees…………………………………….…. $5,030

Expenses

Rent expense………………………………………. $ 775

Wages expense……………………………………. 1,230

Supplies expense…………………………………. 1,700

Utilities expense…………………………………... 300

Depreciation expense……………………………. 74

Total expenses……………………………………. 4,079

Net income………………………………………………… $ 951

Murdock Carpet Cleaners BALANCE SHEET June 30, 2011

Assets Liabilities

Cash $ 1,180 Accounts payable $ 760

Accounts receivable 830 Wages payable 210

Supplies 820 Utilities payable 300

Prepaid rent 2,325 Total Liabilities 1,270 Equipment $ 4,440

Less: Accumulated depreciation

74 4,366 Owners’ Equity

Common stock 2,000

Retained earnings 6,251

Total Assets $9,521 Total Liabilities and Owners’ Equity $9,521

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-39

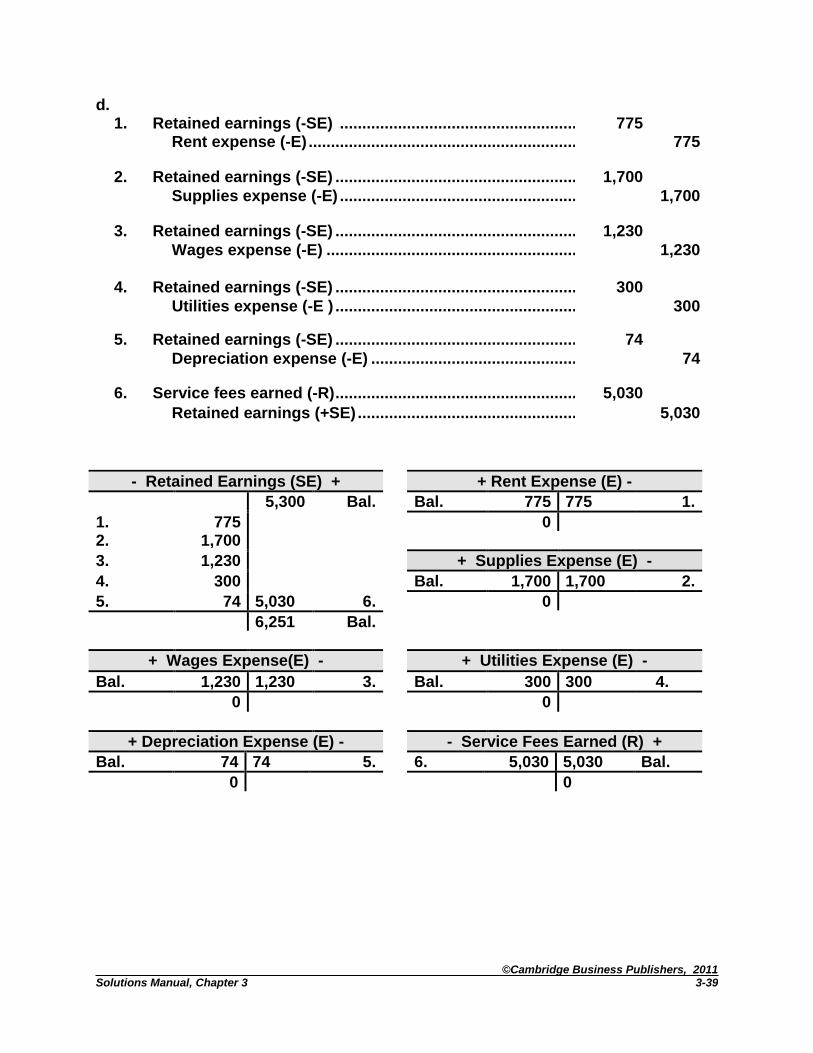

d. 1. Retained earnings (-SE) ...................................................... 775 Rent expense (-E) ............................................................. 775

2. Retained earnings (-SE) ....................................................... 1,700

Supplies expense (-E) ...................................................... 1,700

3. Retained earnings (-SE) ....................................................... 1,230

Wages expense (-E) ......................................................... 1,230

4. Retained earnings (-SE) ....................................................... 300

Utilities expense (-E ) ....................................................... 300

5. Retained earnings (-SE) ....................................................... 74

Depreciation expense (-E) ............................................... 74

6. Service fees earned (-R) ....................................................... 5,030

Retained earnings (+SE) .................................................. 5,030

- Retained Earnings (SE) + + Rent Expense (E) -

5,300 Bal. Bal. 775 775 1.

1. 775 0 2. 1,700

3. 1,230 + Supplies Expense (E) -

4. 300 Bal. 1,700 1,700 2.

5. 74 5,030 6. 0

6,251 Bal.

+ Wages Expense(E) - + Utilities Expense (E) -

Bal. 1,230 1,230 3. Bal. 300 300 4.

0 0

+ Depreciation Expense (E) - - Service Fees Earned (R) +

Bal. 74 74 5. 6. 5,030 5,030 Bal.

0 0

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-40

P 3-43 (30 minutes) a.

Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

1. Accrue salary

expense.

- = +720

Salaries

Payable

-720 Retained

Earnings

- +720 Salaries

Expense

= -720

2. Accrue

interest

expense.

- = +200

Interest

Payable

-200 Retained

Earnings

- +200 Interest

Expense

= -200

3. Accrue fees

receivable.

+900 Fees

Receivable

- = +900 Retained

Earnings

+900 Printing

Revenue

- = +900

4. Accrue

maintenance

expense.

-400 Prepaid

Maintenance

- = -400 Retained

Earnings

- +400

Maintenance

Expense

= -400

5. Accrue ad.

Expense.

-300 Prepaid

Advertising

- = -300 Retained

Earnings

- +300 Ad. Expense

= -300

6. Accrue rent

expanse.

- = +160 Rent

Payable

-160 Retained

Earnings

- +160 Rent

Expense

= -160

7. Accrue

interest

revenue.

+38 Interest

Receivable

- = +38 Retained

Earnings

+38 Interest

Revenue

- = +38

8. Accrue

depreciation

expense.

- +2,175 Accumulated

Depreciation

= -2,175 Retained

Earnings

- +2,175

Depreciation

Expense

= -2,175

Totals 0 + +238 - 2,175 = 1,080 + 0 + -3,017 938 - 3,955 = -3,017

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-41

b.

Date Description Debit Credit

Dec 31 Salaries expense (+E, -SE) 720 Salaries payable (+L) 720

To accrue salaries at December 31 ($1,800 2/5 = $720). 31 Interest expense (+E, -SE) 200 Interest payable (+L) 200 To accrue interest expense at December 31. 31 Fees receivable (+A) 900 Printing revenue (+R, +SE) 900 To record revenue earned but not yet billed. 31 Maintenance expense (+E ,-SE) 400 Prepaid maintenance (-A) 400 To record December maintenance expense. 31 Advertising expense (+E, -SE) 300 Prepaid advertising (-A) 300 To record December advertising expense

($900 1/3 = $300). 31 Rent expense (+E, -SE) 160 Rent payable (+L) 160 To accrue one-half month's rent expense

[(400 $0.80)/2 = $160]. 31 Interest receivable (+A) 38 Interest income (+R, +SE) 38 To accrue interest earned in December. 31 Depreciation expense—Equipment (+E, -SE) 2,175 Accum. depreciation—Equipment (+XA) 2,175 To record annual depreciation on equipment.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-42

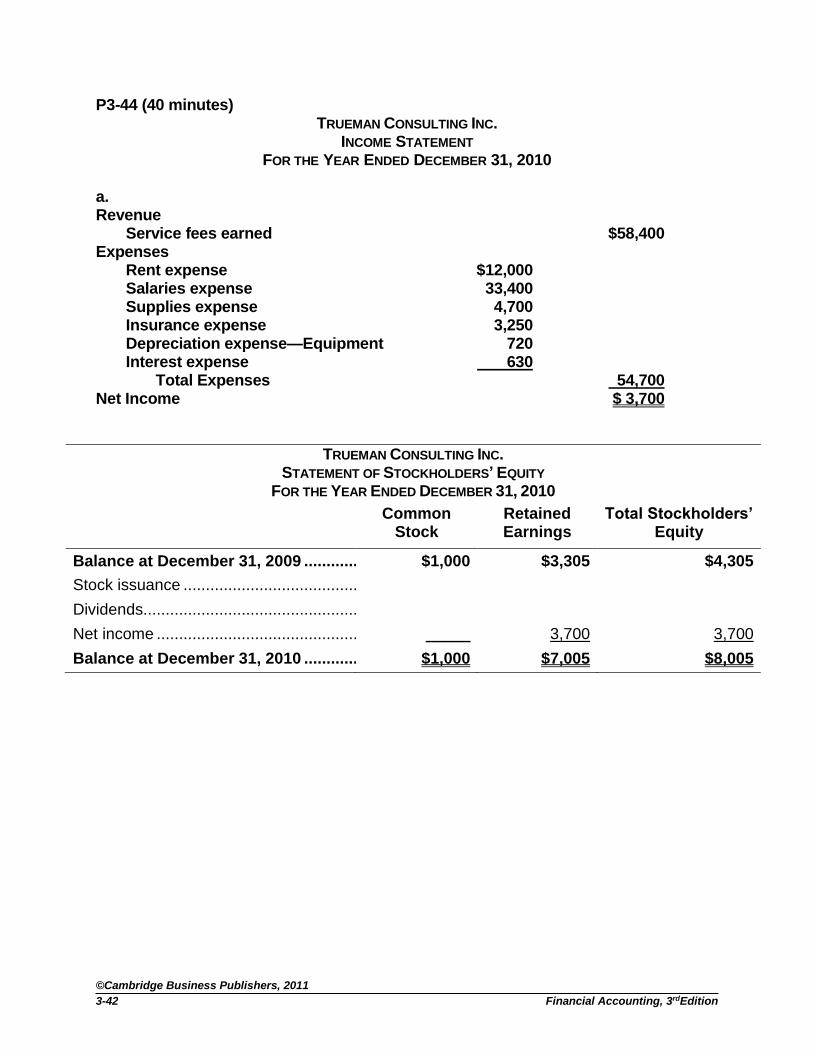

P3-44 (40 minutes) TRUEMAN CONSULTING INC.

INCOME STATEMENT FOR THE YEAR ENDED DECEMBER 31, 2010

a. Revenue Service fees earned $58,400 Expenses Rent expense $12,000 Salaries expense 33,400 Supplies expense 4,700 Insurance expense 3,250 Depreciation expense—Equipment 720 Interest expense 630 Total Expenses 54,700 Net Income $ 3,700

TRUEMAN CONSULTING INC. STATEMENT OF STOCKHOLDERS’ EQUITY

FOR THE YEAR ENDED DECEMBER 31, 2010

Common Stock

Retained Earnings

Total Stockholders’ Equity

Balance at December 31, 2009 ............ $1,000 $3,305 $4,305

Stock issuance .......................................

Dividends................................................

Net income ............................................. _____ 3,700 3,700

Balance at December 31, 2010 ............ $1,000 $7,005 $8,005

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-43

TRUEMAN CONSULTING BALANCE SHEET

DECEMBER 31, 2010

Assets Liabilities

Cash $ 2,700 Accounts payable $ 845

Accounts receivable 3,270 Long-term notes payable 7,000

Supplies 3,060 Total Liabilities 7,845

Prepaid insurance 1,500 Equipment $ 6,400 Owners’ Equity

Less: Accumulated depreciation

1,080 5,320 Common stock 1,000

Retained earnings 7,005

Total Assets $15,850 Total Liabilities and Owners’ Equity $15,850

b.

Date 2010 Description Debit Credit

Dec. 31 Service fees earned (-R) 58,400 Retained earnings (+SE) 58,400 To close the revenue account. 31 Retained earnings (-SE) 54,700 Rent expense (-E) 12,000 Salaries expense(-E) 33,400 Supplies expense (-E) 4,700 Insurance expense (-E) 3,250 Depreciation expense—Equip (-E) 720 Interest expense (-E) 630 To close the expense accounts.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-44

P3-45 (30 minutes) a.

Date 2010 Description Debit Credit

Dec. 31 Service fees earned (-R) 97,200 Miscellaneous income (-R) 4,200 Retained earnings (+SE) 101,400 To close the revenue accounts. 31 Retained earnings (-SE) 74,800 Salaries expense (-E) 42,800 Rent expense (-E) 13,400 Insurance expense (-E) 1,800 Depreciation expense (-E) 8,000 Income tax expense (-E) 8,800 To close the expense accounts.

b. After the closing entries are posted, Retained Earnings has a $45,700 credit

balance ($19,100 + $26,600 net income). c.

Wilson Company Post-Closing Trial Balance

December 31, 2010 Debit Credit

Cash $8,500 Accounts Receivable 8,000 Prepaid Insurance 3,600 Equipment 72,000 Accumulated Depreciation $12,000 Accounts Payable 600 Income Tax Payable 8,800 Common Stock 25,000 Retained Earnings ______ 45,700 $92,100 $92,100

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-45

P3-46 (30 minutes) a.

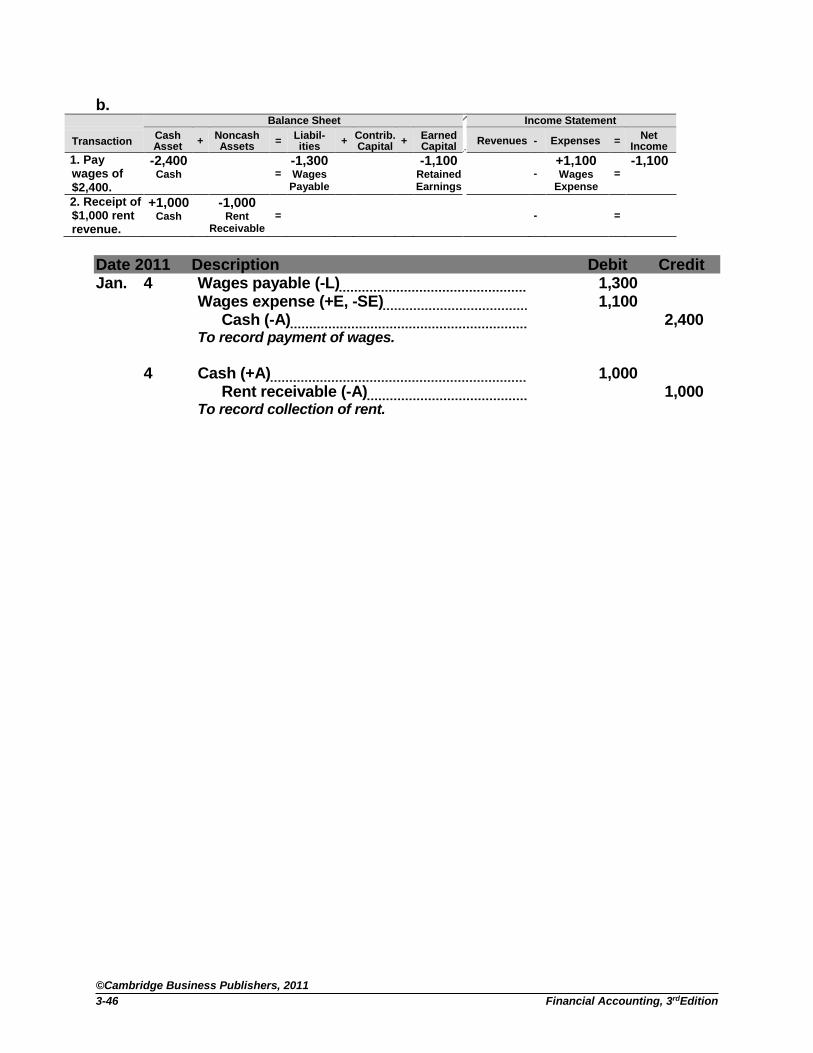

*Assumes wages earned had not been accrued or recognized yet as an expense.

Date 2010 Description Debit Credit

Dec. 31 Advertising expense (+E, -SE) 400 Prepaid advertising (-A) 400 To record advertising expense ($1,200 $800 = $400).

31 Wages expense (+E, -SE) 1,300 Wages payable (+L) 1,300 To record accrued wages.

31 Insurance expense (+E, -SE) 1,140 Prepaid insurance (-A) 1,140 To record insurance expense ($3,420 $2,280 = $1,140).

31 Unearned service fees (-L) 2,400 Service fees earned (+R, +SE) 2,400 To recognize unearned fees as earned

($5,400 $3,000 = $2,400).

31 Rent receivable (+A) 1,000 Rental income (R, +SE) 1,000 To record rent earned but not yet recorded.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income 1. Recognize

Advertising expense.

-400 Prepaid

Advertising =

-400

Retained Earnings

-

+400

Advertising Expense

= -400

2. Accrue wage expense.

=

+1,300 Wages

Payable*

-1,300 Retained Earnings

-

+1,300 Wages

Expense =

-1,300

3. Recognize insurance expense.

-1,140 Prepaid

Insurance =

-1,140

Retained Earnings

-

+1,140

Insurance Expense

=

-1,140

4. Recognize service fees earned.

=

-2,400

Unearned Service Fees

+2,400

Retained Earnings

+2,400

Service Fees Earned

-

=

+2,400

5. Recognize rent revenue.

+1,000

Rent Receivable

=

+1,000 Retained Earnings

+1,000 Rental Income

-

= +1,000

Totals 0 + -540 = -1,100 + 0 + 560 3,400 - 2,840 = 560

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-46

b. Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

1. Pay wages of $2,400.

-2,400 Cash

= -1,300

Wages Payable

-1,100

Retained Earnings

- +1,100

Wages Expense

= -1,100

2. Receipt of $1,000 rent revenue.

+1,000 Cash

-1,000 Rent

Receivable

=

-

=

Date 2011 Description Debit Credit Jan. 4 Wages payable (-L) 1,300 Wages expense (+E, -SE) 1,100 Cash (-A) 2,400 To record payment of wages.

4 Cash (+A) 1,000 Rent receivable (-A) 1,000 To record collection of rent.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-47

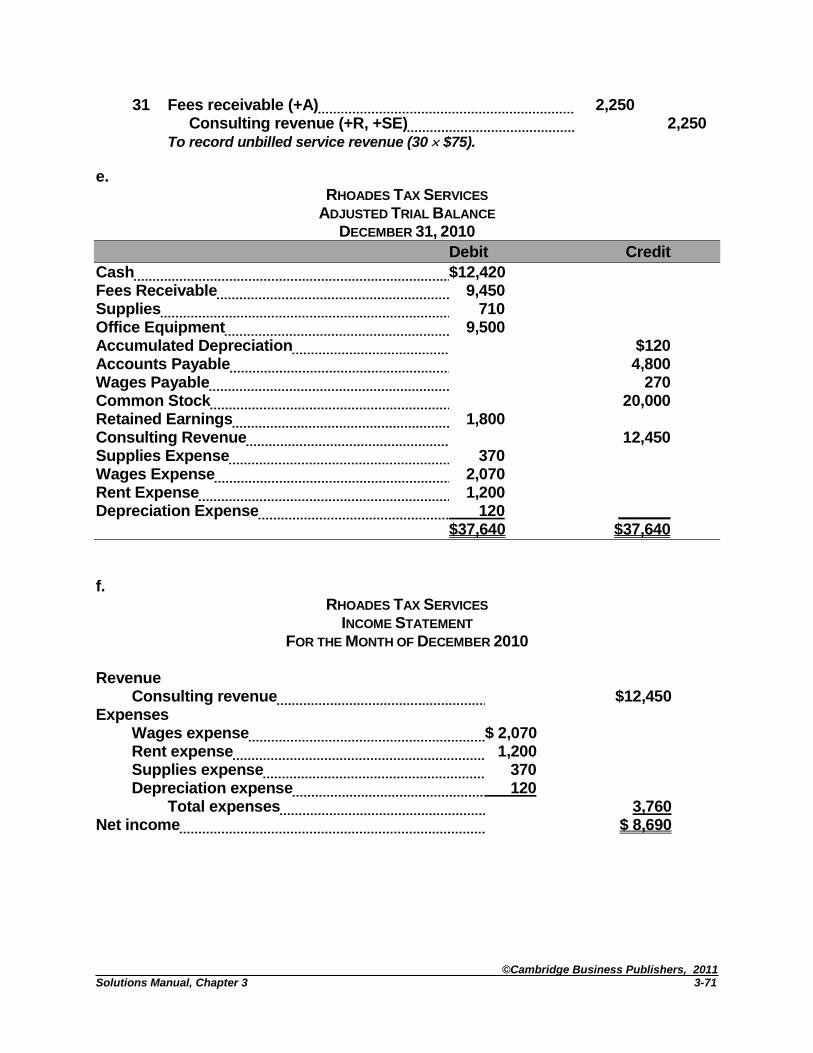

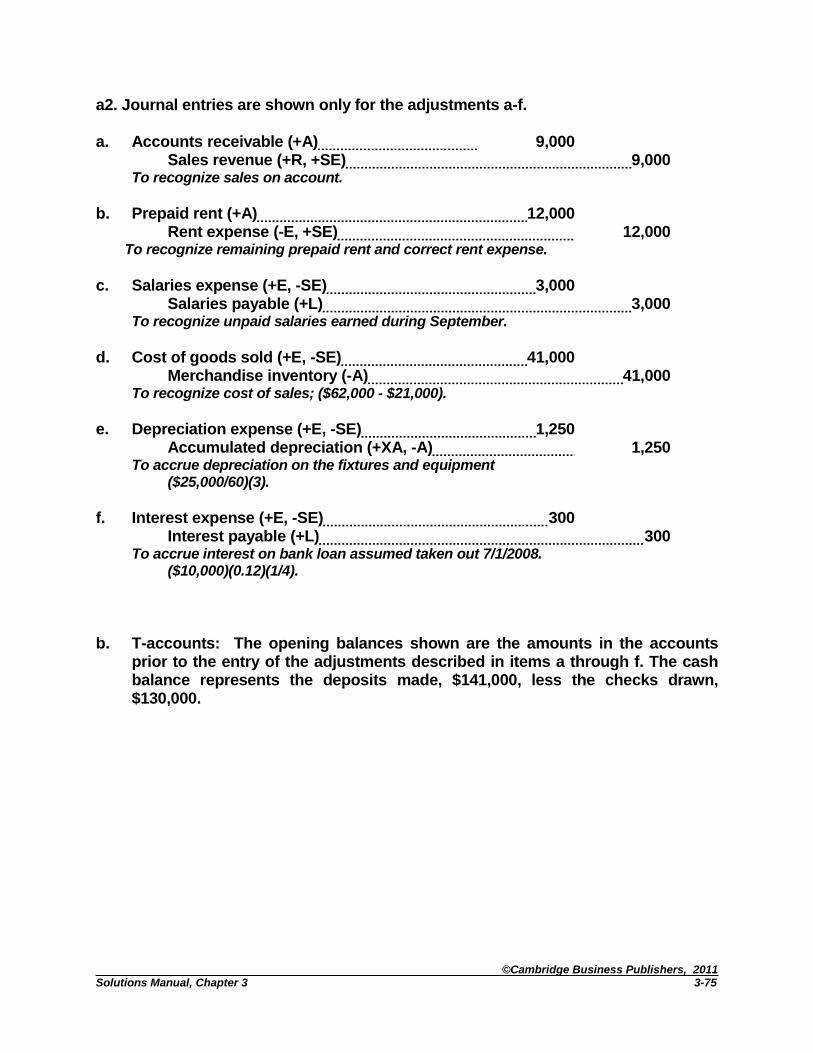

P3-47 (90 minutes) a, b and d. For part d, the adjusting entries are indicated by the numbers 1-5. The unadjusted trial balance required in part c is calculated before the adjusting entries are made.

+ Cash (A) - - Accounts Payable (L) +

6/1 24,000 4,400 6/1 9,480 6/1

6/2 6,400 875 6/2 6/30 7,800 930 6/2

3,600 6/12 - Salaries Payable (L) +

1,240 6/15 725 2.

520 6/18 3,600 6/26

1,500 6/30 - Unearned Service Fees (L) +

21,535 5. 3,200 6,400 6/2

3,200

+ Accounts Receivable (A) -

6/10 5,800 7,800 6/30 - Common Stock (SE) +

6/28 5,200 24,000 6/1

3,200

+ Prepaid Advertising (A) - - Retained Earnings(SE) +

6/2 930 310 4. 6/30 1,500

620

+ Office Supplies (A) - + Supplies Expense (E) -

6/1 2,840 1,310 1. 1. 1,310

1,530

+ Office Equipment (A) - + Travel Expense (E) -

6/1 11,040 6/15 1,240

- Acc. Depreciation – Off. Equip (XA) + + Depreciation Expense(E) -

115 3. 3. 115

+ Advertising Expense (E) - + Rent Expense (E) -

4. 310 6/2 875

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-48

+ Salaries Expenses (E) - - Service Fees Earned (R) +

6/12 3,600 5,800 6/10

6/26 3,600 5,200 6/28

2. 725 3,200 5.

7,925 14,200

+ Postage Expense (E) -

6/18 520

b.

Balance Sheet Income Statement

Transaction Cash Asset

+ Noncash Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

6/1. Investment for common stock.

+24,000 Cash

=

+24,000

Common Stock

-

=

6/1. Purchase of assets for cash & on account.

-4,400 Cash

+ 11,040 Office

Equipment

+2,840

Supplies

=

+9,480

Accounts Payable

-

=

6/2. Pay rent $875. -875 Cash

=

-875

Retained Earnings

- +875

Rent Expense

= -875

6/2.Purchase $930 of advertising in advance.

-930 Cash

+930 Prepaid

Advertising

=

-

=

6/2Signed research contract.

+6,400 Cash

= +6,400

Unearned Service Fees

-

=

6/10. Bill customers for services.

+5,800

Accounts Receivable

=

+5,800 Retained Earnings

+5,800 Service Fees

Earned

-

= +5,800

6/12. Paid salaries. -3,600 Cash

=

-3,600

Retained Earnings

- +3,600 Salaries Expense

= -3,600

6/15. Paid travel expenses.

-1,240 Cash

=

-1,240

Retained Earnings

- +1,240 Travel

Expense

= -1,240

6/18. Paid postage. -520 Cash

=

-520

Retained Earnings

- +520

Postage Expense

= -520

6/26. Paid salaries. -3,600 Cash

=

-3,600

Retained Earnings

- +3,600 Salaries Expense

= -3,600

6/28. Bill customers for services.

+5,200 Accounts

Receivable =

+5,200 Retained Earnings

+5,200 Service

Fees Earned

-

=

+5,200

6/30. Collect service fees.

+7,800 Cash

-7,800

Acts. Rec. =

-

=

6/30. Cash dividend paid.

-1,500 Cash

-1,500

Retained Earnings

-

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-49

Date 2010 Description Debit Credit

June 1 Cash (+A) 24,000 Common stock (+SE) 24,000 Owner invested cash for common stock.

1 Office equipment (+A) 11,040 Office supplies (+A) 2,840 Cash (-A) 4,400 Accounts payable (+L) 9,480 Purchased equipment and supplies; $4,400 cash paid with the remainder due in 60 days.

2 Rent expense (+E, -SE) 875 Cash (-A) 875 Paid June rent.

2 Prepaid advertising (+A) 930 Cash (-A) 930 Paid three months' advertising in advance.

2 Cash (+A) 6,400 Unearned service fees (+L) 6,400 Received two months' fees in advance on six-month contract.

10 Accounts receivable (+A) 5,800 Service fees earned (+R, +SE) 5,800 Billed customers for services.

12 Salaries expense (+E, -SE) 3,600 Cash (-A) 3,600 Paid two weeks' salaries to employees.

15 Travel expense (+E, -SE) 1,240 Cash (-A) 1,240 Paid business travel expenses.

18 Postage expense (+E, -SE) 520 Cash (-A) 520 Paid postage for questionnaire mailing.

26 Salaries expense (+E, -SE) 3,600 Cash (-A) 3,600 Paid two weeks' salaries to employees.

28 Accounts receivable (+A) 5,200 Service fees earned (+R, +SE) 5,200 Billed customers for services.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-50

30 Cash (+A) 7,800 Accounts receivable (-A) 7,800 Collections from customers on account.

30 Retained earnings (-SE) 1,500 Cash (-A) 1,500 Declared and paid dividends.

c.

MARKET-PROBE UNADJUSTED TRIAL BALANCE

JUNE 30, 2010

Debit Credit

Cash $21,535 Accounts Receivable 3,200 Office Supplies 2,840 Prepaid Advertising 930 Office Equipment 11,040 Accounts Payable $9,480 Unearned Service Fees 6,400 Common Stock 24,000 Retained Earnings* 1,500 Service Fees Earned 11,000 Salaries Expense 7,200 Rent Expense 875 Travel Expense 1,240 Postage Expense 520 ______ $50,880 $50,880

* The negative (debit) balance in Retained Earnings reflects the dividend paid. d.

Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabilities + Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

a. Recognize

supplies

expense.

-1,310 Office

Supplies -

= -1,310 Retained

Earnings

- +1,310 Supplies

Expense

= -1,310

b. Recognize

salaries

expense.

-

= +725 Salaries

Payable

-725 Retained

Earnings

- +725 Salaries

Expense

= -725

c. Accrue

depreciation

expense.

-

+115 Accumulated

Depreciation

= -115 Retained

Earnings

- +115 Depreciation

Expense

= -115

d. Recognize

advertising

expense.

-310 Prepaid

Advertising

- = -310

Retained

Earnings

- +310 Advertising

Expense

= -310

e. Recognize

earned

service fees.

-

= -3,200 Unearned

Service Fees

+3,200 Retained

Earnings

+3,200 Service Fees

Earned

- = +3,200

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-51

Date 2010 Description Debit Credit June 30 Supplies expense (+E, -SE) 1,310 Office supplies (-A) 1,310 To record supplies used during June

($2,840 $1,530 = $1,310). 30 Salaries expense (+E, -SE) 725 Salaries payable (+L) 725 To record unpaid salaries at June 30.

30 Depreciation expense—Office equipment (+E, -SE) 115 Accum. deprec. Off. equipment (+XA, -A) 115 To record June depreciation ($11,040/96 mo. = $115). 30 Advertising expense (+E, -SE) 310 Prepaid advertising (-A) 310 To record one month's advertising expense. 30 Unearned service fees (-L) 3,200 Service fees earned (+R, +SE) 3,200 To record one month's fees earned, received in advance.

©Cambridge Business Publishers, 2011

Financial Accounting, 3rdEdition 3-52

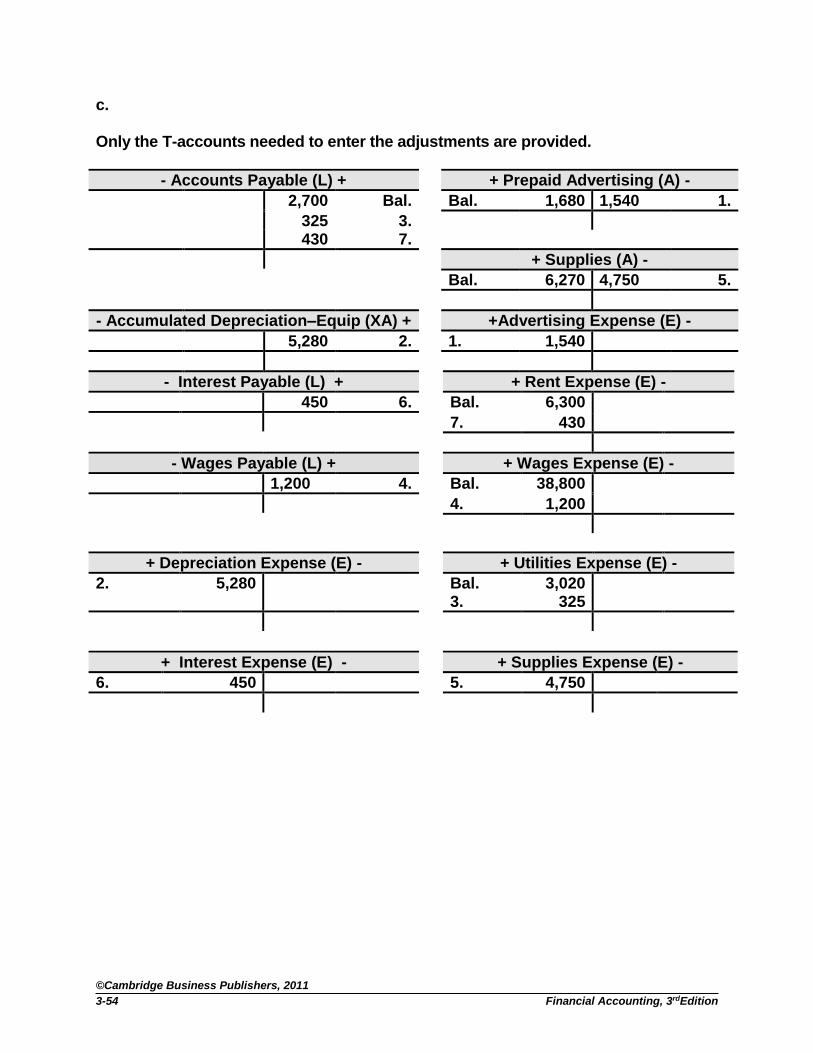

P3-48 (40 minutes)

DELIVERALL

UNADJUSTED TRIAL BALANCE DECEMBER 31, 2010

a.

Debit Credit

Cash $ 2,300 Accounts Receivable 5,120 Prepaid Advertising 1,680 Supplies 6,270 Equipment 42,240 Notes Payable $7,500 Accounts Payable 2,700 Common Stock 9,530 Mailing Fees Earned 86,000 Wages Expense 38,800 Rent Expense 6,300 Utilities Expense 3,020 ________ $105,730 $105,730

b.

Balance Sheet Income Statement

Transaction Cash Asset

+

Noncash Assets -

Contra Assets

= Liabil-ities

+ Contrib. Capital

+ Earned Capital

Revenues - Expenses = Net

Income

1. Recognize

advertising

expense.

-1,540 Prepaid

Advertising

-

= -1,540 Retained

Earnings

- +1,540

Advertising

Expense

= -1,540

2. Recognize

depreciation

expense.

- +5,280

Accumulated

Depreciation

= -5,280 Retained

Earnings

- +5,280

Depreciation

Expense

= -5,280

3. Recognize

utilities

expense.

-

= +325 Accounts

Payable

-325 Retained

Earnings

- +325 Utilities

Expense

= -325

4. Accrue wages

expense.

-

= +1,200 Wages

Payable

-1,200 Retained

Earnings

- +1,200 Wages

Expense

= -1,200

5. Recognize

supplies

expense.

-4,750 Supplies -

= -4,750 Retained

Earnings

- +4,750 Supplies

Expense

= -4,750

6. Accrue interest

expense.

-

= +450 Interest

Payable

-450 Retained

Earnings

- +450 Interest

Expense

= -450

7. Recognize rent

expense*.

-

= +430 Accounts

Payable

-430 Retained

Earnings

- +430 Rent

Expense

= -430

*(1/2% $86,000 = $430). The rent for the year ($6,300 = $525 x 12) has already been recognized in the accounts. See the beginning balances given in the problem statement.

©Cambridge Business Publishers, 2011 Solutions Manual, Chapter 3

3-53

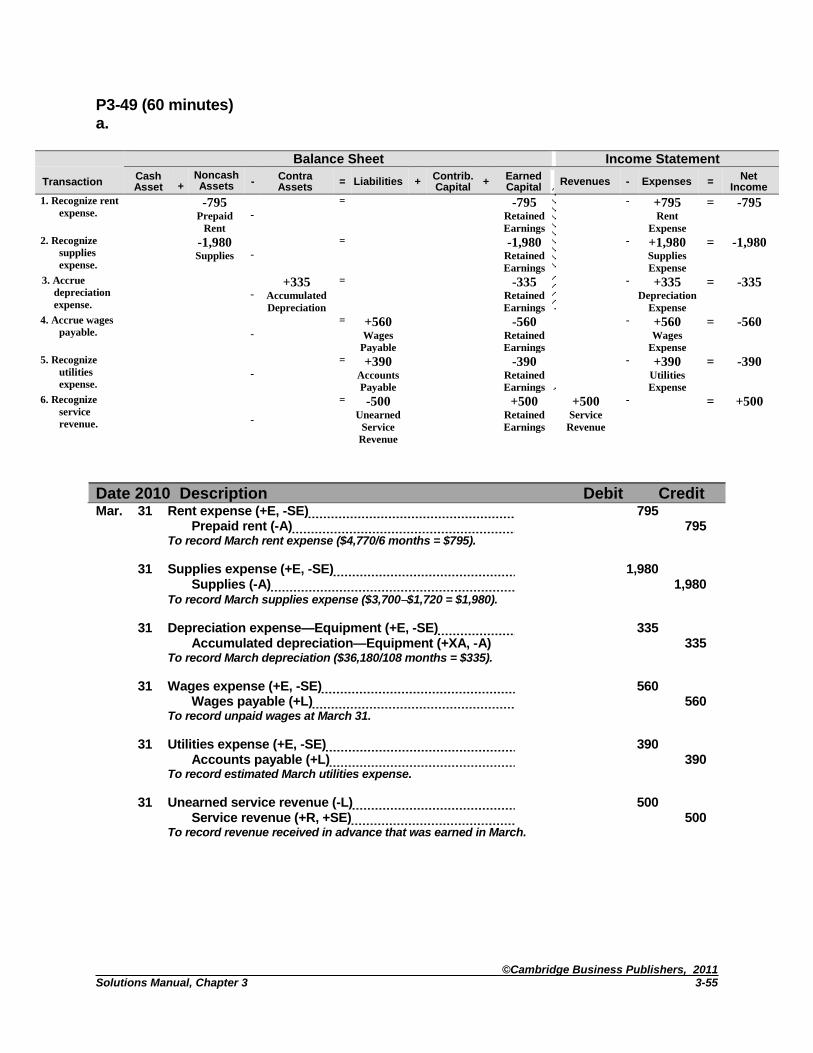

Date 2010 Description Debit Credit

Dec. 31 Advertising expense (+E, -SE) 1,540 Prepaid advertising (-A) 1,540 To record 11 months' advertising expense