Xerox Partner Print Services Profitable, sustainable growth for

Artificial Intelligence

Brian Morgan FCICM Business Growth & Partner Director

To turn data into Intelligence

We exist to simplify the complex

Software that finance people love

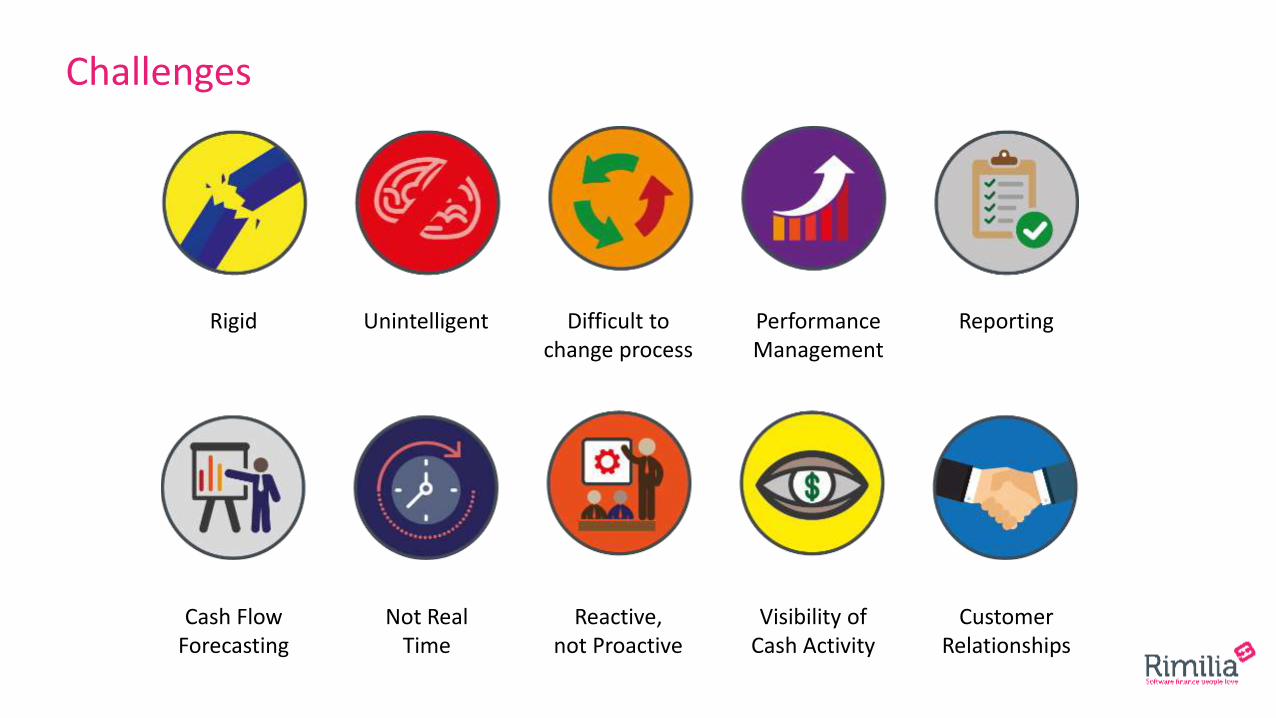

Rigid Unintelligent Difficult to change process

PerformanceManagement

Reporting

Visibility of Cash Activity

CustomerRelationships

Reactive,not Proactive

Not Real Time

Cash FlowForecasting

Challenges

Phone: +44 (0) 1527 872 123

[email protected] | www.rimilia.com

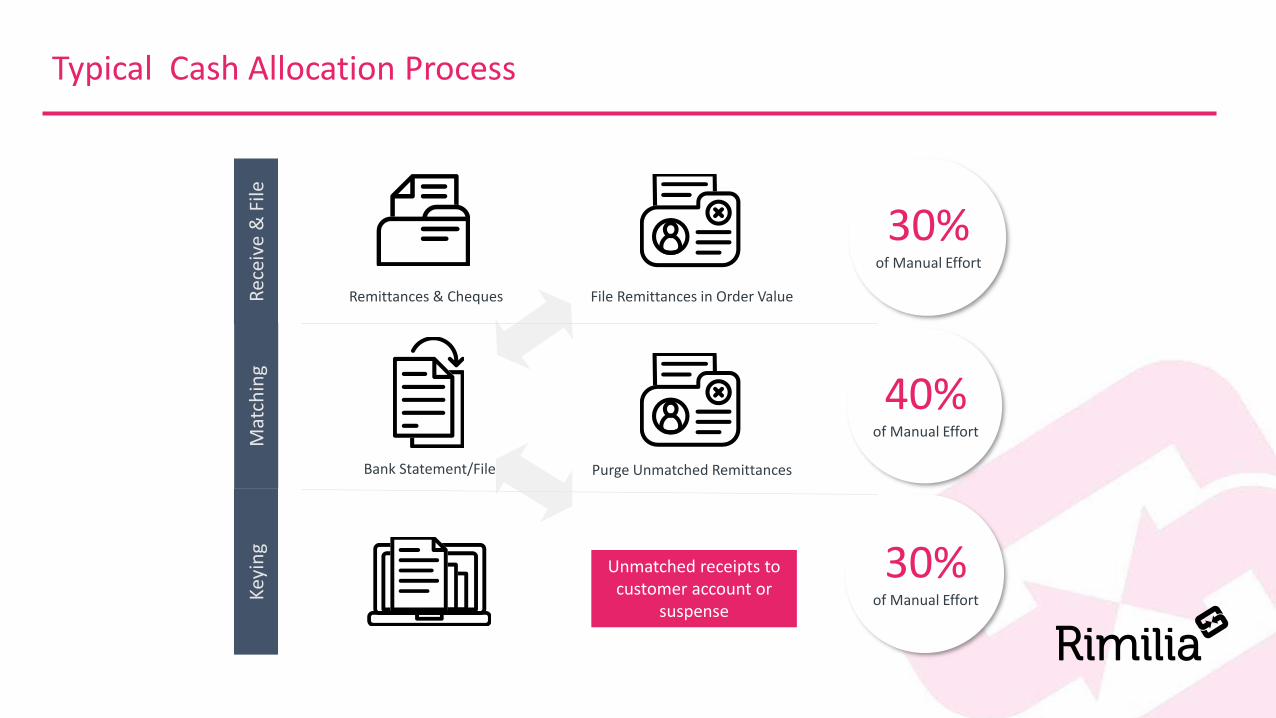

Typical Cash Allocation Process

30%of Manual Effort

40%of Manual Effort

Rec

eive

& F

ileM

atch

ing

Key

ing

Remittances & Cheques

Bank Statement/File

File Remittances in Order Value

Purge Unmatched Remittances

30%of Manual Effort

Unmatched receipts to customer account or

suspense

Phone: +44 (0) 1527 872 123

[email protected] | www.rimilia.com

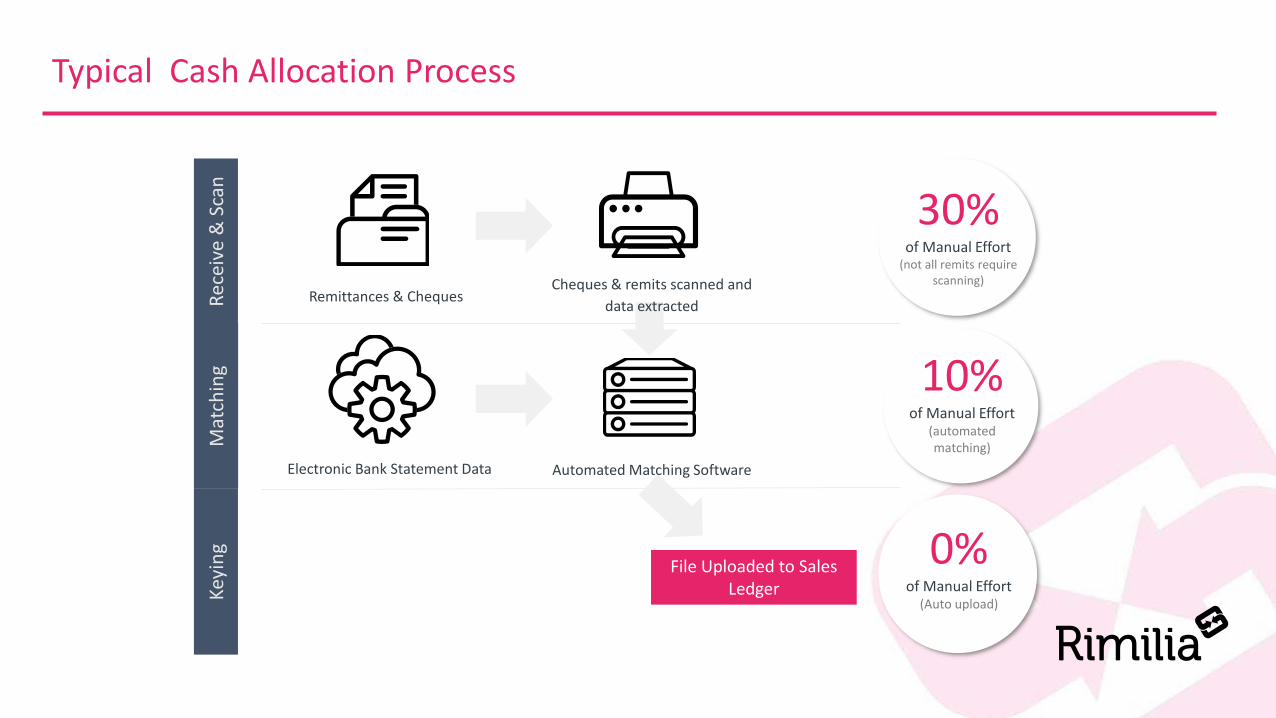

Typical Cash Allocation Process

Remittances & Cheques

30%of Manual Effort

(not all remits require scanning)

10%of Manual Effort

(automatedmatching)

Rec

eive

& S

can

Mat

chin

gK

eyin

g

File Uploaded to Sales Ledger

0%of Manual Effort

(Auto upload)

Cheques & remits scanned and

data extracted

Automated Matching Software Electronic Bank Statement Data

Industry-leading utilization of AI for faster, quicker, better decision-making

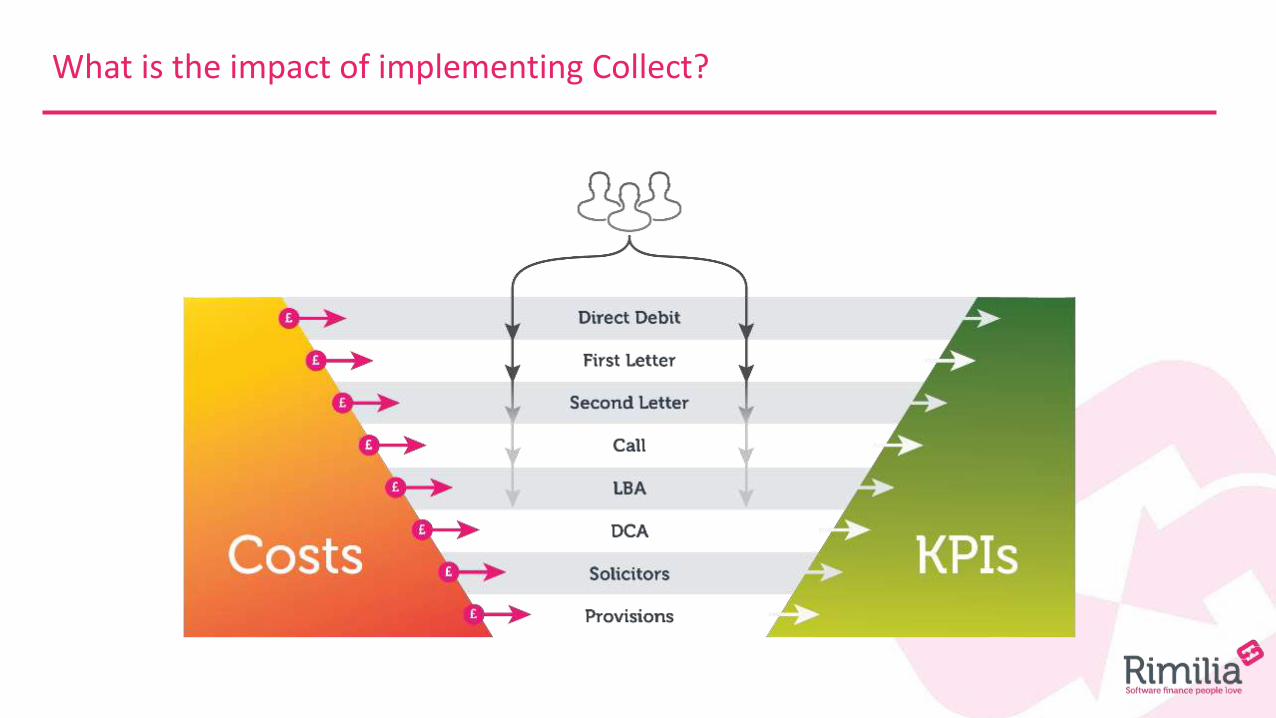

What is the impact of implementing Collect?

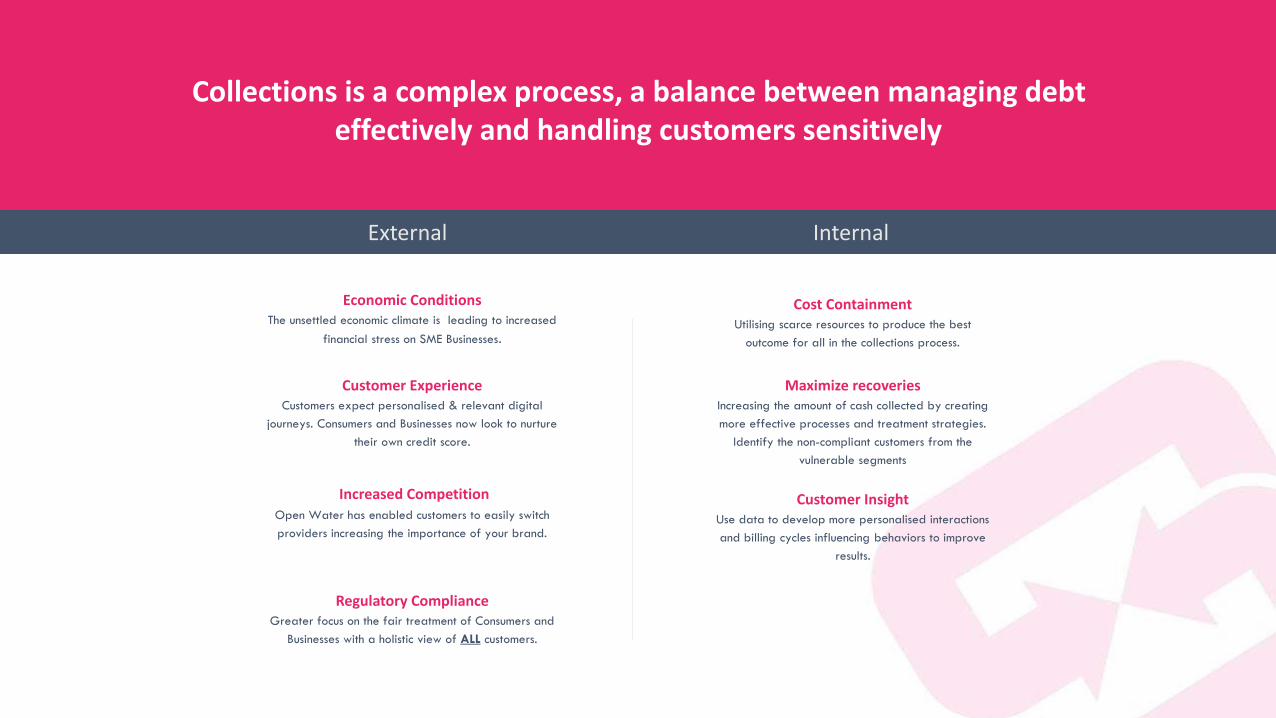

Collections is a complex process, a balance between managing debt effectively and handling customers sensitively

Cost ContainmentUtilising scarce resources to produce the best

outcome for all in the collections process.

Maximize recoveriesIncreasing the amount of cash collected by creating

more effective processes and treatment strategies.

Identify the non-compliant customers from the

vulnerable segments

Customer InsightUse data to develop more personalised interactions

and billing cycles influencing behaviors to improve

results.

Economic ConditionsThe unsettled economic climate is leading to increased

financial stress on SME Businesses.

Regulatory ComplianceGreater focus on the fair treatment of Consumers and

Businesses with a holistic view of ALL customers.

Customer ExperienceCustomers expect personalised & relevant digital

journeys. Consumers and Businesses now look to nurture

their own credit score.

Increased CompetitionOpen Water has enabled customers to easily switch

providers increasing the importance of your brand.

External Internal

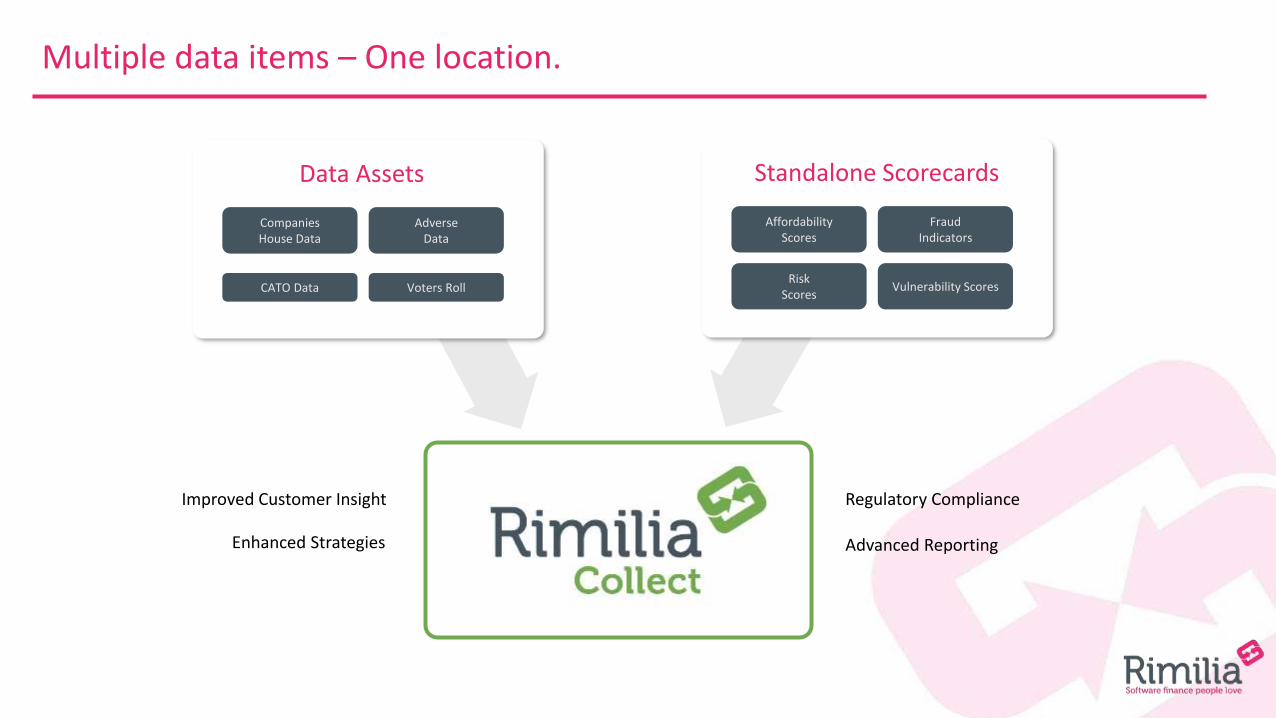

Multiple data items – One location.

Standalone Scorecards

AffordabilityScores

FraudIndicators

RiskScores

Vulnerability Scores

Data Assets

CompaniesHouse Data

AdverseData

CATO Data Voters Roll

Improved Customer Insight

Enhanced Strategies

Regulatory Compliance

Advanced Reporting

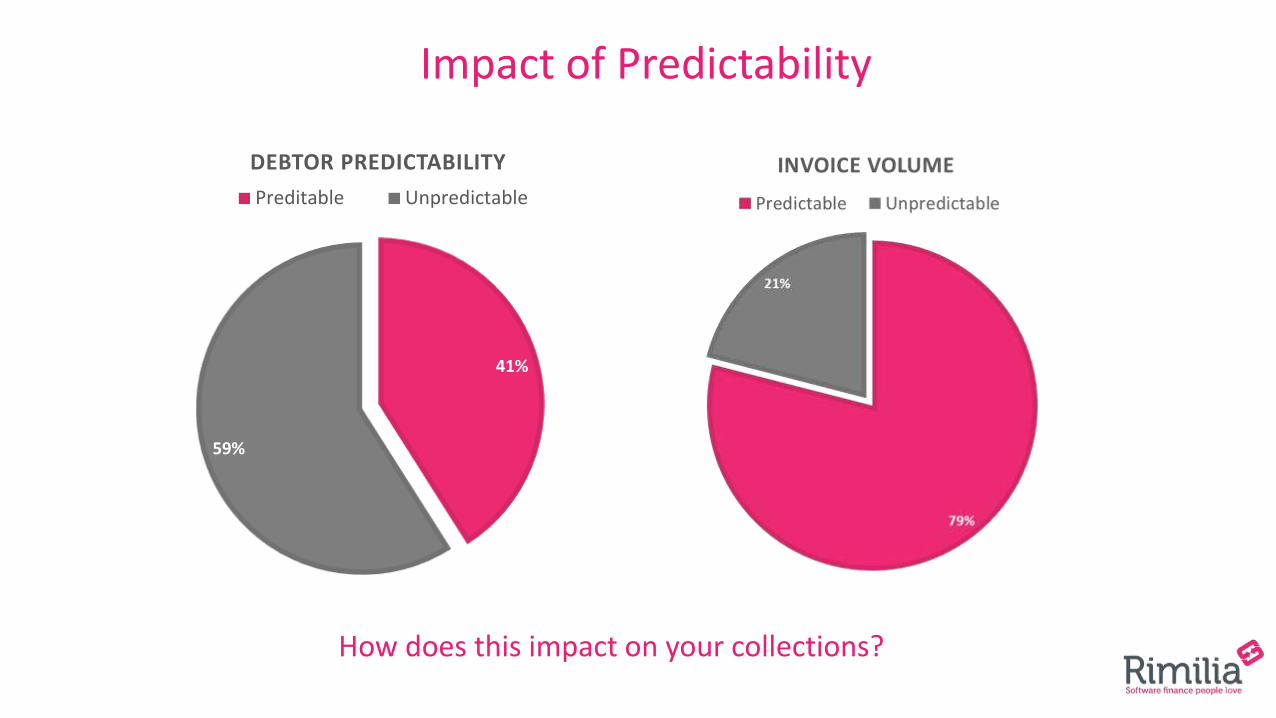

41%

59%

DEBTOR PREDICTABILITY

Preditable Unpredictable

How does this impact on your collections?

Impact of Predictability

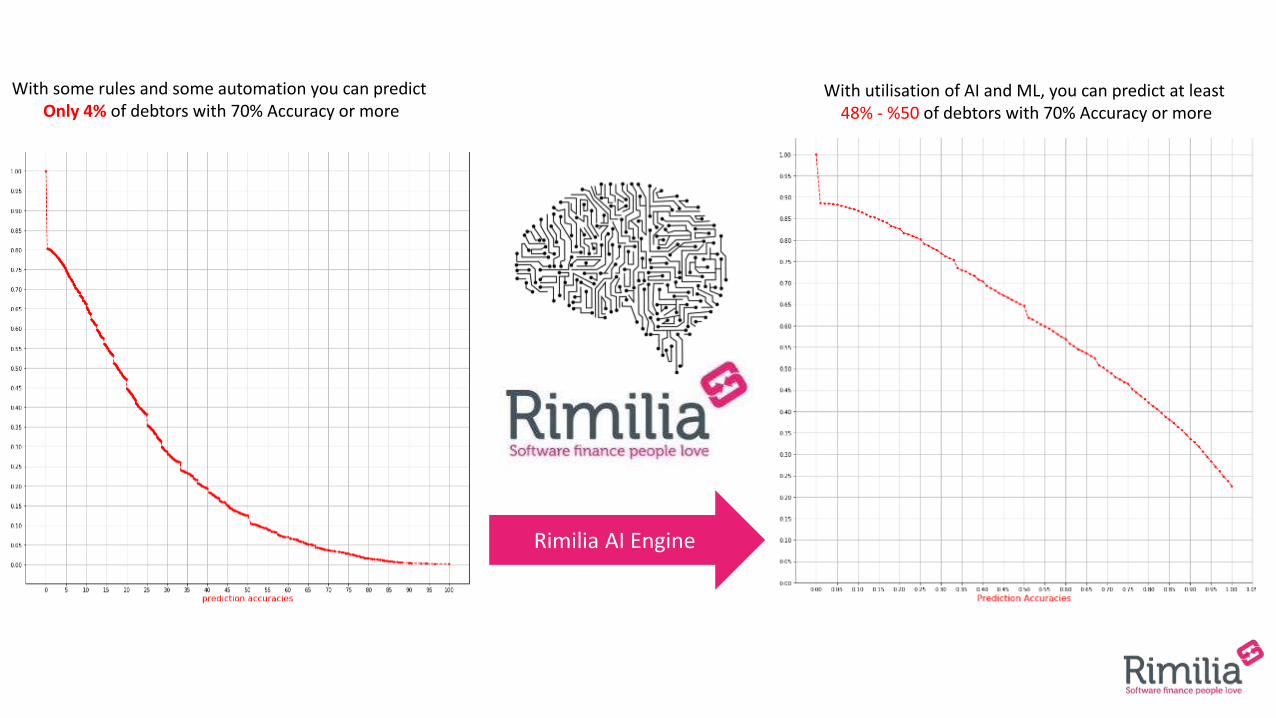

With some rules and some automation you can predict Only 4% of debtors with 70% Accuracy or more

Rimilia AI Engine

With utilisation of AI and ML, you can predict at least 48% - %50 of debtors with 70% Accuracy or more

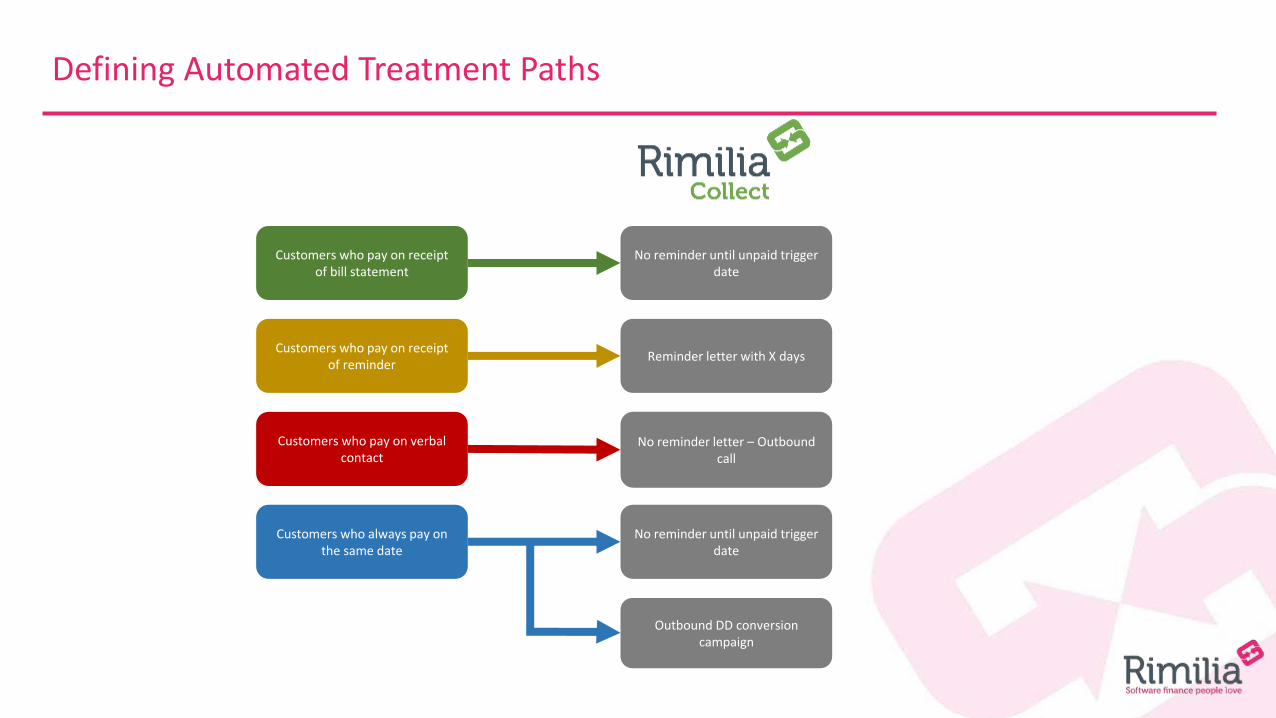

Customers who pay on receipt of bill statement

Customers who pay on receipt of reminder

Customers who pay on verbal contact

Customers who always pay on the same date

No reminder until unpaid trigger date

Reminder letter with X days

No reminder letter – Outbound call

No reminder until unpaid trigger date

Outbound DD conversion campaign

Defining Automated Treatment Paths

Information never changed anything

Application brings transformation

Turning Information into Intelligence into Wisdom

Our Customers

Finance pioneers who want to make a significant difference because they know

“we have always done it this way”is the wrong answer

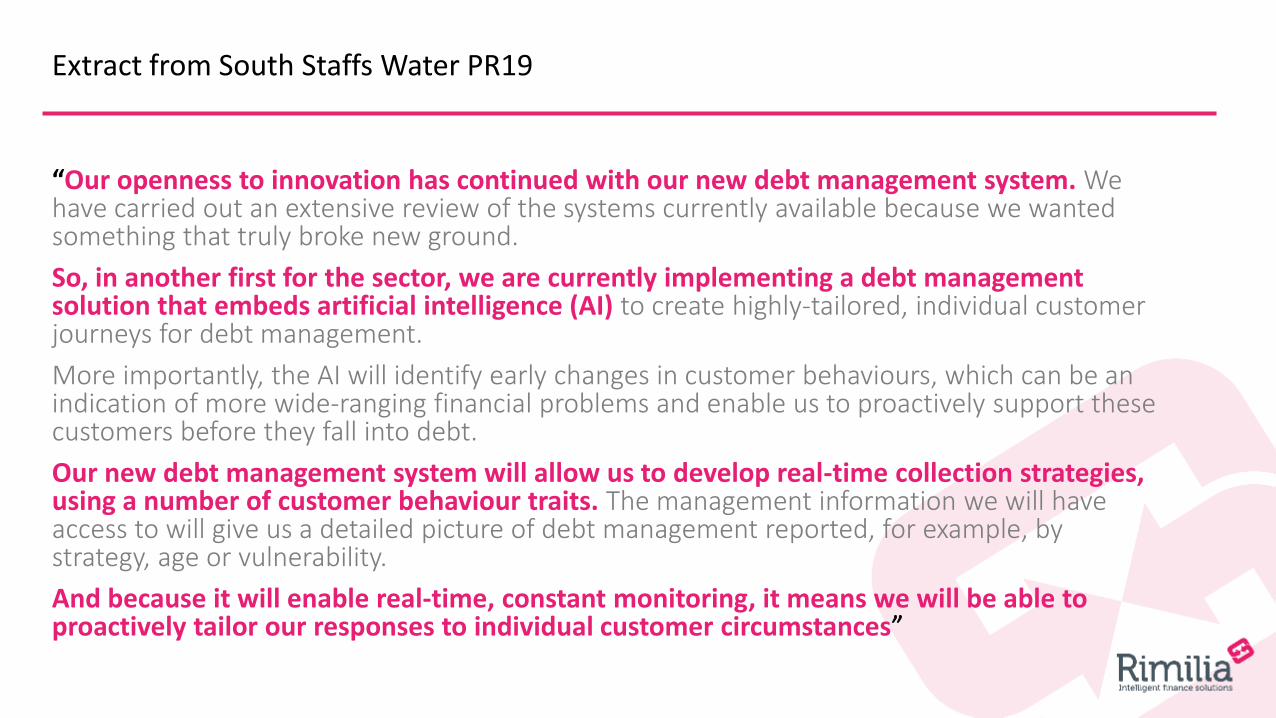

Extract from South Staffs Water PR19

“Our openness to innovation has continued with our new debt management system. We have carried out an extensive review of the systems currently available because we wanted something that truly broke new ground.

So, in another first for the sector, we are currently implementing a debt management solution that embeds artificial intelligence (AI) to create highly-tailored, individual customer journeys for debt management.

More importantly, the AI will identify early changes in customer behaviours, which can be an indication of more wide-ranging financial problems and enable us to proactively support these customers before they fall into debt.

Our new debt management system will allow us to develop real-time collection strategies, using a number of customer behaviour traits. The management information we will have access to will give us a detailed picture of debt management reported, for example, by strategy, age or vulnerability.

And because it will enable real-time, constant monitoring, it means we will be able to proactively tailor our responses to individual customer circumstances”

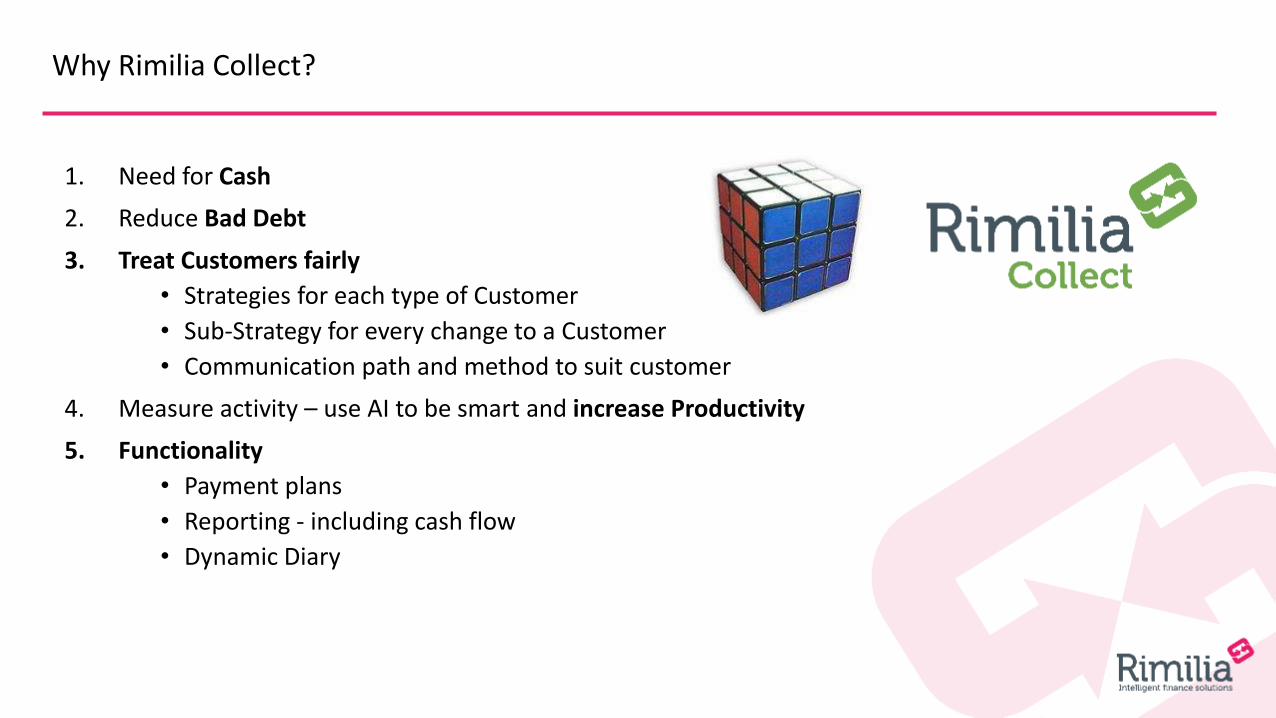

Why Rimilia Collect?

1. Need for Cash

2. Reduce Bad Debt

3. Treat Customers fairly

• Strategies for each type of Customer

• Sub-Strategy for every change to a Customer

• Communication path and method to suit customer

4. Measure activity – use AI to be smart and increase Productivity

5. Functionality

• Payment plans

• Reporting - including cash flow

• Dynamic Diary

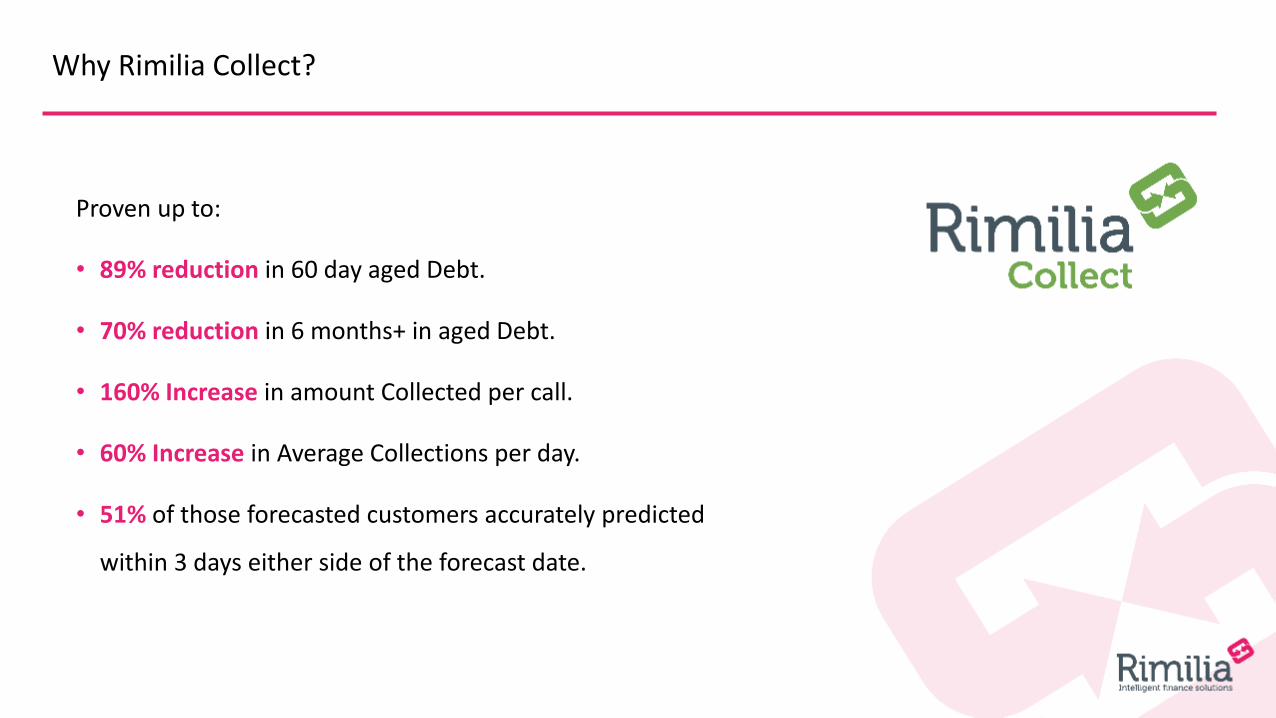

Why Rimilia Collect?

Proven up to:

• 89% reduction in 60 day aged Debt.

• 70% reduction in 6 months+ in aged Debt.

• 160% Increase in amount Collected per call.

• 60% Increase in Average Collections per day.

• 51% of those forecasted customers accurately predicted

within 3 days either side of the forecast date.

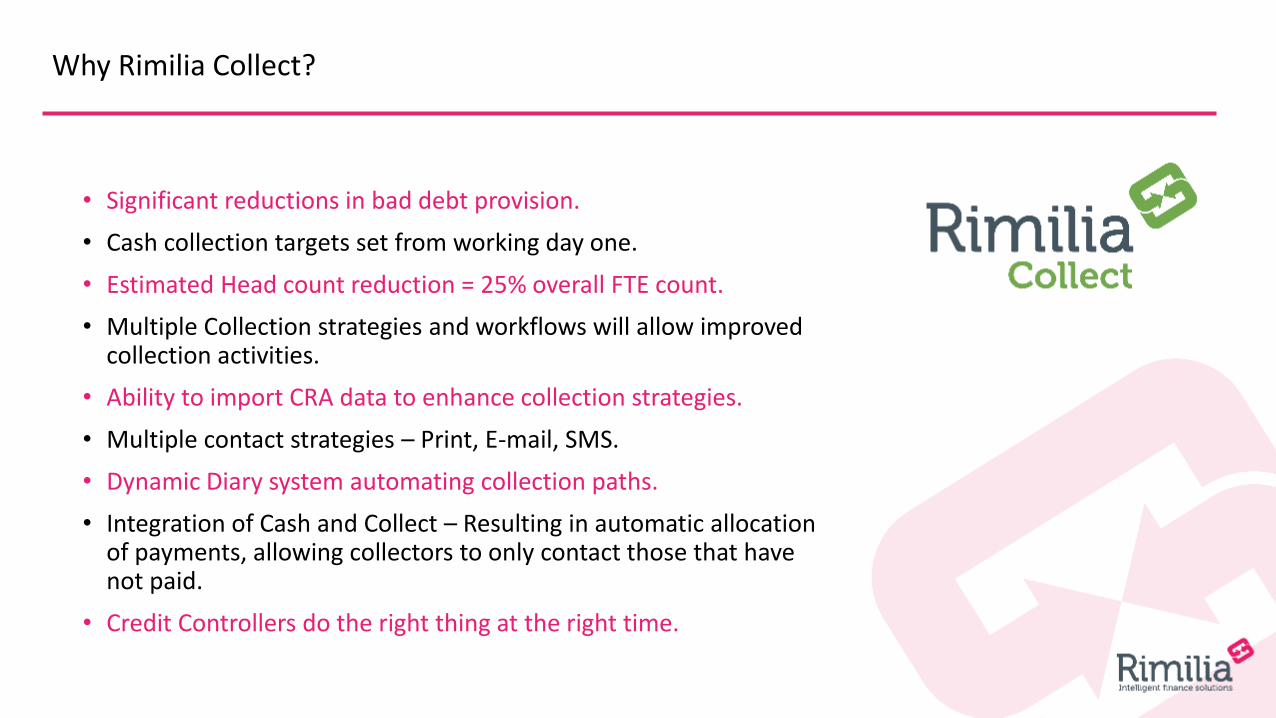

Why Rimilia Collect?

• Significant reductions in bad debt provision.

• Cash collection targets set from working day one.

• Estimated Head count reduction = 25% overall FTE count.

• Multiple Collection strategies and workflows will allow improved collection activities.

• Ability to import CRA data to enhance collection strategies.

• Multiple contact strategies – Print, E-mail, SMS.

• Dynamic Diary system automating collection paths.

• Integration of Cash and Collect – Resulting in automatic allocation of payments, allowing collectors to only contact those that have not paid.

• Credit Controllers do the right thing at the right time.