Air Cargo Market Outlookaircargopedia.com/pdf/GMF2014Presentation.pdfMonthly air freight evolution...

26

Overview of the Airbus Cargo Global Market Forecast 2014-2033 Air Cargo Market Outlook

Transcript of Air Cargo Market Outlookaircargopedia.com/pdf/GMF2014Presentation.pdfMonthly air freight evolution...

Overview of the Airbus Cargo Global Market Forecast 2014-2033

Air Cargo Market Outlook

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

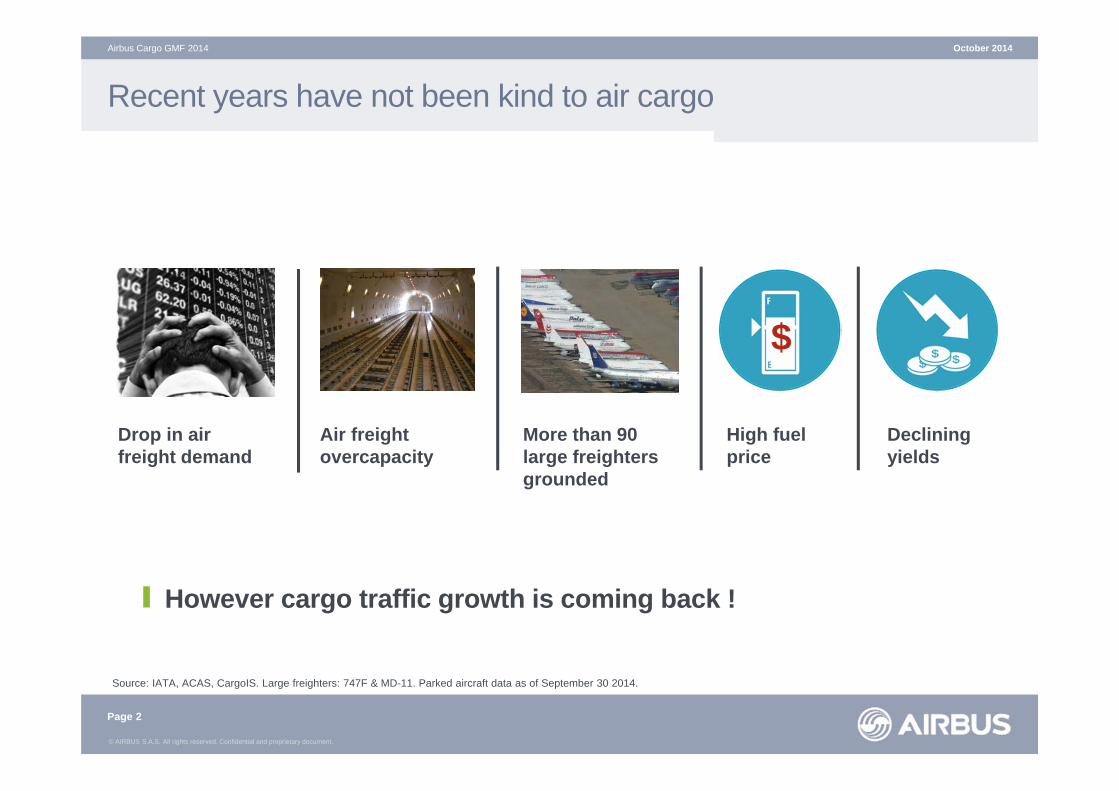

Recent years have not been kind to air cargo

More than 90 large freighters grounded

Air freightovercapacity

Source: IATA, ACAS, CargoIS. Large freighters: 747F & MD-11. Parked aircraft data as of September 30 2014.

However cargo traffic growth is coming back !

October 2014Airbus Cargo GMF 2014

Declining yields

High fuel price

$

Page 2

Drop in air freight demand

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

10

11

12

13

14

15

16

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

2014 growth rate estimate:

4.7%

…but today the air freight industry is growing again

October 2014Airbus Cargo GMF 2014

Source: Seabury, IATA, Airbus

Monthly air freight evolutionBillion FTKs (Freight tonne kilometres) Air freight volumes just

reached again the 2011 peak-Growth drivers:• Regional traffic• Express traffic• Emerging economies

Page 3

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

Time sensitive express goods proved more resilient to the crisis

Source: Seabury

October 2014

Page 4

Airbus Cargo GMF 2014

International air freight growthyear-over-year evolution (%)

11%

1%

-7%

20%

8%4% 5%4%

-3%

-12%

25%

-1%

-5%

0%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30% Express

General Cargo

2007 2008 2009 2010 2011 2012 2013

Express Cargo grew

50% in 7 years-General cargo

stagnatedin the last 7 years

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

Freight traffic growth and GDP are closely linked

Source: DOT, IATA, IHS Global Insight

GDP FTK

GDP and FTKs year on year growth evolution

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1989 1994 1999 2004 2009 2014 est

GDP FTK

October 2014

Page 5

Airbus Cargo GMF 2014

2014 YoY growth (estimates)

GDP 2.6%FTK 4.7%-Together traffic and world GDP are recovering

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

47%

49%

4%

34%

62%

4%

World GDP is set to nearly double over 20 years

Source: IHS Global Insight

2013

2033Emerging economies will account for almost half of world GDP in 2033

Distribution of worldwide GDP

0

20

40

60

80

100

120

140

2001 2005 2009 2013 2017 2021 2025 2029 2033

DevelopingEmergingAdvanced

History Forecast

34%

62%

47%

49%

Total worldwide GDP evolution Real in $US trillion

October 2014

Page 6

Airbus Cargo GMF 2014

DevelopingEmergingAdvanced

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1989 1994 1999 2004 2009 2014 est.

World Trade FTK

Cargo traffic and world trade are also well linked

Source: ICAO, IATA, Airbus

World trade and FTKs growth evolution

October 2014

Page 7

Airbus Cargo GMF 2014

World trade shows continuous signs of improvement-World trade is driven by emerging markets, which are experiencing solid

growth momentum

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

World trade is set to more than double by 2033

Source: IHS Global Insight, Airbus, Seabury

Total world international trade evolution (Trillion $US)

In the future, the traditional air cargo trade links will further diversify

October 2014

Page 8

Airbus Cargo GMF 2014

0

10

20

30

40

50

60

2001 2005 2009 2013 2017 2021 2025 2029 2033

DevelopingEmergingAdvanced

History Forecast

x3

World trade will grow on average

4.3%over the next 20 years -Emerging countries’ trade

to almost triple over the next 20 years

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

New trade links will alter the current trunk routes

World trade in 2013 and 2033 by region

Geographic locations for supply and demand will be different – traffic and cargo capacity will follow

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000 50,000

Asia/Pacific

Europe

North America

Latin America

Africa

CIS

Middle East

Trade (billion $US)

2013 trade 2033 trade

October 2014

Page 9

Airbus Cargo GMF 2014

Source: IHS Global Insight

Traffic within Asia-Pacific will be equivalent to PRC-North America flow-Latin America and

Africa will also drive growth

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

Africa, Middle East and Latin America to lead growthalong with Asia-Pacific

GDP growth rate, historical and forecast

4.1%4.2%

4.4%

3.2%

2.4%2.6%

1.9%

4.6%4.5%

3.9% 3.8%

3.1%

2.5%

1.9%

0%

1%

2%

3%

4%

5%

6%

Africa Asia/Pacific Middle East LatinAmerica

CIS NorthAmerica

Europe

1993-2013 2013-2033

October 2014

Page 10

Airbus Cargo GMF 2014

Source: IHS Global Insight, Airbus

Mature economies’ GDP to grow at

2.1%Rest of the world to grow at

4.8% -Asymmetric economic

growth will alter cargo traffic

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

0

50

100

150

200

250

300

Advanced Developing Emerging

2033

2013

1993

X2.7

X1.9X1.5

Global supply: production centres will shift even further into emerging economies

Source: IHS Global Insight, Airbus

Industrial Production by market(base year 2013 = 100)

In the future, air cargo traffic between production centres will be redefined

October 2014

Page 11

Airbus Cargo GMF 2014

Further outsourcingof production to low labour cost countries-• More market

fragmentation will be experienced

• New routes will add to traditional East-West trunk routes

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

Global demand: purchasing power will follow suit

Source: Kharas and Gertz, Airbus

Global Middle Class(Millions of people)

Middle-class: Households with daily expenditures between $10 and $100 per person (at PPP)

October 2014

Page 12

Airbus Cargo GMF 2014

679 673264 252

1,413

4,450

0

1,000

2,000

3,000

4,000

5,000

6,000

2013 2033

Emerging countries2,356

5,375

North AmericaEurope

World Population

% of world population

8,500

63%

7,200

33%

X2.3

X3.2

Middle class in mature economies will stagnate-Middle class in emerging

countries will triple

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

Emerging economies are not only located in Asia-Pacific

Source: IHS Global Insight, Airbus

500 million people

Latin America

430 million people

Africa

380 million people

Eastern Europe & CIS

3500 million people

Asia-Pacific

60million people

Middle East

October 2014

Page 13

Airbus Cargo GMF 2014

Growing population and consumption will drive trade and air freight

Population in emerging countries in 2014

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

GMF freight forecast overview

• 20 years freighter aircraft demand forecast of jet freighters over 10 tonnes

• Traffic forecast modeling 150 distinct traffic flows

• Fleet build-ups covering 197 freight carriers

• Freighters fleet divided in 3 segments:• Small jet freighters: 10-30 tonnes• Mid-size freighters: 30-80 tonnes• Large freighters: >80 tonnes

October 2014

Page 14

Airbus Cargo GMF 2014

Source: Airbus GMF 2014

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

4.5% world FTK growth, driven by the strong traffic growth of emerging countries

Freight traffic growth, domestic + internationalFTKs (billions)

Future traffic with emerging economies will alter today’s freighter fleets and networks

Growth Rate 2013-2033

October 2014

Page 15

Airbus Cargo GMF 2014

0

100

200

300

400

500

ForecastHistory2.7%

Advanced –Advanced CAGR

4.9%

Advanced –Emerging CAGR

5.0%

Emerging –Advanced CAGR

6.2%

Emerging –Emerging CAGR

Source: Airbus GMF 2014

80%

20 year world annual FTK growth

4.5 %-Total traffic growth includes main deck and belly capacity

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

0

100

200

300

400

500

2013 2033

Dedicated freightersBelly cargo

51%

56%

Belly capacity to capture market shares over main deck

Airbus Cargo GMF 2014

Page 16

October 2014

Worldwide share of belly vs dedicated cargo trafficEstimates FTKs (billion)

Cargo traffic growth 4.5%

Belly traffic growth 4.9%

Source: Airbus GMF 2014

Due to the faster expansion of passenger traffic, belly capacity will capture market shares-Impact is mainly on long haul flows and larger freighters

Page 16

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

Dedicated freightersBelly cargo

0

50

100

150

200

250

FTK 2013 FTK 20330

50

100

150

200

250

FTK 2013 FTK 2033

Cargo growth 4.7% p.a.

55%

65%

Belly shift will impact particularly long haul flows

Airbus Cargo GMF 2014

43% 45%

Page 17

October 2014

Short haul <1,500nm

Medium haul1,500nm< & <5,000nm

Share of belly vs dedicated cargo trafficEstimated FTKs (billion)

0

50

100

150

200

250

FTK 2013 FTK 2033

Cargo growth 4.8% p.a.

54%

55%

Long Haul >5,000nm

Cargo growth 3.4% p.a.

Belly growth 3.6% p.a. Belly growth 4.9% p.a.

Page 17

Belly growth 5.6% p.a.

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

Freighter fleet will increase to almost 2700 aircraft over 20 years

Freighter fleet

1,605

287

1,318

1040

0

500

1,000

1,500

2,000

2,500

3,000

Beginning 2014 2033

October 2014

Page 18

Airbus Cargo GMF 2014

Source: Airbus GMF 2014

Growth

Replacement

Stay in service

New Built803

Conversion1555

2,645

55% of deliveries are for replacement-Future fleet will be a mix of new built and converted freighters

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

The future freighter fleet distribution will reflect the growing influence of emerging markets

World fleet

Asia Pacific fleet is setto triple as growth market

North America fleet is mainlya replacement market

775977

North America

337452

Europe & CIS

74162

Latin America 4986Africa

67170

Middle East

303798

Asia Pacific

2033: 26452014: 1605

October 2014

Page 19

Airbus Cargo GMF 2014

Source: Airbus GMF 2014, ASCEND

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

800 new built freighters to be delivered over the next 20 years

Freighter deliveries over the next 20 years

731

212

414

389

0

500

1,000

1,500

Small Mid-Size Large

New freighters

Conversions

601612

1145

10t < payload < 30t 30t < payload < 80t payload > 80t

October 2014

Page 20

Airbus Cargo GMF 2014

Source: Airbus GMF 2014

Mid-size drivers• Replacement for: US,

EU• Large growth in Asia

Pacific• New routes in Middle

East, Latin America, Africa-

Large freighters will face increasing competition from belly capacity

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

Proportion of future freighters

29%

Airbus 2014 forecast key numbers

20 year annual FTK growth

4.5%

20 year demand for aircraft deliveries

2358803

Total

New

Business volume for new freighters

$210bn

Mid-size

Large

47%24%Small

October 2014

Page 21

Airbus Cargo GMF 2014

Source: Airbus GMF 2014

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

Airbus recognises the need for mid-size freighters

October 2014Airbus Cargo GMF 2014

Page 22

Nearly 50% of all freighters will be mid-size-The A330-200F is the most modern mid-size freighter on the market

A330 Freighters: From short, regional express routes to long haul general cargo

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

The A330F concept: Connecting diverse economies with diverse networks

204,447flight hours

59,614take-offs

99.5%reliability

Flying East-West, North-South, long-haul, short-haul, regional operations and to new markets

October 2014

Page 23

Airbus Cargo GMF 2014

Source: Airbus (Data up to September 2014 OR = >15’ delays + Cancellations + Diversions + IFTBs

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

October 2014Airbus Cargo GMF 2014

Page 24

$300

$500

$700

$900

$1,100

$1,300

$1,500

$1,700

$1,900

$2,100

$2,300

20 30 40 50 60 70 80 90 100 110 120 130 140

COC*/t

Demand(Tonnes)

A330-200F

777F

747-8F

Today’s large freighters only work on the heaviest trade lanes

Large freighters need high demand and payloads all year-Mid-size freighters are more efficient when fuel, demand or yields fluctuate

As the global economy changes shape, airlines must adapt their capacity and network

Costs per tonne carried

- 35% High risk

COC*: Cash Operating Costs - Includes Fuel, Maintenance, Nav&Landing fees, Crew costs 3,000nm sector – JAR 5% flight profile

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

October 2014Airbus Cargo GMF 2014

Page 25

The ‘one-type-fits-all’ air cargo model no longer works

Mid-sized freighters

• When belly cargo is non existent or insufficient

• For diversified networks• A flexible option for a

changing industry

Belly cargo

• Basic cargo offering: limited cost, limited risk

• Growing available capacity on long haul trunk routes

100t+ freighters

• For a limited number of high demand trunk routes

• Challenged by growing belly lift on longer hauls

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document.

© AIRBUS S.A.S. All rights reserved. Confidential and proprietary document. This document and all information contained herein is the sole property of AIRBUS S.A.S. No intellectual property rights are granted by thedelivery of this document or the disclosure of its content. This document shall not be reproduced or disclosed to a third party without the express written consent of AIRBUS S.A.S. This document and its content shall not beused for any purpose other than that for which it is supplied. The statements made herein do not constitute an offer. They are based on the mentioned assumptions and are expressed in good faith. Where the supportinggrounds for these statements are not shown, AIRBUS S.A.S. will be pleased to explain the basis thereof.AIRBUS, its logo, A300, A310, A318, A319, A320, A321, A330, A340, A350, A380, A400M are registered trademarks.

October 2014

Page 26

Airbus Cargo GMF 2014