Advisory Board Presentation - AIMaim.nd.edu/assets/225946/aim_xliii_final_presentation.pdf ·...

121

Advisory Board Presentation AIM XLIII | December 5, 2016

Transcript of Advisory Board Presentation - AIMaim.nd.edu/assets/225946/aim_xliii_final_presentation.pdf ·...

Advisory Board Presentation

AIM XLIII | December 5, 2016

AIM XLIII t

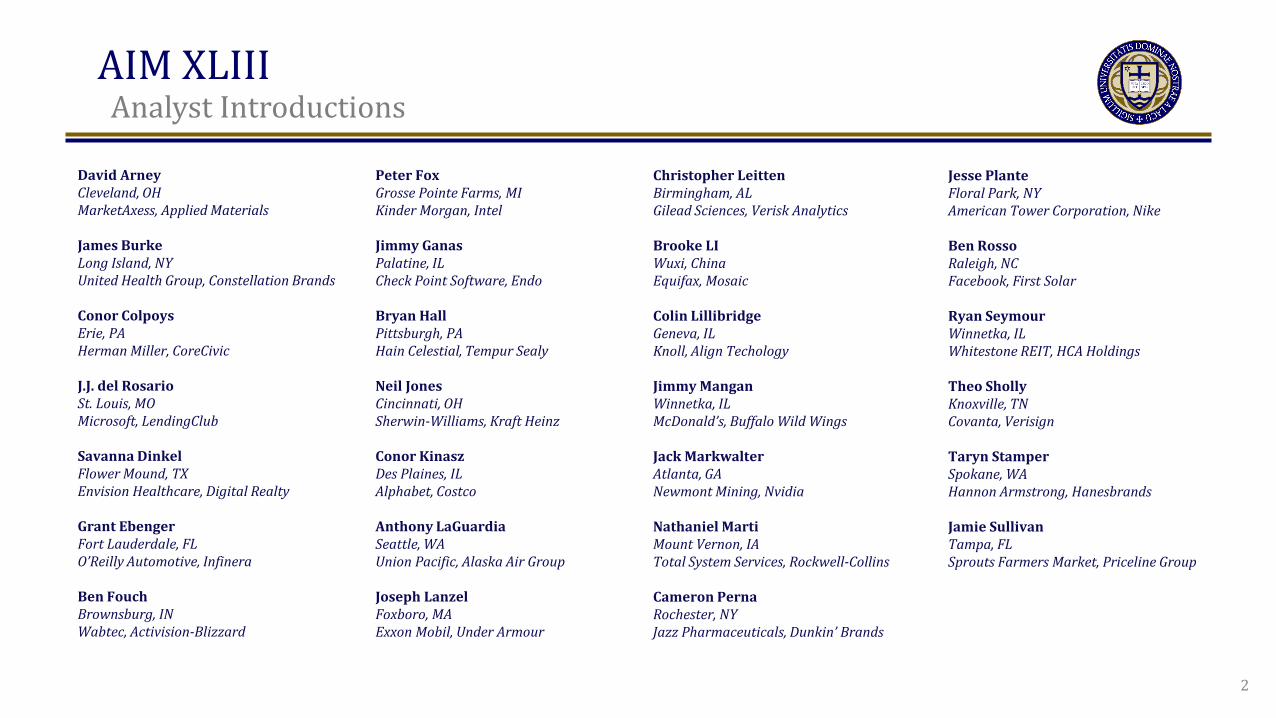

Analyst Introductions

David Arney Cleveland, OH MarketAxess, Applied Materials James Burke Long Island, NY United Health Group, Constellation Brands Conor Colpoys Erie, PA Herman Miller, CoreCivic J.J. del Rosario St. Louis, MO Microsoft, LendingClub Savanna Dinkel Flower Mound, TX Envision Healthcare, Digital Realty Grant Ebenger Fort Lauderdale, FL O’Reilly Automotive, Infinera Ben Fouch Brownsburg, IN Wabtec, Activision-Blizzard

Peter Fox Grosse Pointe Farms, MI Kinder Morgan, Intel Jimmy Ganas Palatine, IL Check Point Software, Endo Bryan Hall Pittsburgh, PA Hain Celestial, Tempur Sealy Neil Jones Cincinnati, OH Sherwin-Williams, Kraft Heinz Conor Kinasz Des Plaines, IL Alphabet, Costco Anthony LaGuardia Seattle, WA Union Pacific, Alaska Air Group Joseph Lanzel Foxboro, MA Exxon Mobil, Under Armour

Christopher Leitten Birmingham, AL Gilead Sciences, Verisk Analytics Brooke LI Wuxi, China Equifax, Mosaic Colin Lillibridge Geneva, IL Knoll, Align Techology Jimmy Mangan Winnetka, IL McDonald’s, Buffalo Wild Wings Jack Markwalter Atlanta, GA Newmont Mining, Nvidia Nathaniel Marti Mount Vernon, IA Total System Services, Rockwell-Collins Cameron Perna Rochester, NY Jazz Pharmaceuticals, Dunkin’ Brands

Jesse Plante Floral Park, NY American Tower Corporation, Nike Ben Rosso Raleigh, NC Facebook, First Solar Ryan Seymour Winnetka, IL Whitestone REIT, HCA Holdings Theo Sholly Knoxville, TN Covanta, Verisign Taryn Stamper Spokane, WA Hannon Armstrong, Hanesbrands Jamie Sullivan Tampa, FL Sprouts Farmers Market, Priceline Group

2

Agenda Course Overview Economic Outlook Security Analysis Portfolio Performance AIM XLIII Review Concluding Remarks

Course Overview Fundamentals Analyst Responsibilities Investment Philosophy and Policies

Course Overview t

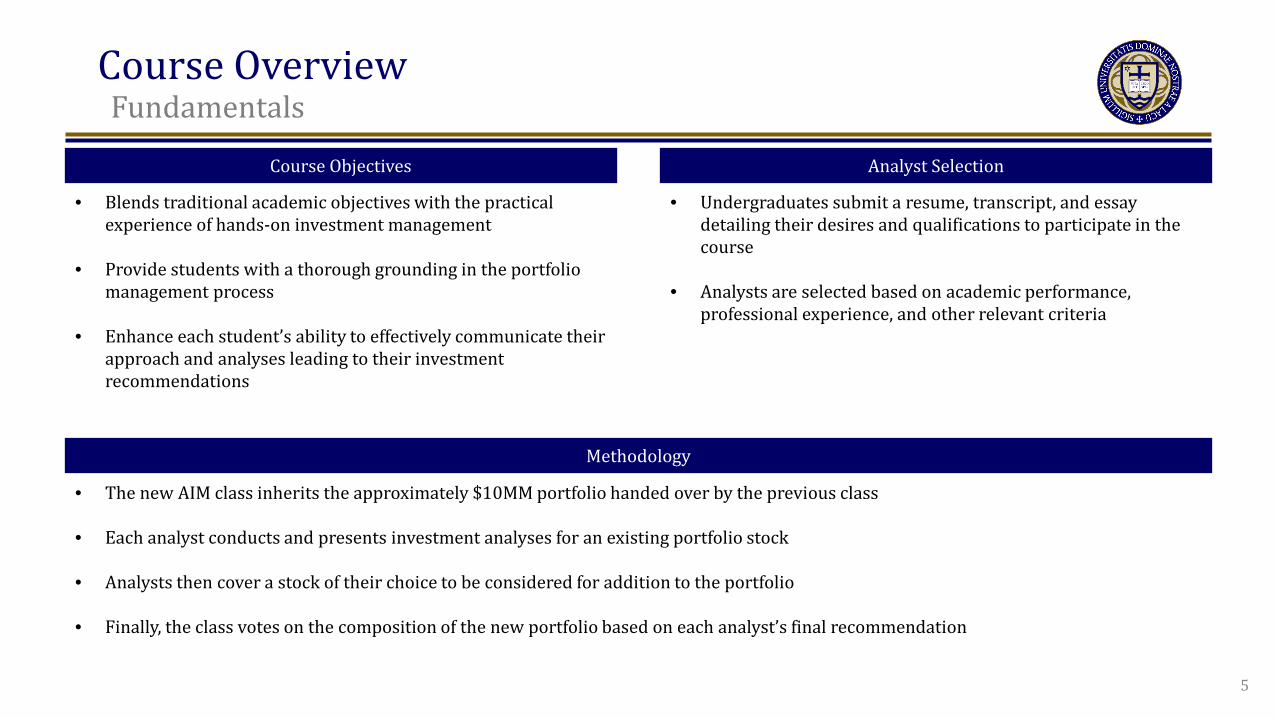

Fundamentals

Methodology

Analyst Selection Course Objectives

• Blends traditional academic objectives with the practical experience of hands-on investment management

• Provide students with a thorough grounding in the portfolio management process

• Enhance each student’s ability to effectively communicate their approach and analyses leading to their investment recommendations

• Undergraduates submit a resume, transcript, and essay detailing their desires and qualifications to participate in the course

• Analysts are selected based on academic performance, professional experience, and other relevant criteria

• The new AIM class inherits the approximately $10MM portfolio handed over by the previous class

• Each analyst conducts and presents investment analyses for an existing portfolio stock

• Analysts then cover a stock of their choice to be considered for addition to the portfolio

• Finally, the class votes on the composition of the new portfolio based on each analyst’s final recommendation

5

Course Overview t

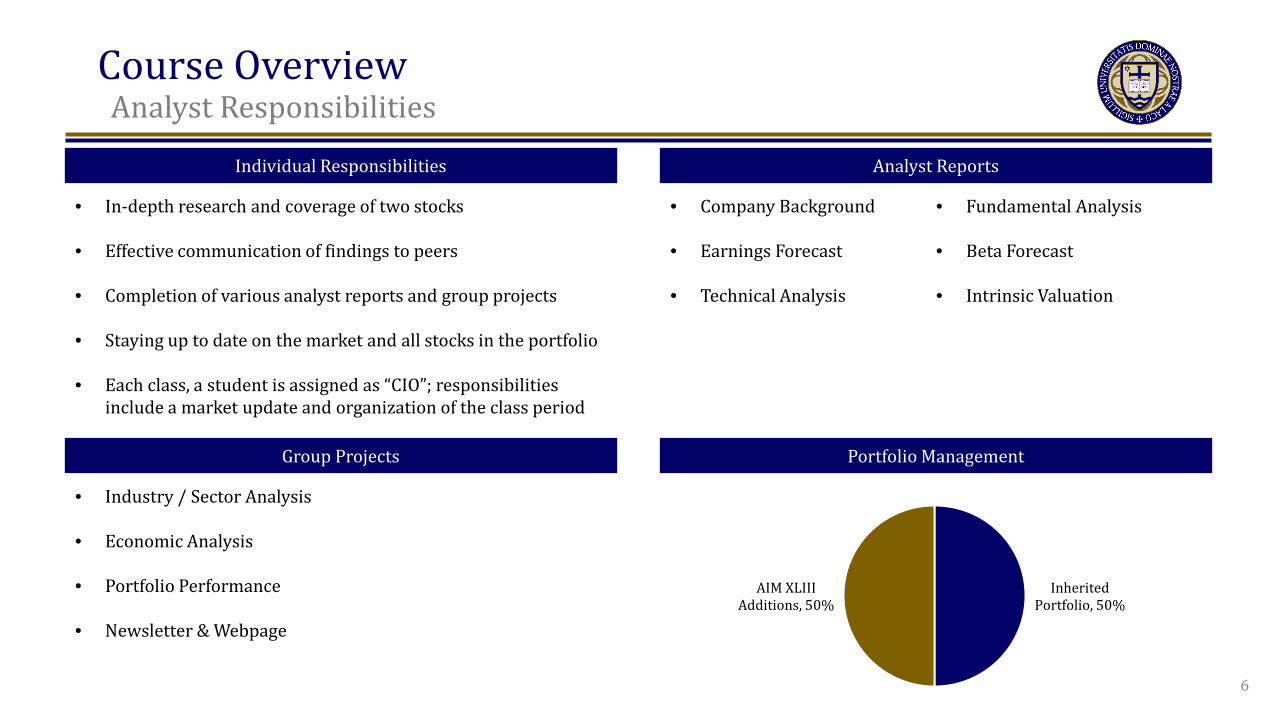

Analyst Responsibilities

Analyst Reports Individual Responsibilities

Portfolio Management Group Projects

• Company Background

• Earnings Forecast

• Technical Analysis

• Fundamental Analysis

• Beta Forecast

• Intrinsic Valuation

• Industry / Sector Analysis

• Economic Analysis

• Portfolio Performance

• Newsletter & Webpage

• In-depth research and coverage of two stocks

• Effective communication of findings to peers

• Completion of various analyst reports and group projects • Staying up to date on the market and all stocks in the portfolio

• Each class, a student is assigned as “CIO”; responsibilities

include a market update and organization of the class period

Inherited Portfolio, 50%

AIM XLIII Additions, 50%

6

Course Overview t

Investment Philosophy and Policies

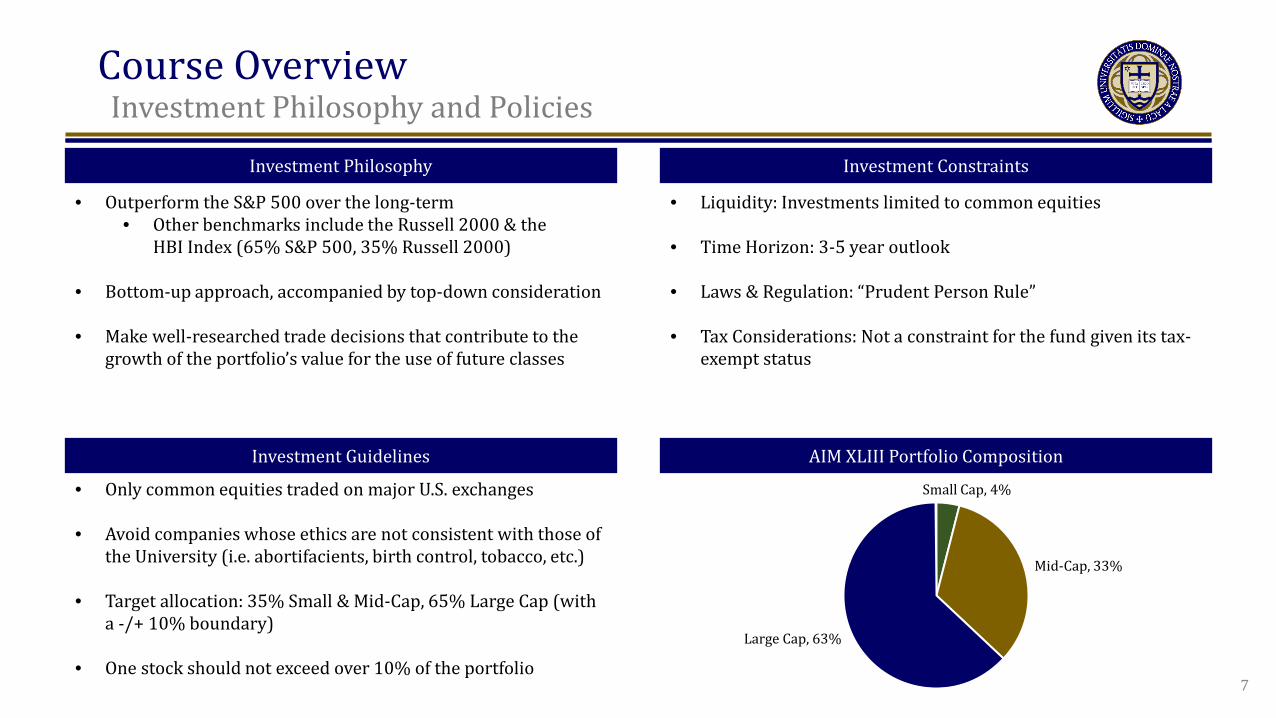

Investment Constraints Investment Philosophy

AIM XLIII Portfolio Composition Investment Guidelines

• Liquidity: Investments limited to common equities

• Time Horizon: 3-5 year outlook

• Laws & Regulation: “Prudent Person Rule”

• Tax Considerations: Not a constraint for the fund given its tax-exempt status

• Outperform the S&P 500 over the long-term • Other benchmarks include the Russell 2000 & the

HBI Index (65% S&P 500, 35% Russell 2000)

• Bottom-up approach, accompanied by top-down consideration • Make well-researched trade decisions that contribute to the

growth of the portfolio’s value for the use of future classes

• Only common equities traded on major U.S. exchanges

• Avoid companies whose ethics are not consistent with those of the University (i.e. abortifacients, birth control, tobacco, etc.)

• Target allocation: 35% Small & Mid-Cap, 65% Large Cap (with

a -/+ 10% boundary)

• One stock should not exceed over 10% of the portfolio

Small Cap, 4%

Mid-Cap, 33%

Large Cap, 63%

7

Economic Outlook Overview Sovereign Yields Central Bank Policy Labor Market Household Data and Consumption Foreign Exchange Current Events Impact on Portfolio

Economic Outlook t

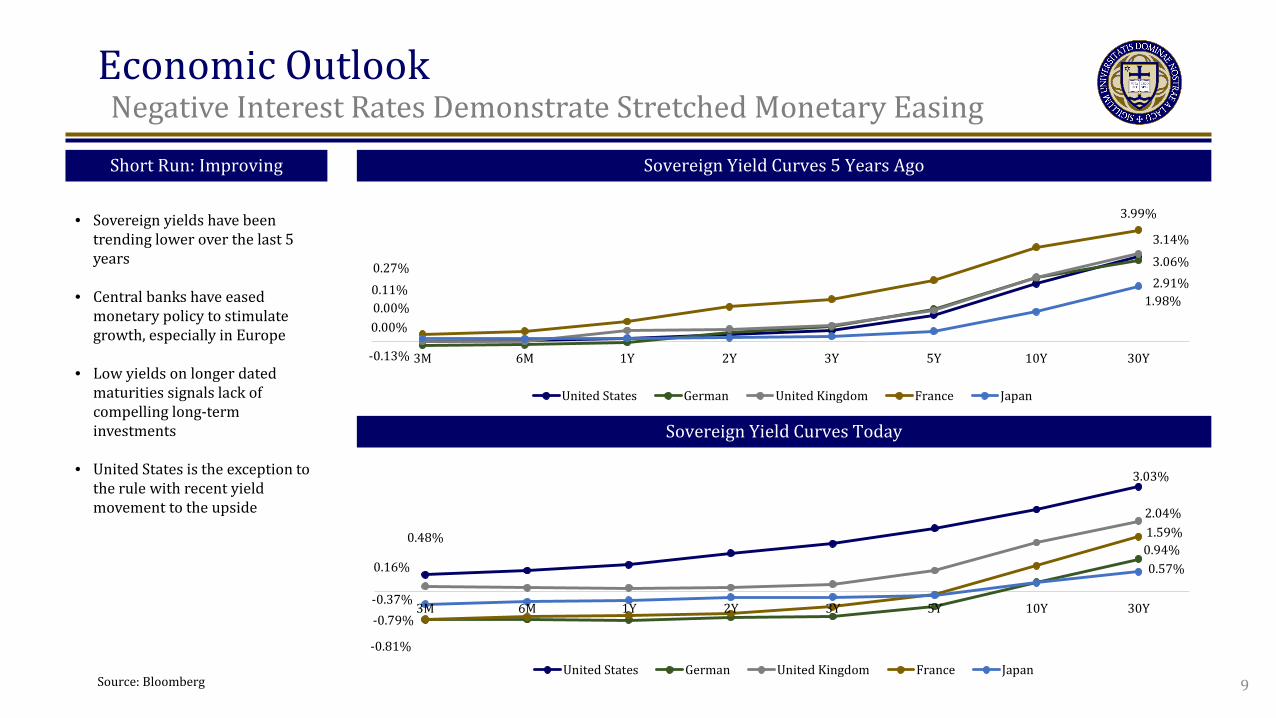

Negative Interest Rates Demonstrate Stretched Monetary Easing

Sovereign Yield Curves 5 Years Ago

Sovereign Yield Curves Today

0.48%

3.03%

-0.81%

0.94% 0.16%

2.04%

-0.79%

1.59%

-0.37%

0.57%

3M 6M 1Y 2Y 3Y 5Y 10Y 30Y

United States German United Kingdom France Japan

0.00%

3.06%

-0.13%

2.91%

0.00%

3.14%

0.27%

3.99%

0.11% 1.98%

3M 6M 1Y 2Y 3Y 5Y 10Y 30Y

United States German United Kingdom France Japan

Short Run: Improving

• Sovereign yields have been trending lower over the last 5 years

• Central banks have eased monetary policy to stimulate growth, especially in Europe

• Low yields on longer dated maturities signals lack of compelling long-term investments

• United States is the exception to the rule with recent yield movement to the upside

9 Source: Bloomberg

Economic Outlook t

Central Bank Balance Sheet Expansion

Central Bank Assets to GDP Commentary

• Central Banks have used their balance sheets to fuel asset purchases

• Goal has been to lower interest rates on longer dated maturities and provided liquidity

• Limits of QE have likely been reached as Central Bank balance sheets have grown

• Indicative of less monetary tools available in the future

5.6% 5.3% 5.4% 8.7% 12.4% 14.7% 15.9% 18.9%

23.0% 17.9%

14.9% 13.7% 14.7%

15.8% 18.4%

22.5%

31.2%

45.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014

FED BOJ

BOJ Oct. 2012: second increase in asset buybacks to curb deflation

BOJ Oct. 2012: increase in asset buybacks as Abe promises accommodative stance

BOJ Apr. 2013: Plan to purchase 60-70 trillion Yen a year, double money base in 2 years

BOJ Oct. 2014: Asset purchases begin at 80 trillion Yen a year

FED Nov. 2008: $30bn in Treasury purchases every month “QE1”

FED Nov. 2010: purchases of $600bn in Treasury securities for one year “QE2”

FED Jun. 2013: launch of $40bn additional purchases of agency mortgages back securities “QE3”

10 Source: St. Louis Fed

Economic Outlook t

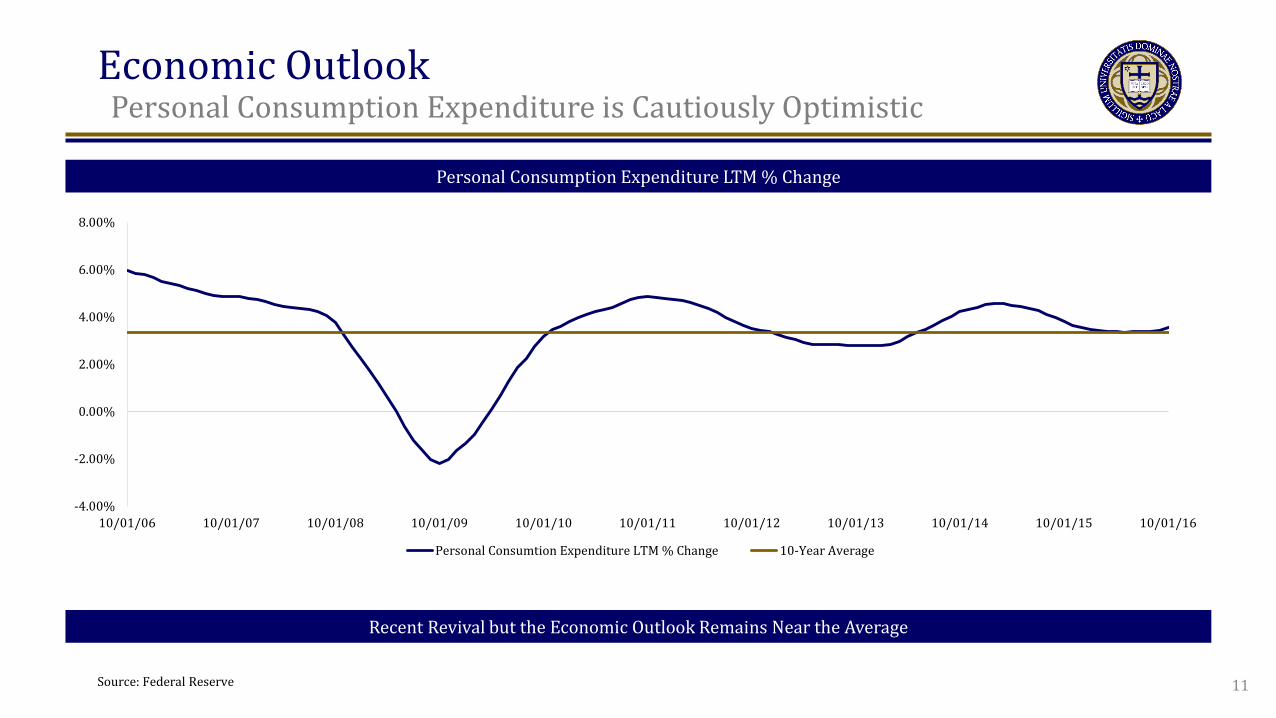

Personal Consumption Expenditure is Cautiously Optimistic

Personal Consumption Expenditure LTM % Change

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

10/01/06 10/01/07 10/01/08 10/01/09 10/01/10 10/01/11 10/01/12 10/01/13 10/01/14 10/01/15 10/01/16

Personal Consumtion Expenditure LTM % Change 10-Year Average

Recent Revival but the Economic Outlook Remains Near the Average

11 Source: Federal Reserve

Economic Outlook t

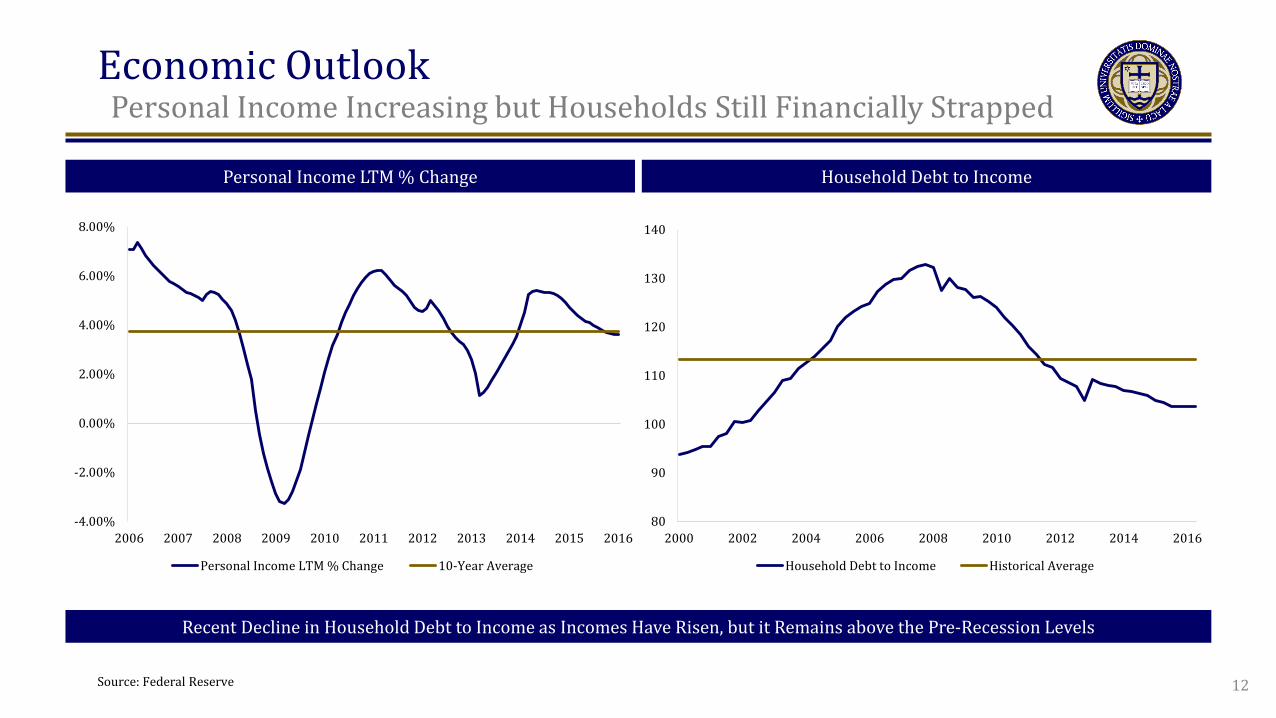

Personal Income Increasing but Households Still Financially Strapped

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Personal Income LTM % Change 10-Year Average

Household Debt to Income Personal Income LTM % Change

80

90

100

110

120

130

140

2000 2002 2004 2006 2008 2010 2012 2014 2016

Household Debt to Income Historical Average

Recent Decline in Household Debt to Income as Incomes Have Risen, but it Remains above the Pre-Recession Levels

12 Source: Federal Reserve

Economic Outlook t

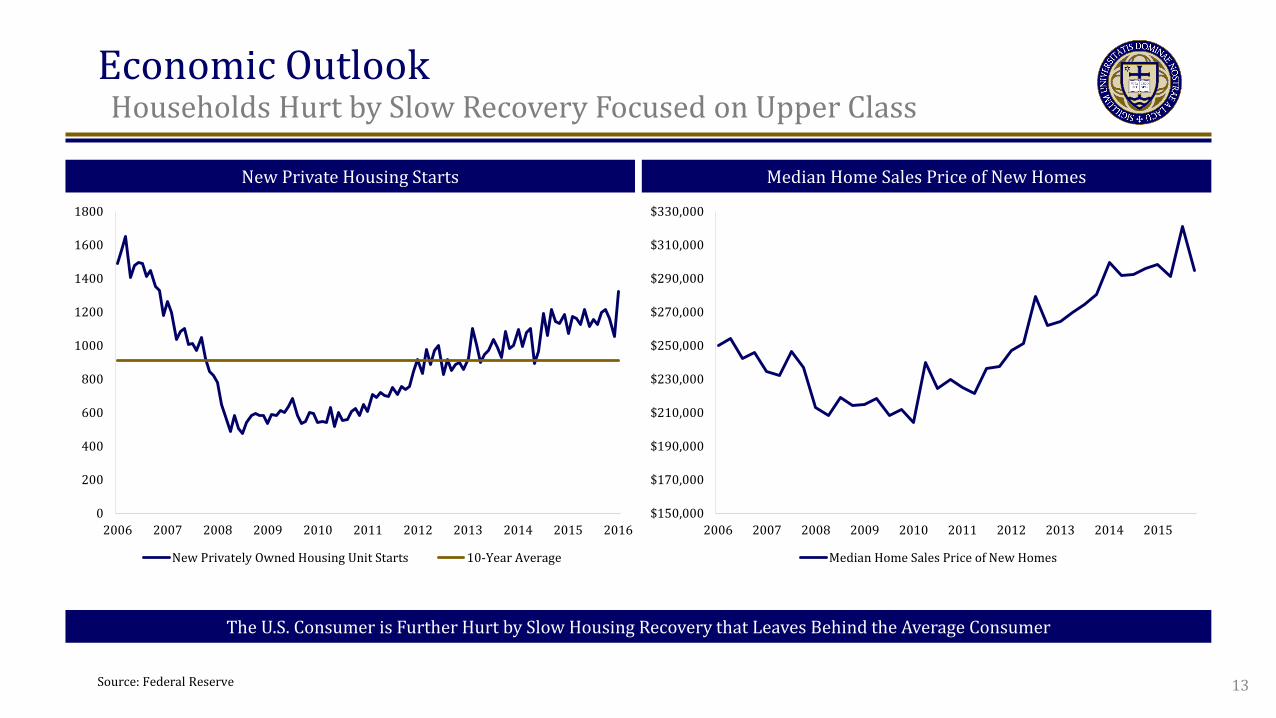

Households Hurt by Slow Recovery Focused on Upper Class

0

200

400

600

800

1000

1200

1400

1600

1800

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

New Privately Owned Housing Unit Starts 10-Year Average

$150,000

$170,000

$190,000

$210,000

$230,000

$250,000

$270,000

$290,000

$310,000

$330,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Median Home Sales Price of New Homes

Median Home Sales Price of New Homes New Private Housing Starts

The U.S. Consumer is Further Hurt by Slow Housing Recovery that Leaves Behind the Average Consumer

13 Source: Federal Reserve

Economic Outlook t

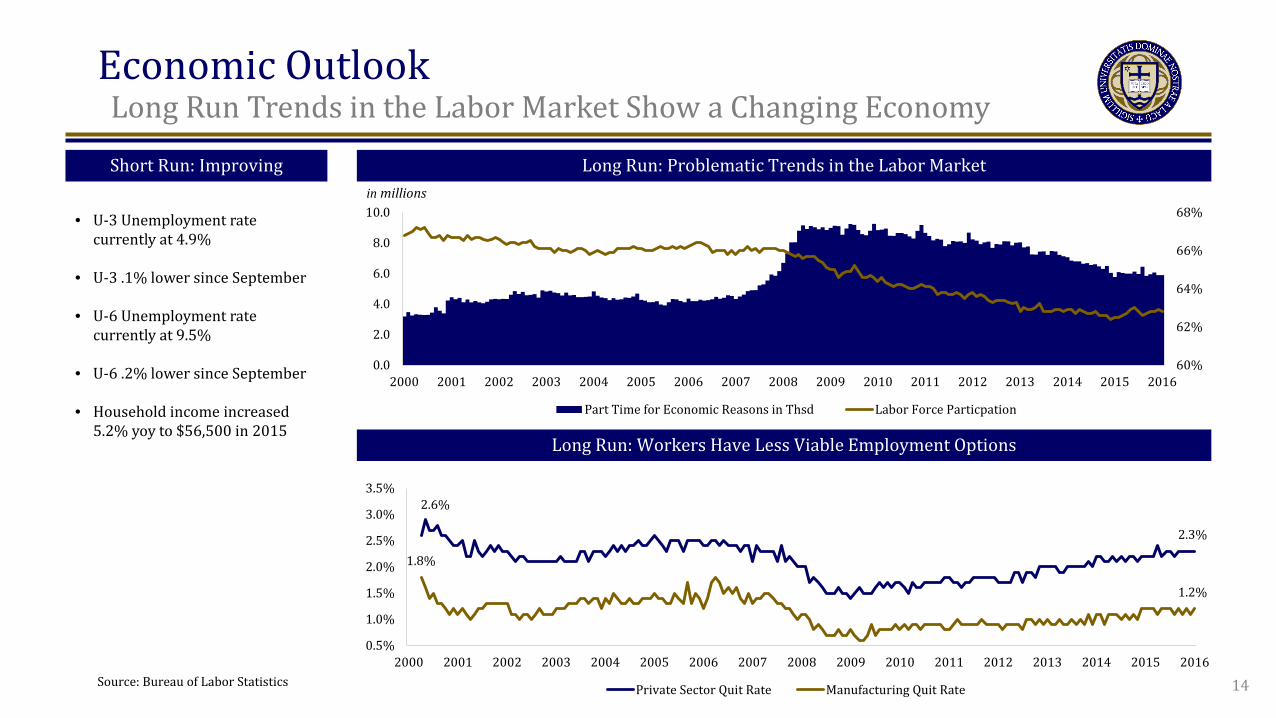

Long Run Trends in the Labor Market Show a Changing Economy

Long Run: Problematic Trends in the Labor Market

60%

62%

64%

66%

68%

0.0

2.0

4.0

6.0

8.0

10.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Part Time for Economic Reasons in Thsd Labor Force Particpation

2.6%

2.3%

1.8%

1.2%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Private Sector Quit Rate Manufacturing Quit Rate

Long Run: Workers Have Less Viable Employment Options

in millions

Short Run: Improving

• U-3 Unemployment rate currently at 4.9%

• U-3 .1% lower since September

• U-6 Unemployment rate currently at 9.5%

• U-6 .2% lower since September

• Household income increased 5.2% yoy to $56,500 in 2015

14 Source: Bureau of Labor Statistics

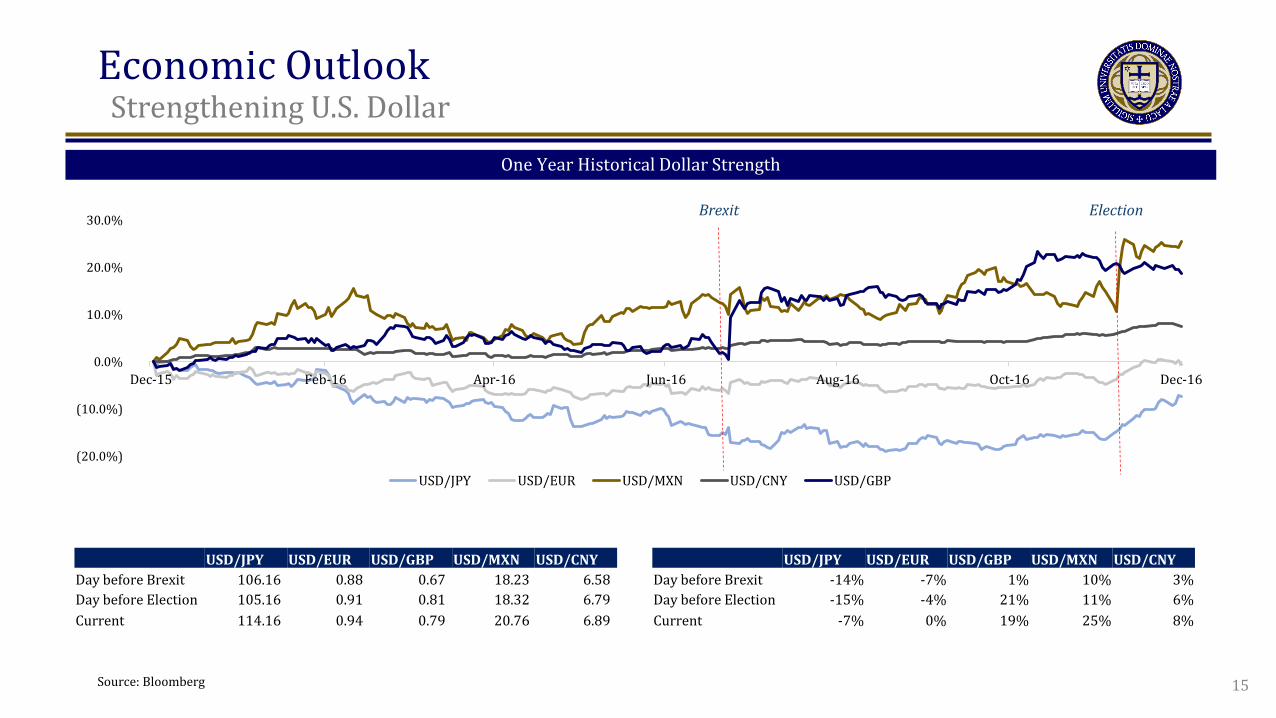

Economic Outlook t

Strengthening U.S. Dollar One Year Historical Dollar Strength

(20.0%)

(10.0%)

0.0%

10.0%

20.0%

30.0%

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16 Dec-16

USD/JPY USD/EUR USD/MXN USD/CNY USD/GBP

USD/JPY USD/EUR USD/GBP USD/MXN USD/CNY Day before Brexit -14% -7% 1% 10% 3% Day before Election -15% -4% 21% 11% 6% Current -7% 0% 19% 25% 8%

USD/JPY USD/EUR USD/GBP USD/MXN USD/CNY Day before Brexit 106.16 0.88 0.67 18.23 6.58 Day before Election 105.16 0.91 0.81 18.32 6.79 Current 114.16 0.94 0.79 20.76 6.89

Brexit Election

15 Source: Bloomberg

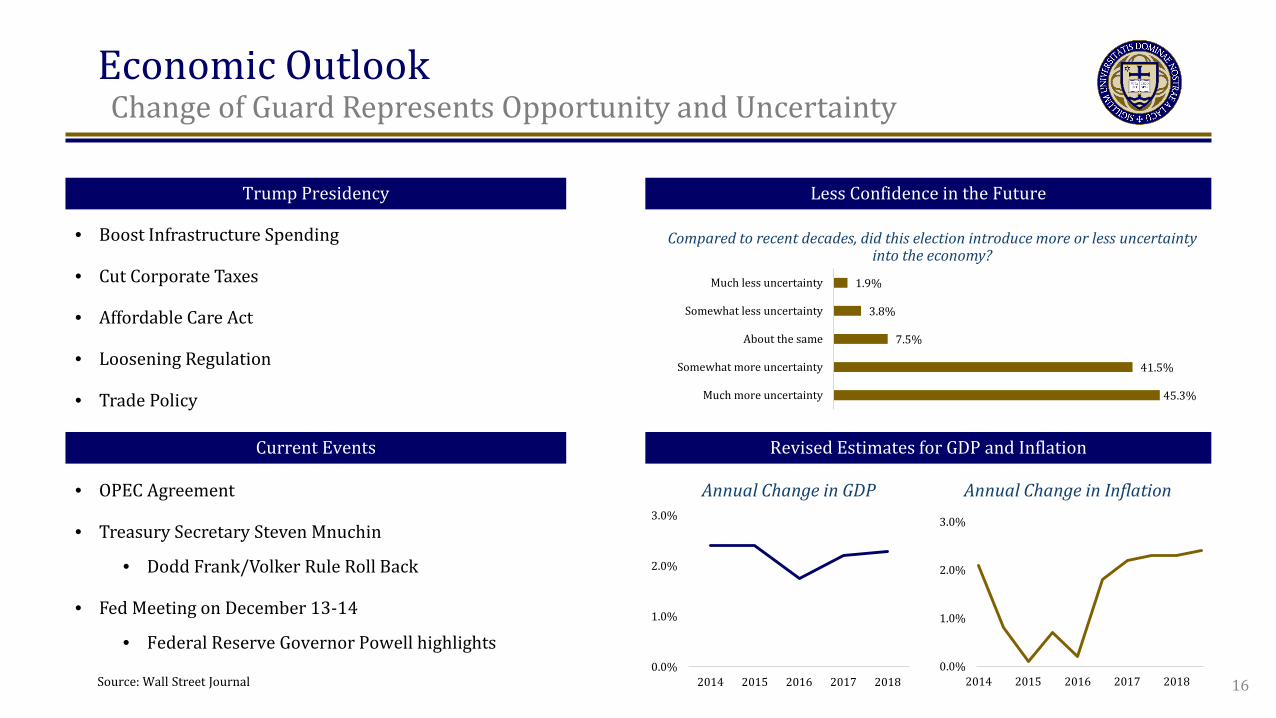

Economic Outlook t

Change of Guard Represents Opportunity and Uncertainty

• Boost Infrastructure Spending

• Cut Corporate Taxes

• Affordable Care Act

• Loosening Regulation

• Trade Policy 45.3%

41.5%

7.5%

3.8%

1.9%

Much more uncertainty

Somewhat more uncertainty

About the same

Somewhat less uncertainty

Much less uncertainty

Compared to recent decades, did this election introduce more or less uncertainty into the economy?

0.0%

1.0%

2.0%

3.0%

2014 2015 2016 2017 20180.0%

1.0%

2.0%

3.0%

2014 2015 2016 2017 2018

Current Events

Annual Change in GDP Annual Change in Inflation

Trump Presidency

• OPEC Agreement

• Treasury Secretary Steven Mnuchin

• Dodd Frank/Volker Rule Roll Back

• Fed Meeting on December 13-14

• Federal Reserve Governor Powell highlights

Revised Estimates for GDP and Inflation

Less Confidence in the Future

16 Source: Wall Street Journal

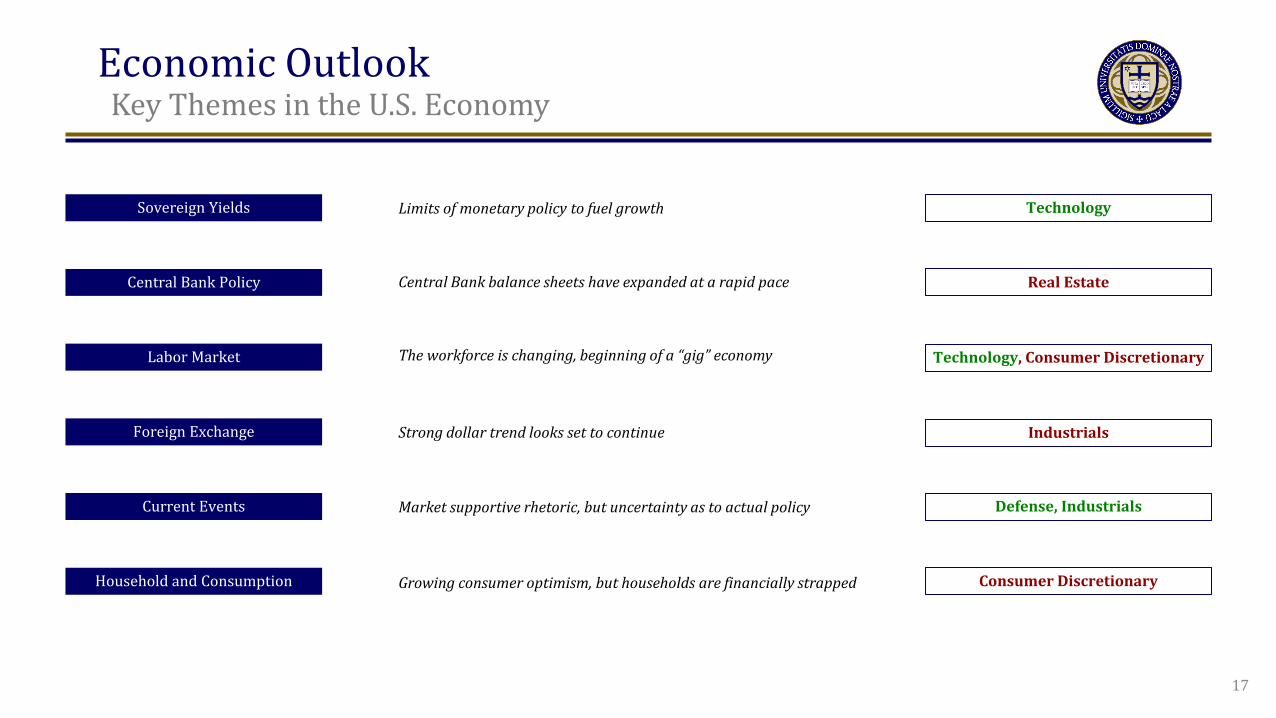

Economic Outlook t

Key Themes in the U.S. Economy

Sovereign Yields

Central Bank Policy

Labor Market

Current Events

Household and Consumption

Limits of monetary policy to fuel growth

Central Bank balance sheets have expanded at a rapid pace

The workforce is changing, beginning of a “gig” economy

Market supportive rhetoric, but uncertainty as to actual policy

Growing consumer optimism, but households are financially strapped

Technology

Real Estate

Technology, Consumer Discretionary

Defense, Industrials

Consumer Discretionary

Foreign Exchange Strong dollar trend looks set to continue Industrials

17

Security Analysis Company & Industry Overview Fundamental Analysis Discovery Earnings Analysis Beta Analysis Relative Valuation Discounted Cash Flow Valuation Alternative Valuation

Security Analysis t

Equities and Focus of Analysis

19

Earnings Analysis

Technical Analysis

Relative Valuation

Discounted Cash Flow

Discovery Company & Industry Overview Company & Industry Overview

Company & Industry Overview Discounted Cash Flow Discovery

Discovery Discounted Cash Flow Company & Industry Overview

Company & Industry Overview Relative Valuation Beta Analysis

Technical Analysis Fundamental Analysis Alternative Valuation Method Fundamental Analysis

Constellation Brands t

NYSE: STZ

One-Year Price Chart

Focus

Earnings Analysis

Price (As of November 30, 2016): $155.80

TTM Price-to-Earnings: 28.78x

Market Capitalization: $31.32Bn

Dividend Yield: 1.02%

TTM Adjusted Earnings per Share: $5.82

Source: S&P Capital IQ, Yahoo! Finance

$130

$140

$150

$160

$170

$180

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16

20

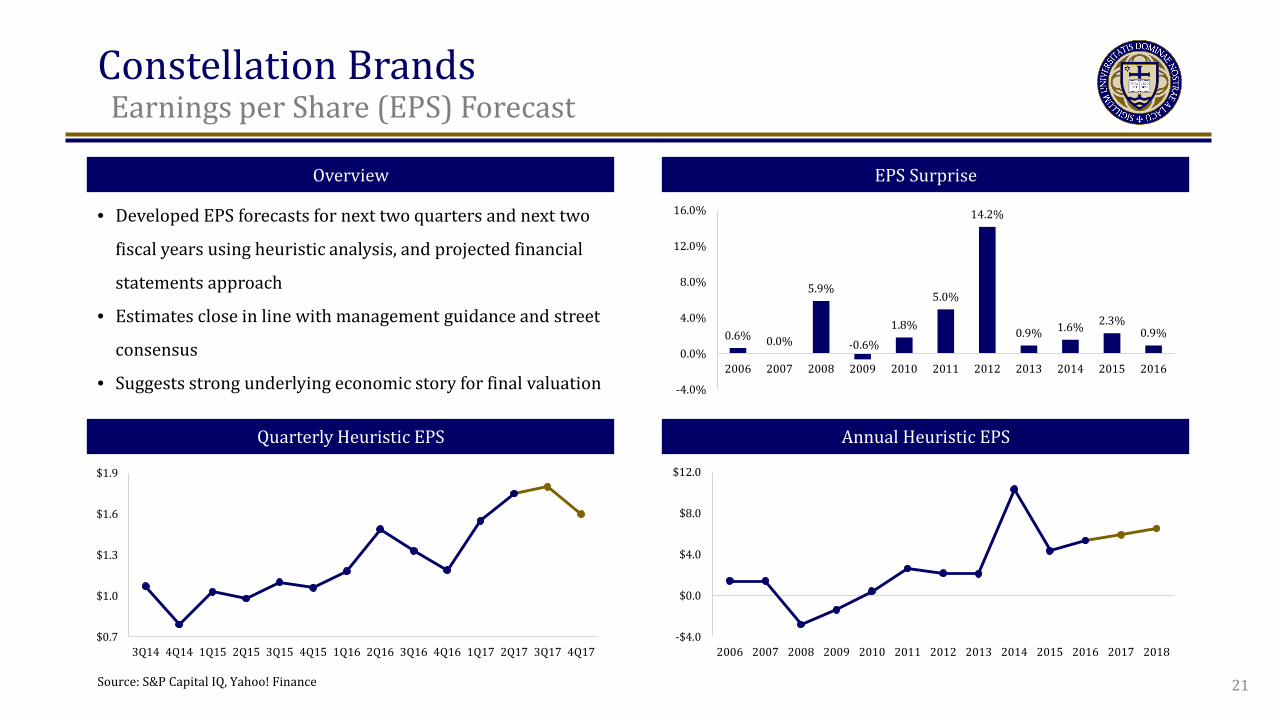

Constellation Brands t

Earnings per Share (EPS) Forecast

EPS Surprise Overview

Quarterly Heuristic EPS Annual Heuristic EPS

• Developed EPS forecasts for next two quarters and next two

fiscal years using heuristic analysis, and projected financial

statements approach

• Estimates close in line with management guidance and street

consensus

• Suggests strong underlying economic story for final valuation

0.6% 0.0%

5.9%

-0.6% 1.8%

5.0%

14.2%

0.9% 1.6% 2.3% 0.9%

-4.0%

0.0%

4.0%

8.0%

12.0%

16.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

-$4.0

$0.0

$4.0

$8.0

$12.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018$0.7

$1.0

$1.3

$1.6

$1.9

3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17

21 Source: S&P Capital IQ, Yahoo! Finance

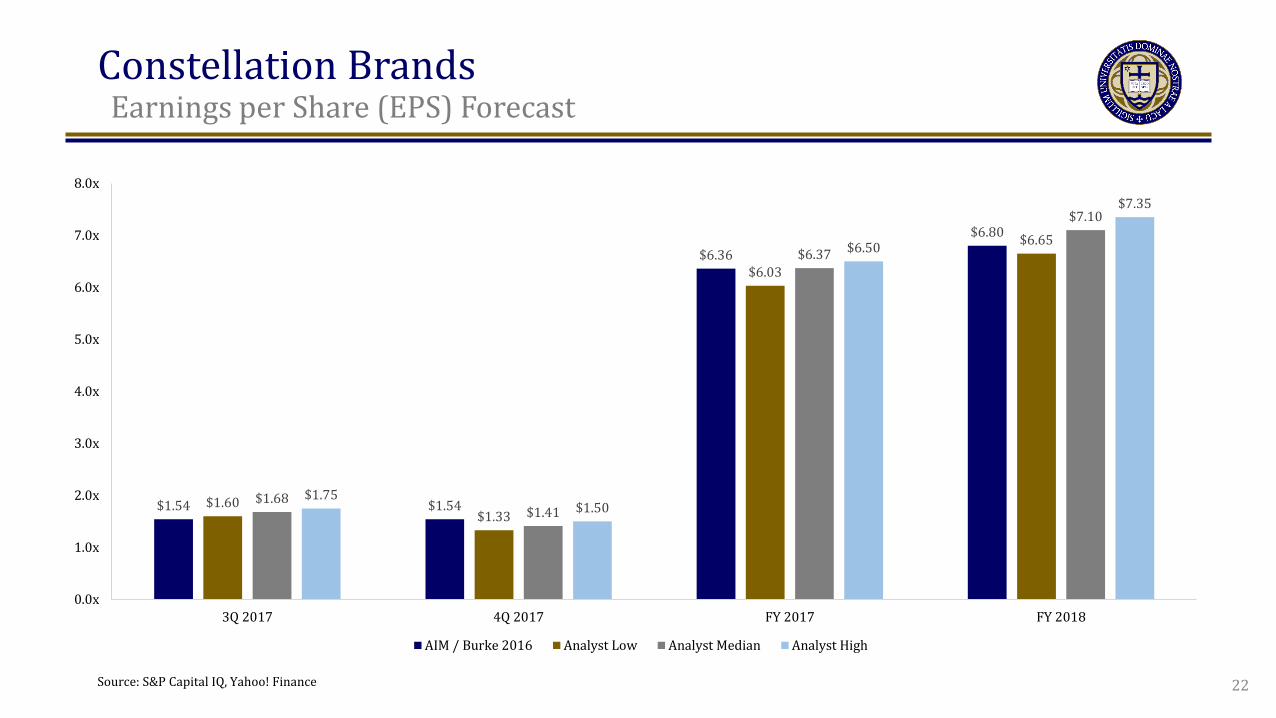

Constellation Brands t

Earnings per Share (EPS) Forecast

22

$1.54 $1.54

$6.36 $6.80

$1.60 $1.33

$6.03

$6.65

$1.68 $1.41

$6.37

$7.10

$1.75 $1.50

$6.50

$7.35

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

8.0x

3Q 2017 4Q 2017 FY 2017 FY 2018

AIM / Burke 2016 Analyst Low Analyst Median Analyst High

Source: S&P Capital IQ, Yahoo! Finance

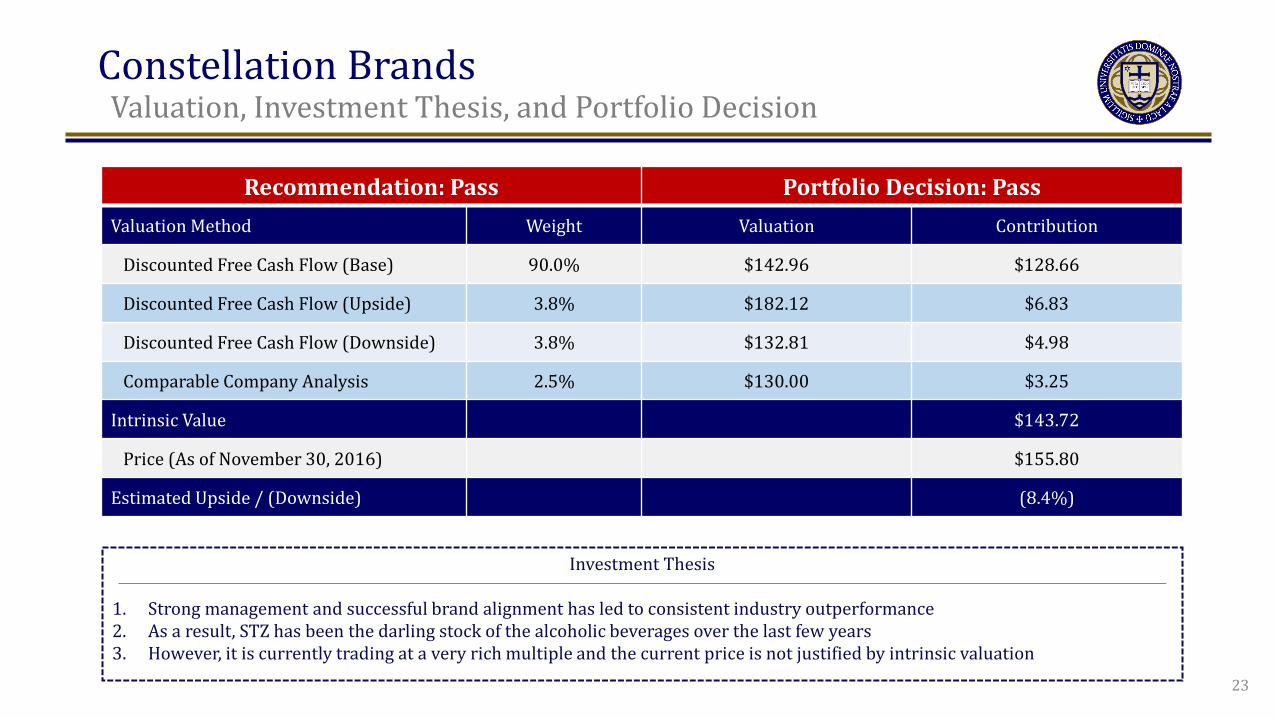

Constellation Brands t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Pass Portfolio Decision: Pass Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow (Base) 90.0% $142.96 $128.66

Discounted Free Cash Flow (Upside) 3.8% $182.12 $6.83

Discounted Free Cash Flow (Downside) 3.8% $132.81 $4.98

Comparable Company Analysis 2.5% $130.00 $3.25

Intrinsic Value $143.72

Price (As of November 30, 2016) $155.80

Estimated Upside / (Downside) (8.4%)

Investment Thesis

1. Strong management and successful brand alignment has led to consistent industry outperformance 2. As a result, STZ has been the darling stock of the alcoholic beverages over the last few years 3. However, it is currently trading at a very rich multiple and the current price is not justified by intrinsic valuation

23

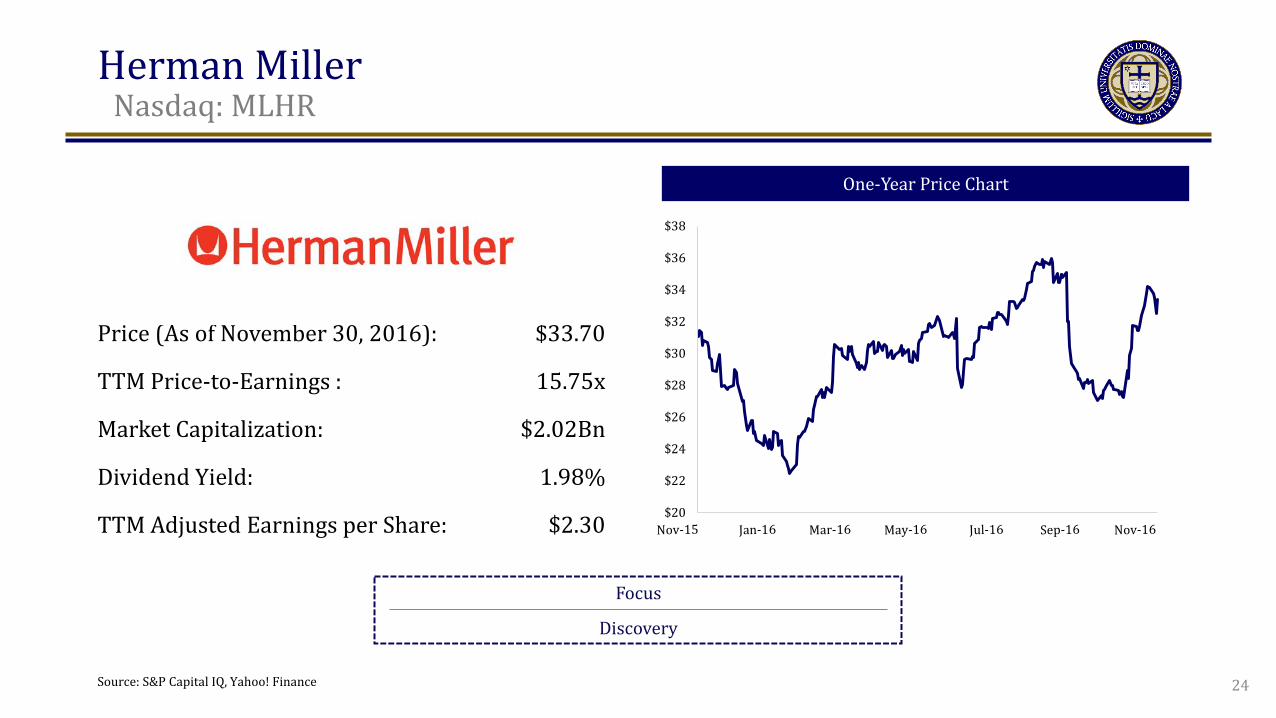

Herman Millert

Nasdaq: MLHR

One-Year Price Chart

Focus

Discovery

Price (As of November 30, 2016): $33.70

TTM Price-to-Earnings : 15.75x

Market Capitalization: $2.02Bn

Dividend Yield: 1.98%

TTM Adjusted Earnings per Share: $2.30

Source: S&P Capital IQ, Yahoo! Finance

$20

$22

$24

$26

$28

$30

$32

$34

$36

$38

24

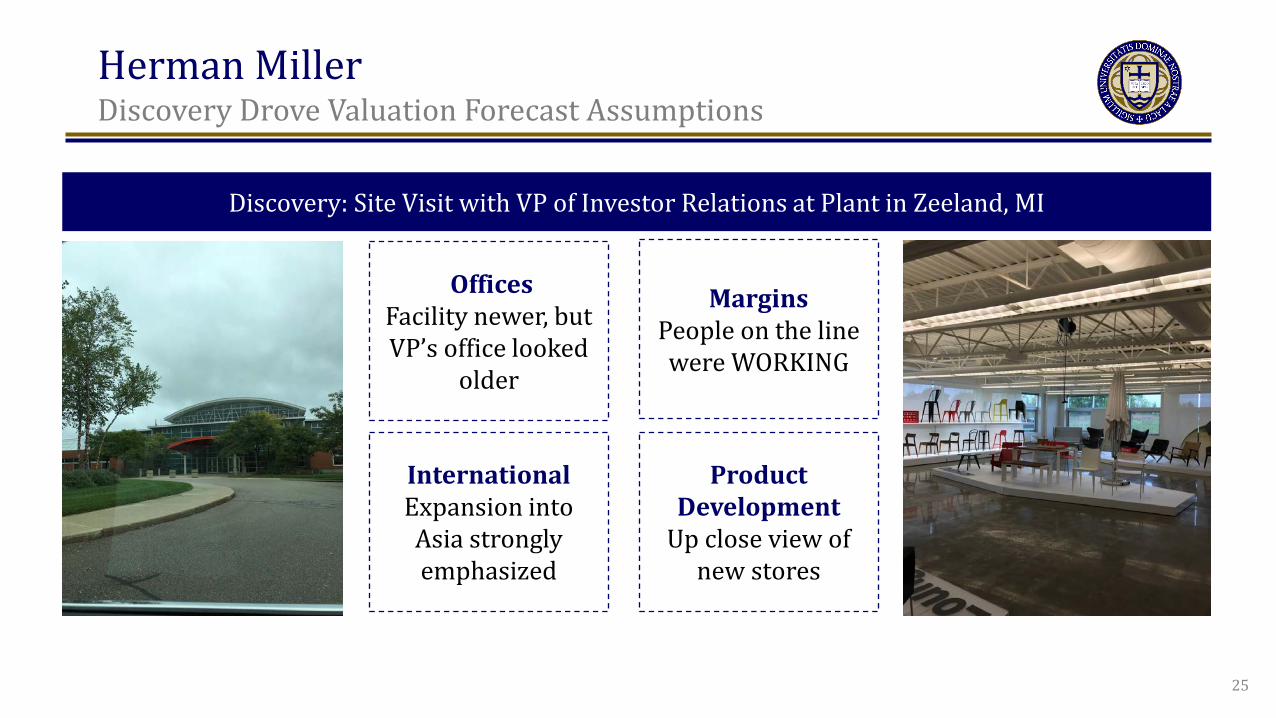

Herman Miller Discovery Drove Valuation Forecast Assumptions

Discovery: Site Visit with VP of Investor Relations at Plant in Zeeland, MI

Offices Facility newer, but VP’s office looked

older

Margins People on the line were WORKING

International Expansion into Asia strongly emphasized

Product Development

Up close view of new stores

25

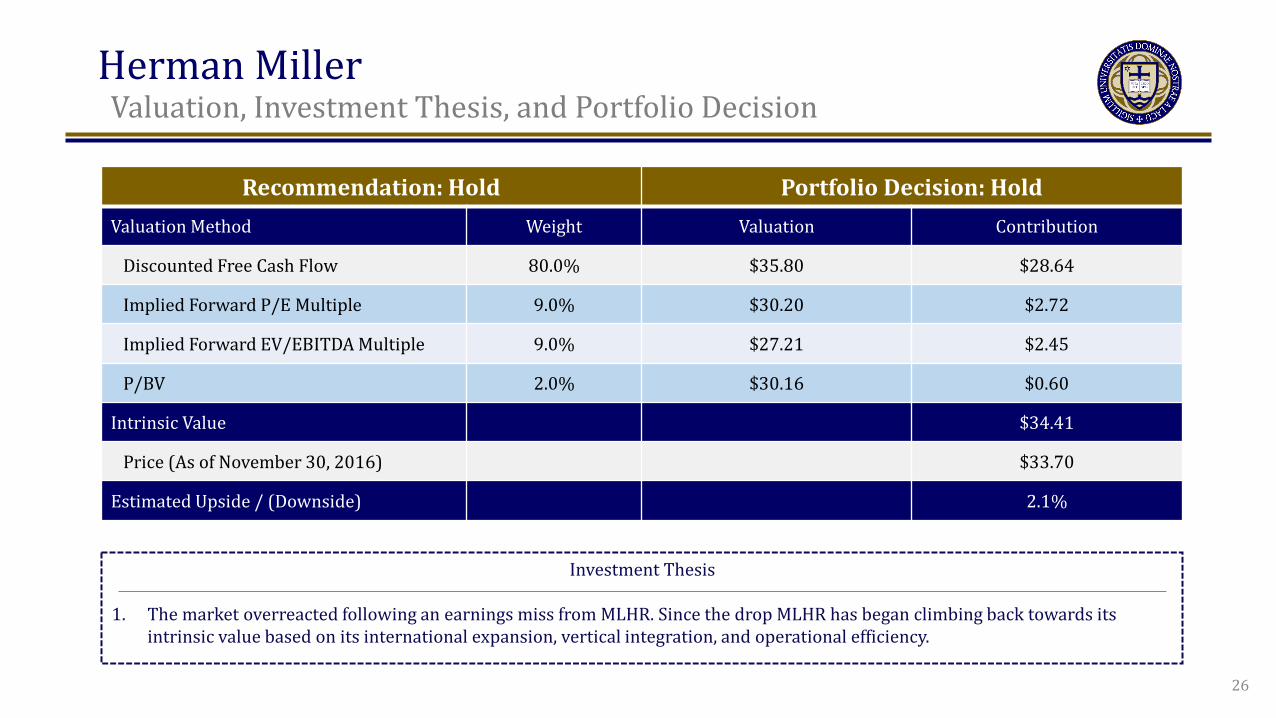

Herman Miller t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Hold Portfolio Decision: Hold Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 80.0% $35.80 $28.64

Implied Forward P/E Multiple 9.0% $30.20 $2.72

Implied Forward EV/EBITDA Multiple 9.0% $27.21 $2.45

P/BV 2.0% $30.16 $0.60

Intrinsic Value $34.41

Price (As of November 30, 2016) $33.70

Estimated Upside / (Downside) 2.1%

Investment Thesis

1. The market overreacted following an earnings miss from MLHR. Since the drop MLHR has began climbing back towards its intrinsic value based on its international expansion, vertical integration, and operational efficiency.

26

LendingClub Corporation t

NYSE: LC

One-Year Price Chart

Focus

Company and Industry Overview

Price (As of November 30, 2016): $5.62

TTM Price-to-Earnings: N/A

Market Capitalization: $2.22Bn

Short Interest: 17.03%

TTM Adjusted Earnings per Share: ($0.28) $0

$2

$4

$6

$8

$10

$12

$14

$16

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16

27 Source: S&P Capital IQ, Yahoo! Finance

LendingClub Corporation t

Overview

Historical Revenue ($MM) Company Background

Business Model

• Online market maker for unsecured credit 1. Consumers/small businesses apply for loans online 2. Algorithm assesses credit, approves loans, sets interest

rates 3. LendingClub issues loans and securitizes them 4. Investors and banks purchase notes as investments 5. LendingClub takes a percentage of loans originated and of

interest/principal serviced Primary Loan Purposes

• Personal Loans • Credit Card Refinancing • Small Business Loans • Auto Loan Refinancing

$34 $98

$211

$430

$506

$0

$150

$300

$450

$600

2012 2013 2014 2015 LTM

Source: Company Filings

Historical Margins

-20.3%

7.5%

-15.6%

-1.2% -14.1%

-60.5% -48.5%

-13.2%

5.4% -8.7%

-80.0%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

2012 2013 2014 2015 LTM

Net Profit Margin After-tax Operating Margin28

LendingClub Corporation t

Industry Trends in Peer-to-Peer Lending

U.S. Consumer Loan Originations ($Bn) Total Addressable Market: Credit Outstanding ($Bn)

$7,236 $7,376

$7,495 $7,573 $7,634 $7,734 $7,821 $7,907 $7,994

0%

1%

2%

3%

$6,800

$7,200

$7,600

$8,000

$8,400

2014 2015 2016E 2017E 2018E 2019E 2020E 2021E 2022E

Total Consumer Loans Originated Projected Market Penetration

Key Takeaways US Peer-to-Peer Lending Market Share (2015)

$0

$1,000

$2,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Revolving Consumer Credit

46%

12%

12%

11%

19%

LendingClub Prosper OnDeck SoFi Other

Attractive Form of Borrower Financing • Competitive interest rates versus credit cards

Appeal of Unsecured Credit • Economically difficult for banks to underwrite small loans

Partnerships versus Direct Competition • Many banks pursue exposure through trusted platforms

that pass due diligence • Other banks have chosen compete directly

29

Revolving $853

Non-revolving $1,621

[SERIES NAME] [VALUE]

$0 $500 $1,000 $1,500 $2,000 $2,500 $3,000

1

Source: Statista, FRED, Federal Reserve

LendingClub Corporation t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Buy Portfolio Decision: Pass Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 100.0% $6.69 $6.69

Implied Trailing P/S Multiple 0.0% $4.50 $0.00

Implied Forward EV/Revenue Multiple 0.0% $1.67 $0.00

Implied Forward P/E Multiple 0.0% N/A $0.00

Intrinsic Value $6.69

Price (As of November 30, 2016) $5.62

Estimated Upside / (Downside) 19.0%

Investment Thesis

1. Market over-reaction to resignation of Founder and CEO despite strong relationships with investor base 2. New management team tailored to developing relationships with financial institutions 3. Strong value proposition for borrowers; 80% use LendingClub for refinancing/debt consolidation of traditional loans

30

Infinera Corporation Nasdaq: INFN

One-Year Price Chart

Focus

Company and Industry Overview

Price (As of November 30, 2016):

TTM Price-to-Earnings:

Market Capitalization:

Dividend Yield:

TTM Adjusted Earnings per Share:

$8.54

26.1x

$1.2Bn

N/A

$0.19 $0

$5

$10

$15

$20

$25

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16

31 Source: Bloomberg

Infinera Corporation t

Company and Industry Overview

PIC-Enabled Technology

• PIC Enables Scalable, Intelligent Functions: SDN, integrated switching, sliceable bandwidth

• High Capacity Applications: Long-haul, Metro Cloud, Metro Core

New Purpose-Built Products

• Cloud Xpress for DC Interconnect • XT-Series for Long-haul • XTM-Series & XTC-2 for Metro • 3x TAM expansion to >$15B in 2020

Vertical Integration

• Lower cost structure than competition • Supply chain control • Additional functionality due to

integration synergies

Infinera has a competitive advantage due to its unique PIC technology, market expansion opportunities, and vertically integrated business model.

32

Competitive advantages have launched INFN to grow Long-Haul market share by 500+ basis points in the past five years.

Source: Investor Presentation

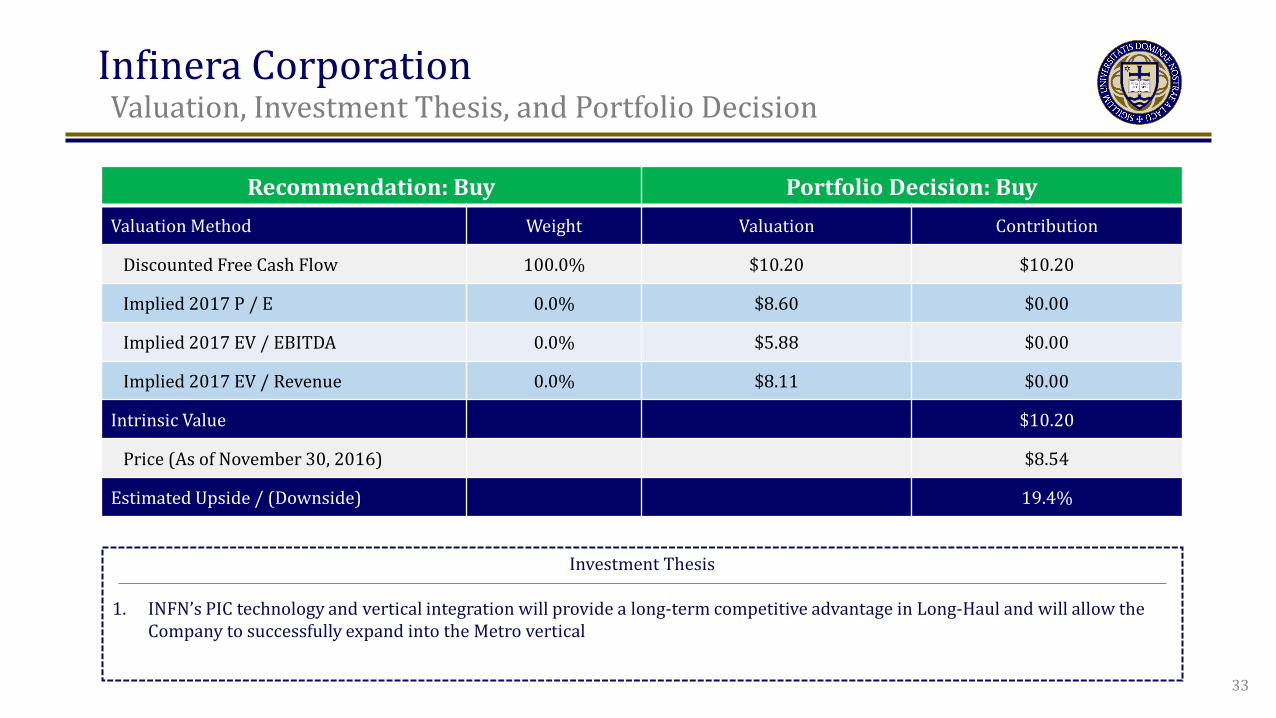

Infinera Corporation t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Buy Portfolio Decision: Buy Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 100.0% $10.20 $10.20

Implied 2017 P / E 0.0% $8.60 $0.00

Implied 2017 EV / EBITDA 0.0% $5.88 $0.00

Implied 2017 EV / Revenue 0.0% $8.11 $0.00

Intrinsic Value $10.20

Price (As of November 30, 2016) $8.54

Estimated Upside / (Downside) 19.4%

Investment Thesis

1. INFN’s PIC technology and vertical integration will provide a long-term competitive advantage in Long-Haul and will allow the Company to successfully expand into the Metro vertical

33

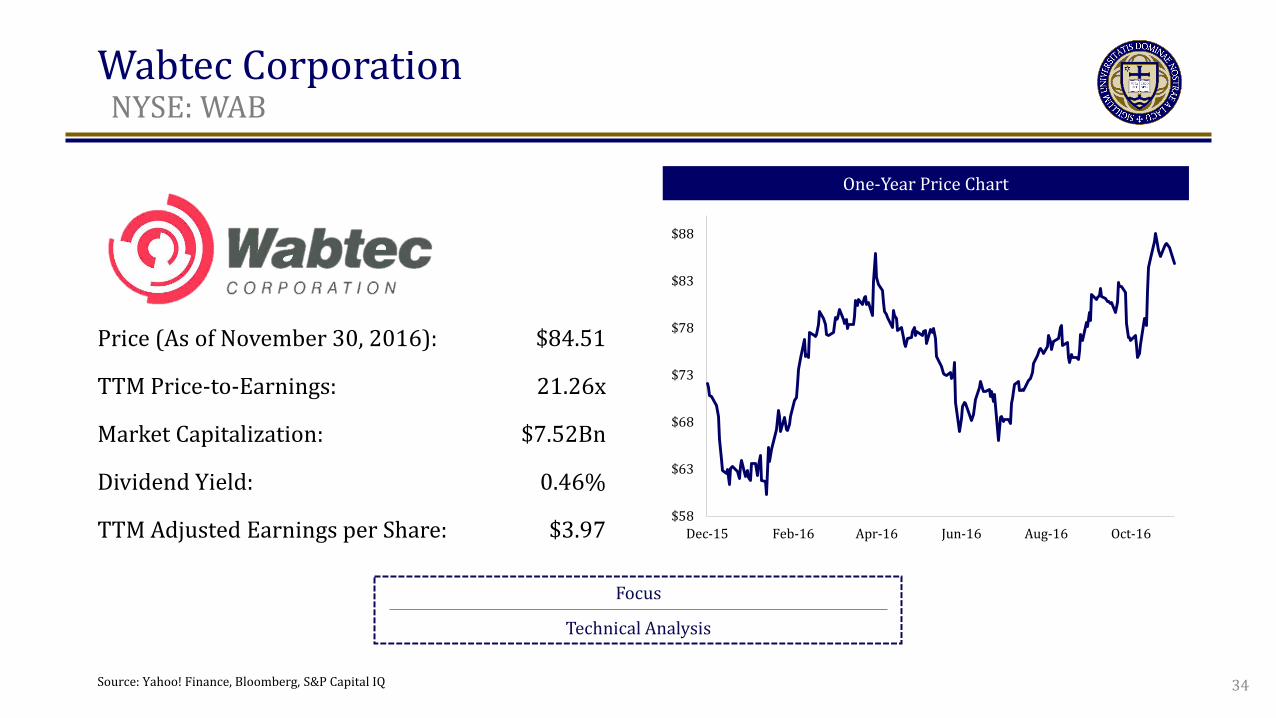

Wabtec Corporation t

NYSE: WAB

One-Year Price Chart

Focus

Technical Analysis

Price (As of November 30, 2016): $84.51

TTM Price-to-Earnings: 21.26x

Market Capitalization: $7.52Bn

Dividend Yield: 0.46%

TTM Adjusted Earnings per Share: $3.97 $58

$63

$68

$73

$78

$83

$88

Dec-15 Feb-16 Apr-16 Jun-16 Aug-16 Oct-16

Source: Yahoo! Finance, Bloomberg, S&P Capital IQ 34

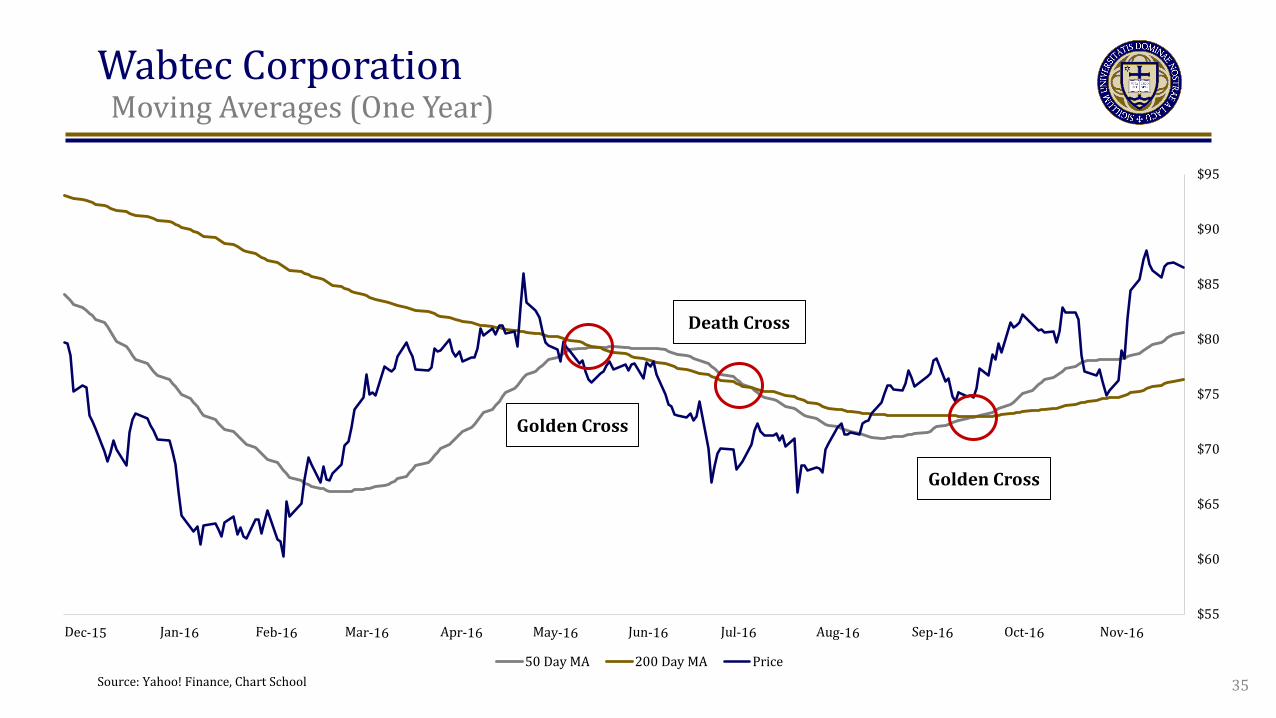

Wabtec Corporation t

Moving Averages (One Year)

$55

$60

$65

$70

$75

$80

$85

$90

$95

50 Day MA 200 Day MA Price

Golden Cross

Death Cross

Golden Cross

Source: Yahoo! Finance, Chart School 35

Wabtec Corporation t

Bollinger Bands

$58

$63

$68

$73

$78

$83

$88

Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jul-16 Aug-16 Sep-16 Oct-16 Nov-16

WAB Price Upper Bound Lower Bound

Source: Yahoo! Finance, Chart School 36

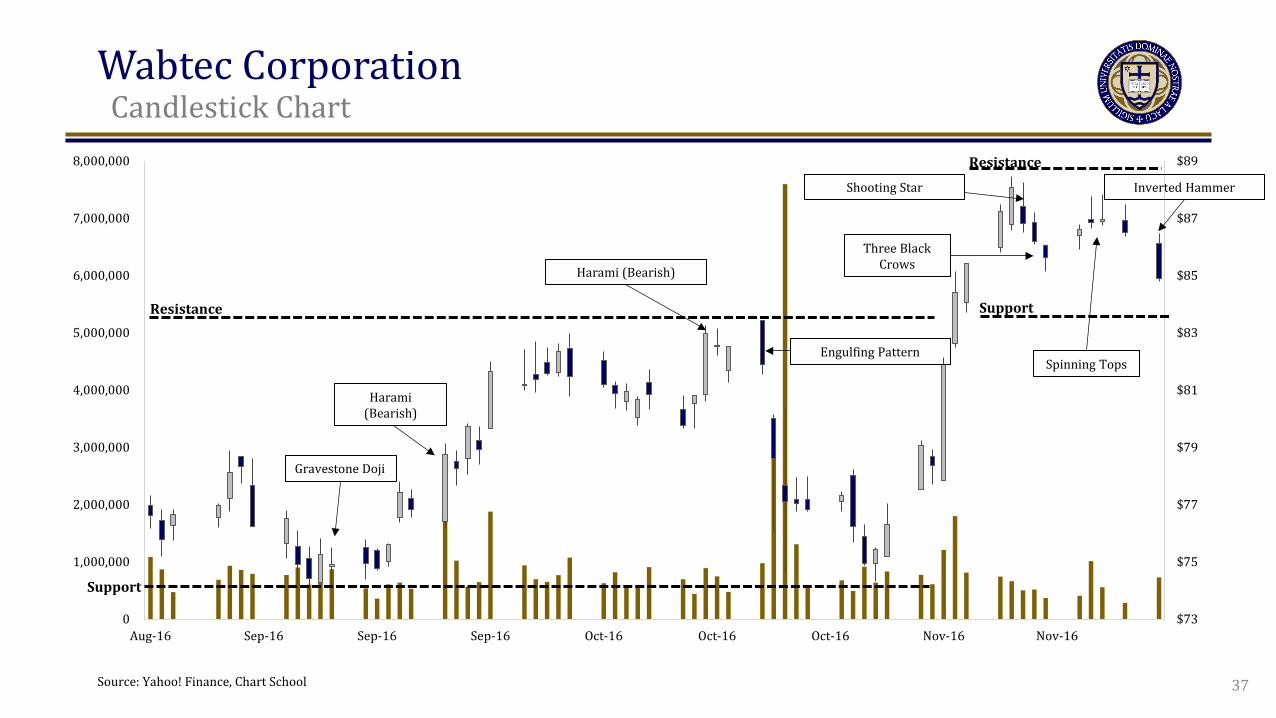

Wabtec Corporation t

Candlestick Chart

$73

$75

$77

$79

$81

$83

$85

$87

$89

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

Aug-16 Sep-16 Sep-16 Sep-16 Oct-16 Oct-16 Oct-16 Nov-16 Nov-16

Resistance

Support

Support

Resistance

Spinning Tops

Inverted Hammer

Gravestone Doji

Harami (Bearish)

Three Black Crows

Shooting Star

Harami (Bearish)

Engulfing Pattern

37 Source: Yahoo! Finance, Chart School

Wabtec Corporation t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Hold Portfolio Decision: Hold Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 85.0% $88.98 $75.63

Price / Earnings 5.0% $90.11 $4.51

Enterprise / EBITDA 5.0% $87.99 $4.40

Enterprise / Revenue 5.0% $71.74 $3.59

Intrinsic Value $88.13

Price (As of November 30, 2016) $84.51

Estimated Upside / (Downside) 4.3%

Investment Thesis

1. Dominance across the domestic market and leadership within almost all product classes in original and aftermarket sales promise a steady revenue stream with decreasing service costs

2. Heavy investment in emerging Rail and Transit technologies will sustain above average growth in the US 3. Expansion into Europe with the Faiveley Transport Group acquisition opens the door to Europe and Near East Transit growth 38

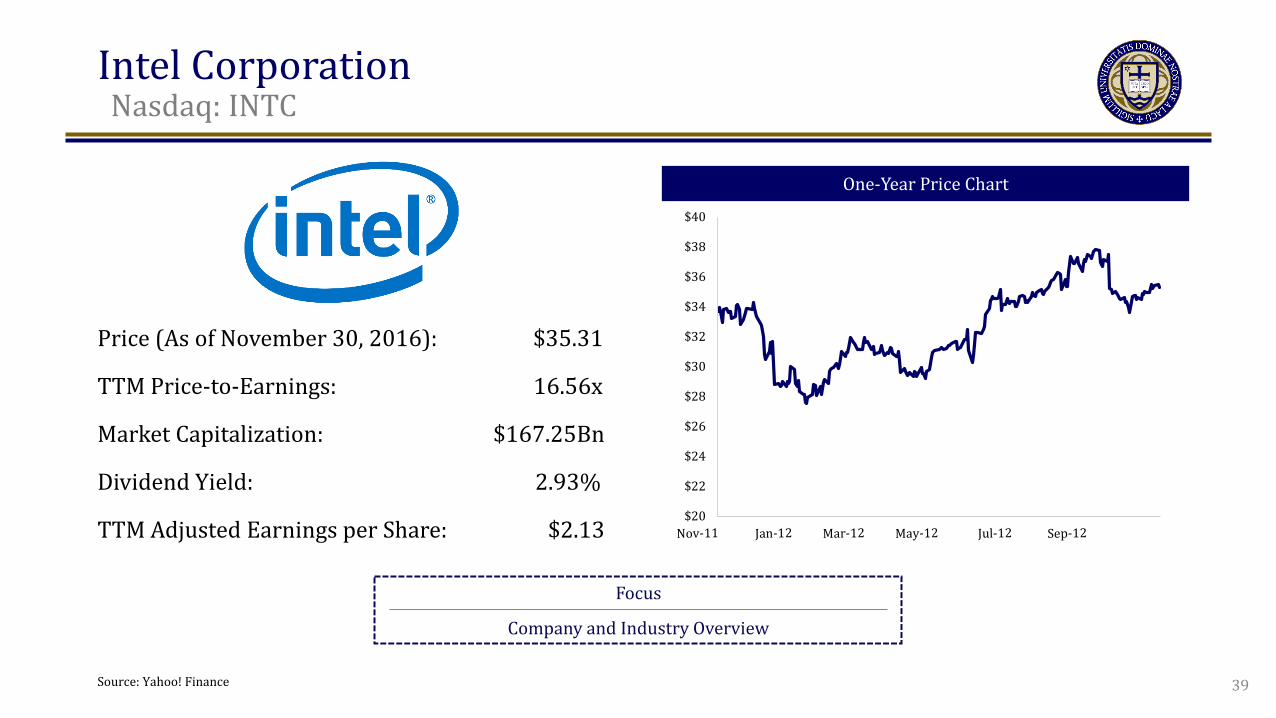

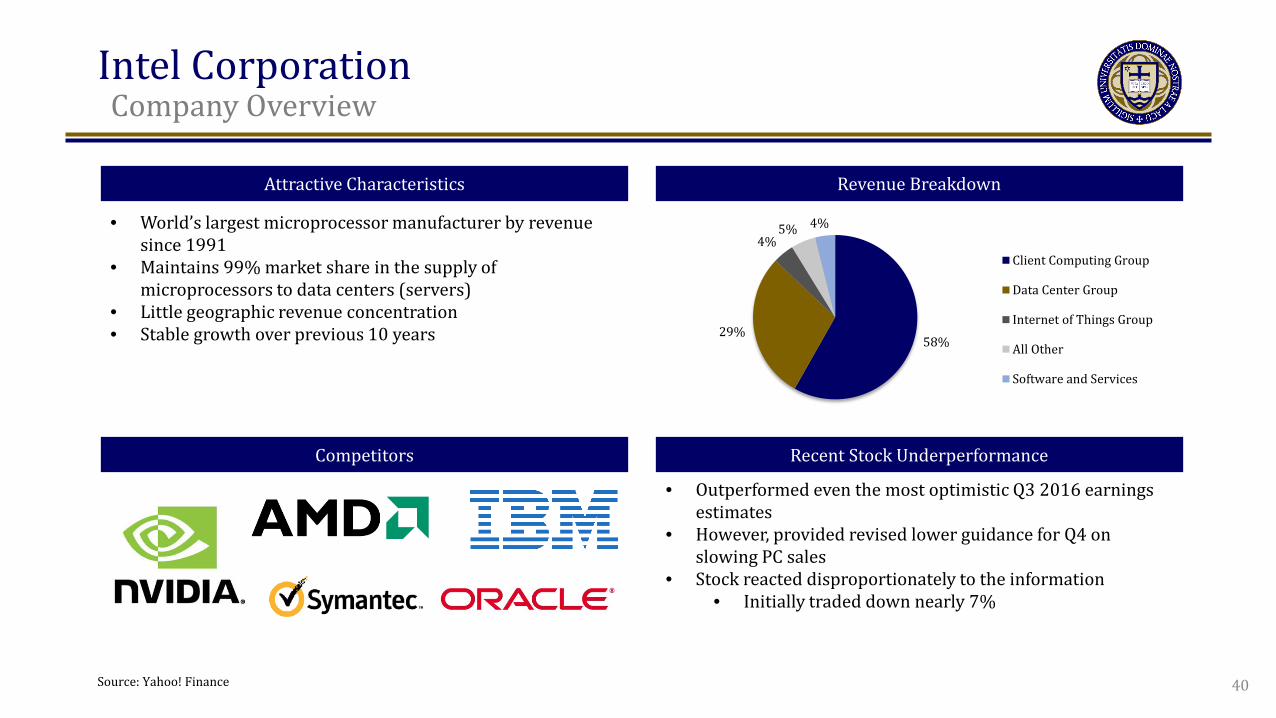

Intel Corporation Nasdaq: INTC

One-Year Price Chart

Focus

Company and Industry Overview

Price (As of November 30, 2016): $35.31

TTM Price-to-Earnings: 16.56x

Market Capitalization: $167.25Bn

Dividend Yield: 2.93%

TTM Adjusted Earnings per Share: $2.13 $20

$22

$24

$26

$28

$30

$32

$34

$36

$38

$40

39 Source: Yahoo! Finance

Intel Corporation Company Overview

Revenue Breakdown Attractive Characteristics

Recent Stock Underperformance Competitors

58% 29%

4% 5% 4%

Client Computing Group

Data Center Group

Internet of Things Group

All Other

Software and Services

• World’s largest microprocessor manufacturer by revenue since 1991

• Maintains 99% market share in the supply of microprocessors to data centers (servers)

• Little geographic revenue concentration • Stable growth over previous 10 years

40

• Outperformed even the most optimistic Q3 2016 earnings estimates

• However, provided revised lower guidance for Q4 on slowing PC sales

• Stock reacted disproportionately to the information • Initially traded down nearly 7%

Source: Yahoo! Finance

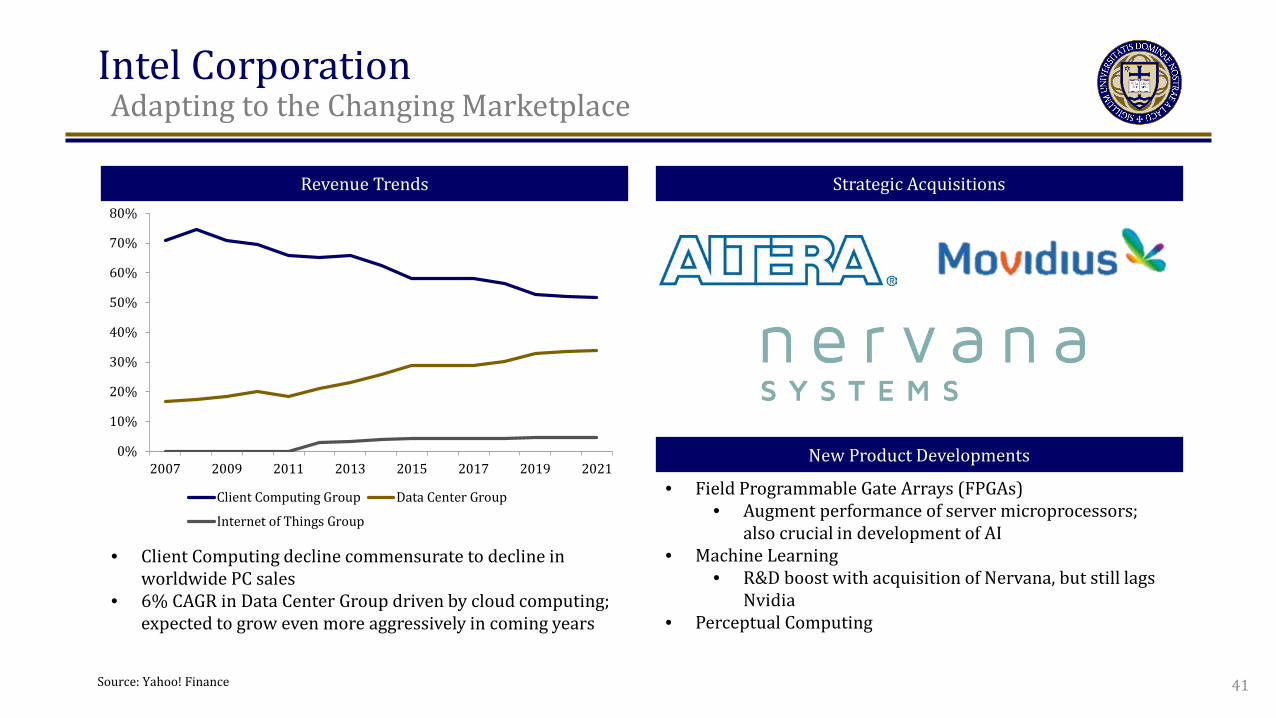

Intel Corporation Adapting to the Changing Marketplace

Strategic Acquisitions Revenue Trends

New Product Developments 0%

10%

20%

30%

40%

50%

60%

70%

80%

2007 2009 2011 2013 2015 2017 2019 2021

Client Computing Group Data Center Group

Internet of Things Group

• Field Programmable Gate Arrays (FPGAs) • Augment performance of server microprocessors;

also crucial in development of AI • Machine Learning

• R&D boost with acquisition of Nervana, but still lags Nvidia

• Perceptual Computing

• Client Computing decline commensurate to decline in worldwide PC sales

• 6% CAGR in Data Center Group driven by cloud computing; expected to grow even more aggressively in coming years

41 Source: Yahoo! Finance

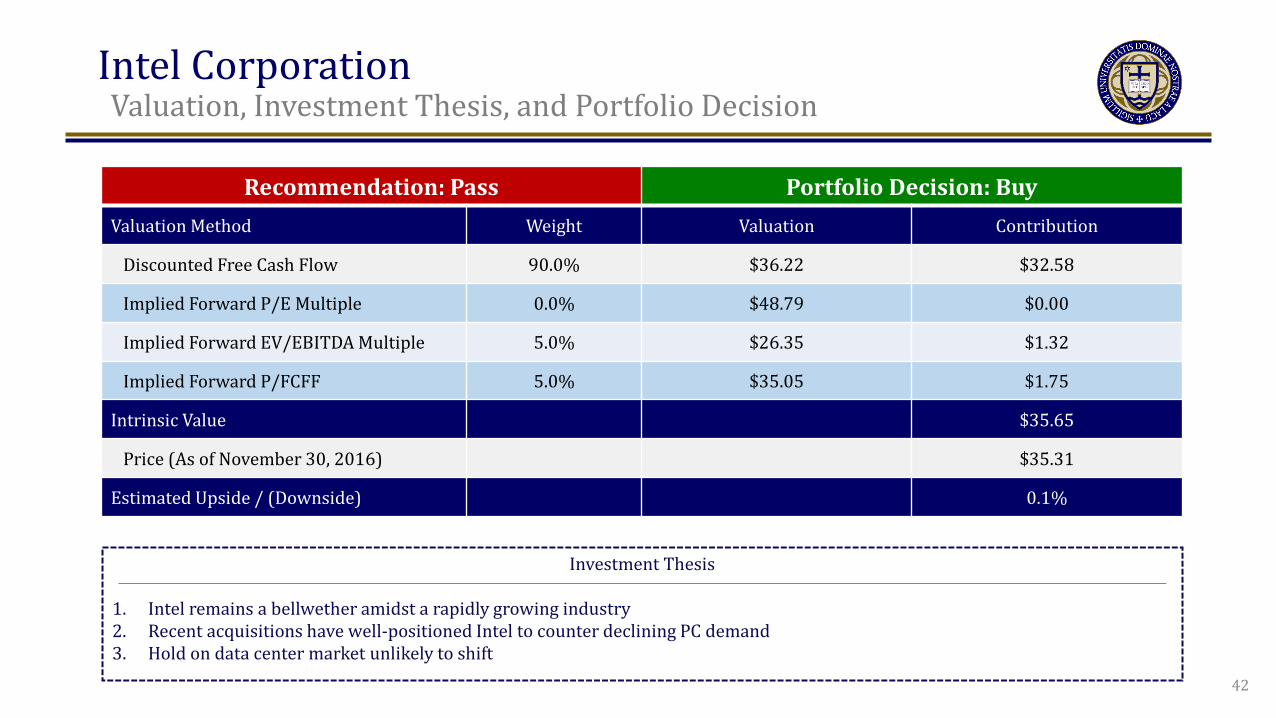

Intel Corporation Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Pass Portfolio Decision: Buy Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 90.0% $36.22 $32.58

Implied Forward P/E Multiple 0.0% $48.79 $0.00

Implied Forward EV/EBITDA Multiple 5.0% $26.35 $1.32

Implied Forward P/FCFF 5.0% $35.05 $1.75

Intrinsic Value $35.65

Price (As of November 30, 2016) $35.31

Estimated Upside / (Downside) 0.1%

Investment Thesis

1. Intel remains a bellwether amidst a rapidly growing industry 2. Recent acquisitions have well-positioned Intel to counter declining PC demand 3. Hold on data center market unlikely to shift

42

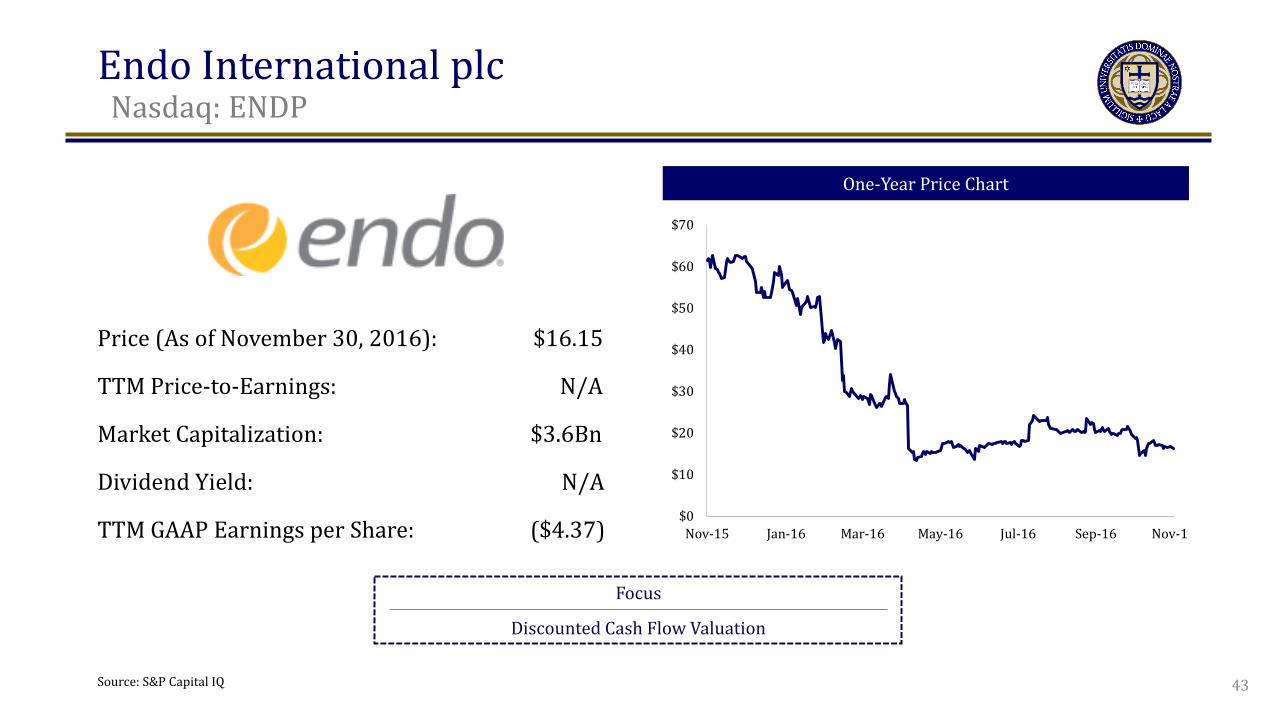

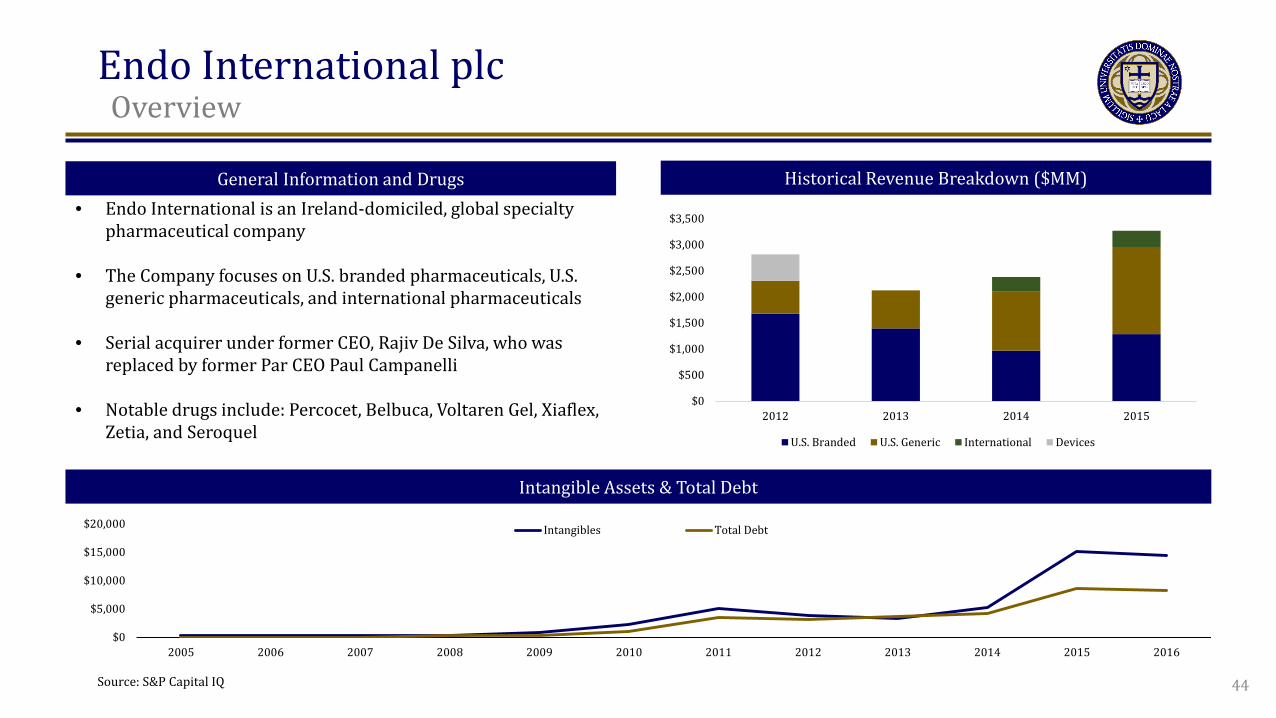

Endo International plc t

Nasdaq: ENDP

One-Year Price Chart

Focus

Discounted Cash Flow Valuation

Price (As of November 30, 2016): $16.15

TTM Price-to-Earnings: N/A

Market Capitalization: $3.6Bn

Dividend Yield: N/A

TTM GAAP Earnings per Share: ($4.37)

Source: S&P Capital IQ

$0

$10

$20

$30

$40

$50

$60

$70

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16

43

Endo International plc t

Overview

Intangible Assets & Total Debt

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

2012 2013 2014 2015

U.S. Branded U.S. Generic International Devices

Historical Revenue Breakdown ($MM) General Information and Drugs • Endo International is an Ireland-domiciled, global specialty

pharmaceutical company • The Company focuses on U.S. branded pharmaceuticals, U.S.

generic pharmaceuticals, and international pharmaceuticals • Serial acquirer under former CEO, Rajiv De Silva, who was

replaced by former Par CEO Paul Campanelli • Notable drugs include: Percocet, Belbuca, Voltaren Gel, Xiaflex,

Zetia, and Seroquel

$0

$5,000

$10,000

$15,000

$20,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Intangibles Total Debt

44 Source: S&P Capital IQ

Endo International plc t

Discounted Cash Flow

Key Assumptions Revenue Build ($MM)

Weighted Average Cost of Capital Sensitivity Analysis

• Most revenue assumptions are based on management guidance ‒ When not applicable, drug-specific industry averages

are used • Projected costs are predominantly taken as a percentage of

sales $0$1,000$2,000$3,000$4,000$5,000$6,000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

U.S. Branded U.S. Generic International Devices

Perpetuity Growth 15.72 0.50% 0.75% 1.00% 1.25% 1.50%

5% $ 31.88 $ 34.62 $ 37.69 $ 41.14 $ 45.05 6% $ 20.92 $ 22.69 $ 24.63 $ 26.76 $ 29.11

WACC 7% $ 13.19 $ 14.41 $ 15.72 $ 17.14 $ 18.69 8% $ 7.44 $ 8.32 $ 9.25 $ 10.26 $ 11.33 9% $ 3.00 $ 3.65 $ 4.34 $ 5.08 $ 5.86

Perpetuity Growth 11.04 0.50% 0.75% 1.00% 1.25% 1.50%

5% 97% 114% 133% 155% 179% 6% 30% 40% 52% 66% 80%

WACC 7% -18% -11% -3% 6% 16% 8% -54% -48% -43% -36% -30% 9% -81% -77% -73% -69% -64%

Assumptions Market Risk Premium (Rm - Rf) 5.0% Multiplied by: ENDP Beta 1.30 Adjusted Market Risk Premium 6.5% Add: Risk-Free Rate of Return (Rf) 2.0% Cost of Equity 8.5% Multiply by: ENDP E/(D+E) 40.9% Cost of Equity Portion 3.5% Cost of Debt 8.0% Tax Rate 20% After Tax Cost of Debt 6% Multiply by: ENDP E/(D+E) 59.1% Cost of Debt Portion 3.8% WACC 7.3% 45

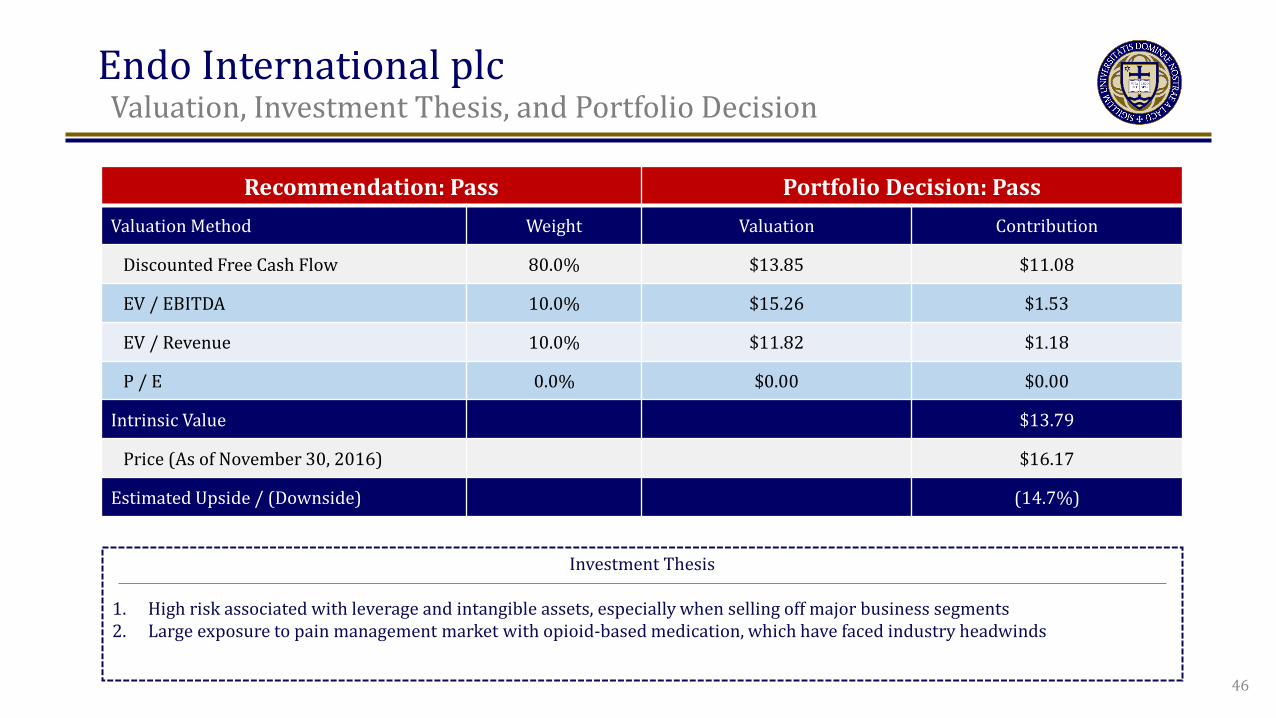

Endo International plc t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Pass Portfolio Decision: Pass Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 80.0% $13.85 $11.08

EV / EBITDA 10.0% $15.26 $1.53

EV / Revenue 10.0% $11.82 $1.18

P / E 0.0% $0.00 $0.00

Intrinsic Value $13.79

Price (As of November 30, 2016) $16.17

Estimated Upside / (Downside) (14.7%)

Investment Thesis

1. High risk associated with leverage and intangible assets, especially when selling off major business segments 2. Large exposure to pain management market with opioid-based medication, which have faced industry headwinds

46

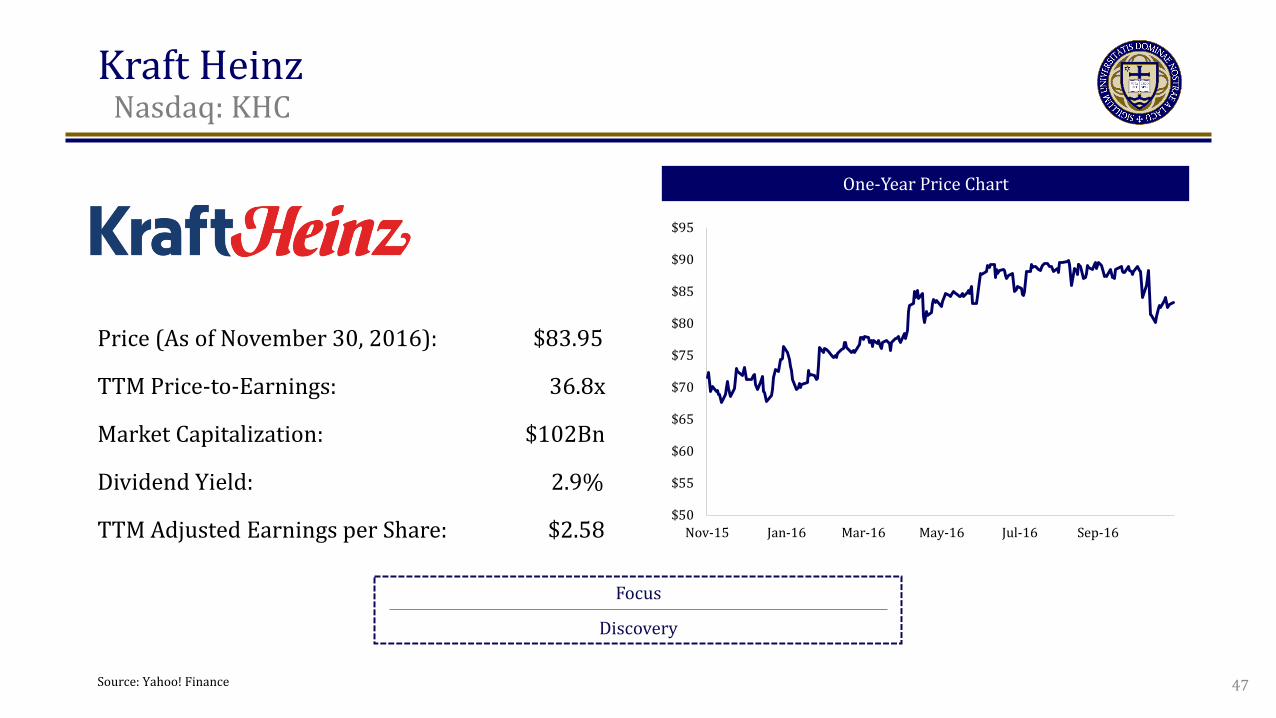

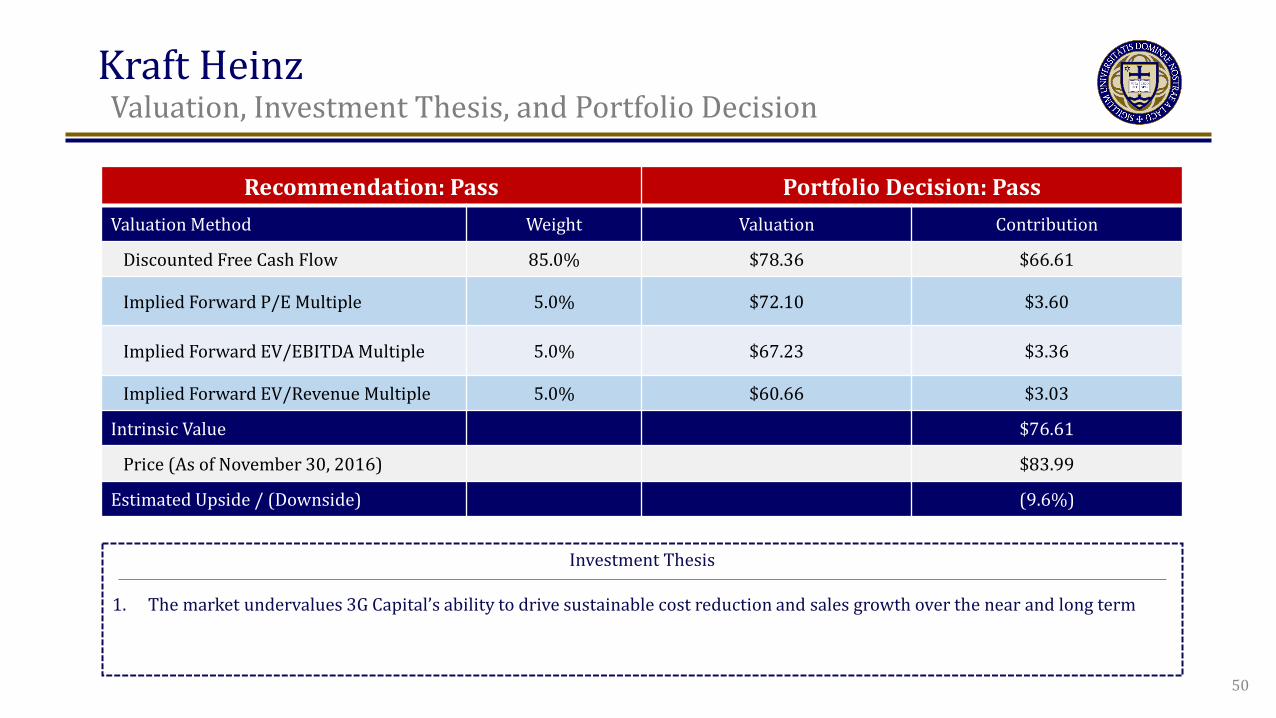

Kraft Heinz t

Nasdaq: KHC

One-Year Price Chart

Focus

Discovery

Price (As of November 30, 2016): $83.95

TTM Price-to-Earnings: 36.8x

Market Capitalization: $102Bn

Dividend Yield: 2.9%

TTM Adjusted Earnings per Share: $2.58

Source: Yahoo! Finance

$50

$55

$60

$65

$70

$75

$80

$85

$90

$95

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16

47

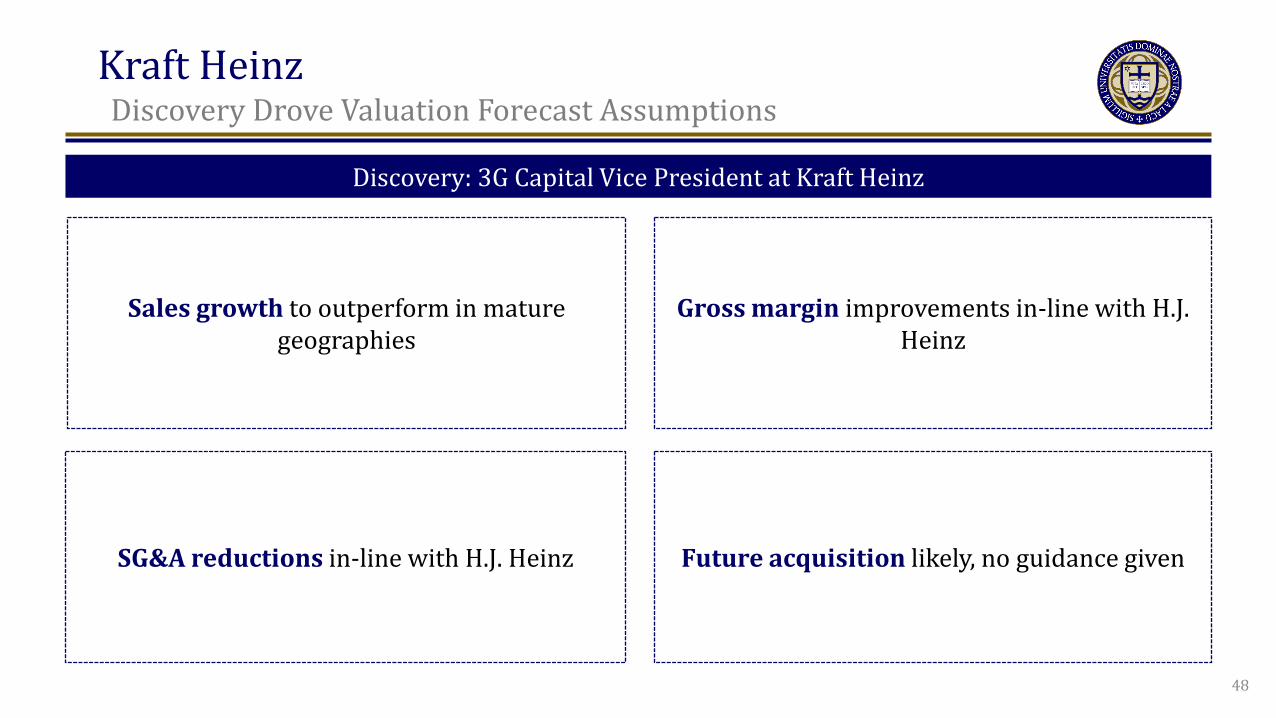

Kraft Heinz Discovery Drove Valuation Forecast Assumptions

Sales growth to outperform in mature geographies

Gross margin improvements in-line with H.J. Heinz

SG&A reductions in-line with H.J. Heinz Future acquisition likely, no guidance given

Discovery: 3G Capital Vice President at Kraft Heinz

48

Kraft Heinz t

COGS and SG&A Forecasts Based on Discovery

4%

7%

10%

13%

16%

SG&A % of Revenue - Historical

SG&A % of Revenue - Base Case

SG&A % of Revenue - Downside Case

SG&A % of Revenue - Upside Case

50%

55%

60%

65%

70%

75%COGS % of Sales (Historical)

COGS % of Sales Forecast - Base Case

COGS % of Sales Forecast - Downside Case

COGS % of Sales Forecast - Upside Case

COGS % of Revenue

49

SG&A % of Revenue

Kraft Heinz t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Pass Portfolio Decision: Pass Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 85.0% $78.36 $66.61

Implied Forward P/E Multiple 5.0% $72.10 $3.60

Implied Forward EV/EBITDA Multiple 5.0% $67.23 $3.36

Implied Forward EV/Revenue Multiple 5.0% $60.66 $3.03

Intrinsic Value $76.61

Price (As of November 30, 2016) $83.99

Estimated Upside / (Downside) (9.6%)

Investment Thesis

1. The market undervalues 3G Capital’s ability to drive sustainable cost reduction and sales growth over the near and long term

50

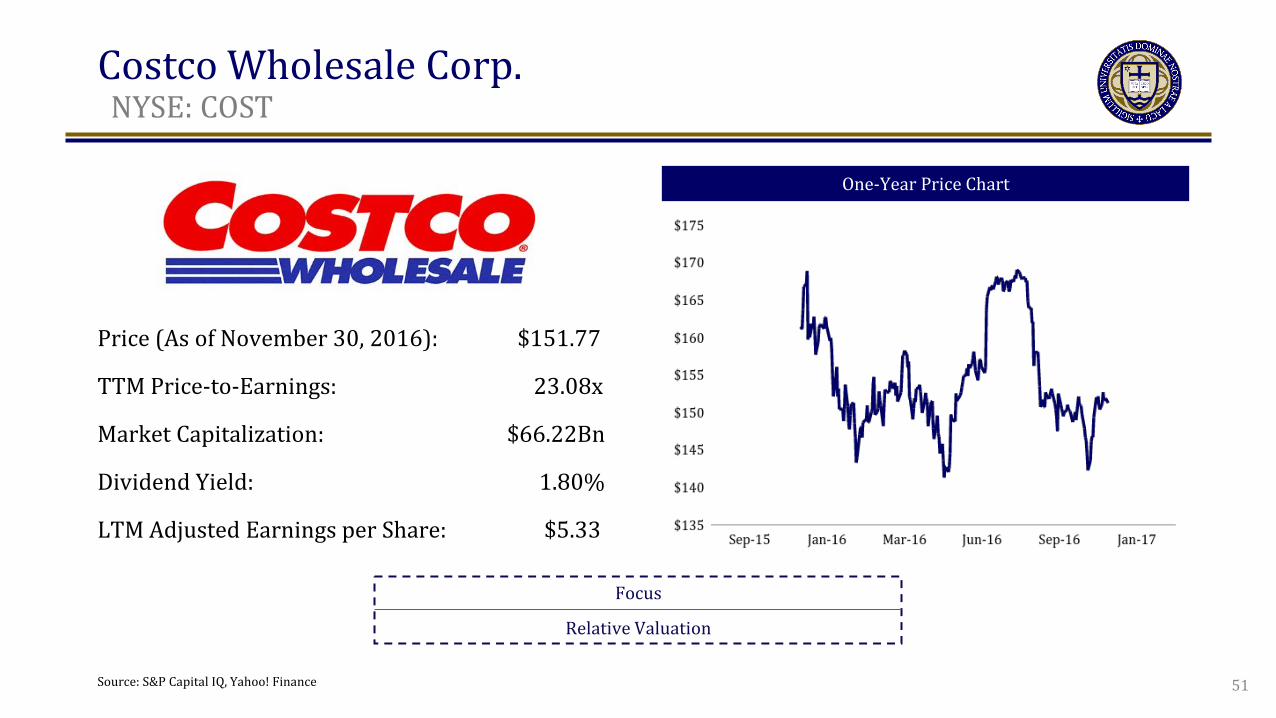

Costco Wholesale Corp. t

NYSE: COST

One-Year Price Chart

Focus

Relative Valuation

Price (As of November 30, 2016): $151.77

TTM Price-to-Earnings: 23.08x

Market Capitalization: $66.22Bn

Dividend Yield: 1.80%

LTM Adjusted Earnings per Share: $5.33

Source: S&P Capital IQ, Yahoo! Finance 51

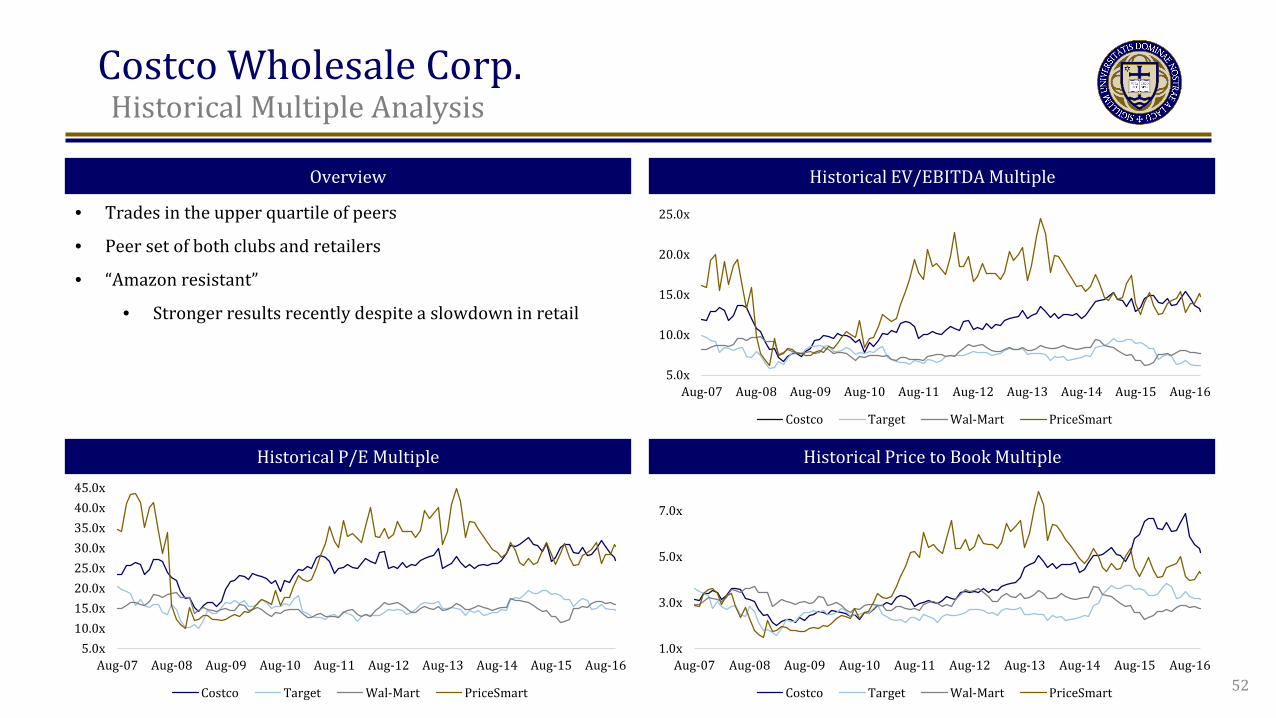

Costco Wholesale Corp. t

Historical Multiple Analysis

Overview

Historical P/E Multiple Historical Price to Book Multiple

Historical EV/EBITDA Multiple

• Trades in the upper quartile of peers

• Peer set of both clubs and retailers

• “Amazon resistant”

• Stronger results recently despite a slowdown in retail

52

5.0x10.0x15.0x20.0x25.0x30.0x35.0x40.0x45.0x

Aug-07 Aug-08 Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

Costco Target Wal-Mart PriceSmart

1.0x

3.0x

5.0x

7.0x

Aug-07 Aug-08 Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

Costco Target Wal-Mart PriceSmart

5.0x

10.0x

15.0x

20.0x

25.0x

Aug-07 Aug-08 Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16

Costco Target Wal-Mart PriceSmart

Costco Wholesale Corp. t

Relative Valuation Calculation

Forward P/E Multiple Forward Price to Book Multiple Forward EV/EBITDA Multiple

53

13.0x

16.1x

24.0x

27.4x

0.0x

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

Target Wal-Mart Costco PriceSmart

Implied Multiple: 25.3x

6.9x

7.9x

11.7x

13.4x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

Target Wal-Mart Costco PriceSmart

Implied Multiple: 11.1x

3.2x

4.3x

5.1x

5.9x

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

7.0x

PriceSmart Wal-Mart Target Costco

Implied Multiple: 5.1x

Costco Wholesale Corp. t

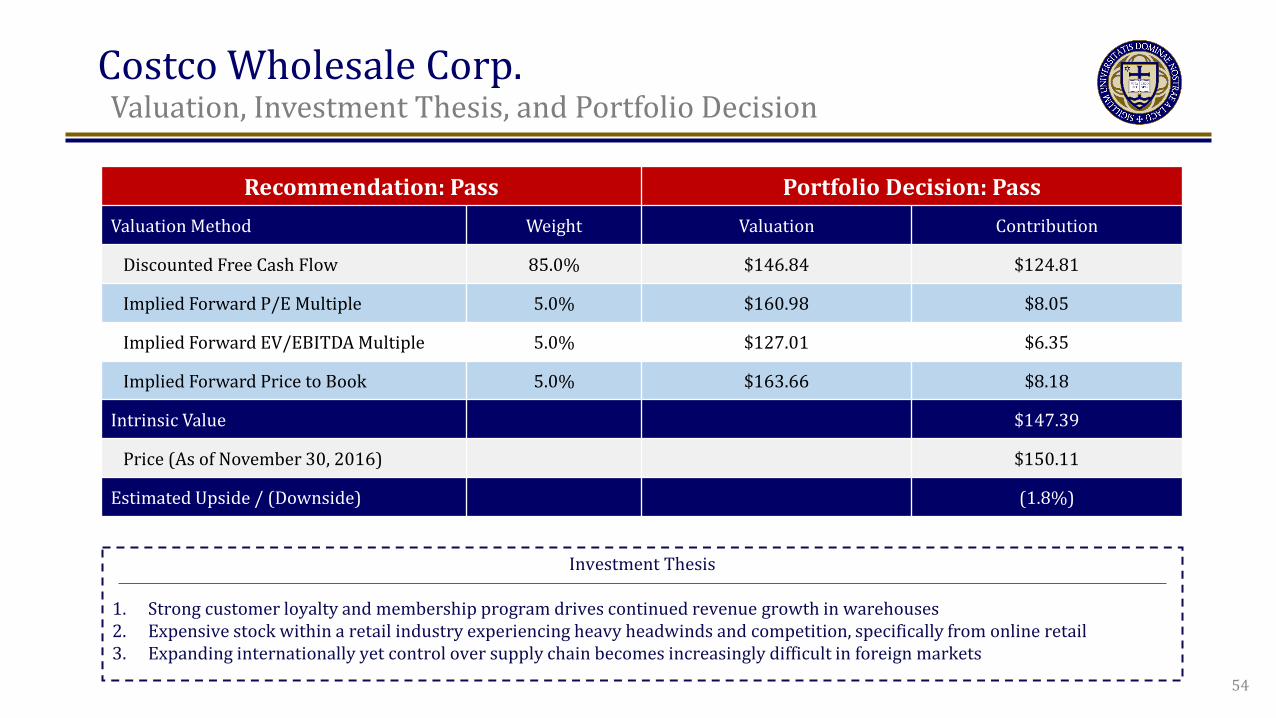

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Pass Portfolio Decision: Pass Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 85.0% $146.84 $124.81

Implied Forward P/E Multiple 5.0% $160.98 $8.05

Implied Forward EV/EBITDA Multiple 5.0% $127.01 $6.35

Implied Forward Price to Book 5.0% $163.66 $8.18

Intrinsic Value $147.39

Price (As of November 30, 2016) $150.11

Estimated Upside / (Downside) (1.8%)

Investment Thesis

1. Strong customer loyalty and membership program drives continued revenue growth in warehouses 2. Expensive stock within a retail industry experiencing heavy headwinds and competition, specifically from online retail 3. Expanding internationally yet control over supply chain becomes increasingly difficult in foreign markets

54

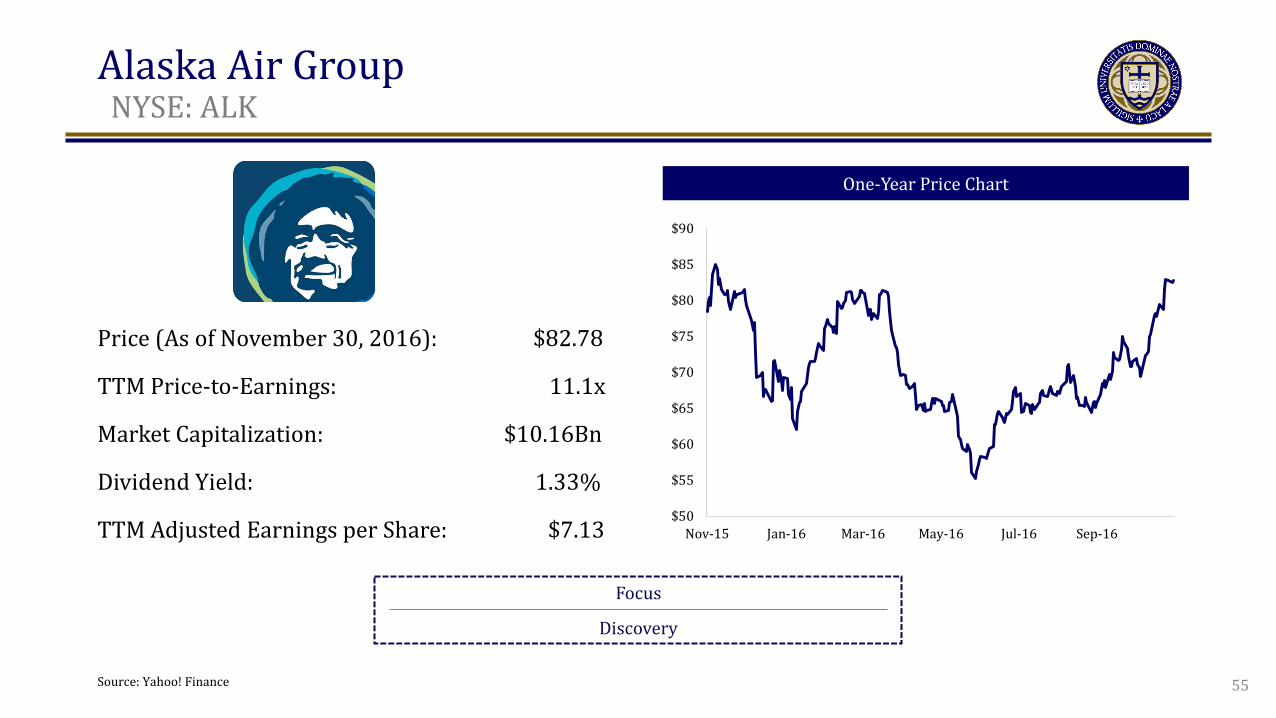

Alaska Air Group t

NYSE: ALK

One-Year Price Chart

Focus

Discovery

Price (As of November 30, 2016): $82.78

TTM Price-to-Earnings: 11.1x

Market Capitalization: $10.16Bn

Dividend Yield: 1.33%

TTM Adjusted Earnings per Share: $7.13

Source: Yahoo! Finance

$50

$55

$60

$65

$70

$75

$80

$85

$90

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16

55

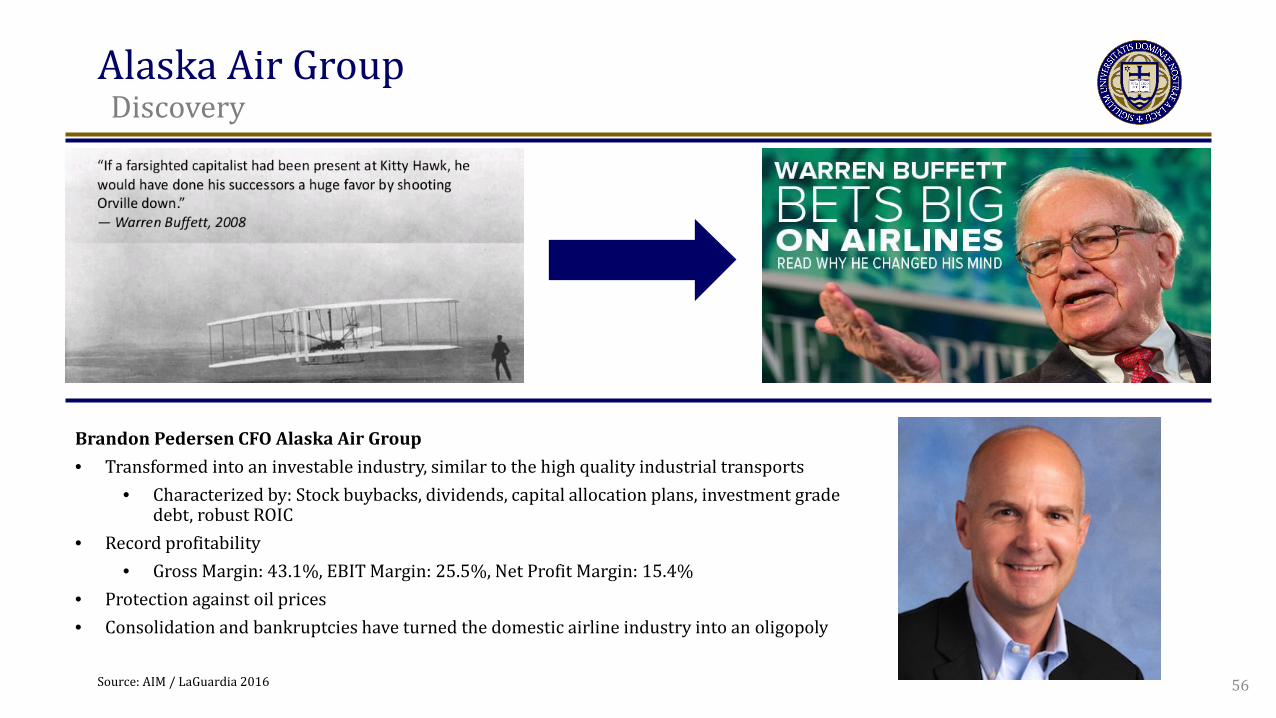

Alaska Air Group t

Discovery

Source: AIM / LaGuardia 2016

Brandon Pedersen CFO Alaska Air Group • Transformed into an investable industry, similar to the high quality industrial transports

• Characterized by: Stock buybacks, dividends, capital allocation plans, investment grade debt, robust ROIC

• Record profitability • Gross Margin: 43.1%, EBIT Margin: 25.5%, Net Profit Margin: 15.4%

• Protection against oil prices • Consolidation and bankruptcies have turned the domestic airline industry into an oligopoly

56

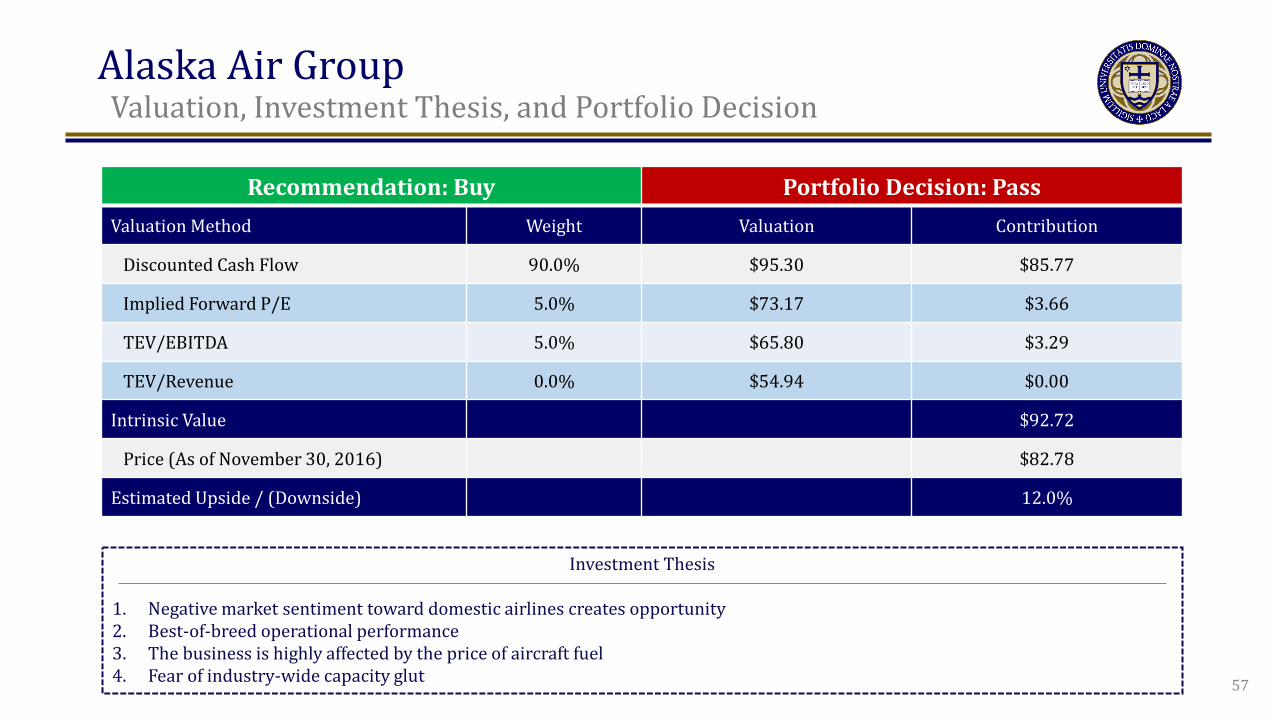

Alaska Air Group t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Buy Portfolio Decision: Pass Valuation Method Weight Valuation Contribution

Discounted Cash Flow 90.0% $95.30 $85.77

Implied Forward P/E 5.0% $73.17 $3.66

TEV/EBITDA 5.0% $65.80 $3.29

TEV/Revenue 0.0% $54.94 $0.00

Intrinsic Value $92.72

Price (As of November 30, 2016) $82.78

Estimated Upside / (Downside) 12.0%

Investment Thesis

1. Negative market sentiment toward domestic airlines creates opportunity 2. Best-of-breed operational performance 3. The business is highly affected by the price of aircraft fuel 4. Fear of industry-wide capacity glut 57

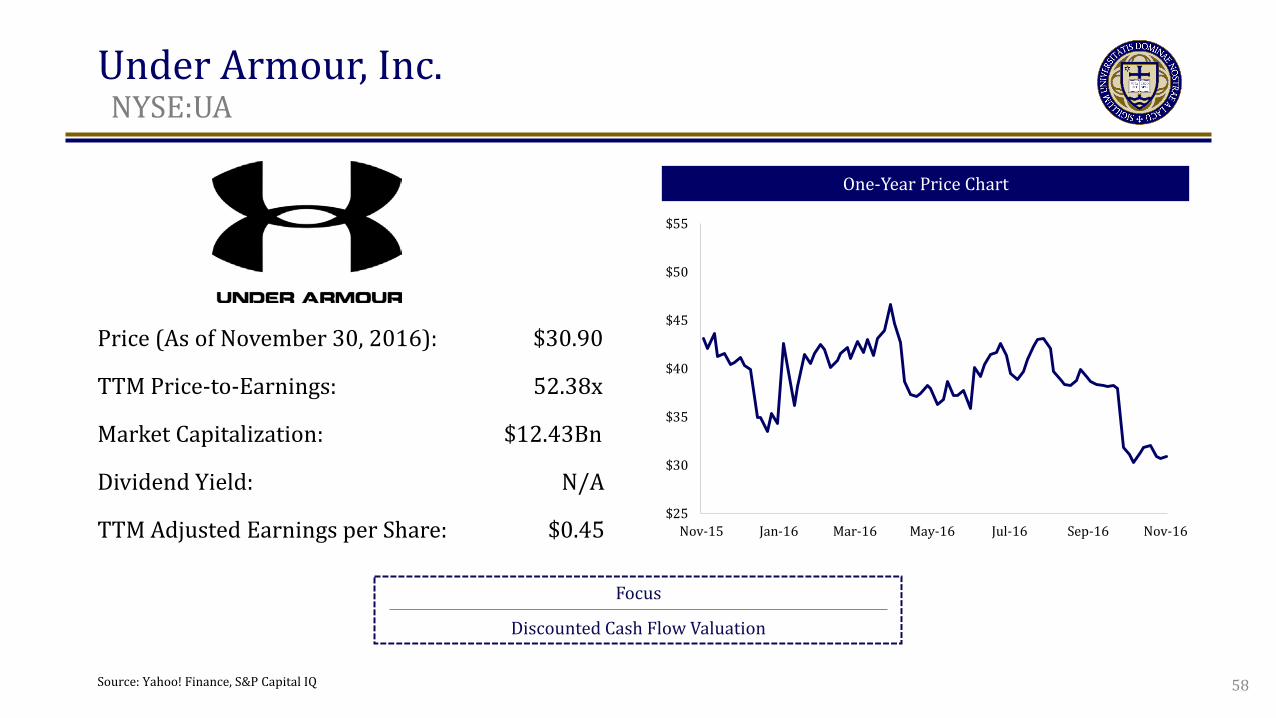

Under Armour, Inc. t

NYSE:UA

One-Year Price Chart

Focus

Discounted Cash Flow Valuation

Price (As of November 30, 2016): $30.90

TTM Price-to-Earnings: 52.38x

Market Capitalization: $12.43Bn

Dividend Yield: N/A

TTM Adjusted Earnings per Share: $0.45

Source: Yahoo! Finance, S&P Capital IQ

$25

$30

$35

$40

$45

$50

$55

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16

58

Under Armour, Inc. t

Discounted Cash Flow Valuation

Source: Bloomberg, S&P Capital IQ, Company Filings, AIM / Lanzel 2016

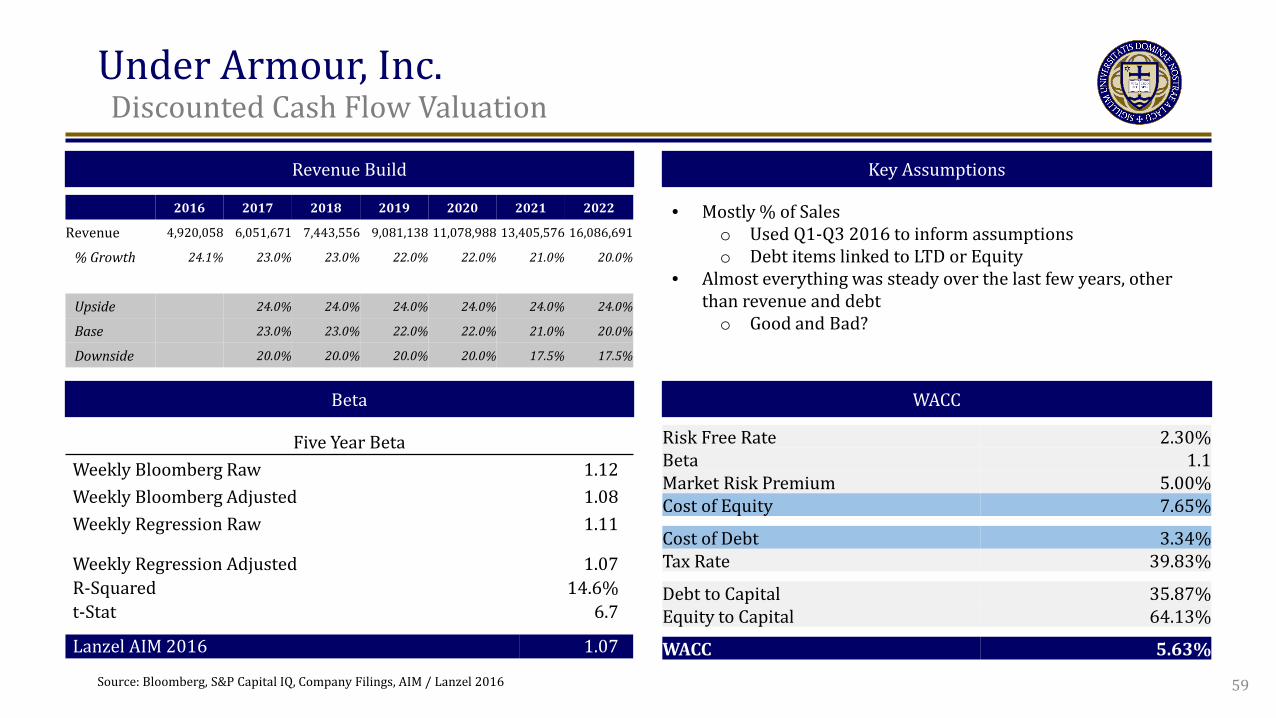

Revenue Build Key Assumptions

• Mostly % of Sales o Used Q1-Q3 2016 to inform assumptions o Debt items linked to LTD or Equity

• Almost everything was steady over the last few years, other than revenue and debt o Good and Bad?

Beta WACC

Risk Free Rate 2.30% Beta 1.1 Market Risk Premium 5.00% Cost of Equity 7.65%

Cost of Debt 3.34% Tax Rate 39.83%

Debt to Capital 35.87% Equity to Capital 64.13%

WACC 5.63%

Five Year Beta Weekly Bloomberg Raw 1.12 Weekly Bloomberg Adjusted 1.08 Weekly Regression Raw 1.11

Weekly Regression Adjusted R-Squared t-Stat

1.07 14.6%

6.7

Lanzel AIM 2016 1.07

59

2016 2017 2018 2019 2020 2021 2022

Revenue 4,920,058 6,051,671 7,443,556 9,081,138 11,078,988 13,405,576 16,086,691

% Growth 24.1% 23.0% 23.0% 22.0% 22.0% 21.0% 20.0%

Upside 24.0% 24.0% 24.0% 24.0% 24.0% 24.0%

Base 23.0% 23.0% 22.0% 22.0% 21.0% 20.0%

Downside 20.0% 20.0% 20.0% 20.0% 17.5% 17.5%

Under Armour, Inc. t

Discounted Cash Flow Valuation

Source: Bloomberg, S&P Capital IQ, Company Filings, AIM / Lanzel 2016 60

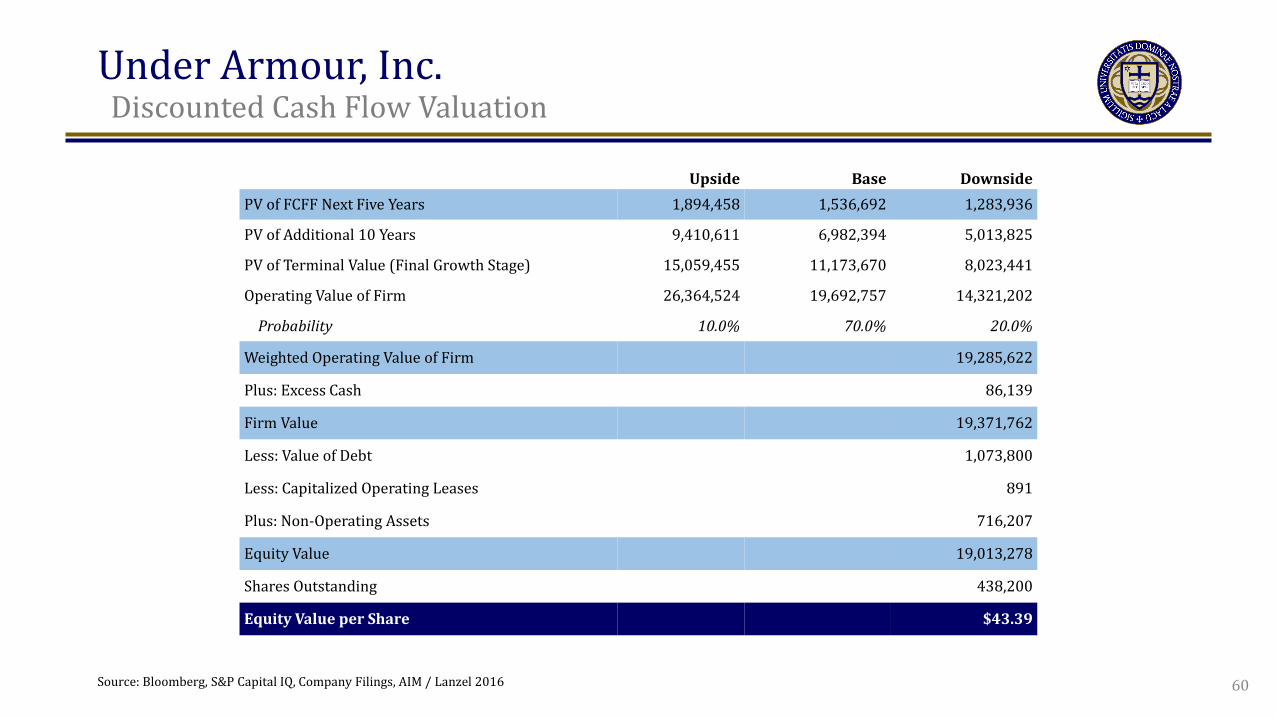

Upside Base Downside PV of FCFF Next Five Years 1,894,458 1,536,692 1,283,936

PV of Additional 10 Years 9,410,611 6,982,394 5,013,825

PV of Terminal Value (Final Growth Stage) 15,059,455 11,173,670 8,023,441

Operating Value of Firm 26,364,524 19,692,757 14,321,202

Probability 10.0% 70.0% 20.0%

Weighted Operating Value of Firm 19,285,622

Plus: Excess Cash 86,139

Firm Value 19,371,762

Less: Value of Debt 1,073,800

Less: Capitalized Operating Leases 891

Plus: Non-Operating Assets 716,207

Equity Value 19,013,278

Shares Outstanding 438,200

Equity Value per Share $43.39

Under Armour, Inc. t

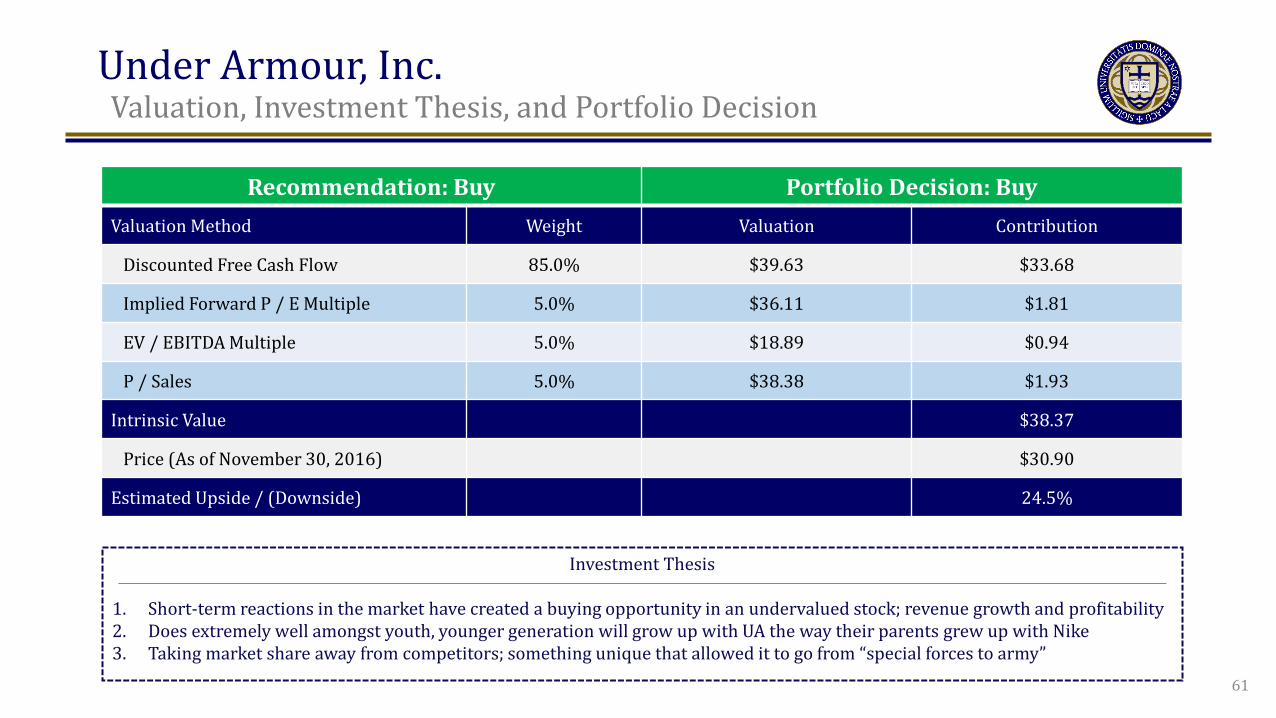

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Buy Portfolio Decision: Buy Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 85.0% $39.63 $33.68

Implied Forward P / E Multiple 5.0% $36.11 $1.81

EV / EBITDA Multiple 5.0% $18.89 $0.94

P / Sales 5.0% $38.38 $1.93

Intrinsic Value $38.37

Price (As of November 30, 2016) $30.90

Estimated Upside / (Downside) 24.5%

Investment Thesis

1. Short-term reactions in the market have created a buying opportunity in an undervalued stock; revenue growth and profitability 2. Does extremely well amongst youth, younger generation will grow up with UA the way their parents grew up with Nike 3. Taking market share away from competitors; something unique that allowed it to go from “special forces to army”

61

Verisk Analytics t

Nasdaq: VRSK

One-Year Price Chart

Focus

Company & Industry Overview

Price (As of November 30, 2016): $83.88

TTM Price-to-Earnings: 24.2x

Market Capitalization: $14.05Bn

Beta: 0.65

TTM Adjusted Earnings per Share: $3.47

Source: Yahoo! Finance 62

Verisk Analytics t

Development of VRSK Business Model

1971: Insurance

Services Office (ISO) started as a not-for-profit

1997: Acquired American Insurance

Group (AISG) for large

insurance claim database

1998: Acquired National

Insurance Crime Bureau

2002: Acquired AIR, a

technology leader in

catastrophe modeling

2004: Entered Healthcare

space

2005: Entered mortgage

market

2006: Acquired Xactware, estimating

software for business/const

ruction

2009: IPO of Verisk

Analytics

2011-2015: Various

Acquisitions

1997: Converted to for-profit with ESOP structure

1971: Founded as not-for-profit advisory organization 2009: Began trading on Nasdaq

63 Source: Company Filings

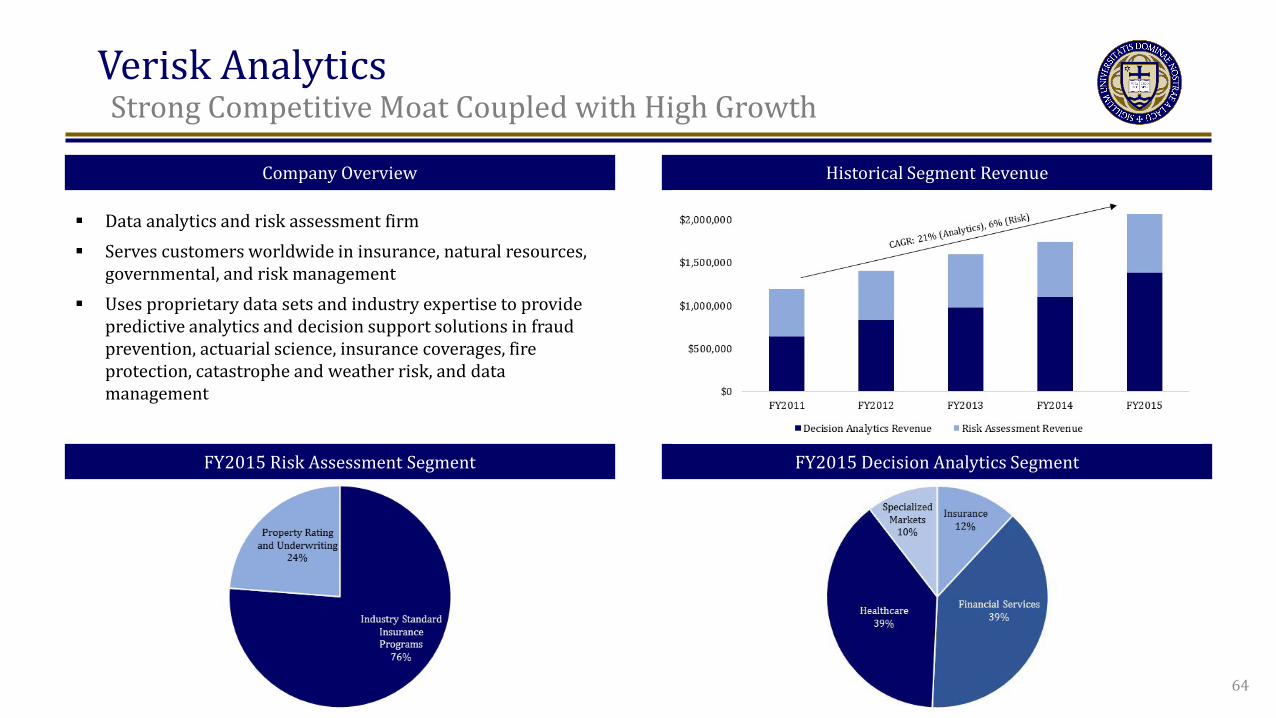

Verisk Analytics t

Strong Competitive Moat Coupled with High Growth

Company Overview Historical Segment Revenue

FY2015 Risk Assessment Segment FY2015 Decision Analytics Segment

Data analytics and risk assessment firm Serves customers worldwide in insurance, natural resources,

governmental, and risk management Uses proprietary data sets and industry expertise to provide

predictive analytics and decision support solutions in fraud prevention, actuarial science, insurance coverages, fire protection, catastrophe and weather risk, and data management

64

Verisk Analytics t

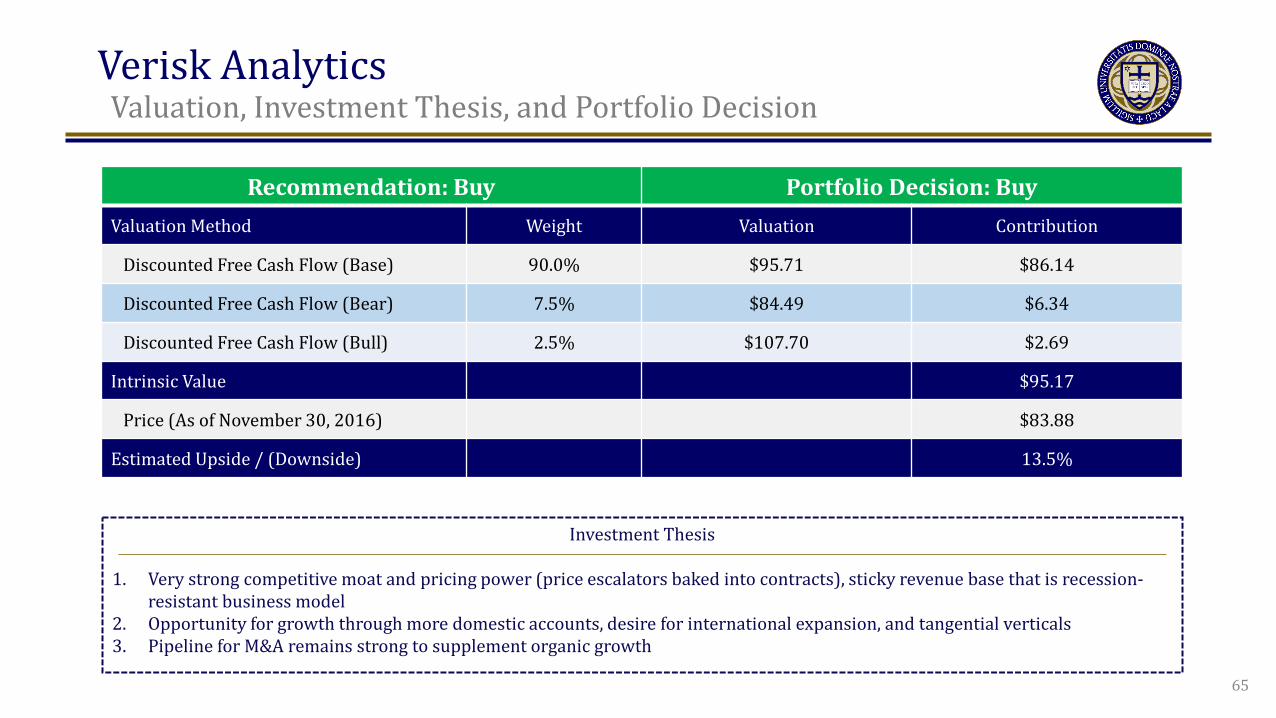

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Buy Portfolio Decision: Buy Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow (Base) 90.0% $95.71 $86.14

Discounted Free Cash Flow (Bear) 7.5% $84.49 $6.34

Discounted Free Cash Flow (Bull) 2.5% $107.70 $2.69

Intrinsic Value $95.17

Price (As of November 30, 2016) $83.88

Estimated Upside / (Downside) 13.5%

Investment Thesis

1. Very strong competitive moat and pricing power (price escalators baked into contracts), sticky revenue base that is recession-resistant business model

2. Opportunity for growth through more domestic accounts, desire for international expansion, and tangential verticals 3. Pipeline for M&A remains strong to supplement organic growth

65

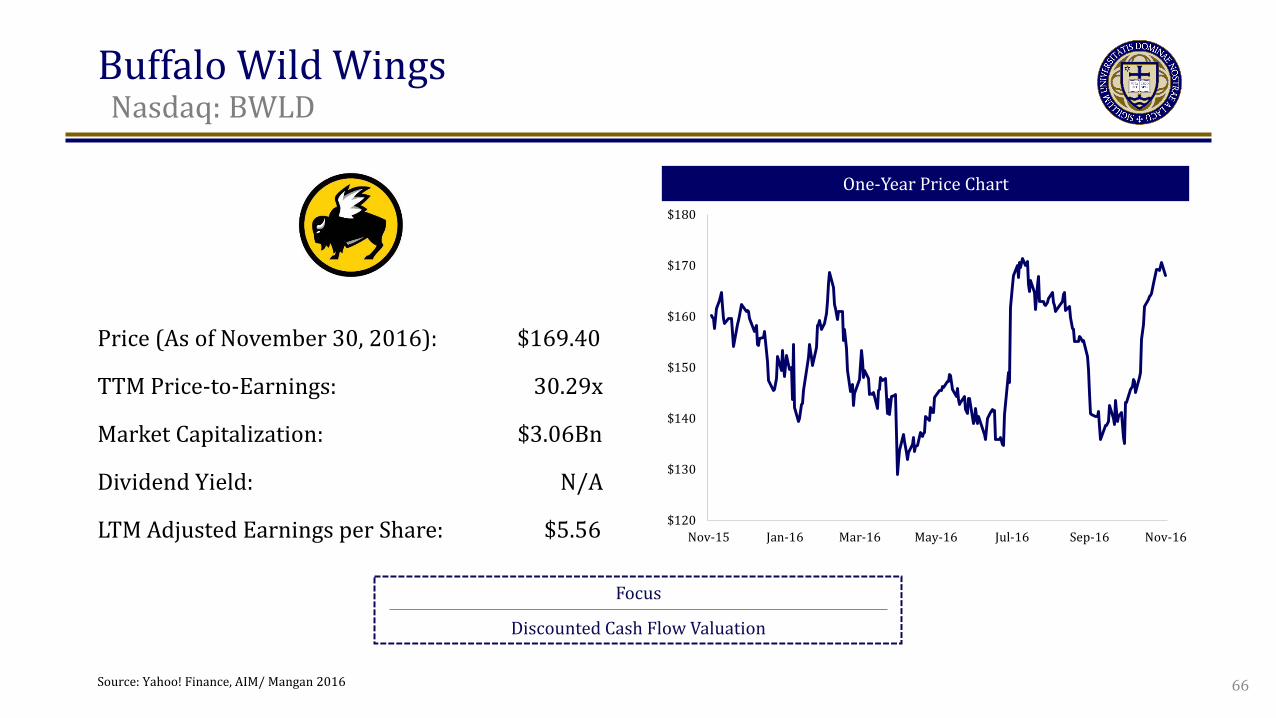

Buffalo Wild Wings t

Nasdaq: BWLD

One-Year Price Chart

Focus

Discounted Cash Flow Valuation

Price (As of November 30, 2016): $169.40

TTM Price-to-Earnings: 30.29x

Market Capitalization: $3.06Bn

Dividend Yield: N/A

LTM Adjusted Earnings per Share: $5.56

Source: Yahoo! Finance, AIM/ Mangan 2016

$120

$130

$140

$150

$160

$170

$180

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16

66

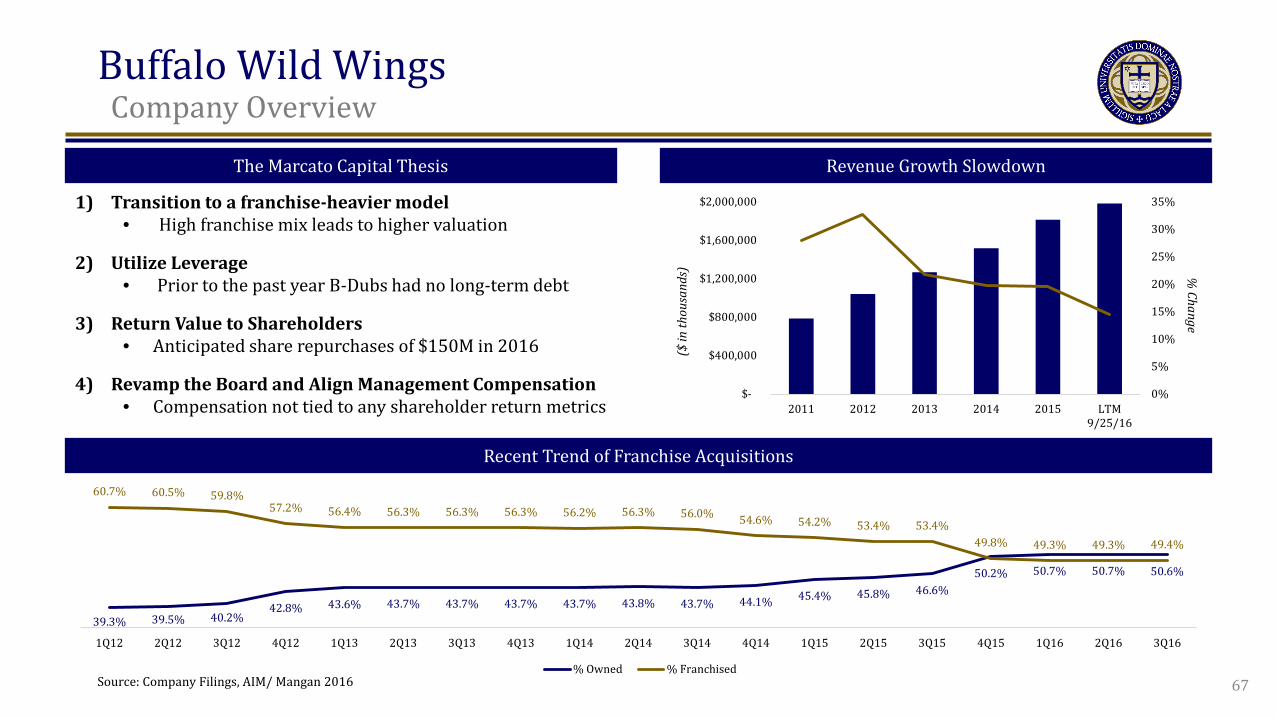

Buffalo Wild Wings t

Company Overview

0%

5%

10%

15%

20%

25%

30%

35%

$-

$400,000

$800,000

$1,200,000

$1,600,000

$2,000,000

2011 2012 2013 2014 2015 LTM9/25/16

% Change

($ in

thou

sand

s)

Recent Trend of Franchise Acquisitions

Revenue Growth Slowdown The Marcato Capital Thesis

1) Transition to a franchise-heavier model • High franchise mix leads to higher valuation

2) Utilize Leverage • Prior to the past year B-Dubs had no long-term debt

3) Return Value to Shareholders • Anticipated share repurchases of $150M in 2016

4) Revamp the Board and Align Management Compensation • Compensation not tied to any shareholder return metrics

39.3% 39.5% 40.2% 42.8% 43.6% 43.7% 43.7% 43.7% 43.7% 43.8% 43.7% 44.1% 45.4% 45.8% 46.6%

50.2% 50.7% 50.7% 50.6%

60.7% 60.5% 59.8% 57.2% 56.4% 56.3% 56.3% 56.3% 56.2% 56.3% 56.0% 54.6% 54.2% 53.4% 53.4%

49.8% 49.3% 49.3% 49.4%

1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16

% Owned % Franchised67 Source: Company Filings, AIM/ Mangan 2016

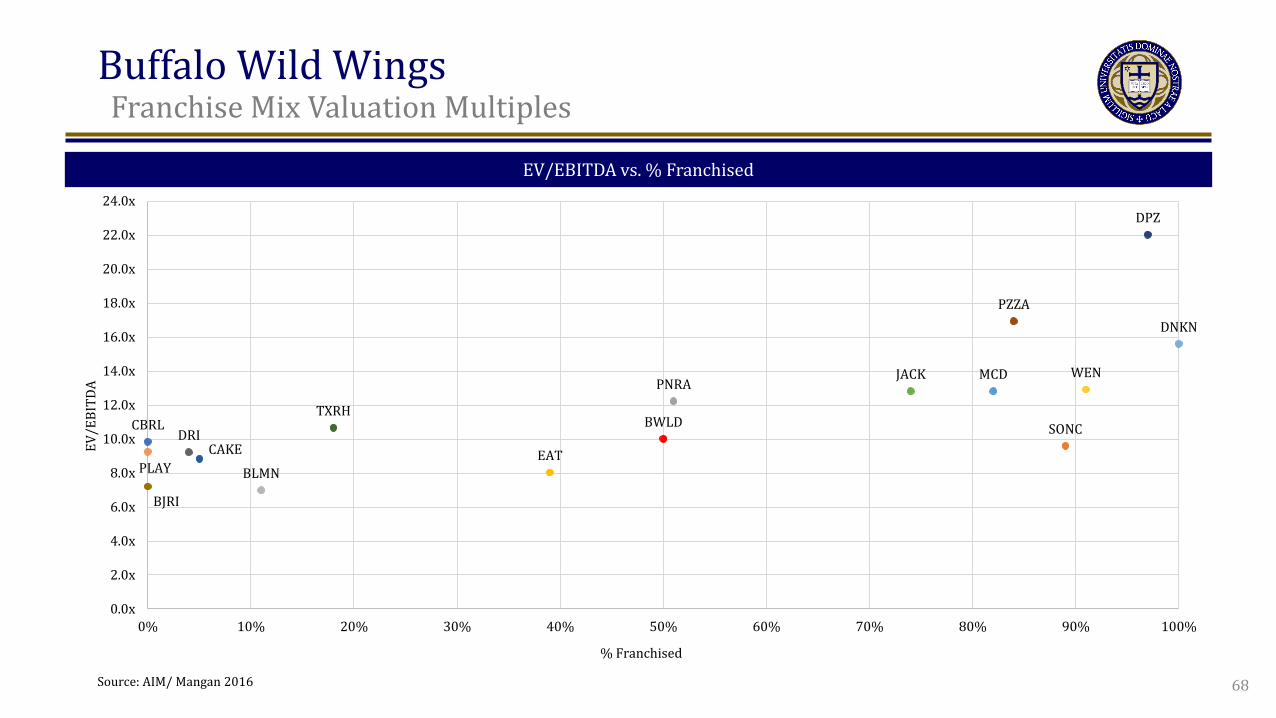

Buffalo Wild Wings t

Franchise Mix Valuation Multiples

EV/EBITDA vs. % Franchised

68

MCD

SONC

PNRA

EAT

CBRL

JACK

CAKE

PZZA

DRI

BJRI

DPZ

TXRH

DNKN

PLAY BLMN

WEN

BWLD

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

20.0x

22.0x

24.0x

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

EV/E

BITD

A

% Franchised

Source: AIM/ Mangan 2016

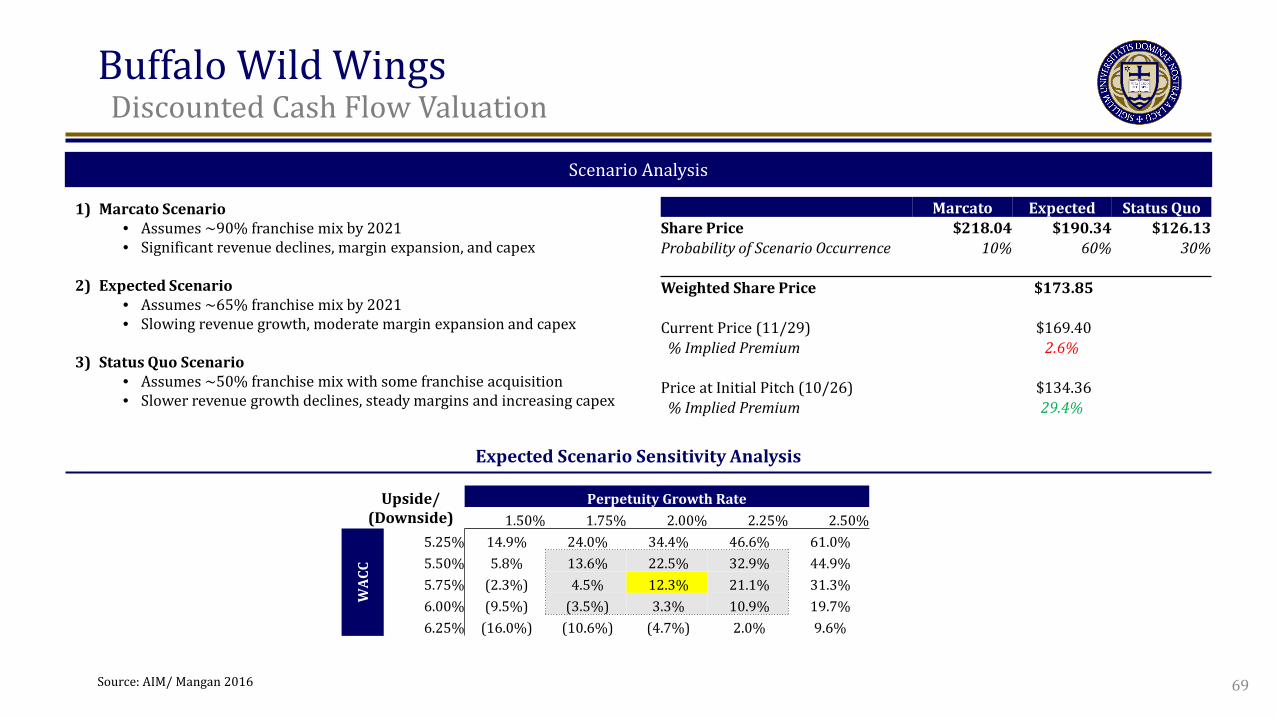

Buffalo Wild Wings t

Discounted Cash Flow Valuation

Scenario Analysis

Marcato Expected Status Quo Share Price $218.04 $190.34 $126.13 Probability of Scenario Occurrence 10% 60% 30% Weighted Share Price $173.85 Current Price (11/29) $169.40 % Implied Premium 2.6%

Price at Initial Pitch (10/26) $134.36 % Implied Premium 29.4%

1) Marcato Scenario • Assumes ~90% franchise mix by 2021 • Significant revenue declines, margin expansion, and capex

2) Expected Scenario • Assumes ~65% franchise mix by 2021 • Slowing revenue growth, moderate margin expansion and capex

3) Status Quo Scenario • Assumes ~50% franchise mix with some franchise acquisition • Slower revenue growth declines, steady margins and increasing capex

Expected Scenario Sensitivity Analysis

Perpetuity Growth Rate 1.50% 1.75% 2.00% 2.25% 2.50%

WAC

C

5.25% 14.9% 24.0% 34.4% 46.6% 61.0% 5.50% 5.8% 13.6% 22.5% 32.9% 44.9% 5.75% (2.3%) 4.5% 12.3% 21.1% 31.3% 6.00% (9.5%) (3.5%) 3.3% 10.9% 19.7% 6.25% (16.0%) (10.6%) (4.7%) 2.0% 9.6%

Upside/ (Downside)

69 Source: AIM/ Mangan 2016

Buffalo Wild Wings t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Pass Portfolio Decision: Pass Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 90.0% $173.85 $156.46

Implied Forward P/E Multiple 2.5% $127.39 $3.18

Implied EV/EBITDA Multiple 2.5% $116.36 $2.91

Franchise Mix Valuation Multiple 5.0% $169.25 $8.48

Intrinsic Value $171.02

Price (As of November 30, 2016) $169.40

Estimated Upside / (Downside) 1.0%

Investment Thesis

1. Declining revenue growth and questionable capital allocation decisions led to stock struggles and activist interest 2. Potential for excess return exists through refranchising and capital optimization – all depends on management’s ability to do so 3. Uncertainty around future strategy and expensive current price make B-Dubs a risky opportunity with a depressed upside

70

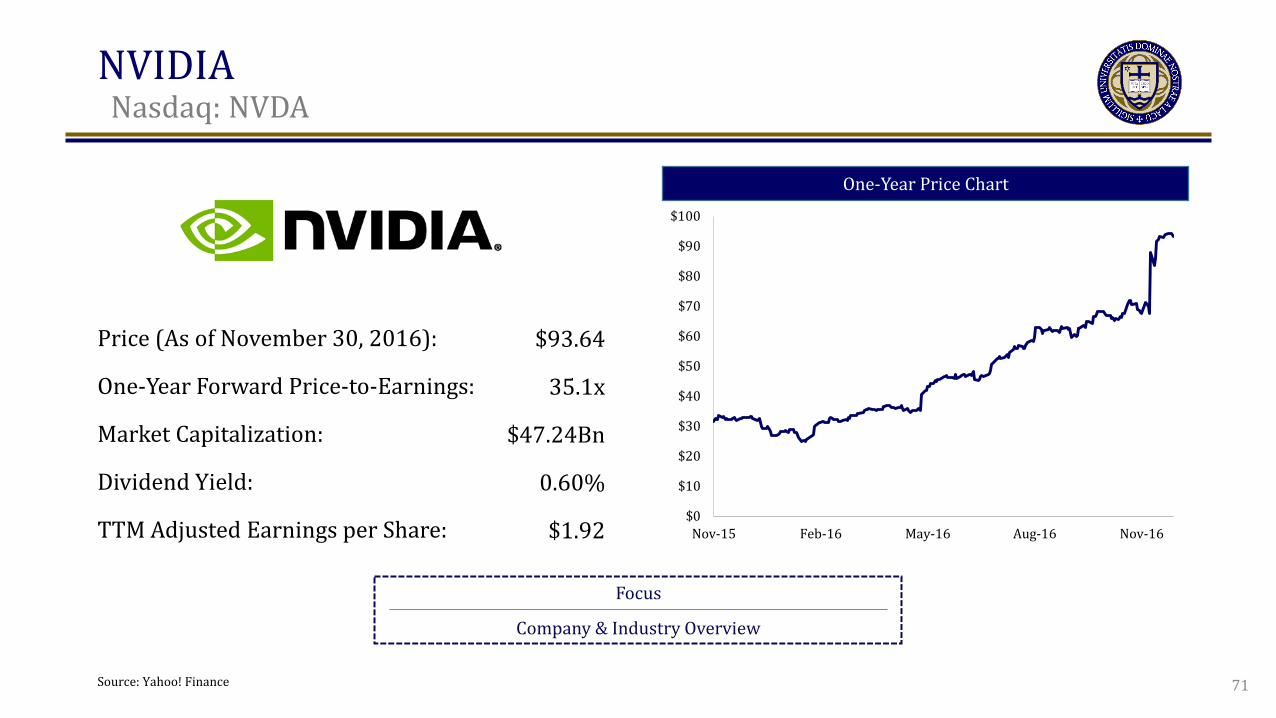

NVIDIA t

Nasdaq: NVDA

One-Year Price Chart

Focus

Company & Industry Overview

Price (As of November 30, 2016):

One-Year Forward Price-to-Earnings:

Market Capitalization:

Dividend Yield:

TTM Adjusted Earnings per Share:

Source: Yahoo! Finance

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

Nov-15 Feb-16 May-16 Aug-16 Nov-16

$93.64

35.1x

$47.24Bn

0.60%

$1.92

71

NVIDIA t

Growth Segments

Virtual Reality

Self-Driving Cars Artificial Intelligence

eSports

Source: Company Filings, AIM/Markwalter 2016 72

NVIDIA t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Buy Portfolio Decision: Buy Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 100.0% $102.36 $102.36

Implied Forward P/E Multiple 0.0% $32.47 $0.00

Implied Forward EV/Revenue Multiple 0.0% $39.35 $0.00

Implied Forward EV/EBITDA Multiple 0.0% $34.97 $0.00

Intrinsic Value $102.36

Price (As of November 30, 2016) $92.20

Estimated Upside / (Downside) 11.0%

Investment Thesis

1. Artificial intelligence hardware market is not as competitive as the sell-side analysts believe it to be. 2. The market for artificial intelligence is larger than analysts believe it to be. 3. NVIDIA has a sustainable competitive advantage within the GPU market for the coming years.

73

Dunkin’ Brands Group, Inc. t

NasdaqGS: DNKN

One-Year Price Chart

Focus

Relative Valuation

Price (As of November 30, 2016): $54.19

TTM Price-to-Earnings: 38.10x

Market Capitalization: $4.97Bn

Dividend Yield: 2.22%

TTM Adjusted Earnings per Share: $1.41

Source: Bloomberg, S&P Capital IQ

$30

$35

$40

$45

$50

$55

$60

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16

+ 27.75%

74

Dunkin’ Brands Group, Inc. t

Dunkin’ Donuts U.S. Medium- to Long-Term Expansion

Average Initial Capital Requirement: $485,000 Average Annual Revenue: $900,000 Cash-on-Cash Return: 20.0%

Mid-West & West New Store Economics

Operational Initiatives

Comparable Stores Sales Growth: 38/39 Q’s Total Cost Savings Since 2014: $250.0mm

Source: Bloomberg, S&P Capital IQ 75

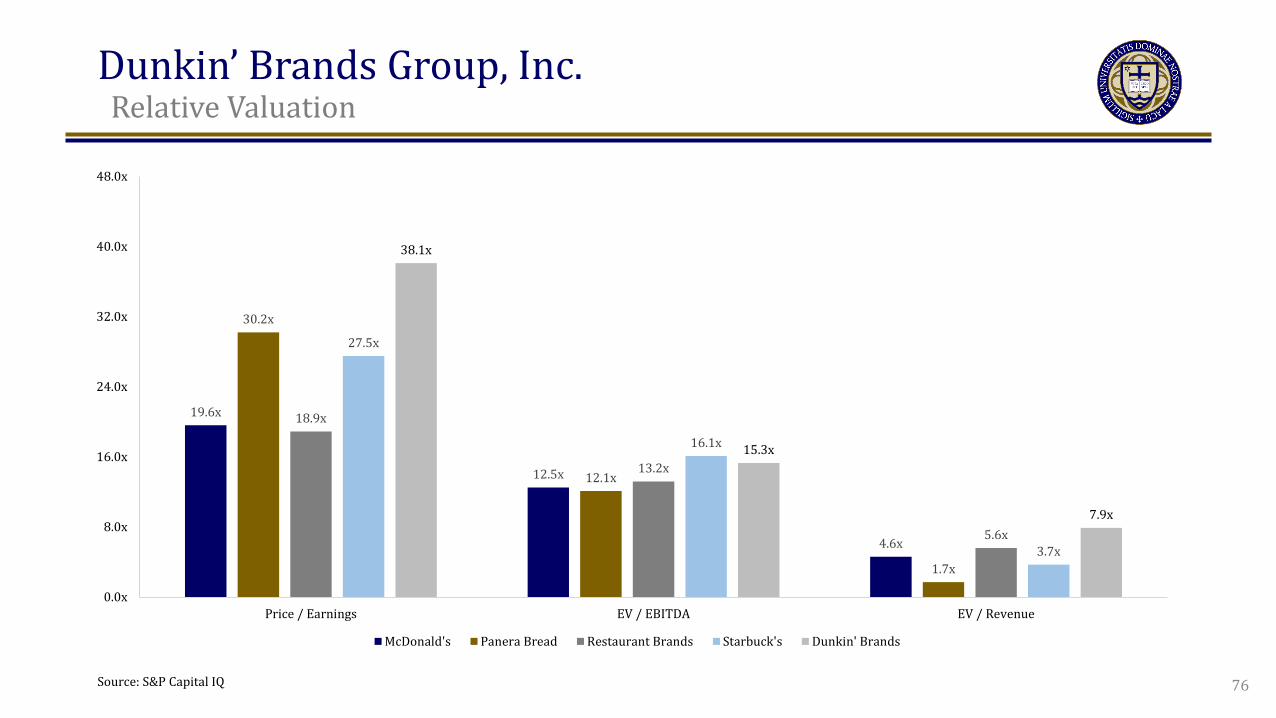

Dunkin’ Brands Group, Inc. t

Relative Valuation

19.6x

12.5x

4.6x

30.2x

12.1x

1.7x

18.9x

13.2x

5.6x

27.5x

16.1x

3.7x

38.1x

15.3x

7.9x

0.0x

8.0x

16.0x

24.0x

32.0x

40.0x

48.0x

Price / Earnings EV / EBITDA EV / Revenue

McDonald's Panera Bread Restaurant Brands Starbuck's Dunkin' Brands

Source: S&P Capital IQ 76

Dunkin’ Brands Group, Inc. t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Pass Portfolio Decision: Pass Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 90.0% $50.84 $45.75

Price / Earnings 3.3% $34.23 $1.14

TEV / EBITDA 3.3% $41.86 $1.40

TEV / Revenue 3.3% $29.85 $1.00

Intrinsic Value $49.29

Price (As of November 30, 2016) $54.19

Estimated Upside / (Downside) (9.0%)

Investment Thesis

1. Strong, established brand with compelling opportunities in the Midwest, Texas, and international markets 2. Franchise-based business model offers growth with captivating store economics 3. Unattractive entry price

77

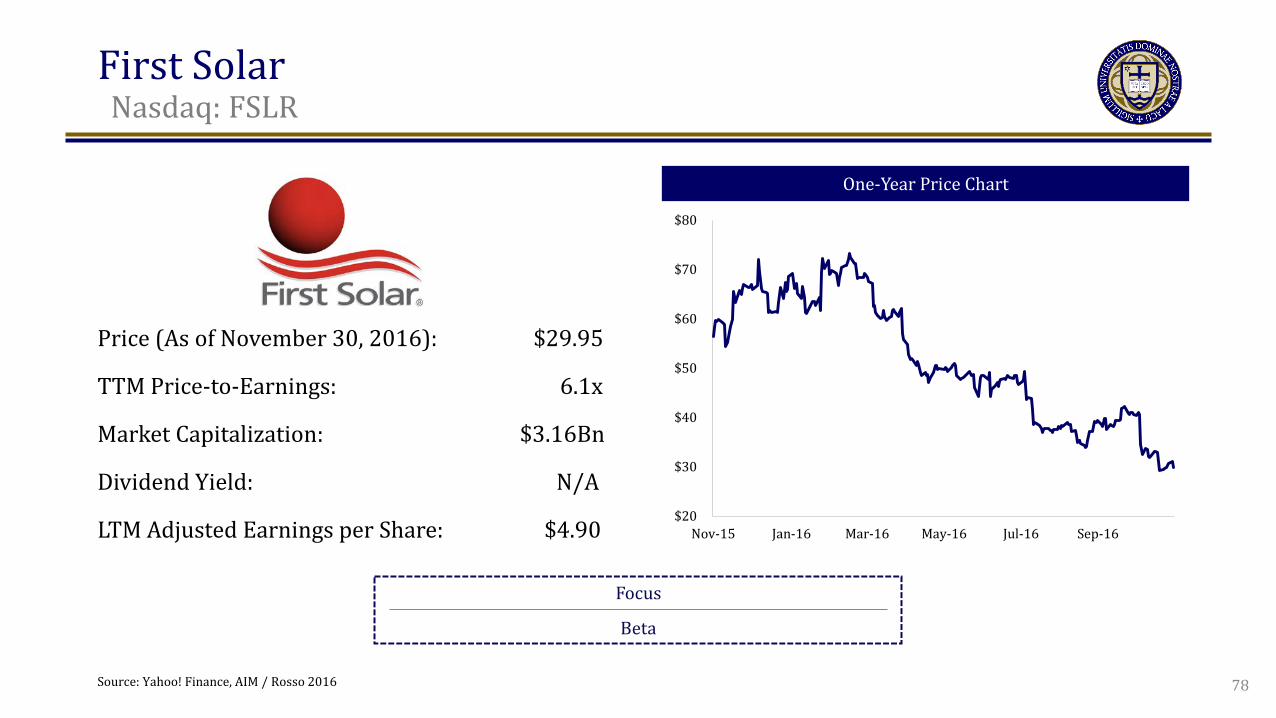

First Solar t

Nasdaq: FSLR

One-Year Price Chart

Focus

Beta

Price (As of November 30, 2016): $29.95

TTM Price-to-Earnings: 6.1x

Market Capitalization: $3.16Bn

Dividend Yield: N/A

LTM Adjusted Earnings per Share: $4.90 $20

$30

$40

$50

$60

$70

$80

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16

78 Source: Yahoo! Finance, AIM / Rosso 2016

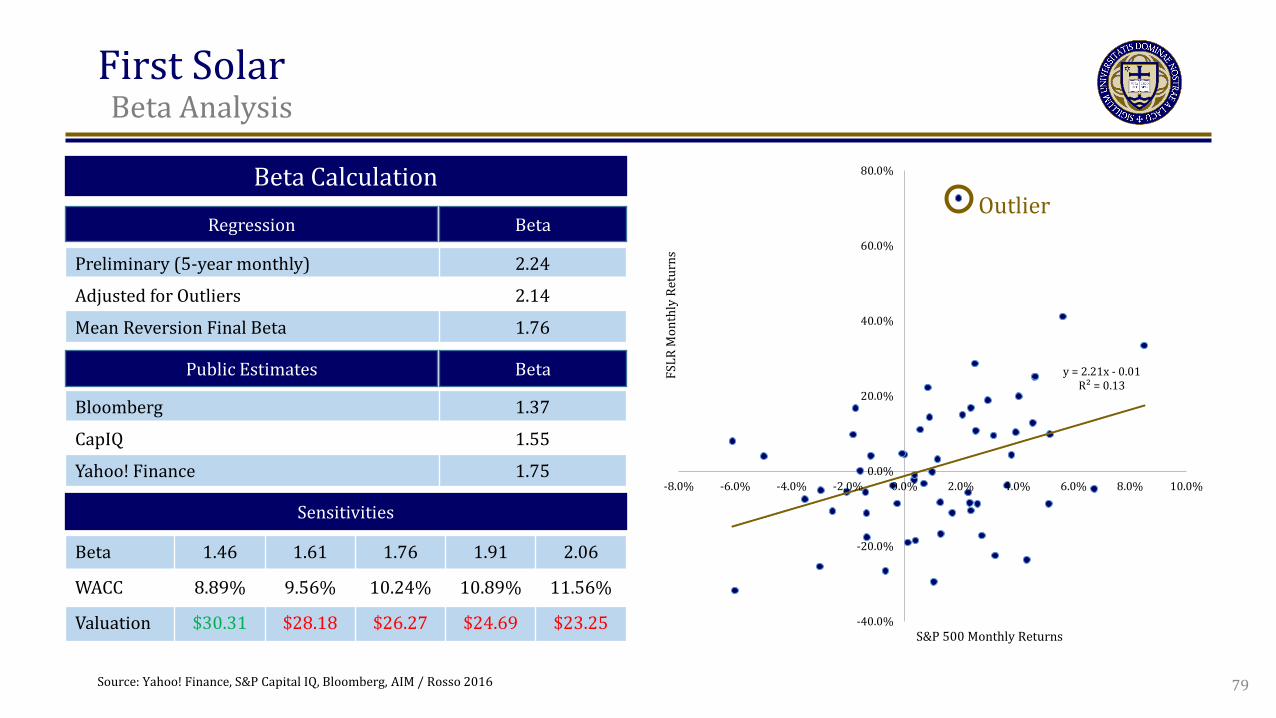

First Solar t

Beta Analysis

Beta Calculation

Regression Beta

Preliminary (5-year monthly) 2.24

Adjusted for Outliers 2.14

Mean Reversion Final Beta 1.76

Public Estimates Beta

Bloomberg 1.37

CapIQ 1.55

Yahoo! Finance 1.75

y = 2.21x - 0.01 R² = 0.13

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

-8.0% -6.0% -4.0% -2.0% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0%

FSLR

Mon

thly

Ret

urns

S&P 500 Monthly Returns

Outlier

Sensitivities

Beta 1.46 1.61 1.76 1.91 2.06

WACC 8.89% 9.56% 10.24% 10.89% 11.56%

Valuation $30.31 $28.18 $26.27 $24.69 $23.25

79 Source: Yahoo! Finance, S&P Capital IQ, Bloomberg, AIM / Rosso 2016

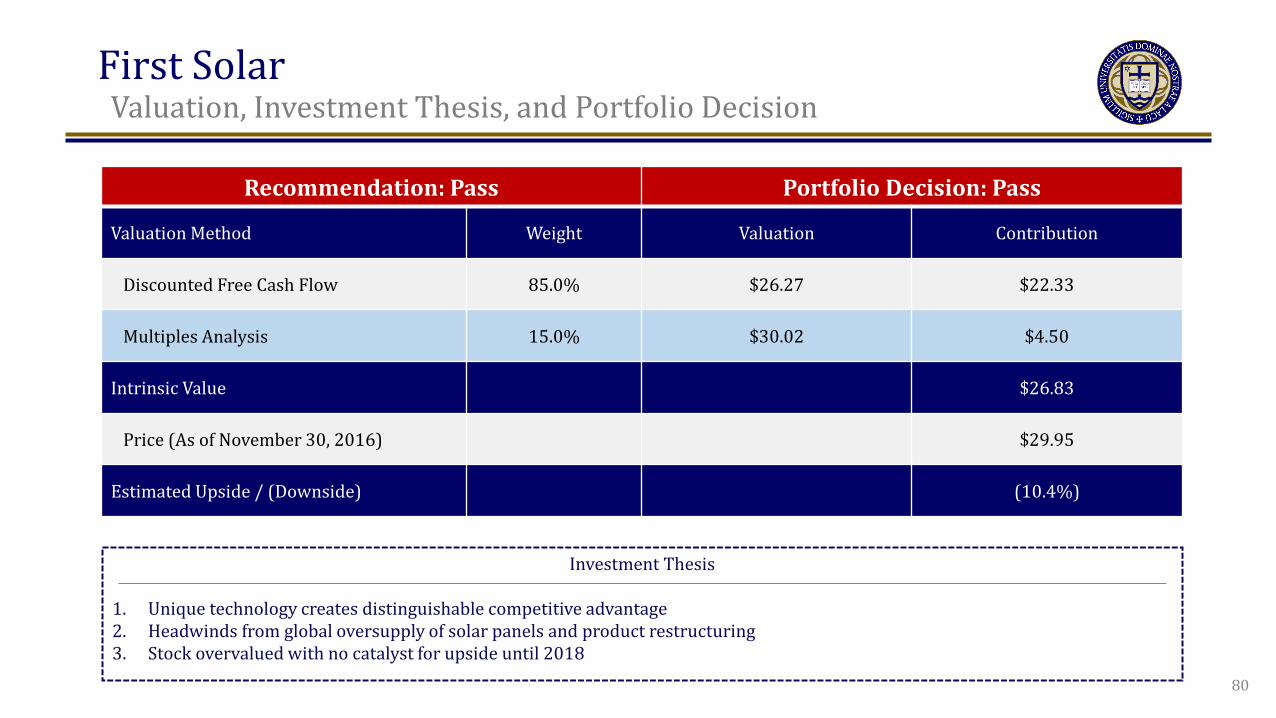

First Solar t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Pass Portfolio Decision: Pass

Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 85.0% $26.27 $22.33

Multiples Analysis 15.0% $30.02 $4.50

Intrinsic Value $26.83

Price (As of November 30, 2016) $29.95

Estimated Upside / (Downside) (10.4%)

Investment Thesis

1. Unique technology creates distinguishable competitive advantage 2. Headwinds from global oversupply of solar panels and product restructuring 3. Stock overvalued with no catalyst for upside until 2018

80

Whitestone REIT t

NYSE: WSR

One-Year Price Chart

Focus

Alternative Valuation Methods

Price (As of November 30, 2016): $13.59

TTM Price-to-Earnings: 10.32x

Market Capitalization: $0.41Bn

Dividend Yield: 8.23%

TTM Adjusted Earnings per Share: $0.32

Source: Yahoo! Finance, AIM / Seymour 2016

$8

$9

$10

$11

$12

$13

$14

$15

$16

$17

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16

81

Whitestone REIT t

Investment Highlights

Tenant Industry Distribution by Annualized Base Revenue Company Overview

• Whitestone REIT acquires and redevelops “Community

Center Properties”

• Diverse, “internet-resistant” tenant mix

• Grow through acquisitions and unlocking untapped

potential in high-growth, high-income communities

• 12 acquisitions in 2015, 2 YTD 2016; 71 total properties

Annualized Base Revenue by Geography ($ in thousands) Average Median Household Income ($ in thousands)

Services and Entertainment

23%

Dining 21%

Health & Wellness

20%

Specialty Retail 17%

Grocery 13%

Education 6%

77.4 75.7 70.5 60.3 58.7 57.1 53.8 52.7

FRT WSR REG KIM EQY DDR BRX WRI

Source: WSR 10-K, WSR August 2016 Investor Presentation, AIM / Seymour 2016 82

$5,329 $710

$10,726

$22,319 $26,735

$3,762

$0$5,000

$10,000$15,000$20,000$25,000$30,000

Austin Chicago Dallas Houston Phoenix San Antonio

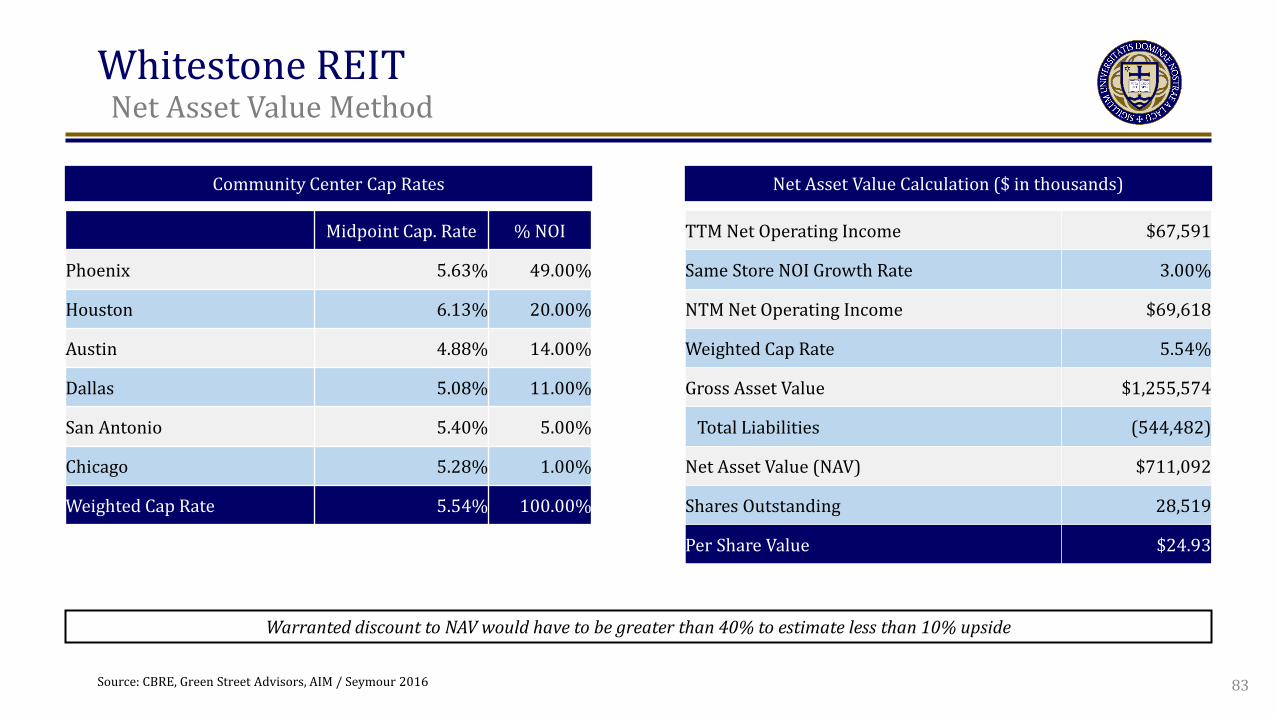

Whitestone REIT t

Net Asset Value Method

Community Center Cap Rates

Source: CBRE, Green Street Advisors, AIM / Seymour 2016

Midpoint Cap. Rate % NOI

Phoenix 5.63% 49.00%

Houston 6.13% 20.00%

Austin 4.88% 14.00%

Dallas 5.08% 11.00%

San Antonio 5.40% 5.00%

Chicago 5.28% 1.00%

Weighted Cap Rate 5.54% 100.00%

Net Asset Value Calculation ($ in thousands)

TTM Net Operating Income $67,591

Same Store NOI Growth Rate 3.00%

NTM Net Operating Income $69,618

Weighted Cap Rate 5.54%

Gross Asset Value $1,255,574

Total Liabilities (544,482)

Net Asset Value (NAV) $711,092

Shares Outstanding 28,519

Per Share Value $24.93

83

Warranted discount to NAV would have to be greater than 40% to estimate less than 10% upside

Whitestone REIT t

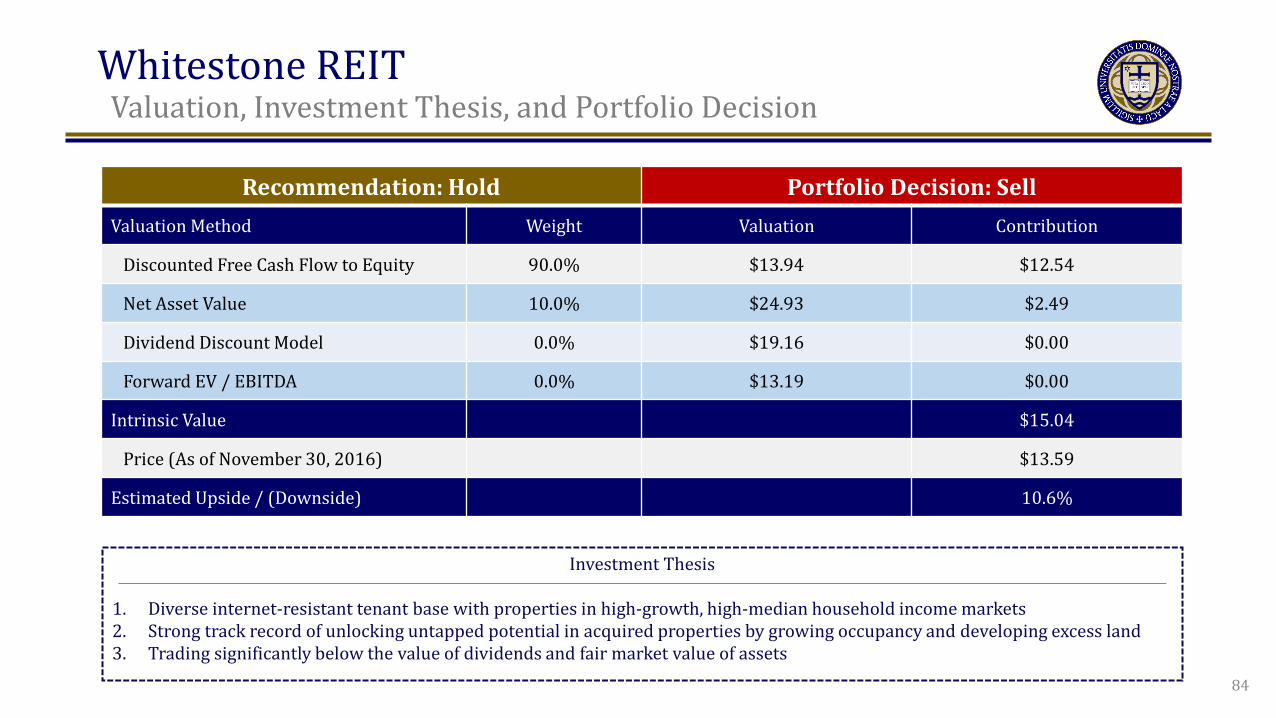

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Hold Portfolio Decision: Sell Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow to Equity 90.0% $13.94 $12.54

Net Asset Value 10.0% $24.93 $2.49

Dividend Discount Model 0.0% $19.16 $0.00

Forward EV / EBITDA 0.0% $13.19 $0.00

Intrinsic Value $15.04

Price (As of November 30, 2016) $13.59

Estimated Upside / (Downside) 10.6%

Investment Thesis

1. Diverse internet-resistant tenant base with properties in high-growth, high-median household income markets 2. Strong track record of unlocking untapped potential in acquired properties by growing occupancy and developing excess land 3. Trading significantly below the value of dividends and fair market value of assets

84

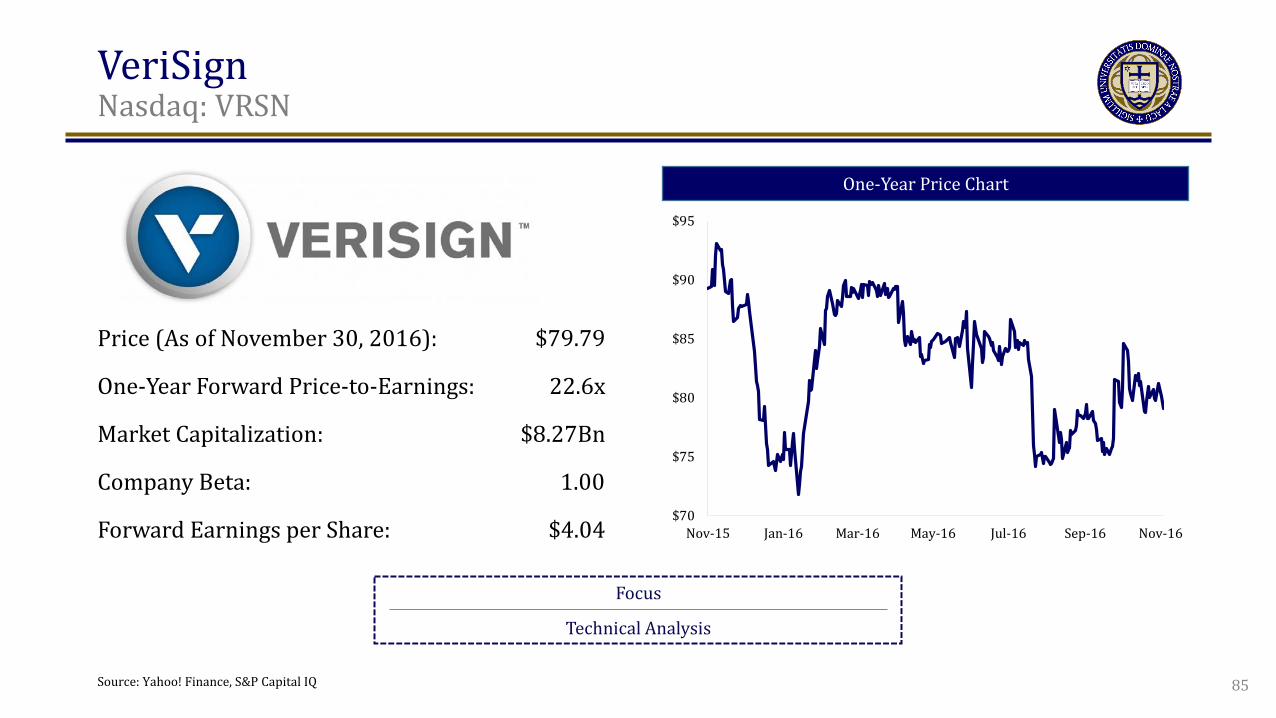

VeriSignt

Nasdaq: VRSN

One-Year Price Chart

Focus

Technical Analysis

Price (As of November 30, 2016): $79.79

One-Year Forward Price-to-Earnings: 22.6x

Market Capitalization: $8.27Bn

Company Beta: 1.00

Forward Earnings per Share: $4.04

Source: Yahoo! Finance, S&P Capital IQ 85

$70

$75

$80

$85

$90

$95

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16

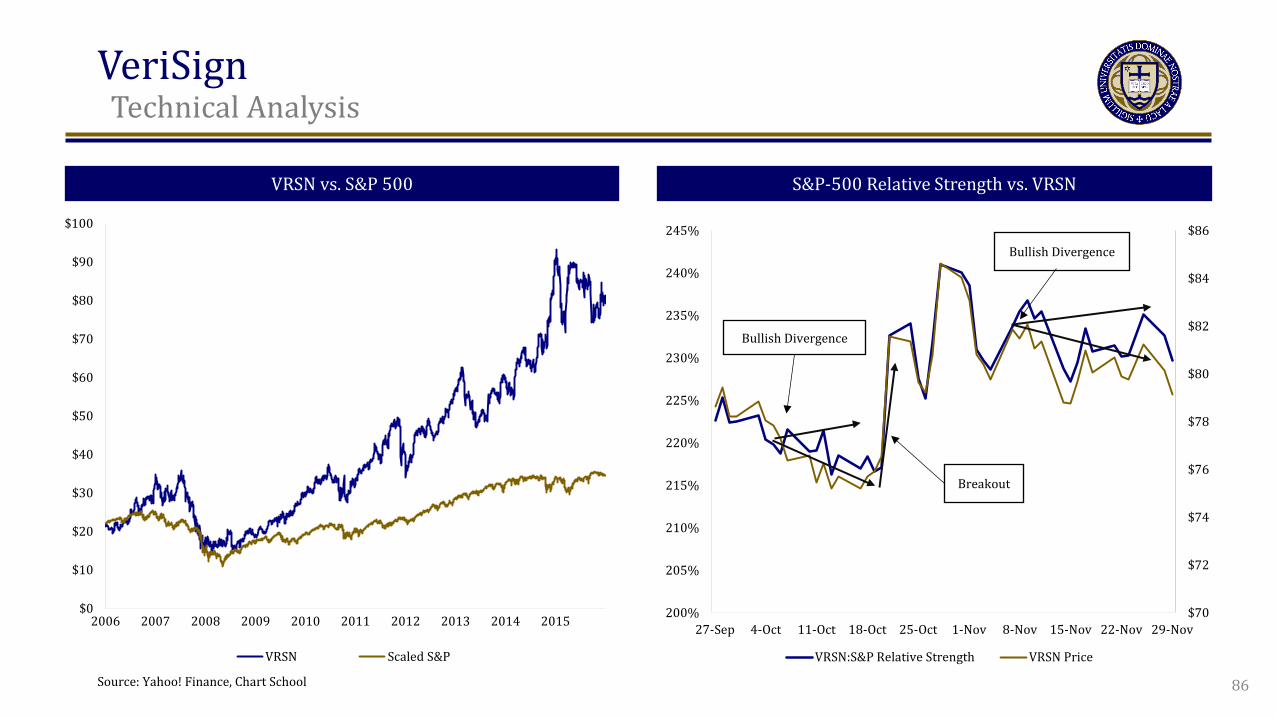

VeriSign t

Technical Analysis

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

VRSN Scaled S&P

$70

$72

$74

$76

$78

$80

$82

$84

$86

200%

205%

210%

215%

220%

225%

230%

235%

240%

245%

27-Sep 4-Oct 11-Oct 18-Oct 25-Oct 1-Nov 8-Nov 15-Nov 22-Nov 29-Nov

VRSN:S&P Relative Strength VRSN Price

Bullish Divergence

Breakout

Bullish Divergence

86

VRSN vs. S&P 500 S&P-500 Relative Strength vs. VRSN

Source: Yahoo! Finance, Chart School

VeriSign t

Technical Analysis

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

-10

-5

0

5

10

15

20

28-Nov 28-Feb 31-May 31-Aug 30-Nov 29-Feb 31-May 31-Aug

Bearish

Neutral

Bullish

$60

$65

$70

$75

$80

$85

$90

$95

$100

30-Nov 31-Jan 31-Mar 31-May 31-Jul 30-Sep

Close -2 sdma +2 sdma

Breakout

87

5 Year Seasonality 1 Year Bollinger Bands

MACD

Downward Momentum

W-Bottom W-Bottom

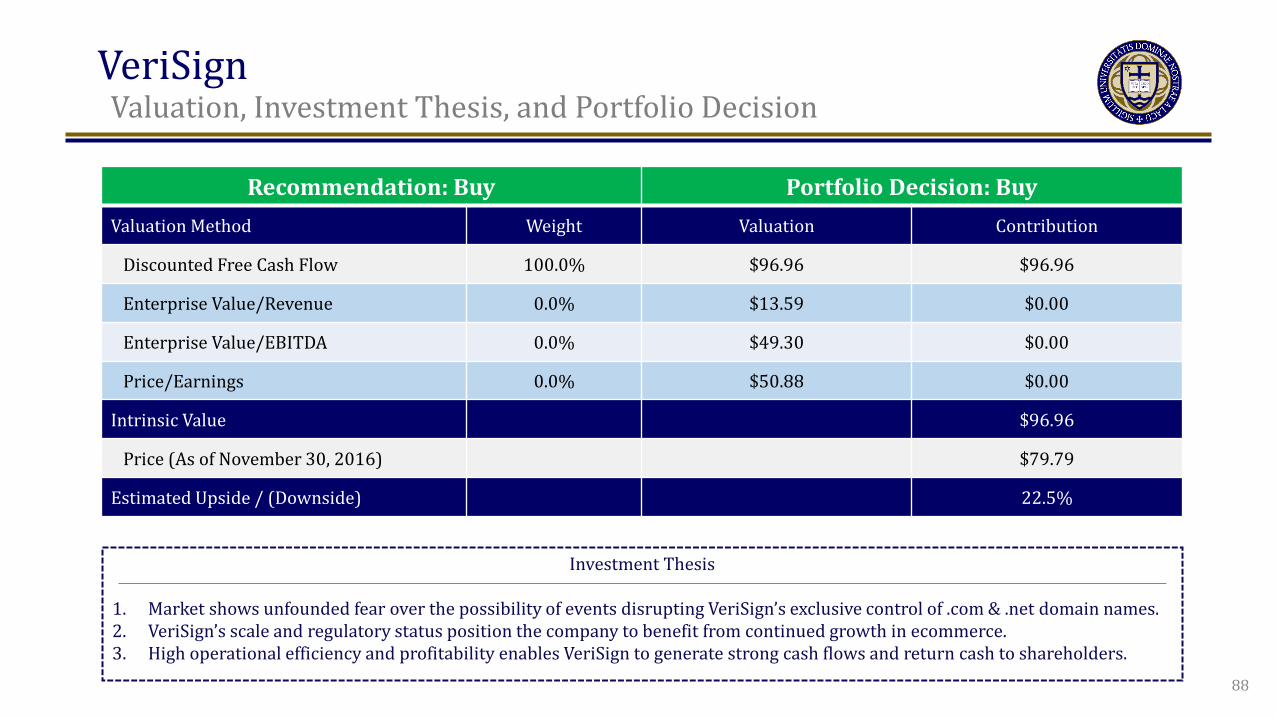

VeriSign t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Buy Portfolio Decision: Buy Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 100.0% $96.96 $96.96

Enterprise Value/Revenue 0.0% $13.59 $0.00

Enterprise Value/EBITDA 0.0% $49.30 $0.00

Price/Earnings 0.0% $50.88 $0.00

Intrinsic Value $96.96

Price (As of November 30, 2016) $79.79

Estimated Upside / (Downside) 22.5%

Investment Thesis

1. Market shows unfounded fear over the possibility of events disrupting VeriSign’s exclusive control of .com & .net domain names. 2. VeriSign’s scale and regulatory status position the company to benefit from continued growth in ecommerce. 3. High operational efficiency and profitability enables VeriSign to generate strong cash flows and return cash to shareholders.

88

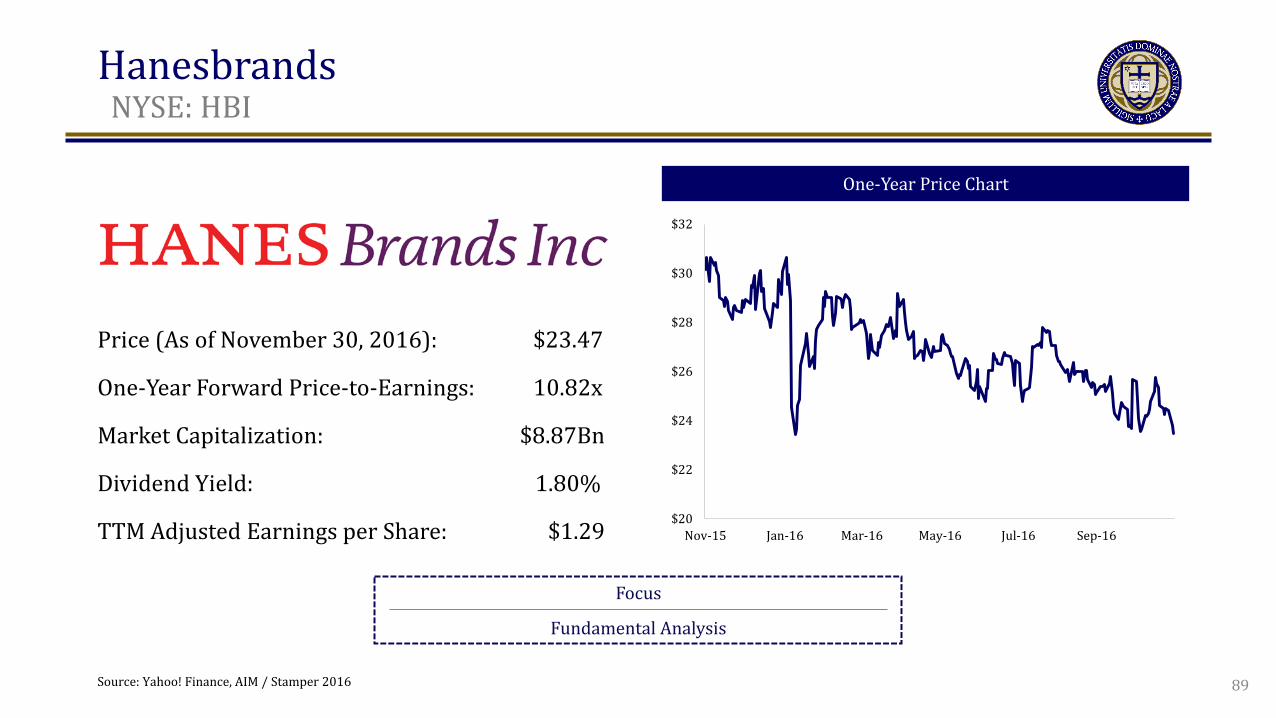

Price (As of November 30, 2016): $23.47

One-Year Forward Price-to-Earnings: 10.82x

Market Capitalization: $8.87Bn

Dividend Yield: 1.80%

TTM Adjusted Earnings per Share: $1.29

Hanesbrands t

NYSE: HBI

One-Year Price Chart

Focus

Fundamental Analysis

Source: Yahoo! Finance, AIM / Stamper 2016

$20

$22

$24

$26

$28

$30

$32

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16

89

Hanesbrands t

Fundamental Analysis

–

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

14.0x

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Accounts Receivable Turnover Inventory Turnover Accounts Payable Turnover

Adjusted Efficiency Ratios Accounts Payable Turnover Comparison

Source: Company Filings, S&P Capital IQ, AIM / Stamper 2016 Note: 2014 ratios due to restructuring in 2015

90

5.5x

8.8x

8.2x 6.1x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Hanesbrands L Brands Gap Gildan Activeware

Net Profit Comparison

8.6%

9.7%

4.6%

0%

2%

4%

6%

8%

10%

12%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Hanesbrands L Brands Gap

$0

$1

$2

$3

$4

$5

$6

$7

0%5%

10%15%20%25%30%35%40%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Net sales Net Profit Margin After-tax Operating Margin Gross Profit Margin

Sales and Margins (%, $Bn)

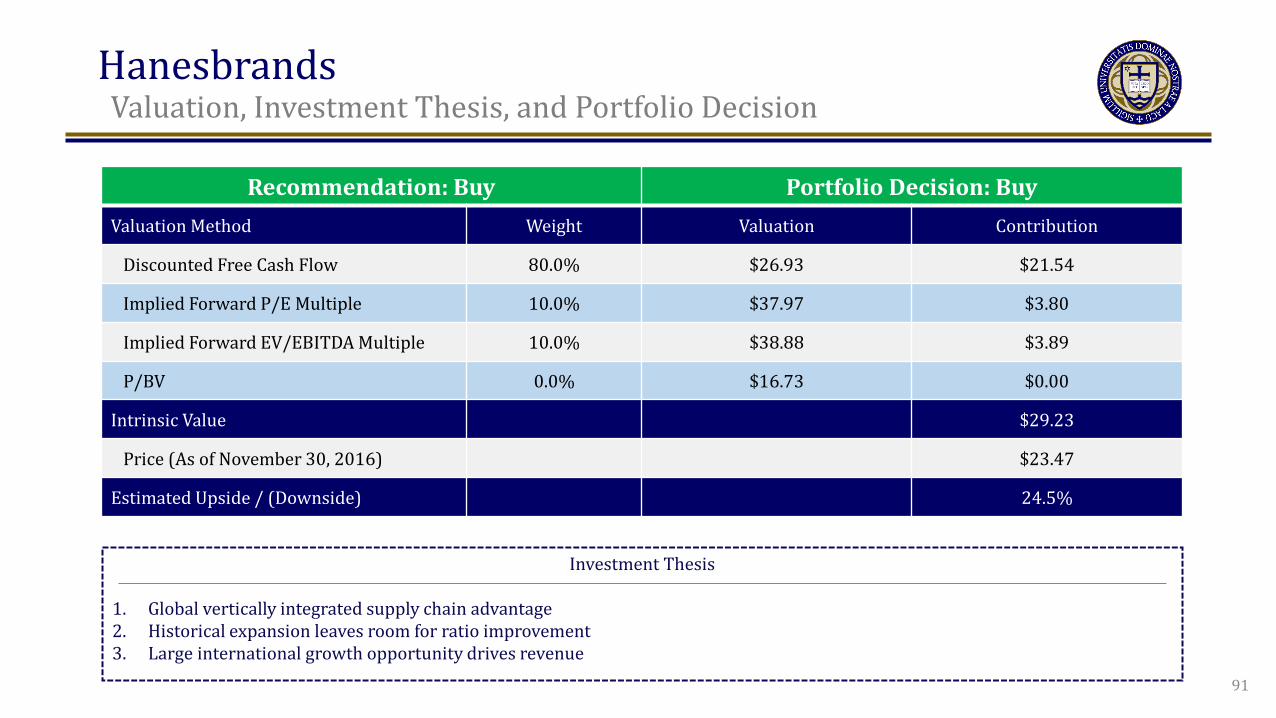

Hanesbrands t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Buy Portfolio Decision: Buy Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 80.0% $26.93 $21.54

Implied Forward P/E Multiple 10.0% $37.97 $3.80

Implied Forward EV/EBITDA Multiple 10.0% $38.88 $3.89

P/BV 0.0% $16.73 $0.00

Intrinsic Value $29.23

Price (As of November 30, 2016) $23.47

Estimated Upside / (Downside) 24.5%

Investment Thesis

1. Global vertically integrated supply chain advantage 2. Historical expansion leaves room for ratio improvement 3. Large international growth opportunity drives revenue

91

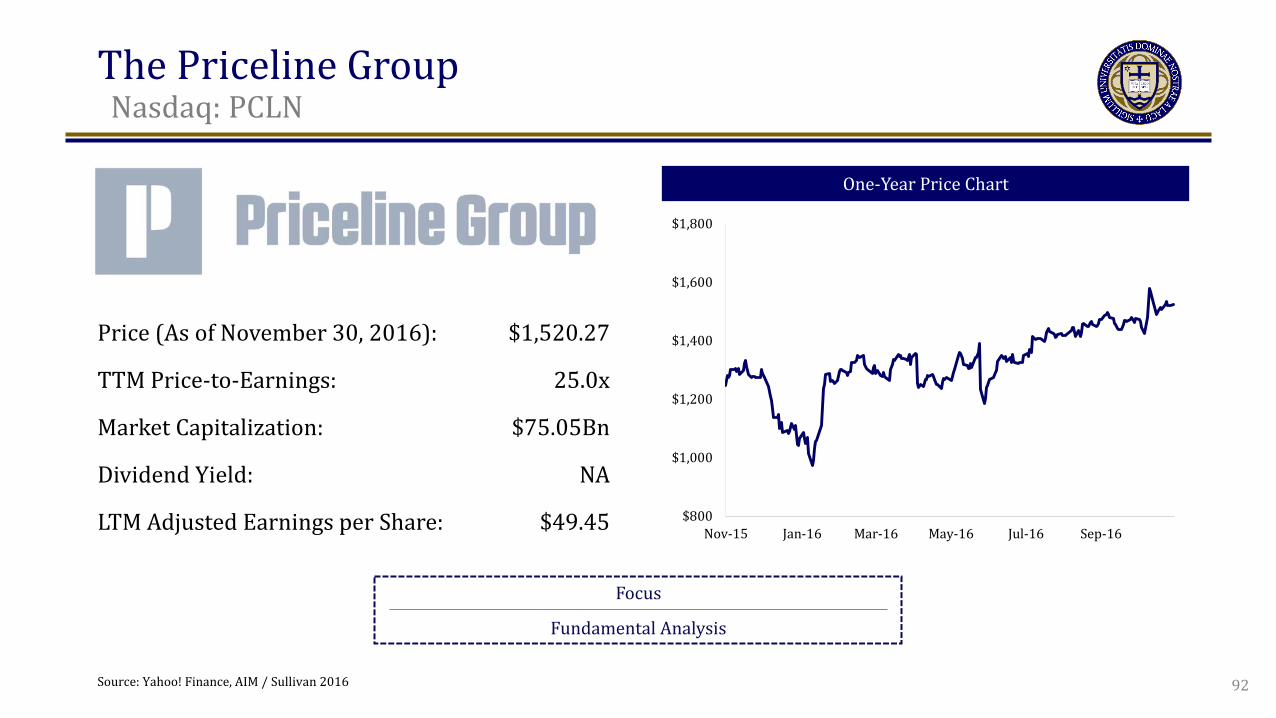

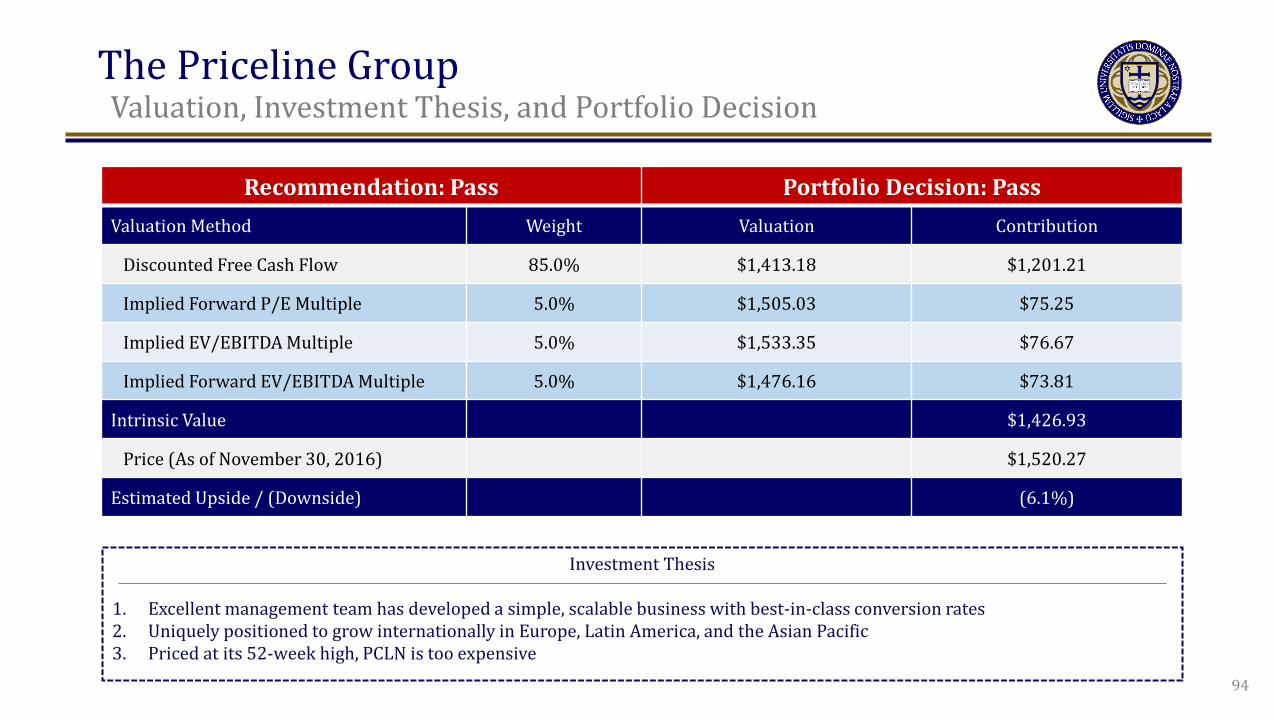

The Priceline Group t

Nasdaq: PCLN

One-Year Price Chart

Focus

Fundamental Analysis

$800

$1,000

$1,200

$1,400

$1,600

$1,800

Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16

Price (As of November 30, 2016): $1,520.27

TTM Price-to-Earnings: 25.0x

Market Capitalization: $75.05Bn

Dividend Yield: NA

LTM Adjusted Earnings per Share: $49.45

92 Source: Yahoo! Finance, AIM / Sullivan 2016

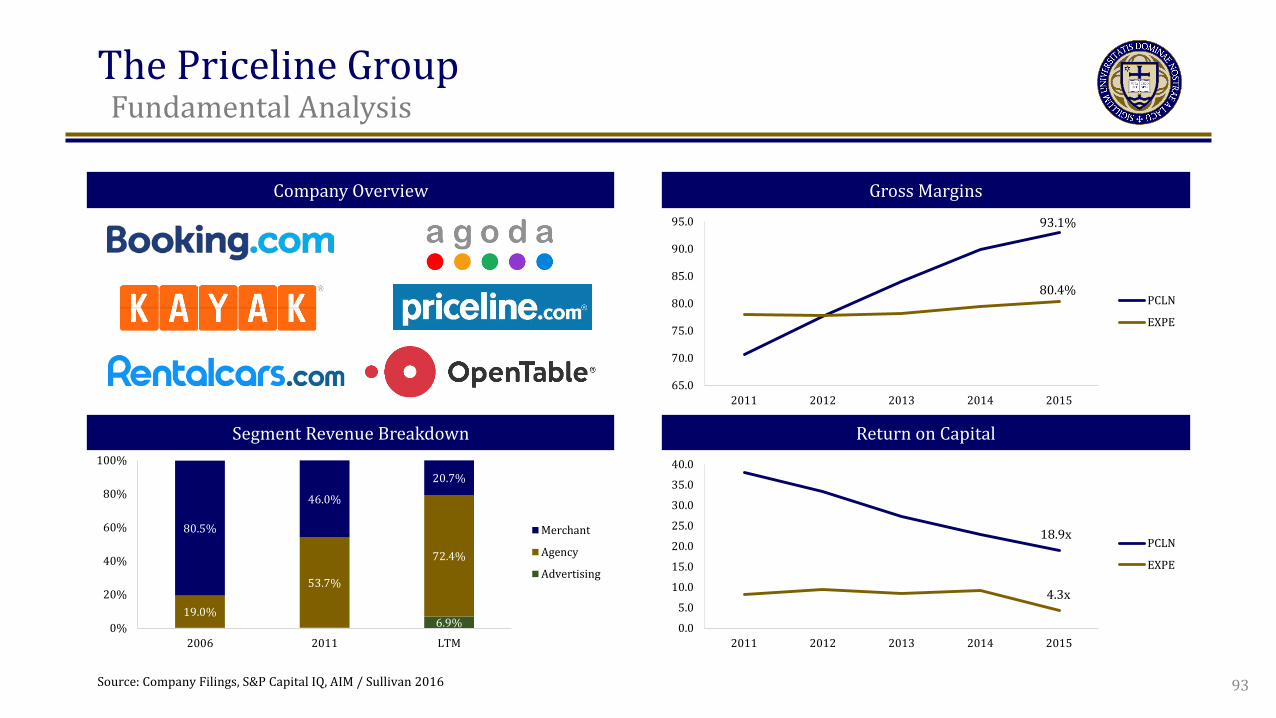

The Priceline Group t

Fundamental Analysis

Company Overview Gross Margins

Segment Revenue Breakdown Return on Capital

65.0

70.0

75.0

80.0

85.0

90.0

95.0

2011 2012 2013 2014 2015

PCLN

EXPE

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2011 2012 2013 2014 2015

PCLN

EXPE

6.9% 19.0%

53.7%

72.4%

80.5%

46.0%

20.7%

0%

20%

40%

60%

80%

100%

2006 2011 LTM

Merchant

Agency

Advertising

93.1%

80.4%

18.9x

4.3x

93 Source: Company Filings, S&P Capital IQ, AIM / Sullivan 2016

The Priceline Group t

Valuation, Investment Thesis, and Portfolio Decision

Recommendation: Pass Portfolio Decision: Pass Valuation Method Weight Valuation Contribution

Discounted Free Cash Flow 85.0% $1,413.18 $1,201.21

Implied Forward P/E Multiple 5.0% $1,505.03 $75.25

Implied EV/EBITDA Multiple 5.0% $1,533.35 $76.67

Implied Forward EV/EBITDA Multiple 5.0% $1,476.16 $73.81

Intrinsic Value $1,426.93

Price (As of November 30, 2016) $1,520.27

Estimated Upside / (Downside) (6.1%)

Investment Thesis

1. Excellent management team has developed a simple, scalable business with best-in-class conversion rates 2. Uniquely positioned to grow internationally in Europe, Latin America, and the Asian Pacific 3. Priced at its 52-week high, PCLN is too expensive

94

Portfolio Performance Historical Returns Against Benchmarks Risk-Adjusted Performance Attribution Analysis Best and Worst Performers Portfolio Additions and Deletions Finalized Portfolio

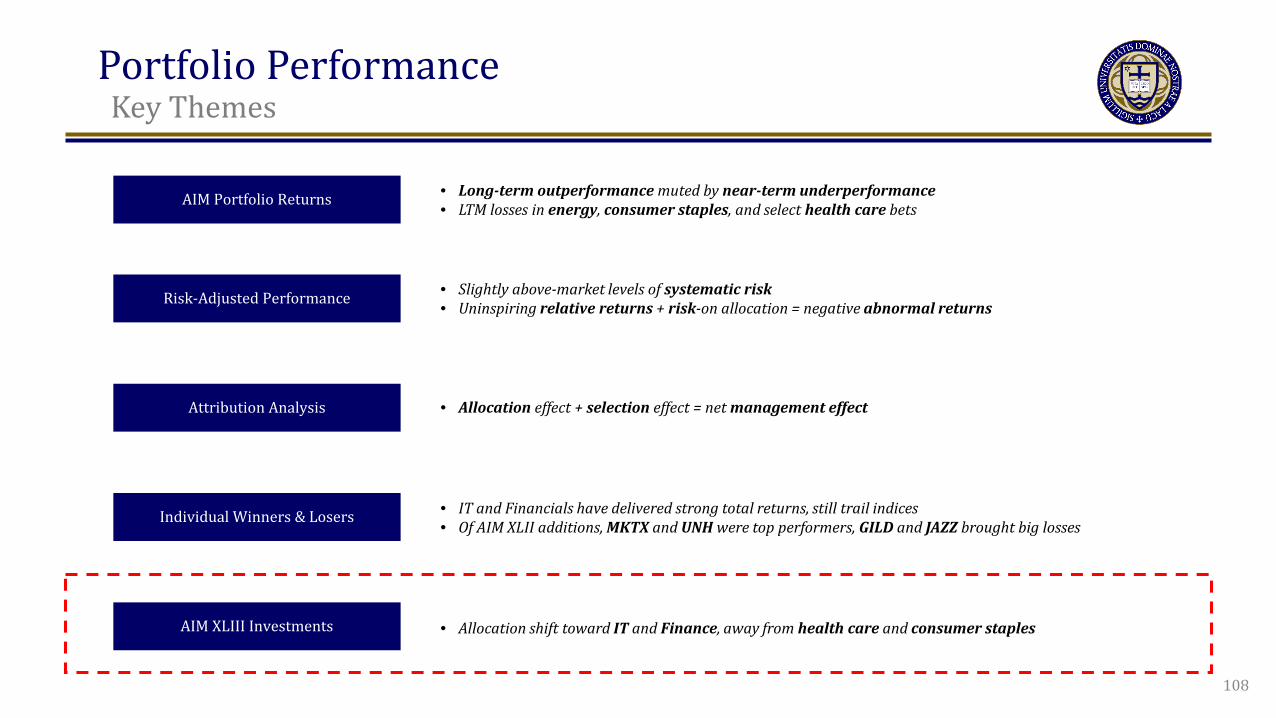

Portfolio Performance t

Key Themes

AIM Portfolio Returns

Risk-Adjusted Performance

Attribution Analysis

AIM XLIII Investments

• Long-term outperformance muted by near-term underperformance • LTM losses in energy, consumer staples, and select health care bets

• Allocation effect + selection effect = net management effect

• Allocation shift toward IT and Finance, away from health care and consumer staples

96

• Slightly above-market levels of systematic risk • Uninspiring relative returns + risk-on allocation = negative abnormal returns

Individual Winners & Losers • IT and Financials have delivered strong total returns, still trail indices • Of AIM XLII additions, MKTX and UNH were top performers, GILD and JAZZ brought big losses

Portfolio Performance t

Key Themes

AIM Portfolio Returns

Risk-Adjusted Performance

Attribution Analysis

AIM XLIII Investments

• Long-term outperformance muted by near-term underperformance • LTM losses in energy, consumer staples, and select health care bets

• Allocation effect + selection effect = net management effect

• Allocation shift toward IT and Finance, away from health care and consumer staples

97

• IT and Financials have delivered strong total returns, still trail indices • Of AIM XLII additions, MKTX and UNH were top performers, GILD and JAZZ brought big losses

• Slightly above-market levels of systematic risk • Uninspiring relative returns + risk-on allocation = negative abnormal returns

Individual Winners & Losers

Portfolio Performance t

Historical Returns Against Benchmarks

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

$10.00

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

AIM S&P 500 Russell 2000

$3.78

$8.52

$3.34

Cumulative Return of a $1.00 Investment January 1, 1996 to October 31, 2016

98 Source: BNY Mellon Statement, AIM / Marti 2016

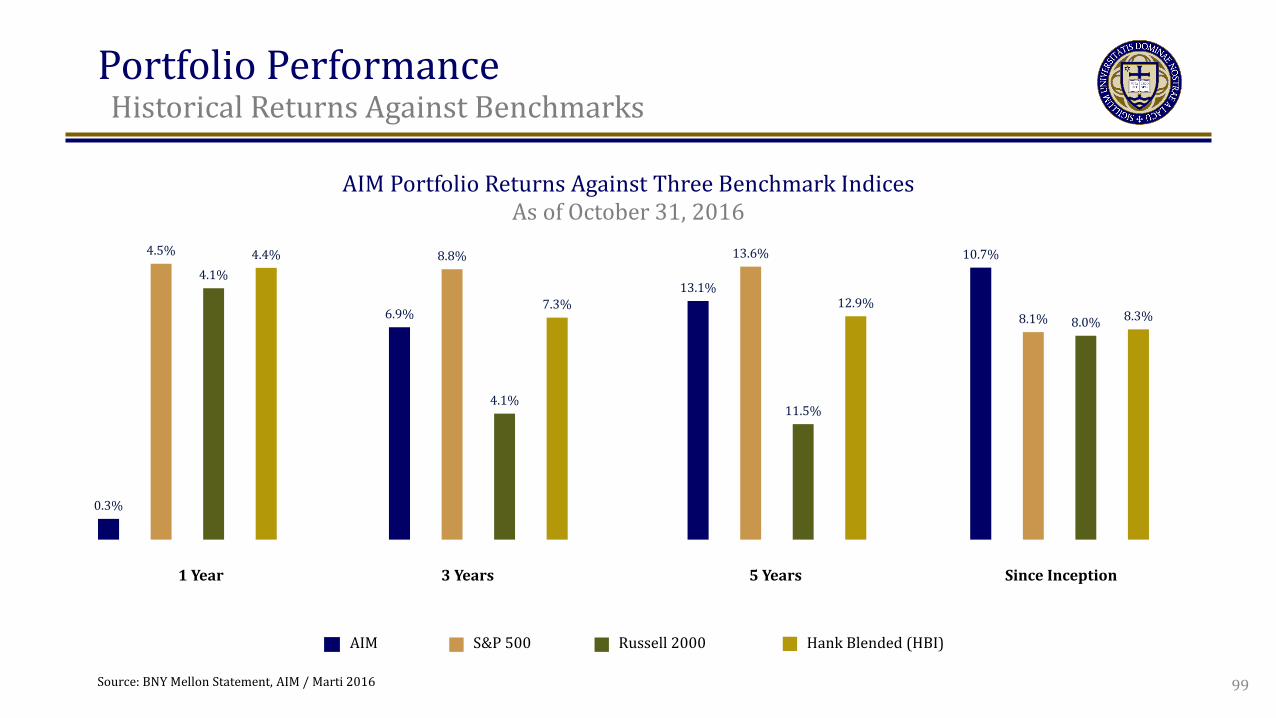

Portfolio Performance t

Historical Returns Against Benchmarks

AIM Portfolio Returns Against Three Benchmark Indices As of October 31, 2016

0.3%

4.5%

4.1% 4.4%

6.9%

8.8%

4.1%

7.3% 13.1%

13.6%

11.5%

12.9%

10.7%

8.1% 8.0% 8.3%

AIM S&P 500 Russell 2000 Hank Blended (HBI)

1 Year 3 Years 5 Years Since Inception

99 Source: BNY Mellon Statement, AIM / Marti 2016

Portfolio Performance t

Risk Profile

Beta: Systematic Risk Relative to Three Benchmark Indices As of October 31, 2016

1.13 1.12 1.08

0.65 0.69 0.71

0.93

1.02 1.00

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1 Year 3 Years 5 Years

AIM vs. S&P AIM vs. Russell AIM vs. HBI

100 Source: BNY Mellon Statement, AIM / Marti 2016

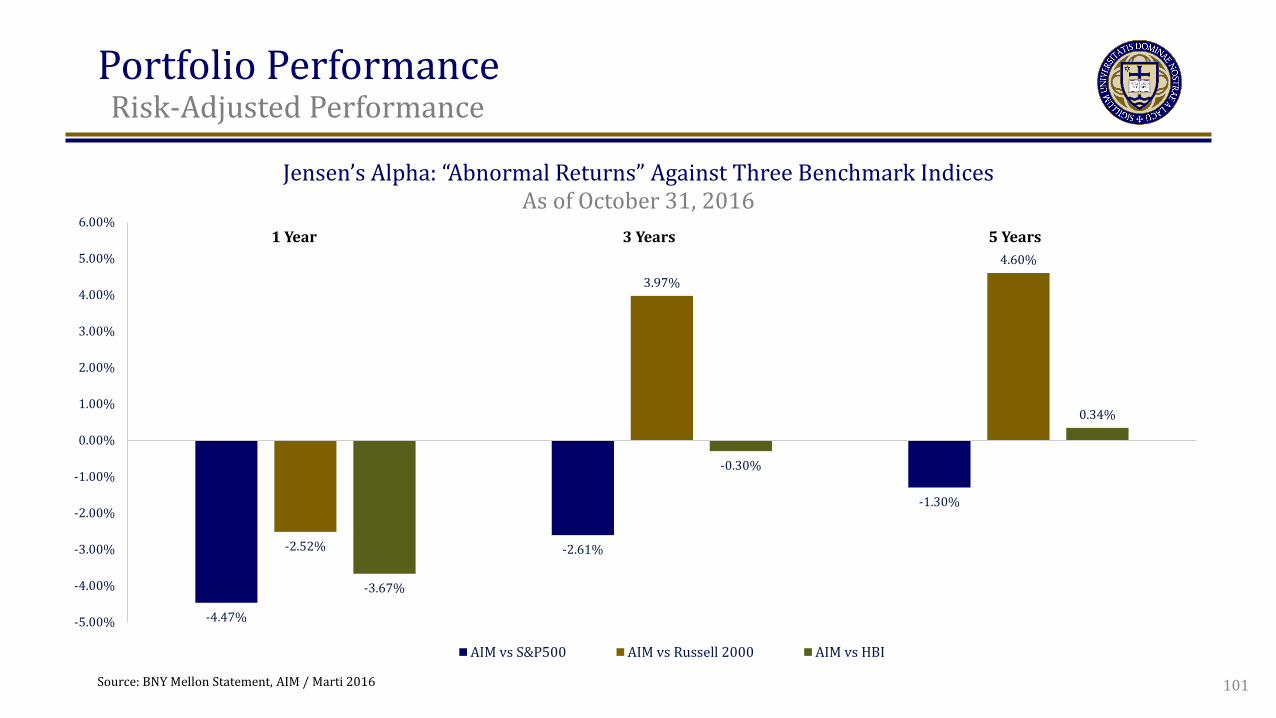

Portfolio Performance t

Risk-Adjusted Performance

Jensen’s Alpha: “Abnormal Returns” Against Three Benchmark Indices As of October 31, 2016

-4.47%

-2.61%

-1.30%

-2.52%

3.97%

4.60%

-3.67%

-0.30%

0.34%

-5.00%

-4.00%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

AIM vs S&P500 AIM vs Russell 2000 AIM vs HBI

1 Year 3 Years 5 Years

101 Source: BNY Mellon Statement, AIM / Marti 2016

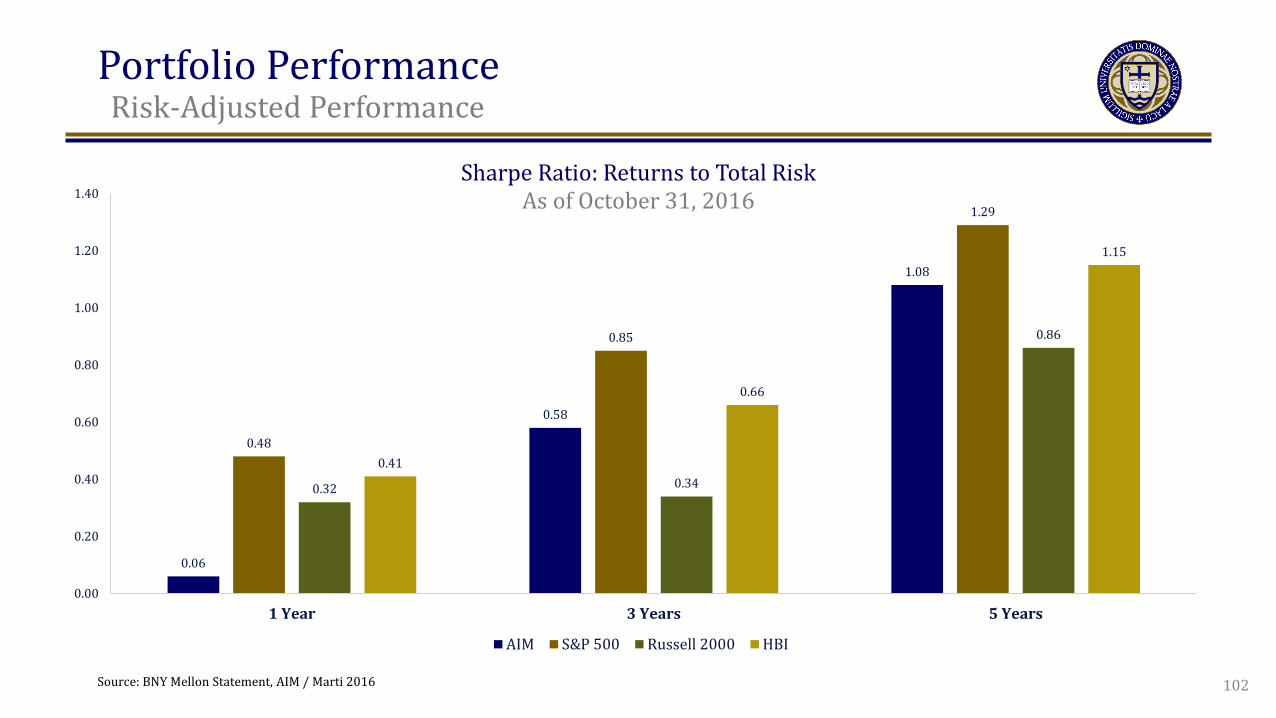

Portfolio Performance t

Risk-Adjusted Performance

Sharpe Ratio: Returns to Total Risk As of October 31, 2016

0.06

0.58

1.08

0.48

0.85

1.29

0.32 0.34

0.86

0.41

0.66

1.15

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1 Year 3 Years 5 Years

AIM S&P 500 Russell 2000 HBI

102 Source: BNY Mellon Statement, AIM / Marti 2016

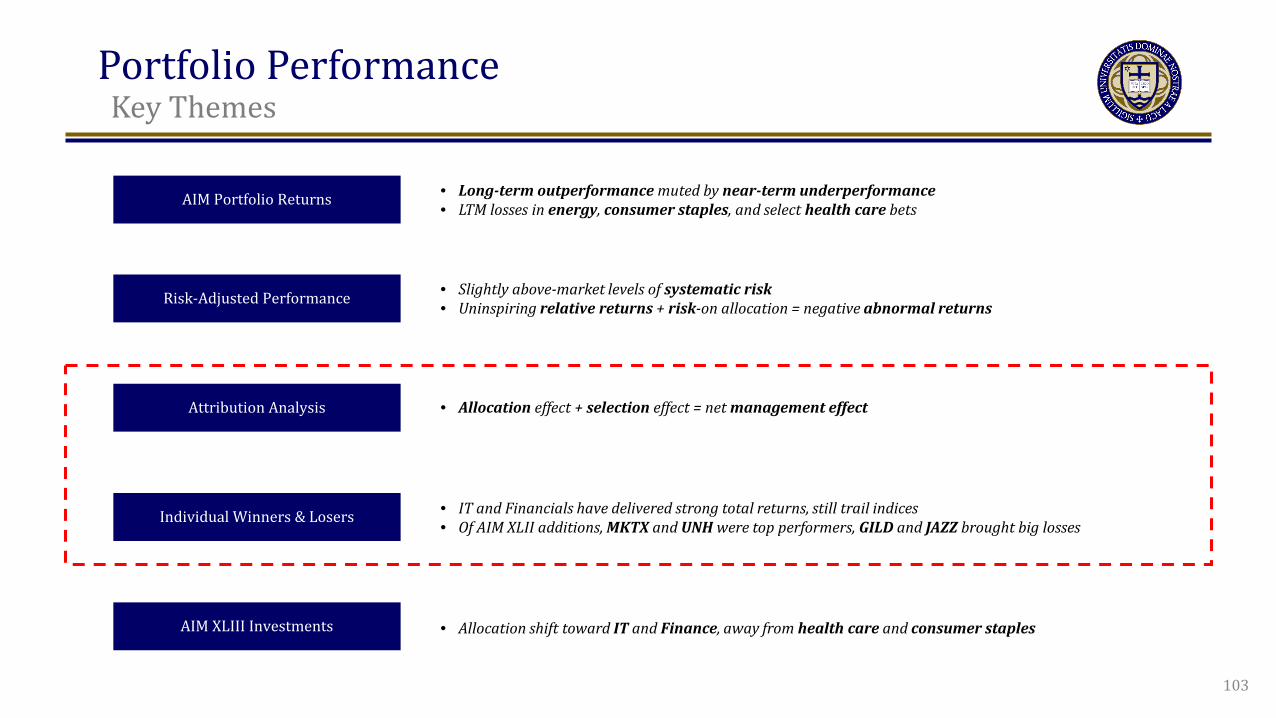

Portfolio Performance t

Key Themes

AIM Portfolio Returns

Risk-Adjusted Performance

Attribution Analysis

AIM XLIII Investments

• Long-term outperformance muted by near-term underperformance • LTM losses in energy, consumer staples, and select health care bets

• Allocation effect + selection effect = net management effect

• Allocation shift toward IT and Finance, away from health care and consumer staples

103

• IT and Financials have delivered strong total returns, still trail indices • Of AIM XLII additions, MKTX and UNH were top performers, GILD and JAZZ brought big losses

• Slightly above-market levels of systematic risk • Uninspiring relative returns + risk-on allocation = negative abnormal returns

Individual Winners & Losers

Portfolio Performance t

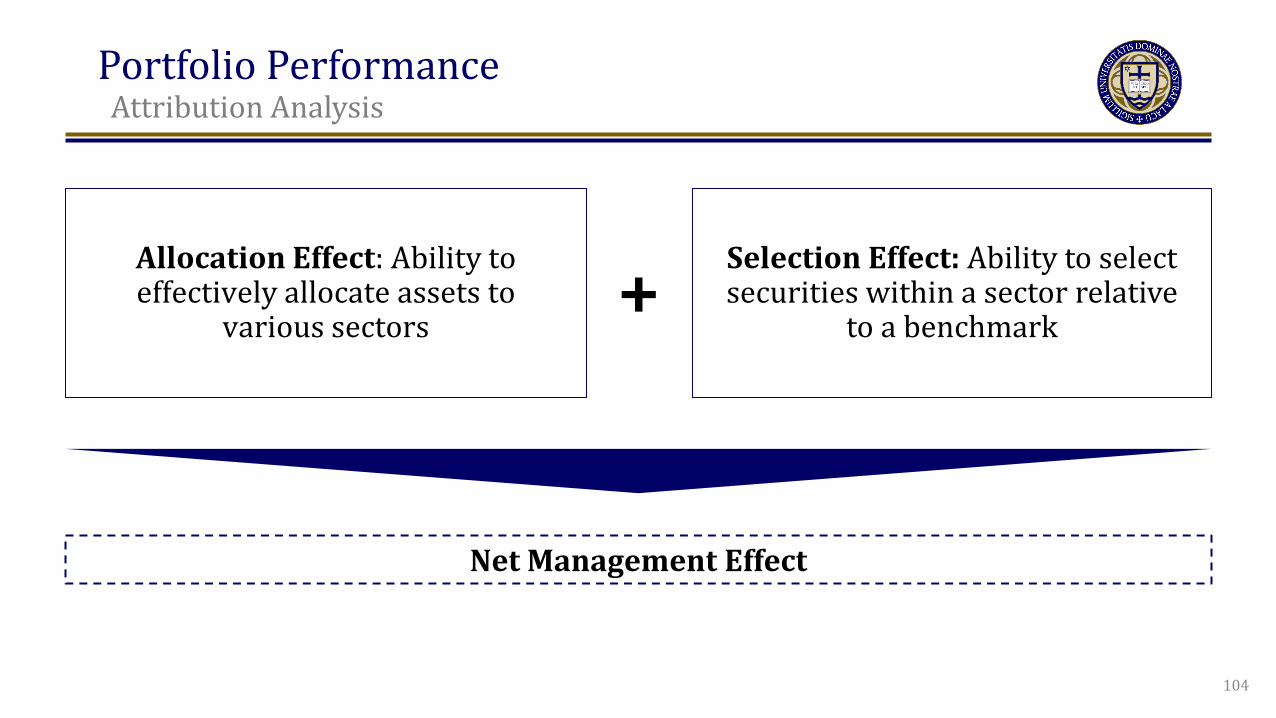

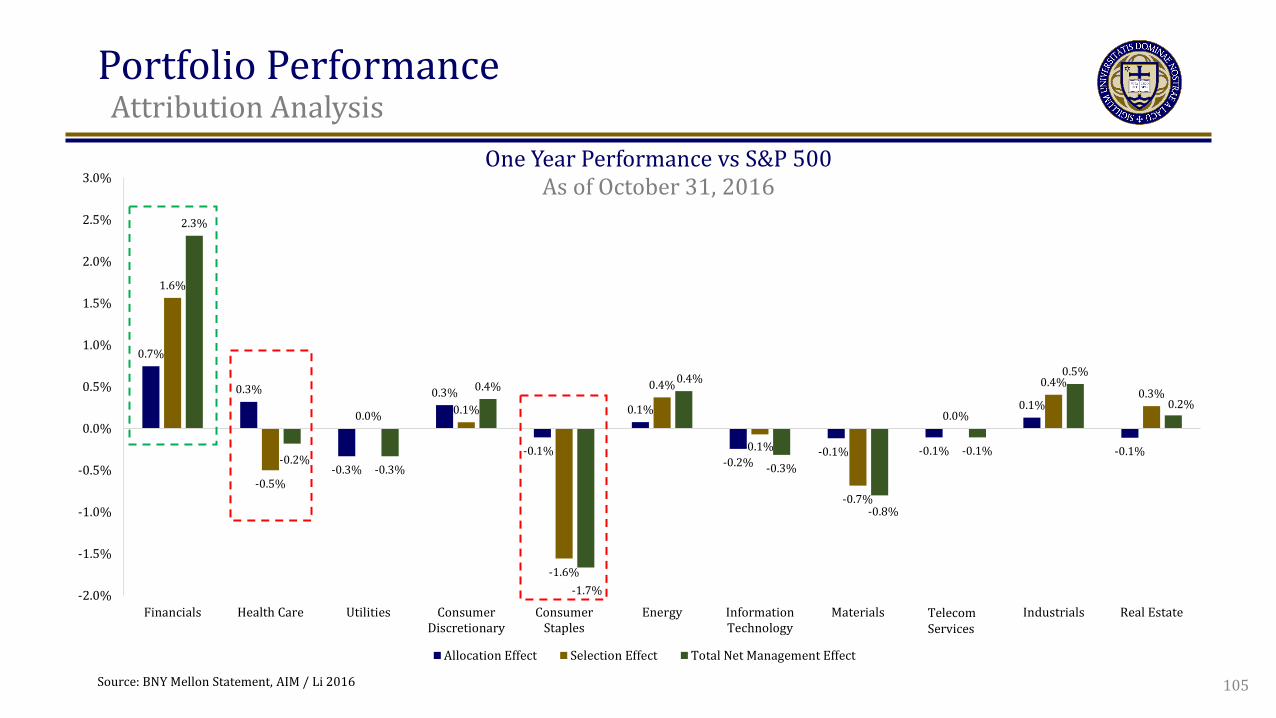

Attribution Analysis

Net Management Effect

104

Allocation Effect: Ability to effectively allocate assets to

various sectors

Selection Effect: Ability to select securities within a sector relative

to a benchmark +

Portfolio Performance t

Attribution Analysis

0.7%

0.3%

-0.3%

0.3%

-0.1%

0.1%

-0.2% -0.1% -0.1%

0.1%

-0.1%

1.6%

-0.5%

0.0% 0.1%

-1.6%

0.4%

-0.1%

-0.7%

0.0%

0.4% 0.3%

2.3%

-0.2% -0.3%

0.4%

-1.7%

0.4%

-0.3%

-0.8%

-0.1%

0.5%

0.2%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Financials Health Care Utilities ConsumerDiscretionary

ConsumerStaples

Energy InformationTechnology

Materials TelecommServices

Industrials Real Estate

Allocation Effect Selection Effect Total Net Management Effect

105

One Year Performance vs S&P 500 As of October 31, 2016

Telecom Services

Source: BNY Mellon Statement, AIM / Li 2016

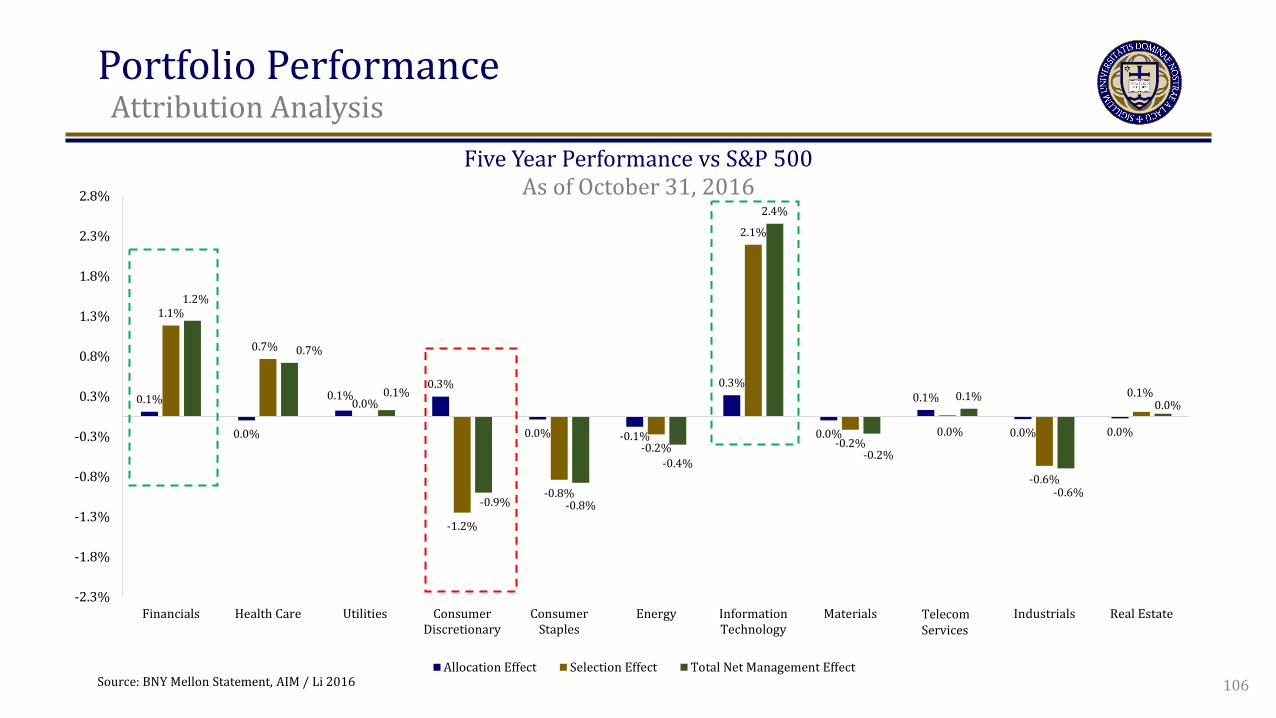

Portfolio Performance t

Attribution Analysis

0.1%

0.0%

0.1% 0.3%

0.0% -0.1%

0.3%

0.0%

0.1%

0.0% 0.0%

1.1%

0.7%

0.0%

-1.2%

-0.8%

-0.2%

2.1%

-0.2% 0.0%

-0.6%

0.1%

1.2%

0.7%

0.1%

-0.9% -0.8%

-0.4%

2.4%

-0.2%

0.1%

-0.6%

0.0%

-2.3%

-1.8%

-1.3%

-0.8%

-0.3%

0.3%

0.8%

1.3%

1.8%

2.3%

2.8%

Financials Health Care Utilities ConsumerDiscretionary

ConsumerStaples

Energy InformationTechnology

Materials TelecommServices

Industrials Real Estate

Allocation Effect Selection Effect Total Net Management Effect

Five Year Performance vs S&P 500 As of October 31, 2016

Telecom Services

106 Source: BNY Mellon Statement, AIM / Li 2016

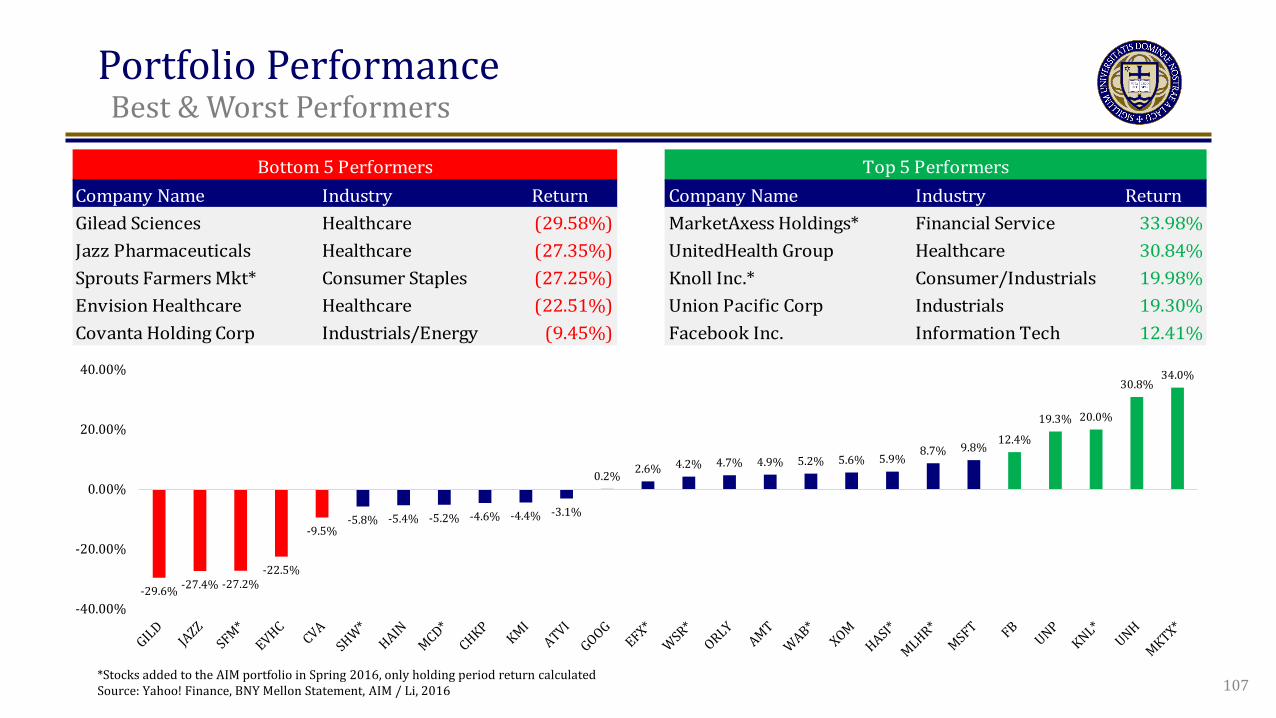

Portfolio Performance t

Best & Worst Performers

Company Name Industry Return Company Name Industry ReturnGilead Sciences Healthcare (29.58%) MarketAxess Holdings* Financial Service 33.98%Jazz Pharmaceuticals Healthcare (27.35%) UnitedHealth Group Healthcare 30.84%Sprouts Farmers Mkt* Consumer Staples (27.25%) Knoll Inc.* Consumer/Industrials 19.98%Envision Healthcare Healthcare (22.51%) Union Pacific Corp Industrials 19.30%Covanta Holding Corp Industrials/Energy (9.45%) Facebook Inc. Information Tech 12.41%

Bottom 5 Performers Top 5 Performers

-29.6% -27.4% -27.2% -22.5%

-9.5% -5.8% -5.4% -5.2% -4.6% -4.4% -3.1%

0.2% 2.6% 4.2% 4.7% 4.9% 5.2% 5.6% 5.9% 8.7% 9.8% 12.4%

19.3% 20.0%

30.8% 34.0%

-40.00%

-20.00%

0.00%

20.00%

40.00%

107 *Stocks added to the AIM portfolio in Spring 2016, only holding period return calculated Source: Yahoo! Finance, BNY Mellon Statement, AIM / Li, 2016

Portfolio Performance t

Key Themes

AIM Portfolio Returns

Risk-Adjusted Performance

Attribution Analysis

AIM XLIII Investments

• Long-term outperformance muted by near-term underperformance • LTM losses in energy, consumer staples, and select health care bets

• Allocation effect + selection effect = net management effect

• Allocation shift toward IT and Finance, away from health care and consumer staples

108

• IT and Financials have delivered strong total returns, still trail indices • Of AIM XLII additions, MKTX and UNH were top performers, GILD and JAZZ brought big losses

• Slightly above-market levels of systematic risk • Uninspiring relative returns + risk-on allocation = negative abnormal returns

Individual Winners & Losers

Financials, 9%

Health Care, 14%

Consumer Discretionary, 11%

Consumer Staples, 6% Energy, 8%

Information Technology, 20%

Materials, 3%

Industrials, 21% Real Estate, 8%

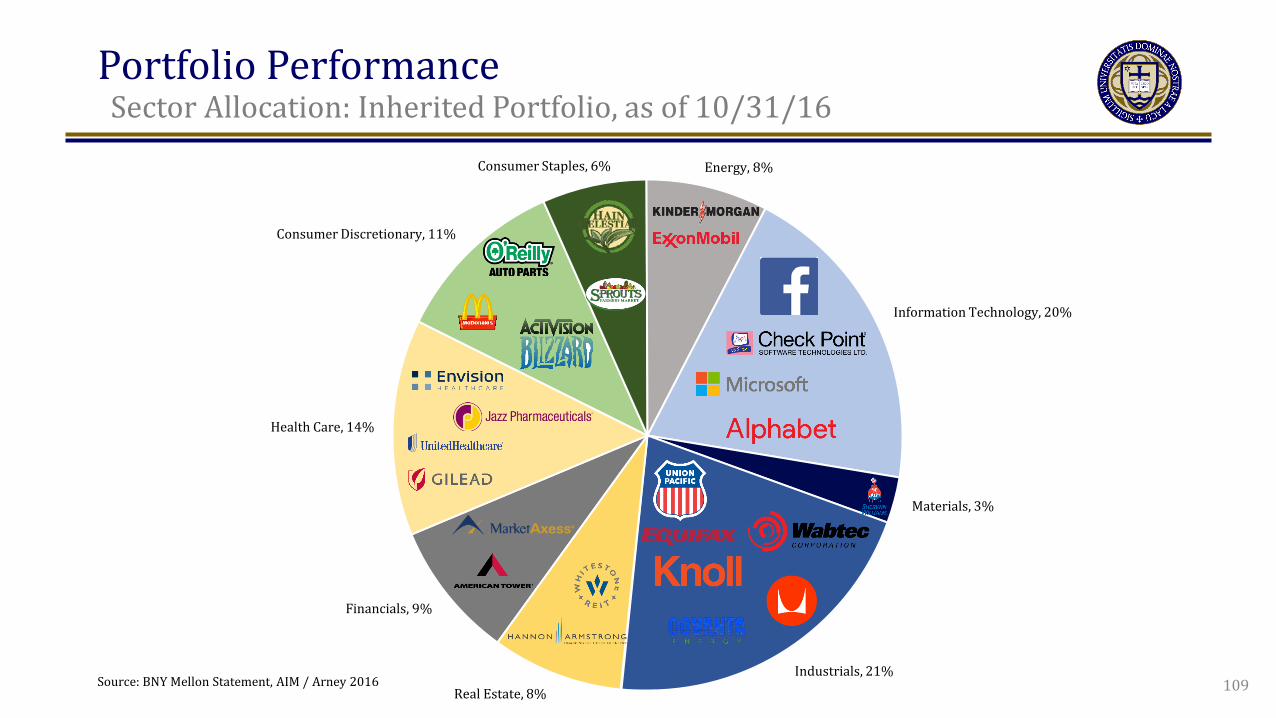

Portfolio Performance t

Sector Allocation: Inherited Portfolio, as of 10/31/16

109 Source: BNY Mellon Statement, AIM / Arney 2016

Portfolio Performance t

Additions and Deletions

Hanes Brands Under Armour Total System Services Align Technology Rockwell Collins Verisk Analytics Infinera Corp Intel Corp Nvidia Verisign Mosaic Co. Digital Reality REIT

McDonald's Corp O'Reilly Automotive Hain Celestial Group Sprouts Farmers Mkt Envision Healthcare Jazz Pharmaceuticals UnitedHealth Group Covanta Holding Corp Knoll Inc. Union Pacific Corp Check Point Software Sherwin-Williams Hannon Armstrong Whitestone REIT

Consumer Discretionary Consumer Discretionary Financials Health Care Industrials Industrials Information Technology Information Technology Information Technology Information Technology Materials Real Estate

Consumer Discretionary Consumer Discretionary Consumer Staples Consumer Staples Health Care Health Care Health Care Industrials Industrials Industrials Information Technology Materials Real Estate Real Estate

Portfolio Additions Portfolio Deletions

Company Industry Company Industry

110 Source: BNY Mellon Statement, AIM / Arney 2016

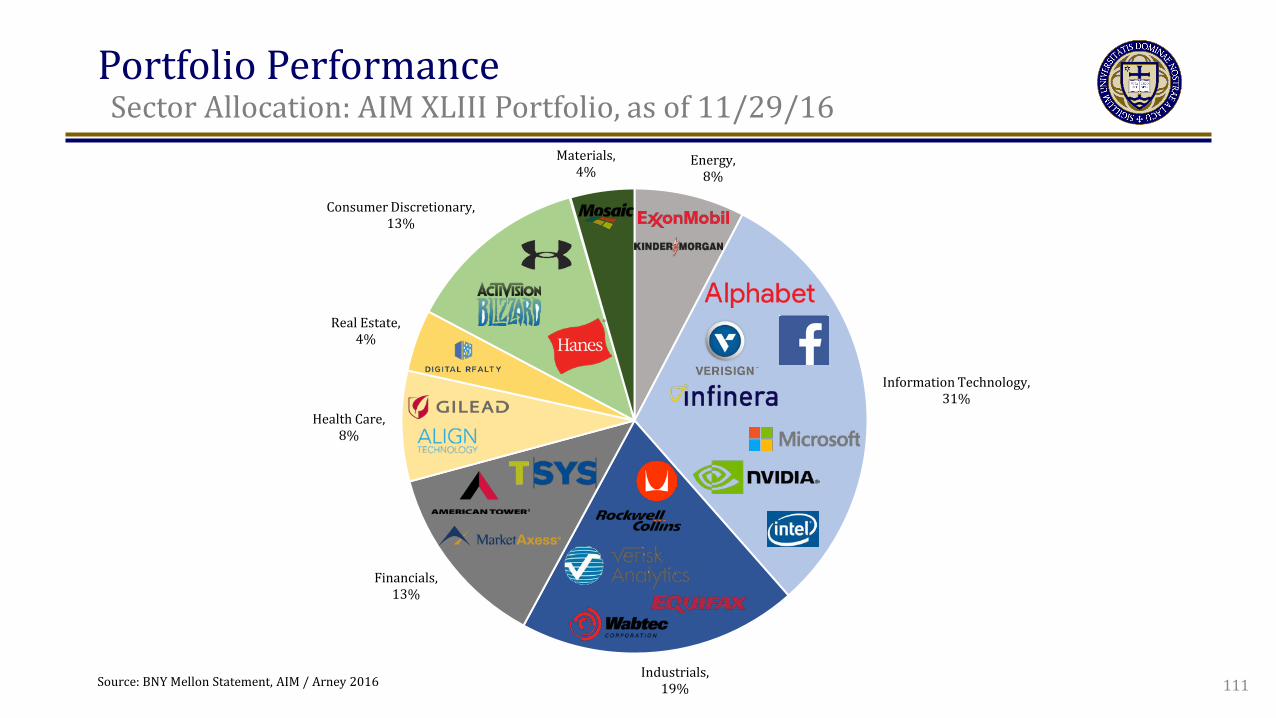

Energy, 8%

Information Technology, 31%

Industrials, 19%

Financials, 13%

Health Care, 8%

Real Estate, 4%

Consumer Discretionary, 13%

Materials, 4%

Portfolio Performance t

Sector Allocation: AIM XLIII Portfolio, as of 11/29/16

111 Source: BNY Mellon Statement, AIM / Arney 2016

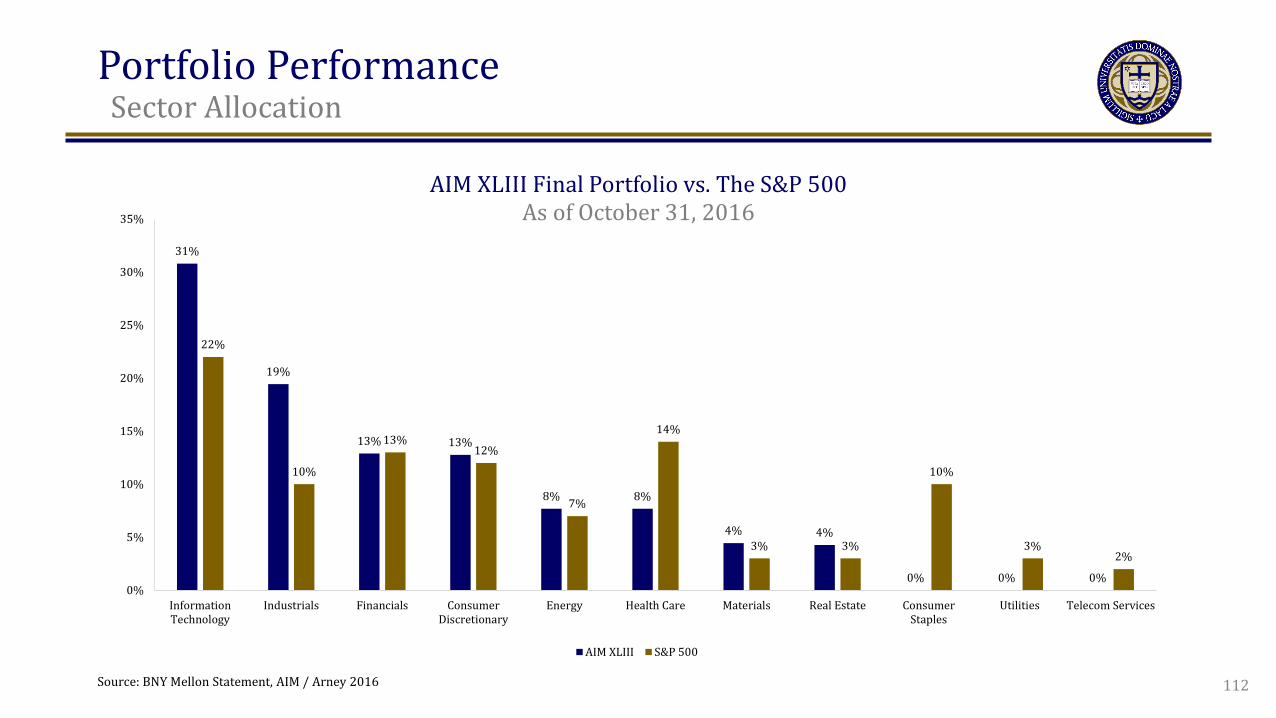

Portfolio Performance t

Sector Allocation

112

31%

19%

13% 13%

8% 8%

4% 4%

0% 0% 0%

22%

10%

13% 12%

7%

14%

3% 3%

10%

3% 2%

0%

5%

10%

15%

20%

25%

30%

35%

InformationTechnology

Industrials Financials ConsumerDiscretionary

Energy Health Care Materials Real Estate ConsumerStaples

Utilities Telecom Services

AIM XLIII S&P 500

AIM XLIII Final Portfolio vs. The S&P 500 As of October 31, 2016

Source: BNY Mellon Statement, AIM / Arney 2016

AIM XLIII Review Guest Speakers San Francisco Trip Website & Newsletter Concluding Remarks

AIM XLIII Review t

Guest Speakers

• Dave Baram – Founding Partner, VMG Partners

• Ted Weschler – Investment Manager, Berkshire Hathaway

• Kristen Collett-Schmitt – Professor, Finance, University of Notre Dame

• Tom Digenan – Managing Director & Head of the U.S. Intrinsic Value Equity, UBS

• Scott Malpass – CIO, University of Notre Dame

114

AIM XLIII Review t

San Francisco Trip

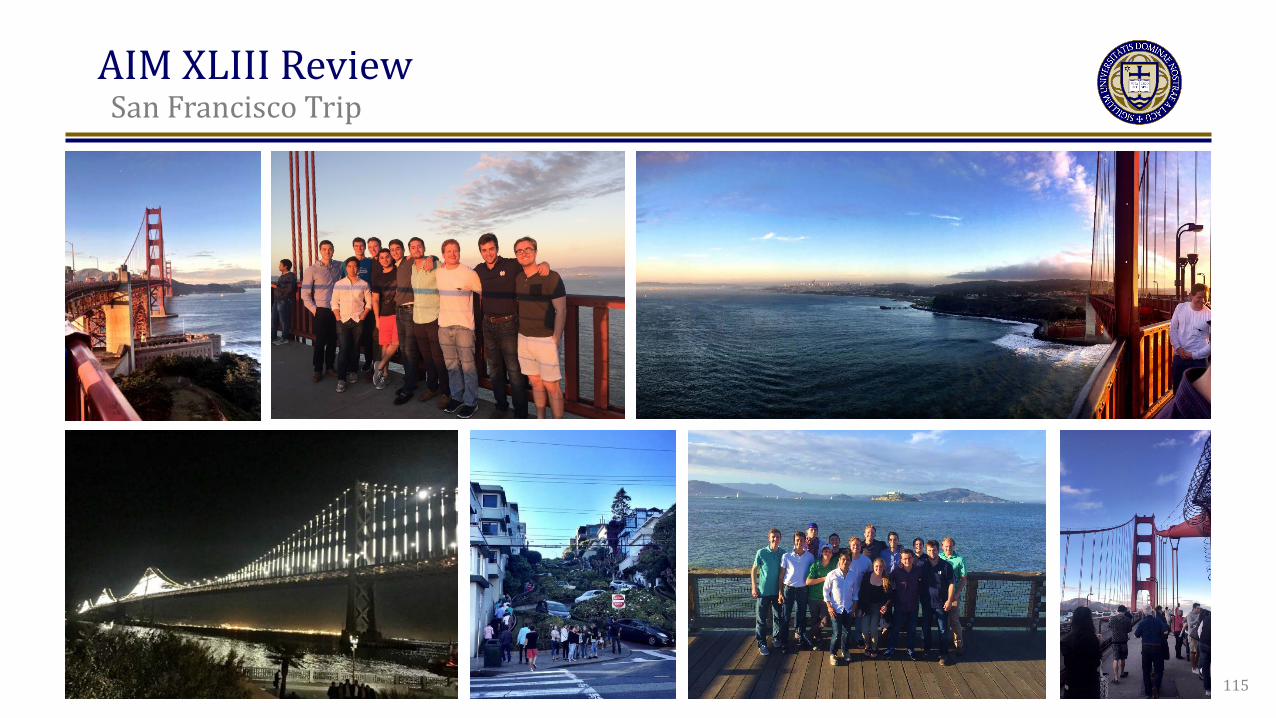

115

AIM XLIII Review t

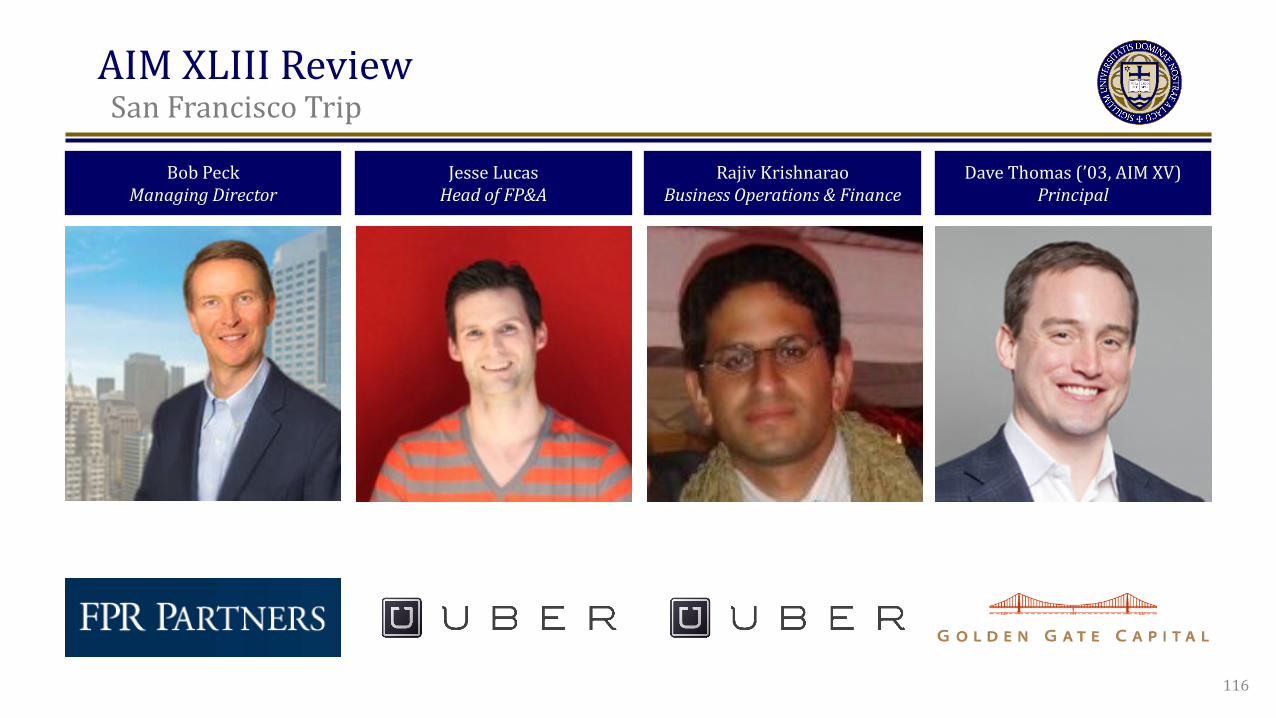

San Francisco Trip

Bob Peck Managing Director

Jesse Lucas Head of FP&A

Rajiv Krishnarao Business Operations & Finance

Dave Thomas (’03, AIM XV) Principal

N/A

116

AIM XLIII Review t

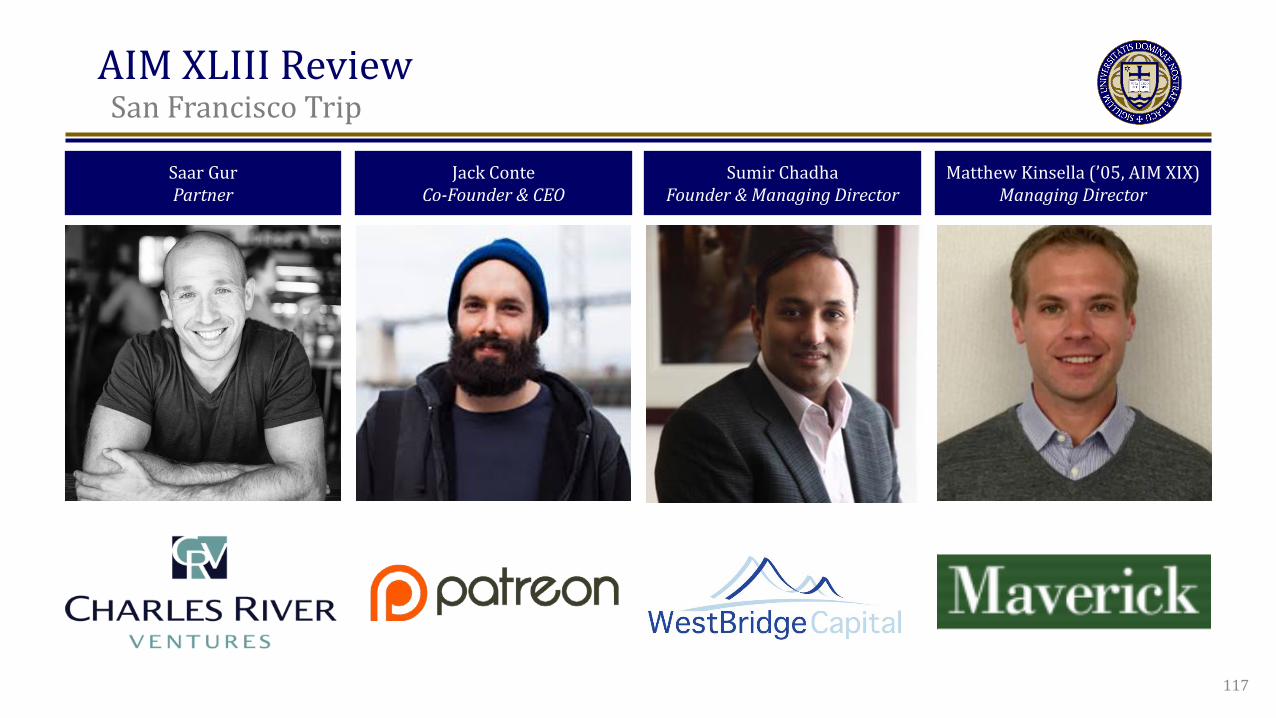

San Francisco Trip

Saar Gur Partner

Jack Conte Co-Founder & CEO

Sumir Chadha Founder & Managing Director

Matthew Kinsella (’05, AIM XIX) Managing Director

117

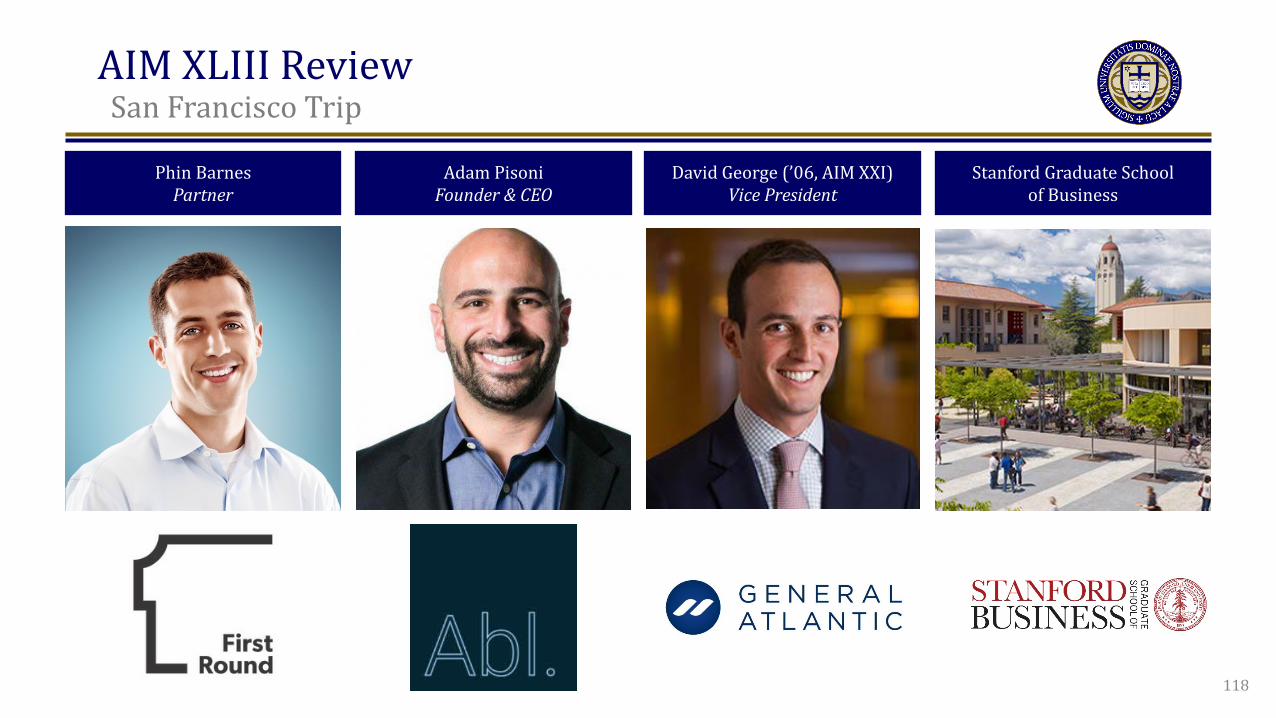

AIM XLIII Review t

San Francisco Trip

Phin Barnes Partner

Adam Pisoni Founder & CEO

David George (’06, AIM XXI) Vice President

Stanford Graduate School of Business

118

AIM XLIII Review t

Website & Newsletter

Newsletter AIM Website: aim.nd.edu

• AIM course description and history