1.14 Assets

12

1.14 ASSETS

-

Upload

vce-accounting-michael-allison -

Category

Education

-

view

55 -

download

2

Transcript of 1.14 Assets

1.14 ASSETS

Video of this presentation at…

YouTube Channel for VCE Accounting

© Michael Allison. Author’s permission required for external use.

1.14 ASSETS

Assets

Liabilities

Owner’s Equity

Revenues

Elements of Accounting

Expenses

© Michael Allison. Author’s permission required for external use.

Assets

Definition:

An asset is:

1. A resource controlled by the entity

2. As a result of past events (transactions)

3. From which future economic benefits are expected to flow to the entity

1.14 ASSETS

© Michael Allison. Author’s permission required for external use.

Assets

Resources controlled by the entity:

The resource must be under the control of the fi rm , i.e. the fi rm decides how and when it is used and not someone else

E.g. Jack owns a small business – his brother has lent him the use of his delivery van to use in the business, valued at $50,000

Is this an Asset of the business?

1.14 ASSETS

$50,000 No – the business does NOT

have an Asset

The business (or Jack) does not control the resource – the van belongs to his brother

The brother can make decisions about the van – not the business, e.g.

Sel l the van

Put new tyres of the van

© Michael Allison. Author’s permission required for external use.

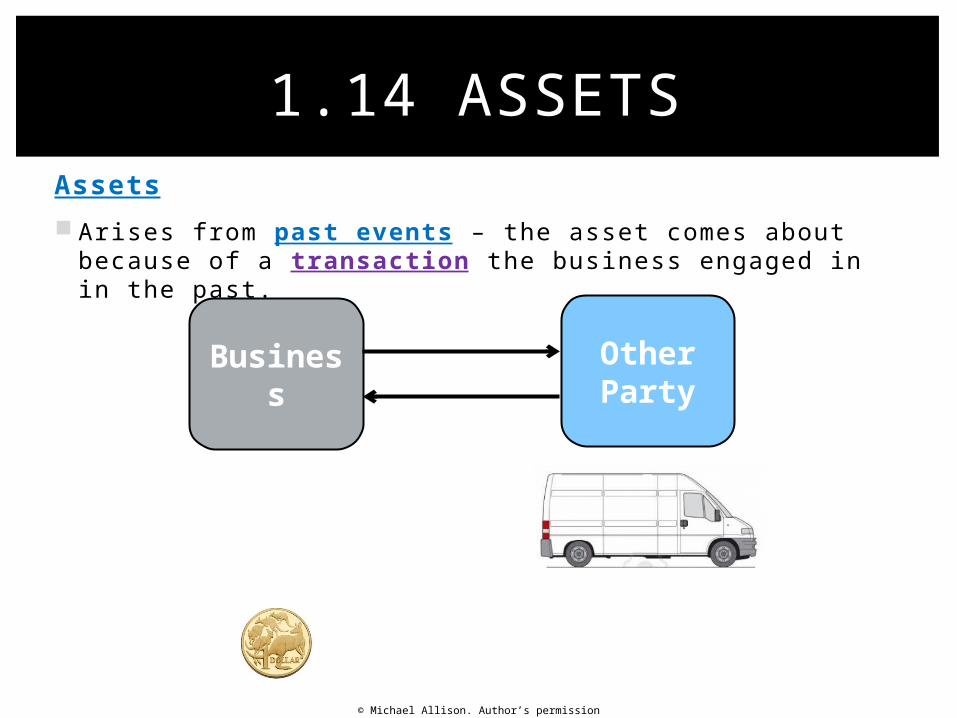

Assets

Arises from past events – the asset comes about because of a transaction the business engaged in in the past.

1.14 ASSETS

Business

Other Party

© Michael Allison. Author’s permission required for external use.

Assets

Will provide future economic benefi ts

The resource must be capable of generating some sort of economic gain for the fi rm in the future.

There must be some sort of benefi t that is yet to be received.

Business

Future economic benefit

1.14 ASSETS

© Michael Allison. Author’s permission required for external use.

Assets

The future economic benefi t provided by an asset can be cash…

Example: a fi rm has a debtor owing $1,000

Business

Future economic benefit

When the debtor pays the business, the economic benefit flowing into the business will be money…

1.14 ASSETS

© Michael Allison. Author’s permission required for external use.

Assets

The future economic benefi t provided by an asset is not always cash…

Example: a fi rm has a delivery vehicle valued at $30,000

Business

Future economic benefit

The economic benefit provided by the vehicle will be the ability to make deliveries to customers in the future

1.14 ASSETS

© Michael Allison. Author’s permission required for external use.

Assets

The future economic benefi t provided by an asset is not always cash…

Example: a fi rm prepaid $1,200 of insurance for 2015…

Business

Future economic benefit

The economic benefit provided during the rest of 2015 is insurance protection in the event of an emergency

Insurance protection

1.14 ASSETS

© Michael Allison. Author’s permission required for external use.

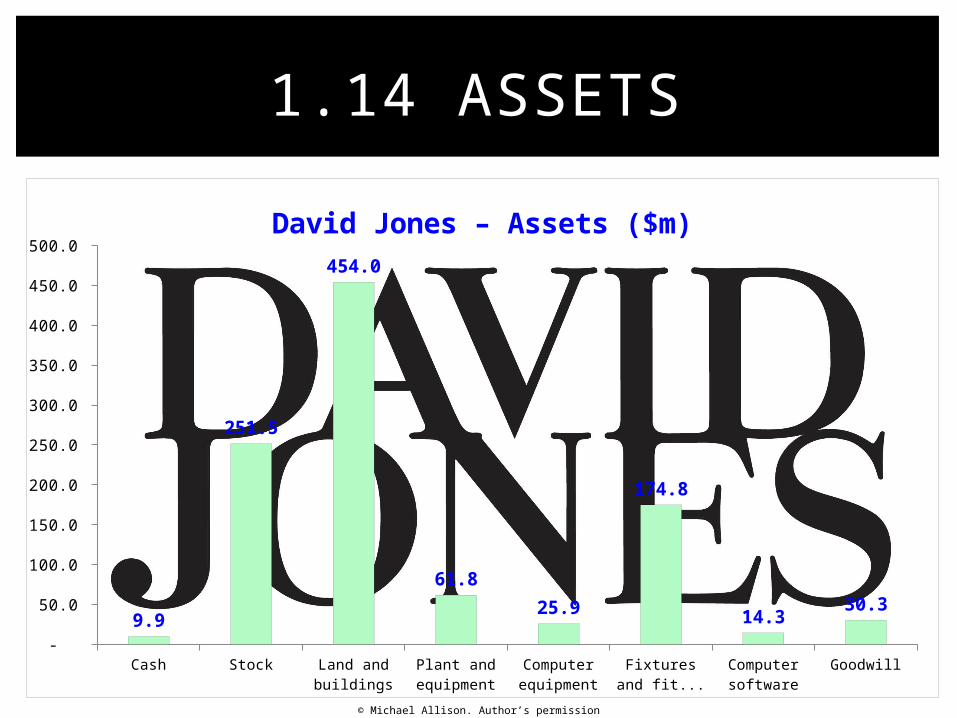

Cash Stock Land and buildings

Plant and equipment

Computer equipment

Fixtures and fittings

Computer software

Goodwill -

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

450.0

500.0

9.9

251.5

454.0

61.8

25.9

174.8

14.3 30.3

David Jones – Assets ($m)

1.14 ASSETS

© Michael Allison. Author’s permission required for external use.

TASK

In-class Homework

Cambridge Exercise 1.6 - Assets X

![Скачать [1.14 MB]](https://static.fdocuments.net/doc/165x107/58a174791a28ab384d8c047a/-114-mb.jpg)