1. Domestic transactions - Transfer Pricing Inspired by – Apex court ruling – Glaxo Smithkline...

40

1

-

Upload

primrose-parsons -

Category

Documents

-

view

219 -

download

0

Transcript of 1. Domestic transactions - Transfer Pricing Inspired by – Apex court ruling – Glaxo Smithkline...

11

Domestic transactions - Transfer Pricing

Inspired by – Apex court ruling – Glaxo Smithkline (2010) 195 Taxman 35 (SC):Inspired by – Apex court ruling – Glaxo Smithkline (2010) 195 Taxman 35 (SC):

• we are of the view that certain provisions of the Act, like section 40A(2) and section 80-we are of the view that certain provisions of the Act, like section 40A(2) and section 80-IA(10), need to be amended empowering the Assessing Officer to make adjustments to the IA(10), need to be amended empowering the Assessing Officer to make adjustments to the income declared by the assessee having regard to the fair market value of the transactions income declared by the assessee having regard to the fair market value of the transactions between the related parties. The Assessing Officer may thereafter apply any of the between the related parties. The Assessing Officer may thereafter apply any of the generally accepted methods of determination of arm’s length price, including the methods generally accepted methods of determination of arm’s length price, including the methods provided under Transfer Pricing Regulations. However, in a number of matters, we find provided under Transfer Pricing Regulations. However, in a number of matters, we find that, many a times, the Assessing Officer is constrained by non-maintenance of relevant that, many a times, the Assessing Officer is constrained by non-maintenance of relevant documents by the taxpayers as, currently, there is no specific requirement for maintenance documents by the taxpayers as, currently, there is no specific requirement for maintenance of documents or getting specific transfer pricing audit done by the taxpayers in respect of of documents or getting specific transfer pricing audit done by the taxpayers in respect of domestic transactions between the related parties. The suggestions which need domestic transactions between the related parties. The suggestions which need consideration are whether the law should be amended to make it compulsory for the consideration are whether the law should be amended to make it compulsory for the taxpayer to maintain books of account and other documents on the lines prescribed under taxpayer to maintain books of account and other documents on the lines prescribed under rule 10D of the Income-tax Rules in respect of such domestic transactions and whether the rule 10D of the Income-tax Rules in respect of such domestic transactions and whether the taxpayer should obtain an audit report from his Chartered Accountant so that the taxpayer taxpayer should obtain an audit report from his Chartered Accountant so that the taxpayer maintains proper documents and requisite books of account reflecting the transactions maintains proper documents and requisite books of account reflecting the transactions between related entities as at arm’s length price based on generally accepted methods between related entities as at arm’s length price based on generally accepted methods specified under the Transfer Pricing Regulations”specified under the Transfer Pricing Regulations”

22

Domestic transactions - Transfer Pricing

May lead to economic double taxationMay lead to economic double taxation

Inline with some tax jurisdictions like Australia, Inline with some tax jurisdictions like Australia,

Thailand , Denmark etc.,Thailand , Denmark etc.,

Increase in compliance burdenIncrease in compliance burden

33

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing

New sub.sec (2A) to sec.92New sub.sec (2A) to sec.92

““((2A) Any allowance for an expenditure or interest or allocation of 2A) Any allowance for an expenditure or interest or allocation of

any cost or expense any cost or expense or or any any incomeincome in relation to the specified in relation to the specified

domestic transaction shall be computed having regard to the domestic transaction shall be computed having regard to the

arm’s length price.” w.e.f 1arm’s length price.” w.e.f 1stst Apr ‘13 Apr ‘13

Specified domestic transaction means Specified domestic transaction means ““92BA. For the purposes of this section and sections 92, 92C, 92D 92BA. For the purposes of this section and sections 92, 92C, 92D

and 92E, “specified domestic transaction” in case of an assessee and 92E, “specified domestic transaction” in case of an assessee

means any of the following transactions, not being an means any of the following transactions, not being an

international transaction, namely:—international transaction, namely:—

44

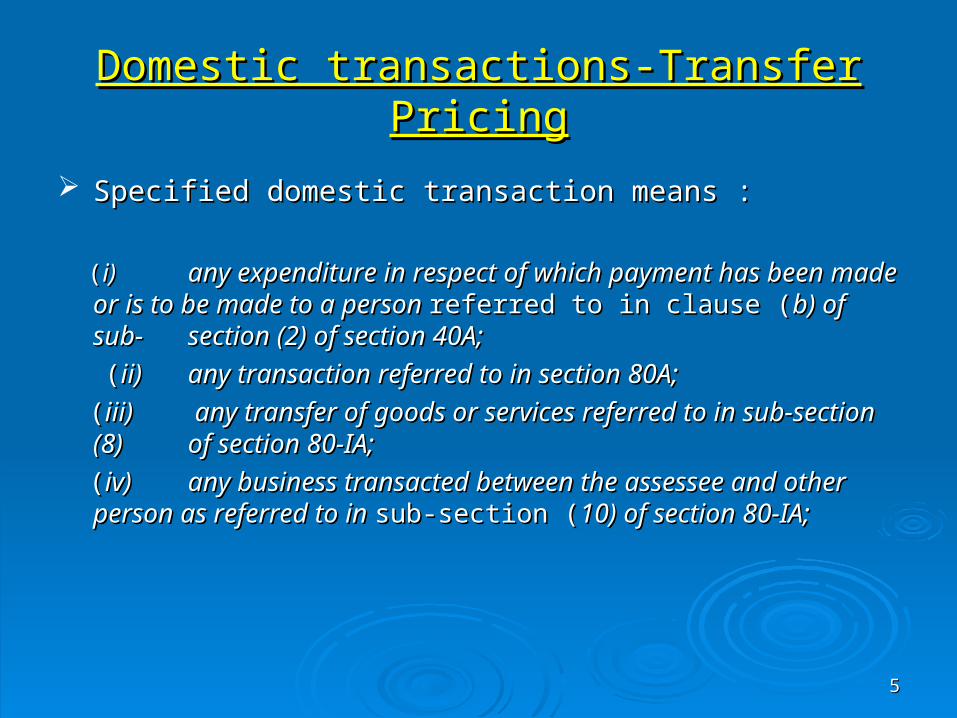

Domestic transactions-Transfer PricingDomestic transactions-Transfer Pricing

Specified domestic transaction means :Specified domestic transaction means :

((i) i) any expenditure in respect of which payment has been any expenditure in respect of which payment has been made made or is to be made to a person or is to be made to a person referred to in clause (referred to in clause (b) of sub-b) of sub-

section (2) of section 40A;section (2) of section 40A;

((ii) ii) any transaction referred to in section 80A;any transaction referred to in section 80A;

((iii)iii) any transfer of goods or services referred to in sub-section any transfer of goods or services referred to in sub-section (8) (8) of section 80-IA;of section 80-IA;

((iv) iv) any business transacted between the assessee and other any business transacted between the assessee and other person as referred to in person as referred to in sub-section (sub-section (10) of section 80-IA;10) of section 80-IA;

55

Domestic transactions-Transfer PricingDomestic transactions-Transfer Pricing

Specified domestic transaction means :Specified domestic transaction means :

((v) v) any transaction, referred to in any other section under any transaction, referred to in any other section under Chapter Chapter VI-A or section 10AA, to VI-A or section 10AA, to which provisions of sub-which provisions of sub-section (section (8) or 8) or sub-section (10) of section 80-IA are applicable; orsub-section (10) of section 80-IA are applicable; or

((vi) vi) any other transaction as may be prescribed, any other transaction as may be prescribed,

and where the aggregate of such transactions entered into by the and where the aggregate of such transactions entered into by the

assessee in the previous year exceeds a sum of assessee in the previous year exceeds a sum of five crore rupees.”five crore rupees.” - -

w.e.f. 1w.e.f. 1stst Apr 2013 Apr 2013

66

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing

S.10AAS.10AA

S.40A(2)(b) – FMV vs. ALPS.40A(2)(b) – FMV vs. ALP

S.80A - Scope of deductions & FMV for inter business S.80A - Scope of deductions & FMV for inter business

transferstransfers

S.80IA (8) – Eligible business Vs. Other businessS.80IA (8) – Eligible business Vs. Other business

S. 80IA (10) - Eligible assessee Vs. Other personS. 80IA (10) - Eligible assessee Vs. Other person

S.80IAB(3), 80IB(13),80IC (7), 80ID (5), 80IE (6) S.80IAB(3), 80IB(13),80IC (7), 80ID (5), 80IE (6)

77

Domestic transactions-Transfer PricingDomestic transactions-Transfer Pricing

S.92C – computation of ALP – methodologies- also S.92C – computation of ALP – methodologies- also

apply to Spec. dom. transactionsapply to Spec. dom. transactions

S.92CA (1)(2)&(3)- reference , service of notice & order S.92CA (1)(2)&(3)- reference , service of notice & order

to be made by TPO to be made by TPO

S.92D – documentation – maintenance & productionS.92D – documentation – maintenance & production

S.92E – report from an accountant – may be a new formS.92E – report from an accountant – may be a new form

88

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing Corresponding Amendments :Corresponding Amendments : S. 40A(2) – Proviso inserted to provide for ALP in cl(a) :S. 40A(2) – Proviso inserted to provide for ALP in cl(a) : “ “ Provided that no disallowance, on account of any expenditure Provided that no disallowance, on account of any expenditure being excessive or unreasonable having regard to the fair market being excessive or unreasonable having regard to the fair market value, shall be made in respect of a specified domestic transaction value, shall be made in respect of a specified domestic transaction referred to in S.92BA, if such transaction is at arm’s length price as referred to in S.92BA, if such transaction is at arm’s length price as defined in cl.(ii) of S.92F” defined in cl.(ii) of S.92F”

- - FMV different from ALP?FMV different from ALP?

In cl.(b) (iv) , after the words In cl.(b) (iv) , after the words “ or any relative of such director, “ or any relative of such director, partner or member” , the words “or partner or member” , the words “or any other company any other company carrying on carrying on business or profession in which the first mentioned company has business or profession in which the first mentioned company has substantial interest” substantial interest” shall be insertedshall be inserted..

99

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing

Corresponding Amendments :Corresponding Amendments : S. 80A – S. 80A – Cl (iii) to ExplanationCl (iii) to Explanation inserted inserted ::

““in relation to any goods or services sold, supplied or acquired in relation to any goods or services sold, supplied or acquired means the arm’s length price as defined in cl.(ii) of S.92F of such means the arm’s length price as defined in cl.(ii) of S.92F of such goods or services, if it is a specified domestic transaction referred to goods or services, if it is a specified domestic transaction referred to in S.92BA” in S.92BA” is ALP synonymous with Market valueis ALP synonymous with Market value ? ?

S. 80-IA – S. 80-IA – Explanation substituted in Explanation substituted in Ss(8) :Ss(8) :Market Value , in relation to any goods or services means – Market Value , in relation to any goods or services means –

i.i. the price that such goods or services would ordinarily fetch in the the price that such goods or services would ordinarily fetch in the open market: oropen market: or

ii.ii. the arm’s length price as defined in cl(ii) of S.92F, where the the arm’s length price as defined in cl(ii) of S.92F, where the transfer of such goods or services is a specified domestic transfer of such goods or services is a specified domestic transaction referred to in S.92BA transaction referred to in S.92BA

1010

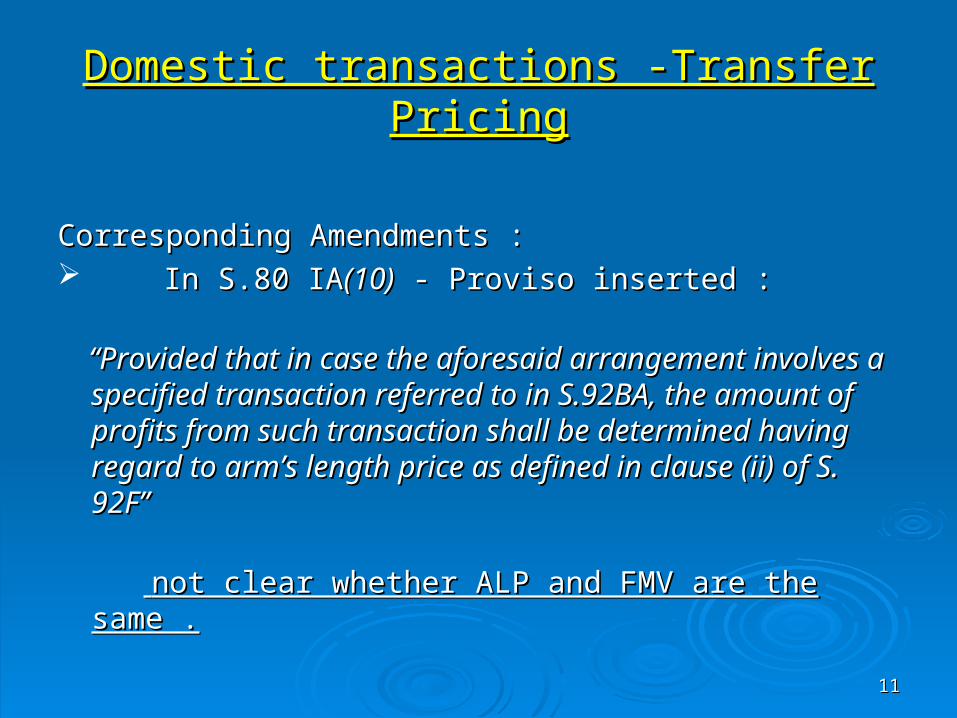

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing

Corresponding Amendments :Corresponding Amendments : In S.80 IAIn S.80 IA(10)(10) - Proviso inserted : - Proviso inserted :

“ “Provided that in case the aforesaid arrangement Provided that in case the aforesaid arrangement involves a specified transaction referred to in S.92BA, involves a specified transaction referred to in S.92BA, the amount of profits from such transaction shall be the amount of profits from such transaction shall be determined having regard to arm’s length price as determined having regard to arm’s length price as defined in clause (ii) of S. 92F” defined in clause (ii) of S. 92F”

not clear whether ALP and FMV are the same .not clear whether ALP and FMV are the same .

1111

1212

Sec 40A (2)(b) – Related Party

Sr.No Payer / assesseePayee

(i) IndividualAny relative

[defined in sec. 2(41) to mean husband, wife, brother, sister, lineal ascendant or descendant]* Definition of Relative u/s 56(2) not relevant

(ii) Company any director or relative of such director

Firm (includes LLP) any partner or relative of such partner

AOP any member or relative of such member

HUF any member or relative of such member

(iii) Any Assessee any individual having substantial interest in the assessee’s business or relative of such individual

(iv) Any assessee a Company, Firm, AOP, HUF having substantial interest in the assessees business

orany director, partner, member

or relative of such director, partner or member

or (newly inserted)any other company carrying on business or profession in which the first mentioned company has substantial interest.

X Ltd. (subsidiary co)A Ltd. (holding co) Y Ltd. (subsidiary co)

Relationship can exists any time during the

year

Type of transactions Type of transactions coveredcovered (illustrations for (illustrations for payments made by a Company) …payments made by a Company) …

1313

Case 1 - Director or any relative of the Director of the taxpayer – Section 40A(2)(b)(ii)

Mr. AMr. A Mr. CMr. C

Assessee (Taxpayer)Assessee (Taxpayer)

Mr. DMr. D

Dire

cto

r

Relative

Dire

ctor

Covered transactions

Case 2 - To an individual who has substantial interest in the business or profession of the taxpayer or relative of such individual – Section 40A(2)(b)(iii)

Mr. AMr. A Mr. CMr. C

Assessee (Taxpayer)Assessee (Taxpayer)

Mr. DMr. DRelative

Sub

stan

tial i

nter

est

>2

0%

Relative

Holding Structure

Type of transactions covered (illustrations for payments Type of transactions covered (illustrations for payments made by a Company) …made by a Company) …

1414

Case 3 – To a Company having substantial interest in the business of the taxpayer or any director of such company or relative of the director – Section 40A(2)(b)(iv)

A LtdA Ltd

Mr. CMr. C

Assessee (Taxpayer)Assessee (Taxpayer)

Mr. DMr. D

Rel

ativ

e

Dire

cto

r

Covered transactions

Case 4 – Any other company carrying on business in which the first mentioned company has substantial interest – Section 40A(2)(b)(iv)

C LtdC Ltd

B LtdB Ltd

Assessee (Taxpayer)Assessee (Taxpayer)

A LtdA Ltd

Sub

stan

tial i

nter

est

>2

0%

Holding Structure

Substantial interest >20%

Substantial interest >20%

Sub

stan

tial i

nter

est

>2

0%

Type of transactions covered (illustrations for payments made Type of transactions covered (illustrations for payments made by a Company) …by a Company) …

1515

Case 5 – To a Company of which a director has a substantial interest in the business of the taxpayer or any director of such company or relative of the director – Section 40A(2)(b)(v)

Mr. AMr. A

Mr. CMr. C

Assessee (Taxpayer)Assessee (Taxpayer)

B LtdB LtdD

irect

or

Director

Covered transactions

Holding Structure

Substantial interest >20%

Mr. DMr. D

Rel

ativ

e

Type of transactions covered (illustrations for payments made by a Type of transactions covered (illustrations for payments made by a Company)…Company)…

1616

Case 6 – To a Company in which the taxpayer has substantial interest in the business of the company – Section 40A(2)(b)(vi)(B)

B LtdB Ltd

Assessee (Taxpayer)Assessee (Taxpayer)

Covered transactions

Case 7 – Any director or relative of the director of taxpayer having substantial interest in that person– Section 40A(2)(b)(vi)(B)

Mr CMr C

Mr BMr B

Assessee (Taxpayer)Assessee (Taxpayer)

A LtdA LtdSubstantial interest >20%

Holding Structure

Su

bst

an

tial

inte

rest

>2

0% Director

Rel

ativ

e

D LtdD LtdSubstantial interest >20%

Tax burden, if transaction not at ALPTax burden, if transaction not at ALP

1717

X Ltd.(non-tax holiday)

Disallowance of ` 20 to Y Ltd

[40A(2)(b)]

Y Ltd.(non-tax holiday)

Sale at ` 120 v/s ALP i.e. `

100

X Ltd.(tax holiday)

Y Ltd.(non-tax holiday)

Sale at ` 120 v/s ALP i.e. `

100

Double Adjustment

Tax holiday on ` 20 not allowed to X Ltd – [80IA(10)] (more than ordinary

profits)

Disallowance of ` 20 to Y Ltd -

[40A(2)(b)]

X Ltd.(tax holiday)

Y Ltd.(non-tax holiday)

Sale at ` 80 v/s ALP i.e. ` 100

Inefficient pricing structure – reduced tax holiday benefit since

sale price is lower than ALP

Section 80IA (8) & 80IA (10) – Deduction in respect of profits and gains from industrial undertaking or enterprise engaged in infrastructure development, etc.

No guidance on the meaning of close connection No guidance on the meaning of close connection To align ordinary profits with arm’s length price. For example:To align ordinary profits with arm’s length price. For example:

OP/ TC of 30% considered to be at arm’s length by the TPOOP/ TC of 30% considered to be at arm’s length by the TPO

Under 801A(10) the AO states that the profits are more than ordinaryUnder 801A(10) the AO states that the profits are more than ordinary

SolutionSolution: : Defend price or evaluate alternate methods (other then profit based)Defend price or evaluate alternate methods (other then profit based)

Impact of non-charging of services/ costs to tax holiday undertakingImpact of non-charging of services/ costs to tax holiday undertaking1818

80IA (8) 80IA (10)

Inter-unit transaction of goods or services • Business transacted with any person generates more than ordinary profits

• Owing to either close connection or any other reason

Applicable where transfer is not at market value

Applicable to tax holiday units earning more than ordinary profit

Onus on tax payer • Primary onus on taxpayer• Onus on tax authorities as well

ALP of 5 comparable companies OP/TC Mark-up of the tax holiday entity OP/TC

Arithmetic mean = 15% 30%

Tax holiday undertakingTax holiday undertaking

International TP International TP Vs. Vs. Tax holiday profitsTax holiday profits

Sec 10A(7) / 10B (7)Sec 10A(7) / 10B (7)Case laws - Case laws - Visual Graphics Computing Services (India) Pvt. Visual Graphics Computing Services (India) Pvt.

Ltd vs ACIT 2012) 52 SOT 172 (URO), Ltd vs ACIT 2012) 52 SOT 172 (URO), Weston Knowledge Systems & Solutions (India) Pvt. Ltd. vs Weston Knowledge Systems & Solutions (India) Pvt. Ltd. vs ITO (2012) 52 SOT 120 (Hyd)(URO)ITO (2012) 52 SOT 120 (Hyd)(URO)

AO has no authority to reduce tax holiday claim once AO has no authority to reduce tax holiday claim once approved by TPOapproved by TPO

Whether same approach is possible when domestic TP is Whether same approach is possible when domestic TP is targeted in computing ordinary profits.targeted in computing ordinary profits.

Domestic TP supports the approach of AO in restricting ordinary profits?Domestic TP supports the approach of AO in restricting ordinary profits?

1919

Cost allocationCost allocation

Whether corporate group expenses to be Whether corporate group expenses to be allocated?allocated?

Courts held that it need not be allocatedCourts held that it need not be allocated

• Case laws - Case laws - Wipro Information Technology vs DCIT Wipro Information Technology vs DCIT (2004) 88 TTJ(Bang) 778 ; (2004) 88 TTJ(Bang) 778 ; Zandu Pharmaceuticals Works Ltd, vs CIT (2013) 213 Zandu Pharmaceuticals Works Ltd, vs CIT (2013) 213 Taxman 207 Taxman 207 Ponds India Ltd (ITA NO. 2047/Mad/88)Ponds India Ltd (ITA NO. 2047/Mad/88)

• Whether every cost allocation should have a mark up? Whether every cost allocation should have a mark up?

2020

2121

Transfer Pricing Process

Identification ofIntra Group

Transactions

FAR Analysis

Identification of ComparableTransactions

EstablishingComparability,Adjustment for

Material Differences

Selection of Most

Appropriate Method

Determination ofA L P

Adjustments

Documentation

Return Filing

TP Assessment

2222

S. 92 F (ii)

“arm’s length price” means a price which is applied

or proposed to be applied in a transaction between

persons other than associated enterprises, in

uncontrolled conditions”

Arm’s length price

2323

Traditional transaction methods

Comparable Uncontrolled Price Method (CUP)

Resale price method (RPM)

Cost plus method (CPM)

Transactional profit methods

Profits split method (PSM)

Transactional net margin method (TNMM)

Other method

2424

New Rule 10AB inserted vide Notification

No.18/2012 dated 23-05-2012

Refers to “price which has been charged or

paid, or would have been charged or paid, for

the same or similar uncontrolled transaction,

with or between non-associated enterprises,

under similar circumstances, considering all

the relevant facts”

“Other Method” for determination of ALP

2525

New Rule 10AB inserted vide Notification

No.18/2012 dated 23-05-2012

Refers to “price which has been charged or

paid, or would have been charged or paid, for

the same or similar uncontrolled transaction,

with or between non-associated enterprises,

under similar circumstances, considering all

the relevant facts”

“Other Method” for determination of ALP

Objectives – Specified Domestic Transactions (SDT)

When profit getting shifted from profit making When profit getting shifted from profit making unit to a loss making unit ;unit to a loss making unit ;

Profit shift from taxable unit to tax free unit ;Profit shift from taxable unit to tax free unit ;

SDT is not meant to cover revenue neutral SDT is not meant to cover revenue neutral

transactions- lest it would result in economic transactions- lest it would result in economic

double taxation double taxation

2626

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing

S.92CA (2A) , (2B) & (2C) apply only to S.92CA (2A) , (2B) & (2C) apply only to international transactions and not to SDTinternational transactions and not to SDT

Non-reference and non-reporting of SDTs Non-reference and non-reporting of SDTs are not covered by new Ss (2A) & (2B)are not covered by new Ss (2A) & (2B)

APA mechanism proposed u/s 92CC & APA mechanism proposed u/s 92CC & CD is not available for SDTsCD is not available for SDTs

2727

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing

If SDTs do not cross threshold INR 5 If SDTs do not cross threshold INR 5 Crores, TP Documentation & Reporting Crores, TP Documentation & Reporting not applicable ; however, original not applicable ; however, original requirement to comply with market value requirement to comply with market value concept of u/s 40A(2)(b) / 10AA/ 80A/ 80IA concept of u/s 40A(2)(b) / 10AA/ 80A/ 80IA (8) & (10) still continues.(8) & (10) still continues.

◊ ◊ then how is it a safe harbor?then how is it a safe harbor?

2828

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing

Typical SDTs: Typical SDTs: Rent paymentsRent payments Intra- group transactionsIntra- group transactions Financial transactionsFinancial transactions Managerial remuneration etcManagerial remuneration etc Corporate guaranteeCorporate guarantee Equity contributionsEquity contributions Reimbursement of expensesReimbursement of expenses Commission paid and discount allowedCommission paid and discount allowed

2929

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing

Expenditure incurred by a resident Expenditure incurred by a resident against non-resident – though not covered against non-resident – though not covered as AE , as ownership and control being as AE , as ownership and control being less than 26% voting, but may be covered less than 26% voting, but may be covered as SDT if voting power is ≥20%as SDT if voting power is ≥20%

3030

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing

AE Vs Related Party creates dichotomyAE Vs Related Party creates dichotomy

Circular 6-P dated 6Circular 6-P dated 6thth July 1968 provides – no July 1968 provides – no disallowance- where there is no attempt to evade disallowance- where there is no attempt to evade taxestaxes

SDT covers only assessee spending u/s SDT covers only assessee spending u/s

40A(2)(b) and will not cover entity 40A(2)(b) and will not cover entity receiving payments receiving payments

3131

Domestic transactions -Transfer PricingDomestic transactions -Transfer Pricing

OECD TP guidelines apply to SDTs?OECD TP guidelines apply to SDTs?

Benefit of range available to SDTsBenefit of range available to SDTs

TP adjustments for SDTs result in double TP adjustments for SDTs result in double

taxation – in revenue neutral cases – hence taxation – in revenue neutral cases – hence corresponding adjustments warrantedcorresponding adjustments warranted

3232

3333

Rule 10D is amended to cover SDTs – sub rule (2) applies only to international transactions

Need based documentation good enough even for SDTs

Should be contemporaneous and be in place by specified date

Initial burden lies with the assessee

DocumentationDocumentation

3434

Section 271 –Penalty ImplicationsSection 271 –Penalty ImplicationsSr.No.

Type of penalty Section Penalty quantified

1 a) Failure to maintain prescribed information/ documents

271AA 2% of transaction value

(b) Failure to report any such transaction or

(c) Furnish incorrect information

2 Failure to furnish information/ documents during assessment u/s 92D

271G 2% of transaction value

3 Adjustment to taxpayer’s income during assessment

271(1)(c) 100% to 300% of tax on adjustment amount

4 Failure to furnish accountant’s report u/s 92E

271BA INR 100,000

3535

IssuesIssues

Whether payment for capital expenditure Or expenditure capitalized is

also covered ?

Whether the provisions will apply in case the payer’s income is chargeable to tax under the head ‘Income from other sources’, because section 58(2) says –The provisions of section 40A shall, so far as may be, apply in computing the income chargeable under the head “Income from other sources” as they apply in computing the income chargeable under the head “Profits and gains of business or profession” ?

Whether new provision applies to - Public Charitable Trust paying remuneration to related persons. Co-operative Societies Social Clubs having a business undertaking

IssuesIssues

Transfer pricing provisions are not applicable in case Transfer pricing provisions are not applicable in case where income is not chargeable to tax at all.where income is not chargeable to tax at all.

Correlative adjustments - if excessive or unreasonable Correlative adjustments - if excessive or unreasonable expenses are disallowed in the hands of tax payer at expenses are disallowed in the hands of tax payer at time of the assessment then corresponding adjustment time of the assessment then corresponding adjustment to the income of the recipient will not be allowed in the to the income of the recipient will not be allowed in the hands of recipient of income. Hence, it would lead to hands of recipient of income. Hence, it would lead to double taxation in India.double taxation in India.

3636

ChallengesChallenges

3737

Type of payments/ transactions Challenges• Salary and Bonuses paid to the

partners

• Remuneration paid to the Directors

• Transfer of land

• Joint Development agreements

• Project management fees

• Allocation of expenses between the same taxpayer having an eligible unit and non-eligible unit

• Definition of Related Party

• Benchmarking?• Whether the limit as mentioned in section 40

(b) would be the ALP?• Benchmarking?• Whether the limit as mentioned in Schedule

XIII would be the ALP?

• Whether the rates mentioned in the ready reckoner be considered as ALP?

• Benchmarking?

• Benchmarking?

• Whether these allocation would be SDT – Sec 80-IA(10)?

• Directly v/s Indirectly

New Rules & FormsNew Rules & Forms

Form 3 CEB enlarged – Part C inserted Form 3 CEB enlarged – Part C inserted with respect to details of specified with respect to details of specified domestic transactions.domestic transactions.

Rule 10A – Expands AE definition when Rule 10A – Expands AE definition when Sec.92A(1) & (2) doesn’t do so.Sec.92A(1) & (2) doesn’t do so.

3838

Action AwaitedAction Awaited

Clarifications in line with old circular 6-P Clarifications in line with old circular 6-P (supra)(supra)

Revenue neutral transactions – avoidance of Revenue neutral transactions – avoidance of double taxation – criticaldouble taxation – critical

3939

![Foro de la OMPI para Jueces de Propiedad Intelectual de 2019 · of Food & Drugs and Glaxo SmithKline, asunto N.º 149907 − Tribunal de Casación de Turquía [2014]: Merinos v n11.com,](https://static.fdocuments.net/doc/165x107/5fcc233718f5196d093fddfa/foro-de-la-ompi-para-jueces-de-propiedad-intelectual-de-2019-of-food-drugs.jpg)