1 5 June 2015 Paris, France - International Gas Unionmembers.igu.org/old/IGU...

31

TS WOC 1-4 MONETISING STRANDED GAS RESOURCES ONSHORE AND OFFSHORE - The Palette Of Enabling Technologies, Their Comparative Merits And Challenges In Commercial Application Joe T. Verghese WorleyParsons Europe Ltd London, United Kingdom 1 – 5 June 2015 – Paris, France 26 th World Gas Conference

Transcript of 1 5 June 2015 Paris, France - International Gas Unionmembers.igu.org/old/IGU...

TS WOC 1-4 MONETISING STRANDED GAS RESOURCES ONSHORE

AND OFFSHORE

- The Palette Of Enabling Technologies, Their Comparative

Merits And Challenges In Commercial Application

Joe T. Verghese WorleyParsons Europe Ltd

London, United Kingdom

1 – 5 June 2015 – Paris, France

26th World Gas Conference

Monetising Stranded Gas Resources Onshore and Offshore

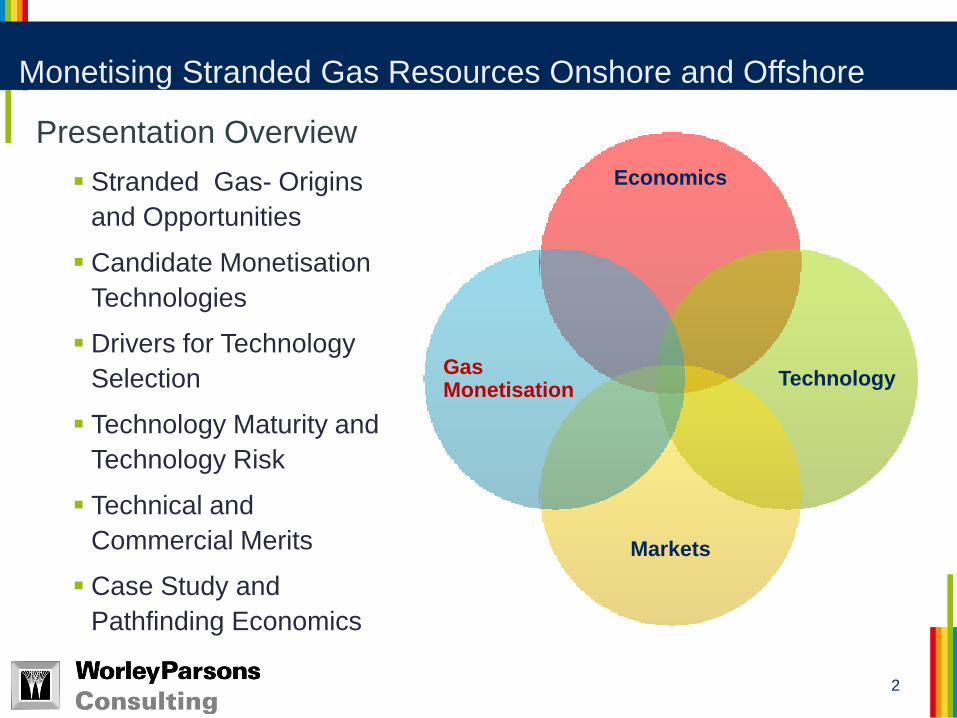

Stranded Gas- Origins

and Opportunities

Candidate Monetisation

Technologies

Drivers for Technology

Selection

Technology Maturity and

Technology Risk

Technical and

Commercial Merits

Case Study and

Pathfinding Economics

2

Presentation Overview

Economics

Technology

Markets

Gas Monetisation

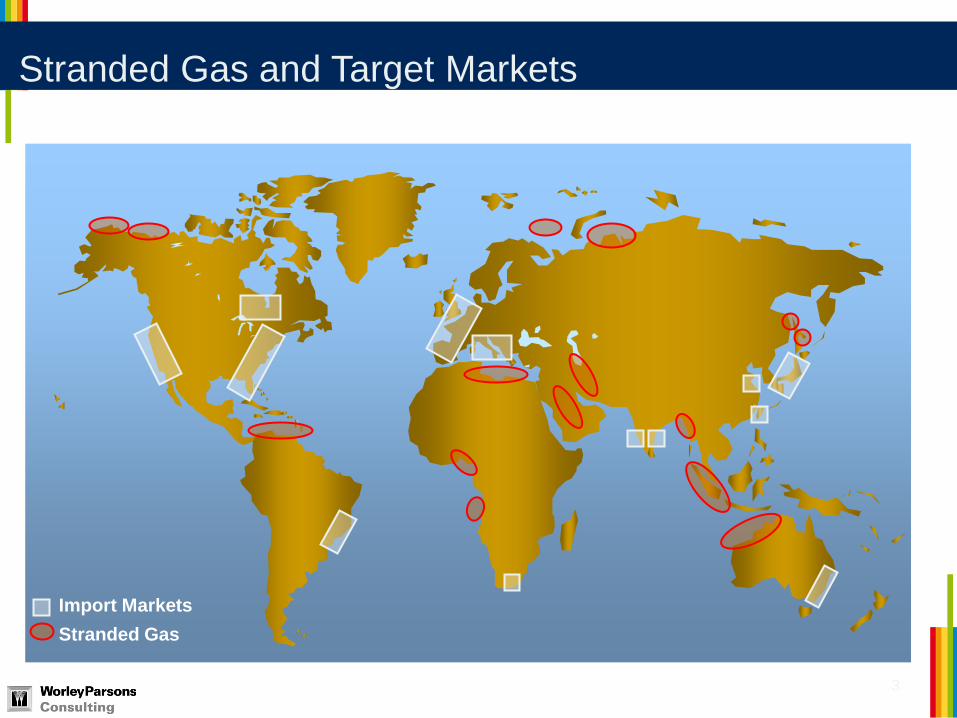

Stranded Gas and Target Markets

3

Import Markets

Stranded Gas

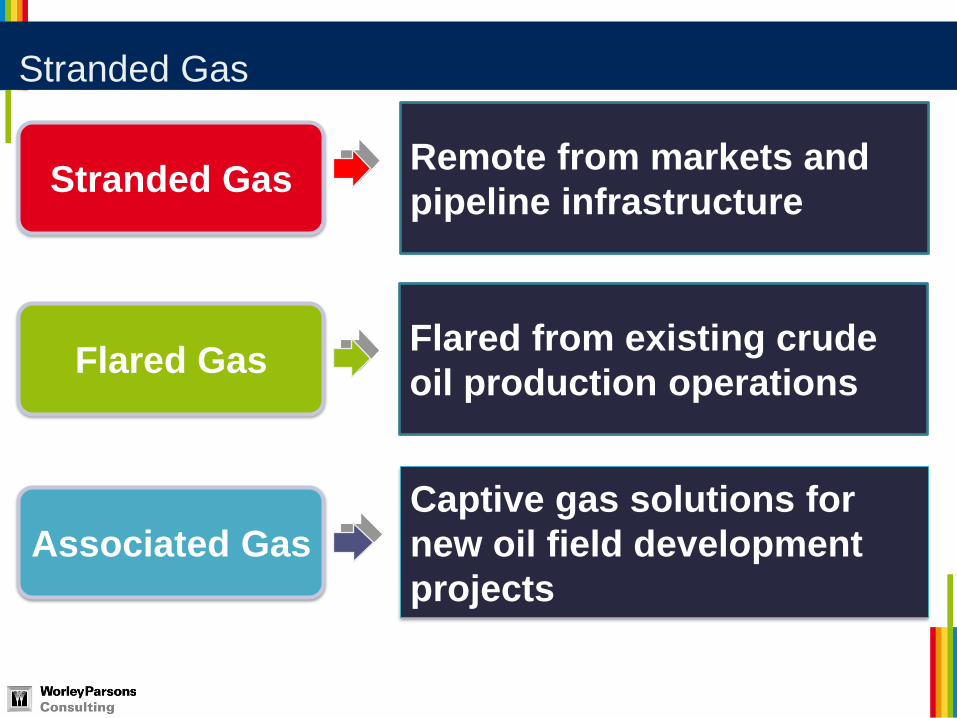

Stranded Gas

Remote from markets and

pipeline infrastructure Stranded Gas

Flared from existing crude

oil production operations Flared Gas

Captive gas solutions for

new oil field development

projects

Associated Gas

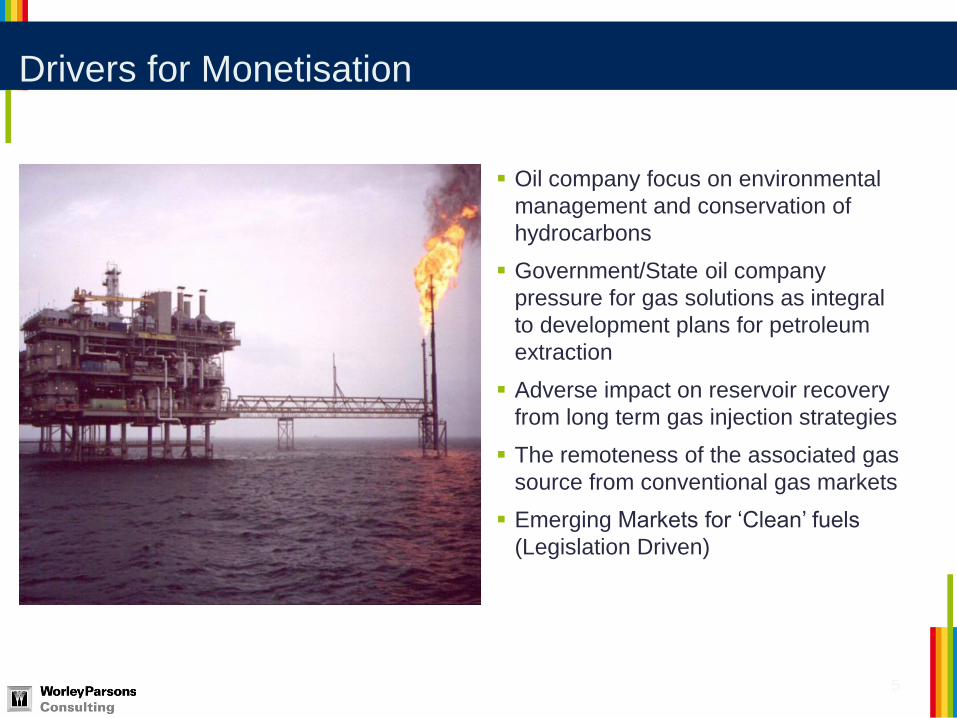

Drivers for Monetisation

Oil company focus on environmental

management and conservation of

hydrocarbons

Government/State oil company

pressure for gas solutions as integral

to development plans for petroleum

extraction

Adverse impact on reservoir recovery

from long term gas injection strategies

The remoteness of the associated gas

source from conventional gas markets

Emerging Markets for ‘Clean’ fuels

(Legislation Driven)

5

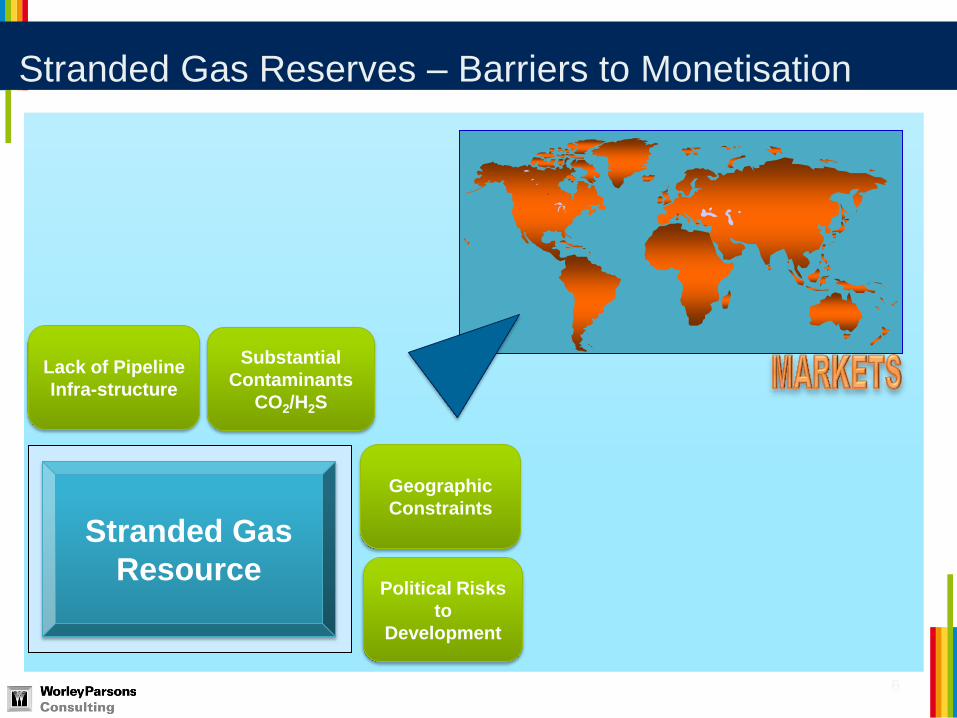

Stranded Gas Reserves – Barriers to Monetisation

6

Stranded Gas

Resource

Lack of Pipeline

Infra-structure

Substantial

Contaminants

CO2/H2S

Political Risks

to

Development

Geographic

Constraints

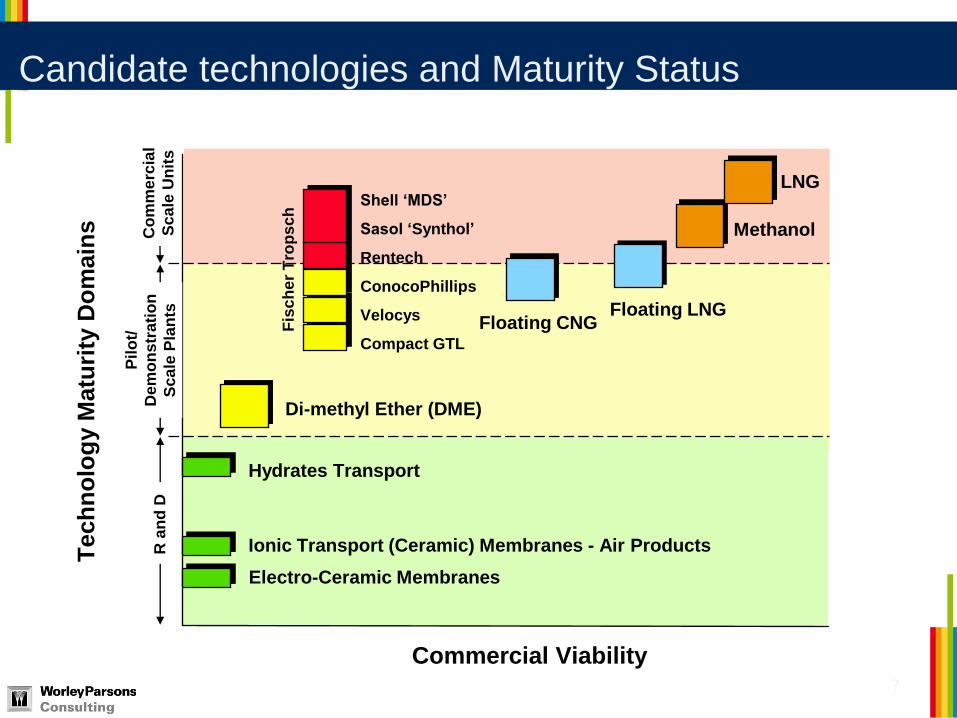

Candidate technologies and Maturity Status

7

R a

nd

D

Pil

ot/

Dem

on

str

ati

on

Sc

ale

Pla

nts

Co

mm

erc

ial

Sc

ale

Un

its

Commercial Viability

Te

ch

no

log

y M

atu

rity

Do

main

s

Di-methyl Ether (DME)

Ionic Transport (Ceramic) Membranes - Air Products

Hydrates Transport

LNG

Methanol

Shell ‘MDS’

Sasol ‘Synthol’

Rentech

ConocoPhillips

Velocys

Compact GTL

Fis

ch

er

Tro

ps

ch

Electro-Ceramic Membranes

Floating CNG Floating LNG

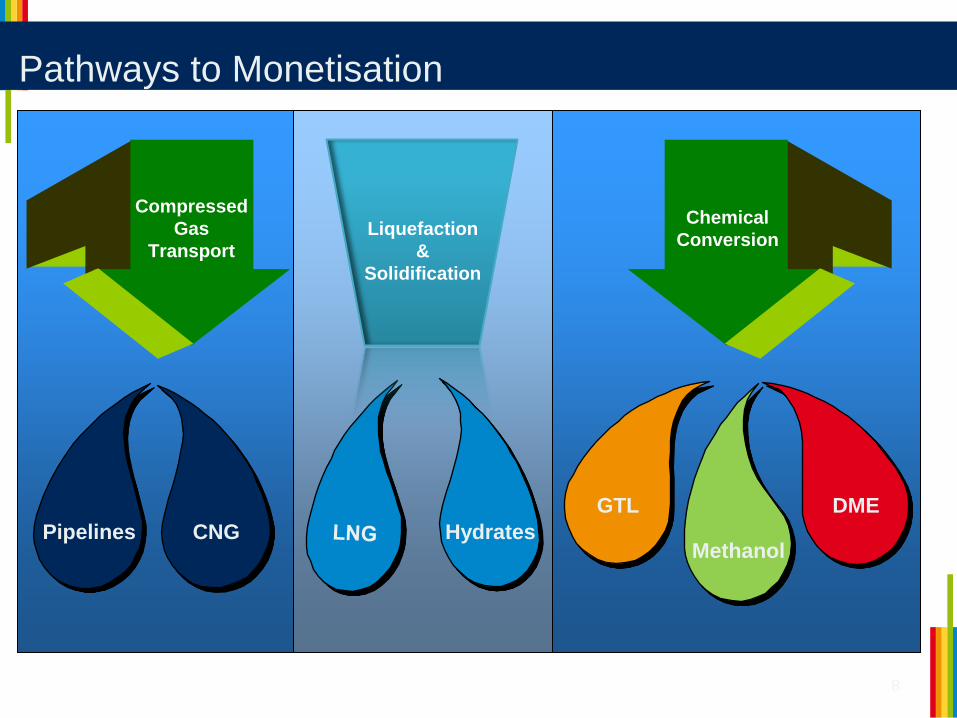

Pathways to Monetisation

8

CNG Pipelines

Liquefaction

&

Solidification

Methanol

DME GTL

Chemical

Conversion

Hydrates

Compressed

Gas

Transport

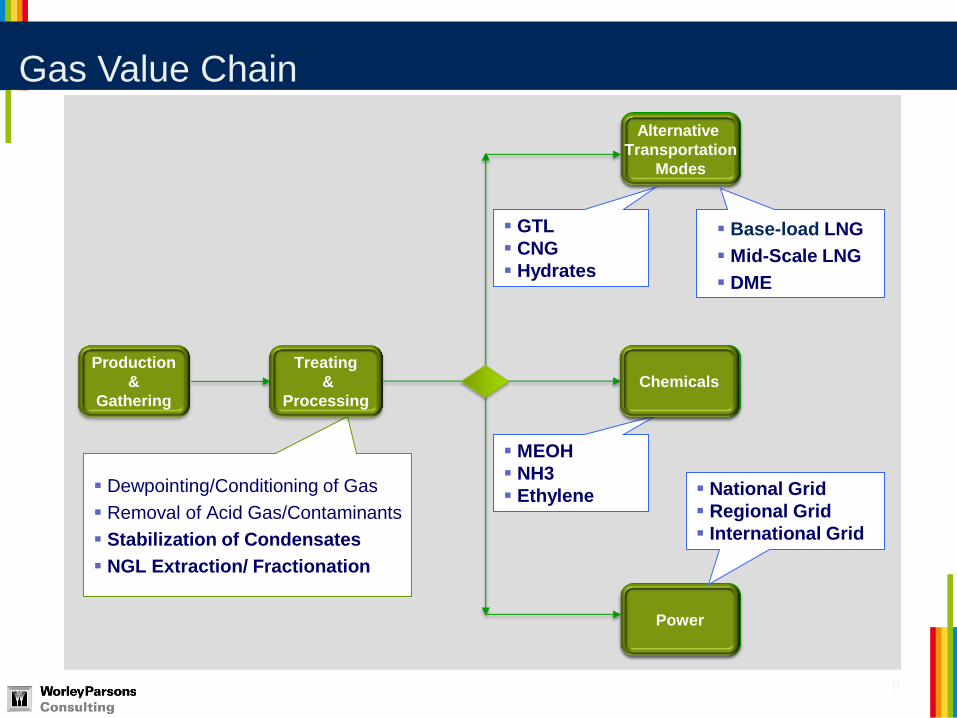

Gas Value Chain

9

Dewpointing/Conditioning of Gas

Removal of Acid Gas/Contaminants

Stabilization of Condensates

NGL Extraction/ Fractionation

Base-load LNG

Mid-Scale LNG

DME

GTL

CNG

Hydrates

MEOH

NH3

Ethylene

Treating

&

Processing

Production

&

Gathering

Alternative

Transportation

Modes

Power

Chemicals

National Grid

Regional Grid

International Grid

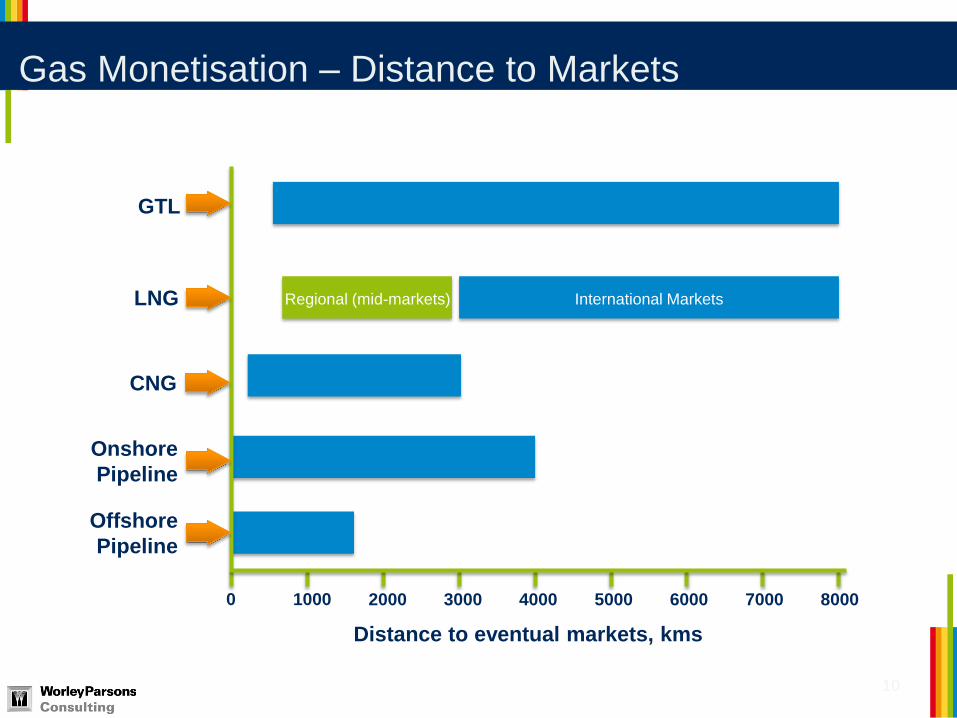

Gas Monetisation – Distance to Markets

10

GTL

LNG

Onshore

Pipeline

Offshore

Pipeline

1000 2000 3000 4000 5000 6000 7000 8000

Distance to eventual markets, kms

CNG

0

International Markets Regional (mid-markets)

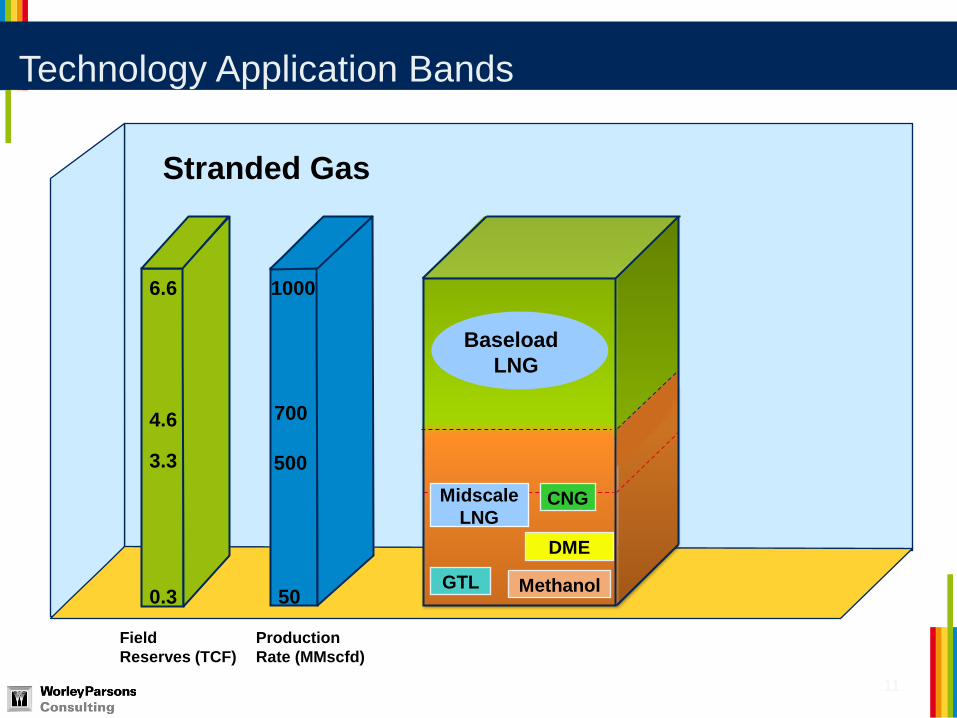

Technology Application Bands

11

3.3

4.6

6.6

0.3

Field

Reserves (TCF)

Production

Rate (MMscfd)

Stranded Gas

Baseload

LNG

Midscale

LNG

GTL

DME

Methanol

CNG

1000

700

500

50

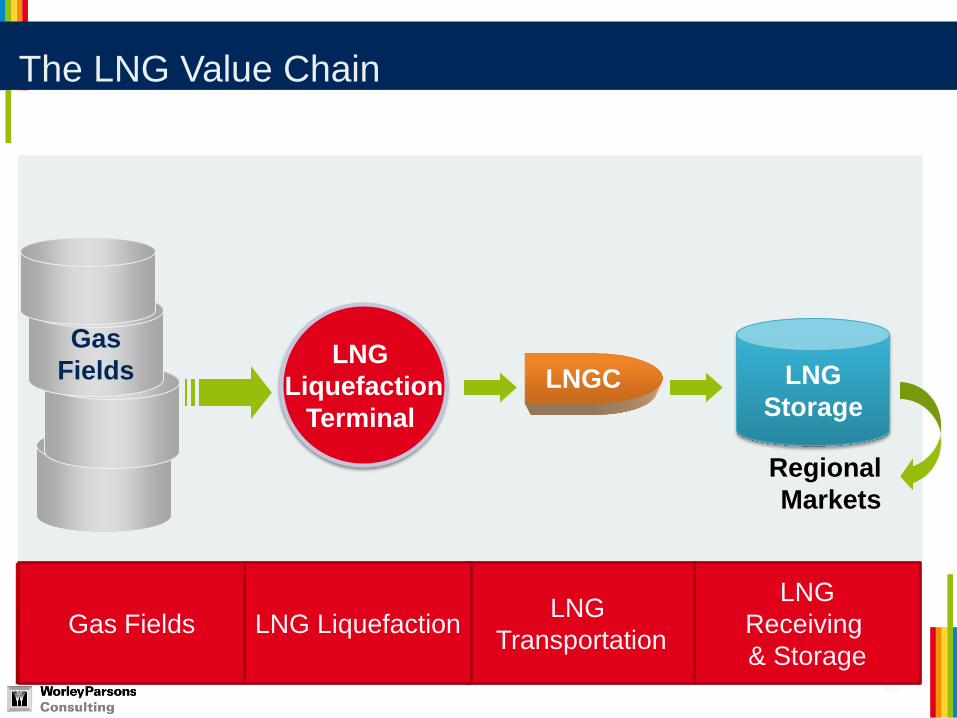

The LNG Value Chain

12

LNG

Receiving

& Storage

LNG

Transportation LNG Liquefaction Gas Fields

Gas

Fields LNG

Liquefaction

Terminal

LNGC LNG

Storage

Regional

Markets

LNG Liquefaction Gas Fields

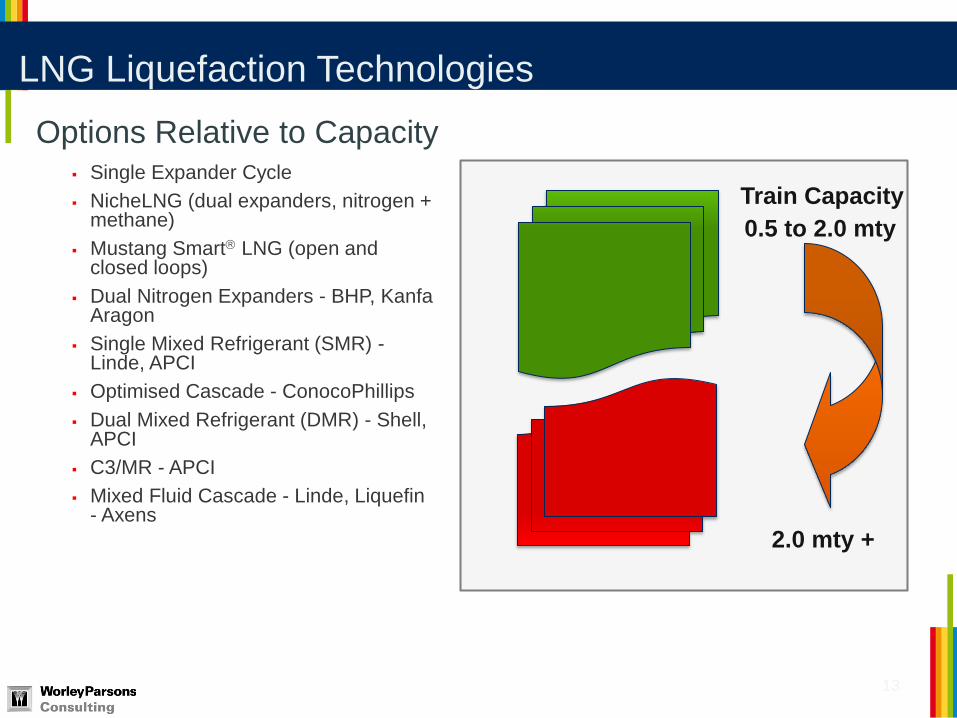

LNG Liquefaction Technologies

Single Expander Cycle

NicheLNG (dual expanders, nitrogen + methane)

Mustang Smart LNG (open and closed loops)

Dual Nitrogen Expanders - BHP, Kanfa Aragon

Single Mixed Refrigerant (SMR) - Linde, APCI

Optimised Cascade - ConocoPhillips

Dual Mixed Refrigerant (DMR) - Shell, APCI

C3/MR - APCI

Mixed Fluid Cascade - Linde, Liquefin - Axens

13

Options Relative to Capacity

Train Capacity

0.5 to 2.0 mty

2.0 mty +

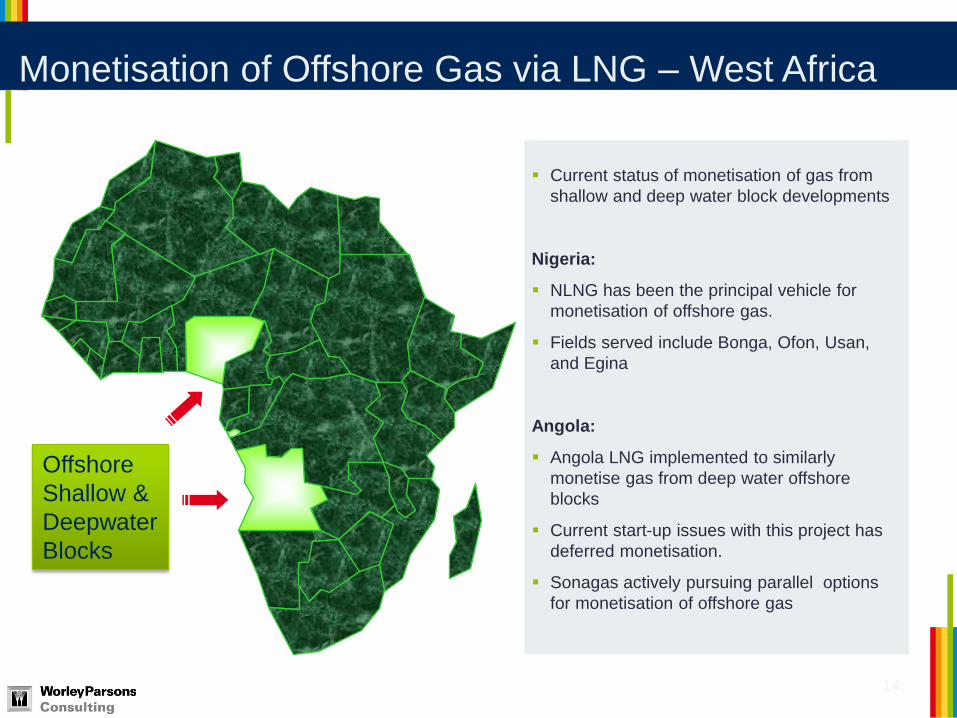

Monetisation of Offshore Gas via LNG – West Africa

14

Offshore

Shallow &

Deepwater

Blocks

Current status of monetisation of gas from

shallow and deep water block developments

Nigeria:

NLNG has been the principal vehicle for

monetisation of offshore gas.

Fields served include Bonga, Ofon, Usan,

and Egina

Angola:

Angola LNG implemented to similarly

monetise gas from deep water offshore

blocks

Current start-up issues with this project has

deferred monetisation.

Sonagas actively pursuing parallel options

for monetisation of offshore gas

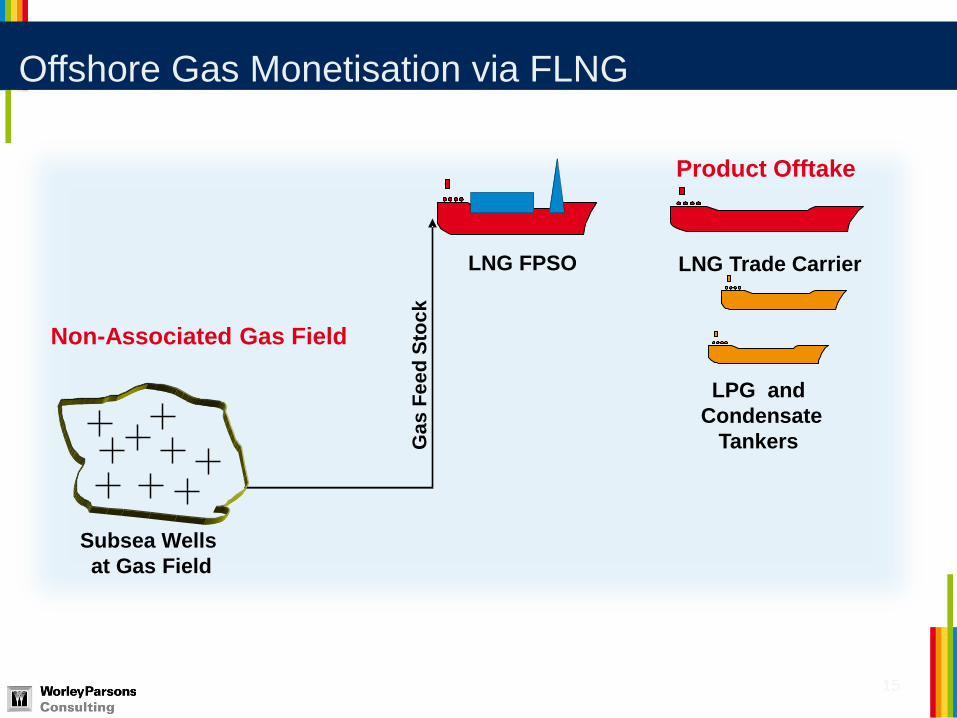

Offshore Gas Monetisation via FLNG

15

Product Offtake

Non-Associated Gas Field

Subsea Wells

at Gas Field

LNG FPSO

LPG and

Condensate

Tankers

LNG Trade Carrier

Gas

Fe

ed

Sto

ck

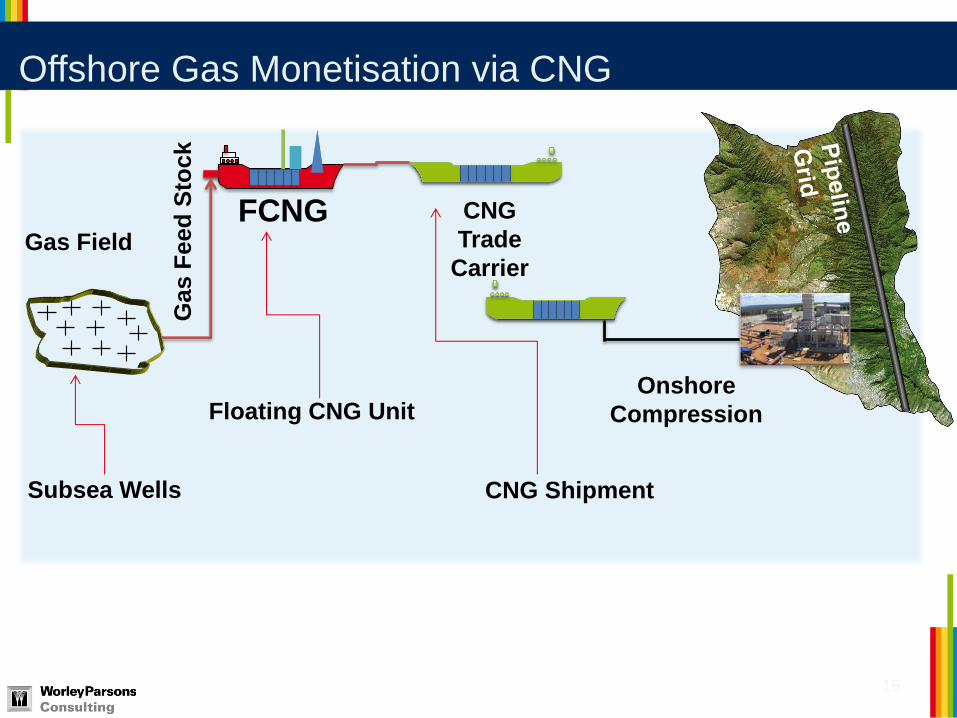

Offshore Gas Monetisation via CNG

16

Subsea Wells

FCNG CNG

Trade

Carrier

Gas F

eed

Sto

ck

Gas Field

Onshore

Compression Floating CNG Unit

CNG Shipment

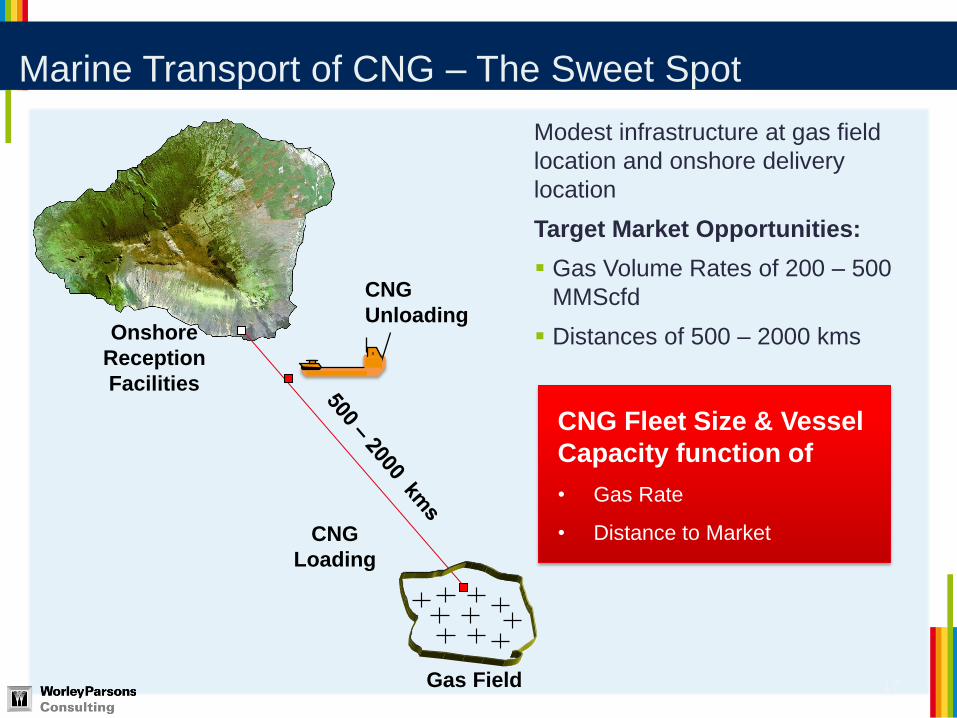

Marine Transport of CNG – The Sweet Spot

17

Onshore

Reception

Facilities

CNG

Unloading

CNG

Loading

Gas Field

Modest infrastructure at gas field

location and onshore delivery

location

Target Market Opportunities:

Gas Volume Rates of 200 – 500

MMScfd

Distances of 500 – 2000 kms

CNG Fleet Size & Vessel

Capacity function of

• Gas Rate

• Distance to Market

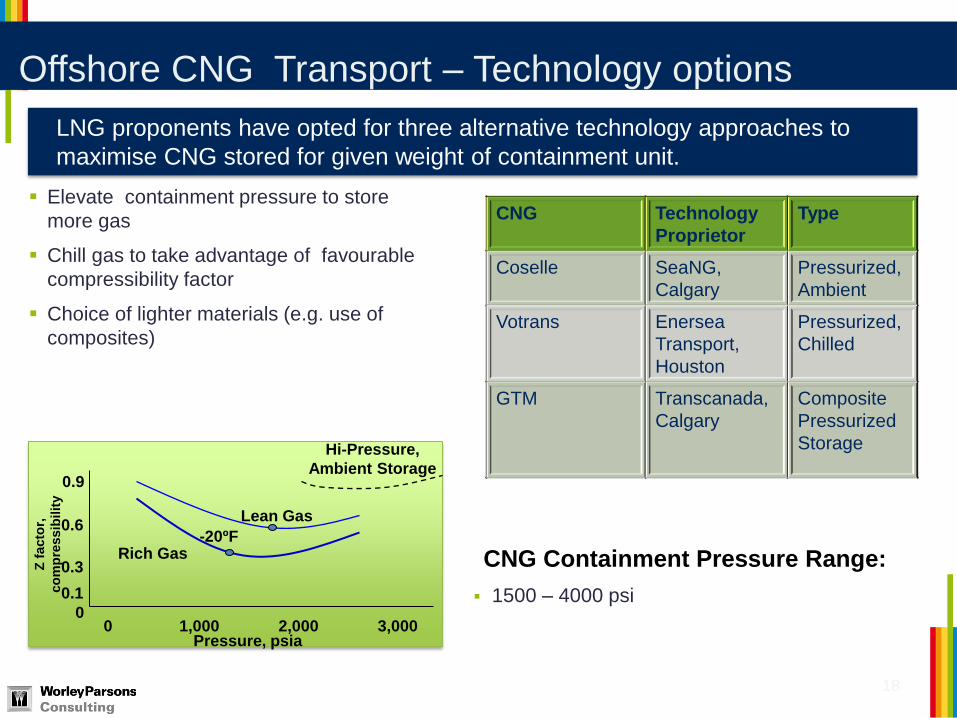

Offshore CNG Transport – Technology options

18

0 1,000 2,000 3,000

0.9

0.6

0.3

0.1

0

Z f

acto

r,

co

mp

ressib

ilit

y

Hi-Pressure,

Ambient Storage

Rich Gas -20ºF

Lean Gas

Pressure, psia

CNG Technology

Proprietor

Type

Coselle SeaNG,

Calgary

Pressurized,

Ambient

Votrans Enersea

Transport,

Houston

Pressurized,

Chilled

GTM Transcanada,

Calgary

Composite

Pressurized

Storage

LNG proponents have opted for three alternative technology approaches to

maximise CNG stored for given weight of containment unit.

CNG Containment Pressure Range:

1500 – 4000 psi

Elevate containment pressure to store

more gas

Chill gas to take advantage of favourable

compressibility factor

Choice of lighter materials (e.g. use of

composites)

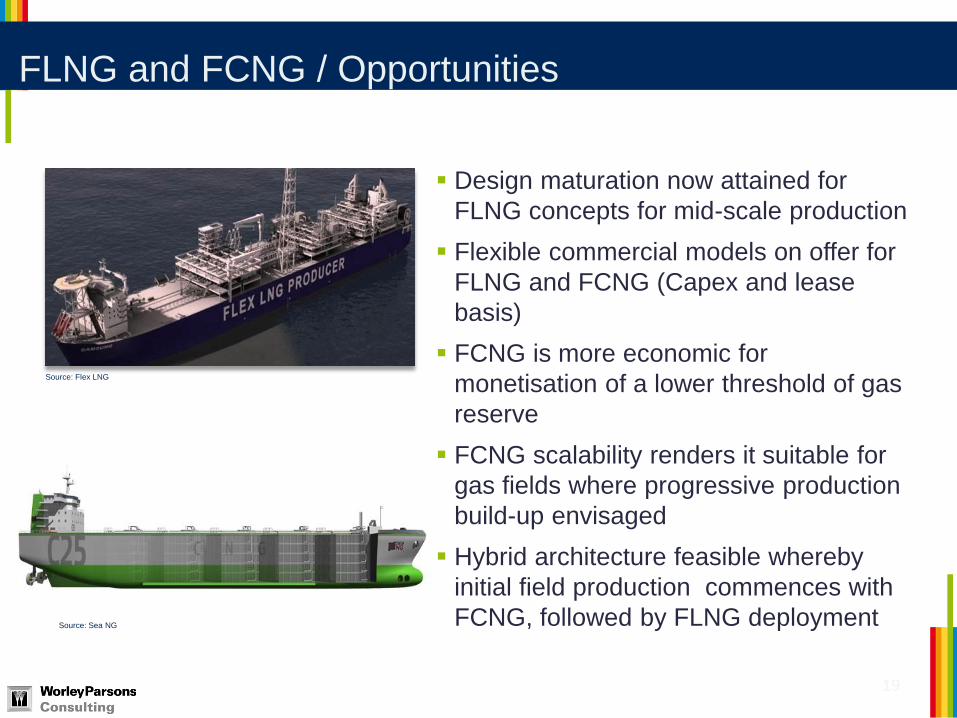

FLNG and FCNG / Opportunities

Design maturation now attained for

FLNG concepts for mid-scale production

Flexible commercial models on offer for

FLNG and FCNG (Capex and lease

basis)

FCNG is more economic for

monetisation of a lower threshold of gas

reserve

FCNG scalability renders it suitable for

gas fields where progressive production

build-up envisaged

Hybrid architecture feasible whereby

initial field production commences with

FCNG, followed by FLNG deployment

19

Source: Flex LNG

Source: Sea NG

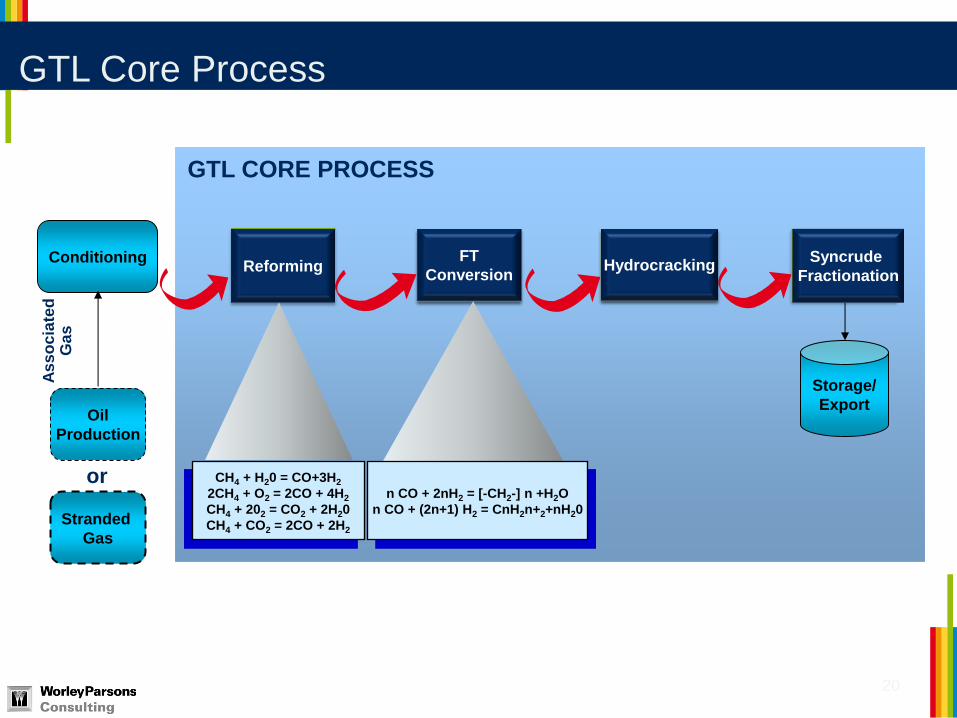

GTL Core Process

20

GTL CORE PROCESS

As

so

cia

ted

G

as

Oil

Production

Conditioning

Stranded

Gas

Storage/

Export

or

Reforming FT

Conversion Hydrocracking

Syncrude

Fractionation

CH4 + H20 = CO+3H2

2CH4 + O2 = 2CO + 4H2

CH4 + 202 = CO2 + 2H20

CH4 + CO2 = 2CO + 2H2

n CO + 2nH2 = [-CH2-] n +H2O

n CO + (2n+1) H2 = CnH2n+2+nH20

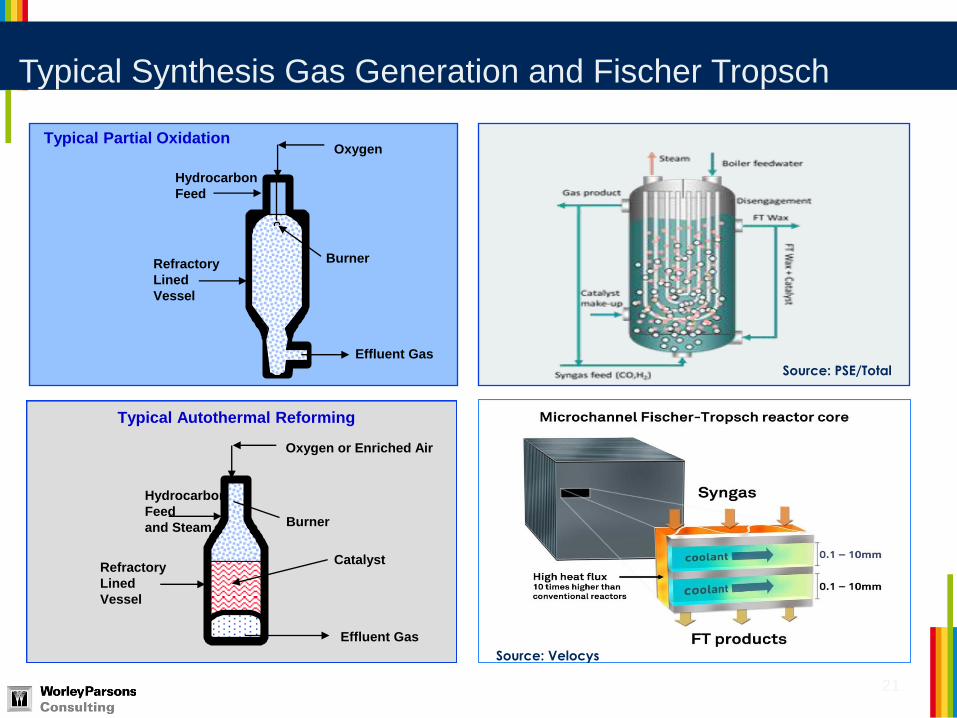

Typical Synthesis Gas Generation and Fischer Tropsch

21

Catalyst

Effluent Gas

Burner

Oxygen or Enriched Air

Refractory

Lined

Vessel

Hydrocarbon

Feed

and Steam

Typical Autothermal Reforming

Source: PSE/Total

Source: Velocys

Burner

Oxygen

Refractory

Lined

Vessel

Effluent Gas

Hydrocarbon

Feed

Typical Partial Oxidation

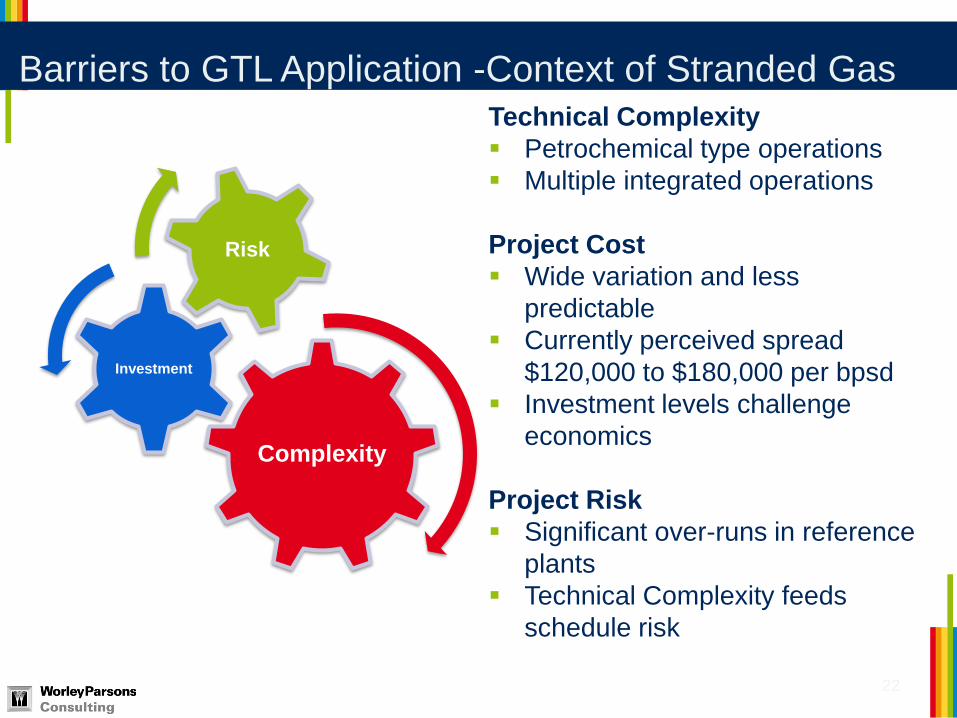

Barriers to GTL Application -Context of Stranded Gas

22

Technical Complexity

Petrochemical type operations

Multiple integrated operations

Project Cost

Wide variation and less

predictable

Currently perceived spread

$120,000 to $180,000 per bpsd

Investment levels challenge

economics

Project Risk

Significant over-runs in reference

plants

Technical Complexity feeds

schedule risk

Complexity

Investment

Risk

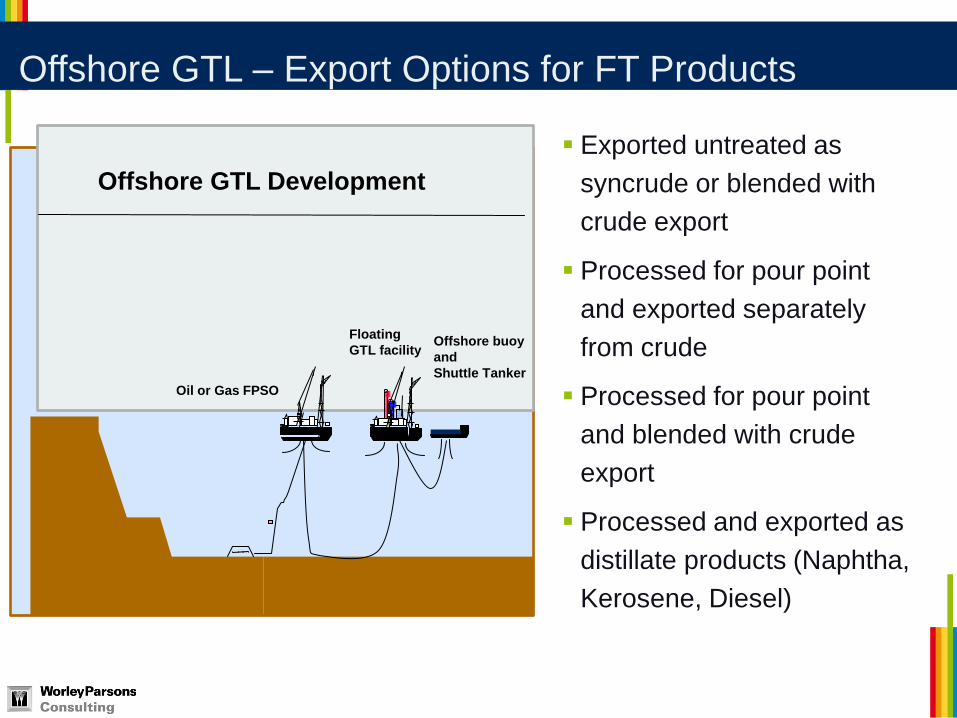

Offshore GTL – Export Options for FT Products

Exported untreated as

syncrude or blended with

crude export

Processed for pour point

and exported separately

from crude

Processed for pour point

and blended with crude

export

Processed and exported as

distillate products (Naphtha,

Kerosene, Diesel)

Offshore GTL Development

Floating

GTL facility

Oil or Gas FPSO

Offshore buoy

and

Shuttle Tanker

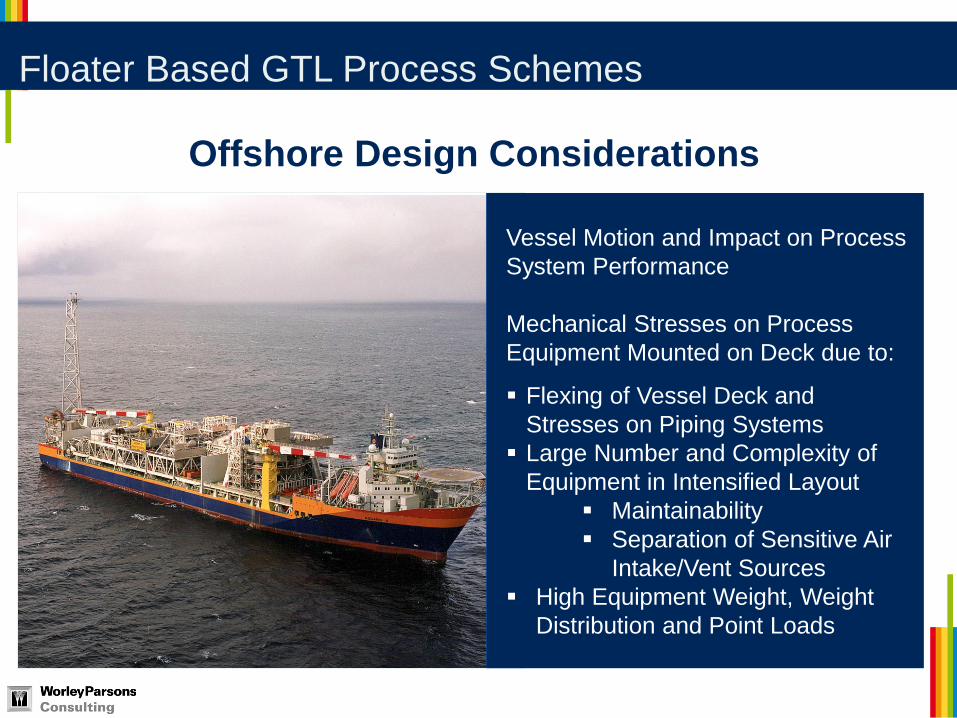

Vessel Motion and Impact on Process

System Performance

Mechanical Stresses on Process

Equipment Mounted on Deck due to:

Flexing of Vessel Deck and

Stresses on Piping Systems

Large Number and Complexity of

Equipment in Intensified Layout

Maintainability

Separation of Sensitive Air

Intake/Vent Sources

High Equipment Weight, Weight

Distribution and Point Loads

Offshore Design Considerations

Floater Based GTL Process Schemes

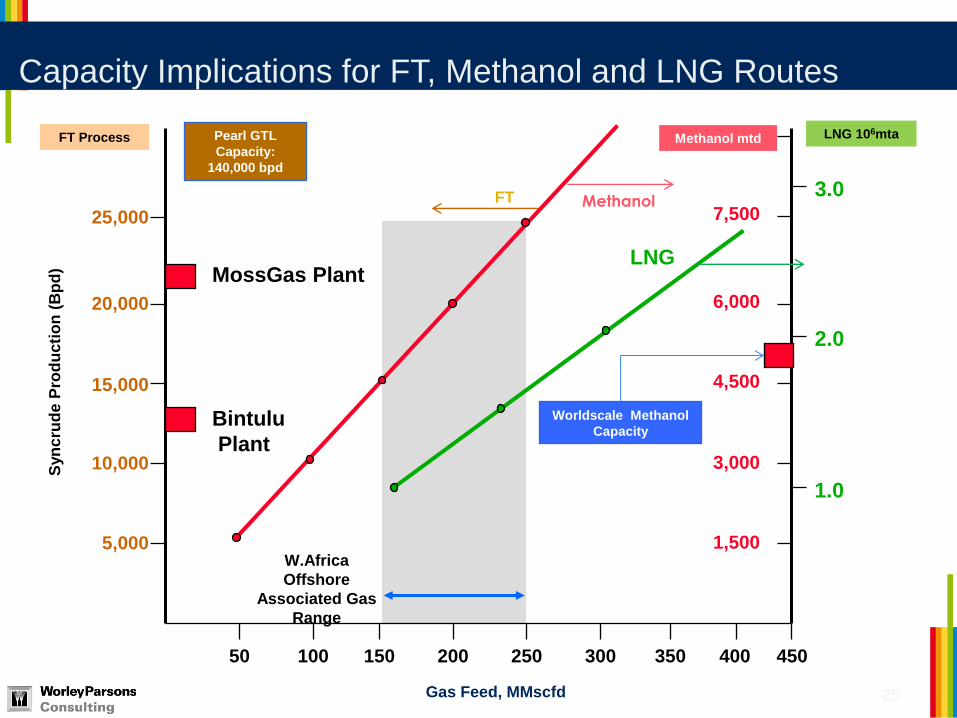

Capacity Implications for FT, Methanol and LNG Routes

25

25,000

20,000

15,000

10,000

5,000

50 100 150 200 250 300

Syn

cru

de

Pro

du

cti

on

(B

pd

)

FT Process Methanol mtd

MossGas Plant

Bintulu

Plant

LNG 106mta

7,500

6,000

4,500

3,000

1,500

1.0

2.0

3.0

350 400 450

Worldscale Methanol

Capacity

W.Africa

Offshore

Associated Gas

Range

Pearl GTL

Capacity:

140,000 bpd

LNG

FT

Gas Feed, MMscfd

Methanol

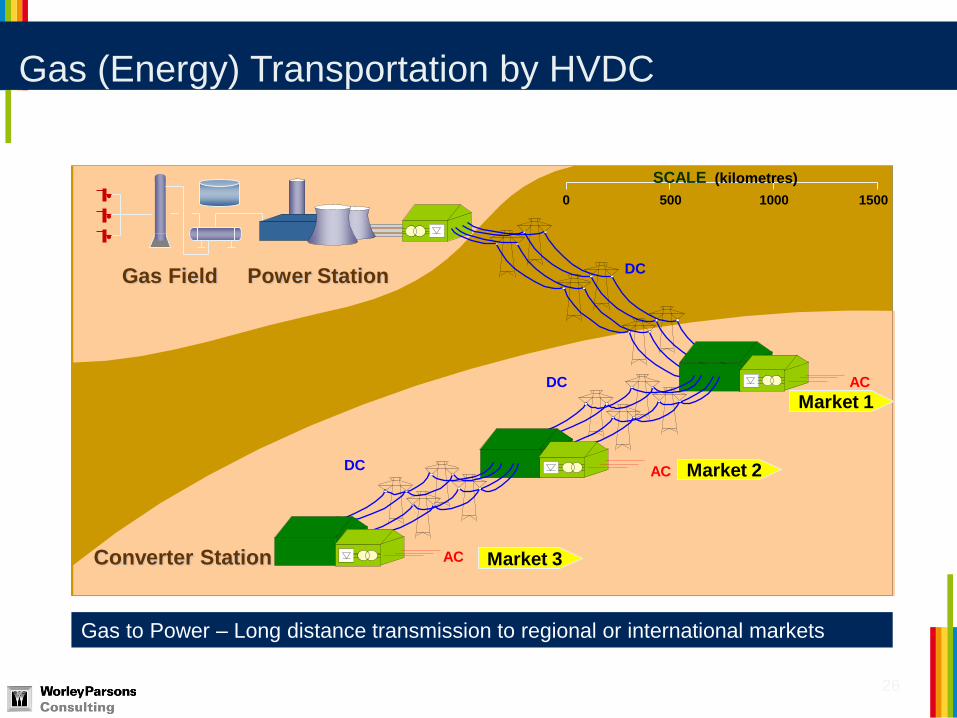

Gas (Energy) Transportation by HVDC

26

DC

DC

DC AC

AC

AC Market 3

Market 2

Market 1

Gas Field Power Station

•

• 0 500 1000 1500

SCALE

Converter Station

•

(kilometres)

Gas to Power – Long distance transmission to regional or international markets

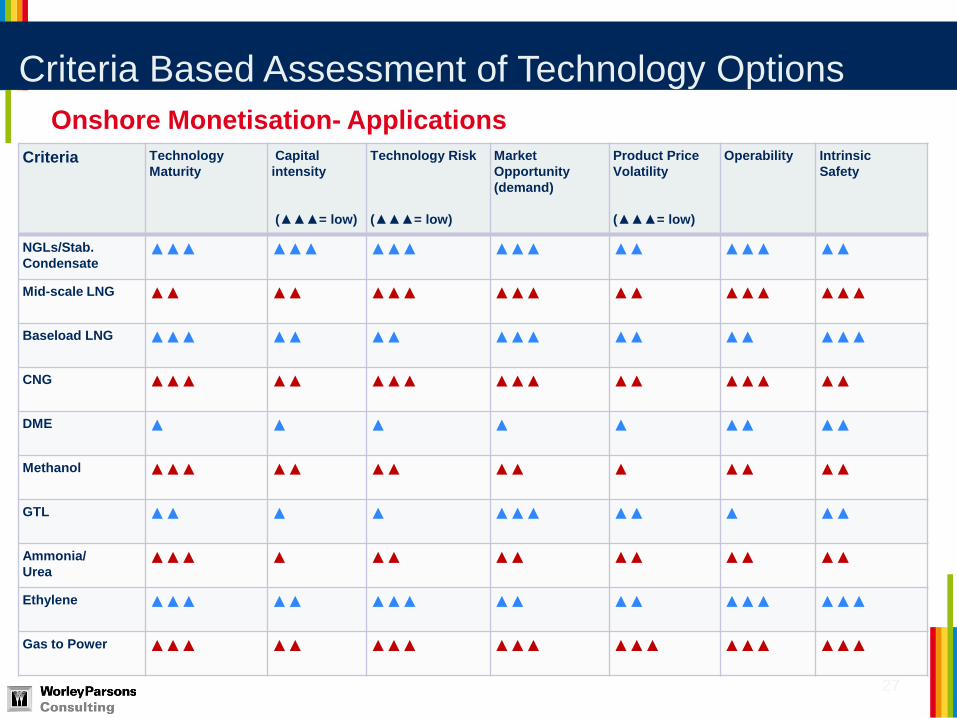

Criteria Based Assessment of Technology Options

27

Criteria Technology

Maturity

Capital

intensity

(▲▲▲= low)

Technology Risk

(▲▲▲= low)

Market

Opportunity

(demand)

Product Price

Volatility

(▲▲▲= low)

Operability Intrinsic

Safety

NGLs/Stab.

Condensate ▲▲▲ ▲▲▲ ▲▲▲ ▲▲▲ ▲▲ ▲▲▲ ▲▲

Mid-scale LNG ▲▲ ▲▲ ▲▲▲ ▲▲▲ ▲▲ ▲▲▲ ▲▲▲

Baseload LNG ▲▲▲ ▲▲ ▲▲ ▲▲▲ ▲▲ ▲▲ ▲▲▲

CNG ▲▲▲ ▲▲ ▲▲▲

▲▲▲ ▲▲ ▲▲▲ ▲▲

DME ▲

▲ ▲ ▲ ▲ ▲▲ ▲▲

Methanol ▲▲▲

▲▲

▲▲

▲▲

▲

▲▲

▲▲

GTL ▲▲

▲

▲

▲▲▲

▲▲

▲

▲▲

Ammonia/

Urea ▲▲▲

▲

▲▲

▲▲

▲▲

▲▲

▲▲

Ethylene ▲▲▲

▲▲

▲▲▲

▲▲

▲▲

▲▲▲

▲▲▲

Gas to Power ▲▲▲

▲▲

▲▲▲

▲▲▲

▲▲▲

▲▲▲

▲▲▲

Onshore Monetisation- Applications

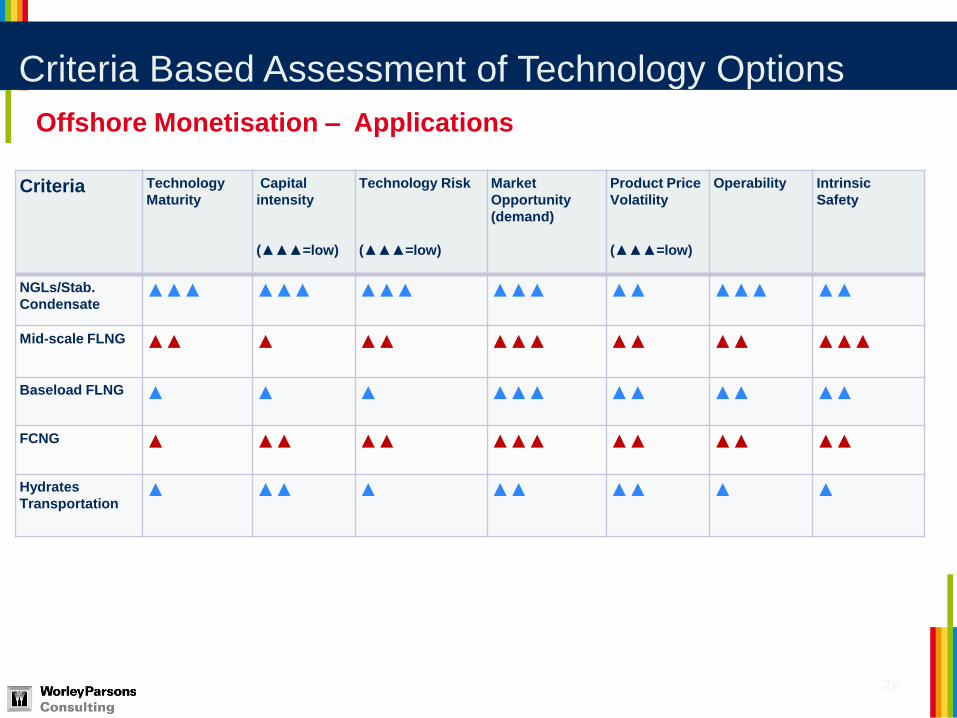

Criteria Based Assessment of Technology Options

28

Criteria Technology

Maturity

Capital

intensity

(▲▲▲=low)

Technology Risk

(▲▲▲=low)

Market

Opportunity

(demand)

Product Price

Volatility

(▲▲▲=low)

Operability Intrinsic

Safety

NGLs/Stab.

Condensate ▲▲▲ ▲▲▲

▲▲▲ ▲▲▲

▲▲

▲▲▲

▲▲

Mid-scale FLNG ▲▲ ▲

▲▲ ▲▲▲ ▲▲

▲▲

▲▲▲

Baseload FLNG ▲

▲

▲ ▲▲▲ ▲▲ ▲▲ ▲▲

FCNG ▲

▲▲

▲▲

▲▲▲ ▲▲

▲▲

▲▲

Hydrates

Transportation ▲ ▲▲ ▲ ▲▲ ▲▲ ▲ ▲

Offshore Monetisation – Applications

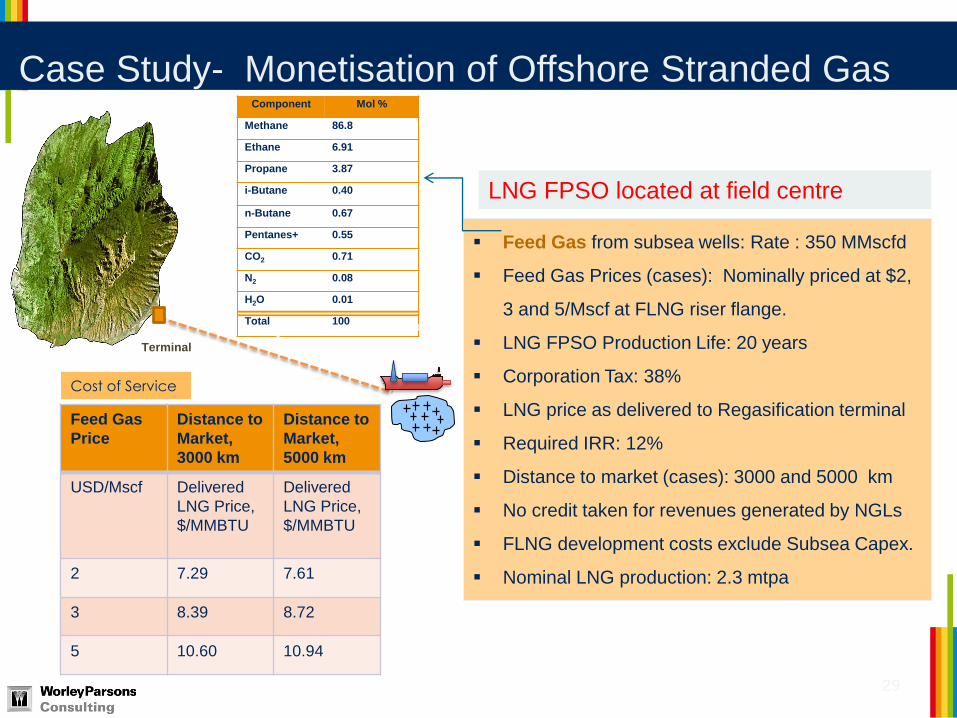

Case Study- Monetisation of Offshore Stranded Gas

29

Component Mol %

Methane 86.8

Ethane 6.91

Propane 3.87

i-Butane 0.40

n-Butane 0.67

Pentanes+ 0.55

CO2 0.71

N2 0.08

H2O 0.01

Total 100

Gas Field

FLNG or FCNG

Terminal

LNG FPSO located at field centre

Feed Gas

Price

Distance to

Market,

3000 km

Distance to

Market,

5000 km

USD/Mscf Delivered

LNG Price,

$/MMBTU

Delivered

LNG Price,

$/MMBTU

2 7.29 7.61

3 8.39 8.72

5 10.60 10.94

Feed Gas from subsea wells: Rate : 350 MMscfd

Feed Gas Prices (cases): Nominally priced at $2,

3 and 5/Mscf at FLNG riser flange.

LNG FPSO Production Life: 20 years

Corporation Tax: 38%

LNG price as delivered to Regasification terminal

Required IRR: 12%

Distance to market (cases): 3000 and 5000 km

No credit taken for revenues generated by NGLs

FLNG development costs exclude Subsea Capex.

Nominal LNG production: 2.3 mtpa

Cost of Service

Concluding Observations

30

Technology developments

herald unprecedented

opportunities for exploitation of

stranded gas.

Geography, size of gas reserves,

distance to markets etc will

determine the optimum mode of

energy delivery

Base load LNG remains a prime

contender for large stranded gas

reserves.

Mid-scale LNG technologies are

emerging as interesting options

for mid-tier gas reserves.

Ship transport of CNG has

commercial potential for energy

delivery to mid-markets &

regional markets.

Conventional Fischer Tropsch GTL offers key opportunities

for gas monetisation but scale of investment and project

risk are key co-determinants of application.

Horizon technology such as hydrates transport will further

expand an already impressive solutions portfolio.

Source : Alaska LNG