Languages

Pages

Legal

Using a Self-directed IRA to Create Hassle-free Cashflow

David Campbellwww.HasslefreeCashflowInvesting.com

Kaaren Hallwww.uDirectIRA.com

David Campbell

Former high school & college band director

Professional investorSelf-made multi-millionaire

Real estate developer

Real estate broker

Real estate & business advisor

Financial mentor

Over $800 million of real estate experience

Houses, condo-conversion, multi-family, winery, resort, office,

retail, medical office, commercial development, home building

California, Texas, North Carolina, Mexico, and Belize

Kaaren Hall, President

uDirect IRA Services, LLC

(866) 538-3539

uDirect IRA Services, LLC2522 Chambers Road, Ste 100

Tustin, CA 92780

Begin with end in mind

NOT a sales pitch

NOT investment, legal, or tax advice

NOT a securities offering

My Philanthropy: helping other people live more

abundant lives through hassle-free investments by

giving the knowledge and support for our others to

invest with mental tranquility.

WHAT THIS IS !

This IS a service to our existing clients

This IS an opportunity to introduce other

people to the possibility of living more abundant

lives through hassle-free investments by giving

the knowledge and support for our others to

invest with mental tranquility.

This IS a job interview

Husband

Father

Musician

Regular guy

Compelling WHY

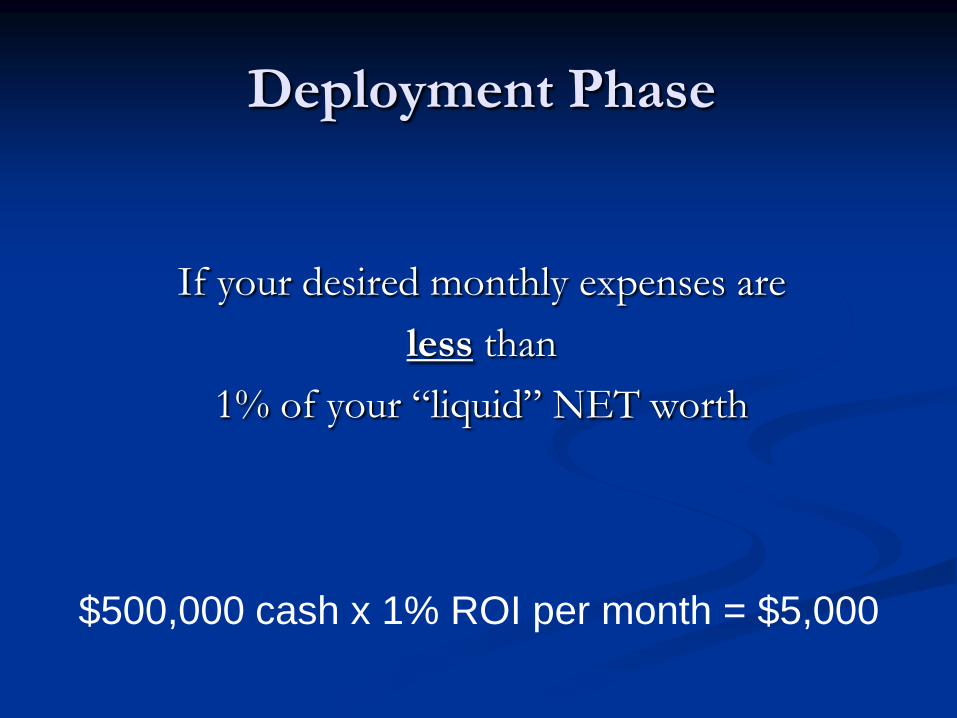

Deployment Phase

If your desired monthly expenses are

less than

1% of your “liquid” NET worth

$500,000 cash x 1% ROI per month = $5,000

If your desired monthly expenses are

greater than

1% of your “liquid” NET worth

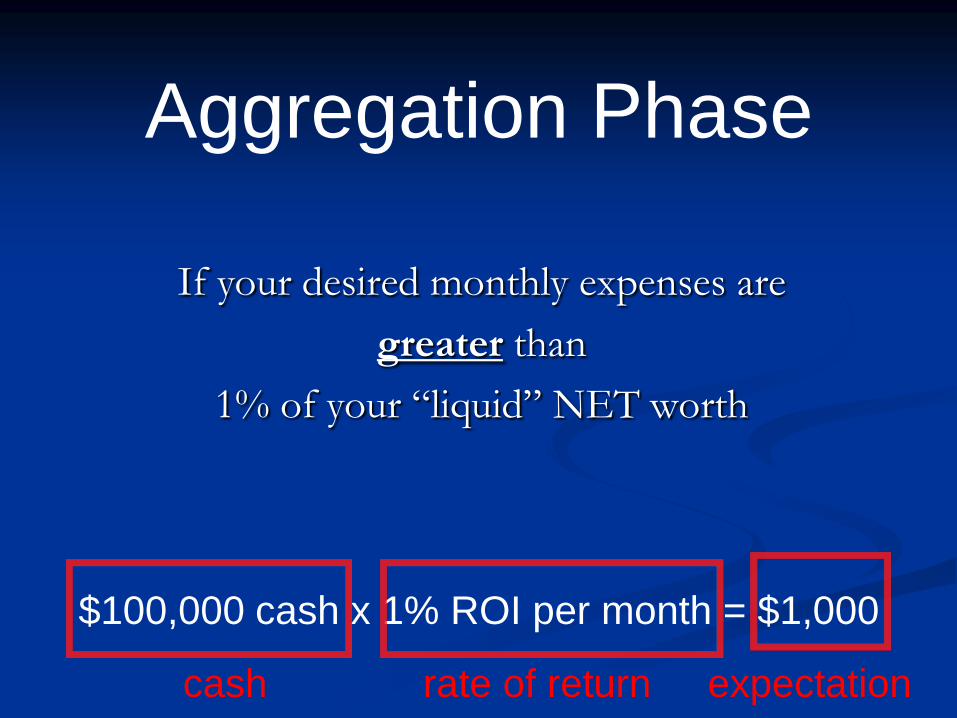

Aggregation Phase

$100,000 cash x 1% ROI per month = $1,000

If your desired monthly expenses are

greater than

1% of your “liquid” NET worth

Aggregation Phase

$100,000 cash x 1% ROI per month = $1,000

cash rate of return expectation

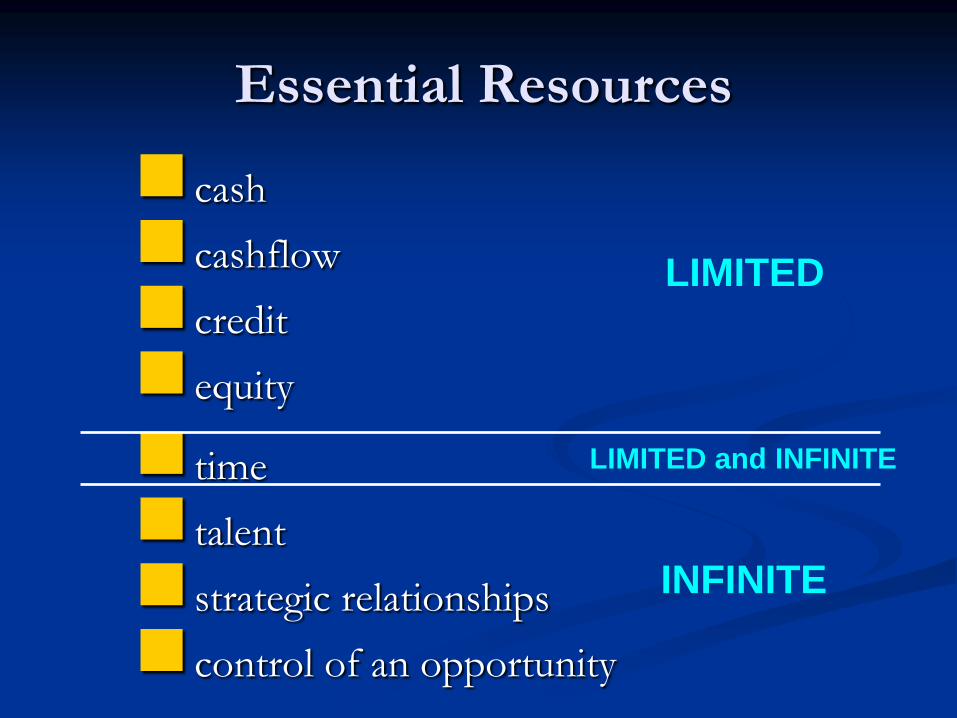

Essential Resources

cash

cashflow

credit

equity

time

talent

strategic relationships

control of an opportunity

LIMITED

INFINITE

LIMITED and INFINITE

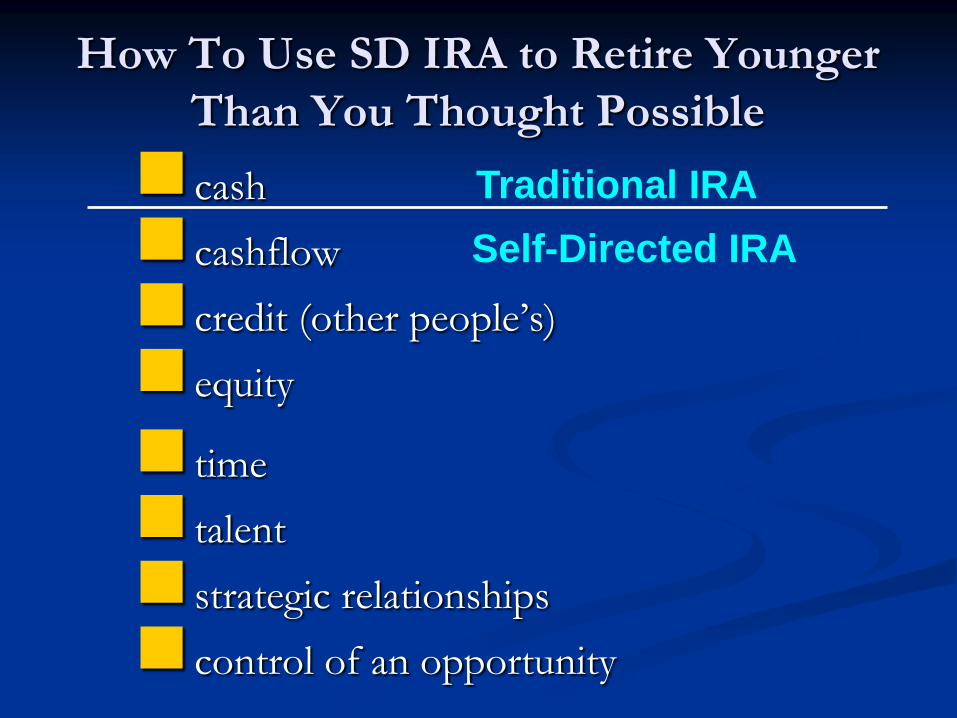

How To Use SD IRA to Retire Younger

Than You Thought Possible

cash

cashflow

credit (other people’s)

equity

time

talent

strategic relationships

control of an opportunity

Traditional IRA

Self-Directed IRA

How to Self-Direct Your Retirement Savings

uDirect IRA Services, LLC is not a fiduciary and does not render tax, legal, accounting, investment, or other professional advice. If tax, legal, accounting, investment, or other similar expert assistance is required, the services of a competent professional should be sought.

Self-DirectionWhy Haven’t I Heard About This?

• Few attorneys are knowledgeable – About self-directed plans

• Few CPAs are knowledgeable– About self-directed plans

• IRS rules have allowed self-direction since IRAs were created in mid-1970s

What’s the Difference?

Typical IRA

• Stocks

• Bonds

• Mutual Funds

• CD’s

Self-Directed IRA

• Rental Property

• Notes

• Private Stock

• LLC’s

• Tax Liens

• Foreign Property

• Raw Land

• Etc.

What About Losses?

Losses

• Cannot be written off taxes

• Cannot be replaced in the retirement plan

What Are The Limits?

A Self-Directed IRA can invest in anything EXCEPT

1. Life Insurance Policies

2. Collectibles1. Artworks

2. Coins

3. Collectible Cars

4. Antiques

5. Gems

6. Stamps

7. Rugs

What if your funds are with your current employer?

Your plan will probably NOT allow you to self-direct

Must wait until you leave the companyTo rollover retirement plan

You can request an “in-service” transfer from your current plan administrator.

Prohibited Transactions(IRS Publication 590)

• Borrowing money from the IRA

• Selling property to it.

• Using it as security for a loan.

• Buying property for personal use (present or future) with IRA funds.

Disqualified Person

• Disqualified persons include your fiduciary and members of your family (spouse, ancestor, lineal descendant, and any spouse of a lineal descendant).

Qualified Persons

• Aunts & Uncles

• Cousins

• Brothers & Sisters

• Unrelated friends

• Nieces & Nephews

Prohibited Transactions

• Neither you nor any disqualified people may benefit from IRA

• Cannot buy, sell or exchange property between plan and

– Self or

– Disqualified people

• Cannot provide goods, services or facilities

Self-Directed IRA - Structure

• You

• Your IRA

• TPA

• Custodian

Buying Real Estate With Your IRA

Pros

1. Capital gains are tax free

2. Positive cash flow is tax free

3. No time limit for holding property

4. IRA can borrow money

– Leverage your investment

5. Potential to earn a larger rate of return on invested capital

Buying Real Estate With Your IRA

Cons

1. No tax advantages of owning real estate

2. No deduction for capital losses

3. You are solely responsible for all gains or losses

4. You cannot replace losses

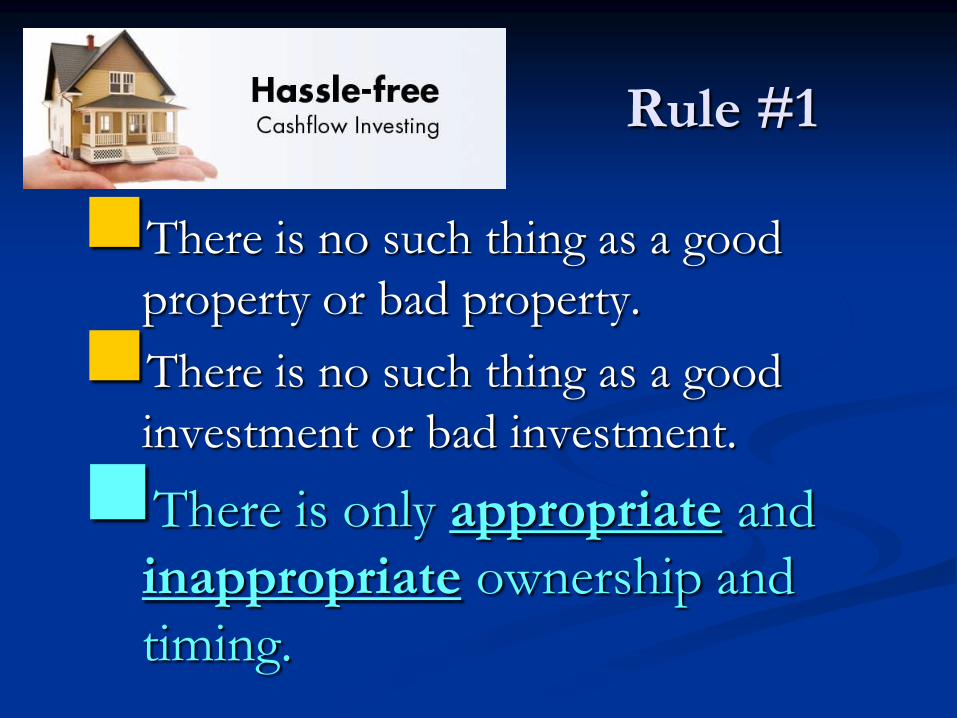

Rule #1

There is no such thing as a good

property or bad property.

There is no such thing as a good

investment or bad investment.

There is only appropriate and

inappropriate ownership and

timing.

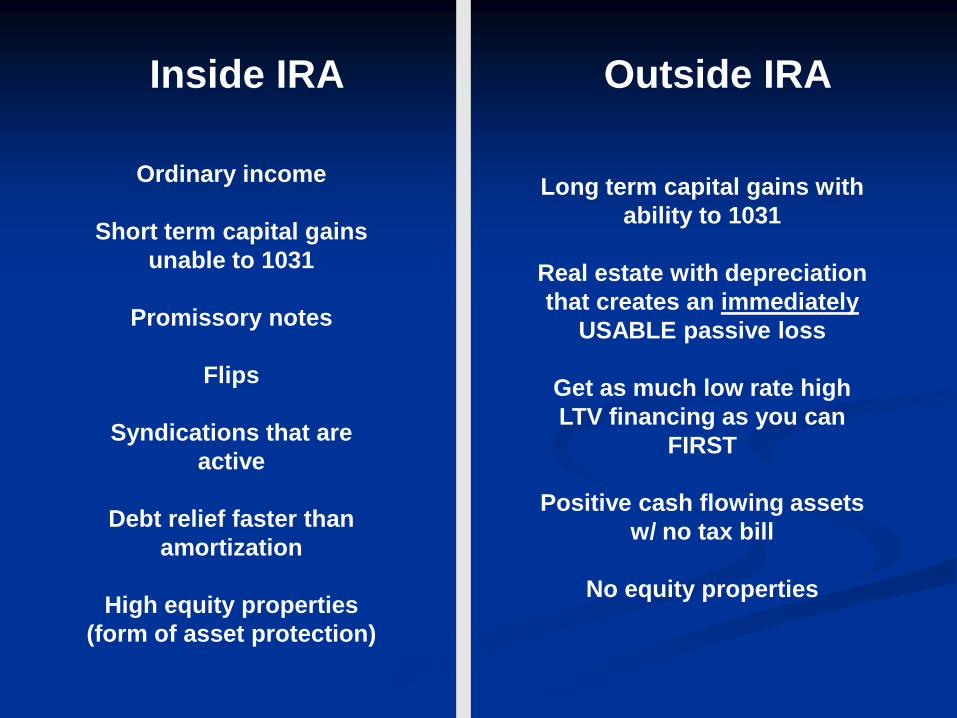

Inside IRA

Ordinary income

Short term capital gains

unable to 1031

Promissory notes

Flips

Syndications that are

active

Debt relief faster than

amortization

High equity properties

(form of asset protection)

Long term capital gains with

ability to 1031

Real estate with depreciation

that creates an immediately

USABLE passive loss

Get as much low rate high

LTV financing as you can

FIRST

Positive cash flowing assets

w/ no tax bill

No equity properties

Outside IRA

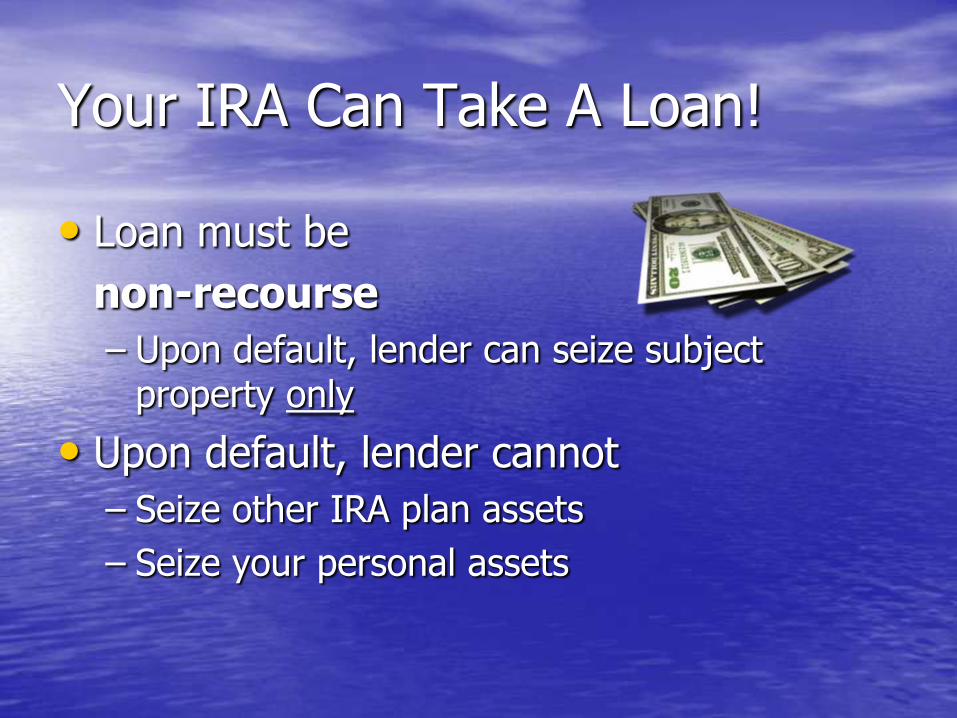

Your IRA Can Take A Loan!

• Loan must be

non-recourse

– Upon default, lender can seize subject property only

• Upon default, lender cannot

– Seize other IRA plan assets

– Seize your personal assets

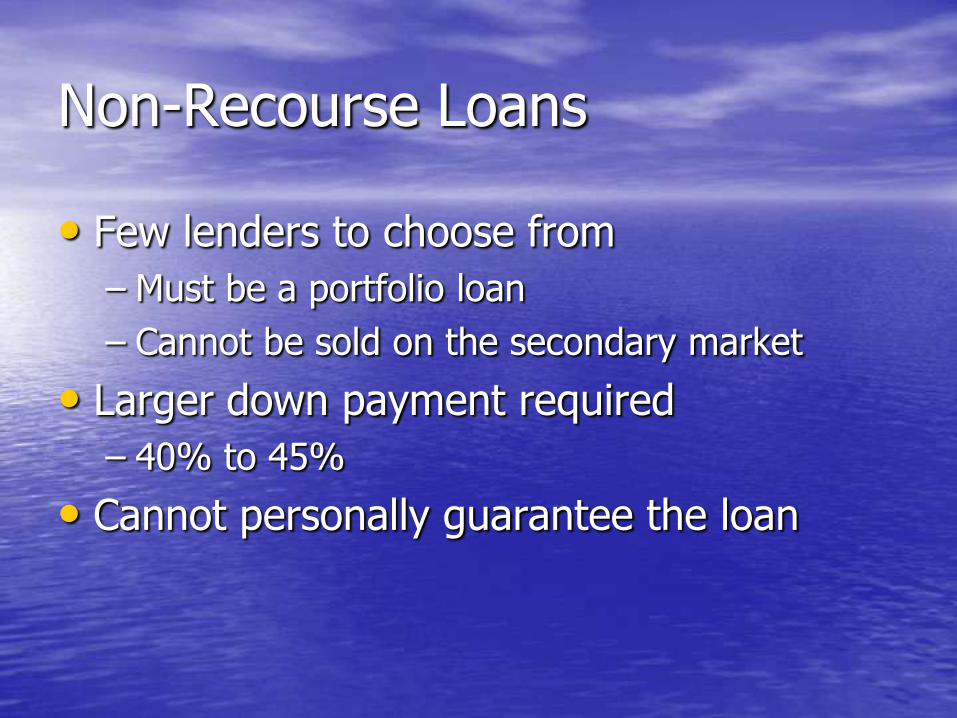

Non-Recourse Loans

• Few lenders to choose from

– Must be a portfolio loan

– Cannot be sold on the secondary market

• Larger down payment required

– 40% to 45%

• Cannot personally guarantee the loan

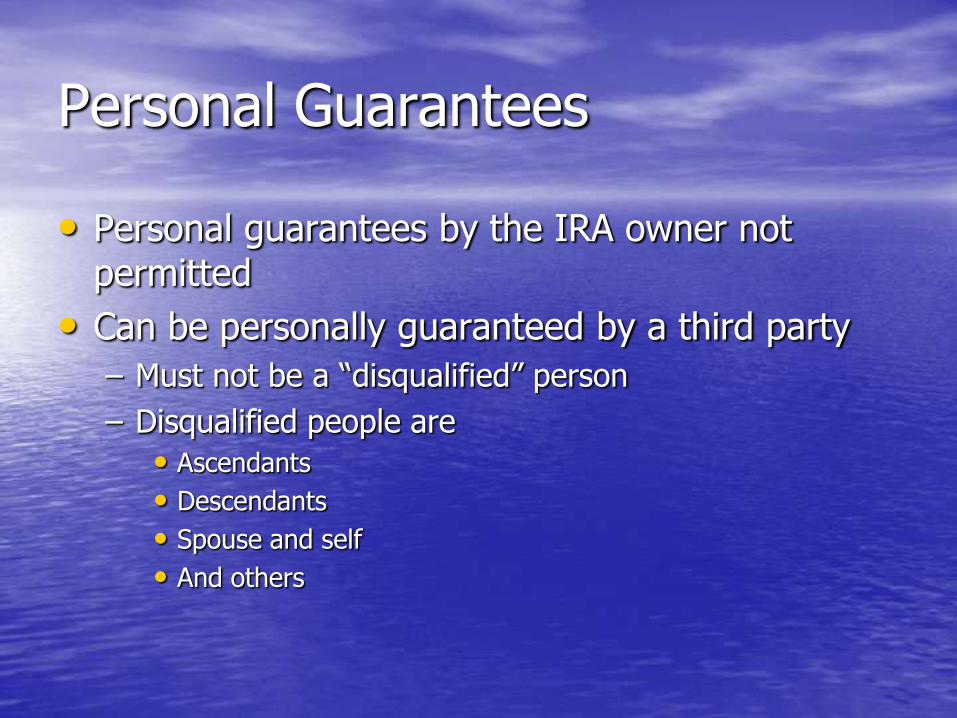

Personal Guarantees

• Personal guarantees by the IRA owner not permitted

• Can be personally guaranteed by a third party

– Must not be a “disqualified” person

– Disqualified people are

• Ascendants

• Descendants

• Spouse and self

• And others

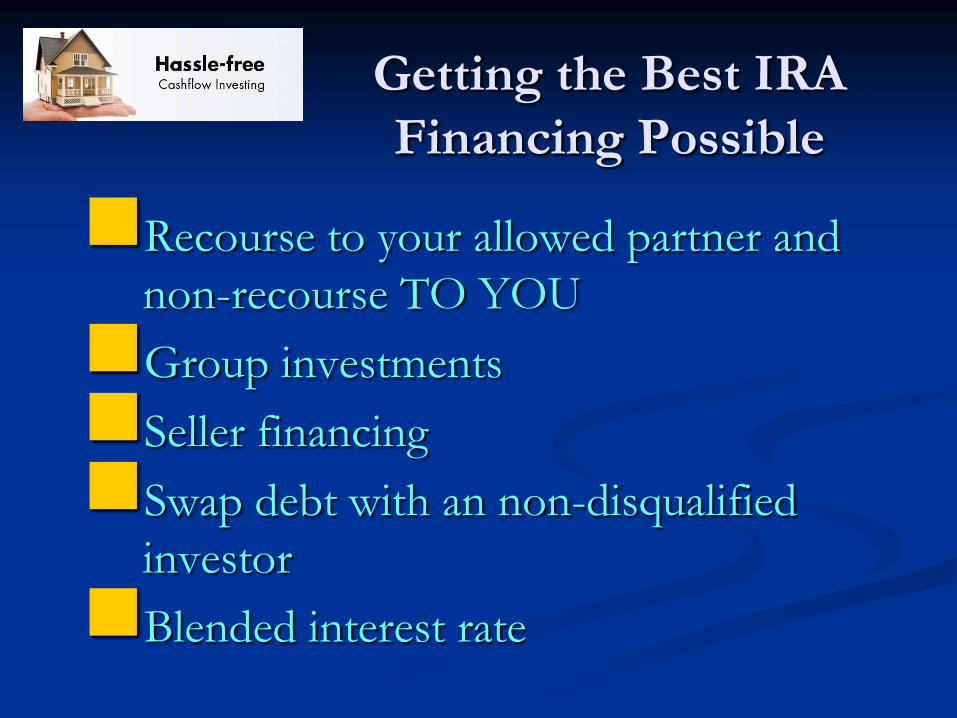

Getting the Best IRA

Financing Possible

Recourse to your allowed partner and

non-recourse TO YOU

Group investments

Seller financing

Swap debt with an non-disqualified

investor

Blended interest rate

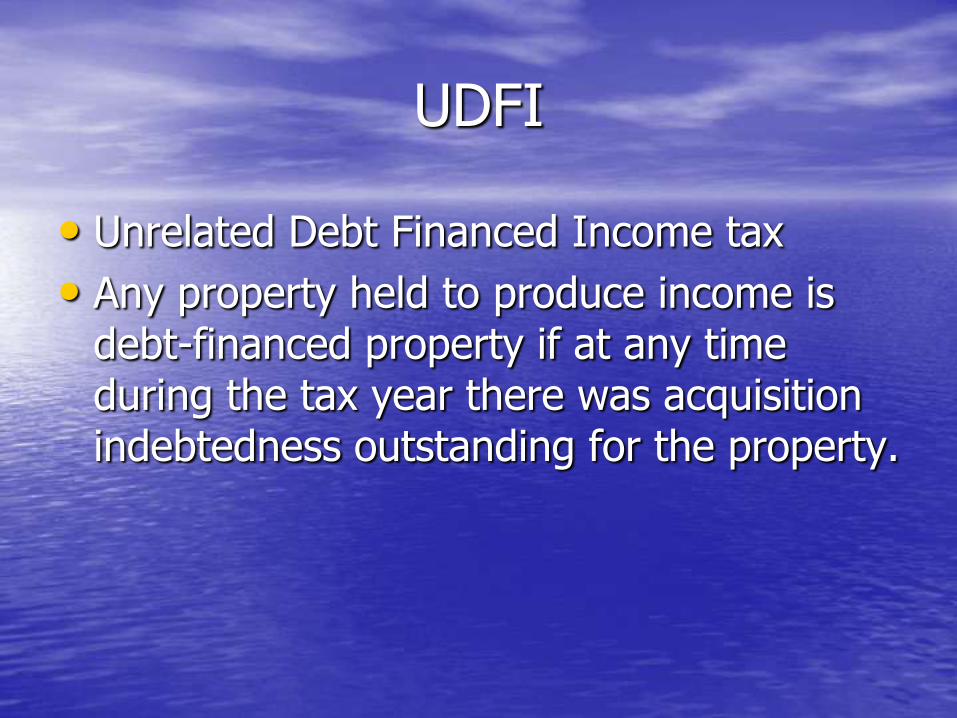

UDFI

• Unrelated Debt Financed Income tax

• Any property held to produce income is debt-financed property if at any time during the tax year there was acquisition indebtedness outstanding for the property.

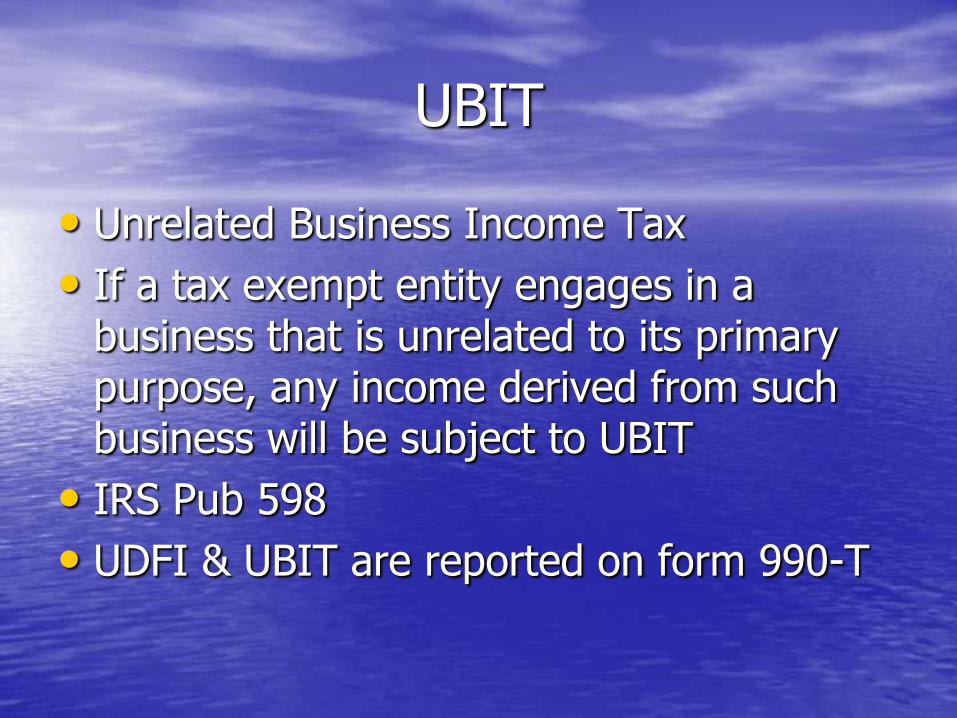

UBIT

• Unrelated Business Income Tax

• If a tax exempt entity engages in a business that is unrelated to its primary purpose, any income derived from such business will be subject to UBIT

• IRS Pub 598

• UDFI & UBIT are reported on form 990-T

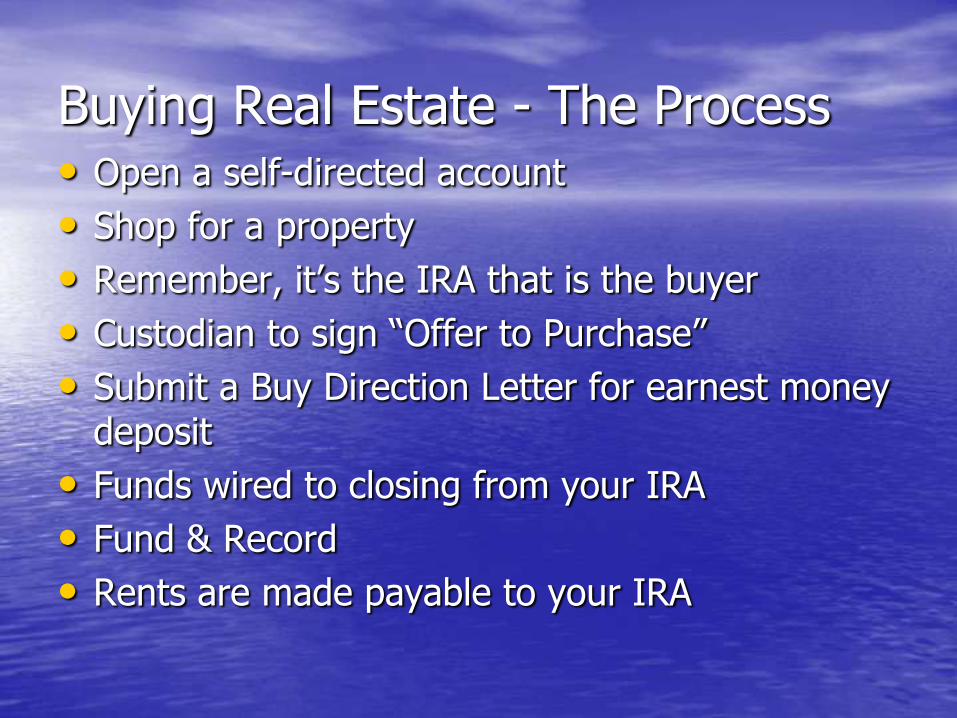

Buying Real Estate - The Process• Open a self-directed account

• Shop for a property

• Remember, it’s the IRA that is the buyer

• Custodian to sign “Offer to Purchase”

• Submit a Buy Direction Letter for earnest money deposit

• Funds wired to closing from your IRA

• Fund & Record

• Rents are made payable to your IRA

Example

Father & Son buy a house

Father: 50% Cash

Son: 50% Traditional IRA

Title reads as:

Custodian FBO Son’s IRA 50%, Father 50%, TIC

Disqualified?

• Before the deal

– Father has no ownership

– Son’s Traditional IRA has no ownership

• Because this is a new deal

– Father and son do not have to worry about the “disqualified person” rule

Disqualified?

• After the deal

– The “disqualified person” rule comes into effect

• Neither Father nor Son can live in the condo

– No one who is disqualified to either of them can live in the house

• Ascendants, descendants, etc.

After the deal….

• After the deal

• Neither Father nor Son can ever buy out each other’s ownership

– They are disqualified to each other

• Expenses and profits are split

– 50% to Father

• Taxable

– 50% to Son’s Traditional IRA

• Tax-deferred

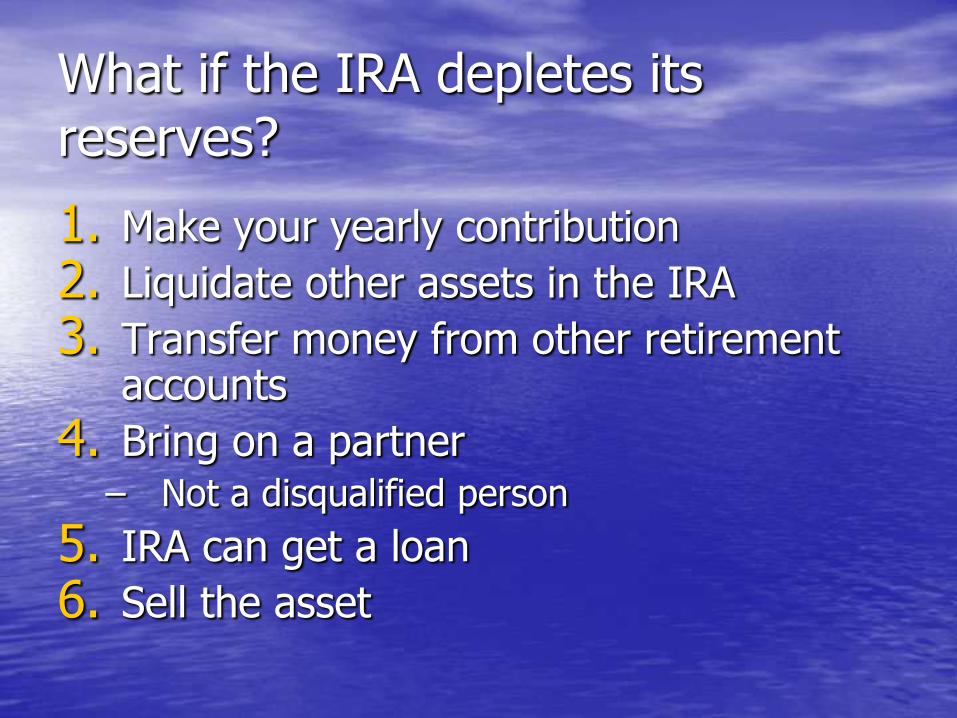

What if the IRA depletes its reserves?

1. Make your yearly contribution

2. Liquidate other assets in the IRA

3. Transfer money from other retirement accounts

4. Bring on a partner– Not a disqualified person

5. IRA can get a loan

6. Sell the asset

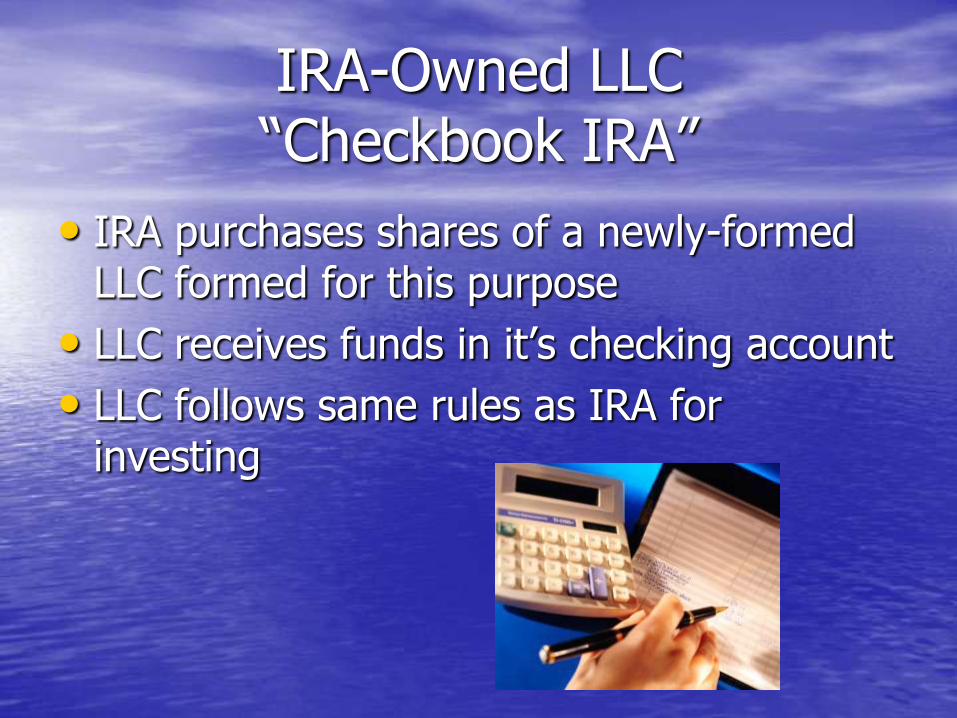

IRA-Owned LLC“Checkbook IRA”

• IRA purchases shares of a newly-formed LLC formed for this purpose

• LLC receives funds in it’s checking account

• LLC follows same rules as IRA for investing

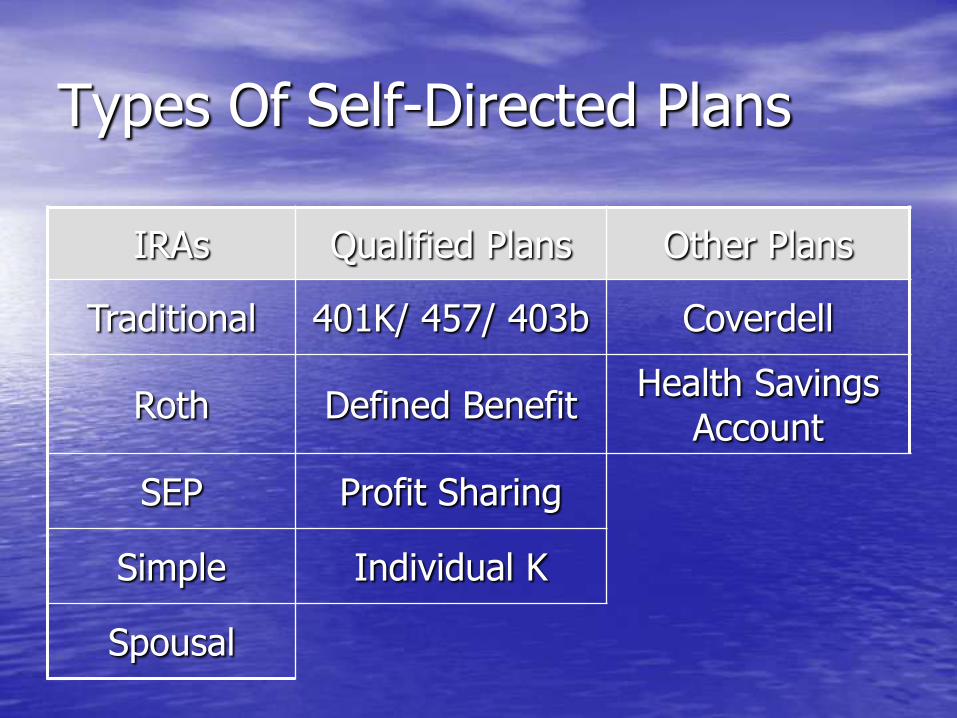

3 Types of Plans

• IRAs– Individual Retirement Accounts

– What you are doing for your own retirement

• Qualified Plans– ERISA controlled

– Typically, what an employer provides you

• Other Plans– Education

– Health

Types Of Self-Directed Plans

IRAs Qualified Plans Other Plans

Traditional 401K/ 457/ 403b Coverdell

Roth Defined BenefitHealth Savings

Account

SEP Profit Sharing

Simple Individual K

Spousal

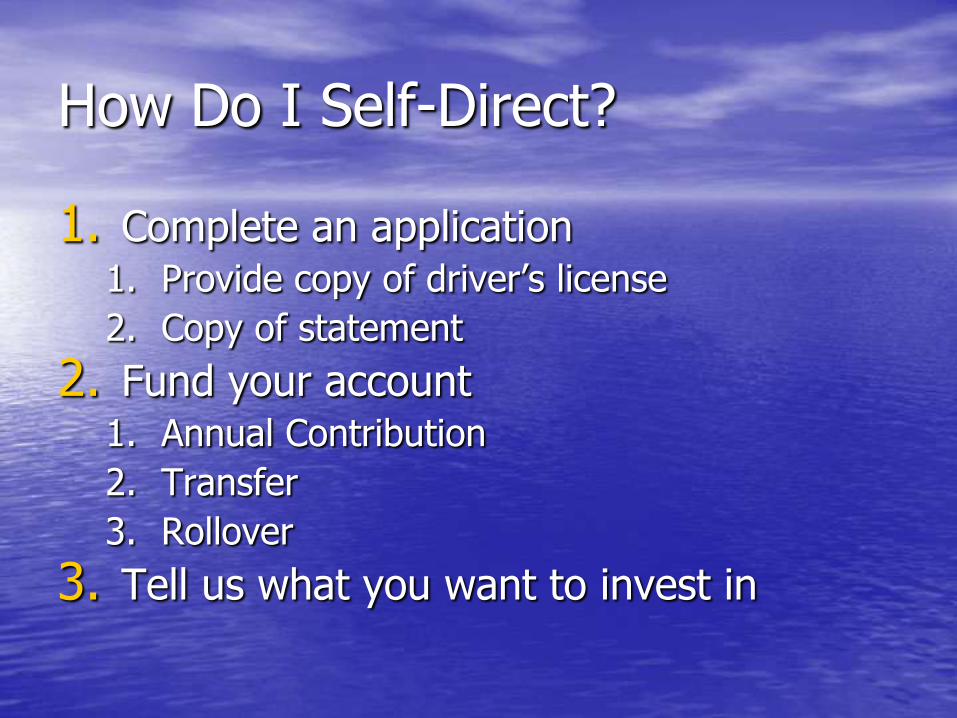

How Do I Self-Direct?

1. Complete an application1. Provide copy of driver’s license

2. Copy of statement

2. Fund your account1. Annual Contribution

2. Transfer

3. Rollover

3. Tell us what you want to invest in

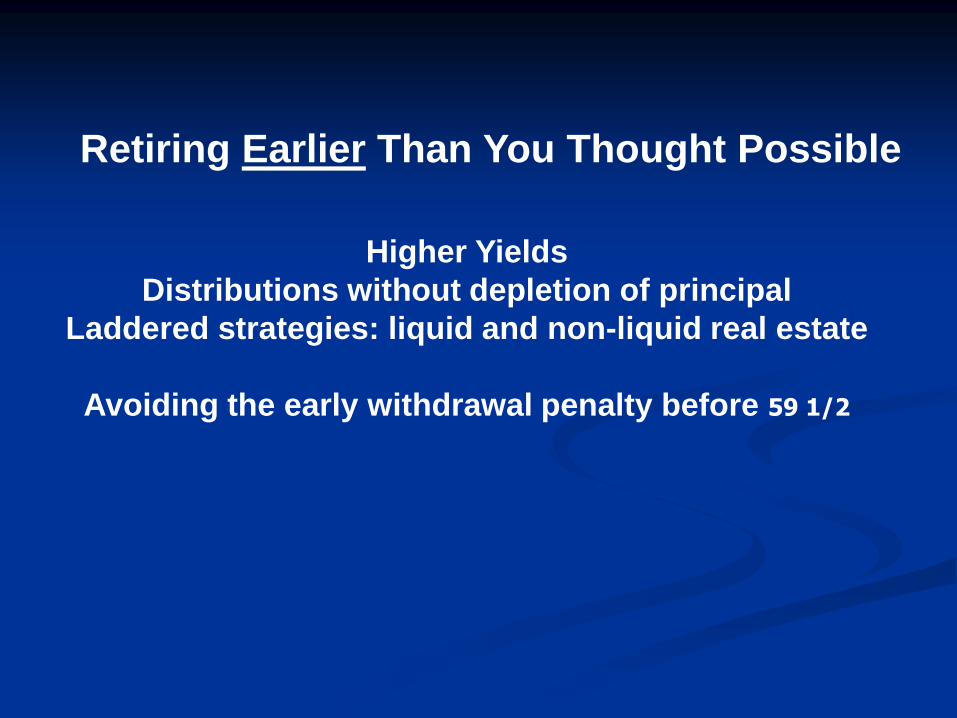

Retiring Earlier Than You Thought Possible

Higher Yields

Distributions without depletion of principal

Laddered strategies: liquid and non-liquid real estate

Avoiding the early withdrawal penalty before 59 1/2

Retirement Distributions at Any Age

NO early withdrawal penalty

Substantially equal payments for 5 years

or until 59 ½ years old

Early withdrawal penalty EXEMPTION

“IRS 72 t”

$500,000 principal x 20% ROI = $100,000 annual profit

$50,000 profit distributed and TAXED as ordinary income

$50,000 income remains in IRA and is TAX DEFERRED

Rule #1

There is no such thing as a good

property or bad property.

There is no such thing as a good

investment or bad investment.

There is only appropriate and

inappropriate ownership and

timing.

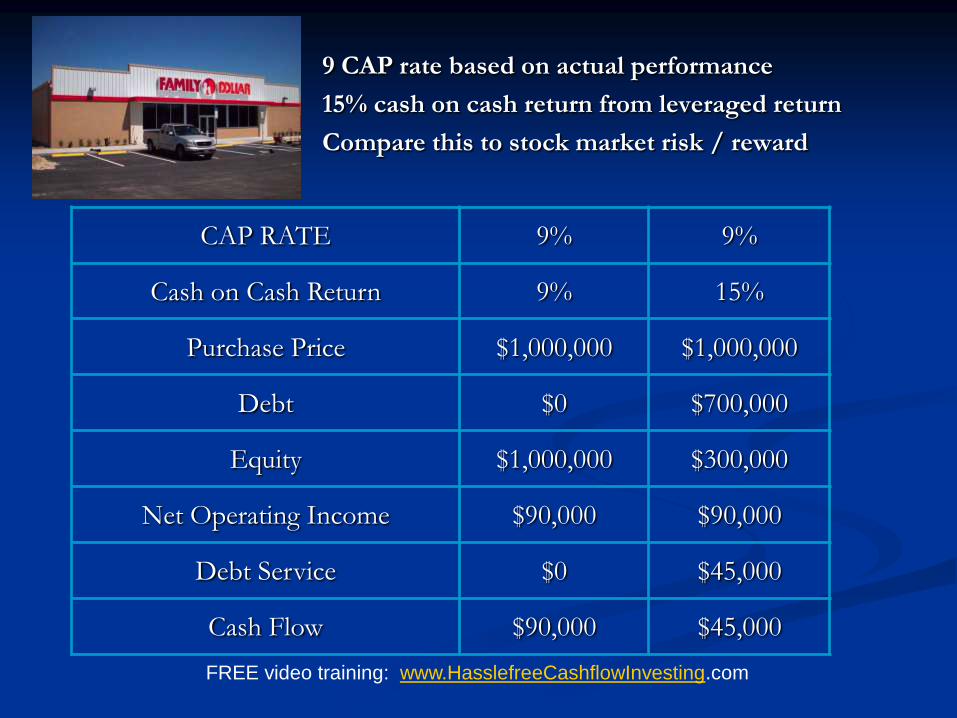

9 CAP rate based on actual performance

15% cash on cash return from leveraged return

Compare this to stock market risk / reward

CAP RATE 9% 9%

Cash on Cash Return 9% 15%

Purchase Price $1,000,000 $1,000,000

Debt $0 $700,000

Equity $1,000,000 $300,000

Net Operating Income $90,000 $90,000

Debt Service $0 $45,000

Cash Flow $90,000 $45,000

FREE video training: www.HasslefreeCashflowInvesting.com

must take house

Paid $30,000

Rehab: $15,000

Appraised: $55,000

Rents: $550/month

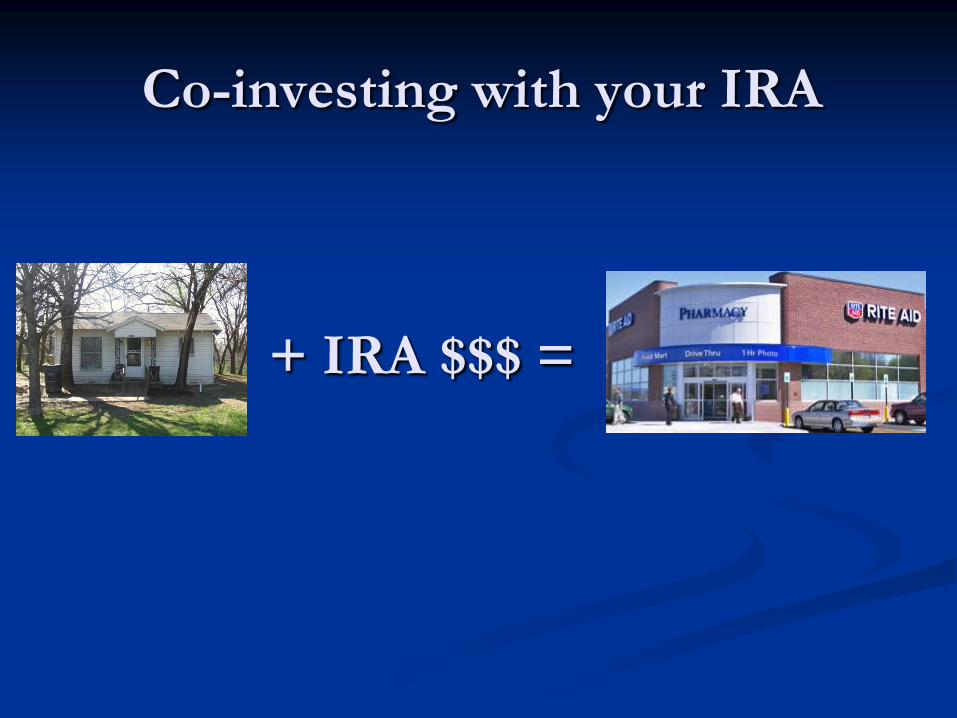

Co-investing with your IRA

+ IRA $$$ =

Real estate equity as a down

party 1 party 2

property House Rite Aid

value $500,000 $4,000,000

debt $100,000 $2,500,000

real estate equity $400,000 $1,500,000

cash to balance $1,100,000 $0

TOTAL EQUITIES $1,500,000 $1,500,000

Personal Investment Philosophy

FREE Consultation

Passive investing

Active syndicating

Equity Exchanging

New Houses In Dallas

Hard Money Lending

Creative solutionist

Dallas Field Trip

REG Cruise

“There are no risky investments, only

risky investors.”

- Robert Kiyosaki

Real Estate Guys

10th Annual Investor Summit at SeaMarch 30th

– April 7th, 2012

FACULTY: Robert and Kim Kiyosaki, David Campbell,

Rich Dad Advisors - Ken McElroy, Wayne Palmer, Tom Wheelwright, Wayne Kirk,

Robert Helms and Russell Gray - Hosts of the Real Estate Guys Radio Program.

Using a Self-directed IRA to Create

Hassle-free Cashflow

David Campbellwww.HasslefreeCashflowInvesting.com

Kaaren Hallwww.uDirectIRA.com