Languages

Pages

Legal

Status of Coal-Fired Power Plants in Poland

2013 U.S.-Poland Energy Roundtable

Territory: 322 575 km2 Population: 38.5 mln Capital city: Warsaw

Polish Power System

key figures 2012

Installed capacity: 38 GW

Available capacity: 37.7 GW

Reliable capacity of domestic power stations: 28.5 GW

Maximum demand: 25.8 GW

Gross electricity generation : 162 TWh

Gross consumption: 159 TWh

Length of transmission electric lines (750kV and 220 kV): 13 500 km

Length of distribution electric lines (110 kV and low lines): 774 200 km

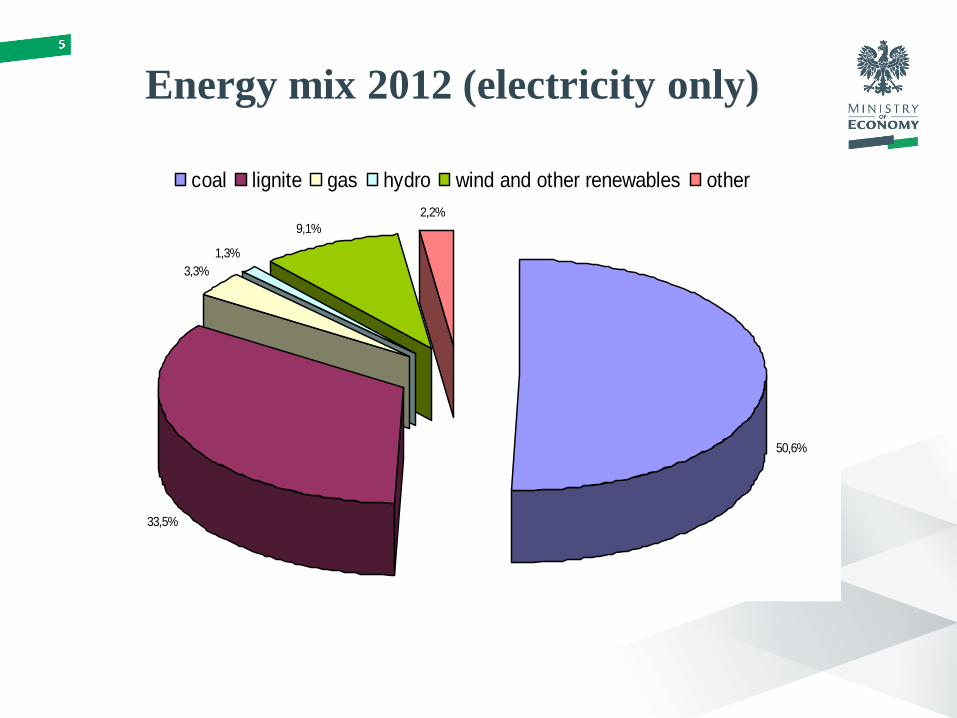

Energy mix 2012 (electricity only)

50,6%

33,5%

3,3%

1,3%

9,1%

2,2%

coal lignite gas hydro wind and other renewables other

6

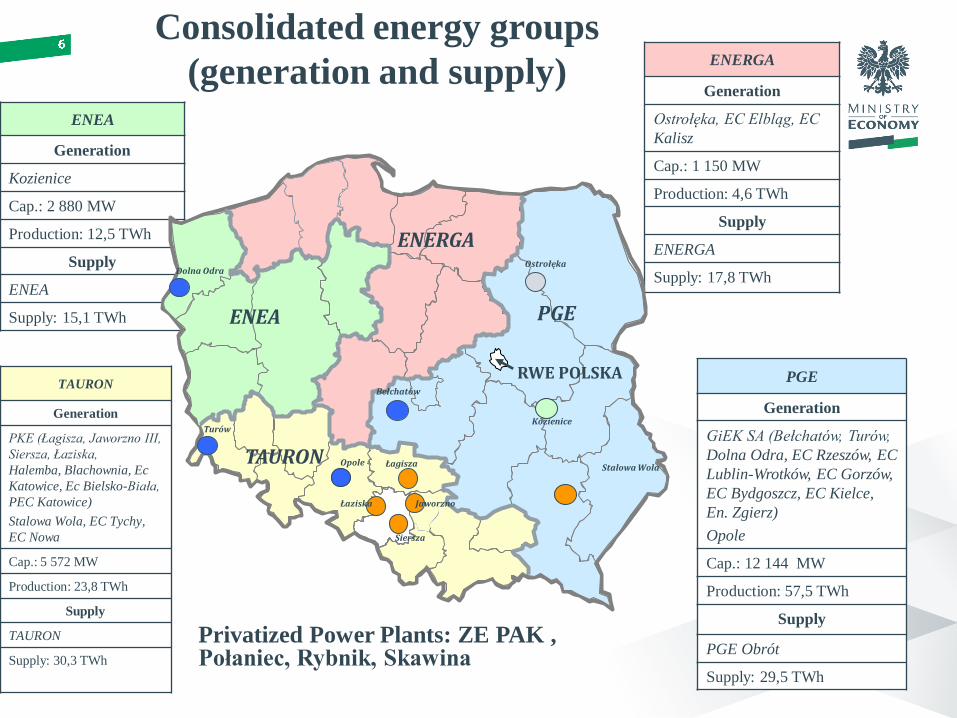

ENEA

Generation

Kozienice

Cap.: 2 880 MW

Production: 12,5 TWh

Supply

ENEA

Supply: 15,1 TWh

ENERGA

Generation

Ostrołęka, EC Elbląg, EC

Kalisz

Cap.: 1 150 MW

Production: 4,6 TWh

Supply

ENERGA

Supply: 17,8 TWh

TAURON

Generation

PKE (Łagisza, Jaworzno III,

Siersza, Łaziska,

Halemba, Blachownia, Ec

Katowice, Ec Bielsko-Biała,

PEC Katowice)

Stalowa Wola, EC Tychy,

EC Nowa

Cap.: 5 572 MW

Production: 23,8 TWh

Supply

TAURON

Supply: 30,3 TWh

PGE

Generation

GiEK SA (Bełchatów, Turów,

Dolna Odra, EC Rzeszów, EC

Lublin-Wrotków, EC Gorzów,

EC Bydgoszcz, EC Kielce,

En. Zgierz)

Opole

Cap.: 12 144 MW

Production: 57,5 TWh

Supply

PGE Obrót

Supply: 29,5 TWh

Privatized Power Plants: ZE PAK , Połaniec, Rybnik, Skawina

PKE

PGE

(BOT)

Enion

Energia Pro

Ł - 2

ŁZE

Łódź Teren L - 5

(WGE)

RZE

Energetyka

Podkarpacka

ENEA

El. Kozienice

ENERGA

PAK (50%)

Brunatnego

Z. El. Ostrołęka

TAURON

PGE ENEA

Dolna Odra

ENERGA Ostrołęka

Turów

Opole

Bełchatów

Łaziska Jaworzno

Łagisza

RWE POLSKA

Kozienice

Siersza

Stalowa Wola

Consolidated energy groups

(generation and supply)

Major power plants in Poland

Bełchatów

12x370 MW

1x858 MW

(new)

Kozienice

2x500+8x225 MW

Stalowa Wola

2x125 MW

Połaniec

8x225 MW

Dolna Odra

8x220 MW

Rybnik

8x225 MW

Pątnów

6x200 MW

Adamów

5x120 MW

Konin

2x120 MW

Łaziska

2x125+4x225 MW

Ostrołęka

3x220 MW

Jaworzno

6x225 MW

Łagisza

7x120 MW

Siersza

2x160+4x120 MW

Skawina

4x110 MW

Turów

3x260 + 3x235 + 3x200 MW

Porąbka-Żar

4x135 MW

Żarnowiec

4x180 MW

water pump

storage

plant

Opole

4x380 MW

lignite

hard coal

Generation of

electricity

Electricity generation [TWh]

lata

Years 2007 2008 2009 2010 2011 2012

0 1 2 3 4 5 6

Total generation 159.3 155.3 151.7 157.7 163.5 162

Hard coal 92.8 85.6 83.2 87.9 87.3 82

Lignite 51.0 53.2 50.2 48.7 52.5 54.2

Hard coal+lignite 143.8 138.8 133.4 136.6 139.8 136.2

Electricity generation from

hard coal and lignite

Age structure of electricity generation

devices

4,95 4,667,02 7,91

3,11 4,156,71 6,81

13,37 14,0417,33 17,96

47,5344,47

0

10

20

30

40

50

boilers turbosets

[%]

under 5 years 5-10 years 10-15years 15-20 years 20-25 years 25-30 years over 30 years

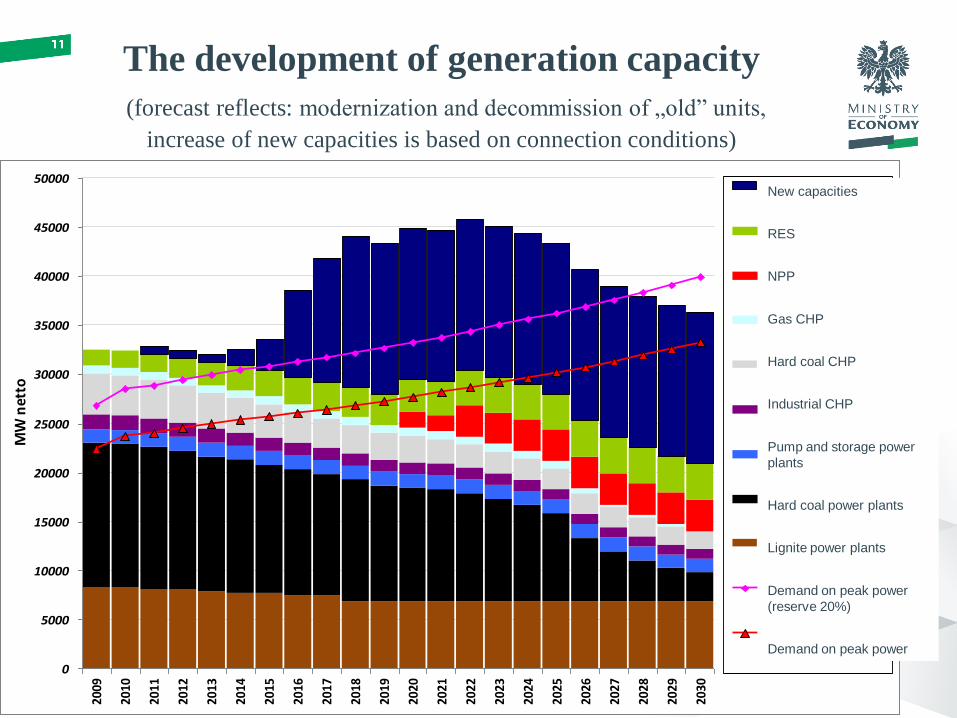

The development of generation capacity

(forecast reflects: modernization and decommission of „old” units,

increase of new capacities is based on connection conditions)

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

50000

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

MW

net

to

Nowe moce (warunkiprzyłączeniowe)

OZE (mocdyspozycyjna)

EL_Jądrowe

EC_Gaz

EC_WK

EC_Przemysłowe

EL_Pompowe

EL_WK_Stare

EL_WB_Stare

Zapotrzebowanie namoc szczytową imargines mocy (+20%)Zapotrzebowanie namoc szczytową netto

New capacities

RES

NPP

Gas CHP

Hard coal CHP

Industrial CHP

Pump and storage power

plants

Hard coal power plants

Lignite power plants

Demand on peak power

(reserve 20%)

Demand on peak power

Losses and increase in power generation from coal

based on estimates of energy producers

The installed capacity will decrease by 2015 by about 1100 MW.

By 2025 total decrease will reach a level of 2500 MW

At the same time it is planned to install 10 600 MW of new capacities till 2025

It is planned that total increase in installed capacity till 2025

will reach a level of 8100 MW

Thank you for your attention

Energy Department

Top Related