Languages

Pages

Legal

U.S. employment situation: September 2013

Release date: October 22, 2013

2016’s volatility continues, but overall

picture remains healthy

U.S. employment situation: August 2016 September 2, 2016

August 2016 employment summary

• After a rebound in June and July, volatility returns

- 151,000 net new jobs were created in August, falling below the 250,000+ monthly additions over the previous two months. Although still at

average levels of growth, August demonstrated the continued volatility of the labor market in 2016, which has at times both sharply

exceeded and underperformed compared to estimates and consensus figures.

- Unemployment once again remained stable at 4.9 percent as growth in the workforce has aligned with employment gains. Due to the

stability of the official rate as well as total and white-collar unemployment in recent months, we believe that the market’s cyclical low in

terms of unemployment has likely been reached.

• Tech is now correcting, but still far outpacing the overall economy

- Throughout 2012 through to early 2016, tech was the star performer of the national economy, posting annual gains in excess of 5.5 or even

6.0 percent consistently. Talent shortages and the inability to sustain such rapid levels of growth have begun to show up in data, with year-

over-year change now at 4.5 percent. Despite this slowdown, tech is still growing 2.6x faster than the overall economy and will remain a

critical component of the labor market.

• Due to mixed figures, Federal Reserve likely to push back rate hike

- The Federal Reserve has been keenly watching jobs figures as a key metric to determine the timing of the next rate hike. While the overall

fundamentals of the labor market remain strong, with the overall economy is approaching its cyclical peak, unemployment consistently

below 5.0 percent, next to no upward movement in initial claims and employment gains relatively diversified, the Federal Reserve is likely to

hold off on the next rate hike due to inconsistent monthly additions and weaker-than-expected wage growth.

Source: JLL Research, Bureau of Labor Statistics

2

August 2016 U.S. labor market at a glance

+151,000(71 consecutive months

of growth)1-month net change

+2,447,000(+1.7% y-o-y)

12-month change

+781,00010-year average annual growth

Source: JLL Research, Bureau of Labor Statistics

4.9%Unemployment rate

-20bp12-month change in unemployment

62.8%Labor force participation rate

5,624,000(+8.8% y-o-y)

Job openings

5,131,000(-0.3% y-o-y)

Hires

2,723(+5.7% y-o-y)

Quits

3

After two very strong months of rebound, August growth was

more muted at 151,000 new jobs; revisions had little impact

360,

000

226,

000

243,

000

96,0

0011

0,00

088

,000 10

6,00

012

2,00

022

1,00

018

3,00

016

4,00

0 196,

000

360,

000

226,

000

243,

000

96,0

0011

0,00

088

,000

160,

000

150,

000

161,

000

225,

000

203,

000

214,

000

197,

000

280,

000

141,

000

203,

000

199,

000

201,

000

149,

000

202,

000

164,

000

237,

000 27

4,00

084

,000

166,

000

188,

000 22

5,00

033

0,00

023

6,00

028

6,00

024

9,00

021

3,00

0 250,

000

221,

000

423,

000

329,

000

221,

000 26

5,00

084

,000

251,

000

273,

000

228,

000

277,

000

150,

000

149,

000

295,

000

280,

000

262,

000

168,

000

233,

000

186,

000

277,

000

24,0

0027

1,00

027

5,00

015

1,00

0

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2011

2012

2013

2014

2015

2016

1-m

onth

net

cha

nge

4

Source: JLL Research, Bureau of Labor Statistics

Unemployment is in its third consecutive month of 4.9 percent

as job and workforce growth are in alignment

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-1,000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

Une

mpl

oym

ent r

ate

(%)

1-m

onth

net

cha

nge

(tho

usan

ds)

Monthly employment change Unemployment rate

Source: JLL Research, Bureau of Labor Statistics

5

Job openings are likely at an inflection point, remaining

relatively consistent throughout late 2015 and so far in 2016

Source: JLL Research, Bureau of Labor Statistics

6

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Job

open

ings

(th

ousa

nds)

1.9%

3.0%

3.0%

3.0%

3.0%

3.3%

3.6%

4.7%

4.7%

5.0%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

Mining and logging

Other services

Trade, transportation and utilities

Construction

Manufacturing

Information

Financial activities

Education and health

Leisure and hospitality

Professional and business services

12-month % change in job openings

Facing a talent shortage and sustained demand for services,

PBS job openings continue to outpace other industries

Source: JLL Research, Bureau of Labor Statistics

7

0

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Hire

s an

d qu

its (

thou

sand

s)

Hires Quits

Like job openings, hires and quits are beginning to plateau but

still trending up

Source: JLL Research, Bureau of Labor Statistics

Wage growth dropped by 20bp to 2.4 percent, although a similar

decline in inflation kept real earnings growth positive

Source: JLL Research, Bureau of Labor Statistics – CPI data as of March 2016

9

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016

12-m

onth

% c

hang

e

Hourly wage growth CPI growth

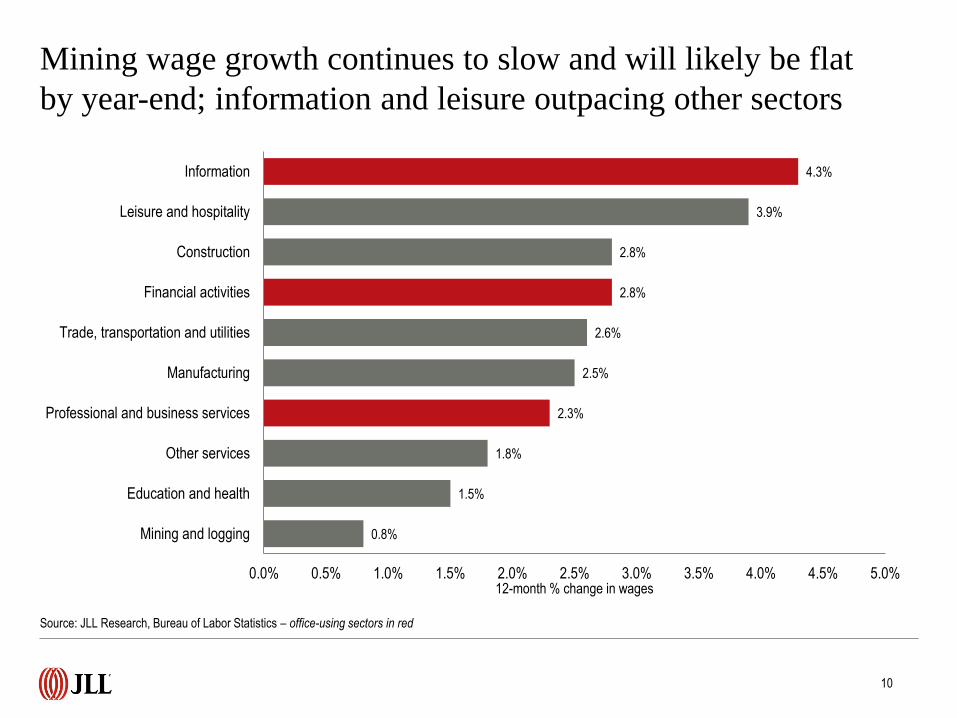

0.8%

1.5%

1.8%

2.3%

2.5%

2.6%

2.8%

2.8%

3.9%

4.3%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% 5.0%

Mining and logging

Education and health

Other services

Professional and business services

Manufacturing

Trade, transportation and utilities

Financial activities

Construction

Leisure and hospitality

Information

12-month % change in wages

Mining wage growth continues to slow and will likely be flat

by year-end; information and leisure outpacing other sectors

Source: JLL Research, Bureau of Labor Statistics – office-using sectors in red

10

-16.0

-14.0

-6.0

-5.6

-4.0

-3.1

-0.8

2.0

3.9

4.0

7.0

14.9

15.0

15.1

22.0

25.0

29.0

36.1

39.0

-20 -10 0 10 20 30 40 50

Durable goods

Manufacturing

Construction

Motor vehicles and parts

Mining and logging

Temporary help services

Utilities

Nondurable goods

Wholesale trade

Information

Other services

Transportation and warehousing

Financial activities

Retail trade

Professional and business services

Government

Leisure and hospitality

Health care and social assistance

Education and health services

1-month net change (thousands)

Monthly figures pulled downward by slight contraction in

construction and below-average PBS and health gains

11

Source: JLL Research, Bureau of Labor Statistics

-125.0

-87.0

-37.0

3.4

8.8

29.0

33.3

47.0

50.0

51.2

76.0

164.0

167.0

199.0

293.4

418.0

542.0

556.0

618.0

-200 0 200 400 600 800

Mining and logging

Durable goods

Manufacturing

Utilities

Motor vehicles and parts

Information

Temporary help services

Wholesale trade

Nondurable goods

Transportation and warehousing

Other services

Government

Financial activities

Construction

Retail trade

Leisure and hospitality

Professional and business services

Health care and social assistance

Education and health services

12-month net change (thousands)

618.0

556.0

418.0

293.4

167.0

394.6

Education and health PBS

Leisure and hospitality Retail trade

Financial activities Manufacturing

All other jobs

Over the course of 2016, annual levels of growth have yet to

budge and composition remains consistent

Source: JLL Research, Bureau of Labor Statistics

12

Core subsectors added 83.9 percent

of all jobs over the past 12 months.

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Une

mpl

oym

ent r

ate

for

bach

elor

’s d

egre

e ho

lder

s (%

)Unemployment for bachelor’s degree holders rose slightly to

2.7 percent, but remains near its cyclical low

Source: JLL Research, Bureau of Labor Statistics

13

As with the general labor market, office-using industries saw

much slower growth in August, particularly PBS

-300

-250

-200

-150

-100

-50

0

50

100

150

200

2009 2010 2011 2012 2013 2014 2015 2016

Information Professional and business services Financial activities

Source: JLL Research, Bureau of Labor Statistics

14

Tech continues to stabilize and now stands at 4.5-percent

growth, while energy has surpassed its cyclical trough

-11.0

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

2008 2009 2010 2011 2012 2013 2014 2015 2016

High-tech Energy, Mining, and Utilities Office-using industries Total non-farm

Source: JLL Research, Moody’s. Note: Due to data lags, high-tech employment only available through January 2015.

15

12-m

onth

% c

hang

e (jo

bs)

Initial claims have yet to budge over the course of 2016,

demonstrating economic momentum in spite of volatility

Source: JLL Research, U.S. Department of Labor

16

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

Cla

ims

Initial claims 4-week moving average

0

20

40

60

80

100

120

140

Con

sum

er c

onfid

ence

Inde

xConsumer confidence broke the 100-point mark for the first

time this year, but has yet to reach 2015 levels

Source: JLL Research, Conference Board

17

Ongoing tech correction has resulted in the Bay Area no longer

being among the fastest-growing labor markets

Source: JLL Research, Bureau of Labor Statistics

18

Austin

3.9%

Seattle-

Bellevue

3.9%

Fort

Lauderdale

4.6%

Orlando

4.1%

Jacksonville

3.6%

Denver

3.7%

As with the official unemployment rate, total unemployment is

beginning to reach its trough at 9.7 percent

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Tot

al u

nem

ploy

men

t (%

)

Total unemployment U-6 10-year average

Source: JLL Research, Bureau of Labor Statistics

19

Balanced increases in the workforce (+176,000) and

employment (+151,000) kept participation flat at 62.8 percent

Source: JLL Research, Bureau of Labor Statistics

20

60.0%

61.0%

62.0%

63.0%

64.0%

65.0%

66.0%

67.0%

2008 2009 2010 2011 2012 2013 2014 2015 2016

Labo

r fo

rce

part

icip

atio

n ra

te (

%)

©2016 Jones Lang LaSalle Research IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

For more information, please contact:

Ben Breslau

Managing Director - Americas Research

Phil Ryan

Senior Research Analyst – Office and Economy Research

Top Related