![Results Presentation for Financial Quarter and year ended 31st March 2016 [Company Update]](https://static.fdocuments.net/doc/165x107/577c7c621a28abe0549a6205/results-presentation-for-financial-quarter-and-year-ended-31st-march-2016-company.jpg)

Languages

Pages

Legal

Presentation of Results for the year ended31st March 2015

4th June 2015

Follow us on Twitter: @johnson_matthey

Scan to download our IR app or visit www.matthey.com/app

Cautionary StatementThis presentation contains forward looking statements that are subject to risk factors associated with, amongst other things, the economic and business circumstances occurring from time to time in the countries and sectors in which Johnson Matthey operates. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a wide range of variables which could cause actual results to differ materially from those currently anticipated.

Introduction

Robert MacLeodChief Executive

Key Messages

4

Good progress in2014/15, led by ECT

Underlying EPS up6% and 9% increasein dividend proposed

Focusing on attractive growth markets which fit with our core strengths

Good underlying growth expected in continuing businesses in 2015/16

Long term growthdrivers remain strong

£

Health and Safety is Our Priority

5

LTIIR (lost time injury and illness rate) = number of lost workday cases per 200,000 total hours worked in a rolling year

LTIIR reduced by 25% to 0.49due to renewed groupwidefocus on behavioural safety

Over 50% of accidents caused by manual handling incidents,

slips, trips and falls

Only 5% werechemical related

0

0.2

0.4

0.6

0.8

Apr‐14

May‐14

Jun‐14

Jul‐1

4

Aug‐14

Sep‐14

Oct‐14

Nov

‐14

Dec‐14

Jan‐15

Feb‐15

Mar‐15

LTIIR ‐ 12 month rolling year

LTIIR

H&S programme introduced

Financial Review

Den JonesGroup Finance Director

Underlying Results

7

Note: All figures are before amortisation of acquired intangibles, major impairment and restructuring charges, profit or loss on disposal of businesses, significant tax rate changes and, where relevant, related tax effects

Year to 31st March 2015£m

2014£m % change

% at constant rates (cr)

% at cr & excl. Anglo

Revenue 10,060 11,155 ‐10 ‐8

Sales excluding precious metals 3,125 2,981 +5 +8 +9

Operating profit 477.1 468.9 +2 +5

Interest and share of JV profit (37.0) (41.6)

Profit before tax 440.1 427.3 +3 +7 +15

Tax (74.9) (82.7)

Profit after tax 365.2 344.6 +6

Earnings per share 180.6p 170.6p +6

Dividend per share 68.0p 62.5p +9

Good Business Growth

8

Divisional profit movements are shown at constant rates. For Precious Metal Products movement also excludes loss of income from contracts with Anglo Platinum

2013/14 uPBT

Exchange Anglo ECT PT PMP FC NBRebased2013/14uPBT

2014/15 uPBT

£427m

£16m

£30m

£381m

£41m

£7m£4m

£6m £4m £5m

£440m

350

360

370

380

390

400

410

420

430

440

450

Underlying Profit Before Tax Bridge – 2013/14 to 2014/15(£m)

‐4%

‐7%

+10%+2%

+1%+1%

‐1%

+1%

Other

Reconciliation to Reported Results

9

Year to 31st March 2015£m

2014£m

Underlying profit before tax 440.1 427.3

Amortisation of acquired intangibles (17.3) (20.7)

Profit on sale of Gold and Silver Refining 69.7 ‐

Exchange on liquidation of businesses 3.3 ‐

Profit before tax 495.8 406.6

Earnings per share 211.2p 167.7p

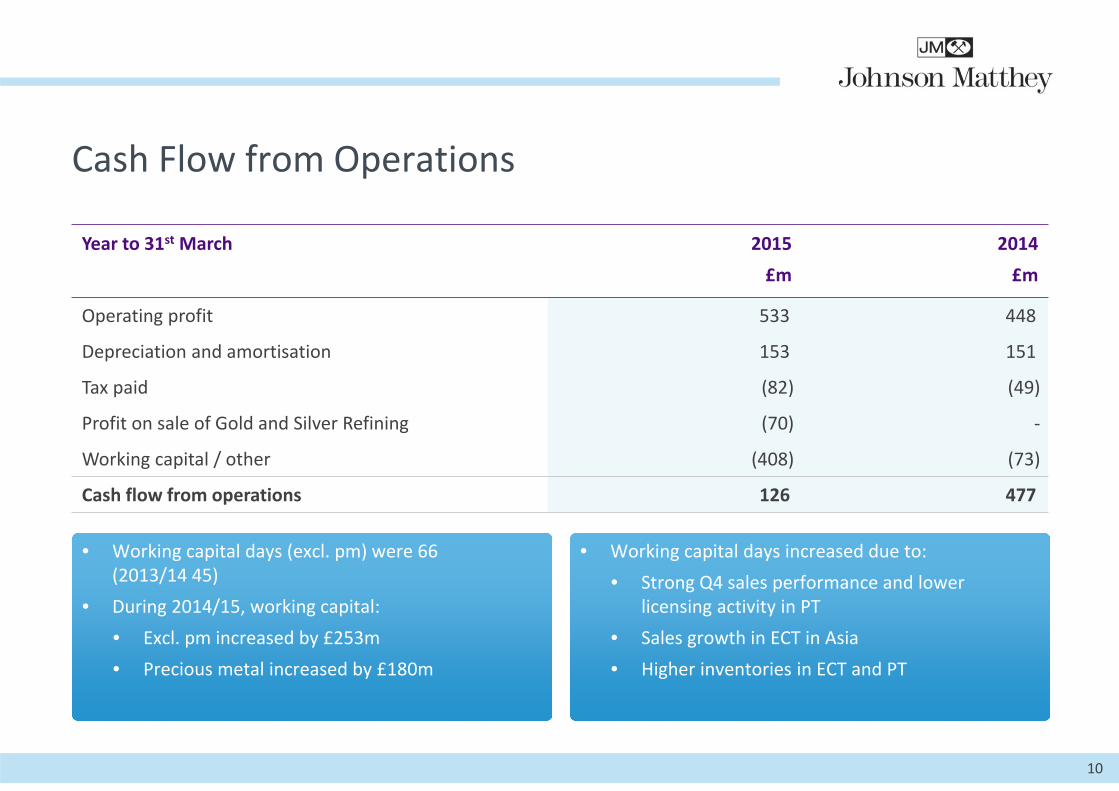

Cash Flow from Operations

10

Year to 31st March 2015£m

2014£m

Operating profit 533 448

Depreciation and amortisation 153 151

Tax paid (82) (49)

Profit on sale of Gold and Silver Refining (70) ‐

Working capital / other (408) (73)

Cash flow from operations 126 477

• Working capital days (excl. pm) were 66 (2013/14 45)

• During 2014/15, working capital:• Excl. pm increased by £253m• Precious metal increased by £180m

• Working capital days increased due to:• Strong Q4 sales performance and lower

licensing activity in PT• Sales growth in ECT in Asia• Higher inventories in ECT and PT

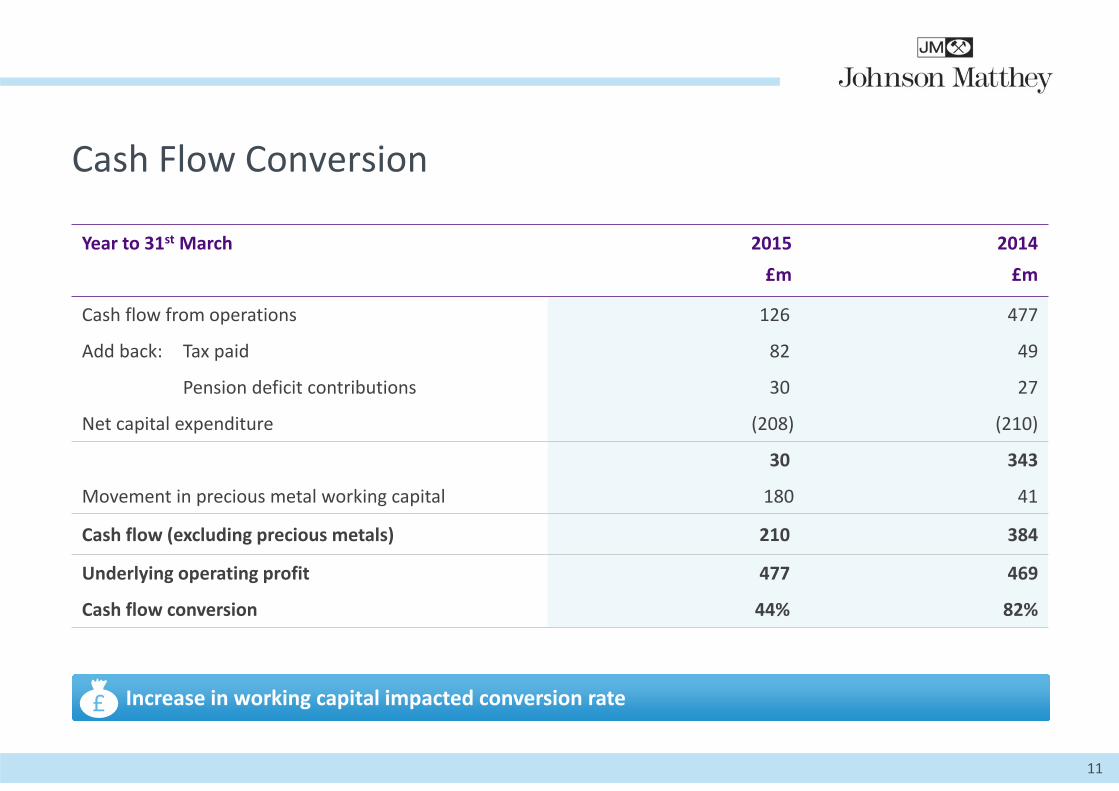

Cash Flow Conversion

11

Year to 31st March 2015£m

2014£m

Cash flow from operations 126 477

Add back: Tax paid 82 49

Pension deficit contributions 30 27

Net capital expenditure (208) (210)

30 343

Movement in precious metal working capital 180 41

Cash flow (excluding precious metals) 210 384

Underlying operating profit 477 469

Cash flow conversion 44% 82%

Increase in working capital impacted conversion rate£

Working Capital and Cash Flow Conversion Dynamics

Working capital days return tohistorical levels• 2013/14 unusually low• Expect range of 50 to 60 days due to:

• Growing business• Increasing business in China –

payment terms longer

Cash flow conversion expected to rise • Cash flow conversion expected to

average around 70% over the nextfew years

• Higher capex to support business growth

12

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

Days

303540455055606570

2010 2011 2012 2013 2014 2015 2016

57 6054 53

45

66

50‐60

~70%

Continued Investment to Support Business Growth

Capital expenditure £211.8m(2013/14 £218.3m)• Key projects:

• Extension of European ECT facilities tomeet demand from new legislation

• Expansion of PT’s chemical catalyst manufacturing capacity in China and Europe

• Capex:depreciation = 1.6 times• Capex expected to be around £280m for

next two years• Capex:depreciation range 1.6 to 1.8 times• Investment in core business systems

R&D – gross expenditure up 12% at £169.9m

13

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

0

50

100

150

200

250

300

2012/13 2013/14 2014/15

Emission Control Technologies Process TechnologiesPrecious Metal Products Fine ChemicalsNew Businesses Corporate

Capex / depn (times)£m

Return on Invested Capital (ROIC)

14

8%

12%

16%

20%

24%

2011 2012 2013 2014 2015

Cost of capital

Target

Decline following change in Anglo contracts

Increase in precious metal balances

Group ROIC 18.8%

Remain committed to 20% target

£

Pt

Balance Sheet Remains Strong

• Net debt increased to £994.4m (2013/14 £729.2m)

• Net debt (including post tax pension deficits) / EBITDA 1.7 times

• Average cost of debt 2.4%• Average tenure 5.7 years

• Number of actions over last few years to reduce deficits

• UK scheme actuarial valuation underway

15

Treasury£ Pension Actuarial Basis

• £15m increase in pension costs in 2015/16 in underlying operating profit

• Mainly non‐cash and predominantly due to significantly lower discount rates

Pension Accounting (IAS 19)

Operating Review

Robert MacLeodChief Executive

Emission Control Technologies – Another Strong Year

17

Year to 31st March

£m 2015 2014 % change

% atconstantrates (cr)

Sales (excluding precious metals) 1,782 1,645 +8 +12

Underlying operating profit 236.9 203.6 +16 +21Return on sales 13.3% 12.4%Return on invested capital (ROIC) 24.1% 21.0%

Another strong year with:• Benefit from tighter legislation in Europe for cars and trucks• Continued growth in Asia, especially China• Strong demand for HDD trucks in the US• Process efficiency improvements and higher plant utilisation

HDD

41% LDV

59%

Sales

Outpacing Global Light Duty Growth

18

£181m £183m £179m

£543m £571m £622m

£214m £255m £257m

£938m£1,009m £1,058m

0

200

400

600

800

1000

1200

2012/13 2013/14 2014/15 2012/13 2013/14 2014/15 2012/13 2013/14 2014/15 2012/13 2013/14 2014/15

North America• North American car

production up 3%• JM volumes grew

broadly in line with market

Europe• JM’s sales well

ahead in a flat market

• Boosted by Euro 6b and a good performance by customers

Global• Sales at constant

rates well ahead of 1% growth in global car production

Johnson Matthey’s Light Duty Catalyst Sales£m

+9%

+1%

+5%

+9% at cr

+5% at cr

+14% at cr

‐1% at cr

Total sales

£1,058m up 5%

‐2%

Asia• Sales growth in China

supported by 7% increase in car production

• Increased demand in South East Asia and India but slower market in Japan

Strong HDD Sales Across all Regions

19

£347m £374m£441m

£148m£212m £225m

£28m £50m £58m

£523m

£636m£724m

0

100

200

300

400

500

600

700

800

2012/13 2013/14 2014/15 2012/13 2013/14 2014/15 2012/13 2013/14 2014/15 2012/13 2013/14 2014/15

Johnson Matthey’s Heavy Duty Diesel Catalyst Sales£m

+18%

+6%

+14%

Total sales

£724m up 14%

+20% at cr

+13% at cr

+25% at cr

+18% at cr

North America• Strong sales slightly

ahead of 16% growth in truck production

• Good demand for ‘Class 8’ trucks

Europe• Strong JM sales

supported by first full year of Euro VI

• Weaker truck market after pre‐buy in 2013

Global• Non‐road applications

around £58m of sales• Sales to stationary

applications around £50m

Asia• Growth driven by

continued roll out of Euro IV in China

• Around 35% fitment in China – now expanding beyond big cities

+17%

Looking Ahead – Air Quality Remains a Major Global Issue

20

Outlook 2015/16: Continued strong performance in line with medium term target

Light duty – good structural growthShort term:• Full introduction of Euro 6b in 2015/16

Medium term:• Euro 6c and real world driving emission

standards• Early signs of increased diesel penetration

in US

Heavy duty – further growth ahead• Further fitment of Euro IV systems in China

• Increasingly includes more smaller enginedvehicles

• Beijing VI expected from 2018

• Stage V non‐road expected in Europefrom 2019/20

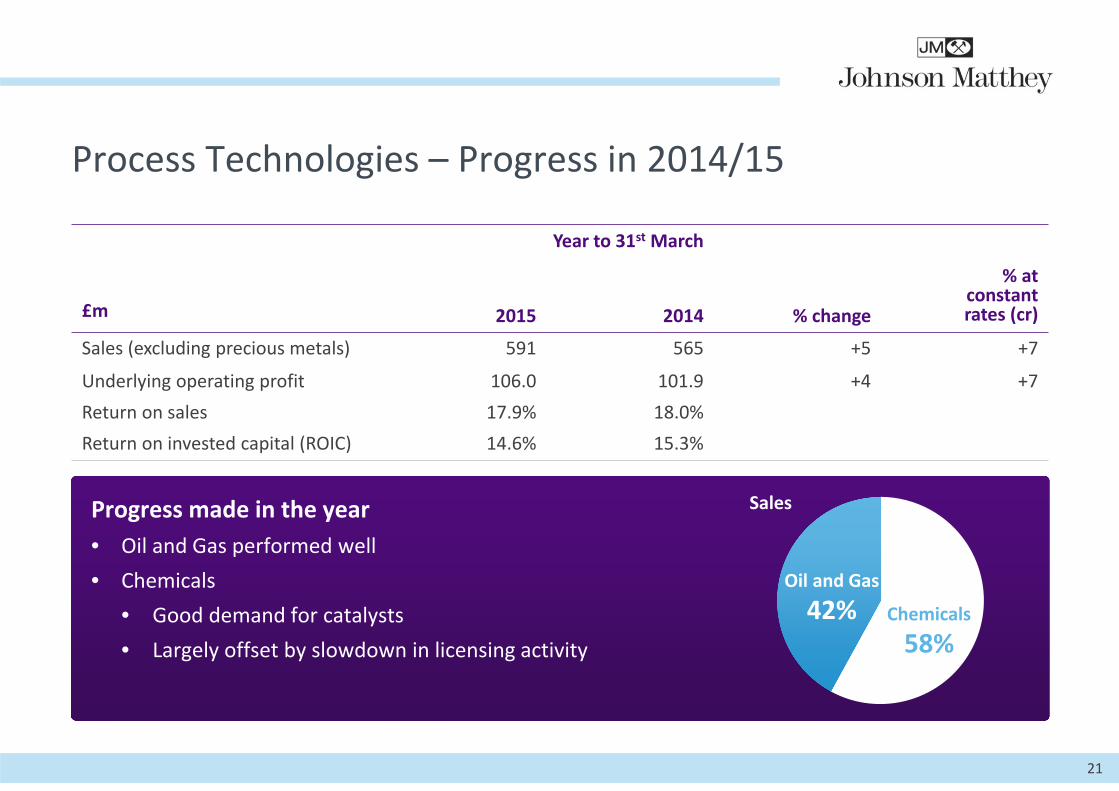

Process Technologies – Progress in 2014/15

21

Year to 31st March

£m 2015 2014 % change

% atconstant rates (cr)

Sales (excluding precious metals) 591 565 +5 +7

Underlying operating profit 106.0 101.9 +4 +7Return on sales 17.9% 18.0%Return on invested capital (ROIC) 14.6% 15.3%

Progress made in the year• Oil and Gas performed well• Chemicals

• Good demand for catalysts• Largely offset by slowdown in licensing activity

Oil and Gas

42% Chemicals

58%

Sales

Syngas54%

Petrochemicals25%

Oleo/biochemicals

21%

Ammonia16%

Methanol17%

Other 6%

Formaldehyde15%

0

5

10

15

2011 2012 2013 2014 2015

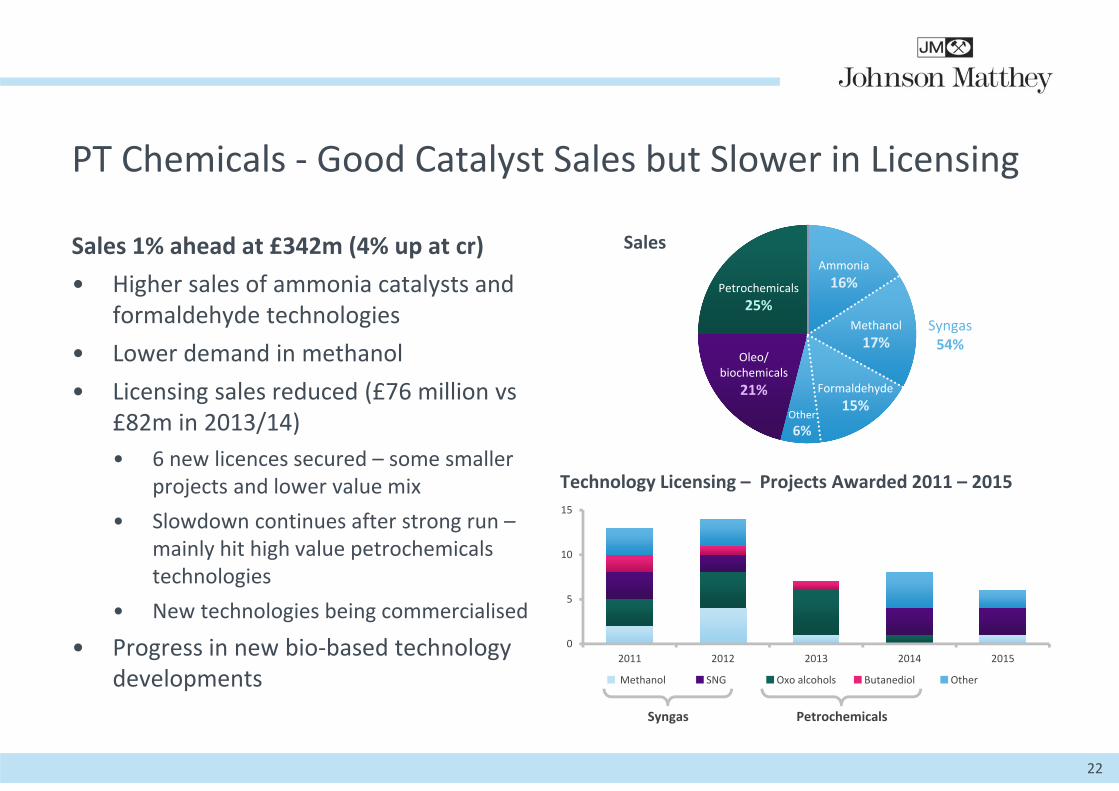

PT Chemicals ‐ Good Catalyst Sales but Slower in Licensing

Sales 1% ahead at £342m (4% up at cr)• Higher sales of ammonia catalysts and

formaldehyde technologies• Lower demand in methanol• Licensing sales reduced (£76 million vs

£82m in 2013/14) • 6 new licences secured – some smaller

projects and lower value mix • Slowdown continues after strong run –

mainly hit high value petrochemicals technologies

• New technologies being commercialised

• Progress in new bio‐based technology developments

22

Sales

Technology Licensing – Projects Awarded 2011 – 2015

Syngas

Methanol SNG Oxo alcohols Butanediol Other

Petrochemicals

Hydrogen

27%

Additives

27%Gas

Processing

15%

DiagnosticServices

31% Refineries54%

PT Oil and Gas – Performed Well Across All Sectors

Sales up 10% to £249m (up 11% at cr)• Growth supported by strong drivers in

mid/downstream markets• Strong sales of refinery hydrogen catalysts

boosted by new plant builds• Benefit from shift in mix towards higher

margin performance additives for FCC

• Diagnostic Services had a good year• Good demand for specialist measurement

products and services • Slightly lower demand for reservoir studies

due to lower oil price

23

Sales

Looking Ahead – Short Term Hiatus, Long TermDrivers Remain

24

Outlook 2015/16: Expected to be broadly in line with 2014/15

Usual dynamics in timing of orders –stronger H2• Good catalyst demand across PT; Oil and Gas

businesses expected to perform well • Lower licensing income will offset growth

• Slowdown in coal to SNG projects• Petrochem capacity in line with current demand• Lower oil price impacts investment decisions

Long term drivers remain in place• Tighter emissions regulations and energy

security concerns support future demand• Ongoing development of new technologies;

strategic collaborations• Availability of cheap shale gas in US

continues to stimulate market

Precious Metal Products – Impacted by Anglo

25

Year to 31st March

£m 2015 2014 % change

% atconstantrates (cr)

Sales (excluding precious metals) 379 430 ‐12 ‐9

Underlying operating profit 101.5 130.9 ‐22 ‐21Return on sales 26.8% 30.5%Return on invested capital (ROIC) 21.6% 36.6%

• Steady performance excluding Anglo• Weakness in some of the Manufacturing

businesses’ markets• Completed sale of Gold and Silver Refining

business for £124m (10% of division’s sales)

Services

32%Manufacturing

68%

AdvancedGlass

Technologies21%

Noble Metals35%

ChemicalProducts12%

Sales

PMP Services – Strategic Supplier for JM Businesses

Sales down 26% at £120m (24% downat cr)• Precious Metals Management

impacted by change in Anglo contracts • Mixed year in Pgm Refining and

Recycling • Volumes slightly higher overall –

increased palladium intakes from Stillwater

• Some fall off in intakes in Q4 due to pgm price drop

• Operating profit and ROIC impacted by higher costs due to less favourable intake mix

26

Platinum and Palladium Prices

500

1,000

1,500

Mar‐14 Sep‐14 Mar‐15

Palladium Platinum

Pgm Refining and RecyclingThroughput by Sector

End of lifeautocatalysts

41%

JM12%

Others18%

Mines12%

Refiners11%

Pharma/chems

6%

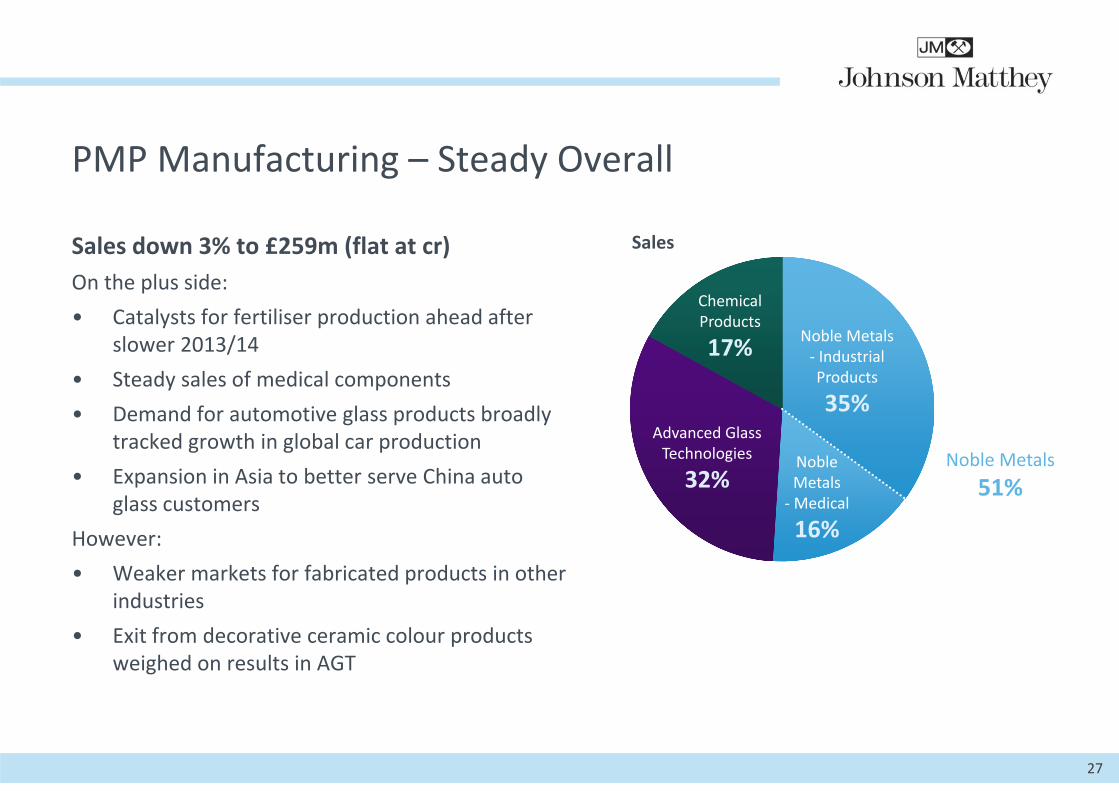

PMP Manufacturing – Steady Overall

Sales down 3% to £259m (flat at cr) On the plus side: • Catalysts for fertiliser production ahead after

slower 2013/14 • Steady sales of medical components • Demand for automotive glass products broadly

tracked growth in global car production• Expansion in Asia to better serve China auto

glass customersHowever: • Weaker markets for fabricated products in other

industries• Exit from decorative ceramic colour products

weighed on results in AGT

27

Sales

Noble Metals‐ Industrial Products

35%

NobleMetals

‐Medical

16%

Advanced GlassTechnologies

32%

ChemicalProducts

17%

Noble Metals51%

Looking Ahead – Short Term Tough but Investing for Growth

28

Outlook 2015/16: Performance expected to be significantly down

Pgm Refining• Lower metal prices currently impacting sales

and volumes• Higher costs expected ‐ shift to more

complex intake product mix• Efficiency improvement projects• Investment in China refinery

Absence of Gold and Silver Refining

Manufacturing businesses• Stable outlook for 2015/16• Focus on accessing higher growth markets

• Increased investment in new product development

• Some time until growth is realised

Fine Chemicals – A Good Year

29

Year to 31st March

£m 2015 2014 % change

% atconstant rates (cr)

Sales (excluding precious metals) 327 322 +1 +3

Underlying operating profit 88.8 84.1 +6 +7

Return on sales 27.2% 26.1%

Return on invested capital (ROIC) 18.4% 18.8%

• Steady sales growth in API Manufacturing• Process efficiency and supply chain

improvements benefited operating profit• Advanced negotiations on sale of Research

Chemicals businessAPI

Manufacturing66%

ResearchChemicals24%

Catalysisand Chiral

Technologies10%

Sales

Expanding API Capabilities, Leveraging Synergies

30

API Manufacturing• Sales up 3% to £216m (also up 3% at cr)• Demand for APIs mixed across our portfolio

with steady sales overall• Growth supported by custom API

development

Catalysis and Chiral Technologies (CCT)• Sales up 4% to £34m (up 7% at cr)• Good demand for catalyst products • Leveraging synergies with API Manufacturing

Research Chemicals• Sales down 3% to £77m (1% down at cr)

Looking Ahead – Robust Longer Term Growth Potential

31

Outlook 2015/16: Expect good progress (adjusted for sale of Research Chemicals)

Good growth expected in API Manufacturing and CCT

• Continue to invest in development of complex APIs

• Acquired API manufacturing facility in Scotland to support growth in Europe –regulatory compliant mid 2016

Sale of Research Chemicals anticipated to be completed before end of calendar year

Strong global drivers support future growth • Focus on complex, smaller volume APIs• Working with customers / partners to

formulate and develop generic drugs• A number of ANDAs received, or

awaiting, FDA approval

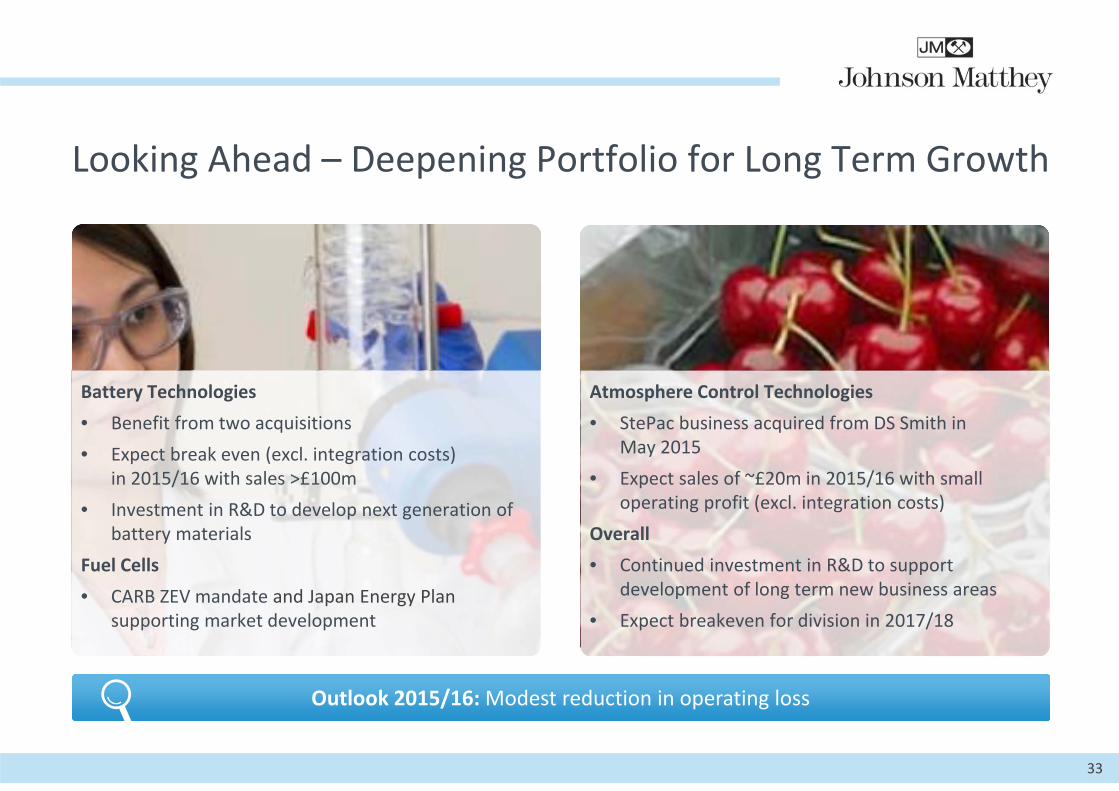

New Businesses – Good Progress in 2014/15

32

Year to 31st March

£m 2015 2014 % change

% atconstant rates (cr)

Sales (excluding precious metals) 91 76 +20 +27

Underlying operating profit / (loss) (22.1) (18.3) ‐21 ‐19

Battery Technologies (sales 23% ahead at £84m)• Good demand from power tools and e‐bikes sectors• Two battery materials acquisitions made small contribution• Acquisitions and investment in R&D led to slight operating loss

Fuel Cells (sales £6m, 2013/14 £7m)• Impacted in 1H by key customer in administration• Ongoing work with automotive OEMs on development programmes

Continued investment in other opportunities

BatteryTechnologies

92%

Fuel Cells7%

Other1%Sales

Looking Ahead – Deepening Portfolio for Long Term Growth

33

Outlook 2015/16: Modest reduction in operating loss

Battery Technologies• Benefit from two acquisitions• Expect break even (excl. integration costs)

in 2015/16 with sales >£100m • Investment in R&D to develop next generation of

battery materials Fuel Cells• CARB ZEV mandate and Japan Energy Plan

supporting market development

Atmosphere Control Technologies • StePac business acquired from DS Smith in

May 2015• Expect sales of ~£20m in 2015/16 with small

operating profit (excl. integration costs)Overall• Continued investment in R&D to support

development of long term new business areas• Expect breakeven for division in 2017/18

Outlook 2015/16

34

Good underlying growth incontinuing businesses

Expect 2015/16 to be slightlyahead of 2014/15

Well placed for longterm growth

Key Messages

35

Good progress in2014/15, led by ECT

Underlying EPS up6% and 9% increasein dividend proposed

Focusing on attractive growth markets which fit with our core strengths

Good underlying growth expected in continuing businesses in 2015/16

Long term growthdrivers remain strong

£

Questions and Answers

36

Robert MacLeodChief Executive

Den JonesGroup Finance Director

Larry PentzExecutive Director

John WalkerExecutive Director, Emission Control Technologies

John FowlerDivision Director,Fine Chemicals

Nick GarnerDivision Director,

New Businesses and Corporate Development

Alan MyersDivision Director,

Precious Metal Products

Geoff OttermanDivision Director,

Process Technologies

37

Estimated Light Duty Vehicle Sales and Production

38

Source: LMC Automotive

Year to 31st March 2H 2H

2015millions

2014millions

%change

2014/15millions

2013/14millions

%change

NorthAmerica

Sales 19.6 18.4 +6 9.4 8.8 +7

Production 16.8 16.3 +3 8.4 8.2 +3

EuropeSales 18.0 18.1 ‐ 9.1 9.0 +1

Production 19.9 19.9 ‐ 10.1 10.2 ‐1

AsiaSales 39.6 38.5 +3 21.2 21.1 ‐

Production 44.9 43.6 +3 23.1 23.0 +1

GlobalSales 88.5 86.7 +2 45.3 44.8 +1

Production 86.8 85.6 +1 44.2 44.0 ‐

Global Growth in Vehicle Production Drives ECT

16.2 17.0 17.5 17.9 18.2 19.1 19.5 20.1 20.1 20.5 21.9 23.4

43.1 44.6 46.4 49.1

51.5 58.8

84.7 87.1 89.5

93.6 98.2

109.3

0

20

40

60

80

100

120

2013 2014 2015 2016 2017 2020 2013 2014 2015 2016 2017 2020 2013 2014 2015 2016 2017 2020 2013 2014 2015 2016 2017 2020

CAGR 2.0%(2014 – 2020)

CAGR 2.6%(2014 – 2020)

CAGR 4.7%(2014 – 2020)

CAGR 3.9%(2014 – 2020)

39

Source: LMC Automotive (April 2015)

Light Duty Vehicle Production Outlook – 2013 ‐ 2020 (calendar years)million

North America Europe Asia Global

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

USA Tier II Tier III

USA (CARB) LEV II LEV III

EU Euro 5 Euro 6b Euro 6c

Russia Euro 3 Euro 4 Euro 5 (proposed)

Japan Japan 2009

China National Euro 4 Euro 5

India ‐ National BS II BS III BS IV

India ‐ Cities BS III BS IV

S Korea (Gasoline) LEV II

S Korea (Diesel) Euro 5 Euro 6

Indonesia Euro 2 Euro 3 or 4 (expected)

Thailand Euro 3 Euro 4 Euro 5 (expected)

Brazil L5 L6 L7 (proposed)

Emission Control Technologies

40

Light Duty Vehicle Legislation

Estimated HDD Truck Sales and Production

41

Source: LMC Automotive

Year to 31st March 2H 2H

2015thousands

2014thousands

%change

2014/15thousands

2013/14thousands

%change

NorthAmerica

Sales 514.0 446.6 +15 256.5 221.7 +16

Production 542.9 467.2 +16 271.0 230.0 +18

EUSales 272.9 298.2 ‐8 143.3 163.6 ‐12

Production 387.3 436.2 ‐11 201.1 229.0 ‐12

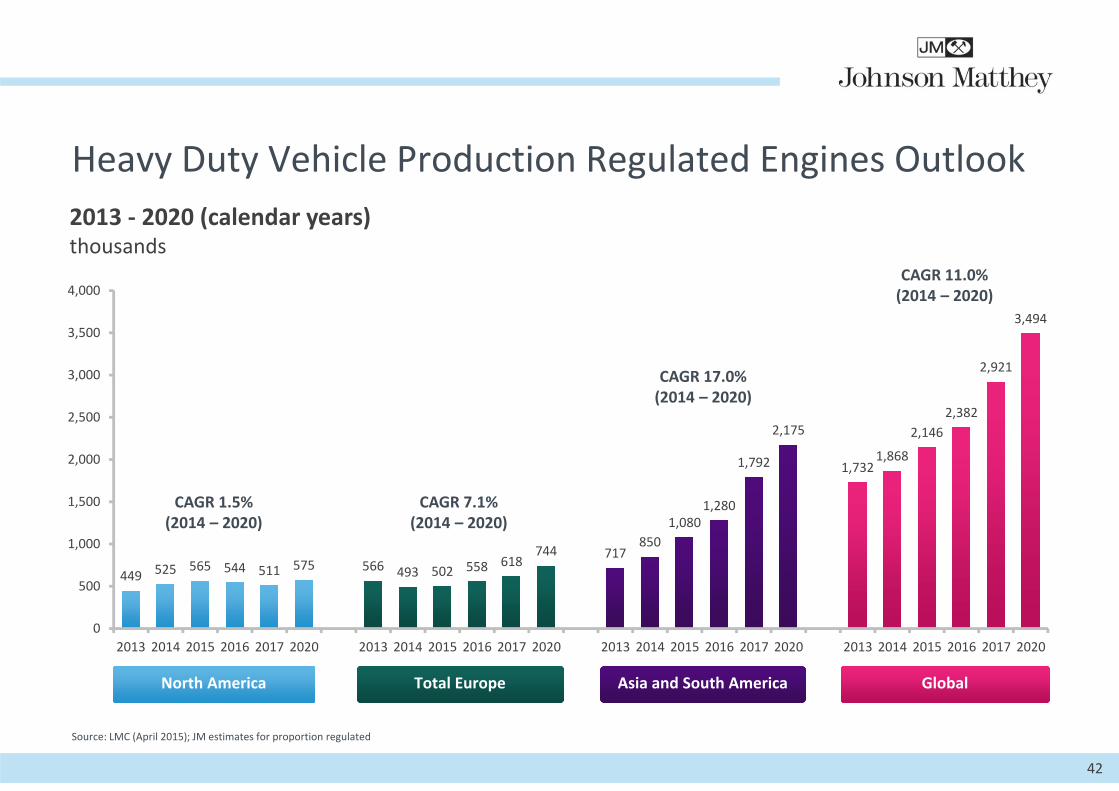

Heavy Duty Vehicle Production Regulated Engines Outlook

42

Source: LMC (April 2015); JM estimates for proportion regulated

449 525 565 544 511 575 566 493 502 558 618744 717

850 1,080

1,280

1,792

2,175

1,732 1,868

2,146 2,382

2,921

3,494

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2013 2014 2015 2016 2017 2020 2013 2014 2015 2016 2017 2020 2013 2014 2015 2016 2017 2020 2013 2014 2015 2016 2017 2020

CAGR 1.5%(2014 – 2020)

CAGR 7.1%(2014 – 2020)

CAGR 17.0%(2014 – 2020)

CAGR 11.0%(2014 – 2020)

2013 ‐ 2020 (calendar years)thousands

North America Total Europe Asia and South America Global

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

ON ROAD Europe EU V EU VINorth America EPA10 EPA10 + Greenhouse Gas RegulationJapan JP 09 JP 16South Korea EU V EU VIBrazil EU III EU V EU VI?Russia EU III EU IV EU VIndia (Main Cities) BS IVIndia (Nationwide) BS III BS IV?China (Beijing) EU IV EU V EU VI? (some expected from 2016)

China (Nationwide) EU III EU IV EU V?Thailand EU III EU IV

NON‐ROAD Europe Stage IIIa Stage IIIb Stage IV Stage VNorth America Tier 3 Tier 4 Interim Tier 4 FinalJapan Tier 3 Tier 4 Interim Tier 4 FinalSouth Korea Tier 3 Tier 4 FinalBrazil Stage IIIa

Emission Control Technologies

43

Heavy Duty Diesel Legislation

Top Related