Languages

Pages

Legal

1

Abstrac

INDIA SMART GRID [Can it become a Reality?]

Submitted by,

Mirdul Amin Sarkar

MBA-Power Management R130215017

Email: [email protected] / [email protected]

2

TABLE OF CONTENTS :

1.Introduction ………………………………………………………………………………..3 2.Background …………………………………………………………………………………5 3.Need for Smart Grids in India :……………………………………………………..6 2.What are the Smart Grid Implementation Challenges in India?.....7 5.Smart Grid Drivers:……………………………………………………………………..8 6.Smart Grid Technologies:…………………………………………………………...9 7.Key Characteristics of Smart Grid:……………………………………………..10 8.Smart Grid and Integration of Renewable Energy Sources:………..11 9.Indian Government Initiatives toward a Smart Grid:…………………11 10. India Smart Grid Vision:…………………………………………………….…..13 11.National smart grid mission:…………………………………………………..14 12.Smart Grid Projects in India:…………………………………………………..14 13.Upcoming/Proposed:………………………………………………………….....16 14. Barriers in implementation of smart grid : …………………………....17 15.Solutions to overcome the barriers in implementation: …………20 16.On-going smart grid activities:………………………………………………..21

17.Recommendations :…………………………………......22

18.Conclusion………………………………………………………..22

3

Introduction:

“The time has come to look at Smart Grid as a Necessity rather than an opportunity’’

There are many ways to look at Smart

Grid reality in India. However, there are many challenges to it. As per power ministry, over 18000 villages in India are still un-electrified. It becomes even more important to ensure minimal pilferage in power usage in form of tamper or theft, wrong billing and delayed payment. In addition, India having natural advantage of being close to equator gets abundant supply of solar power, and if harnessed efficiently can source all our basic needs sufficiently.

Consistent high growth of Indian

economy has resulted in a surging

demand for energy. Since, independence

Indian power system has grown from

1362 MW to 308.83 GW. In the past

decade, installation of renewable sources

of energy for electricity has grown at an

annual rate of 25%. Despite this,

presently 400 million people in the

country have no access to electricity and

hundreds of millions get electricity for

only a few hours. Distribution system is

suffering from frequent and long duration

outages. To supplement capacity addition

as well as electrification of remote areas,

development of micro-grid also needs

attention. Standalone/decentralized

micro grid can provide basic energy

access to all. Presently, high AT&C losses

of utilities are resulting into poor

financial health of distribution utilities

across the country. To address these

issues and bring efficiency, seamless

integration of emerging technologies in

the field of monitoring, automation,

control, communication and IT systems

with active participation of all

stakeholders are inevitable. It is expected

that the far-reaching goals of modern

Indian power system can be achieved by

deployment of smart grids which can help

to improve efficiency of Indian power

sector. In this direction, several initiatives

have been taken to implement smart grid

in entire supply value chain - generation,

transmission distribution and consumer

participation in power sector.

Electricity grids around the world are

getting increasingly intelligent and

responsive, ensuring the supply of better,

continuous and cost-efficient power,

while making it possible for both

consumers and suppliers to coexist

happily. In India, where the power sector

faces several challenges— including up to

15 percent peak power shortage, only 75

4

percent access to power and nonpolluting

cooking facilities, and high accumulated

losses with the distribution companies

(the state electricity boards)—smart

grids can soon make it possible to ensure

stable, reliable, safe and affordable power

supply using two-way

communication and remote intelligent

sensors to further serve and engage

customers. Indeed, the scenario that we

described may arrive sooner than we

would expect.

India plans to invest billions of dollars

into smart grid development over the

next ten years to get electricity theft

under control. Smart grid market to touch

Rs 50,000 crore in five years from the

present level of sub Rs 100 crore. This

would be fuelled by the government’s

plan of setting up 100 smart cities and

500 smart town.

India today is in a strong position for an

advanced smart grid infrastructure. A few

factors are in the country’s favor:

Growing pressure to improve

transmission efficiencies

Increased emphasis on power cost

management and reliability

Increasing adoption of renewable

energy, including captive micro-

installations in industrial and

residential spaces, which require

options for feeding electricity back into

the grid

Rapid IT infrastructure growth across

the country, including broadband

access

The industry expects a lot of changes in

smart grid space in the coming years, in

terms of investment and innovation.

Although many advantages of smart grid

technology are apparent, it will merely be

a question of time before everyone agrees

to accept smart grids. This is relatively a

new concept, and the decision making has

been slow. Even companies around the

world have just started gaining

experience in smart grid technologies.

Then there are no established standards

for communication with a smart meter.

The urgency for Smart Grids in India emerges

from the key challenges that the industry is

currently facing. India operates the 3rd

largest transmission and distribution

network in the world, yet faces a number of

challenges such as: inadequate access to

electricity, supply shortfalls (peak and

energy), huge network losses, poor quality

and reliability and rampant, theft. The

evolution towards Smart Grid would address

these issues and transform the existing grid

into a more efficient, reliable, safe and less

constrained grid that would help provide

access to electricity to all.

5

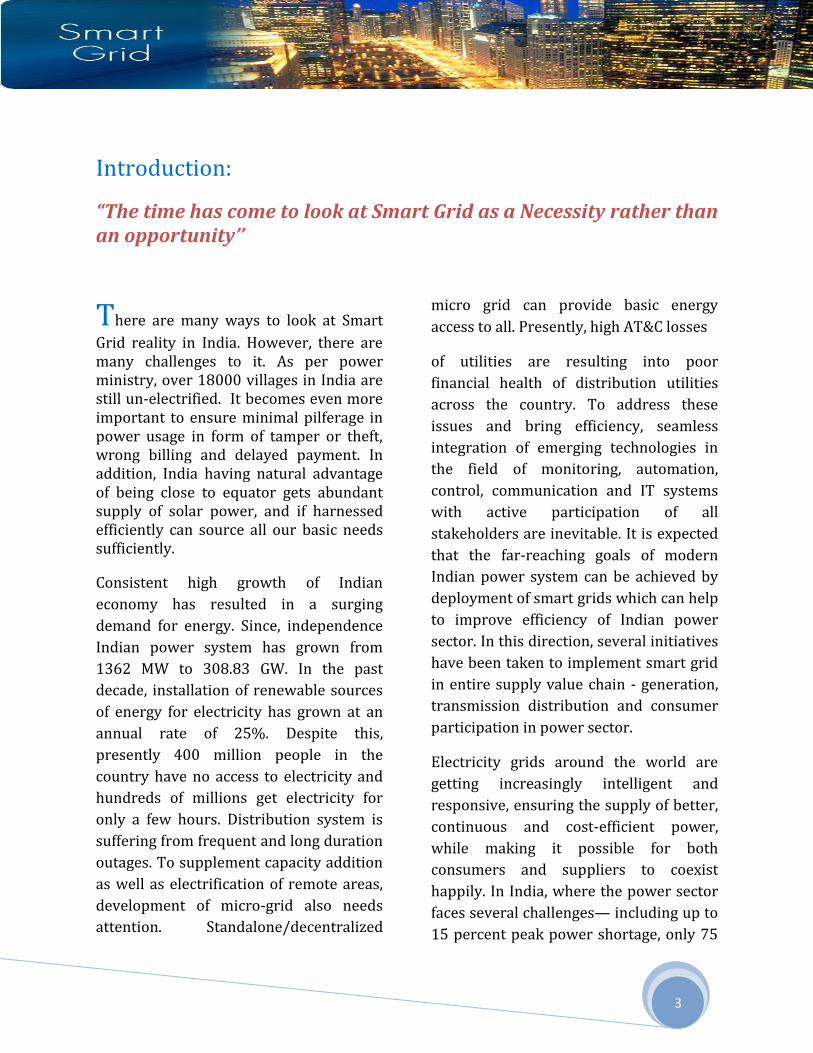

2.Background What is Smart Grids? Smart Grid uses computer hardware and software, sensors, telecommunication equipment and

services to:

Helps the customer to manage consumption and use electricity wisely.

Enables customer to respond to utility that help minimize the period of surpluses,

bottlenecks, and outages.

Helps utilities in improving their performance and controlling costs by timely availability of

information.

Thus Smart Grids associates customer to electricity by an information rich network. And also it

provides utilities with valuable operational information that helps them to improve efficiency.In a

layman's term Smart Grid is an efficient combination of electrical infrastructure and information

technology.

Figure 1: Smart Grid

6

3.Need for Smart Grids in India :

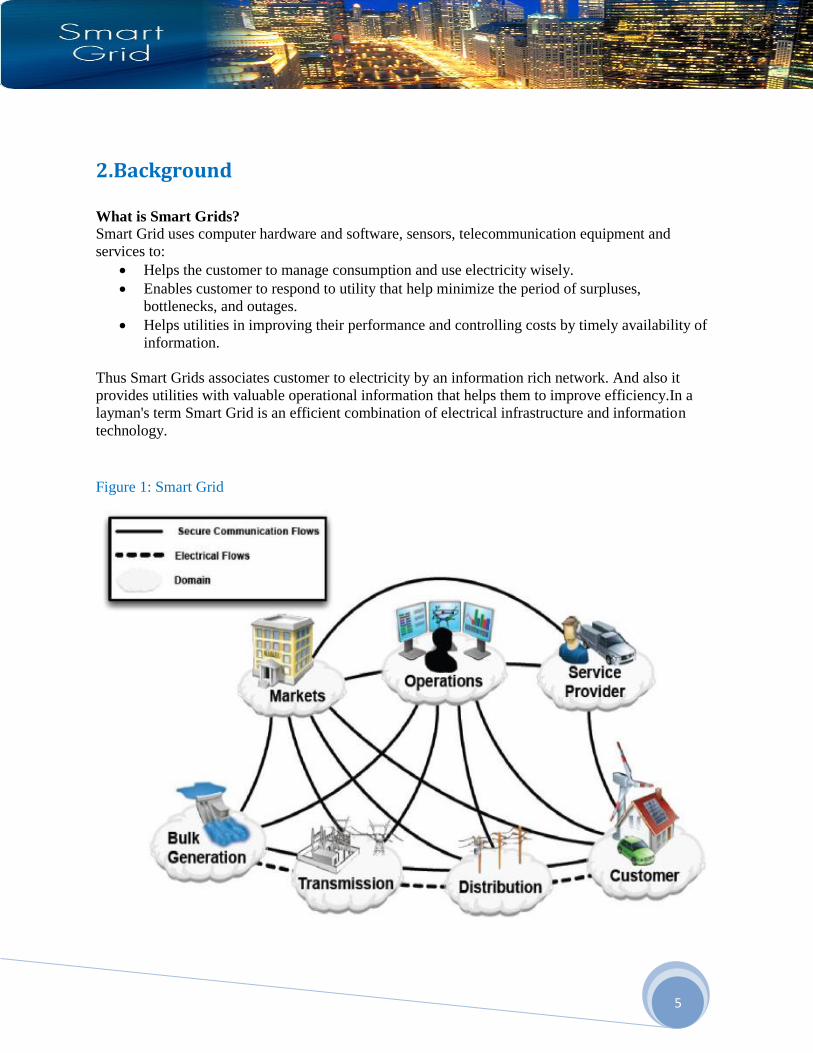

According to the Ministry of Power, India’s

transmission and distribution losses are

amongst the highest in the world, averaging

26 per cent of total electricity production, and

as high as 62 per cent in some states. These

losses do not include non-technical losses like

theft etc.; if such losses are included, the

average losses are as high as 50 per cent.

India losses money for every unit of

electricity sold, since India has one of the

weakest electric grids in the world. Some of

the technical flaws in the Indian power grid

are - it is a poorly planned distribution

network, there is overloading of the system

components, there is lack of reactive power

support and regulation services, there is low

metering efficiency and bill collection, etc.

India is venturing very fast into renewable

energy (RE) resources like wind and solar.

Solar has great potential in India with its

average of 300 solar days per year. The

government is also giving incentives for solar

power generation in the form of subsidies for

various solar applications; and has set a goal

that solar should contribute 7 per cent of

India’s total power production by 2022. With

such high targets, solar is going to play a key

role in shaping the future of India’s power

sector. A lacuna of renewable resources is

that their supply can be intermittent i.e. the

supply can only be harnessed during a

particular part of the day, like day time for

solar energy and windy conditions for

harnessing wind energy, also these conditions

cannot be controlled. With such

unpredictable energy sources feeding the

grid, it is necessary to have a grid that is

highly adaptive (in terms of supply and

demand). Hence, the opportunities for

building smart grids in India are immense, as

a good electric supply is one of the key

infrastructure requirements to support

overall development.

7

4.What are the Smart Grid Implementation Challenges in India? The Power Industry calls for a complete switch into the next generation through automation. Despite monetary issues, power utilities need to begin with basic automation systems eventually upgrading to the advanced systems. By analyzing the growing power demand and market competence, this is the only way-forward for the domestic power industry. The implementation of Smart Grid is not going to be an easy task as the Indian power sector poses a number of issues such as minimizing T&D losses, power theft, inadequate grid infrastructure, low metering efficiency and lack of awareness. Power Theft: Power theft has been one of the major issues in India. A few ways to help prevent the power theft are the use of overhead lines that are insulated and the LT overhead wires used for distribution of power could be replaced with insulated cables in order to minimize the theft of energy through hooking. The conventional energy meters could be replaced with digital tamper proof meters and the use of prepaid card is yet another solution to eradicate theft of energy.

Inadequate Grid Infrastructure: For India to continue along its path of aggressive economic growth, it needs to

build a modern, intelligent grid. It is only with a reliable, financially secure Smart Grid that India can provide a stable environment for investments in electric infrastructure - a prerequisite to fixing the fundamental problems with the grid.

Low metering efficiency: The commercial losses are mainly due to low metering efficiency, theft & pilferage. This may be eliminated by improving metering efficiency, proper energy accounting & auditing and improved billing & collection efficiency. Fixing of accountability of the personnel / feeder managers may help considerably in reduction of AT&C loss.

Lack of awareness: The understanding of consumers on how power is delivered to their homes is very minimal. Before implementing Smart Grid concepts, they should be educated about the Smart Grids, the benefits of Smart Grid and Smart Grid’s contribution to low carbon economy. Consumers should be made aware about their energy consumption pattern at home, office etc. Utilities need to focus on the overall capabilities of Smart Grids rather than mere implementation of smart meters. Policy makers and regulators must be very clear about the future prospects of Smart Grids.

8

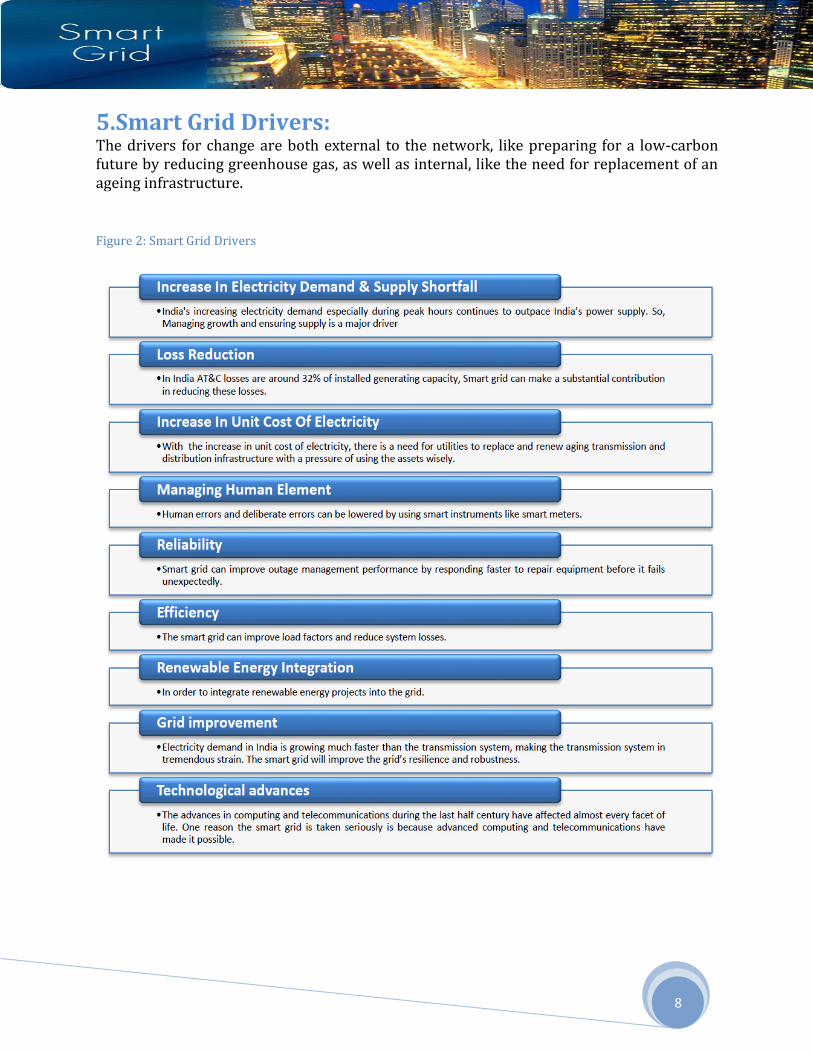

5.Smart Grid Drivers: The drivers for change are both external to the network, like preparing for a low-carbon future by reducing greenhouse gas, as well as internal, like the need for replacement of an ageing infrastructure.

Figure 2: Smart Grid Drivers

9

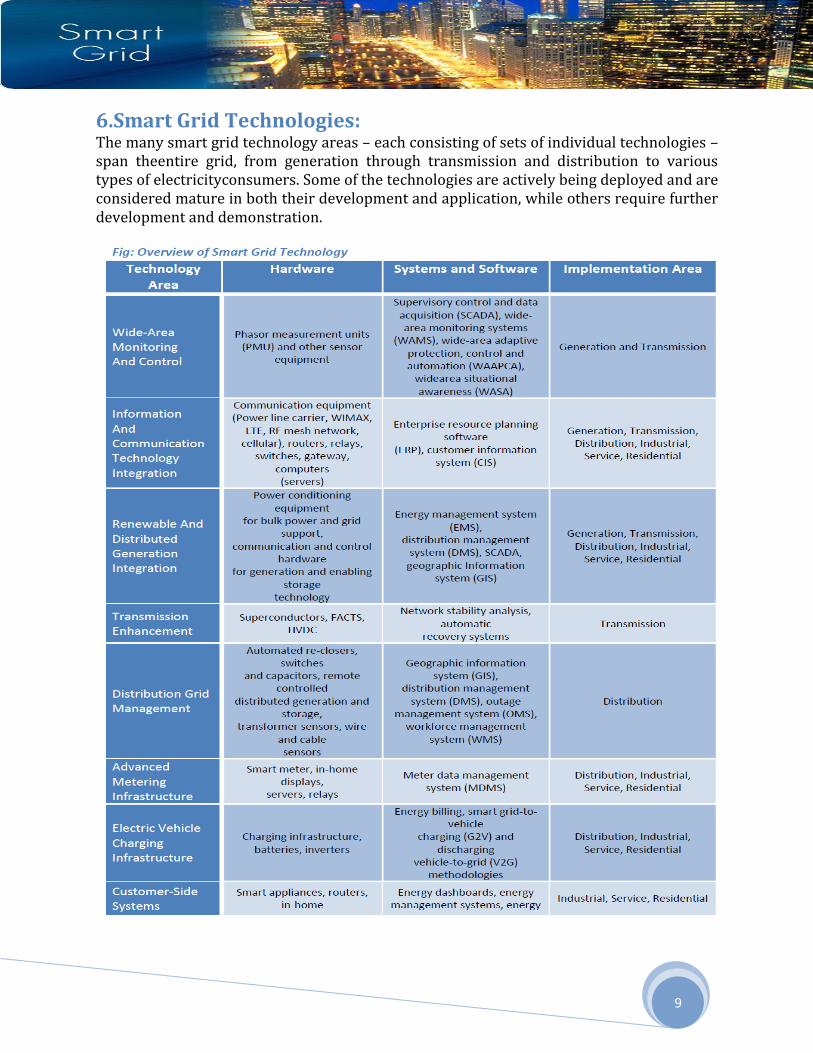

6.Smart Grid Technologies: The many smart grid technology areas – each consisting of sets of individual technologies – span theentire grid, from generation through transmission and distribution to various types of electricityconsumers. Some of the technologies are actively being deployed and are considered mature in both their development and application, while others require further development and demonstration.

10

7.Key Characteristics of Smart Grid:

Smart grid might be defined by its capabilities and operational characteristics rather than by

theuse of any particular technology. Deployment of smart grid technologies will occur over a

longperiod of time, adding successive layers of functionality and capability onto existing

equipment and systems. Technology is the key consideration to build smart grids and it can be

defined by broader characteristics.

11

8.Smart Grid and Integration of Renewable Energy Sources: Renewable-energy resources vary widely in type and scalability. They include biomass, waste,geothermal, hydro, solar, and wind. Renewable-energy resources can be used for standalone or islanded (system isolated) power generation, but their benefits are greatly enhanced when they are integrated into broader electric power grids. With greater use of smart grid technologies, higher degrees and rates of penetration can be accommodated. Each resource is different

from the grid’s perspective and some are easier to integrate than others. Variable generation, provided by many renewable-energy sources, can be a challenge to electric system operations, but when used in conjunction with smart grid approaches, responsive distributed generation also can be a benefit to system operations if coordinated to relieve stress in the system.

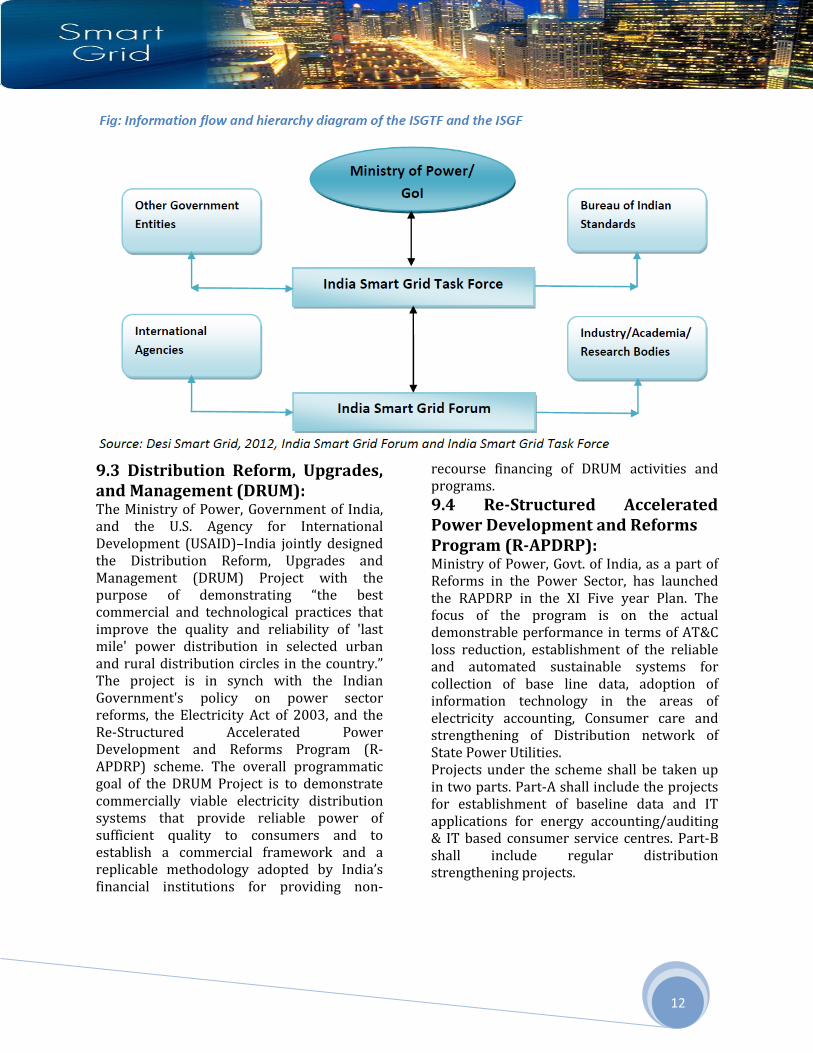

9.Indian Government Initiatives toward a Smart Grid: 9.1.India Smart Grid Task Force (ISGTF): The Government of India formed the India Smart Grid Task Force in 2010 as an inter-ministerial group and will serve as the government focal point. It is a body composed of officials from different government departments and is primarily meant for understanding and advocating policies in smart grid technologies. Major functions of the ISGTF are: a. Ensure awareness, coordination, and integration of diverse activities related to smart grid technologies b. Promote practices and services for R&D of smart grids c. Coordinate and integrate other relevant intergovernmental activities d. Collaborate on an interoperability framework

e. Review and validate recommendations from the India Smart Grid Forum.

9.2. India Smart Grid Forum (ISGF): The Government of India also formulated the India Smart Grid Forum in 2010 as a non-profit, voluntary consortium of public and private stakeholders with the prime objective of accelerating development of smart grid technologies in the Indian power sector. The ISGF has roles and responsibilities complementary to the ISGTF. The goal of the Forum is to help the Indian power sector to deploy Smart Grid technologies in an efficient, cost-effective, innovative and scalable manner by bringing together all the key stakeholders and enabling technologies. The India Smart Grid Forum will coordinate and cooperate with relevant global and Indian bodies to leverage global experience and standards where ever available or helpful, and will highlight any gaps in the same from an Indian perspective.

12

9.3 Distribution Reform, Upgrades, and Management (DRUM): The Ministry of Power, Government of India, and the U.S. Agency for International Development (USAID)–India jointly designed the Distribution Reform, Upgrades and Management (DRUM) Project with the purpose of demonstrating “the best commercial and technological practices that improve the quality and reliability of 'last mile' power distribution in selected urban and rural distribution circles in the country.” The project is in synch with the Indian Government's policy on power sector reforms, the Electricity Act of 2003, and the Re-Structured Accelerated Power Development and Reforms Program (R-APDRP) scheme. The overall programmatic goal of the DRUM Project is to demonstrate commercially viable electricity distribution systems that provide reliable power of sufficient quality to consumers and to establish a commercial framework and a replicable methodology adopted by India’s financial institutions for providing non-

recourse financing of DRUM activities and programs.

9.4 Re-Structured Accelerated Power Development and Reforms Program (R-APDRP): Ministry of Power, Govt. of India, as a part of Reforms in the Power Sector, has launched the RAPDRP in the XI Five year Plan. The focus of the program is on the actual demonstrable performance in terms of AT&C loss reduction, establishment of the reliable and automated sustainable systems for collection of base line data, adoption of information technology in the areas of electricity accounting, Consumer care and strengthening of Distribution network of State Power Utilities. Projects under the scheme shall be taken up in two parts. Part-A shall include the projects for establishment of baseline data and IT applications for energy accounting/auditing & IT based consumer service centres. Part-B shall include regular distribution strengthening projects.

13

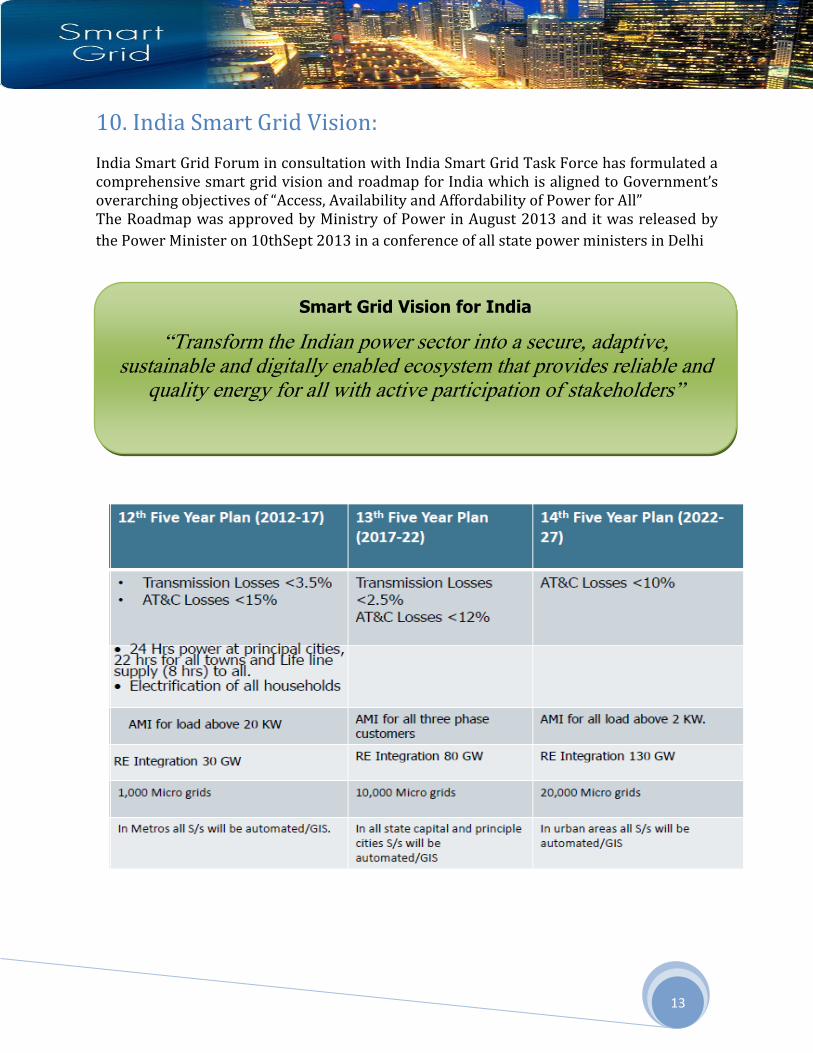

10. India Smart Grid Vision:

India Smart Grid Forum in consultation with India Smart Grid Task Force has formulated a comprehensive smart grid vision and roadmap for India which is aligned to Government’s overarching objectives of “Access, Availability and Affordability of Power for All” The Roadmap was approved by Ministry of Power in August 2013 and it was released by

the Power Minister on 10thSept 2013 in a conference of all state power ministers in Delhi

Smart Grid Vision for India

“Transform the Indian power sector into a secure, adaptive, sustainable and digitally enabled ecosystem that provides reliable and

quality energy for all with active participation of stakeholders”

14

11.National smart grid mission: Role of National Smart Grid Mission(NSGM):

Pre-feasibility study

Technology selection

Cost-Benefit analysis

Financing models

Training & capacity building

Technology selection guide lines & best practices

Consumer awareness

Project appraisal post implementation

12.Smart Grid Projects in India:

12.1.Running/Implemented:

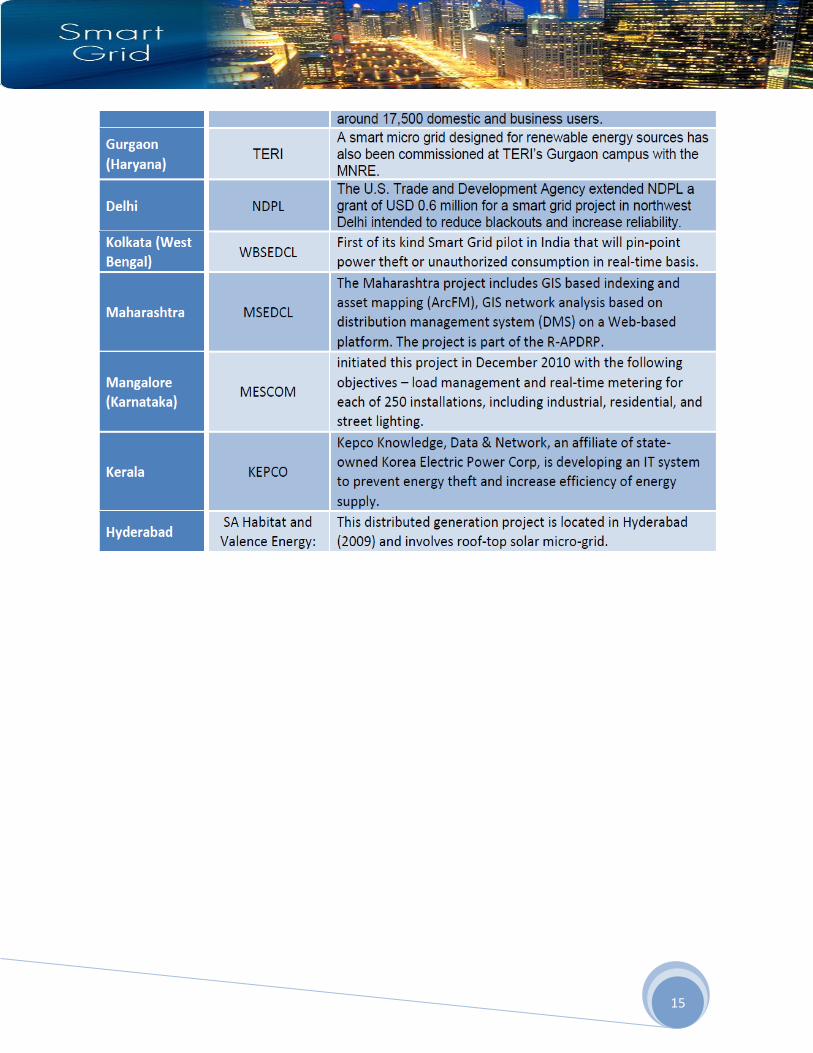

Fig: Major Initiatives taken for Smart Grid Implementation in India

15

16

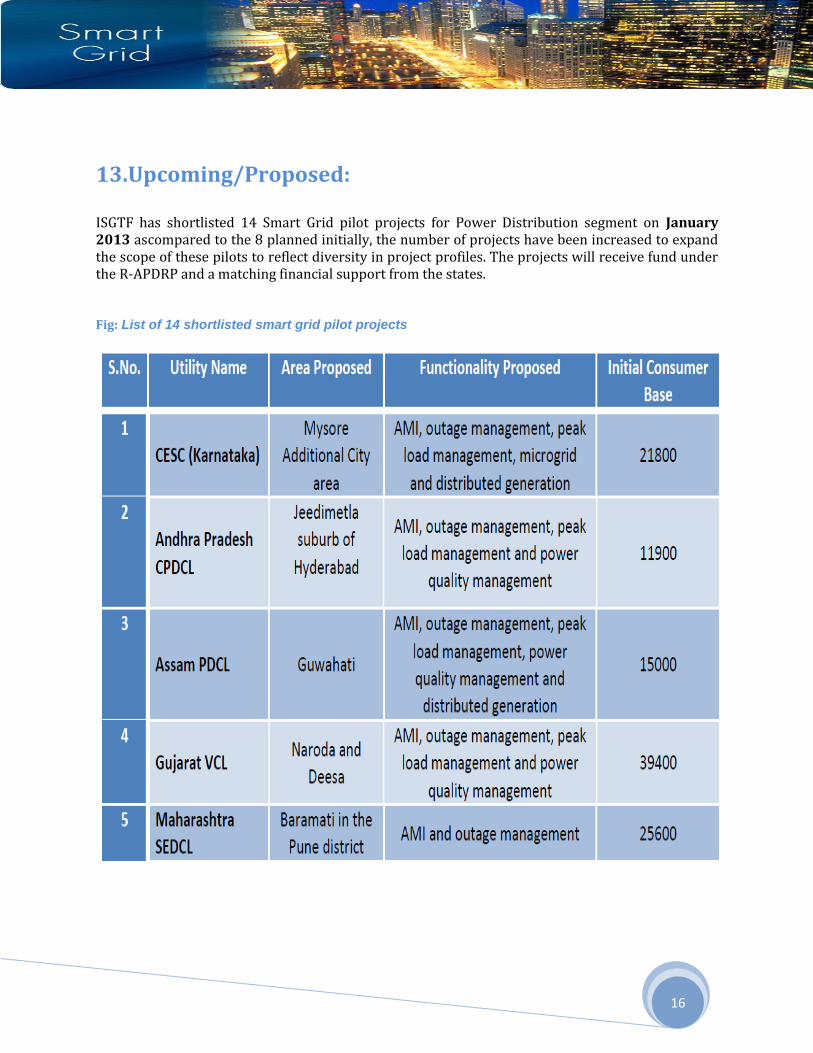

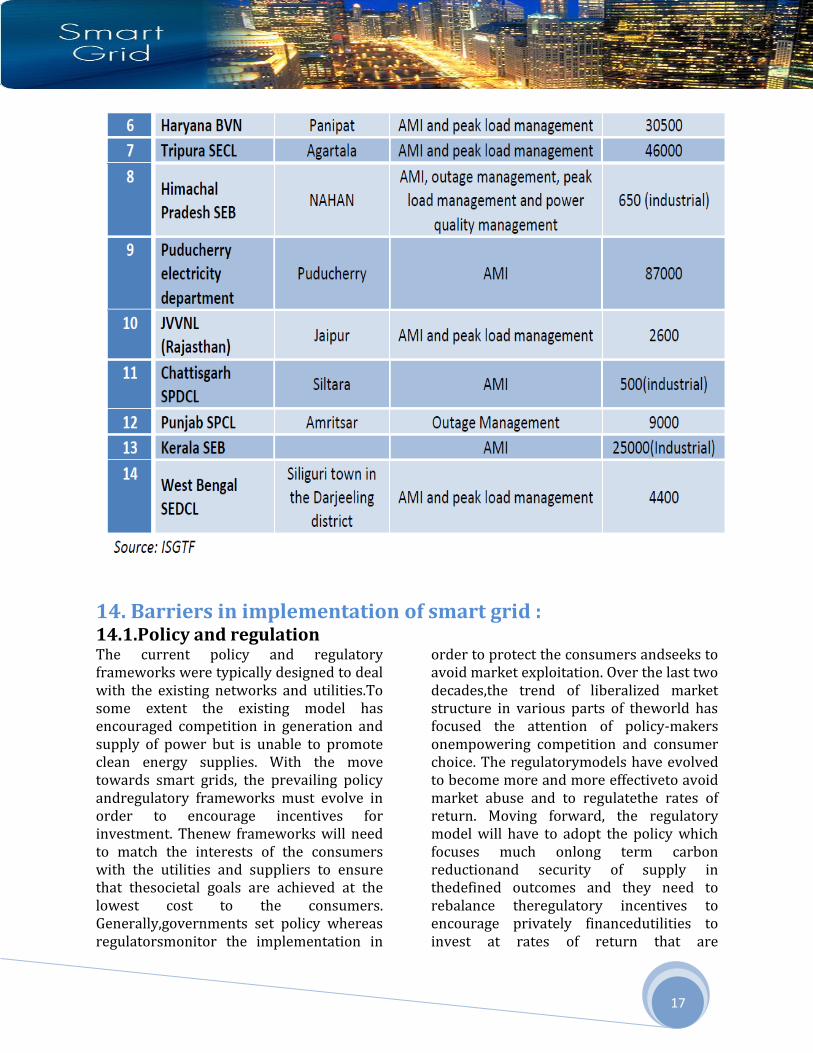

13.Upcoming/Proposed: ISGTF has shortlisted 14 Smart Grid pilot projects for Power Distribution segment on January 2013 ascompared to the 8 planned initially, the number of projects have been increased to expand the scope of these pilots to reflect diversity in project profiles. The projects will receive fund under the R-APDRP and a matching financial support from the states. Fig: List of 14 shortlisted smart grid pilot projects

17

14. Barriers in implementation of smart grid : 14.1.Policy and regulation The current policy and regulatory frameworks were typically designed to deal with the existing networks and utilities.To some extent the existing model has encouraged competition in generation and supply of power but is unable to promote clean energy supplies. With the move towards smart grids, the prevailing policy andregulatory frameworks must evolve in order to encourage incentives for investment. Thenew frameworks will need to match the interests of the consumers with the utilities and suppliers to ensure that thesocietal goals are achieved at the lowest cost to the consumers. Generally,governments set policy whereas regulatorsmonitor the implementation in

order to protect the consumers andseeks to avoid market exploitation. Over the last two decades,the trend of liberalized market structure in various parts of theworld has focused the attention of policy-makers onempowering competition and consumer choice. The regulatorymodels have evolved to become more and more effectiveto avoid market abuse and to regulatethe rates of return. Moving forward, the regulatory model will have to adopt the policy which focuses much onlong term carbon reductionand security of supply in thedefined outcomes and they need to rebalance theregulatory incentives to encourage privately financedutilities to invest at rates of return that are

18

commensurateto the risk. This may mean creatingframeworks that allow risk to be shared betweencustomers andshareholders, so that risks and rewards are balanced providing least aggregate cost to the customer. Business Scenario : Themajority of examples results in negative business cases, undermined by two fundamental challenges:

High capital and operating costs – Capital and operating costs include large fixed costs linked to the chronic communications network. Hardware costs do not cause in significant growths in economies of scaleand software integration possess a significant delivery and integration risks.

Benefits are constrained by the regulatoryframework – When calculating the benefits, organizations tend to be conservative in what theycan gather as cash benefits to the shareholders. Forexample, in many cases, line losses are considered to be put on to the customer and as a result anydrop in losses would have no net impact on theutility shareholder. The smart gridbenefits case may begin on a positive note but, as misalignedpolicy and regulatory incentives are factored in, theinvestment becomes less attractive. Therefore regulators are required to place such policies and regulations in place which could provide benefits both to the utilities and the consumers. Therefore the first factor to be considered is to provide incentives to the utilities in order to remove inefficiencies from the system. They should be aptlyremunerated for the line losses on their networks.

On the budget side of the calculation, there is no avoiding the fact that smart technologies are expensive to implement, and at the present level it is right to factor inthe risk associated with delivery. But the policy makers and regulators can mitigate that risk by seeking economies of scale and implementing advanced digital technologies. Technology maturity and delivery risk : Technology is one of the essential constituents of Smart Grid which include a broad range of hardware, software, and communication technologies.Insome cases, the technology is well developed; however,in many areas the technologies are still at a very initial stage of development and are yet to be developedtoa significantlevel. As the technologiesadvances, it will reduce the delivery risk; but till then risk factor have to be included in the business situation. On the hardware side, speedy evolution of technology is seen from vendors all over the world. Many recently evolved companies have become moreskeptical to the communications solutions and havefocused on operating within a suite of hardware andsoftware solutions. Moreover the policy makers, regulators, and utilities look upon well-established hardware providers for Smart Grid implementation.And this trend is expected to continue with increasingcompetition from Asian manufacturers and, as aconsequence, standards will naturally form andequipment costs will drop as economies of scale arisesand competition increases. On the software and data management side, the majorchallengeis to overcome the integration of the entire hardware system and to managehigh volume of data. With multiple software providers come multiple data formats and the need for complex data models. In

19

addition, the proliferation of data puts stresses on the data management architecture that are much similar to the

telecommunications industry than the utilities industry. Many of these issues are

currently being addressed in pilots such as SmartGrid task force and, as a consequence, the delivery risk will reduce as standards will be set up. Lack of awareness Consumer’s level of understanding about how power is delivered to their homes is often low. So before going forward and implementing Smart Grid concepts, they should be made aware about what Smart Grids are? How Smart Grids can contribute to low carbon economy? What benefits they can drive from Smart Grids? Therefore:

Consumers should be made aware about their energy consumption pattern at home, offices...etc.

Policy makers and regulators must be very clear about the future prospects of Smart Grids.

Utilities need to focus on the overall capabilities of Smart Grids rather than mere implementation of smart meters. They need to consider a more holistic view.

Access to affordable capital Funds are one of the major roadblocks in implementation of Smart Grid. Policy makers and regulators have to make more conducive rules and regulations in order to attract more and more private players. Furthermore the risk associated with Smart Grid is more; but in long run it is expected that risk-return profile will be closer to the current situation as new policy framework will be in place and risk will be optimally shared across the value chain. In addition to this, the hardware manufacturers are expected to invest more and more on mass production and R&D activities so that technology obsolescence risk can be minimized and access to the

capital required for this transition is at reasonable cost. Skills and knowledge As the utilities will move towards Smart Grid, there will be a demand for a new skill sets to bridge the gap and to have to develop new skills in analytics, data management and decision support. To address this issue, a cadre of engineers and managers will need to be trained to manage the transition. This transition will require investment of both time and money from both government and private players to support education programs that will help in building managers and engineers for tomorrow. To bring such a change utilities have to think hard about how they can manage the transition in order to avoid over burdening of staff with change. Cyber security and data privacy With the transition from analogous to digital electricity infrastructure comes the challenge of communication security and data management; as digital networks are more prone to malicious attacks from software hackers, security becomes the key issue to be addressed. In addition to this; concerns on invasion of privacy and security of personal consumption data arises. The data collected from the consumption information could provide a significant insight of consumer’s behavior and preferences. This valuable information could be abused if correct protocols and security measures are not adhered to. If above two issues are not addressed in a transparent manner, it may create a negative impact on customer’s perception and will prove to be a barrier for adoption

20

15.Solutions to overcome the

barriers in implementation:

Despite the challenges mentioned above, there

are anumber of steps that can be taken tospeed

up the implementation of smart grid

technologies. Foremost step that is required to

be taken is that policy-makers andregulators

need to restructure the economic incentives

and align riskand reward across the value

chain. By building the righteconomic

environment for the private sector investment

andfocusing more broadly about the way that

social valuecases are created and presented

implementation would become much easier.

By analyzing thesesolutions in bigger

environments i.e. in cities, the entireindustry

will learn what it takes to implement smart

gridssuccessfully and will result in developing

an industrythat is set to boomin the

comingperiods.

15.1.Forming Political and Economic

Frameworks:

Policy makers and regulators have to

implement a framework which optimally

spread the risk over the whole value chain i.e.

to guard the investors from risk and to yield

the result at lower cost to the customers. They

have to form a robust incentive model in order

to attract more and more private investment.

Also rate of return should be based on the

output generated. Rewards and penalty

mechanism should be considered in order to

monitor the performance of the utilities and to

encourage them to deliver the outcomes in the

most efficient manner. Technological and

delivery risk associated with Smart Grid are

significant. And this can be overcome over a

due course of time as more issues arise and are

addressed. Risks associated with Smart Grid

have to be shared by every member across the

value chain. While making the framework

regulators must consider how much of that

risk a utility can pass on to the contractors,

suppliers and consumers. By maintaining the

proper balance, there will be an improved

alignment of the incentives. And further they

have to tackle numerous policy disputes and

recommend potential solutions.

15.2.Moving Towards a Societal Value

System: The major challenge for the transition from

analogous to digital infrastructure will be to

move from utility-centric investment decision

to societal-level decisions which determine

wider scopes of the Smart Grid. This would

help in the accelerated adoption of Smart Grid

Technology by the society.

15.3.Achieving greater efficiency in energy

delivery : Smart Grid Technology should consider

building greater efficiency into the energy

system which would result in reduction of

losses, peak load demand and thereby

decreasing generation as well as consumption

of energy. New regulatory framework which

incentivizes utilities for reducing the technical

losses would help utilities to perform more

efficiently.

15.4.Enabling distributed generation and

storage: Smart grids will change where, when and how

energy is produced. Each household and

business will be empowered to become a

micro-generator. Onsite photovoltaic panels

and small-scale wind turbines are the

predominant examples; developing resources

consist of geothermal, biomass, hydrogen fuel

cells, plug-in hybrid electric vehicles and

batteries. As the cost of traditional energy

sources continues to rise and the cost of

distributed generation technologies falls, the

economic situation for this evolution will

build.

15.5.Increasing Awareness on Smart Grids:

21

There is an imperative need to make the

society and the policy makers aware about the

capabilities of a Smart Grid. The main step is

to form a perfect, universal description onthe

common principles of a smart grid.Beyond

agreement ona characterization, the matter

also needs to be debated moreholistically as a

true enabler to the low-carbon economy,rather

than as an investment decision to be taken

within the meeting room of distinct

utilities.The importance of consumer

education is not to be underestimated.The

formation of user-friendly andstate-of-the-art

products and services will play a

significantrole in convincing the societyabout

Smart Grids. Also the utilities are required to

scrutinize the major challenges in

implementation of Smart Grid and their

impact on their business model and

operations.

15.6.Creating a Fresh Pool of Skills

andKnowledge : Successful implementation of the smart grid

will require alarge number of highly skilled

engineers and managers mainly thosewho are

trained to work on transmission and

distribution networks.As a result to on-

jobtraining and employees development will

be vitalacross the industry. Simultaneously,

there is a requirement forinvestment in the

development of relevant

undergraduate,postgraduate and vocational

training to make sure theavailability of a

suitableworkforcefor the future. The

investment in T&D should not be limited and

neither in research and knowledge

development, which would be essential for the

development of this sector.

15.7.Addressing Cyber security Risks

andData Privacy Issues Smart Grid success depends on the successful

handling of two major IT issues:

Security

Integration and data handling

With increase in computers and

communication networks comes the increased

threat of cyber-attack. The Government should

look into this matter because

consumer’sconsumption data can be misused

by the utilities and the third party. Utilities

have to give assurance to the consumers that

their valuable information is handled by

authorized party in ethical manner. The

government has to adopt high standard level in

order to withstand cyber-attacks.

16.On-going smart grid activities:

APDRP, R-APDRP initiative for distribution reform (AT&C focus)

DRUM India – Distribution Reform Upgrade, Management

Four pilot sites (North Delhi, Bangalore, Gujarat, Maharashtra)

Smart Grid Vision for India

Smart Grid Task Force – Headed by Sam Pitroda

BESCOM project – Bangalore – Integration of renewable and distributed energy

resources into the grid

KEPCO project in Kerala India - $10 Billion initiative for Smart-Grid

L&T and Telvent project – Maharashtra – Distribution Management System roll-out

Distributed generation via roof-top solar for 40% in a micro-grid

22

17.Recommendations :

Regulators

Create a regulatory framework which

aligns incentives of each member in

the value chain.

Allocate risk and reward efficiently.

Consider both utilities and customer

while making policies.

Adopt output based regulatory system

(Reward/Penalties) which stresses on

utilities to perform better.

Utilities

Adopt more holistic approach about

Smart Grids, so that they can convey

its future benefits to the customers.

Reduce the risk of

technologyobsolescence by R&D

activities.

Undertake large scale pilot projects

and analyze the benefits.

Transformation from utility-centric

investment decision to societal-level

decisions.

Vendors

Required to play important role in

policy making process

To help utilities to adopt flexible

design and compatibility of Smart

Grid fast.

To convince customers about the

acceptance of changing trend by

product and service offering.

Customers

Plays critical role by demanding for

more flexible service.

To encourage more players to enter in

this field and in order to make the

market competitive.

To help utilities and regulators to set

goals and make conducive policies.

To increase the awareness in society.

18.Conclusion:

“Smart Grid is a technology that will solve many issues once it becomes a Reality in India’’

It is high time that we start looking at smart grid as a necessity then an opportunity. With

an exponentially increasing demand of power, the supply and pilferage needs to be catered

with whatever it takes. For power sector to continue on the path of economic growth,

deployment and adoption of latest technologies, introduction of more intelligence into the

grid in the form of Smart Grid are inevitable.

The smart grid shall bring efficiency and sustainability in power sector, meeting the

growing electricity demand with reliability, resilience, stability and best of the quality

while reducing the electricity bill of a consumer. It also enables consumer participation in

energy management.

23

BIBILOGRAPHY

http://mnre.gov.in/file-manager/akshay-urja/july-august-2011/EN/Smart%20Grid%20in%20India.pdf

http://www.nsgm.gov.in//upload/files/India-Smart-Grid-Vision-and-Roadmap.pdf

http://ictpost.com/its-time-for-the-electric-grid-to-smarten-up-in-india-2/

http://www.desismartgrid.com/2014/03/can-smart-grid-technology-immersion-linked-better-progress-nation/

http://smartgrid-for-india.blogspot.in/ http://www.iitk.ac.in/npsc/Papers/NPSC2014/1569993451.pdf http://asian-power.com/power-utility/commentary/reality-check-are-indian-utilities-

prepared-smart-metering http://asian-power.com/power-utility/commentary/reality-check-are-indian-utilities-

prepared-smart-metering http://www.nsgm.gov.in//upload/files/India-Smart-Grid-Vision-and-Roadmap.pdf

Top Related