Languages

Pages

Legal

FINANCING OF SMALL SCALE INDUSTRIES SSI BY J&K BANK

Yasir Yousoof Mir , MBA-USB

Priyanka Panday, Research Scholar,USB,Chandigarh university

Dr. Sajjan Chaudhary,Associate professor,Chandigarh university

Abstract

The study was conducted in Jammu and Kashmir bank and has special implications for J & K

bank in long run. The reason behind the financing of small scale industries in special

reference to J & K Bank has to be briefly analysed in order to bring out certain judicious

justifications.

OBJECTIVES: Objectives of this study to find out the key role of J&K bank in financing

SSI units with special focus on challenges faced by SSI in availing credit facility and the

satisfaction level of SSI holders with J& K bank. The study is related to the role played by

the J&K Bank Ltd in financing the small-scale industries operating in Kashmir to ascertain

how far the bank has succeeded in fulfilling the working capital financial requirements of

these industries and what factors influence the loan disbursement to small‐scale industries

METHOD/STATISTICAL TOOL: Primary data was collected through structured

questionnaire and secondary data was used from internet. The data collected is raw and it is

compiled, classified, tabulated and then analyzed using financial techniques and statistical

tools. The data collected was analysed with the help of using Microsoft Excel

APPLICATION: This study was being undertaken and helps us to explore future prospects of

the topic.

Keywords: SSI units, J&K bank, Kashmir, credit facilities

1. Introduction:

The industrial sector plays an important role in the economic growth of both developed and

developing countries. The Small-Scale Industrial (SSI) sector is very important for any

country irrespective of the level of development because, SSI contributes maximum socio-

economic benefits with low level of investment and results in employment creation, income

generation, and poverty alleviation and restricts migration of unemployed and

underemployed workers into cities. It is also one that maximizes the utilization of local

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/148

resources and results in innovations, new technology and is a pathway to emerging

entrepreneurs. It is a starting point for industrial growth.

The Department of Industries & Commerce has a history of hundreds of years. However, the

department was organized in the systematic manner after independence. The last official

document available in the department is of year 1945. Since then Department is continuously

making efforts to promote and develop industrial activity in the state of Jammu & Kashmir.

The Department provides authorization to consultancy set up by unemployed but skilled and

educated youth. At present there are about twenty two consultancy units functioning under

the said departmental authorized to encourage new entrepreneurs to establish new industrial

units. The department has the following approach & strategy to augment industrial activities.

i) Rehabilitation of potentially viable sick industrial units.

ii) Enabling manufactures of quality consistent products to augment their sales within and

outside the state by brand promotion.

iii) Export promotional measures to augment export of products of the state outside the

country.

iv) Environment protection, to conform to state, national & global regulations.

v) Entrepreneurship development in the state, to provide opportunities to educated but

unemployed.

vi) To encourage research and development.

Previously the definition of SSI was any industrial unit in which the investment in fixed

assets in plant and machinery does not exceed Rs 10 lakh but after the enactment of MSME

Act 2006 from in order to ensure the balanced developed of the industrial sector throughout

the country. Under this act the erstwhile “Industry” has been replaced by the nomenclature

“Enterprise” and this has been done with the view to emphasise the importance of service

sector. The act has classified the enterprises into two categories:

1) Enterprises doing manufacturing of goods

2) Enterprises providing services

Manufacturing industries have been defined in terms of investment in machinery and

equipment as under and further classified into:

MICRO ENTERPRISES INVESTIMENT UPTO RS. 25.00 LACS

SMALL ENTERPRISES INVESTIMENT ABOVE RS.25.00 LACS UPTO

RS. 5 CRORE

MEDIUM ENTERPRISES INVESTIMENT ABOVE RS.5.00 CRORE UPTO

RS. 10.00 CRORES

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/149

2. Review of literature:

Nayak and Purusottam (2015) conducted a similar study in north east part of India to find out

the challenges of SSI units. Researchers explained the various aspects of entreprenureship in

these states. Government is promoting this at bigger leel but in line with the earlier studies,

they also concluded the lack of technical assistance and credit facilities as a one of the biggest

challenges. Magnus Magnusson et.al (2012) conducted a study on financing SSI and

concluded that low credit worthiness make these units vulnerable for denial of credits and

even difficult for government to finance fully. One suggestion was also given by the author to

make use of institutional investors for the same purpose.

Rubayat( 2012) found out that there is a greater need to assess the funding requirement and

should provide a wider access to such unit for financing their projects. Various studies have

shown various challenges faced by these SSI units and most of the studies agreed on to the

point of credit related challenges. Gonzaleset et al. (2001) concluded in his study that

financing the projects of SSI is the most critical factor in Asian countries. Many companies

face liquidity issue and find difficult to operate with their internal funding. Saikia and

hemanta(2011) conducted one study on condition of SSIs post globalaization and concluded

that SSIs have played a very important role in the recent development as far as employment

generation is concerned, contribution is significant.G.T, Fatunla et.al (1999) asserted that

SSI should be given proper technical assistance in order to switch from traditional units to

modern way of production. Their capacity is under utilized as they are still not able to have

access to easy credit.

3. Research methodology

The study is confined to five small scale industries in Kashmir (Handi-Crafts, Sericulture,

Cement, Khadi and Food Processing industries). The study is related to the role played by the

J&K Bank Ltd in financing the small-scaleindustries operating in Kashmir to ascertain how

far the bank has succeeded in fulfilling the working capital financial requirements of these

industries and what factors influence the loan disbursement to small‐scale industries

3.1 scope of the study

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/150

This study is confined to five small scale industries (Handi-Crafts, Sericulture, Cement,

Khadi and Food Processing industries), operating in the Kashmir division. This study is

related to the role played by The Jammu & Kashmir Bank in financing the small-scale

industries in Kashmir.

3.2 Objective of the study

The various objectives of the study are:

To study the key role of J&K Bank in financing SSI.

To study the problems faced by small scale industries in availing the credit

facility.

To Study the level of satisfaction of SSI’s holders with J&K bank

regarding the financial help provided by the bank.

To find out the present requirements of financing products by SSI’s.

To study the incentives provided by the Department. Of Industries &

Commerce J&K for SSI, s in the Valley.

3.3 Sampling and data collection

Survey method and personal interview is used to collect data from the randomly selected five

small scale industries by using the close‐ended structured questionnaire. This study is

empirical and mostly depends on primary data. Study is based on the various data provided

by bank officials and data from research literature is thoroughly studied and interpretations

made thereof. Primary data has also been collected from anonymous bank staff. The

responses of all the questions in the questionnaire were tested by using the five-points Likert

scale.

3.4 sample size

In the study the sample size was 60, the respondents were selected from different regions

across the valley. For the study I have targeted respondents from major areas.

These areas were selected for the data collection due to certain reasons. Here I have easy

access to the targeted people, easily targeted different income group respondent. The target

respondents were Entrepreneurs, Managers and employees of SSI’s. I have targeted

respondent from different Managerial levels and occupations. The technique of sampling

used is Simple Random Sampling

3.4 sources of data

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/151

Primary data was collected through structured questionnaire and secondary data was used

from internet and other internal sources of company. Additionally many finance blogs were

consulted including some books and some journals, pump-lets published by DIC as well.

Some research papers on financing of small scale industries also proved to be of very great

help.

3.5 Data analysis method

The data collected is raw and it is compiled, classified, tabulated and then analyzed using

financial techniques and statistical tools. Graphs and charts are used to highlight the statistics.

Based on this data and analysis, inferences were drawn.

4. Data analysis

The data collected was analysed with the help of using Microsoft Excel

Pie Chart

Bar Chart

Mean

1: Age of the industry [SSI unit financed by jk bank?

0-10yrs 10-20yrs 20-30yrs 30-40yrs Above 40yrs

15 6 29 7 3

2: Investment in the industry for establishment of the unit?

0-10yrs25%

10-20yrs10.00%

20-30yrs48.33%

30-40yrs12%

Above 40yrs5.00%

Age of the Industry

0-10 yrs

10-20 yrs

20-30 yrs

30-40 yrs

Above 40 yrs

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/152

3:Your Banking Relationship?

25%

41.66%

16.66%10%

5% 1.66%0

20

40

60

80

100

0-15 lacs 15-30 lacs 30-45 lacs 45-60 lacs 60-75 lacs 75lacs-1cr

Investment

Banking Relations

83.33%

6.66% 3.33% 3.33% 3.33%

0

20

40

60

80

100

JK bank HDFC PNB SBI None

Banking Relations

Banking Relations

% a

ge o

fSS

I's

0-15

Lacs

15-30

Lacs

30-45

lacs

45-60

Lacs

60-75

lacs

75 lacs-1 cr

15 25 10 6 3 1

JK BANK HDFC PNB SBI None

50 4 2 2 2

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/153

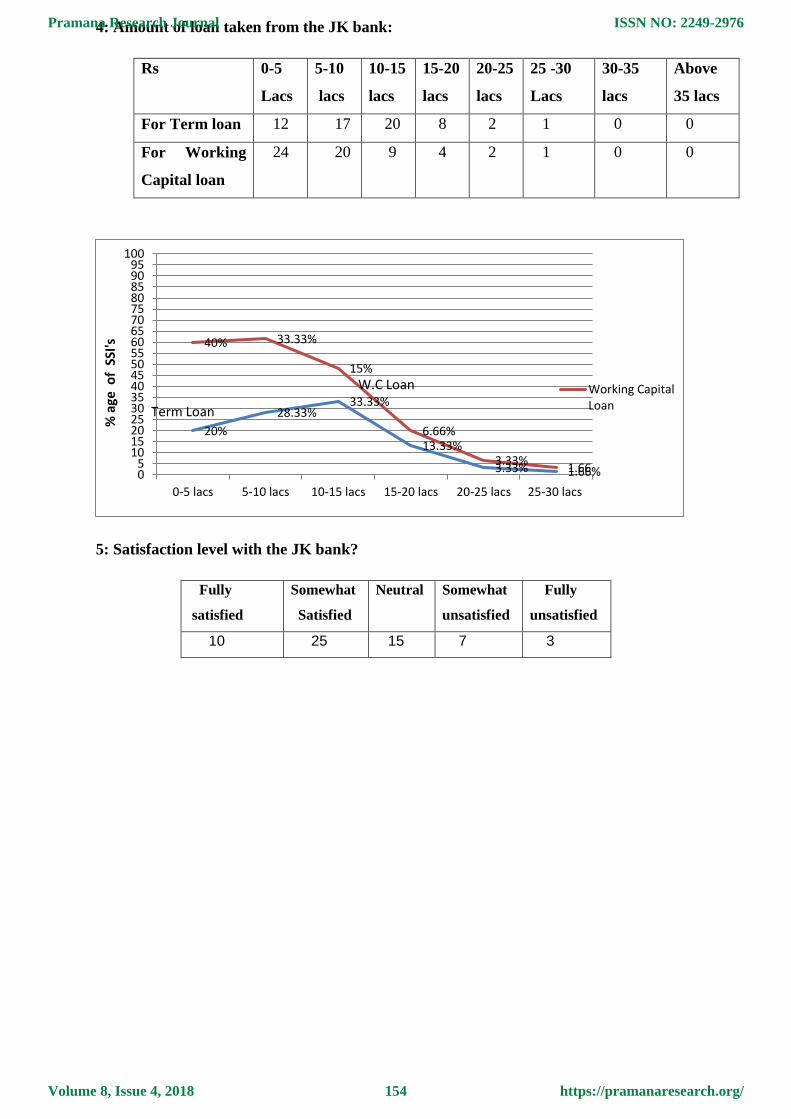

4: Amount of loan taken from the JK bank:

Rs 0-5

Lacs

5-10

lacs

10-15

lacs

15-20

lacs

20-25

lacs

25 -30

Lacs

30-35

lacs

Above

35 lacs

For Term loan 12 17 20 8 2 1 0 0

For Working

Capital loan

24 20 9 4 2 1 0 0

5: Satisfaction level with the JK bank?

Fully

satisfied

Somewhat

Satisfied

Neutral Somewhat

unsatisfied

Fully

unsatisfied

10 25 15 7 3

20%

28.33%33.33%

13.33%

3.33% 1.66%

40% 33.33%

15%

6.66%

3.33%1.660

5101520253035404550556065707580859095

100

0-5 lacs 5-10 lacs 10-15 lacs 15-20 lacs 20-25 lacs 25-30 lacs

Working CapitalLoan

% a

ge o

f S

SI's

W.C Loan

Term Loan

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/154

6: Awareness about the RBI guidelines (regarding SSI loans)?

7:

7: Satisfaction with the security demanded by the JK Bank for loans?

0

5

10

15

20

25

30

F.S Sw. S Neutral Sw. NS F.Us

Column1

Series 1

10%16.66%

35% 31.66%

6.66%

0

20

40

60

80

100

Fully aware Somewhat aware Neutral Somewhatunaware

fully unaware

Awareness

% age

of SSI's

Fully

Aware

Somewhat

aware

Neutral Somewhat

unaware

Fully

unaware

6 10 21 19 4

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/155

8: JK bank keeps privacy & confidentiality of your business & personal information?

9: How much of your profitability has been increased by getting loan?

46.66%

16.66%

16.66%

13.3%

6.6%

Satisfaction

fully satisfied

somewhat satisfied

neutral

somewhat unsatisfied

fully unsatisfied

S.D.A11.66%

D.A13.33%

N18.33%A

33.33%

S.A23.33%

.

Strongly disagreed(S.D.A)

Disagreed(D.A)

Neutral(N)

Agreed(A)

Strongly agreed(S.A)

Strongly

disagreed

Disagreed Neutral Agreed Strongly

agreed

7 8 11 20 14

Fully

satisfied

Somewhat

Satisfied

Neutral Somewhat

unsatisfied

Fully

unsatisfied

28 10 10 8 4

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/156

10: Which measure will be more effective to improve SSI’s?

Implementation

of schemes

Decreasing

Interest

rate

Introduction

new

schemes

Advertiseme

nt

Decreasing

Demand for securities

8 26 6 13 5

48.33%

25%16.66%

8.33%1.66%0

10

20

30

40

50

60

70

80

90

100

0 5 10 15 20 25

Profitability

% age

of

SSI'

s

13.33%

43.33%

10%

21.66%

8.33%

0102030405060708090

100

Implementation ofschemes

Decreasing int.rate Itroduction of newschemes

Advertisement Decreasing Demandfor security

Effectiveness

.

% a

ge o

f S

SI's

0-5% 5-10% 10-15% 15-20% Above 20%

29 15 10 5 1

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/157

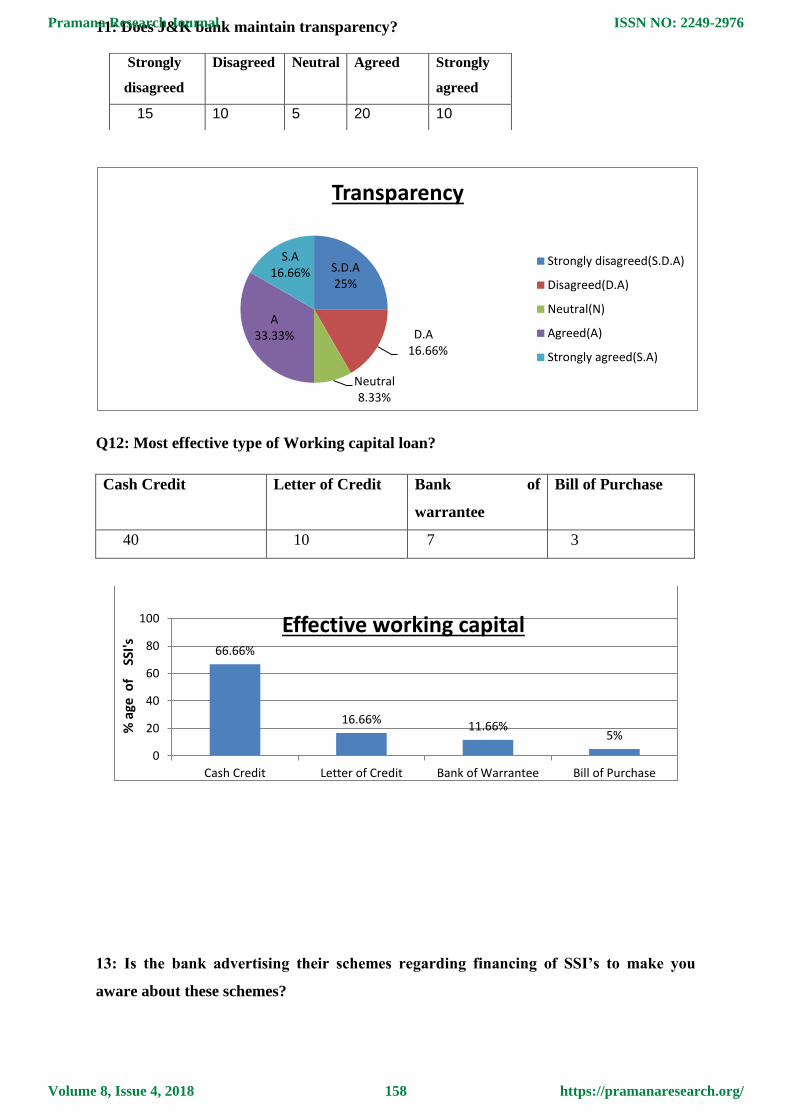

11: Does J&K bank maintain transparency?

Q12: Most effective type of Working capital loan?

Cash Credit Letter of Credit Bank of

warrantee

Bill of Purchase

40 10 7 3

13: Is the bank advertising their schemes regarding financing of SSI’s to make you

aware about these schemes?

S.D.A25%

D.A16.66%

Neutral8.33%

A33.33%

S.A16.66%

Transparency

Strongly disagreed(S.D.A)

Disagreed(D.A)

Neutral(N)

Agreed(A)

Strongly agreed(S.A)

66.66%

16.66%11.66%

5%

0

20

40

60

80

100

Cash Credit Letter of Credit Bank of Warrantee Bill of Purchase

Effective working capital

% a

ge o

f

SSI's

Strongly

disagreed

Disagreed Neutral Agreed Strongly

agreed

15 10 5 20 10

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/158

Yes No

40 20

14: what type of Promotional mix will be effective to make you aware about the schemes

regarding financing of SSI’s?

0

20

40

60

80

100

Advertising

.

% a

ge o

f

SSI's

Sales promotion Advertisement Publicity Personal

selling

Social mobalisation

& ownership capital

2 18 5 15 20

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/159

FINDINGS

JK Bank is the bank providing loans to SSI’s at very low interest rate.

The study reveals that about 90% of Small Scale Industries in Kashmir have

maintained their relationship with JK Bank and only 10% of SME’s have maintained

their relationship with other (i.e. SBI ,PNB etc) banks.

The study reveals that most of the SSI’s have investment not greater than 20 lacks i.e.

these industries are at the bottom of given value of investment given by RBI for an

industry for being an SSI (i.e. 1 corer).

The study reveals that most of the SSI’s are satisfied with the overall contribution of

JK bank towards SSI’S.

The study reveals that most of the SSI’s are not fully aware from the guidelines given

by RBI to the banks for financing SSI’s.

About 70% of SSI’s are not satisfied with securities demanded by the bank for getting

loans. According to them bank is demanding collateral securities which is about two

times greater than the actual loan to be taken, While as other banks are demanding

less collateral securities in comparison to JK Bank.

The study reveals that 70-75% Management of SSI’s in Kashmir are not satisfied with

the Privacy & confidentiality of their information(both of business & personal) kept

by the bank.

About 85% of SSI’s are saying that they are making a reasonable increase (from 5-

15%) in the profit by getting loan from the bank.

Most of the SSI’s are more interested in getting working capital loan rather than Term

loans .Only about 25% of SME’s are interested in taking Term loans for purchasing

the new technological machineries.

3.33%

30%

8.33%

25%33.33

0

20

40

60

80

100

Sales promotion Advertisement Publicity Personal selling SM&OC

Effectivness

.

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/160

Most of the SSI’s want decrease in the Interest rate, also are unsatisfied with

commitments of the bank to implement new schemes & also are unsatisfied with the

Advertisement strategy of the bank for the new schemes.

Most of the SSI’s are more interested in the Cash credit type of working capital loan.

About all SSI’s are complaining about the low consideration by the government.

Bank is continuously taking steps to improve SME’s.

SSI managers are also complaining about the slow service & overall behaviour of the

bank staff.

This time bank is continuously organizing meetings with the entrepreneurs of SSI’s in

order to discuss the new steps that should be taken to improve SSI’s.

The managers of SSI’s are also complaining about the non-implementation of the

scheme i.e. lower down rate and also rescheduling the instalment schedule.

The managers of SSI’s are also complaining about the winding up of Business

Development Promotion Cell (BDPC) and are not satisfied with Cluster making

strategy by the bank.

Most of the Sick industries are winded up in the valley because of 30% margin kept

by bank to sick industries.

.Most of the %age of the managers of SME’s are complaining about the editing of

Project plan (deposited by SME’s to the bank for which they have applied for loan) by

the bank.

Most of the %age of the managers of SSI’s are not satisfied with the Marketing

strategies of the bank.

Suggestions and Recommendations

RBI should make new strategies to make Industries and SSI’s particularly aware

about their guidelines to the banks for financing Industries and SSI’s in the Valley.

The formalities for SSI’s for getting loan should be reduced.

The Securities especially Collateral securities demanded for getting loans, which are

about twice the actual amount of loan, should be decreased.

Although the bank is providing loan to SSI’s at low rate of interest in comparison

with the other banks , but SSI’s have more expectations on J&K Bank ,so the bank

should decrease the interest rate which is PLR-1.50 for 2-5 lacks should be

decreased to PLR-2.

J&K Bank should keep Privacy & confidentiality of information (both of business &

personal) of SSI’s.

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/161

Bank should not do any kind of editing in SME’s Project plan for which they have

applied for loan because it can make failure of that plan.

All loan applications received under SSI Sector should be disposed Off by the

branches within in minimum period of time

The bank should follow sharply all the RBI guidelines in financing SSI’s .

The bank should make available, free of cost, simple standardized, easy to understand,

and application form for loans.

The bank should focus more on improvement of SSI’s and should achieve targets in

Priority Sector Lending.

The bank should restore Business Development Promotion Cell (BDPC).If BDPC is

restored their focal point should be industries.

The bank should locate branches in every industrial area for the convenience of SSI’s.

Every SSI Entrepreneur should be given rights to present their grievances and

suggestions to the bank.

Government should help SSI’s through providing Subsidy, good Infrastructure and

also should help them in the marketing of their products.

The new schemes/policies should be implemented which needs sharp supervision on

middle and lower management.

Bank should do proper recruitment, and train the staff about the proper and quick

service.

Bank should make regular advertisement of their new schemes for SSI’s in order to

make them familiar with the new schemes introduced by the bank.

There should be more than 20 lacks sanctioning competence to the branch placed in

the industrial area.

The bank should introduce new schemes for SSI’s in order to improve them.

Government intervention is very must for the Small Scaleindustries in the valley.

Sound government policy is required for the promotion of this industrial sector.

Financial institutions need to be strengthened.

Entrepreneurs of SSI’s need to come forward with their innovative projects.

LIMITATIONS OF THE STUDY

Some of the information is considered confidential and not available for study

The data taken for interpretation is for a limited period.

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/162

The study is limited to the Kashmir region only.

As the questionnaire was self-administered personal bias of administrator may be

a limiting factor.

CONCLUSION

The industrial sector plays an important role in the economic growth of both developed and

developing countries.

The Small Scale Industrial (SSI) sector is very important for any country irrespective

of the level of development because, SSI contributes maximum socio economic

benefits with low level of investment and results in employment creation, income

generation, and poverty alleviation and restricts migration of unemployed workers

into cities.

SSI’s is also one that maximizes the utilization of local resources and results in

innovations, new technology and is a pathway to emerging entrepreneurs.

SSI’s are the starting point for industrial growth.

Small and medium scale industries (SMIs) have been considered essential for

economic development not only in less developed countries (LDCs) but also in more

developed regions of the world. Since they are seen being more dynamic, innovative

and have higher labour absorptive capacities than their corporate counterparts, the

SMI sector has been the backbone of industrial development in many developed

countries.

SMIs have played a significant role in Valley’s economic development. In Kashmir,

SSI’s have been estimated as providing 21% of total employment and have fulfilled

important functions such as being the foundation for local entrepreneurship and

innovation, as critical supporting industry.

Problems faced by the SMI sector in the Valley can be divided into those from the

demand and supply side.

Constraints of the demand side cover competition from domestic and foreign sources,

non-availability of market information and inadequate market access

The working in DIC is slow which should be streamlined for disposal of cases of

SSI’s

The unit holders requires hassle free services from DIC for clearness and registration

of cases

J&K Bank should categorize its credit policy towards the SSI sector ,this sector has

high potential in the Valley.

The performance of the J&K Bank is quite satisfactory.

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/163

BIBLIOGRAPHY

Websites

https://www.jkbank.net

http://shodhganga.inflibnet.ac.in/bitstream/10603/684/7/07_chapter-i.pdf

https://www.preservearticles.com.

https://moneycontrol.com

Research Papers

Daniel L. Bond, Daniel Platz and Magnus Magnusson, “Financing small-scale

infrastructure investments in developing countries”,may 2012.

Alan Dale C. Gonzales, “Financing Issues and Options for Small-Scale Industrial

CDM Projects in Asia”.

Jesmin, Rubayat, “financing the small scale industries in bangladesh: the much-talked

about, but less implemented issue”,vol 16 ,no1.

Purusottam Nayak, “Role of Financial Institutions in Promoting Entrepreneurship

In Small Scale Sector in Assam.”

Hemanta Saikia, “Total Factor Growth in Small Scale Industries Some Evidences

from India,the Romanian Economic Journal,sep2012.

DamayanthiMenike MGP, “Role of bank in financing SSI’s in srilanka.”

Annul Report 2011-2012, “MSME-DI Jammu Kashmir.”

Magazines/Journals

Prof. Jayshri J Kadam,Prof. Dr. V.N. Laturkar, Lecturer, IBMRD, A.Nagar, India

Reader, SRTMU, Nanded, India,(aug 2011), Intrernational Journal of Exclusive

Management Research”,A study of Financial Management in Small Scale Industries

in India vol 1, issue 3,pp.1 -8.

Dr. K.A. Goyal & Vijay Joshi,(2012) Indian Banking Industry Challenges And

Opportunities .International Journal of Business Research and Management

(IJBRM), Vol 3, no 1, pp.30 -48

Dr k Ramakrishnan,(2013)The Indian Banker.the Monthly Journal Published by the

Indian Bank’s Association,vol 8, no 7, pp. 44-48

A.K.Dewani (2005),j&k state industrial policy 2002-2015,Avinash &Avinash.,pp 19-

25

Bajpai ,Naval,Business Research Methods,Pearson publishers Ltd.,pp 70-86, 93-

95,699-705

Pramana Research Journal

Volume 8, Issue 4, 2018

ISSN NO: 2249-2976

https://pramanaresearch.org/164

Top Related