Languages

Pages

Legal

Algorithmic Trading

and

Trading Platform

Sergey Troshin, Ph.D.

EXANTE. Director

[email protected] www.exante.eu

SSE, Riga, Jan 2015

Contents

• EXANTE history and Unique Selling Points (5 min)

• Trading. Manual. Automatic - well known approaches (30 min)

• Broker inside out - technical aspects (30 min)

• Questions and Answers (15+ min)

• Working in EXANTE

EXANTE History

Global HedgeCapital Fundby EXANTE founders2007

November

Frustrationwith brokers increases

slow!

limited products!

primitive!

not flexible!

2007

2010

Brokerageplatform startsnamed EX ANTE2010

January

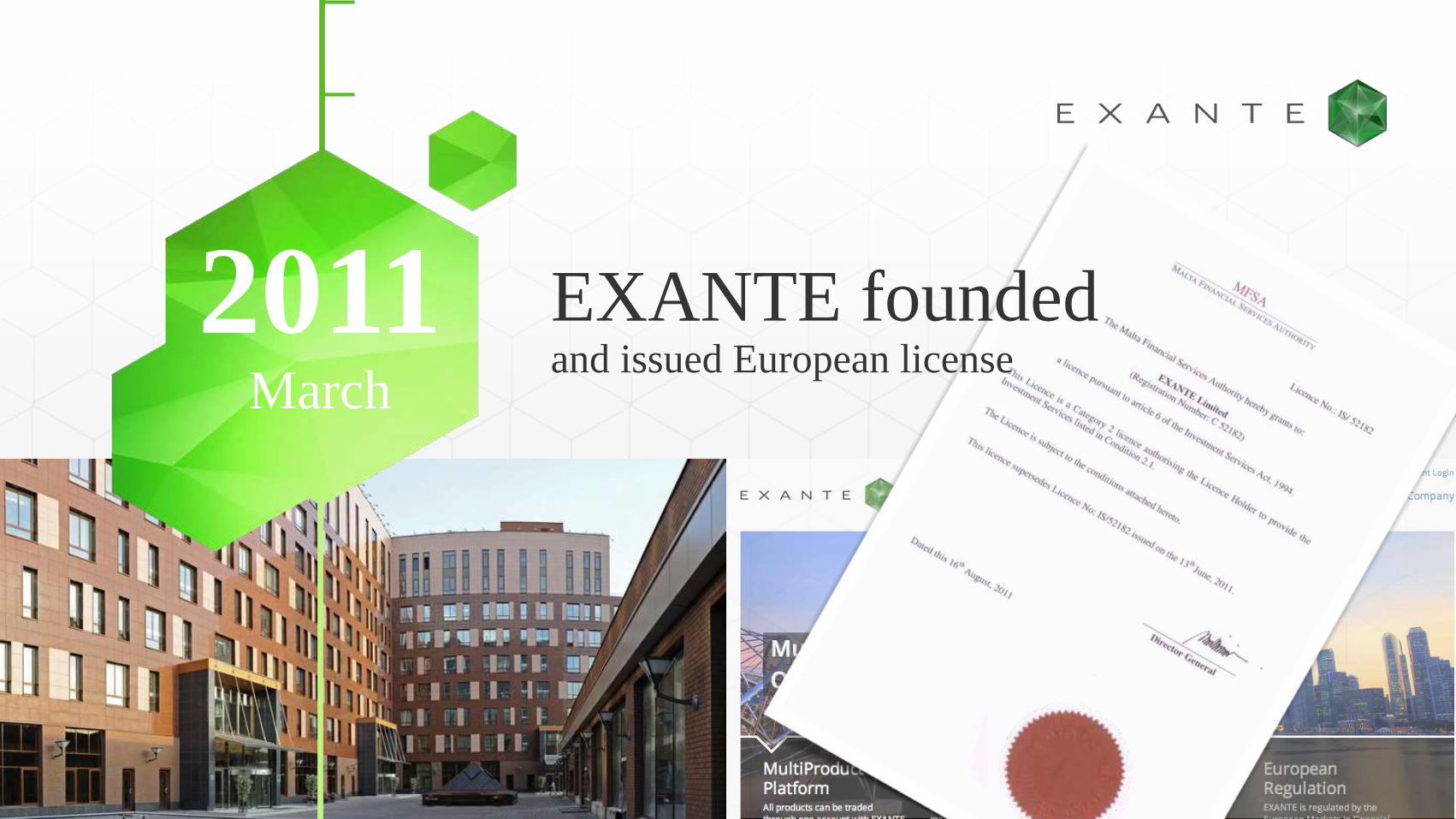

EXANTE foundedand issued European license

2011March

6 Offices

Coverage

FiFixed Income

FtFutures

OpOptions

FnFunds

BfBitcoin Fund

StStocks & ETFs

FxFX & Metals

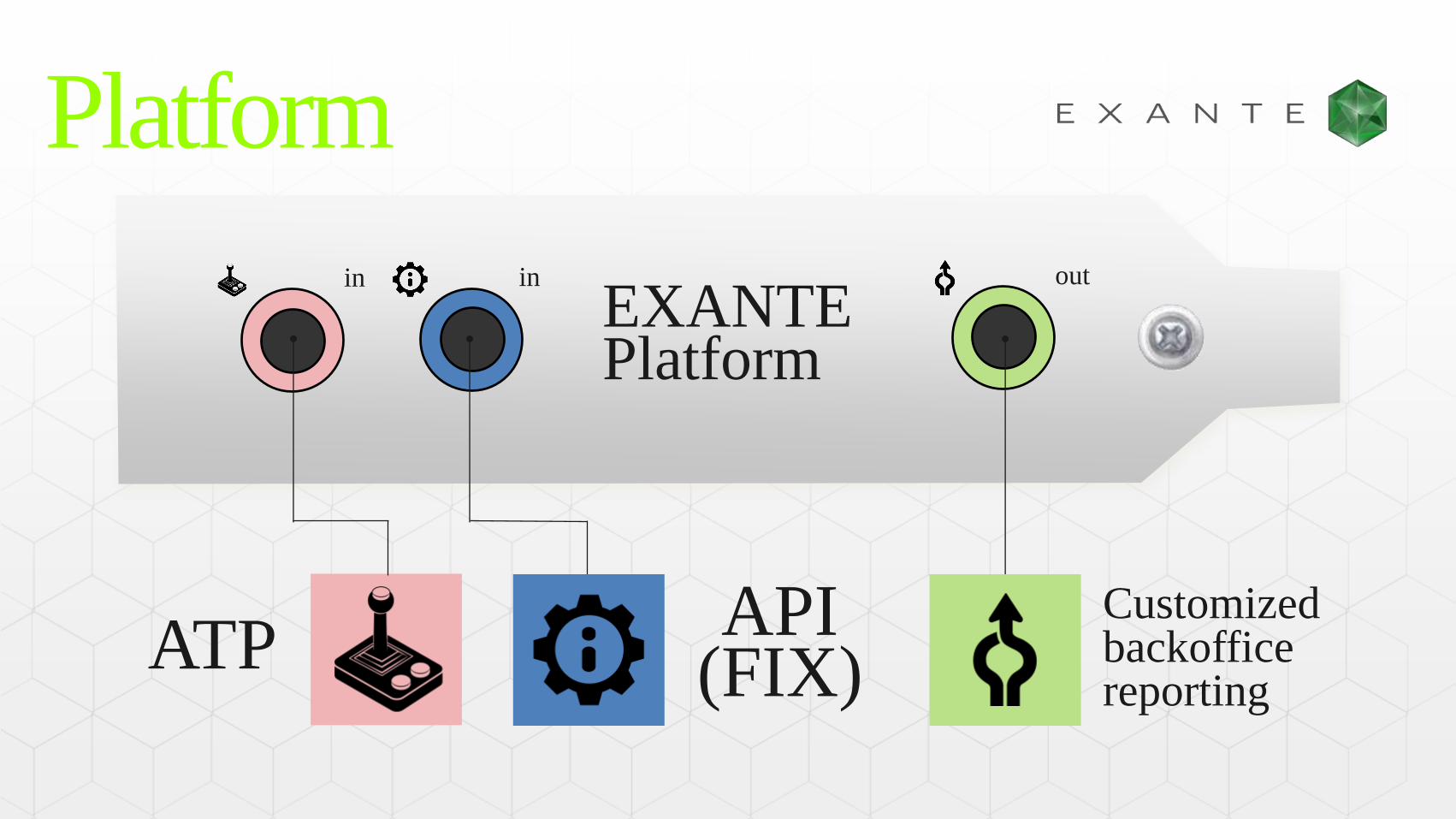

EXANTE Platform

inin

ATP

out

Customized backoffice reporting

API(FIX)

Platform

300 +

Servers

Trading. Manual and Algorithms.

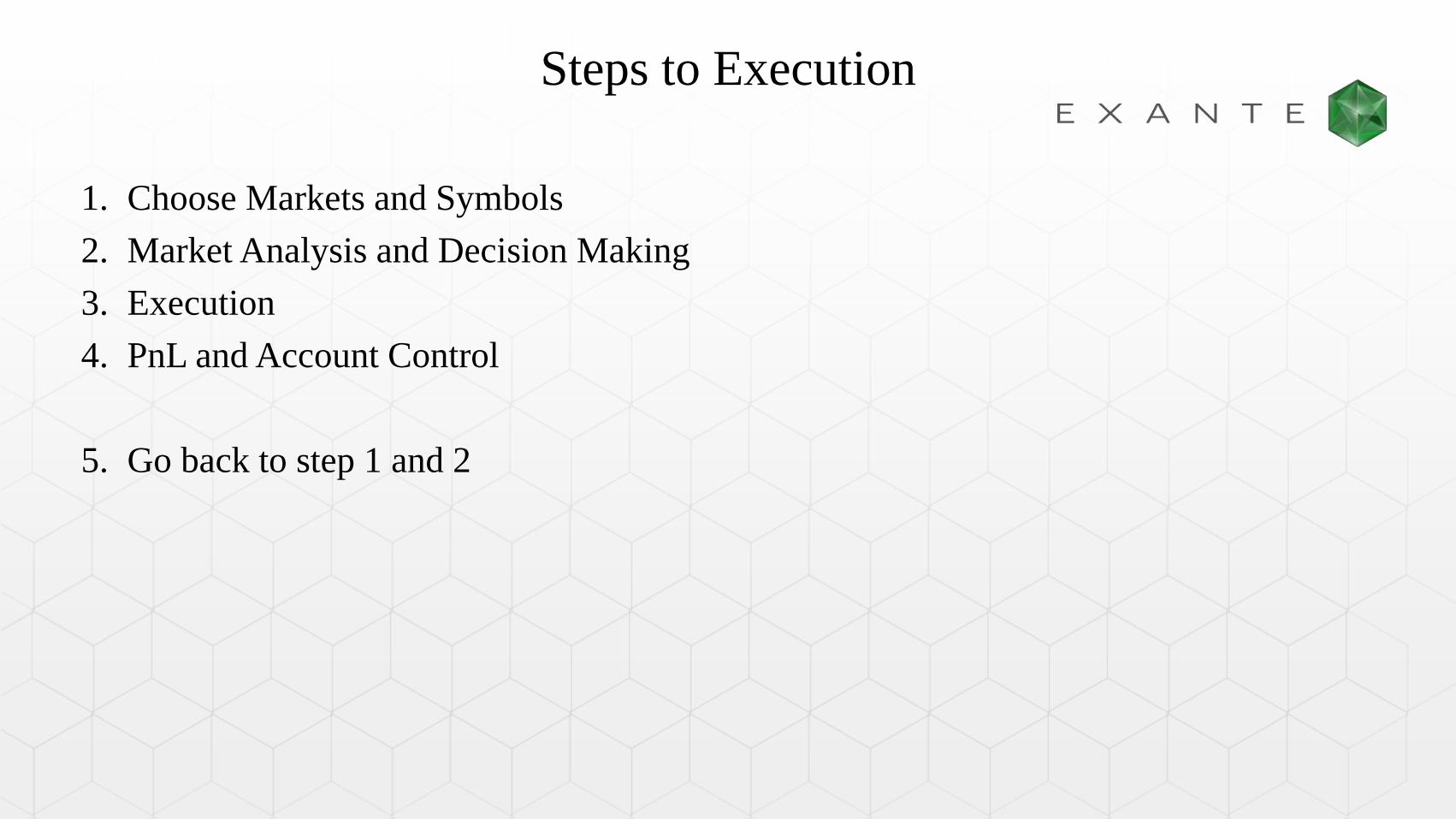

Steps to Execution

1. Choose Markets and Symbols

2. Market Analysis and Decision Making

3. Execution

4. PnL and Account Control

5. Go back to step 1 and 2

Manual Trading

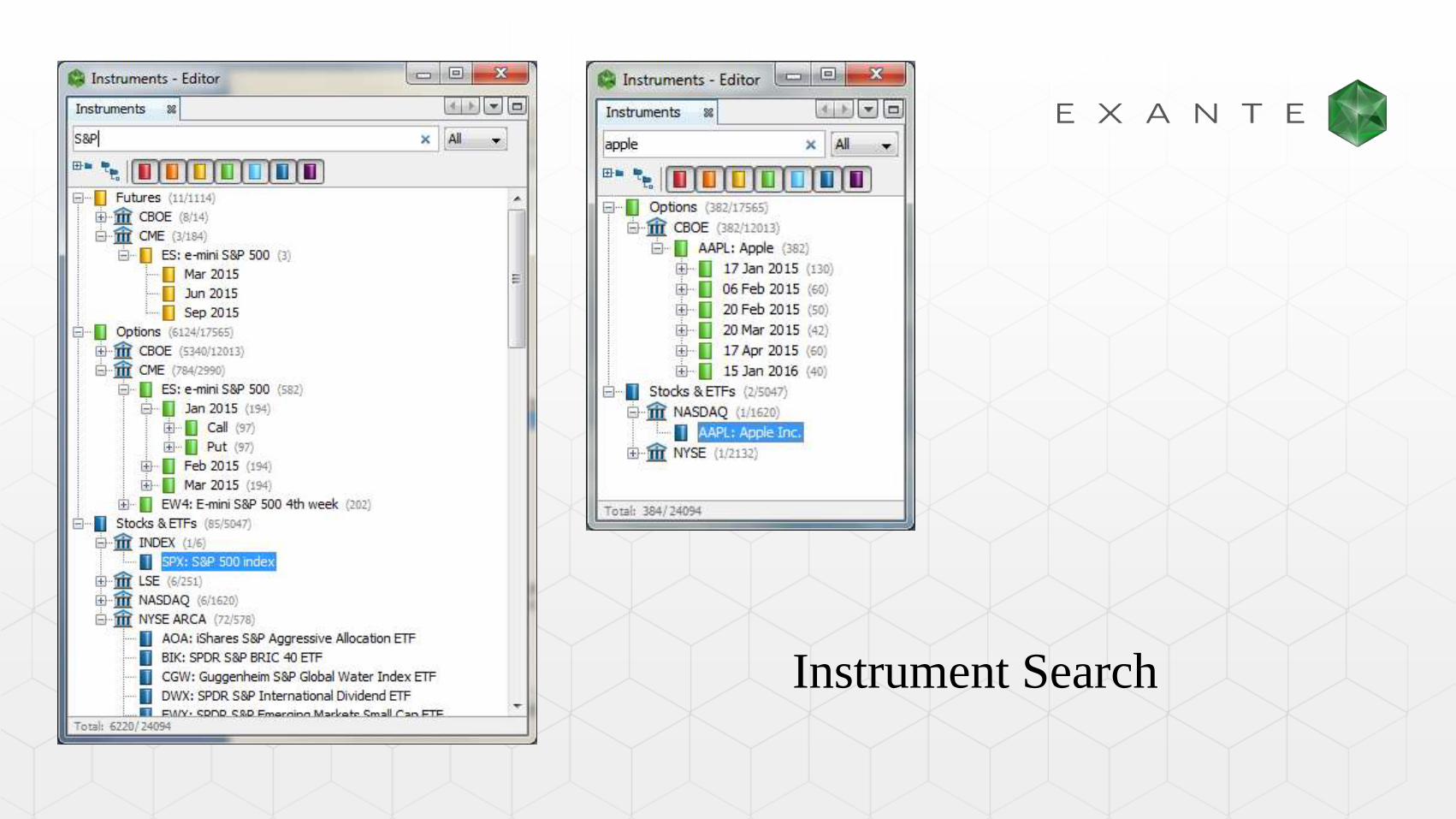

Instrument Search

Market Analysis

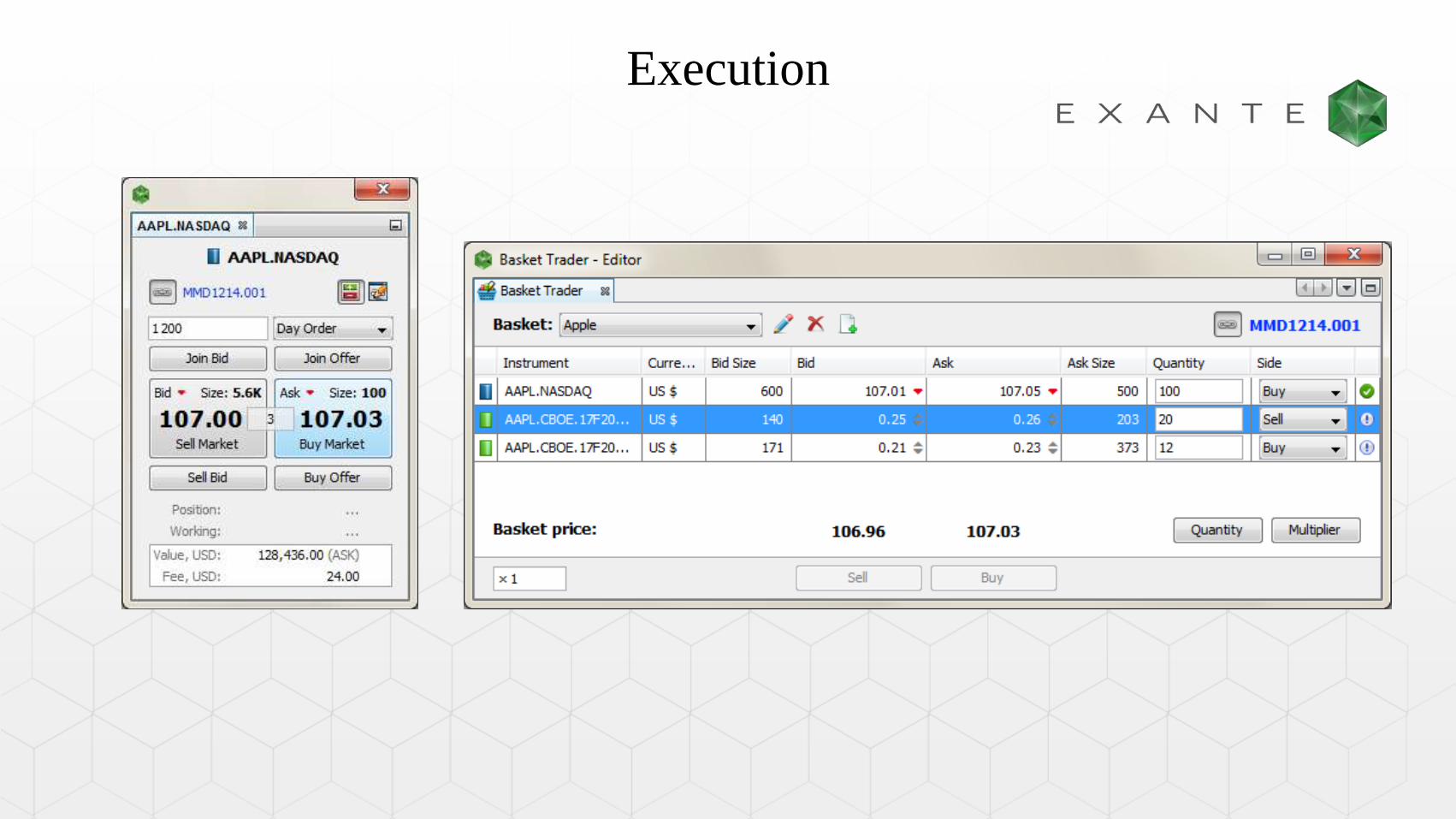

Execution

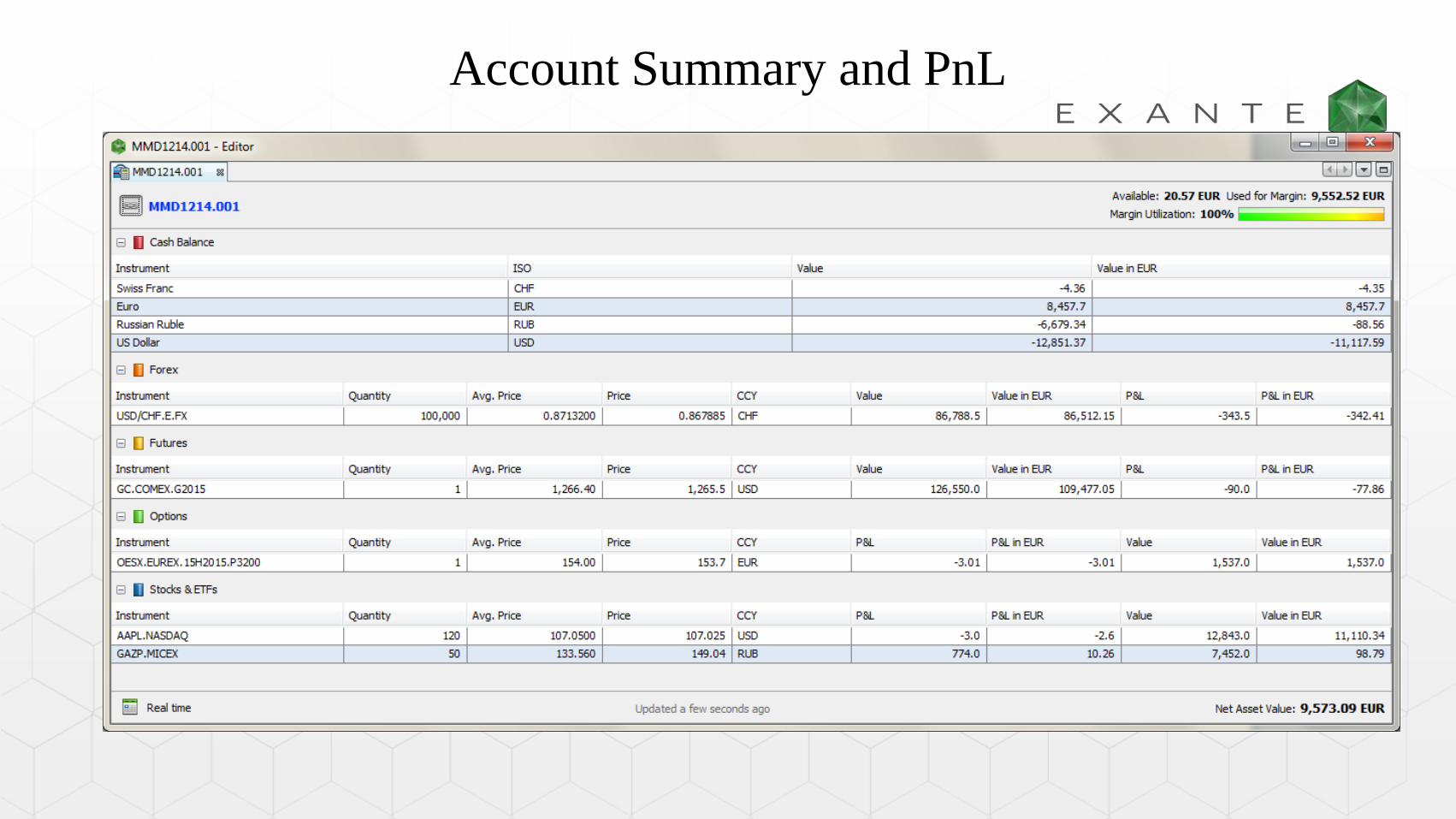

Account Summary and PnL

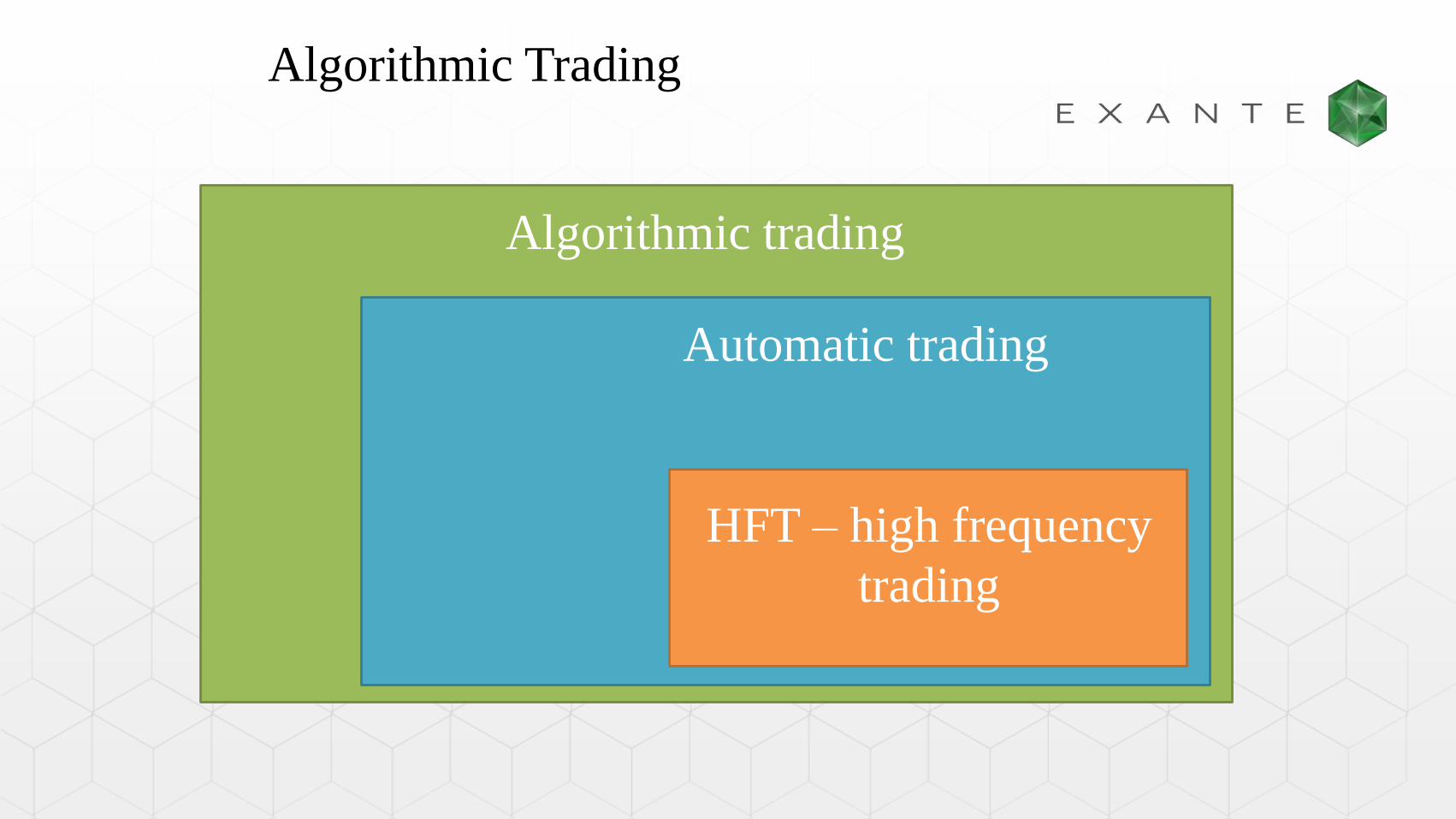

Algorithmic Trading

Algorithmic trading

Automatic trading

HFT – high frequency

trading

Algorithmic Trading

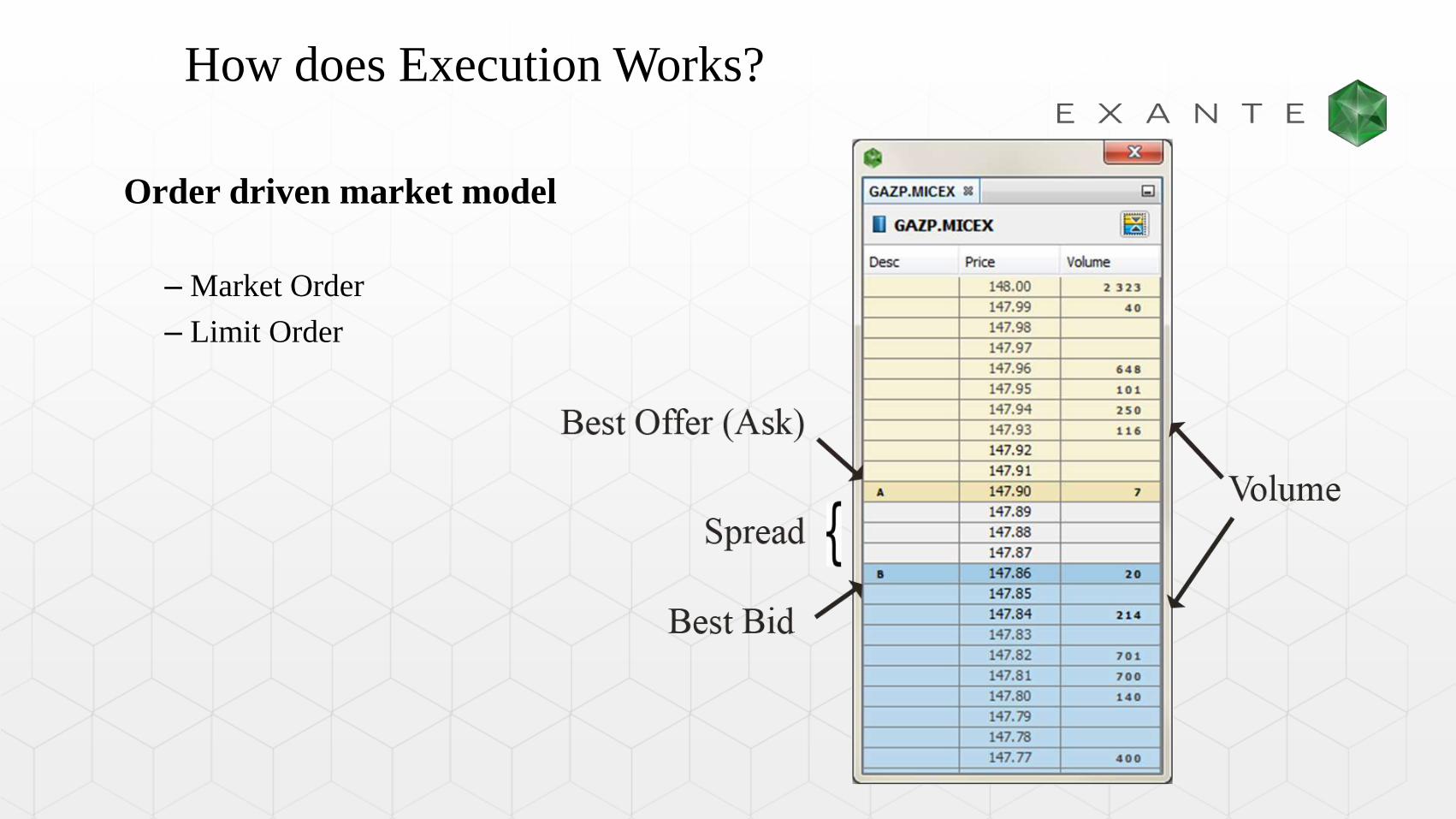

How does Execution Works?

Order driven market model

– Market Order

– Limit Order

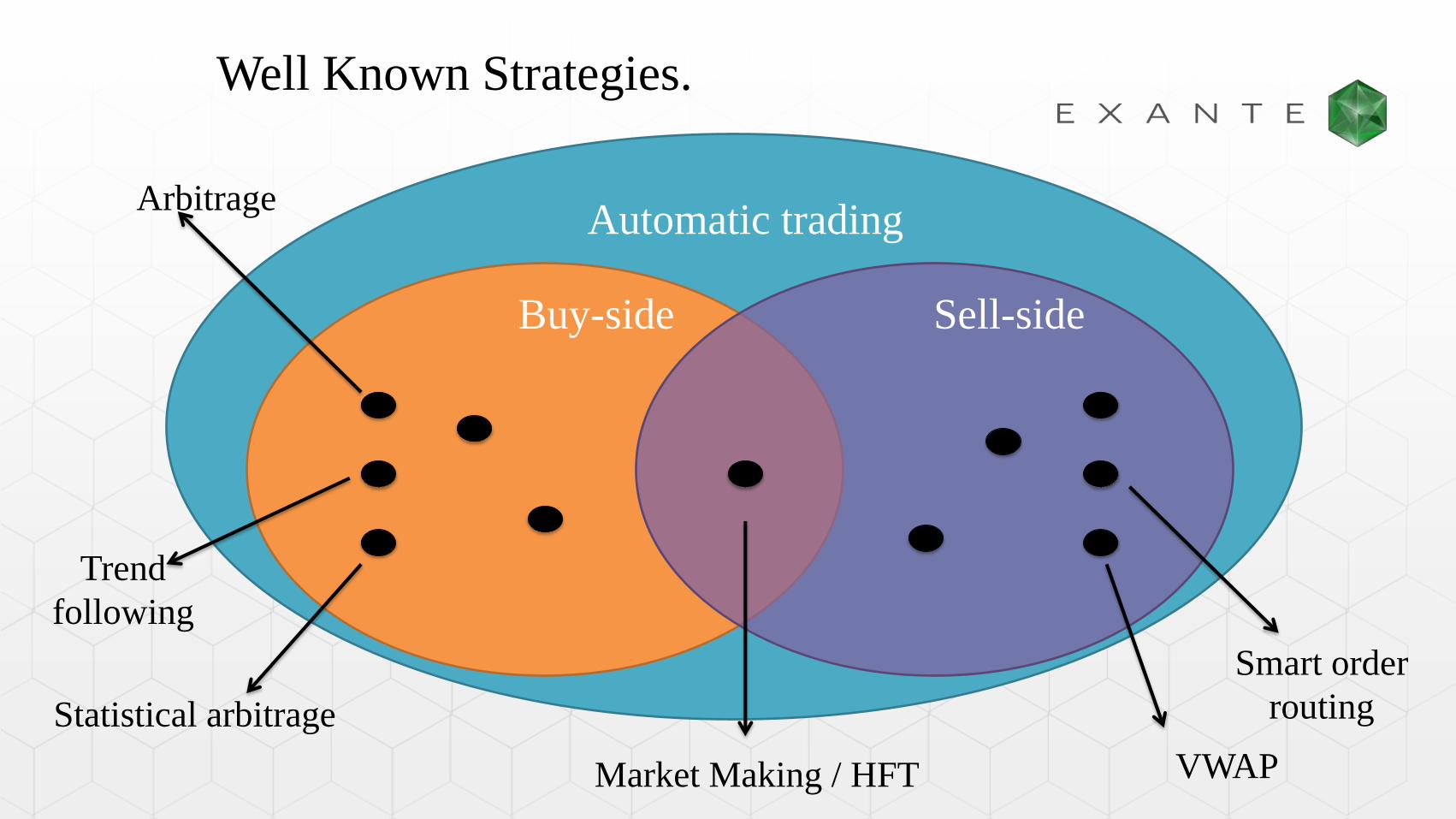

Automatic trading

Buy-side Sell-side

Statistical arbitrage

VWAPMarket Making / HFT

Trend

following

Arbitrage

Smart order

routing

Well Known Strategies.

Automatic trading

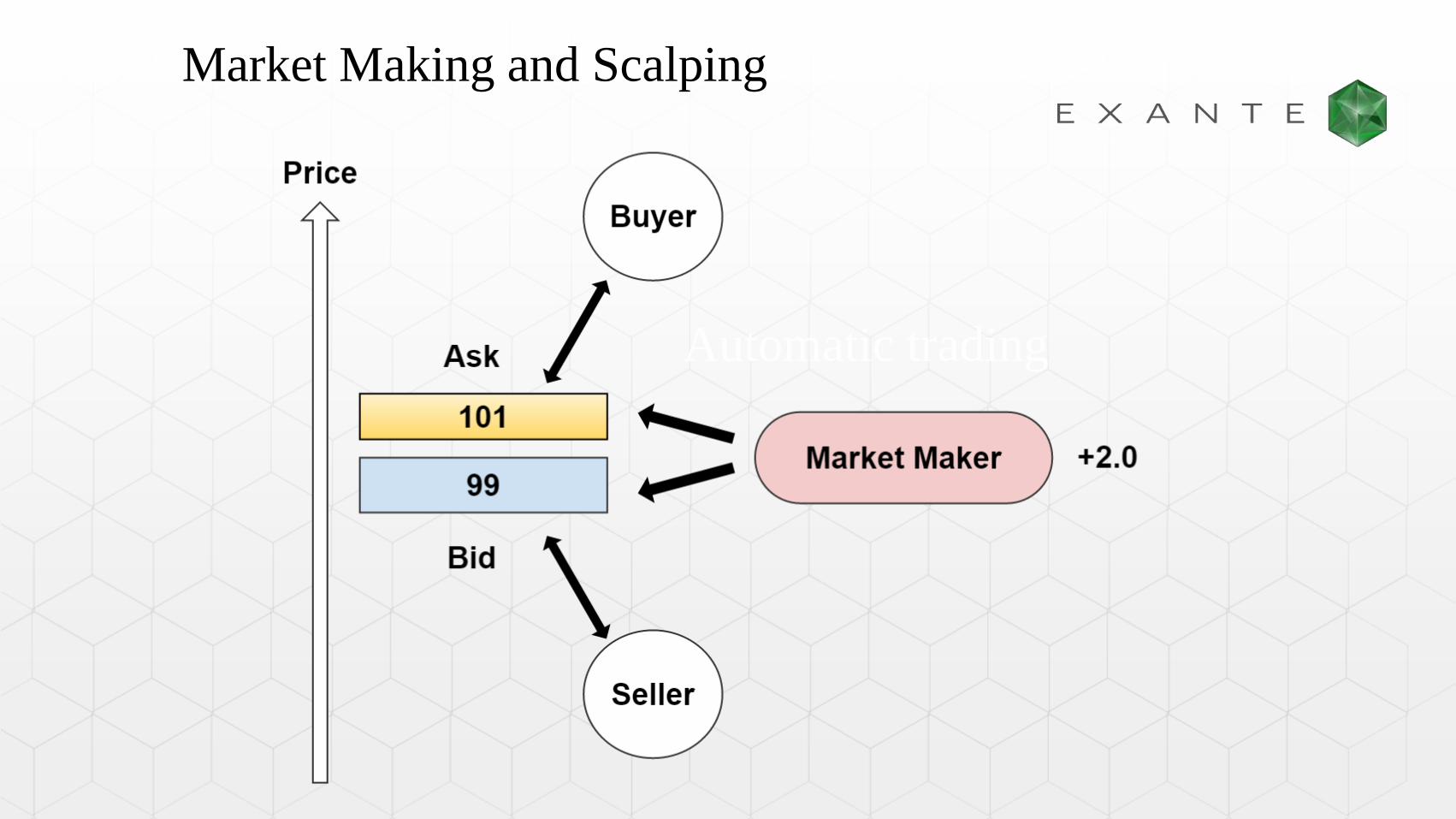

Market Making and Scalping

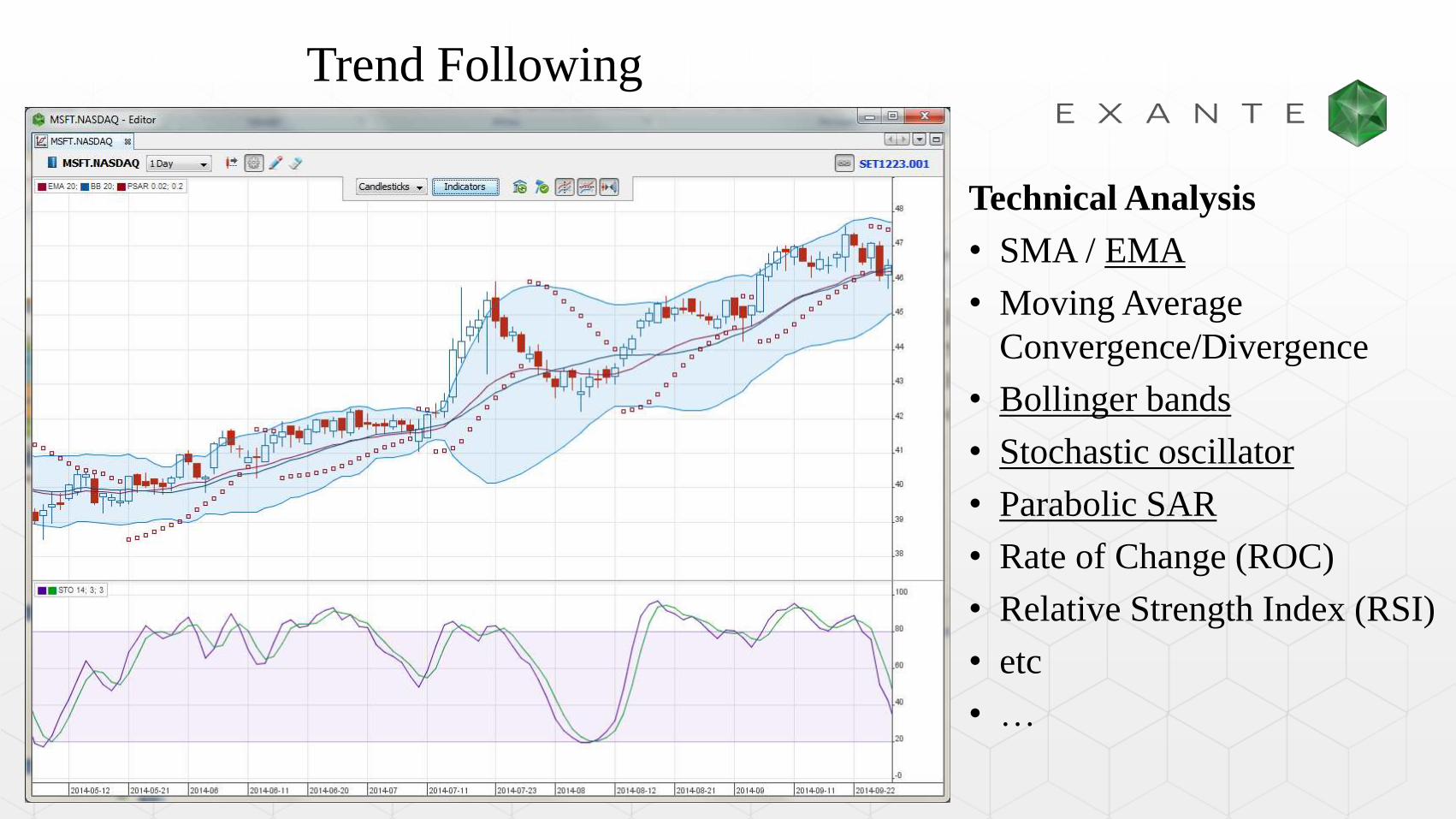

Trend Following

Technical Analysis

• SMA / EMA

• Moving Average

Convergence/Divergence

• Bollinger bands

• Stochastic oscillator

• Parabolic SAR

• Rate of Change (ROC)

• Relative Strength Index (RSI)

• etc

• …

Mean Reversion

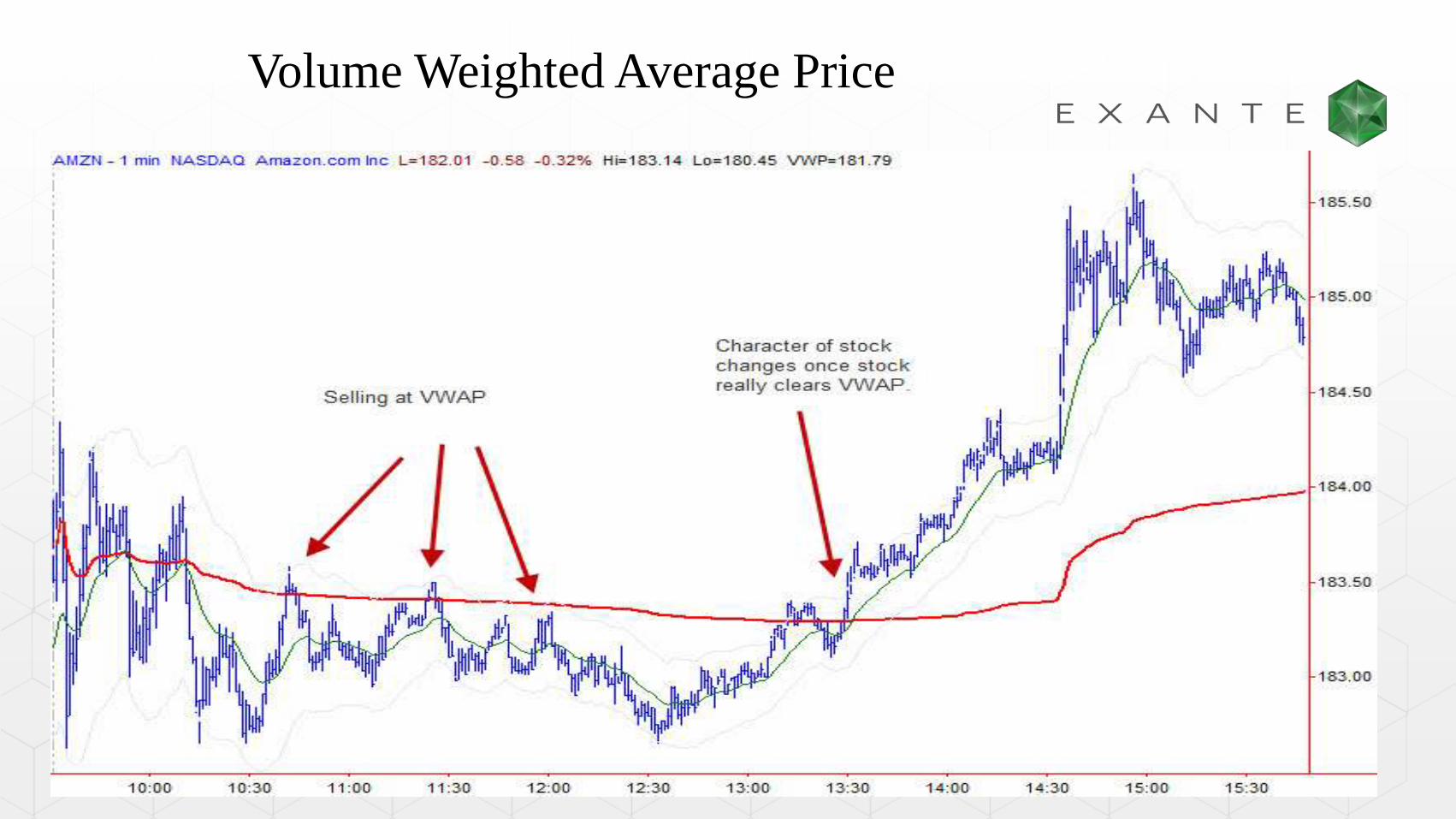

Volume Weighted Average Price

Volatility and Option Trading

Implied volatility prediction

1. Delta neutral portfolio

– Buy option / sell stock on volatility going up

– Sell Option / buy stock on volatility going down

2. Various options strategies

– Straddle

– Strangle

– Butterfly

– Etc.

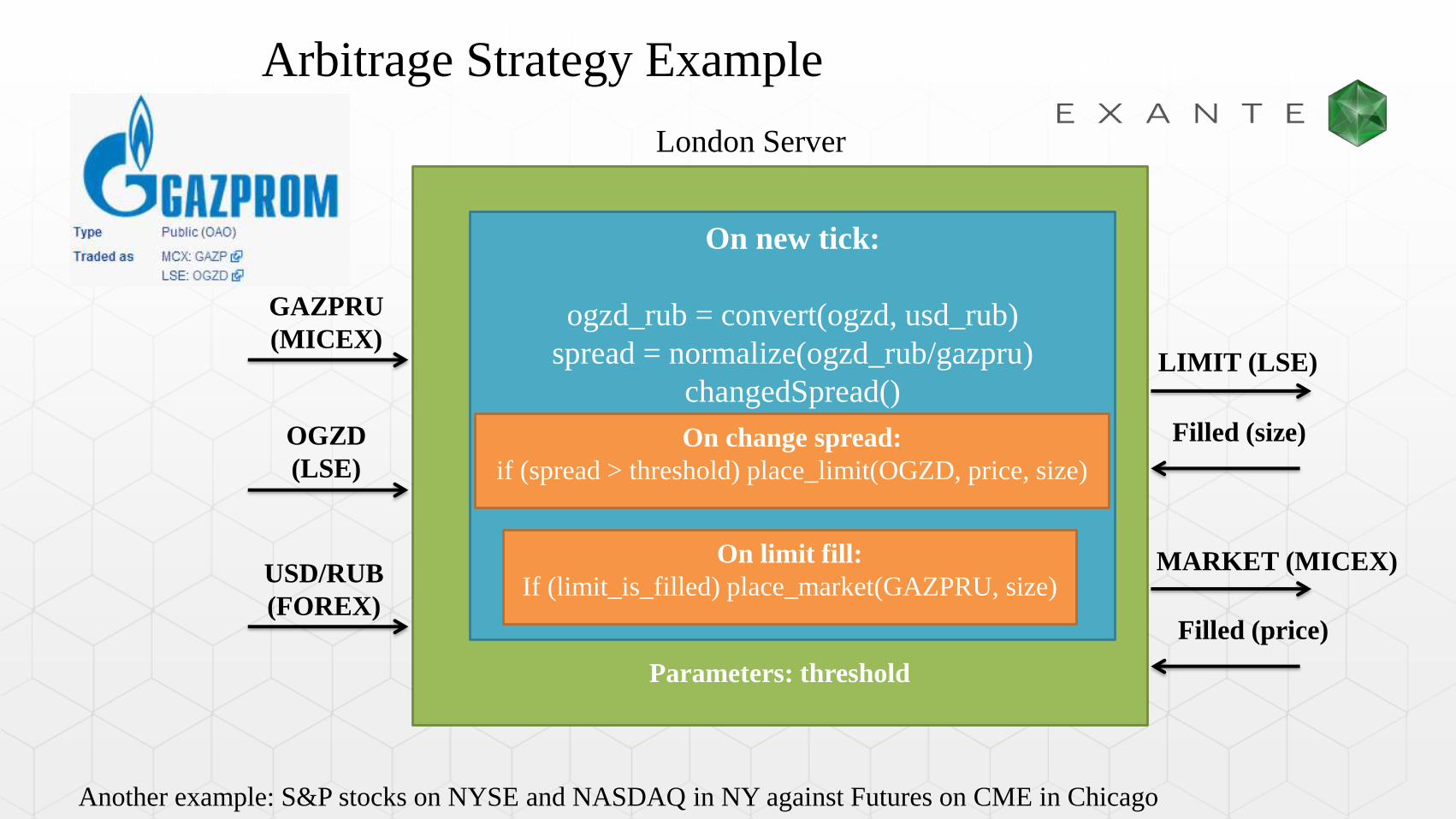

Arbitrage Strategy Example

GAZPRU

(MICEX)

On new tick:

ogzd_rub = convert(ogzd, usd_rub)

spread = normalize(ogzd_rub/gazpru)

changedSpread()

OGZD

(LSE)

USD/RUB

(FOREX)

LIMIT (LSE)

London Server

Filled (size)

MARKET (MICEX)

Filled (price)

On change spread:

if (spread > threshold) place_limit(OGZD, price, size)

On limit fill:

If (limit_is_filled) place_market(GAZPRU, size)

Parameters: threshold

Another example: S&P stocks on NYSE and NASDAQ in NY against Futures on CME in Chicago

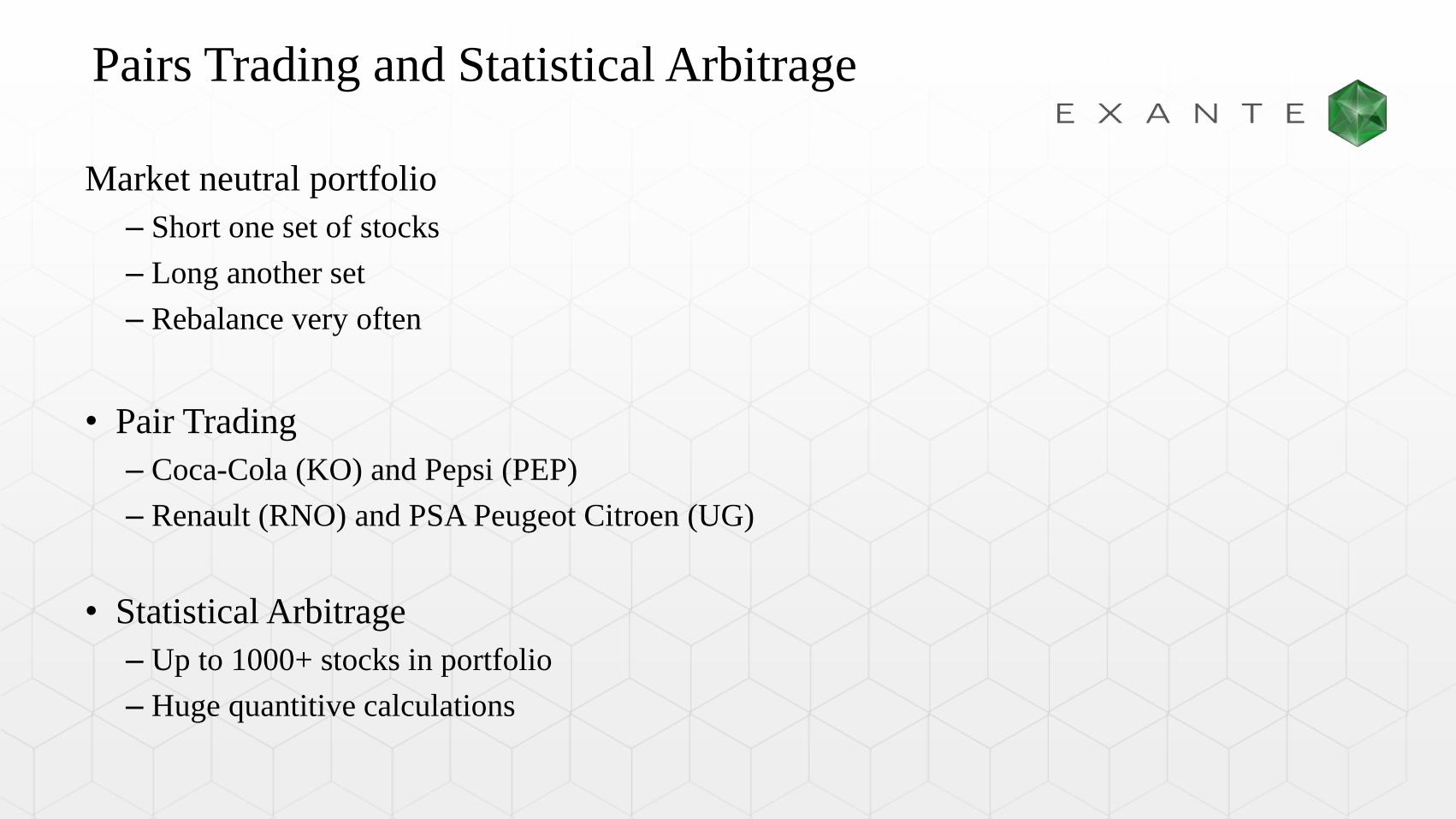

Pairs Trading and Statistical Arbitrage

Market neutral portfolio

– Short one set of stocks

– Long another set

– Rebalance very often

• Pair Trading

– Coca-Cola (KO) and Pepsi (PEP)

– Renault (RNO) and PSA Peugeot Citroen (UG)

• Statistical Arbitrage

– Up to 1000+ stocks in portfolio

– Huge quantitive calculations

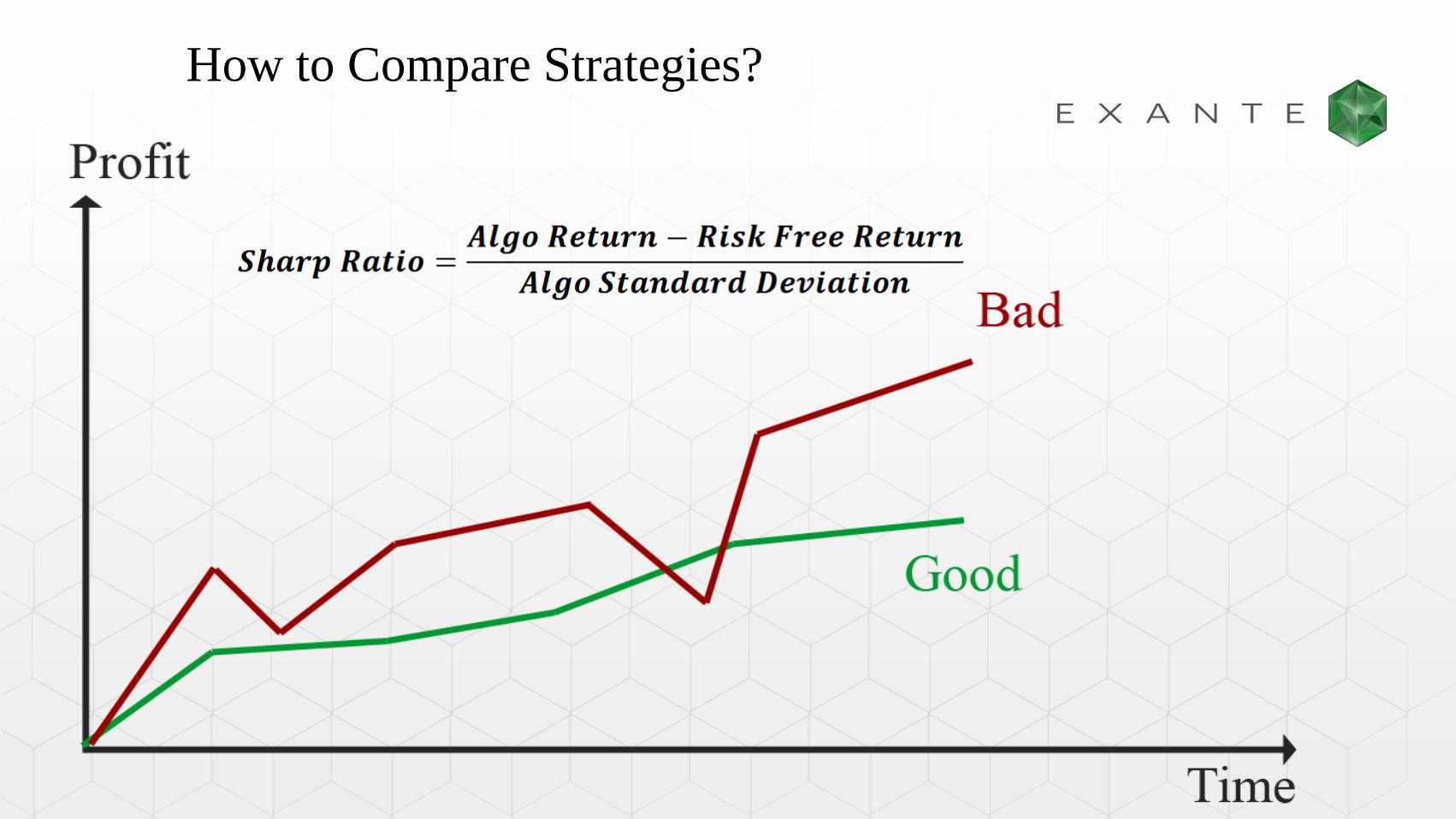

How to Compare Strategies?

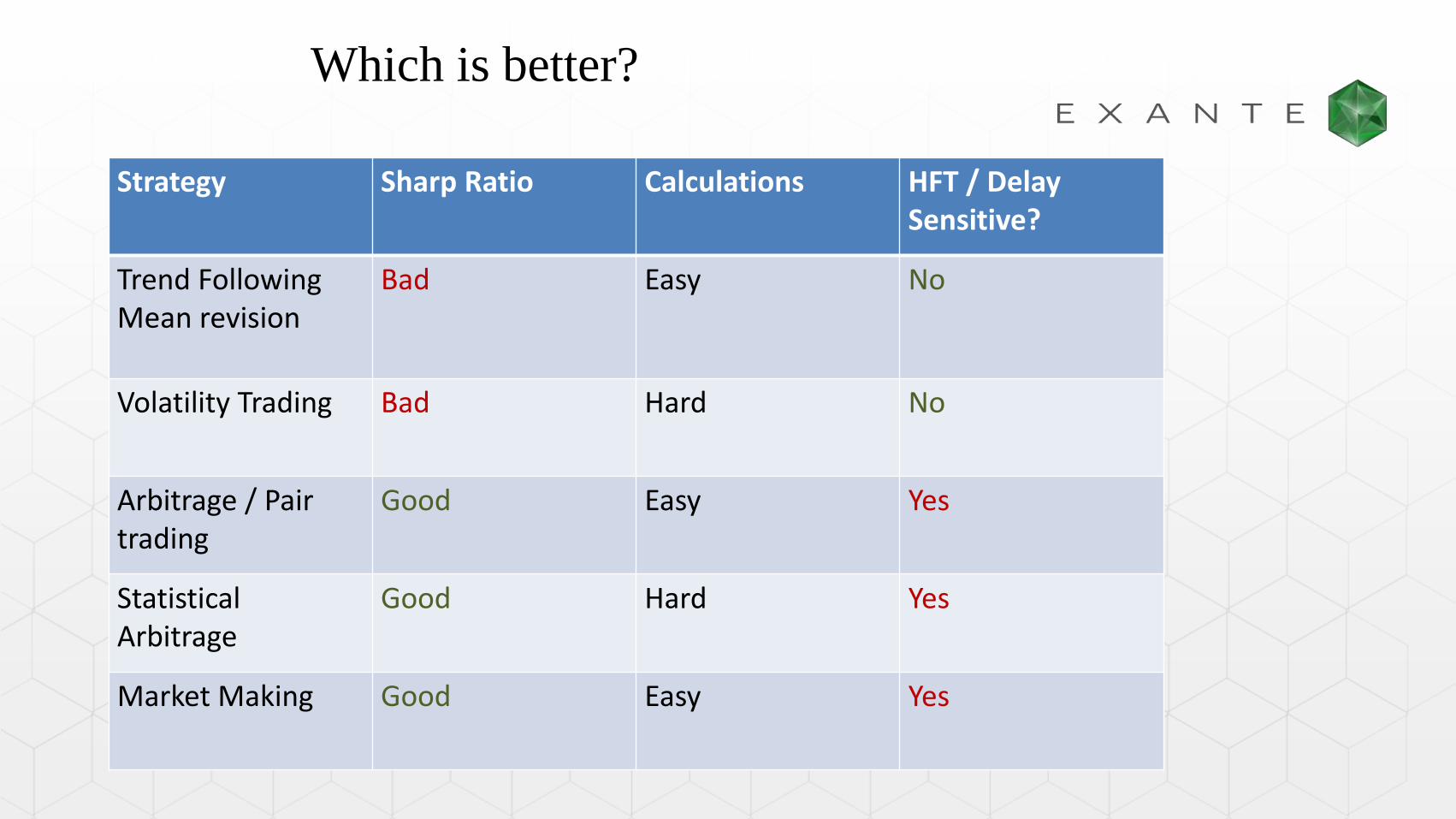

Which is better?

Strategy Sharp Ratio Calculations HFT / Delay Sensitive?

Trend FollowingMean revision

Bad Easy No

Volatility Trading Bad Hard No

Arbitrage / Pairtrading

Good Easy Yes

Statistical Arbitrage

Good Hard Yes

Market Making Good Easy Yes

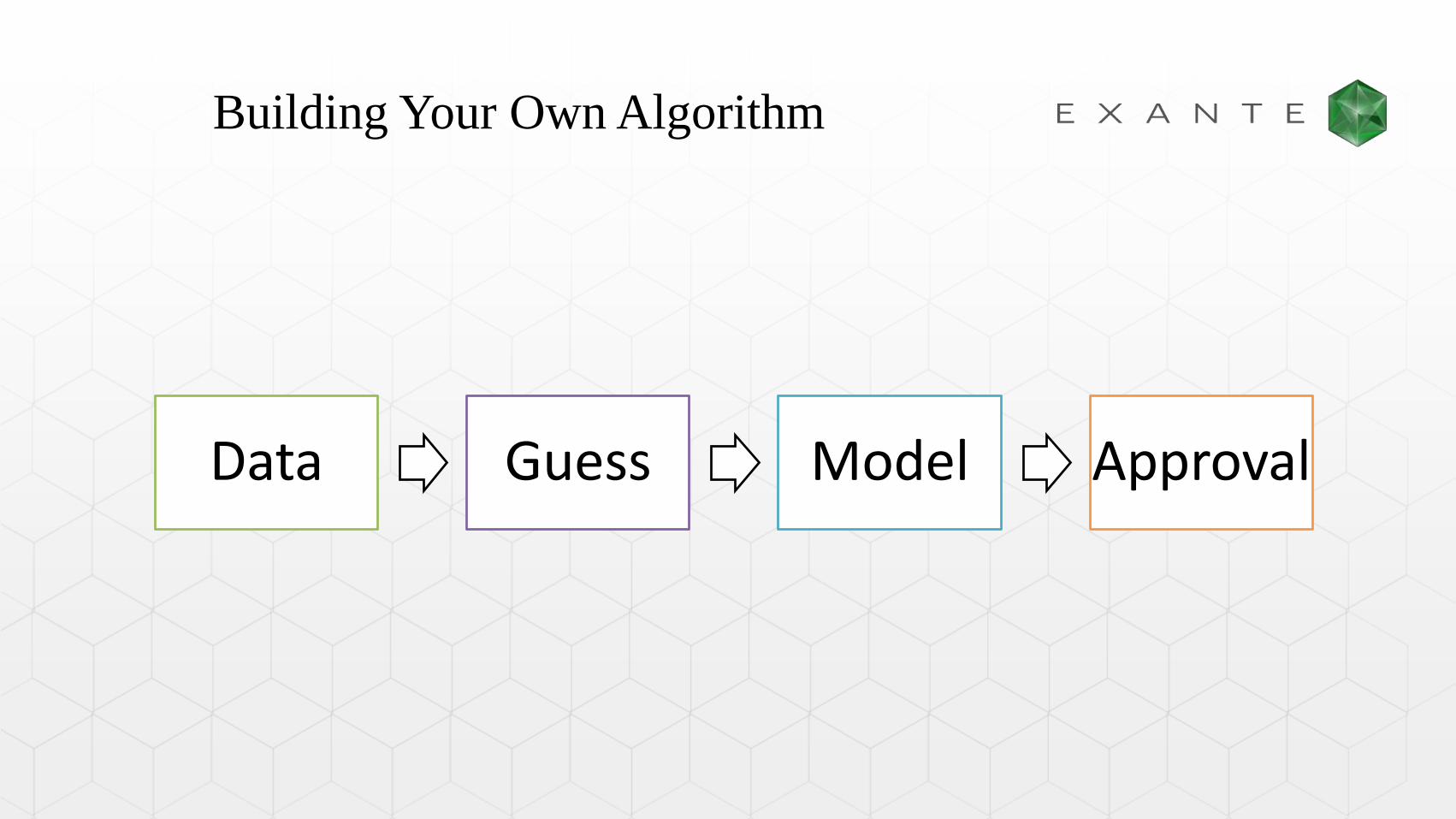

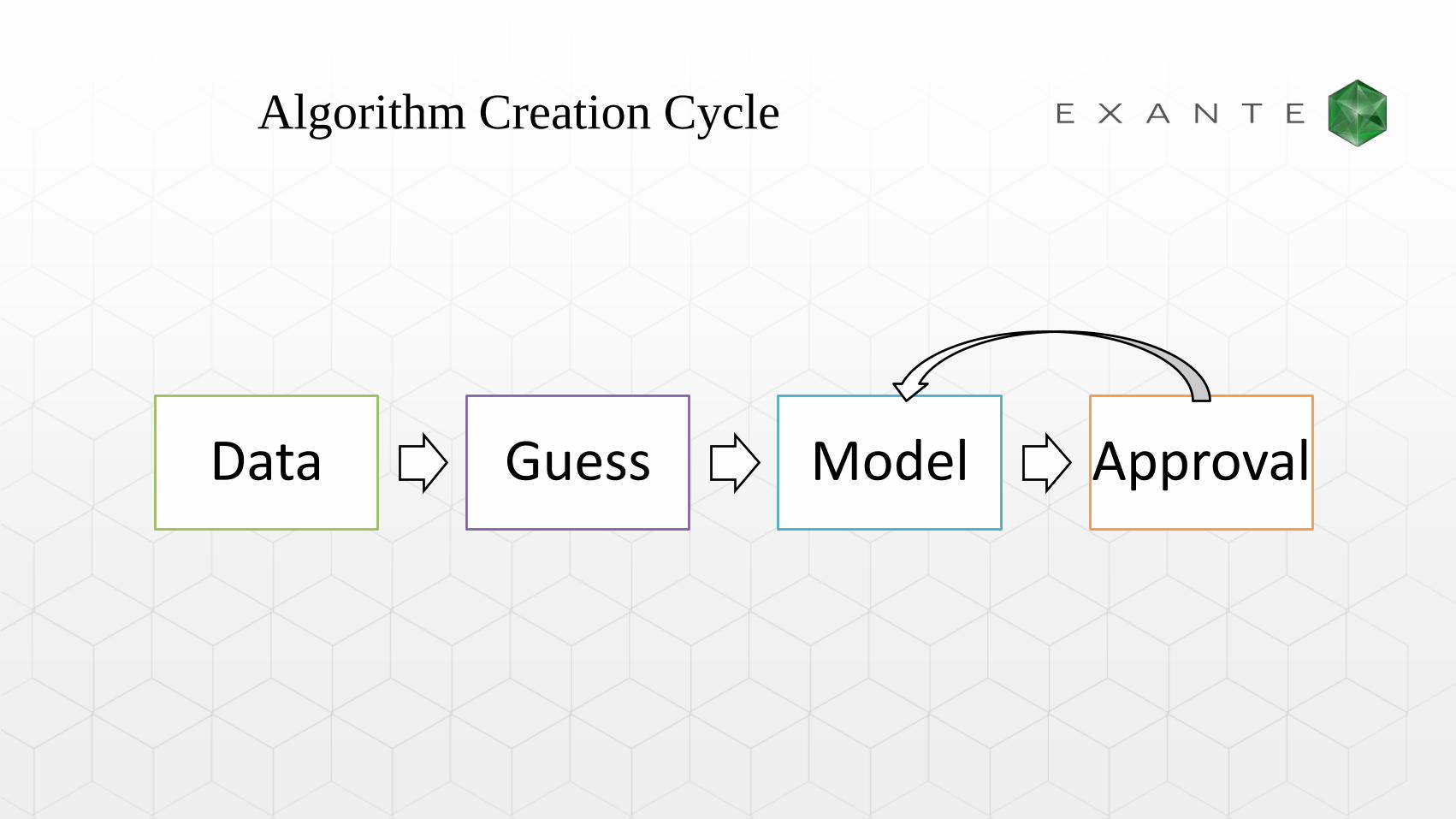

Data Guess Model Approval

Building Your Own Algorithm

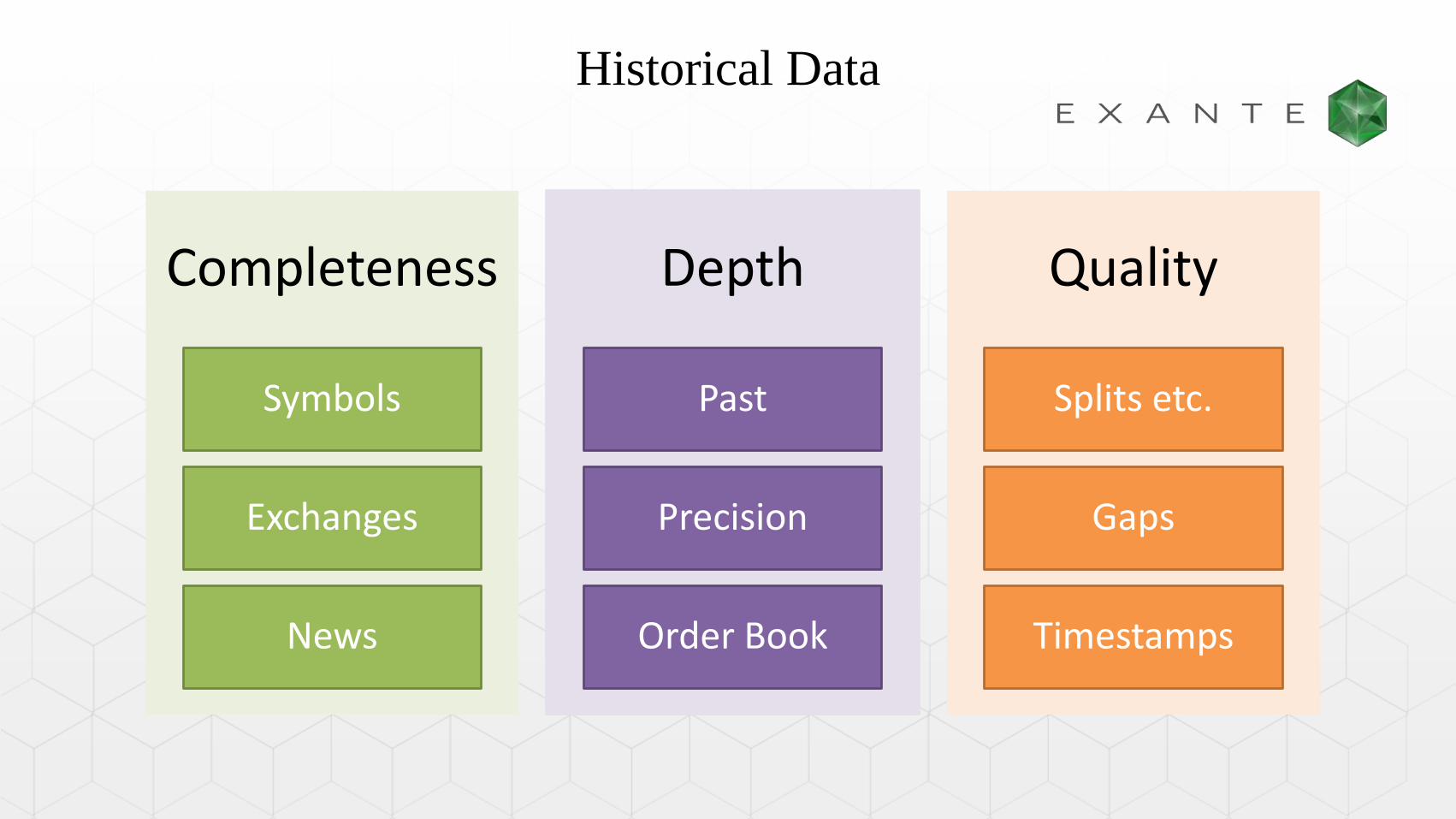

Historical Data

Completeness

Symbols

Exchanges

News

Depth

Past

Precision

Order Book

Quality

Splits etc.

Gaps

Timestamps

Data Rendering

Huge

Volume

Processing

Speed

Technical

analysis

Иллюстрация с panopticon.com

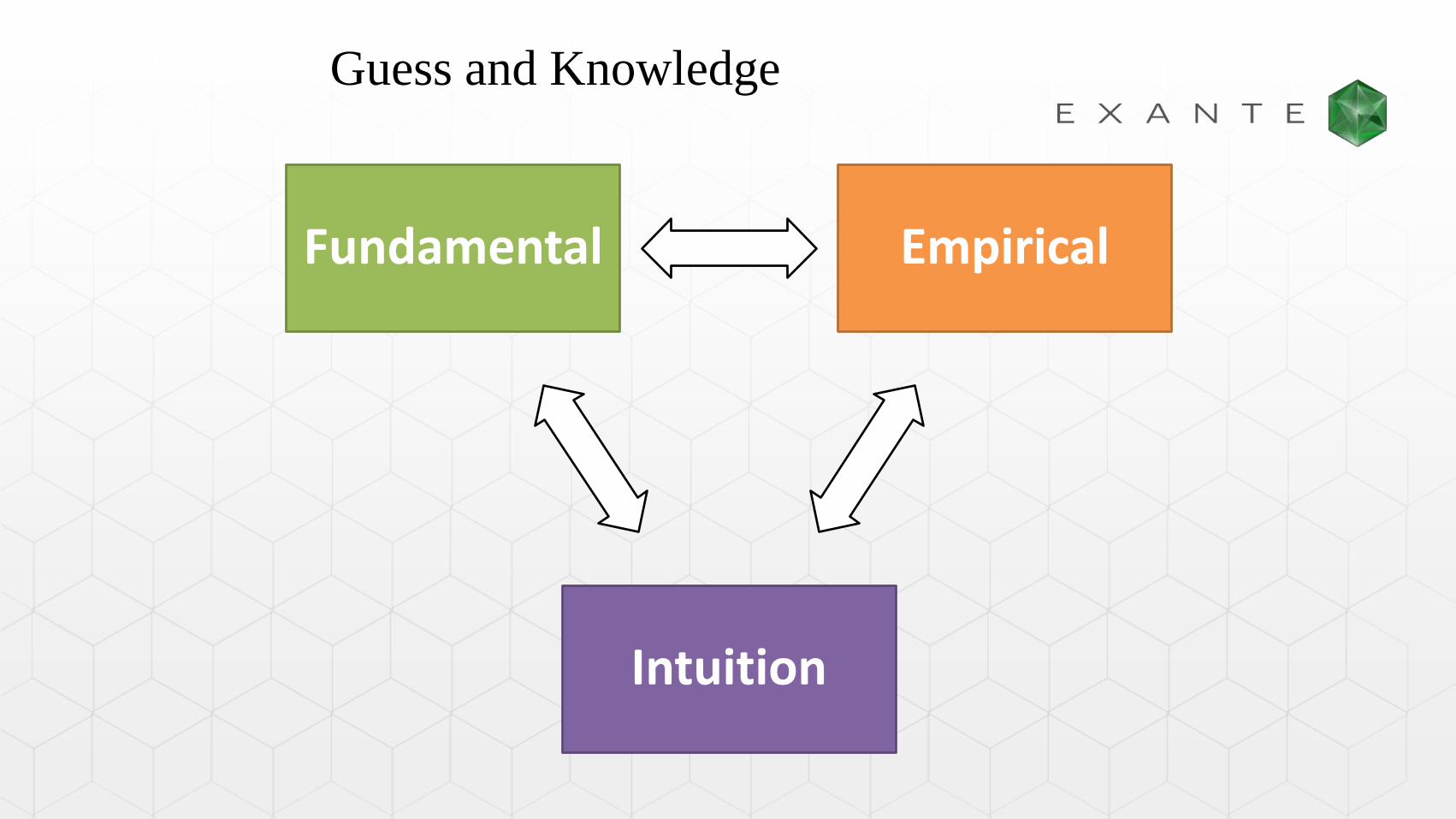

Guess and Knowledge

Intuition

EmpiricalFundamental

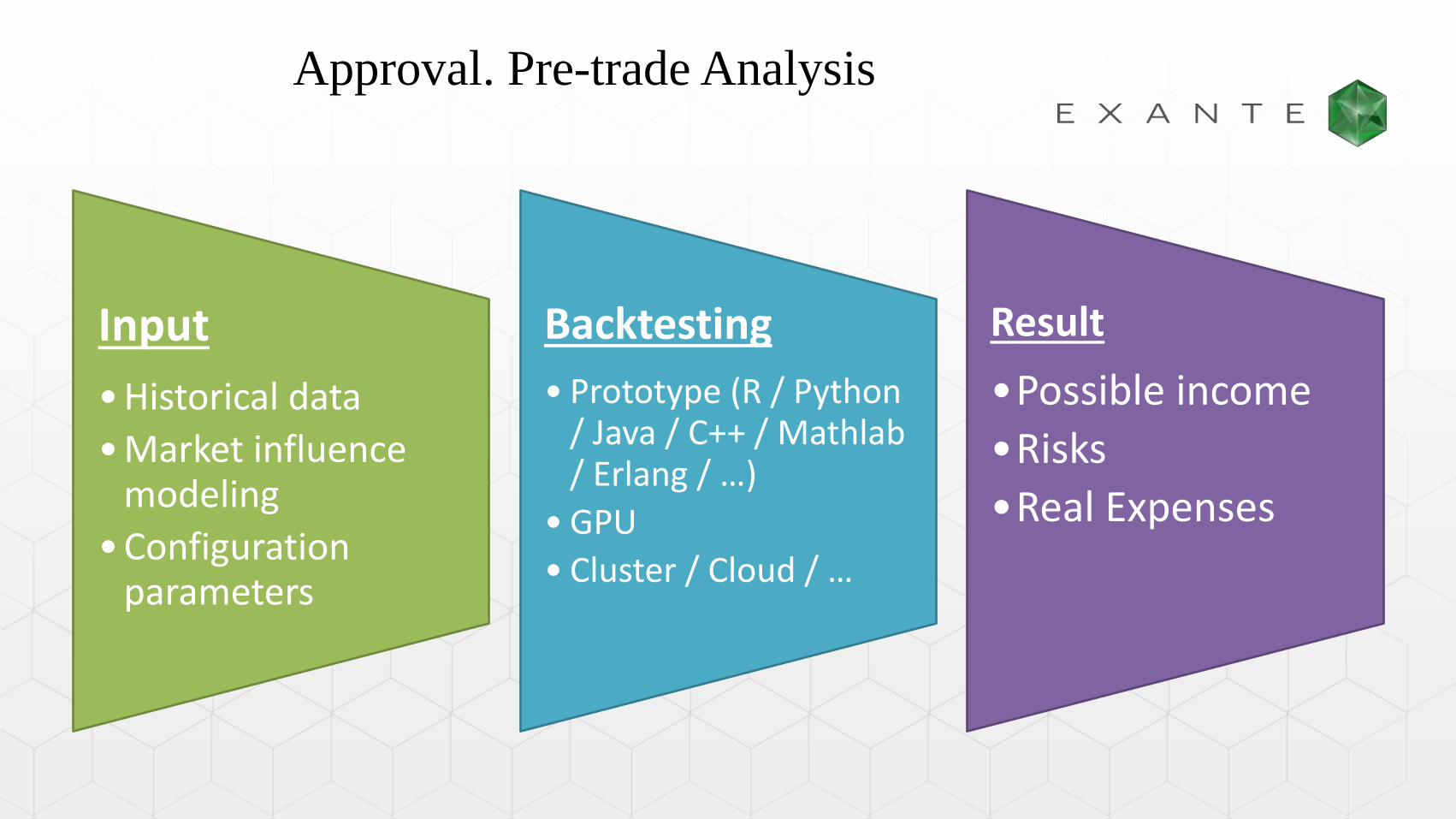

Approval. Pre-trade Analysis

Input

• Historical data

• Market influence modeling

• Configuration parameters

Backtesting

• Prototype (R / Python / Java / C++ / Mathlab/ Erlang / …)

• GPU

• Cluster / Cloud / …

Result

•Possible income

•Risks

•Real Expenses

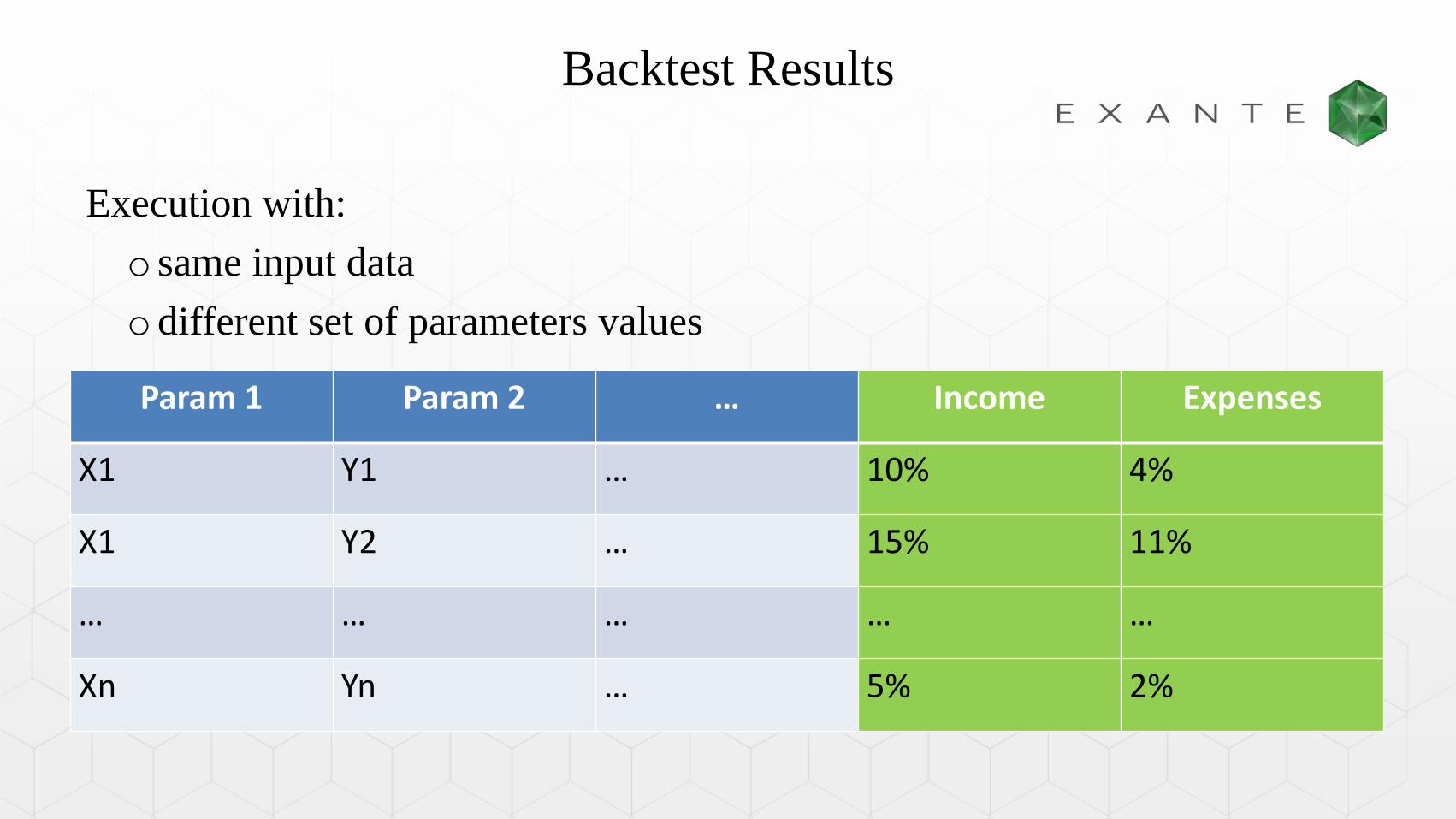

Backtest Results

Param 1 Param 2 … Income Expenses

X1 Y1 … 10% 4%

X1 Y2 … 15% 11%

… … … … …

Xn Yn … 5% 2%

Execution with:

o same input data

odifferent set of parameters values

Data Guess Model Approval

Algorithm Creation Cycle

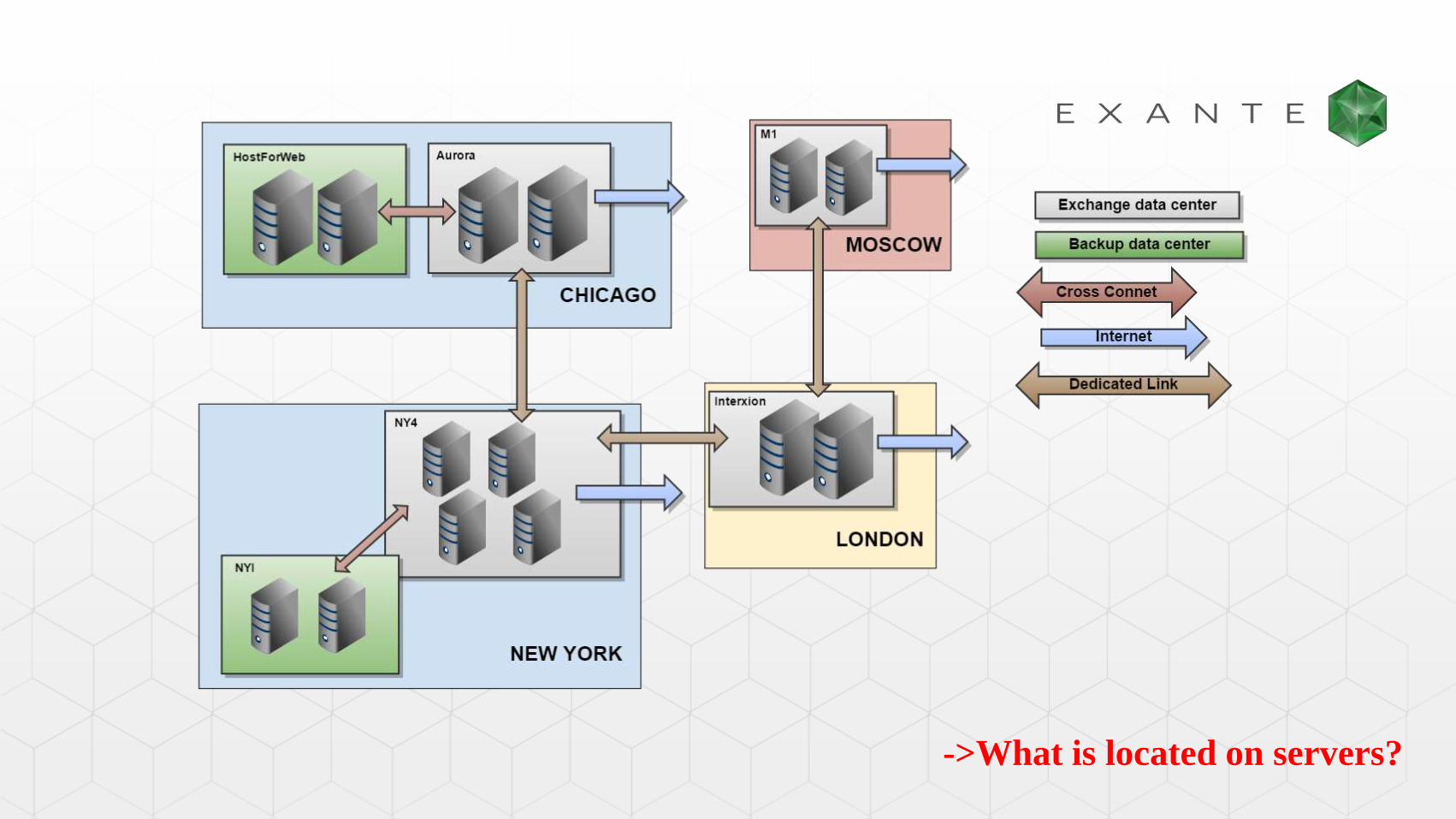

Technical Background

300 +

Servers

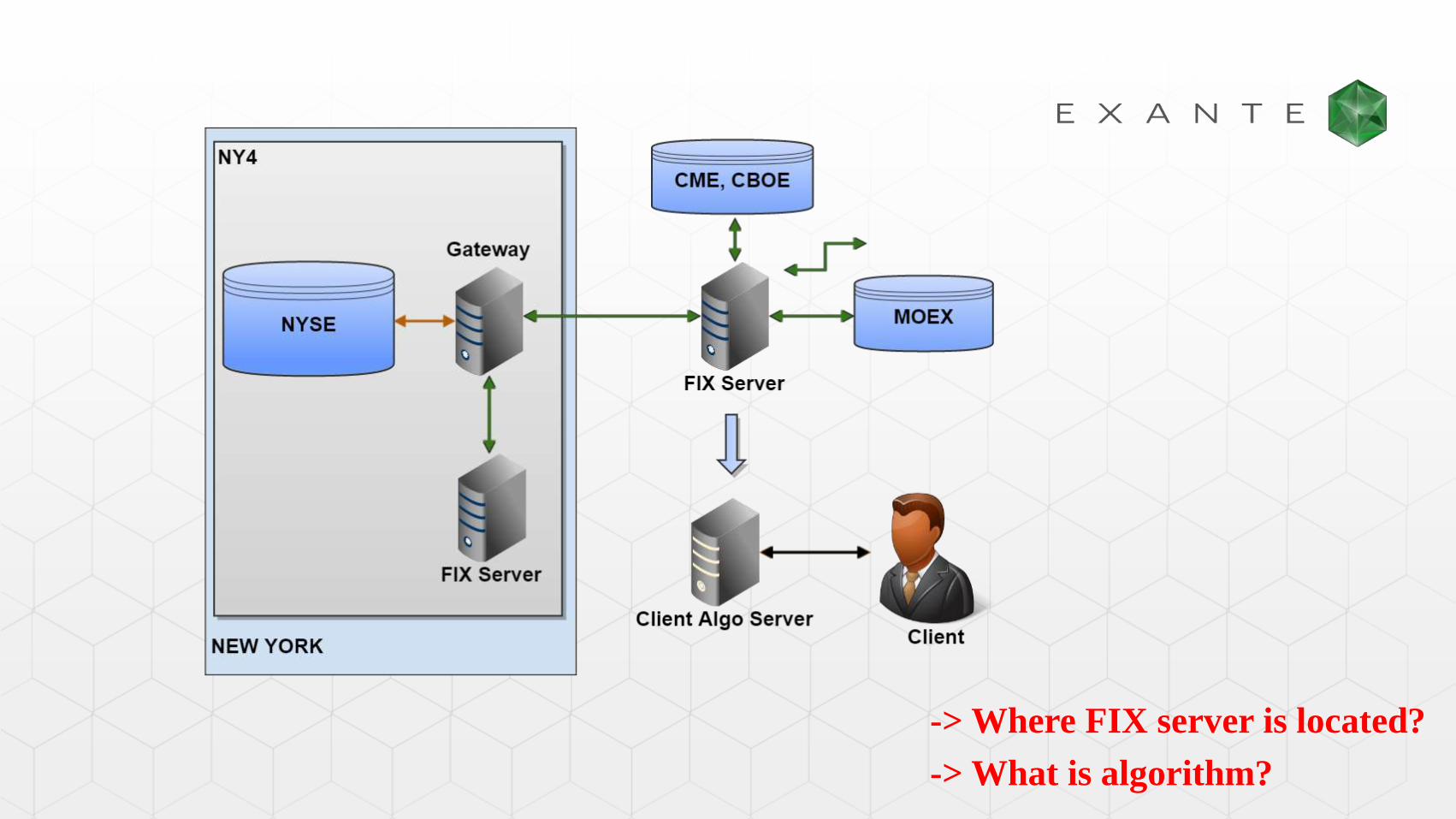

->What is located on servers?

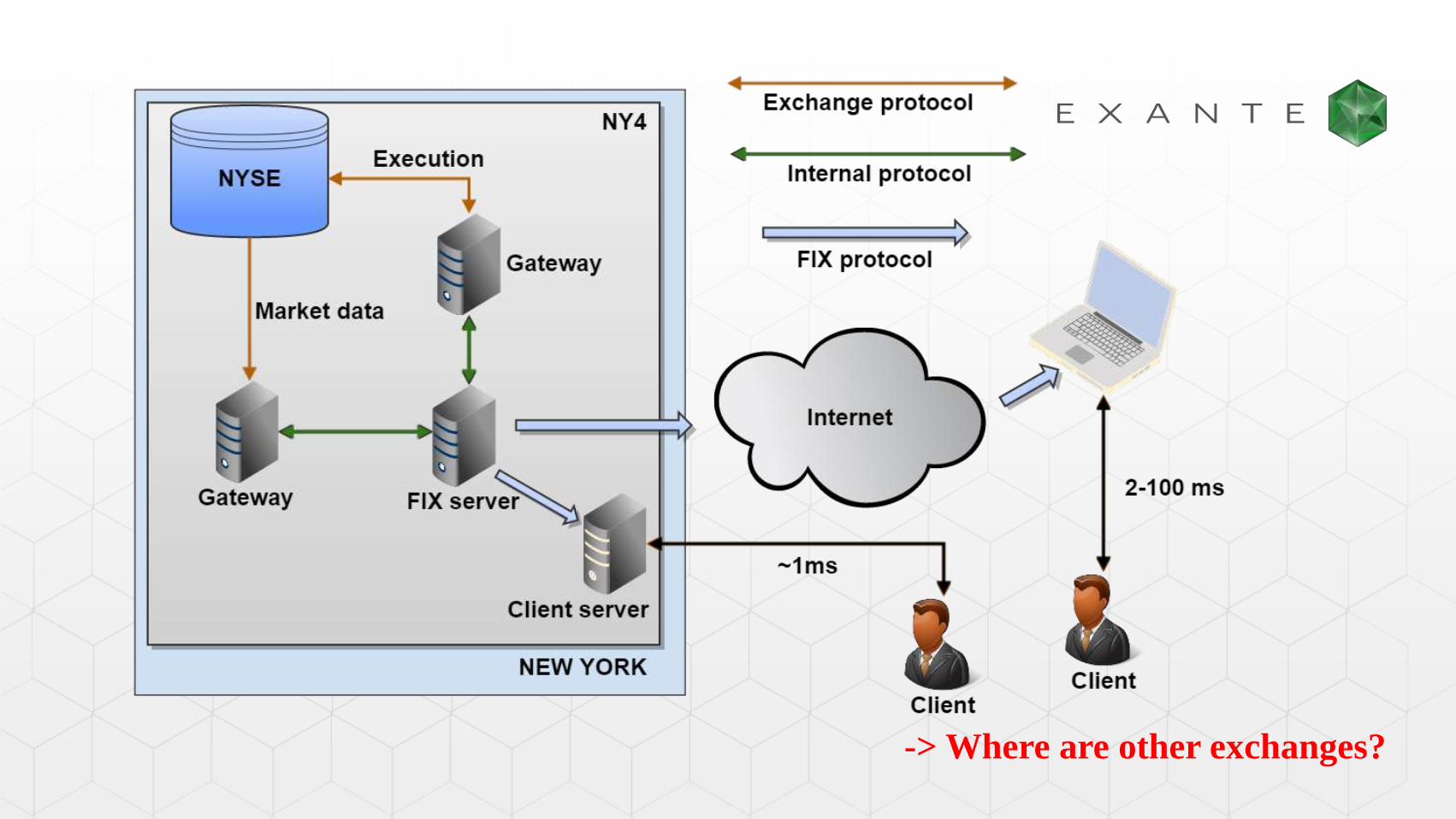

-> Where are other exchanges?

-> Where FIX server is located?

-> What is algorithm?

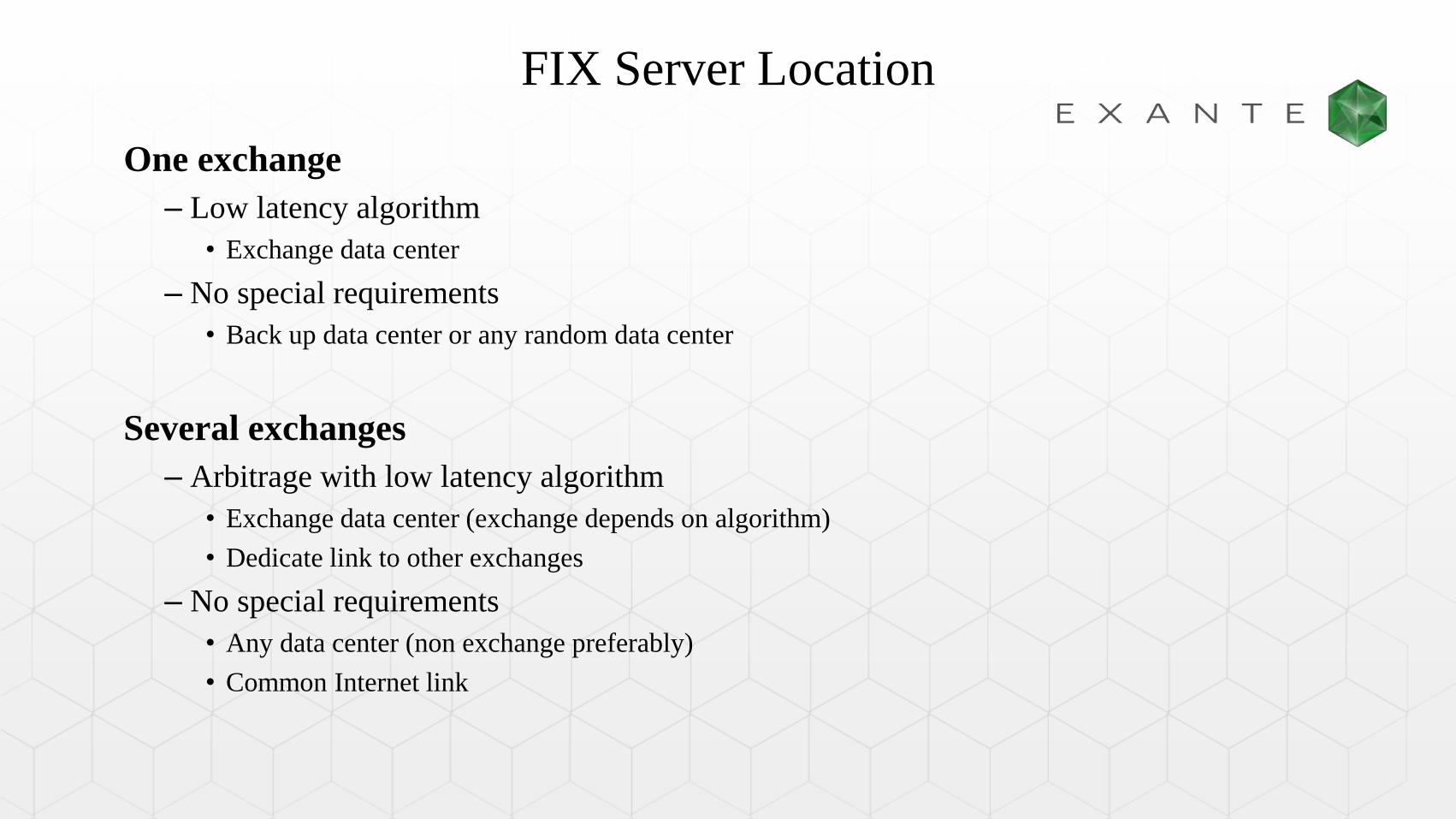

FIX Server Location

One exchange

– Low latency algorithm

• Exchange data center

– No special requirements

• Back up data center or any random data center

Several exchanges

– Arbitrage with low latency algorithm

• Exchange data center (exchange depends on algorithm)

• Dedicate link to other exchanges

– No special requirements

• Any data center (non exchange preferably)

• Common Internet link

Creating an Algorithm

• Any programming language

• 3rd party software

• Run algorithm on your server or in

broker’s VM

• Control through the trading terminal

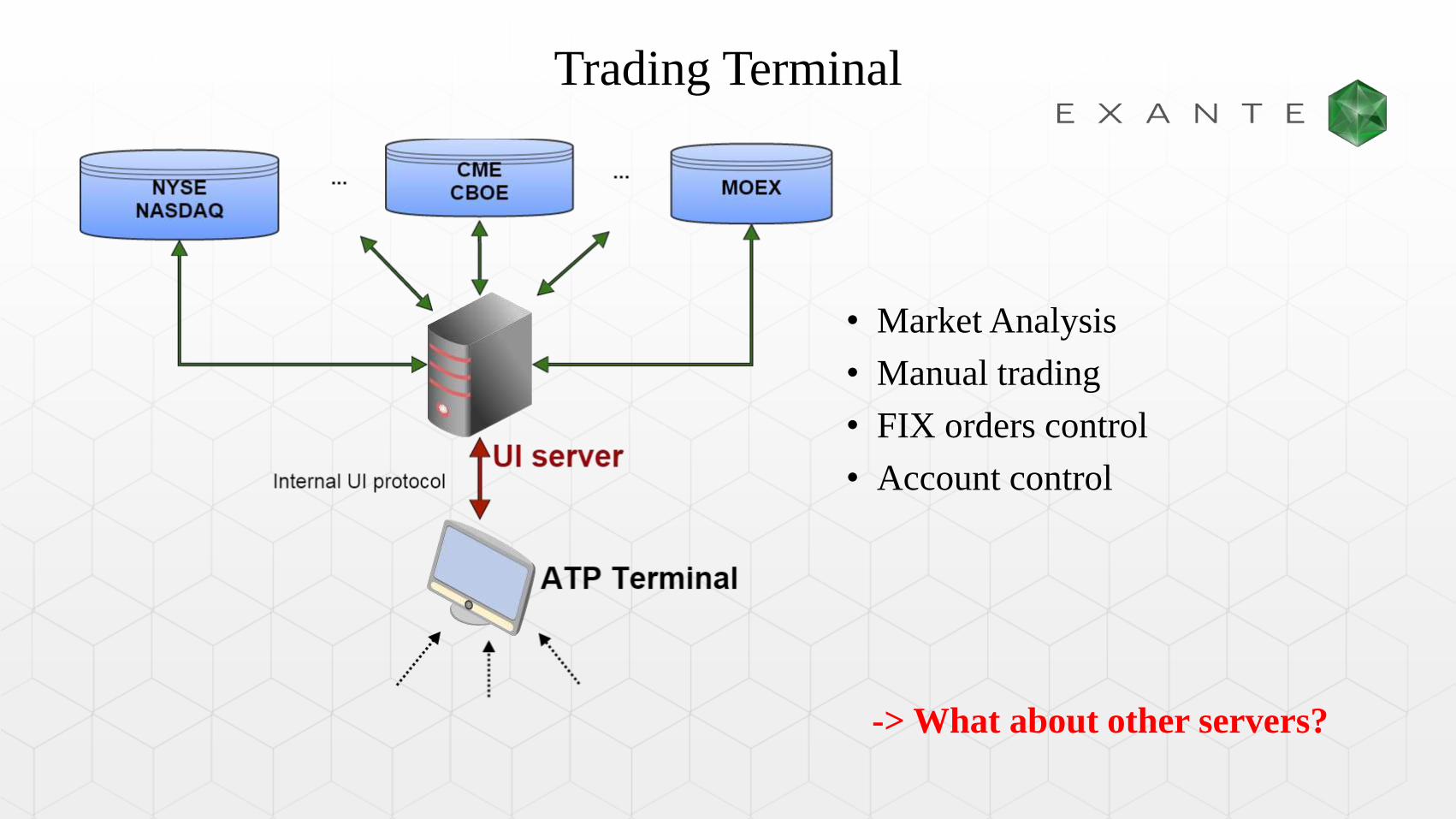

Trading Terminal

• Market Analysis

• Manual trading

• FIX orders control

• Account control

-> What about other servers?

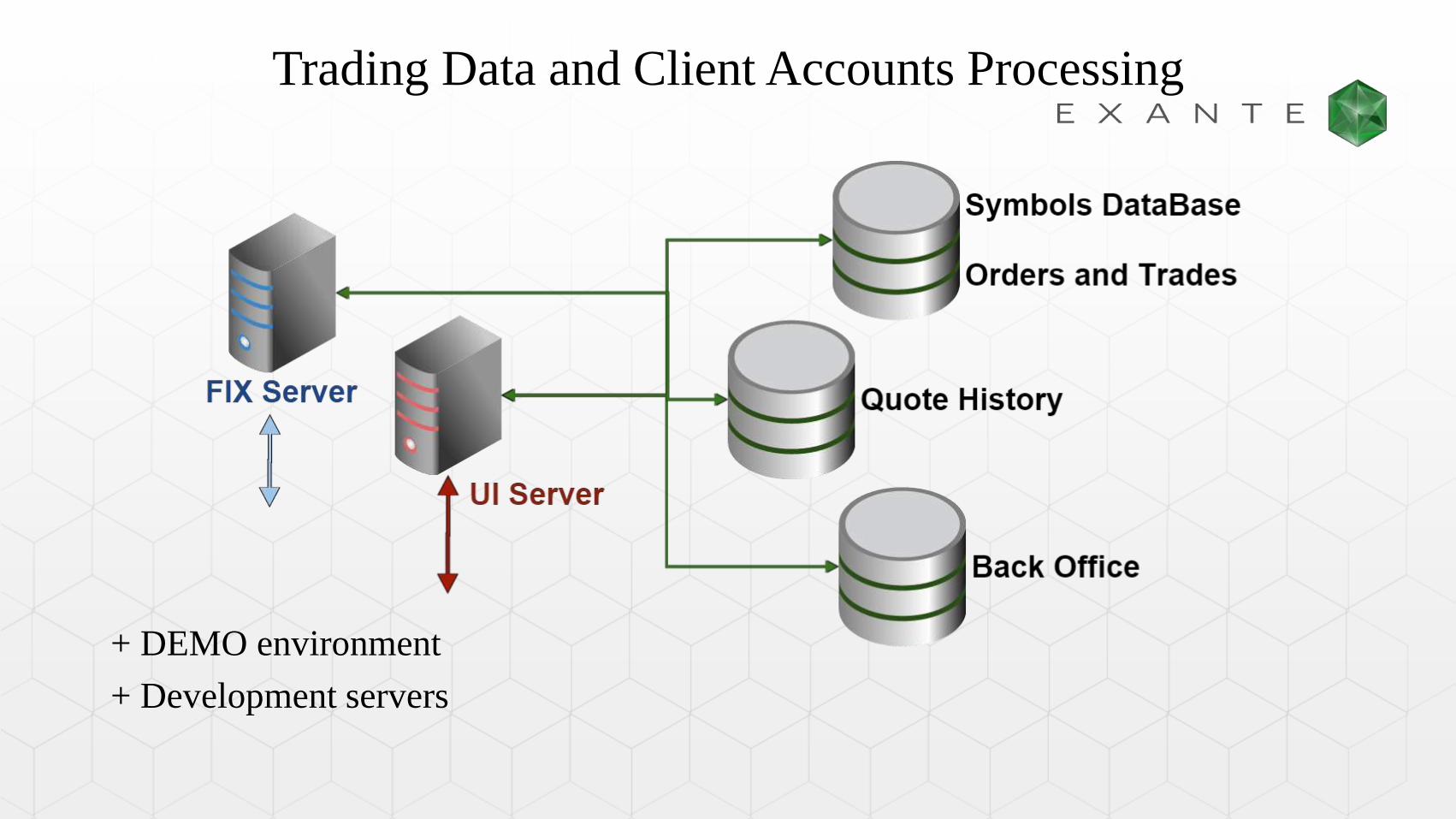

Trading Data and Client Accounts Processing

+ DEMO environment

+ Development servers

Have a Strategy?

Ready For Production?

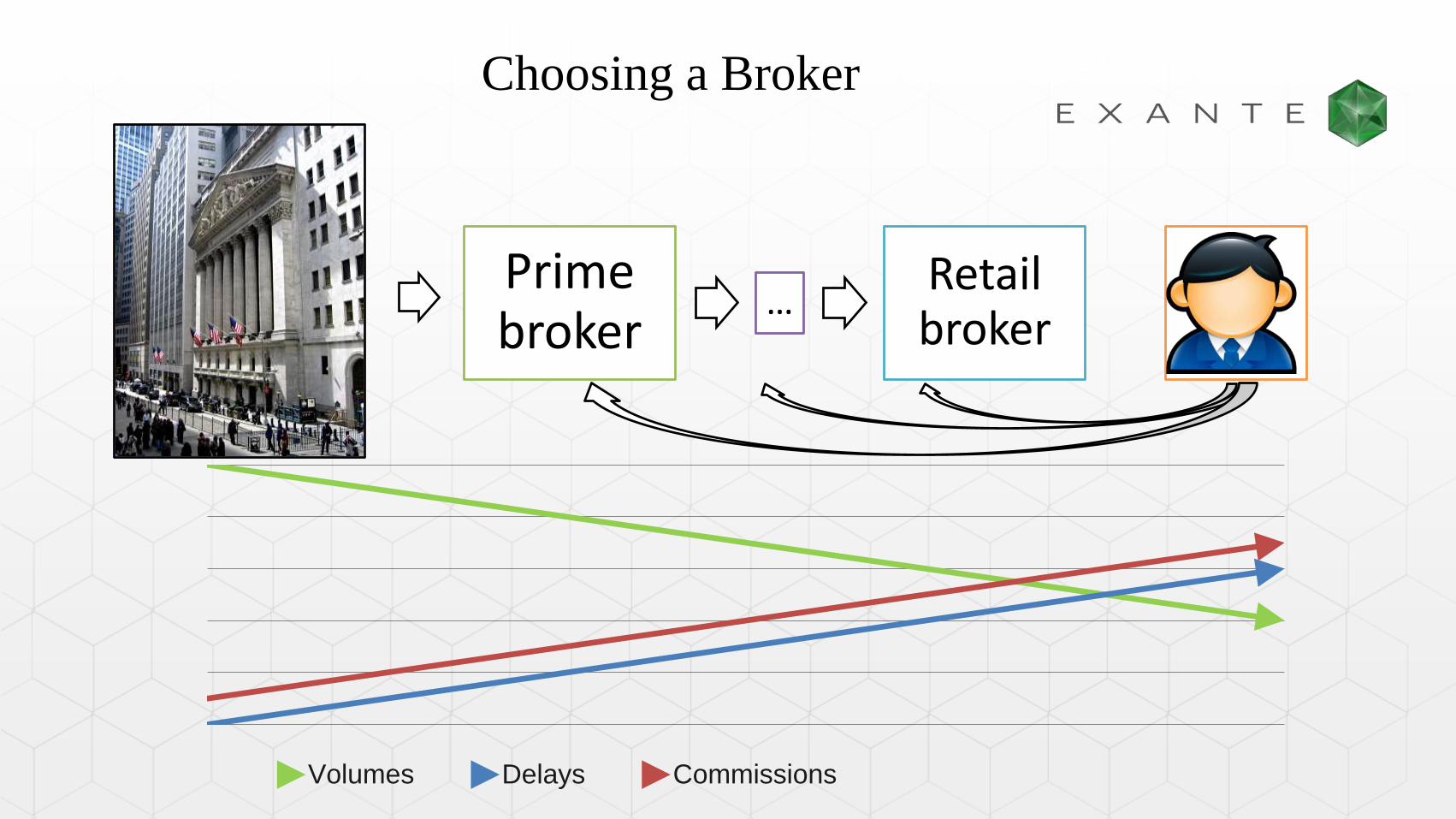

Prime broker

…Retail broker

Choosing a Broker

Volumes Delays Commissions

General

1. Exchanges/Markets coverage

2. Trading volumes

3. Regulation issues

4. Legal issues

5. Commissions and fees

Technology

Market data

Delays

Market Depth Best Bid Offer

Trades

Execution

Delays

Client side / Server side

Pre-trade risks, Software

Connection

Protocol

Virtual Machines

Co-location

Control

Trades Export

Interface

Error handling

NEXT GENERATION

PRIME BROKER

Questions?

Portomaso Business Tower, Level 7, ST. Julians, Malta

[email protected] | [email protected] | www.exante.eu

Top Related