Languages

Pages

Legal

Competitiveness of Pakistan Textile IndustryCompetitiveness of Pakistan Textile Industry

Issues and ChallengesIssues and Challenges

By. Syed Mumtaz AliBy. Syed Mumtaz Ali

Presentation Structure

Globalization & Changing Scenarios

Competitiveness in Textile Trade

Competitiveness of Pakistan Textile Industry

Issues and Challenges

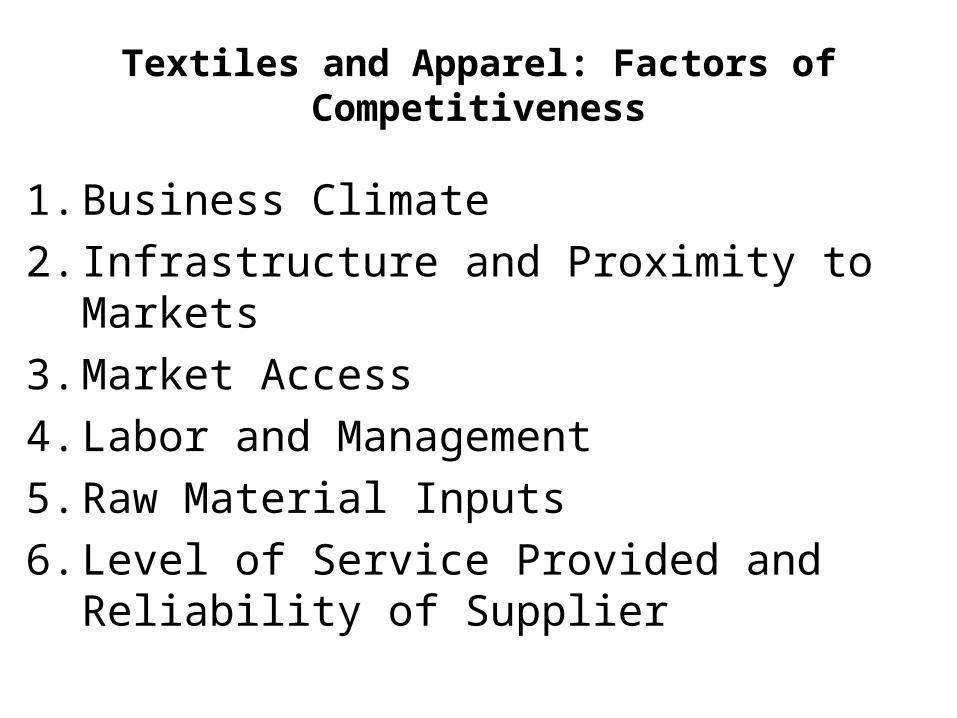

Textiles and Apparel: Factors of Competitiveness

1. Business Climate

2. Infrastructure and Proximity to Markets

3. Market Access

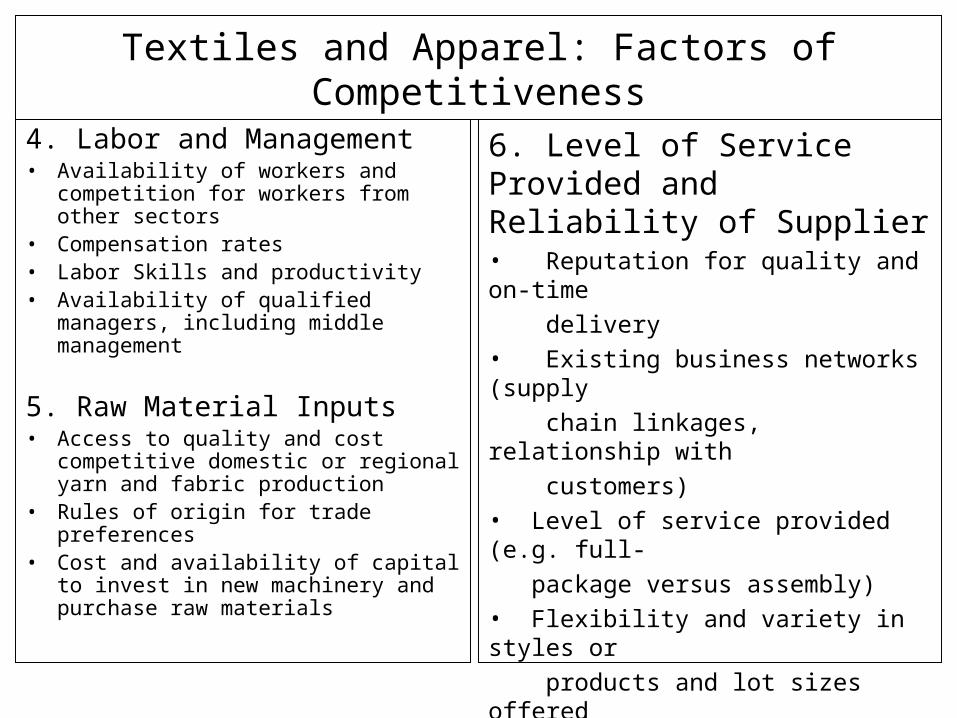

4. Labor and Management

5. Raw Material Inputs

6. Level of Service Provided and Reliability of Supplier

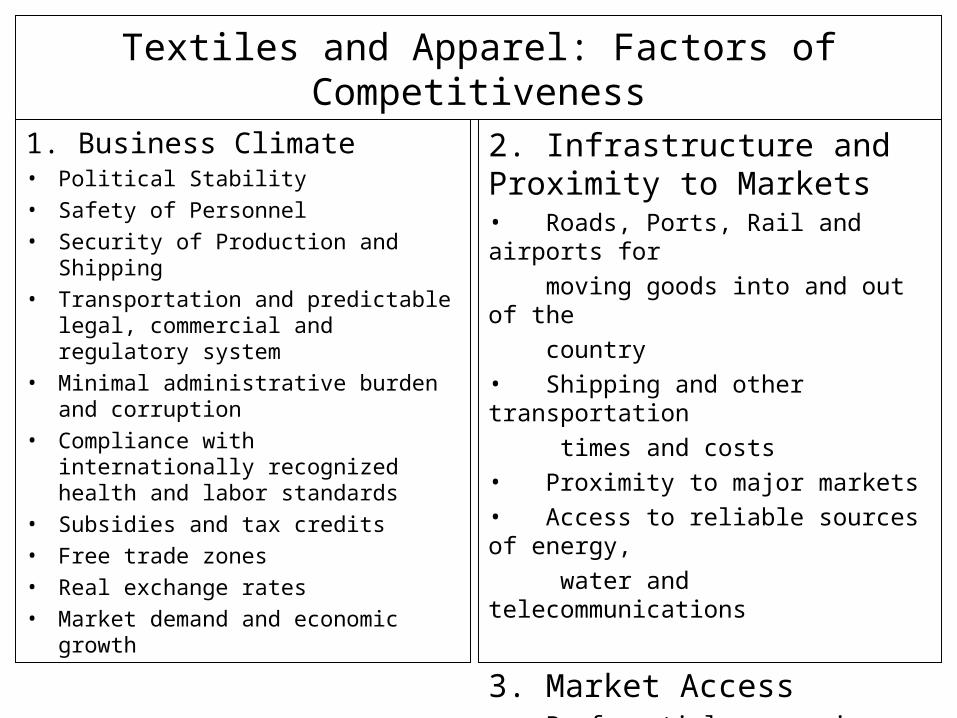

Textiles and Apparel: Factors of Competitiveness

1. Business Climate• Political Stability

• Safety of Personnel

• Security of Production and Shipping

• Transportation and predictable legal, commercial and regulatory system

• Minimal administrative burden and corruption

• Compliance with internationally recognized health and labor standards

• Subsidies and tax credits

• Free trade zones

• Real exchange rates

• Market demand and economic growth

2. Infrastructure and Proximity to Markets• Roads, Ports, Rail and airports for

moving goods into and out of the

country

• Shipping and other transportation

times and costs

• Proximity to major markets

• Access to reliable sources of energy,

water and telecommunications

3. Market Access• Preferential access in major markets

Textiles and Apparel: Factors of Competitiveness

4. Labor and Management• Availability of workers and

competition for workers from other sectors

• Compensation rates• Labor Skills and productivity• Availability of qualified managers,

including middle management

5. Raw Material Inputs• Access to quality and cost

competitive domestic or regional yarn and fabric production

• Rules of origin for trade preferences• Cost and availability of capital to

invest in new machinery and purchase raw materials

6. Level of Service Provided and Reliability of Supplier• Reputation for quality and on-time

delivery

• Existing business networks (supply

chain linkages, relationship with

customers)

• Level of service provided (e.g. full-

package versus assembly)

• Flexibility and variety in styles or

products and lot sizes offered

• Lead time and flexibility to respond to

quick turnaround orders

Globalization & Changing Scenarios

Global Trade is Growing

201 232 258

281351

397

0

100

200

300

400

500

600

700

2005 2008 2010

Textile Apparel

US

$ B

n

CAGR

Textile: 5.8%

Apparel: 9.6%

482 Bn

583 Bn

655 Bn

Projections of World Textile and Apparel Trade

Source: ITC

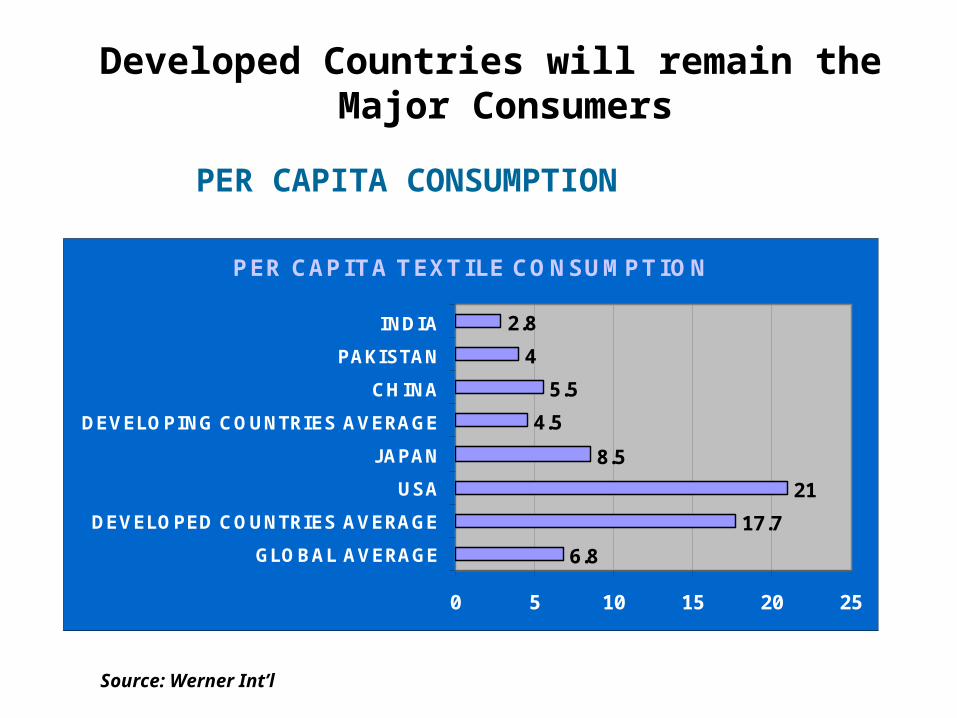

Developed Countries will remain the Major Consumers

PER CAPITA CONSUMPTION

PER CAPITA TEXTILE CONSUMPTION

6.8

17.7

21

8.5

4.5

5.5

4

2.8

0 5 10 15 20 25

GLOBAL AVERAGE

DEVELOPED COUNTRIES AVERAGE

USA

JAPAN

DEVELOPING COUNTRIES AVERAGE

CHINA

PAKISTAN

INDIA

Source: Werner Int’l

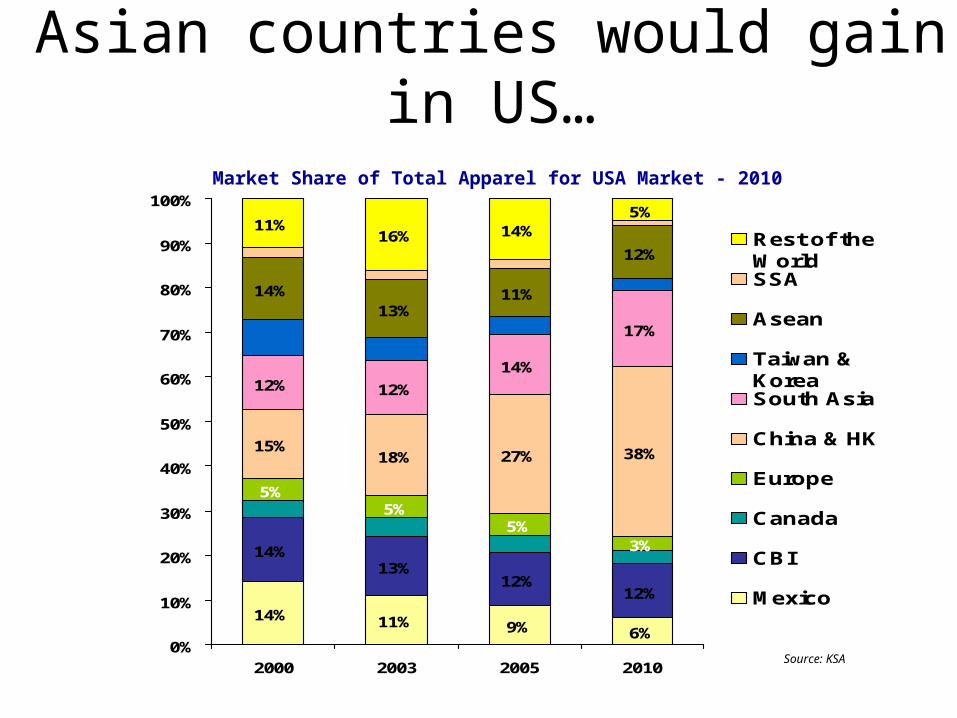

Market Share of Total Apparel for USA Market - 2010

Asian countries would gain in US…

14% 11% 9% 6%

14%13%

12%12%

5%5%

5%3%

15%18% 27% 38%

12% 12%

14%

17%

14%13%

11%

12%

11%16% 14%

5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2003 2005 2010

Rest of theWorldSSA

Asean

Taiwan &KoreaSouth Asia

China & HK

Europe

Canada

CBI

Mexico

Source: KSA

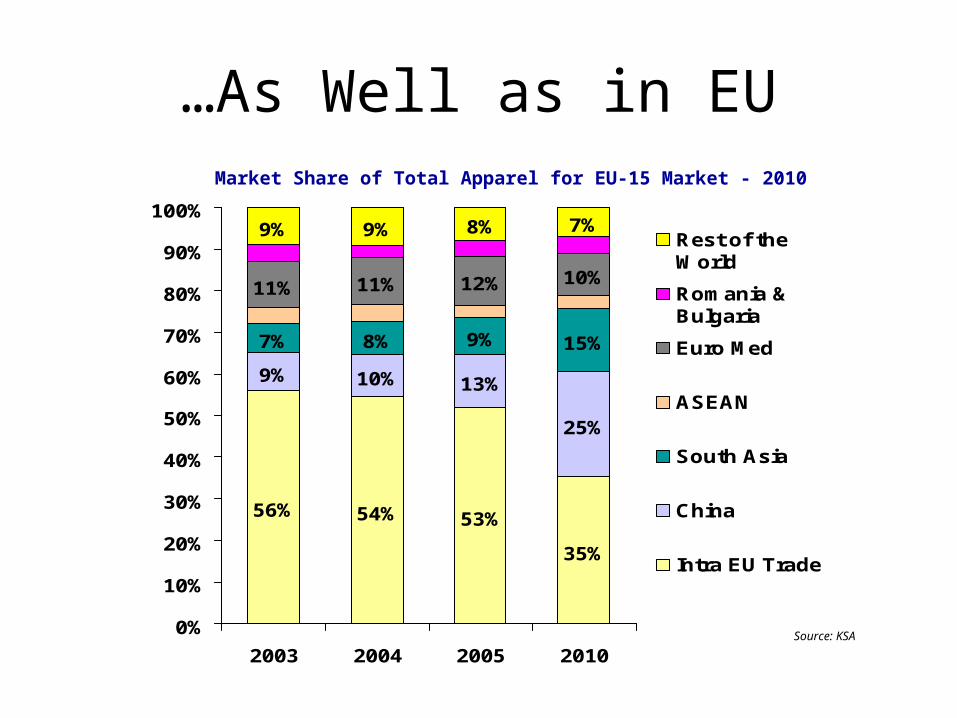

…As Well as in EU

56% 54% 53%

35%

9% 10% 13%

25%

7% 8% 9% 15%

11% 11% 12% 10%

9% 9% 8% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2003 2004 2005 2010

Rest of theWorld

Romania &Bulgaria

Euro Med

ASEAN

South Asia

China

Intra EU Trade

Source: KSA

Market Share of Total Apparel for EU-15 Market - 2010

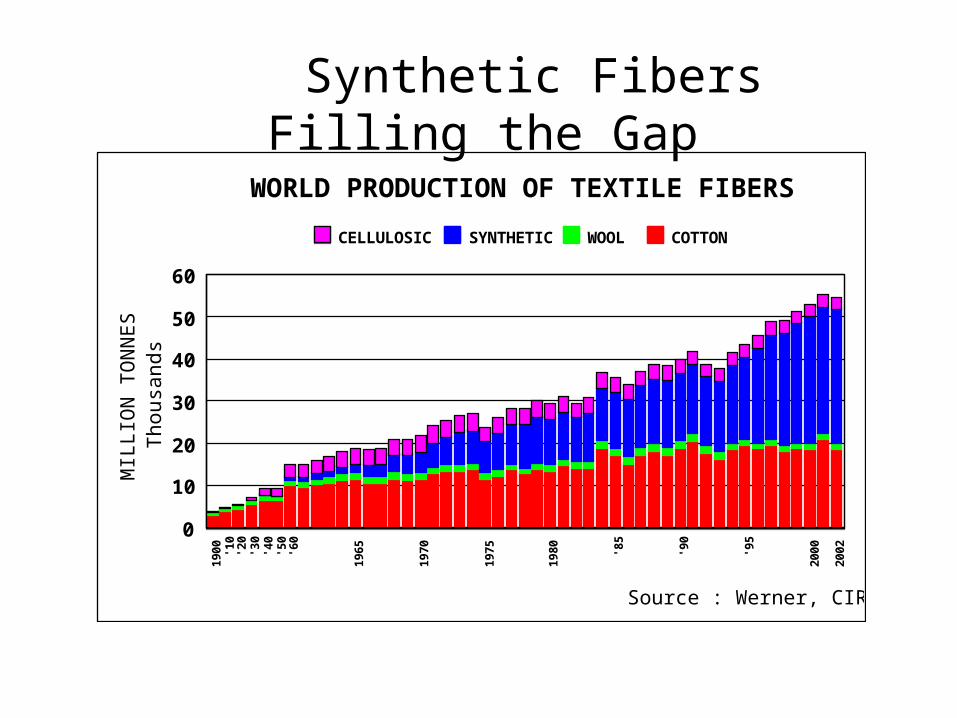

1900 '10

'20

'30

'40

'50

'60

1965

1970

1975

1980 '85

'90

'95

2000

2002

0

10

20

30

40

50

60

Tho

usan

dsM

ILLI

ON

TO

NN

ES

CELLULOSIC SYNTHETIC WOOL COTTON

Source : Werner, CIRFS

WORLD PRODUCTION OF TEXTILE FIBERS

Synthetic Fibers Filling the Gap

Changing Requirements of Customers

Customers are……• Focusing more on Retail end

and • Looking to Optimize Sourcing Costs

Therefore………• Identifying Their Strategic Partners …..and• Increasing Direct Sourcing

Traditional VS Strategic Relationships

80%

20%

Past

TransactionalVendors

Relationship

StrategicPartnerships

Future

20%

80%

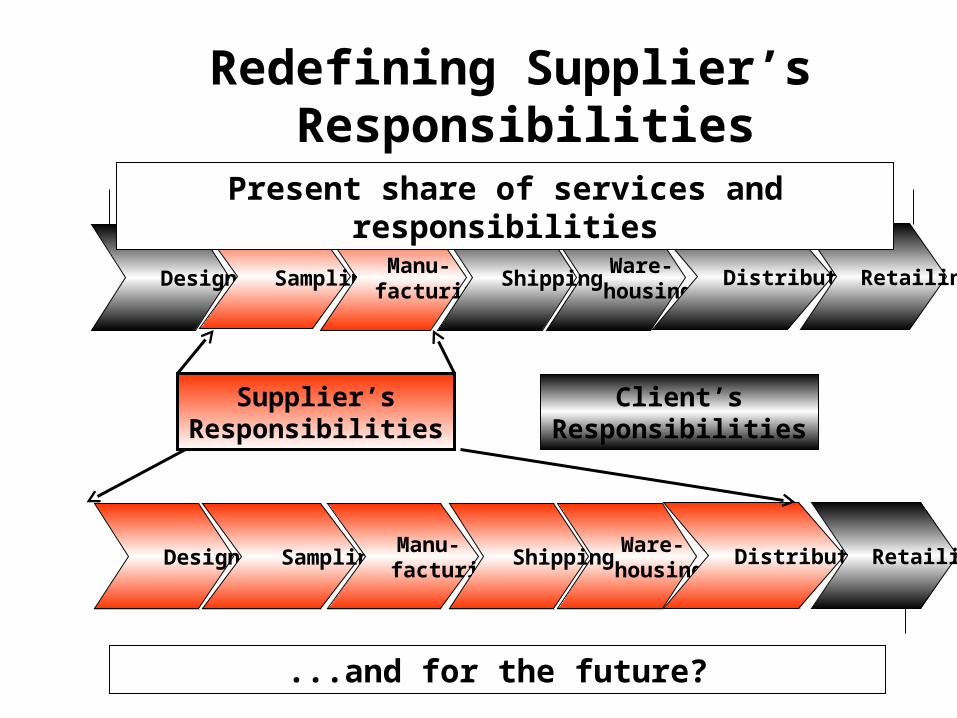

Redefining Supplier’s Responsibilities

Ware- housing

Distribution Retailing

Client’sResponsibilities

Design Sampling Manu-

facturing Shipping

Supplier’sResponsibilities

Ware- housing

Distribution Retailing Design Sampling Manu-

facturing Shipping

Present share of services and responsibilities

...and for the future?

Buyers are looking for complete Solutions

Convenience

Compliance

Cost

Flexibility

Speed

Innovation

Buyer Requirements

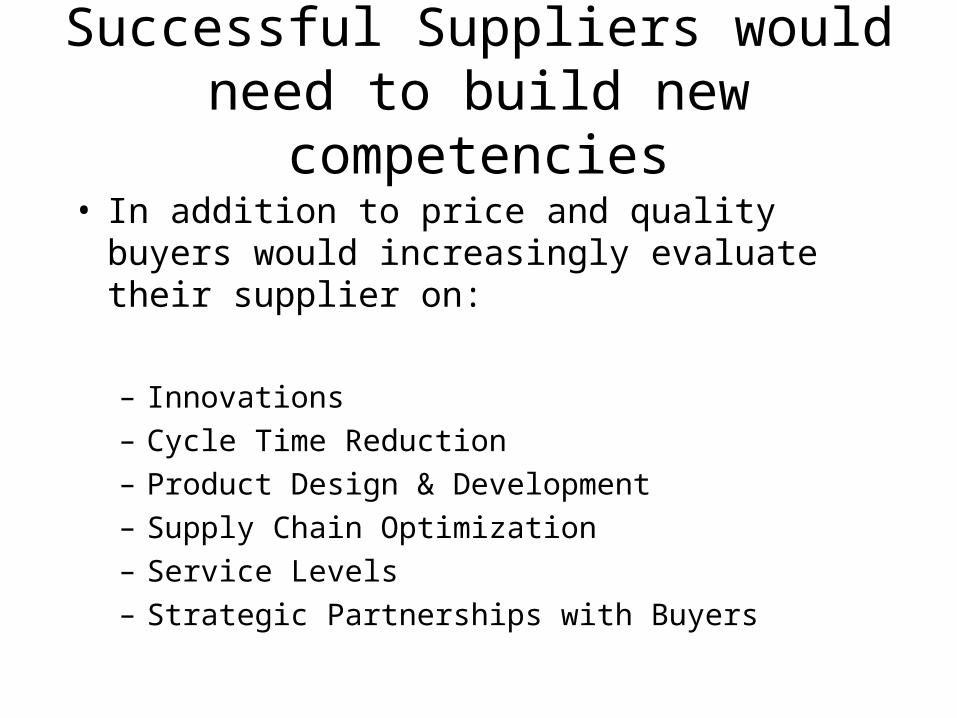

Successful Suppliers would need to build new competencies

• In addition to price and quality buyers would increasingly evaluate their supplier on:

– Innovations– Cycle Time Reduction – Product Design & Development– Supply Chain Optimization– Service Levels– Strategic Partnerships with Buyers

Globalization

Equally easy access to latest technologies for all players. Capital not technology is the only restricting factor

to set up new capacities

Equally easy access to latest technologies for all players. Capital not technology is the only restricting factor

to set up new capacities

Fully integrated textile chain becomes a strategic asset

Fully integrated textile chain becomes a strategic asset

Reliability in services and short lead times being THE KEY purchasing factors for buyers

initiating partnership and alliances

Reliability in services and short lead times being THE KEY purchasing factors for buyers

initiating partnership and alliances

The strategic choice for textile manufacturers is between high volume low

cost products or niche products

The strategic choice for textile manufacturers is between high volume low

cost products or niche products

Closures or reduction of textile production capacities in high cost countries, mainly EU, Japan, USA

Closures or reduction of textile production capacities in high cost countries, mainly EU, Japan, USA

Exchangeability of the products, price becomes major factor of

differentiation

Exchangeability of the products, price becomes major factor of

differentiation

In a Nutshell the Effects of Globalisation are…..

Competitiveness of Pakistan Textile Industry

Issues and Challenges

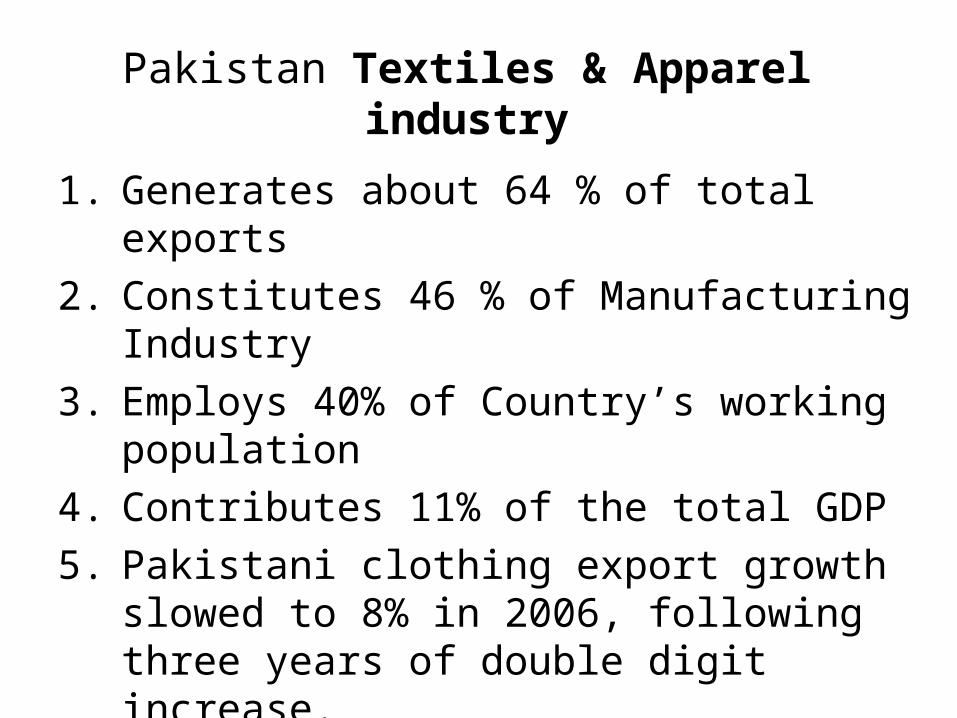

Pakistan Textiles & Apparel industry

1. Generates about 64 % of total exports2. Constitutes 46 % of Manufacturing

Industry3. Employs 40% of Country’s working

population

4. Contributes 11% of the total GDP

5. Pakistani clothing export growth slowed to 8% in 2006, following three years of double digit increase.

World Trade Share

China, 24%

Hong Kong, 9%

Italy, 7%Taiwan, 2%

Pakistan, 2%Mexico, 2%

Indonesia, 2%

Other, 27%

Germany, 6%

Turkey, 4%Belgium, 3%

France, 3%

United States, 4%

India, 3%

Korea, Republic of, 3%

Pakistan’s Textile & Apparel Industry…

% Share in Global trade

Pakistan Textile Exports – Major Categories

Fabrics 24%

Ready Made Garments 12%

Knitwear (Hosiery)18%

Madeups Incl. Bedwear 21%

Tents & Canvas 1%

Art Silk & Syn.Tex 3%

Towels 6%

Other textiles2%

Yarn 12%

Raw Cotton 1%

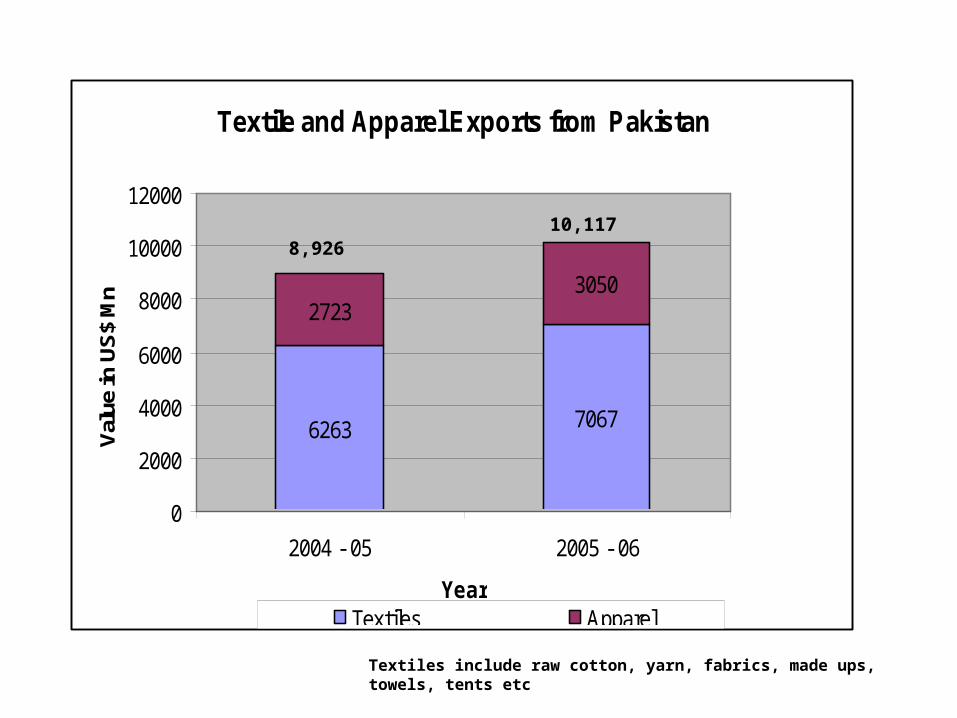

Textile and Apparel Exports from Pakistan

6263 7067

27233050

0

2000

4000

6000

8000

10000

12000

2004 - 05 2005 - 06

Year

Val

ue in

US

$ M

n

Textiles Apparel

8,92610,117

Textiles include raw cotton, yarn, fabrics, made ups, towels, tents etc

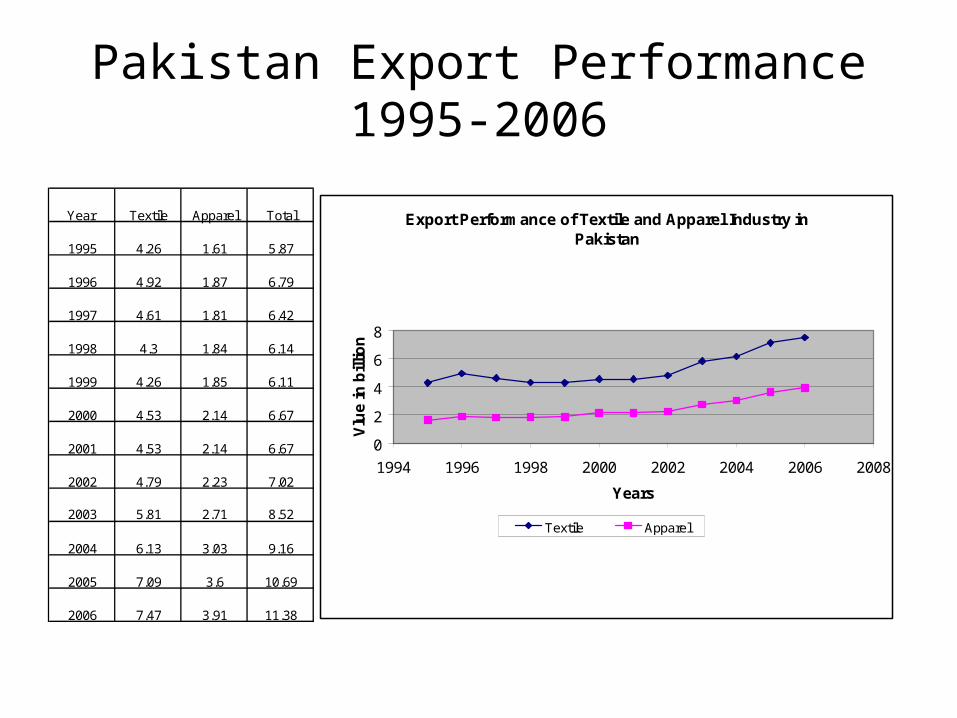

Pakistan Export Performance1995-2006

Year Textile Apparel Total

1995 4.26 1.61 5.87

1996 4.92 1.87 6.79

1997 4.61 1.81 6.42

1998 4.3 1.84 6.14

1999 4.26 1.85 6.11

2000 4.53 2.14 6.67

2001 4.53 2.14 6.67

2002 4.79 2.23 7.02

2003 5.81 2.71 8.52

2004 6.13 3.03 9.16

2005 7.09 3.6 10.69

2006 7.47 3.91 11.38

Export Performance of Textile and Apparel Industry in Pakistan

0

2

4

6

8

1994 1996 1998 2000 2002 2004 2006 2008

Years

Vlu

e in

bill

ion

Textile Apparel

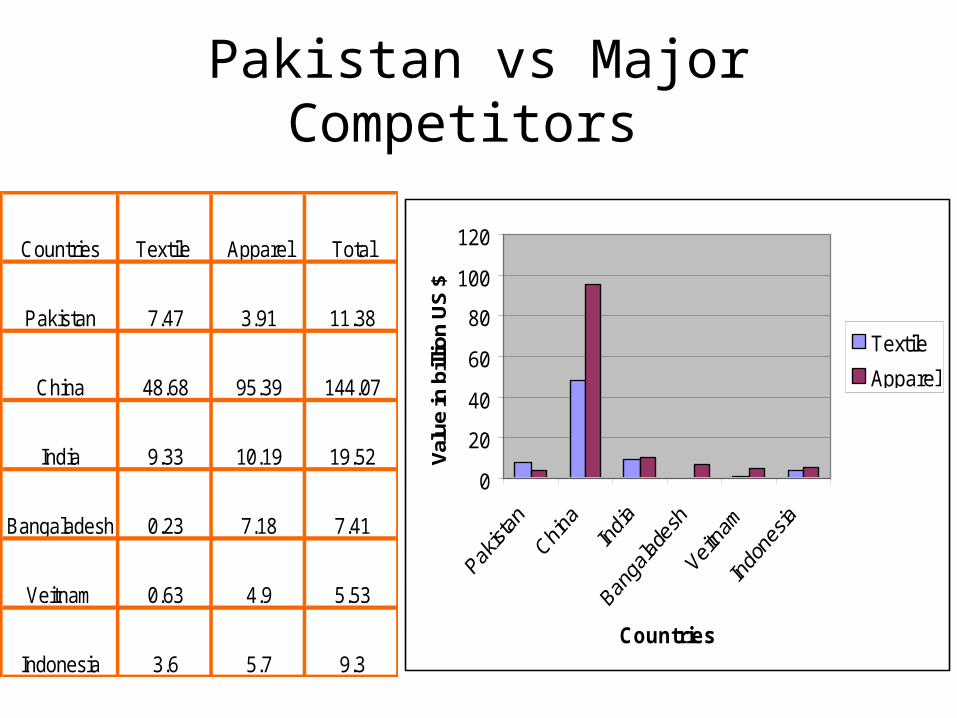

Pakistan vs Major Competitors

Countries Textile Apparel Total

Pakistan 7.47 3.91 11.38

China 48.68 95.39 144.07

India 9.33 10.19 19.52

Bangaladesh 0.23 7.18 7.41

Veitnam 0.63 4.9 5.53

Indonesia 3.6 5.7 9.3

0

20

40

60

80

100

120

Countries

Valu

e in

bill

ion

US

$

Textile

Apparel

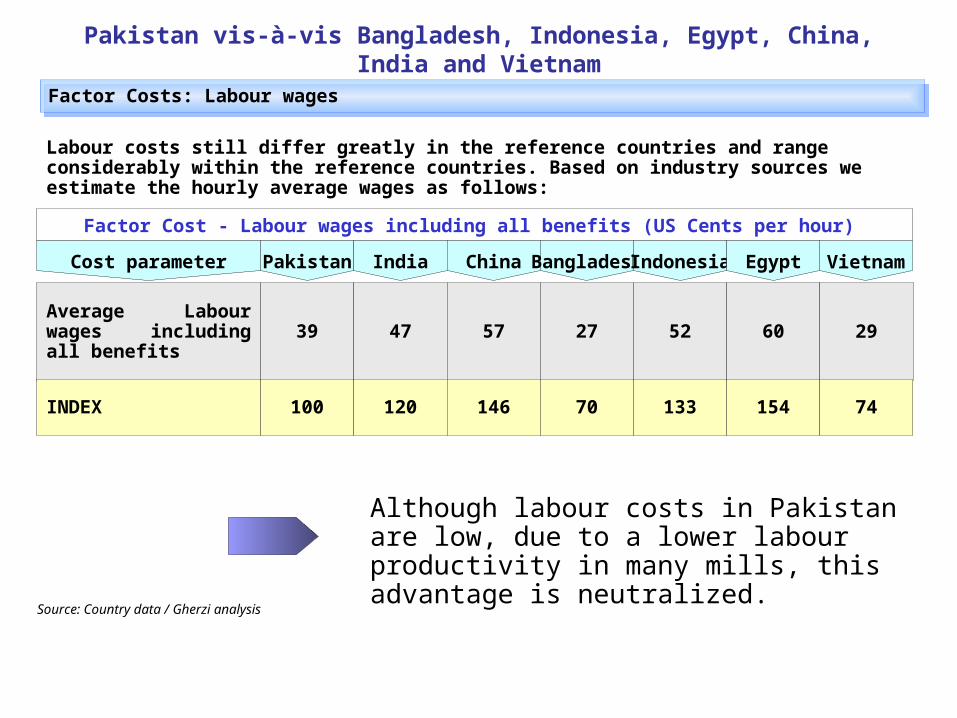

Cost parameter Pakistan India China Bangladesh Indonesia Egypt

Average Labour wages including all benefits 39 47 57 27 52 60

Factor Cost - Labour wages including all benefits (US Cents per hour)

Source: Country data / Gherzi analysis

Factor Costs: Labour wages Factor Costs: Labour wages

29

Vietnam

Labour costs still differ greatly in the reference countries and range considerably within the reference countries. Based on industry sources we estimate the hourly average wages as follows:

INDEX 100 120 146 70 133 154 74

Although labour costs in Pakistan are low, due to a lower labour productivity in many mills, this advantage is neutralized.

Pakistan vis-à-vis Bangladesh, Indonesia, Egypt, China, India and Vietnam

Source: Country data / Gherzi analysis

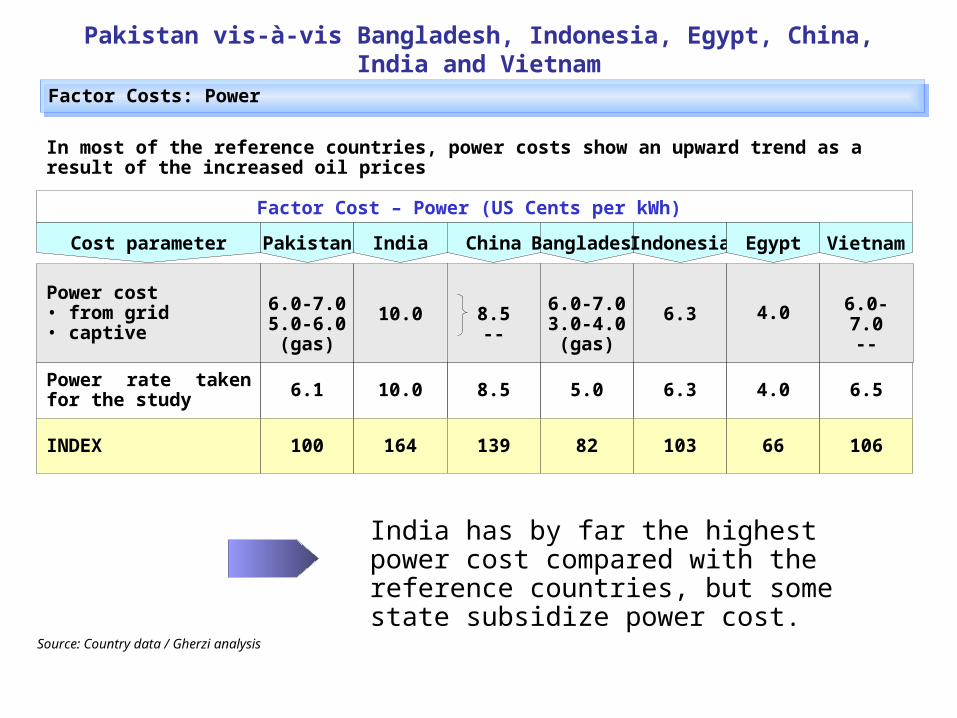

Factor Costs: PowerFactor Costs: Power

Cost parameter Pakistan India China Bangladesh Indonesia Egypt

Power cost• from grid• captive

6.0-7.05.0-6.0

(gas)

10.0 8.5--

6.0-7.03.0-4.0(gas)

6.3 4.0

Factor Cost – Power (US Cents per kWh)

6.0-7.0--

Vietnam

In most of the reference countries, power costs show an upward trend as a result of the increased oil prices

Power rate taken for the study 6.1 10.0 8.5 5.0 6.3 4.0 6.5

INDEX 100 164 139 82 103 66 106

India has by far the highest power cost compared with the reference countries, but some state subsidize power cost.

Pakistan vis-à-vis Bangladesh, Indonesia, Egypt, China, India and Vietnam

Factor Cost - Raw water (US Cents per m3) 2006

Source:Gherzi analysis

Cost parameter Pakistan India China Bangladesh Indonesia Egypt

Raw water cost US Cents per m3

18.2*60***

14* 46** 42.0

Ground water, onlytreatment

costs

River water, onlytreatment

costs

0.23 24.0

Vietnam

Factor Costs: Raw Water and SteamFactor Costs: Raw Water and Steam

•In Bangladesh and Indonesia most mills use ground water from their own wells, which results in low water costs

* Borewell

** Industrial Development Corporation

***Tanker Water (Karachi)

Factor Cost - Steam (US Cents per kg of steam) 2006

Cost parameter Pakistan India China Bangladesh Indonesia Egypt

US Cents per kg of steam

Generated from

2.0

Furnace Oil

1.1

Coal

2.0

Coal

0.8

Gas

1.0

Furnace Oil

2.0

Furnace Oil

Vietnam

1.6

Furnace Oil

India and China have the highest water rates of the reference countries

Compared with Pakistan and China, India has a lower cost of steam

Pakistan vis-à-vis Bangladesh, Indonesia, Egypt, China, India and Vietnam

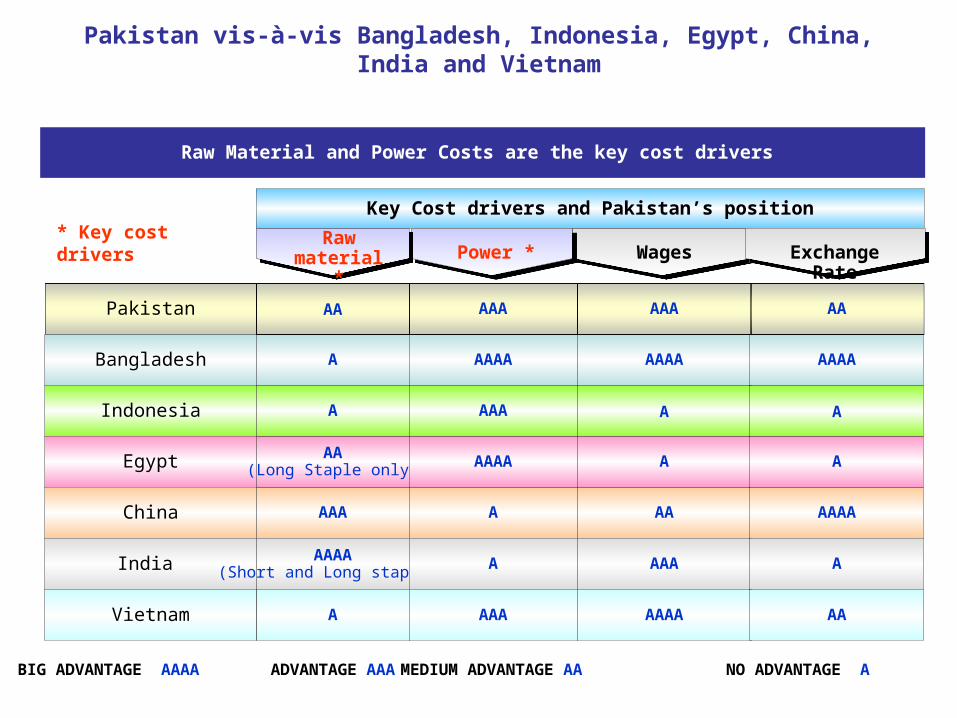

Raw Material and Power Costs are the key cost drivers

BIG ADVANTAGE AAAA ADVANTAGE AAA MEDIUM ADVANTAGE AA NO ADVANTAGE A

Raw material

*Power * Wages

Key Cost drivers and Pakistan’s position* Key cost drivers

Exchange Rate

Pakistan

Bangladesh

Indonesia

Egypt

China

India

AAA A AA

AA(Long Staple only) AAAA A

A AAA A

A AAAA AAAA

AA AAA AAA

AAAA(Short and Long staples) A AAA

A AAA AAAAVietnam

AAAA

A

A

AAAA

AA

A

AA

Pakistan vis-à-vis Bangladesh, Indonesia, Egypt, China, India and Vietnam

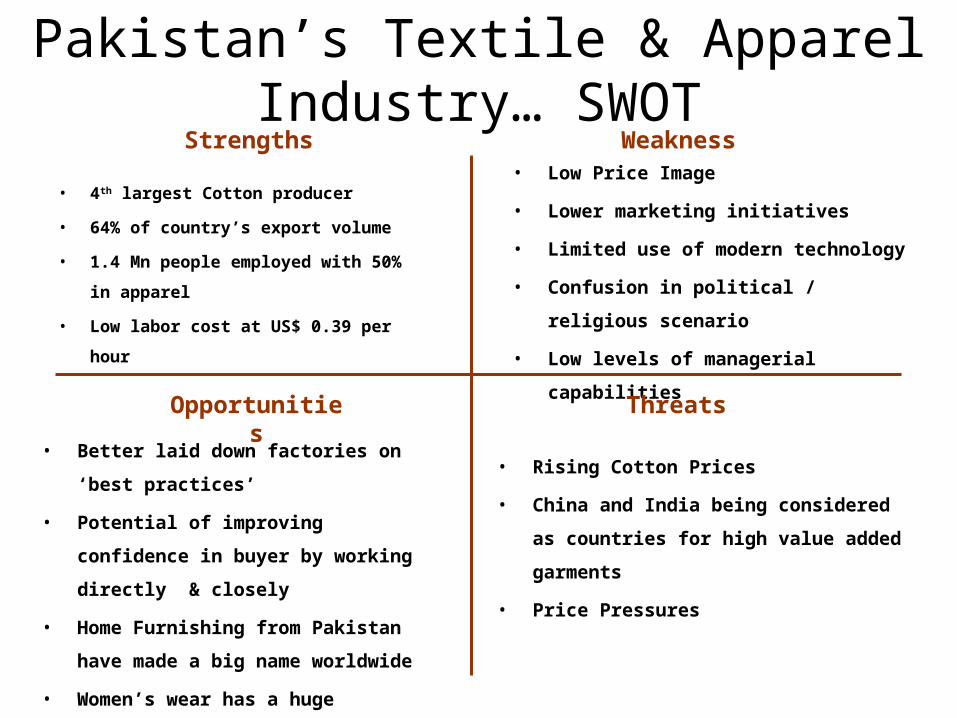

Pakistan’s Textile & Apparel Industry… SWOT

• 4th largest Cotton producer

• 64% of country’s export volume

• 1.4 Mn people employed with 50% in

apparel

• Low labor cost at US$ 0.39 per hour

• Low Price Image

• Lower marketing initiatives

• Limited use of modern technology

• Confusion in political / religious

scenario

• Low levels of managerial capabilities

• Rising Cotton Prices

• China and India being considered as

countries for high value added garments

• Price Pressures

• Better laid down factories on ‘best

practices’

• Potential of improving confidence in

buyer by working directly & closely

• Home Furnishing from Pakistan have

made a big name worldwide

• Women’s wear has a huge potential

Strengths Weakness

Opportunities Threats

What Needs to be done

Use of Technology

Collaboration in Product

Development

Increase Efficiency and Productivity

Consistent Manufacturing

Standards

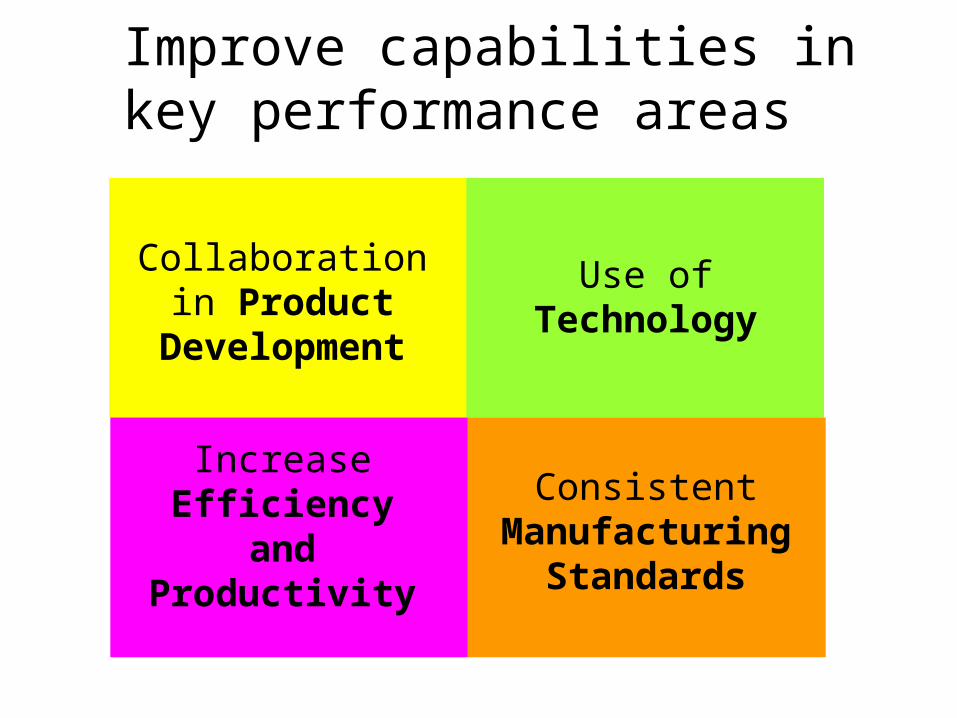

Improve capabilities in key performance areas

• Build capabilities in the following areas:

– Productivity Improvements across Supply Chain

– Consolidating Operations

– Building Logistic Capabilities

– Developing long term relationships with Clients

– Collaborating with buyers on forecasting and

inventory management

– Investing in IT infrastructure and compliance

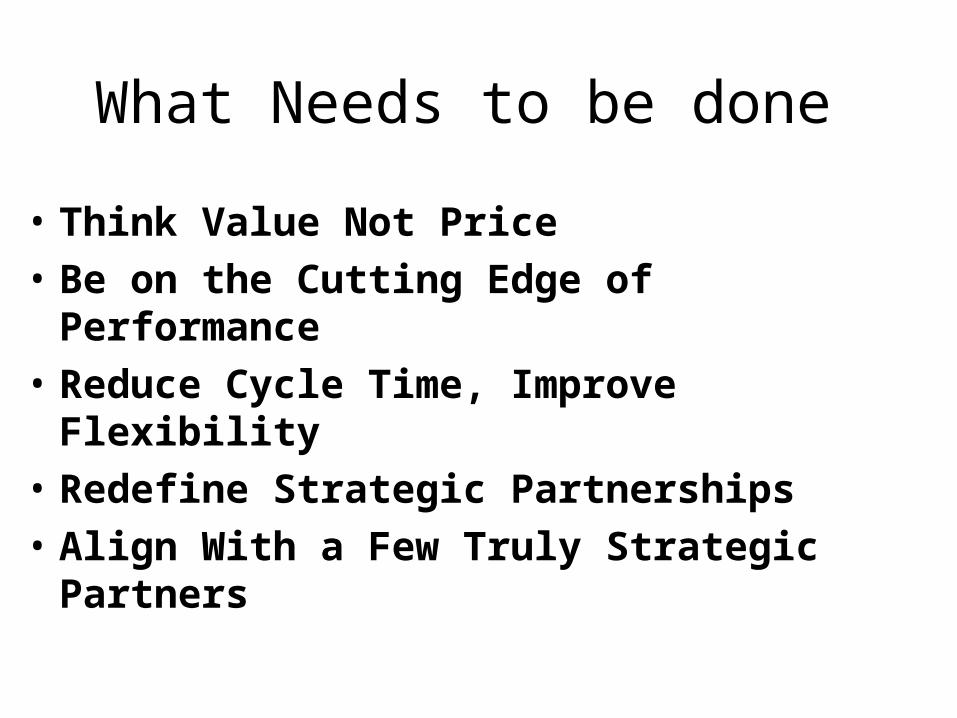

What Needs to be done

What Needs to be done

• Think Value Not Price

• Be on the Cutting Edge of Performance

• Reduce Cycle Time, Improve Flexibility

• Redefine Strategic Partnerships

• Align With a Few Truly Strategic Partners

Thank You

Top Related