Languages

Pages

Legal

Cautionary statement

This presentation contains certain statements that are neither reported financial results nor other historical information. These statements are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements include information with respect to National Grid’s financial condition, National Grid’s results of operations and businesses, strategy, plans and objectives. Words such as “anticipates”, “expects”, “intends”, “plans”, “believes”, “seeks”, “estimates”, “may”, “will”, “continue”, “project” and similar expressions, as well as statements in the future tense, identify forward-looking statements. These forward-looking statements are not guarantees of National Grid’s future performance and are subject to assumptions, risks and uncertainties that could cause actual future results to differ materially from those expressed in or implied by the forward-looking statements. Many of these assumptions, risks and uncertainties relate to factors that are beyond National Grid's ability to control or estimate precisely, such as delays in obtaining, or adverse conditions contained in, regulatory approvals and contractual consents, including those required to complete the proposed acquisition of KeySpan when or as planned, unseasonable weather affecting the demand for electricity and gas, competition and industry restructuring, changes in economic conditions, currency fluctuations, changes in interest and tax rates, changes in energy market prices, changes in historical weather patterns, changes in laws, regulations or regulatory policies, developments in legal or public policy doctrines, the impact of changes to accounting standards and technological developments. Other factors that could cause actual results to differ materially from those described in this presentation include the ability to integrate the businesses relating to announced acquisitions with our existing business and realise the expected synergies from such integration, the availability of new acquisition opportunities and the timing and success of future acquisition opportunities, the impact of the sales of businesses by National Grid, the failure for any reason to achieve reductions in costs or to achieve operational efficiencies, the failure to retain key management, the behaviour of UK electricity market participants on system balancing, the timing of amendments in prices to shippers in the UK gas market, the performance of National Grid's pension schemes and the regulatory treatment of pension costs, and any adverse consequences arising from outages on or otherwise affecting energy networks, including gas pipelines, owned or operated by National Grid. For a more detailed description of some of these assumptions, risks and uncertainties, together with any other risk factors, please see National Grid's filings with and submissions to the US Securities and Exchange Commission (the “SEC”) (and in particular the "Risk Factors" and "Operating and Financial Review" sections in its most recent Annual Report on Form 20-F and the “Risk Factors” section in its Registration Statement on Form F-3 filed with the SEC on 28 June 2006). Except as may be required by law or regulation, National Grid undertakes no obligation to update any of its forward-looking statements. The effects of these factors are difficult to predict. New factors emerge from time to time and National Grid cannot assess the potential impact of any such factor on its activities or the extent to which any factor, or combination of factors, may cause results to differ materially from those contained in any forward-looking statement.

Sir John Parker

Chairman

Steve Lucas

Finance Director

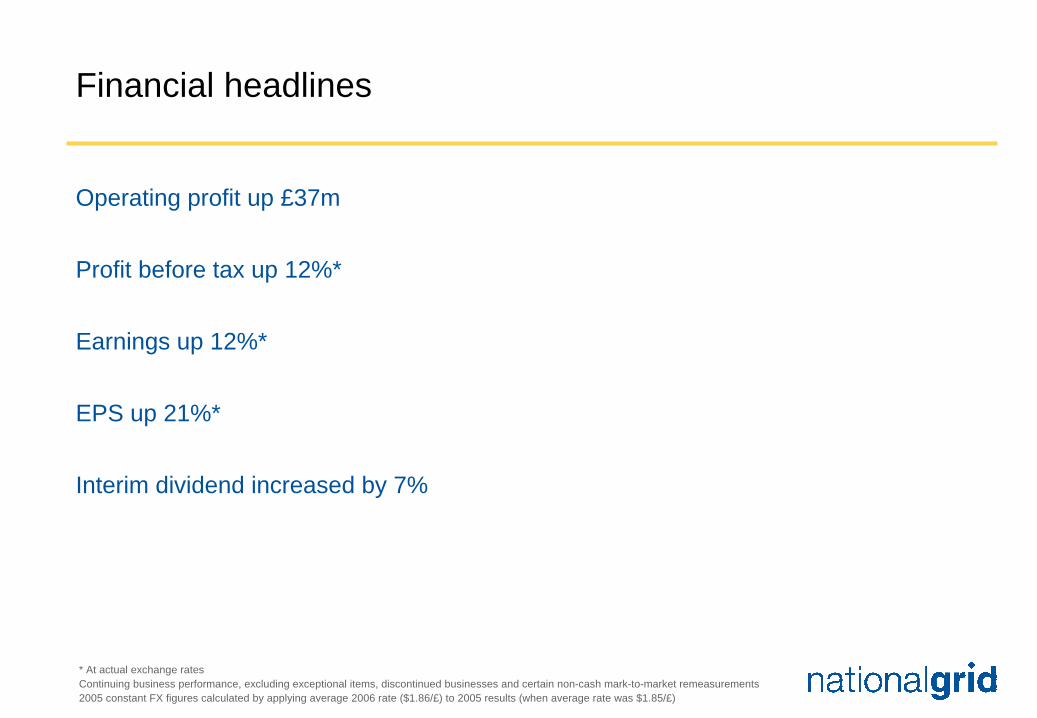

Financial headlines

Operating profit up £37m

Profit before tax up 12%*

Earnings up 12%*

EPS up 21%*

Interim dividend increased by 7%

* At actual exchange ratesContinuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements2005 constant FX figures calculated by applying average 2006 rate ($1.86/£) to 2005 results (when average rate was $1.85/£)

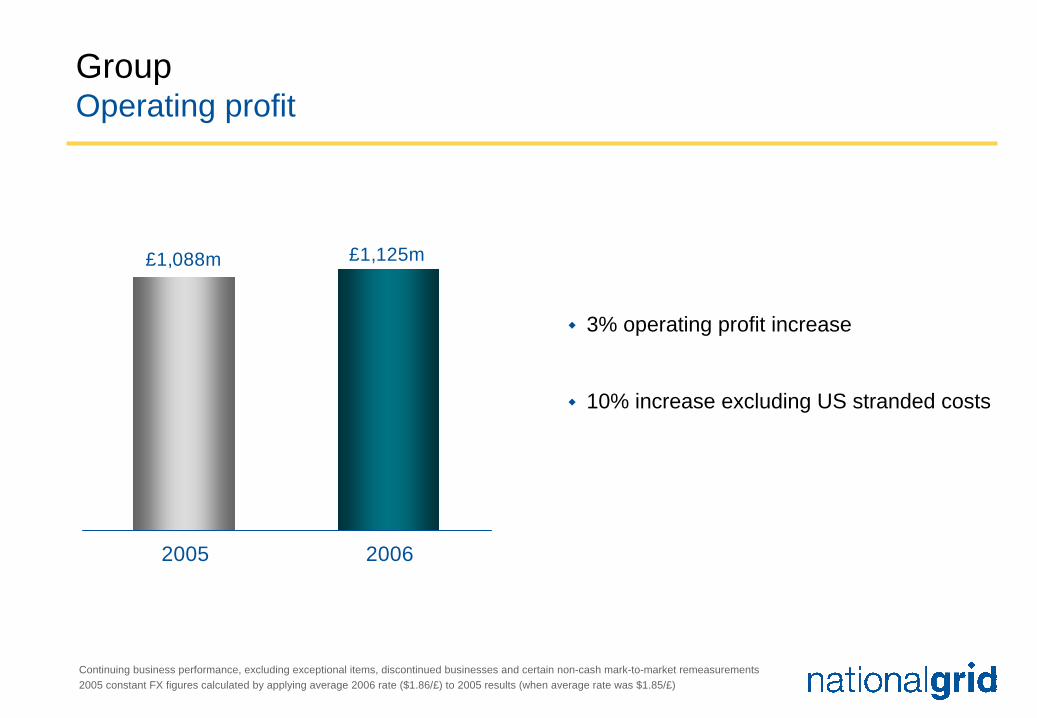

£1,088m £1,125m

2005 2006

GroupOperating profit

3% operating profit increase

10% increase excluding US stranded costs

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements2005 constant FX figures calculated by applying average 2006 rate ($1.86/£) to 2005 results (when average rate was $1.85/£)

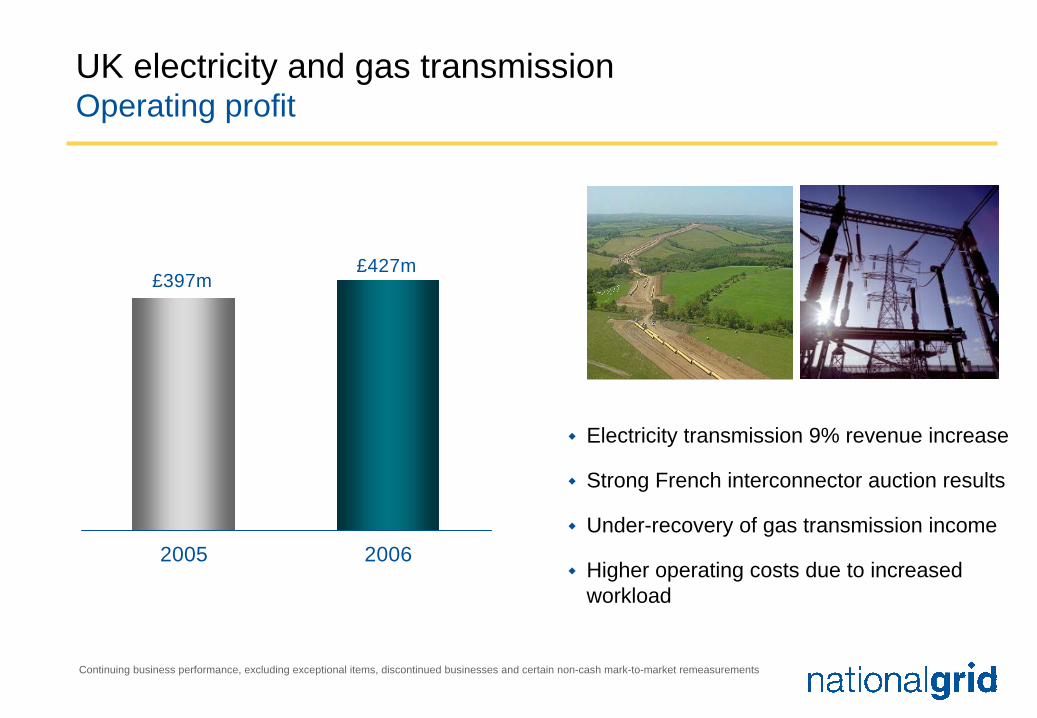

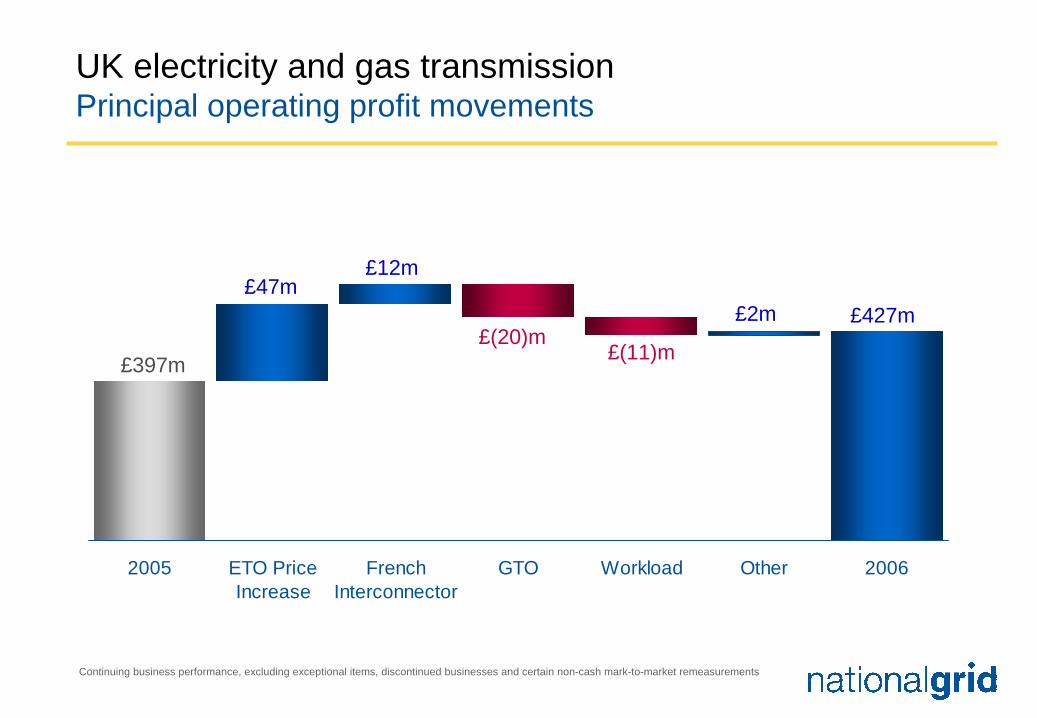

UK electricity and gas transmissionOperating profit

Electricity transmission 9% revenue increase

Strong French interconnector auction results

Under-recovery of gas transmission income

Higher operating costs due to increased workload

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements

£427m£397m

2005 2006

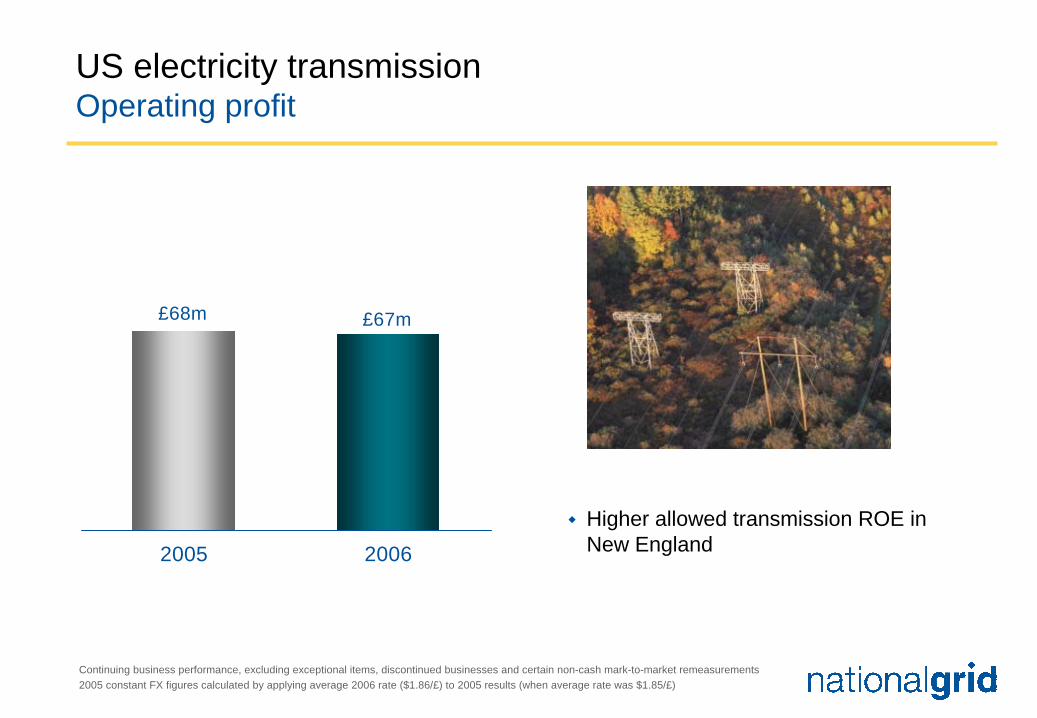

US electricity transmissionOperating profit

Higher allowed transmission ROE inNew England

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements2005 constant FX figures calculated by applying average 2006 rate ($1.86/£) to 2005 results (when average rate was $1.85/£)

£67m£68m

2005 2006

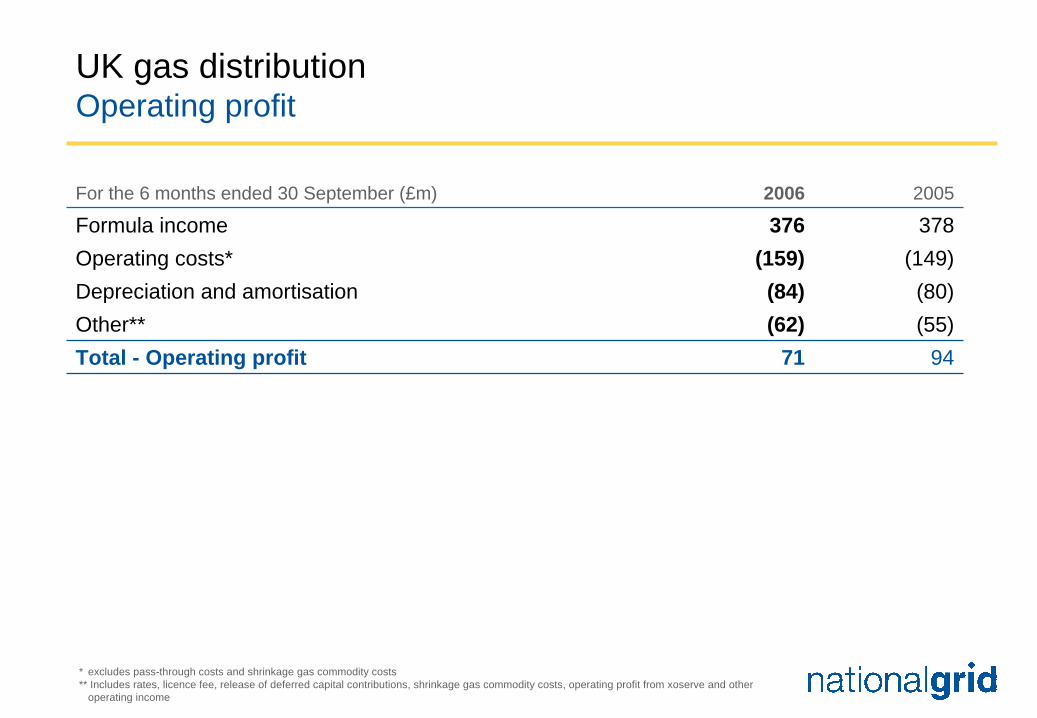

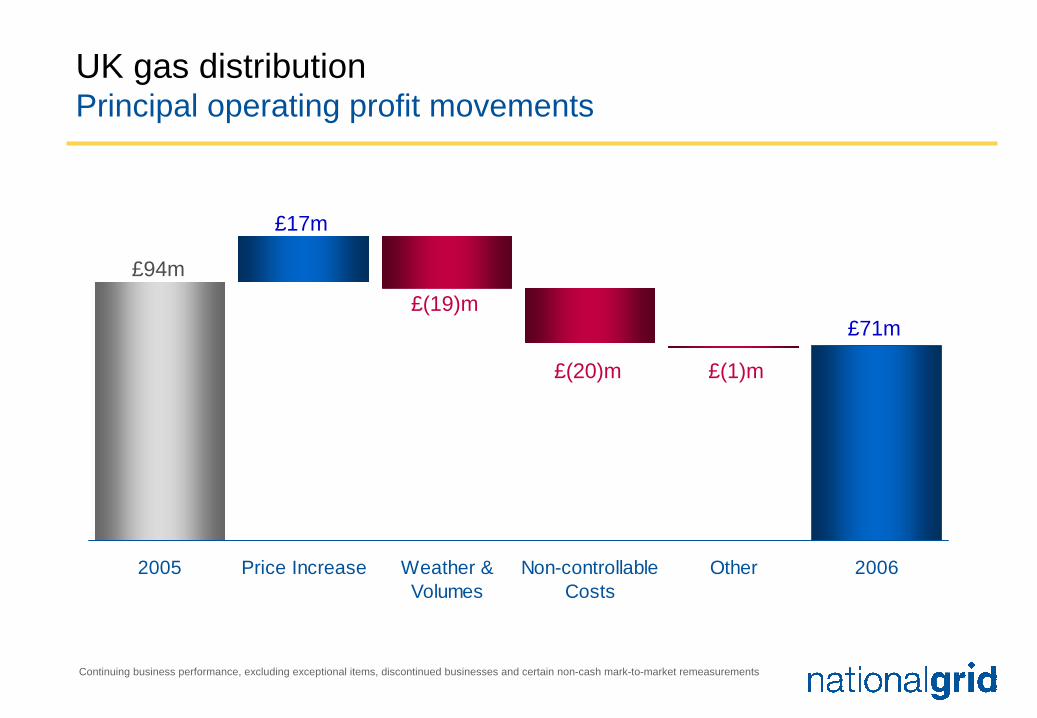

UK gas distributionOperating profit

Warm weather and lower volumesBusiness rate increase

9% gas distribution price increase in October

Other non-controllable costs Pensions and shrinkage gas

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements

£71m

£94m

2005 2006

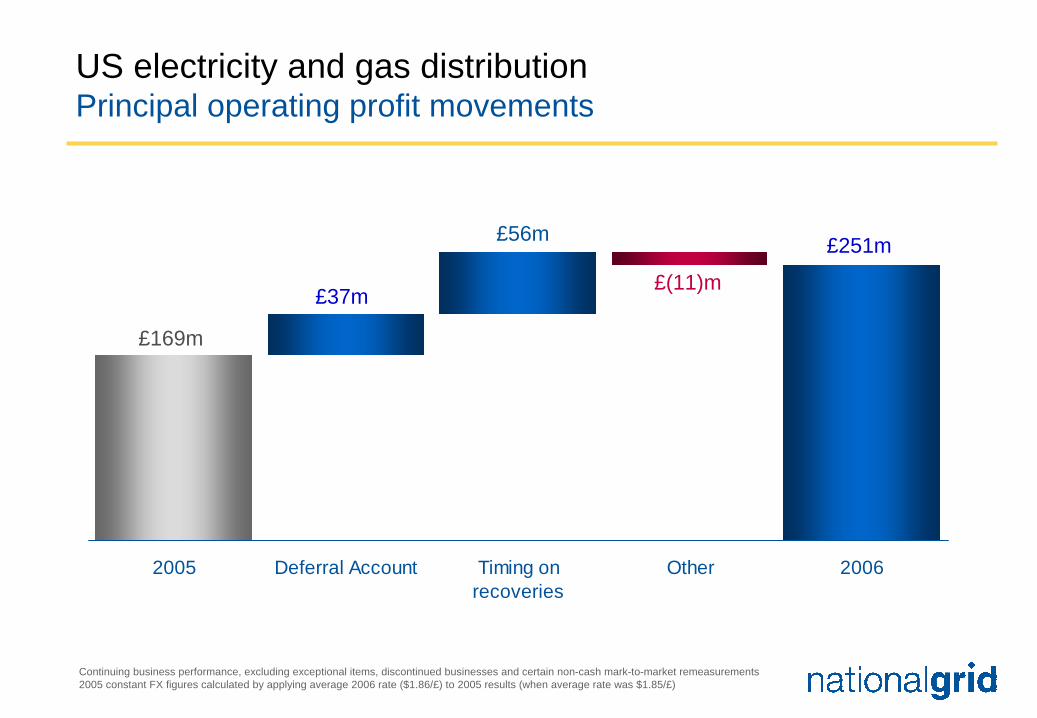

US electricity and gas distribution Operating profit

New York deferral account recoveryTiming of pass through costs recoveryOther impacts:

Increased reliability andmaintenance spend

Lower delivery volumes

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements2005 constant FX figures calculated by applying average 2006 rate ($1.86/£) to 2005 results (when average rate was $1.85/£)

£251m

£169m

2005 2006

US stranded cost recoveriesOperating profit

Decline in stranded asset base

USGen settlement last year

Contract settlements flat

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements2005 constant FX figures calculated by applying average 2006 rate ($1.86/£) to 2005 results (when average rate was $1.85/£)

£202m

£249m

2005 2006

Wireless infrastructureOperating profit

17% operating profit growth

Strong Broadcast performanceTwo new channel contracts

Continued growth in mobile tenancies

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements

£42m

£36m

2005 2006

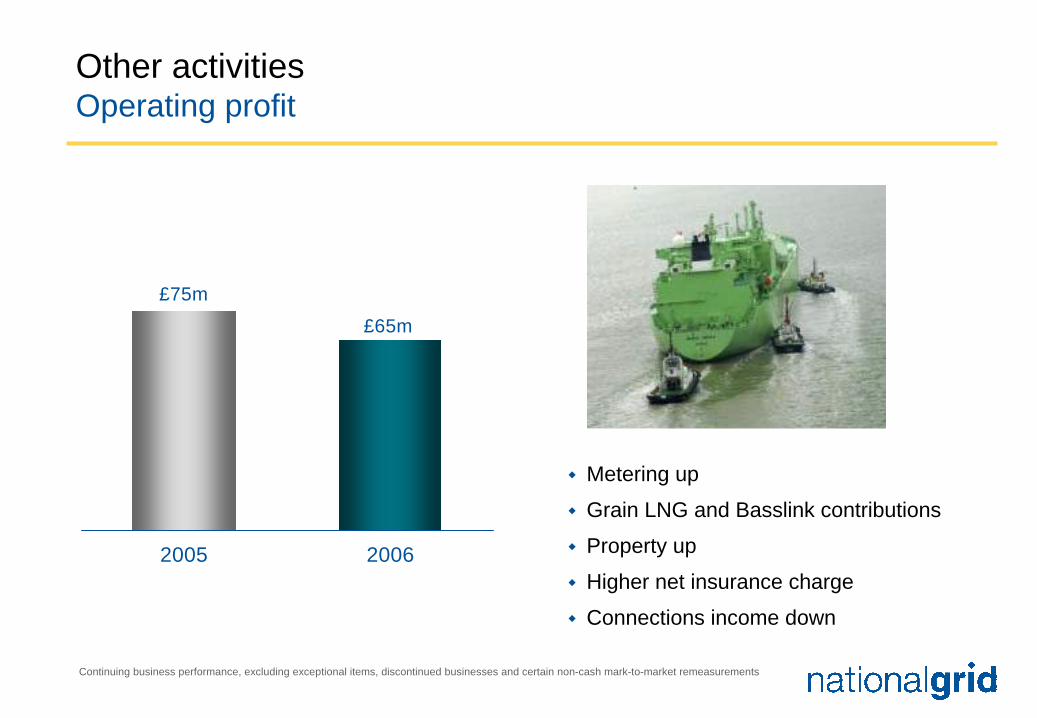

Other activitiesOperating profit

Metering up

Grain LNG and Basslink contributions

Property up

Higher net insurance charge

Connections income down

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements

£65m

£75m

2005 2006

Group Segmental operating profit

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements

4% 6%

38%

6%6%22%

18%

UK transmission US transmission

US stranded costs

UK gas distribution

Other activities

Wireless

US distribution

£1,125m£1,088m

2005 2006

Interest, tax, earnings and dividend

32%32%Effective Tax Rate*(317)(255)Net Finance Cost (actual FX)

10.2p10.9pDPS - ordinary

17.9p21.7pEPS

20052006For the 6 months ended 30 September (£m)

Note: The dividend per American Depository Share for the 6 months ending 30 September 2006 is $1.0279* Expressed as a % of profits pre-exceptional and remeasurement adjustments

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements2005 constant FX figures calculated by applying average 2006 rate ($1.86/£) to 2005 results (when average rate was $1.85/£)

£827m

£1,072m

2005 2006

Capital investment

Continuing business capital investment only* 2006 UK gas distribution includes £159m (2005 £139m) of replacement expenditure (repex)

Other activities

Wireless

US transmission

US distribution

UK gas distribution

UK transmission

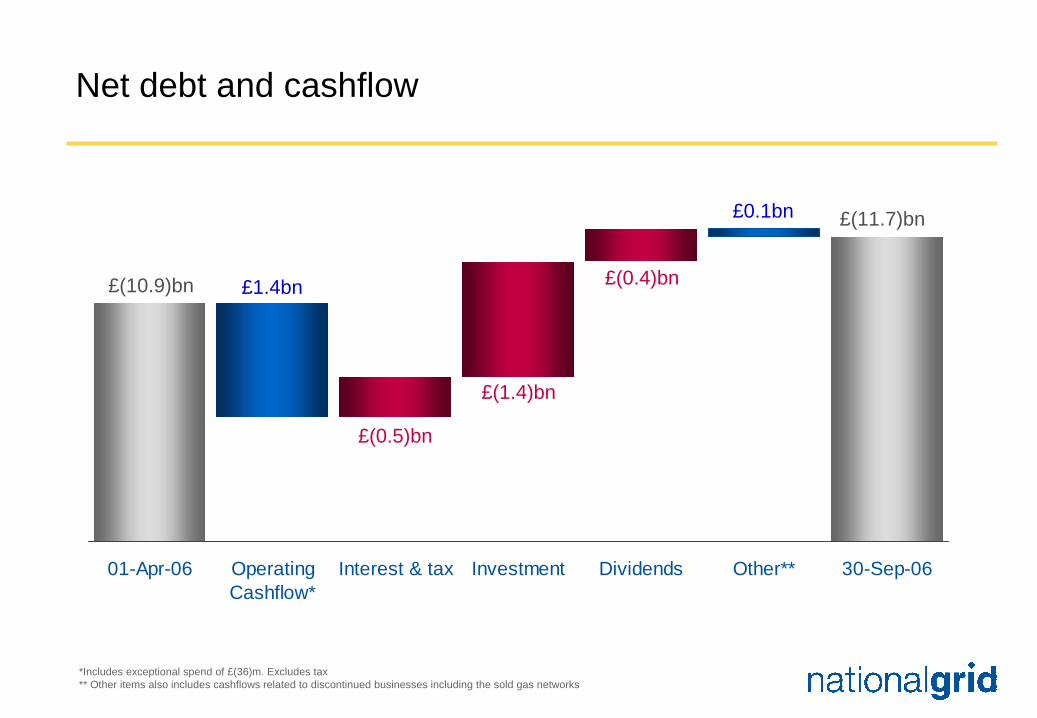

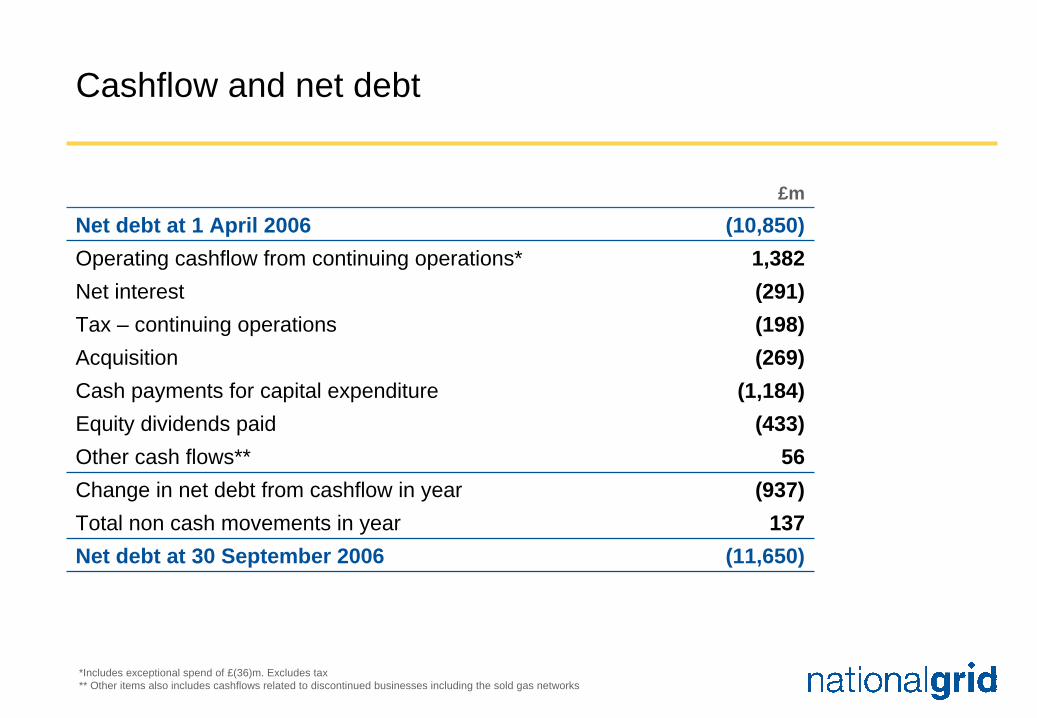

Net debt and cashflow

£(10.9)bn £1.4bn

£(0.5)bn

£(1.4)bn

£(0.4)bn

*Includes exceptional spend of £(36)m. Excludes tax ** Other items also includes cashflows related to discontinued businesses including the sold gas networks

01-Apr-06 OperatingCashflow*

Interest & tax Investment Dividends Other** 30-Sep-06

£(11.7)bn£0.1bn

Financial summary

Good first half

EPS up 21%

Interim dividend increased by 7%

Investment up 30%

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements2005 constant FX figures calculated by applying average 2006 rate ($1.86/£) to 2005 results (when average rate was $1.85/£)

Steve Holliday

Chief Executive Officer Designate

My priorities…

Strategy and growth

Driving performance

Senior management

Improving relationships

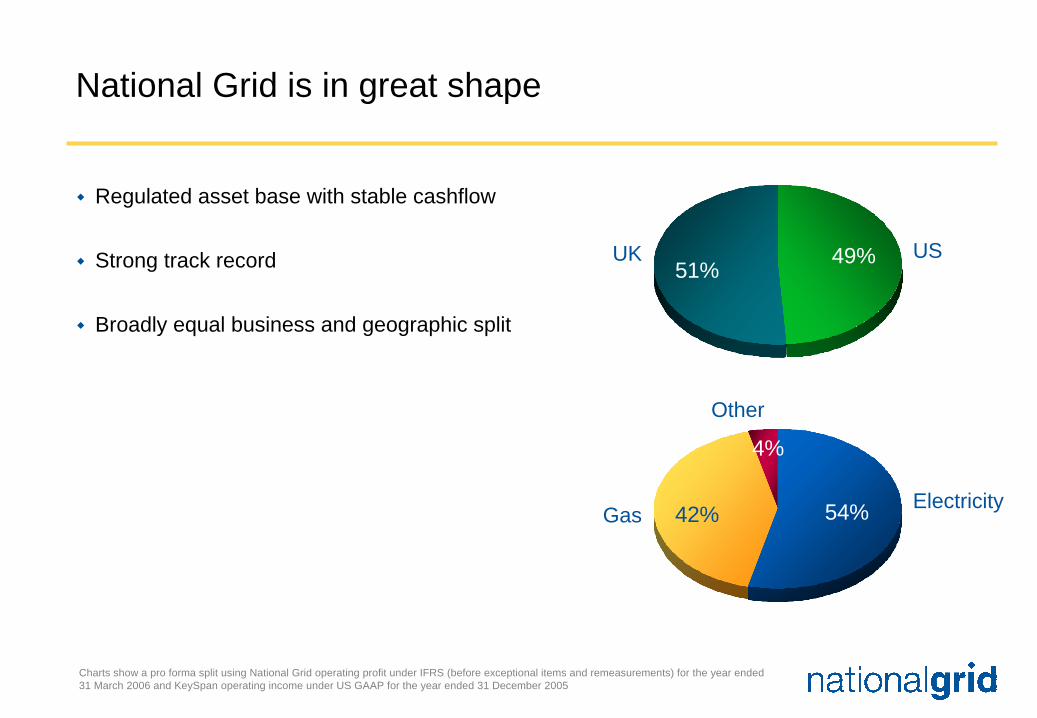

National Grid is in great shape

Regulated asset base with stable cashflow

Strong track record

Broadly equal business and geographic split

Charts show a pro forma split using National Grid operating profit under IFRS (before exceptional items and remeasurements) for the year ended 31 March 2006 and KeySpan operating income under US GAAP for the year ended 31 December 2005

54%42%

4%

ElectricityGas

Other

USUK 49%51%

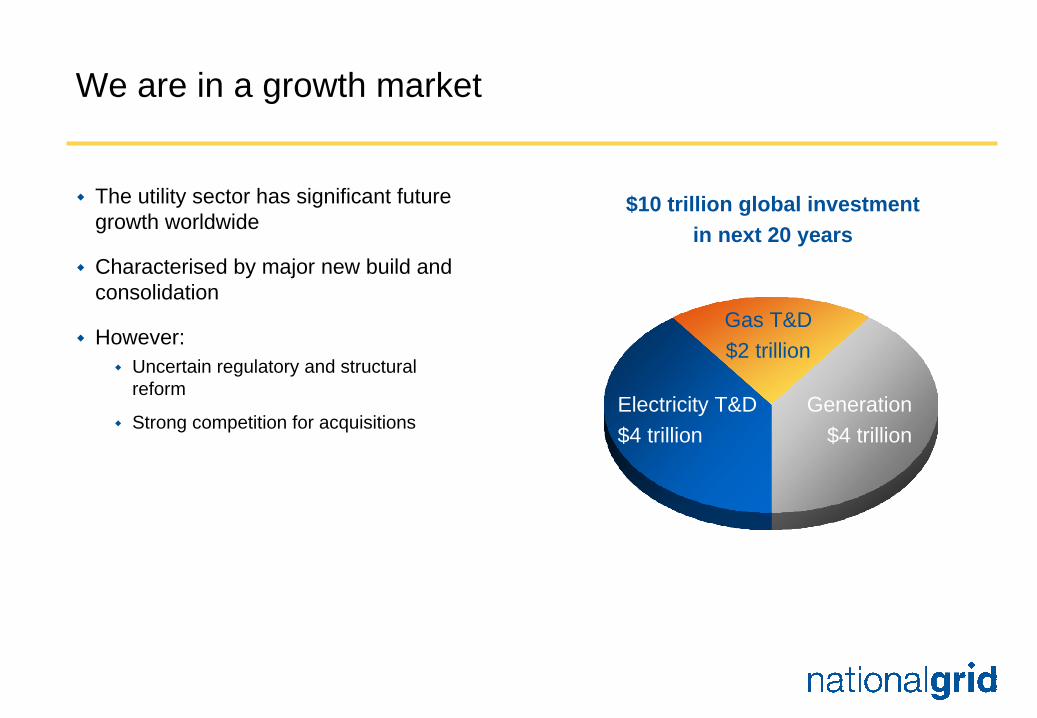

We are in a growth market

$10 trillion global investment in next 20 years

The utility sector has significant future growth worldwide

Characterised by major new build and consolidation

However:Uncertain regulatory and structural reform

Strong competition for acquisitionsElectricity T&D$4 trillion

Generation$4 trillion

Gas T&D$2 trillion

Strategy guided by 4 key factors

Strategy

Mar

ket T

rend

s

& Opp

ortu

nities

Competitive

Position

Capita

l Mar

ket

View

sValue

Drivers

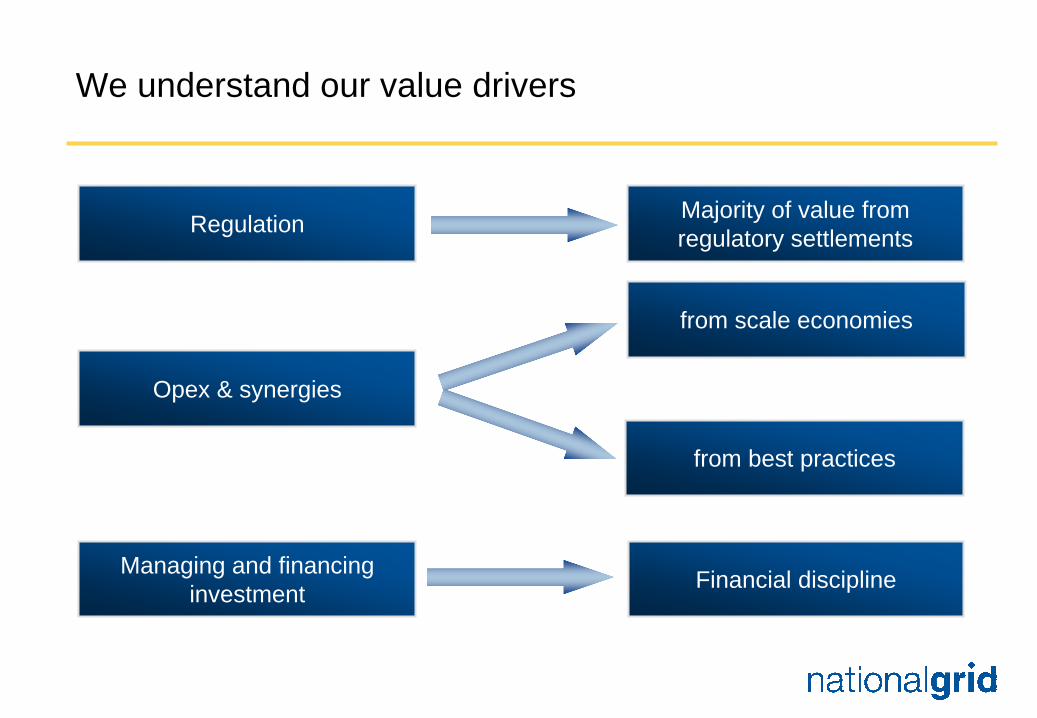

We understand our value drivers

Regulation

Opex & synergies

from best practices

from scale economies

Managing and financing investment

Majority of value from regulatory settlements

Financial discipline

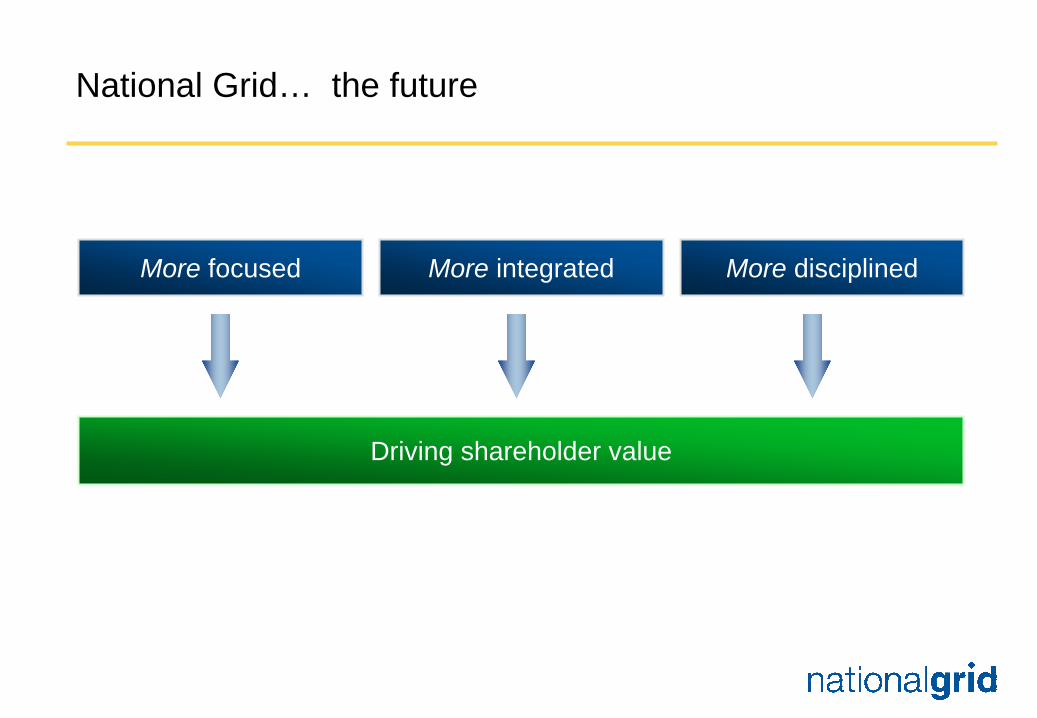

National Grid… the future

More focused More integrated More disciplined

Driving shareholder value

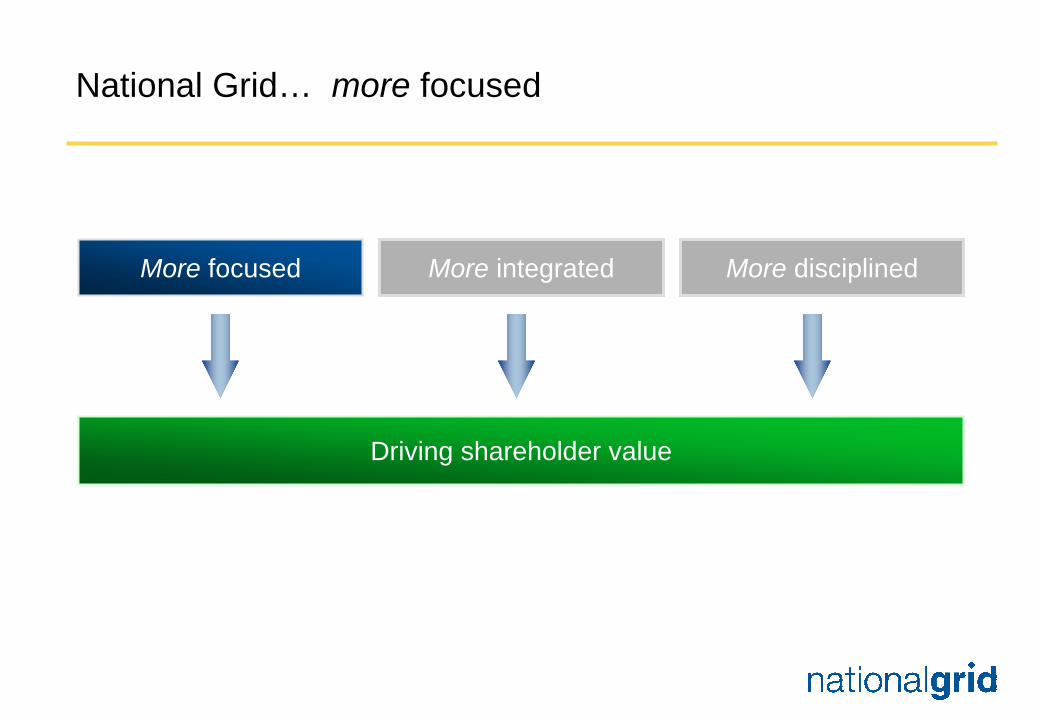

National Grid… more focused

More focused More integrated More disciplined

Driving shareholder value

More focused – a clear business model

Gas and electricity(including low-risk

generation)

Focus on prioritymarkets in the

UK and US

Own and operateasset-intensive

businesses

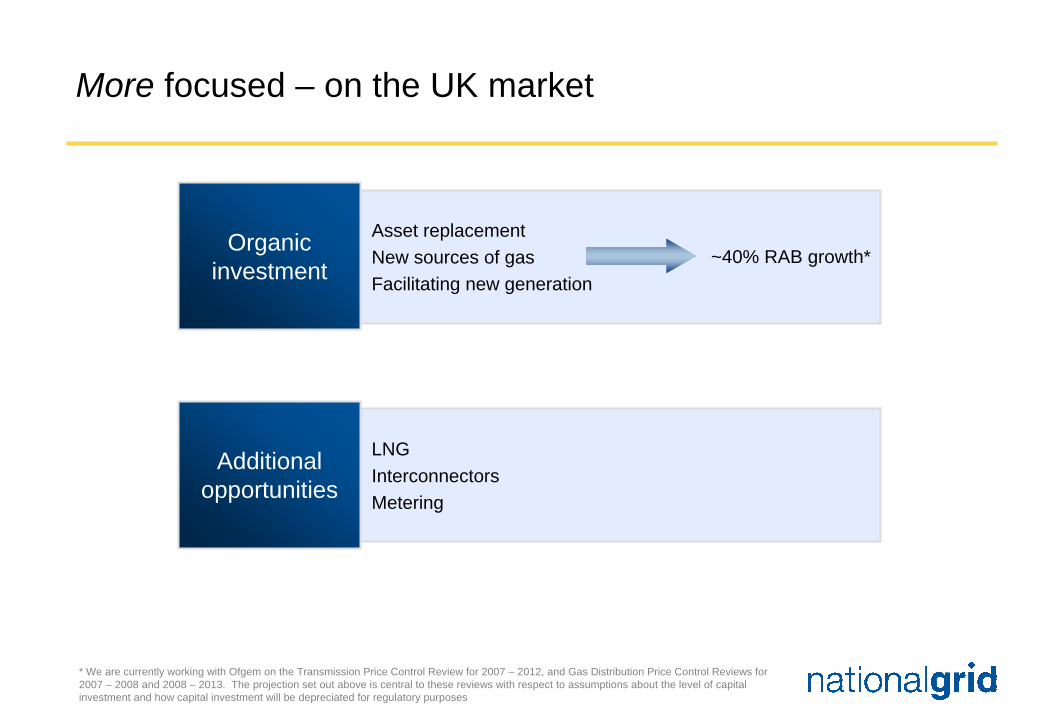

Asset replacementNew sources of gasFacilitating new generation

More focused – on the UK market

LNGInterconnectorsMetering

Organic investment

Additional opportunities

* We are currently working with Ofgem on the Transmission Price Control Review for 2007 – 2012, and Gas Distribution Price Control Reviews for 2007 – 2008 and 2008 – 2013. The projection set out above is central to these reviews with respect to assumptions about the level of capital investment and how capital investment will be depreciated for regulatory purposes

~40% RAB growth*

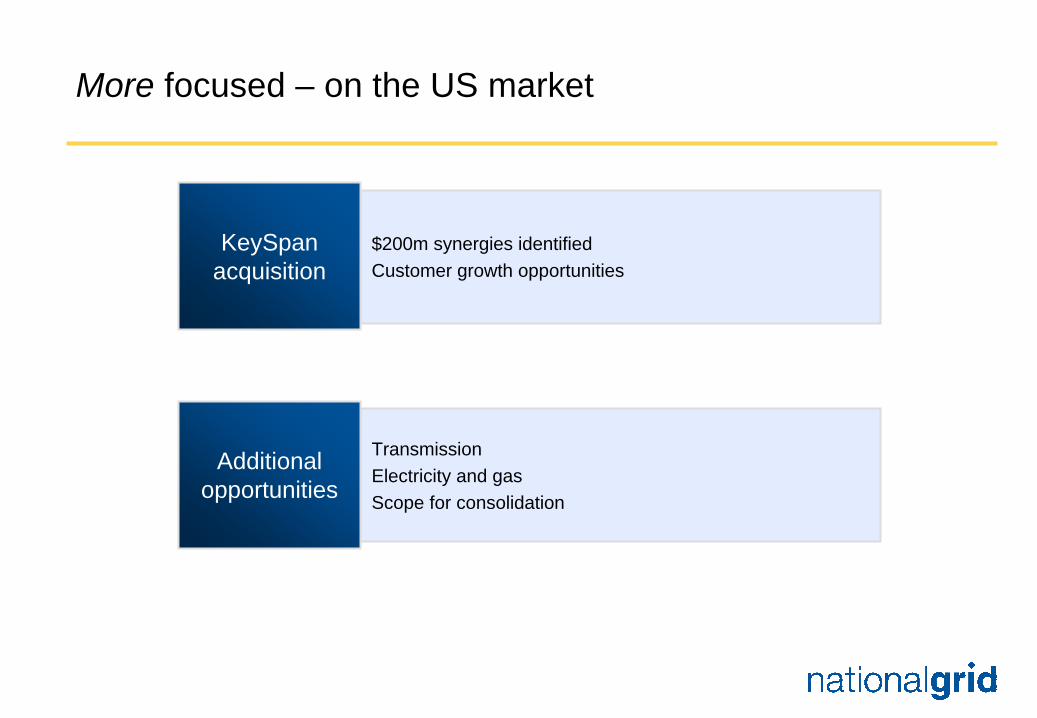

More focused – on the US market

$200m synergies identifiedCustomer growth opportunities

TransmissionElectricity and gasScope for consolidation

KeySpanacquisition

Additional opportunities

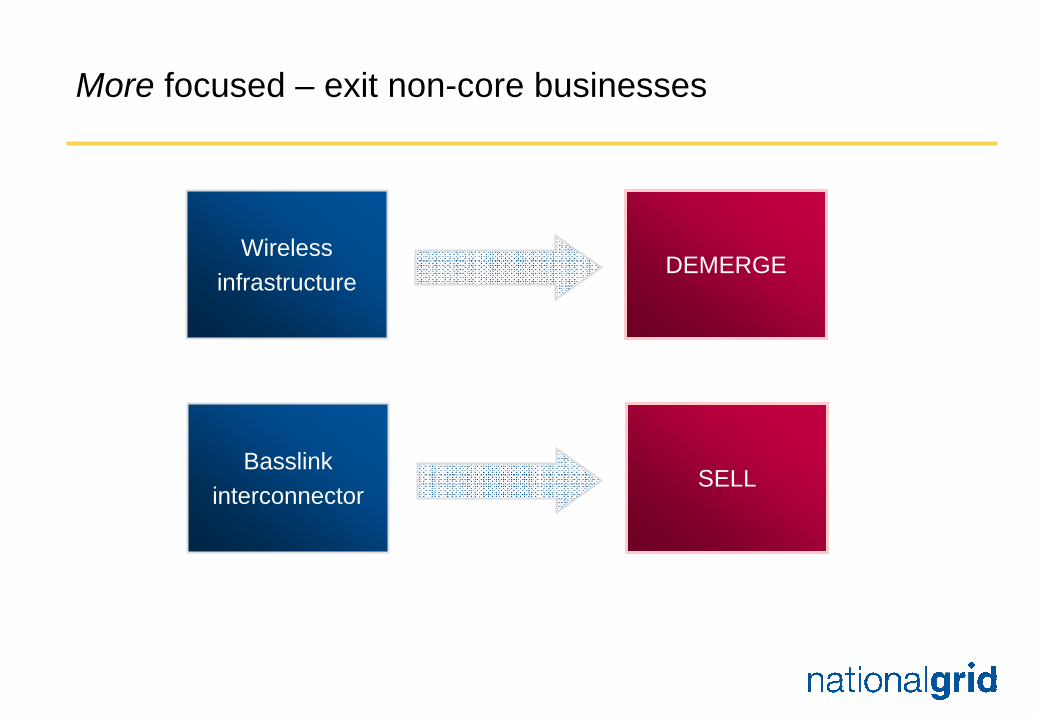

More focused – exit non-core businesses

Wirelessinfrastructure

DEMERGE

Basslinkinterconnector

SELL

National Grid… more integrated

More focused More integrated More disciplined

Driving shareholder value

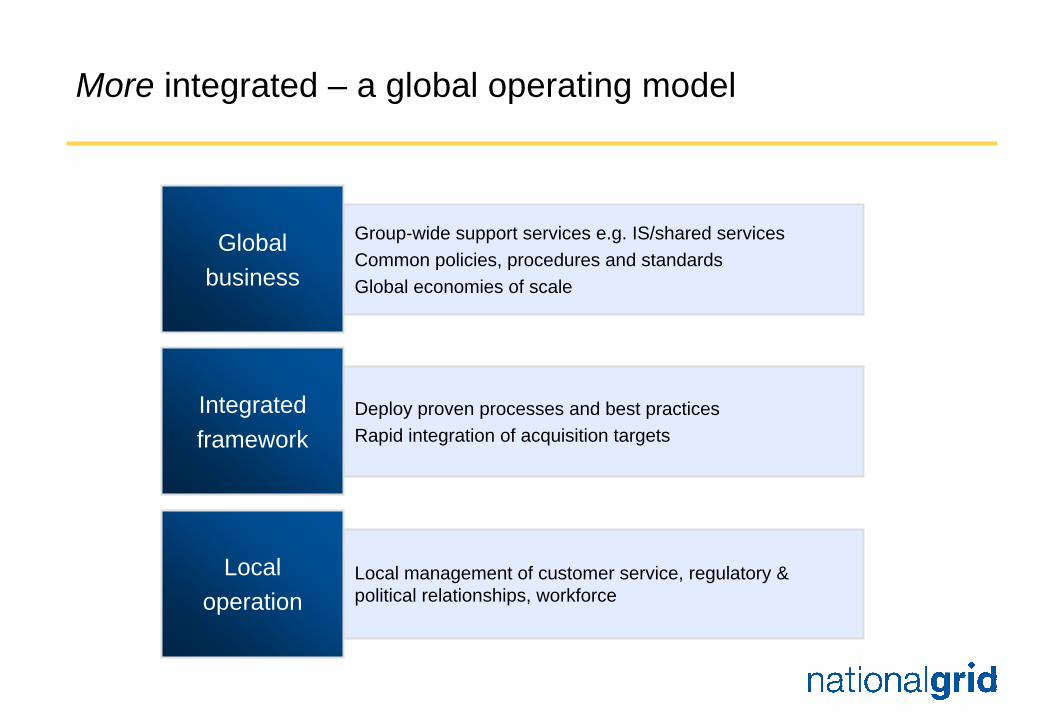

More integrated – a global operating model

Group-wide support services e.g. IS/shared servicesCommon policies, procedures and standardsGlobal economies of scale

Deploy proven processes and best practices Rapid integration of acquisition targets

Local management of customer service, regulatory & political relationships, workforce

Globalbusiness

Integratedframework

Localoperation

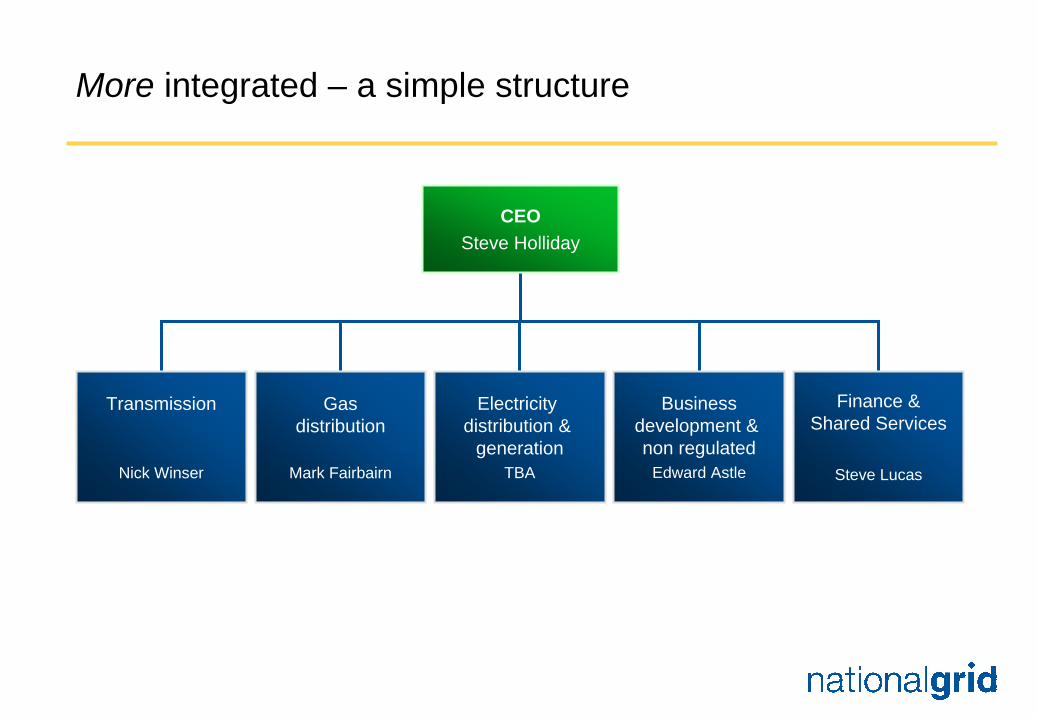

More integrated – a simple structure

Transmission

Nick Winser

Gasdistribution

Mark Fairbairn

Electricity distribution &

generationTBA

Finance &Shared Services

Steve Lucas

CEOSteve Holliday

Businessdevelopment & non regulated

Edward Astle

National Grid… more disciplined

More focused More integrated More disciplined

Driving shareholder value

More disciplined – balance sheet and dividend

Maintain efficient balance sheet followingthe KeySpan acquisition

Return surplus cash to shareholders

Balance Sheet

7% annual increase targeted through to March 2008

Return US stranded asset cash via a share buy-back

Dividend

National Grid… the future

Focus on principal growth markets in the UK and US

Demerge Wireless infrastructure

Sell Basslink

More focused

Global operating modelDriving efficiencies

KeySpan acquisition and integration

Simple organisation structure

More integrated

Maintain efficientbalance sheet

Return cash

More disciplined

Driving shareholder value

Appendix

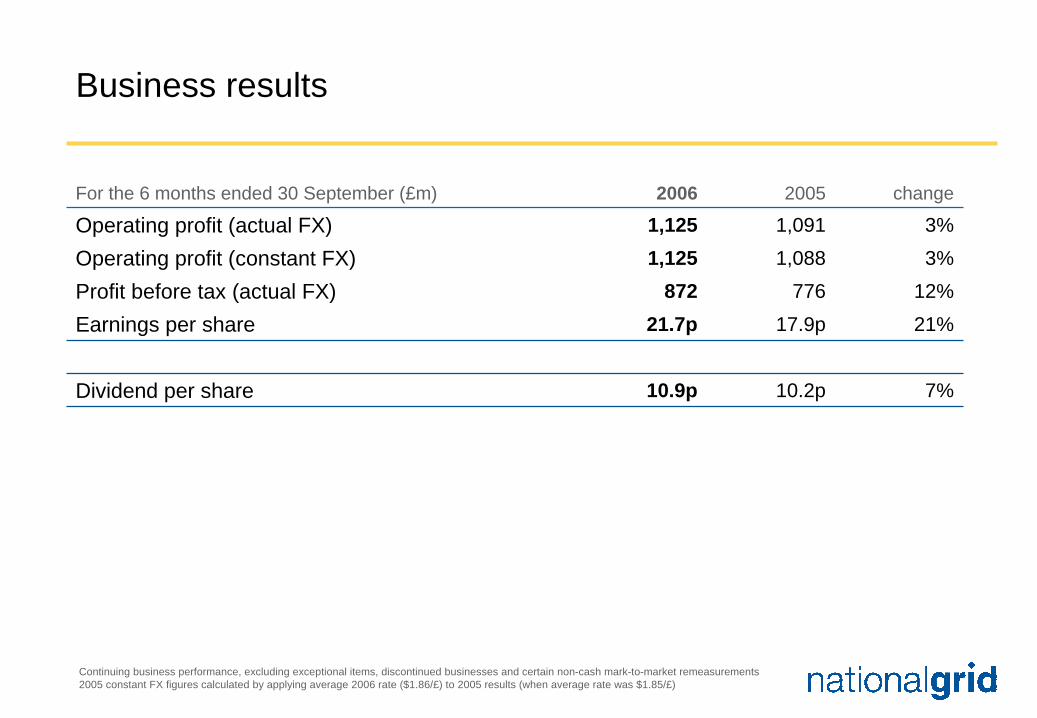

Business results

10.9p

21.7p872

1,1251,1252006

7%10.2pDividend per share

21%17.9pEarnings per share12%776Profit before tax (actual FX)3%1,088Operating profit (constant FX) 3%1,091Operating profit (actual FX)

change2005For the 6 months ended 30 September (£m)

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements2005 constant FX figures calculated by applying average 2006 rate ($1.86/£) to 2005 results (when average rate was $1.85/£)

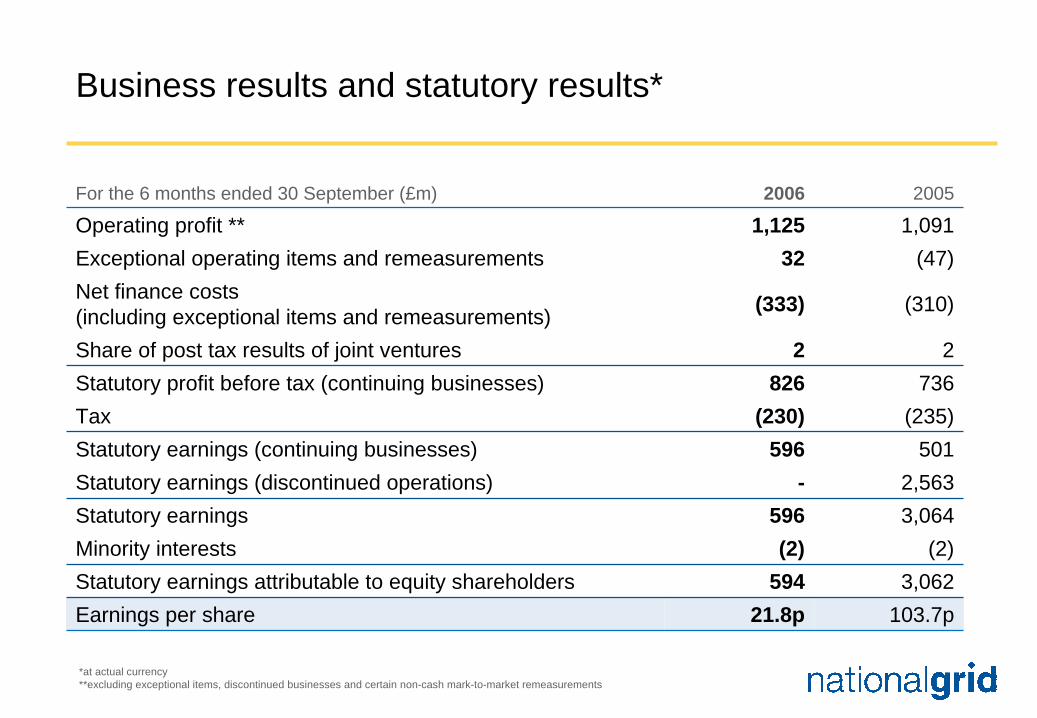

Business results and statutory results*

(47)32Exceptional operating items and remeasurements1,0911,125Operating profit **

501596Statutory earnings (continuing businesses)(235)(230)Tax

736826Statutory profit before tax (continuing businesses)22Share of post tax results of joint ventures

(310)(333)Net finance costs (including exceptional items and remeasurements)

103.7p21.8pEarnings per share3,062594Statutory earnings attributable to equity shareholders

(2)(2)Minority interests3,064596Statutory earnings2,563-Statutory earnings (discontinued operations)

20052006For the 6 months ended 30 September (£m)

*at actual currency**excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements

UK electricity and gas transmissionOperating profit

2326Electricity System Operator252270Electricity Transmission Owner*

1-Other gas1825Gas System Operator6752Gas Transmission Owner

275298Sub total – UK electricity transmission-2Other electricity

397427Total – UK electricity & gas transmission3652Sub total – other1923LNG1729Interconnectors8677Sub total – UK gas transmission

20052006For the 6 months ended 30 September (£m)

Continuing business performance, excluding exceptional items, and certain non-cash mark-to-market remeasurements* Includes the Scottish Interconnector

UK electricity and gas transmissionPrincipal operating profit movements

2005 ETO PriceIncrease

FrenchInterconnector

GTO Workload Other 2006

£427m

£397m

£47m£12m

£(20)m£(11)m

£2m

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements

UK gas distributionOperating profit

(149)(159)Operating costs*378376Formula income

9471Total - Operating profit(55)(62)Other**(80)(84)Depreciation and amortisation

20052006For the 6 months ended 30 September (£m)

* excludes pass-through costs and shrinkage gas commodity costs** Includes rates, licence fee, release of deferred capital contributions, shrinkage gas commodity costs, operating profit from xoserve and other

operating income

UK gas distributionPrincipal operating profit movements

2005 Price Increase Weather &Volumes

Non-controllableCosts

Other 2006

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements

£71m

£94m£(19)m

£(20)m

£17m

£(1)m

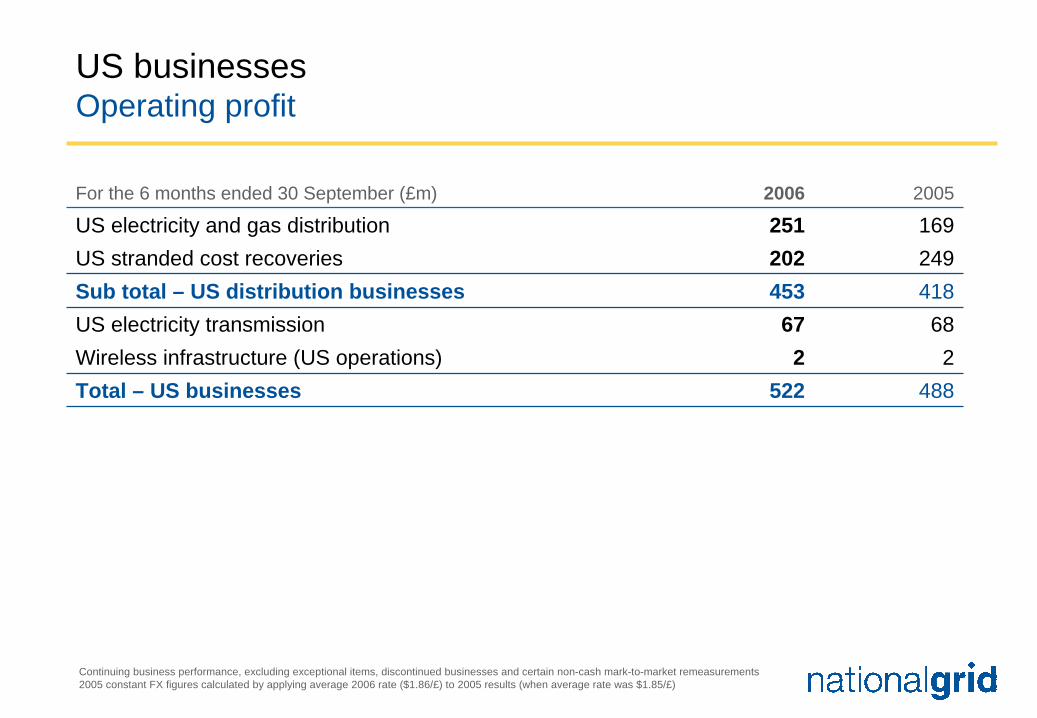

US businessesOperating profit

418453Sub total – US distribution businesses249202US stranded cost recoveries

6867US electricity transmission

169251US electricity and gas distribution

488522Total – US businesses22Wireless infrastructure (US operations)

20052006For the 6 months ended 30 September (£m)

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements2005 constant FX figures calculated by applying average 2006 rate ($1.86/£) to 2005 results (when average rate was $1.85/£)

US electricity and gas distributionPrincipal operating profit movements

2005 Deferral Account Timing onrecoveries

Other 2006

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements2005 constant FX figures calculated by applying average 2006 rate ($1.86/£) to 2005 results (when average rate was $1.85/£)

£251m

£169m

£37m

£56m

£(11)m

Other activities

15Isle of Grain3132Property

-5Basslink

5254Metering

7565Total - Other activities(9)(31)Other

20052006For the 6 months ended 30 September (£m)

Continuing business performance, excluding exceptional items, discontinued businesses and certain non-cash mark-to-market remeasurements

Cashflow and net debt

(10,850)Net debt at 1 April 20061,382Operating cashflow from continuing operations*(291)Net interest(198)Tax – continuing operations(269)Acquisition

(1,184)Cash payments for capital expenditure(433)Equity dividends paid

56Other cash flows**(937)Change in net debt from cashflow in year

137Total non cash movements in year(11,650)Net debt at 30 September 2006

£m

*Includes exceptional spend of £(36)m. Excludes tax ** Other items also includes cashflows related to discontinued businesses including the sold gas networks

Operating cashflow

1,125Operating profit *460Depreciation and amortisation

(203)Working capital and other1,382Operating cashflow **

For the 6 months ended 30 September (£m)

* Excluding exceptional items and certain non-cash mark-to-market remeasurements** Includes exceptional spend of £(36)m. Excludes tax

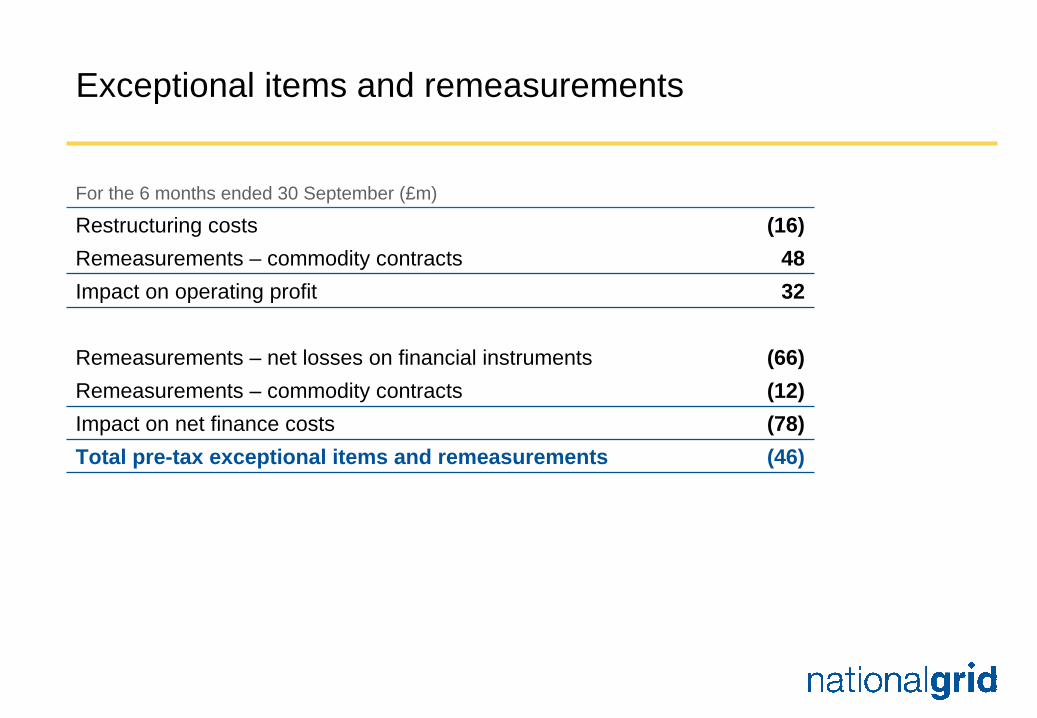

Exceptional items and remeasurements

32Impact on operating profit48Remeasurements – commodity contracts

(16)Restructuring costs

(12)Remeasurements – commodity contracts(66)Remeasurements – net losses on financial instruments

(78)Impact on net finance costs(46)Total pre-tax exceptional items and remeasurements

For the 6 months ended 30 September (£m)

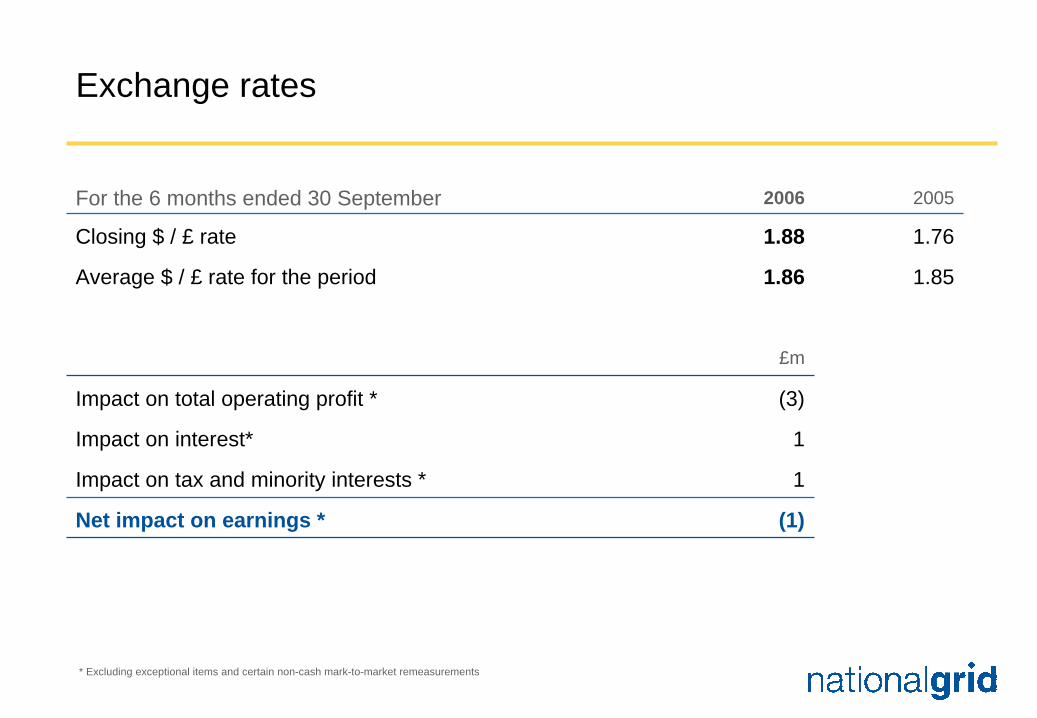

Exchange rates

(1)Net impact on earnings *

1Impact on tax and minority interests *

1Impact on interest*

(3)Impact on total operating profit *

£m

1.851.86Average $ / £ rate for the period

1.761.88Closing $ / £ rate

20052006For the 6 months ended 30 September

* Excluding exceptional items and certain non-cash mark-to-market remeasurements

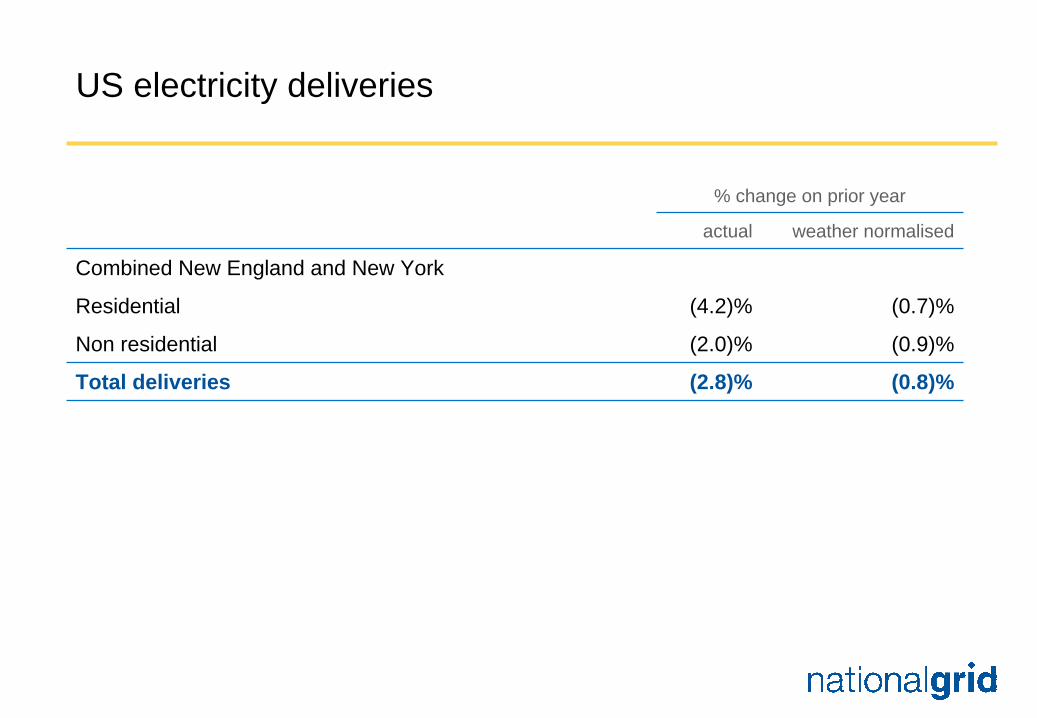

US electricity deliveries

(0.8)%(2.8)%Total deliveries

(0.9)%(2.0)%Non residential

(0.7)%(4.2)%Residential

Combined New England and New York

weather normalisedactual

% change on prior year

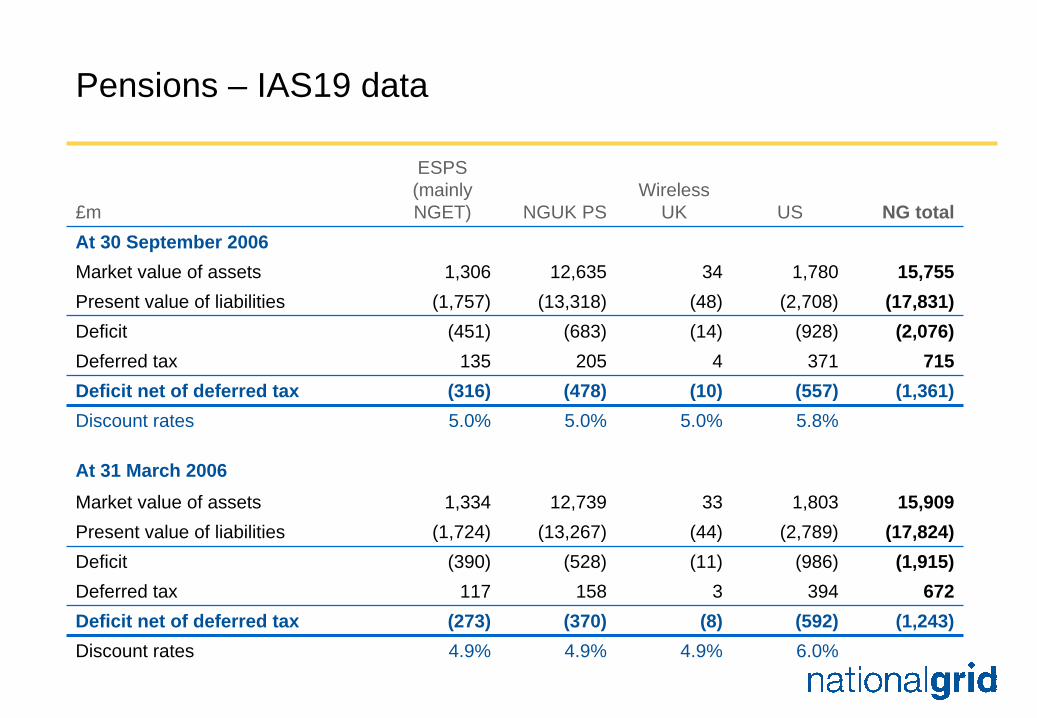

Pensions – IAS19 data

6.0%4.9%4.9%4.9%Discount rates(1,243)(592)(8)(370)(273)Deficit net of deferred tax

6723943158117Deferred tax(1,915)(986)(11)(528)(390)Deficit

(17,824)(2,789)(44)(13,267)(1,724)Present value of liabilities15,9091,8033312,7391,334Market value of assets

At 31 March 2006

5.8%5.0%5.0%5.0%Discount rates(1,361)(557)(10)(478)(316)Deficit net of deferred tax

7153714205135Deferred tax(2,076)(928)(14)(683)(451)Deficit

(17,831)(2,708)(48)(13,318)(1,757)Present value of liabilities15,7551,7803412,6351,306Market value of assets

At 30 September 2006NG totalUS

Wireless UKNGUK PS

ESPS (mainly NGET)£m

Top Related