Zelaya Family Vision Board Party 2014

30

FIRST ANNUAL VISION BOARD PARTY STARTING THE NEW YEAR RIGHT Presented by the Zelaya Family on 12/31/13

-

Upload

jeff-zelaya -

Category

Self Improvement

-

view

139 -

download

0

Transcript of Zelaya Family Vision Board Party 2014

FIRST ANNUAL VISION BOARD PARTY

STARTING THE NEW YEAR RIGHT

Presented by the Zelaya Family on 12/31/13

We were BROKE and sick and tired of it

Poor People Rich People

No Vision

Lack Goals

Low Financial Literacy

No Financial Discipline

Lack Total Work Ethic

Have Vision

Set SMART Goals

Financial Know How

Financial Discipline

Work Hard & Smart

Work with Purpose

What’s The Difference

In 2005 We Ranked in the Bottom 34% of Income Earners

In 2013 we moved to the Top 10%

1 ) C A S T A V I S I O N F O R O U R L I F E

2 ) W R O T E D O W N S M A R T G O A L S

3 ) I M P R O V E D O U R W O R K E T H I C

4 ) G A I N E D F I N A N C I A L K N O W L E D G E

5 ) C R E A T E D A B U D G E T ( A N D S T U C K T O I T )

6 ) T O O K A C T I O N

7 ) P E R I O D I C A L L Y R E V I E W E D P R O G R E S S

This is HOW we did it

Zelaya Family 12/31/2012

Creating our Vision Boards and writing down our 2013 goals.

As of 12/31/2013 many of those goals that were written down were accomplished.

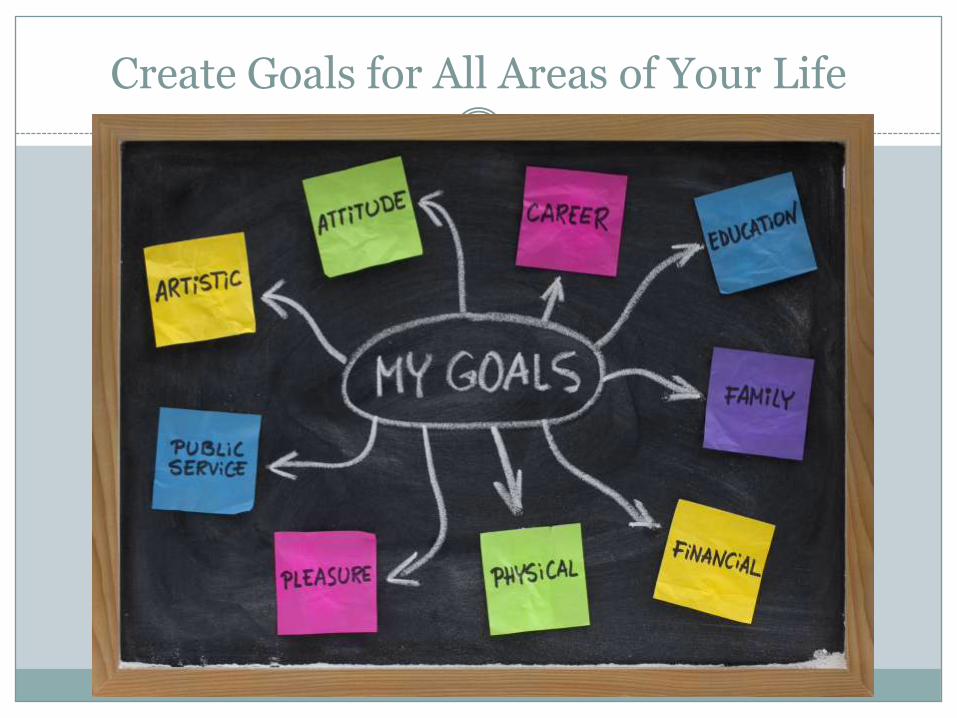

Create Goals for All Areas of Your Life

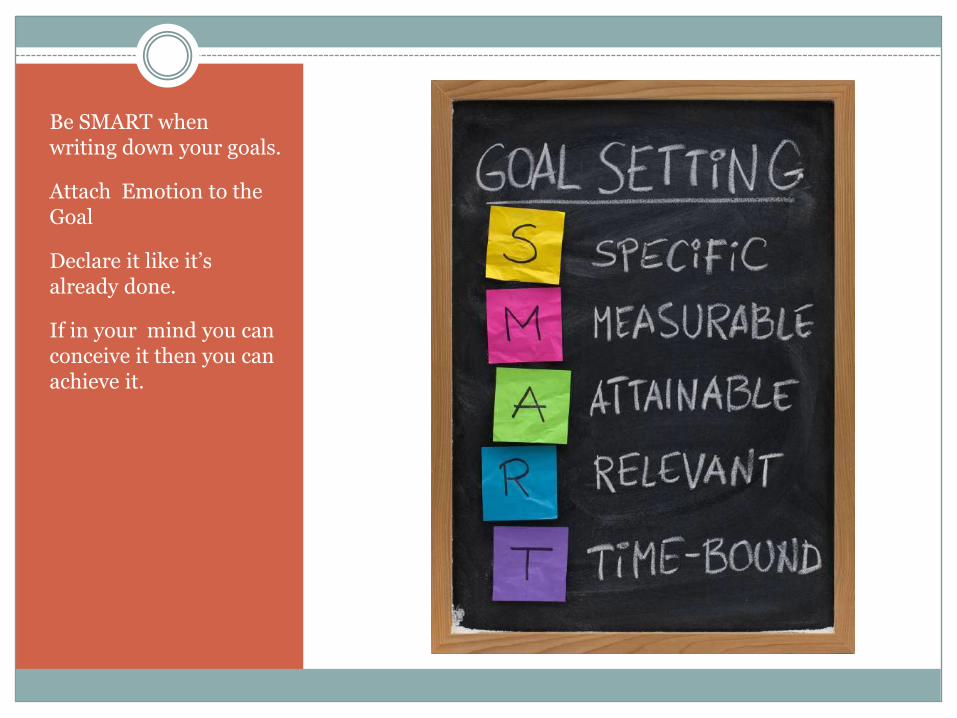

Be SMART when writing down your goals.

Attach Emotion to the Goal

Declare it like it’s already done.

If in your mind you can conceive it then you can achieve it.

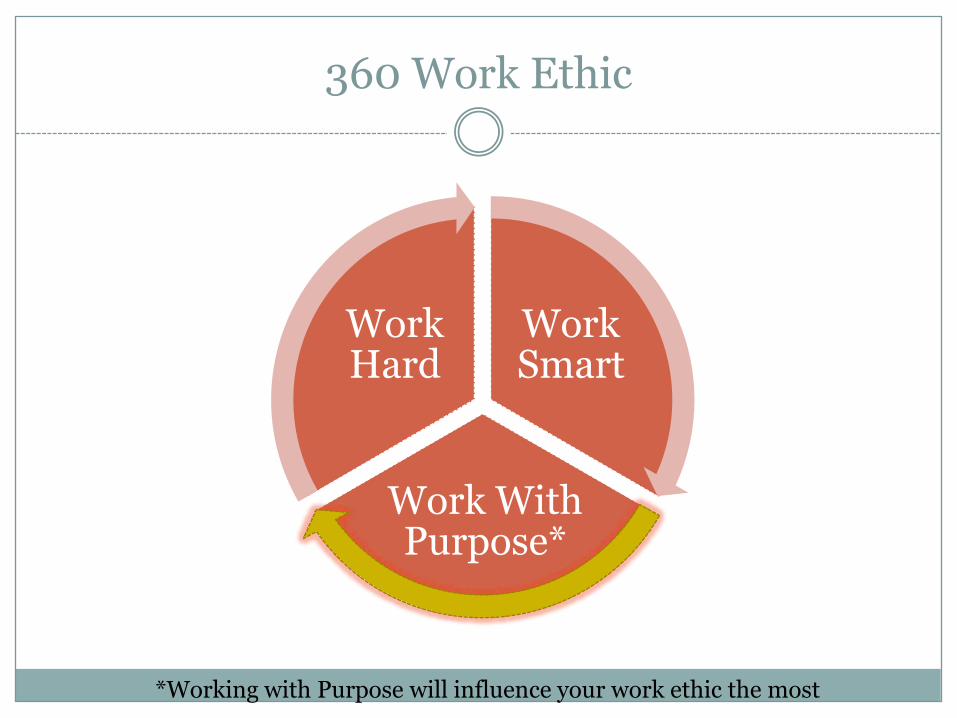

WORK HARD

WORK SMART

WORK WITH PURPOSE

360▫Work Ethic

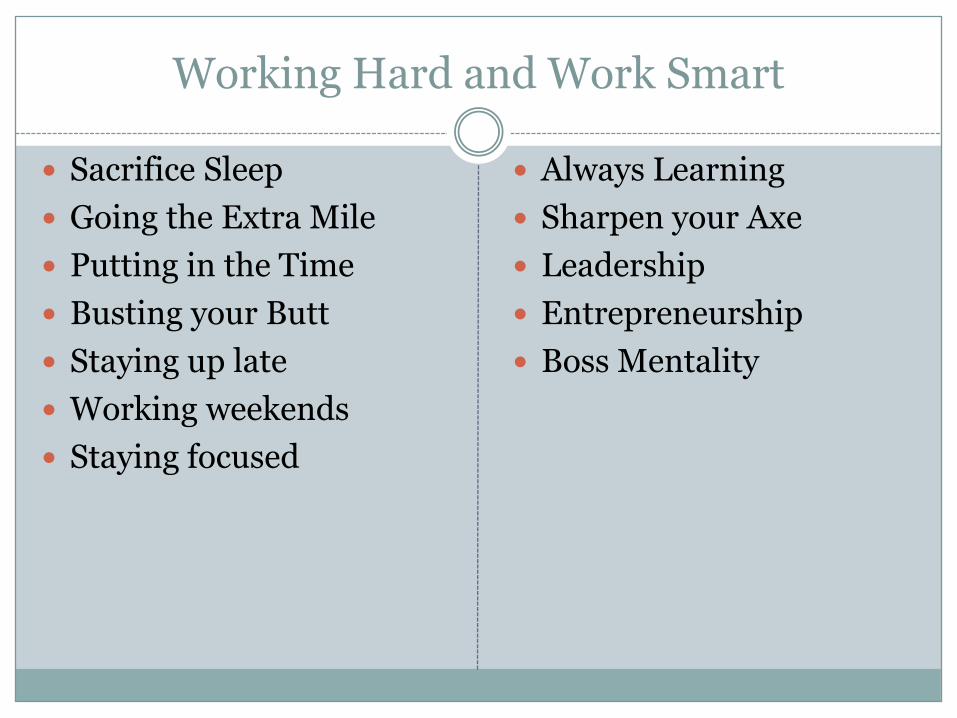

Working Hard and Work Smart

Sacrifice Sleep

Going the Extra Mile

Putting in the Time

Busting your Butt

Staying up late

Working weekends

Staying focused

Always Learning

Sharpen your Axe

Leadership

Entrepreneurship

Boss Mentality

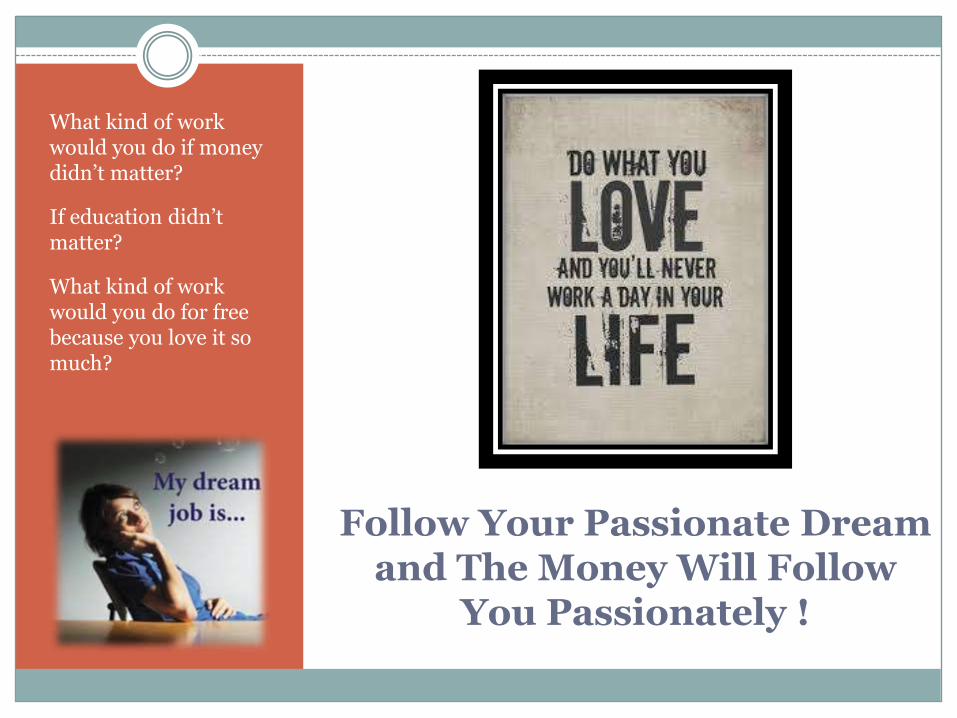

Follow Your Passionate Dream and The Money Will Follow

You Passionately !

What kind of work would you do if money didn’t matter?

If education didn’t matter?

What kind of work would you do for free because you love it so much?

360 Work Ethic

Work Smart

Work With Purpose*

Work Hard

*Working with Purpose will influence your work ethic the most

DEPENDS ON

LITERACY

&

DISCIPLINE

Your Financial Growth

FINANCIAL LITERACY

SAVING – the amount left over after personal expenses have been met

BUDGETING – summary of estimated expenditures for a given period along with the projected cash flow for financing them

FINANCIAL DISCIPLINE – determines success and the probability of achieving our goals

SAVING

One size doesn’t fit all

Gross Income vs. Net Income

Making your paycheck work for you

Tithe thyself (direct deposit)

“Take home income”

Net Income

- Tithe____

SAVING (Cont’d)

Make it a Habit

Set up bank accounts with purposes

High yield savings account (“best cash cow” bank rate, etc.)

Diversify

Where should I start

SAVINGS (Cont’d)

Go Offshore

Minimize ATM withdraw

Don’t Borrow against self

Track Spending

Debit Card vs. Credit Card

Long term vs. short term goals

BUDGETING

Identifying how you’re spending money (Elizabeth Formula)

Evaluate your spending

Track your spending

IDENTIFY

3 main category of budgetingEssential expensesFinancial prioritiesLifestyle choices

50/20/30 Rule of Budgeting Essential expenses – 50% (shelter, food, electricity) Financial Priorities – 20% (retirement, savings, debt

payments) Lifestyle choices – 30% (cable, internet, phone plans,

childcare, gym, shopping etc.) FORECAST Cash Flow??

50/20/30 Rule Example

Shelly has net income of $1400 below are her expenses

(Remember net income is net income less taxes)

Essential expenses 50%

Rent - $450

Grocery – $120

Insurance - $60

Transportation - $60

690/1400 = 49%

50/20/30 Rule Example

Financial Priorities 20%

Savings - $140

Student Loan - $60

Emergency Fund - $50

Church Tithes - $50

300/1400 = 21%

Lifestyle Choices 30%

Cable - $80

Cell Phone - $120

Restaurant - $100

Vacation - $ 75

375/1400 = 27%

EVALUATE

Are you meeting your financial objectives

Are your financial objective realistic

Do I really need to spend my money on “THAT” –eliminating discretionary spending

2 to 3 Revision

TRACK

Bank Account in system or download

Software (i.e. Quicken)

Mint.com

Excel

Actual vs. Forecast

Revision

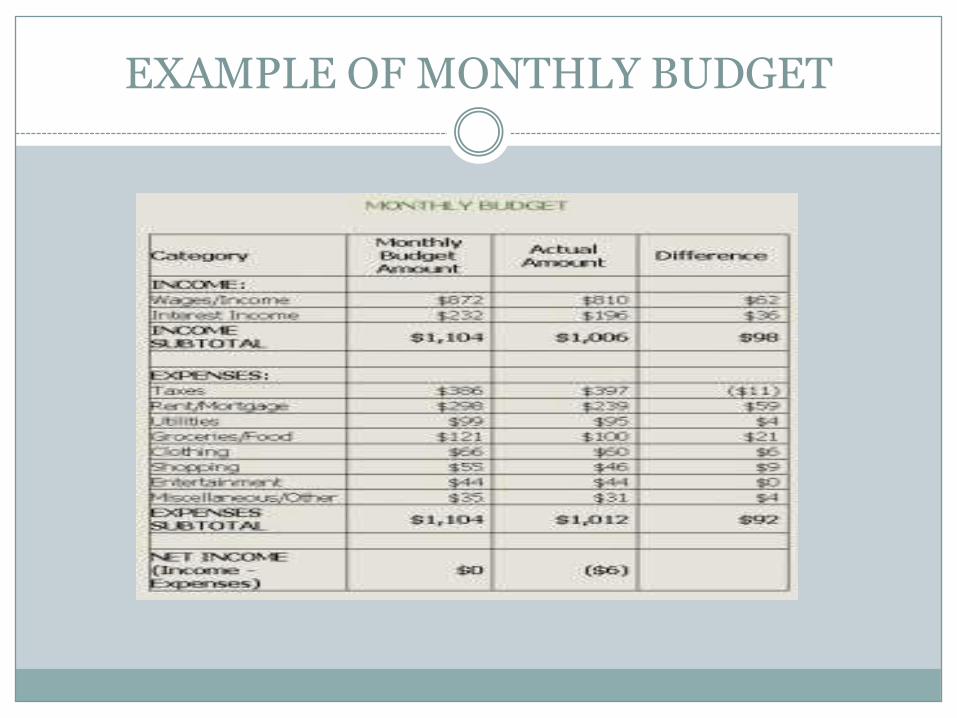

EXAMPLE OF MONTHLY BUDGET

FINANCIAL DISCIPLINE

Budget/Saving main two elements of financial discipline

SMART financial planning ( yearly, quarterly, monthly, weekly)

Set a long term vision (ex. Financial freedom 2025)

Financial Planning course

Concept of Inflation

Keeping up with the Joneses

Make transfers inconvenient

Take advantage of discounts

Don’t pay for space you don’t need (Buying a house)

Luxury items

FINANCIAL DISCIPLINE (CONT’D)

TEACH OUR CHILDREN

Your Next Steps

1) Cast a vision for your life

2) Write down SMART goals

3) Develop a 360 Work Ethic

4) Gain Financial Knowledge

5) Create a Budget

6) Take Action! Do it.

7) Periodically review progress of goals with your accountability partner

Congratulations! You’re on your way to Financial Independence