World Bank Documentdocuments.worldbank.org/curated/en/775781468768302910/pdf/multi... ·...

51

Policy, Research, and External Affairs WORKING, PAPERS,- Debt and International Finance International Economics Department The World Bank July 1991 WPS 720 The Outlook for Commercial Bank Lending to Sub-Saharan Africa Ellen Johnson Sirleaf and Francis Nyirjesy Key issues in the future of long-term commercial bank lending in Africa, constraints on increased commercial bank lending there, and special initiatives for removing those constraints and stimulating lending to Sub-Saharan Africa. The Policy, Research, and Fxtemal Affairs Complex distributes PRI' Working Papers todisserunate thefitdmgs of work in progress and to encourage the exchange of ideas among Bank staff and all others interested in development issues. These papers cafry the names of the authors, inflecL only their views, and shouild he used and cited accordingly. The findings, interpretations, and conclusions are the authors' own. They should not be attributed to the World Bank, its Board of Directors, its management. or any of its member countries. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Documentdocuments.worldbank.org/curated/en/775781468768302910/pdf/multi... ·...

Policy, Research, and External Affairs

WORKING, PAPERS,-

Debt and International Finance

International Economics DepartmentThe World Bank

July 1991WPS 720

The Outlookfor CommercialBank Lending

to Sub-Saharan Africa

Ellen Johnson Sirleafand

Francis Nyirjesy

Key issues in the future of long-term commercial bank lendingin Africa, constraints on increased commercial bank lendingthere, and special initiatives for removing those constraints andstimulating lending to Sub-Saharan Africa.

The Policy, Research, and Fxtemal Affairs Complex distributes PRI' Working Papers todisserunate thefitdmgs of work in progress andto encourage the exchange of ideas among Bank staff and all others interested in development issues. These papers cafry the names ofthe authors, inflecL only their views, and shouild he used and cited accordingly. The findings, interpretations, and conclusions are theauthors' own. They should not be attributed to the World Bank, its Board of Directors, its management. or any of its member countries.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

[ Policy, Research, and External Affairs

Debt and International Finance

WPS 720

This paper- a product of thC Dcbt and International Finance Division, Intcrnational Economics Departnient -- w asprepared for the Symposium on African External Finance in thc 1990s, hield September 18-19, 1990, at the WorldBank. Copies arc available frce from the World Bank, 1818 H Street NW, Washington, DC 20433. Please conlactSheilah King-Watson, room S8-040, extension 31047 (46 pages, with tables).

Since its peak in 1980-82, medium and long-term o Scvcral steps can be taken to acceleratc debtcommercial bank lending to Sub-Saharan Africa has reduction through conversion mechanisms. Specialbecn de.lihning -- partly becausc of many banks' funds could be created for the investment of-debt, forperception that lending to the African market repre- example.sents high risks unjustified by the available returns.

- Given the small share of African debt in mostThe prospects for an appreciable increase in such banks' portfolios and the conservative posture of

lending are not promising. Despite some progress those banks, a strong case can be made to the regula-under economic a(ljustlnenl programs, banks are tory authorities to climinate mandatory provisioningskeptical about Sub-Saharan African govenmcnits' regulations as quickly as possible.ability and willingness to continuc with reform.Many of those countries have been unable to cstablish * Therc is scope tor rethinking the way risk iscreditworthincss and the ability to service commieircial allocated in facilities cofinanced by commercialdebt - and are saddled with (lebts to multilateral banks and official agencics.agencies. And in a time of tight regulation, mostbanks have ample opportunities in other parts of the - More open attitudes toward Lhe commnitmcnt ofworld. export cash flows appear to be important in accelerat-

ing resumcd lcnding, until a country has adopted anOn the positive side, the portfolio clean-up that opcn foreign exchange regimc or has achieved full

has occupied commercial banks' resources for threce convertibility. Concerns about possible distortionsyears should be nearing a close, making it possible for could best be mitigated by setting a limit on thethem to begin considering a rcsumption of lending to amount of funds that can bc so committed by a givenqualified borrowers under specified conditions. country or borrower, and by improved appraisal of the

underlying projects.Siricaf and Nyirjesy examine kcy issues in the

luturc of long-term commercial bank lending in * Commercial banks are at a disadvantage inAfrica, identify constraintis on and opportunities for analyzing or projecting a developing country'sincreased commercial bank lending (as perceived by creditworthincss and fear of the unknown can besome commercial U.S., European, and Japanese particularly acute in Sub-Saharan Africa. The in-bankers), and suggest special initiatives lor removing depth economic analyscs of the IMF and the Worldconstraints on and stimnulating lending to these Sub- Bank are the closest the international community hasSaharan African markets. Among poinits they make: come to establishing an "independent audit function."

These are not available to the public unless the- Private invesimcnt and linancing will not member government authorizes their releasc. Thcse

improve in the region without a satisfactory enabling authorizations should be routinely granted - at leastenvironment, including an appropriate policy frame- for basic, accurate, qualitative, and quantitativcwork, tho protection of rights and properties, and macrocconomic infomiation.wider political participation and consensus -

con(litions thal lead to political stability and engenderconfidence among private decisionmakers.

Thic lRE Working lPaper Series (isseminales thc findings of work under way in thc Bank's l'olicy. Res,earch, and ExtemralAffifirsComplex. An objeclive ofthc scrics is to get thcsc findings out quickly, even ifpresentutions arc Iess than fully polished.Thc findings, intcrprctations, and conclusions in thesc papcrs do not neccssarilv represent official Baunk policy.

Produced by the PRE Dissemination Ccnter

The Outlook for Commercial Bank Lendingto Sub-Saharan Africa

byEiien Johnson Sirleaf

andFrancis Nyirijesy

Table of Contents

Introduction 1

Chapter One: The Record of Commercial Bank Lending

A. Statistical Overview 3

B. Nature of Commercial Bank Lending 10

C. Foreign Commercial Bank Presences 13

Chapter Two: Perceptions of the Commercial Banks

A. Perceived Constraints 14

B. Perceived Opportunities 18

Chapter Three: Scope for Action

A. Opportunities and Commercial Borrowing Capacity 21

B. Prospects and Proposals for the Alleviation of Constraints 24

C. Potential Impact on Commercial Bank Lending 31

Statistical Annex

Page 1

In the past decade Sub-Saharan Africa has faced an unparalleled economic crisisthat has threatened to reverse the progress achieved during two earlier decadesof generally higher primary commodity prices and financial flows. In response,many countries have adopted stringent economic reform programs aimed atstabilizing the decline and putting in place the policy framework needed toachieve structural transformation and sustainable growth. A key element of these

reform programs involves a shifting of the primary responsibility forintervention in the economy from the state to private enterprises. This shiftrequires not just support from the donor community, but also the mobilizationof significantly higher levels of private financial and management resources--both domestic and foreign--to stimulate trade and investment.

Since its peak at more than $4 billion per year in disbursements between 1980-82, representing annual net flows in excess of $2.5 billion, medium and long-term commercial bank lending to Sub-Saharan Africa has been declining. Althoughthe statistics on short-term lending do not permit a quantitative analysis ofstocks and flows by type of lender, it also appears that this important form of

commercial bank credit for the region has been stagnant. The decline is due inpart to the perception by a large number of banks that lending to the Africanmarket presents high risks that are not justified by the available returns.

The prospects for a widespread, appreciable increase in commercial bank lending

in the foreseeable future do not appear promising. Despite the progress madeunder economic adjustment programs, there is still skepticism among the banksregarding the ability and willingness of Sub-Saharan African governments tocontinue with the reform measures and the likelihood that they will result ina proliferation of viable lending opportunities. Moreover, the borrowingcountries in partnership with the official agencies have been unable to restorethe creditwortniness of Sub-Saharan Africa and the abiliLy of many countries toservice commercial bank debt. At the same time, the loans of the multilateralagencies are being serviced to maintain their own ability to mobilize the bulkof Africa's external assistance. In addition, the banks are faced with a morestringent regulatory environment as regards lending to Sub-Saharan Africa at a

time when there are emerging opportunities in other regions of the world.

On the positive side, the portfolio "clean-up" that has employed commercialbanks' resources for the past three years should be near4ng a close, making it

possible for them to begin to consider a resumption o. lending to qualifyingborrowers under specified conditions, primarily in successfully adjustingcountries that can foresee an end to their economic and debt crises. Lendingis likely to encompass innovative new banking products that engage banks,

borrowers and official agencies in joint partnership arrangements, as well as

traditional but more properly targeted and structured transactions.

The purpose of this paper is to identify and examine key issues involved in thefuture of long-term commercial bank lending to Africa. Chapter One and the

Statistical Annex present the historical record and briefly review the nature

Page 2

of commercial bank lending and the changing profile of foreign commercial bank

presences in the region.

Chapter Two examines the constraints to and opportunities for increased

commercial bank lending as perceived by a representative sampling of commercialbanks in the United States, Europe and Japan, whose contribution to the study

is gratefully acknowledged.

Chapter Three presents a scope for action, a pulling together of ideas that couldhelp remove constraints to lending to a select number of Sub-Saharan African

markets in the short term, with a view to stimulation of lending to the entire

region in the long-term.

Page 3

GHARXER ONE THE RECORD OF CO?hRCIAL BANK LENDING

Commercial bank lending to Sub-Saharan Africa over the past thirty years reflectsto a large extent the changes in economic performance in various countries andthe vagaries in external conditions that affected this performance or providedunusual opportunities for business.

In the period 1960-1970, when commodity prices were strong and per capita incomeswere rapidly rising, commercial bank lending was negligible. Between 1970 andthe early 1980s, due to strong fluctuations in commodity prices and the need forpetrodollar recycling, commercial lending increased exponentially; from less thanihalf a billion dollars in 1970 to a stock of $13 billion in long-term loans, onthe strength of annual net flows peaking at nearly $3 billion in 1980. Sincethat time the level of stocks and flows has moved in response to a combinationof factors, including new lending as a function of the perceived creditworthinessof individual borrowing countries or entities and the viability of particularforms of security for loans; the effect of a depreciated U.S. dollar on the valueof debt stocks; the volume of debt reschedulings and debt service performance;and the development of activity in the secondary debt markets.

A. STATISTICAL OVERVIEU

Unless otherwise stated, the data presented in the Statistical Annex anddiscussed below are drawn from the World Bank Debt Tables (WDTs). The aggregatestatistics for the past few years are considerably overstated, since C6ted'Ivoire's private sector is shown to have received some $900 million per yearin commercial bank medium-term loan disbursements in 1985-88, a significantportion of all new lending to the region. Since this statistic represents 10percent of C6te d'Ivoire's GNP, it bears little relation to actual lendingactivities and must be heavily discounted.

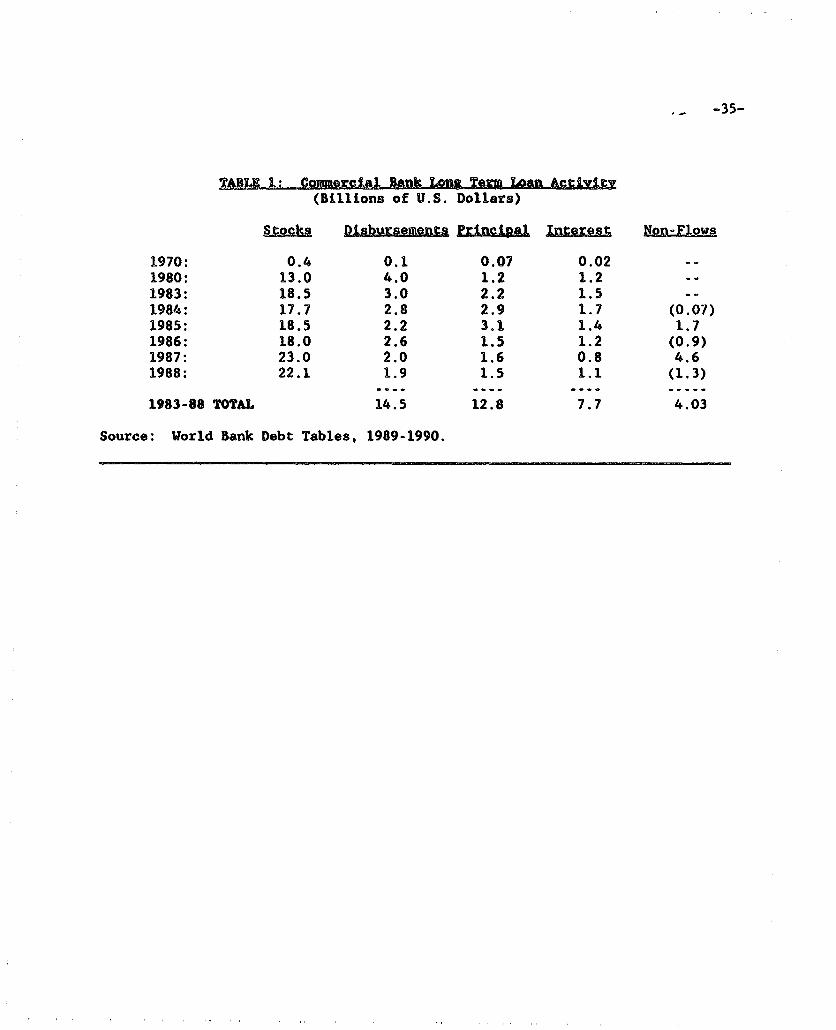

Table 1 summarizes the WDTs' estimates of aggregate commercial bank long-termloan activity as measured by the following definitions:

Lona-term loans: (a) commercial bank loans with original maturities ofmore than one year and (b) formally rescheduled interest arrears on bothlong-term and short-term loans.

Debt stocks: outstanding principal amounts on long-term loans.

Disbursements: actual drawings on loan commitments.

Principal reDavments: actual amounts of principal paid in foreign currency,goods or services during the year specified.

nterest paymnents: actual amounts of interest paid during the yearspecified.

Net_flows: disbursements minus principal repayments.

Pago 4

kfe r =MfeKg: net flows minus interest payments.

Nogn-flows: changes in stocks le_s net flows.

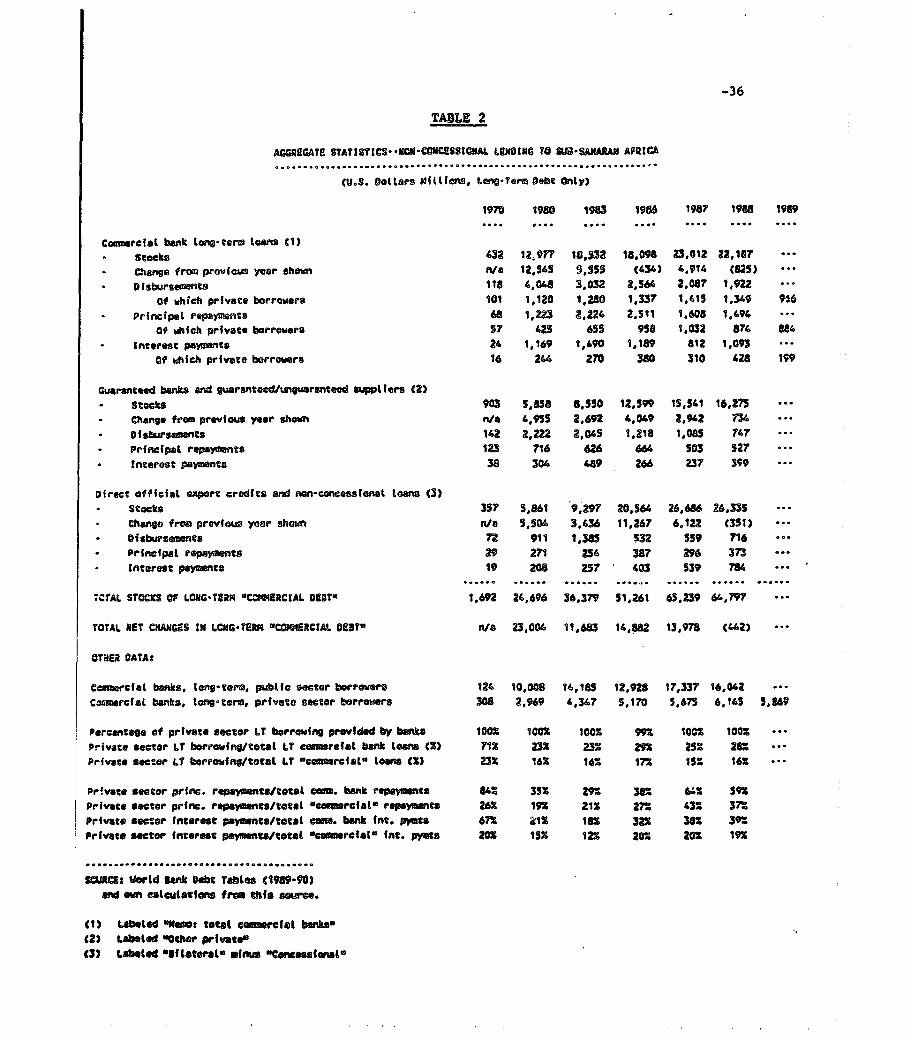

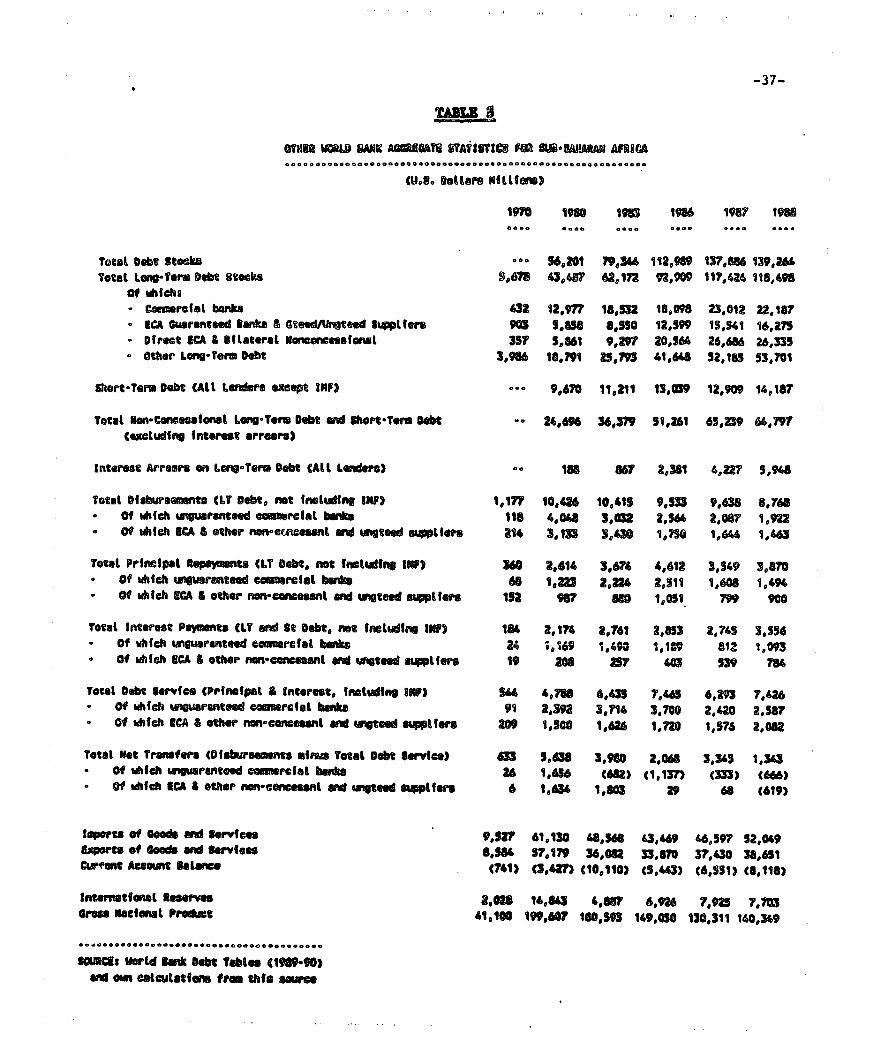

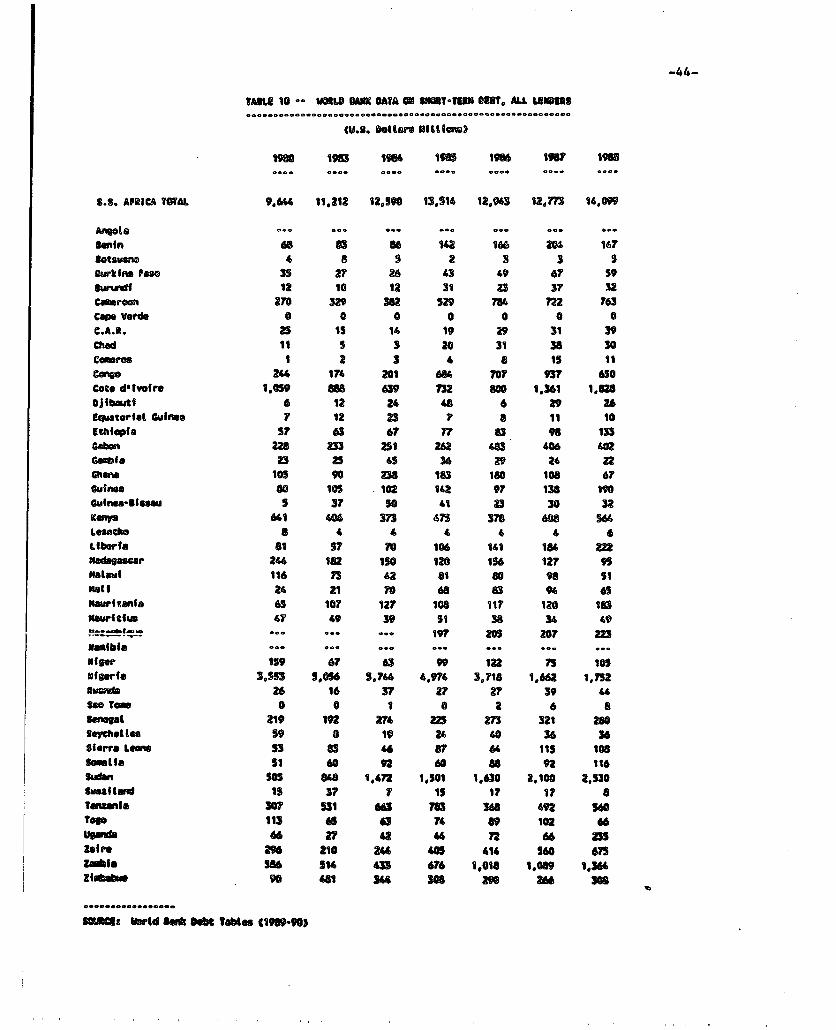

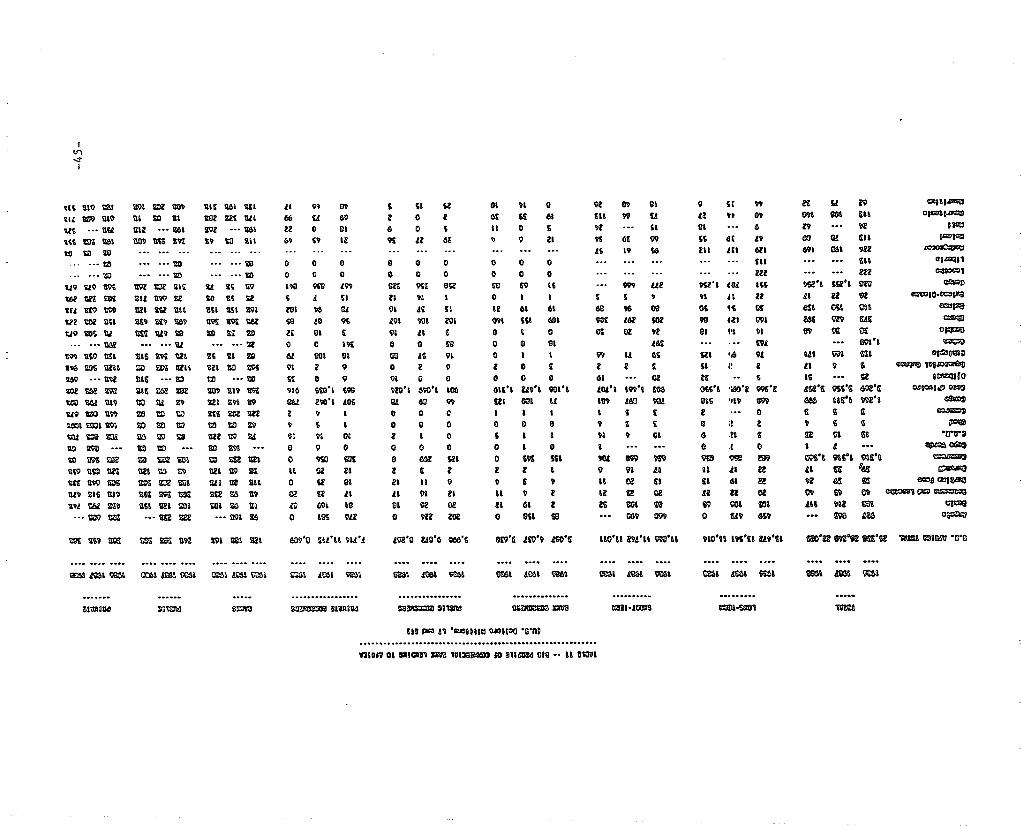

At the end of 1988, Sub-Saharan Africa's total long-term dpht to all external

lenders stood at $118 billion. According to the WDTs, commercial banks accountedfor $22 billion of these stocks, as compared with $44 billion for official export

credit agencies and suppliers, and $52 billion for concessional lenders and theJBRD (Tables 2-3).

Until 1970, commercial bank debt stocks had remained at relatively insignificantlevels: governments relied mainly on donor credits and internally generatedforeign exchange to finance economic expansion. The sharp increase in oil and

primary commodity prices at different times in the 1970s reversed this trend.As the Sub-Saharan African countries were perceived to become generally more

creditworthy and petrodollars more available, commercial credit expanded.

The WDTs report that commercial bank long-term debt stocks, which stood at $430

million in 1970, rose to $13 billion in 1980 and to a further $18 billion in

1982. They remained relatively stable in the $17-18 billion range until 1987,when, largely due to a depreciation of the U.S. dollar and formal reschedulingsof interest arrears in a number of countries, stocks increased to $22-23 billion

(Table 4).

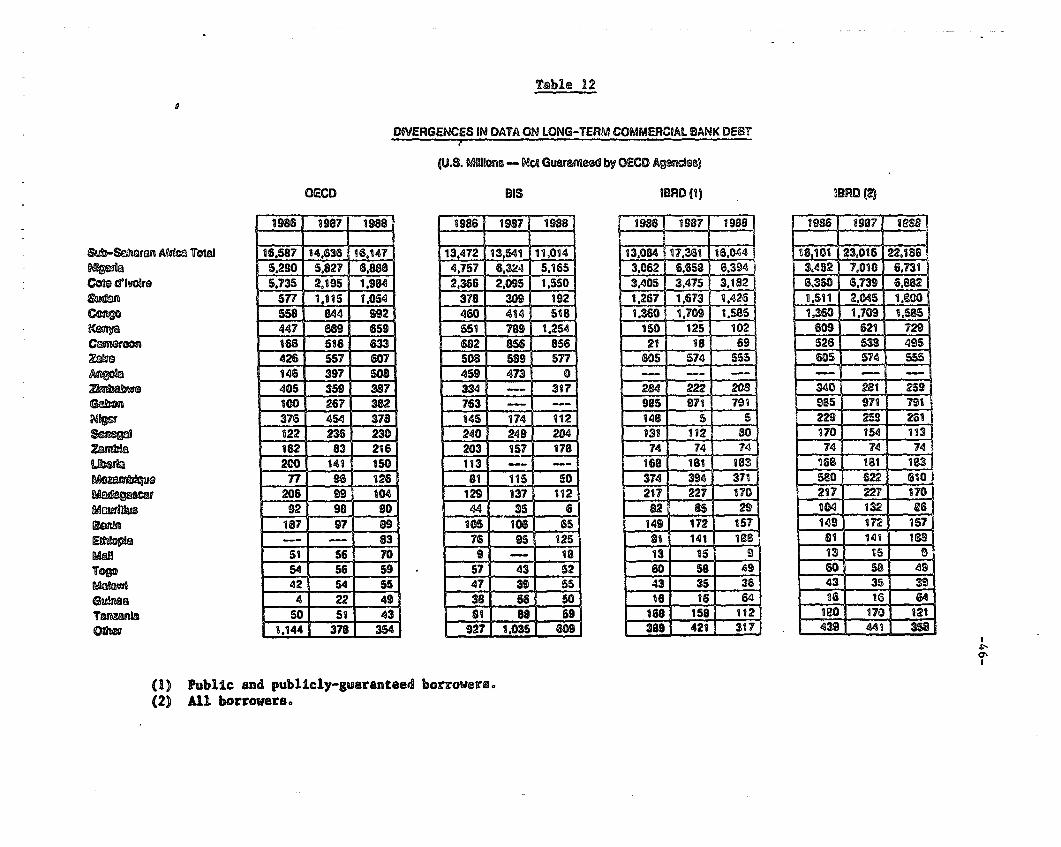

In sharp contrast, the Bank for International Settlements (BIS) places end-1988commercial bank long-term debt stocks at only Sll billion in its semi-annualreports on The Maturity and Sectoral DLstribution of International Bank Lending.

The BIS statistics were derived by subtracting the column 'Cross-Border Claims--Total" from the column "Cross-Border Claims--Up to and Including One Year".The ainual OECD External Debt Statistics of the Organization for EconomicCooperation and Development reports k16 biJlion of these stocks at en".-1988(Table 12), entitled "Other Bank Claims--Long-Term".

The divergences shown in Table 12 between these three statistical sources, dueto the different methodologies and sources being used, are very substantial, bothin the aggregate and on a country-by-country basis. For example, for C6ted'Ivoire, the OECD shows $2 billion outstanding at end-1988, the BIS reports$1.55 billion and the WDTs $6.8 billion. For Sudan the figures are $1 billion,

$192 million and $1.8 billion respectively. Since the BIS relies on information

supplied largely by the banks themselves, its figures should be taken more as

an indication of (a) the book value of these assets after the provisioning

exercises of recent years and (b) the extent to which the banks view their loans

as African "country risk," than as a profile of legally outstanding obligations.

In any case, there are many reasons for the divergences. Both the figures and

some of the definitions provided in the various publications can be misleading

to the casual reader.

Page 5

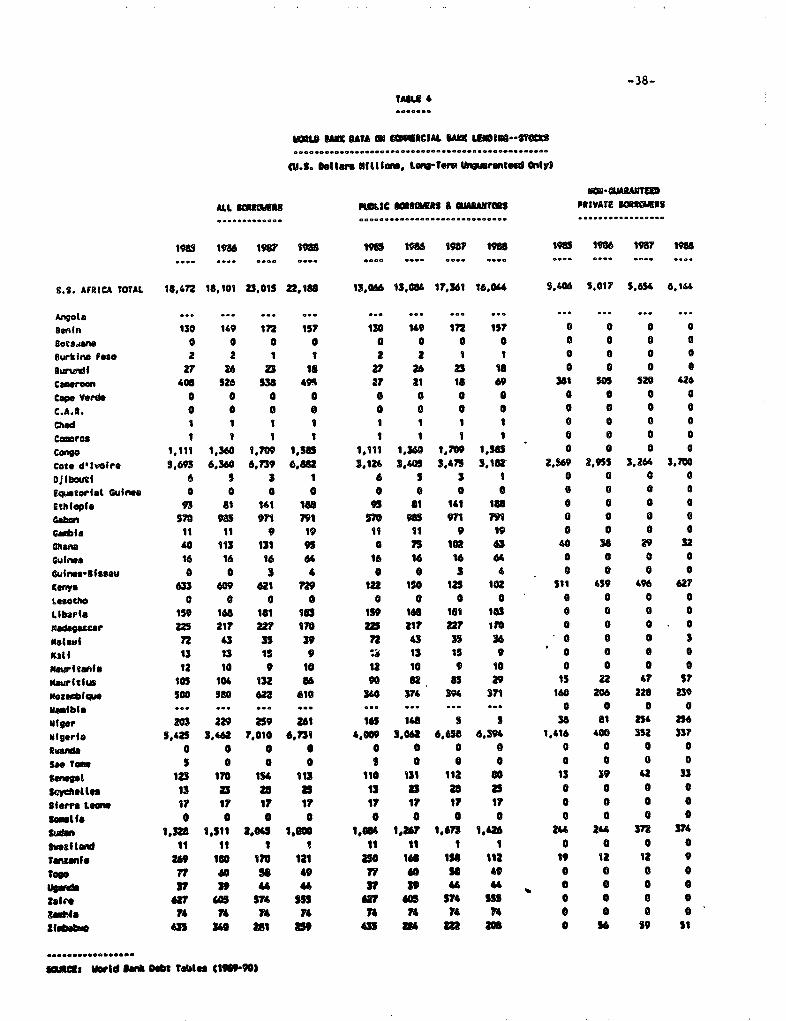

The WDTs report that the debt stocks were highly concentrated, with some 15 ofthe 44 Sub-Saharan countries accounting for 97 percent of the total. C6ted'Ivoire and Nigeria each accounted for nearly $7 billion, or a combined 60percent; Sudan, Co%igo and Gabon accounted for another $4.6 billion, or 21percent. An additional 13% represented the outstandings of Kenya, Mozambique,Zaire, Came'roon, Zimbabwe and Niger; while Liberia, Madagascar, Ethiopia andTanzania, each with stocks of over $100 million, accounted for an aggregate 3percent of the total.

Zambia is also considered to be a major debtor country, but most of itscommercial bank debt stocks are classified as short-term debt, consisting inlarge part of non-rescheduled principal and interest arrears on short-term andlong-term debt.

In addition, the commercial banks are believed to account for a major portionof Africa's estimated $13 billion in short-term debt stocks (section 5 below).

2. Long-Term Debt Flows

After averaging over $2.5 billion per year between 1980-1982, net flows of longterm commercial debt declined sharply as of 1983, as both banks and borrowingcountries began to feel the pinch of a global economic contraction and a growinginternational debt crisis. In the period 1985-1988 flows remained sluggishdespite the improvement in the performance of both some Sub-Saharan Africancountries and the global economy.

Disbursements

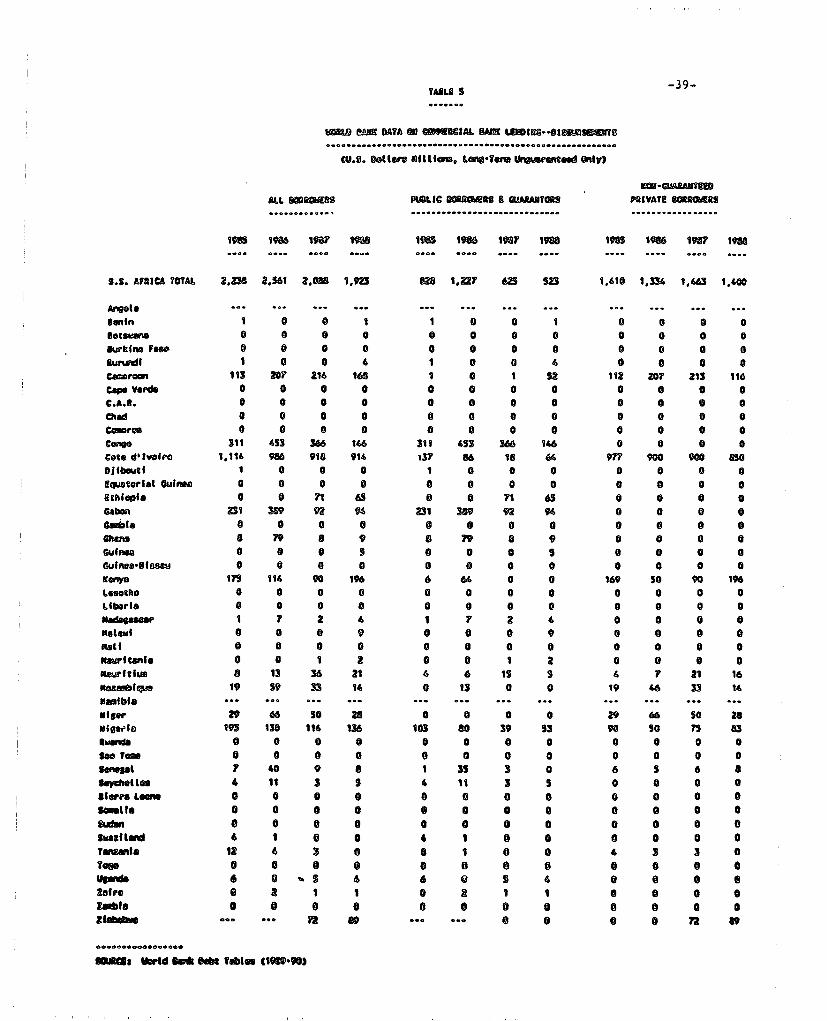

From a peak level of some $4 billion per year in 1980-82, the WDTs report thatcommercial bank long-term loan disbursements to Sub-Saharan Africa totalled $14.5billion from 1983-88, or $2.4 billion per year (Table 5).

in addition to the overstatement resulting from C6te d'Tvoire statistics, therelatively high level of disbursements in recent years do not reflect a generalmaintenance of lending activities in the region. Disbursements were heavilyconcentrated in a few countries, primarily the oil exporters and those with amore vibrant private sector. During 1985-88, with COte d'Ivoire arguably in thelead, Kenya, Gabon, Nigeria, Cameroon, Congo and Zimbabwe each generateddisbursements in the $100-200 million range. During this same period some 26African countries are shown to have received no long-term commercial bankdisbursements,

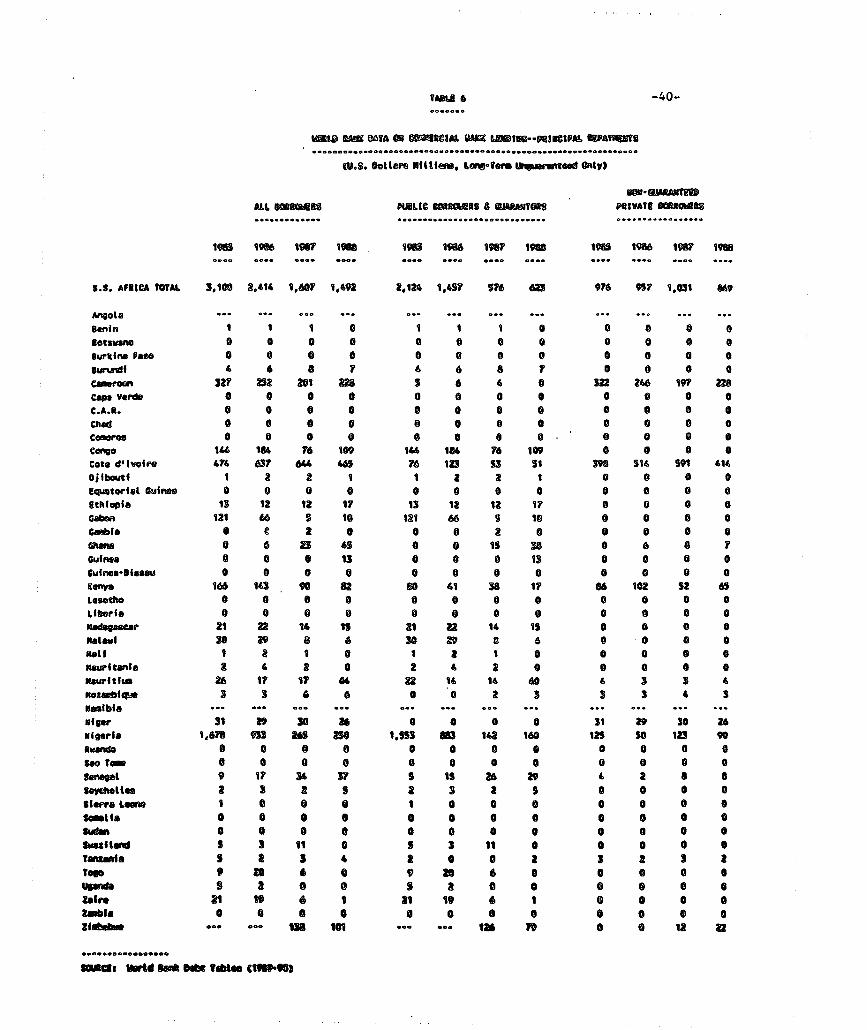

Commercial banks received an average $1.5 billion per year in principalrepayments for the period 1980-82, rising to an average $2.1 billion per yearin 1983-88, for a total of $12.8 billion during this more recent period (Table6).

Page 6

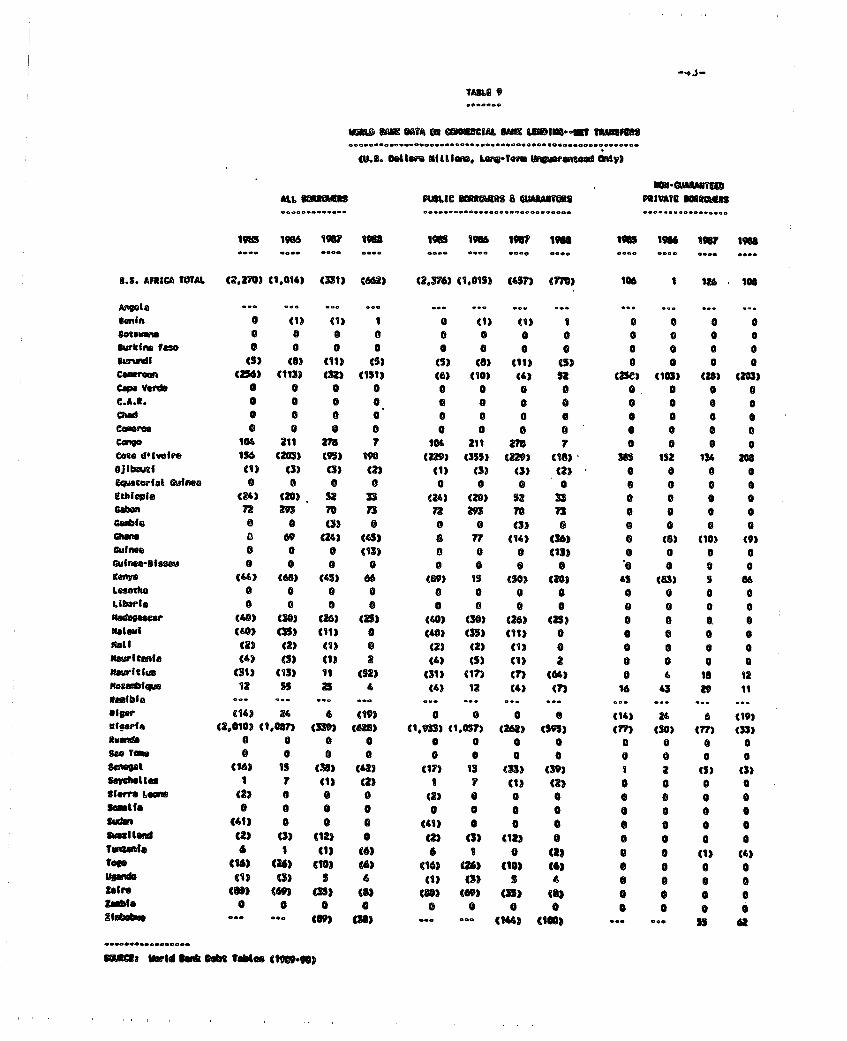

Net flows, the difference between disbursements and principal repayments,averaged $2.5 billion per year in 1980-82. They fell sharply to an average ofless than $300 million per year in 1983-88, for a cunig4itv surplus of only $1.7billion over these last six years (Table 8).

Net flows stwung from a surplus of $800 million in 1983 to a deficit of $965million in 1985. Although some recovery was registered in 1987 and 1988, at anaverage annual $400 million, the results remained significantly below the levelof previous years, and once again are distorted by reporting for Cote d'Ivoire.

Looking at the most recent 1985-88 period, net flows over the four years resultedin a cumulative surplus of only $200 million for all of Africa, with isolatedsurpluseL heavily concentrated in seven countries. Besides C6te d'Ivoire'sprivate sector, for which $1.7 billion in net flows are reported, only Congo,Ethiopia, Gabon, Ghana, Mozambique and Niger experienced positive flows, for anadditional cumulative surplus of $1.6 billion. This implies that all otherborrowers in the region experienced negative cumulative net flows of $3.1 billionin 1985-1988.

Net Transfars

Net transfers, the difference between disbursements and both principal andinterest payments, amounted to an aggregate cumulative net cash outflow of some$5.5 billion from Sub-Saharan Africa to the commercial banks from 1983 to 1988.The banks disbursed $14.5 billion and received $20 billion in total debt servicepayments.

In the more recent period 1985-1988, only Congo, Ethiopia and Gabon experiencedpositive net transfers, totalling a cumulative $1.1 billion (Table 9).

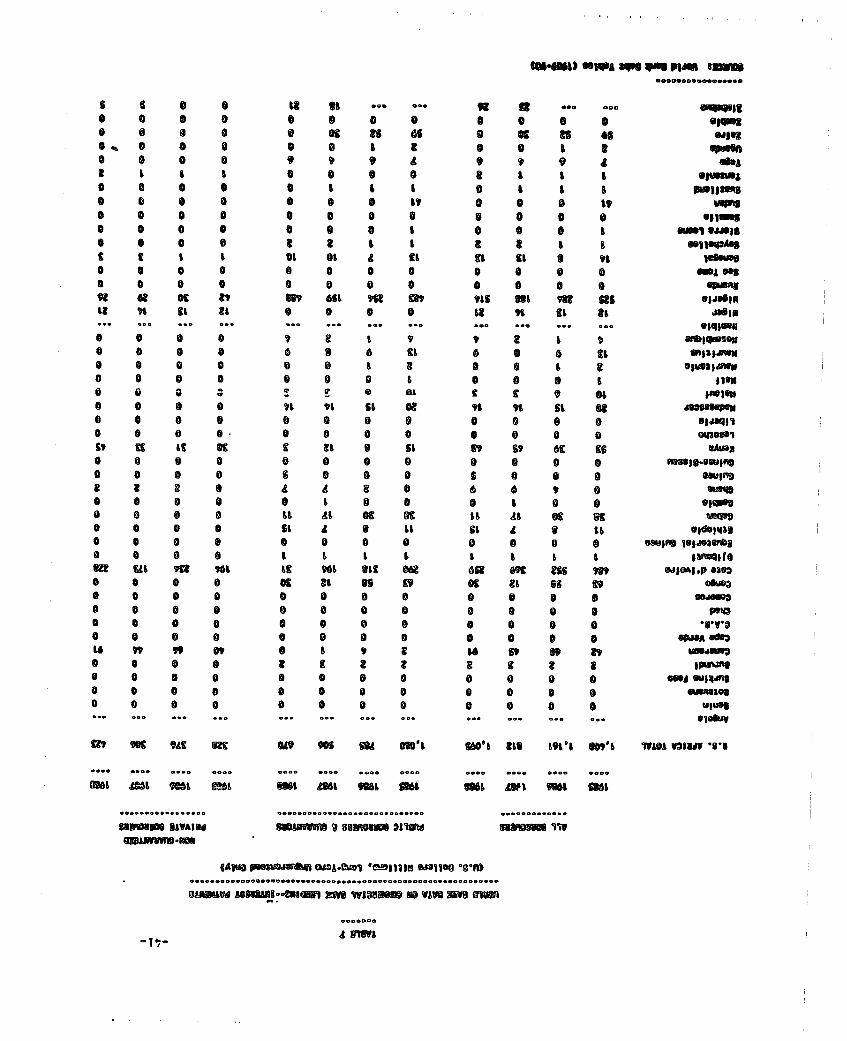

Interest payments, which had remained steady at average annual $1.4 billionbetween 1980-1985, declined by 1987 to $800 million as a result of arrears build-ups and debt reschedulings. They recovered slightly to $1.1 billion in 1988(Table 7).

Partly as a result of arrears, and partly of grace periods on principalrepayments and lower interest margins extended to borrowing countries throughLondon Club reschedulings, the region's total annual debt service payments tocommercial banks, which peaked at $4.5 billion in 1984-1985, experienced a sharpdecline to $2.5 billion in 1987-1988.

3. lic Sector Lone-term Borroving

The World Bank Debt Tables distinguish between African public borrowers andguarantors ("public and publicly guaranteed debt") on the one hand and privateborrowers ("private non-guaranteed debt") on the other.

Lacking information on the actual apportionment of credit between commercialbanks and suppliers within individual transactions, the WDTs assume that thecommercial banks have been the sol source of long-term external lending to the

Page 7

African private sector, with the exception of supplier credits in Sudan. TheWDTs also narrowly define private non-guaranteed borrowers as entities that aremajority privately-owned and have received no guarantees from public entitiesin the borrowing country. Because of this strict interpretation, whicheliminates state-owned enterprises, including large local commercial banks andproductive enterprises, private sector borrowing appears in only 12 of the 44Sub-Saharan African countries during the 1980s.

Nevertheless, because long-term finance provided by suppliers is deemed to bemarginal in relation to the banks' share, the WDTs' assumption is plausible.Moreover, other long-term lenders to private sector projects, with the exceptionof the International Finance Corporation, such as export credit agencies andother quasi-donor institutions, have only recently begun to modify policies thatrequire sovereign or state guarantees, which would change the profile of long-term borrowing by type of borrower.

The share of private borrowers in total Sub-Saharan African commercial bank longterm debt stocks remained steady at 25-30% between 1980-1988. However, partlyon the strength of the WDTs' overstated figures on C6te d'Ivoire's private sectorborrowing, by 1988 private borrowers accounted for 70% of new disbursements and50% of the region's debt service payments. In the most recent period 1986-88,both net flows and net transfers to private borrowers were reported as positive,representing a cumulative $1.8 billion and $350 million, respectively. Thiscontrasts sharply with the net flow deficit of $1.6 billion and net transferdeficit of $4.6 billiorn experienced by public borrowers for the same three-yearperiod.

Nevertheless, these more robust flows to the private sector were also heavilyconcentrated. The Ivoirian private sector's net flows of $1.1 billion between1986-88 must be discounted to a large extent, while the WDTs show that privateborrowers in Kenya, Mauritius, Mozambique, Niger and Zimbabwe accounted for acumulative net flows surplus of only $420 million. All other private borrowersexperienced deficits in net flows, for a cumulative deficit of $180 million overthe 3-year period.

The record on net transfers is similar. The Ivoirian private sector is shownto have received positive net transfers totalling $492 million in 1986-88. Allother private borrowers in all countries except Kenya, Niger, Mozambique andZimbabwe, which registered modest positive transfers, experienced cumulativedeficits of $373 million. While Cameroon's private sector received substantialdisbursements of $650 million in 1985-88, they were outweighed by over $1 billionin debt servicing.

Thus, while in aggregate terms private borrowers have fared much better thanpublic borrowers and/or have performed better on their obligations, most of themodest surplus for the period under review was concentrated in five countries.

The Maturity and Sectoal DistributionL Reoots of the Bank for InternationalSettlements (BIS) provide a more nuanced view of the pattern of commercial banklong-term and short-term lending (Table 11). Private sector borrowing appearsin nearly every country and accounts for more than 50% of the total in 25

Page 8

countries. Overall, the BIS reports show the African private sector accountingfor 38% of total commercial bank stocks and African comme._ial banks a further16% in 1988.

4. _4mparisons with Other Lenders

Total long-term debt stocks from sources other than the commercial banks rosefrom $44 billion in 1983 to $96 billion in 1988 (Tables 2-3). This was due inlarge measure to exchange adjustments, rescheduled interest arrears and othernon-flow factors which contributed an estimated $33 billion of the $52 billionincrease.

Inclusive of 1984-85 data, not shown in the tables, long-term disbursements fromall lenders other than the commercial banks totalled nearly $42 billion from1983-88, as compared with principal and interest pavments of $23 billion. Netflows totalled $28 billion and net transfers $18.5 billion.

The commercial banks held 18% of total long-term debt stocks by the end of 1988,a percentage which rises to 35% when combined and compared solely with debtstocks of other non-concessional lenders (other than IBRD), such as export creditagencies, suppliers and investment agencies such as the International FinanceCorporation and the European Investment Bank. This compares at the end of 1983with 30% and 51% respectively. The decline reflected the declining share of norn-concessional lenders in total debt stocks.

While moving in tandem in so far as stocks are concerned, the record shows amarked difference in net flows from commercial banks vis-a-vis other quasi-commercial lenders. Sub-Saharan Africa experienced a cumulative $5.5 billionnet transfer deficit vis-a-vis the commercial banks over the 1983-88 period,while other non-concessional lenders provided marginally positive net transfersin all years except 1985 and 1988, yielding a cumulative net transfer surplusof $646 million for the same period. This suggests that since 1983 thecommercial bank category has represented the largest net outflow of funds fromAfrica.

Nevertheless, since 1986 the WDTs indicate a narrowing in the flows gap betweencommercial and non-concessional lenders, subject to the overstated figures forC6te d'Ivoire. For instance, in 1986-1988, the commercial banks share ofcombined disbursements increased to an average annual 55% compared with 45% in1983. During the same time, the commercial banks' share of debt service paymentsfell from 70% to 55%. In 1988, commercial banks provided some $1.9 billion innew long-term debt as compared with $1.5 billion by other non-concessionallenders. Representing the fourth consecutive yesr of decline, debt servicepayments to the commercial banks registered $2.5 billion in 1988, as comparedwith the $2 billion paid to non-concessional lenders. This resulted in nettransfer deficits in excess of $600 million for both categories of lenders in1988.

The statistical trends presented in the WDTs suggest that the commercial banksin the aggregate do continue to disburse fairly significant medium-term credit

Page 9

to the region relative to other non-concessional lenders, despite the subsidiesavailable to the export credit agencies and the substantial profit margins oncommercial transactions which motivate the suppliers, in those rare cases wherethey lend.

5. ShoTerm Lendig

According to the WDTs, Sub-Saharan Africa's short-term debt stocks, defined asloans with original maturities of less than one year and including only non-rescheduled interest arrears on this short-term debt ( i.e., non-rescheduledinterest arrears on long-term debt not included), increased sharply between 1980and 1983 but have remained fairly stable at around $13 billion since that time.

For lack of accurate information, the WDTs do not distinguish between types ofshort-term lenders and borrowers. However, it is believed that a major portionof the outstanding short-term debt is owed to the commercial banks.

The primary short-term debtors are Sudan, Congo, Nigeria and Zambia (all withstocks in excess of $1.3 billion), followed by a second tier of countries owingmore than $500 million: Cameroon, Congo, Kenya, Tanzania and Zaire.

In general, short-term debt stocks are more evenly distributed than long-termdebt stocks. Only 9 countries are shown to have stocks of less than $30 millionin 1988, while 22 of the 44 countries had stocks of over $100 million.

The variations in short-term debt stocks over the 1980-88 period are due toactual increases or decreases in new lending and to performance on short andlong-term debt.Thus in many countries, such as Sudan, Congo, C6te d'Ivoire, Gabon, Liberia,Mala*i, Zaire, Uganda and Benin, the sharp increases were due to non-rescheduledinterest arrears, some of which were reduced in 1988. The major drop in short-term debt in Nigeria in 1987 is due to thie consolidation and long-termrescheduling of short-term debt in the London Club, preceded by an actual declinein short-term credit facilities in 1984-86.

In other countries, such as Guinea, Tanzania, Ethiopia and Burundi, the increasein short-term debt represents actual new lending.

6. Performance Record

According to World Bank statistics, of the approximately $10 billion outstandingin the London Club reschedulings of 18 Sub-Saharan African countries, about $8billion, representing 35% of Sub-Saharan Africa's long-term commercial bank debtstocks, are owed by public and publicly-guaranteed borrowers in Nigeria and C6ted'Ivoire. Both countries have been attempting to renegotiate their London Clubagreements on concessional terms and are starting to pursue buy-back and debtconversion options.

Page 10

Although all of the London Club agreements still carry market rates of interest(Libor plus a margin) and most are for relatively short terms (under 10 years),several borrowers have rescheduled several times, others have interrupted theirpayments, and a few arrangements have totally broken down. Nevertheless, somesmaller borrowers have performed well on their restructured debt, e.g. Malabi,Madagascar, Senegal, Togo and Gambia.

There are few instances where short-term debt has been rescheduled (Nigeria,Madagascar, Sudan, and Zambia), but interest arrears have been rescheduled injust about every rescheduling country. Most countries that have had continuedaccess to short-term trade finance facilities have performed well, with notableexceptions in countries such as C6te d'Ivoire and Congo whose local banks haveexperienced severe liquidity crises. However, the commercial banks' responseto liberalized exchange controls, well-funded auctions and other improvedpayments systems in countries such as Nigeria, Madagascar, Guinea and Ghana hasgenerally been disappointing, as much from lack of attention as from lack ofconfidence.

B. NATURE OF COMMERCIAL BANK LENDING

The various forms of commercial bank cross-border lending are best categorizedby the type of risk assumed, the type of borrower, the term of the loan and thenature of the underlying activity being financed. Four fundamental riskcategories are briefly characterized below, with an indication of recent trendsin the region: unsecured lending, exporc-secured lending, asset-based financeand secured lending.

While individual transactions often combine different forms of risks, all of thecategories are typically counted as cross-border loans in the World Bank DebtTables.1. Unecured Lending

Unsecured lending encompasses loans that are extended on the basis of theborrower's ability to service the loan from resources generated within theborrowing country and transferred to the lending bank through the country'snormal foreign exchange allocation system. The lender assumes both the"commercial" risk, i.e. the borrower's solvency and the 'political" risk, i.e.principally that of foreign exchange availability.

Under this category, the three most prevalent forms of lending to Africa havebeen the following:

a) Short-term revolving facilities extended to central and commercialbanks for the advance settlement of obligations to offshore suppliers of goodsand services, typically through confirmation and negotiation of letters of creditor through short-term advances. As these advances are repaid by foreign exchangetransfers from the borrowing country, new availability for further advances is Kcreated within the limits of the facility.

Page 11

b) Loans to non-bank borrowers (sometimes underwritten by local banks)in the form of guarantees to their offshore suppliers or through discountedpurchases of suppliers' credits.

c) Medium-term loans, typically for specific private or parastatalinvestment projects, based on the borrower's creditworthiness, the viability ofa project as established by cash flow projections, and confidence in theavailability of foreign exchange for debt servicing.

The degree of risk in unsecured lending tends to increase in those cases whereforeign exchange availability is regulated and/or constrained. Thus banks havecontinued to provide short and medium-term unsecured loans to profitable bankand non-bank borrowers in the CFA zone, given their automatic access to FrenchFrancs. Banks have also tended to be more active on an unsecured basis incountries with adequately funded auction systems - such as Guinea, Madagascarand Nigeria, though generally restricted to short-term financing, and incountries that have not experienced payment problems, such as Zimbabwe, Kenya,Ethiopia, Mauritius, Burundi and Rwanda, among others.

Increasingly, banks have been moving away from unsecured lending and for manycountries now require some form of offshore security. This may take the formof cash deposits formally committed as collateral, or of revolving flows ofexport proceeds that are ultimately repatriated to the borrowing country. Thus,partly as a means of preserving commercial bank lending and services, since 1983Zaire has required that all cross-border loans be fully secured by foreignexchange deposits with the lending bank.

2. n Lend

A variety of mechanisms are used to mitigate transfer risk by establishing lienson exports and/or export proceeds. Banks may require, ner, All, (a) assignmentof title to exports, (b) the issuance of irrevocable instructions to a buyer tomake payment directly to a lending bank, or (c) the establishment of foreignexchange escrow accounts which are held in the bank's or the exporter's nameeither with the lending bank, another offshore bank, or within the borrowingcountry's foreign exchange system.

A classic form of export-secured lending, and an area where there continues tobe considerable activity and competition, is pre-export finance. Individualbanks and syndicates have been providing substantial facilities, essentially forpurposes of balance-of-payments support, to a wide range of countries, such asAngola, Cameroon, Tanzania, Uganda and Zimbabwe. The structure of the facilitiesranges from single disbursements repayable in one 'bullet' (typically within lessthan one year) to multi draws/multi installment repayments, revolving on a moreor less permanent basis, but typically with terms of not more than three years.In addition, formal control over exports or export proceeds is used extensivelyby the oil and mining sectors to secure medium-term loans.

The private 4nsurance industry has played an important role in secured lending,both as facilitator and competitor to the banks. Typically the industry insures

Page 12

either suppliers or banks against non-delivery and export contract frustration.Some insurers provide coverage directly to banks, while in the case of otherswho generally do not (e.g., Lloyds of London), suppliers may assign their rightsunder these policies to their lending banks. On the other hand, a significantvolume of African exports is financed directly by suppliers under insurancecover, without the intervention of banks. It is also true that banks do not

necessarily seek insurance coverage for large pre-export finance facilities,given the high cost of such insurance and the anticipated delays in makingrecoveries should problems arise.

3. Asset-Based Finance

Banks have demonstrated a willingness to finance high-value, moveable assets suchas aircraft, vessels and mobile equipment, based on a lien on the asset typicallyfor a reasonable percentage (50 to 70 percent) of the asset's market value. Theprivate insurance industry generally supports such transactions by providing lossand/or repossession coverage.

Except in the case of Liberia's vessel registry, asset-based loans tend to berecorded in the World Bank statistics as cross-border credits, unless structuredas leasing arrangements, which often applies in the aviation sector.

4. Secured Lending

Secured lending encompasses loans that are collateralized by an offshore cashdeposit or protected by an identified external irrevocable source of repayment.Unless guaranteed by an official agency (such as an export credit agency), theseloans tend to appear in the World Bank statistics, but typically are not included

in the BIS reports.

Typical security includes cash deposits, cross guarantees among suppliers, buyersand direct investors, commitments or undertakings from official agencies, mosttimes conditional on borrower performance, and private political risk insurance.

Increasingly, commercial banks are involved in the intermediation of donor funds,which involves the provision of normal correspondent banking services againstcash deposits or reimbursement guarantees from donors. To some extent, thesefacilities, which also can enable banks to take some form of "clean" risk withfunded credit, are replacing the unsecured short-term credit lines that the banks

have traditionally provided to their subsidiaries and to correspondents in anumber of countries.

Another form of secured lending involves the provision of guarantees to the banksby offshore private entities, such as oil exploration and production companies.These guarantees can vary from "comfort letters" to legally-binding full orpartial guarantees, depending on the nature of the relationship between the

corporation and its bank, and the degree of risk associated with a given

transaction.

Page 13

C. FOREIGN CONNRCIAL AA-N PRESENCES

By the early 1980s, some 38 international banks had established and maintaineda presence in at least 23 Sub-Saharan African countries in the form of branchesor effective control of locally incorporated entities. The presence of severalBritish, French and Belgian banks, such as Barclays, Standard Chartered,Grindlays, Banque Nationale de Paris, Banque Internationale pour l'AfriqueOccidentale, Societe Gdndrale, and so on, go back many decades to traditionalcolonial ties. Many increased their presence over the years by expansion inbranch networks nationally and regionally. A few local banks have alsoestablished branches outside their countries as a means of fostering intra-regional trade.

A slow exodus of the international banks from Sub-Saharan Africa commenced in1985. Some British banks reduced their local branch networks but most haveremained in their traditional spheres of influence. The same was true of Frenchbanks until recently. Faced with severe illiquidity in several countries in theCFA Zone, they appear poised for further reductions in their presences there,while at the same time entering new markets, such as Guinea and Madagascar.Other than Citibank, all large American international banks, many of whichoperated through representative offices rather than full fledged branches, haveleft, including Bank of America, Chase, Bank of Boston, Manufacturers Hanover,and Chemical. However, most banks continue to do selected offshore risk-freebusiness, such as the provision of correspondent services under donor fundedprograms.

Countries affected by the exodus of the banks include Cameroon, Congo, C6ted'Ivoire, Gabon, Kenya, Liberia, Mauritius, Niger, Nigeria, Senegal, SierraLeone, and Sudan. Because these countries represent both good and bad economicperformers, it appears that part of the reason for the banks' departure has toAn with the chaneing nature of their business objectives and target markets.Departure of the banks has not gone without response. Some new banks, eitherbranches of international banks from other regions of the world, or locallyconstituted institutions with or without foreign technical partners, have beenfilling the void. Ecobank, a privately-owned financial institution whichoperates in the Economic Community of West African States (ECOWAS); MeridienBank, a subsidiary of the international trading firm ITH, with significantAfrican holdings; and Equator Bank, a subsidiary of the HongKongBank Group, aretypical of the financial institutions that continue to be active and to expandtheir activities in the region.

Page 14

CHPE TO PFERCPIN P H OMRCA AK

In a series of informal interviews with commercial banks in France, the UnitedKingdom, the United States and Belgium that have been traditionally active inSub-Saharan Africa, little optimism was expressed about the prospects for newmedium-term lending to Africa on a wide scale during the 1990s. Nor did manybanks foresee aggregate net increases in their short-term portfolios for theregion in the immediate future.

A. ERCEIVED COSAINT

The principal causes of this pessimism are summarized for the purpose ofdiscussion into seven broad issue areas.

1. mantory Proinina

Host OECD iountries have imposed selective provisioning requirements orguidelines on the commercial banks in respect of their developing countryexposure. These regulations, as well as voluntary provisioning practices of mostbanks, have generated significant losses on the affected LDC portfolios and havemade it difficult to justify new lending to non-performing countries.

Beyond this inevitable consequence of the debt crisis, the extension ofprovisioning requirements to naglenin continues to be a major deterrent andfor some banks an absolute bar to further activity since they can lead toimmediate accounting losses. These policies are perceived as signals that manyOECD banking authorities do not want banks to be active in the affectedcountries.

Many of these regimes, whether covering past loans or new loans as well, becamemore stringent in 1988-89: for example, the Bank of England issued a tougher"matrix" in January, 1990 and private sector/local bank risk in the CFA zone hascome under tighter scrutiny in France and other lending countries. Some of thecases are viewed as excessive, such as the 100% provisioning on Zairean debtimposed in the United States, which normally oiuwlwa wi4or liberal and sclcct,vepolicy than most other OECD countries.

2. CaI Adeauecv and RLsk:Revard Re1ationshJ9s

In the cases of relatively undercapitalized banks, portfolio growth isconstrained generally, and higher risk lending most particularly. Not only mustcapital adequacy be strengthened to comply with regulatory targets, but somebanks are particularly sensitive to the judgement of bank stock price analysts,who reportedly are quick to view any African lending as a negative. In response,the dominant tendency of these banks in the past 2-3 years, which is likely tocontinue into the future unless new mechanisms are found to mitigate risks, isto reduce aggregate LDC exposure (as well as activities in other poorly

Page 15

performing sectors), minimize and absorb current losses, and generally improve

asset quality and streamline their operations.

In this context, it has become more difficult to draw the attention of analysts

and bank management to the potential of certain lending opportunities in Sub-Saharan Africa, an attention which is a prerequisite to mobilizing support for

renewed wider-scale banking activities.

A related problem is the fact that the scope for adjusting pricing to reflect

actual or perceived risks and to take advantage of the relative scarcity of long-

term commercial bank financing has been declining, Decision-makers in the

banking industry are strongly averse to lending at any price to non-performingborrowers, while some borrowers and external public officials appear to have

difficulty accepting the high fees and interest margins that lenders considercommensurate with the perceived risks.

It may be possible to establish a more realistic Irisk:reward" relationship in

lending that is shifting to the private sector, perhaps more along the lines of

venture capital support and more commercial activities that can generate far

higher returns than traditional interest margins and fees on loans. However,in the present situation, commercial banks appear unlikely to pursue new

strategies of this nature.

Instead, the primary approaches that are being used to improve risk:return ratios

on African business appear to be the provision of no-risk, fee-based services,

by means of fully secured letter-of-credit and other traditional trade-related

facilities, intermediation and management of donor funds, representation of

governments in debt negotiations, and general merchant banking or financialengineering services.

3. ExIROrt Credit AgAnen SuoD2rt

The WDTs' aggregate statistics suggest that the OECD export credit agencies have

also been less active in Sub-Saharan Africa in recent years as they too face non-

performing loans, budgetary discipline, more conservative borrowing practices

and otherwise depressed demand in a number of countries. Many agencies have

suspended or been slow to re-open or commit resources under various credit,

guarantee and insurance programs.

Given the fact that a classic role of the commercial banks has been to providefunding and/or residual risk financing in conjunction with official export

finance programs, the reduction in lending from this source has translated into

fewer opportunities for the banks.

In some cases, the decline in export credit agency support may also be related

to an increase in concessional financing. An increasingly critical event in

country-donor relationships, the Consultative Group meetings, now generates

virtually all of the long-term financing support for public investment programs

that traditionally received some commercial bank and export credit agency

support. Similarly, on the short-term side, balance-of-payments support in the

Page 16

form of structural adjustment facilities may have reduced the need for importfinancing by banks, suppliers and official export finance agencies.

4. Co-Financing Mechanismg and Other Security Arrangements

Given the foreign exchange constraints and debt servicing difficulties of manycountries, commercial lenders are particularly wary of projects that generateno foreign exchange revenues. They are equally unenthusiastic about exportprojects in countries where export receipts and debt service payments have totransit through the host country's foreign exchange allocation system. Further,little or no interest exists for projects that involve lending to non-performingpublic borrowers and/or state-controlled entities.

Some banks expressing concern about mandatory provisioning rules indicate thatthey would participate to a significant degree in new lending only if thesecurity is sufficiently enhanced to remove or reduce the "sovereign risk"component in loans to borrowers in the countries affected.

Three recurrent themes emerged clearly with respect to the perception of banks(not necessarily based on full information) regarding prospects for improvingco-financing structures and enhancing of other security arrangements:

- Some of the co-financing mechanisms currently available in Africa do notappear to provide sufficient comfort to the banks. In particular, thebanks would (a) like to share in a more formal sense in the "seniorcreditor status" enjoyed by multilateral co-financing agencies and (b)like to see the agencies take more responsibility for the political riskand/or the monitoring and enforcement of debt servicing obligations. Theco-financing structures being offered by the International FinanceCorporation (IFC) do generally meet these concerns, since IFC acts as thelender of record, with bank syndicates taking sub-participations.

- There is concern both about the lengthy process involved and about thepressure exerted on them by most sponsoring agencies to reduce pricing inco-financing transactions.

- Some donors and African policy-makers are perceived to be opposed to theassignment of export proceeds and royalties and to other project-relatedmechanisms that would reduce various political and commercial risks oflending, whether within or outside of co-financing arrangements.

While there is certainly a trend towards greater quality in transactions, moreflexible and mutually satisfactory forms of donor-bank partnerships and moreactive marketing to banks by sponsoring agencies, it is still too early toconsider that a sufficient framework exists for a major surge in bank lendingthrough co-financing arrangements.

Page 17

5. Credit ExSerienco_and the Handling of the Debt Crisis

Some banks perceived a lack of political will to service debt in some Africancountries and expressed concern that donors and African governments underestimatethe negative impact that undue pressure for outright debt forgiveness would haveon future bank lending. The "forgive (debt) and forget (new lending)" theme wasraised on a number of occasions.

While reschedulings and market-based reductiono--including discreet buy-backschemes in which the banks themselves are participating--are not as stronglyopposed, the banks view these initiatives as seriously undermining the positionof pro-African lending constituencies within their ranks. An aggravating factorfor some banks is the perception that the official creditors and donors areoverzealous in requiring commercial bank debt restructuring on terms similar toParis Club creditors and/or in advocating sweeping debt forgiveness.

It was also perceived that an effort to differentiate between certain types ofcommercial bank lending could help mitigate negative reactions of banks toinitiatives involving elements of debt forgiveness or particularly drawn-outrescheduling terms. In particular, it is argued that a renewed commitment toservicing responsible trade finance facilities and past loans to viable andhealthy projects could yield long-term benefits in terms of restoring Africa'slinks to the private financial markets.

By their own admission the banks acted irresponsibly in contributing to Africa'sdebt growth, often citing the balance-of-payments loans (straight cash transfers)and "white elephant" projects of the late 1970s and early 1980s. However, somealso opined that the official agencies have also extended questionable financing,whether in terms of the quality of the underlying activities being financed orthe reality of corruption and/or weak economic management performance in someof the borrowing country governments.

Judging from comments such as these, the banks' role in debt relief on the onehand, and radical options such as debt forgiveness on the other, should bereviewed more carefully, with more bank involvement, in the context of a broadereffort to revive prospects for new lending.

6. Project QOualty

All banks indicate their willingness to support important "corporate customers"doing business in Sub-Saharan Africa, and most expressed interest in financingprofitable and economically justified investment projects undertaken by Africanenterprises. However, several raised the point that transactions of the scale,quality, or strategic importance to warrant the banks' attention are rarelyavailable or brought to them for financing, sometimes due to lower-costalternative sources of support from official agencies.

On the other hand, several banks expressed dismay at the number of solicitationsthat involve speculation in short-term trade activities and establishment of

Page 18

commercial monopolies in contravention of official policies in the borrowing

countries.

Finally, the banks point out that few prospective private borrowers are ableand/or prepared to take a reasonable proportion of project risk, even when theyhold significant assets outside of their home countries.

7. Focus on Other J?3Xt

A handful of the traditionally active banks profess to have ceased focusing onAfrica as a market for new lending in the foreseeable future, no matter how well-secured or potentially profitable. In these institutions there has been a markedreduction in the number of professionals working in or visiting the Africaregion. For a variety of strategic reasons, the banks are allocating a largershare of their resources to new domestic opportunities and to 'more stable"regional markets.

Other reasons cited by the banks for the poor prospects for commercial lendingto Sub-Saharan Africa, albeit less frequently, included the following:

- rThe perceived weakness of African domestic banking systems andinstitutions, whether in terms of their financial condition or of thequality of services provided.

- A deep-rooted view that commercial banks are being largely ignored by thedonor community as significant players in Africa in the 1990s.

- An insufficient recognition given to restructured or non-performing bankdebt as a financial resource: policy-makers, designers of donor-sponsoredprojects, and private investors, whether African or non-African, are saidto pay too little attention to the desirable objectives of maximizinglocal currency components in projects and of establishing appropriate debtconversion mechanisms to help finance these local costs.

The exchange risk inherent in cross-border transactions with borrowers incountries likely to undergo progressive currency devaluations in thecontext of reform programs.

B. PERCEI-VaED OPPORgITIE

There was some discussion of relative opportunities for bank lending in differentSub-Saharan African countries, and about the appropriateness and/or likelihoodof different forms of lending. However spontaneous, there was some consistencyin the views expressed, as summarized below.

Page 19

1. Secto

The mining sector is likely to attract the most support from commercial banks,due to better-known project and market variables, the scale of the projects, theimportance and reputation of corporate investors generally undertaking suchprojects, and the quality of security that is likely to be obtained.

In part because of these factors, the oil, gold and diamond producing countrieswere! often pointed out as more likely candidates for new medium-term loancommitments during the next five years. This preference is already evidencedby the pattern of lending in the last two years. To illustrate, in addition toconsiderable lending for oil exploration and production, a major IFC co-financedsyndication in Ghana was recently completed for a large gold project, and therehave been a few smaller-scale commercial bank loans for other mining projectsthroughout the region.

Banks believe it unlikely that the models for lending to the mining sector couldeasily be extended to agriculture, industry, tourism and fishing, due to thehigher project risks (climate, market, etc), the smaller project size, and therelative lacSk of aLttenton from corporate sponsors which characterizes thesesectors. Only improved co-financing arrangements, expanded export credit agencyactivity and/or major corporate sponsor guarantees and relationships are likelyto attract banks to these other sectors.

2. Asset-Based Financ

A number of banks are still competing for aircraft and major (e.g. mining)equipment financing in Africa, secured by the value of the underlying assetfinanced, but there is also no indication that these models could be stretchedvery far into the various economic sectors in Africa. Because other types ofassets are less mobile and depreciate more quickly, they are not viewed asadequate security for loans, and the general perception is that the underlyingeconomic activities are more vulnerable to changes in the policy and marketenvironments.

at a*. eveloomnJ. malmal mentand Prolect

Several references were made to prospective improvements in the Southern Africapolitical climate and in South Africa's relationships with the neighbouringmembers of the Southern Africa Development Coordinating Conference (SADCC). Itis perceived that closer economic links and more visible and substantial businessrelationships within the subregion could provide a heretofore missing stimulusfor economic expansion which could lead to the development of high-qualityinvestment projects, new intra-regional financial arrangements and a moreattractive financing environment. To a similar but lesser extent, Nigeria couldserve as a "growth pole" for the West Africa sub-region. However, some felt thatresumed lending to South Africa could come at the expense of other Africancountries.

Page 20

4.

Banks pointed to the contributions that their subsidiaries operating in Sub-Saharan Africa have made over the decades. In recent years, this contributionhas taken more the form of local currency working and investment capitalfinancing, financial sector development, and training. Whether or not they hadlocal subsidiaries or representation, many banks feel that the importance oftheir personal and institutional relationships in the various countries is beingoverlooked in the analysis of future bank roles in African external finance.There is also a wide-spread feeling that while they have a comparative advantagein evaluating private sector risk and in responding quickly to opportunities,few banks are presently prepared or have specific plans to expand theiractivities to take advantage of this experience and strategic posture.

5. Short-Term Lending

Short-term lending is viewed as the principal means for maintaining continuityin the banking industry's relationship with Sub-Saharan Africa, while effortsare made to rebuild confidence and renew the banks' understanding of the region'sneeds and opportunities.

The banks recognize that despite widespread skepticism, reform efforts and donorsupport are improving the creditworthiness of a number of countries and/or theirprivate sectors, tiereby creating new opportunities for short-term lending. Inparticular, there appears to be increased attention to or at least some interestin developing new mechanisms to support Africa's export sectors through bothshort- and medium term lending. To some extent this interest is due to aperceived minimization of risks through security arrangements, but this does notnegate the fact that in a general sense the banks are capable of designinginnovative products to promote an expansion in Africa's export base and to startthe process of resuming general lending to the regi4 n

Page 21

CHAPTER THECE- -SCOPE FOR ACTION

Under what circumstances are commercial banks at all likely to resume normallending to Sub-Saharan Africa, and what are the prospects that these conditionswill materialize? What innovations might accelerate these changes and alter thecontext of the discussion? What particular opportunities are available tocommercial banks and how are these constrained by the borrowing capacities of

the African countries themselves? In considering the prospects for increasedcommercial bank lending to Africa, with an emphasis on long-term lending, astarting point would be to define the objectives of new lending and target orders

of magnitude.

The statistical profile of Africa's long-term debt stocks and debt servicepayments over the next five years will depend largely on factors relating tocurrent outstandings. Important in this determination will be the debtperformance of the four sovereign borrowers (C6te d'Ivoire, Nigeria, Gabon,Congo) who hold the bulk of the region's long-term commercial bank debt.Totalling $12.5 billion, their debt represents 80 percent of long-term publicand publicly-guaranteed debt of $16 billion, and 60 percent of the total long-term commercial bank debt of $22 billion reported by the World Bank Debt Tables.Non-flow factors such as more accurate debt information, exchange ratefluctuations, reschedulings of interest arrears, market-based debt reductions(through conversions and discounted trading) and negotiated debt cancellationsmay also have an impact on these statistics.

Without attempting to project the future profile of Sub-Saharan Africa's debtoverhang, but using as a key measure of progress anticipated future levels and

geoeraohical distribution of commercial bank disbursements, the following couldform the minimum objectives for commercial bank long-term lending by the year*2000:

double the aggregate level of annual disbursements to the private sector,as narrowly defined by the World Bank, from their present base of about$600 million per year (excluding the statistics for C6te d'Ivoire);

achieve a broader distribution of disbursements to the private sector inmore countries and economic sectors;

bring aggregate disbursements to public and publicly guaranteed borrowers,as broadly defined, at minimum to their 1986 levels of $1.2 billion.

Such a performance would bring the commercial banks to somewhat over half of

their peak new lending level of $4 billion achieved in 1980.

A. QPPQORTNITIES AND_COMMERCIAL BORPOWIXG CAPAGITY

Sub-Saharan African governments have accepted the view put forth by the WorldBank's Long Term Perspectives Study that future development strategies must

emphasize the development of human resources and improvement in physical

Page 22

infrastructure, in addition to conventional policy reforms, as the means forproviding an enabling environment for producers in the private sector. Thisimplios a shifting of intervention in the economy from the state to privateenterprises. Herein lies Africa's most important opportunity for increasedcommercial bank lending.

A large number of productive assets lie idle or operate at low capacity in thehands of discredited state agencies. The introduction of new productive assetsis stymied by the lack of physical infrastructure to support their exploitation.These include mineral reserves which have yet to be explored. The region'sfishing potential remains under-exploited or adversely exploited, while othernatural resources lay fallow. The development of agriculture which has as acentral focus the commercialization of the millions of subsistence producers isa clear and constant priority. A buoyant agriculture sector and the links thatthis would provide to an expanding manufacturing base represents a growth modelwhich has succeeded in other regions. The potential for direct investment--local and foreign--supplemented by commercial bank lending to intrepreneu rs iswell established.

In the authors' view, it is premature and it would be unfortunate to diminishthe prospects for significant aggregate increases in commercial bank medium-termlending to Sub-Saharan Africa. Indeed, there are a number of advantages to begained from increased commercial bank lending, as exemplified below.

° First, the growing emphasis on and support for private sector initiativeraises the hope that high value-added, profitable projects, and in manycases focusing on export activities, will be developed more quickly thanin the past and begin to proliferate in Africa.

Many such projects should be capable of supporting commercial borrowingterms and generating incremental foreign exchange earnings and/or savingsfor debt service. Frequently, the cost of borrowing directly from abroadis lower than local market rates of interest, particularly if there is nosignificant exchange risk or if this risk is mitigated by a local currencyguarantee fund. Such guarantees are being offered in some of the medium-term onlending facilities being offered to the private sector in a numberof countries, including some of the World Bank "APEX" lines. Moreover,as comoared with the impact of foreign direct investment, a borrowingcountry's outflows on debt service over a limited number of years typicallyshould amount to a fraction of the outflows on dividends and capital gainsover the life of a project, assuming that the host countries are willingand able to respect commitments to dividend and capital repatriation.

- Second, equity investors seeking to leverage their capital with debtfinancing should have the widest possible range of institutions to turnto for this support. To the extent that they are at all interested inresuming lending or other forms of support for African projects, commercialbanks have substantial human and financial resources that can be put towork and are capable of responding more quickly and with less red tape tosponsors of attractive projects than public agencies.

Page 23

- Third, private borrowers, particularly foreign investors, can takeadvantage of their traditional banks' existing relationships with Africandecision-makers and potential partners, the banks' local subsidiaries andother sources of financing (e.g. the private insurance industry) toaccelerate the structuring of their projects and develop various supportmechanisms for their development and ongoing management (including short-term trade finance support).

- Fourth, the banks' rescheduled debt remains an important resource that canbe constructively utilized to advance Africa's privatization, exportdiversification and infrastructure development objectives. Market-baseddebt reduction through conversion mechanisms should be heavily encouraged:as a form of balance-of- payments support for the region, as a disciplinefor more judicious use of local currency components in public and privateinvestment projects, and as an incentive for the banks to renew theirinterest in Africa's economic potential and development strategies.

Despite the important role that the banks could be playing, much of theliterature, as well as informal views expressed by African governments, donoragencies and others, suggests that under present conditions, the capacity of manyAfrican countries to borrow from commercial banks is extremely limited, giventhe fact that (a) overall external indebtedness is already far too high inrelation to most of the countries' foreign exchange earning capacity and (b) thebanks' credit terms (fees, interest rates and repayment schedules) are tooonerous in relation to the grants and low-cost financing available fromconcessional and ECA-type sources.

The prevailing view is that commercial bank support will be required and providedessentially in the area of short-term trade finance and non-risk banking servicesduring the 1990s and possibly beyond. Even with respect to financing for theprivate sector, much of the hope is pinned (a) on an increase in equity financingfrom foreign and local investors, whether individual entrepreneurs, corporationsor public agencies and (b) on longer-term, fixed rate debt financing primarilyfrom donor or export credit agencies, such as the APEX lines being establishedby the World Bank in a number of countries and new programs Deing aeveloped byIFC, DEG, FMO, PROPARCO and similar quasi-donor agencies.

However, it should be clear that ALL external sources of financing, even ifproviding support to Africa within the context of a satisfactory regulatoryenvironment for productive enterprise, will not necessarily be capable ofproviding sufficient resources to help Africa exploit its considerableopportunities on a sustained basis.

The African countries ultimately will have to become creditworthy in their ownright for sustained access to the international financial markets. JoakimStymnel (IMF Working Paper WP/89/71) shows clearly in his 1989 simulation ofSub-Saharan Africa's payments capacity that export growth supplemented by debt

1 Stymne, Joakim, "Debt Growth and the Prospects for Debt Reduction." TheCase of the Sub-Saharan African Countries." IMF Working Paper, September 1989.

Page 24

relief is the key to improvement in the borrowing capacity or creditworthinessof Sub-Saharan African countries.

Assuming a perhaps optimistic annual export growth rate of 7 percent and no debtforgiveness over a five-year period, Sub-Saharan Africa's composite debt ratio(total debt:total exports) would fall to 180 percent, implying a cumulativecurrent account surplus of $30.6 billion and cumulative imports of $178.5 billionover the period. This compares with the composite debt ratio of 330 percent in1987. If, however, export growth were only 3 percent per year, debt cancellationof $5 billion would be required to accomplish a comparable current accountsurplus and import figure. Because it is bound to be affected by suchcancellations, commercial bank lending would be in clear jeopardy under thelatter scenario, while the requirements for external support would also strainthe international community's overall ability to bridge Africa's resource gaps.

Generally speaking, the banks should be pulled closer into the dialogue overAfrican external finance in the 1990s, rather than marginalized on the basis oftheir own apparently diminished interest and the problem of Africa's commercialborrowing capacity. The challenge is to encourage all potential partners,including the commercial banks, to contribute their particular skills andresources to developing Africa's potential.

B. PROSPECTS AND PROPOSALS FOR THE ALLEVIATION OF CONSTRAINTS

It was quite clear from the interviews that the scope of the commercial banks'activities and their future plans for Africa have never been narrower, as seenin the limited range of perceived opportunities represented in Chapter II. Whilethe industry possesses the institutional skills to lend to Africa, as a wholeits posture is a passive one, particularly with regards to medium-term lending.For have the banks been actively engaged by policy-makers in a search forinnovative solutions. Having witnessed the deterioration in their Sub-Saharanportfolios over the past 3 years, however insignificant these amounts might bein comparison to the banks' total assets, on the whole the banks appear resignedto "waiting out the debt crisis" while re-focusing elsewhere the financial andhuman resources once devoted to Africa.

Policy-makers should not be overly discouraged by this passive situation. Asevoked above, Africa's commercial potential is vast and there is scope forstimulating commercial bank lending during the 1990s. However, if the Africanand OECD government communities wish to see a resumption of lending to Africa,it appears that they will have to take much of the initiative for restoringgenuine interest and confidence among the banks. A number of concretesuggestions are presented for discussion in this section.

An appropriate starting point would be to address the constraints cited by thebanks (detailed in Chapter II), in conjunction with the broader initiativesunderway to resolve the immediate debt crisis and restore economic growth. Asthe context improves, these efforts should be supplemented by a more direct,promotional approach that would encourage the banks to observe and analyze more

Page 25

carefully the changes taking place in the region which could lead to a resumptionin wider-ranging marketing activities.

1. Mandatory Provisions on New Lending

Manidatory provisioning regulations generally imply an immediate loss on new loansextended to the affected African countries and thus represent a powerfuldisincentive to new lending. Some banks have already established excessprovisions, or achieved a critical mass of "revolving provisions", where normaldebt servicing permits past provisions to be reversed, offsetting provisions onnew loans in the relevant accounting period. In these cases the provisioningrequirements would not necessarily ifncrease their aggregate loan loss reserveexpenses.

Given the small share of African debt in most banks' portfolios, and theextremely conservative posture of the banks, a strong case can and should be madeto the regulatory authorities for the elimination of these provisioningrequirements as quickly as possible.

As a positive development in this connection, the banking authorities in mostcountries, including France, the UK and the Netherlands, have ruled that co-financings with IFC and in some cases other multilateral lenders, under the typesof structures currently offered by these agencies, are exempted from provisioningrules. Some jurisdictions accord similar treatment to other well-securedtransactions (such as aircraft financings or cash-collateralized facilities),a practice which should be extended to an ever-increasing range of transactions,if not across-the-beard.

2. Co-Financing

The principal rationale for seeking commercial bank participation in co-financedfacilities is to leverage the official agencies' risk and funds, bearing in mindthat when donors are prepared to bear all of the risk, they are capable ofobtaining lower-cost funding than that provided by the banks.

Nevertheless, there is scope for rethinking the way that risk is allocated.Until now, it has been the practice of the major official co-financing agencies,excepting IFC with its "lender of record" system, to finance and/or guaranteea certain portion of the principal, leaving Lo Lhe oLhei pa± Licipat-Lts th Le balanceof all risks inherent in the transaction. IHowever, some of the bilateralpolitical risk insurance programs maintained by agencies such as the U.S.Overseas Private Investment Corporation (OPIC), do provide coverage for loansto eligible countries.

In countries where this appears necessary, it is not impossible from a technicalstandpoint to devise a formula whereby the sponsoring agency in "parallelfinancing" arrangements would take a larger portion of the sovereign and/ortransfer risk on a transaction, while the private participants would bear a

Page 26

larger portion of the commercial .isk. The principal difficulty lies in drawingthe line between political and commercial risk.

A potentially simple and clear formula would be as follows:

- if the borrowing entity has the necessary local currency funds and hasapplied for a foreign exchange transfer, but for any reason the transferis not made, the sponsoring institution's transfer risk guarantee of thecommercial bank funded portion of the facility will be invoked; and

- if the borrowing entity for any reason does not have the local currencyfunds available to apply for a foreign exchange transfer, the commercialbanks' commercial risk guarantee of the donor funded portion of thefacility will be invoked.

While neither the agencies nor the banks are likely to provide such guaranteesfor 100% of the principal amount of a given loan, the concept recognizes thecomparative advantage of the official agencies in assessing the transfer risk,providing balance-of-payments support to countries on a long-term basis, andencouraging debt service. In parallel, it would place more of the onus foranalyzing project risk on the participating banks. The commercial banks wouldnot obtain unfair advantage by such a procedure, as commercial risk can indeedbe considerable, involving a wide range of variables from climatic and marketconditions to management performance. I

The suggested formula is not a panacea however, particularly for transactionsin countries where banks have insufficient understanding of or confidence in thepolicy and political environment. Banks are aware that changes in the economicenvironment, even those changes that are necessary and beneficial, such asdevaluation, as well as uncertainties relating to government ownership of orpotential interference in the affairs of a borrowing entity, can be detrimentalto the borrowers' local currency solvency, affecting debt service performancejust as surely as any lack of foreign exchange availability.

These issues are not easy to address, and are best resolved through the improvedeconomic health, economic management and political performance of the borrowingcountry, as well as through continued fine tuning of improved risk-sharingmechanisms over the longer term. For more immediate results, a strictdistinction between the foreign exchange and local currency performance of agiven transaction, based on a reasonable "valuation" of each type of risk and

limited to appropriate percentages of principal, seems more promising.

Discussions or experiments concerning a more realistic allocation of risk shouldalso be accompanied by heightened sensitivity to the banks' concerns aboutpricing and the time lags involved in completing co-financing packages. On thelatter point, IFC's recently established "agency agreement" with the Dutch bank