World Bank Document - Documents & Reports · PROJECT APPRAISAL DOCUMENT ON A PROPOSED LOAN IN THE...

63

Document of The World Bank Report No: 21778-AL PROJECT APPRAISAL DOCUMENT ON A PROPOSEDLOAN IN THE AMOUNT OF US$18.0 MILLION TO THE PEOPLE'S DEMOCRATIC REPUBLIC OF ALGERIA FOR AN ENERGY AND MINING TECHNICAL ASSISTANCE LOAN (EMTAL) February 2, 2001 InfrastructureDevelopment Group Middle East and North Africa Region Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Document - Documents & Reports · PROJECT APPRAISAL DOCUMENT ON A PROPOSED LOAN IN THE...

Document of

The World Bank

Report No: 21778-AL

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED LOAN

IN THE AMOUNT OF US$18.0 MILLION

TO THE

PEOPLE'S DEMOCRATIC REPUBLIC OF ALGERIA

FOR AN

ENERGY AND MINING TECHNICAL ASSISTANCE LOAN (EMTAL)

February 2, 2001

Infrastructure Development GroupMiddle East and North Africa Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

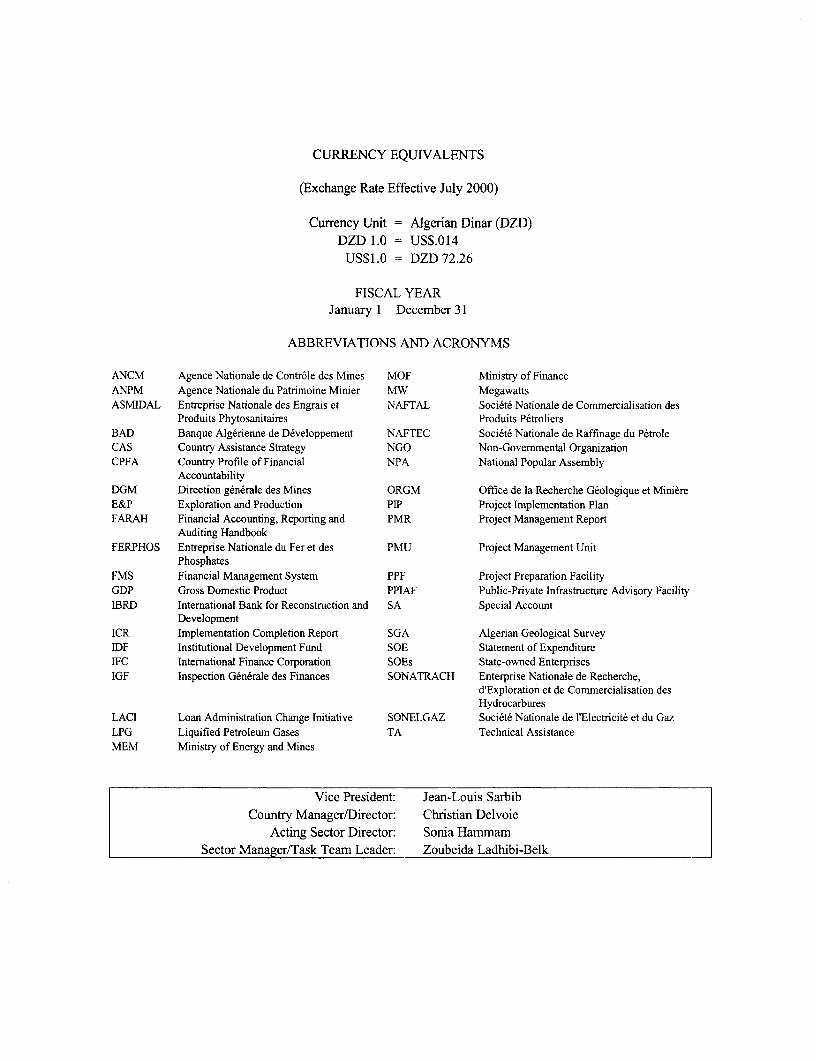

CURRENCY EQUIVALENTS

(Exchange Rate Effective July 2000)

Currency Unit = Algerian Dinar (DZD)DZD 1.0 = US$.014

US$1.0 = DZD 72.26

FISCAL YEARJanuary 1 December 31

ABBREVIATIONS AND ACRONYMS

ANCM Agence Nationale de Contr6le des Mines MOF Ministiy of FinanceANPM Agence Nationale du Patrimoine Minier MW MegawattsASM1DAL Entreprise Nationale des Engrais et NAFTAL Societe Nationale de Commercialisation des

Produits Phytosanitaires Produits Petroliers

BAD Banque Algerienne de Developpement NAFTEC Societ6 Nationale de Raffinage du PetroleCAS Country Assistance Strategy NGO Non-Governmental OrganizationCPFA Country Profile of Financial NPA National Popular Assembly

AccountabilityDGM Direction generale des Mines ORGM Office de la Recherche Geologique et MiniereE&P Exploration and Production PIP Project Implementation PlanFARAH Financial Accounting, Reporting and PMR Project Management Report

Auditing HandbookFERPHOS Entreprise Nationale du Fer et des PMU Project Management Unit

Phosphates

FMS Financial Management System PPF Project Preparation FacilityGDP Gross Domestic Product PPIAF Public-Private Infrastructure Advisory FacilityIBRD International Bank for Reconstruction and SA Special Account

DevelopmentICR Implementation Completion Report SGA Algerian Geological SurveyIDF Institutional Development Fund SOE Statement of ExpenditureLFC International Finance Corporation SOEs State-owned EnterprisesIGF Inspection Generale des Finances SONATRACH Enterprise Nationale de Recherche,

d'Exploration et de Commercialisation desHydrocarbures

LACI Loan Administration Change Initiative SONELGAZ Societe Nationale de l'Electricite et du GazLPG Liquified Petroleum Gases TA Technical AssistanceMEM Ministry of Energy and Mines

Vice President: Jean-Louis SarbibCountry Manager/Director: Christian Delvoie

Acting Sector Director: Sonia HammamSector Manager/Task Team Leader: Zoubeida Ladhibi-Belk

ALGERIAENERGY AND MINING TECHNICAL ASSISTANCE LOAN (EMTAL)

CONTENTS

A. Project Development Objective Page

1. Project development objective 22. Key performance indicators 2

B. Strategic Context

1. Sector-related Country Assistance Strategy (CAS) goal supported by the project 22. Main sector issues and Government strategy 23. Sector issues to be addressed by the project and strategic choices 6

C. Project Description Summary

1. Project components 62. Key policy and institutional reforms supported by the project 83. Benefits and target population 84. Institutional and implementation arrangements 9

D. Project Rationale

1. Project alternatives considered and reasons for rejection 112. Major related projects financed by the Bank and other development agencies 123. Lessons learned and reflected in proposed project design 134. Indications of borrower commitment and ownership 135. Value added of Bank support in this project 13

E. Summary Project Analysis

1. Economic 142. Financial 143. Technical 144. Institutional 155. Environmental 166. Social 177. Safeguard Policies 18

F. Sustainability and Risks

1. Sustainability 182. Critical risks 193. Possible controversial aspects 20

G. Main Loan Conditions

1. Effectiveness Condition 20

2. Other 20

H. Readiness for Implementation 21

I. Compliance with Bank Policies 21

Annexes

Annex 1: Project Design Summary 22

Annex 2: Detailed Project Description 28

Annex 3: Estimated Project Costs 42

Annex 4: Cost Benefit Analysis Summary, or Cost-Effectiveness Analysis Summary 43

Annex 5: Financial Summary for Revenue-Earning Project Entities, or Financial Summary 44

Annex 6: Procurement and Disbursement Arrangements 45

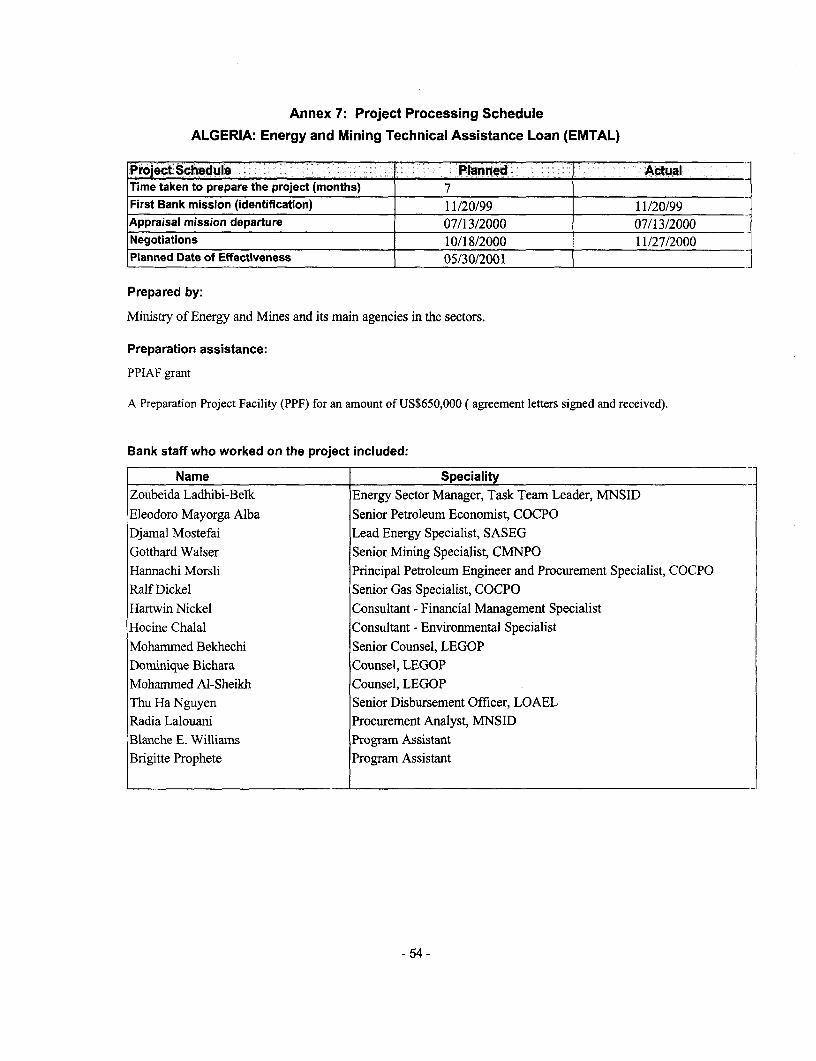

Annex 7: Project Processing Schedule 54

Annex 8: Documents in the Project File 55

Annex 9: Statement of Loans and Credits 56

Annex 10: Country at a Glance 57

MAP(S)IBRD 29992

ALGERIA

Energy and Mining Technical Assistance Loan (EMTAL)

Project Appraisal Document

Middle East and North Africa RegionMNSID

Date: February 2, 2001 Team Leader: Zoubeida Ladhibi-BelkCountry Director: Christian Delvoie Acting Sector Dir.: Sonia HammamProject ID: P067567 Sector(s): GP - Oil & Gas Transportation, NN - Mining &

Other Extractive, PP - Electric Power & Other EnergyAdjustment

Lending Instrument: Technical Assistance Loan (TAL) Theme(s): Energy; MiningPoverty Targeted Intervention: N

Project Financing Data[X] Loan [ ] Credit [ ] Grant [ ] Guarantee [ Other:

For Loans/Credits/Others:Amount (US$m): 18.0

Proposed Terms: Fixed-Spread Loan (FSL)Grace period (years): Years to maturity: 16.5Commitment fee: 0.85% of Service charge: %undisbursed balances for first fouryears; 0.75% thereafterFront end fee on Bank loan: 1.00%Financing Plan: Source Local Foreign TotalBORROWER 4.00 0.00 4.00IBRD 1.80 16.20 18.00

Total: 5.80 16.20 22.00

Borrower: GOVERNMENT OF ALGERIAResponsible agency: MINISTRY OF ENERGY AND MINES

Address: 80, Avenue Ahmed Ghermoul, Algiers, AlgeriaContact Person: Ms. Nour-El-Houda Boughalem, Project Management Unit ManagerTel: 213-21-67-02-78 Fax: 213-21-67-03-37 Email: [email protected]

Estimated disbursements ( Bank FY/USSM):FY 2001 2002 2003 2004 2005

Annual 1.50 4.00 6.50 4.50 1.50Cumulative 1.50 5.50 12.00 16.50 18.00

Project implementation period: 4.5 years: July 01, 2000 - December 31, 2004Expected effectiveness date: 05/30/2001 Expected closing date: 06/30/2005

X:S PAD Fon R.v Mwdh, 2000

A. Project Development Objective

1. Project development objective: (see Annex 1)

In December 1999, the Government of Algeria announced its new policy and strategic objectives for theenergy and mining sectors. The main thrust of this policy is to: (i) improve efficiency in the energy andmining sectors while securing adequate energy supplies to the economy; (ii) allow market forces to playtheir respective roles; (iii) increase revenues by further developing untapped resources; (iv) addressenvironmental concerns; (v) promote efficient use of public resources and protect public interest; and (vi)alleviate the financial burden of energy and mining enterprises on public finances.

The proposed project will assist the Ministry of Energy and Mines (MEM) to implement the Government'smarket-oriented reform program in the energy and mining sectors, and would particularly assist in the: (i)separation of the role of the state, as policy maker, regulator and owner of mining resources, from its roleas owner of public enterprises, enabling these latter to become fully commercially-oriented entities; (ii)development and implementation of a legal and institutional environment conducive to develop marketmechanism, increase competition, and private sector participation; (iii) improvement of service quality andenergy access, energy efficiency and environmental standards; and (iv) state-owned enterprises (SOEs)'efforts to adapt to sector reforms and the new business environment. Also, the proposed project will assistMEM in launching its first and innovative power generation plant(s) for 2000MW with private sectorparticipation.

2. Key performance indicators: (see Annex 1)

Progress towards achieving the project development objective will be monitored with the following keyperformance indicators for each of the sectors (mining, electricity and hydrocarbons):

* increase in private sector participationa improvement in the efficiency of the restructured SOEs* increase in Government's revenues from the sector* reduction of pricing subsidies.

B. Strategic Context1. Sector-related Country Assistance Strategy (CAS) goal supported by the project: (see Annex 1)Document number: 15316-AL Date of latest CAS discussion: 02/05/96

The project will contribute to the Government of Algeria's objective of achieving sustainable economicgrowth through increased competition and private sector participation. The legal, regulatory andinstitutional reforms supported by the project will create an enabling environment conducive to morecompetition and private sector participation. It is expected that the next CAS, scheduled for FY2002, willtake up these objectives.

2. Main sector issues and Government strategy:

Main Sector Issues:

The fundamental issues in the energy and mining sectors in Algeria are:

* Volatility of oil and gas prices having considerable impact on the macro-economic situation

- 2 -

of Algeria. Algerian economy is heavily dependent on the income from the export of crude oil,oil products and natural gas, which accounted for about 30% of GDP in 1998. Therefore thevolatility of oil prices is having a considerable impact on the macro economic situation ofAlgeria. Because of the importance of hydrocarbons revenues, the collapse in intemationalprices in 1998, which led to about 40% fall in total export revenues, largely explains thecontraction of GDP growth from an average annual increase of 4.5 percent in 1995-1998, to anaverage decline of 0.4 percent between 1998-1999. Hydrocarbons are expected to remain thepredominant source of export earnings for years to come, generating some U$15-20 billion peryear during the period 2000-2005, depending on the crude oil price. Similarly to virtually allproducer countries, Algeria experienced a fiscal crisis (limited access to foreign credit) andbalance of payments crisis. It has tried to increase diversification of its source of revenues byinvesting more in export of petroleum products and natural gas.

* Sector operated by quasi-monopolistic state-owned enterprises (SOEs) that play both stateand commercial roles with limited managerial autonomy. In the hydrocarbons sector,SONATRACH focuses on oil and gas research, exploration, production, transport, marketing andexport; NAFTEC is the refining enterprise, and NAFTAL is responsible for distributinghydrocarbons products within the country. In the electricity sector, SONELGAZ is a fullyintegrated SOE responsible for generation, transmission and distribution of electricity anddistribution of natural gas by pipeline. As for the mining sector, exploration services aremonopolized by the state-owned agency, Office de la Recherche Geologique et Miniere (ORGM),and industrialized operations are dominated by the enterprises of the state-controlled Holding SidMines. It has been recognized by all concemed parties, that this institutional arrangement giveslimited incentives to stimulate managerial dynamism, control costs, and improve efficiency.

* Pricing systems with levels below economic costs that provide implicit subsidies for certainconsumers, and lead to wasteful consumption and limited cost efficiency. There is currently adistortion between domestic prices and intemational prices with an impact on Governmentrevenues and equity distribution. In the hydrocarbons sector, a preliminary estimate of thesesubsidies amounts to about US$ 500 million per year. In the electricity sector, while high voltageand medium tariffs are already above and near their economic cost respectively, low voltagetariffs, which relate to about 42% of total consumption, are still below economic costs.

* Sectors are putting a burden on public finances either for investment finances orconsumption subsidies. As a result of the institutional arrangements, the pricing policydescribed above, and high debt service requirements, the SOEs are financially constrained andunable to maintain let alone expand their productive capacity. In the electricity sector forexample, Govemrnment contributions amounted to about US$ 1.0 billion in 1998.

* Substantial capital requirements to meet demand and to optimize the use of Algeriannatural resources and increase Government's revenues. As indicated in the Govemrnment'sprogram, hydrocarbons exploration, production, refining and distribution need to be enhanced;SONATRACH's investment requirements for the next 5 years are estimated at about US$ 20billion. In the electricity sector, needs to meet future demand as well as to rehabilitate theexisting power system and reduce system bottlenecks, are estimated at about US$ 12.0 billion forthe next 10 years. Finally the mining sector is characterized by substantial untapped resources,due to lack of financial resources for exploration and development.

- 3 -

* Little private sector participation in the sectors. Despite the adoption of the 1991 petroleumlegislation which opened the hydrocarbons sector to investments by foreign oil companies,exploration activities are low compared to the potential and remain concentrated in prolific areas;and refining and distribution of petroleum products remain almost exclusively the responsibilityof SOEs. In the electricity sector, responsibility for generation, transmission and distribution ofelectricity remains with Sonelgaz and attempts towards introducing private sector participationare just at the initial stages. As for the mining sector, the existing legal and institutionalframework maintains considerable barriers to private investment, resulting in difficult access tomineral resources because of discretionary and unclear conditions to obtain and maintain miningtitles, unavailability of adequate data, perceived unstable investment conditions, and a sectordomination by mining SOEs.

* Large scope for improving energy efficiency. Algeria has taken several steps to improveend-use energy efficiency and conservation. The Agence pour la Promotion de la Rationalisationde l'Utilisation de l'Energie (APRUE), a national agency, under the authority of the Ministry ofEnergy and Mines, has been established to promote energy efficiency and conservation. In 1999,Algeria has enacted a law on energy efficiency and conservation which sets up a national fundfor energy efficiency and makes energy audits compulsory. In spite of these measures, thepotential for improving end-use energy efficiency remains large, and its realization wouldrequire, as demonstrated in other countries, the development of incentive measures, competitivepressures, market-based energy and financial services.

v Limited awareness to environmental issues. In the upstream sector there are pending issuessuch as significant gas flaring which impact on the global environment, and also local issuessuch as oily waters from the production facilities discharged in the environment. The downstreamsector is still struggling with non-compliance with the decree 93-160 on industrial effluentsdischarges in the environment which impact on coastal zones, wadis and harbor environments.The downstream sector is also characterized by air pollution problems coming from refiningfacilities, storage facilities and by fuel quality problems essentially due to lead content ofgasoline. Despite the adoption of environmental Law in 1983 (Law 83-03), environmental rulesand regulations are still to be improved.

Government Strategv:

As stated earlier, the energy and mining sectors are critical to the overall Algerian economy, accounting forabout 95% of total exports and 60% of budgetary revenues. During the years of high oil prices, the statehad the resources to provide employment, infrastructure and services through an inefficient centrallycontrolled system. Social indicators improved markedly and poverty declined thanks to high investment ineducation, health, basic infrastructure, and generous subsidies. The decline in oil prices in the 1980s put anend to this, highlighting the inefficiencies of the economic structure. Unemployment grew rapidly to 25percent, and acute housing shortages developed. The housing crisis was further compounded by a highpopulation growth rate (2.9 percent) and continued rural migration to cities.

The Government recognizes that the rehabilitation and growth of the overall economy hinges to a largeextent on addressing the issues listed above through profound reforms and strengthening of the energy andmining sectors. Efforts to introduce reforms in the sectors have been initiated as early as 1991 in thehydrocarbons sector and 1995 in the power sector, when Sonelgaz and the Government commissioned aPower Sector Restructuring Study, used as a basis for the proposed reform program in the power sector.However, much remains to be done and the Government's program as outlined in December 1999 has

- 4 -

established long-range policies for the energy and mining sectors to: (i) modernize and strengthen the legal,regulatory and institutional frameworks; (ii) maximize the role of competition and market forces; (iii)establish economic principles and commercial incentives; (iv) promote private sector participation in allactivities by creating a level playing field for the private investors and the SOEs; and (v) reorganize thecorporate structure of the SOEs. Government's strategy for the sectors is in Project files and wasconfirmed formally to the Bank by letter dated August 7, 2000.

Specific to the hydrocarbons sector, the Government strategy is to: (a) establish an enabling legal andinstitutional framework conducive to private investments through a new hydrocarbons law being prepared;(b) set-up new autonomous regulatory and contracting agencies, that will take over the governmentfunctions currently exercised by SONATRACH; (c) gradually deregulate prices and open the downstreammarkets to private participation and competition; (d) introduce a model contract and tender procedure foraward of exploration/development rights, ensuring both streamlining and transparency in the procedure andintemational competitiveness; (e) encourage private investments downstream and improve the quality offuels; (f) update and enforce environmental impact assessment procedures, and develop environmentalprotection standards; and (g) optimize the valorization of gas resources both for export and domesticmarket, through a strategy of diversification and market penetration. During negotiations, agreementshave been reached that the process of submission of a draft hydrocarbon law, acceptable to the Bank, tothe Competent Authorities,i.e Council Of Government, Council of Ministers as well as the NationalPopular Assembly (NPA), will be completed no later than December 31, 2001.

In the electricity sector, the key policy objective is to meet rapidly rising demand while maintaining qualityof service at reasonable cost. The institutional framework is being defined in an electricity law thepreparation of which is well advanced. The draft law provides for an enabling legal and institutionalframework conducive to private investments in generation and distribution with the following principles: (a)generation will be deregulated and subject to market forces; (b) transmission will remain publicly ownedand provide open access to suppliers and purchasers; (c) distribution as a natural monopoly will be fullyregulated; (d) prices will be liberalized at the generation level and regulated at the transmission anddistribution levels; (e) retail competition will be introduced for large consumers; (f) an independentregulatory authority will be established; and (g) Sonelgaz will be reorganized to adjust to the new legalframework and market forces. During negotiations, agreements have been reached that the process ofsubmission of a draft electricity law, acceptable to the Bank, to the Competent Authorities,i.e Council OfGovernment, Council of Ministers as well as the National Popular Assembly (NPA), will be completedno later than June 30, 2001.

In the case of mining, the legal regulatory and institutional framework has been reviewed and defined in anew draft mining law approved by the Council of Government and the Council of Ministers, and submittedto the NPA for approval. The new mining law establishes: (a) an enabling legal framework tosignificantly increase private investment in Algeria's mining sector; (b) sector institutions to effectivelyenforce laws and regulations, administer mining titles, and monitor sector performance and development;(c) provisions for environmental and safety protection during the whole mining operation cycle; and (d) theprovision of basic geological data and other services for promotion of private investments.

- 5 -

3. Sector issues to be addressed by the project and strategic choices:

The project will help addressing the sector issues as identified in Section 2. Through the establishment ofadequate legal and institutional framework conducive to private sector participation, the strengthening ofexisting and/or creation of new institutions in the sectors, the reliance on market forces to establish prices,and the reorganization of SONELGAZ and other enterprises in the mining subsector to adjust to the newstrategy, the project will set the stage to:

* demonopolize the sector activities with the exception of the natural monopolies, and increasecompetition;

* help control costs and improve efficiency of the sectors* increase private sector participation;* develop operations in an environmentally sustainable manner;* increase Government revenues; and* reduce the burden of the sectors on public finances.

A prerequisite for all these reforms is the commitment (i) to reach consensus on principles of reforms withall stakeholders, including labor unions, SOEs; and (ii) to develop a comprehensive strategy and road mapper sub-sector, identifying options and action plans in order to meet the objectives of the reform. Theanalysis of the various options led the Government to make several strategic choices which have been thebasis for designing the proposed project:

(i) Private versus public ownership: The Government has opted to introduce gradually private participationin the development and operations of the sectors, which is consistent with its strategy to primarily directpublic resources to social sectors, and increase Government's revenues. Accordingly, and as a first step,SOEs in the electricity and mining subsectors will be restructured to become more commercially-orientedentities.

(ii) Creation of autonomous regulatory agencies for each subsector (i.e hydrocarbons, electricity andmining): The Government has committed to divest MEM's existing regulatory functions and to empowerand staff an independent regulatory authority for each subsector.

(iii) One versus three regulatory agencies: Given the status of preparation of the various laws, and inorder to expedite the process while taking into account the specifics of each sector, the decision was takento go with three separate regulatory authorities, one each for hydrocarbons, electricity and the miningsubsector. The possibility of combining two or three agencies will remain open for the future.

(iv) Multi-buyer model in the electricity sector and retail competition: The Government is planning toimplement models which would progressively provide wholesale competition and also allow thedevelopment of retail competition.

C. Project Description Summary

1. Project components (see Annex 2 for a detailed description and Annex 3 for a detailed costbreakdown):

The project would comprise the following components (Annex 2 also provides a brief background andstrategy for reforms for each subsector):

-6 -

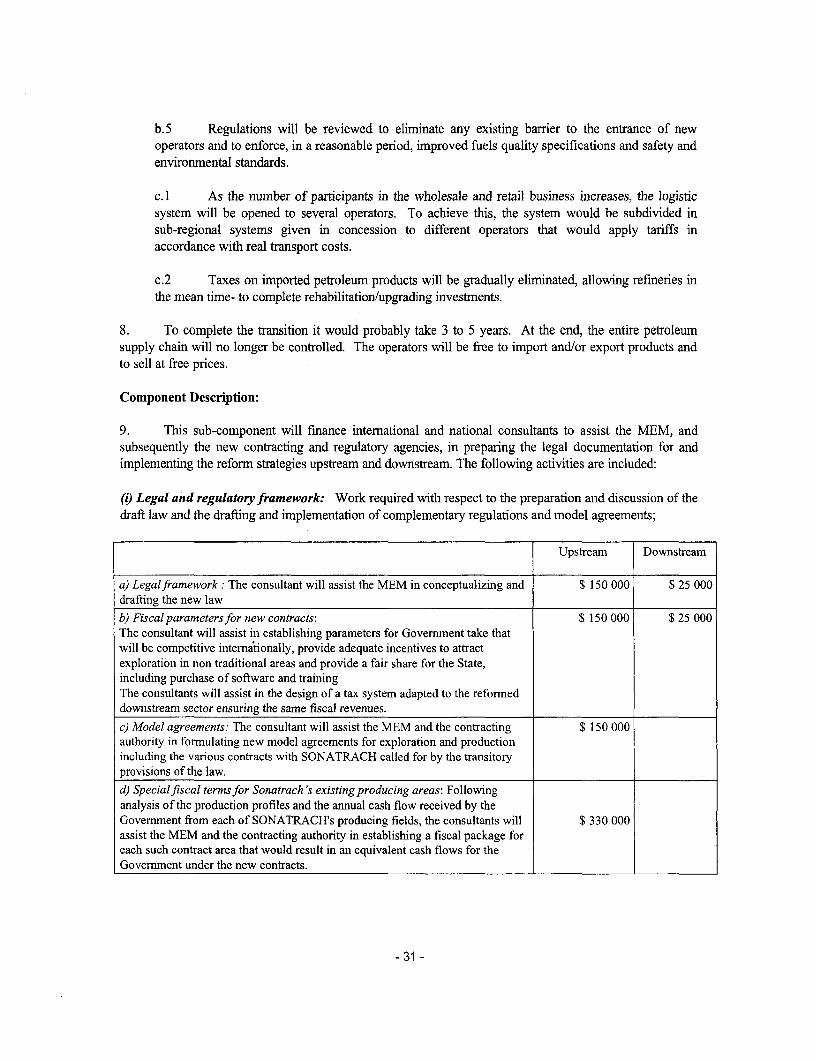

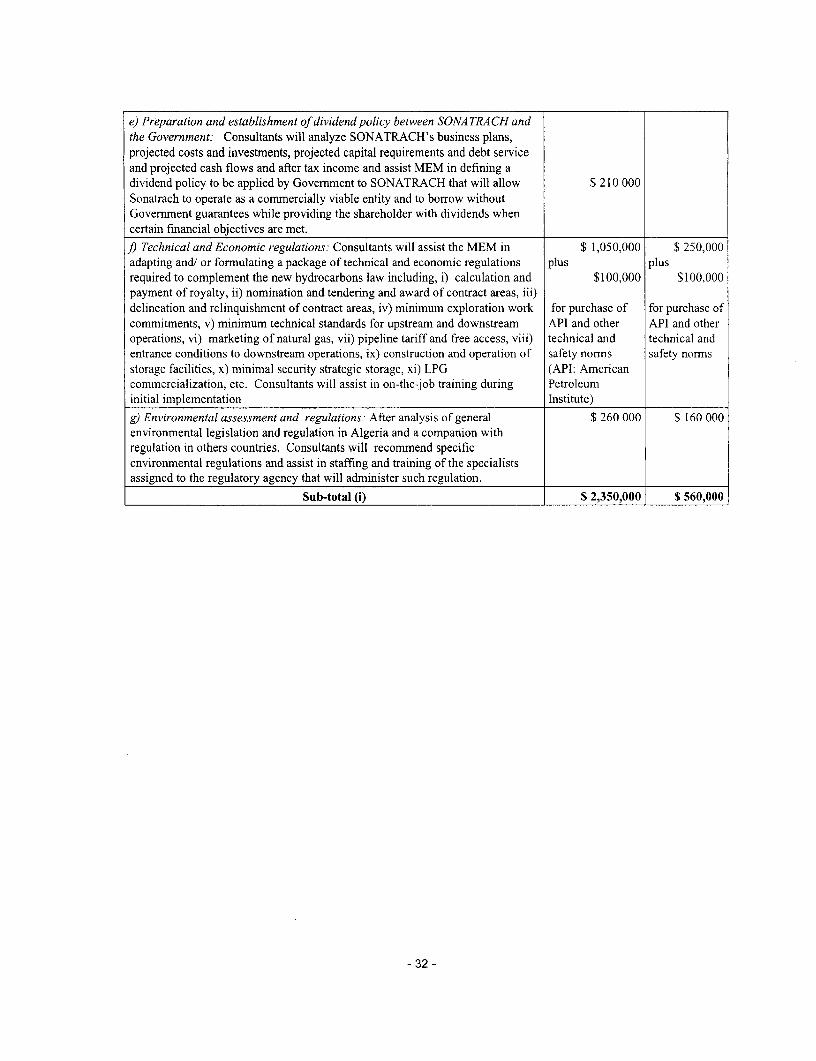

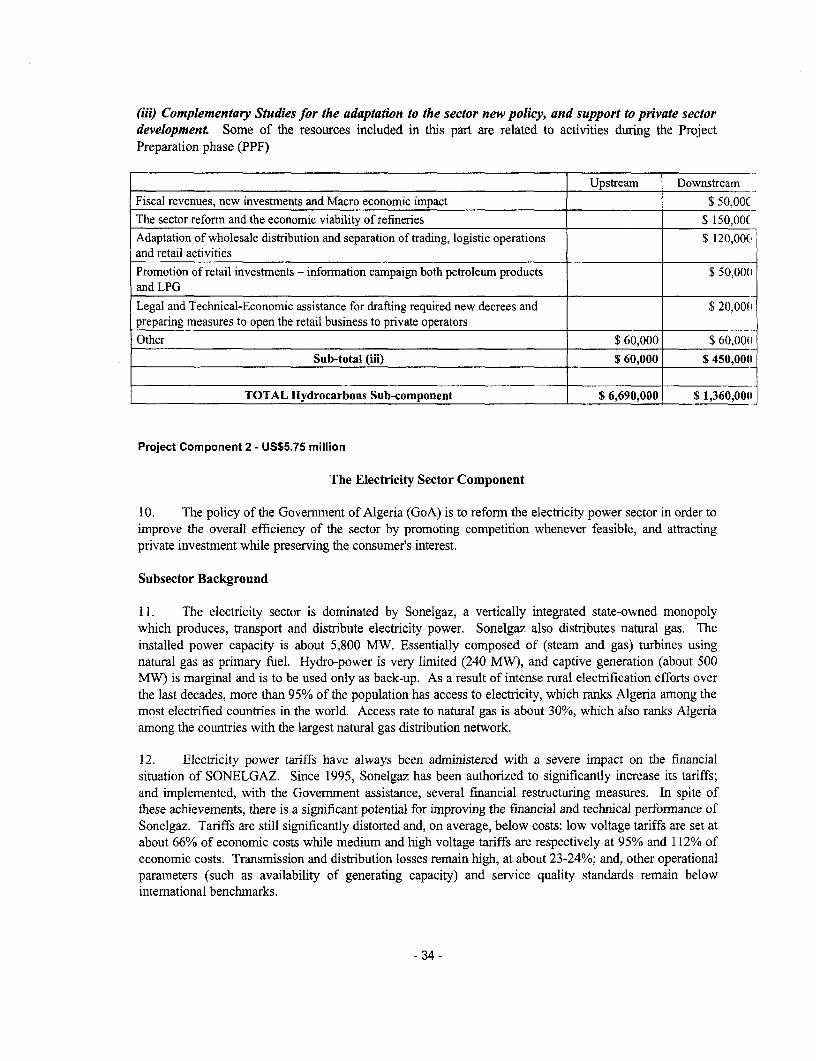

(a) Hydrocarbons: (i) review, design and implementation of a legal, regulatory and institutionalframework, upstream and downstream, consistent with the proposed strategy and reforms includingthe development of suitable environmental policies and regulations for the hydrocarbon sector on thebasis of sectoral environmental assessments for said sector; (ii) set-up and assistance in initialoperation of a contract management and promotion agency with a state of the art data center; (iii)set-up and assistance in initial operation of an autonomous regulatory entity; and (iv) training ofrelevant staff.

(b) Electricity: (i) review, design and implementation of a legal, regulatory and institutionalframework, for electricity and natural gas distribution by pipelines, consistent with the proposedstrategy and reforms including the development of suitable environmental policies and regulationsfor the electricity sector on the basis of sectoral environmental assessments for said sector; (ii)design, establishment, and operation of an autonomous regulatory entity and, at a later stage, asystem operator and a market operator; (iii) implementation of the restructuring and reform programof the sector in general and the reorganization of SONELGAZ in particular; (iv) assistance in thelaunching of an innovative and challenging first power generation program with private sectorparticipation ("2000 MW Project"), to be used for local market and export; and (v) training ofrelevant staff of the various sector institutions mainly in reforms and regulations.

(c) Mining: (i) review, design and implement the legal, regulatory and institutional framework andrespective regulations consistent with the proposed strategy and reforms including the developmentof suitable environmental policies and regulations for the mining sector on the basis of sectoralenvironmental assessments for said sector; (ii) establishment and assistance for initial operation ofan autonomous national agency for geological survey and mining control and an autonomousnational cadastral agency; (iii) implementation of a mining promotion program; (iv) assistance to theHolding SIDMINES {comprising the Entreprise Nationale du Fer et des Phosphates (FERPHOS),the Entreprise Nationale des Engrais et Produits Phytosanitaires (ASMIDAL), and the EntrepriseNationale du Marbre (ENAMARBRE)}, the Office de la Recherche Geologique et Miniere(ORGM), and the Entreprise Nationale de l'Or (ENOR), in their effort to adapt to the sector reform,and with strategic private partnership; and (v) training.

(d) PMU: institutional strengthening of MEM and set-up of a Project Management Unit (PMU)within MEM.

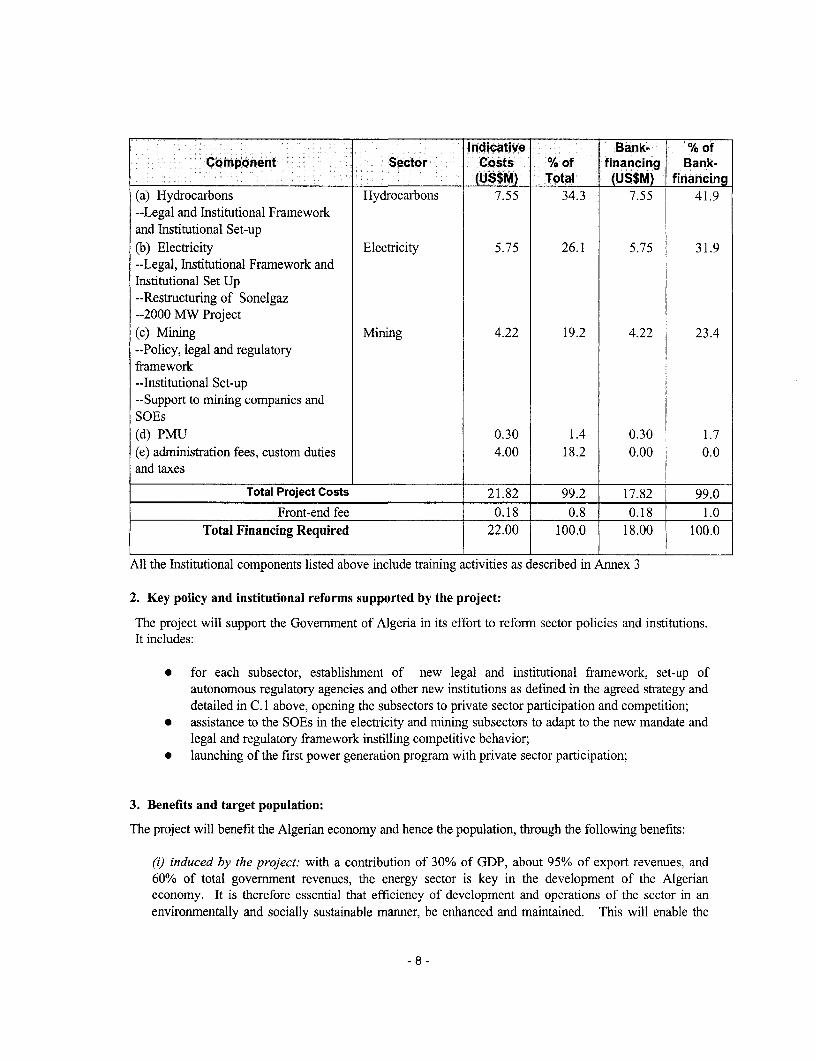

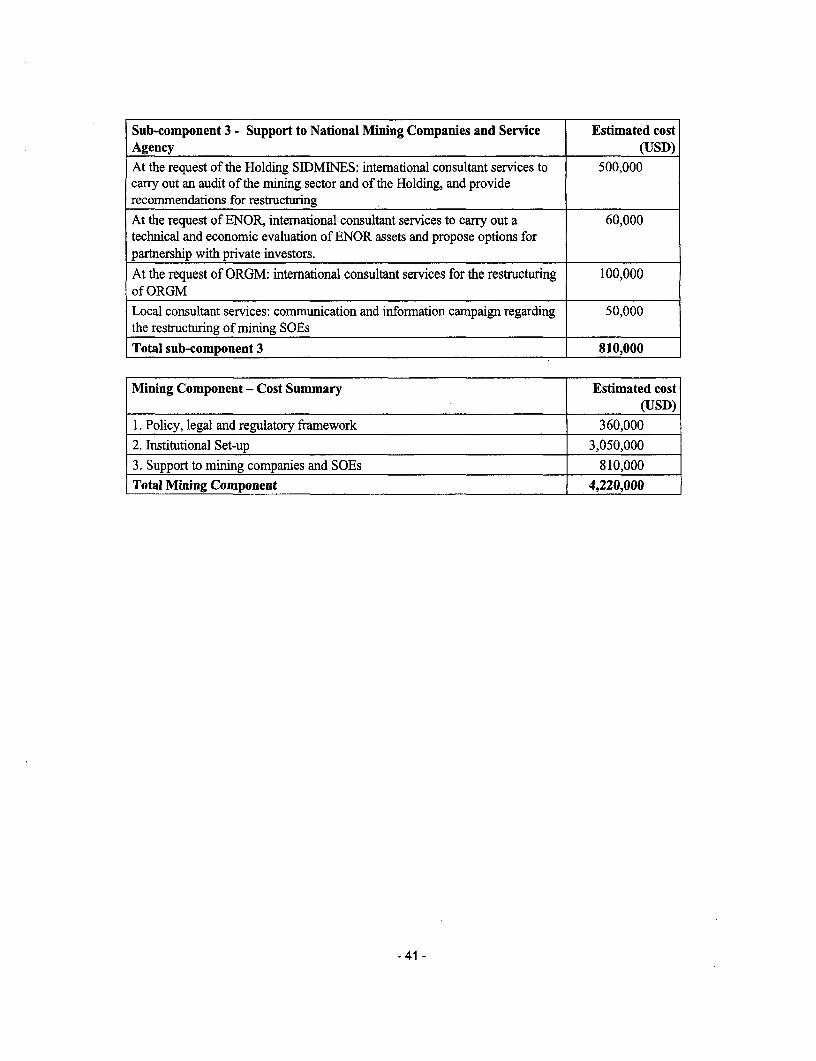

Estimated cost: Table below gives the summary of the estimated costs by components (includingcontingencies):

-7-

Indicative Bank- % ofComponent Sector Costs % of financing Bank-

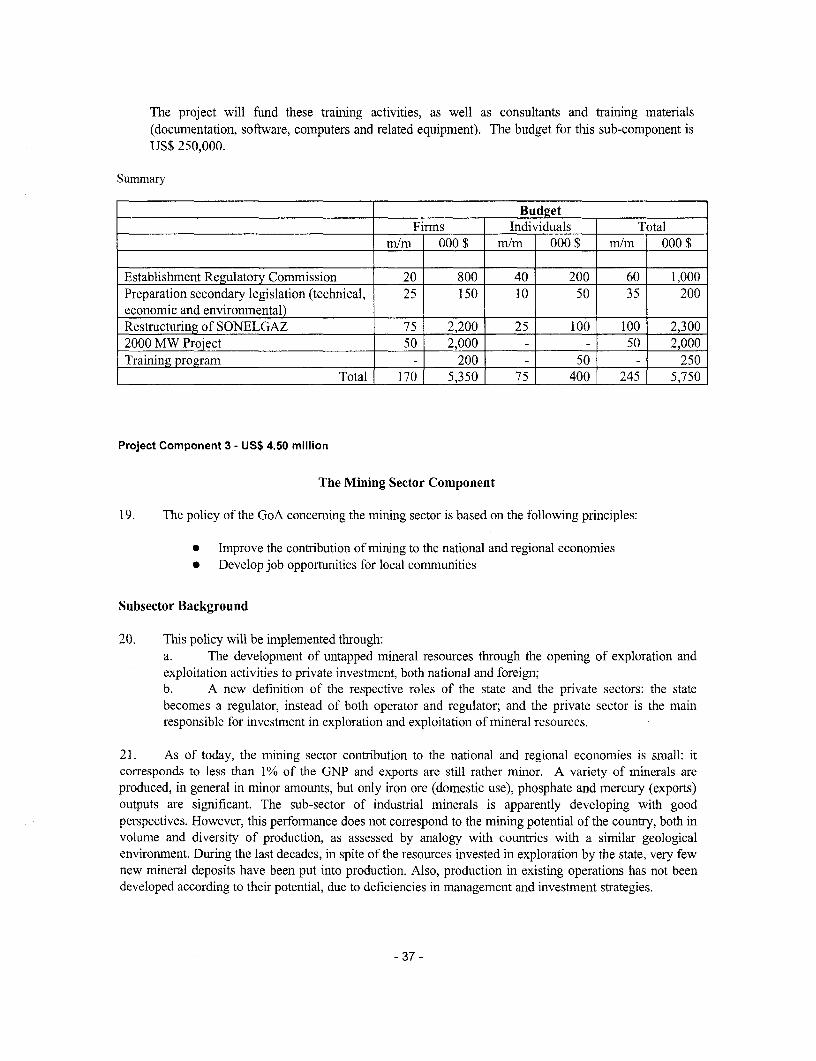

S(U$M) Total (US$M) financing(a) Hydrocarbons Hydrocarbons 7.55 34.3 7.55 41.9--Legal and Institutional Frameworkand Institutional Set-up(b) Electricity Electricity 5.75 26.1 5.75 31.9--Legal, Institutional Frarnework andInstitutional Set Up--Restructuring of Sonelgaz--2000 MW Project(c) Mining Mining 4.22 19.2 4.22 23.4--Policy, legal and regulatoryframework--Institutional Set-up--Support to mining companies andSOEs(d) PMU 0.30 1.4 0.30 1.7(e) administration fees, custom duties 4.00 18.2 0.00 0.0and taxes

Total Project Costs 21.82 99.2 17.82 99.0

Front-end fee 0.18 0.8 0.18 1.0Total Financing Required 22.00 100.0 18.00 100.0

All the Institutional components listed above include training activities as described in Annex 3

2. Key policy and institutional reforms supported by the project:

The project will support the Government of Algeria in its effort to reform sector policies and institutions.It includes:

* for each subsector, establishment of new legal and institutional framework, set-up ofautonomous regulatory agencies and other new institutions as defined in the agreed strategy anddetailed in C. 1 above, opening the subsectors to private sector participation and competition;

* assistance to the SOEs in the electricity and mining subsectors to adapt to the new mandate andlegal and regulatory framework instilling competitive behavior;

* launching of the first power generation program with private sector participation;

3. Benefits and target population:

The project will benefit the Algerian economy and hence the population, through the following benefits:

(i) induced by the project: with a contribution of 30% of GDP, about 95% of export revenues, and60% of total government revenues, the energy sector is key in the development of the Algerianeconomy. It is therefore essential that efficiency of development and operations of the sector in anenvironmentally and socially sustainable manner, be enhanced and maintained. This will enable the

- 8-

Government to further support economic growth, and the social infrastructure to meet the needs of thepoor.

(ii) as a direct result of the project: (a) establishment of a modem, consistent and homogeneous energyand mining legal and regulatory framework, and state of the art institutions that will provide thegovernance to protect public interest, and assure efficient use of public resources; (b) betterunderstanding of how Government, private sector, and communities can work together in dealing withforeign investors; (c) transparent administration of the state's revenues from the hydrocarbons sector;(d) restructuring of the SOEs into efficient and commercially oriented enterprises; (e) establishment ofnew agencies to assure faster and non-discretionary award and administration of contracts, improvedunderstanding of issues involved in managing such rights, and improved enforcement capacity ofenvironmental, health and safety regulations; (f) improved knowledge of existing environmental andsocio-economic conditions, as a basis for improved management and participation of localcommunities; (g) protection of the environrnent from potential damage caused by activities and a bettergrasp of how to improve fuel quality and, in general, how to define environmental protection norms andstandards in the energy and mining sectors.

4. Institutional and implementation arrangements:

Implementation period: July 2000 - December 2004

Implementing Agency: Implementation of the proposed project will be the responsibility of MEM throughthe Project Management Unit (PMU). PMU will be assisted by consultants and the various concernedenterprises in the sectors. The Manager of the PMU has already been appointed. Measures to appoint therest of the key PMU staff, namely the financial/accounting and the procurement specialists have beeninitiated. In addition, PMU will be initially assisted by a sector specialist from the various concernedenterprises until the required appointment is made.

Project oversight and policy guidance:

Project Administration: The Manager heading the PMU reports directly to the Minister, and will beresponsible for coordinating the services of the consultants financed by the project and for ensuring properprocurement, financial and administrative management of the project. A Project Implementation Plan (PIP)has been prepared by the PMU. The PIP defines the various roles and responsibilities, individual workprograms, and performance indicators, and includes a timetable to be closely monitored for successful andtimely project execution. The PIP includes detailed arrangements for project and financial management,procurement and accounting procedures. The PIP is in the Project Files.

Project Management Reporting: The PMU will prepare quarterly Project Management Reports (PMRs),consisting of analysis of the project implementation progress (narrative and indicators), procurementactivities, and project financial statements including summaries of all sources and uses of project funds,expenditures detailed by category and contract, and Special Account statements. Copies of such quarterlyPMRs will be submitted to the Bank 45 days after the end of each quarter.

Financial Management Systems of MEM: The Financial Management System (FMS) currently in place inthe MEM is part of the overall FMS of the Government, and is based on principles and procedures definedby the legal framework applicable to the pubic sector and more specifically to governmental institutions,including the Law on Government Accounting of 1990.

-9-

MEM prepares an annual budget for its current and capital expenditures. The annual budget is submittedfor approval to the Ministry of Finance (MOF), which closely controls budget preparation and execution.Payments against the budget are authorized by MOF's representatives in the MEM. The Government'saccounting system registers commitments and actual expenditures against the budget. The accountingsystem uses the cash method.

The Ministry's accounts are subject to annual audits by the Government's audit department, InspectionGenerale des Finances (IGF).

Project Financial Management: Financial management arrangements for the project are detailed in Annex6 and summarized below. The expenditures of the proposed project and their financing will beadministered by the PMU. An action plan for developing the necessary systems and procedures at thePMU has been agreed, and is detailed in the PIP. Accounting and financial procedures have been alsodefined in the PIP. An assessment by the Bank of the financial management system to be developed by thePMU will aim at ensuring that the system is operating satisfactorily and generating PMRs acceptable to theBank. The assessment of the financial management system will take place no later than June 30, 2002.

Special Account: To facilitate disbursements from the proposed loan, a Special Account (SA) for anamount of US$ 1.5 million equivalent will be established at the Central Bank (Banque d'Algerie). Initiallythe funds in the SA will be limited to US$ 1.0 million equivalent until project expenditures will havereached US$ 5.0 million equivalent.

Loan Disbursements and Payments Processing: Disbursements from the Bank loan will use traditionalprocedures, i.e. other than those based on PMRs. Payments from the SA and requests to the Bank forreplenishment of the SA will be initiated by the PMU and processed through the Government-ownedAlgerian Development Bank (Banque Algerienne de Developpement: BAD). This is based on proceduresapplicable to foreign-financed projects implemented by the Government and its non-commercial entities, i.e.Law 90-21 of August 15, 1990 on Government accounting, and the Economics Ministry Resolution ofAugust 14, 1993 defining the implementation modalities of Government projects supported by externalfinancing through the Algerian Development Bank, together with regulations and instructions of 1987,1994, and 1997.

Project Accounting: Accounting for all project expenditures and their financing will be done by the PMU,in addition to the accounts kept by BAD for the proposed loan. As already mentioned, the staff of the PMUwill include a qualified accountant. The PMU will acquire the necessary computers (PCs), other officeequipment, and a project accounting software, all to be funded from the proposed loan.

Project Audits: The project accounts and financial statements, the Special Account and all disbursementsbased on Statements of Expenditure (SOEs) will be audited each year by independent auditors acceptableto the Bank. The auditors will apply international audit standards and follow the Bank's guidelines in theFinancial Accounting, Reporting and Auditing Handbook (FARAH), as well as specific terms of referencefor the audits of this project to be prepared during the project launch mission. During negotiations,agreements were reached that audit reports will be sent to the Bank annually six months after the fiscalyear closing date (December 31), i.e., by June 30 of the following year, and that the audit of the PPF willbe included in thefirst year audit of the project.

Monitoring and Evaluation: The PMU will be responsible for monitoring progress against agreedperformance indicators specified in Annex 1. As stated earlier, the PMU will submit quarterly PMRssummarizing project implementation and the utilization of project funds. They will cover implementation

- 10-

status; deviations, if any, from the implementation plan; problems and constraints and corrective actionsbeing taken; and updated disbursement and commitment tables. During negotiations, agreements werereached that not later than December 31, 2002, the PMU will prepare a detailed mid-termn report toserve as the basis for a Project Mid-Term Review to be carried out on February 28, 2003. The PMU willalso prepare and submit to the Bank an Implementation Completion Report (ICR) within six months ofthe Closing Date of the Loan.

D. Project Rationale

1. Project alternatives considered and reasons for rejection:

The proposed project approach is consistent with the Bank's strategy for the energy and mining sectors,which calls for shifting the government's role from ownership and operations to policy making andregulation, promoting efficiency and quality of services, and increased private sector participation.

Rationale

The Government of Algeria is committed to this strategy and the choice to open the sector for privateinvestments has clearly been made. To pursue its policy objectives, the Government of Algeria is movingon a fairly fast track The preparation of modem mining, hydrocarbons and electricity laws, which includenew institutional and regulatory frameworks for all these sectors, is well advanced, and the draft mininglaw has been already submitted to the NPA. Dealing in an integrated way with the preparation andimplementation of the energy and mining reform programs will create substantial synergies.

Alternatives

The Government of Algeria has decided to request a technical assistance loan instead of an investment loanto benefit from the Bank's global knowledge and experience in these sectors.

Provide separate technical assistance loans for each subsector. This approach was rejected because oftiming, inconsistency with Government's approach and fear to lose the benefits of synergies.

Process the operation as a Learning and Innovation Loan: This option was disregarded because sectorreforms similar to the ones proposed are well proven Bank products and the amount required exceeds theLIL limits.

-1 1-

2. Major related projects financed by the Bank and/or other development agencies (completed,ongoing and planned).

Latest SupervisionSector Issue Project (PSR) Ratings

I_________________________________ ___________________________ (Bank-financed projects only)Implementation Development

Bank-financed Progress (IP) Objective (DO)

Improve power sector financial Power III (Loan 2981 -AL), S Sperformance through financial completed in June 1997.restructuring and institutionalrestructuring of the public power utilitySonelgaz, while supporting theexpansion of its transmission system.

Help attract foreign investments, First Petroleum project( Loan S Simprove efficiency of petroleum 3395-AL); completed in Juneservices companies and drilling 1997.operations, optimize production ofSonatrach's oil fields and addressenvironmental problems.

Improve telecommunications First telecommunication S Sinfrastructure, strengthen MPT's Project( Loan 2370-AL);organization and financial management completed in June 1992capabilities, and restructure tariffs.

Acceleration of the Govermment's Privatization support S Sprivatization program project-LIL (Loan 70290-AL);

approved on June 26, 2000

Creation of an enabling environment to Telecommunications and postal S Simprove access to efficient and sector reform project ( Loanaffordable communications services by 70270-AL); approved on Juneopening the telecommunications and 27,2000.postal services to competition andprivate participation.

Other development agenciesCanadian Intemational Development Private Sector DevelopmentAgency Fund ( ongoing)

European Union Privatization TA Project(ongoing)

IP/DO Ratings: HS (Highly Satisfactory), S (Satisfactory), U (Unsatisfactory), HU (Highly Unsatisfactory)

- 12-

3. Lessons learned and reflected in the project design:

The Bank has gained a broad experience in providing Technical Assistance to Governments willing to carryout similar sector reforms. Lessons learned in other energy sector restructuring and privatization programsand in the completed operations in the power and petroleum sectors in Algeria are reflected in the projectdesign. These lessons include:

* political commitment, ownership and consensus building among all stakeholders including laborunions are a prerequisite to ensure effective implementation of far reaching reforms, and theirsustainability;

* far reaching reforms can only be achieved gradually;* bringing international expertise on reforms early in the process increases the chances for success;* a clear legal and regulatory framework has to be defined as early as possible in the reform process;* establishment of self financed and autonomous regulatory entities early in the process;* relevant borrower's staff need to be trained in major aspects of the reform program and project

implementation mainly regulation, procurement;* the project management unit has to be functional as early as possible during the preparation of the

project.

4. Indications of borrower commitment and ownership:

The Borrower commitment to the project is high. The Government has long been aware of the necessarychanges to be brought to the energy and mining sectors in order to enhance their efficiency and make themreliable support to the growth of the economy, and took the initiative in requesting the Bank's assistance inthis respect. This commitment is demonstrated by:

- Government's policy for the energy and mining, encompassing the major principles for reforms, hasbeen indicated in the Government's Program, already approved by the National Popular Assembly(NPA), and confirmed to the Bank by letter dated August 7, 2000;

- Preparation of the various draft laws setting the main rules and regulations of the reform programis well underway. The draft mining law has been approved by the Council of Ministers andsubmitted to the NPA. Drafting of the Electricity Law is well advanced; the draft was presented tovarious stakeholders in an open seminar on July 18-19, 2000; its finalization for submissiori to theCompetent Authorities is expected in mid-2001. Drafting of the hydrocarbons law is also ongoing,and its submission to the Competent Authorities is expected in 2001;

* availability of funding out of a Project Preparation Facility (PPF) was finalized in August 2000;* efforts are being made to inform and build consensus among the various stakeholders through

numerous seminars/workshops, media campaigns, meetings with labor unions, etc.;* measures have been taken to initiate the procurement process for hiring consultants to assist in the

tender process for the first power plant to be implemented with private sector participation, and forthe hiring of consultants to advise in the design and set up of regulatory agencies and other newinstitutions; and

* the setting up of the PMU has been initiated with the recruitment of the Head of the Unit, andmeasures are underway to select the procurement and financial specialists.

5. Value added of Bank support in this project:

The Bank has a long track record in the development of similar energy and mining sector reforms in LatinAmerica, Eastem Europe and Asia. Algeria will be able to benefit from the Bank's experience in sector

- 13-

reform, including particularly formulation of strategic choices, modernization of its legal and institutionalframeworks and restructuring of State owned enterprises. The Bank is well positioned to provideassistance in this transformation process by bringing its knowledge about other countries' experience andhelping Algeria address properly the issues of its energy and mining sectors, while taking good stock of thelessons learned. The Government of Algeria recognizes the Bank's extensive experience and has soughtBank's assistance as it embarks in its reform program. In addition, the Bank's group could offer, throughvarious instruments (lending from IBRD and IFC, guarantees, advisory services) the support that theGovernment of Algeria may request to further develop private sector involvement in the energy and miningsectors.

E. Summary Project Analysis (Detailed assessments are in the project file, see Annex 8)

1. Economic (see Annex 4):0 Cost benefit NPV=US$ million; ERR = % (see Annex 4)O Cost effectiveness* Other (specify)Given the size and nature ( technical assistance) of the project, an economic analysis is not required. Theproject focuses on policy, legal and institutional reforms which, if implemented successfully, will enable theenergy and mining sectors to contribute more effectively to economic growth and poverty reduction.

The economic benefits of the reform program supported by the project are likely to include: discovery ofadditional reserves and increased production, improved efficiency of operations, increase in exports andfiscal revenues, and increase in private capital flows, allowing for more resources to be allocated to socialsectors development.

2. Financial (see Annex 4 and Annex 5):NPV=US$ million; FRR = % (see Annex 4)Given the size and nature ( technical assistance ) of the proposed project, a financial analysis is notrequired.

The past and current financial performance of SOEs to be restructured under the proposed project will beexamined and financial projections established, in the context of the assistance to the restructuring of theseSOEs.

Fiscal Impact:

The required changes in the taxation system for new hydrocarbons exploration and production contractswill be designed and implemented as part of the proposed project with the objectives to be competitiveinternationally, provide adequate incentives to attract exploration activities in non traditional areas andmaintain a fare share for the State. Moreover, the project is expected to result in increased fiscal revenuesin absolute value from the increased activity in the sector.

As to the downstream reforms, the project will analyze the impact of lifting subsidies andgradual pricing liberalization on fiscal revenues, new investments and macro economicaggregates.

3. Technical:The introduction and use of state-of-the-art technology and systems to support sector management hasbeen, as a rule, very successful under technical assistance projects in other countries, particularly within

- 14-

the fields of surveying and management, environmental impact assessments review and monitoring, dataprocessing and information management, software for support to decision-making, etc. Similar technologiesand systems will be introduced through the proposed loan and no particular difficulties are foreseen.

4. Institutional:The implementing agency, MEM, and its PMU will face an ambitious schedule for carrying out a set ofclosely inter-related project activities, which are relatively novel and complex. Their ability to implementthe project has been assessed and will be enhanced through local and foreign technical assistance andtraining programs included in the proposed project, to assist PMU to reinforce its financial, procurement,and sectoral coordination capabilities. Local and foreign technical assistance and training are alsoenvisaged for: (i) the various regulatory agencies and other new institutions in the sectors, to develop theireconomic, financial, technical and legal skills; and (ii) the SOEs to be restructured, to help them implementtheir restructuring program and operate within the new mandate.

4.1 Executing agencies:

The Ministry of Energy and Mines (MEM) and its various agencies in the sectors.

The project would support the setting up of new sector agencies which will result in an important culturalchange for public employees. At the start and during the planned transition period, staff experience andimplementation capacity of the new agencies will be limited within this new environment. Therefore, thereis a major need for technical transfer at all levels, including management and operation. The projectincludes a substantial provision for training as well as hiring international consultants and national staffwho will be in charge of the implementation of specific project sub-components. The Project will alsocontribute to strengthen management capacity in the various existing and new agencies through targetedspecific training programs, as well as through on-the-job training with the support of consultants to becontracted under the loan.

4.2 Project management:

In order to ensure adequate project implementation, MEM decided the setting up of a PMU and appointedthe Manager of PMU early in the process. In order to adhere to World Bank guidelines, these efforts willbe complemented by the appointment of experienced procurement and financial specialists, and later bysectoral specialists.

4.3 Procurement issues:

The project will finance technical assistance services for studies and other consultant assignments (57% ofthe project cost). Procurement of goods will be limited (19% of the project cost, with one packageaccounting for 14%). Procedures for selection of consultants and procurement of goods will be inaccordance with applicable Bank's policy and guidelines. The project elements, their estimated costs andprocurement methods are summarized in Annex 6, Table A. All other procurement information, including:(a) publication of General Procurement Notice (GNP); (b) Bank procurement thresholds and prior reviewprocess with the implementation agency's procurement capacity assessment and required training; and (c)procurement plan providing packaging and estimated schedule of the major procurement actions, aresummarized in Annex 6, and detailed in the PIP.

No Bank's Country Procurement Assessment Report (CPAR) has been made yet. Existing country's legaland institutional frameworks for public enterprise procurement were reviewed during the procurement

- 15 -

capacity assessment of the project agency and found to be generally in line with the Bank's ProcurementGuidelines. However, the capacity assessment identified certain practices and procedures not acceptable tothe Bank for which assurances were obtained from MEM' s officials, for not using them under the project.Theses practices and procedures and the procurement capacity assessment of the project agency arereflected in Annex 6. The overall procurement risk assessment rating for the project is considered asaverage.

4.4 Financial management issues:

During project preparation, an evaluation of the PMU's financial management capacity and its ability tomeet Bank's requirement was carried out. The action plan resulting from this assessment is incorporated inthe PIP. The PMU will procure a computerized financial management and accounting system to be usedfor management of the Bank's project. During negotiations, agreements have been reached that adequatecomputerization, accounting and financial management system in the PMU will be a condition ofeffectiveness.

5. Environmental: Environmental Category: C (Not Required)5.1 Summarize the steps undertaken for environmental assessment and EMP preparation (includingconsultation and disclosure) and the significant issues and their treatment emerging from this analysis.

The project is a Technical Assistance Project supporting reforms in the energy and mining sectors, toimprove efficiency, and lay the ground for more competition and private sector participation. The Projectincludes legal, institutional and capacity building components. As a result, there are no environmentalissues in the proposed Project. The Project is expected to have a positive impact on the environment, bybuilding capacity for environmental management at the national level and within the energy and miningsectors especially in the new regulatory agencies. It will include in particular development of sectoralenvironmental assessments and respective guidelines for energy and mining projects and will therebysupport the Government's environmental strategy. For the sub-component related to the assistance forlaunching a 2000 MW power generation program with private sector participation, the call for proposalswill include terms of reference for the development of the related Environmental Assessment.

5.2 What are the main features of the EMP and are they adequate?

Not applicable.

5.3 For Category A and B projects, timeline and status of EA:Date of receipt of final draft: N/A

Not applicable

5.4 How have stakeholders been consulted at the stage of (a) environmental screening and (b) draft EAreport on the environmental impacts and proposed environment management plan? Describe mechanismsof consultation that were used and which groups were consulted?

Not applicable.

5.5 What mechanisms have been established to monitor and evaluate the impact of the project on theenvironment? Do the indicators reflect the objectives and results of the EMP?

During project implementation consultation will take place with NGOs, landowners, and industryrepresentatives regarding the energy and mining sector environmental aspects.

- 16 -

6. Social:6.1 Summarize key social issues relevant to the project objectives, and specify the project's socialdevelopment outcomes.

The Government has already initiated the launch of media campaigns on the overall benefits of the reformprogram, and to promote social acceptance of this program. Social concerns were discussed, since thereform and restructuring program could have an impact on employment. The reform program will have anet positive effect through: (i) improvement of services; (ii) creation of new institutions and hence new jobs;(iii) new private investments induced by the establishment of the new legal and regulatory framework whichwill boost the creation of new job opportunities in new areas that will be opened for oil and miningexploration and exploitation; and (iv) the reallocation of more public resources to social programs.However, possible negative impact on employment could be induced by the reforms and the restructuringprogram. The Government confirmed that it will include in its action program a more detailed evaluationof the social impact of these reforms to adopt appropriate safeguard measures.

Furthermore, and under the newly approved Privatization Assistance Loan, the Ministry of Participationand Coordination of Economic Reforms is setting up a Division in charge of addressing the labor issues incoordination with other ministries and agencies concerned . Specifically, the mandate of this Division is tohelp design and implement plans mitigating the social impact of the reforms and future privatization.

These plans will complement an already comprehensive social safety net in Algeria which has been enactedwith the beginning of the macroeconomic program in 1994, including broad legislation pertaining toretrenchment benefits, early retirement schemes and social security compensation.

6.2 Participatory Approach: How are key stakeholders participating in the project?

Workshops involving major stakeholders, including representatives of labor unions and civil society havealready been organized, and will continue to be organized, to discuss the new legal and institutionalframework, and the main concepts underlining the development of the energy and mining sector, includingsocial issues. The Bank is assisting in this aspect through a PPIAF grant and the proposed loan willenhance this activity.

Discussions between Government, unions and employers, and between unions and employers' associationand the industries are taking place and are intended to improve the social climate and create an environmentfavorable to the reform program. In addition the information campaign launched to explain the process tothe general public will also help build a broad consensus.

6.3 How does the project involve consultations or collaboration with NGOs or other civil societyorganizations? 0

In addition to the various workshops and seminars already held since April 2000, the proposed projectincludes activities to: (a) develop a consultation/communication policy and strategy regarding energy andmining in Algeria; and (b) increase the awareness within sector institutions, companies, local governnents,labor unions, NGOs and civil society, including local communities.

6.4 What institutional arrangements have been provided to ensure the project achieves its socialdevelopment outcomes?

Not applicable

- 17 -

6.5 How will the project monitor performance in terms of social development outcomes?

Not applicable

7. Safeguard Policies:7.1 Do any of the following safeguard policies apply to the project?

Polioy ApplicabilityEnvironmental Assessment (OP 4.01, BP 4.01, GP 4.01) 0 Yes * NoNatural habitats (OP 4.04, BP 4.04, GP 4.04) 0 Yes * NoForestry (OP 4.36, GP 4.36) 0 Yes * NoPest Management (OP 4.09) 0 Yes * NoCultural Property (OPN 11.03) 0 Yes * NoIndigenous Peoples (OD 4.20) 0 Yes * NoInvoluntary Resettlement (OD 4.30) 0 Yes 0 NoSafety of Dams (OP 4.37, BP 4.37) 0 Yes * NoProjects in International Waters (OP 7.50, BP 7.50, GP 7.50) 0 Yes * NoProjects in Disputed Areas (OP 7.60, BP 7.60, GP 7.60) 0 Yes 0 No

7.2 Describe provisions made by the project to ensure compliance with applicable safeguard policies.

Not applicable.

F. Sustainability and Risks

1. Sustainability:

By developing a competitive framework for market-oriented reforms in the energy and mining sectors, theproject will help accelerate investments, address market failures and enhance service efficiency and energyaccess, while improving environmental standards. Incentives to sustain project objectives includetransparency and competitiveness of the overall contractual arrangements. Improved service coverage andquality at more competitive prices will be sustained as competition develops and private investment growsin both infrastructure and services. Empowering the new regulatory authorities and ensuring financialindependence will enable regulatory functions to be sustained without dependence on budgetary support.

- 18 -

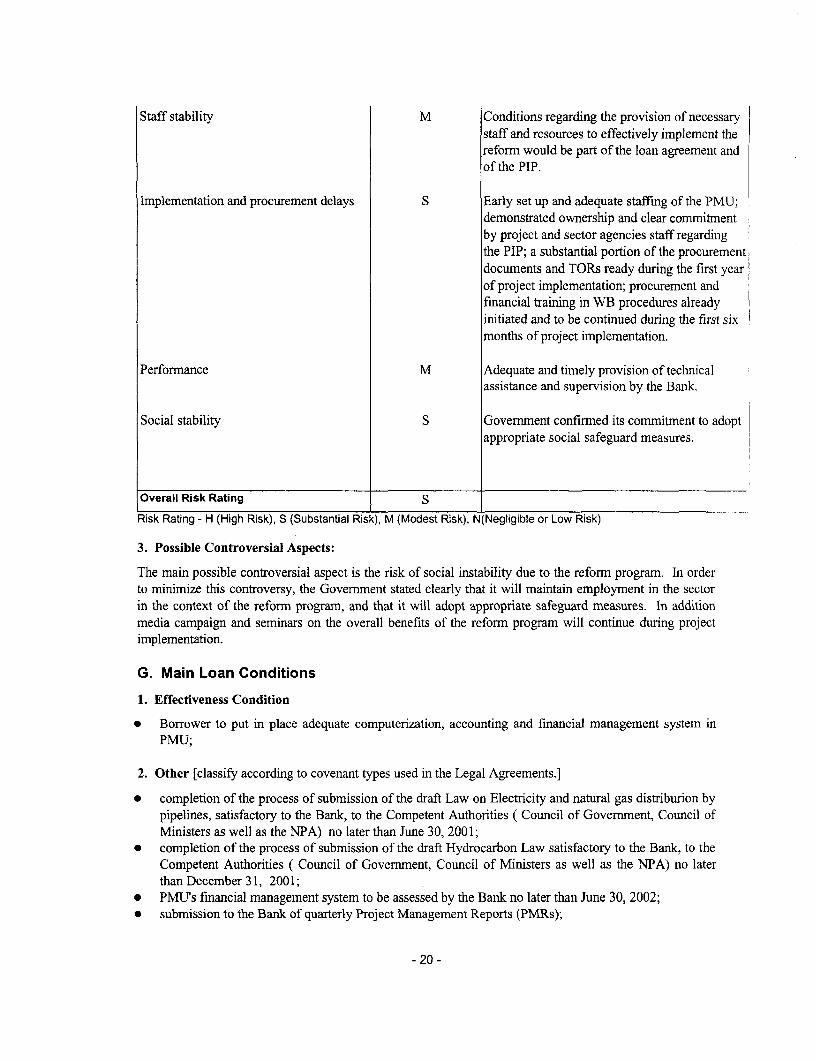

2. Critical Risks (reflecting the failure of critical assumptions found in the fourth column of Annex 1):

Risk Risk Rating Risk Mitigation MeasureFrom Outputs to ObjectiveGovernment commitment to implement M (a) Govermnent's Program; (b) Government'sreform program request to the Bank to assist in implementing the

reform program; (c) early start of preparation ofthe primary legislation accompanied by mediacampaigns, seminar and workshops to buildconsensus; (d) support of the Bank as part ofoverall sector reform dialogue with allconcerned parties. In addition the mid-termreview will ensure that the reform is proceedingin conformity with the project developmentobjectives.

Stakeholders and population concerns vis S (a) broad information campaigns; and (b) MEMa vis the reform program constant dialogue with major stakeholders

throughout the implementation process andinitial operation.

Overall investments conditions stability S (a) preparation of secondary legislation and itsadoption early in the process (covenant of themid-term review); (b) early set up of the newagencies, in particular the regulatory agencies;(c) road-shows and promotion activities.

Inadequate recurrent budgets for the M (a) rapid executive decrees to facilitate initialnewly set up agencies and inefficient operations of Regulatory institutions; (c)management adequate budgetary provisions for the first year

of operation of the new agencies; and technicalassistance for the new agencies funded under theproject.

From Components to OutputsContinued project ownership S (a) Continued progress in implementing the

sectoral reforms; (b) continued sector reformdialogue with stakeholders, from preparationthroughout implementation; (c) timelyimplementation of sector reforms and projectactivities, including training of staff andprovision of adequate infrastructure.

- 19 -

Staff stability M Conditions regarding the provision of necessarystaff and resources to effectively implement thereform would be part of the loan agreement andof the PIP.

Implementation and procurement delays S Early set up and adequate staffing of the PMU;demonstrated ownership and clear commitmentby project and sector agencies staff regardingthe PIP; a substantial portion of the procurementdocuments and TORs ready during the first yearof project implementation; procurement andfinancial training in WB procedures alreadyinitiated and to be continued during the first sixmonths of project implementation.

Performance M Adequate and timely provision of technicalassistance and supervision by the Bank.

Social stability S Government confirmed its commitment to adoptappropriate social safeguard measures.

Overall Risk Rating

Risk Rating - H (High Risk), S (Substantial Risk), M (Modest Risk), N(Negligible or Low Risk)

3. Possible Controversial Aspects:

The main possible controversial aspect is the risk of social instability due to the reform program. In orderto minimize this controversy, the Government stated clearly that it will maintain employment in the sectorin the context of the reform program, and that it will adopt appropriate safeguard measures. In additionmedia campaign and seminars on the overall benefits of the reform program will continue during projectimplementation.

G. Main Loan Conditions

1. Effectiveness Condition

* Borrower to put in place adequate computerization, accounting and financial management system inPMU;

2. Other [classify according to covenant types used in the Legal Agreements.]

* completion of the process of submission of the draft Law on Electricity and natural gas distriburion bypipelines, satisfactory to the Bank, to the Competent Authorities ( Council of Government, Council ofMinisters as well as the NPA) no later than June 30, 2001;

* completion of the process of submission of the draft Hydrocarbon Law satisfactory to the Bank, to theCompetent Authorities ( Council of Government, Council of Ministers as well as the NPA) no laterthan December 31, 2001;

* PMU's financial management system to be assessed by the Bank no later than June 30, 2002;* submission to the Bank of quarterly Project Management Reports (PMRs);

- 20 -

* project accounts audits to be submitted to the Bank not later than six months after the end of eachfiscal year;

* complete staffing of the PMU as needed and with a core of sectoral staff no later than one year afterproject effectiveness;

* promulgation of required decrees and regulations specific to each subsector (hydrocarbons, electricity,and mining) no later than December 31, 2002;

* set up of the three regulatory agencies (one for each subsector, i.e., hydrocarbon, electricity, andmining respectively), agreement on their respective organization chart, and appointment of core localstaff to contract out consultant services to assist in this design/concept stage and in the initial operationof the agencies no later than one year after enactrnent of the relevant laws;

* set up of other institutions as foreseen by the various laws, in particular a contract management andpromotion agency for the hydrocarbon subsector, a power system operator and a power marketoperator for the electricity subsector, and a Cadastrial Agency for the mining subsector;

* mid-term review (MTR) report to be submitted to the Bank not later than June 30, 2002, and MTR ofthe project to be carried by February 28, 2003.

H. Readiness for Implementation

D1 1. a) The engineering design documents for the first year's activities are complete and ready for the startof project implementation.

1 1. b) Not applicable.

1 2. The procurement documents for the first year's activities are complete and ready for the start ofproject implementation.

1 3. The Project Implementation Plan has been appraised and found to be realistic and of satisfactoryquality.

El 4. The following items are lacking and are discussed under loan conditions (Section G):

1. Compliance with Bank Policies

Z 1. This project complies with all applicable Bank policies.DG 2. The following exceptions to Bank policies are recommended for approval. The project complies with

all other applicable Bank policies.

Zoubeida Ladhibi-Belk Sonia Hammam Christian DelvoieTeam Leader Acting Sector Dir. Country Director

- 21 -

Annex 1: Project Design Summary

ALGERIA: Energy and Mining Technical Assistance Loan (EMTAL)

Hierarchy f Objectives Indicators !MonitoringA &Evaluation Crntical AssumptionsSector-related CAS Goal: Sector Indicators: Sector/ country reports: (from Goal to Bank Mission)Higher and sustainable rate ofeconomic growth through * Increase in private * CAS discussions * Macroeconomicincreased competition and sector participation * Portfolio reviews environment and politicalprivate sector participation in * Improvement in the stabilitythe Energy and Mining efficiency of theSectors. restructured SOEs

* Increase in Governmentrevenues from thesectors

* Reduction of pricingsubsidies

Project Development Outcome / Impact Project reports: (from Objective to Goal)Objective: Indicators:Reform of the energy andmining sectors, setting the * Enactment of laws on * Governmentstage to improve sector Mining, Hydrocarbon and * Government commitment andefficiency, introduce market Electricity self-evaluation of policy acceptance by otherforces, develop untapped * Establishment of the and institutional stakeholders of theresources, address agencies foreseen under progress. reform process.environmental concerns and the new legal framework * Supervision mission by * Successful operation ofalleviate financial burden on * Restructuring of WB the new agencies.public finances SONELGAZ and support * Participation by the

to the public enterprises of private sectorConsistent with the the Mining Holding * Creation of aGovernment Energy and (ENAMARBRE, competitive marketMining Program which FERPHOS), ENOR and structurereceived support from the ORGM for adapting to theWorld Bank reforms

Impact indicators:* Award of new mining

titles and newhydrocarbon explorationand production contractsbased on the newcontractual instruments

* Successful biddingauction for the 2000MWproject(s)

* Effective reduction offunding of investment inthe MEM's sectors by thestate budget

- 22 -

Key PerformanceHierarchy of Objectives Indicators Monitoring & Evaluation Critical Assumptions

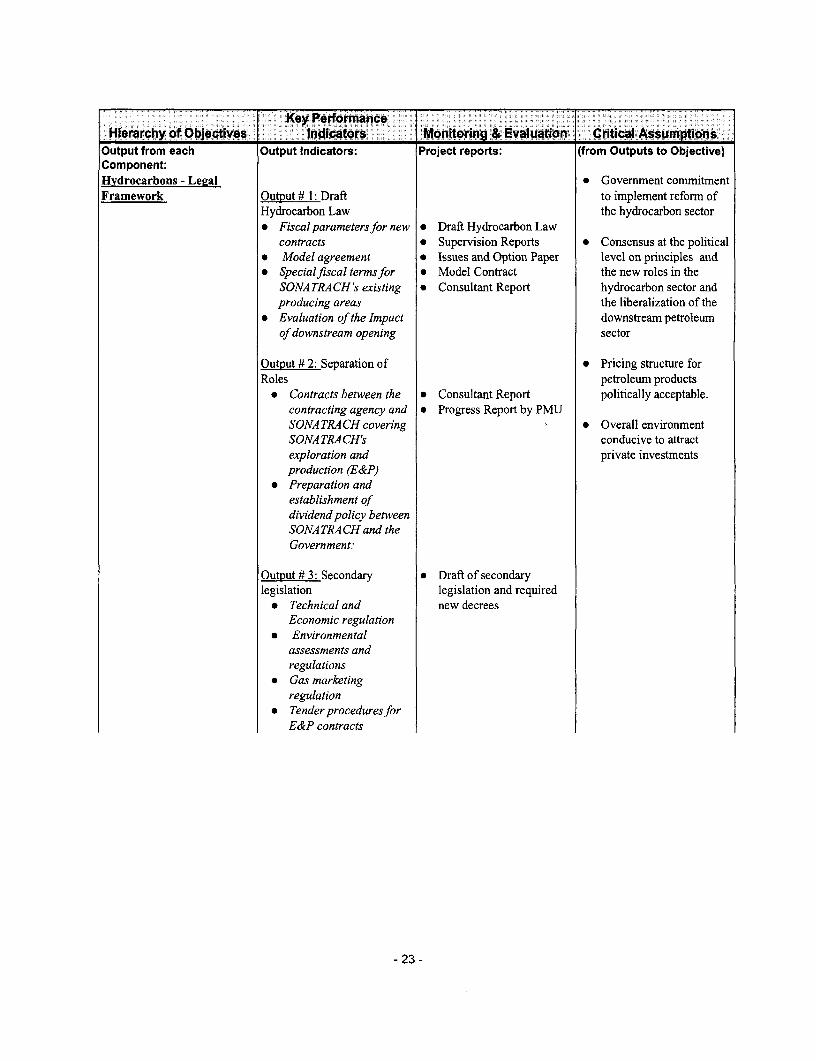

Output from each Output Indicators: Project reports: (from Outputs to Objective)Component:Hydrocarbons - Le2al * Government commitmentFramework Output # 1: Draft to implement reform of

Hydrocarbon Law the hydrocarbon sector* Fiscal parameters for new * Draft Hydrocarbon Law

contracts * Supervision Reports * Consensus at the political* Model agreement * Issues and Option Paper level on principles and* Specialfiscal terms for * Model Contract the new roles in the

SONATRACH's existing * Consultant Report hydrocarbon sector andproducing areas the liberalization of the

* Evaluation of the Impact downstream petroleumof downstream opening sector

Output # 2: Separation of * Pricing structure forRoles petroleum products

* Contracts between the * Consultant Report politically acceptable.contracting agency and * Progress Report by PMUSONA TRA CH covering * Overall environmentSONA TRACH's conducive to attractexploration and private investmentsproduction (E&P)

* Preparation andestablishment ofdividend policy betweenSONA TRA CH and theGovernment:

Output # 3: Secondary * Draft of secondarylegislation legislation and required

* Technical and new decreesEconomic regulation

* Environmentalassessments andregulations

* Gas marketingregulation

* Tender procedures forE&P contracts

- 23 -

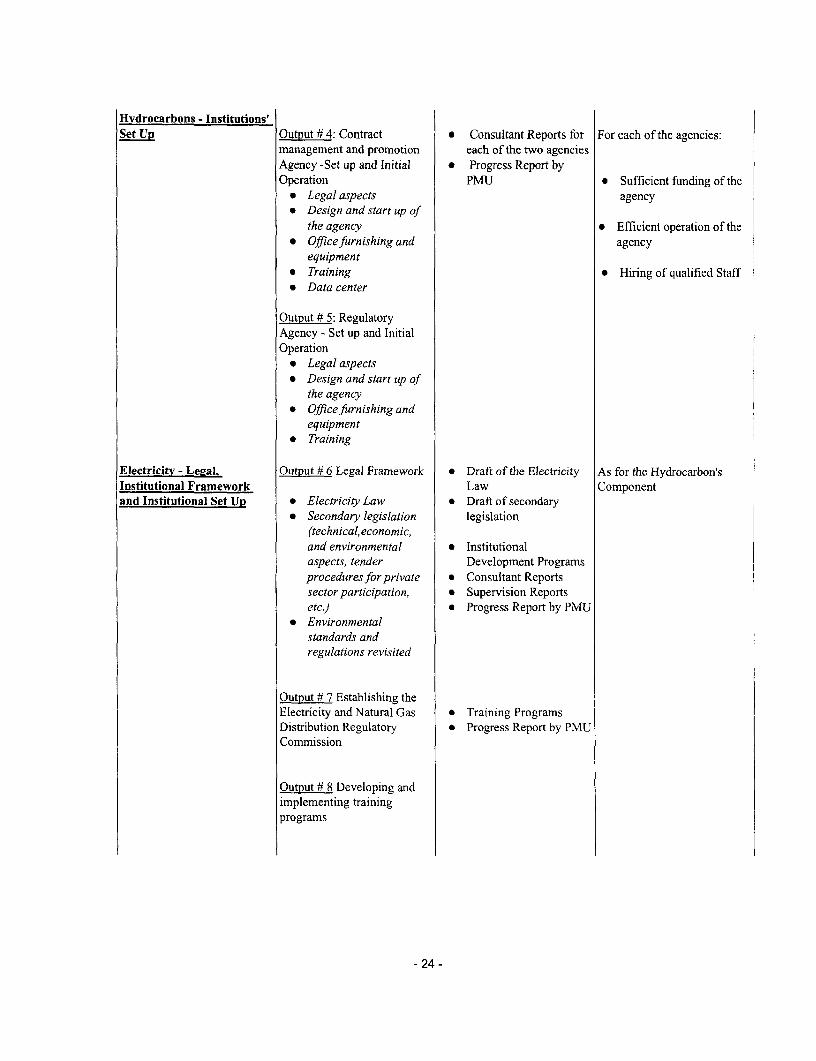

Hydrocarbons - Institutions'Set Up Output # 4: Contract * Consultant Reports for For each of the agencies:

management and promotion each of the two agenciesAgency -Set up and Initial * Progress Report byOperation PMU * Sufficient funding of the

* Legal aspects agency* Design and start up of

the agency * Efficient operation of the* Office furnishing and agency

equipment* Training * Hiring of qualified Staff* Data center

Output # 5: RegulatoryAgency - Set up and InitialOperation

* Legal aspects* Design and start up of

the agency* Office furnishing and

equipment* Training

Electricity - Leeal. Output # 6 Legal Framework * Draft of the Electricity As for the Hydrocarbon'sInstitutional Framework Law Componentand Institutional Set UP * Electricity Law * Draft of secondary

* Secondary legislation legislation(technical, economic,and environmental * Institutionalaspects, tender Development Programsprocedures for private * Consultant Reportssector participation, * Supervision Reportsetc.) * Progress Report by PMU

* Environmentalstandards andregulations revisited

Output # 7 Establishing theElectricity and Natural Gas a Training ProgramsDistribution Regulatory * Progress Report by PMUCommission

Output # 8 Developing andimplementing trainingprograms

- 24 -

Electricity - Restructuring Output # 9 Sonelgaz * Draft legislationof the SOE - Sonelgaz restructured and creation of * Audit Report

separate corporatized entities * Consultant Reports* Audit of Sonelgaz' * Opening Balance Sheet

accounts* Establishment of the

new generation,transport, distribution(electricity and naturalgas by pipelines)companies

* Transfer of assets,liabilities and otherrights and obligations tothe new companies

* Decentralization andtransfer of managementinformation systems andstaff to the newcompanies

* Financial restructuringmeasures

Electricity - 2000 MW Output # 10: Agreement * Consultant ReportProiect between Government of * Bidding Document Issued

Algeria and private parties for * Environmental assessmentthe development of the 2000 completedMW Project(s): * Finalized Legal

* Preparation, processing documentationand completion of the * Progress Report by PMUtransaction throughfinancial closure.

- 25 -

Minin2 -Policy. Ieeal and Output # 11 Completion of As for the Hydrocarbon'sreLulatory framework the regulatory framework and * Secondary Legislation Component

operative procedures * Consultant Report* Progress Report by PMU

Output # 12 Workshops andseminars:

* in Algeria, for publicofficers to explain thenew legalframeworkand its application;

* in Algeria, for investors,operators and otherstakeholders to informabout the new legalframework;

* abroad, to promote thebenefits of the new legalframework

Minin2 - Institutional Set-up * Consultant Reportand Information Systems Output # 13: Regulatory * Progress Report by PMU

Agency and InformationSystem- Set up and InitialOperation

* Legal aspect* Design and Start-Up of

the agency* assessment and

establishment of sectorenvironmentalregulations

* Office furnishing andequipment

* Training* Data Center

Mining Support tostate-owned mining Output # 14: SOEs * Audit Reportenterprises restructured * Consultant Reports

* Audit of the miningsector's SOEs * Consultant Report

* Technical and economic * Progress Report by PMUevaluation of ENORassets

* Propose options forpartnership with privateinvestors

* Restructuring of ORGM

- 26 -

Key PerformanceHierarchy of Objectives Indicators Monitoring & Evaluation Critical Assumptions

Project Components / Inputs: (budget for each Project reports: (from Components toSub-components: component) Outputs)

Financed by the BankHydrocarbon (in US$) * Adequate Capacity to

(see Annex 2 for details) 7,550,000 Consultant Reports implement the project( see Annex 2 for the list of

* Legal, Institutional and reports) * Timely procurement inFiscal Framework accordance with Bank

* Institutional Set-up Monitoring through Bank task guidelines* Data Bank management procedures for a

sector reform project.

Electricity 5,750,000(see Annex 2 for details)

*Legal, InstitutionalFramework and InstitutionalSet Up

*Restructuring of the SOEs

* 2000 MW Project(s)

Mining: 4,220,000(see Annex 2 for details)*Legal, institutional andregulatory framework

*Institutional Set-up*Support to miningcompanies and SOEs

Project Management Unit 300,000

- 27 -

Annex 2: Detailed Project DescriptionALGERIA: Energy and Mining Technical Assistance Loan (EMTAL)

Detailed Project Description and cost estimate

The project will consist of four components: I) hydrocarbons; 2) electricity; 3) mining; and 4) assistance tothe setting up of the Project Management Unit (PMU). The hydrocarbons, electricity and miningcomponents will basically comprise three similar sub-components as indicated below. The electricitycomponent will also include assistance to MEM in launching the 2000 MW power generation plant(s) withprivate sector participation:

(a) assitance on legal and regulatory matters, dealing mainly with the preparation of new laws and/orregulations and procedures;(b) assistance on institutional matters, dealing mainly with the establishment and the initial operationof new institutions, including the contracting and regulatory agencies; and(c) assistance to reform the state-owned entities (SOEs) in the electricity and mining subsectors,dealing with the adaptation of SOEs to the new sector policy, and support to private sectordevelopment.

By Component:

Project Component I - US$7.55 million

The Hydrocarbons Sector Component

I The policy of the Government of Algeria concerning the hydrocarbons sector is based on thefollowing principles:

* optimizing the value of the vast natural resources,* preservation and increase of the State revenues

2. Sub-sector background:

A -Upstream

As of today, the upstream hydrocarbons operations are dominated by the national company,SONATRACH which is:

* the main oil and gas producer (approx. 88%);* the owner and operator of the pipeline network;* the responsible entity for the management of the data base, the promotion and negotiation of

exploration and production (E&P) contracts (30 contracts) and related administrative tasks;* the entity that collects on behalf of the state royalties and taxes;* the only crude oil and gas supplier to the domestic market;* the entity in charge of all gas exports;* called to play a state policy role in addition to its commercial role;

- 28 -

* faced for the next five years, with investments needs in the order of 20 billion US$ forexploration and production activities;

* benefiting from government guarantees for financing its investment plans.

In general, the system of management and control of the sector is characterized by a weak performance, inspite of the recognized large production and geological potential and the success of the exploration carriedout by international partners of SONATRACH since early 1990. In concrete terms, the upstream sector ischaracterized by:

* a limited number of new contracts;* an exploration effort concentrated in a specific geological region;* an insufficient cost management;* an insufficient technical and environmental control of the operations; and* a lengthy negotiation process for awarding contracts to private investors.

3. The key objectives of the reform program for the upstream hydrocarbons sector are to:

* separate the commercial functions of the SOEs from the state roles.* assign the functions related to negotiations, management and control of contracts and of

implementation of regulations to autonomous government agencies.* allow the public company to focus solely on commercial activities in competition with private

companies* accelerate and promote a larger and diversified private participation* reduce the state debt and limit state guarantees to SOEs in future investmnents

4. The reform strategy upstream includes two key aspects:

Legal. fiscal, and contractual -- basically to put in place a framework, applicable in particular to newventures, that will ensure:

* the development of exploration and production (E&P) model contracts that provideinternational competitive terms and a level playing field for the private investors and the SOEs;

* transparency and efficiency in procedures from access to data bases through award, signingand management of the contract;

* promulgation of regulations;* promotion private sector participation in all exploration and production activities, including

pipelines;* receipt by the government of a fair share of the economic rent from exploitation of

hydrocarbon* the exploration of frontier zones and the exploitation of marginal fields and gas resources* respect for technical and environmental standards and norms.

Institutional -- basically to create and implement two new entities:

* A contractual autonomous agency - in charge of the management of the data base, thepromotion of E&P activities and the signing and management of contracts

* An autonomous regulatory agency - in charge of the application of regulations (inter-alia,technical, safety, environmental and, specific to pipelines, economic regulations)

- 29 -