Ideas to Help you Never Outlive Your Money or its Purchasing Power

Outlive Your Savings?

Will You

How Equities Can Reduce Longevity Risk

Presented by

Around the world,more people are living longer.

Despite this, many peopleunderestimate their life expectancy.

Why?

Source: World Bank

Life Expectancy At Birth (Years)

52

54

56

58

60

62

64

66

68

70

72

74

1960 1970 1980 1990 2000 2010

World

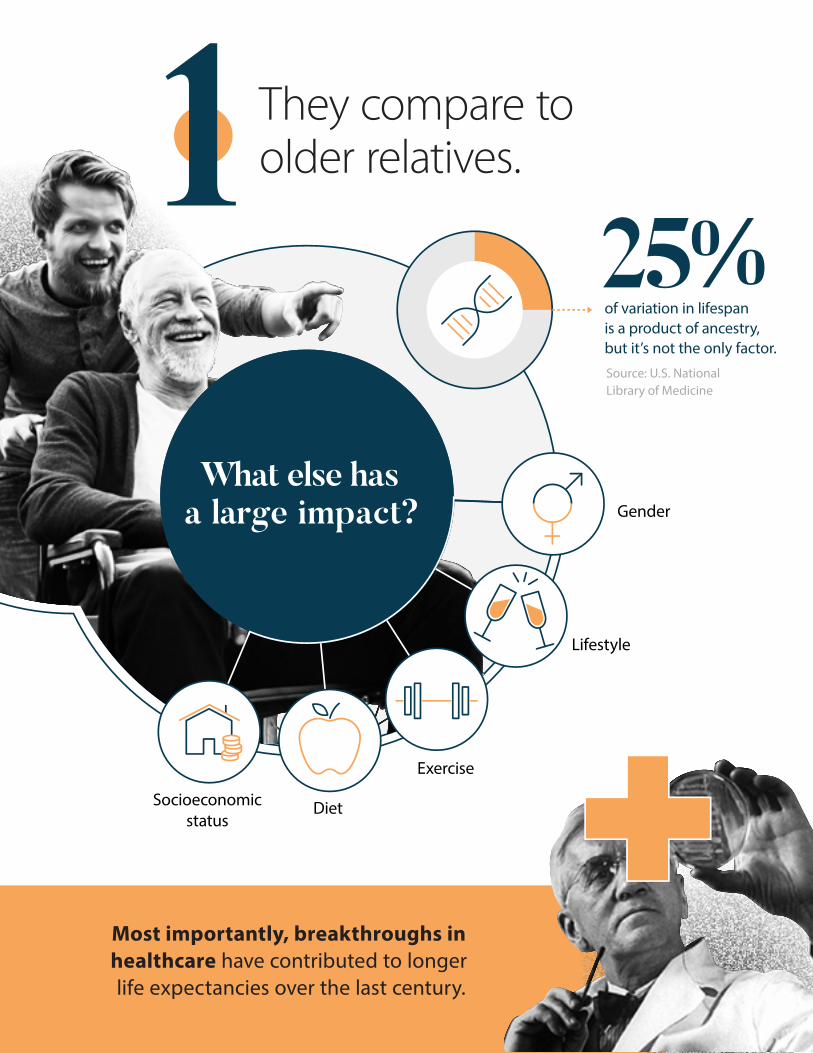

of variation in lifespan is a product of ancestry, but it’s not the only factor.

Gender

Lifestyle

Exercise

DietSocioeconomicstatus

Source: U.S. National Library of Medicine

What else hasa large impact?

They compare toolder relatives.1

25%

Most importantly, breakthroughs in healthcare have contributed to longer life expectancies over the last century.

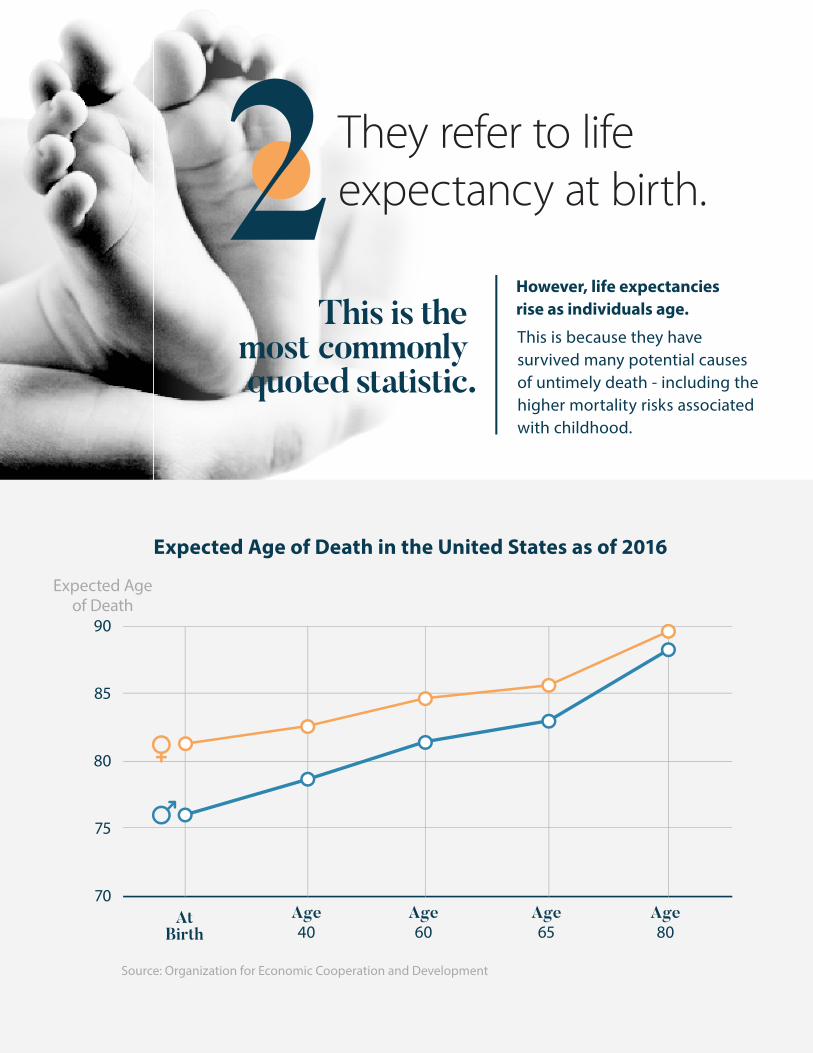

Expected Age of Death in the United States as of 2016

They refer to life expectancy at birth.2

This is themost commonlyquoted statistic.

However, life expectancies rise as individuals age.

This is because they have survived many potential causes of untimely death - including the higher mortality risks associated with childhood.

70

75

80

85

90

AtBirth

Age40

Age60

Age65

Age80

Source: Organization for Economic Cooperation and Development

Expected Ageof Death

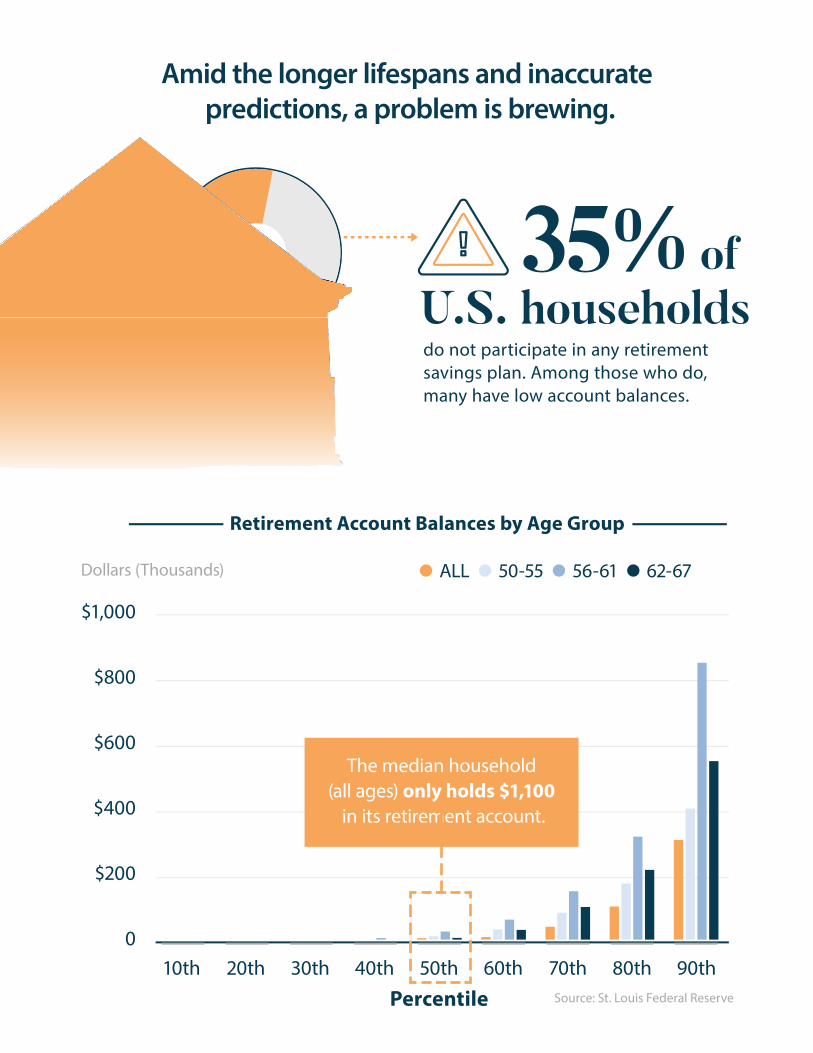

Amid the longer lifespans and inaccurate predictions, a problem is brewing.

Source: St. Louis Federal Reserve

do not participate in any retirement savings plan. Among those who do, many have low account balances.

of35%U.S. households

ALL 50-55 56-61 62-67

Retirement Account Balances by Age Group

Dollars (Thousands)

Percentile

$1,000

$800

$600

$400

$200

010th 20th 30th 40th 50th 60th 70th 80th 90th

The median household (all ages) only holds $1,100

in its retirement account.

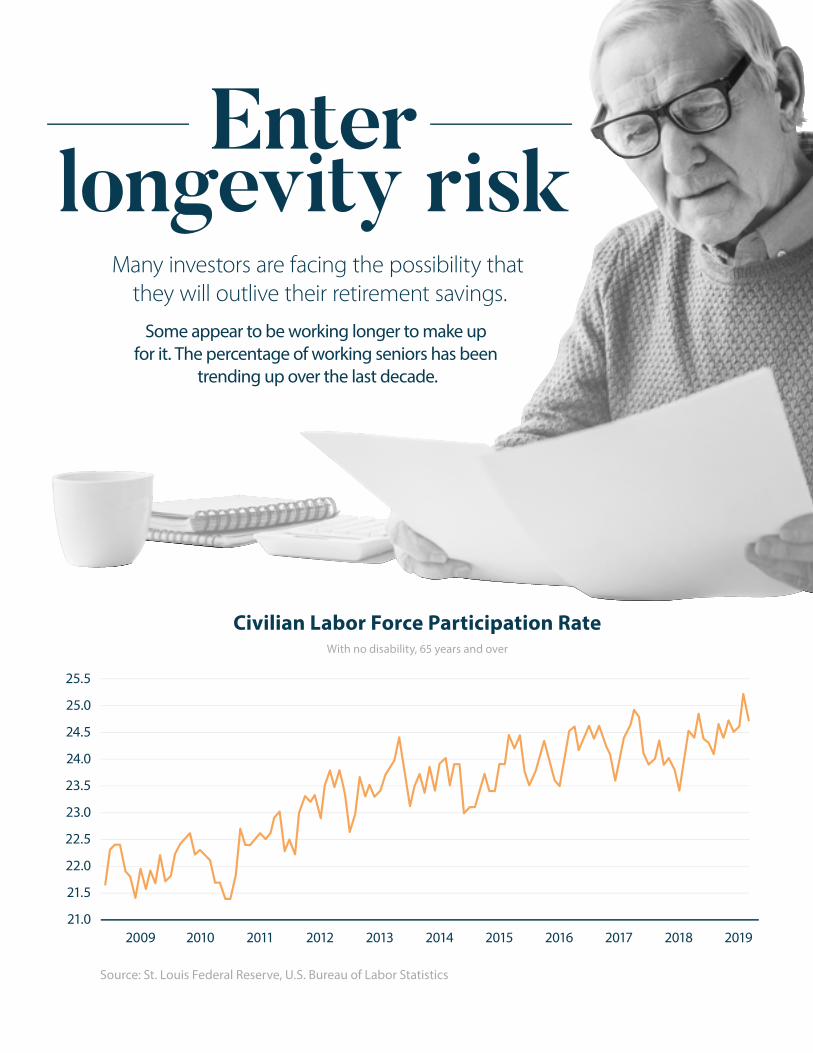

Some appear to be working longer to make up for it. The percentage of working seniors has been

trending up over the last decade.

longevity riskEnter

21.5

21.0

22.0

22.5

23.0

23.5

24.0

24.5

25.0

25.5

Civilian Labor Force Participation RateWith no disability, 65 years and over

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Source: St. Louis Federal Reserve, U.S. Bureau of Labor Statistics

Many investors are facing the possibility that they will outlive their retirement savings.

Source: Bankrate, Federal Reserve

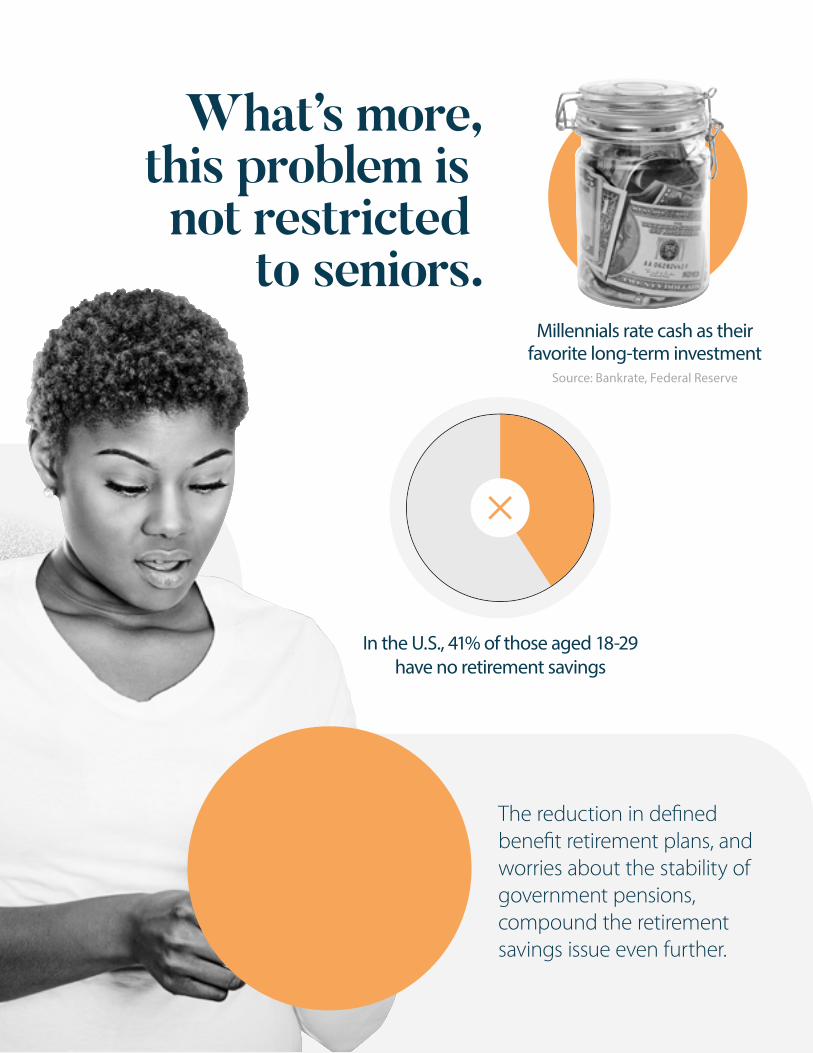

What’s more, this problem isnot restricted

to seniors. Millennials rate cash as their

favorite long-term investment

In the U.S., 41% of those aged 18-29 have no retirement savings

The reduction in de�ned bene�t retirement plans, and worries about the stability of government pensions, compound the retirement savings issue even further.

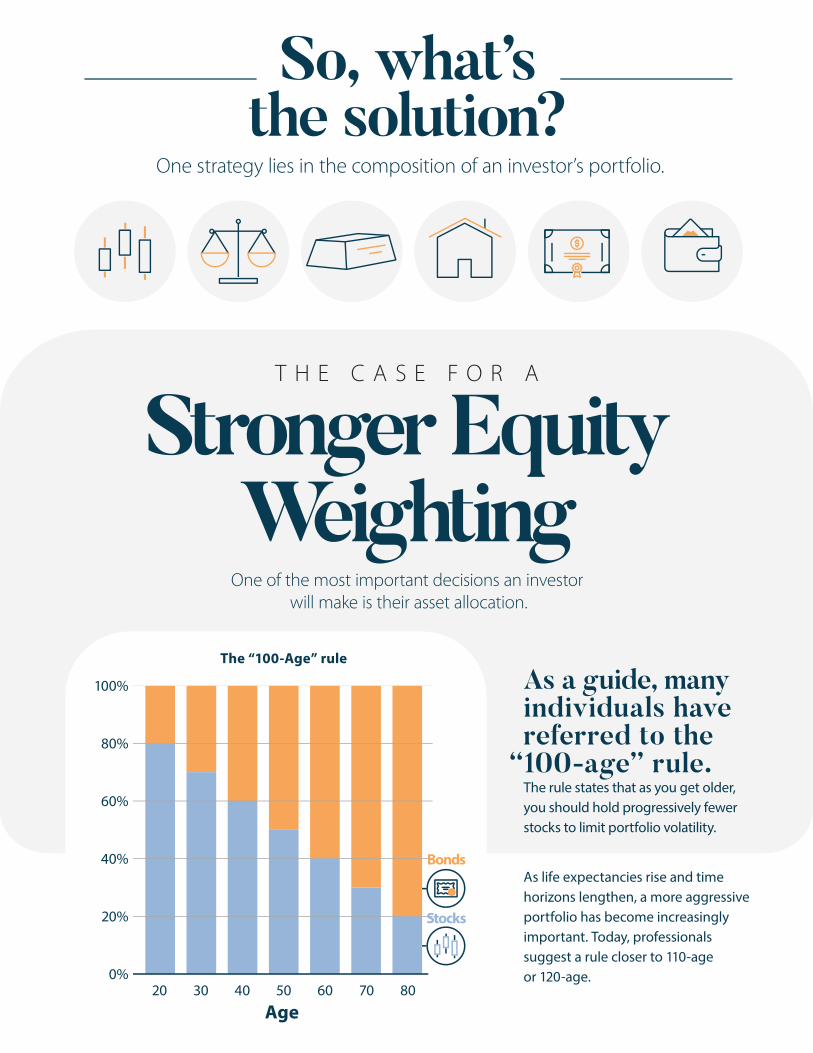

One of the most important decisions an investor will make is their asset allocation.

One strategy lies in the composition of an investor’s portfolio.

So, what’sthe solution?

T H E C A S E F O R A

Stronger EquityWeighting

As a guide, many individuals have referred to the

“100-age” rule. The rule states that as you get older, you should hold progressively fewer stocks to limit portfolio volatility.

As life expectancies rise and time horizons lengthen, a more aggressive portfolio has become increasingly important. Today, professionals suggest a rule closer to 110-ageor 120-age.0%

20%

40%

60%

80%

100%

The “100-Age” rule

20 30 40 50 60 70 80

Bonds

Stocks

Age

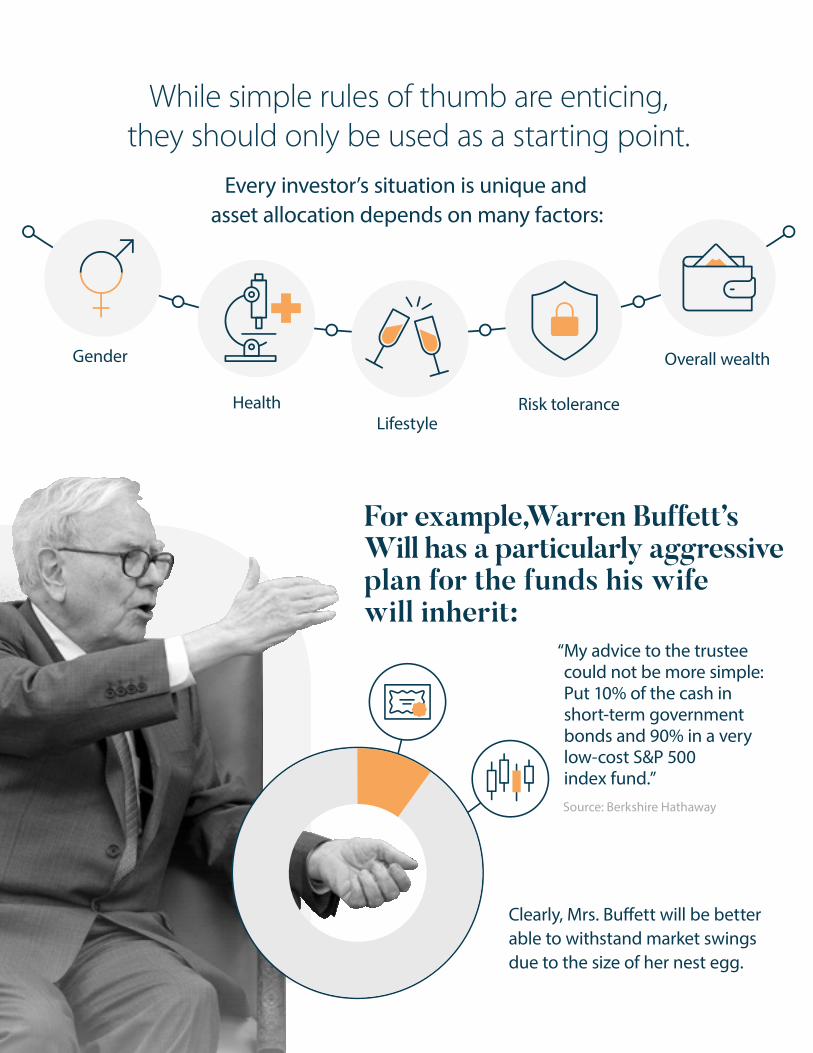

While simple rules of thumb are enticing,they should only be used as a starting point.

Every investor’s situation is unique andasset allocation depends on many factors:

For example,Warren Buffett’s Will has a particularly aggressive plan for the funds his wifewill inherit:

Source: Berkshire Hathaway

“My advice to the trustee could not be more simple:Put 10% of the cash in short-term government bonds and 90% in a very low-cost S&P 500index fund.”

Clearly, Mrs. Bu�ett will be better able to withstand market swings due to the size of her nest egg.

Gender

HealthLifestyle

Risk tolerance

Overall wealth

Equities Have Exhibited Strong Long-Term Performance1 Equities have delivered much higher returns than other

asset classes over time. Not only have they outpaced in�ation by a wide margin, many also pay dividends that boost performance when reinvested.

Source: NYU Stern School of Business and author's calculations

Investing primarily in bonds or cash equivalentswill generate minimal returns. To build a sizeable retirement fund,

investors must incorporate equities.

$26,535.19

$506.56

$143.01

However, there are many reasons why the average investorshould consider holding a larger equity weighting.

$5K

$10K

$15K

$20K

$25K

$30K

1928 ‘30 ‘40 ‘50 ‘60 ‘70 ‘80 ‘90 ‘00 ‘10 2018

Stock performance is measured by the S&P 500 and includes both price appreciation and dividends.The raw data for treasury bond and bill returns is obtained from the Federal Reserve database in St. Louis (FRED). The treasury bill rate is a 3-month rate and the treasury bond is the constant maturity 10-year bond, but the treasury bond return includes coupon and price appreciation. It will not match the treasury bond rate each period. The S&P 500 Index is widely regarded as the standard index for measuring large-cap U.S. stock market performance. Past performance is no guarantee of future results. An investment cannot be made directly into an index.

In�ation is as per the CPI Index obtained from the Federal Reserve Bank of Minneapolis.

Bonds

Bills

Stocks

Compounded Value of $100, In�ation Adjusted

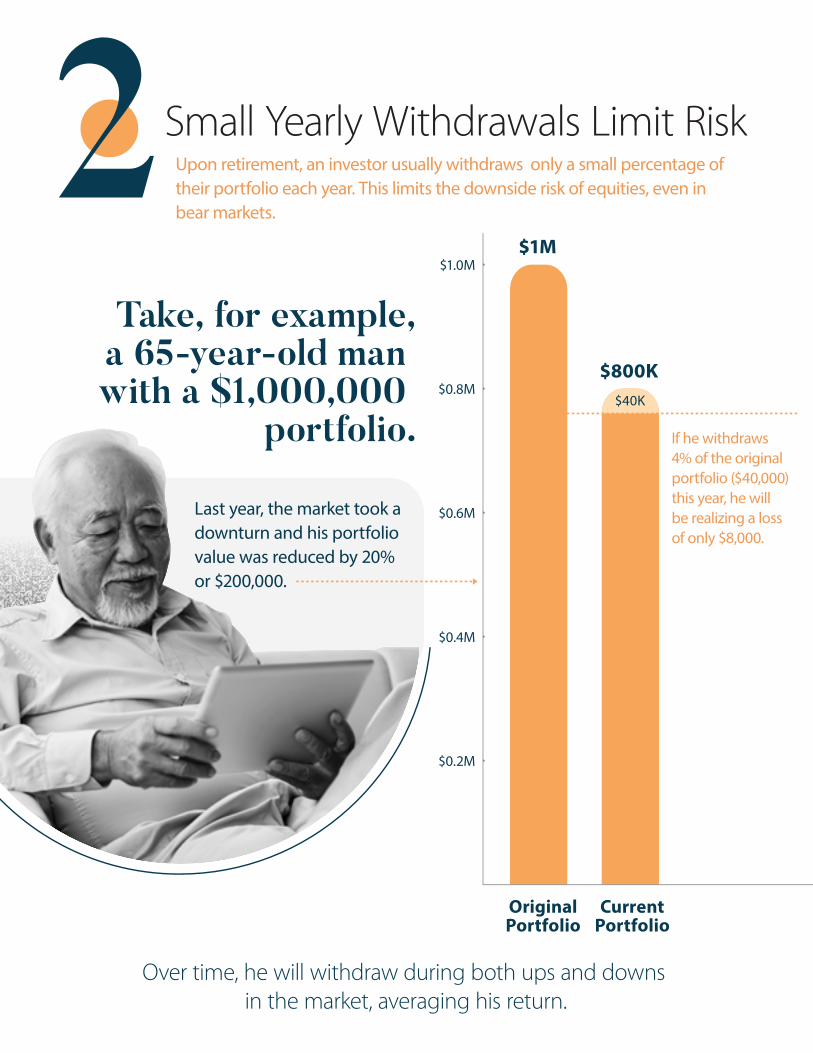

Small Yearly Withdrawals Limit Risk2Take, for example,

a 65-year-old man with a $1,000,000

portfolio.

Last year, the market took a downturn and his portfolio value was reduced by 20% or $200,000.

Over time, he will withdraw during both ups and downs in the market, averaging his return.

Upon retirement, an investor usually withdraws only a small percentage of their portfolio each year. This limits the downside risk of equities, even in bear markets.

If he withdraws4% of the original portfolio ($40,000) this year, he will be realizing a loss of only $8,000.

$0.2M

$0.4M

$0.6M

$0.8M

$1.0M$1M

$800K$40K

CurrentPortfolio

OriginalPortfolio

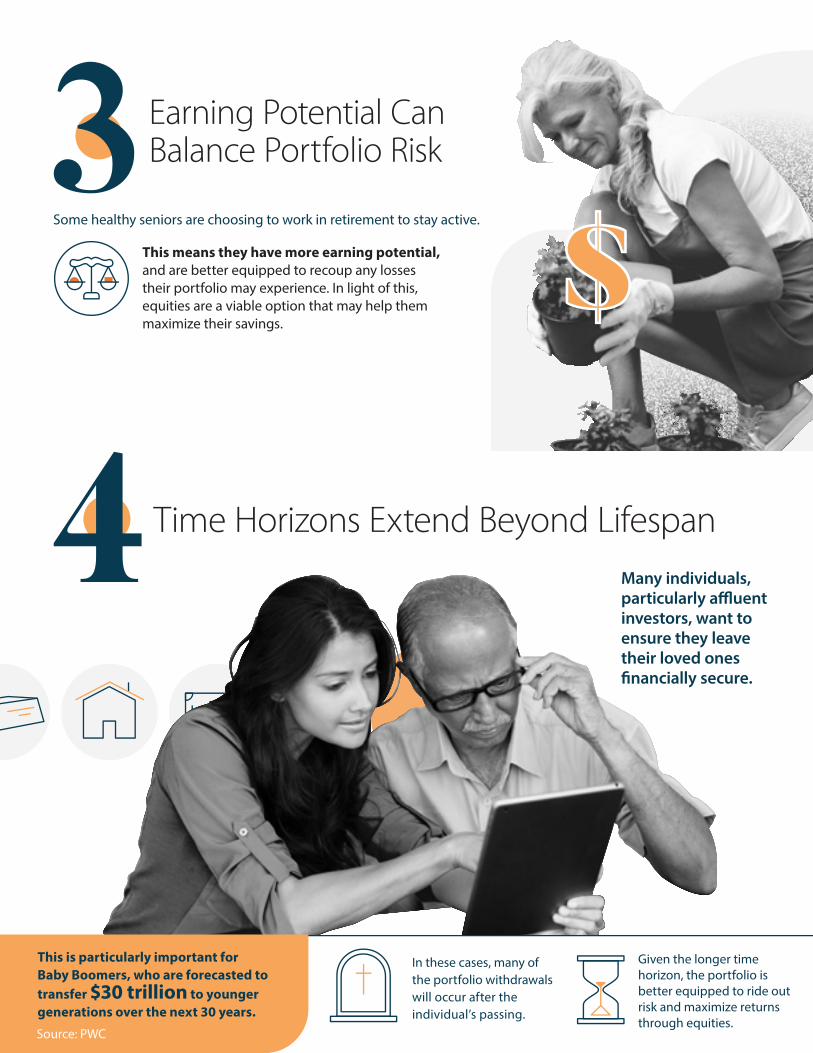

Many individuals, particularly a�uent investors, want to ensure they leave their loved ones �nancially secure.

This means they have more earning potential, and are better equipped to recoup any losses their portfolio may experience. In light of this, equities are a viable option that may help them maximize their savings.

Some healthy seniors are choosing to work in retirement to stay active.

Earning Potential Can Balance Portfolio Risk3

Time Horizons Extend Beyond Lifespan 4

Given the longer time horizon, the portfolio is better equipped to ride out risk and maximize returns through equities.

In these cases, many of the portfolio withdrawals will occur after the individual’s passing.

This is particularly important for Baby Boomers, who are forecasted to transfer $30 trillion to younger generations over the next 30 years.

Source: PWC

Holding equities can be an exercise in psychological discipline. An investor must be able to ride out the ups and downs in the stock market.

If they can, there’s a good chance they will be rewarded. Equities have the potential to deliver long-term returns that combat longevity risk.

By allocating more of their portfolio to equities, investors can greatly increase the odds of retiring whenever they want - with funds that will last their entire lifetime.

H I G H E R R I S K ,

Higher PotentialReward

Pr e s e n te d by

More than investing.Invested.

MS37dd-05/191814291

New York Life Investments is both a service mark and the common trade name of the investment advisors a�liated with New York Life Insurance Company. New York Life Investments, an indirect subsidiary of New York Life Insurance Company, New York, NY 10010, provides investment advisory products and services. Securities distributed by NYLIFE Distributors LLC, 30 Hudson Street, Jersey City, NJ 07302. NYLIFE Distributors LLC is a Member FINRA/SIPC.

New York Life, MainStay Investments, and their a�liates do not provide legal, accounting, or tax advice. You should obtain advice speci�c to your circumstances from your own legal, accounting, and tax advisors.

This material represents an assessment of the market environment as at a speci�c date; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

This material contains general information only and does not take into account an individual's �nancial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a �nancial advisor before making an investment decision.