What can be learned from the UK - German Run-Off …. IFDS GRF 2015...AMP Hazell Carr £35m Group...

33

Confidential Closed book strategy. What can be learned from the UK ? Ian Betley VP, Head of Sales EMEA, DSTi Holdings and IFDS Group

Transcript of What can be learned from the UK - German Run-Off …. IFDS GRF 2015...AMP Hazell Carr £35m Group...

Confidential

Closed book strategy. What can be learned from the UK ?

Ian Betley

VP, Head of Sales EMEA,

DSTi Holdings and IFDS Group

2 Confidential

Agenda

• A brief history of closed book in the UK

• The main players and their approach

• What can you learn ?

• The Good

• The Bad

• The Ugly

• What does next generation look like ?

• Insurer demands

• Consumer demands

• Market Sector influences

• Summary

3 Confidential

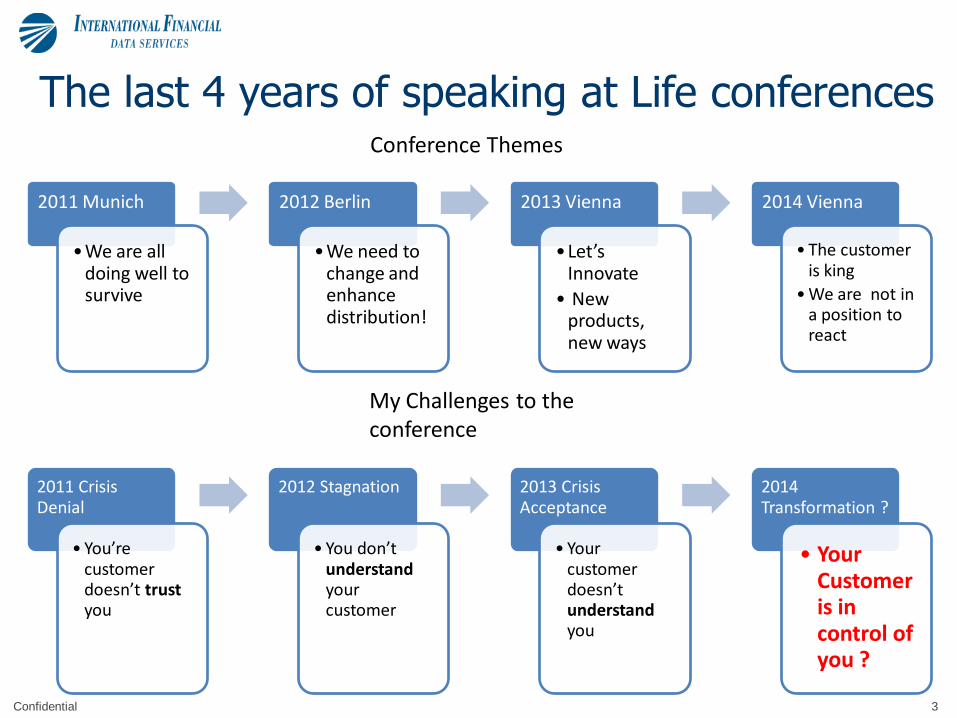

2011 Munich

•We are all doing well to survive

2012 Berlin

•We need to change and enhance distribution!

2013 Vienna

•Let’s Innovate

• New products, new ways

2014 Vienna

• The customer is king

• We are not in a position to react

The last 4 years of speaking at Life conferences

2011 Crisis Denial

• You’re customer doesn’t trust you

2012 Stagnation

• You don’t understand your customer

2013 Crisis Acceptance

• Your customer doesn’t understand you

2014 Transformation ?

• Your Customer is in control of you ?

Conference Themes

My Challenges to the conference

4 Confidential

Insurer

Challenges in the UK market

Customer Fragility

• Confidence in the financial services market

• Transparency of suppliers

• Customer Experience

• Customer needs – portfolio v commoditisation

Product Innovation

• Throw away the Heritage

• Buy new platforms

• Tactical Reponses

• Partner v build

Economy & market

• Low savings & annuity rates

• Market volatility

• Pension Gap

• Regulation

• Government initiatives e.g auto enrollment – does that make EBC’s a channel ?

Cost of Entry

• Speed to market

• Brand protection

• Getting it right first time

• Cost of failure / exit

• Cost of Channel maintenance

5 Confidential

Now the ‘real’ challenges

• Legacy technology with poor quality data

• Spaghetti of systems caused by mergers and tactical solutions

• Processes embedded in peoples heads, with many manual workarounds

• Stagnation of the working population

• Poor quality staff – with no design or implementation skills

• Lifers in the business

• Union protected

• Public Sector / Fiefdom culture

• Short-termism view of any change or transformation

• Driven by shareholders and executive bonuses

6 Confidential

The drivers for outsourcing: UK vs Europe

Platform Consolidation

Process Rationalisation

New Products Processes

Divest Non-Core

UK market Europe comparison

• Problems with old and multiple platforms. Inefficient and costly to maintain.

• Duplication of activities into multiple systems

• Fewer legacy products so fewer truly legacy platforms

• However, systems replacement and consolidation still attractive in some cases

• Inefficient processes and duplication of activities across locations

• Non-standard processes

• Positioning new products, admin capability in a cost-efficient way post-RDR etc.

• Faster time to market

• Focus on core business / what they do best • Manage out overheads associated with niche

lines (e.g. DB Pensions) or non-core activities.

• Opportunities for improved efficiency will be attractive

• Less fundamental restructuring of products due to regulation

• However, improved time to market still attractive

• Probably less of an issue for most European players

Cost avoidance / mgmt

• Convert fixed costs to variable for reducing books

• Mitigate set-up costs for new businesses

• Cost reduction always attractive

Many of the drivers for L&P BPO in the UK are more intense than they are in Europe, hence the

European market has been slower to develop

• Standardise platforms

• Data migration to preferred platform

• Standardisation, de-duplication

• Process re-engineering

• Improve efficiency

• Offshore

• Create compelling new products that can

be serviced at low cost

• Create IFA interfaces

• Access to more plentiful skills in non-core

areas

• Specific niche processor providing

services

• Benefit from TPA operational efficiencies

and economies of scale

• Contractual certainty on costs and

operational risk

Solution requirements

6

7 Confidential

UK market landscape

Market trends

Outsourcing well established in the UK L&P market - few large players left to

outsource, however not all deals have achieved the sought-for levels of

transformation (especially systems consolidation)

Potentially becoming saturated as far as closed books (which account for the

majority of the market to date) are concerned

However, some deals due for renewal in the next 2-3 years and many small books

still run in-house

Increasing willingness to consider outsourcing as a strategic approach to launching

new products and developing new business

Largest L&P market in Europe in terms of premium (although

Germany and France now employ more people)

Protection market has been flat for a number of years,

investment AUM impacted by the GFC

RDR, as well as developments in consumer attitudes, shifting the

balance of distribution, but only slowly

Increasing interest in on-line and multi-channel transaction and

servicing driving new system requirements

TPA development

Regulation constantly evolving in both UK and

Europe, with uncertain future effects on e.g. VAT

treatment

Recent years have seen significant IT change

driven by e.g. Solvency II and RDR

The FSA has become significantly stricter on the

regulatory status of TPAs

Regulation

The UK outsourcing market is well-established, but growth has slowed significantly…

8 Confidential

8

UK market landscape

0

10

20

30

40

50

60

70

200020012002200320042005200620072008200920102011201220132014

Policies (m)

Policies (m)

UK L&P TPA market growth by number of policies…

9 Confidential

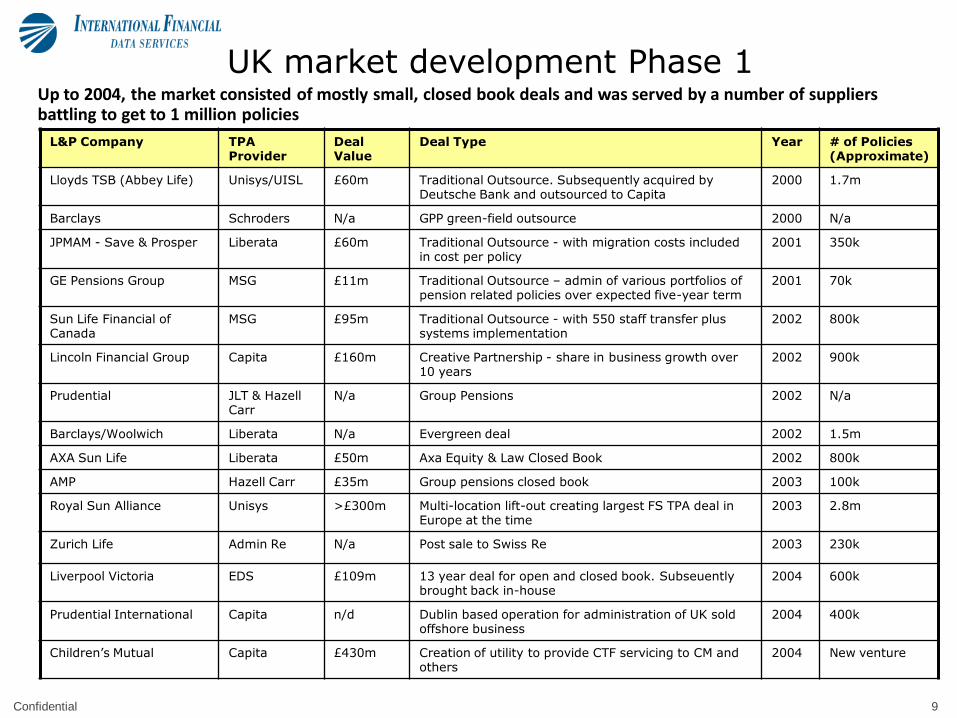

Up to 2004, the market consisted of mostly small, closed book deals and was served by a number of suppliers battling to get to 1 million policies

L&P Company TPA Provider

Deal Value

Deal Type Year # of Policies (Approximate)

Lloyds TSB (Abbey Life) Unisys/UISL £60m Traditional Outsource. Subsequently acquired by Deutsche Bank and outsourced to Capita

2000 1.7m

Barclays Schroders N/a GPP green-field outsource 2000 N/a

JPMAM - Save & Prosper Liberata £60m Traditional Outsource - with migration costs included in cost per policy

2001 350k

GE Pensions Group MSG £11m Traditional Outsource – admin of various portfolios of pension related policies over expected five-year term

2001 70k

Sun Life Financial of Canada

MSG £95m Traditional Outsource - with 550 staff transfer plus systems implementation

2002 800k

Lincoln Financial Group Capita £160m Creative Partnership - share in business growth over 10 years

2002 900k

Prudential JLT & Hazell Carr

N/a Group Pensions 2002 N/a

Barclays/Woolwich Liberata N/a Evergreen deal 2002 1.5m

AXA Sun Life Liberata £50m Axa Equity & Law Closed Book 2002 800k

AMP Hazell Carr £35m Group pensions closed book 2003 100k

Royal Sun Alliance Unisys >£300m Multi-location lift-out creating largest FS TPA deal in Europe at the time

2003 2.8m

Zurich Life Admin Re N/a Post sale to Swiss Re 2003 230k

Liverpool Victoria EDS £109m 13 year deal for open and closed book. Subseuently brought back in-house

2004 600k

Prudential International Capita n/d Dublin based operation for administration of UK sold offshore business

2004 400k

Children’s Mutual Capita £430m Creation of utility to provide CTF servicing to CM and others

2004 New venture

UK market development Phase 1

10 Confidential

From 2005-2010, deals increased in size, included more open books and the market became dominated by Capita with circa 26 million policies

L&P Company TPA Provider Deal Value Deal Type Year # of Policies (approximate)

Pearl TCS (Diligenta) £486m Collection of closed books acquired by Pearl 2005 3.8m

Living Time (AIG) Vertex n/a Launch of new virtual life company 2006 n/a

Zurich UK Life Capita £300m Closed and open book. Planned future product development on Elixir platform

2006 2.8m

Aviva Swiss Re n/a System consolidation and cost reduction play 2007 3m

Prudential Capita £722m Predominantly “mature” (closed) L&P book. Capita also acquired PPMS (Mumbai)

2007 5.5m

Resolution Capita £580m Collection of mostly closed books acquired by Resolution. Resolution since acquired by Pearl. Scottish Provident since sold to Royal London

2007 4.5m

CFS Capita £270m Open book and future product development 2007 4.5m

HSBC Life Vertex n/a Support for new product launches 2007 n/a

Deutsche Bank (Abbey Life) Capita £130m Closed book acquired from LTSB in 2007 2009 1.1m

AXA Capita £500m Closed life and pensions book 2009 3.2m

Equitable Life HCL £120m 30 year deal to cover areas such as IT operational support, policy administration and financial, actuarial and call centre.

2009

UK market development Phase 2

11 Confidential

11

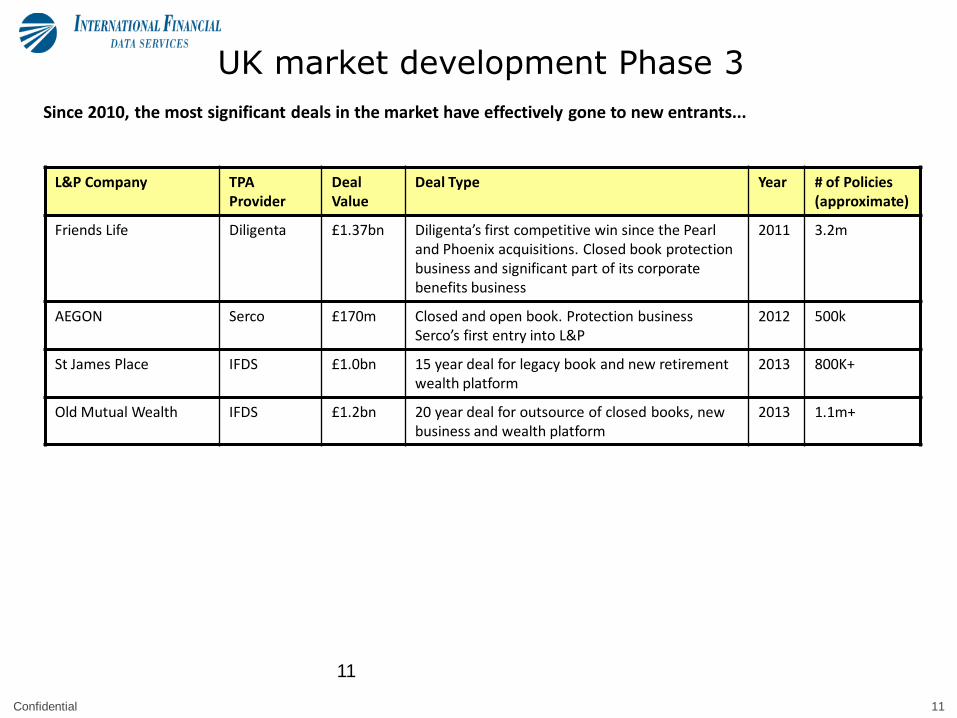

Since 2010, the most significant deals in the market have effectively gone to new entrants...

L&P Company TPA Provider

Deal Value

Deal Type Year # of Policies (approximate)

Friends Life Diligenta £1.37bn Diligenta’s first competitive win since the Pearl and Phoenix acquisitions. Closed book protection business and significant part of its corporate benefits business

2011 3.2m

AEGON Serco £170m Closed and open book. Protection business Serco’s first entry into L&P

2012 500k

St James Place IFDS £1.0bn 15 year deal for legacy book and new retirement wealth platform

2013 800K+

Old Mutual Wealth IFDS £1.2bn 20 year deal for outsource of closed books, new business and wealth platform

2013 1.1m+

UK market development Phase 3

12 Confidential

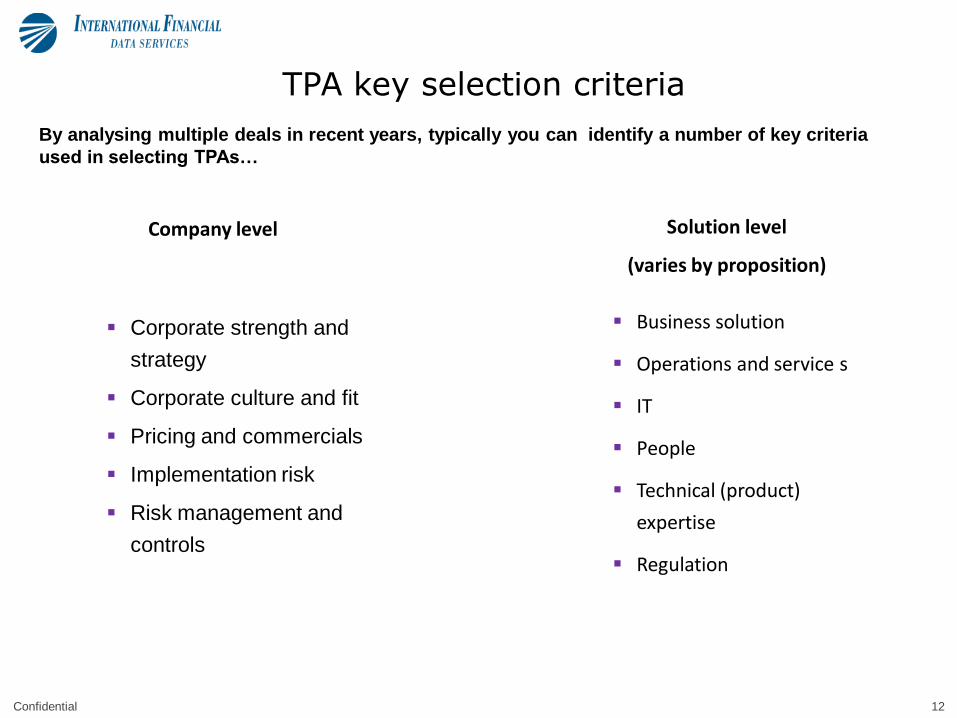

TPA key selection criteria

Company level Solution level

(varies by proposition)

Corporate strength and

strategy

Corporate culture and fit

Pricing and commercials

Implementation risk

Risk management and

controls

Business solution

Operations and service s

IT

People

Technical (product)

expertise

Regulation

By analysing multiple deals in recent years, typically you can identify a number of key criteria

used in selecting TPAs…

13 Confidential

One approach to segmenting the UK market (in terms of both deals and competitors) is by level of process-driven vs systems-driven rationalisation…

Significant

Significant

Low

Low Platform Rationalisation

Pro

ce

ss R

atio

na

lisa

tio

n

UK market segmentation – outsourced positioning

Transformational change including

process and platform

rationalisation

New Products

Niche

Process rationalisation

on current platform

IT system consolidation

programs

14 Confidential

Deal type Typical characteristics Example competitors

Transformation

al change

• Focused on cost and service

• Ongoing scale efficiency through platform migration

• Closed and open books

• Liberata (now HCL) once dominated this

market (for closed books), but failed to achieve

scale

• Diligenta the only player currently claiming to

be able to achieve large-scale platform

migration

• Wipro, Cognizant etc with aspirations but not

yet credible track record in UK

Process

rationalisation

• Focused on driving down costs, often at the

(perceived) expense of service

• Usually using existing systems, often existing

infrastructure and staff (after TUPE)

• Capita

• Serco (new entrant, just won AEGON)

System

consolidation

• Often in-house or with ITO assistance

• Significant use of offshore IT resources

• Frequently consolidating among existing in-house

platforms

• Wipro

• Cognizant

• HCL

New products • Often gap-fill products

• Need for speed to market

• Existing systems unable to support

• May be on “Build Operate Transfer” basis

• Opal

Niche • Relatively small (typically less than 500k policies)

• Closed books, no longer core products

• Old, complex products – e.g. DB pensions –

requiring significant technical expertise

• JLT

• Hazell Carr

• Capita Hartshead

UK market segmentation

15 Confidential

Comparison of Market

Capita IFDS Diligenta HCL Liberata

Cost reduction

Operational efficiency

Flexibility of service

model

Breadth of technology

coverage

Risk & compliance

framework / control

Proven Migration

Capability

Brand / reputation

Future TCO/ Contract

Sustainability

Ease / cost of exit

Focus on FS

Industry / appetite

16 Confidential

IFDS Market Position

Total Cost

of

Ownership

True business value

Low

High

Low High

Limited sustainability in contracts – high degrees of

financial engineering / short-termism

Indian Pure Plays

minimal local touch – high arbitrage

Distanced delivery empowerment

IFDS Model

Right blend of on/offshore resources. Operational efficiency.

Modern Technology

Large multinational consultancies / high cost base / high client growth

aspirations

Disjointed & diverse structures

Tactical BPO / Technology replacement

Same Mess for Less Operations and Offshore driven

Heritage Outsource (price per policy $/hr )

Strategic integration of wealth and heritage - Customer Centricity

GenPact

Wipro

Capgemini

Accenture

TCS Diligenta

Capita HCL

IFDS Patni

17 Confidential

Offshore ITO BPO Transformational BPO

Continuous transformation

/ GBS Outsource Maturity

Val

ue

ad

d

Same mess for less Sustainable value

Supplier / Partner evolution

18 Confidential

0204060

80

Cost benefit

Benefit Impact across the maturity model

Transformation

Same mess for less

19 Confidential

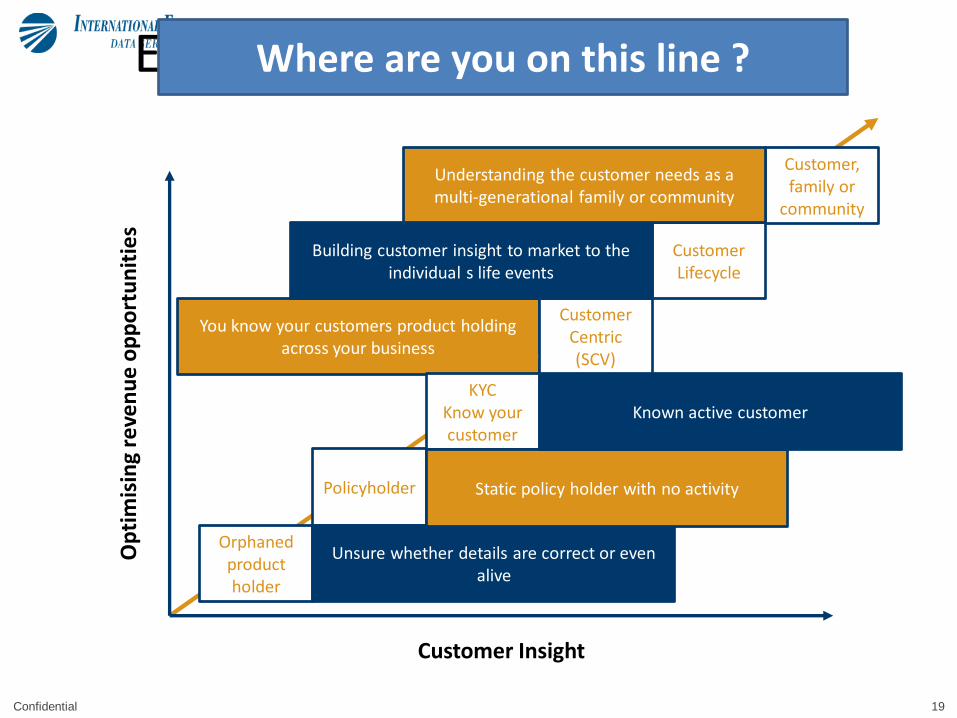

You know your customers product holding across your business

Op

tim

isin

g re

ven

ue

op

po

rtu

nit

ies

Customer Insight

Orphaned product holder

Policyholder

KYC Know your customer

Customer Centric (SCV)

Customer Lifecycle

Customer, family or

community

Unsure whether details are correct or even alive

Static policy holder with no activity

Known active customer

Building customer insight to market to the individual s life events

Understanding the customer needs as a multi-generational family or community

Engaging with your customer Where are you on this line ?

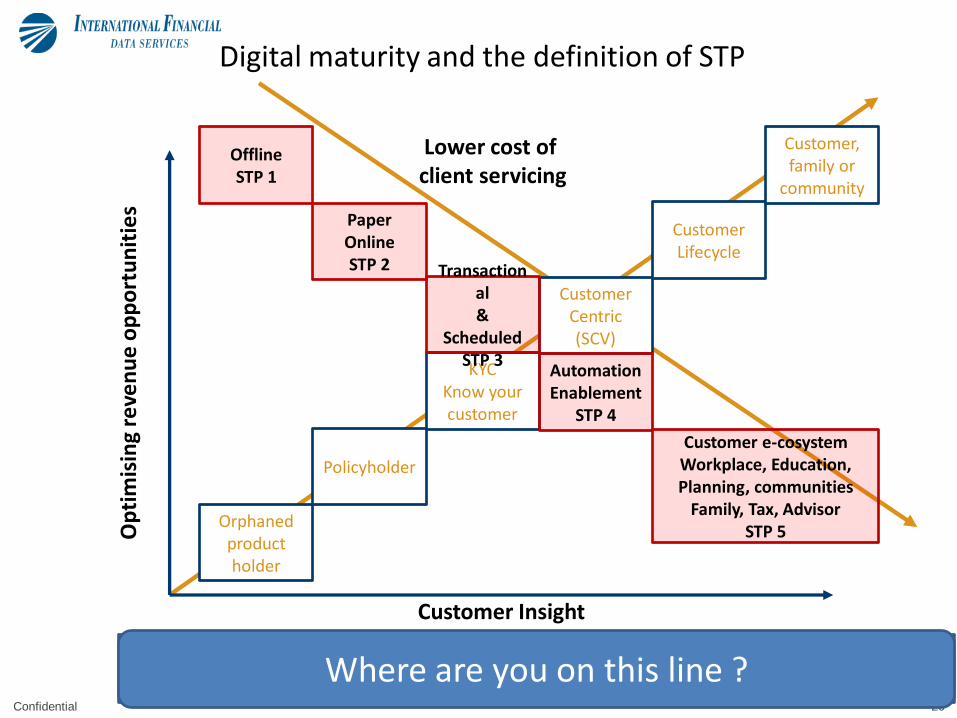

20 Confidential

Op

tim

isin

g re

ven

ue

op

po

rtu

nit

ies

Customer Insight

Orphaned product holder

Policyholder

KYC Know your customer

Customer Centric (SCV)

Customer Lifecycle

Customer, family or

community

Transactional &

Scheduled STP 3

Customer e-cosystem Workplace, Education, Planning, communities

Family, Tax, Advisor STP 5

Automation Enablement

STP 4

Offline STP 1

Paper Online STP 2

Lower cost of client servicing

Conclusion : The more you know about your customer the more you can sell. The more the customer engages the more you can automate and the cheaper they are

to administer.

Digital maturity and the definition of STP

Where are you on this line ?

21 Confidential

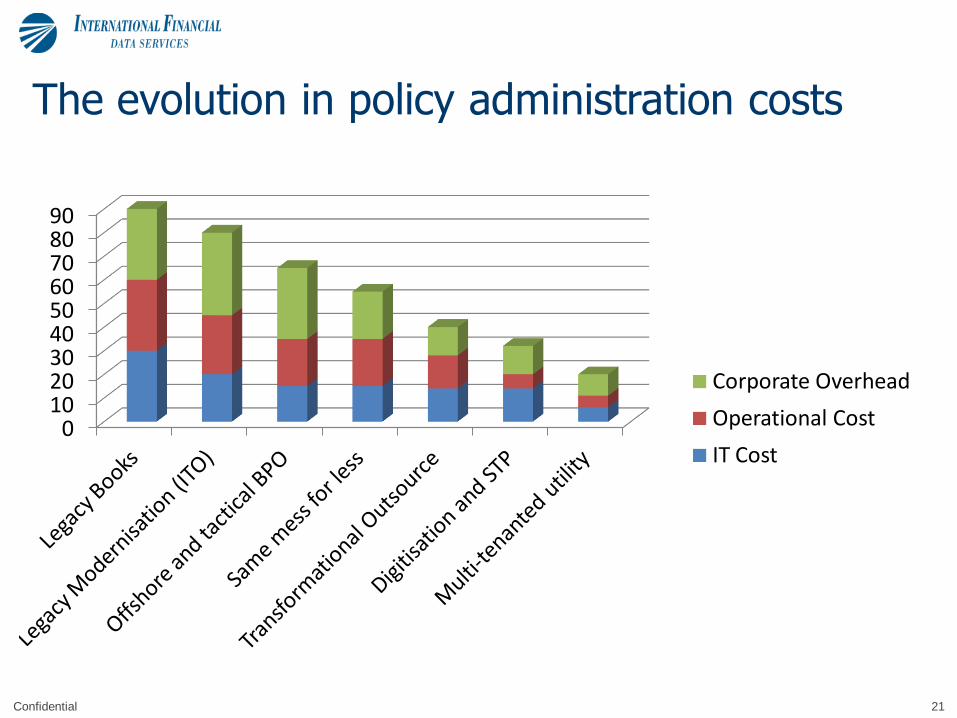

The evolution in policy administration costs

0 10 20 30 40 50 60 70 80 90

Corporate Overhead

Operational Cost

IT Cost

22 Confidential

recommendations

• Build the old world in the new

• Underestimate migration and the data

• Lose sight of retention and customer experience

• Legacy products not legacy customers

• Take a short term view

• Build a business case around the as is – to be model – look at sustainability

• Workers union – legacy staff/ culture

• Jp’s retention slide

• Adopt v adapt

• Issues

• Bad contracts – unsustainable

• rationalisation

• Sack the old / offshore – lose the knowledge

• Tell the story of wesleyan and guardian life aviva prudential

• Round 1 - 90% contracts unsustainable / failed to deliver / renegotiated over budget / high attrition / poor customer experience

23 Confidential

So how has it gone ? • 80% of the contracts are unsustainable and clients are unhappy

with the outcome

• They have failed due to • Inability to migrate / rationalise platforms (Prudential)

• Inability to change due to legacy – same staff different employer (Liberata)

• Poor knowledge transfer has led to programme failure or added cost to buy back in the knowledge

• Contracts badly written

• Old processes implemented – cost of keeping lights on too high

• Staff protected against redundancy / performance management

• Short term view on cost certainty with too many dependencies on building scale or driving out efficiencies

• Consequences

• Margin pressure by outsourcers lead to poor customer service

• Stagnation and no thought-leadership innovation or drive for improvement

• Treated as a wasting asset – no performing as a wasting asset – or the value has been bled out of the books

• High risk from regulatory change

24 Confidential

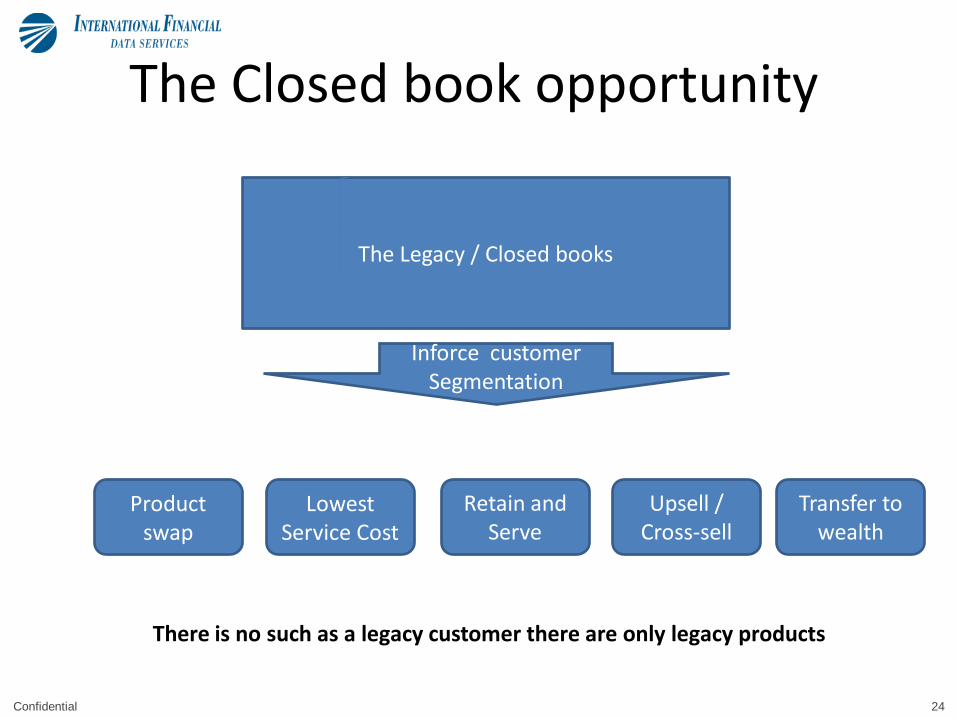

The Closed book opportunity

The Legacy / Closed books

There is no such as a legacy customer there are only legacy products

Inforce customer Segmentation

Product swap

Upsell / Cross-sell

Retain and Serve

Lowest Service Cost

Transfer to wealth

25 Confidential

Closed book – release the embedded value

Low Value but potential

Upsell and Cross-sell more products

High Value in Transition

Engage & Transfer to wealth platform

Offer new products for at and post retirement

Low Value

Service at lowest cost of ownership

High Value

Engage protect and provide excellent customer experience

Closed Book

Strategy

Assets Under Management

Customer Insight

26 Confidential

Focus on asset retention and embedded value

0

200'000

400'000

600'000

800'000

1'000'000

1'200'000

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Lapse 10%

Lapse 13%

Added value

Difference in total policy years over 10 years at 10% lapse rate to 13% is just under 1,000,000

TIME

AV

. CO

ST P

ER

PO

LIC

Y

27 Confidential

What could this look like ? Assisting our clients’ business evolution

• True transformation of operating models to one that can absorb business change incrementally and fluidly, instead of requiring periodic step changes and transition projects.

• We can service both old and new worlds and enable a customer centric view across all books of business

Upgrade of closed book or open book customers to wealth platform services (e.g. as wealth increases with age or third party assets are captured and consolidated)

Closed book customers becoming open book or wealth customers (e.g. up-sell / cross-sell), capture of third party investment assets or insurance covers, especially on life events)

Wealth customers becoming open book or closed book customer (e.g. wealth services are no longer required by the customer as asset values decline)

Open book or wealth customers becoming closed book customers (e.g. product closure)

28 Confidential

Service model flexibility – it’s not all or nothing

Service model

Capable of serving insurance companies with technology and BPO solutions for wealth, heritage / traditional L&P and funds in an owner-operated, multi-tenanted/shared service environment

Alternatively, our clients have the flexibility to adjust their servicing model based on:

• business segment

• business function

• service channel

• product type or variant

• by customer or customer segment

• by distribution channel

Goal alignment – we use the same systems!

29 Confidential

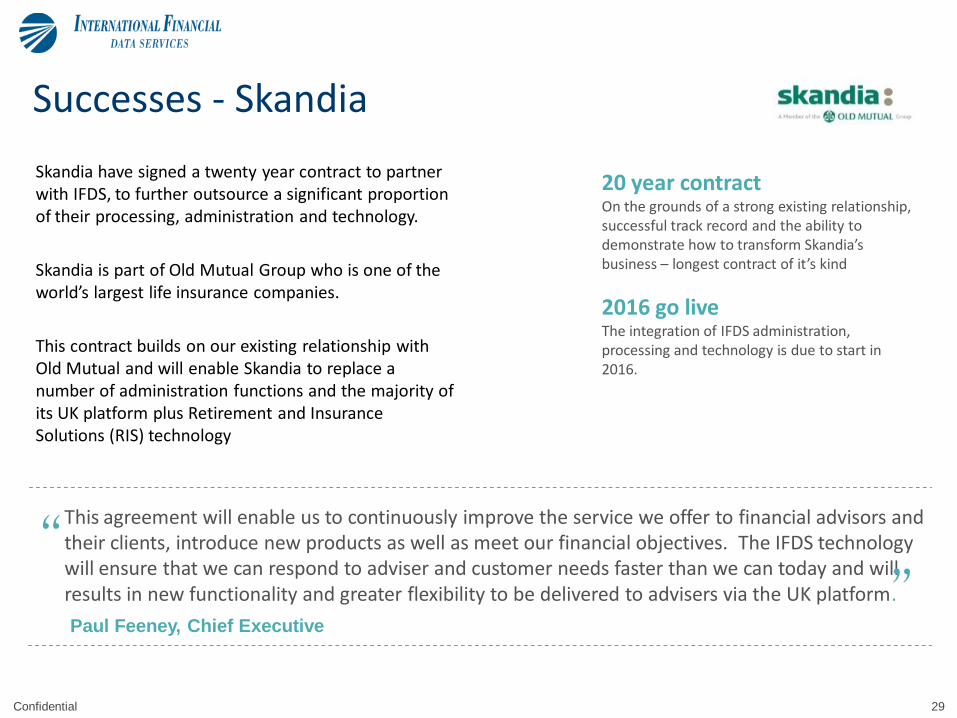

Successes - Skandia

Skandia have signed a twenty year contract to partner with IFDS, to further outsource a significant proportion of their processing, administration and technology.

Skandia is part of Old Mutual Group who is one of the world’s largest life insurance companies.

This contract builds on our existing relationship with Old Mutual and will enable Skandia to replace a number of administration functions and the majority of its UK platform plus Retirement and Insurance Solutions (RIS) technology

This agreement will enable us to continuously improve the service we offer to financial advisors and their clients, introduce new products as well as meet our financial objectives. The IFDS technology will ensure that we can respond to adviser and customer needs faster than we can today and will results in new functionality and greater flexibility to be delivered to advisers via the UK platform.

Paul Feeney, Chief Executive

“ “ 20 year contract On the grounds of a strong existing relationship, successful track record and the ability to demonstrate how to transform Skandia’s business – longest contract of it’s kind

2016 go live The integration of IFDS administration, processing and technology is due to start in 2016.

30 Confidential

Closed book total value proposition?

Support the whole of business lifecycle

Our end to end service model with our own technology (plus surround technologies) can accommodate both life and savings products to support the whole customer journey

Exceptional experience throughout the whole customer journey

Customer benefits

Insurer benefits

Insurer outcomes

IFDS delivery

31 Confidential

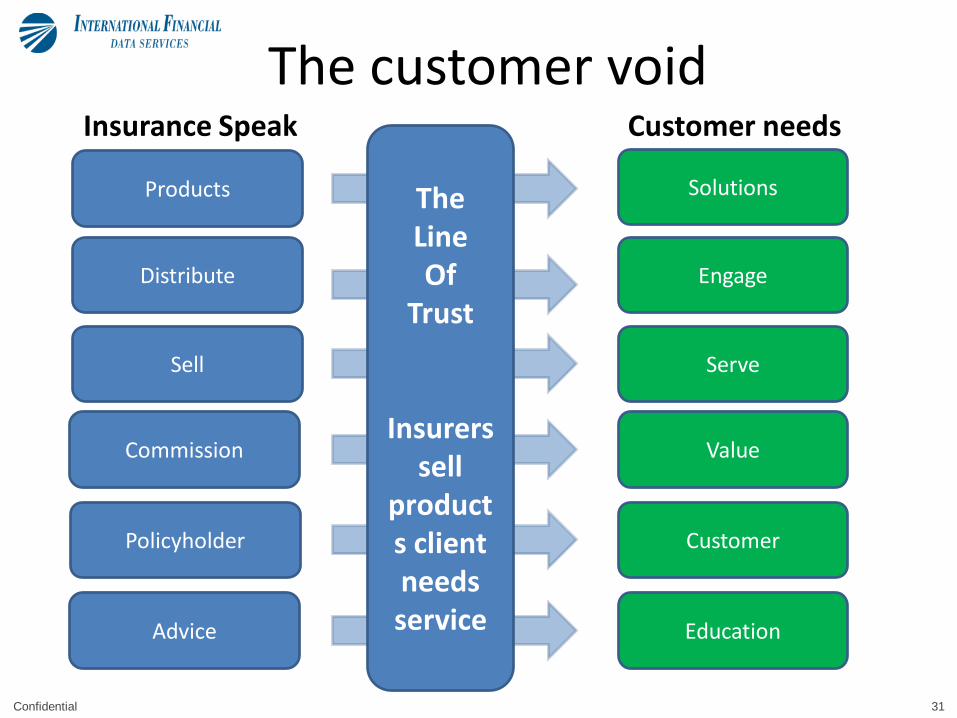

The customer void

Products

Insurance Speak

Distribute

Sell

Commission

Policyholder

Advice

Solutions

Customer needs

Education

Customer

Value

Serve

Engage

The Line Of

Trust

Insurers sell

products client needs service

32 Confidential

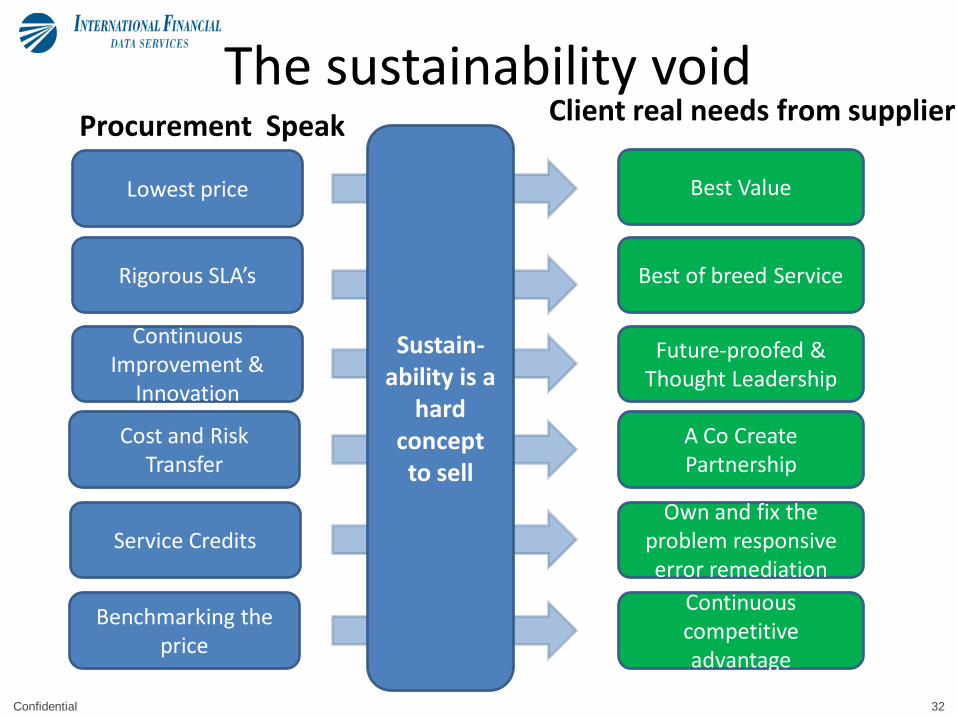

The sustainability void

Lowest price

Procurement Speak

Rigorous SLA’s

Continuous Improvement &

Innovation

Cost and Risk Transfer

Service Credits

Benchmarking the price

Best Value

Client real needs from supplier

Continuous competitive advantage

Own and fix the problem responsive error remediation

A Co Create Partnership

Future-proofed & Thought Leadership

Best of breed Service

Sustain-ability is a

hard concept to sell

33 Confidential

Top 5 recommendations / considerations

1. You have legacy products not legacy customers – run-off does not have to be treated as a wasting asset – don’t forget retention and customer experience

2. This is a complex business, tactical tinkering will create a bigger technology or operational debt

3. Outsourcing can work well, but the contracts need to be sustainable and release the embedded value in the business not destroy it

4. When building the business case – it’s not just an ‘as is – to be’ comparison. Look at the future cost of ownership as that is the only way to build sustainability into any outsource contract

5. Don’t try and replicate the old world in the new world. Adopt don’t adapt.