Welcome to the TSAHC Lender Training Module I - … · Welcome to the TSAHC Lender Training ....

41

Welcome to the TSAHC Lender Training Module I - The Basics Audio available through computer speakers and by dialing (877) 347-4079 using code: 3333

Transcript of Welcome to the TSAHC Lender Training Module I - … · Welcome to the TSAHC Lender Training ....

Welcome to the TSAHC Lender Training

Module I - The Basics Audio available through computer speakers and by dialing

(877) 347-4079 using code: 3333

About TSAHC TSAHC is a 501(c)3 nonprofit organization. Our mission is to serve the housing needs of low-income Texans and other underserved populations. We fulfill our mission through our concept of:

About TSAHC As a part of our “Buy” component, we have two programs available to help Texans purchase a home.

Home Buyer Programs: • Homes for Texas Heroes Home Loan Program • Home Sweet Texas Home Loan Program

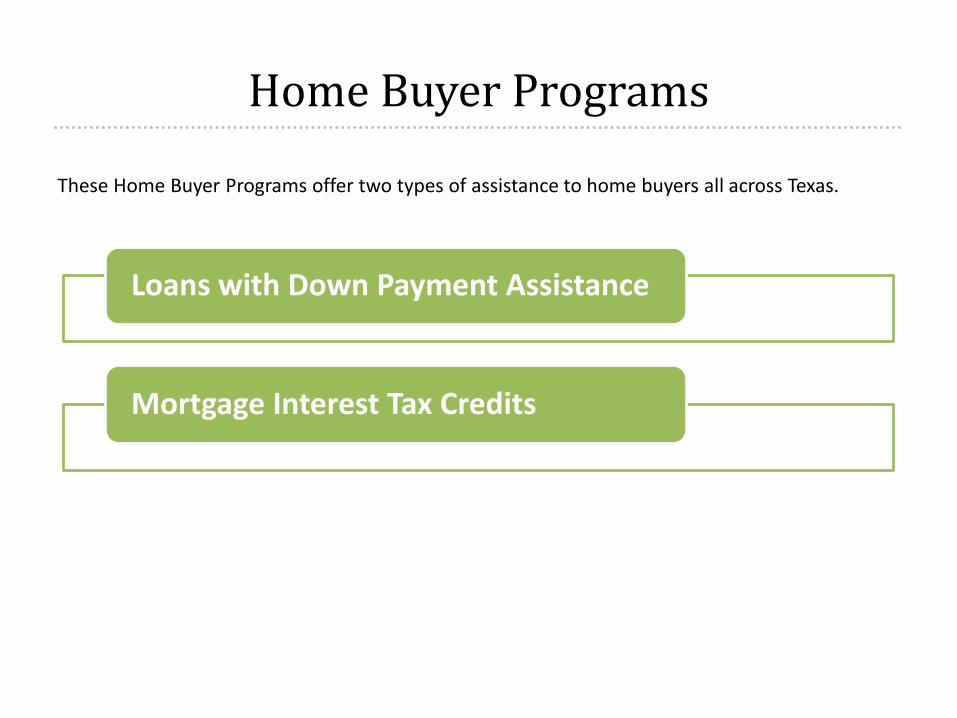

Home Buyer Programs

These Home Buyer Programs offer two types of assistance to home buyers all across Texas.

Loans with Down Payment Assistance

Mortgage Interest Tax Credits

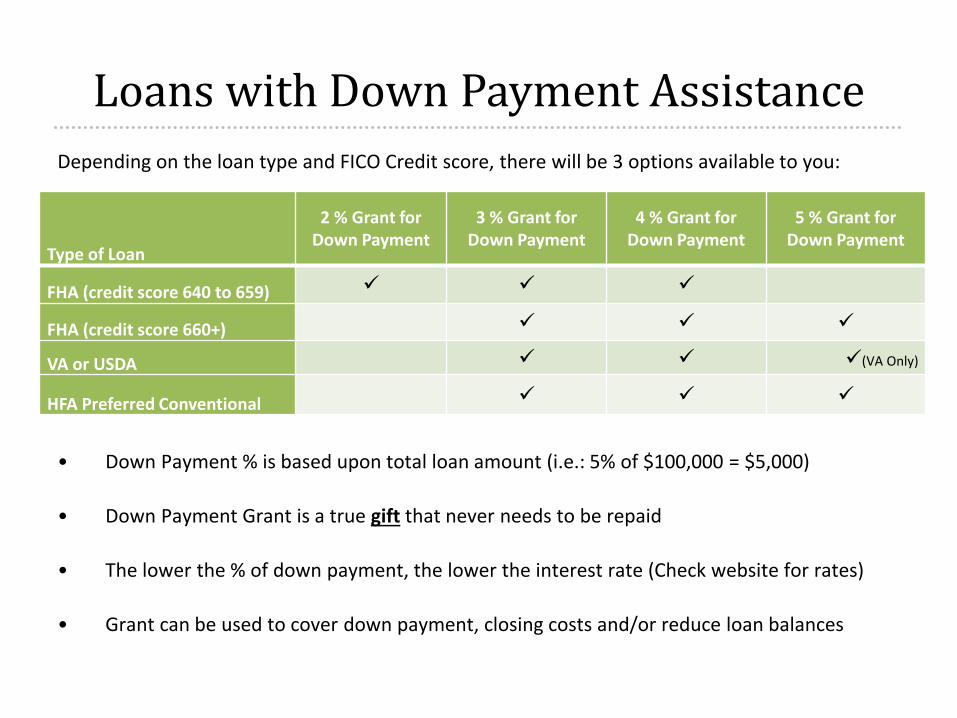

Loans with Down Payment Assistance Depending on the loan type and FICO Credit score, there will be 3 options available to you:

• Down Payment % is based upon total loan amount (i.e.: 5% of $100,000 = $5,000)

• Down Payment Grant is a true gift that never needs to be repaid

• The lower the % of down payment, the lower the interest rate (Check website for rates)

• Grant can be used to cover down payment, closing costs and/or reduce loan balances

Type of Loan

2 % Grant for Down Payment

3 % Grant for Down Payment

4 % Grant for Down Payment

5 % Grant for Down Payment

FHA (credit score 640 to 659)

FHA (credit score 660+)

VA or USDA (VA Only)

HFA Preferred Conventional

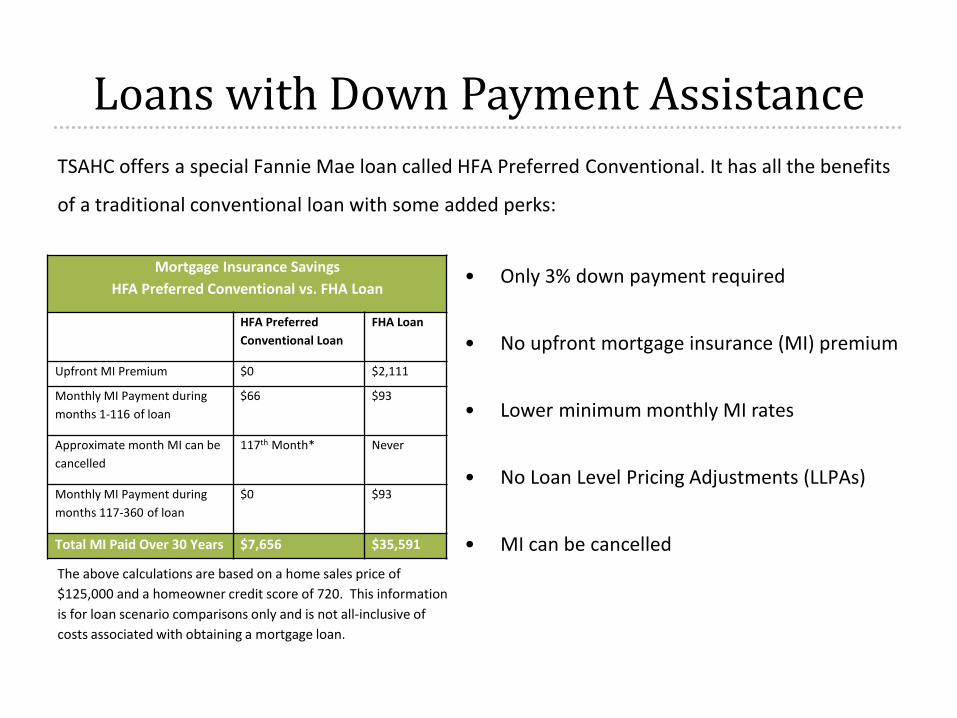

TSAHC offers a special Fannie Mae loan called HFA Preferred Conventional. It has all the benefits

of a traditional conventional loan with some added perks:

Mortgage Insurance Savings HFA Preferred Conventional vs. FHA Loan

HFA Preferred Conventional Loan

FHA Loan

Upfront MI Premium $0 $2,111

Monthly MI Payment during months 1-116 of loan

$66 $93

Approximate month MI can be cancelled

117th Month* Never

Monthly MI Payment during months 117-360 of loan

$0 $93

Total MI Paid Over 30 Years $7,656 $35,591

The above calculations are based on a home sales price of $125,000 and a homeowner credit score of 720. This information is for loan scenario comparisons only and is not all-inclusive of costs associated with obtaining a mortgage loan.

Loans with Down Payment Assistance

• Only 3% down payment required

• No upfront mortgage insurance (MI) premium

• Lower minimum monthly MI rates

• No Loan Level Pricing Adjustments (LLPAs)

• MI can be cancelled

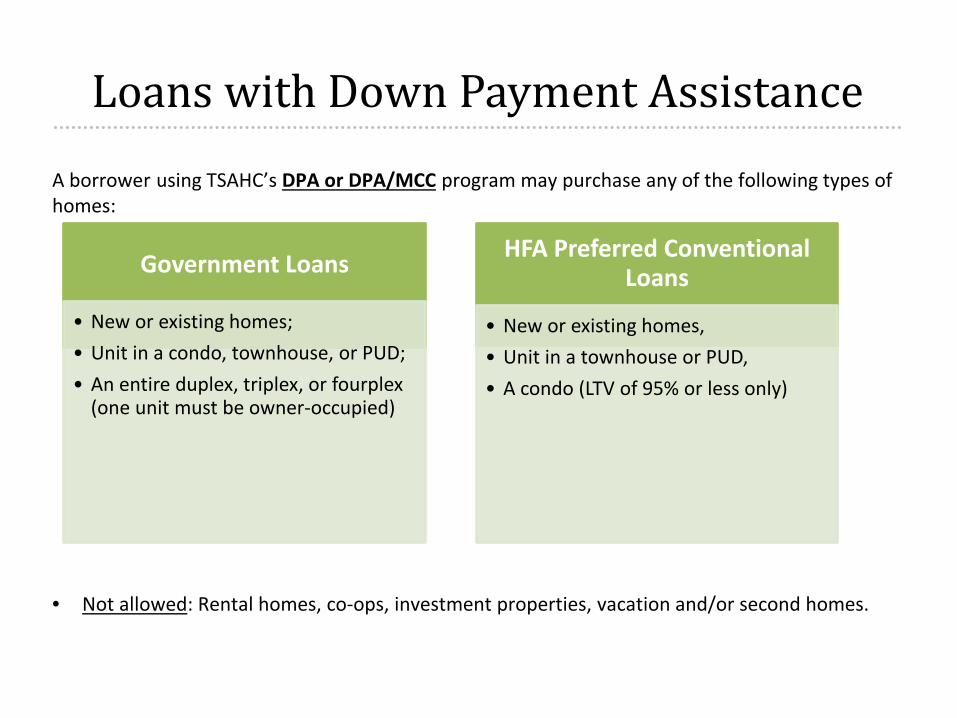

A borrower using TSAHC’s DPA or DPA/MCC program may purchase any of the following types of homes:

• Not allowed: Rental homes, co-ops, investment properties, vacation and/or second homes.

Government Loans

• New or existing homes; • Unit in a condo, townhouse, or PUD; • An entire duplex, triplex, or fourplex

(one unit must be owner-occupied)

HFA Preferred Conventional Loans

• New or existing homes, • Unit in a townhouse or PUD, • A condo (LTV of 95% or less only)

Loans with Down Payment Assistance

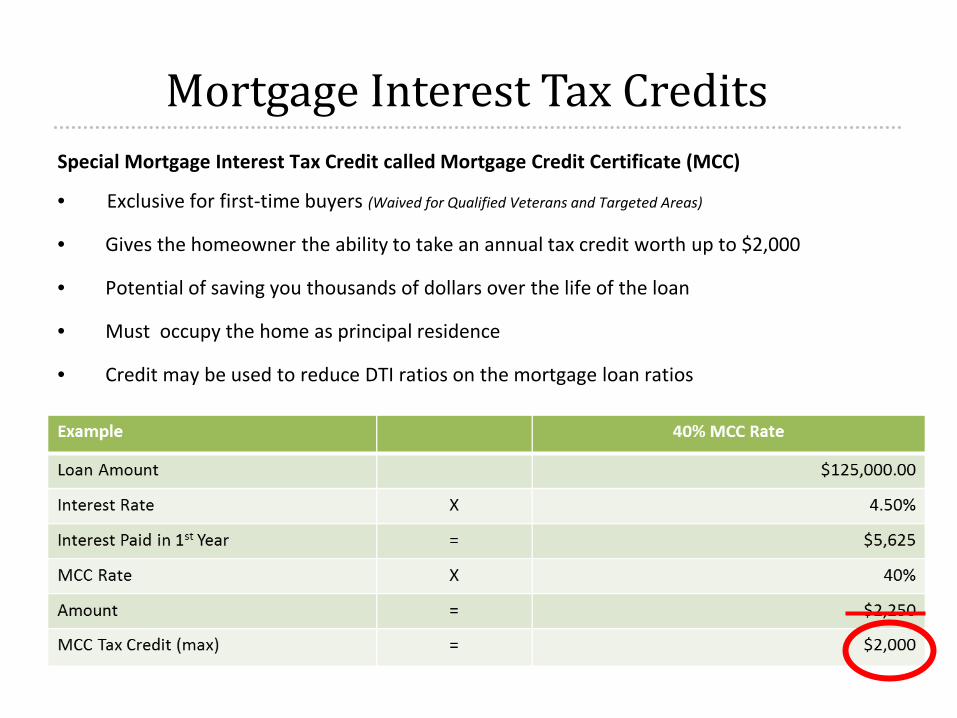

Mortgage Interest Tax Credits Special Mortgage Interest Tax Credit called Mortgage Credit Certificate (MCC)

• Exclusive for first-time buyers (Waived for Qualified Veterans and Targeted Areas)

• Gives the homeowner the ability to take an annual tax credit worth up to $2,000

• Potential of saving you thousands of dollars over the life of the loan

• Must occupy the home as principal residence

• Credit may be used to reduce DTI ratios on the mortgage loan ratios

Mortgage Interest Tax Credits

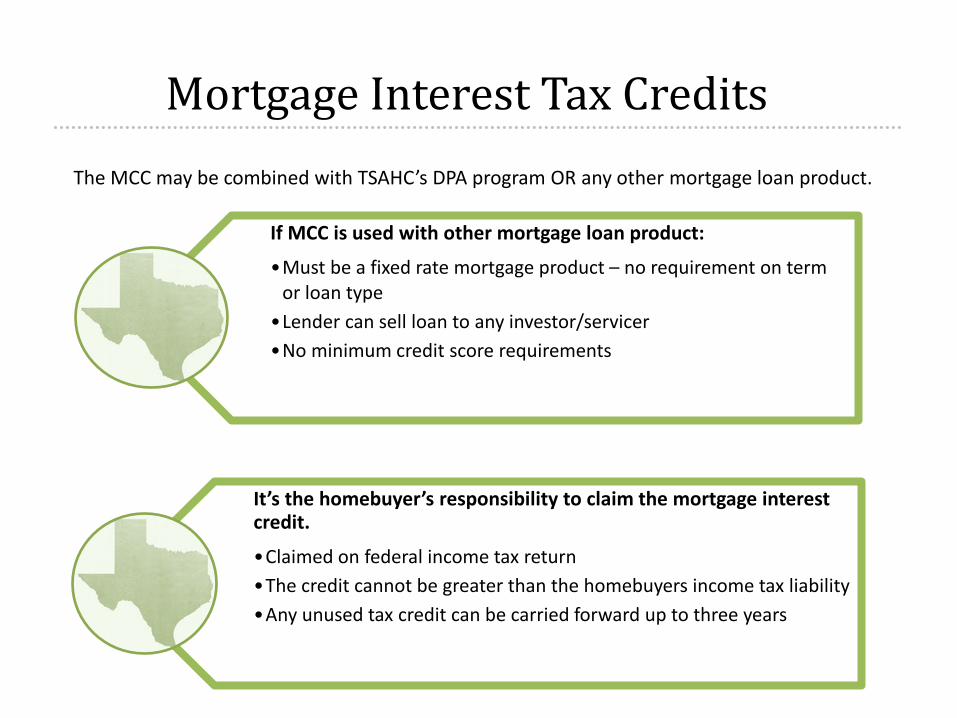

If MCC is used with other mortgage loan product:

•Must be a fixed rate mortgage product – no requirement on term or loan type

•Lender can sell loan to any investor/servicer •No minimum credit score requirements

It’s the homebuyer’s responsibility to claim the mortgage interest credit.

•Claimed on federal income tax return •The credit cannot be greater than the homebuyers income tax liability •Any unused tax credit can be carried forward up to three years

The MCC may be combined with TSAHC’s DPA program OR any other mortgage loan product.

Mortgage Interest Tax Credits

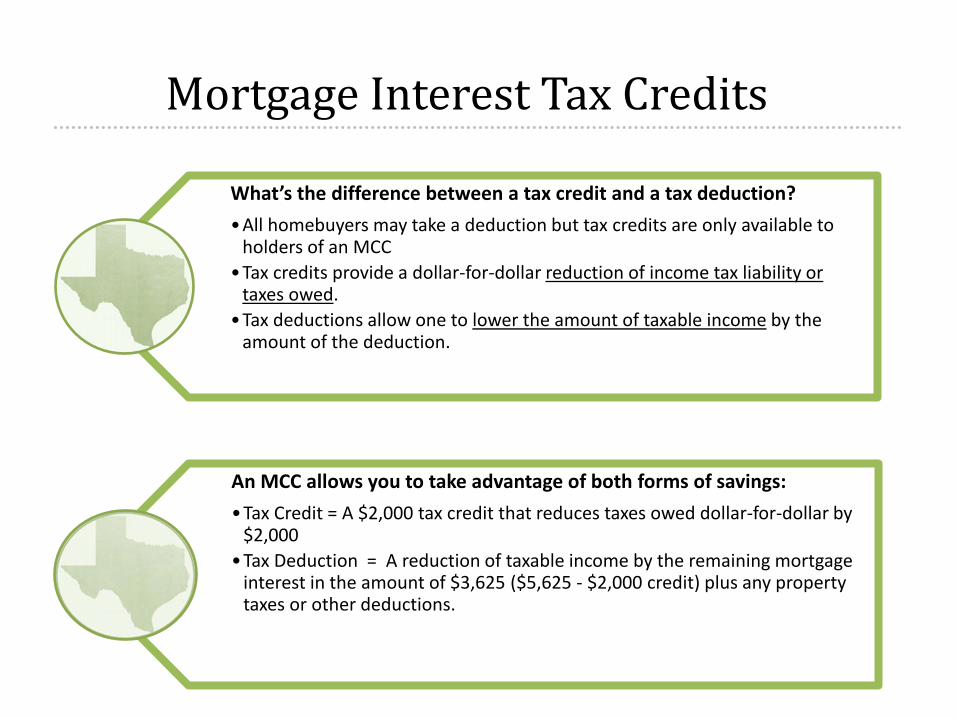

What’s the difference between a tax credit and a tax deduction? •All homebuyers may take a deduction but tax credits are only available to

holders of an MCC •Tax credits provide a dollar-for-dollar reduction of income tax liability or

taxes owed. •Tax deductions allow one to lower the amount of taxable income by the

amount of the deduction.

An MCC allows you to take advantage of both forms of savings: •Tax Credit = A $2,000 tax credit that reduces taxes owed dollar-for-dollar by

$2,000 •Tax Deduction = A reduction of taxable income by the remaining mortgage

interest in the amount of $3,625 ($5,625 - $2,000 credit) plus any property taxes or other deductions.

Mortgage Interest Tax Credits

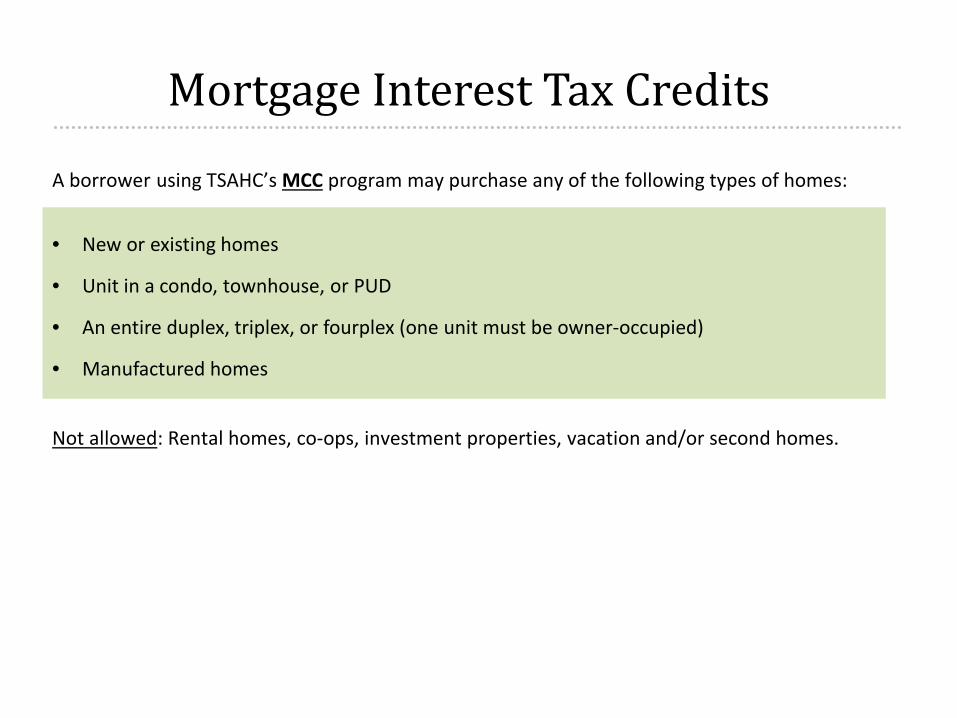

A borrower using TSAHC’s MCC program may purchase any of the following types of homes: • New or existing homes

• Unit in a condo, townhouse, or PUD

• An entire duplex, triplex, or fourplex (one unit must be owner-occupied)

• Manufactured homes

Not allowed: Rental homes, co-ops, investment properties, vacation and/or second homes.

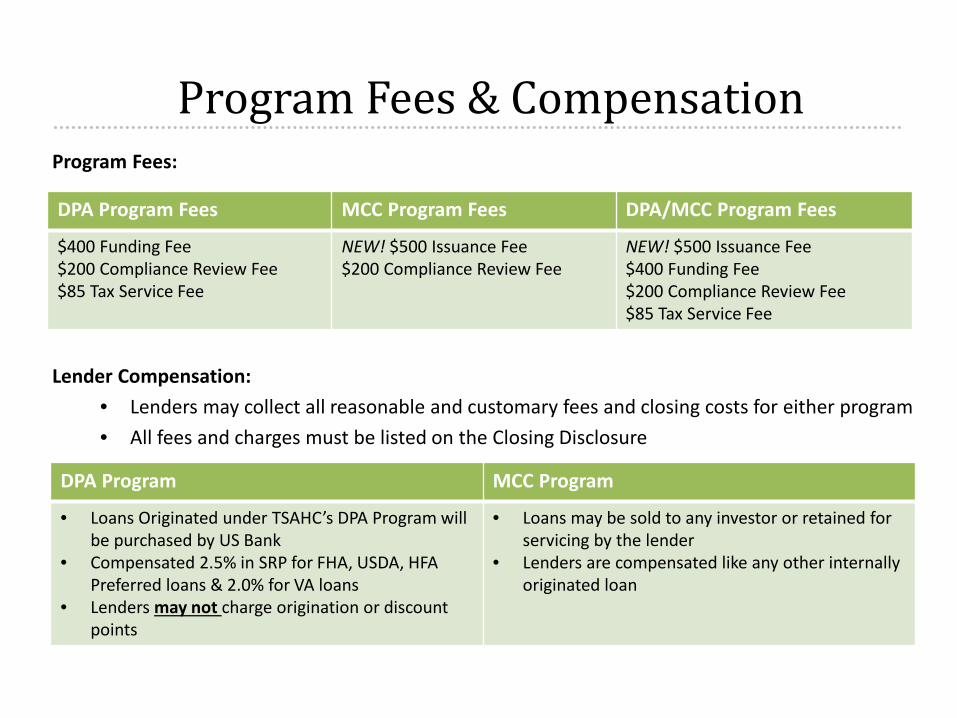

Program Fees & Compensation Program Fees: Lender Compensation:

• Lenders may collect all reasonable and customary fees and closing costs for either program • All fees and charges must be listed on the Closing Disclosure

DPA Program Fees MCC Program Fees DPA/MCC Program Fees

$400 Funding Fee $200 Compliance Review Fee $85 Tax Service Fee

NEW! $500 Issuance Fee $200 Compliance Review Fee

NEW! $500 Issuance Fee $400 Funding Fee $200 Compliance Review Fee $85 Tax Service Fee

DPA Program MCC Program

• Loans Originated under TSAHC’s DPA Program will be purchased by US Bank

• Compensated 2.5% in SRP for FHA, USDA, HFA Preferred loans & 2.0% for VA loans

• Lenders may not charge origination or discount points

• Loans may be sold to any investor or retained for servicing by the lender

• Lenders are compensated like any other internally originated loan

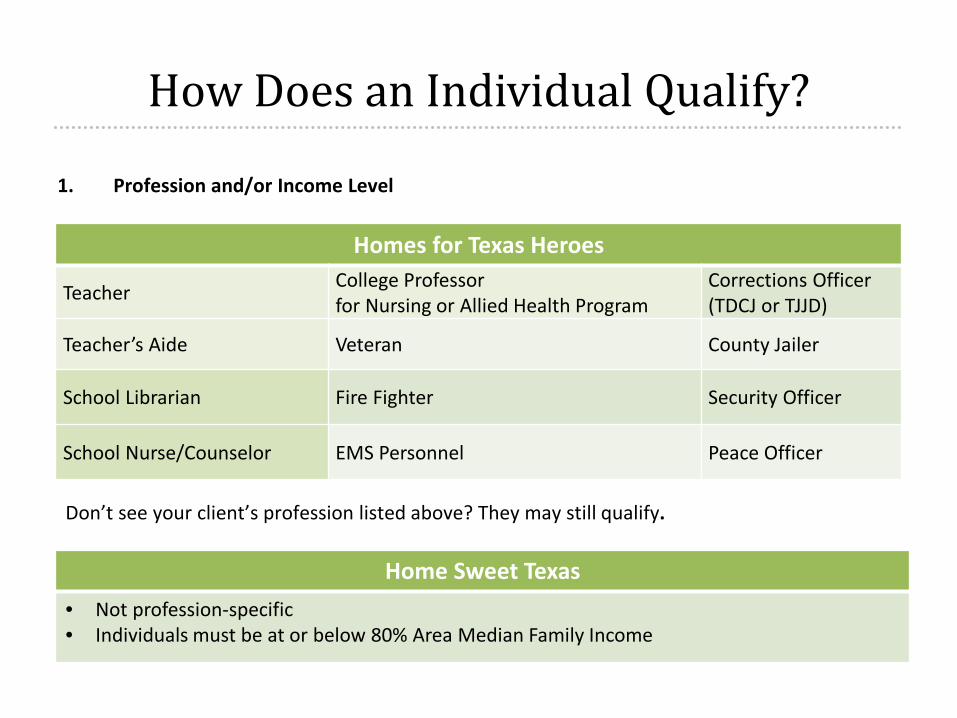

How Does an Individual Qualify?

1. Profession and/or Income Level

Don’t see your client’s profession listed above? They may still qualify.

Home Sweet Texas • Not profession-specific • Individuals must be at or below 80% Area Median Family Income

Homes for Texas Heroes

Teacher College Professor for Nursing or Allied Health Program

Corrections Officer (TDCJ or TJJD)

Teacher’s Aide Veteran County Jailer

School Librarian Fire Fighter Security Officer

School Nurse/Counselor EMS Personnel Peace Officer

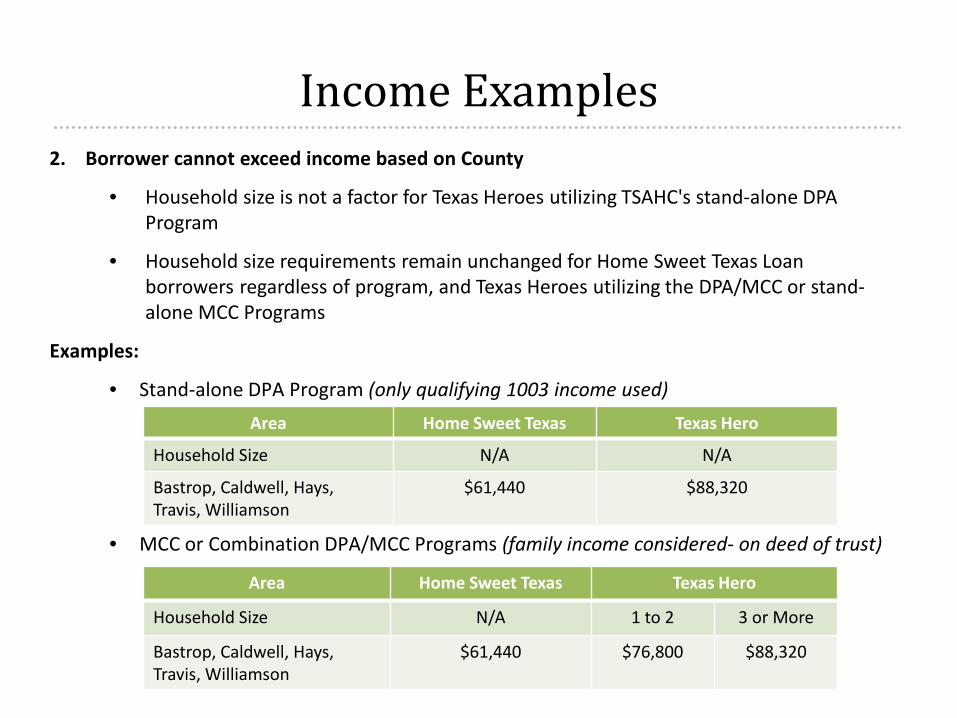

Income Examples

Area Home Sweet Texas Texas Hero

Household Size N/A 1 to 2 3 or More

Bastrop, Caldwell, Hays, Travis, Williamson

$61,440 $76,800 $88,320

2. Borrower cannot exceed income based on County

• Household size is not a factor for Texas Heroes utilizing TSAHC's stand-alone DPA Program

• Household size requirements remain unchanged for Home Sweet Texas Loan borrowers regardless of program, and Texas Heroes utilizing the DPA/MCC or stand-alone MCC Programs

Examples:

• Stand-alone DPA Program (only qualifying 1003 income used)

• MCC or Combination DPA/MCC Programs (family income considered- on deed of trust)

Area Home Sweet Texas Texas Hero

Household Size N/A N/A

Bastrop, Caldwell, Hays, Travis, Williamson

$61,440 $88,320

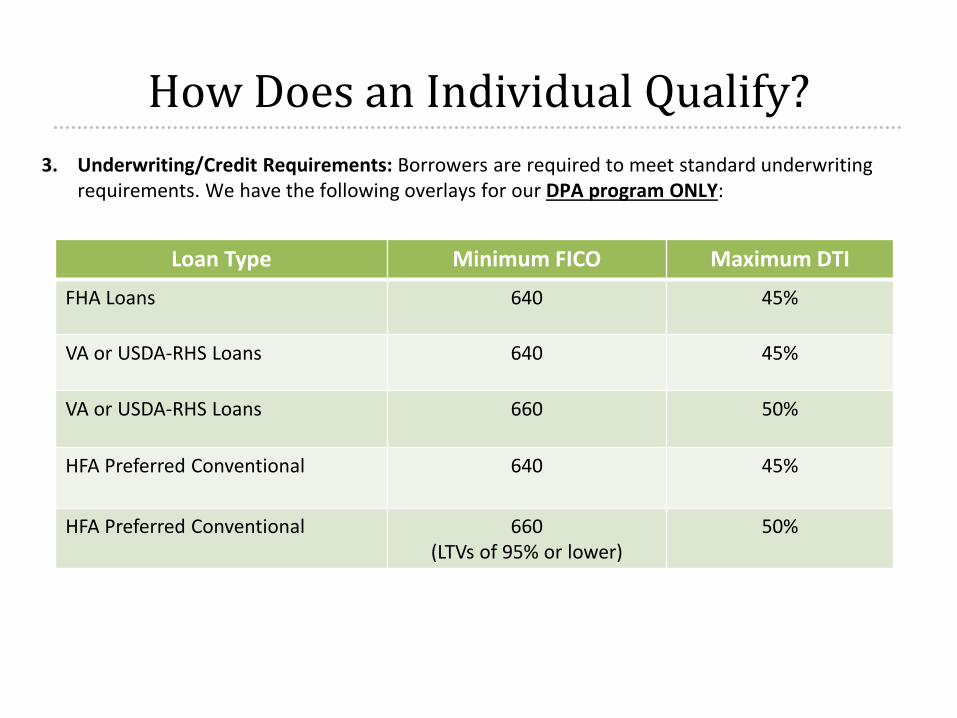

3. Underwriting/Credit Requirements: Borrowers are required to meet standard underwriting requirements. We have the following overlays for our DPA program ONLY:

How Does an Individual Qualify?

Loan Type Minimum FICO Maximum DTI

FHA Loans 640 45%

VA or USDA-RHS Loans 640 45%

VA or USDA-RHS Loans 660 50%

HFA Preferred Conventional 640 45%

HFA Preferred Conventional 660 (LTVs of 95% or lower)

50%

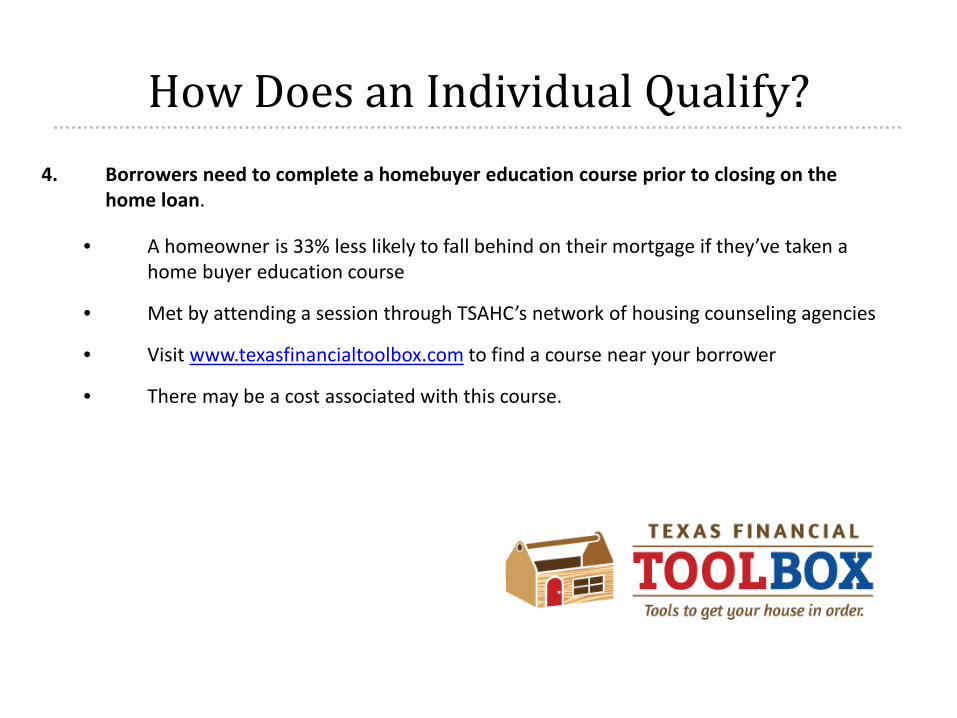

How Does an Individual Qualify? 4. Borrowers need to complete a homebuyer education course prior to closing on the

home loan.

• A homeowner is 33% less likely to fall behind on their mortgage if they’ve taken a home buyer education course

• Met by attending a session through TSAHC’s network of housing counseling agencies

• Visit www.texasfinancialtoolbox.com to find a course near your borrower

• There may be a cost associated with this course.

Type in City

How Does an Individual Qualify?

5. Work with an approved participating lender

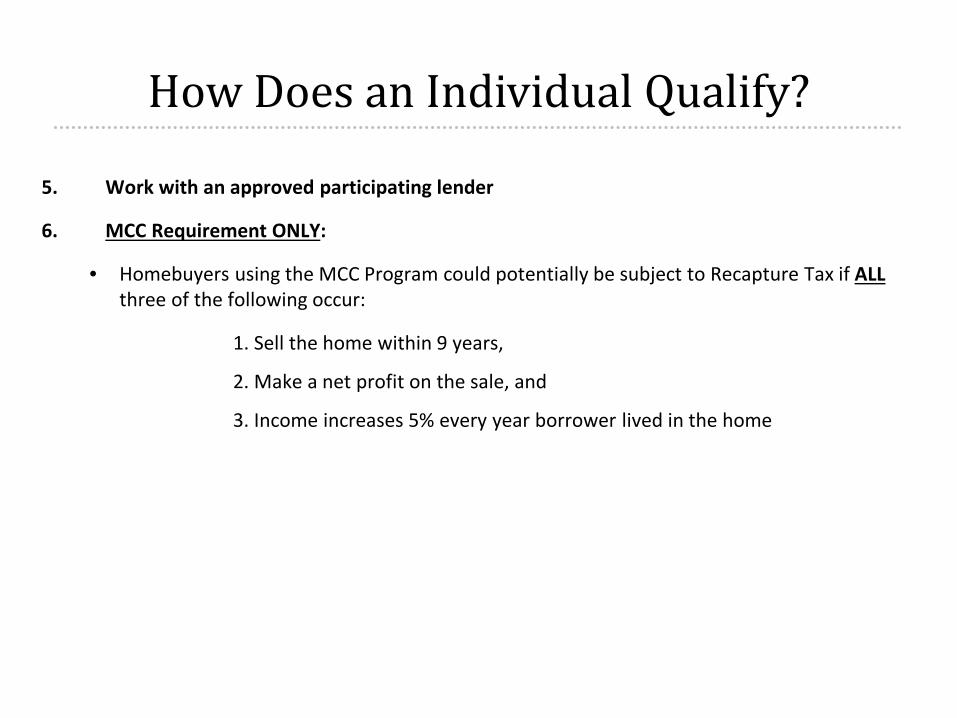

6. MCC Requirement ONLY:

• Homebuyers using the MCC Program could potentially be subject to Recapture Tax if ALL three of the following occur:

1. Sell the home within 9 years,

2. Make a net profit on the sale, and

3. Income increases 5% every year borrower lived in the home

How Does an Individual Qualify?

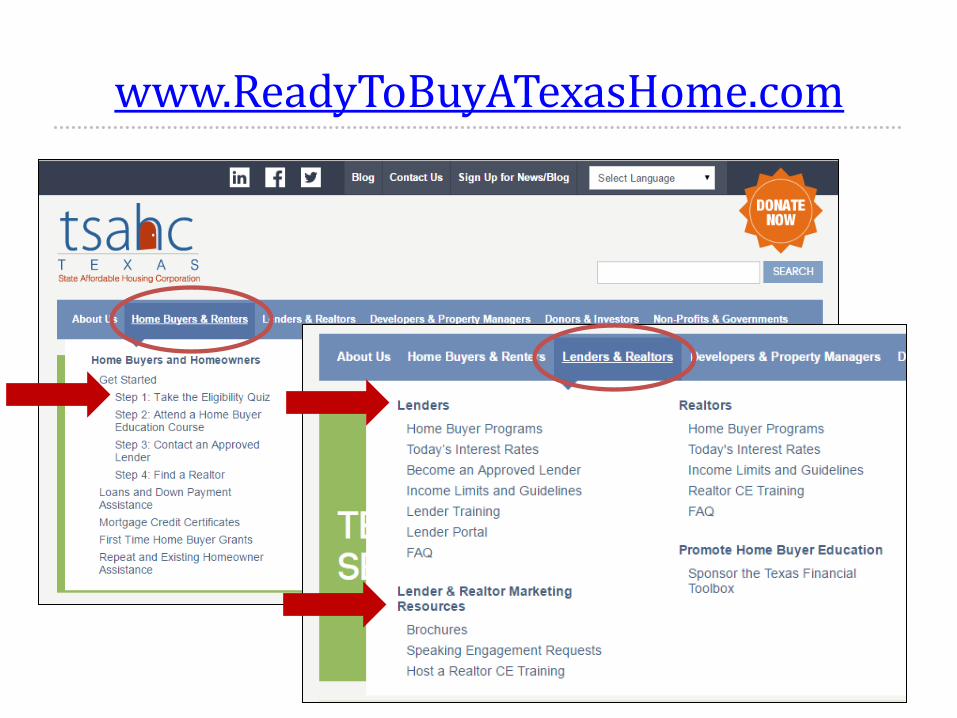

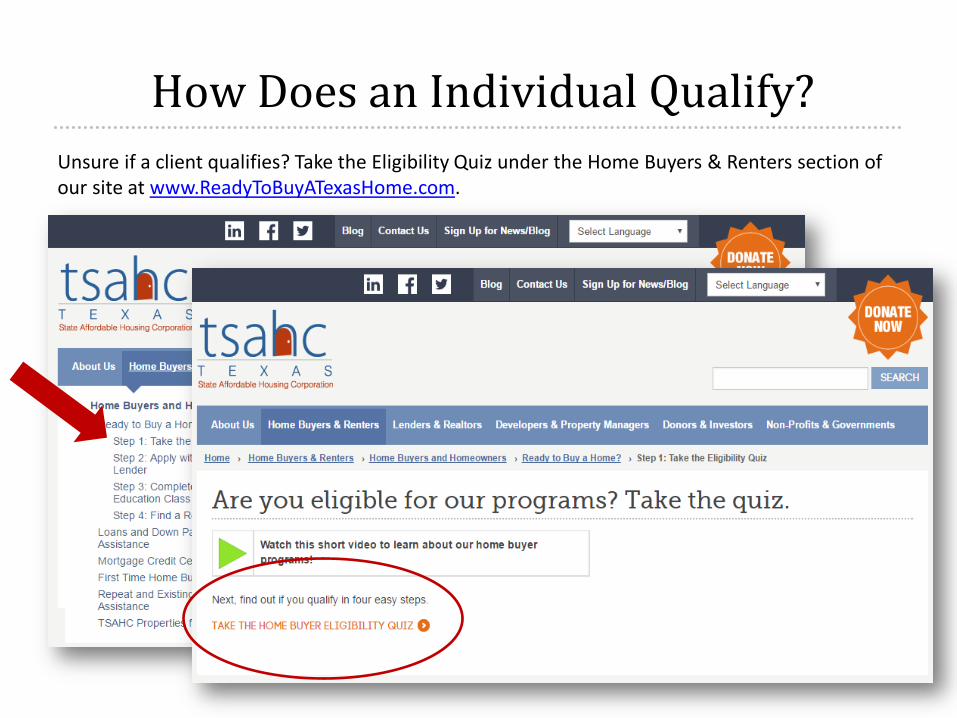

Unsure if a client qualifies? Take the Eligibility Quiz under the Home Buyers & Renters section of our site at www.ReadyToBuyATexasHome.com.

Important Takeaways!

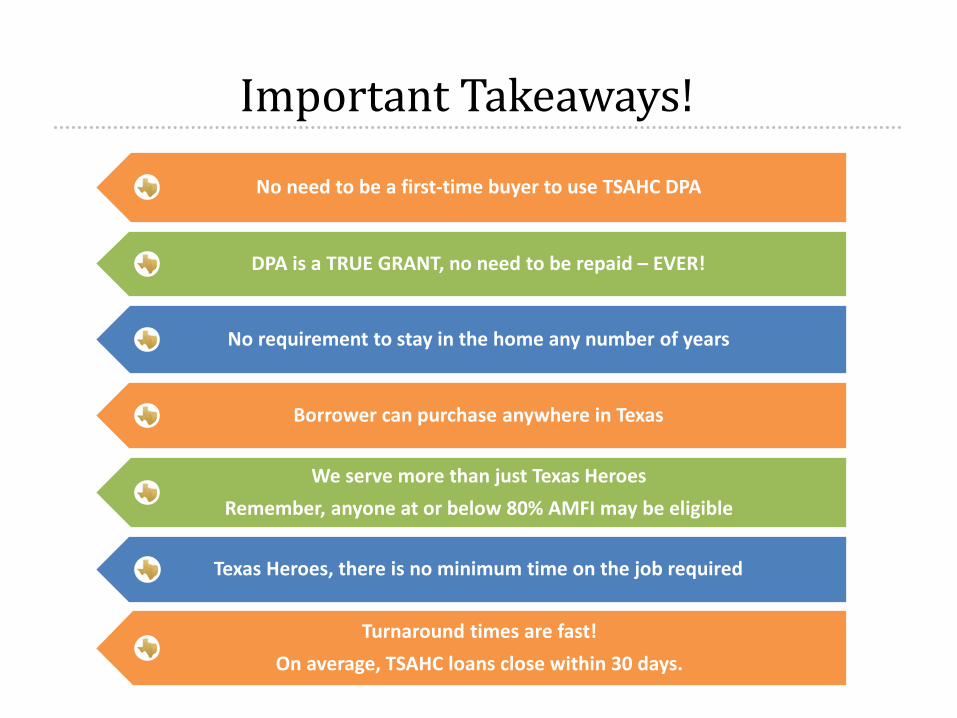

No need to be a first-time buyer to use TSAHC DPA

DPA is a TRUE GRANT, no need to be repaid – EVER!

No requirement to stay in the home any number of years

Borrower can purchase anywhere in Texas

We serve more than just Texas Heroes Remember, anyone at or below 80% AMFI may be eligible

Texas Heroes, there is no minimum time on the job required

Turnaround times are fast! On average, TSAHC loans close within 30 days.

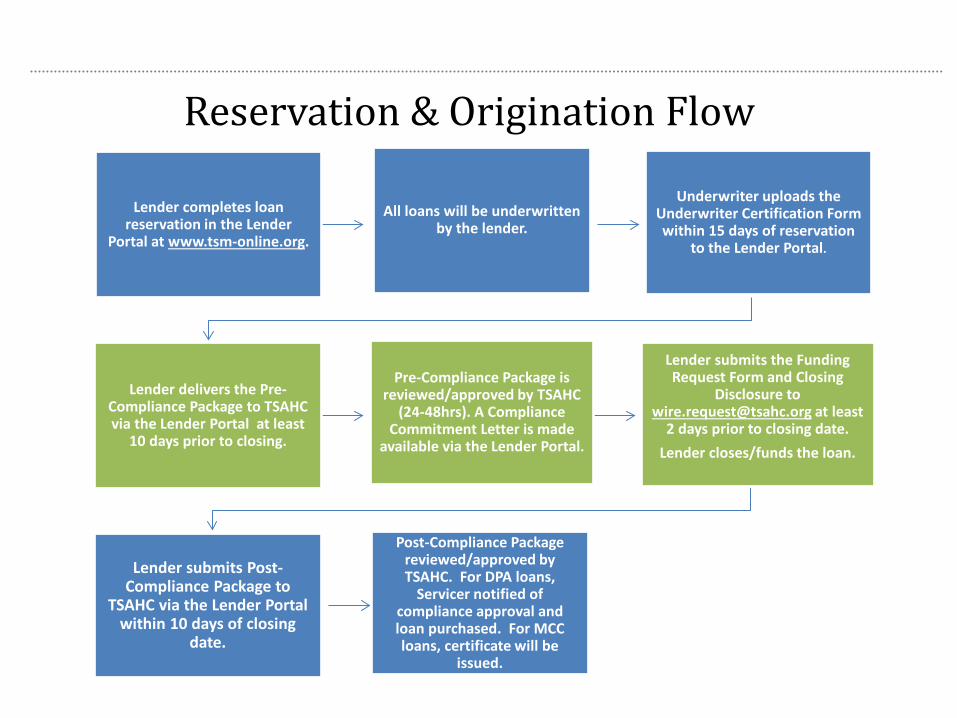

Reservation & Origination Flow

Lender completes loan reservation in the Lender

Portal at www.tsm-online.org.

All loans will be underwritten by the lender.

Underwriter uploads the Underwriter Certification Form within 15 days of reservation

to the Lender Portal.

Lender delivers the Pre-Compliance Package to TSAHC via the Lender Portal at least

10 days prior to closing.

Pre-Compliance Package is reviewed/approved by TSAHC

(24-48hrs). A Compliance Commitment Letter is made

available via the Lender Portal.

Lender submits the Funding Request Form and Closing

Disclosure to [email protected] at least

2 days prior to closing date. Lender closes/funds the loan.

Lender submits Post-Compliance Package to

TSAHC via the Lender Portal within 10 days of closing

date.

Post-Compliance Package reviewed/approved by TSAHC. For DPA loans,

Servicer notified of compliance approval and loan purchased. For MCC loans, certificate will be

issued.

Accessing the Lender Portal Participating lenders will reserve loans and submit compliance packages through TSAHC’s Lender Portal at www.tsm-online.org.

• One person from each Lender’s organization will be designated the “TSAHC Administrator” of the Lender Portal for purposes of granting access to company personnel.

• The administrator is responsible for determining who within their company will have access and as well as the level of access each employee will have.

• TSAHC does NOT create login credentials.

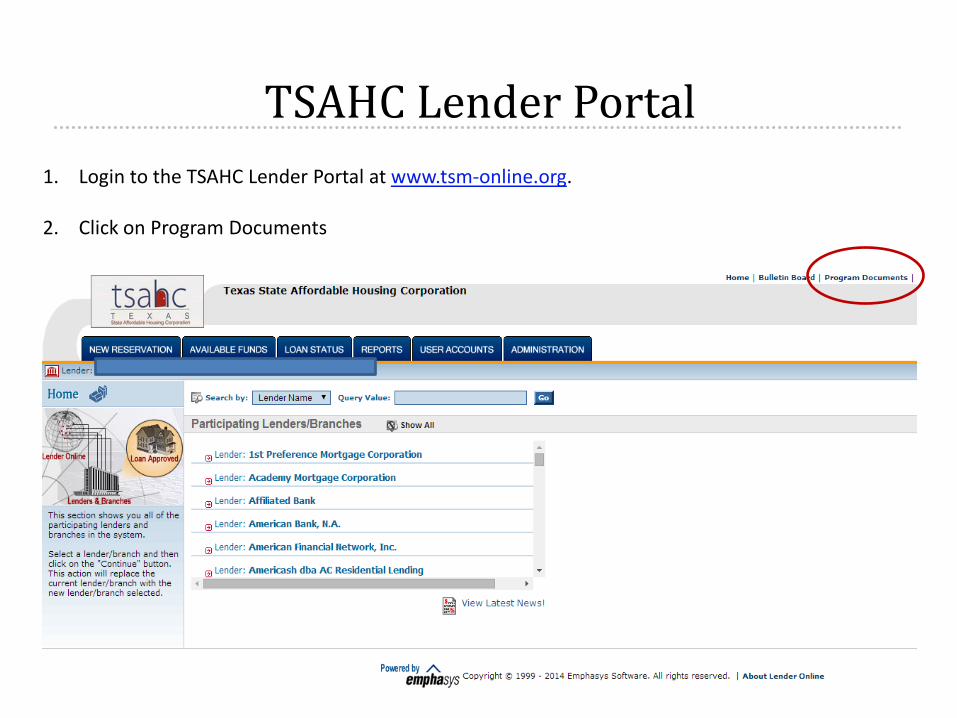

TSAHC Lender Portal 1. Login to the TSAHC Lender Portal at www.tsm-online.org.

2. Click on Program Documents

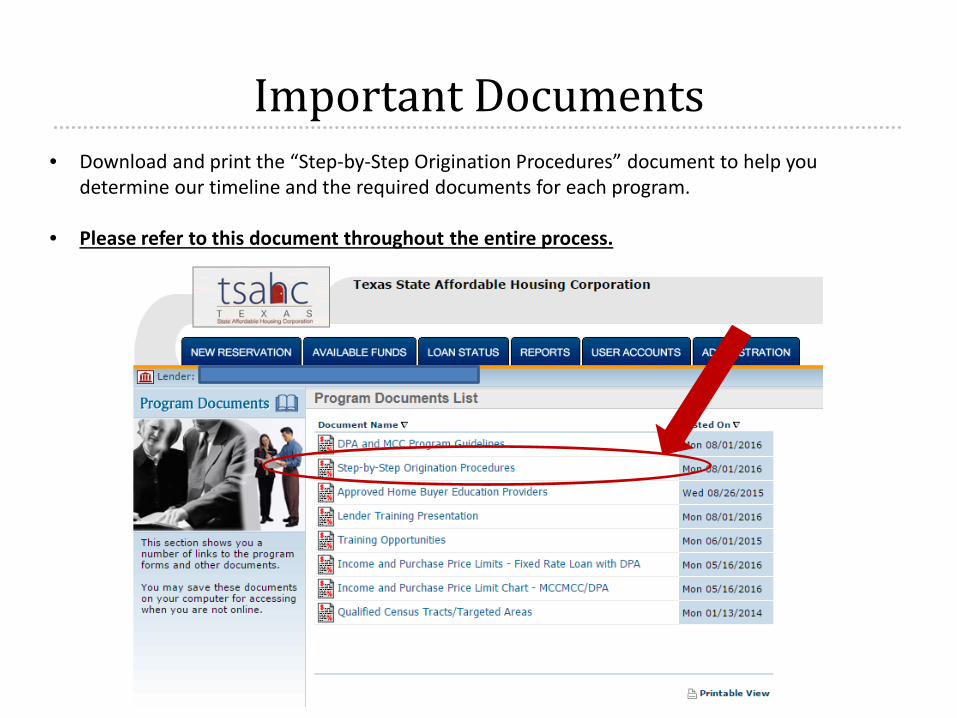

Important Documents • Download and print the “Step-by-Step Origination Procedures” document to help you

determine our timeline and the required documents for each program.

• Please refer to this document throughout the entire process.

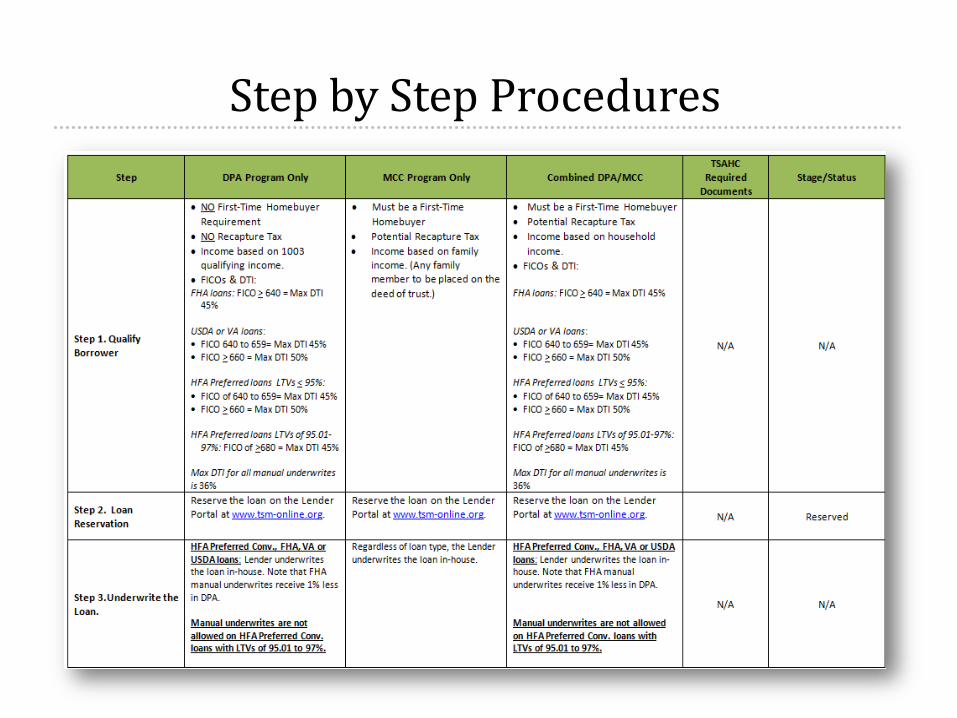

Step by Step Procedures

Loan Officer Responsibilities

1. Pre-qualify borrower per Program Guidelines

• Must have an execute sales contract

• Ensure they met requirements and do not exceed Income Limits or DTI Maximums

2. Complete the Loan Reservation

• Reserve the loan on the Lender Portal at http://www.tsm-online.org

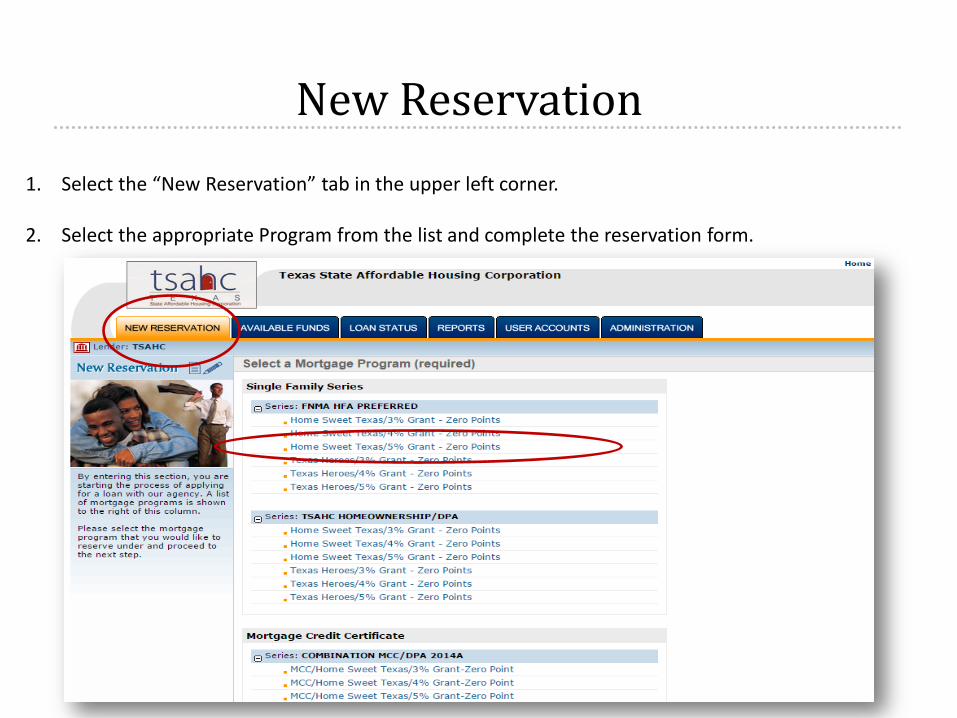

New Reservation

1. Select the “New Reservation” tab in the upper left corner.

2. Select the appropriate Program from the list and complete the reservation form.

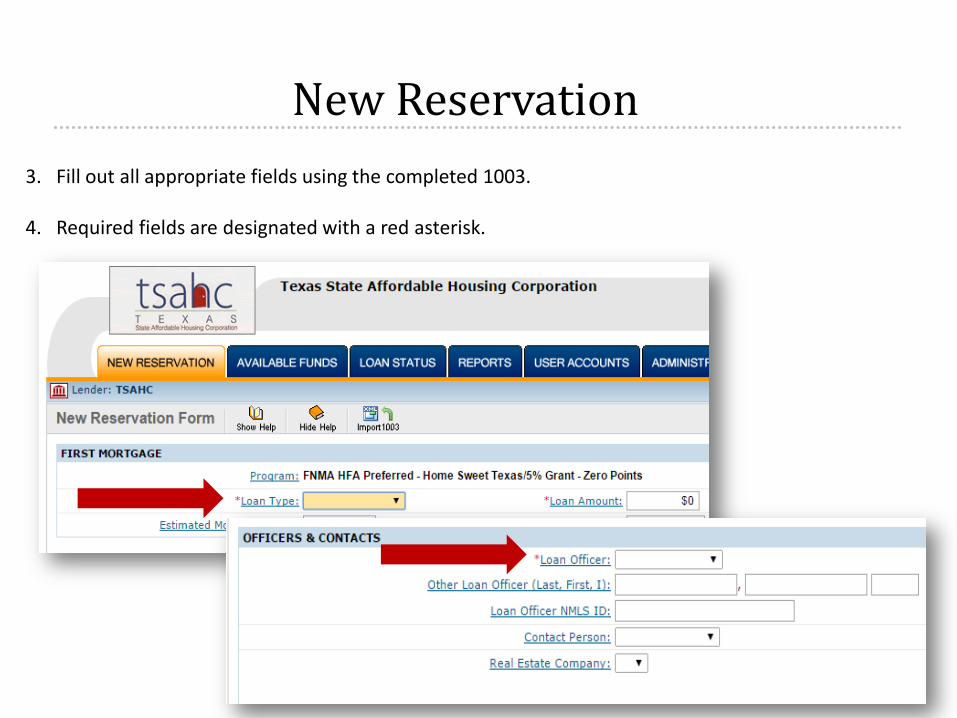

New Reservation

3. Fill out all appropriate fields using the completed 1003.

4. Required fields are designated with a red asterisk.

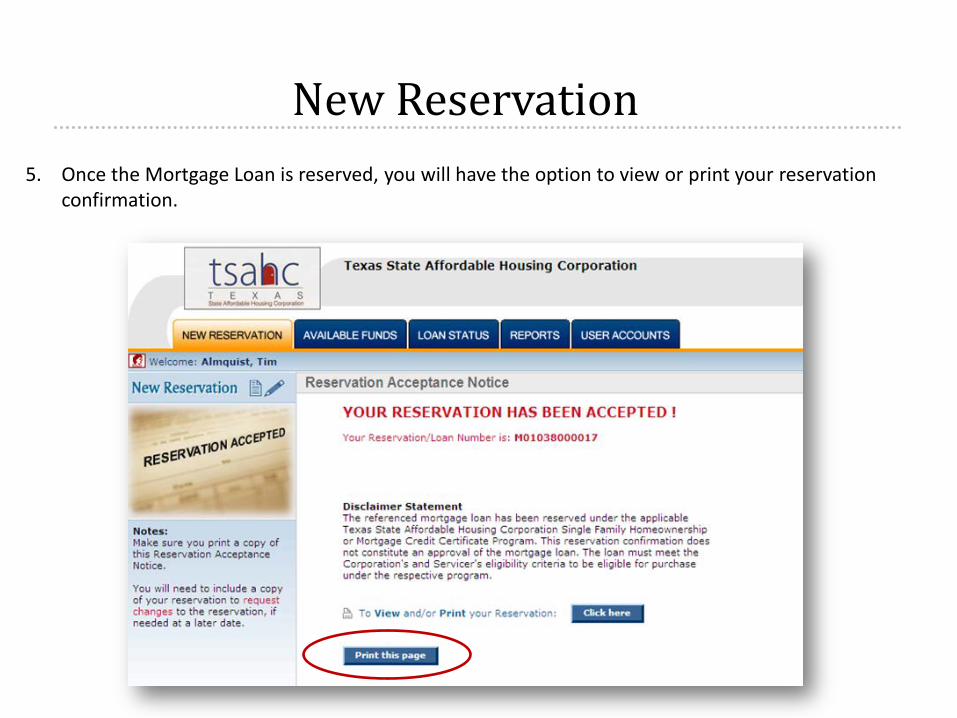

New Reservation 5. Once the Mortgage Loan is reserved, you will have the option to view or print your reservation

confirmation.

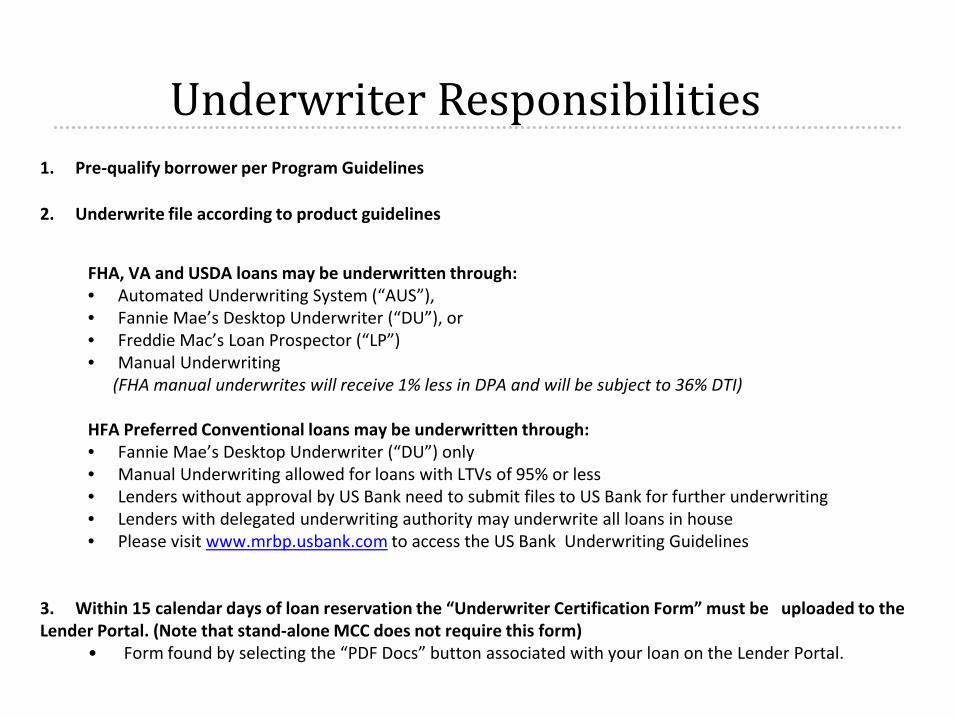

Underwriter Responsibilities 1. Pre-qualify borrower per Program Guidelines

2. Underwrite file according to product guidelines

FHA, VA and USDA loans may be underwritten through: • Automated Underwriting System (“AUS”), • Fannie Mae’s Desktop Underwriter (“DU”), or • Freddie Mac’s Loan Prospector (“LP”) • Manual Underwriting (FHA manual underwrites will receive 1% less in DPA and will be subject to 36% DTI) HFA Preferred Conventional loans may be underwritten through: • Fannie Mae’s Desktop Underwriter (“DU”) only • Manual Underwriting allowed for loans with LTVs of 95% or less • Lenders without approval by US Bank need to submit files to US Bank for further underwriting • Lenders with delegated underwriting authority may underwrite all loans in house • Please visit www.mrbp.usbank.com to access the US Bank Underwriting Guidelines

3. Within 15 calendar days of loan reservation the “Underwriter Certification Form” must be uploaded to the Lender Portal. (Note that stand-alone MCC does not require this form)

• Form found by selecting the “PDF Docs” button associated with your loan on the Lender Portal.

TSAHC Electronic Documents

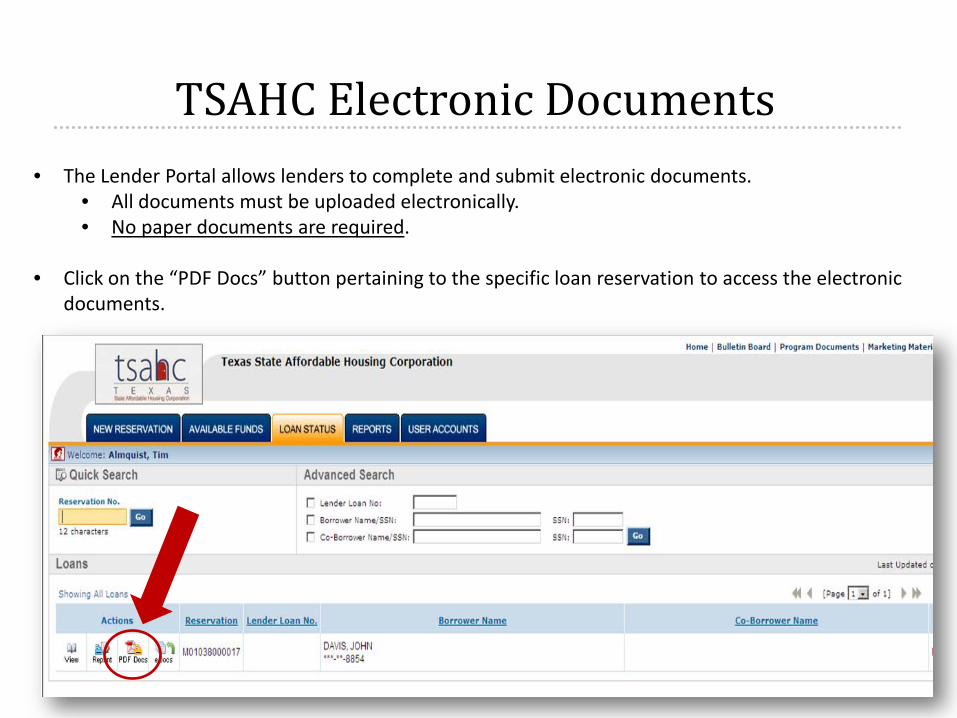

• The Lender Portal allows lenders to complete and submit electronic documents. • All documents must be uploaded electronically. • No paper documents are required.

• Click on the “PDF Docs” button pertaining to the specific loan reservation to access the electronic documents.

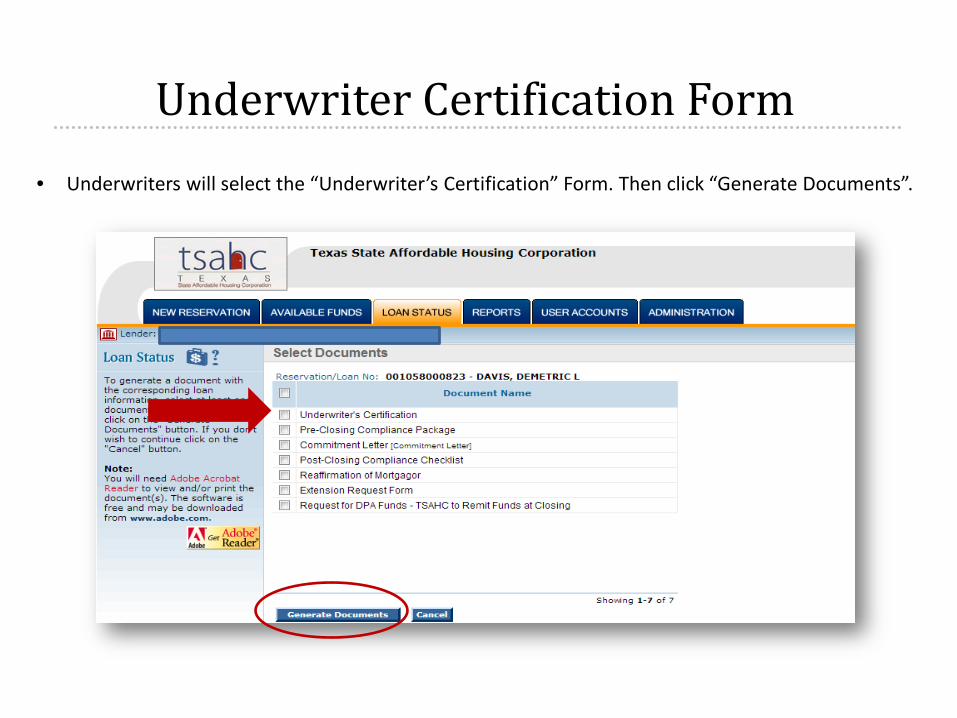

Underwriter Certification Form • Underwriters will select the “Underwriter’s Certification” Form. Then click “Generate Documents”.

Underwriter Certification Form

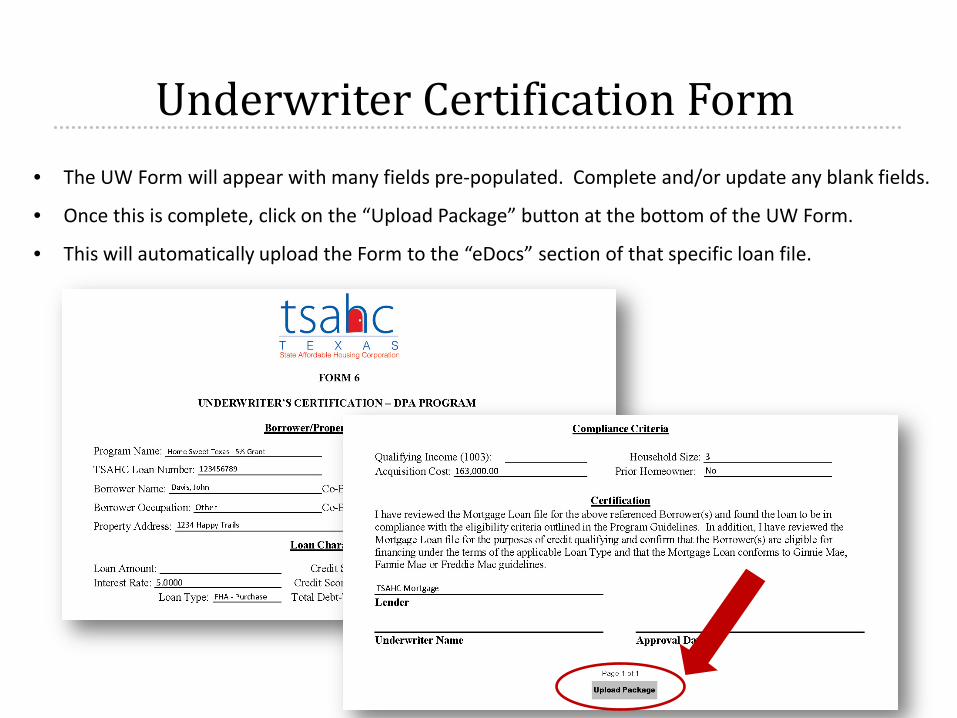

• The UW Form will appear with many fields pre-populated. Complete and/or update any blank fields.

• Once this is complete, click on the “Upload Package” button at the bottom of the UW Form.

• This will automatically upload the Form to the “eDocs” section of that specific loan file.

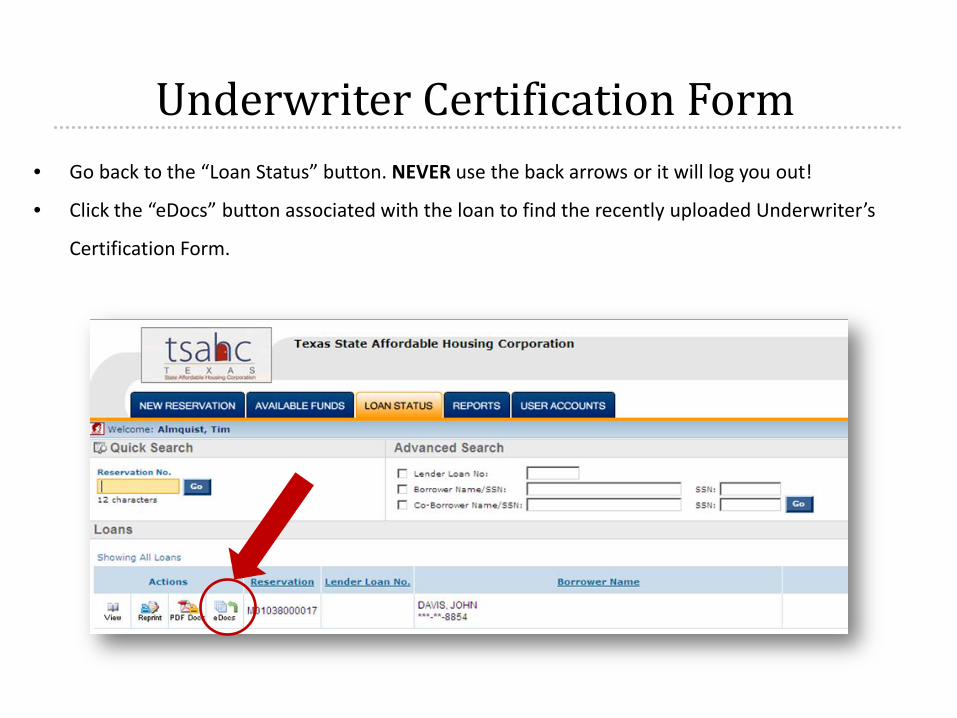

Underwriter Certification Form • Go back to the “Loan Status” button. NEVER use the back arrows or it will log you out!

• Click the “eDocs” button associated with the loan to find the recently uploaded Underwriter’s

Certification Form.

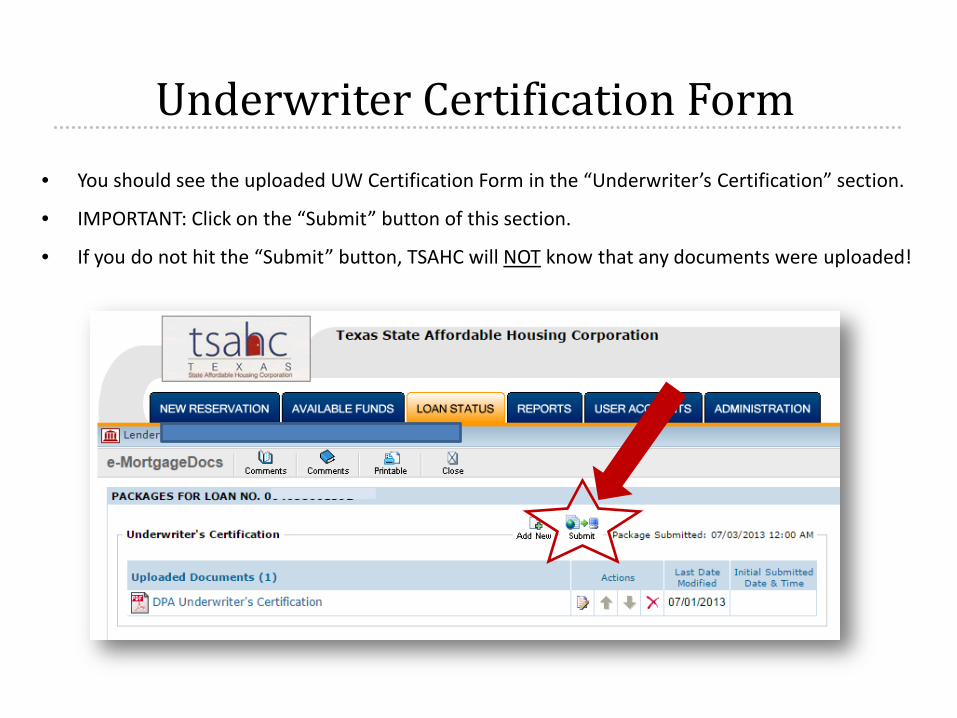

Underwriter Certification Form • You should see the uploaded UW Certification Form in the “Underwriter’s Certification” section.

• IMPORTANT: Click on the “Submit” button of this section.

• If you do not hit the “Submit” button, TSAHC will NOT know that any documents were uploaded!

Other Responsibilities Processor Responsibilities

• Upload Pre-Closing Compliance Package within 10 calendar days prior to closing.

• Commitment Letter Issued by TSAHC

Closer Responsibilities

• DPA or DPA/MCC Loans: Complete and submit the “Funding Request Form” and the final Closing Disclosure to [email protected] at least 2 business days prior to closing.

• Close and fund the loan according to Agency and Program Guidelines

• Upload Post-Closing Compliance Package within 10 calendar days following loan closing.

Shipper Responsibilities

• DPA or DPA/MCC Loans must be approved by TSAHC, delivered and purchased by U.S. Bank within 70 calendar days of loan reservation

• Once the Post- Closing Compliance Package has been approved by TSAHC, U.S. Bank will be authorized to purchase the loan (subject to U.S. Bank requirements) and/or the MCC will be issued to the borrower.

Brochures

Fillable Flyers

10 Step Checklists

Homeownership Hotline: (877) 508-4611

Training/Marketing Questions:

Joniel Crim (512) 477-3561

Sarah Ellinor (512) 220-1171

Compliance Questions:

Tim Almquist (512) 334-2156

Delia Davila (512) 334-2158