Vox eu schoenmaker_(21-12)

15

Macroprudentialism A new Vox eBook Dirk Schoenmaker Duisenberg school of finance 15 December 2014

-

Upload

duisenberg-school-of-finance -

Category

Economy & Finance

-

view

50 -

download

0

Transcript of Vox eu schoenmaker_(21-12)

Macroprudentialism

A new Vox eBook Dirk Schoenmaker Duisenberg school of finance 15 December 2014

2

Overview

1. Why macroprudentialism?

2. Two pillars

3. What objectives?

4. European coordination

5. More of an art than a science!

3

Why?

• Currently: low interest rates, but risk of (housing) bubbles

• Before crisis: Ø Monetary policy: inflation of consumption goods, but

not inflated asset prices Ø Microprudential: individual institutions, with models

assuming exogeneous risk

• Macropru missing link: need to look at financial system as a whole + endogeneous feedback loops

4

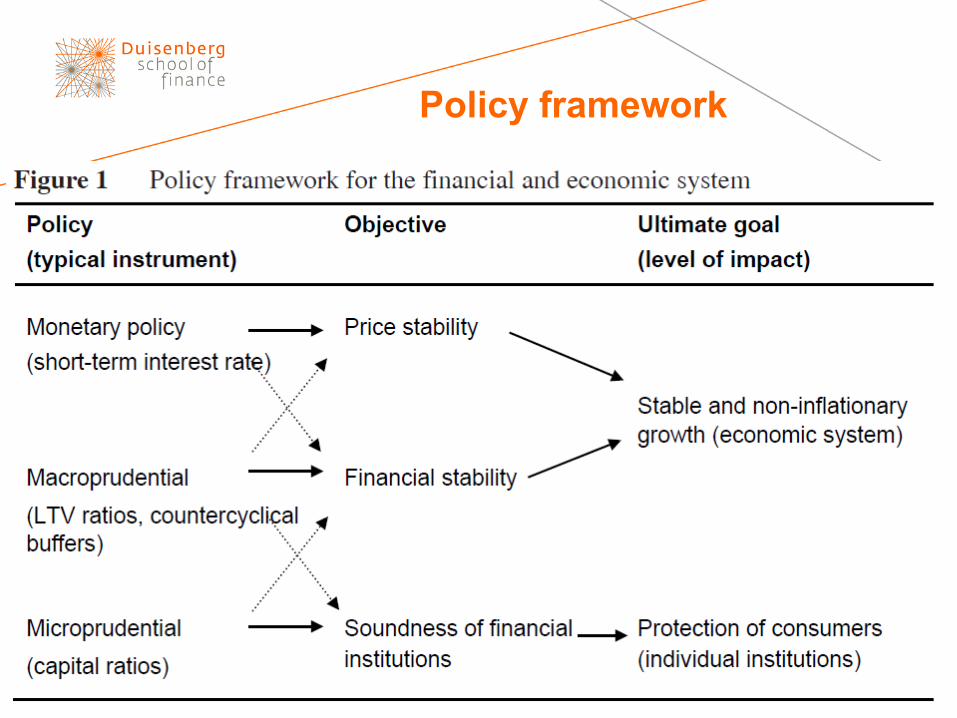

Policy framework

5

Two pillars

6

What objectives?

• On the cyclical (time-series) dimension: Ø Just increasing resilience of financial system against

financial shocks (Borio); or Ø Stabilising credit cycle (Gersbach and Rochet)

• On the structural (cross-sectional) dimension: Ø Capital surcharges for systemic banks to reduce TBTF Ø But how high?

• Scope: banking, or also securities, insurance and pensions?

Financial cycle is strong!

8

Monetary vs Macroprudential

• Tinbergen: two objectives – two instruments:

Ø Yes, Goodhart and Tucker: macropru more targeted at particular risks (e.g. housing/property); or

Ø No, Borio: interest rates also needed for risk-taking channel

Ø Middleground, Portes: sometimes need to struck compromise

9

Macro vs micro prudential

• Different perspective / orientation: Ø Borio: Macro lens towards prudential rules Ø Operational: when designing prudential rules, choose the

macro least damaging

• Hierarchy of objectives: Ø Tucker and Dirks et al: macro should come first Ø But be careful for forbearance (delaying necessary action)

10

Hierarchy of objectives

7

Figure 2. Hierarchy of objectives

Source: Kremers and Schoenmaker (2014) 4. Emerging arrangements in the European Union As mentioned in the introduction, both a 2012 ESRB recommendation (ref. ESRB/2011/3) and the EU Capital Requirements Regulation (CRR, Regulation No 575/2013) required EU Member States to set up a ‘designated authority’ for macro-prudential supervision. The ESRB has completed a review of the (likely) designated authorities (IWG WP/2013/011). From this review, we distil four main institutional models where the formal powers for macro-prudential supervision are located:

1. the ministry of finance (or economics);

2. the central bank;

3. the financial authority;

4. an “ad-hoc” committee. Table 2 shows that the central bank has most often been designated as the responsible authority (see Table 3 in the annex for a breakdown at country level). While several European central banks combine monetary policy and supervisory tasks, they typically have separate departments for financial stability (macro-prudential) and financial supervision (micro-prudential). In these cases, there is an organisational separation between the macro- and micro-prudential tasks. In some countries, the stand-alone financial authority has been designated for macro-prudential policy.

Monetary stability

Financial stability: macro-prudential

Financial soundness: micro-prudential

Level

Economy

Individual institutions

↔

↔

Objectives

11

Eurozone

• Monetary and Banking Union: Ø Centralised monetary policy Ø Centralised banking supervision (micro prudential) Ø But decentralised macroprudential supervision

• Is that all right? Ø Sapir and Acharya/Calomiris: need for centralised macro

prudential supervision by ECB (together with national) Ø With differentiated implementation as financial cycle differs

across countries

Eurozone

13

Concluding

• Need for analytical framework / model: Ø Difficult because externalities are multifacetted and

endogeneous feedback loops Ø Be aware of unintended consequences

• But we need to get into action: Ø Macroprudentialism is more art than science Ø Democratic accountability important because of impact

on citizens

14

Download

• Download the Vox eBook on macroprudentialism: http://www.voxeu.org/article/macroprudentialism-new-vox-ebook

15