VIETNAM RETAIL MARKET AND COMSUMER

27

VIETNAM RETAIL MARKET AND COMSUMER TRENDS 2020 Consumer and retail trends for FMCG in 2020. Understand and anticipate Vietnam retail and consumer dynamics. Wednesday December 2 nd 2020 Kantar, Worldpanel Division, in partnership with Eurocham

Transcript of VIETNAM RETAIL MARKET AND COMSUMER

VIETNAM RETAIL MARKET AND COMSUMER TRENDS 2020Consumer and retail trends for FMCG

in 2020.

Understand and anticipate Vietnam

retail and consumer dynamics.

Wednesday December 2nd 2020

Kantar, Worldpanel Division, in partnership with

Eurocham

Macro trends

2

There remains an elevated concern towards the current financial situation of

the HH with over 1/3 HH depriving themselves or worse…

How do you evaluate the current financial situation of your Household?

Source: Worldpanel Division | Households Panel | Urban Vietnam 4 key cities | MAT Q2’20

17

2725

29

2 7 4 5

Q4 2019 Q1 2020 Q2 2020 Q3 2020

We are not doing well at all

We need to deprive ourselves sometimes

It comes out correctly

We have enough money to allow us someextras once in a while

No financial worries, we don’t need to pay attention

% HW agree

3

When asked about the family's

financial situation in the future:

10 7 7 7

46

3341 40

41

44

45 43

3

167 9

3 yearaverage

Q1 20 Q2 20 Q3 20

Will get much worse

Will get worse

Will not change

Will improve

Will strongly improve

% Agree

Source: Worldpanel Division | Households Panel | Urban 4 key cities | Lifestyle survey

Urban 4 cities

…while the optimism towards the future financial situation also remains lower.

Consumers are still concerned about income and job security

0

10

20

30

40

50

60

70

80

Food s

afe

ty

Pandem

ic

Incom

e

Incre

asin

g c

osts

Envir

onm

ent

Pollution

Job s

ecurity

Food e

xpense

Natu

ral dis

aste

r

Oil p

rice

Dis

ease in liv

esto

ck

Q4_2019 Q3_2020

Concerns about income and job security are still higher than usual

(% HW Agree)

4

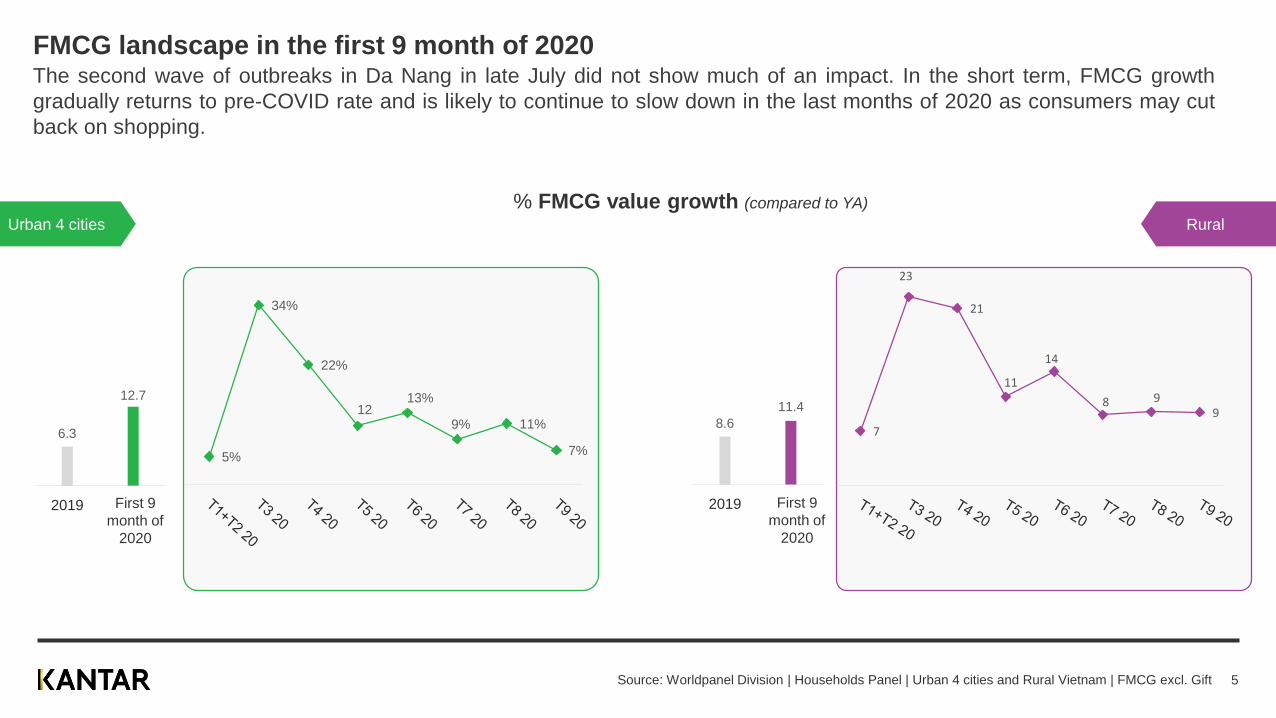

6.3

12.7

2019 YTDP9'20

5%

34%

22%

1213%

9% 11%

7%

8.6

11.4

2019 YTDP9'20

7

23

21

11

14

8 99

The second wave of outbreaks in Da Nang in late July did not show much of an impact. In the short term, FMCG growth

gradually returns to pre-COVID rate and is likely to continue to slow down in the last months of 2020 as consumers may cut

back on shopping.

FMCG landscape in the first 9 month of 2020

Urban 4 cities Rural

% FMCG value growth (compared to YA)

Source: Worldpanel Division | Households Panel | Urban 4 cities and Rural Vietnam | FMCG excl. Gift

First 9

month of

2020

First 9

month of

2020

5

Stocking behavior happens intensively due to the pandemic and slowly returning to normal

During the pandemic months, consumers tended to buy a lot in each shopping occasion to stock. Recently, the shopper's basket

size has gradually returned to normal rate.

6

2

7

5

2

13

1

11

8

3

9

1

9

7

2

FMCG index Occasion Spend/trip Average price pervolume

Volume/trip

9

1

8

4 4

11

2

9

3

6

10

1

9

4

5

FMCG index Occasion Spend/trip Average price pervolume

Volume/trip

FY 2019 YTD P9’20 Q3’20

% change of key indicators (compared to YA)Urban 4 cities Rural

Source: Worldpanel Division | Households Panel | Urban 4 cities and Rural Vietnam | FMCG excl. Gift 6

COVID-19 impact on channel choices

7

Retail environment is changing with the evolution of emerging channels* and big retail formats, which is more apparent during the pandemic

% Value share across channels

Source: Worldpanel Division | Households Panel | Urban 4 Key Cities | Total FMCG excluding Gift | YTD P6 20 vs YA

Emerging channels* including specialty stores, pharmacy, minimarkets, convenience stores, drug stores and online.

Urban 4 cities

56 54 53

9.2 8.9 8.7

8.1 8.86.5

13.8 14.215.0

4.4 5.2 6.2

1.9 2.7 3.4

FY 2018 FY 2019 H1 2020

Street Shops

Wet Market

Specialty Stores

Pharmacy

Hyper & Super

Cash & Carry

Minimarket

Convenience Stores

Drug Stores

Online

Others

8

Source: Worldpanel Division | Households Panel | Urban 4 Key Cities | Total FMCG excluding Gift | H1 2020 vs YA

-10-6

51

25

13

-1

103 3

85

70 67

45

24 2721

159

Drug Stores Pharmacy Online Minimarket CVS Cash & Carry Hyper & Super Wet Market Street Shops

FY 2019 H1 2020

% YoY Change across key channels

Amid C19 situation, emerging channels and big modern formats are riding the growth wave, which might continue post pandemic

Urban 4 cities

Emerging channels Big modern formats Traditional trade

9

2 Key Retail trends in the new normal

10

Digital Acceleration

11

56%Online

shoppers

44%Non-online shoppers

Source: Worldpanel Division | Vietnam Urban 4 cities | Smart shopper | June 2020

Online channel today has reached over half of population, yet having many things to do in order to tap into the other half, mostly in +50yo

% Online penetration – MAT P6’20(FMCG + non-FMCG)

(2/3 of non-online shoppers are > 50YO)

12

For FMCG purchases, more and more consumers move to online

Source: Worldpanel Division | Households Panel | Urban 4 key cities Vietnam | Total FMCG excluding Gift

There is still headroom to further grow in both shopper base and shopping traffic, which is expected to bring more incrementality to FMCG market.

• More than 1/3 of urban households (35%) now

shop FMCG online, adding +500,000 new households in 2 years.

• Shoppers buy FMCG online every 2 months and a half…

• …and spend more than 300k each trip on average.

13

Online shopping for FMCG products sees a step change in monthly shopper traffic under C19, which will likely accelerate post pandemic

Source: Worldpanel Division | Households Panel | Urban 4 key cities Vietnam | Total FMCG excluding Gift

FMCG Online - % Monthly Penetration (shoppers)

16.8

10.9

24.5

0

5

10

15

20

25

30

P13'16 P6'17 P13'17 P6'18 P13'18 P6'19 P13'19 P6'20 P13'20 P6'21

Online Forecast (Online) Upper Confidence Bound (Online)

Urban 4 cities

With current trends we could expect monthly penetration to be between

17% - 25% in one year

14

E-commerce grows in all demographics, even in 50+yo and in rural and it is mostlyincremental for FMCG

Source: Worldpanel Division | Households Panel | Urban 4 key cities & Rural Vietnam | Total FMCG excluding Gift | H1 2020 vs YA

% Online shoppers by demographic

0

5

10

15

20

25

30

35

40

45

50

Main ShopperAge <30

Main ShopperAge 30-39

Main ShopperAge 40-49

Main ShopperAge 50+

H1 2020H1 2019

0

5

10

15

20

25

30

Urban 4 key cities Rural

Among Urban 4 key cities

15

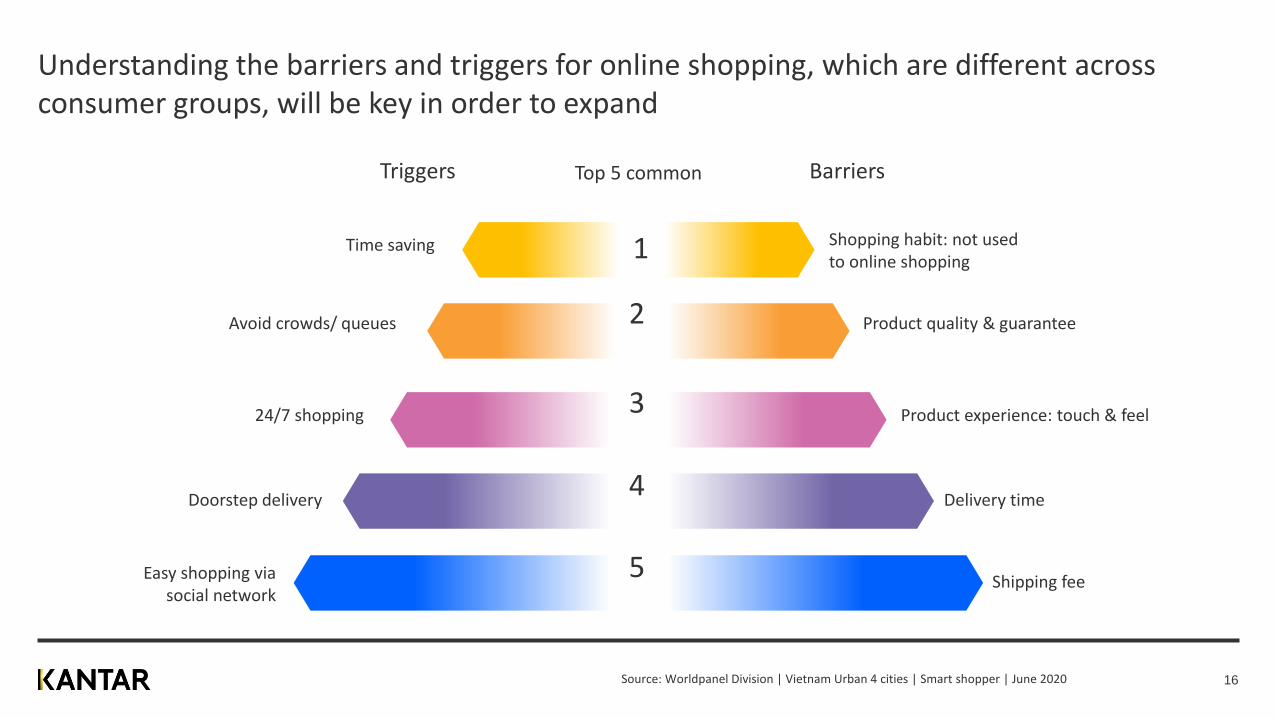

Understanding the barriers and triggers for online shopping, which are different across consumer groups, will be key in order to expand

1

2

3

4

5

Top 5 commonTriggers Barriers

Shopping habit: not used to online shopping

Product quality & guarantee

Product experience: touch & feel

Delivery time

Shipping fee

Time saving

Avoid crowds/ queues

24/7 shopping

Doorstep delivery

Easy shopping via social network

Source: Worldpanel Division | Vietnam Urban 4 cities | Smart shopper | June 2020 16

Source: Worldpanel Division | Vietnam Urban 4 cities | Smart shopper | June 2020

100

21

95

28

Cash Digital payment*

Total Online & Offline Online

% Shoppers - Payment method when shopping Online or Offline

Most consumers prefer cash on delivery (COD) method when making online purchases, yet great promising for digital payment to take off

*Digital payment: Bank transfer, e-wallet, credit card.

The younger, the more exposure to digital payment

Half of shoppers <30yo today use digital payment

17

What’s next: Direct to consumer (D2C), subscription model!?

Unilever solutions: D2C platform

18

Convenience, Greater Convenience!

19

Consumers now seek for a greater convenience, which means not only proximity but also ease and speed

Urban 4 citiesTop 7 reasons to choose a shopping place (% agree vs YA)

1 The store is clean

2 It has good quality products

3 You can easily find what you want

4 It's near my home or on my way back to home

5 The staff are friendly/ responsive to my request

6 I save a lot of time shopping there

7 It's convenient to get there

Source: Worldpanel Division | Households Panel | Urban 4 Key Cities | Lifestyle survey 2019 20

As such, street shops – a traditional channel remain dominant and manage to grow healthily even in challenging time amid the fiercer competition coming from modern & emerging channels

5 pts vs 2 YA

Street shop during C19 time…(H1 2020)

+9%Value growth

% Contribution to FMCG growth

More than

1/3

More than half (54%) of

consumer spend on FMCG happened in street shops in 2019.

Source: Worldpanel Division | Households Panel | Urban 4 Key Cities | Total FMCG excluding Gift 21

In the context of C19, they quickly adapt and respond to consumer changing needs in order to survive

#1. Safety first

In support of national social distancing campaign, they applied many measures to control the spread of COVID-19.

• Wearing mask

• Limiting physical contact

• Washing hands

#2. Product availability

Prioritize “pandemic” categories which are in high demand during quarantine time.

Work with more than one supplier/distributor both online and offline to make sure products available to capture consumer needs.

#3. Improvisation

Provide safe, speedy and convenient solutions to their consumers: “Less physical contact” shopping via phone/online & doorstep delivery.

22

24

29

0

5

10

15

20

25

30

35

Minimarkets continue growing its shopper base, which even shows a significant uplift under pandemic, promising to keep momentum post C19

Source: Worldpanel Division | Households Panel | Vietnam Urban 4 Key Cities | Total FMCG excluding Gift

Transactions (100,000 times) Penetration (%)

Under COVID19

MCO

FMCG purchases in Minimarket – 4 week rolling

On average, shoppers make 4trips every quarter, spend about

100k each trip in

minimarkets.

Minimarkets now have reached nearly 2/3of urban households, adding 240,000 new

households into its shopper base over 12 months to June 2020.

23

This smaller modern format is also an organic source of FMCG growth with the majority of its FMCG sales increase not being shifted from other channels

Source of value changeUrban 4 cities

Source: Worldpanel Division | Households panel | Urban 4 Key Cities Vietnam | FMCG excluding Gift

Of FMCG sales gained in Minimarkets are incrementality, by adding or increasing incremental spend to total market, not from switching among channels.

80%

24

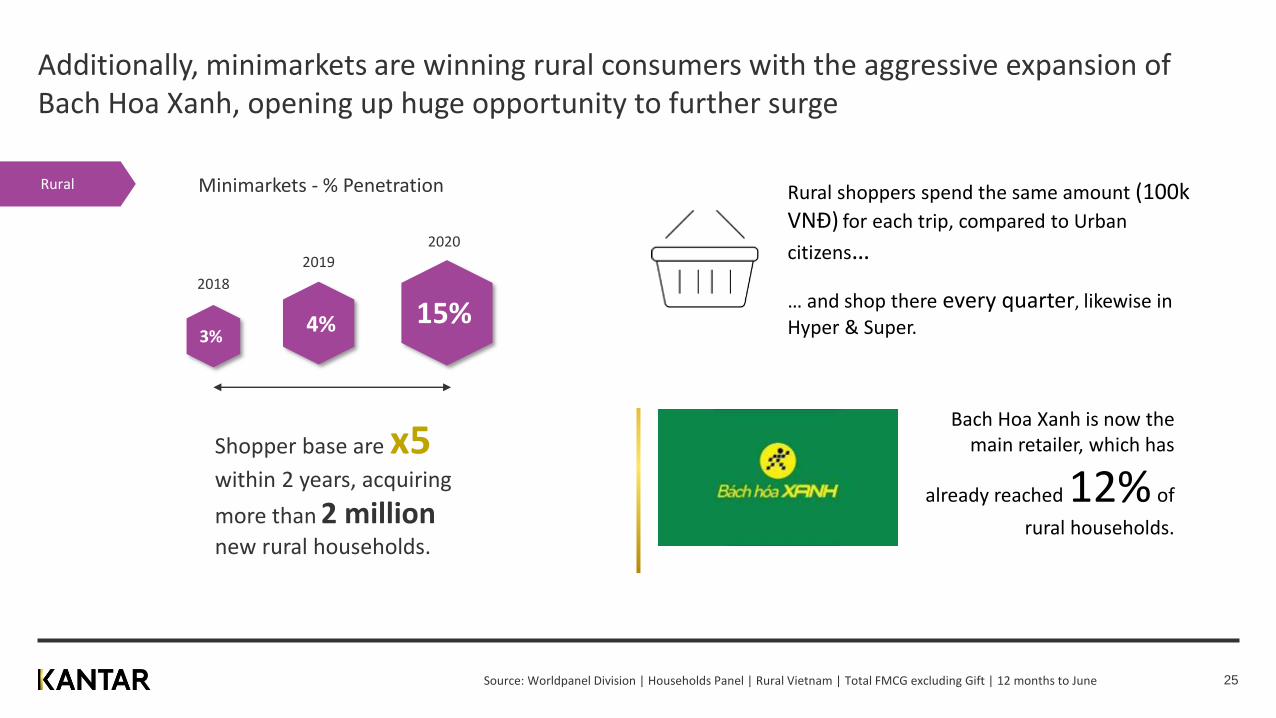

Additionally, minimarkets are winning rural consumers with the aggressive expansion of Bach Hoa Xanh, opening up huge opportunity to further surge

Bach Hoa Xanh is now the main retailer, which has

already reached 12% of

rural households.

Source: Worldpanel Division | Households Panel | Rural Vietnam | Total FMCG excluding Gift | 12 months to June

Rural Minimarkets - % Penetration

3%4% 15%

2018

2019

2020

Shopper base are x5within 2 years, acquiring

more than 2 millionnew rural households.

Rural shoppers spend the same amount (100k VNĐ) for each trip, compared to Urban

citizens…

… and shop there every quarter, likewise in Hyper & Super.

25

What’s next: Virtual stores, vending machines, click & collect

Vingroup chose 20 points in Hanoi and Ho Chi Minh City to officially launch the VinMart virtual store 4.0 which allows users to buy a product by scanning its QR code via smartphone. The products are listed on large banners in crowded public areas such as bus stations and office buildings, offering delivery within 2-4 hours.

There is an increasing number of vending machines in public areas i.e. bus station and soon metro stations. The format which skews more to younger consumer groups is potential for drinks & snacks brands to win impulse purchases. It is expected to see more in the near future.

26

• There is a huge amount of content on

Kantar.com/inspiration/coronavirus

• News/updates specific to Vietnam on

Kantarworldpanel.com/vn

We are here to help – additional resources and further content

linkedin.com/company/worldpanelbykantar/

To discuss on your key business questions at

category/ brand level, please get in touch with me

via [email protected] or

THANK YOU!

27