Venezuela Structural and Macroeconomic Reforms The...

97

Report No. 10404-VE Venezuela Structuraland Macroeconomic Reforms - The New Regime March18, 1993 Country Operations Division Country Department I Latin America and the Caribbean Region iI- .;i: . I1 1 . I ; :a,, ,.; 1 1. t .' ' ' 1 : . ; . ~~~~ ti,.~~~~~~~~~~~ FOR OFFICIALUSEONLY ji ,i Document of the World Bank Thisdocument has a restricted distribution and maybe used by recipients only in the performance of their official duties. Itscontents maynot otherwise bedisclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Venezuela Structural and Macroeconomic Reforms The...

Report No. 10404-VE

Venezuela Structural and MacroeconomicReforms - The New RegimeMarch 18, 1993

Country Operations DivisionCountry Department ILatin America and the Caribbean Region iI- .;i: .

I1 1 . I ; :a,, ,.;

1 1. t .' ' ' 1 : . ; .

~~~~ ti,.~~~~~~~~~~~

FOR OFFICIAL USE ONLY ji ,i

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

FISCAL YEAR

January 1 to December 31

CURRENCY EQUIVALENTS

Currency Unit = Bolivar (Bs)Exchange Rate Effective December 31, 1992

US$1 = Bs. 79.7Bs. 1 = US$0.012

Bs. 1,000 = US$12.55

FOR OFFICIAL USE ONLY

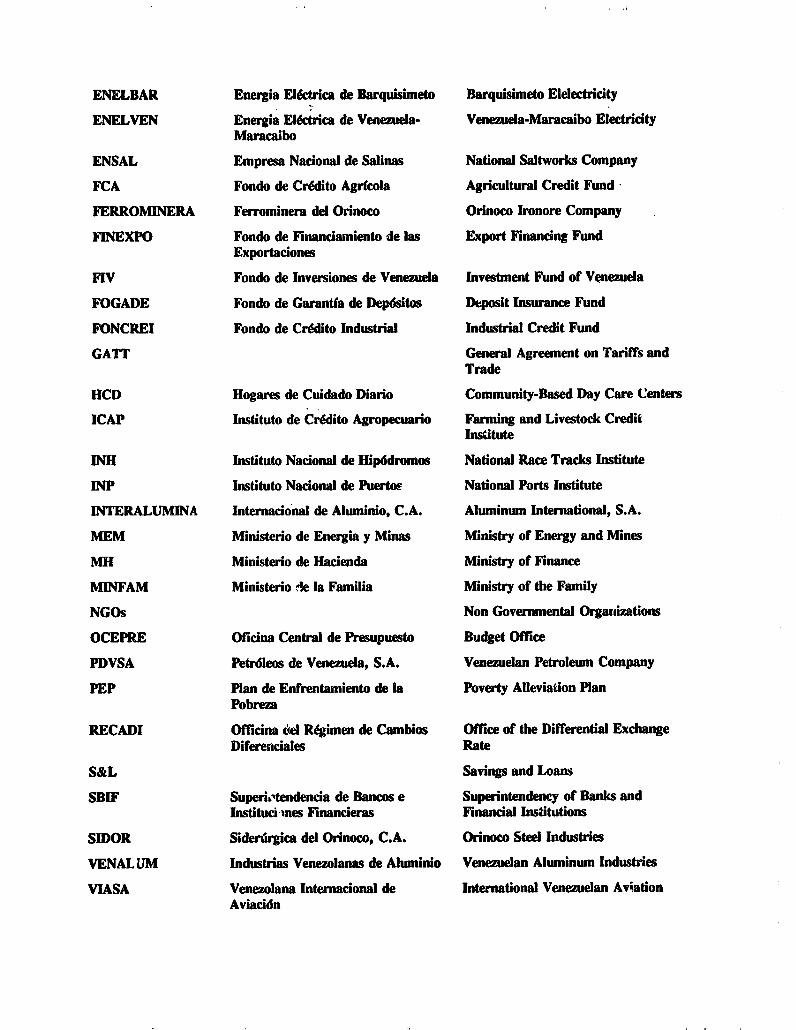

GLOSSARY OF ACRONYMS

AEROPOSTAL LUnea Aeropostal Venezolana Venezuelan Postal Airliie

ALCASA Aluminio del Caroni, S.A. Caroni Aluminum, S.A.

BANAP Banco Nacional de Ahorro y National Savings and Loan BankPrestlmo

BANDAGRO Banco de Desarrollo Agrfcola Agricultural Development Bank

BAUXIVEN Bauxita Venezolana, C.A. Venezuelan Bauxite, S.A.

BCV Banco Central de Venezuela Central Bank of Venezuela

BIV Banco Industrial de Venezuela Venezuelan Industrial Ea ,k

CADAFE Compania Anonima de Desarrollo y Development and Cooperation forFomento Electrico Electrical Power Company

CAMETRO Compailia An6nima Metro de Caracas Subway CompanyCaracas

CANTV Compafilia Andnima Nacional de National Telephone, S.A.Telefono

CARBOSUROESTE Carbones del Suroeste Southwest Coal Company

CASA Agricolas, S.A. Agrarian Industries, S.A.

CAVEINEL Camara Venezolana de la Industria Venezuelan Chamber of ElectricalElectrica Industries

CAVN Compaffia An6nima Venezolana de Venezuelan Navigation, S.A.Navegaci6n

CORDIPLAN Ministerio de Planificacion y Ministry of Coordination andCoordinacion Planning

CORPOINDUSTRIA Corporaci6n de Dsarollo de la Corporation for the Development ofPequefla y Mediana Industria Small and Medium Industry

CTV Confederacdon Trabajadores de Venezuelan Workers ConfederationVenezuela

CVF Corporaci6n de Venezolana de Venezuelan DevelopmentFomento Corporation

CVG Corporaci6n Venezolana de Guayana Development CorporationGuayana

DFI Instituciones Financieras de Development Financial InstitutionsDesanrollo

EDELCA Electrificacid6n del Caroni Caroni Electrification Company

ELECAR Electricidad de Caracas Caracas Electricity Company

This document has a restricted distribution and mav be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

ENELBAR Energia Electrica de Barquisimeto Barquisimeto Elelectricity

ENELVEN Energia Electrica de Venezuela- Venezuela-Maracaibo ElectricityMaracaibo

ENSAL Empresa Nacional de Salinas National Saltworks Company

FCA Fondo de Credito Agrfcola Agricultural Credit Fund

FERROMINERA Ferrominera del Orinoco Orinoco Ironore Company

FINEXPO Fondo de Financiamiento de las Export Financing FundExportaciones

FIV Fondo de Inversiones de Venezuela Investment Fund of Venezuela

FOGADE Fondo de Garantfa de Dep6sitos Dtposit Insurance Fund

FONCREI Fondo de Credito Industrial Industrial Credit Fund

GATT General Agreement on Tariffs andTrade

HCD Hogares de Cuidado Diario Community-Based Day Care Centers

ICAP Instituto de Credito Agropecuario Fanning and Livestock CreditInsCitute

INH Instituto Nacional de Hipodromos National Race Tracks Institute

INP Instituto Nacional de Puertos National Ports Institute

INTERALUMINA Internacional de Aluminio, C.A. Aluninum International, S.A.

MEM Ministerio de Energia y Minas Ministry of Energy and Mines

MH Ministerio de Hacienda Ministry of Finance

MINFAM Ministerio -le la Familia Ministry of the Family

NGOs Non Governmental Organizations

OCEPRE Oficina Central de Presupuesto Budget Office

PDVSA Petrdleos de Venezuela, S.A. Venezuelan Petroleun Company

PEP Plan de Enfrentamiento de la Povert Alleviation PlanPobreza

RECADI Officina dAel Rgtinen de Cambios Office of the Differential ExchangeDiferenciales Rate

S&L Savings and Loans

SBIF Superiotendencia de Bancos e Superintendency of Banks andInstituci snes Financieras Financial Institutions

SIDOR Siderqrgica del Orinoco, C.A. Orinoco Steel Industries

VENAL UM Industrias Venezolanas de AlMninio Venezuelan Aluminum Industries

VIASA Venezolana Internadonal de International Venezuelan AviationAviaci6n

VV3UgEL1 STRUB-RAL AND NACR-O0C IC 33 ME-!3 3EV RESINS

TABLE OF CONTETS

ABSTRACT . . .. . . . . . . . . . . . . . . iv

BXECUTIVE SUMMARY . . . . . . . . . . . . . . . . . . . vi

1. STRUCTURAL REFORMS . . . . . . . 1 . . . . . . . . . . 1

A. IntroductLon ........... a. *.. 1

B. Major Areas of Reform ................. 2

Prlvatization . . . . . . . . . 2Prior Conditions. 2objectives, Policies and Targets . . . . . . . . . 3ImplementatLon 5Lessons and Issues... 5

Foreign-Trade Reforms ............. 6Prior CondLtionsdit.n..... . ....... 6

(a) Foreign Exchange Controls and Import Bazriers 6(b) Tariffs . . . . . . . . . * . . . . . . . 9(c) Export Incentives . . . . . . . . . . . . . 11

Reform Measures .................. 12Evaluation and Further Reforms . . . . . . . . . . . 15

C. 8ectoral Surveys . ....... . ........ . . . . 16

Agriculture ............... *......16Prior CondLtLonsi ................ 16Policy Reforms. ..... .. ........ . 17Zvaluation and Further Reforms . . . . . . . . . . . 18

Power and Energy . . . .. ............ . . 19Prior CondLtLonsiti ............... 19PolLcy Reformso. ..... ........... 21Evaluation and Fu:ther Reforms . . . . . . . . . . . 23

Infrastructure.. .. 24Prior Conditions . ............ 24Policy Reforms. .. ............... 27Evaluation and Further Reforms . . . o . . . . . . 30

Financial Sector ...... .......... . 34PrLor Conditions.......... .... . 34Pol$cyReform s ............. . ... 36Evaluation and Further Reforms . 37

Social Sectors . . . . . . . . . . . . . . . . . . . 39Prior Conditions ...... .. .. .. .. .. . . 39Policy Reforms . :... ... ... . 40Evaluation and Further Reforms. .. . . . 42

II. MACROECONOMIC REFORMS . . . . . . . . . . . . . . . . . . . . . . . 46

A. The Stabilization Policy ...... .. .. .. .. .. . . 46

Prior Conditions ....... .. ......... . 46

Major Elements of the Stabilization Policy . . . . . . 47The Foreign-Exchange Rate . . . . . . . . . . . . . 47Fiscal Policy . . . . . . . . . . . . . . . . . . . 49Monetary Policy . . . . . . . . . . . . . . . . . . 50

Impact of the Stabilization Policy . . . . . . . . . . 52

The Policy Change ....... ... .. .. .. .. . 55

Evaluation of the Stabilization Policy . . . . . . . . 58

S. Inherent Macroeconomic Problems . . . . . . . . . . . . . . . 59

Fiscal Issues ........ ... ... .. ... . 60Government Revenues . . . . . . . . . . . . . . . . 60

Government Expenditures . . . . . . . . . . . . . . 61The Budgetary Process . . . . . . . . . . . . . . . 63

Fluctuations in Oil Revenues . . . . . . . . . . . . . 64

Targets and Instruments of Monetary Policy . . . . . . 66

The Real Exchange Rate ................ . 70

- iii -

LIST 0P TABLES

Table 1: IMPORT RESTRICTIONS AND AVERAGE TARIFFS BY SECTOR AND

STAGE OF PROCESSING, 1989-91 . . . . . . . . . . . . . . . 10

Table 2: IMPORT RESTRICTIONS AND AVERAGE TARIFFS BY

MANUFACTURING SURSECTOR, 1989-91 . . . . . . . . . . . . . 14

Table 3: RATE OF INFLATION AND THE FOREIGNEXCHANGE RATE, 1970-91 . . . . . . . . . . . . . . . . . . 46

Table 4: NOMINAL AND REAL EXCHANGE RATES, 1988-91 . . . . . . . . . . 48

Table 5: FISCAL ACCOUNTS, 1988-91 (ANNUAL) . . . . . . . . . . . . . . 49

Table 6: MONEY SUPPLY, 1988-91 .51

Table 7: THE RATE OF INFLATION, 1988-91 . . . . . . . . . . . . . . . 53

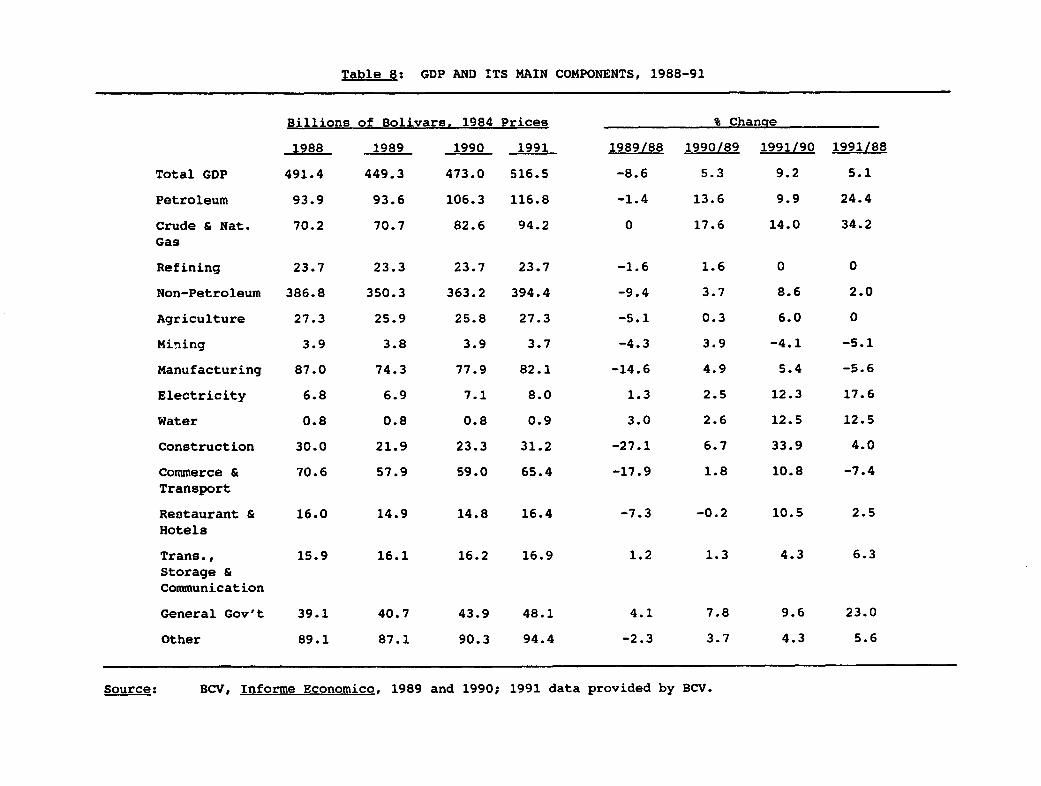

Table 8: GDP AND ITS MAIN COMPONENTS, 1988-91 . . . . . . . . . . . . 54

Table 9: FISCAL SURPLUS OR DEFICIT, 1989-91, (QUARTERLY) . . . . . . . 56

- iv -

PREFACE

The Administration of Fresident P6rez, which assumed power inearly 1989, has introduced several fundamental measures of ezonomic reform andmacroeconomic stabilization. The present study, three years after theintroduction of these policies, is intended to serve as a stock-taking. Itdescribes and analyzes the circumstances under which the policies were adoptedand the nature of the policies as they were announced and implemented. Italso evaluates the achievement of the policies, and indicates the directionsin wwhich policies could be further pursued, improved, or changed. Structuralreforms are discussed in the first part of the study and macroeconomicpolicies are analyzed in the second part.

The first part has drawn on sector work and current sources ofknowledge in the Department. It encompasses the contributions of Malcolm Bale(Agriculture); Bruce Fitzgerald (the Foreign-Trade Regime); Feliciano Iglesias(the Financial Secto, Vladimir Jadrijevic (Power and Energy); Robert Taylor(Privatization and I- tructure); and Cecilia Valdivieso (the SocialSectors). The saca- -t is the work of a macroeconomic evaluation missionthat visited Venezueli .u June 25 to July 5, 1991. Mission members wereBruce Fitzgerald, Felica.dno Tglesias, Mayra Zermeno, and Michael Michaely(Mission Leader and principal author of the report). The analysis also drawson deliberations in a worksh p. on Ver- Aela's macroeconomic policies held inAnnapolis, Maryland, from September 23-24, 1991, and attended by Venezuelanofficials, World Bank staff, ane -ml _l of academia.

A draft of the report was submitted to the Venezuela Government inApril 1992, and discussed with the Government in a seminar held in Caracas onAugust 29-30, 1992. Written comments have also been made subsequently by theGovernment. The Government's concerns are addressed in this revised versionof the report.

Some of the issues discussed in Part II of this report(Macroeconomic Reforms) are analyzed more thorcughly in a study authored bySebastian Edwards, on "Venezuela: Oil and Exchange Rates--HistoricalExperience and Policy options" (Report No. 10481-VE, February 1993).Consulting that report, in conjunction with the present one, would shedfurther light on the issue of the real exchange rate.

ABSTRACT

This report provides an evaluation of the policy changesimplemented by the new administration of President Perez in Venezuela threeyears after their introduction. The pattern mostly followed in the discussion

of each policy &rea is as follows: a description of conditions andcircumstances in the opening position, prior to the introduction of newpolicies; a presentation of the nature of these policy changes; a discussionof the effectiveness of the new policies; and a suggestion of further policyrevisions. The report is presented in two parts: structural reforms in thefirst part, and macro-economic policies in the second.

Structural reforms are discussed under two headings. One is

functional: in this way, two major areas of reform, i.e., privatization and

the reform of the foreign-trade regime, are examined. The other framework issectoral. Under the latter heading the major sectors in which reforms havebeen undertaken are snrveyed: agriculture; power and energy; infrastructure;the financial sector; and the social sectors.

By and large, the report's findings indicate a deep, as well asbroad, process of structural reforms in Venezuela, leading to substantialrationalization of the operation of the economy along with an improvement ofthe Government's handling of poverty and human resources issues. Much,however, still remains to be done, particularly in extending the process ofprivatization to the Government's major enterprises and in strengtheningreforms in the agriculture and the power and energy sectors.

The analysis of the episode of macro-economic stabilizationindicates that the policies undertaken to achieve stabilization were indeedeffective, and a large measure of balance was achieved. These policies were,

however, of a transitory nature, so that in time they were at least partly

reversed. Stabilization is, thus, not entirely assured. The developments of

this episode illustrate several fundamental factors and inherent long-term

macro-economic problems such as the effect of fluctuations of oil revenues,

the low level of non-oil taxation, and some salient implications of the systemfor the country's real exchange rate and its economic structure. Thesefundamental issues, beyond the analysis of stabilization, form part of the

topic of the report's macro-economic discussion.

- vi -

EXEuTIVE SUNW&RY

i. For many years, through 1989, Venezuela .ollowed a policy markedby economic insulation and pervasive government intervention in the country'seconomic life. This policy was reinforced in the mid-1970s by the sharpincrease in oil prices--followed, a short time later, by nationalization ofthe oil industry--which handed the government a large share of the country'seconomic resources.

ii. After oil prices collapsed in the early 1980s, many Venezuelansrealized that this model of economic life and development was grosslydeficient. Perceptions of the magnitude of waste, inefficiency, anddistortion created by the government's pervasive intervention undoubtedly wereheightened by the accumulating experience of countries, particularly in LatinAmerica, that had discarded intervention in favor of free markets, withbeneficial results.

iii. In 1987-88, Venezuela, for the first time in its postwar history,faced a severe macroeconomic imbalance. International experience has shownconvincingly that a macroeconomic crisis, which calls for a radical policychange acceptable to the population and the political organization as a whole,is also an opportune time for significant economic transformations. Thereform policy package was adopted in February 1989, immediately afterPresident P6rez assumed office. Since then, the policies of structuraltransformation have been an on-going process rather tnan a one-shot operation.

Structural Reforms

iv. Privatization. During the 1970s and 1980s, successivegovernments in Venezuela followed a development strategy relying heavily onstate control of productive sectors. In addition to traditional publicservices (e.g., water, telephone, electricity), state-owned enterprises (SOEs)dominated many sectors, including petroleum (PDVSA), mining, aluminum, power,and steel. Expansion into these sectors was part of an ambitious design todirect resources generated by petroleum to develop untapped natural resources,and promote import substitution and self-sufficiency. It was initiated in themid-1970s with the nationalization of the oil and iron ore industries,followed by heavy public investment in power, steel, and aluminum. Fundschannelled through the Fondo de Inversiones de Venezuela (FIV), set up toinvest petroleum revenues, were initially provided as loans which, in mostcases, have been converted to equity as a result of the inability of the SOEsto repay them.

v. In comparison with the other measures in early 1989, theprivatization program was slower to develop and initially very modest inscope. In mid-1989, the Economic Cabinet approved a broad SOE rationalizationstrategy, prepared by CORDIPLAN, that categorized SOEs according to the type

- vli -

of market (competitive vs. monopolistic) in whicr. they operated and thefeasibility of privatizing them. Privatization in the shorc term was to belimited to small- and medium-sized companies in tourism, manufacturing, agro-industry, and bankino.

vi. In mid-1990, the program was expanded considerably when thegovernment decided to privatize CANTV (the telephone company) and VIASA (theinternational airline). In the case of CANTV, it was recognized that the verypoor quality of telephone service was a significant constraint on thecountry's international competitiveness, particularly in the private sector,and that the expansion and improvement of servica could be achieved onlythrough the sale of a controlling block to an experienced internationa.company. In the case of VIASA, the decision was based on VIASA's mount'losses.

vii. The FIV has a well-developed procedure for privatization: aninitial diagnostic analysis of the company and the sector; design of a salesstrategy; valuation; reparation of a sales memorandum or ptospectus (for apublic share issue); nLe-qualification of potential bidders; and the publictender or share offering.

viii. By the end of 1991, the government had sold its holdings in sevenmajor enterprises: VIASA, CANTV, three commercial banks (Italo-Venezolano,Occidental, Republic), a sugar refinery (El Tocuyo), and a shipyard(ASTINAVE). These transactions yielded approximately US$2.2 billion, with thebulk of this amount (US$1.9 billion) coming from the sale of 40 percent ofCANTV to an international consortium led by GTE. In addition to these sales,the government liquidated the national ports agency (INP), privatized cargohandling and stevedoring, and transferred responsibility for administering theports to new regional port authorities. S.milar privatization initiatives areunderway in housing (INAVI) and in trash collection (IMAU).

Poreicn-Trade Reforms

ix. From 1973 to February 1983, Venezuela maintained a fixed exchangerate of 4.3 bo±ivars to the U.S. dollar that increasingly overvalued thebolivar. Early in 1983, a series of currency crises was resolved byintroducing a multiple exchange rate system that prevailed through early 1989.A free market rate applied to nontraditional exports, tourism, and capitaltransfers. From 1984-88, this rate ranged from 60 percent to 200 percentabove the official rate.

x. A pervasive system of noi-tariff barriers reinforcing a highlevel of tariffs had served as the e tctive constraint on imports. For mostitems, a potential importer had first co obtain an import permit from theDevelopment or the Agriculture Ministry that would be granted only if domesticproducers did not object. Importers had then to apply on a case-by-case basisto the Office of the Differential Exchange Rate Regime.

xi. Before the trade reforms of 1989, there were 41 tariff rates, themaximum being 135 percent. Tariffs had been established over the years on acase-by-case basis without guidelines. The spread was great: about a sixth

- viii -

of the items attracted tariffs below 1 percent and a fifth above 80 percent.In addition to ad valorem tariffs, 854 items also attracted spacific duties sothat effective rates *ere as high as 940 percent. Tariff rates by sector andstage of processing hat. the cascading pattern (high for final goods, low forinputs and capital goods) typical of import substitution. Tariff rates foritems restricted by NTBs were higher than for those freely importable. Therewere also large differences 'n average tariffs among the manufacturingsubsectors.

xii. To offset the strong ant-export bias inherent in the importzegime and the overvalued exchange rate, the government offered three exportincentives: the bono de e-vortaci6n, a subsidy to non-traditional exporterspaid as a percentage of tk.Ar export receipts; a currency retention scheme;and subsidized credit for exporters through FINEXPO.

xiii. The policy reforms in February 1989 amounted to a radicaltransformation of the trade regime. In intensity--measured by the extent ofthe changes and the speed with which they were introduced--they rank at thetop, whether in Latin America or in the world as a whole, in recent years.The cornerstone of the reform policy was the unification and floating of theexchange rate. Along with this change came the abolition of foreign-exchangecontrols and, thus, of a major device for import rationing and rent seeking.Import prohibitions and licensing have been sharply reduced, today protectingonly about 2 percent of domestic produc ion, well within the government's goalof no more than 5 percent in the medium term. The greatest incidence of QRsremains in agro-industry. Tcriffs, too, have been lowered substantially. Thetariff code for the manufacturing sector has been restructured to afford eachline of production roughly the same protection. The level and range oftariffs have been cut substantially. The average rate has been reduced from37 percent to 16 percent, with consumer goods--at 33 percent--continuing to besubject to the highest rates. The maximum tariff has been lowered from i35percent to 80 percent and then to 50 percent, and the government's announcedtarget is to reduce it to 10 to 20 percent by 1993. Discretionary tariffexonerations have been eliminated. However, exemptions established by lawremain for some entities such as state-owned enterprises, universities, andthe central government.

xiv. The reforms have been wide and deep and must lead to majoreconomic benefits. The government, to date, has maintained an admirabledegree of uniformity in the treatment of economic sectors, and has replacedthe system of QRs, ad hoc protection, and costly export subsidies with asystem that--when fully implemented by 1993--will use effective exchange ratemanagement in place of import substitution or export promotion. Moderatetariffs--between 10 and 20 percent--will provide additional protection forimport-competing domestic producers, leaving a residual anti-export bias afterexport subsidies have been eliminated.

Maior Sectoral Reforms

xv. Agriculture. Between 1984 and 1988, the government attempted tomaintain high producer prices and profits while maaintaining low and stable

- ix -

consumer prices. Imports and exports were restricted. The critical elementof the policy was that government resources would subsidize producer pricesuntil inefficiencies in the sector were rectified and the productive capacityexpanded.

xvi. The policy was unsustainable and could not have logicallyachieved the coal of removing inefficiencies in the sector. It resulted inhighly distorted relative prices and extensive government intervention. Italso entailed huge subsidies. By 1987, these were estimated at almost US$1billion a year, equivalent to about one-third of agricultural value added and2 percent of GDP. In addition, the policy failed to keep retail and wholesalefood prices low and stable. The attempt to increase resources for privatesector investment in agriculture through subsidized credit have had negativeeffects on the financial sector. Agricultural portfolio requirements anddirect credit subsidies have contributed to the underdevelopment andinefficiency of financial institutions, while poor loan repayments havebankrupted one public sector institution (BANDAGRO) and left two others (FCAand ICAP) in a critical sitiation. Further, leakages of subsidized credit tonon-agricultural activities have partially defeated the purpose of theprogram.

xvii. Unifying and floating the exchange rate has been crucial foragriculture. So were other changes in the foreign-trade regime. Since July1990, prior licensing for most agricultural commodities, with the importantexception of feed grains and poultry, have been removed. A transparent priceband mechanism for wheat, rice, white corn, oilseeds, yellow corn, and sorghumhas also been implemented to stabilize domestic prices and provide additionaltariff protection for these key commodities. Export controls on rice,legumes, and cornmeal have also been ended.

xviii. Administered producer prices have been discontinued except forccmmodities still subject to import licensing. Most agricultural inputsubsidies have besn ended, except for irrigation and fertilizers. Irrigationfees cover only about 1-2 percent of the cost of irrigation. The subsidy onfertilizers was significantly reduced in 1990. All domestic wholesale priceshave also been deregulated. The twelve food items initially subject to pricecontrols were first reduced to five, and more recently to one (sardines).

xix. Several measures have liberalized interest rates and creditallocations to agriculture. But major steps are still required to achievefull liberalization of finance in the sector. Another sphere in which evenless has been done is irrigation. The planned phasing out of water subsidieshas been very slow, and at the present rate is unlikely to achieve full costrecovery in the foreseeable future.

xx. Power and Energv. Power prices in the past decade have notreflected the cost of service and have resulted in an unsatisfactory generalrate level and distorted tariff structure. This policy has had two adverseconsequenc-s: (i) it has compounded the financial difficulties of theutilities and increased their dependence on government contributions; and (ii)it has sent distorted signals to the consumer, promoting waste and inefficient

use. A pricing policy that rationalizes the tariff structure and increases

prices to the level of costs is needed.

xxi. The reforms have been directed att (i) reducing the dominance of

the public sector through restructuring and privatization; (ii) increasing

operational efficiency; (iii) providing a strong central institution to review

and coordinate expansion plans, investment programs, and other activitiesrelated to the sector; and (iv) establishing a rational pricing system based

on long-run marginal cost criteria aimed at improving the economy's efficiency

and reducing government transfers.

xxii. At the start of the reform program, the price of gasoline was

increased significantly. Yet, even today, it is less than US$.30 per gallon--still among the lowest in the world. By comparison, the internationalwholesale price in the Caribbean market is about $.6C-.70 per gallon; anddomestic prices in European countries are about $2 per gallon. It appearsthat the government is no longer adhering to an original adjustment schedule,which was supposed to raise prices to their full opportunity costs.

xxiii. InfrastrMeture. Reforms have been undertaken in the sector's

major subsectors: telecommunications, ports, shipping, water supply andsanitation, interurban transport, and urban transport.

xxiv. The reform of telecommunications has four components, of whichthe principal component has been the privatization of CANTV through the salein November 1991 of a control block of 40 percent of its shares to aninternational consortium led by GTE for US$1.9 billion. Ali additional 11percent has been sold to the employees. Other reform measures are: theinjection of limited private competition in cellular telephones; theintroduction of a new tariff structure, with telephone rates progressivelyadjusted to cost levels; and the submission to Congress of a Telecom Law thatestablishes a new regulatory regime and introduces greater private investment

and competition.

xxv. In early 1990, the government decided to undertake the followingreforms in ports: the dissolution of INP and the dismissal of all INPworkers; the establishment of regional port authorities to oversee the ports

(with the commensurate transfer of responsibility for ports administration tostate governments); and the operation of all ports by the private sector underconcession agreements. Consulting firms and auditors were hired to design thenew ports regime and prepare the dissolution of INP. By the end of 1991, muchof the reform program had been completed.

xxvi. Over the past 12 months, the government has implemented a numberof measures to liberalize shipping and increase competition. Numerous

restrictions faced by importers and exporters have been eliminated, including

those pertaining to transshipment, opening new routes (and route extensions),

and use of CAVN for shipments financed through letters of credit. A number of

regional and bilateral agreements have eliminated cargo reserve requirements,

allowing shippers freedom of choice in selecting a carrier.

- xi -

xxvii. In water supply and sanitation, the government launched a far-reaching restructuring strategy in mid-lS90 aimed at liquidating the nationalagency, establishing autonomous and financially self-sufficient regional watercompanies, and, where feasible, privatizing operations through concessionagreements with private operators. Progress, however, has been slow.

xxviii. In inter urban tranLnortation, the main objectives are todecentralize the management of rural roads and to establish a national roadfund. The fund will be financed by new taxes on petroleum products earmarkedfor the rehabilitation and maintenance of the national highway and ruralfeeder road networks.

xxix. In July 1990, a steering group was formed under theInterministerial Commission on Urban Transport to determine objectives andpriorities, to make recommendations on the sector's institutional andregulatory frameworks, to evaluate policies, and to formulate a strategy forthe short aiid medium terms. A review of tariffs and subsidies has beencompleted, and studies have been launched on financing mechanisms,institutional arrangements (particularly the roles of the various governmentallevels), and options for expanding urban transport to the poorer areas on theoutskirts of Caracas.

xxx. The Financial Sector. Until the reiorm, interest rates weresubject to ceilings. As a result, real interest rates were mostly low and,particularly with the acceleration of inflation in the second half of the1980s, often negative. New liquid assets were formed to circumvent theregulations that made real interest rates on deposits negative (these assetsare not subject to reserve requirements).

xxxi. Beyond the segmentation created by the existence of numerouspublic credit institutions with power to determine rates and conditions ofloans, there were portfolio requirements for private banks. Commercial bankswere subject to a 22.5 percent lending portfolio requirement for agricultureand agro-industry. Interest rates for these loans were required to be belowmarket rates. A particularly serious problem is the weak financial positionof some institutions, which makes insolvency likely. Mortgage banks and S&Lsare experiencing major financial problems because of the mismatch between thematurity and rate structure of their assets and liabilities. Multiplegovernment-sponsored programs that finance housing have made most of theseinstitutions highly dependent on subsidies to survive.

xxxii. The objectives of the financial sector reform are: (i) toliberalize the financial policy environment (interest rates, allocation ofcredit, foreign ownership, universal banking, etc.); (ii) to reduce the roleof government in financial intermediation (by privatization and liquidation ofpublic banks, consolidation of DFIs, rationalization of housing financepolicy, etc.); (iii) to limit the role of the BCV to providing liquidity andto monetary management; (iv) to improve the supervision and handling of bankcrises; and (v) to increase competitiveness in banking.

- xii -

xxxiii. In April 1990, the BCV issued an order setting the minimumdeposit rate at 10 percent and the maximum lending rate at 60 percent forcommercial and mortgage banks, finance companies, and S&Ls. The spreadbetween these limits allows sufficient scope for market determination ofinterest rates at prevailing inflation rates. The policy is to increase thelending rate ceiling and to decrease the limit on deposit rates as soon asthey become binding. The limits have not yet required further change.

xxxiv. Several laws have been sent to Congress to regulate the CentralBank, the SBIF, FOGADE, the Industrial Credit Fund (FONCREI), and theAgricultural Credit Fund (FCA). If approved, these laws will provide therequired framework to support the objectives of reform.

xxxv. The Social Sectors. Venezuela's per-capita income is amcngst thehighest in Latin America. But a highly skewed distribution of income leaveslarge segments of the population in poverty they are unlikely to escape.Infant mortality rates have fallen substantially since 1965 (from 65 per 1,000to 36 per 1,000 in 1988), but still remain double those of Jamaica and CostaRica, which have half the per capita income. Similarly, although schoolenrollments have increased rapidly over the same period, gross secondaryschool enrollment is only two-thirds that of Uruguay, Argentina, and Chile.

xxxvi. Previous anti-poverty programs attempting to redistribute incomethrough general food subsidies and free social services failed despite highexpenditures. The main beneficiaries of food subsidies tended to be themiddle and higher income groups, who could afford to buy greater quantities ofsubsidized goods. While social services were presumed to be universal andfree of charge, poor management and inefficient investment left manyb--neficiaries out of reach of service delivery.

xxxvii. In 1989, the government replaced general food subsidies withprograms specifically for lower-income groups and expanded existing programsthat target the most vulnerable members of society. These actions weredesigned to shield the poorer segments of the population from the adverseeffects of structural adjustment and to overcome past deficiencies intargeting, coverage, and administration of selected social services. Thegovernment has undertaken a huge effort in this area: the resources budgetedfor these programs in 1992 surpassed US$700 million.

xxxviii. The new strategy emphasizes a shift from general subsidies toprograms benefiting lower-income groups. Its principal objectives are to:(i) relieve the severe hardship resulting from economic decline; (ii) mitigatethe impact of adjustments in the economy necessary to achieve sustainable,long-term growth; and (iii) set the basis for human capital development, anessential factor of growth with equity. Other elements of this strategy areto improve the planning and monitoring capacity of participating ministriesand to increase the efficiency of service delivery.

xxxix. To increase the cost effectiveness of social expenditures, thegovernment has emphasized three principles in the selection of projects: (i)increased targeting of the poor; (ii) decentralization of design and

- xiii -

management; and (iii) greater participation of the private sector (both for-profit and non-profit) in service delivery.

xl. Four social programs form the core of the poverty alleviationstrategy: (i) a nutritional grant program consisting of a direct cash subsidyto families of school children in low-income areas (Beca Alimentaria); (ii) amaternal-child health care and feeding program aimed at expanding primaryhealth coverage and improving health service delivery through fooddistribution to vulnerable groups seeking preventive health care (i.e.,primarily pregnant and nursing women and children under six years of age);(iii) Hogares de Cuidado Diario (HCD), a community-based day care programdirected at children of working mothers in low-income neighborhoods; and (iv)a preschool expansion program targeted to poor rural and urban areas.

Evaluation and Recommendations for Further Reforms

xli. Overall, Venezuela's program of structural reforms has been mostimpressive. Radical new policies have been introduced, on a massive scale,and implemented rapidly and without wavering. Within three years, the natureof the operation of most sectors, and in particular the role played bygovernment intervention, have gone through a massive transformation.

xlii. Needless to say, not everything could be accomplished within ashort time. Much is still left to be done--more in some sectors or aspects ofeconomic life, less in others. Of the territory yet to be covered, muchprogress is still contemplated by the Government of Venezuela. In thefollowing, we shall refer to the main changes that still have to beintroduced, whether or not they already are on the agenda of further action ofthe Government.

xliii. The privatization process, slow at the start, has gatheredmomentum and acquired substantial proportions with the sale of, inter alia,VIASA and CANTV. At present, the extension of the process into the majorareas of government-owned enterprises should be contemplated. Specifically,the privatization of the CVG conglomerate of industrial and mining enterprisesshould be the next major step. Privatization of PDVSA cannot be carried outin a single step, given the company's huge size; but a gradual process of saleof shares, rather than of the company as a whole, could be started.

xliv. Probably the most far-reaching transformation has been achievedin the trade reaime. Here, avoiding any reversal is probably more importantthan the achievement of any specific target of further reforms. Among thelatter, three measures would be particularly significant: the abolition ofremaining non-tariff barriers to imports in the agricultural sector; theelimination of remaining tariff exemptions; and the encouragement of privatecredit markets for exports, to replace the subsidized government finance.

xlv. The agriculture sector has adjusted well to the reform process,with the output mix responding to the changes in relative prices and to thelarge measure of removal of protection. But reforms in this sector, whilesignificant, have not gone far enough. The most important further steps whichshould be undertaken are: complete elimination of import licensing and

- xiv -

minimum-price programs--a step the Government plans to take over the next twoyears; phasing out of price-stabilization schemes; elimination, as theGovernment indeed plans, of the fertilizer subsidy; elimination of governmentmarketing and divestiture of its storage facilities; deregulation ofagricultural credit; increase (in fact, introduction) of water charges inirrigation schemes to cover full costs; and land reform, to establish clearerentitlements and property rights.

xlvi. In the sector of Dower and_enerav, while some prices have beenliberalited in the 1989 reform, inadequate prices remain a key issue forpetroleum, electricity, and gas. Likewise, the progress towards privatizationhas been minor. Thus, the two areas of required reforms are, first, theestablishment of prices at the levels of long-run marginal costs--a policy towhich the Government is committed in principle, and which it expects tointroduce gradually; and Pt least a beginning of a gradual, long-tern. processof privatization of activities in the production and distribution ofpetroleum, gas and electricity.

xlvii. In the infrastructure sectors, the greatest progress has beenachieved in telecommunications, with the privatization of CANTV. In oorts,the dissolution of the INP and the transfer of all cargo handling andstevedoring to private forms have already had a dramatic impact on efficiency.Further important reforms would be the granting of concessions to privatefirms for operation of entire ports or individual terminals, allowingcompetition both between ports and within large ports. In water supplv andisanitation, important decisions have been made, but implementation has beendelayed. The actions required now are, primarily, the enactment of a newwater sector law; the development and implementation of a new structure ofwater tariffs; the liquidation of INOS, transferring its assets to the newregional water companies; and the transfer of the Caracas water system to aprivate operation. In the inter-urban transoort sector, the required reformsconsist, first, of establishing appropriate prices--of petroleum, or of roaduses. A concession program should be established for private sectorconstruction and operation of expressways. Finally, in urban transport, therecommended agenda for further reforms should include: the deregulation ofthe bus system--particularly of fares; the replacement of generalizedsubsidies by targeted subsidies; the strengthening of agencies involved inurban transport; and a redefinition of the roles of the public and privatesectors in the provision of passenger services within Caracas.

xlviii. The financial sector has witnessed impressive reforms:establishment of proper rules for a competitive banking system, limitingsegmentation and allowing foreign investment; privatization of banks;establishment of a much higher degree of independence of the Central Bank fromthe Treasury; and equipping the Central Bank with a new set of instruments.Almost all further required reforms are included in legislation alreadysubmitted to Congress. When enacted, these laws would provide further openingof the commercial-banking system to foreign participation; solutions to themain problems of the housing finance system; restructuring of the network ofS&Ls, now badly ailing; and a redefinition of the legal and regulatoryframework of the insurance sector and of capital markets.

xv -

xlix. In the social sectors, finally, a lot has been accomplished, overa wide front. The government has shifted from highly inefficient generalizedsubsidies, available to the entire population, to directly-targeted programsbenefiting those most in need. This strategy represents a serious effort toaddress the issue of poverty both efficiently and equitably. Many problemsremain, though, including: highly centralized management, despite seriousdecentralization efforts; expenditures skewed towards higher-cost, inefficientuses of allocated resources; lack of targeting mechanism or sufficient data toidentify target groups; insufficient attention to design and to deliverymechanisms; and inappropriate or inadequate technical skills in the operationof social-sector programs. All these issues should be addressed, within arevised version of the Government's poverty-alleviation strategy. Inaddition, in all social- sector activities encouragement should be offered tothe use of both for-profit and non-profit private-sector mechanisms fordelivery of social services.

Macroeconomic Reforms

1. The Stabilization Policy. Venezuela has had continuous inflationsince the first major oil-price increase of 1974. Until the late 1980s,however, it was moderate and rather stable, with an average annual rate of 11percent (from 1974-86) and not much variation except for a jump following thesecond oil-price increase of 1979.

li. From 1986-88, however, economic policy became heavilyexpansionary. Public-sector investment jumped from 7.7 percent to around 12percent of GDP in 1987-88, and the budoetary deficit grew to 7.2 percent ofGDP. By early 1988, the inflationarv process had gathered momentum. By thesecond half of 1988 and early 1989, the rate of inflation was roughly 4percent per month, or some 60 percent per year. Throughout these changes, thenominal exchange rate remained fixed. A rapid appreciation of the realexchange rate thus took place, with a consequent deterioration in the balanceof payments. Nominal interest rates, too, remained constant (by decree)throughout the process. At the level of 13 percent per year, the realinterest rate thus assumed a high negative value--a factor that furtherencouraged the inflationary process.

lii. The rapid acceleration of inflation and the loss of foreign-exchange reserves created a perception of crisis heightened by capital flightand the foreign-debt burden. It was the recognition of this crisis that ledthe new Administration to make stabilization the cornerstone of reform inFebruary 1989. The three major and closely interrelated components of thestabilization package were: a new foreign-excha;;ge regime, fiscal policy, andmonetary policy.

liii. The Foreign ExchanQe Rate. The change in the foreign-exchangesystem was clearly the key to the stabilization plan. Under the existingmultiple exchange rate system, the principal (official) rate, applying to mosttransactions and especially to oil exports by PDVSA, had been maintained at aconstant nominal value of 14.5 Bs/US$ since December 1986. The exchange rate,now unified and left free to float, increased immediately to 39.3 Bs/US$ by

- xvi -

the end of February 1989. The nominal devaluation continued throughout 1989,by the end of which the exchange rate reached 43 BS/US$--three times its levelon the eve of the plan.

liv. Fiscal Policy. An increase in revenues from taxes on PDVSA'ssurplus was the predominant element of fiscal change and of the stabilizationpackage as a whole, and is related to the change in the foreign-exchangeregime. Most of PDVSA's income is surplus (i.e., an excess over the cost ofproduction), and most of this surplus, through taxes, constitutes a source ofgovernment revenues, which thus rise with an increase in the real exchangerate. In the event, this rise was dramatic: PDVSA's transfer to the centralgovernment increased from 11.4 percent of GDP in 1988 to 20.5 percent in 1989.A somewhat smaller fiscal improvement resulted from a reduction of thegovernment's capital expenditures. Public-sector investment declined by 2.5percent of GDP--from 13.9 percent in 1988 to 11.4 percent in 1989.

lv. Monetary Policy. Monetary developments largely reflect thechange in the fiscal stance. Having earlier exhibited a very rapid increase,the nominal supply of money (MI) declined by 3.5 percent in the first quarterof 1989, and fell further by 1.4 percent and 2.9 percent, respectively, in thefollowing two quarters. Thus, by the end of the third quarter of 1989,nominal money supply was about 8 percent below its level at the end of 1988.Combined with this change in nominal balances, a very sharp initial increasein prices practically halved real money balances: from the end of 1988 to theend of the third quarter of 1989, real money supply (M,) fell by 47 percent.Interest rates, freed by the plan, increased sharply. The controlled lendingnominal interest rate of 13 percent per year turned into a free rate hoveringat around 32 to 40 percent throughout 1989. During most of the year, thisimplied a slightly negative real interest rate; but it represented,nevertheless, a very sharp increase of the real rate.

lvi. Impact of the Stabilization Policy. The higher exchange ratetranslated into higher prices of tradable goods; combined with the increase ofpublic-sector prices, the elimination of subsidies, and the removal of pricecontrols, this led to a massive increase in the price level. This one-timejump in prices should not be confused with an acceleration of inflation. Theprocess of inflation clearly had been checked. While the monthly increase inconsumer prices averaged around 5 percent during the last quarter of 1988, itwas only about 2 percent in the last quarter of 1989. In terms of annualinflation rates, this is a reduction from about 80 percent to 27 percent. Asharp decline of real activity accompanied this process. GDP fell by 8.6percent from 1988 to 1989 (by 9.4 percent if the petroleum sector isexcluded).

lvii. The Policy Change. Towards the end of 1989, and certainly byearly 1990, the restrictive macroeconomic policy was discontinued. When"budgetary deficit" is properly defined, a deterioration of the fiscal stanceof the order of 3 percent of GDP appears in 1990. The turning point fromsurpluses to deficits occurred in early 1990. Not surprisingly, thiscoincided roughly with the changing real exchange rate, which first stabilizedand by the summer of 1990 began steadily to appreciate. The trend in the

- xvii -

norninal money supply (MI) also changed. In the last quarter of 1989, moneyincreased by about 26 percent (an annual rate of 152 percent). During 1990 asa whole, nominal money supply increased by 43 percent, in contrast with a fallof 8 percent during the first three quarters of 1989. The real interest ratepeaked in the last quarter of 1989 and the first quarter of 1990--the onlyextended period in whicl. it was generally positive (within a range of 5-10percent per year). From then on, nominal interest rates have declined whileinflation has not, so that real interest rates generally have been negativeand declining.

lviii. The impact of tle policy change was almost immediate. Inflation,which had been weakening, stabilized at an average monthly rate of around 2percent during the last quarter of 1989 and the first quarter of 1990. Fromthen on it accelerated, moderately, remaining at an average monthly level of 3percent throughout the second half of 1990. During 1991, it was in the rangeof 2.5-3.0 percent. Real activity too responded to the policy change andalmost as fast. GDP, and particularly its private-sector component, startedincreasing in the second quarter of 1990, rising in 1990 as a whole by 5.3percent (3.7 percent without the oil sector) from 1989. Unemployment, whichincreased from 6.9 percent in the second half of 1989 to 10.9 percent in thefirst half of 1990, declined somewhat to 9.5 percent in the second half of1990.

Inherent Macroeconomic Issues

lix. Government Revenues. Aside from oil revenues, derived from thetax on the PDVSA surplus, government revenues are amongst the lowest in theworld, just 5-6 percent of GDP. Essentially, oil revenues have replaceddomestic taxation as a means of financing both current and capitalexpenditures.

lx. A strong case could be made to justify the increase of non-oilrevenues. First, at present levels of oil exports (volume and price), and ofgovernment expenditures, a substantial gap exists between revenues andexpenditures - the latter exceeding the former by some 4-5 percent of GDP.Second, even if such gap had not existed at present, it may be expected in thefuture: given the constraints on oil exports, government revenues may beexpected to rise, as a trend, less than its expenditures. Finally, it mightbe argued that the assignment of oil revenues is inappropriate: that insteadof financing public current expenditures, as they have all throughtout, theyshould have been used to increase the economy's capital stock, whereas publicconsumption services should be financed through taxation. To the extent thatthis argument is accepted, it would call for gradually increased taxation,although probably not to the extent needed for the full replacement of oilrevenues, and a corresponding increase in the assignment of governmentresources for investment; that is, an increase of the government's saving.

lxi. This should not be confused with an increase in the government'sown investment through state enterprises--a direction which the Government ofVenezuela is indeed reversing following its large-scale privatization effort.The increased government saving rather should be directed to Drivate-sector

- xviii -

investment, through the placement of the government's resources in the capitalmarket.

lxii. It is evident that the existing tax structure could yieldsubstantial additional revenue through improved tax administration, theclosing of loopholes, and the reduction of exemptions. Beyond this, there arethree main candidates for raising the level of net taxation: (i) domestic oilprices, which even after they were raised in early 1989, are still among theworld's lowest and contain a large implicied subsidy; (ii) other public-sectorprices, which still imply large subsidies in various government-provided goodsand services, especially electricity and water; (iii) a value-added tax (VAT),a major government objective during the last two years. Altogether, tCesethree changes could yield a revenue of over 5 percent of GDP.

lxiii. Fluctuations in Oil Revenues. Oil revenues are highly volatile,primarily because of changes in oil prices. Ideally, the government shouldadjust its spending to changes in permanent income, rather than to transitorychanges. Failure to behave according to this pattern would lead to twocomplementary scenarios. One is that the government adjusts its spendingcontinuously to the fluctuations in revenues, opening the way to cycles ofinflation and recession. The other is the well-known "ratchet" effect, wheret' e government matches expenditures to increased oil revenues and maintainsthis higher level of spending even when oil revenues fall, thereby creating afiscal deficit or reinforcing an existing one.

lxiv. An oil stabilization fund should be of prime importance foreconomic policy and a vital condition for the long-term maintenance ofmacroeconomic stability. This fund should perform the following functions:(i) it should establish a formulation for identifying the permanent level ofoil revenues for any given year; (ii) each year it should transfer to thegovernment an amount equal to this permanent level; and (iii) it should investany excess after the transfer in foreign exchange, and draw on its foreignassets if there is a deficit.

lxv. Taraets and Instruments of Monetary Policy. The Central Bank hasa potentially inconsistent set of targets: the level of foreign-exchangereserves; the rate of expansion of the money supply; and, often, the nominaland the real rates of exchange. Both the nominal and real rates of interestari also considered targets. Until recently, the Central Bank attempted tocontrol not money supply but the monetary base. In the absence of a portfolioof government bonds, it does not conduct open-market transactions ingovernment paper. The monetary base is thus determined as follows: A netacquisition of foreign exchange is offset to the desired degree by an open-market sale of the Central Bank's own short-term paper (the zero-coupon bond).This practice has serious implications. To the extent that the rate ofinterest on the paper (deflated by the rate of devaluation) is higher than therate of interest on the foreign-exchange holdings, a fiscal liability iscreated. Even more important is that the paper acquired by the public throughthese sales is liquid enough to be a very good substitute for money.

- xix -

lxvi. There should be just one target for monetary policy: the moneysuoplv. As the system's anchor, it would ensure a stable and low rate ofinflation, given appropriate targeting. of course, a stable and low rate ofexpansion of the money supply presupposes the government has no need toborrow.

lxvii. The Central Bank would determine money supply by the use of threeinstruments that affect either the monetary base or the money multiplier:open-market operations; changes in minimum-reserve ratios; and the discountwindow. In principle, the number of such instruments can be increased asinstitutions develop. In conducting open-market operations, the Central Bankcould add transactions in securities other than its own zero-coupon bonds;specifically, PDVSA bonds may be introduced. As a rule, at least some use ofchanges in minimum-reserve ratios as an instrument of controlling money supplywould be beneficial, although not for fine-tuning through continual smallchanges of monetary aggregates. Rediscounting by the Central Bank iscertainly an effective instrument to control the monetary base and the moneysupply, and its recent use bears repetition.

lxviii. Exchanae-Rate Policy. Whether or not the real exchange rateshould be managed is probably the central issue of macroeconomic policy inVenezuela. There is a strong argument to allow the rate to be determinedstrictly by market forces, which would ensure maximum levels of efficiency andproduction and the highest rate of growth. The only factor that might justifyintervention is the predominant role of oil exports. It is conceivable thatbecause of it the allocation of resources to maximize production is notnecessarily compatible with the achievement of long-term growth, and that thespecial nature of the oil industry denies the country the benefits of theexternalities generated by tradable activities.

lxix. This case is not easy to establish. The government will have tomake a policy decision based more on speculation than on information andquantitative analysis. But the important point is that, if the principle ofdiversifying exports is adopted, the real exchange rate would be the bestinstrument of policy implementation. An exchange-rate policy would uniformlyencourage exports as well as import-competing activities, thus ensuringmaximum efficiency.

lxx. Raising the real exchange rate would require creating, orexpanding, an excess of saving over domestic investment by increasing thebudgetary surplus. This surplus would finance an accumulation of foreign-exchange reserves, which in turn would reflect a current-account surpluscreated by the increased real exchange rate. Without an accompanyingbudgetary surplus, any attempt to increase the exchange rate throughintervention in the foreign-exchange market would lead to a rise in thenominal exchange rate, followed shortly by a nearly equivalent rise indomestic prices, with only a very limited impact on the real rate of exchange.

lxxi. However, the unique position of oil revenues in Venezuela'seconomy, leads automaticallv to the creation of a budgetary surplus by an

- xx -

increase in the real exchange rate. This is the essence of the earlierdiscussion of the nature of the stabilization policy of 1989. Since thegovernment, through PDVSA, is the major supplier of foreign exchange, anincrease in the exchange rate yields increased government revenues and anincreased surplus. It is essential for the government to realize that theincrease in revenues should not be a signal for increasing governmentexpenditures. It should be devoted to creating a budgetary surplus if thereal-exchange rate depreciation is to be sustained. Moreover, this surplusshould not be a temporary phenomenon but a Dermanent feature of the budget.

lxxii. The structural changes resulting from such an exchange-ratepolicy would be a higher real exchange rate leading to the diversification ofnon-oil exports and the creation of a current-account surplus. This surpluswould be reflected in the accumulation of investments abroad. This, in turn,would be offset by a reduction of domestic consumption and investment, withinvestment beiag directed in a pattern quite different from what it would h;-vebeen without a change in the real exchange rate.

It STRUCTURAL REFORMS

A. Introduction

1.1 For many years, through 1989, Venezuela followed a po'i.y markedby economic insulation and pervasive government intervention in the country'seconomic life. This policy was reinforced in the mid-1970s by the sharpincrease in oil prices--followed, a short time later, by nationalization ofthe oil industry--and made the government the major investor in the economyand the major owner of the country's productive wealth. However, theavailability of oil did not explain excessive government interference in theprivate sector through regulation, prohibitions, and discriminatory taxationand subsidization. Nor, a fortiori, did it explain the economic insulation(other than in the oil sector), through widespread import restrictionsenforced by prohibitive tariffs, multiple exchange rates, and non-tariffbarriers. These measures originated from a general belief, held in much ofLatin America until recently, that government knows best; and that governmentintervention, rather than private enterprise, will produce desirable outcomes.

1.2 After oil prices collapsed in the early 1980s, many Venezuelansrealized that this model of economic life and development was grosslydeficient. As the growth rate of an economy used to rapid expansion for manyyears declined sharply, they saw that oil bonuses would not suffice to offsetthe consequences of misguided policies. The volume of oil exports wasrelatively constant, and real oil prices could be expected to keep falling.With the debt crisis of 1982, capital inflows, another source of investmentand growth, were reversed.

1.3 Growing numbers of Venezuelans also began to realize themagnitude of waste, inefficiency, and distortion arising from pervasivegovernment intervention in the country's economic life. They were undoubtedlyinfluenced by the accumulating experience of countries, particularly in LatinAmerica, that had discarded intervention in favor of free markets, withbeneficial results. This experience also reinforced the perception that large-scale economic restructuring was necessary to sustain these benefits.

1.4 In 1987-88, Venezuela, for the first time in its postwar history,faced a severe macroeconomic imbalance (which will be discussed in the secondpart of this study). More than once, international experience has shownconvincingly that a macroeconomic crisis, which makes a radical policy changeacceptable to the population and the political organization as a whole, isalso an opportune moment for significant economic transformations unlikely innornal times. It is thus not surprising that in Venezuela these wereintroduced simultaneously with the policy of macroeconomic stabilization.

1.5 This policy was adopted in February 1989, immediately afterPresident Perez took over the administration. Since then, structuraltransformation has been an ongoing process rather than a one-shot operation;

- 2 -

it will therefore be discussed with reference to announced policy directivesand their implementation.

1.6 The policy changes will be analyzed by their nature and byeconomic sector, leading in consequence to some repetition in the discussionthat follows. The next section treats of their nature, under Drivatizationand dereculation and foreign-trade reforms. The section following thatdiscusses their impact on the agriculture, power and energy, infrastructure,financial, and social sectors.

B. Malor Areas of Reform

Privatization

Prior Conditions

1.7 During the 1970s and 19808, successive governments in Venezuelafollowed a development strategy that relied heavily on state control ofproductive sectors. In addition to traditional public services (e.g., water,telephone, electricity), state-owned enterprises (SOEs) dominated manysectors, including petroleum (PDVSA), mining, aluminum, and steel (CVG).Expansion into these sectors was part of an ambitious design t directresources generated by petroleum to maintain artificially low prices for keygoods and services, develop untapped natural resources, and promote importsubstitution and self-sufficiency. It was initiated in the mid-1970s with thenationalization of the oil and iron ore industries, followed by heavy publicinvestment in power, steel, and aluminum. Funus channelled through the Fondode Inversiones de Venezuela (FIV), set up to invest petroleum revenues, wereinitially provided as loans, which, in most cases, have been converted toequity as a result of the inability of the SOEs to repay them. By the end of1989, the FIV had equity totalling roughly US$2 billion (book value athistoric costs) in more than 30 SOEs in mining, electricity, basic industries(steel, aluminum), manufacturing (cement, pulp and paper), shipping, andfinance.

1.8 By the end of the 1980s, there were about 125 commerciallyoriented SOEs in Venezuela in the following groups:

* The petroleum sector, including PDVSA (the state-owned oilcompany) and seven subsidiaries in associated anddownstream activities (e.g., natural gas, petroleumdistribution, fertilizers, petrochemicals)1';

* Twenty financial SOEs, including banks, specialized creditagencies, and insurance companies;

PDVSA also has equity in several downstream joint ventures.

-3-

* Fourteen basic industry and infrastructure enterprisesunder the Corporaci6n Venezolana de Guyana (CVG), includingsteel (SIDOR), aluminum (VENALUM, ALCASA, INTERALUMINA),iron, bauxite and coal mining (FERROMINERA, BAUXIVEN, and

CARBOSUROESTE), hydro-electric generation (EDELCA), andother capital-intensive industry and mining operations;

* Fifteen SOEs providing public services (e.g., electricity,water, ports, telephones); and

* About 70 smaller SOEs operating in a variety of sectors

(e.g., tourism, agro-industry, manufacturing), many of them

created under the now-defunct Corporaci6n Venezolana de

Fomento (CVF), an industrial development agency established

in the 1970s.

1.9 There was little private investment during this period. In 1984-

88, SOEs accounted for 22 percent of GDP, 34 percent of investment, and 5

percent of employment. Excluding PDVSA, SOEs accounted for 6 percent of GDP,

23 percent of investment and 3 percent of employment during this period.

1.10 The adjustment measures undertaken by the P6rez government had an

immediate detrimental impact on many SOEs, particularly those functioning in a

highly protected and distorted environment (e.g., SIDOR). The overall SOE

deficit increased from 0.9 percent of GDP in 1988 to 2.0 percent in 1989.Government transfers to SOEs exceeded US$1 billion (2.5 percent) in 1989. It

was in this context that the new government initiated a broad public

enterprise reform program aimed at: reducing the scope of the public sector

in the economy; reducing the fiscal burden of SOEs; improving the efficiency

of key public services; and adjusting prices of SOE goods and services to

economic levels.

Obiectives, Policies and Targets

1.11 In comparison with the other measures in early 1989, the

privatization program was slower to develop and initially modest in scope. In

mid-1989, the Economic Cabinet approved a broad SOE rationalization strategy,

prepared by CORDIPLAN, that categorized SOEs according to the type of market

(competitive vs. monopolistic) in which they operated and the feasibility of

privatizing them. Privatization in the short term was to be limited to small-

and medium-sized companies in tourism, manufacturing, agro-industry, and

banking. Most of these (eg., cement, sugar) were CVF holdings and many were

bankrupt or operating at very low capacity. They were targeted for several

reasons. There was no justification for maintaining state ownership; there

was no need for major restructuring prior to privatization (in terms of

layoffs, debt repayments, and legal or regulatory changes); and privatization

was not likely to engender much labor or political opposition. The larger

SOEs, which were thought to be more difficult to sell, were expected to be

privatized in a second phase.

-4-

1.12 The initial program covered 70 majority and minority holdings,including 34 hotels and tourist facilities, 3 banks, 6 cement and brickcompanies, 16 agro-industrial holdings (sugar, milk products), 3 textilecompanies, 4 metallurgical firms, and 2 shipyards. Together they accountedfor less than 1 percent of SOE assets (roughly US$300 million out of a totalof US$42.6 billion, including PDVSA)V and slightly over 2 percent of SOEemployees (4,350 out of 186,000).

1.13 In mid-1990, the program was expanded considerably when thegovernment decided to privatize CANTV (the telephone company) and VIASA (theinternational airline). In the case of CANTV, it was recognized that the verypoor quality of telephone service was a significant constraint on thecountry's international competitiveness, and that the expansion andimprovement of service could be achieved only through the sale of acontrolling block to an experienced international company. In the case ofVIASA, the decision was based on its mounting losses and the realization thatthe only way to stop the financial hemorrhaging was to sell the company.

1.14 By the end of 1991, the government had sold its holdings in sevenmajor enterprises: three commercial banks (Italo-Venezolano, Occidental,Republic); VIASA; CANTV; a sugar refinery (El Tocuyo); and a shipy1ard(ASTINAVE). These transactions yielded approximately US$2.2 billion, with thebulk of this amount (US$1.9 billion) coming from the sale of 40 percent ofCANTV'/ to an international consortium led by GTE. In addition to thesesales, the government liquidated the national ports agency (INP), privatizedcargo handling and stevedoring, and transferred responsibility foradministering the ports to new regional port authorities. Similarprivatization initiatives are underway in housing (INAVI) and in trashcollection (IMAU).

1.15 During 1992, the government expected to privatize the followingenterprises: (a) fifteen hotels, in three separate bidding packages; (b) fiveout of the six remaining state-owned sugar refineries; (c) the domesticairline (AEROPOSTAL); (d) the Caracas water and sewerage system (through aconcession contract with a private operator); (e) the racetracks (INH);(f) the Caracas cable car and associated Humboldt Hotel; (g) the saltrefineries (ENSAL); (h) a Caracas entertainment park (Poliedro); (i) somesmall CVG and CVF holdings in the cement, metallurgical, textile and dairyindustries; and (j) three regional electricity companies (ENELVEN, ENELBAR andENELCO). The successful privatization of these companies is dependent uponthe establishment of an appropriate regulatory framework for the sector.

2/ SOE data for 1987 (most recent complete year available) showtotal assets (historical cost) of Bs618 billion, or US$42.6 billion equivalentat the then-official exchange rate of Bsl4.5/US$. PDVSA accounted for US$12.3billion equivalent of this total.

3/ Forty percent of the common shares, but with control of the Boardof Directors. In addition, 11 percent was sold to CANTV employees. Thegovernment has retained 49 pes cent, but expects to sell this later via publicshare issues.

1.16 An interministerial commission was established by decree in July1989 to oversee privatization. It is chaired by the FIV President(ministerial ranking) and includes the Ministers of Planning, Finance, andDevelopment (Fomento), as well as representatives of the Confederation ofLabor (CTV) and the Chamber of Commerce (FEDECAMARAS). The FIV acts assecretariat to the commission and manages the program. A new law passed byCongress in Devember 1991 formally transforms the FIV into the government'sprivatUation and restructuring agency and calls for the phased elimination ofgovernt'ent transfers to the FIV.W In addition to the FIV Law, Congressrecently passed a Privatization Law formalizing the policies andimplementation procedures for the program.

1.17 The FIV has a well-developed process for preparing andimplementing privatization, which includes the following steps: an initialdiagnostic analysis of the company and the sector; design of a sales strategy;valuation; preparation of a sales memorandum or prospectus (for a public shareissue); pre-qualification of potential bidders; and the public tender or shareoffering. Consulting firms and investment banks are hired for the technicalwork. Virtually all of the privatizations to date have been via sealed bidsthat are opened in public. All transactions have been on a cash basis (i.e.,no debt-equity swaps or installment payments). The major transactions havealso included employee share ownership programs.

Lessons and Issues

1.18 Several lessons can be drawn from the privatization experience todate:

* privatization has been most rapid inthose enterprises where new managementwas brought in to implement the changes(e.g., CANTV, VIASA and INP);

* consensus with the political parties and labor unions isimportant. In this context, FIV management indicated thathaving labor and business representatives on theprivatization commission ensures that all issues arediscussed at an early stage; and

* in more complex cases, privatization needs to beaccompanied by broader reform of the sector to ensurecompetition and economic efficiency (see infrastructurechapter ir paras. 1.111, 1.112 and 1.114 for a discussion

4/ Under the original legislation that created it, the FIV receives5 percent of the government's petroleum revenue. Under the new law, this willbe phased out as follows: 3 percent in 1992, 2 percent in 1993, 1 percent in1994, and zero thereafter.

-6-

of competition issues in the telecommunications and portssectors).

1.19 Two issues have emerged at this stage: the scope and directionof the program for the medium term; and the handling of redundant labor.

(i) ScoRe. The successful privatization of CANTV has generatedpublic support and foreign investor interest in theprogram, making this an opportune time for the governmentto consider privatizing CVG's industrial and mining SOEs(e.g., SIDOR, ALCASA). This would confirm the government'sintent to reduce public sector participation in productionactivities (where direct ownership no longer serves anypublic policy objectives), provide the needed capital forsector expansion, and eliminate government support, eitherdirectly (through loans, equity, or transfers) orindirectly (through loan guarantees), for these companies'ambitious investment programs. It would also improveefficiency and performance through the introduction ofprivate management and shareholders.

The phased privatization of PDVSA and its subsidiariescoulz' also be considered, though this would clearly be morecontentious and would also face constitutionalrestrictions. The example of Petro-Canada may beinstructive. The Canadian Government initiated a phasedprogram to privatize Petro-Canada via a series of publicshare issues, giving Canadian citizens the feeling that theCanadian public owns Petro-Canada. A similar strategy maybe possible for PVDSA.

(ii) Labor. Although more than 20,000 workers have been laidoff in SOE restructurings and liquidations (e.g., ports),there have been no workforce reductions prior to the saleof companies being privatized. Most sales have requiredthe new owners to honor existing collective contracts.While this strategy has bought labor peace for theprivatization, it may lead to future labor strife when thenew owners seek to shed excess labor. Labor problems havealready arisen in VIASA (a pilots' strike in December 1991)and, to a lesser degree, in CANTV (a threatened sympathystrike). The government's position has generally been thatthe problem of excess labor (of which bidders were fullyaware) is better handled by the private sector.

Forei$n-Trade Reforms

Prior Conditions

(a) Foreion Exchange Controls and Import Barriers

1.20 A pervasive system of non-tariff barriers reinforcing a highlevel of tariffs had served as the effective constraint on imports prior tothe reform.

1.21 From 1973 to February 1983, Venezuela maintained a fixed exchangerate of 4.3 bolivars to the U.S. dollar that increasingly overvalued thebolivar. Early in 1983, a series of currency crises was resolved byintroducing the multiple exchange rate system that prevailed through early1989. Initially, an exchar.ge rate of 4.3 Be. per U.S. dollar was set for thepetroleum sector, essential imports, and foreign debt service; an officialrate of 6.0 Bs. applied to most commercial transactions; and a free marketrate applied to nontraditional exports, tourism, and capital transfers. Theofficial rate was raised to 7.5 Bs. in March .;984 and to 14.5 Bs. in December1986, and there were numerous shifts of items among categories. At one pointthe system included four rates: 4.3 Bs. for foreign debt; a 6.0 preferentialrate; the 7.5 official rate; and the free market rate. From 1984-88, the freemarket rate ranged from 60 percent to 200 percent above the official rate,averaging 110 percent. In February 1989, the multiple rates were unified andthe exchange rate was floated.

1.22 For most items, a potential importer had first to obtain animport permit from the Development or the Agricultural Ministry that would begranted only if domestic producers did not object. Since tariffs wereprohibitive, the importer had to apply for the tariff to be reduced to areasonable level.

1.23 Importers had then to apply on a case-by-case basis to the Officeof the Differential Exchange Rate Regime (Oficina del R6gimen de CambiosDiferenciales, RECADI) or its successor organization (commonly called ex-RECADI). The procedures changed frequently, there were no clear criteria fordecisions and the priorities were general: (1) food and medicines; (2) rawmaterials; (3) intermediate goods and CKD kits; (4) capital goods; and (5) allothers.

1.24 From 1983-88, the most heavily subsidized commodities through theexchange rate were food and raw materials, and the most heavily taxed wereconsumer goods--particularly luxuries--and alcoholic beverages. Capital goodsand transportation equipment were taxed about equally. This pattern of taxingconsumer goods and subsidizing inputs was intended to protect domesticproduction. Industry was given greater protection than agriculture, but bothagricultural inputs and food imports entered at favorable rates, so thateffective protection was generally minimal and, in cases, could even have beennegative. For example, in 1984 and 1985, agricultural inputs entered at anaverage exchange rate of 5.0 Bs. and 6.2 Bs. and basic foods at 4.6 Bs. and5.2 Bs., respectively.

1.25 It is difficult to estimate the benefits rendered by RECADI fromexisting data, but it is clear that they were large. For all imports, thebenefits averaged nearly 15 percent of GDP; and for the imports where RECADIexerted the greatest discretion, benefits averaged 6 percent of GDP. Whilethe government's goal was to reduce consumer prices, the benefits may actually

- 8 -

have gone to importers, distributors, or domestic producers. The market pricefor any given item could have been determined by the exchange rate, thelicense, a reduced tariff, or price control.