Value to Outcomes (V2O) in Oncology Drug...

24

© Copyright 2014 Quintiles ™ Value to Outcomes (V2O) in Oncology Drug Development Dr. John J. Doyle June 17, 2016

Transcript of Value to Outcomes (V2O) in Oncology Drug...

© Copyright 2014 Quintiles

™

Value to Outcomes (V2O) in Oncology Drug

Development

Dr. John J. Doyle

June 17, 2016

2

Pharmaceutical companies are making remarkable

investments in cancer research

Source: Lloyd. Citeline Pharma R&D annual review 2015 - PharmaProject Jan 2015

Number of pipeline products in R&D

3

For example, the PD-1/PD-L1 pipeline is intensely

competitive across major oncology markets

Atezolizumab

(28 trials)Launch 2017

Keytruda

(43 trials)

MEDI-4736

(23 trials)Launch 2017

Opdivo

(42 trials)

5 trials

1 trial

There are 143 oncology trials spanning 23 markets and 39 trials are phase III

Phase I-III trials for PD-1 and PD-L1Bla

dder

Bra

inBre

ast

Cer

vica

lC

olor

ecta

lG

astric

Hea

d and

Nec

k H

emat

olo

gic

Hep

atoce

llula

r

Hod

gkin

's L

ymph

oma

Mel

anom

aM

esot

helio

ma

Mul

tiple

Mye

lom

a

Non

-Hod

gkin

's L

ymph

oma

Non

-Sm

all C

ell Lun

g

Oth

er (S

olid

Tum

ors)

Ova

rian

Pan

crea

ticPro

stat

eR

enal

Cel

lSar

com

aSm

all C

ell L

ung

Source: BioMedTracker September 2015, Quintiles Analysis

4

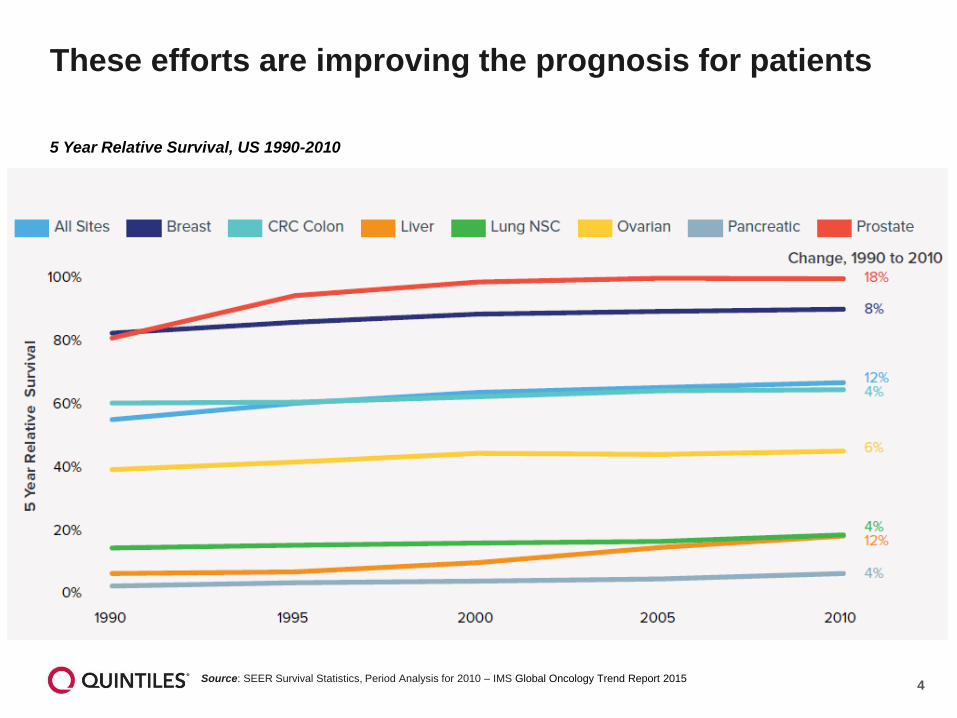

These efforts are improving the prognosis for patients

5 Year Relative Survival, US 1990-2010

Source: SEER Survival Statistics, Period Analysis for 2010 – IMS Global Oncology Trend Report 2015

5

… but this innovation comes at a price that places a

strain on health care budgets

Worldwide Prescription Drug & OTC Sales, by therapeutic area

79.2

153.1

0

200

400

600

800

1000

1200

2014 2020E

Oncology

Anti-diabetics

Anti-rheumatics

Anti-virals

Vaccines

Bronchodilators

Sensory Organs

Anti-hypertensives

MS therapies

Immunosuppressants

Anti-coagulants

Dermatologicals

Anti-hyperlipidaemics

Anti-fibrinolytics

Anti-bacterials

Other

$ B

illi

on

CAGR

+ 11.6%

781

1,029

6

Especially in the US, cancer drug prices have been

rising steadily

Monthly and median costs of cancer drugs at the time of FDA approval, 1965-2015

Source: Peter B Bach, MD Memorial Sloan-Kettering Cancer Center – Available from:

https://www.mskcc.org/research-areas/programs-centers/health-policy-outcomes/cost-drugs

7

There is a bright spotlight on value

8

Prices have been criticized not only by payers, but also

by oncologists

9

How do we solve for value in cancer care?

10

• No unmet need implies no value unless the aim is to drive cost reduction

How do we define and measure unmet need?

• Improved health outcomes, reduced mortality, reduced cost

What is the consequence of addressing the unmet need?

• Clinically meaningful improvement of outcomes in a defined patient population vs an appropriate comparator

How good is this intervention at addressing the unmet

need ?

• Does uncertainty detract from the valueHow good is our evidence of this?

• Does the value of this improved performance match the increased cost? (product price less cost offsets)

• Different health systems take different approaches to value

How do we value the improved

outcomes?

• How does the value translate into price?$

The Value Cascade

11

Value-based assessment frameworks have emerged as

a means to appraise oncology products to control costs

US based Frameworks

EU based Frameworks

ASCO framework to

assess the value of cancer

treatment optionsNCCN Evidence Blocks

Value-based pricing

calculations based on 6

modifiable components using

web-based tool DrugAbacus

Combines a long-term

perspective on value

through CE analyses with

short-term affordability

considerations

The European Society for Medical

Oncology Magnitude of Clinical

Benefit Scale ESMO-MCBS

NHS Cancer Drug Fund

(UK)

NVMO PASKWIL Criteria

(Netherlands)

12

12

InHealth

Historical Evolution of Drug Evaluation in the US

1970 1980 1990 2000

Congress

establishes Office of

Technology

Assessment (OTA)

1972Congress

budget decision

closes OTA

1995

OTA Health

Policy staff

focuses on need

for HTA

RAND call for health

quality measures and

clinical effectiveness

guidelines

Oregon EPC

formed

1997

Network of 14 states

form DERP

AHRQ (Agency

for Healthcare

Research and

Quality)

established

1989

AHRQ Evidence-

based Practice

Centers (EPCs)

established

1997

John M. Eisenberg

Center established

2005

Tech.

Assess-

ment

group

1990

DEcIDE

1992

2003Blue Cross Blue Shield

Association establishes

Technology Evaluation

Center (BCBSA TEC)

1985

Named AHRQ EPC

1997

Kaiser

Permanente

collaboration

1993

1985

1997

Begins HTA; WHO Collaboration

Center

1982

Named AHRQ EPCECRI Institute

established

1968

Designated

CMS advisor

2003

HTAIS HTA database

1993

ICSI

1993

Hayes

Inc.

19942003

Consumer Reports

Best Buy Drugs

2004

United

Biosource

VA TAP

Source: US Federation Scientists OTA Archive; Agency websites; Company

websites; NPC report “Current Evidence Based Medicine Landscape

Government

Select Evidence Based Practice Center (EPC)

Select Private

13

Other countries struggle to determine how to value drugs

• UK undertook a process to

redefine drug price methodology

for PPRS

• VBP (Pricing)

• Renamed VBA (Assessment)

• Initiative failed last year due to

debate over how to measure value

• Issues over differential value for

different people

• Arbitrary “multiplier” for Burden of

Illness and Wider Social Impacts

not justifiable according to critics

14

Value framework implicaitons for drug manufacturers

Clinical Trial Design

• Certain outcomes

(e.g., OS) are

valued more

highly than others

(e.g., Response

Rate)

• NCCN and

DrugAbacus have

metrics for data

quality and

consistency

(multiple trials are

preferred over one

larger trial)

Payer Access

• Major payers (e.g.,

Aetna) have

acknowledged the

potential utility of

value-based

frameworks for

coverage decisions

• Power shifts to

Pharmacy Benefits

Managers and

Accountable Care

Organizations have

placed a premium

on specialty drug

value

Pricing Strategy

• Preliminary and

interim clinical

data will indicate

outputs from

value-based

frameworks

• Increased

scrutiny on drug

prices may lead

to the use of

value-based

frameworks as

guideposts for

drug costs

Provider Usage

• Oncologists have

expressed

discomfort with

discussing the

cost or value of

treatments with

patients

• Providers will rely

on manufacturers

to contextualize

value outputs in

a way that is

useful for patients

15

The healthcare system is moving from volume to value

…. to outcomes.

16

The Healthcare System is migrating from volume to

value … to outcomes (V2O)

Payer & HTA

• Balance of quality and

cost

• Evidence-based care

• Provision of appropriate

care to appropriate

populations

• Balancing care across

the population

Policymaker

• Balance of quality and cost

• Societal considerations

• Health system statutes

and guidelines

Rx & Dx

Manufacturer

• Incentives to develop

evidence

• Reimbursement

commensurate

with value

• Return on investment

• Reward for innovation

Provider & Hospital

• Provision of appropriate care

• Provision of reimbursed

services

• Financial efficiency & viability

• Managing with a budget

Laboratory

• Better, faster, cheaper

• Staff resource requirements and

turn around

• Managing with a budget

Patient

• Need to maintain health

• Benefit/risk tradeoffs

• Affordability of care

V2O

Healthcare

System

17

Market / Patient

AccessDrug/Device

Candidates

Industry Regulators Payers Physicians Patients

• Evaluate evidence

• Advance science

• Improve care

• Ensure continued reimbursement

• Generate publications

• Improve patient outcomes

• Prove value

• Secure coverage and reimbursement

• Enhance understandingof unmet patient needs

• Explore new indications

• Delineate risk-benefit profile

• Detect safety signals

• Ensure long-term safety and effectiveness

• Appraise value for coverage and reimbursement decisions

• Monitor usage within criteria

• Evaluate comparative- and cost-effectiveness

• My own health—what choicesdo I have?

• What are the risks/benefits?

• Which treatmentwill improve my quality of life?

• Which treatmentis safer, more convenient and affordable?

Different stakeholders have various views on risks,

benefits and value

18

Risk-benefit analysis is also becoming personal

PERSONALIZATION

OF CAREMINDING THE

(SYSTEM) GAPS

RISING TIDE OF

CONSUMERISMDEMOCRATIZATION

OF CARE

19

How do we integrate RWE in cancer drug development

development?

20

Launch Pricing

Review

New

Competition

New

Formulation/

Indication

Competitor

Goes Generic

Development Growth Phase Mature Phase

Understand

standard of care

Trial design

Patient recruitment

Unmet need/

disease burden

Budget Impact

Post marketing

commitments

(safety, etc)

Adherence

Utilization/

prescribing

patterns

Long-term

clinical

outcomes

Head to head

comparative

effectiveness

Differentiation in sub-

populations

Target populations Differentiate with or vs.

protected formulation

Effect of switching

on outcomes

Usage

Difference

Evidence

Required

Now Past

Source: Ref. modified from EMA Adaptive Pathways Pilot Presentation at STAMP

http://www.ema.europa.eu/docs/en_GB/document_library/Presentation/2015/11/WC500196727.pdf

Real-world evidence plays an increasing role across the

product lifecycle

Incorporate real-world data needs earlier in the R&D process

- Confidential -

21

RWE can be generated through a variety of study

designs

Retrospective Research

Enriched Retrospective

Observational Prospective

Studies

Enriched Prospective

Studies

Pragmatic

RCTs

Evidence Development Options

Disease registries established

early to investigate real-world

practice patterns and outcomes

RWE databases evaluated to

characterize treatment patterns and

clinical disease patterns; also useful

for informing prospective study

design features

Enriched studies

designed with

experimental and

observational elements

to track real-time risk-

benefit and spawn

further research

Minimally

interventional

trials designed to

include more

representative

populations,

comparators and

endpoints

predicted for

product use

Enriched retrospective studies

conducted to strengthen

secondary data analyses with

information from patients and

clinicians

22

PragmaticDatabase & Hybrid Registries

Changing real world research evidentiary landscape

Explanatory trials (RCT)

Pragmatic Ph IV trials

• High external validity

• Large sample size

• Simple design

• Diverse settings

• Real world late

phase operations • High internal validity

• Smaller sample size

• Sophisticated design

• Controlled environment

Cost/Time Sensitive Approaches

23

PreclinicalClinical Development

Phase I Phase II Phase III

Regulatory

Submission

Real World & Late Phase Research Services

Product Development Services

PRODUCT DECISION

Evidence for Regulators, Providers, Payers, Patients

BioPharma PayersRegulators Providers Patients

Phase IIIB/IV

Healthcare Delivery

REIMBURSEMENT

APPROVAL

Early evidence for better outcomes

Engage Early

24

Reduce Costs

Effic

iency

Effectiveness

Eco

no

mic

s

Equity

System Levers

Healthcare System Goals

What

SuccessLooks

Like

Improve

Population

Outcomes

Enhance

Patient

Experience