Value stream in lean accounting and beyond budgeting...

81

Master Thesis Value stream in lean accounting and beyond budgeting Supervisor: Steen Nielsen Aarhus University – Aarhus School of Business Management Accounting and Controlling By Dinghao Wang 1/7/2012

Transcript of Value stream in lean accounting and beyond budgeting...

Master Thesis

Value stream in lean accounting and beyond budgeting

Supervisor: Steen Nielsen

Aarhus University – Aarhus School of Business

Management Accounting and Controlling

By Dinghao Wang

1/7/2012

Page 1 of 80

Table of Contents

Acknowledgements ........................................................................................................ 3

Abstract .......................................................................................................................... 4

1. Introduction ............................................................................................................ 5

Problem formulation .............................................................................................. 7

What is the difference between Value stream and beyond budgeting in continue

improvement and value creation? ......................................................................... 7

2. Value stream ........................................................................................................... 8

The reasonable factors of value stream ................................................................. 8

2.1 Managing by value stream ..................................................................................... 10

2.1.1 Financial accounting............................................................................................ 10

Account payable ................................................................................................... 10

Accounts receivable ............................................................................................. 11

2.1.2 Operational accounting ....................................................................................... 12

2.1.3Management accounting ..................................................................................... 13

Alignment of lean goals ....................................................................................... 13

Performance measures ........................................................................................ 14

Budgeting and planning ....................................................................................... 15

Managing product profitability ............................................................................ 16

2.1.4 Support for lean transformation ......................................................................... 17

Role of finance people ......................................................................................... 17

Continuous improvement .................................................................................... 17

Empowerment and learning ................................................................................ 18

2.1.5 Lean business management................................................................................ 18

Customer value and target costing ...................................................................... 18

Sub - Conclusion ........................................................................................................... 19

3 Beyond budgeting ..................................................................................................... 20

The reasonable factors of beyond budgeting ...................................................... 20

3.1 Six principle of managing with adaptive process ................................................... 24

3.1.1 Target setting ................................................................................................... 25

3.1.2 Motivation and rewards ...................................................................................... 26

3.1.3Strategy process ................................................................................................... 27

Output .................................................................................................................. 28

Input ..................................................................................................................... 29

Control.................................................................................................................. 29

Resource ............................................................................................................... 29

Performance review process ................................................................................ 29

3.1.4 Resources management ...................................................................................... 30

3.1.5 Coordination ....................................................................................................... 30

3.1.6 Measurement and control .................................................................................. 31

Sub - Conclusion ........................................................................................................... 31

Page 2 of 80

4. Case discussion ..................................................................................................... 32

Case description ................................................................................................... 32

5. The object of value stream ................................................................................... 34

5.1 Financial accounting ............................................................................................... 36

5.2 Operational accounting .......................................................................................... 37

5.3 Management accounting ....................................................................................... 38

Alignment goals in lean and performance measurement ................................... 38

Budgeting and planning ....................................................................................... 40

Managing product profitability ............................................................................ 41

5.4 Support for lean transformation ............................................................................ 41

The role of employees ......................................................................................... 41

Continuous improvement .................................................................................... 42

Empowerment and learning ................................................................................ 43

5.5 Lean business management ................................................................................... 44

Customer value and target costing ...................................................................... 44

Sub - Conclusion ........................................................................................................... 45

6. The budgeting problem ......................................................................................... 46

6.1 Targets setting ........................................................................................................ 47

6.2 Motivation and rewards ......................................................................................... 48

6.3 Strategy process ..................................................................................................... 49

Output .................................................................................................................. 50

Input ..................................................................................................................... 50

Resource ............................................................................................................... 50

Control.................................................................................................................. 52

6.4 Resources management ......................................................................................... 52

6.5 Coordination .......................................................................................................... 53

6.6 Measurement and Control ..................................................................................... 54

Sub - Conclusion ........................................................................................................... 55

7. Compare two methods ......................................................................................... 56

8. Conclusion ............................................................................................................. 60

Reference ..................................................................................................................... 62

Appendix ...................................................................................................................... 63

A ........................................................................................................................... 63

Value stream mapping ......................................................................................... 63

Box score .............................................................................................................. 65

B ........................................................................................................................... 66

Six leadership process .......................................................................................... 66

Case MosCo Inc .................................................................................................... 67

Page 3 of 80

Acknowledgements

I would like to acknowledge the cooperation and support from Aarhus school of

business. And I am sincere gratitude and appreciation to my dedicated supervisors

Steen Nielsen.

Steen Nielsen provided me infinite support and encourages and also guided me to

learn more knowledge and kept me on the right way in my thesis.

I express my appreciation to all my friends and my partner’s encouragement and

support, Keld Christensen, Hongyi Niu and Li Ma, for all their patience and sacrifice

they gave while I spend hundreds of hours working on my thesis. Thank you so much.

Last but not at least, I am sincere thanks to my parents, for their fully support on my

education. And thanks again to my parents and partner that gave me a comfort

environment when I was sick during the thesis.

Page 4 of 80

Abstract

The objective of this thesis is to provide a descriptive and explanative study of lean

value stream and beyond budgeting in MosCo. Meanwhile, give suggestions about

how to continuous improvement performance in both theories. In the end, compare

lean value stream and beyond budgeting, to figure out which the best concept in

future development. MosCo Inc produced x100 CPU for the subsidiary company,

which is not satisfy about price of x100, and asked MosCo to give a competitive price

for sell. In the same time, MosCo had big challenges then a new market opened to sell

x100, x50 and introduced a new product on the market; x75. The problem is financial

department gave a really disappointing two years budget. In order to find a way to

solve the MosCo’s problem and based on the objective presented above; a qualitative

analysis will be conducted from a case study approach.

By doing qualitative study, the major problem is about how should MosCo continuous

improve performance and meanwhile create valuation in lean value stream and

beyond budgeting. So before to start the case discussion, MosCo have an open mind

and willing to decentralization the organization and lean behavior.

The major contents of this thesis are organized as: applying value stream and six

process principles of beyond budgeting model into the MosCo management level to

identify the adjustments when decentralizes decision.

Keywords: value stream, six process principle model, MosCo, operational,

measurement, encourage, resource and decentralization

Page 5 of 80

1. Introduction

In this thesis, I will compare value stream in lean accounting and beyond budgeting.

According to compare the two methods, to display how these two methods were

difference as traditional methods, and realize which will be the better method to solve

problems and performance in the business at the same condition.

Lean management and beyond budgeting started in the 1990s, because of the business

developing and business environment changed fast, more and more companies need

new methods to fit the business changing. At moment, the marketing and organization

needed new methods to improve the business conditions and more competitive in the

business, therefore these two methods came out to the business market. Actually this

is about the performance measurement from two new different ways, and they will be

more efficient by the factory producing and company organizing with developing.

The lean management is to provide a roadmap of lean thinking and lean behavior for

company, to realize finance and control systems are wasteful and ineffective. It’s a

new method of managing a business that is built by lean principle and lean methods,

and these methods will inspire company managers of lean financial thinkers and

doers1.

Lean accounting not only helps company to save financial, performance on product

but also helping the employees understand more information of the company. In

general case, lean management will have two parts: lean manufacturing and lean

accounting, but in this project I will tend to discuss lean accounting value stream. The

value stream management is very different ways of running the business, the position

of managers have to work on the value stream revenue growing, eliminating waste,

1 Maskell & Baggaley, 2003

Page 6 of 80

creating more customer value and make better economy for the company, and frees up

the people to do useful, lean continues improvement, and less misleading information.

The features of lean accounting (Maskell & Baggaley, 2003, P1)

Provides information for better lean decision making.

Reduces times, cost, and waste by eliminating wasteful transactions and systems.

Identifies the potential financial benefits of lean improvement initiatives and

focus on the strategy requires realized the benefits

Motivate long term lean improvement

Support better transformation both from supplier and to customer

Encourage company focus on customer value measurement

The beyond budgeting is to increase the adaptability of enterprises. For this, manager

or controller has to conceive and implement the required control instruments and

processes. It is not only describing performance management and controlling

processes that support a management concept but also the required new leadership

principles.2

The feature of beyond budgeting (Jürgen H. Daum, beyond budgeting model):

Create a performance management measure in both external and internal factors

Motivate through challenge and transfer responsibility within a clearly identify of

organization values

Notice who take the responsibility and make the decision in the operational

process

Based on customer order and needs, manager or collector responsible for satisfied

and profitable customers

Create an open board of information system

Beyond budgeting was a totally different as traditional budget, it ignored the limited

of the number budget, out of the annual budget changed by the season or month

budget, and changed centralization organization to decentralization organization these

make the beyond budgeting more suitable, inflexible and effective with the business

environments at present. It is a multiply level control, at coherent set of alternative

process to support continuous planning, demand resource, Dynamic Corporation in

2 Hope & Fraser , 2003

Page 7 of 80

the organization target and rewards. I will go through the value creation in beyond

budget which suggest providing a simple, low cost and more relevant alternatives

budgeting in developing.

Problem formulation

In this thesis I want to answer following questions:

What is the difference between Value stream and beyond

budgeting in continue improvement and value creation?

What is the value stream behavior in the continuous improvement and value

creation?

What is the beyond budgeting behavior in continuous improvement and value

creation?

How should value stream and beyond budgeting be used in the case discussion?

How does MosCo use the value stream to improve performance?

How does MosCo use the beyond budgeting to improve performance?

Through those questions, I want to make a clear and reasonable analysis and

discussion in value stream and beyond budgeting, as an organization value stream in

lean accounting and beyond budgeting moves from mass production to lean

manufacturing or centralization to decentralization model, the accounting, budgeting,

and control and measurement systems need to change. Traditional systems are based

on the rules and principles of production, it was restricted organization developing

and effective works but lean accounting and beyond budgeting present a simple,

easily understanding by everybody and an alternative, coherent management model

that enables companies to manage performance through processes specifically tailored

to today’s volatile marketplace.

Page 8 of 80

2. Value stream

The reasonable factors of value stream

It’s very important to have lean thinking before to start the value stream Woman &

Jones (lean think, 2003, P256) mentioned:

‘As you get the kink out of your physical production, order-taking and product

development, it will become obvious that recognizing by value stream is the best way

to sustain your achievement.’

Lean thinking gives an idea of how the organization can create more value for

customer and get more benefits for the organization. Thus, the primary importance

idea is the focusing, which one focus in the whole process of product, from the

customer order to the end of delivery, the function of value stream is to maintain the

focusing in the process. This is also why Womack and Jones (2005, lean solution,

preface) mentioned about lean consumption and lean provision3.

‘It’s not brilliant product innovations or culture or a weak currency or strong

government support that makes this company stands out in global competition. It is

the brilliant focus on core process.’

There is another way to describe value steam, which is simplifying the way of works.

This is not only because the people know how to work, but also because it can

simplify the performance and the reports.

Value stream monitor the execution of process that needs value stream team manager

to coordinate in whole organization. In short term all department needs to corporate

and in long term it uses cross training to bridge the gaps. Managers take the full

responsibility in operation value stream and leadership of employee within the values

stream.

3 Appendix A

Page 9 of 80

Stage of lean manufacturing (Maskell & Baggaley, 2003, P101)

Pilot cells, lean manufacturing and lean thought out, these three steps show value

stream team how it starts at control and improvement. In this case, the value stream

people’s mindset, size of value stream and which value stream should be considered

in the whole process.

It is better to start at the most significant value stream for organization in the early

stages. To fully understand what happens with organization and what customers’

needs, it is through the collection of information. Furthermore to consider which

people should be right use in value stream, and start at easy and simple of value

stream from customer to the end of delivery in the organization.

In brief, lean manufacturing and lean accounting is that lean manufacturing is tools

and lean accounting is methods. They are support lean principles. Other way is lean

manufacturing is prerequisite, lean accounting is outcome.

‘The traditional accounting methods are harmful to Lean manufacturing because they

lead people to make decisions that are contrary to Lean thinking and the systems

themselves are very wasteful. Lean Accounting is a great deal more than just applying

lean thinking to bookkeeping. Lean Accounting answers the question; "How do we

measure, manage, and control a Lean operation?”’ 4

4 http://www.productivityinc.com/workshops/lean_accounting.shtml

Page 10 of 80

2.1 Managing by value stream

Value stream gives a win-win situation to all over the organization and consumer, it

brings better economics to the organization and another side it brings more value to

consumer.

Value stream fully consideration structure ( Maskell & Baggaley, 2003, XVII)

Value stream represents in those factors:

- Financial accounting

- Operational accounting

- Management accounting

Alignment of lean goals

Performance measures

Budgeting and planning

Managing product profitability

- Support of lean transformation

Role of finance people

Continuous improvement

Empowerment and learning

- Lean business management

Customer value and target costing

Rewards and reorganization

This thesis will follow this structure to discuss and analyze value stream in general

situation.

2.1.1 Financial accounting

It will follow the process to reduce the transactions processed in accounts payable,

and accounts receivable. ( Maskell & Baggaley, 2003, P217)

Account payable

Based on supplier used by Kanban system to deliver directly to product line, what and

how much has been used in production. Value stream concept in here that is reducing

Page 11 of 80

the product lead time uses less than before and keep a low level, it start from the

receipt of materials to completion and shipment of the product to customers.

These three processes behave the account payable process. How should organization

eliminate and authorize the payment at receiving. The idea about them is that, if

organization started to order materials until supplier gave invoice, during this section

to eliminate the purchase order, receiver, and invoice multiply costs.

The gradual improvement between traditional and value stream function is that

suppliers control, master purchase agreement and invoices elimination.

Accounts receivable

The objective is rapidity changes the flow of cash receipts from the sales of

production and services. ( Maskell & Baggaley, 2003, P218) The traditional think in

account receivable that is to create and submit invoice to customer, the idea of value

stream in here, it is to eliminate the need for the account receivable, this need to

motivate customer to have more responsibility to pay on time, then organization use

bank information to check the payment. Thus save to create an additional transaction

for the invoice.

receiver

invoice

purchase order

Page 12 of 80

2.1.2 Operational accounting5

Traditional accounting Value stream management

Labor tracking Value add by operation code

Up-to-date information

Track labor hours

Spend cost on manage

materials and stockroom

Exception based reporting

minimized to labor law

requirements

Product within MRP6

system

Accurate labor routing

Standard work

Eliminate the work order

Materials costs Up-to-date information

Multiply suppliers chain

Stock lots of materials

Product within MRP system

Accurate bills of materials

Reduce suppliers number

Increase the quality number

of suppliers

Eliminate work order and

standard costing

Inventory tracking Keep materials in the

stockroom before produce

Keep production in

stockroom before sell to

customer

Perpetual inventory system

and standard costing to

value inventory

Inventories are minimized

No stockroom transactions

Stock in delivered to point of

customer

Eliminate the transaction

costs

In tradition accounting, work order take fully charge on Labor tracking, material costs

and inventory tracking, but in lean accounting, pull system can eliminate the non-

necessary costs from materials and labor and minimize the inventory in production.

And Kanban gives visible explanations to control operational accounting and respond

that pull system processes are based on customer demand.

5 Maskell & Baggaley, 2003

6 Materials requirements planning

Page 13 of 80

2.1.3Management accounting

Alignment of lean goals

In lean accounting, goal alignment is that, in the organization from top management

to sales management, all the managers should meet together and discuss the strategy

goals and plan how to support it, and to know which part of strategy goals most

important to focus, after that each department managers need meet the staff to tell

them how to execute the strategy goals. Bottom of line, sales manager is the platform

to meet organization goals and business needs.

Figure of value stream goals ( Maskell & Baggaley, 2003, P294 & P296)

Value stream in the lean performance measurement is the core factors to be

continuous in the whole strategy. The strategy goals relative to the value stream and

value stream is the reason to achieve those goals.

- Name list value stream within business units (depending on which business)

- Select primary value stream to work

- Define the value stream concept and mapping7

- Discus which factors should focus on value stream

The goals of the value stream measure the effectiveness of critical success factors and

7 Appendix value stream mapping

Page 14 of 80

these factors are driven by the lean principles. (The next Figure) 8

Performance measures

The performance measurement of lean is to make sure all the processes are exactly

following the expectation of strategy goals, and value stream performance is to

initiate continuous improvement and create more benefit in the organization. The

significant represent is drawing a value stream map9, which clearly to identify the

detail in the value stream process, and the purpose is to eliminate the waste and to

require increasing the value for customer and money earn.

Some measurements are similar as lean value stream measurement, in most of the

case, they measure by the whole production plant, and then to access the capability of

production plant. In lean value stream, it is not measuring the judgments of

production plant to initiate continues improvements (CI).

It is better to give few measurements to focus and motivate continuous lean

improvements. (Box Scores, it is updated weekly with recently information, such as

financial and operational information.) For example ( Maskell & Baggaley, 2003,

P117-P124)

8 Maskell & Baggaley, 2003

9 Appendix value stream mapping

Value stream

Value stream target

specific value stream results to achieve the

strategy goals

definate the target and time

Value stream measure measure the

attainment of value stream

Page 15 of 80

Value stream measurement

- Sales per person, to know sales and number of people involved

- On time delivery, shipment to customer and measure level of control

- Dock to dock time, use inventory information10

/shipment per hour to measure

- First time though, measure process capability, highlight the level control in CI

- Average cost per unit, indicate of improvement in value stream process

- Account receivable days outstanding, cash flow 11

Budgeting and planning

A monthly formal procedure operate value stream in an orderly and flexible way in

budgeting and planning. According pull system makes a highlight flexible and capable

operational plan. Another way to say, that action planning and cooperation in the

organization, from top management to bottom management, every aspect of value

stream has a good plan and coordinate work together to improve value stream work in

an effective way.

Value stream in budgeting and planning, it involves sales process, leading to the

acceptance order, the manufacture of products, shipments and invoicing of the goods,

and cash flow information from customers. Of course, in the specific case, some of

the factors will change to fit value stream thinking and continuous improvements.

It is suggested to making short-term and medium-term plan to identify the product

cycle time, level of schedule and additional resources requirements. These can clearly

and easily be made to an orderly and flexible way to continuous improvement in value

stream.

10

Raw materials flow increase inventory in value stream decrease= dock to dock decrease. 11

AR days outstanding- AR balance /(monthly sales /days on the month)

Page 16 of 80

Managing product profitability

In a function way to describe product profitability in value stream, is eliminating most

of transaction fees in accounting. The value stream costing are reported by each value

stream weekly up-to-date information, it can save and eliminate the non-necessary

information, therefore save time and cost to collect information, and gives real

information about real cost in value stream.

Value stream costing structure ( Maskell & Baggaley, 2003, P136)

Traditional costing is more suitable in mass production condition, not in lean

manufacturing. In lean manufacturing thinking, is to eliminate inventory costs of

materials and outcome production. Therefore the tradition costing is not good enough

to improve the value creation in lean manufacturing behavior. (Below table shows the

difference12

)

12

Brain Maskell, Bruce Baggaley by practical lean accounting

Page 17 of 80

Traditional Lean

- There is one ideal cost for any

product

- Overhead costs are directly related to

amount of labor required to make the

product

- Maximum profitability comes from

maximum utilization of product

resources

- All excess capacity is bad

- High levels of customer services are

provided by high levels of inventory

- Production cost are controlled by the

detailed tracking of actual costs

- Cost optimization is achieved by

optimizing each individual part of

production process.

- Focus on value stream

- Simple and easy

- Easy to understand

- Provide the value stream

performance

- Eliminate the transaction and

overhead calculation

2.1.4 Support for lean transformation

Role of finance people

Accountant should work much closer to what they are doing now, in order to know

and understand how the value stream is effective with focus on continuous

improvement of performance, how to reach the strategy targets and goals in value

stream. If the accountant wants to answer these questions, then they should be behave

as an active player in each process.

Continuous improvement

Financial accounting and operational accounting has been discussed in the beginning

of thesis. As to how these two accounting works being together and continuous

improvement in value stream? Box Score13

create to evaluate financial and

13

Appendix Box Score table

Page 18 of 80

operational results with information to view how the value stream resources are used

and how the value stream creates values in lean.

In the part of theory introduction, it was mentioned in performance measurement, Box

Score can be used as a planning tool of lean to judge the effectiveness from lean

business perspective, and also monitor how the lean process to achieve the plans.

Empowerment and learning14

Empowering employee authority, make them feel effectiveness and responsibility

working in the organization. This is a strategy that creates a good lean environment in

the whole organization; it gives them the feeling that they are also having the decision

power to influence standard quality, service, product line design, etc. It gives a

confident level of lean thinking and trust level. The employee can show the possibility

of their idea about lean and more respect in their working area. Of course to make this

possible, the employees to have a good lean education background; they know what

the value stream in lean manufacturing and lean accounting is.

The organization need to support and educate workforce to know and understand what

lean is, what value stream behavior is. This needs money and time to invest, but the

results obviously are good for organization’s continuous improvement, employee

knows how to work more effectively, to eliminate the waste or non-necessary process

and cost.

2.1.5 Lean business management

Customer value and target costing

Target costing is a powerful tool in lean continuous improvement, it represent the

management attention on customer value to create improvement.

14

http://EzineArticles.com/2725391

Page 19 of 80

A series of cross-functional process designed to achieve objectives (Maskell &

Baggaley, 2003, P241):

- Establish the value created for customer

- Maximum product costs with value stream, based on win-win situation to create

value.

- Cross-functional increase value created from customer in value stream.

Sub - Conclusion

The value stream plays a big part in lean accounting, it creates value from customers

through the value stream and value is creating within the value stream process. This is

also why when discussed, the value stream should be in lean condition, and each level

of lean has a difference definition of the value stream. Each process should work

together to fully satisfy value stream in lean accounting.

Page 20 of 80

3 Beyond budgeting

Budget is not a down to earth process, it is determined by how people behave in

practical.

The reasonable factors of beyond budgeting

Beyond budgeting is the new concept that is not designed to fix a specific

problemwith budget. It sets in alternative process to support and control in relative

goals, targets, planning, continue performance, resource, demand, and rewards.

Evidently generally budget depends on the leaders to make the decision, they

evaluated on money inflow and outflow to determine financial plan will reach the

company goals. Since budget turns into fixed performance contracts, which used by

generation of financial engineers to control finance number, this leads to a lot of cases

to undesirable and unethical behavior.

After budget people thinking about how to budgeting, which consider the entire

performance process, is about agree and coordinate target, rewards, plans and

resource for the year ahead, uses these information to measure and control

performance, but budgeting was cumbersome and too expensive15

, it took a long time

to confirm and it is a risk in most of cases because of it does not achieve company

target.

15

Hope & Fraser, 2003

Page 21 of 80

Budgeting structure (Hope & Fraser, 2003, P5)

This is traditional way of budgeting structure, it was based on the company hierarchy,

and it reinforced functional barriers and failed to focus on the opportunity for

improving business process. The budget contracts range from highly authoritative to

highly participative, it can be understood as they want the whole organization and

executives to maintain control within the divers divisions and business groups, but it

also will be undesirable and dysfunctional outcomes at every levels of organization.

And most of cases happened as second situation. For example, always negotiate in

lowest target and highest rewards, never put customer care about sales targets, and do

not want to share information and knowledge with other teams even though in the

same company, expect more than they did, never beat number and accurate forecasts,

and never take risks.

People were tired to see the budgeting as an ineffective process in the organization; it

took too long and was costly and it failed to provide the value of future.

Traditional budgeting weakness (Bjarte Bogsnes, 2008, P69)

- Conflicting purpose – target setting vs. financial forecast

- Not only a ceiling – also a floor for cost

- Promotes centralization of decisions and responsibility

- Inflexible to change in planning assumptions

- Tends to make financial control an annual event

- Absorb significant resources across the organization.

Page 22 of 80

There was a lot of opportunities in budget but which way can be truly happened?

Beyond budgeting is a way to adapt management process, which keeps away far from

comfort areas. And use beyond budgeting to change responsibility to front line people,

who needs more radical and determined leadership from the top management.

Meanwhile beyond budgeting also benefits for the investors to know how companies

or organizations to reduce the varieties costs and make a strong relationship at

transparency and practice in corporate governance.

The biggest difference between beyond budgeting and Traditional budget is that

beyond budgeting enable managers to focus on continuous value creation, while

traditional managers focus on the current situations.

Table difference between traditional and beyond budgeting16

This is most impressive figure between traditional budget and beyond budgeting.

Beyond budgeting adapt a new annotation of budget in the organization; the new

theory changed the problems in the traditional budget such as (Bjarte Bogsnes, 2008,

P8):

- Trust17

Traditional budget controls by central of organization and uses fixed performance

16

http://www.12manage.com/methods_fraser_beyond_budgeting.html 17

Appendix B

Page 23 of 80

contract to work, it limits the trust between each other.

- Cost management

The tight budget might be detail and it might tie up people’s hands and feet.

- Target setting and evaluation

Limited information and trust made low and hit target

- Bonus

High expect and low profit

- Rhythm

Un-stable business environment made organization difficult to find a perfect business

rhythm.

- Quality

Good targets, reliable forecast and resource are relative high quality budget and

planning.

- Efficiency

Measurement

These are the typical problems from the organization structure, strategy, control and

relationship in the traditional budget. But in the beyond budgeting, represents a better

theory to fix the business in the organization. It shows how to adaptive and change in

organizations and decentralized organizations.

First part:

-Cost saving

- Less gaming

- Faster response

- Better strategic alignment

- More value from fiancé people

- More value from tools

Second part:

- Higher profits

- More capable people

- More innovation

- Permanent lower costs

- More loyal customer

- More ethical reporting

Decentralization features (Hope & Fraser, 2003, P36)

We may have a doubt about how do you know it is going to happen like this or how

could it happen like this? Beyond budgeting theory based on the traditional budget

theory to change and find a new way to run business, which could easily causes cost

saving, less gaming, faster response, better strategic alignment, more value from

finance people and more valuable performance investigated in organization. The first

part benefits effects on the second parts, the top manger saw the decentralization

opportunity that proved a significant competitive advantage, thus they will commit

and empower people at front line, with the full empower, the frontline people can be

more effective in use of correct information and make fast and effective decision,

Page 24 of 80

which leads organization to reduce costs, produce innovation strategies, create loyal

customer, finally make higher profits to shareholders’ wealth.

Investors would like to know how the organization is working, where the money

going and how much is the return of profit, the most important part is how to trust the

organization uses their resource in a proper way, for all these questions, answers will

be found out from beyond budgeting, which makes it carefully planned together with

strong and reliable leadership, use crucial information to respond frontline people,

that replace budgeting process and fixed performance contract. It is the keyword to

create better reputation of organization and build trust with investors.

It is not only to help organization to break the trap from annual report, and also

release the full capabilities from frontline people. Truthfully it needs a strong and

determined leadership from top management to support organization allocated full

responsibility to frontline people, for which can bet used to help frontline people to

adaptive a comfort condition to work and have a great potential benefits in further.

3.1 Six principle of managing with adaptive process

In the book of “Beyond budgeting” by Jeremy Hope & Robin Fraser, you see the

model that they created, where they explained how to use six principles to perform

beyond budgeting to value creation.

Page 25 of 80

The six principles18

are to remove the fix performance and budgeting process and

able to change the attitudes behaviors of people in the organization from frontline

people to top organization.

3.1.1 Target setting 19

18

Hope & Fraser, 2003 19

Hope & Fraser, 2003

Page 26 of 80

According to the short-long term performance to set the organizations’ goals, this

happened in most cases and organizations. But in beyond budgeting it is, set stretch

goals disconnected from performance, it is based on their own highest aspirations to

set goals that means managers have to use their judgments and take more

responsibility of risks. The fixed performance limited further benefit and develop

business space, therefore stretch goals, it makes everything possible conception,

evidently it has to follow the organizations’ strategy, but the best possible outcome is

to make impossible dreams happening. In other words, it did not tell other managers

to go against target, because it always works on managers to spirit the benefits. The

aims of stretch goals are to drive imaginative strategies developing by beyond

budgeting. Benchmark goals are more suitable use in industry produce line or direct

competitors; it depends on the marketing and business environment. For example,

competitors situation and market performance, it is used to shorten and simplify the

budgeting process and to reduce the amount of produce, where it should be negotiated

with the internal group to active interchange within organization, then it could

become a very useful theory to encourage improving performance. After external

information collection, the decision making of internal group20

has to create

performance in each level to keep coherent within the organization strategies goals.

3.1.2 Motivation and rewards

The concept of motivation and rewards are relative to improve the high contracts with

hindsight, that means do not link rewards to fixed performance contracts. Rewards are

different between organizations, maybe they are highly rewards in a low profit year

while a low rewards in high profit year, and thus, they are related to the competitors,

20

Group might be based on regions, countries, branches, plants and service centers, based on KPIs (key performance indicators) and ROCE to drive same business environment.

Page 27 of 80

market or pervious market it is depending on the relative performance. This focuses

on how managers maximizes the profits from the business instead of only pay

attention on the numbers, because there is no fixed performance against evaluate

performance. Meanwhile, some organizations do not only evaluate the personal

performance but also consider how the whole organization’s performance. It is

decided by the internal group subjective consideration21

.

Contently of rewards, it should base on the equalization of management group in the

organization. It is not important about how much financial number made, but about

how much contribution employee made for the organization in successful way. If

management group drive free rider to expose rewards, I believe some people are

willing to take the performance challenges.

3.1.3Strategy process

Make action planning a continuous and inclusive process (Hope & Fraser, 2003, P77).

Which strategy process depends on types of company that may include in culture,

business environment, capability of organization, and level of team. Different levels

or different leaders obviously make totally different strategies and goals, some of

them may allocate top power slow to lower manager, and rely on more theory

modeling to control organization, and they will focus more on the key value drives

and strategy initiatives and stretch goals. Another may focus on devolution of the

performance, and reply more on local team to charge more responsibility and collect

information to prove the continuous performance. Thus, beyond budgeting tend more

to people behavior; the people in here include employee, customer and shareholders.

It does not take more attention on the numbers, of course it will not be involved in this

case, for example, insurance company.

21

KPIs & Scorecard

Page 28 of 80

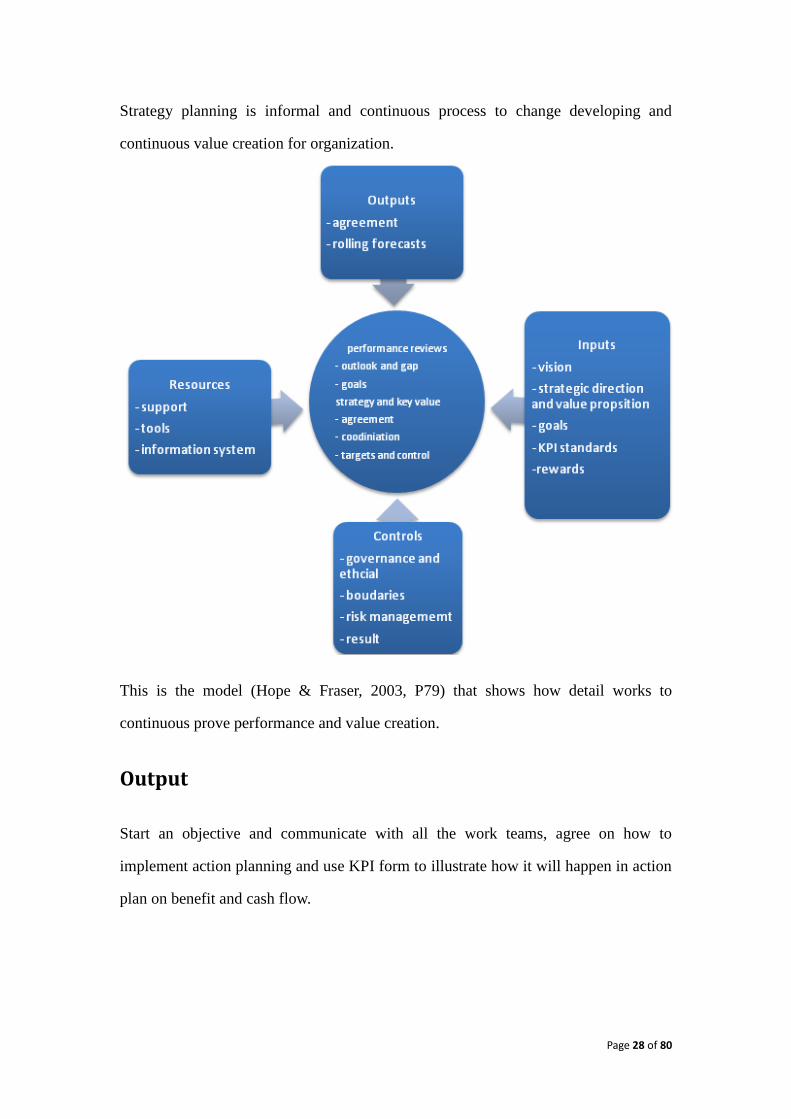

Strategy planning is informal and continuous process to change developing and

continuous value creation for organization.

This is the model (Hope & Fraser, 2003, P79) that shows how detail works to

continuous prove performance and value creation.

Output

Start an objective and communicate with all the work teams, agree on how to

implement action planning and use KPI form to illustrate how it will happen in action

plan on benefit and cash flow.

Page 29 of 80

Input

Managers use organization vision to check with account performance22

and goals,

throughout strategic direction consider customer value proposition. And the rewards

also depend on few of KPI standards to evaluate performance. These are significant

factors to strategy and key value drive review of process.

Control

The clearly stated governance principles, ethical values, strategy and KPI boundaries

guide managers to control how much resource to use in the process. The work unit

team needs to discuss how to combine all the elements23

include in the strategy and

how much risk responsible can take in the process. These can measure how

performance is going in the next level.

Resource24

In here resource means, which used by organization to support team or people, who

works for organization. Help and teach them to make effective strategy and good

performance, and use right information to make decision.

Performance review process

All four elements support the performance review process, these are key factors to

support organization make right strategy decision to continually create more valuation

on the next level.

Performance review more likes the check table, to critical the whole process and find

out where the mistake will happen in the planning action. And make all the thing

22

Activity accounting 23

Activity accounting 24

Activity accounting

Page 30 of 80

works together to reach the target.

3.1.4 Resources management25

- KPI parameters

Definite how utilize of resource

- Operational resources

Identify which level of service should be taking and depend on the customers’ needs

to change the service possibility.

- Fast- track for major projects

Permit the expenditure to approval produce

- Authority for smaller projects

Consider forecast of small investment with whole portfolio, therefore authority level

can used at any time within the year.

3.1.5 Coordination

Coordinate communication to serve the marketing demand. The idea of coordination

is that proves customers satisfaction and use short term capital to reflect how to

satisfy and recover the customers’ needs without any pervious order. Because these

quantity of produce run out of budget, therefore if organization has a short termed

capital that can satisfy this area customers request, it would be perfect. Except starting

the new market and new production, in most of cases, if building up a customer

database is a necessary program, in frontline people or managers need customer

information to make decision, to understand and know the customers’ information is a

key to make the right decisions and create more values in the market.

25

Hope & Fraser,2003

Page 31 of 80

3.1.6 Measurement and control

The whole control system is measurement and control, after mangers measurement

that is control the business on the right to go.

Open mind that means open information, in the organization to mention about

measurement is about to open the mind, to open why we chose this strategy to

continuous and how we should know this is right direction to open mind. All these

questions need more information to support our minds. The information provides will

include key indicators and forecast. Control are strengthened, it needs effect

governance, financial actual, analysis, forecast, KPI, performance and management to

coordinate together.26

Sub - Conclusion

All six principles are relevant to each other; none of them can work perfectly alone

with beyond budgeting in the organization, because they have very strong relationship

among each other. It also tells us how it should remove the fix performance contract

and continuous make value creation.

26

Government framework enables to lead to set boundaries and guideline for strategy developing and decision making, it needs managers to consider the risk of strategy. Keep a relative financial account system it will more effective to update information and more use in the financial report, can help manager to analyze and decision support. Forecast perform a number of roles, rolling forecast performs longer period a view and include sales, costs, profits, cash flows and orders. KPI controls the short term performance, which is happing and will happen, and it used to base on costs of income or costs and profits. Share the information with all the managers in the organization.

Page 32 of 80

4. Case discussion

In this thesis, I used a lot of time to make theories’ conclusion about value stream and

beyond budgeting. I believe in the next chapter: case discussion, those two theories

can inspirit and help MosCo to find a better way to continue improving in the

performance.

Case description

Based on above the theories description and in order to figure out how to compare

lean and beyond budgeting in the same situation, I will start to use a case to make two

different analyses with lean and beyond budgeting.

Before discussion in the case, I will make some of my own hypothesis based on the

case resource, because in this case, there are a lot of financial numbers but in this

thesis, I will not consider that many. And the aim of discussion in the case is to try to

figure out how the organization should save money and work more effectiveness.

Thus, I will make use of value stream and beyond budgeting theories to discuss how

to continuous improve the development in MosCO.

Case study: MosCo, Inc.27

‘The evening before the annual two-year budget review, MosCo’s director Offtiol,

waited for the latest financial estimates, but when controller Jonathan Janus delivered

the requested proforma income28

statement, his mood changed directly difference.

MosCo, a semiconductor design and manufacturing company, is a wholly owned

subsidiary of CSI (computer system, Inc.) a leading manufacturer of client/servies,

work station and personal computer.

In year 1993, MosCo sold a single product (nanosecond microprocessor x100) to CSI,

it was/is used in CSI services and workstation. And during year 1993 to 1994, MosCo

sold full price to CSI, and during the year, CSI asked MosCo to make a competitive

price. In year 1995, CSI management felt each business needed to flexibility and

independence to react to rapidly changing market conditions. For MosCo should sell

their production to other new customer to cover the product capacity and keep the

27

Appendix Case MosCo INC. 28

Appendix case study exhibition 1

Page 33 of 80

same profit as 1993. So in year 1994, MosCo consider the suggestion and

establishment a new marketing department, it was created to identify and open

external market opportunity. Meanwhile, MosCo faced with numbers of pressure and

unknowns situation, and it determined from industry the price/performance for

microprocessor halves every 18 months. And Carlotta, head of marketing department,

thought if they reduce the price product then the cost price will reduce too, therefore

reduced Carlotta the sale price (from 850 to 318.75) to force reduce manufacturing

cost reduction. After he requested 3 million in funding, it accelerates the completion

of an integer-only new CPU microprocessor(x50), because x50 was under developing

and would use 1 million; the rest of 2 million was going to new product’s (x 75)

developing. In the market, company NoTel was the leader developing in x 75and it

sold x 50. And Carlotta based on the estimated and recommends had a big promotion

to get market share in x50, it would use 1.6 million for commercial/promotion in the

next three years.

With the price depression from CSI and external market, product department Scott,

asked Offitol to formulate a new recommendations plan for the new products x50 and

x 75.

Offitol had a better knowledge about cost structures, cost drivers, and highlighting

non-value-add work29

it was a better way to work, he believed that the team used

ABC method can reach the purpose, and to reduce the cost in manufacturing (reach

cost goals in 1995 at 166).

To achieve the 1996 product cost of 332.5, Offitol and his team worked throughout

ABC, and found out wafer fabrication was the largest area of manufacturing cost, he

asked deStepper, who worked in product planning to review fabrication area for

further cost reduction opportunities. He found out 1) reduce the wafer usage, 2)

redesigning wafer produce, 3) better placement of inspection station, but his most

significant suggestion, that increase in capacity attained by increasing equipment

uptime (the time equipment is not undergoing repair or preventive maintenance),

however it requires more money to invest new equipment, and increase the wafer

capacity, decrease the cost. Offtiol did not want to put more money in investment and

then focus on the package costs. It did not work after purchasing manager Polly’s

reply. In the end, product x 50 is the last factors have to consider, the work team used

x 100 to compare with x 50, they found out if it used the same amount of materials to

produce x100 and x 5030

, obviously x 50 used much less cost, Offitol decided to

29

Appendix case study exhibition 5a-c 30

Appendix case study exhibition 2 & 10

Page 34 of 80

produce more x 50 instead x 10031

. Finally before the two years budget review, Offitol

decided to keep the same plan in 1996 reduced32

the x 100 price and expect sell more

and higher price in x 50 and continuous to develop x 7533

. ’

5. The object of value stream

A value stream represents all the business we do to creative value for the customer.

Why this thesis focus on the value stream, is because of the value stream is the

economic for the organization. The organization through the value stream to create

value to customer, meanwhile it makes money from customer. 34

Value stream can identify waste and develop action plans, we can use value stream

map to eliminate the waste.35

Evidently need to fully understand and quite familiar

with whole process of organization, ex. like from the materials, information and cash

flow through each organization, each lean plant has to connect together. It is

important to involve more than just what happen with the production plant. Normally

work in process is the Centrum of changing, that’s why most of organization thought

lean accounting is not working in the beginning period. When they changed to lean

accounting, they forgot the financial is difference; customer, service, supply chain all

changed to different as before.

31

Appendix case study exhibition 13 32

Appendix case study exhibition 12C 33

Appendix case study exhibition 14 34

Maskell & Baggaley ,2003 35

Maskell & Baggaley, Katko & paino edited by Susan Lilly,2007

Page 35 of 80

Typical value stream structure ( Maskell & Baggaley, 2003, P95)

This figure represents lean thinking of the value stream in general, which include

customer, supplier, work in process and management control all include together.

Evidentially, it gives a clear guideline on how to challenge each steps in the

organization to see if they are really create value for the customer and eliminate the

waste, search the perfection process from begin to end , the happy situation, it has to

be zero waste.

That is why I use value stream in this thesis about MosCo, to identify waste and

develop action plans. Value stream structure give the best way for MosCo to

understand and increase value for customer and also growth business, increase sales

and produce more benefits of organization.36

36

Maskell & Baggaley, 2003

Page 36 of 80

5.1 Financial accounting

Purchase order, receiver and invoice took large percent of costs in financial

accounting. So how should take good care relation between them, to eliminate

non-necessary behavior and costs.

All the changes creates threats to exist accounting structure, and sometimes the

changing is dramatic like MosCo and subsidiary CSI, between them may only need

order from CSI to MosCo and manufacturing receive the order and make records

when shipment to CSI, the invoice paper totally can be saved in the whole process,

this behavior can work with suppliers and other customers. In the end, saving lots of

financial department work at collect and recheck times and costs.

receiver

invoice

purchase order

Page 37 of 80

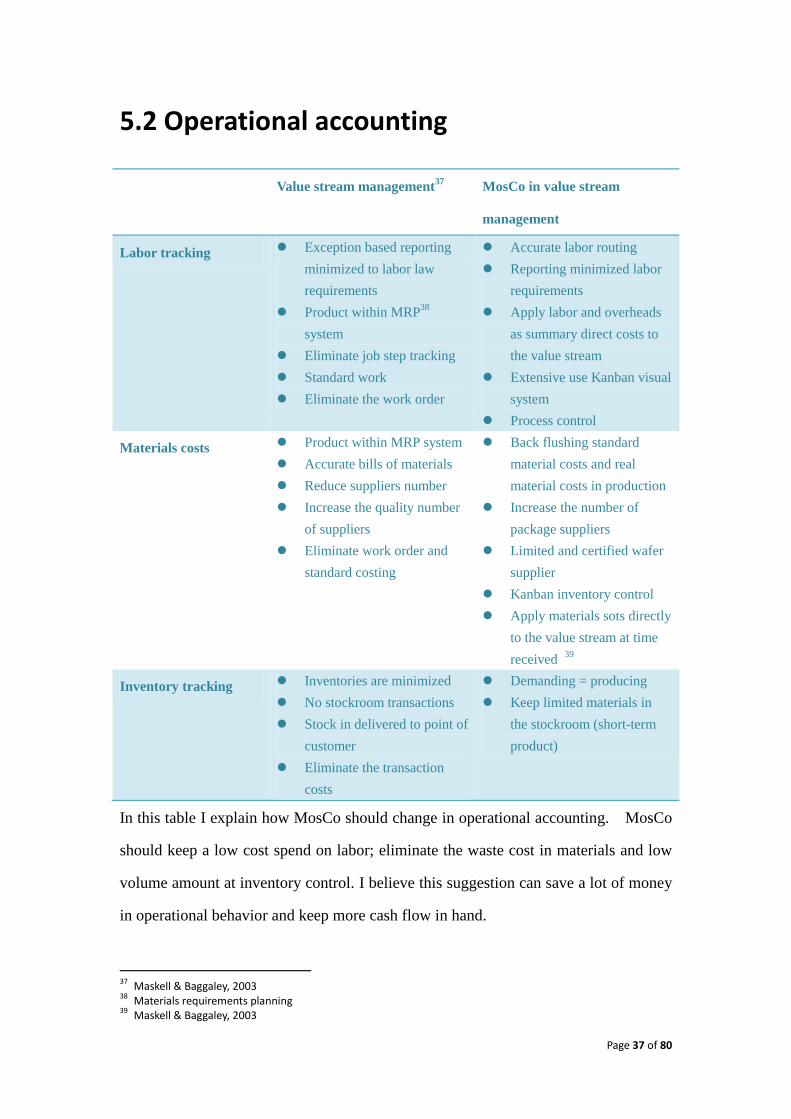

5.2 Operational accounting

Value stream management37

MosCo in value stream

management

Labor tracking Exception based reporting

minimized to labor law

requirements

Product within MRP38

system

Eliminate job step tracking

Standard work

Eliminate the work order

Accurate labor routing

Reporting minimized labor

requirements

Apply labor and overheads

as summary direct costs to

the value stream

Extensive use Kanban visual

system

Process control

Materials costs Product within MRP system

Accurate bills of materials

Reduce suppliers number

Increase the quality number

of suppliers

Eliminate work order and

standard costing

Back flushing standard

material costs and real

material costs in production

Increase the number of

package suppliers

Limited and certified wafer

supplier

Kanban inventory control

Apply materials sots directly

to the value stream at time

received 39

Inventory tracking Inventories are minimized

No stockroom transactions

Stock in delivered to point of

customer

Eliminate the transaction

costs

Demanding = producing

Keep limited materials in

the stockroom (short-term

product)

In this table I explain how MosCo should change in operational accounting. MosCo

should keep a low cost spend on labor; eliminate the waste cost in materials and low

volume amount at inventory control. I believe this suggestion can save a lot of money

in operational behavior and keep more cash flow in hand.

37

Maskell & Baggaley, 2003 38

Materials requirements planning 39

Maskell & Baggaley, 2003

Page 38 of 80

5.3 Management accounting

Alignment goals in lean and performance measurement

Value stream in MosCo

- list the strategy objectives & goals (reduce the cost, product x100, x50 and x75,

create new marketing)

- define the critical success factors with strategy goals

- define the target and goals (x100,x50 product line)

- create lists of performance measurements

The measurement normally designed to report weekly, because of it fits the schedule

of the value stream continuous improvements teams. They drive the changing not

only about results in the report.

In order to help MosCo operating measurement and improvement process in value

stream, to use performance measurement to identify problems and root cause.

Page 39 of 80

Value stream performance

measurements

How should MosCo

measure?

Value stream results in

MosCo

Sales per person Marketing department

collect the market

information to plan sales

amount by number of

people in value stream

Increase value created with

the same or less, resource

On time delivery Manufacturing department

based on the customer

requires to ship CPU to

customer, percentage of

sales order lines shipped

on the right day

All processes within value

stream under control

Dock-to-dock time The amount of inventory

thought the value stream

expressed in days or hours

of requirement, need

purchasing and market

department to support

inventory low capability.

Increase the rate of

material flow

First time through Make sure that the product

and performance is perfect

every time.

Standardized work every

time

Average product cost Limited the cost by

number of product ship to

customer

Reduce the resource

require and make sure sell

all the product

AR outstanding Ship product to customer

on time and then Expect

customer pay on time.

Increase the rate of cash

flow

The section above shows how I suggest in MosCo at alignment goals and

measurement, MosCo should have a clear and unique goal to make developing and

keep the measure at mind to ensure all the behavior and activities follows the goals

and expectation. It is important for MosCo to work cooperatively with value stream

teams, it respond rapidly and continuous improvements of MosCo measurement, the

tables 40

shows a steady, step by step of measurement results.

40

Maskell & Baggaley, 2003

Page 40 of 80

Budgeting and planning

If MosCo want to expand the new market, it needs a retailer or sales department to

sell the production. The retail shop needs a detail schedule to represent planed and

organized in the value stream way.

The form used to explain to MosCo employee about, how to understand the way

transform demand from the customer to planning, and financial department can have a

good understanding of financial impact. (The table41

below just shows the process in

value stream.)

Value stream in planning Value stream in budgeting

- month-end data, (MosCo new

marketing department)

- customer forecast, (MosCo new

marketing department)

- new product plan,( product

developing team about x75)

- new promotion (will sales product

x50 in the totally new external

market)

- update rolling forecast for the next

12 months (need Jonas department

supporting)

- major budget issue

- new expenditure (new market

promotion and increase money at

developing x75)

41

Maskell & Baggaley, 2003

Year 1994 Jan. Feb. March April May June July Aug. Sep.

Value stream

Revenue x Y Z A B C D E F

Materials cost X Y Z A B C D E F

Conversion costs X Y Z A B C D E F

Value stream profit X Y Z A B C D E F

ROS X Y Z A B C D E F

Page 41 of 80

Managing product profitability

How should MosCo achieve better profitability in value stream?

Everyone should know and understand the meaning of where the financial

information comes from. Value stream costing provides the better information, it is

readily and reliably to use in day-to-day decision.

Reporting needs to be by value stream, not each department

Staffs must be assigned to the value stream with little or no double repeat

It is the best proactive to limit the service department, avoiding spend double or

more time costs in the same function area.

It must be have a reasonable control system and low variability

Inventory must be reasonable controlled as relatively low and consistent

MosCo should have low and consistent materials and work-in-process inventory

control. Because performance measurement is a key to understand each process is

under control, MosCo can use management accounting easily and quickly to change

the mistakes and keep them in the right position once some processes goes wrong.

5.4 Support for lean transformation

The role of employees

Janus in the financial department works very hard to collect the finance information in

order to make two years budget. But the result is different from Offitol’s expectation.

Where did it go wrong? How should Offitol help Janus with the value stream?

Page 42 of 80

Figure: Change role figure (Maskell & Baggaley, 2003 P89)

This figure illustrate how lean structure will change in accounting, therefore the

behavior of accountant, Janus can eliminate a lot of bookkeeping time and costs, also

the administration fees.

Janus should know more about marketing forecast, manufacturing cost, purchasing,

employee and MosCo’s strategy targets to change the behavior and support lean

transformation.

Continuous improvement

MosCo can use the Box Score to design improvement process in value stream

continuous improvement. Throughout the Box Score table (appendix Box Score) to

evaluate how impact between operational and financial in current and future state.

From the x50 Box Score42

table to make a general analyze on value stream,43

because the limited information, MosCo needs the financial department, purchasing

department, manufacturing department and new market department to coordinate

together to get comprehensive information in order to ensure the continuous

42

In weekly report shows the summary capacity usage for the value stream as a whole. 43

Maskell & Baggaley, 2003

Page 43 of 80

improvement.

X 50 Box

Score

Current

state(year 95)

Future

state(year 96)

Change

Operational Sales per person

On time shipment

Dock-to Dock times

First time through

Average cost per unit

*AR outstanding ( / Floor

space)

Resources

capacity

(appendix case

exhibition 14)

Productive 7940/ 35% 13312/59% Increase

Non-productive

Available* 345,156

/86%

179,340

/45%

Decrease

Financial44

Exhibition

12B-C

Inventory value

Revenue 11,718,750 33,593,750 Increase

Materials costs 851,235 3,578,910 Increase

Conversion costs

Value stream profit

The example figure results show there is no lean improvement in MosCo on product

x50. The rest of information has been given by the MosCo that makes the analysis

looks worse than in year 1995. Therefore, the completed information from operational

and financial, and capacity used in Box Score, which shows how value stream plan

works in MosCo and which part should implement lean change in order to ensure

continuous improvements.

Empowerment and learning

Empowerment is a good thing to show the workforce in the MosCo, people knows

how to work, and which part of program that do not work with them, if managers

listen the suggestion from the employees that can solve many difficult problems in the

production, shipment, and organization. For example, recently in DK tv2 program

‘under cover boss’, the top leader used undercover ID and went to the local train

44

Financial change shows maximum the financial benefits change.

Page 44 of 80

station area, and worked with local employee to investigate how they work, how the

repairmen working, and how they work more effectiveness and what was biggest

challenge in the train and working system. I believed he got the answers from this

action. What is clearly explained from this example is that empowering workforce is

not a bad thing for MosCo, it does not mean that management give up the control and

let employee do what they want, on the contrary it is about the guideline and

boundaries what can do and can’t do in lean. This lean thinking needs to be

established in the organizations management direction, to let employee find their own

way to achieve goals and targets. During this time, manager will find out this is a

better way to encourage the productivity.

5.5 Lean business management

Customer value and target costing

Product design and process design develop together by target costing. It is designed

for customers value and target cost for highly value profitability. In value stream,

MosCo introduced new market with product x50 and new product x75, use target

costing to provide a method for x50 and x75, design and marketing department

Carlotta to gain customer needs and requirements.

Page 45 of 80

Follow this figure, MosCo will find out what is the customers real needs and what

impact between value in new product (x50 and x75) and customer needs, how MosCo

should design the new product x50 and package.

Sub - Conclusion

One of the processes can’t work in lean implement; they are cross-functional to

complete lean thinking and lean improvement in MosCo. According to those analysis,

it shows if MosCo want to use value stream to continue improvement, it is better to

take short-term projects (two or three months), and in lean accounting that need whole

MosCo department to know and understand the whole process in each department by

lean behavior, certainly it needs time and money to invest, but it creates significant

ongoing improvement to MosCo in lean accounting.

Page 46 of 80

6. The budgeting problem

The major problem at MosCo is uncertainly. The microprocessor industry and has one

subsidiary computer system Inc. is subject to well defined but unpredictable business

cycles that have a dramatic effect on performance. And it does not have close

connection to the subsidiary company; the pricing of x 100 and x 50 is more

complicate than competitors. The work team focuses on how to reduce the cost, this is

the strategy and goals for MosCo, they forgot to consider the whole performance on

the next level, they thought that if they saved the cost then they would solve the entire

problem.

They continued with describing what they saw from the problems with traditional

budgeting, but the issues coming more and more with continue developing.

- How beyond budgeting process replace in MosCo?

This table, shows in the theory part, however It is still a good idea to have a look here,

Offitol had a great idea to continue the MosCo, but when they made the two years

budgets review, they still followed the traditional way, and the key fixed performance

contract is to reduce the cost wafers number and pricing change. Even though there

was a team to solve the problem but they didn’t have connection between each other,

top manager only work with their own department.

In this project, six process principles theory, it is the key ingredients to discuss how

Page 47 of 80

MosCo to prove more value creation in the following subsections.

6.1 Targets setting

MosCo needs to stretch the goals for further development, based on the case

information. It told us that, MosCo has a subsidiary company and just opened the

external marketing, as Bjarte Bogsnes(2008), mentioned,

‘Targets are set in relation to either the completion or best practice. Both internally

and externally on everything to support the cost, the benchmark process should

removes most of internal negotiations. Compare with who to benchmark and where

should to start, the target will coming naturally.’

Obviously, external marketing and competitor NoTel were the biggest consideration

for MosCo to set the benchmark goals, but is this strong enough for new marketing

department to make the whole target setting and use lots of resource to promote the

existed product x 50 into the market? Meanwhile, the sub-company CSI, wants to

reduce the internal x100 pricing, it was higher than marketing price. And x 100 only

produce for CSI, of course MosCo can beat the market prices by a few cents, but the

price level is not uncontrollable and unpredictable by itself. This is also why MosCo

keep the same budget in 1995.

Table: Relative target structure (Bjarte Bogsnes, 2008, P77)

Page 48 of 80

Table: ROCE (Bjarte Bogsnes, 2008, P78)

Financial performance, cost reduction, new production introduction (x75), customer

satisfaction (CSI and external market), business units and marketing expectation are

the medium-term goals to set (See the table relative target structure on the previous

paper). If MosCo set a key performance indicator (KPI) framework and returned on

capital expenditure (ROCE) for goals within the MosCo, I believe all those problems

would not such big that difficult to be addressed.

6.2 Motivation and rewards

In the case, it has any information about motivations and rewards. Even though

between MosCo and CSI, they seemed not to have considered anything about

motivation and reward system, this is also why CSI not satisfy the x100 price. Maybe

they focused too much on the cost reducing producing program, or maybe the

marketing department was new therefore they did not think about it. So this is a new

concept for MosCo to have a motivation and rewards system in the further marketing

expenditure.

I strongly recommend individual bonuses, because it is good for motivations and

further performance. No matter if it is B to B or B to C, bonuses is the best key to

Page 49 of 80

encourage sales and create more potential market share for MosCo.

KPI and Scorecard is a good testing model to measure bonus value. It is easy for

Offitol’s team group to communicate and operate. According to KPI and Scorecard