Value for Money the Road to Excellence pdfs/Presentations/Value for money... · Value for Money –...

35

www.bakertilly.co.uk Value for Money – the Road to Excellence Peter Lunio – Director

Transcript of Value for Money the Road to Excellence pdfs/Presentations/Value for money... · Value for Money –...

www.bakertilly.co.uk

Value for Money – the Road to Excellence Peter Lunio – Director

Agenda

• Introductions

• Self Assessments - personal

view

• Current experiences

• The case for VFM

• Delivering VFM excellence – a

Strategy & Process

• Summary

2

Baker Tilly - Continuing to

Support the RP Sector

•Baker Tilly 7th largest professional services firm in the UK, with

4000+ staff and 45 office locations

• Leading NFP specialists

-No. 2 provider in the SH sector – UK wide

-No. 1 provider in the ALMO sector - UK wide

• Dedicated team of over 30 Partners and 130 staff

Our innovative services include:

• A comprehensive VfM and efficiency programme covering

procurement, business process improvement review and

comparisons from our benchmarking service;

• Social investment and social impact measurement;

• Fraud and risk management;

• ICT – selection and implementation planning, effectiveness and

risk reviews;

• Corporation tax and VAT planning;

• Robust internal and external audit;

• Corporate finance – funding, acquisitions and mergers.

3

HCA’s VFM Standard

4

Required outcomes

Registered providers shall articulate and deliver a comprehensive and strategic approach to

achieving value for money in meeting their organisation’s objectives.

Their boards must maintain a robust assessment of the performance of all their assets and resources

(including for example financial, social and environmental returns). This will take into account the

interests of and commitments to stakeholders, and be available to them in a way that is transparent and

accessible.

This means managing their resources economically, efficiently and effectively to provide quality services

and homes, and planning for and delivering on-going improvements in value for money.

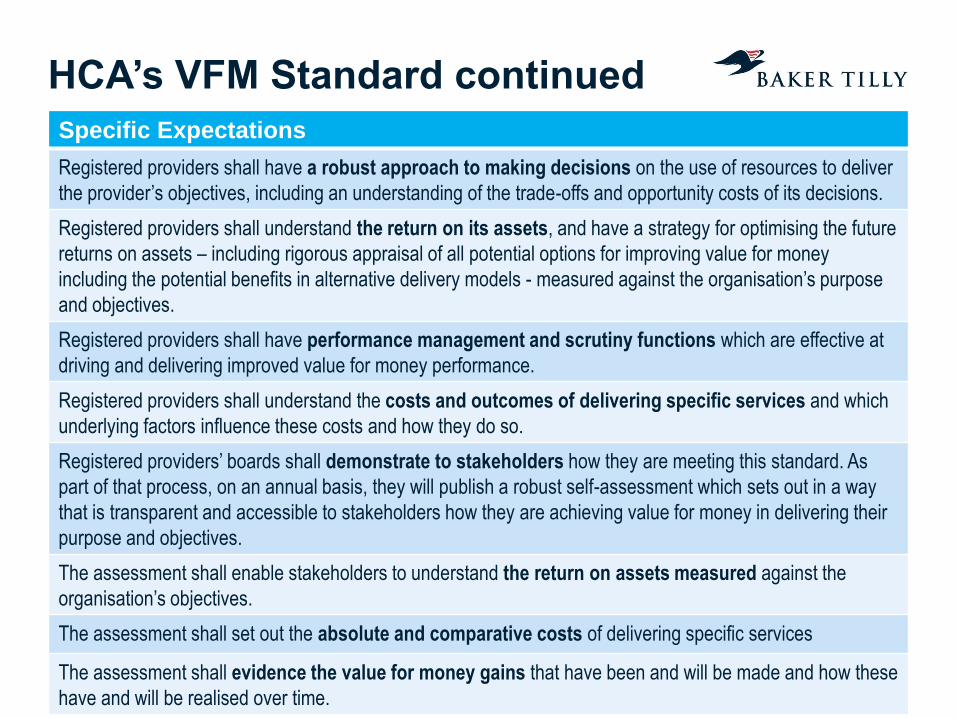

HCA’s VFM Standard continued

5

Specific Expectations

Registered providers shall have a robust approach to making decisions on the use of resources to deliver

the provider’s objectives, including an understanding of the trade-offs and opportunity costs of its decisions.

Registered providers shall understand the return on its assets, and have a strategy for optimising the future

returns on assets – including rigorous appraisal of all potential options for improving value for money

including the potential benefits in alternative delivery models - measured against the organisation’s purpose

and objectives.

Registered providers shall have performance management and scrutiny functions which are effective at

driving and delivering improved value for money performance.

Registered providers shall understand the costs and outcomes of delivering specific services and which

underlying factors influence these costs and how they do so.

Registered providers’ boards shall demonstrate to stakeholders how they are meeting this standard. As

part of that process, on an annual basis, they will publish a robust self-assessment which sets out in a way

that is transparent and accessible to stakeholders how they are achieving value for money in delivering their

purpose and objectives.

The assessment shall enable stakeholders to understand the return on assets measured against the

organisation’s objectives.

The assessment shall set out the absolute and comparative costs of delivering specific services

The assessment shall evidence the value for money gains that have been and will be made and how these

have and will be realised over time.

HCA VFM 13/14 Assessment Summary

• Are not planning to be more prescriptive concerning

what needs to be published

• Think that the response to the standard was very weak

and that the sector overall did not demonstrate ways in

which it is known how they are delivering VFM.

• Expect RP’s to be able to demonstrate how they

understand peaks and troughs in their costs, rather than

detailed accounting and reasoning of their exact Cost

per Unit

• Think that RP’s were very weak in demonstrating the

return on their assets. Assets also encompasses use

of resources.

• Want reassurance from the Self Assessments that the

Board is assured that the RP is delivering VFM and that

they are driving it.

• Would like to see better demonstration of VFM

efficiencies from the business plan and how larger

scale VFM can be demonstrated

• Found only a handful of good Self Assessments out of

the largest 250 HA’s in the country 6

Personal View – to what happened

• Confusion with regards to what the HCA wanted

• Complacency from some organisations within the sector?

• Not taken seriously by the board

• Allocated to the wrong individual?

• Not enough input and scrutiny from other parts of the organisation

• Most assessments were one year snapshots

• Few organisations had a “robust “ self assessment process

.

7

Current experiences

8

What do we think based on what we have seen?

Positives Areas for improvement

Overall, much improved since last time Tends to be written by one particular person

Self-assessments are longer and go into

more detail

Of all the reviews we have conducted, only

one written by somebody other than a

member of the Finance Team.

Has been taken much more seriously by

providers

Lack of scrutiny and involvement by the

Board and Audit Committee

On the whole, providers have a connection

between VfM approach and strategic

objectives

Cherry pick the best Key Performance

Indicators

Lots of evidence to support VfM gains made

during the year

Organisations have found it difficult to collate

data for measurement

Commendable use of benchmarking. There is a financial return focus. Not much

attention paid to social and environmental

return.

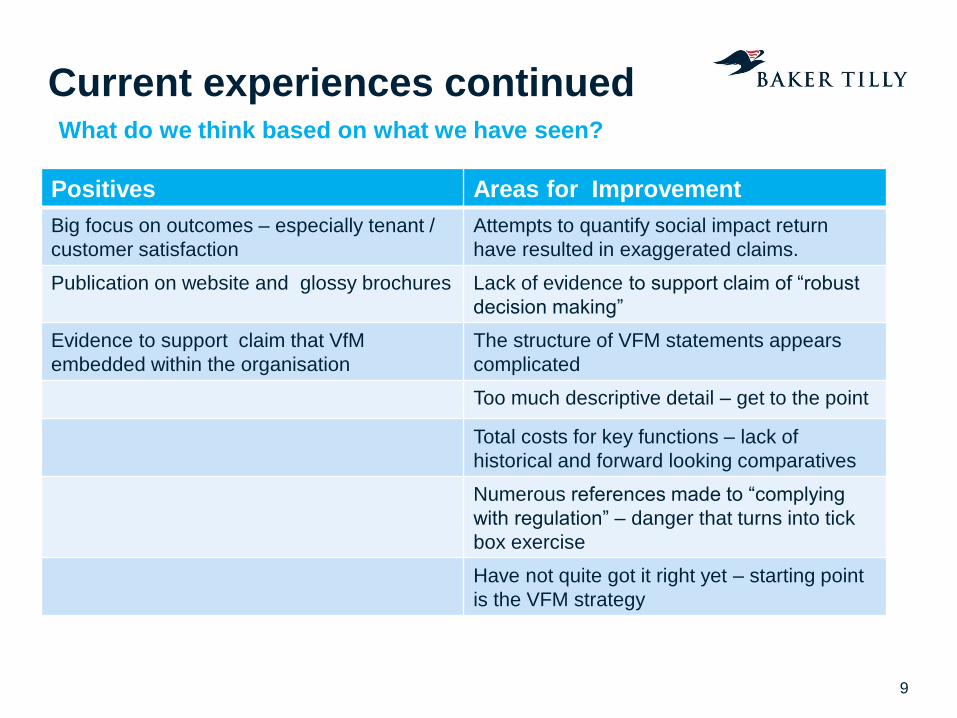

Current experiences continued

9

What do we think based on what we have seen?

Positives Areas for Improvement

Big focus on outcomes – especially tenant /

customer satisfaction

Attempts to quantify social impact return

have resulted in exaggerated claims.

Publication on website and glossy brochures Lack of evidence to support claim of “robust

decision making”

Evidence to support claim that VfM

embedded within the organisation

The structure of VFM statements appears

complicated

Too much descriptive detail – get to the point

Total costs for key functions – lack of

historical and forward looking comparatives

Numerous references made to “complying

with regulation” – danger that turns into tick

box exercise

Have not quite got it right yet – starting point

is the VFM strategy

www.bakertilly.co.uk

The case for having to tell your story….

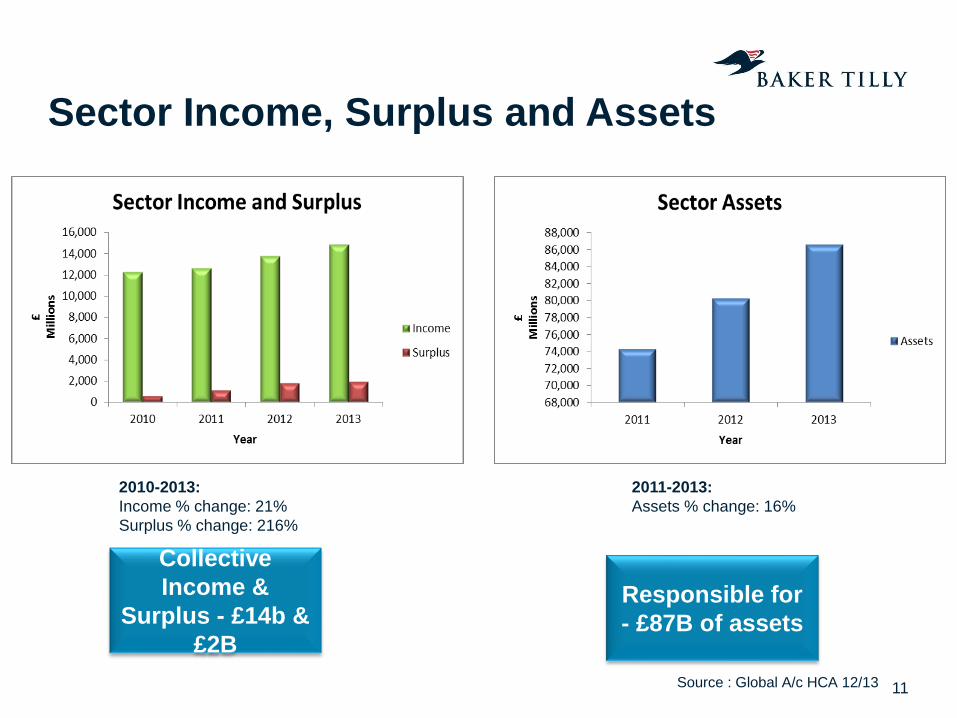

Sector Income, Surplus and Assets

11

2011-2013:

Assets % change: 16%

2010-2013:

Income % change: 21%

Surplus % change: 216%

Source : Global A/c HCA 12/13

Collective

Income &

Surplus - £14b &

£2B

Responsible for

- £87B of assets

How you spend your money….

Source : Global A/c HCA 12/13

Total spend £8.8B – 12/13

To manage ~ 2.5m homes

£3400 per/an home….

£2.3B

£1.8B

Do you know which provides you with …

The best return on Investment?

The best Social Return ?

Community

Investment

Asset

Investment

Development

Investment

Social Enterprise

Investment

13

• Only 22% of registered providers refer to assets.

• Only 45% refer to social, financial and environmental considerations

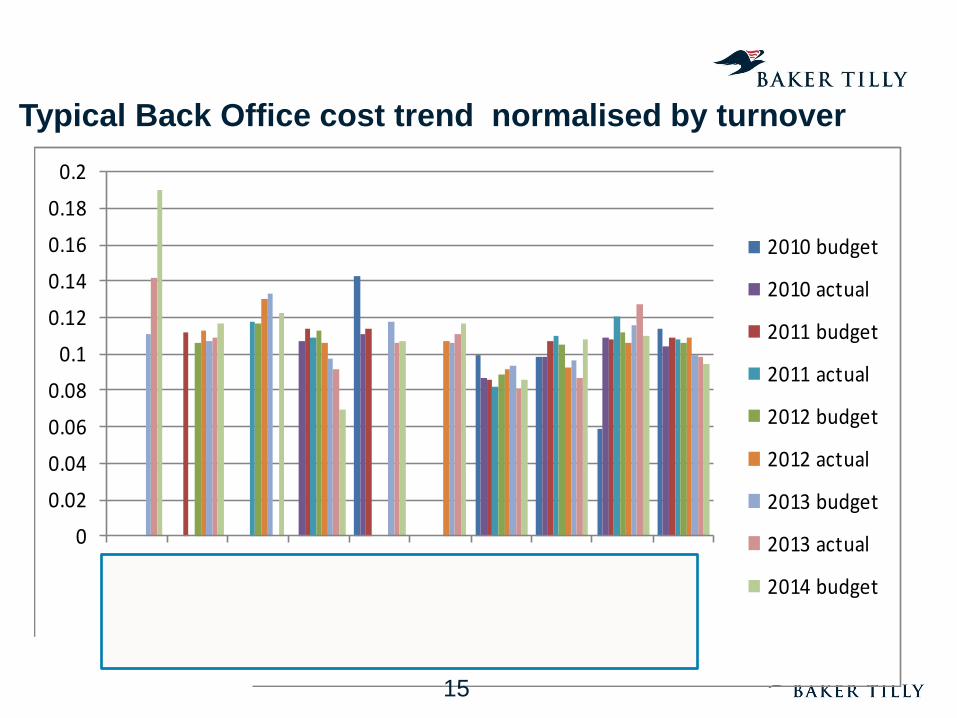

Back Office VFM ???

14

Source BOB

Typical Back Office cost trend normalised by turnover

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

2010 budget

2010 actual

2011 budget

2011 actual

2012 budget

2012 actual

2013 budget

2013 actual

2014 budget

15

www.bakertilly.co.uk

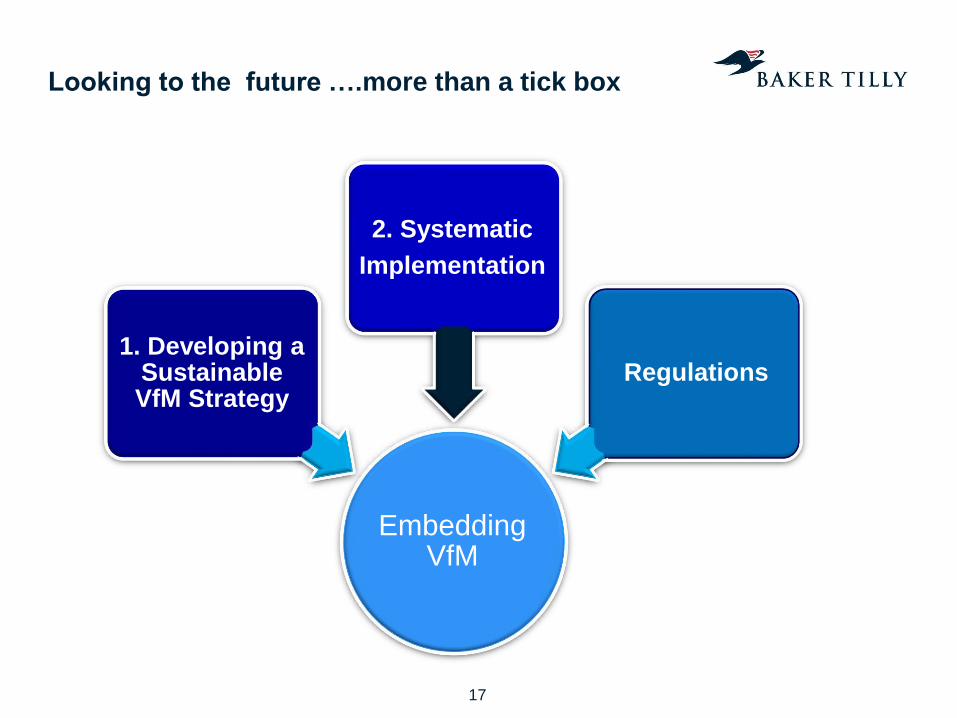

Delivering VFM excellence - a Strategy & Process

Looking to the future ….more than a tick box

Embedding VfM

1. Developing a Sustainable VfM Strategy

2. Systematic

Implementation

Regulations

17

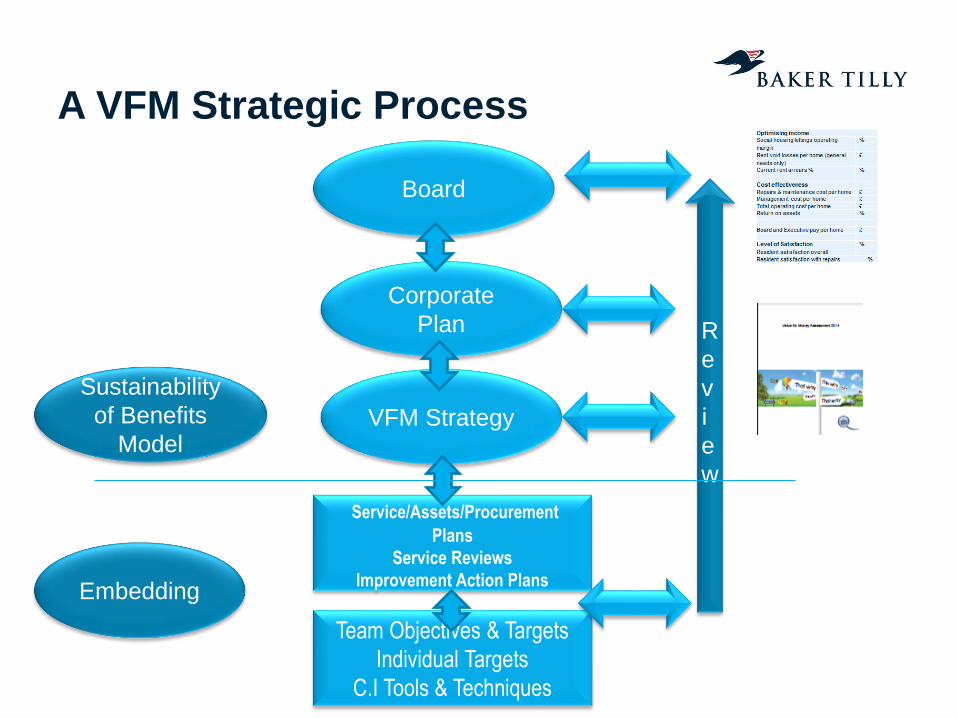

A VFM Strategic Process

Board

Corporate

Plan

VFM Strategy

Service/Assets/Procurement

Plans

Service Reviews

Improvement Action Plans

Team Objectives & Targets

Individual Targets

C.I Tools & Techniques

Embedding

Sustainability

of Benefits

Model

R

e

v

i

e

w

What we mean by VFM

£M

• Performance

Outcomes

• Stakeholder

Satisfaction

= VFM

Value for

Money

Low cost

High perform

ance

High satisfaction

Your Cost Base

19

Measuring VFM Strategically Optimising income

Social housing lettings operating

margin

%

Rent void losses per home (general

needs only)

£

Current rent arrears %

%

Cost effectiveness

Repairs & maintenance cost per home £

Management cost per home £

Total operating cost per home £

Return on assets %

Board and Executive pay per home £

Level of Satisfaction

Resident satisfaction overall

%

Resident satisfaction with repairs %

20

Cultural Value

Historical &

Future

Performance

• 23% of assessments refer to their KPIs and

how they performed against targets.

• 59% either make no reference to their KPIs, or

do not list them.

Strategic KPI’s example L&Q

21

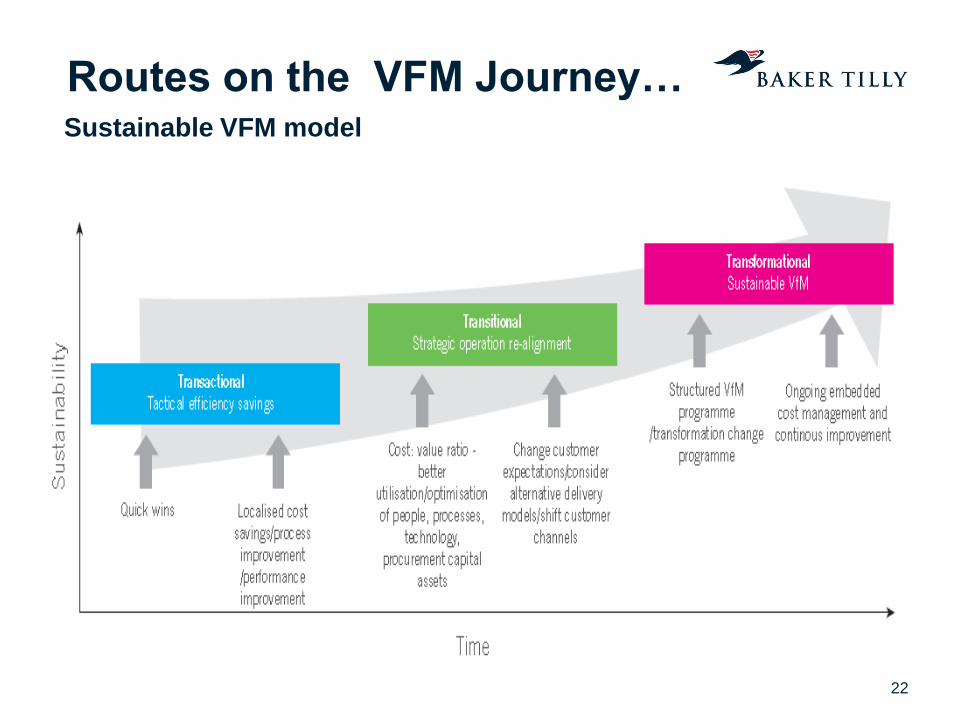

Routes on the VFM Journey… Sustainable VFM model

22

VFM – Transactional (Tactical )

• Performance

Outcomes

• Tenant Satisfaction

Typically remain the

same and not

sustainable

= VFM

Typically 1-3%

Cost Base

Characterised by

• Cost Centre approach

• Recruitment Freeze

• Corporate expense reduction

23

VFM – Transitional (Operational)

• Performance Outcomes

• Tenant Satisfaction

Some improvement and

gains are more

sustainable

= VFM

Typically 6-10%

Cost Base

Characterised by

• Lean Transformation

• Functional Consolidation – Shared

Services

• Market Testing

• Estate Rationalisation

• SROI

24

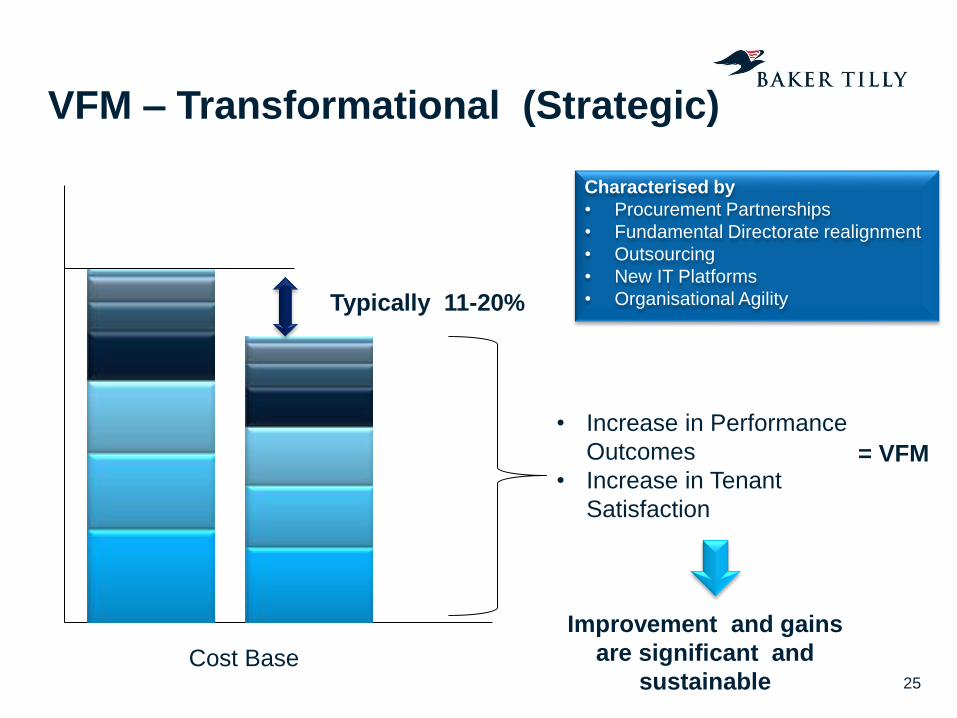

VFM – Transformational (Strategic)

• Increase in Performance

Outcomes

• Increase in Tenant

Satisfaction

Improvement and gains

are significant and

sustainable

= VFM

Typically 11-20%

Cost Base

Characterised by

• Procurement Partnerships

• Fundamental Directorate realignment

• Outsourcing

• New IT Platforms

• Organisational Agility

25

Making VFM stick

26

Typical VFM Route Map summary ….

Transactional

Transitional

Transformation

Recruitment Freeze

Corporate Expense Reduction

Budget Reductions

Process Improvement

Strategic Sourcing

Estate Rationalisation

Partnership Procurement

Directorate Realignment

Outsourcing

Re-investment

Re-investment

Time Typically 2/3 years

Increase in

benefits &

Sustainability

Project & Change Mgt

Social Return

27

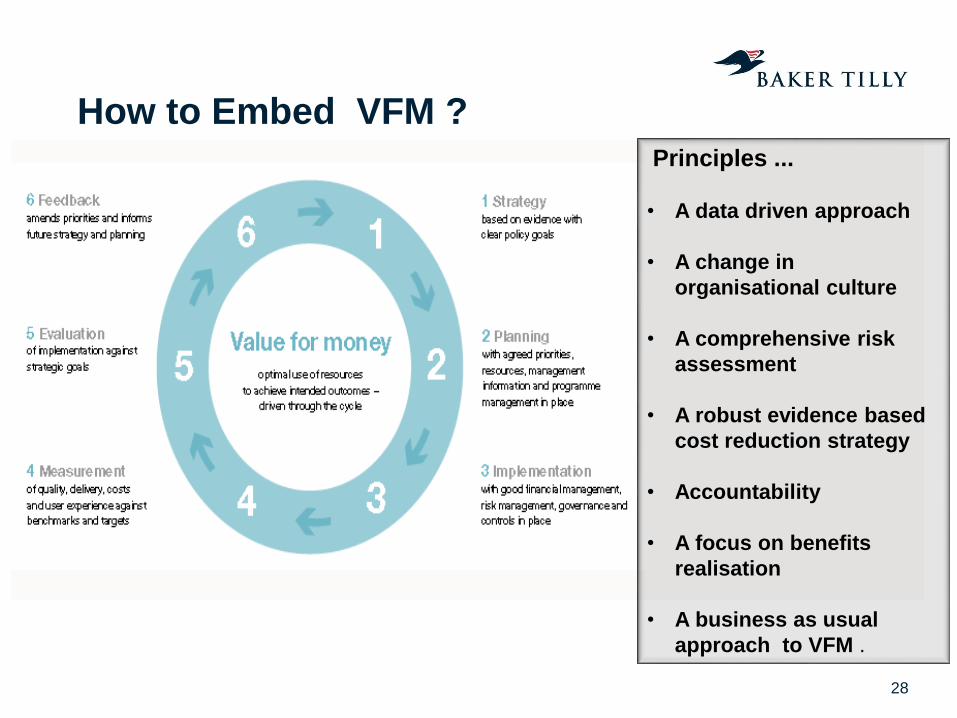

How to Embed VFM ?

Principles ...

• A data driven approach

• A change in

organisational culture

• A comprehensive risk

assessment

• A robust evidence based

cost reduction strategy

• Accountability

• A focus on benefits

realisation

• A business as usual

approach to VFM .

28

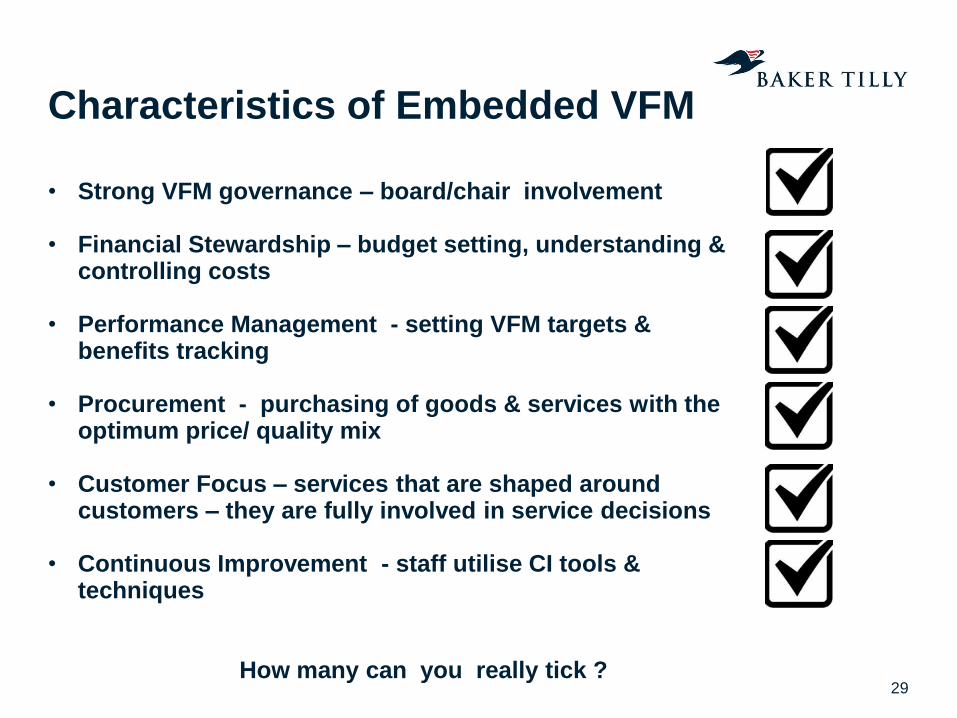

Characteristics of Embedded VFM

• Strong VFM governance – board/chair involvement

• Financial Stewardship – budget setting, understanding & controlling costs

• Performance Management - setting VFM targets & benefits tracking

• Procurement - purchasing of goods & services with the optimum price/ quality mix

• Customer Focus – services that are shaped around customers – they are fully involved in service decisions

• Continuous Improvement - staff utilise CI tools & techniques

How many can you really tick ?

29

Your VFM Strategic Plan which ideally would include

30

Typical Contents Do you have

?

In your VFM

Plan ?

Who owns it

Clear mandate from Exec & Board

VFM Governance structure

Set of Objectives

Cost Effectiveness Strategy

Service Transformation Strategy

Procurement Strategy

Asset Management Strategy

VFM Benefits Realisation Plan & Accountability

12 month detailed initiative plan

2 – 3 year indicative initiative plan

Robust Self Assessment

31

Cultural Value

Where are you and where do you

want to be on your VFM Journey?

How this will help you on going…

• Provide you with a VFM model against which you can assess yourselves against – current and future

• Give you a roadmap and plan on how to

get there

• Identify current and future initiatives

• Enables you to identify current and future benefits – whether they are sustainable or not

• Approach to embedding VFM

• Gives you something to assess yourselves next and the year after

32

VFM Strategic Process

Board

Corporate

Plan

VFM Strategy

Service/Assets/Procurement

Plans

Service Reviews

Improvement Action Plans

Team Objectives & Targets

Individual Targets

C.I Tools & Techniques

Embedding

Sustainability

of Benefits

Model

R

e

v

i

e

w

Your VFM story should demonstrate …

• you have a strategy - owned by the board

• robust self assessment process

• that it addresses the specific requirements of the standard

• provide sufficient evidence/assurance?

• a clear understanding of how you use your assets

• a clear understanding of how you manage your operational

costs

• you have performance management and scrutiny

arrangements to drive continuous improvement in VFM

• transparency with stakeholders on past performance,

direction of travel and improvement plans:

•

34

VFM Excellence – our solution set

Value for

Money

Low cost

High perform

ance

High satisfaction

VFM Strategy

/Embedding

3P’s Benchmarking SROI

VFM Transformation Solution Set

Associated

Guides

Identifying the

journey

Implementation &

CI

Reducing Costs

Increasing Quality

Objective comparison

of performance &

Practices

Delivering better

outcomes Deliverables

35