Sina Yeganeh et al- Chiral electron transport: Scattering through helical potentials

Upload

skylar-burdockCategory

view

217download

0

unido.org/statistics

Seasonal Adjustment of National Index Data at International Level

Shyam Upadhyaya, Shohreh Mirzaei Yeganeh

United Nations Industrial Development

Organization (UNIDO), Vienna, Austria

unido.org/statistics

Overview• What and why• Basic concepts• Costs and risks• Methods• Software• UNIDO experience • Recommendation

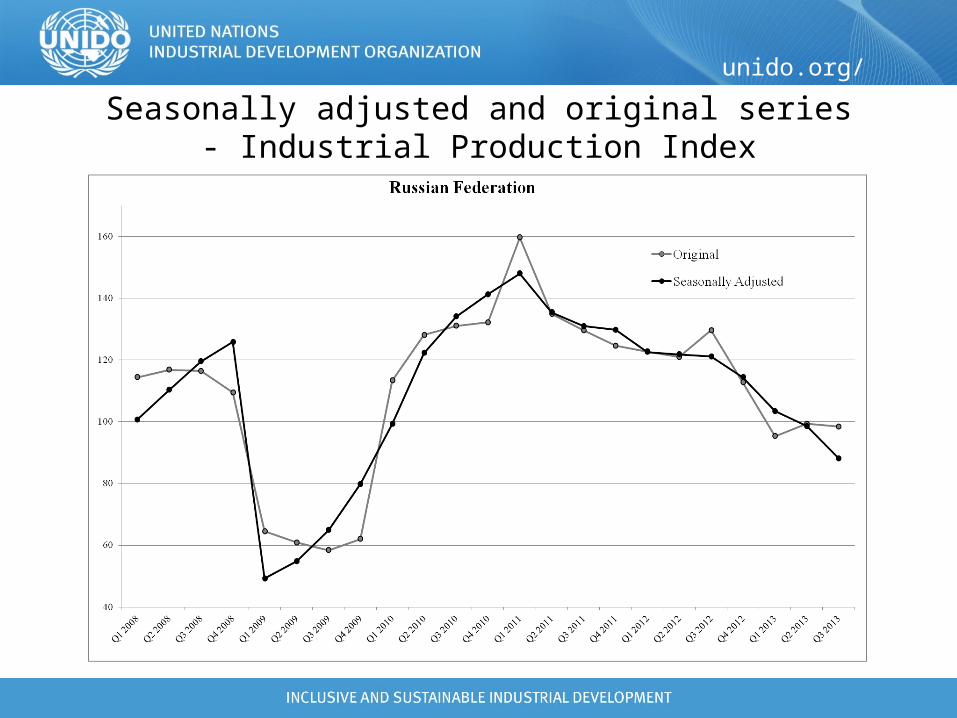

unido.org/statisticsSeasonally adjusted and original series

- Industrial Production Index

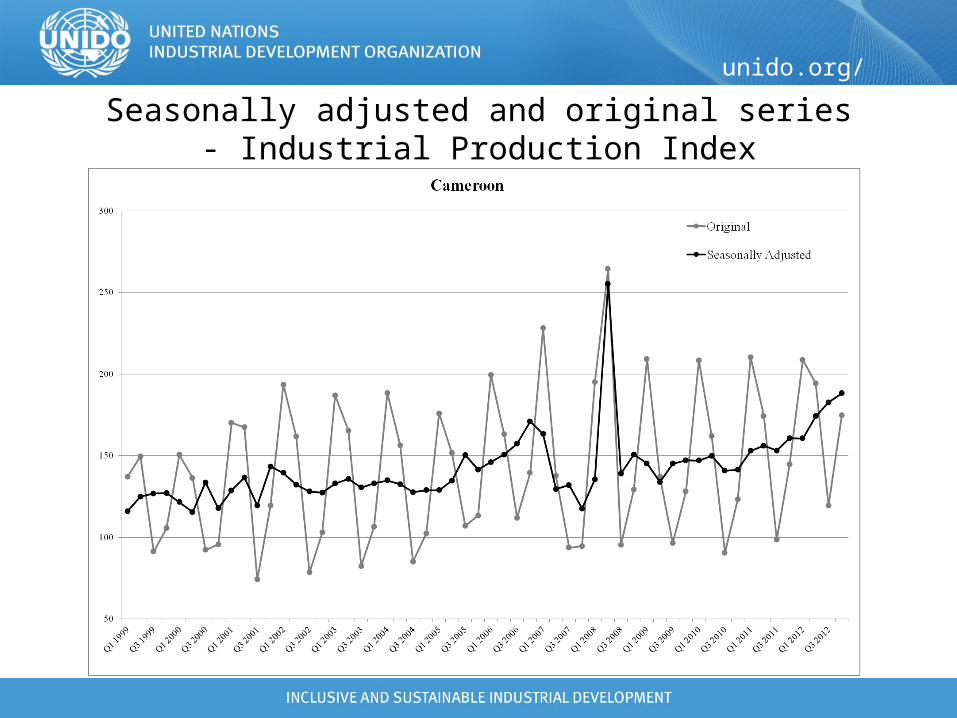

unido.org/statisticsSeasonally adjusted and original series

- Industrial Production Index

unido.org/statistics

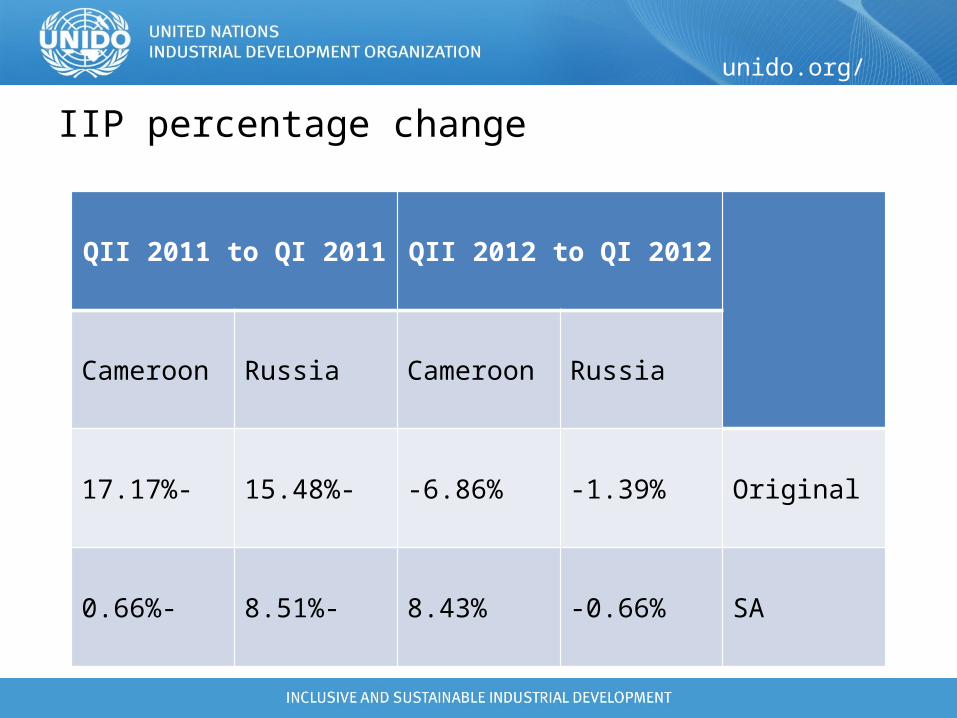

IIP percentage change

QII 2011 to QI 2011 QII 2012 to QI 2012

Cameroon Russia Cameroon Russia

-17.17% -15.48% -6.86% -1.39% Original

-0.66% -8.51% 8.43% -0.66% SA

unido.org/statistics

Why seasonally adjust?• To aid in short term forecasting

• To aid in relating time series to other series including comparison of time series from different countries

• To allow series to be compared from month to month, quarter to quarter

• to see the real movements and turning points in manufacturing production, which may be impossible or difficult to see due to seasonal movements

unido.org/statistics

Seasonal Adjustment

• The process of estimating and removing the Seasonal Effects and filtering out the systematic calendar related influences from the original IIP time series

• One common misconception is that Seasonal Adjustment will also hide any outliers present. This is not the case: if there is some kind of unusual event, we need that information for analysis, and outliers are included in the Seasonally Adjusted series

unido.org/statistics

Seasonal Adjustment• Facilitates the comparison of long-term and short-term

movements among series and countries

• Fluctuations due to exceptionally strong or weak seasonal influences will continue to be visible in the seasonally adjusted series. In general, other random disruptions and unusual movements that are readily understandable in economic terms (for example the consequences of economic policy, large scale orders or strikes) will also continue to be visible

unido.org/statistics

Seasonal Adjustment

• the Seasonally Adjusted results do not show “normal” and repeating events, they provide an estimate for what is new in the series which is the ultimate goal of Seasonal Adjustment

unido.org/statistics

Costs and Risks• Seasonal Adjustment is time consuming, significant

computer/human resources must be dedicated to this task

• Inappropriate or low-quality Seasonal Adjustment can generate misleading results and increase the probability of false signals (credibility effects)

• The presence of residual seasonality, as well as over-smoothing, are concrete risks which could negatively affect the interpretation of Seasonally Adjusted data

unido.org/statistics

Seasonal adjustment methods

• Model based method– TRAMO/SEATS

• Filter based method– X12-ARIMA

unido.org/statistics

TRAMO/ SEATS• TRAMO (Time Series Regression with ARIMA Noise,

Missing Observations and Outliers) and SEATS (Signal Extraction in ARIMA Time Series) developed by Victor Gómez and Agustin Maravall at Bank of Spain.

• The two programs are intensively used at present by data-producing and economic agencies, including Eurostat and the European Central Bank.

• Programs TRAMO and SEATS provide a fully model-based method for forecasting and signal extraction in univariate time series. Due to the model-based features, it becomes a powerful tool for a detailed analysis of series.

unido.org/statistics

Demetra+• When choosing a seasonal adjustment (SA) program, statistical agencies

have had at least two different options in the past: X-12-ARIMA and TRAMO/ SEATS.

• Nowadays, combined software packages exist which merge functionalities of X-12-ARIMA and TRAMO/SEATS: Demetra+.

• Users may thus choose between these approaches for each particular time series under review without switching between different programs.

unido.org/statistics

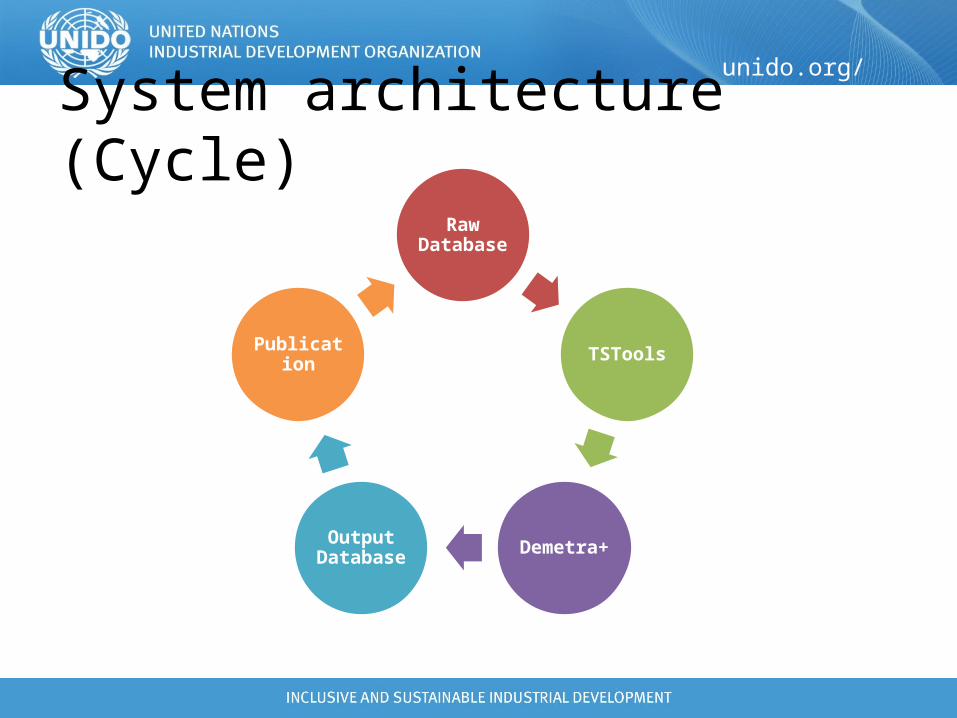

System architecture (Cycle)

Raw Database

TSTools

Demetra+Output Database

Publication

unido.org/statistics

Revision• Three types of Revision Policy

– Current Adjustment → adjusts with fixed specification, user defined regression variables can be updated

– Semi-concurrent Revision → re-estimates respective parameters and factors every time new or revised observation become available

– Concurrent Adjustment → adjustment performed without any fixed specifications

unido.org/statistics

UNIDO experience (IIP)• 334 time series

• Quality of the time series

– Short time series: minimum 3 years long for monthly and 4 years long for quarterly

• Revision policy: semi-concurrent revision (once a year)

• 4 quarterly reports on the world manufacturing production using SA data have been released

unido.org/statistics

Suggestions and recommendations• Aggregation approach

– Indirect approach– Direct adjustment

• It is highly recommended to perform the SA at country level

• Revision policy

• Publication policy– When seasonality is present and can be identified, series should be

made available in seasonally adjusted form. – The method and software used should be explicitly mentioned in the

metadata accompanying the series.

unido.org/statistics

• Countries with no SA experience are encouraged to compile, maintain and update their national calendars or, as a minimal alternative, to supply an historical list of public holidays including, whenever possible, information on compensation holidays. Moreover providing the calendar for the year t+1 or the corresponding holidays

• Users of Seasonally Adjusted data should be aware that their usefulness for econometric modeling purposes needs to be carefully considered

unido.org/statistics

Thank you for your attention!