UAP - OLD MUTUAL MicroInsurance Brief€¦ · 0 uap - old mutual microinsurance brief where we are...

19

0 UAP - OLD MUTUAL MicroInsurance Brief WHERE WE ARE WHERE WE ASPIRE TO BE BECOMING AFRICA’S FINANCIAL SERVICES CHAMPION COUNTRY : KENYA BUSINESS LINE: GENERAL INSURANCE

Transcript of UAP - OLD MUTUAL MicroInsurance Brief€¦ · 0 uap - old mutual microinsurance brief where we are...

0

UAP - OLD MUTUAL

MicroInsurance Brief

WHERE WE ARE

WHERE WE ASPIRE TO BE

BECOMING AFRICA’S FINANCIAL SERVICES

CHAMPION

COUNTRY : KENYA BUSINESS LINE: GENERAL INSURANCE

1

n UAP Microinsurance Basic Design & Experience 1. AfyaKamili 2. SalamaSure 3. Kilimo Salama

Content

n Successes factors and Challenges

n Key Success factor for future growth

2

AfyaKamili – Micro Health Insurance Product

Value Proposition:

Full payment Inpatient and Surgical procedures, no co-pays.

Flexible premium payment plans. (Two Options) • IPF (With Financiers) • Installments: up to 10 monthly installments

Savings For Health: Mobile wallet(MSA) allows you to save for cover.

Affordable cover irrespective of the family size. From Kes 4,000 Per Year, 300 Per Month

Cash Back: Outpatient under member savings account; unutilized money rolled over.

Outpatient can be topped up, -MSA - ‘MPesa style’

AfyaKamili - Product Structure

Supplementary Inpatient cover: • Covers for Surgical

Claims • Pays for co-pays of the

all surgical procedures up to Kes 15,000

• Pays for 50% Dialysis procedure for each event up to Kes 2,500 at referral hospitals only.

Personal Accident Cover – Kshs 50, 000 • Funeral expense for

both Principal Member and/ or Spouse of Kes 50, 000 due to illness or accident.

• Total Permanent Disability-Kes. 50, 000.

Outpatient cover • Member’s savings

account Min. Kes. 5, 000. • The cost of consultation,

diagnosis and medication is drawn from the member’s savings account (MSA).

• This amount is refundable / rolled over to the next period when unutilized. (Unutilized money back guarantee).

• Savings on mobile health wallet

Inpatient:

• This component is provided by NHIF

• The benefit pays all inpatient hospitalization treatments due to illness.

• NHIF pays for surgical procedures net of co-payment of Kes. 15,000.

• Dialysis at referral hospitals payable up to 50%, Max Kes.2, 500.

• One MUST have a valid NHIF card

AfyaKamili Experience

Presentation Title : OMEM IT Page 4

Sales - Three months pilot

covered Approx..

1,350 people

Claims Experience –

Commendable ; less than 25%.

Clientele included corporate

schemes for low category

employees and self sponsored

individuals.

High signups during

campaigns and activations and

convention channels are interested to

distribute micro products

Aggregators distribution

worked

The challenges common to

micro insurance are not unique to this market

but their sensitivity to success is

higher than the convectional

insurance market

Product development

needs to bear in mind behavioral

economics of targeted low end market

clientele.

Supplementary cover and

partnerships between

private sector, public sector have a place in successful

product distribution.

AfyaKamili – Factors That Attributed to Success and Challenges

Factors that Attributed to Success

Factors that Attributed

to Challenges

Presentation Title : OMEM IT Page 5

Aggressive Marketing and

Communication- Activations, Testimonials

campaign - ; White labelling, Opinion leaders

Aggregator & Affinity model;

Distribution partners UNAITAS, MobiKover

Adopting Technology for

product Administration

(sign up, claims etc.)

and Distribution,

Limited / inadequate Partners – Medical Service providers

Limited Insurance principle and practice

knowledge among clients and MSP

High rate of lapses policies

Fraud among clients and

MSP

6

■ UAP Microinsurance Basic Design & Experience 1. AfyaKamili 2. SalamaSure 3. Kilimo Salama

CONTENT

n Successes factors and Challenges

n Key Success factor for future growth

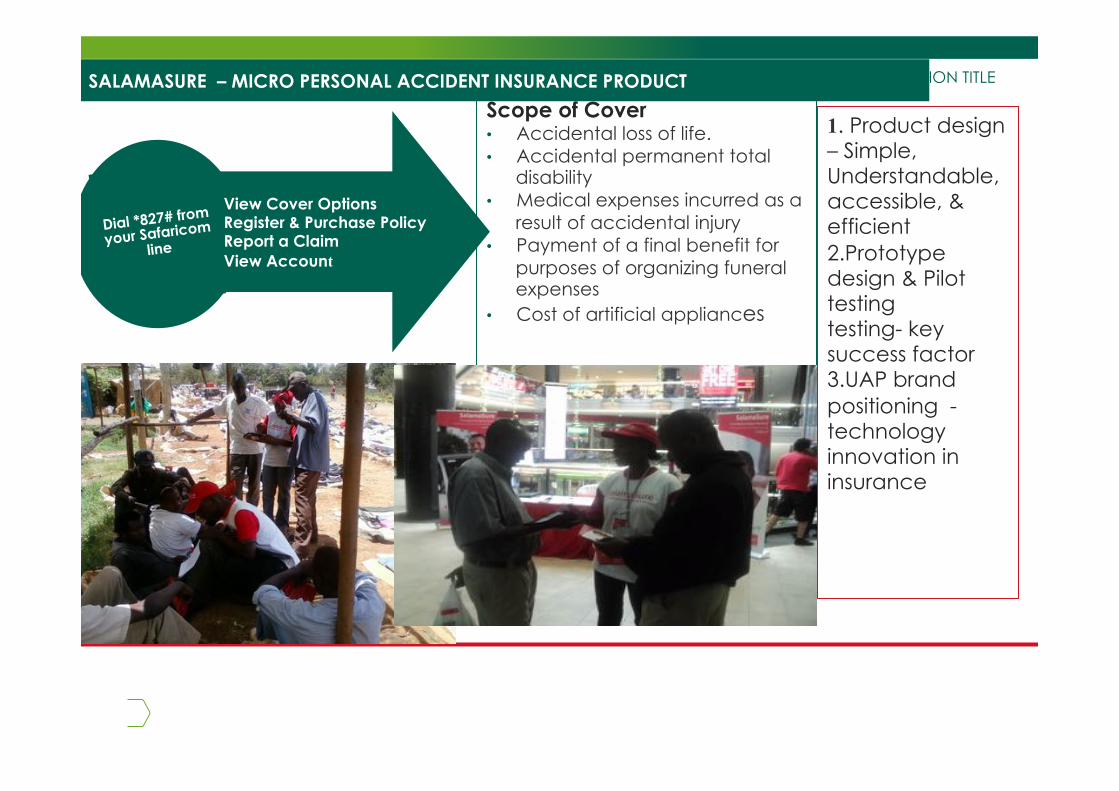

PRESENTATION TITLE SALAMASURE – MICRO PERSONAL ACCIDENT INSURANCE PRODUCT

Dial *827# from

your Safaricom

line

View Cover Options Register & Purchase Policy Report a Claim View Account

Scope of Cover • Accidental loss of life. • Accidental permanent total

disability. • Medical expenses incurred as a

result of accidental injury • Payment of a final benefit for

purposes of organizing funeral expenses.

• Cost of artificial appliances

1. Product design – Simple, Understandable, accessible, & efficient 2.Prototype design & Pilot testing testing- key success factor 3.UAP brand positioning - technology innovation in insurance

8

■ UAP Microinsurance Basic Design & Experience 1. AfyaKamili 2. SalamaSure 3. Kilimo Salama

CONTENT

n Key Success factor for future growth

THE MANDATE OF KILIMO SALAMA

9

“Develop and implement agricultural insurance products

for smallholder farmers”

PRESENTATION TITLE Traditional Insurance

Large scale farm: US$ 1000 Premium - US$ 50 Visit Costs + US$950, insure

Small scale farm: US$ 10 Premium - US$ 50 Visit Costs - US$ 40, can’t insure

PRESENTATION TITLE We don’t visit the farm

Weather station, district yield data or satellite data

+

agronomic formula’s to model required rainfall

Using rainfall data, a pattern is drawn

and a perfect future is predicted which if arrived at the farmers

targeted farmers will be able to harvest satisfactorily for both home

consumption and some surplus to the market. When the complementary

event happen, indemnification start in proportion to the magnitude of

shortfall.

PRESENTATION TITLE

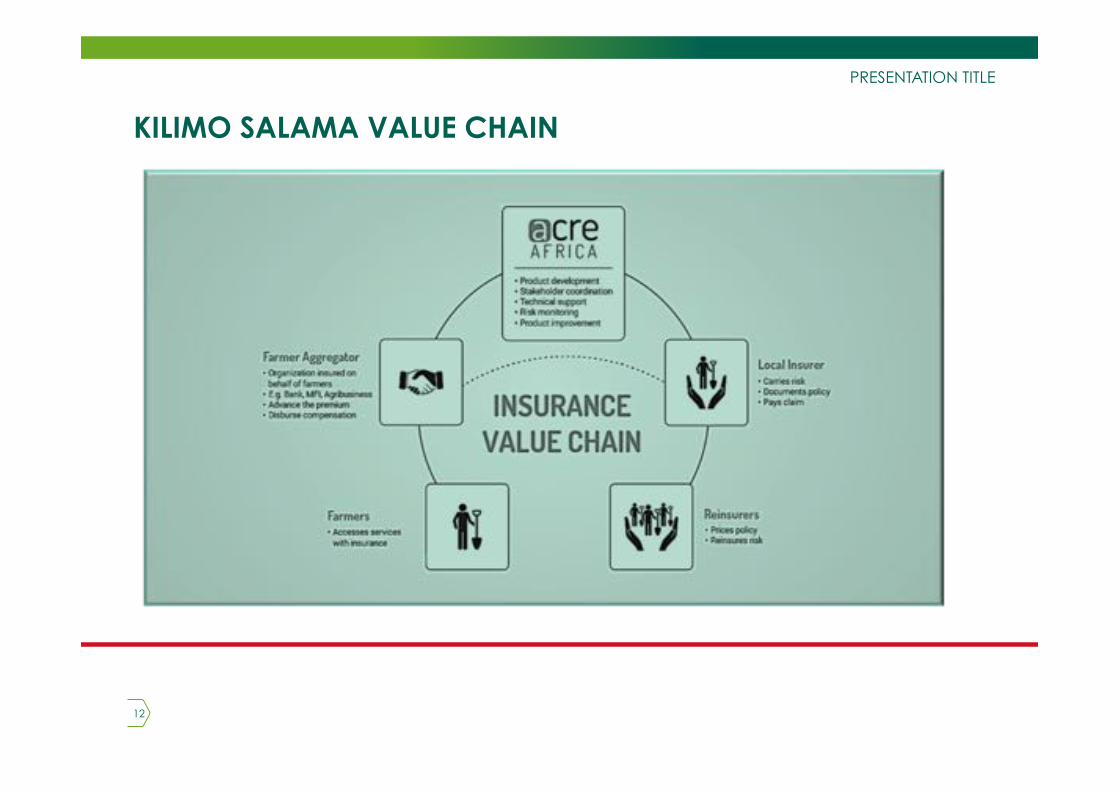

KILIMO SALAMA VALUE CHAIN

12

PRESENTATION TITLE END TO END OPERATION REVIEW

Needs assessment

Index design & incorporation in a policy

Reinsurance arrangement

Communication to the customer acceptance and premium payment through MNOs

Cover commencement and M&E

Season outcome analysis and communication to the customer

Claims payment .

13

PRESENTATION TITLE

KILIMO SALAMA EXPERIENCE

Distribution channels: seed distribution linked to a mobile network operator’s location service, agribusinesses with out-

growers or contracted farmers, lending institutions and savings and credit cooperatives (SACCOs) providing input loans, and

medium-scale professional farmers.

Crops insured include maize, sorghum, coffee, sun -flower, wheat, and potato, with coverage against drought, excess rain

and storms.

Cumulatively, by 2015, over 800,000 farmers in Kenya, Tanzania and Rwanda insured over 646 million USD against a variety of

weather risks.

14

KILIMO SALAMA CHALLENGES ….

• Aggregators - Delay in releasing loan results in yield losses, Farmers default when they know that there is insurance and Banks focus: we want our credit repaid

• Basis Risk- There is data gaps in most of the Historical data for the last 30 years. In some cases the data quality is not high. Both cases comprise the index precision. The positioning of the farmer relative to the weather station is sometimes remote leading to a mismatch in the outcome of index and the true production. We have tried to resolve this through a hybrid solution where one component is an MPCI. Nevertheless this remain a challenge and in many cases we pay some farmers on ex-gratia basis.

• Critical Mass We are yet to reach a critical mass where the solution can run on its own without external funding. We have relooked into the initial idea of insuring small scale to medium scale farmers

16

■ UAP Microinsurance Basic Design & Experience 1. AfyaKamili 2. SalamaSure 3. Kilimo Salama

CONTENT

n Key Success factor for future growth

17

Conducive regulatory

environment / micro

insurance policy /

framework

Collaboration between private

insurers, government/ quasi

government institutions including public sector and NGOS focused on

healthcare and agriculture funding.

Leveraging on mobile technology:

Innovations around the growing mobile

technology industry to drive distribution and

operational excellence.

This will in turn lower the cost of distribution

and administration costs.

Strategic and innovative product development: Product development

models should have a bias on behavioral economics.

In depth longitudinal research to study consumer

behaviors and create propositions around the

consumer lives.

Customer centricity behavior focused on winning customers/ the masses and not

pushing products. Good definition of customer journey and experience

mapping through the entire life cycle.

KEY SUCCESS FACTOR FOR FUTURE GROWTH

Thank you