NUS IPS Young Singaporeans Conference 2012 : Are Young Singaporeans Happy?

Upload

chew-zhan-lunCategory

view

520download

2

Types of Insurance Policies Owned by

Singaporeans

MONEY 101

SEMINAR GROUP 02

LAM HUI PING | LEE TYNG TYNG, YVONNE | LUI WEI SIANG | CHEW ZHAN LUN

Overview of Today’s Presentation

Why Insurance?What is comprehensive financial planning?

Types of Insurance PolicyWhole Life PolicyTerm PolicyEndowment PolicyInvestment-linked Policy

Add-OnsRiders

Case StudyInsurance for young adults

Why Insurance?

Why Insurance? Types of Insurance Add-Ons Case Study

Comprehensive Financial Planning

Risk Management

• Insurance• Protections

WealthAccumulation

• Savings• Investment• RetirementComprehensive

Financial Planning

Main Goal:• To reserve for emergency

needs• To ensure comfortable

future for ourselves and our loved ones

Main Goal:• To have comprehensive

protections for ourselves and our loved ones

• To have access to adequate care when needed

Why Insurance? Types of Insurance Add-Ons Case Study

Five Key Considerations under Risk Management

Risk Management

• Insurance• Protection

Death/ Total and Permanent Disability

Critical Illness

Disability Income

Hospitalization

Accident

Types of Insurance

Why Insurance? Types of Insurance Add-Ons Case Study

Four Types of Insurance Policy

Whole Life Policy Term Policy

Endowment Policy Investment-linked Policy

Why Insurance? Types of Insurance Add-Ons Case Study

Four Types of Insurance Policy

Whole Life Policy Term Policy

Endowment Policy Investment-linked Policy

Why Insurance? Types of Insurance Add-Ons Case Study

Whole Life Policy

Purchase at age 20

Premium payment term ends

Payment of premium for 25 years

Insured for entire life

Death/ TPD

• A type of insurance policy that provides lifelong insurance protection for the policyholders and their dependents in the event of death, total and permanent disability and terminal illness

What is Whole Life Policy

Why Insurance? Types of Insurance Add-Ons Case Study

Whole Life PolicyWhole life policy usually are available in different forms:

Participating(Par)

Non-Participating(Non-par)

Investment-linked(ILP)

• Pay bonuses, building up cash values

• Upon the death of the insured, par policies usually pay the basic sum assured plus any bonuses accumulated to date as the death benefit

• Do not pay bonuses but will build up some cash value over time

• These cash values are guaranteed and are paid out if the policy is surrendered early

• The death benefit comprises the sum assured only

• Payment upon the death of the insured may be the higher of sum assured or the value of the ILP units at the time, or some combination of sum assured plus the value of the ILP units

Most whole life policies in Singapore are in participating form

Why Insurance? Types of Insurance Add-Ons Case Study

Whole Life Policy

• It provides a lifetime protection for policyholders and their dependents

• IPL or par policies are not just paying for insurance coverage, some of the premiums are paid/ invested into a fund to grow money

• Par policies provide guaranteed (i.e. sum assured) and non-guaranteed (i.e. bonus/ cash dividends) benefits

• Premiums are usually fixed throughout the policy

• There is option to withdraw cash value before death

• Premium can be expensive because the policy doesn't’t expire and usually includes a saving component

• It requires long-term commitment and affordability

• Early termination of the policy usually involves high costs and the surrender value may be less than total premiums paid

• Potentially may not meet short to medium term saving goals, as there is no cash values in the early years

Pros Cons

Why Insurance? Types of Insurance Add-Ons Case Study

Whole Life Policy

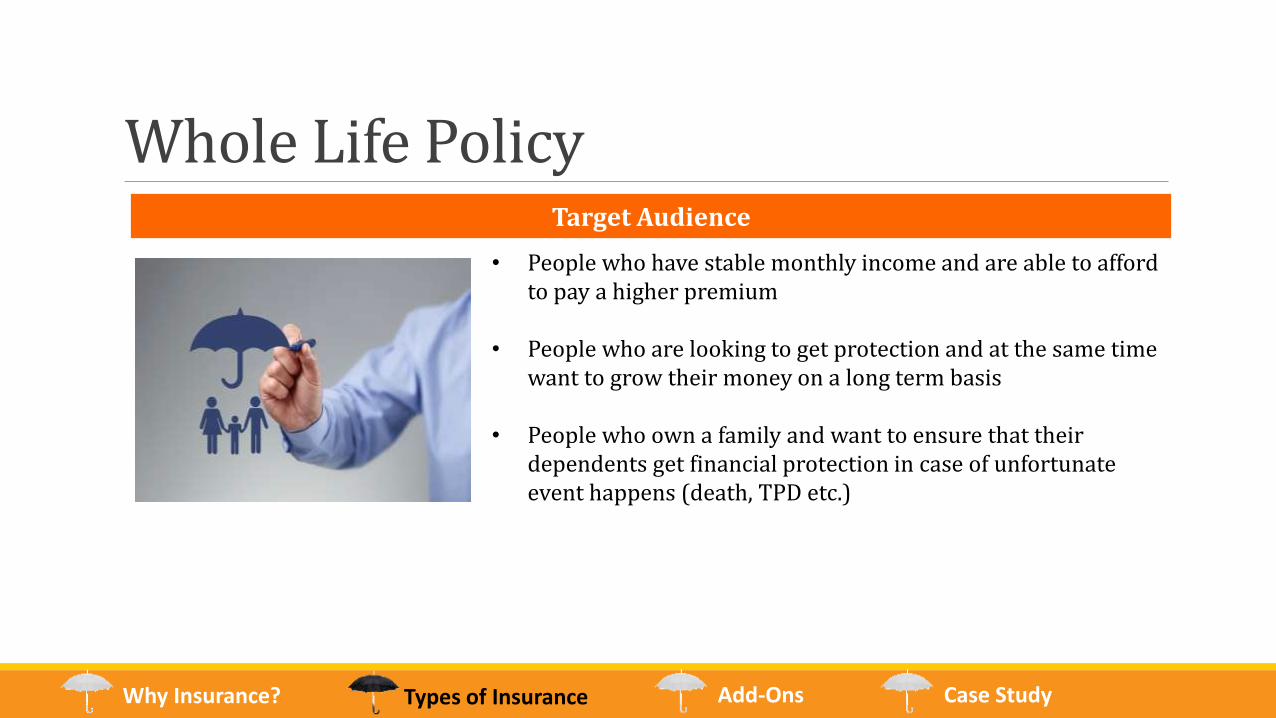

• People who have stable monthly income and are able to afford to pay a higher premium

• People who are looking to get protection and at the same time want to grow their money on a long term basis

• People who own a family and want to ensure that their dependents get financial protection in case of unfortunate event happens (death, TPD etc.)

Target Audience

Why Insurance? Types of Insurance Add-Ons Case Study

Four Types of Insurance Policy

Whole Life Policy Term Policy

Endowment Policy Investment-linked Policy

Why Insurance? Types of Insurance Add-Ons Case Study

What is Term Policy?

Term Policy

Purchases 5 years term insurance

Term insurance lapsed / terminated

Insured for5 years

Not insured

• A type of insurance policy that provides coverage for a certain period of time.

Why Insurance? Types of Insurance Add-Ons Case Study

Term PolicyPurchases 5 years term insurance

Term insurance lapsed / terminatedDies Dies

Pros Cons

• Very affordable, low premiumo With $25,000, a 25 year old non-smoker will

be able to purchase a 60-year term policy. As compared to life policy, this amount is insufficient to even pay for ½ of a 20-year life policy.

o Low penalty if policy is terminated prematurely

• Flexible• Covers only the period that you want to be insured

• More flexibility but lose being insured for period after policy lapses, i.e. when you stop paying premiums, unlike life policies

• Premium increases significantly after policy lapses, even if it is the same policy

• Only insures up to 85 years old

Why Insurance? Types of Insurance Add-Ons Case Study

Examples of Term Policies

Target Audience

Term Policy

• People with tight budget, would like to be temporarily insured until they switch to life policy in the future

• People whose needs do not require life insurance, and a term insurance would be more economical

• Car insurance• Travel insurance• Home fire insurance

• Accident plan• Workmen compensation• Death

Why Insurance? Types of Insurance Add-Ons Case Study

Four Types of Insurance Policy

Whole Life Policy Term Policy

Endowment Policy Investment-linked Policy

Why Insurance? Types of Insurance Add-Ons Case Study

What is an Endowment Policy?

Endowment Policy

Premium of $8,000 per year$160,000 in total

Insurance Savings

Total Permanent Disability / Death

Invested in funds

E.g. 20 year education plan

• A type of insurance policy that allows you to save and meet your financial goals.• Also commonly known as forced savings.

Why Insurance? Types of Insurance Add-Ons Case Study

ConsPros

Endowment Policy

• Flexibleo Can choose a duration of 10, 15, 20 years and

so on for the endowment policyo Can choose how you want to pay the

premium, Quarterly Semi-annually Annually

• If person who purchased the endowment policy for his dependent dies, dependent will still be able to receive the sum of money for his education + sum insured for death

• Although plan may be “education plan”, payout received at period end can be used for any purpose

• Due to the small portion paid for insurance, guaranteed amount at end period may be less than the total premiums paid. Whether or not net returns are positive depends on the non-guaranteed amount invested in funds

• There is a possibility of getting paid less at the end of the period than the total premiums paid over the years

• Insufficient to depend on endowment policies’ insurance for protection as it is a very small portion and coverage is minimal

• Policy would lapse if premium is not paid. All previously paid premiums would be forfeited

Why Insurance? Types of Insurance Add-Ons Case Study

Examples of Endowment Policies

Target Audience

Endowment Policy

• Any persons who has a financial goal and would like to meet it by the end of a certain period in a systematic way

• Any persons who foresee that they will require a lump sum amount by a certain year

• Retirement plans• Tertiary education plans for child(ren)

Why Insurance? Types of Insurance Add-Ons Case Study

Four Types of Insurance Policy

Whole Life Policy Term Policy

Endowment Policy Investment-linked Policy

Why Insurance? Types of Insurance Add-Ons Case Study

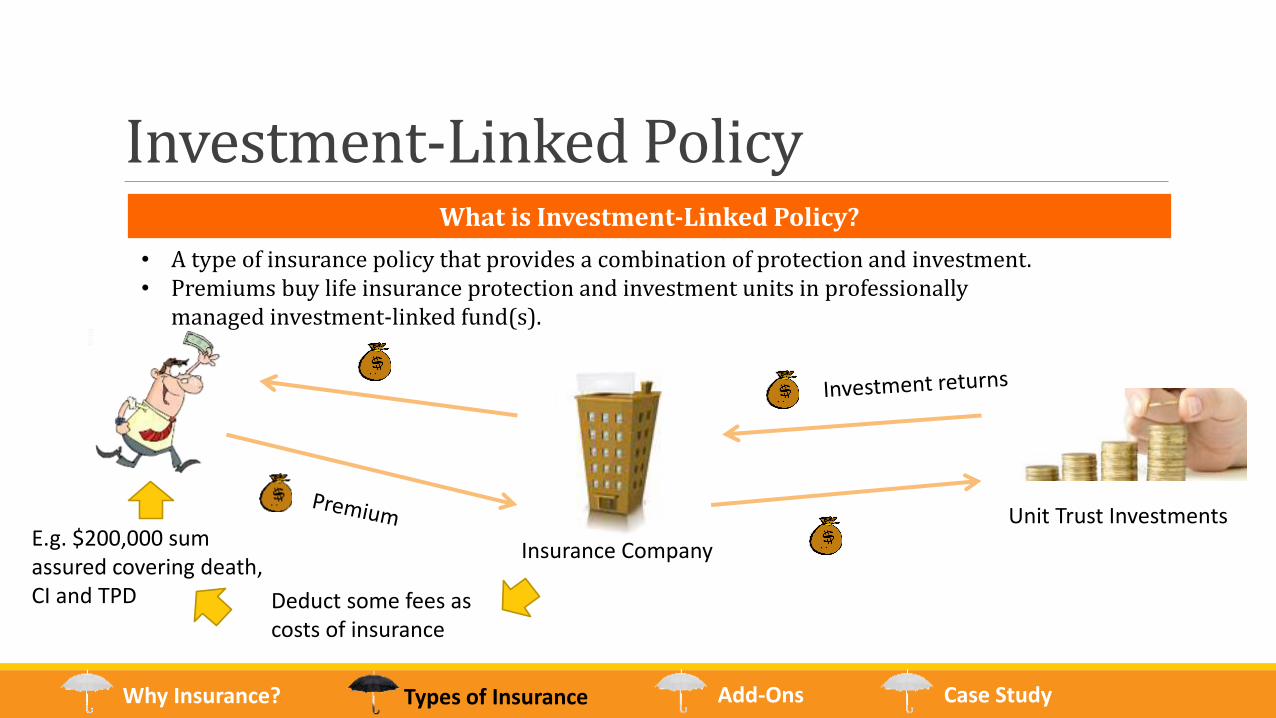

Investment-Linked Policy

• A type of insurance policy that provides a combination of protection and investment. • Premiums buy life insurance protection and investment units in professionally

managed investment-linked fund(s).

What is Investment-Linked Policy?

Insurance Company

Unit Trust Investments

Deduct some fees as costs of insurance

E.g. $200,000 sum assured covering death, CI and TPD

Why Insurance? Types of Insurance Add-Ons Case Study

Investment-Linked PolicyYear Premium Total

AccumulatedPremiums

Allocation Rates

Premium Invested Before Subtracting Cost

of Insurance

1 $ 6,000 $ 6,000 20% $ 1,200

2 $ 6,000 $ 12,000 30% $ 1,800

3 $ 6,000 $ 18,000 55% $ 3,300

4 $ 6,000 $ 24,000 105% $ 6,300

5 $ 6,000 $ 30,000 105% $ 6,300

6 $ 6,000 $ 36,000 105% $ 6,300

7 $ 6,000 $ 42,000 105% $ 6,300

During initial few years, only a small portion of the premium paid is invested in the funds

The remaining amount is used to pay administrative fees such as fund management fees

This is even before the cost of insurance is taken into account

Why Insurance? Types of Insurance Add-Ons Case Study

Investment-Linked Policy

Investments

Cost of insuranceInvestments

Cost of insuranceInvestments Cost of insurance

When we are young As we grow older There will be a point

• Initially, the pie is small as we just started paying premiums and only a small portion is allocated to the funds

• Cost of insurance is low

• Pie size increases as premiums accumulate and investments generates returns

• Cost of insurance also increases

• Pie size continues to increases

• Costs of insurance increases much more than pie size as we get older

Why Insurance? Types of Insurance Add-Ons Case Study

Investment-Linked Policy

Age

Value of ILP

Value of ILP across time

• As you pay more premiums and the investments generate returns, value of your ILP increases

• But there will be a point where the cost of insurance will be so large that it eats up your previously accumulated amounts

Why Insurance? Types of Insurance Add-Ons Case Study

Investment-Linked PolicyPros Cons

• Higher returns as compared to endowments

• No maturity date, can transfer policy to child

• Flexible – Can increase or decrease the sum assured anytime

• Free fund switching – no fees charged when you want to switch funds

• Can choose to use cash value to pay premiums if you are unable to fork out the cash (Premium Holiday)

• Allocation rates are extremely low at the beginning few years

• Cost of insurance increases as you get older and may eliminate your investment returns

• ILP value fluctuates with the market

• Sum insured is small compared to whole life and term policies

Why Insurance? Types of Insurance Add-Ons Case Study

Investment-Linked Policy

• Young adults who just started working and are looking to accumulate their wealth with added insurance coverage. Furthermore, cost of insurance is low when you are younger

• People who wants both investments and insurance coverage but are looking more for wealth accumulation rather than protection

Target Audience

Add-Ons (Riders)

Why Insurance? Types of Insurance Add-Ons Case Study

Riders“A rider is a provision of an insurance policy that is purchased separately from the basic

policy and that provides additional benefits at additional cost.”

Case Study

Why Insurance? Types of Insurance Add-Ons Case Study

Case Study

• Name: Mr Lui Wei Siang

• Age: 24

• More about Mr Lui:

o Fresh graduate, all ready to climb the corporate ladder!

o Auditor at KPMG

o Starting salary of $3000

Profile

Why Insurance? Types of Insurance Add-Ons Case Study

Case Study

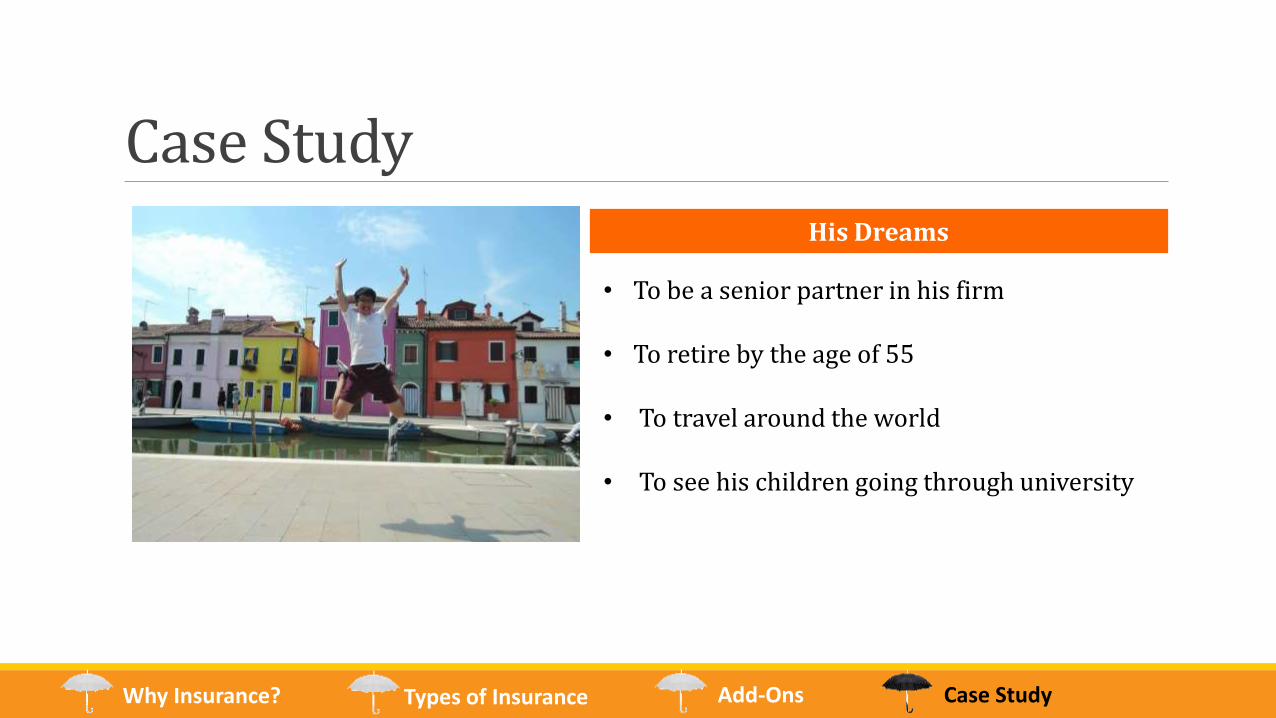

• To be a senior partner in his firm

• To retire by the age of 55

• To travel around the world

• To see his children going through university

His Dreams

Why Insurance? Types of Insurance Add-Ons Case Study

Case Study

• Who will take care of him if he cannot work?

• Who will take care of his family if he is no longer around?

• Will he have enough money for retirement?

• Will his children be able to start their lives with the right foundations?

His Worries

Why Insurance? Types of Insurance Add-Ons Case Study

And so, he starts to ponder…

Why Insurance? Types of Insurance Add-Ons Case Study

His Cash FlowCurrent Income: $Basic Income 3000Less: CPF Contribution (600)Take-home Income 2400

Expenses:Family Expenses 400School Loans 500Insurance Premiums 0Personal Savings 300

Transportation Expenses 100Personal Expenses 500Other Expenses 200Total Cash Outflow 2000

Surplus 400

Why Insurance? Types of Insurance Add-Ons Case Study

His Current Needs

Hospitalization Coverage was paid by his parents

Why Insurance? Types of Insurance Add-Ons Case Study

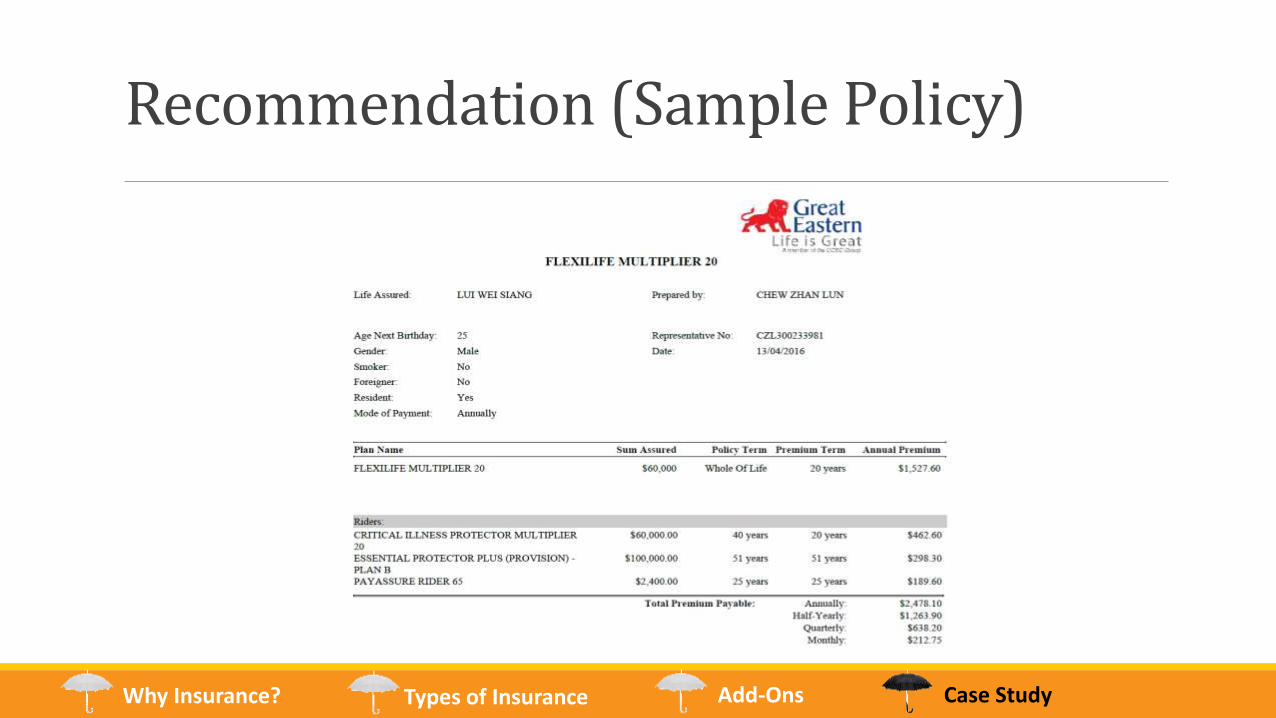

Recommendation (Sample Policy)

Why Insurance? Types of Insurance Add-Ons Case Study

At a Glance

Policy Name Policy Type Main Coverage Details Annual Premiums

FlexiLife Multiplier 20 Whole Life 3 times of $60,000 for Death & TPD for up to 65 old.

$1,527.60

Critical Illness Protector Multiplier 20

Whole Life 3 times of $60,000 for 37 Critical Illnesses for up to 65 years old.

$462.60

Essential Protector Plus – Plan B

Term Personal Accident Plan $298.30

PayAssure Rider 65 Term Monthly Disability Income of $2,400

$189.60

Why Insurance? Types of Insurance Add-Ons Case Study

All ready to conquer the world!

Thank you!

References

References:

Monetary Authority Singapore. (2014, July 17). Particiapting Policies. Retrieved April 7, 2016, from MoneySense: http://www.moneysense.gov.sg/Understanding-Financial-Products/Insurance/Types-of-Insurance/Life-insurance/Types-of-Life-Insurance/Participating-Policies.aspx

Monetary Authority of Singapore. (2014, July 17). Whole Life Insurance. Retrieved April 7, 2016, from MoneySense: http://www.moneysense.gov.sg/Understanding-Financial-Products/Insurance/Types-of-Insurance/Life-insurance/Types-of-Life-Insurance/Whole-Life-Insurance.aspx

Universal Life Singapore. (n.d.). Universal Life - Advantages . Retrieved April 10, 2016, from Universal Life: http://universallife.com.sg/advantages

Mok, F. F. (2015, January 27). Universal life insurance popular among the rich. Retrieved April 10, 2016, from AsiaOneBusiness: http://business.asiaone.com/news/universal-life-insurance-popular-among-the-richAviva Singapore. (2016). Term life Vs. Whole life plans. Retrieved April 7, 2016, from Aviva Singapore: https://www.aviva.com.sg/life-and-health/for-individuals/protection_101/term-life-plan-vs-whole-life-plans.html

Higgins, B. (n.d.). What is term insurance? Retrieved April 3, 2016, from Investopedia: http://www.investopedia.com/ask/answers/08/term-life-insurance.asp

Money Smart. (n.d.). Term Life vs Whole Life Insurance – What’s the Difference? Retrieved April 2, 2016, from MoneySmart.sg: http://learn.moneysmart.sg/insurance/understanding-insurance-products/term-life-vs-whole-life-insurance-whats-the-difference/

Monetary Authority Singapore. (2014, July 14). Term Insurance. Retrieved April 8, 2016, from MoneySense: http://www.moneysense.gov.sg/Understanding-Financial-Products/Insurance/Types-of-Insurance/Life-insurance/Types-of-Life-Insurance/Term-Insurance.aspx

Fontinelle, A. (n.d.). The Pros Of An Endowment Life Insurance Policy. Retrieved April 5, 2016, from Investopedia: http://www.investopedia.com/articles/pf/12/endowment_life_insurance.asp

Monetary Authority Singapore. (2014, July 17). Endowment Insurance. Retrieved April 8, 2016, from MoneySense: http://www.moneysense.gov.sg/Understanding-Financial-Products/Insurance/Types-of-Insurance/Life-insurance/Types-of-Life-Insurance/Endowment-Insurance.aspx

Monetary Authority Singapore. (2015, November 26). Your Guide to Investment-Linked Insurance Plans. Retrieved April 7, 2016, from Guides and Articles: http://www.moneysense.gov.sg/~/media/Moneysense/Guides%20and%20Articles/Guides/Investment-linked%20Policies_English.pdf