Translating ALTA into Texan - Texas Land Title Association · BIO Richard Worsham Richard Worsham...

61

Translating ALTA into Texan (Ver. 1.0 – 11-9-15) Presented By RICHARD D. WORSHAM Vice-President/Texan Region Underwriting Counsel WESTCOR LAND TITLE INSURANCE COMPANY 1776 Woodstead Court THE WOODLANDS, TX 77380 281-362-5860 [email protected] Texas Land Title Association Texas Land Title Institute December 3rd & 4th, 2015,San Antonio, Texas

Transcript of Translating ALTA into Texan - Texas Land Title Association · BIO Richard Worsham Richard Worsham...

Translating ALTA into Texan (Ver. 1.0 – 11-9-15)

Presented By

RICHARD D. WORSHAM Vice-President/Texan Region Underwriting Counsel

WESTCOR LAND TITLE INSURANCE COMPANY 1776 Woodstead Court

THE WOODLANDS, TX 77380 281-362-5860

Texas Land Title Association Texas Land Title Institute

December 3rd & 4th, 2015,San Antonio, Texas

BIO

Richard Worsham

Richard Worsham is a 7th generation Texan and a 1985 graduate of the University of

Houston Law Center.

Mr. Worsham spent 10-years as a commercial litigator, 10-years as a title insurance

fee attorney, and is in his 10th year as a title insurance underwriter. As a former fee attorney and

as an underwriter he has worked with most of the underwriters in Texas, and has extensive

experience underwriting commercial transactions in ALTA states.

In September of this year, Mr. Worsham joined Westcor Land Title as Vice-President

and Texas Region Underwriting Counsel, working exclusively with independent title agents.

Richard Worsham has extensive speaking experience, teaching realtors, escrow

officers and attorneys. He has previously spoken here at the Texas Land Title Institute, taught a

webinar for the TLTA, taught at South Texas College of Law’s Annual Real Estate Conference, for

the Houston Bar Association, and this past Summer at the State Bar of Texas' Advanced Real

Estate Seminar. He has taught numerous realtor seminars, and has conducted continuing education

courses in the law offices of many major law firms here in Texas.

1 2015 TLTA Institute Translating ALTA into Texan

Table of Contents

TRANSLATING ALTA INTO TEXAN

CONTENTSINTRODUCTION ............................................................................................................................................. 2

POLICIES ........................................................................................................................................................ 4

ALTA Standard Coverage ........................................................................................................................... 4

ALTA Extended Coverage .......................................................................................................................... 5

ENDORSEMENTS ........................................................................................................................................... 6

ALTA Endorsement Coverage Not Available in Texas ............................................................................... 6

Endorsements that are Substantially the Same Using ALTA and Texas Forms ......................................... 7

Endorsements Where Texas and ALTA Coverage Require Explanation .................................................... 8

Comprehensive Endorsements ................................................................................................................. 8

ALTA Revisions to the Comprehensive Endorsements ............................................................................. 9

Translating the ALTA Comprehensive Coverage Endorsements to Coverage using the Texas T‐19's 10

Survey Coverage (ALTA 25, Survey Deletion).......................................................................................... 11

Access (ALTA 17, 17.1 / TX T‐23) ............................................................................................................ 12

Future Advance/Revolving Credit (ALTA 14, 14.1, 14.2, 43 / TX T‐35) ................................................... 13

Environmental Lien (ALTA 8.1. 8.2 / TX T‐36, 36.1) ................................................................................ 13

Tie‐In (Aggregation) (ALTA 12, 12.1 / T‐16) ............................................................................................ 14

Planned Unit Development (PUD) (ALTA 5, 5.1 / TX T‐17) .................................................................... 15

Non‐Imputation Endorsements (ALTA 15, 15.1, 15.2/ TX 24) ................................................................ 17

Mezzanine Financing ‐ ALTA T‐16 / Texas T‐24.1 .................................................................................... 17

Co‐Insurance (“Me Too”) (ALTA 23/ TX T‐48) ......................................................................................... 18

Assignment of Rents and Leases (ALTA 37, TX T‐27) .............................................................................. 18

Manufactured Housing Unit (“MHU”) (ALTA 7.1, 7.2 / TX T‐31) ............................................................ 19

Condominium Endorsements (ALTA 4, 4.1 / TX T‐28) ............................................................................ 20

Mechanics Lien's and Construction Issues .................................................................................................. 21

TRANSLATING RATE RULES ......................................................................................................................... 23

OTHER ISSUES ............................................................................................................................................. 25

Assignee Language .................................................................................................................................. 25

ICL versus CPL .......................................................................................................................................... 26

Procedural Rule P‐35 and Texas Insurance Code 2703.101(c) ............................................................... 26

CONCLUSION ............................................................................................................................................... 28

Appendix A .................................................................................................................................................. 29

APPENDIX B ‐ GENERAL NOTES ON tx TITLE COVERAGE VERSUS ALTA ...................................................... 31

2 2015 TLTA Institute Translating ALTA into Texan

Translating ALTA into Texan

INTRODUCTION

One of the surprises for the title insurance customer coming into Texas for the first time

is how tightly regulated the Texas title insurance industry is. It contrasts sharply with Texas' carefully

cultivated national reputation for little or no business regulation. While you often meet sophisticated

and experienced counsel who understand and expect Texas' to be different, for others it comes as a

complete surprise. Even if the customer is aware of the differences, or at least that there are

differences, there is a discomfort level in working in a regulatory environment they are not accustomed

to. .

To out of state customers, Texas is the oddball. All of the other States are "ALTA

States," where title insurance forms are sourced from the American Land Title Association, commonly

known by the acronym ALTA. ALTA is not a state or federal regulator, but a trade association

representing the title insurance industry. It creates forms with no obligation for anyone to use them.

Some states subtly alter the ALTA forms and claim them as their own, and some states may allow

limited use of the other forms (California Land Title Association forms being popular in California and

the Rocky Mountain states). Texas is the only state where ALTA forms are not used.

Title Insurance forms in Texas are promulgated by the state regulator, the Texas

Department of Insurance (“TDI”). The confusion is so great among ALTA users, that out of state

customers often mischaracterize the Texas forms as "TLTA forms."

Further, Texas is one of a few states that prohibit modifying forms, and nowhere is the

rule so strict. Procedural Rule P-1 defines both "Policy" and "Endorsement" as those forms

promulgated by the Texas Department of Insurance. Procedural Rule P-35 of the Texas Basic Manual

for Title Insurance states specifically that:

“No Title Insurance Company, Title Insurance Agent, Direct Operation, Escrow Officer, nor any employee, officer, director or agent of any such entity or person, shall issue or deliver any form of

3 2015 TLTA Institute Translating ALTA into Texan

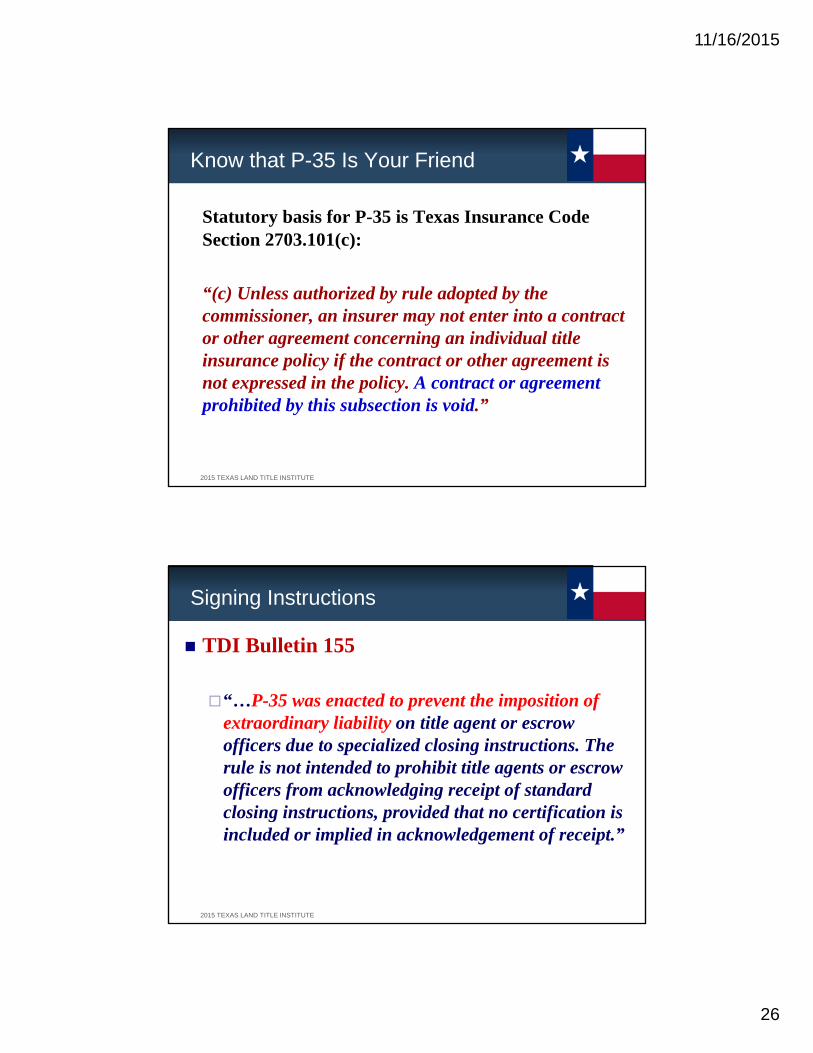

verbal or written guaranty, affirmation, indemnification, or certification of any fact, insurance coverage or conclusion of law to any insured or party to a transaction other than: (i) a statement that a transaction has closed and/or has been funded, (ii) issuance of an insured closing service letter, or any insuring form or endorsement promulgated by the State Board of Insurance, or (iii) certification of copies of documents as being true and exact copies of the original document or of the document recorded in the public records.” Texas Insurance Code Section 2703.101(c) take the issue further, still, stating that,

“Unless authorized by rule adopted by the commissioner, an insurer may not enter into a contract or

other agreement concerning an individual title insurance policy if the contract or other agreement is

not expressed in the policy. A contract or agreement prohibited by this subsection is void.”

That is, according to Texas law, if the title insurance coverage is not on a Texas

Department of Insurance promulgated form, it is not valid title insurance in Texas, or even a binding

contract.

The most difficult problem for the out of state customer can be a lack of understanding

by the title company. As a Texas closer, escrow assistant, attorney, examiner, or underwriter, you have

become accustomed to a certain level of understanding from customers about what you do, and a

common way of speaking about title insurance. The truth is that probably all of us within the title

insurance industry assume an understanding by our clients that does not always exist, but it becomes

particularly difficult when the customer comes from a different experience, with different ideas and

difference preconceptions about what title insurance is or should be. The out of state customer may be

very experienced and quite sophisticated about title insurance under ALTA, but that tends to make

them seem more nonsensical to someone whose experience is limited to Texas. It's important that we

learn how to communicate with our customer in a language they understand. That requires at least a

cursory understanding of the differences between Texas and ALTA, so you can translate instructions

from ALTA to Texan.

4 2015 TLTA Institute Translating ALTA into Texan

POLICIES

While there are several ALTA residential policies, this paper is limited to commercial

closings. The only relevant ALTA policies are loan and owner, each of which comes in a "standard

version" and "extended version".

ALTA Standard Coverage

While the standard ALTA policy and Texas policies are similar, and in places virtually

identical, the substantial difference is that the ALTA policy covers marketable title, or more

specifically, insures against, "unmarketability of the title..." By contrast, the Texas policy insures only

against indefeasible title. In fact, in the policy exclusions, the Texas policy expressly says, "The

following matters are expressly excluded from coverage.....The refusal of any person to purchase, lease

or lend money on the estate or interest covered hereby in the land described in Schedule A because of

Unmarketable Title."

The phrase "marketable title" somewhat varies in interpretation in the various states, but

essentially means the title company insures there are no defects which will affect the marketability of

the property. "Indefeasible title" insures there is no one with a superior right to title who may

challenge ownership. The different standard can change underwriting decisions.

As an example, consider the doctrine of strips and gores. This doctrine says that if

grantor provides a legal description which leaves out a narrow strip which grantor owns, for which

there is no other use by the grantor, it is presumed to have been intended to be conveyed by the grantor

to the grantee. On a subsequent transaction where the putative owner wants the title company to insure

that strip, a title company insuring marketable title would almost always except to ownership of that

strip. By contrast, a title company insuring indefeasible title would only look at whether there is

another party with an adverse claim to that strip, and if they found none, would insure ownership of

that strip missing from the last description. In a marketable title state, the discrepancy in legal

5 2015 TLTA Institute Translating ALTA into Texan

description is an instant claim situation, whereas in an indefeasible title state, a third party must

actually have a claim to the strip before there is a claim on the policy. Whether there is a claim of a

third party to the strip is usually a matter that can be determined by a title exam or survey, making it a

far simpler underwriting decision in Texas versus ALTA states.

People coming into Texas do not always read the policy and understand this nuanced

difference in coverage. Likely the first time they encounter this issue is when they have a claim.

However, on commercial transactions you often get an astute out of state counsel or other experienced

title professional who will look at the policy form and require an explanation. Be prepared to explain,

or know when to call your underwriting counsel and have them explain.

ALTA Extended Coverage

Your instructions from the customer, whether from the lender or from a party to the

transaction, are likely to refer to "ALTA Extended Coverage," or just "ALTA Extended." ALTA

extended coverage provides additional coverage for the following:

Taxes or assessments not shown by the taxing authority or public records.

Defects not in the public records but could be discovered by an inspection of the land or

making inquiry of persons in possession thereof.

Easements, liens or encumbrances which are not shown by the public records.

Problems that a correct survey would disclose, not shown by the public records.

Unpatented mining claims, patent reservations and water rights.

Mechanics Liens not shown by the public records.

Translating that "ALTA Extended" coverage into Texas coverage, this implies:

Survey deletion

Tax Deletion

No Mineral Exception

No "Parties in Possession"

No P-8 mechanics lien exceptions

6 2015 TLTA Institute Translating ALTA into Texan

Possibly T-19 or T-19.1 coverage for encroachments.

However, just because the client asks for extended coverage does not mean they are

entitled to it. If a lender gets an extended coverage policy for a construction loan in an ALTA state,

the policy will likely still come with mechanics lien exceptions. While the phrase "extended coverage"

sets certain expectations of coverage, those expectations are still dependent on circumstance.

Obviously, in Texas, you will issue a standard Loan Policy or Owner's Title Policy as

circumstance dictates, but understanding what the commercial customer is looking for when they say

"extended coverage" may be important to understanding any subsequent discussion about coverage.

ENDORSEMENTS

A quick and dirty count of endorsements indicates there are about 42 available Texas

endorsements and about 105 ALTA endorsements. Both of those counts are probably low, as they

don't account for those endorsements that have been created but not offered, or various permutations of

the endorsements. However, from the ALTA customer's viewpoint, there are a lot of missing

endorsements when they come to Texas. Where did they all go?

ALTA Endorsement Coverage Not Available in Texas

Some of the difference in the number of endorsements can be summarized in those

ALTA endorsements where coverage is simply unavailable in Texas. These include the following

Zoning – ALTA 3.1, 3.2. Insures the zoning designation and that a specific use is allowed.

Tax Lot - Insures that the insured land has its own tax ID# and is not part of any other tax lot ALTA 18 – Multiple Tax Lots ALTA 18.1 – Single Tax Lot

Subdivision – ALTA 26 - Insures the land is a legally created parcel under state law

Address/Improvements – ALTA 22 - Insures loss arising from the failure of the insured land to bear a specific address and/or have certain identified improvements located thereon.

7 2015 TLTA Institute Translating ALTA into Texan

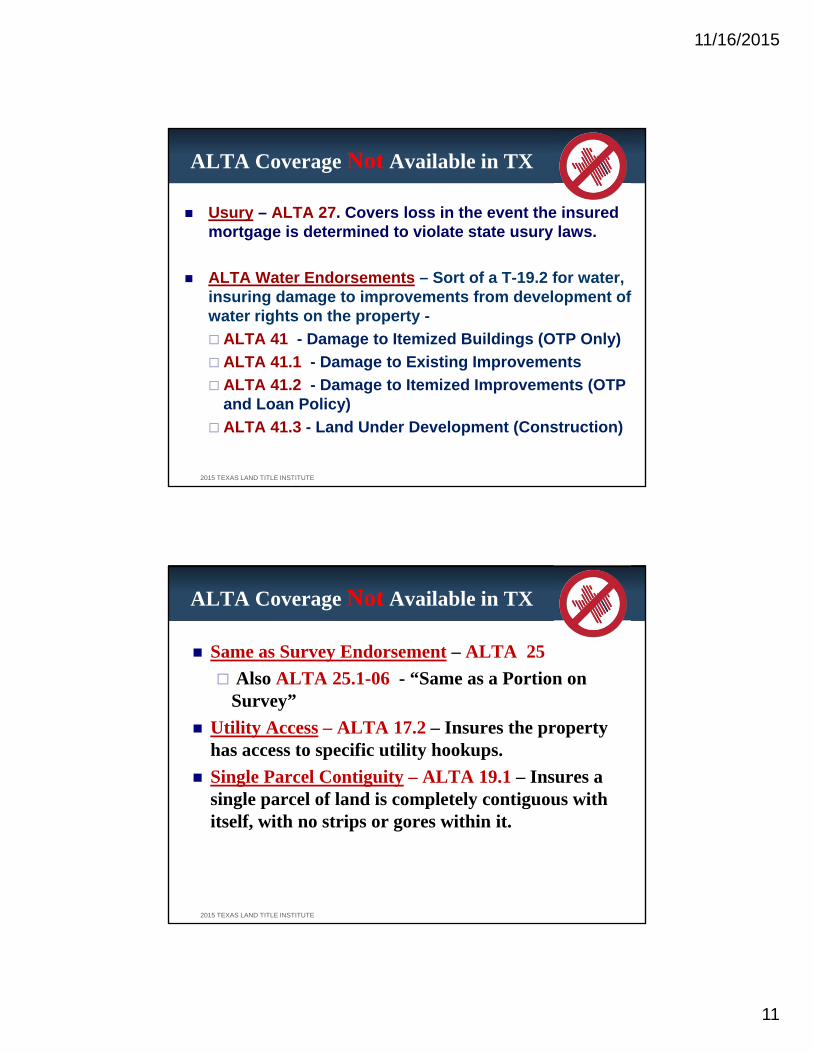

Usury – ALTA 27. Covers loss in the event the insured mortgage is determined to violate state

usury laws.

ALTA Water Endorsements – Sort of a T-19.2 for water, insuring damage to improvements from development of water rights on the property - ALTA 41 - Damage to Itemized Buildings (OTP Only) ALTA 41.1 - Damage to Existing Improvements ALTA 41.2 - Damage to Itemized Improvements (OTP and Loan Policy) ALTA 41.3 - Land Under Development (Construction)

Same as Survey Endorsement – ALTA 25 Also ALTA 25.1-06 - “Same as a Portion on Survey” (However, see survey discussion, below)

Utility Access – ALTA 17.2 – Insures the property has access to specific utility hookups.

Variable Rate – Regulations – ALTA 6.2 – A little used specialized variable rate endorsement carving out coverage for certain regulations specified in the endorsement. (However, other variable rate endorsements discussed below)

Indirect Access - ALTA 17.1 (However, see discussion on access below)

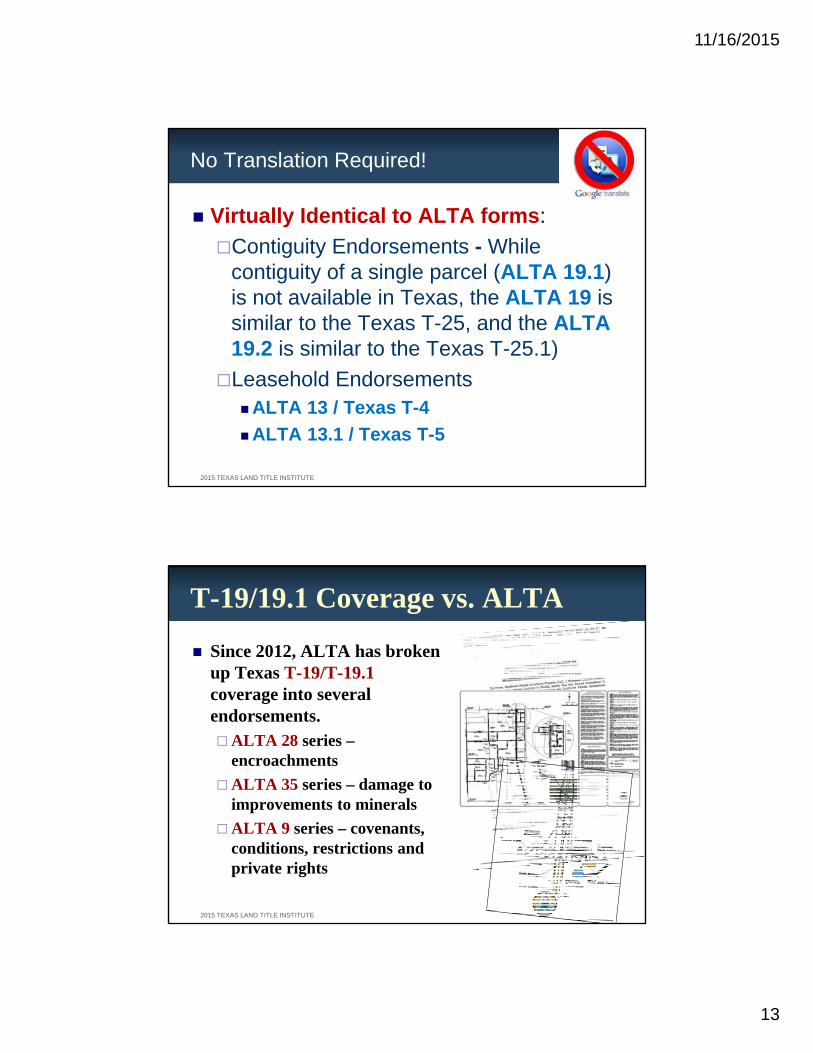

Contiguity (of a Single Parcel) - ALTA 19.1 - ALTA contiguity endorsement which insures a single parcel is contiguous, without any strips or gores within it. Texas contiguity endorsements may only be issued when you have multiple parcels (see discussion below), and this coverage is unavailable in Texas.

"Anti-Taint" endorsement - ALTA 43 - This almost can't be translated, but is a modified revolving credit endorsement insuring priority when a loan is paid down and the principle increased again.

Any time a coverage is not available, customers from out of state may ask you for

alternatives. In some cases there will be none, but for many you need to be able to discuss what

common practice is for this problem in Texas.

Endorsements that are Substantially the Same Using ALTA and Texas Forms

While there are some endorsements that are unavailable in Texas, there are a handful of

endorsements issued by TDI that provide virtually the same coverage as the ALTA forms, and in most

cases have nearly identical language:

8 2015 TLTA Institute Translating ALTA into Texan

First Loss Endorsement – ALTA 20 / Texas T-14

Variable Rate Endorsements o ALTA 6 “Variable Rate” / Texas T-33 “Adjustable Rate” o ALTA 6.2 “Variable Rate – Negative Amortization” / Texas T-33.1 “Adjustable Rate –

Negative Amortization”

Aggregation Endorsements – ALTA 12 / Texas T-16

PUD Endorsement – ALTA 5 / Texas T-17

ALTA 16 “Mezzanine Financing Endorsement" / Texas T-24.1 “Non-Imputation Endorsement (Mezzanine Financing).”

Condominium Endorsement - ALTA 4 / Texas T-28

Contiguity Endorsements - While contiguity of a single parcel (ALTA 19.1) is not available in Texas, the ALTA 19 is similar to the Texas T-25, and the ALTA 19.2 is similar to the Texas T-25.1)

Leasehold Endorsements o ALTA 13 /. Texas T-4 o ALTA 13.1 /. Texas T-5

Endorsements Where Texas and ALTA Coverage Require Explanation

ComprehensiveEndorsements Originally there was the ALTA Form 9 endorsements, consisting of the ALTA 9 and

9.1, for owner and loan policies respectively, commonly called a "comprehensive endorsement," These

insured against losses due to encroachment of improvements, damage to improvements from

development of minerals, and violation of covenants, conditions and restrictions (CCR's). From these

the Texas T-19 and 19.1 were developed. For many years we could say the ALTA and Texas forms

were at least similar, if not the same. That is no longer true.

On the ALTA side these forms continued to develop, coverage was expanded, and in

2012 ALTA fractured the ALTA 9 coverage into a plethora of endorsements separately covering each

of the itemized matters in the original. ALTA 9 forms now primarily cover compliance with CCR's,

9 2015 TLTA Institute Translating ALTA into Texan

ALTA 28 forms cover encroachments, and ALTA 35 forms cover damage due to mineral production.

To confuse things further, there are various versions of each form tailored to particular circumstance.

By contrast Texas kept the T-19 and T-19.1 as comprehensive endorsements covering

multiple issues: violations of CCR's, encroachments, damage due to mineral production. Texas also

added the limited purpose T-19.2 and T-19.3 in 2010, covering only damages due to mineral

production. In 2014, Texas modified and expanded the T-19 and T-19.1 coverage to match some of

the available ALTA coverages, adding coverage for private rights, and adopting carve outs from

coverage and definitions similar to those in the three ALTA forms, the 9, 28 and 35 series.

ALTARevisionstotheComprehensiveEndorsements Between 2012 and 2015 the ALTA Forms Committee extensively revise the ALTA 9 coverage,

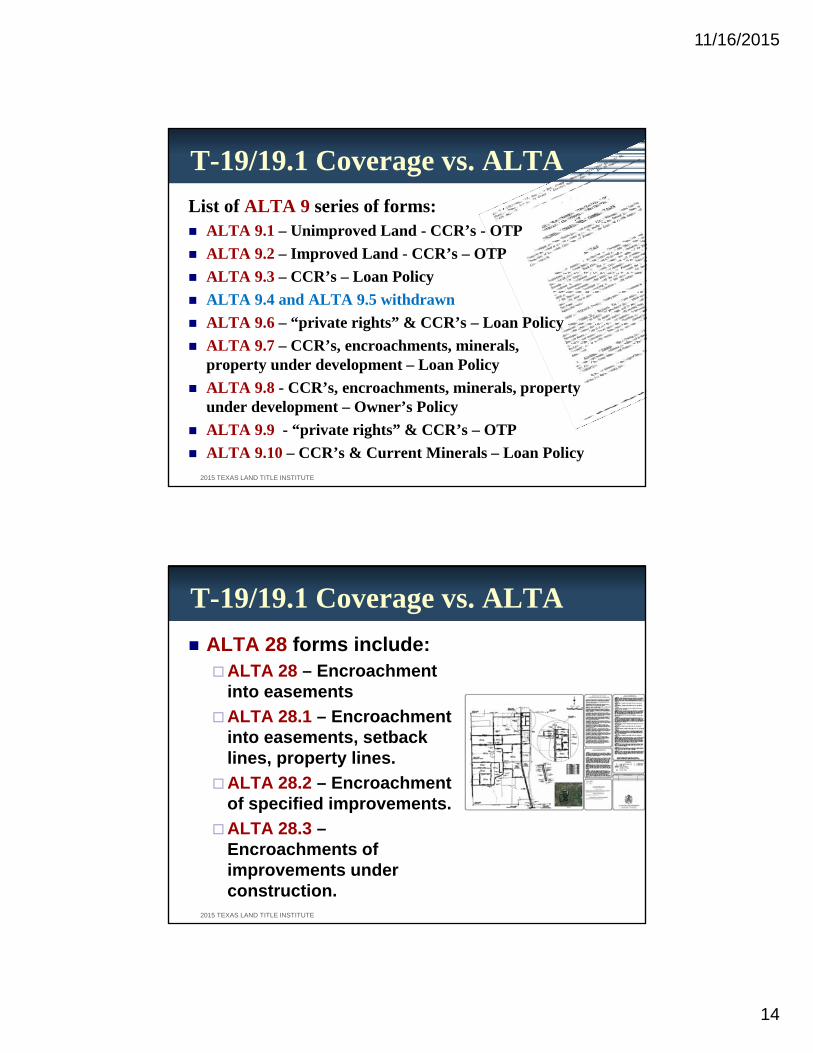

producing 9 different versions of the ALTA 9:

◦ ALTA 9.1 – Unimproved Land - CCR’s - OTP ◦ ALTA 9.2 – Improved Land - CCR’s – OTP ◦ ALTA 9.3 – CCR’s – Loan Policy ◦ ALTA 9.6 – Particular “private rights”, CCR’s – Loan Policy ◦ ALTA 9.6.1 – Same as 9.6, but “private rights” coverage limited to date of policy ◦ ALTA 9.7 – CCR’s, encroachments, minerals, land under development – Loan Policy ◦ ALTA 9.8 – CCR’s, encroachments, minerals, land under development – OTP ◦ ALTA 9.9 – Particular Private Rights and CCR’s – OTP ◦ ALTA 9.10 – CCR’s and Encroachments – Loan Policy

(ALTA 9.4 and ALTA 9.5 were withdrawn in 2012)

Generally, the ALTA 9.1, 9.2, and 9.3 protect the insured from violations of covenants,

conditions and restrictions existing at the time of closing. The ALTA 9.7 and 9.8 provide more

comprehensive coverage for land under development, provided you build the property to particular

defined “Plans.” The ALTA 9.6, 9.6.1, and 9.9 insure against particular private rights, which include

leases, rights of first refusal, options, and, for the loan policy only, private assessments such as

property owner’s association dues. The 9.6.1 was added in April, 2015, for the specific purpose of

limiting the private rights coverage to the date of the policy, to avoid title company liability for future

10 2015 TLTA Institute Translating ALTA into Texan

property association assessments. The ALTA 9.10 covers CCR’s and some encroachments, but not

minerals.

To provide coverage similar to the Texas T-19's or the older ALTA 9 forms, the ALTA

policy now needs an endorsement from two additional endorsement groups: the ALTA 28 series for

encroachments into setback lines, easements, and across property lines, and the ALTA 35 series to

protect against damages to improvements from development of minerals.

ALTA 28 forms include:

ALTA 28 – Encroachment into easements ALTA 28.1 – Encroachment into easements, setback lines, property lines. ALTA 28.2 – Assures specified improvements do not encroach. ALTA 28.3 – Encroachment coverage for new construction built to specified plans. (The ALTA

28.3 was only added as of April, 2015.)

ALTA 35 forms include:

◦ ALTA 35 – Enforced removal of buildings for mineral production. ◦ ALTA 35.1 – Enforced removal of “improvements” as defined. ◦ ALTA 35.2 – Enforced removal of specifically listed improvements. ◦ ALTA 35.3 – Enforced removal of improvements for new construction built to specified plans.

The 2012-2015 revisions to these forms define coverage more clearly by both adding

definitions for certain terms and specifically carving out certain coverage. These changes include:

◦ Defining the term “covenant” in all of the ALTA 9 series forms. ◦ Defining “improvement” in all ALTA 9 and ALTA 35 series forms. ◦ Defining “future Improvement” and “plans” in the ALTA 9.7 and 9.8 ◦ In each of the ALTA 9 and ALTA 35 series forms, listing matters specifically not covered by the

particular endorsement.

TranslatingtheALTAComprehensiveCoverageEndorsementstoCoverageusingthe TexasT‐19's The good news is that customers from ALTA states seem to miss the simplicity of the

original ALTA 9 forms, and do not particularly care for the proliferation of endorsements. So the

explanation as to the T-19 or T-19.1 is usually welcome when they are described as, "Similar to the

11 2015 TLTA Institute Translating ALTA into Texan

pre-2012 ALTA 9, but with added coverage for private rights, and some of the definitions and carve

outs from coverage contained in the ALTA 9, 28 and 35 series of endorsements,"

The key to providing coverage is that you provide the ALTA 19 or 19.1, as appropriate

to circumstance, any time you are requested to issue any ALTA 9 or 28 series endorsement. You may

provide the T-19, 19.1, 19.2 or 19.3, as appropriate to circumstance, any time you are requested to

provide any ALTA 35 series endorsement.

SurveyCoverage(ALTA25,SurveyDeletion) As noted above, the ALTA 25 and 25.1 survey coverage is not available in Texas.

However, in Texas we do have “survey deletion.” The standard Texas survey exception states, “Any

discrepancies, conflicts, or shortages in area or boundary lines, or any encroachments or protrusions, or

any overlapping of improvements.” Survey deletion reduces it to, “shortages in area.” This implies

discrepancies, conflicts, boundary lines encroachments, protrusions or overlapping of improvements

would be covered, although deleting this provision does not mean that the policy says so, and leaves

much open to interpretation.

However, the Court have interpreted "survey deletion" to provide some survey

coverage, and ambiguities in the policy are, as a rule, interpreted against the title insurer. See,

Lawyer’s Title Insurance Company vs. Doubletree Partners, LP, 739 F.3d 848 (5th Cir. 2014).

On commercial transactions, customers will almost always ask that exceptions to survey

matters be limited with the addition of the phrase, "as shown on survey," or "and as also shown on

survey." Per the Doubletree Partners case, supra, this has been interpreted to create ambiguity in the

exception, which when combined with payment for survey deletion, may limit the exception to only as

it appears on the survey. This is effectively affirmative coverage as to the accuracy of the survey's

depiction of the exception. Use of language limiting an exception to a survey depiction should

always be reviewed by an underwriting counsel, and particular care should be used not to use such

12 2015 TLTA Institute Translating ALTA into Texan

qualifying language any time the exception includes restrictions or other limitations on the exception

which cannot be accurately depicted on a survey. For example, an exception to an easement "as shown

on the survey" may not include as part of the exception limitations on use of the easement that are set

forth in the document creating the easement.

Generally, commercial customers should rely on their survey, and expect their surveyor

to have E&O coverage.

Access(ALTA17,17.1/TXT‐23) Texas and ALTA policies each insure “legal access,” but do not insure the quality of the

access or vehicular access. A T-23 or ALTA 17 Access Endorsement each insure actual vehicular and

pedestrian access to a named public roadway, and that the named roadway is physically open. In

addition, the ALTA version insures that there is a right to use existing curb-cuts.

Owing to syntax, a separate Texas T-23 should be issued for each road, though the title

company may charge only once. By contrast, it is common to modify the ALT 17 and list multiple

roads on one ALTA 17. Expect your ALTA customers to require an explanation when you issue

multiple T-23's.

As noted above, ALTA also has a form 17.1, not available in Texas, referred to as an

Indirect Access Endorsement, usually used when the only access is via an easement benefitting the

insured tract. Texas does not have a similar form. However, in Texas, if your filed documentation

supports adding the easement tract as an additional insured tract, and your survey reflects the easement

abuts both the primary property and the road, it is possible to issue a contiguity endorsement insuring

the easement tract is contiguous to the property benefitting from the easement, and get an access

endorsement stating that the easement tract has access to a physically open public road.

13 2015 TLTA Institute Translating ALTA into Texan

FutureAdvance/RevolvingCredit(ALTA14,14.1,14.2,43/TXT‐35) While the Texas T-35 endorsement is a near mirror of the ALTA 14 endorsement,

ALTA has variations not available in Texas.

The ALTA 14.1 that excludes coverage for an advance made after the Lender has

knowledge of the existence of an outstanding lien or encumbrance that arises after the date of policy

and the date of an advance under the Credit Agreement.

The ALTA 14.2 applies specifically to Letters of Credit.

When requested to issue the ALTA 14.1 or 14.2, the closer should have an experienced

attorney or underwriting counsel review the facts to see if the Texas T-14 can be made to fit the

situation. Otherwise the coverage is unavailable.

EnvironmentalLien(ALTA8.1.8.2/TXT‐36,36.1) The Texas T-36 endorsement, as well as its ALTA counterpart, the ALTA 8.1, insures

against a loss of priority of the insured mortgage against an environmental protection lien filed under

Federal or State law. In Texas, the T-36 is available only on property used “..for residential purposes.”

This not only includes 1-4 family residences, but also apartment complexes, nursing homes,

dormitories and any other structure where people reside. In ALTA states, the ALTA 8.2 is available

for commercial property.

In the Fall of 2013, Texas adopted the T-36.1 form as a commercial environmental

endorsement similar to the ALTA 8.2. However, Rate Rule R-2 in the Texas Basic Manual for Title

Insurance states, inter alia, “A company shall not issue or deliver a policy, binder or endorsement until

a rate therefor has been adopted by the Commissioner.” The T-36.1 is therefore unavailable until the

Texas Department of Insurance adopts a rate rule providing a charge for the endorsement. Given the

normal scheduling for rate rule hearings by TDI, this is unlikely to occur before 2016.

14 2015 TLTA Institute Translating ALTA into Texan

While the forms are similar, your "translation problem" here is that many ALTA

customers do end up browsing the Texas Basic Manual, and often request the T-36.1. You will need to

explain to them the Texas rate setting structure and that R-2 prohibits issuing the T-36.1 for now.

Tie‐In(Aggregation)(ALTA12,12.1/T‐16) In the case of a single loan or series of loans secured by multiple properties, often in

different states, the ALTA 12 Aggregation endorsement is used to allow the Lender to aggregate its

coverage and spread it out over any of the listed properties/policies in any combination. Some states

(such as Florida and New York) have restrictions about aggregating policies to cover properties outside

state boundaries, but allow aggregation of sites within state lines, and for these ALTA has issued the

ATLA 12.1. Texas does allow aggregation of policies insuring properties outside Texas, using the T-

16, which is very similar to the ALTA 12. Texas does not have any equivalent version of the ALTA

12.1.

The issue that comes up with out of states customers using aggregation endorsements

on a portfolio of properties is their desire to save money. Because the aggregation endorsement allows

the insured to reach policies outside of the state for losses within Texas, and Texas has somewhat

higher title insurance rates than many other states, there is a customer's tendency when requesting an

aggregation endorsement for an attorney to undervalue the Texas property and overvalue the out of

state property, thereby purchasing coverage in Texas at a discount. Procedural Rule P-66.B.2 of the

Texas Basic Manual for Title Insurance requires, “When the land covered in the policy represents only

part of the security of the loan(s), then the policy shall be written in the amount of the value of such

land or the amount of the loan, whichever is the lesser.” This means that where the insured is blatant

in such valuations, the title company is not only within its right to state the policy must be issued for

the value of collateral under P-66, but could be subject to fine by the Texas Department of Insurance if

15 2015 TLTA Institute Translating ALTA into Texan

it fails to object. If interpreted by TDI to be an illegal kickback in violation of Procedural Rule P-53,

TDI could also fine the insured, so the title company is not only protecting itself, but also the customer.

Title companies tend to be liberal in interpreting P-66, but they cannot accept a property valuation

from the insured that is both unbelievable and undocumented.

PlannedUnitDevelopment(PUD)(ALTA5,5.1/TXT‐17) The T-17 and ALTA 5 PUD endorsements provide coverage to a Lender against:

◦ loss caused by a present violation of covenants;

◦ lack of priority to present and future assessments by an “association of homeowner’s”;

◦ forced removal of an improvement due to an encroachment; and

◦ failure of title due to a right of first refusal

In Texas, the T-17 may only be issued on “residential property” as defined in

Procedural Rule P1.u of the Texas Basic Manual for Title Insurance (1-4 family residential or up to

200 acres primarily used for agricultural production and containing a residence). The ALTA 5 could

theoretically be issued on non-residential property, but the reference to “association of homeowner’s”

makes clear it is intended for residential property as well.

Nevertheless, it is not unusual to receive a request from an out of state attorney for

ALTA 5 coverage on commercial property. You should explain that P-9.b.14 prohibits you from

issuing this endorsement if the property does not meet the definition of "residential property" under P-

1.u. This can create confusion if you've already explained that you can issue the T-36 Environmental

Endorsement on property used for, "residential purposes," but property used for residential purposes is

not the same thing as "residential property" under the Texas Basic Manual for Title Insurance.

16 2015 TLTA Institute Translating ALTA into Texan

ALTA also has the ALTA 5.1, which insures against enforcement of present home

owner’s assessments but no future homeowner’s association assessments, for which there is no Texas

equivalent.

The desirability of the ALTA 5.1 points out a common problem which occurs when

issuing the T-17 in Texas. Many residential developments were developed before the legalization of

home equity loans in Texas, and the restrictive covenants state that the homeowner’s association

assessments are subordinate to purchase money and home improvement loans only, since home equity

or other cash out loans were not contemplated at the time. Also, some restrictive covenants do not

contemplate making the homeowner’s association assessments subordinate to mortgages at all. Issuing

a complete T-17 would therefore make the title company potentially liable for the homeowner

association assessments. The title company is authorized by Procedural Rule P-9.b(14) to delete any

provision of the T-17 it considers unacceptable, and the title company may delete that portion of the T-

17 endorsement insuring that the mortgage is superior to the homeowner’s association assessments.

The amendments to the T-19 effective January 3, 2014, adding so-called “private

rights” coverage, increase redundancy between the T-17 and T-19 endorsements, since the Lender is

being insured for priority of the insured lien over private assessments of all types, including HOA

assessments. The new “private rights” provisions in the T-19 brings the issue of priority of the insured

lien over property owner association assessments into the commercial side of the title insurance

business, where it was not a concern previously.

If a commercial customer asks for ALTA 5 coverage, you should point out not only that

the T-17 is unavailable on commercial property, but that the private rights provisions of the T-19.1 or

T-19 will insure against property owner association assessments. However, that also makes it

incumbent on the closer or examiner to except to property association assessments and delete portions

17 2015 TLTA Institute Translating ALTA into Texan

of the T-19.1 or T-19 if assessments under the CCR's are not expressly subordinate to the insured

interest.

Non‐ImputationEndorsements(ALTA15,15.1,15.2/TX24) The T-24 Non-Imputation Endorsement may only be given concurrently with the

policy, and insures the insured only against knowledge imputed from investors in the company. This is

in contrast with the ALTA 15, which can be issued at any time. You will therefore occasionally get

requests for the Texas title policy to be amended with a non-imputation endorsement, but Procedural

Rule P-55 does not allow that.

In addition, ALTA has 3 different Non-Imputation Endorsement forms to cover distinct

fact situations, one for a Full Equity Transfer (ALTA 15), one to add an additional insured when a

partner or equity member is added (ALTA 15.1) and the last to cover when there is only a partial

transfer of an equity or ownership interest (ALTA 15.2). Generally the only way to give similar

coverage to the ALTA 15.1 and 15.2 is if the T-24 was added at the time of the original policy; that

coverage extends to subsequent incoming partners only if a T-38 endorsements is given.

MezzanineFinancing‐ALTAT‐16/TexasT‐24.1 Texas has an additional non-imputation form, the T-24.1, termed a “Non-Imputation

Endorsement (Mezzanine Financing).” Mezzanine financing is essentially anytime a lender has the

ability to convert debt to equity in the project, thereby becoming an owner of the investing entity. Like

any other incoming partner, shareholder or investor, the lender does not desire its coverage limited by

imputed knowledge of the existing owners.

ALTA handles mezzanine coverage through an ALTA 16 Mezzanine Financing

Endorsement, which provides similar coverage to the Texas T-24.1. Because these two forms have

distinctly different headings, this creates confusion as to the availability of mezzanine financing

18 2015 TLTA Institute Translating ALTA into Texan

coverage in Texas. You will occasionally get a question prefaced with, "...I see there's no mezzanine

financing endorsement in Texas..." Be aware that the coverage is available.

Co‐Insurance(“MeToo”)(ALTA23/TXT‐48) On a large commercial transaction, a Lender will often not allow a single Title

Company to insure the full amount of the transaction as a single risk, and require the liability be shared

between two or more companies as co-insurers. Usually one Title Company is designated to act as the

“lead”, and any other co-insurer can agree to rely on the lead Title Company’s title exam and

underwriting. This is accomplished by what some call a “me too” endorsement, which is exactly as its

nickname implies. The Co-Insurance Endorsement binds the second Title Company to the same

exceptions and coverage as provided by the lead, to the extent of the second Company’s involvement

in the co-insurance of the deal.

The form for doing this outside of Texas is the ALTA 23, and in Texas, the T-48. The

forms are substantially the same.

The catch in Texas is that if the transaction is less than $15-million, the T-48 cannot be

issued, and the customer must instead get two title insurance policies. This rule has a financial impact.

When the Texas T-48 is used in transactions exceeding $15-million, the premium on the total coverage

is prorated between the two title insurance companies based on their percentage of the coverage

assumed, whereas for amounts under $15-million, when the insured must get two separate policies,

each policy is charged for separately. Since the premium rates decline as the policy coverage increases

in Texas, getting separate policies for a transaction under $15-million incurs an additional financial

cost within Texas. In ALTA states the ALTA 23 can be used in transactions of any value, and the

premium is always prorated between the 2 companies.

AssignmentofRentsandLeases(ALTA37,TXT‐27)

19 2015 TLTA Institute Translating ALTA into Texan

The Texas T-27 Assignment of Rents and Leases Endorsement may only be issued

contemporaneously with a Loan Policy, and cannot be issued at a later date. It insures against loss

sustained by a defect in the execution of the assignment and against the existence of a prior recorded

assignment of the lessor’s interest in the leases specified in the document. The title company must

verify no previous assignment of rents and/or leases has been granted by the current or a prior owner,

unless such an assignment was as additional security for a loan since released or being paid out of

closing. A release of a deed of trust will normally be considered to have released the assignment of

rents and leases related to the same loan. The conflict in assignments is most often encountered when

the lender is asking for this endorsement in connection with a second lien, and the first lien already

contains an assignment of rents and leases.

The ALTA 37 is substantially similar to the Texas T-27, but whereas Texas Rule P-60

prohibits the T-27 from being issued on residential property, there is no such prohibition for the ALTA

37.

Both endorsement forms require reference to an assignment of rents in the Schedule B

exceptions. Where the assignment of rents is instead contained within the deed of trust or mortgage

agreement itself, it requires the form to be altered to reference the insured deed of trust or insured

mortgage in Schedule A. While that is commonly done in ALTA states, there is no specific authority

allowing such revision in the Texas Procedural Rules, though it is often done. The correct way to do it

in Texas is to separately except to the assignment of rents and leases contained in the insured deed of

trust in Schedule B, which is often done incorrectly.

ManufacturedHousingUnit(“MHU”)(ALTA7.1,7.2/TXT‐31) While you will rarely, if ever, issue a manufactured home endorsement on commercial

property, a few comments should be made.

20 2015 TLTA Institute Translating ALTA into Texan

The Texas T-31 Manufactured Housing Endorsement insures that the land described in

the policy and improvements thereon, including a manufactured housing unit identified by serial

number, constitute real property. As simple as this insurance is, it is actually a fairly complicated

process, and no attorney or title officer should close a property with a manufactured housing unit

without carefully reviewing the Texas guidelines for obtaining and filing a Statement of Location from

the Texas Department of Housing, contained on their web site.

ALTA divides their “Manufactured Housing Unit Conversion” Endorsement into a

Loan Policy form, the ALTA 7.1, and an Owner’s Policy form, the ALTA 7.2.

The ALTA 7.1 and 7.2 each insure that the MHU is part of the real property under local

state law, that it is located on the land, that the owner of the land is the owner of the MHU, and that

there are no liens attached to the MHU as personal property. The ALTA 7.1 additional insures that the

lender’s lien is enforceable against the MHU as well as the land, and that both the MHU and land can

be foreclosed against in a single foreclosure procedure.

While the ALTA endorsements are more verbose, the Texas T-31 implicitly assumes

much of the same obligations set forth in the ALTA 7 series by merely insuring the MHU is part of the

real property.

CondominiumEndorsements(ALTA4,4.1/TXT‐28) The Texas T-28 Condominium Endorsement is a loan policy endorsement only, and

insures against loss created by the unit not being a part of the condominium regime and the failure of

the condominium declaration to meet the statutory requirements to the extent such failure affects the

title to the unit. It also insures against violations of restrictive covenants unless a notice of violation of

those restrictions has been filed in the real estate records and excepted to in Schedule B of the policy,

and that those covenants do not provide for a forfeiture or reversion of title. Additional insured items

21 2015 TLTA Institute Translating ALTA into Texan

are that any lien for charges or assessments do not have priority over the insured mortgage, the failure

of the unit to be entitled to be assessed as a separate parcel, any obligation to remove improvements

which encroach upon another unit or the elements of another unit, and the exercise of any right of first

refusal to purchase the unit.

The T-28 has two ALTA counterparts, the ALTA 4 for loan policies only, and the 4.1

for both owner and loan policies. The ALTA 4 is essentially identical to the Texas T-28. The ALTA

4.1 is substantially the same, except it insures against any assessments being due on the date of closing

rather than insuring priority of the lien over such assessments.

MECHANICS LIEN'S AND CONSTRUCTION ISSUES

Texas, like most states, has what are called "inchoate mechanics liens," meaning that

once filed, a mechanics lien takes priority from the moment work began, not from the time and date of

the lien filing. Consequently, when you are within the statutory lien filing period, you must except to

mechanics liens that could be filed in the future, which may prime your insured interest even though

filed in the future

Texas handles this by making Procedural Rule P-8 exceptions mandatory any time the

insured amount includes "contemplated improvements," on both an owner or loan policy. The Rule P-

8 mechanics lien exception excepts to all mechanics liens except those filed of record as of the date of

closing, meaning in Texas we insure only against those liens that can be searched in the real property

records. The Basic Manual instructions for filling out the T-3 down date endorsement also require

exception to unfiled mechanics liens. A closer can still run afoul of insuring against unfiled mechanics

liens after the construction is complete, but on construction loans, P-8 generally protects Texas title

companies from insuring against unfiled mechanics liens which might prime the insured interest in the

future.

22 2015 TLTA Institute Translating ALTA into Texan

This is not what happens in most ALTA states. Typical down date coverage in ALTA

states insure against mechanics liens whether or not filed of record. This means that the title company

is insuring against a future event, the possibility that a contractor, subcontractor or worker will file a

mechanics lien in the future which relates back to before the insured interest was created, creating a

claim.

Title companies handle this risk in a variety of ways in ALTA states, depending on

local state law, but most frequently they (1) inspect the premises pre-closing to assure pristine priority,

(2) obtain an indemnity and financials from the borrower or developer to protect the title company

from risk, (3) get lien waivers from each party who works on the project as they're paid, (4) conduct

"draw audits," or some combination of those approaches. A draw audit works like this: Show me the

money we are insuring has been advanced, show me who you paid it to, show me the work they've

done, show me the lien waivers for the work done. It's a lot of paperwork, particularly when it comes

to large construction projects. In some cases, a title company in ALTA states will charge additionally

for the draw audit.

We don't have this problem in Texas because we don't insure against unfiled inchoate

mechanics liens. However, if you have an out of state lender making a loan in Texas for the very first

time, they generally do not believe they cannot get coverage for inchoate mechanics liens until they

hire their own Texas counsel to tell them. Expect some very adverse responses when you refuse to

change the P-8 exceptions, until the lender has an opportunity to speak with their own counsel.

Another major difference in construction coverage is that many ALTA endorsements

have versions for “Land Under Development.” On these "L-U-D" forms, the insured provides plans to

the title company on how the construction is to be done. The plans are carefully described in the

endorsements by architect or engineer, date, project name and number of pages, and the coverage is

expressly conditioned on the construction being complete according to the plans provided. Numerous

23 2015 TLTA Institute Translating ALTA into Texan

problems arise because of this approach, and the L-U-D forms are new enough (2012) that there is

little or no case law interpreting their enforceability.

Texas has no similar "land under development" coverage, but there are provisions in the

instructions for filling out the T-3 endorsement for down dating T-19 or T-19.1 comprehensive

coverage, and survey deletion, in the final down date. The proper procedure is to get an as built

survey, review it for any potential risk, and down date the policy to bring the survey coverage to date,

add coverage for survey deletion, or add T-19 coverage if not previously issued. If there is no final

down date of survey coverage, all construction on the property constitutes matters created, suffered or

assumed by the owner or lender, and changes arising from construction on the Land are not covered by

the policy or its endorsements. While we occasionally see lenders properly down date their loan

policies with this coverage, the failure of owners to down date their OTP's for survey matters after

construction is completed is one of the most overlooked matters in title insurance.

When an out of state customer raises the issue of "Land Under Development"

endorsements, or their instructions request the ALTA 3.2, 9.7, 9.8, 28.3, or 35.3, you should take that

opportunity to not only explain that these endorsements are not available, but to explain the Texas

down date process for the improvements to be covered as built.

TRANSLATING RATE RULES

Out of state customers simply do not know what to ask for? There is always a moral versus

business question as to whether you should inform the customer of his own ignorance, when it will make you

money and cost the customer a great deal more than they should be spending? There are plenty of opportunities

to plead ignorance when the customer discovers later that you took advantage of them, because the customer

often doesn't give you the information necessary for you to make the right evaluation. This is particularly true

with out of state customers, who simply don't understand Texas rate rules. The safe and ethical course is to err

24 2015 TLTA Institute Translating ALTA into Texan

in favor of saving the customer money, so they never have that epiphany that your title insurance policy was

overpriced. That requires you ask questions, to make sure you're giving the right rates.

One of the most common questions is, "We would like to increase the principle balance of an

outstanding loan and get a modification endorsement for our loan policy to increase the balance." It's not even

really a question, it's merely a statement of what the customer wants.

There are several ways to answer that question:

1. "No, Procedural Rule P-9.b.3 specifically prohibits giving a T-38 endorsement any time

there is an increased in the principle balance of the loan."; or

2. "If it's been less than 7-years, we can treat that as a refinance and give you an R-8 credit.";

or

3. "Why?"

"Why?" is the correct answer! Why? It turns out that in most circumstance when you get this

request, the lender is about to advance money for improvements to the property securing the loan. In that

situation, if it's within 4-years, the borrower can get a new OTP issued, get a full credit for the prior OTP under

Rate Rule R-3, including all endorsements, AND get a simultaneous issue rate on the loan policy under Rate

Rule R-5.c. This is usually vastly cheaper to the borrower. If you don't ask, "why," it's likely that your

borrower and lender won't even know to mention that the increase in the loan is for construction purposes, and

while you will get more premium for that newly issued policy, you won't know that you should have P-8

exceptions in the new policy until you get a claim. That is a good way to end up with a mechanics lien claim

and an unhappy underwriter.

Another common situation is where a commercial customer requests a construction loan policy

without asking for an owner's title policy. Procedural Rule P-65 requires that on residential transactions you

always get a waiver of an owner's policy when issuing a loan policy, but this requirement does not exist for

commercial policies. Nevertheless, on large construction loans, this can create a serious cost to the customer.

While the simultaneous rate can be given if the OTP is purchased later, that rate cannot be blended with the R-

18 credit, and the customer will essentially pay for some of the insurance twice when getting an OTP later. On

25 2015 TLTA Institute Translating ALTA into Texan

one $265-million transaction, it saved the customer over $355-thousand to get the OTP and loan policy at the

simultaneous rate up front, rather than delay and get an OTP after construction was complete.

While out of state lenders understand that Texas rates are higher as the amount of the policy

increases, they usually do not realize the great difference it makes in coverage. For example, one national

lender insisted they wanted 5 separate policies for 5 separate properties in Texas, and an aggregation

endorsement with out of state properties in a multi-state portfolio transaction. They were repeatedly told it

would save them money to have one policy for the Texas properties, but they paid no attention until the numbers

were run and they were informed it would save them $90-thousand dollars to insure them on one policy versus

five. The lender then insisted on getting one policy in Texas.

The reality is that only someone intimately familiar with the rate rules can determine how to

save the customer money, and the customer is at a considerable disadvantage in dealing with the title company

on this issue.

OTHER ISSUES

Assignee Language

All the way back in 1992, the Texas Department of Insurance issued Bulletin 157 stating that

you could use no assignee language in the title policy other than this promulgated language:

“_________________________ (Insured Name), and each successor in ownership of the

indebtedness secured by the insured mortgage, except a successor who is an obligor under the

provisions of Section 12(c) of the Conditions and Stipulations."

Bulletin 157 clearly states, "The language may not be added to, deleted from, or altered in any

manner."

Subsequently, Texas incorporated Bulletin 157 into Procedural Rule P-7, which contains all of

the Bulletins terms. When the "Conditions and Stipulations" were changed to just "Conditions" in the policy

form, P-7 was amended to drop the phrase, "..and Stipulations." It should properly now read:

“_________________________ (Insured Name), and each successor in ownership of the

indebtedness secured by the insured mortgage, except a successor who is an obligor under the

provisions of Section 12(c) of the Conditions."

26 2015 TLTA Institute Translating ALTA into Texan

This change was made several years ago, but a substantial number of the title company forms

still have the phrase "and Stipulations."

Out of state attorneys are accustomed to seeing other assignee language, and occasionally even

the abbreviation, "ISAOA," meaning, "It's successor and/or assigns." While there may be a desire to meet

lender requests and provide language naming the insured in the form they request, several years ago TDI handed

out several large fines for violating P-7 in order to emphasize its requirements are now well over 20-years old.

This is a practice to be avoided.

The Insured Closing Letter (ICL) is another matter. There is no specific rule limiting the ICL

language, and a some attorney's notice this. However, the ICL's liability extends only to those who

subsequently also have a policy issued to them, and the name of the insured on the ICL needs to match the

policy in order to have proper coverage.

ICL versus CPL

When you use the acronym, "ICL" with out of state customers, or even the phrase, "Insured

Closing Letter," with out of state customers, they may draw a blank and not know what you're talking about.

Everywhere else in the country it is referred to as a "CPL," or "Closing Protection Letter." This is just one of

those situations where the language is different, where on both sides of a telephone call people may be rolling

their eyes because they think the other side does not know what they're talking about.

Procedural Rule P-35 and Texas Insurance Code 2703.101(c)

P-35 and Texas Insurance Code were set forth at the front of this article. That is because there

are no rules quite like Procedural Rule P-35 or Texas Insurance Code Section 2703.101(c) any place else in the

United States. It is always a surprise to out of state customers. These rules affect the customer in a number of

ways.

Form Alterations

In most states, forms can be freely modified based on risk analysis by the title insurance

company. Consequently, when changes are requested to a policy form, the out of state customer tends to think

27 2015 TLTA Institute Translating ALTA into Texan

it's merely an underwriting decision when you refuse to make changes. They often wish to argue with you or

your underwriter. A copy of the rule and statutes is often required to quiet them.

Commercial attorneys also expect you to sign instruction letters without equivocation. There

are several ways of handling this.

The most common course is the use of the so-called "P-35 Stamp." This is not a promulgated

procedure or form. It is merely common for closers in Texas to qualify their signature with a stamp indicating it

was signed subject to Procedural Rule P-35. The language used in my office when I was a fee attorney was,

"This instrument was signed subject to Procedural Rule P-35, which prohibits Title Companies from making any

statement of fact or coverage except on forms promulgated by the Texas Department of Insurance."

The "P-35 stamp" was created in response to Texas Department of Insurance Bulletin 155,

which, among other matters states, “…P-35 was enacted to prevent the imposition of extraordinary liability on

title agent or escrow officers due to specialized closing instructions. The rule is not intended to prohibit title

agents or escrow officers from acknowledging receipt of standard closing instructions, provided that no

certification is included or implied in acknowledgement of receipt.” The P-35 stamp is intended to

acknowledge receipt without committing the title company in any manner.

Arguably, given the laws are out there, it would be sufficient to sign instructions as, "To

Acknowledge Receipt Only." On commercial transactions, this is likely to engender a conversation with

counsel as to exactly what this means?

Many commercial closers simply sign instructions without any qualification, as the least line of

resistance, and the question then becomes do the statutes and regulations adequately protect the title company?

The short answer is that Procedural Rule P-35 and Insurance Code Section 2703.101(c) have

not been adequately tested in court. The reason why is that the Insured Closing Letter provides coverage for

"actual loss" arising out of, "Failure of the Issuing Agent to comply with your written closing instructions...." In

order to have a true test of the enforceability of P-35 and Insurance Code Section 2703.101(c) in a court of law,

it would need to be a loss encompassed by signed closing instructions which are not covered by the ICL. There

are limitations in the ICL which could give rise to this situation, but that appellate case has not happened yet.

28 2015 TLTA Institute Translating ALTA into Texan

There is a case to be made that a contract is a contract regardless of state statutory or regulatory limitations, and

that it's a finable offense by TDI rather than something limiting liability of the title company.

Given that situation, the closer should be hesitant to unequivocally sign closing instructions that

greatly increase liability to the title agent or the title company over what is contained in the title policy. Use of

the P-35 stamp or other qualifying language in connection with signing documents is recommended. As always,

the closer should follow their underwriter's policy on this issue.

In discussing these matters with an out of state attorney, you can not only provide copies of P-

35 and Section 2703.101(c) of the Texas Insurance Code, but discuss the regulatory structure in Texas. Texas

rates are set by the state based on experience reports of the underwriters and agents turned into the State of

Texas every two years. Anything likely to increase claims on Texas policies is likely to eventually increase

losses to the title companies, and result in rate increases. The only way TDI can control the rates is to also

control the risk that the title companies can incur, by mandating the forms and the risk that title companies are

allowed to assume. The Bulletin 155 language quoted above sets forth TDI's attitude, " ...to prevent the

imposition of extraordinary liability on title agent or escrow officers..." TDI could have easily added

underwriters to that list.

CONCLUSION

The general rule in dealing with people from ALTA states is to expect them to

misunderstand the differences between ALTA and Texas forms and coverage, but don't talk down to

them. When there are conflicts, anticipate the conversation. Start with an explanation that coverage is

different in Texas. Make sure they understand it is a Texas regulatory issue and not underwriting

policy. Be prepared to reference the rate rules and procedural rules. Be knowledgeable, polite and

helpful, and you can become their Texas "go to" person.

29 2015 TLTA Institute Translating ALTA into Texan

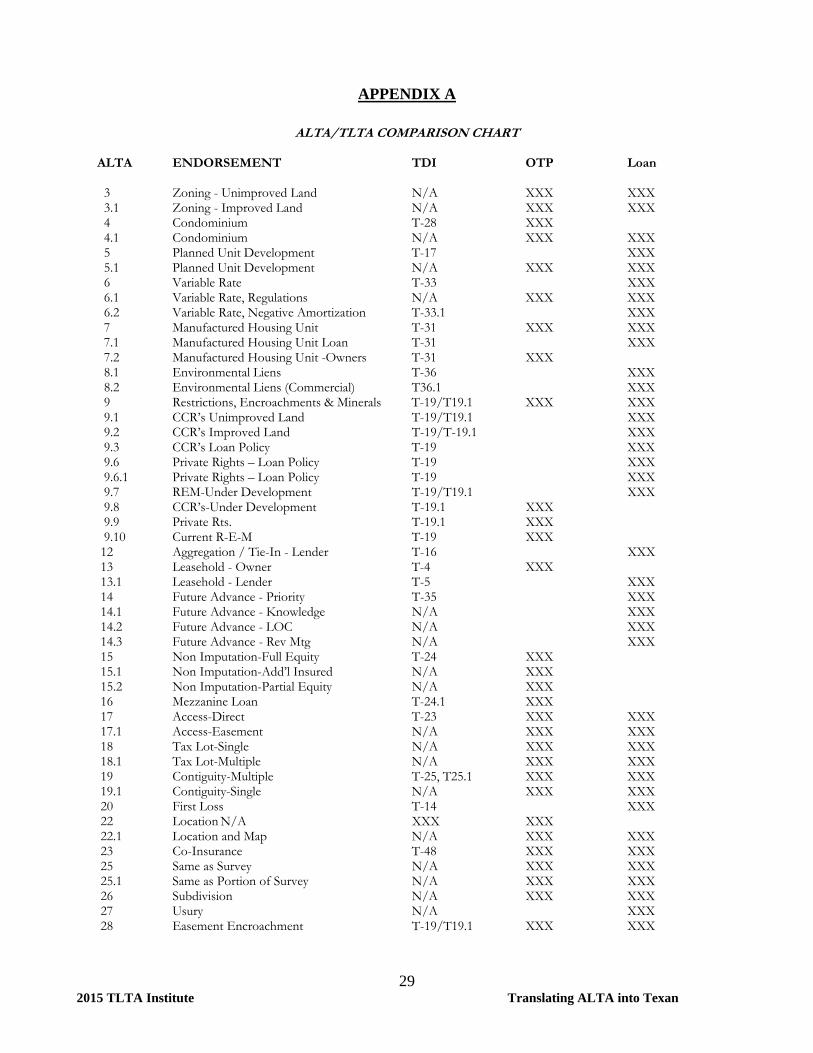

APPENDIX A

ALTA/TLTA COMPARISON CHART

ALTA ENDORSEMENT TDI OTP Loan

3 Zoning - Unimproved Land N/A XXX XXX 3.1 Zoning - Improved Land N/A XXX XXX 4 Condominium T-28 XXX 4.1 Condominium N/A XXX XXX 5 Planned Unit Development T-17 XXX 5.1 Planned Unit Development N/A XXX XXX 6 Variable Rate T-33 XXX 6.1 Variable Rate, Regulations N/A XXX XXX 6.2 Variable Rate, Negative Amortization T-33.1 XXX 7 Manufactured Housing Unit T-31 XXX XXX 7.1 Manufactured Housing Unit Loan T-31 XXX 7.2 Manufactured Housing Unit -Owners T-31 XXX 8.1 Environmental Liens T-36 XXX 8.2 Environmental Liens (Commercial) T36.1 XXX 9 Restrictions, Encroachments & Minerals T-19/T19.1 XXX XXX 9.1 CCR’s Unimproved Land T-19/T19.1 XXX 9.2 CCR’s Improved Land T-19/T-19.1 XXX 9.3 CCR’s Loan Policy T-19 XXX 9.6 Private Rights – Loan Policy T-19 XXX 9.6.1 Private Rights – Loan Policy T-19 XXX 9.7 REM-Under Development T-19/T19.1 XXX 9.8 CCR’s-Under Development T-19.1 XXX 9.9 Private Rts. T-19.1 XXX 9.10 Current R-E-M T-19 XXX 12 Aggregation / Tie-In - Lender T-16 XXX 13 Leasehold - Owner T-4 XXX 13.1 Leasehold - Lender T-5 XXX 14 Future Advance - Priority T-35 XXX 14.1 Future Advance - Knowledge N/A XXX 14.2 Future Advance - LOC N/A XXX 14.3 Future Advance - Rev Mtg N/A XXX 15 Non Imputation-Full Equity T-24 XXX 15.1 Non Imputation-Add’l Insured N/A XXX 15.2 Non Imputation-Partial Equity N/A XXX 16 Mezzanine Loan T-24.1 XXX 17 Access-Direct T-23 XXX XXX 17.1 Access-Easement N/A XXX XXX 18 Tax Lot-Single N/A XXX XXX 18.1 Tax Lot-Multiple N/A XXX XXX 19 Contiguity-Multiple T-25, T25.1 XXX XXX 19.1 Contiguity-Single N/A XXX XXX 20 First Loss T-14 XXX 22 Location N/A XXX XXX 22.1 Location and Map N/A XXX XXX 23 Co-Insurance T-48 XXX XXX 25 Same as Survey N/A XXX XXX 25.1 Same as Portion of Survey N/A XXX XXX 26 Subdivision N/A XXX XXX 27 Usury N/A XXX 28 Easement Encroachment T-19/T19.1 XXX XXX

30 2015 TLTA Institute Translating ALTA into Texan

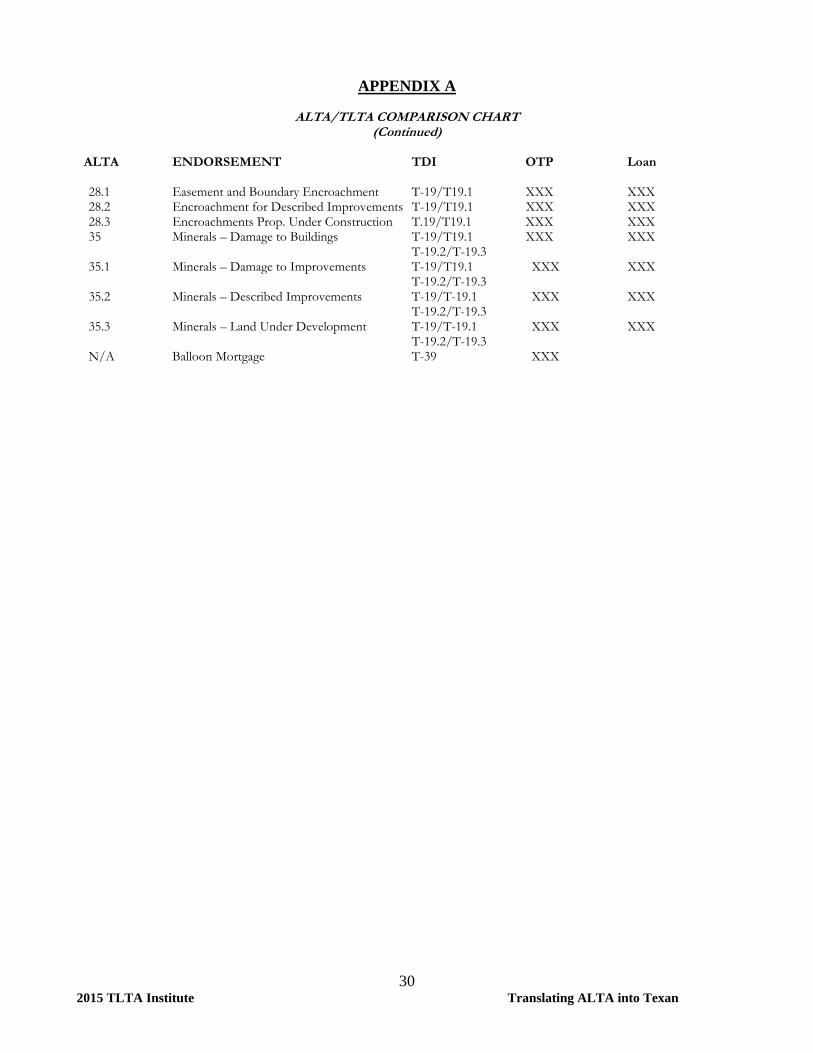

APPENDIX A

ALTA/TLTA COMPARISON CHART (Continued)

ALTA ENDORSEMENT TDI OTP Loan

28.1 Easement and Boundary Encroachment T-19/T19.1 XXX XXX 28.2 Encroachment for Described Improvements T-19/T19.1 XXX XXX 28.3 Encroachments Prop. Under Construction T.19/T19.1 XXX XXX 35 Minerals – Damage to Buildings T-19/T19.1 XXX XXX T-19.2/T-19.3 35.1 Minerals – Damage to Improvements T-19/T19.1 XXX XXX T-19.2/T-19.3 35.2 Minerals – Described Improvements T-19/T-19.1 XXX XXX T-19.2/T-19.3 35.3 Minerals – Land Under Development T-19/T-19.1 XXX XXX T-19.2/T-19.3 N/A Balloon Mortgage T-39 XXX

31 2015 TLTA Institute Translating ALTA into Texan

APPENDIX B - GENERAL NOTES ON TX TITLE COVERAGE VERSUS ALTA

Texas title insurance is tightly regulated, and ALTA forms may not be issued for property in Texas. Title Companies do not have the legal right to alter standardized forms promulgated by the Texas Department of Insurance. Procedural Rule P-35 of the Texas Basic Manual for Title Insurance specifically prohibits Texas title insurance companies from making any statements of fact or coverage except on forms promulgated by the State of Texas. See, also, Section 2703.101(c) of the Texas Insurance Code, making any such agreement void. NAME OF INSURED: The named insured cannot include any “assignee language” except that allowed by Procedural Rule P-7.B of the Texas Basic Manual for Title Insurance, and the words may not be altered per P-7.C. See, http://www.tdi.texas.gov/title/titlem4b.html#P-7,:“_________________________ (Insured Name), and each successor in ownership of the indebtedness secured by the insured mortgage, except a successor who is an obligor under the provisions of Section 12(c) of the Conditions.” GAP COVERAGE – Gap coverage is automatic on all Texas title insurance policies. ENDORSEMENTS NOT AVAILABLE: The following commonly requested endorsements are NOT available in Texas:

Subdivision Same as Survey (But, see below) Single Tax Parcel Street Assessments Utility Access

Usury Zoning Last Dollar (withdrawn in Texas) Lack of Signatures Survey (see below)

AVAILABLE ENDORSEMENTS. The following are available endorsements: T-14 First Loss Endorsement.Requires real property collateral securing the debt other than the subject property.

T-16 Aggregation Endorsement.Aggregates coverage when multiple policies are issued.

T-19/T-19.1 Restrictions, Encroachments and Minerals Endorsement.Similar to the ALTA 9 series.Requires a survey evidencing no encroachments, evidence of no mineral production, no violation of CCR’s, no notices of violations of environmental covenants of record, no “private rights” priming the insured interest (the last like ALTA 9.9).

T-23 Access Endorsement - Available only on property with improvements. Endorsement must name a particular road. Must have a survey, and surveyor should indicate that there is access to a particular road and that the road is open to the public. If you are using a pre-existing survey, the title company will need be able to determine there is access from the survey and review of the property.

T-25 Contiguity Endorsement. Requires there be multiple tracts in the policy, and that there be a survey evidencing the two tracts are, in fact, contiguous. Cannot be issued on property not covered in the current policy.

T-27 Assignment of Rents and Leases. The deed of trust or other filed instrument must provide for such assignment, and they must not have been previously assigned by another instrument (not being released at closing).

T-33 Variable Rate Mortgage Endorsement. Requires debt instrument have variable rate provisions.

T-35 Future Advancement Revolving Credit Endorsement. Requires provisions for a revolving credit line be in the deed of trust.

32 2015 TLTA Institute Translating ALTA into Texan

T-36 Environmental Endorsement. This is only available on property, “primarily used for residential purposes.” We do provide this on apartment complexes. T-39 Balloon Mortgage.Requires a balloon provision be in the deed of trust. SURVEY COVERAGE

Survey Deletion: Although we have no survey endorsement, in Texas we provide what is called Survey Deletion, which will reduce the survey exception to, “shortages in area,” with a valid survey in hand per Procedural Rule P-2 of the Texas Basic Manual. Company may add specific exceptions for matters on the survey after review. Per Procedural Rule P-2, title Company cannot provide survey deletion in Texas without a survey. The Title Company may use an old survey provided a survey affidavit is signed and sworn to by a person with personal knowledge the survey has not changed. A Texas Class 1A or ALTA Survey is required. For a customer asking a survey exception be limited to “as shown on survey,” underwriter should be familiar with Lawyers Title vs. Doubletree Partners, or discuss with Texas Underwriter before giving this coverage. MINERALS–Your commitment and policy will have either (a) specific exceptions showing the minerals wholly severed from property ownership, (b) the general exception allowed by P-5.1 of the Texas Basic Manual or (c) all deeds should be searched back to at least 1900, evidencing no severance of the minerals from the fee estate. Your standard Texas search is to the early 1970’s, so a search back to 1900 must be specifically requested.Note that such a search will reflect only where minerals have been severed, not current mineral ownership. MECHANIC’S LIENS –Standardized mechanics lien exception and pending disbursement exception are mandatory if any a portion of the insured value is for contemplated improvements, on both owner and loan policies. See Procedural Rule P-8 of the Texas Basic Manual. Down dates are by T-3 endorsement, which may only be completed according to instructions set forth in the Texas Basic Manual. Down dates cover ONLY mechanics liens filed of record; you cannot get inchoate lien coverage in Texas. COMMITMENT - The company issues one commitment for both the owner’s and loan policy, and they cannot be separated. There may be exceptions in the commitment which apply to one policy but not the other. There are provisions in the policy and commitment which cannot be deleted because they are in the promulgated forms; however:

Survey deletion will reduce exception 2 to “shortages in area” in the final policy if a survey is provided.

A survey is required by Procedural Rule P-2.

The tax exception will be changed to an exception to “201_ and subsequent years” in the final policy if taxes have been paid current.

Rights of parties in possession will be deleted upon providing an owner’s affidavit regarding occupancy, (in a form provided by the Company)

Those exceptions which state they are for the owner’s policy only will not appear in a final loan policy, just as those exceptions for the loan policy only will not appear in the final owner’s policy.

PRO FORMA –You cannot issue a Texas pro forma for insured amounts less than $500,000. EXPRESS INSURANCE – Including any affirmative coverage, may only be given in compliance with Procedural Rule P-39, which may not be used if there is a promulgated form covering the matter. RATES: Rates on policies and endorsements are set by the State, and are not negotiable.

11/16/2015

1

Commercial Transactions:Translating ALTA into Texan

Richard D. Worsham, Vice-President/Texas Region Underwriting Counsel

2015 TEXAS LAND TITLE INSTITUTE

11/16/2015

2

2015 TEXAS LAND TITLE INSTITUTE

What the %&+! is ALTA?

Everywhere in the United states except Texas, they use forms promulgated by the American Land Title Association (“ALTA”).

2015 TEXAS LAND TITLE INSTITUTE

11/16/2015

3

It’s not Their Fault!

Accept that customers and attorneys from ALTA states are frustrated that Texas is different, just as you are frustrated they don’t know the Texas rules and forms.

2015 TEXAS LAND TITLE INSTITUTE

ALTA Forms Committee

The ALTA Forms Committee meets and changes the forms every once in awhile:

2006 – Major Form overhaul

2010, Improved, Revised, Added and Standardized Forms

2012, Revised 7 Forms and Added 15 (Major revisions to the ALTA 9, 28 and 35 comprehensive series)

2013 and 2014, forms added

2015 TEXAS LAND TITLE INSTITUTE

11/16/2015

4

We’re not going to talk about CLTA forms.

The California Land

Title Association

(CLTA) is even more

prolific than ALTA,

but duplicates much

of ALTA’s coverage.

Available in California and some Rocky

Mountain States, we won’t be discussing them.

2015 TEXAS LAND TITLE INSTITUTE

We Are Also Not Going to Talk about Residential

ALTA Residential Only Loan Policy forms-

Expanded Coverage Residential Loan Policy) (Revised 12-2-13)

Expanded Coverage Residential Loan Policy – Assessments Priority (4-2-15)

Expanded Coverage Residential Loan Policy – Current Assessments (4-2-15)

Residential Limited Coverage Junior Loan Policy (8-1-2)

Short form versions of each of the above (4 more)

Short form Residential Loan Policy

Short Form Residential Loan Policy – Current Violations (04-02-15)

2015 TEXAS LAND TITLE INSTITUTE

11/16/2015

5

ALTA Commercial Policy Forms

Loan Policy (6-17-06)

Owner’s Policy (6-17-06)

Extended Loan Policy

Extended Owner’s Policy

2015 TEXAS LAND TITLE INSTITUTE

Standard ALTA Coverage:

Insured is the record owner.

No recorded defects, liens or encumbrances on title.

Right of access.

Marketable Title.

2015 TEXAS LAND TITLE INSTITUTE

11/16/2015

6

ALTA Standard Does NOT Cover

Taxes or assessments not shown by the taxing authority or public records.

Defects not in the public records but could be discovered by an inspection of the land or making inquiry of persons in possession thereof.

Easements, liens or encumbrances which are not shown by the public records.

Problems that a correct survey would disclose, not shown by the public records.

Unpatented mining claims, patent reservations and water rights.

Mechanics Liens not shown by the public records.

2015 TEXAS LAND TITLE INSTITUTE

ALTA Extended Does Cover

Taxes or assessments not shown by the taxing authority or public records.

Defects not in the public records but could be discovered by an inspection of the land or making inquiry of persons in possession thereof.

Easements, liens or encumbrances which are not shown by the public records.

Problems that a correct survey would disclose, not shown by the public records.

Unpatented mining claims, patent reservations and water rights.

Mechanics Liens not shown by the public records.

2015 TEXAS LAND TITLE INSTITUTE

11/16/2015

7

In the World of Texas

2015 TEXAS LAND TITLE INSTITUTE

Texas Policy Translation

If they ask for ALTA extended coverage - they are implicitly asking for:Survey deletion

Tax Deletion

No mineral exception

No “Parties in Possession” exception

No P-8 Mechanics Lien exceptions