TITLE Hedging strategies using LIFFE listed equity...

29

1 TITLE Hedging strategies using LIFFE listed equity options Dritsakis Nikolaos, University of Macedonia Grose Christos, University of Macedonia Keywords: efficiency, options, implied volatility, hedge, portfolio Dr. Dritsakis Nikolaos Associate Professor of Econometrics Department of Applied Informatics University of Macedonia, Thessaloniki P.O. Box 1591, 54006, Greece Phone: ++30310891876 e-mail: [email protected] Mr. Grose Christos Doctoral Student Department of Applied Informatics University of Macedonia, Thessaloniki P.O. Box 1591, 54006, Greece Phone: ++30310891847 e-mail: [email protected]

-

Upload

nguyenhuong -

Category

Documents

-

view

213 -

download

0

Transcript of TITLE Hedging strategies using LIFFE listed equity...

1

TITLE

Hedging strategies using LIFFE listed equity options

Dritsakis Nikolaos, University of Macedonia

Grose Christos, University of Macedonia

Keywords: efficiency, options, implied volatility, hedge, portfolio

Dr. Dritsakis Nikolaos Associate Professor of Econometrics Department of Applied Informatics University of Macedonia, Thessaloniki P.O. Box 1591, 54006, Greece Phone: ++30310891876 e-mail: [email protected] Mr. Grose Christos Doctoral Student Department of Applied Informatics University of Macedonia, Thessaloniki P.O. Box 1591, 54006, Greece Phone: ++30310891847 e-mail: [email protected]

2

Abstract

Ex ante tests of the efficiency of the London options market explain

alternative hedging strategies to fund managers who seek to comprehend the

opportunities in the options markets and profit by potential market

inefficiencies. Over and under valued options were used to form hedge

portfolios, which were mostly positive indicating potential inefficiencies in

LIFFE. Therefore options appear to incorporate the role of an investment

strategy on their own and not only as a hedge against positions in the

underlying stocks while the Black-Scholes formula proved to be an easily

computed and implemented way to make above normal, zero risk profits. This

paper also confirms the ability of a weighted implied standard deviation to

explain future volatility more accurately than historical volatility by use of

regression analysis.

1. Introduction

The London International Financial Futures and Options Exchange

(LIFFE) was established in 1982 in the wake of the lifting of UK foreign

exchange controls. Equity options have been trading in LIFFE, in its current

form, since 1992 when it was merged with the London Traded Options Market

(LTOM). This paper contains an empirical analysis directed towards an

investigation of whether equity options trading in LIFFE is efficient.

3

This study attempts to trace potential arbitrage opportunities in the

market. If such opportunities do not exist market efficiency appears to hold.

Since the introduction of the Black-Scholes option-pricing model many papers

have attempted to test market efficiency. However, the majority of these

studies have focused on the Chicago Board of Options Exchange. Although

LIFFE is one of the major European derivate exchanges it has not been largely

investigated.

The efficiency of LIFFE is tested against the Black-Scholes formula for

the pricing of traded options. This is because it is both easy to implement and is

widely used by dealers1. The Black-Scholes model is used to identify

overvalued and undervalued option contracts on an ex post basis by using the

hedging technique suggested by Black-Scholes (Black, 1972). The weak form

of market efficiency is tested by utilising the model’s ability to identify

overvalued and undervalued option contracts, forming hedged positions and

constructing portfolios of hedges on a one month basis. Hence, the tests for

market efficiency are jointly tests for the validity of the model and its ability in

selecting the mispriced option contracts.

In this way two further aspects of market efficiency are highlighted. First,

the ability of a trading rule to distinguish profitable from unprofitable

investments. Thus, the ability of the trading rule to explain observed prices is

ascertained. The second issue is the establishment of a trading strategy based

on this rule that will ensure above normal profits relative to the risk taken. In

1 Empirical analysis of alternative option pricing models can be found in Bakshi, Can and Chen (1997).

4

order to establish this, one can perform an ex ante test (on past data) by

replicating the existing opportunities for a trader. An ex post test on such a

trading model might give us false results. The lack of all relevant information

might lead us into falsely determining that the market is efficient.

An increasing number of investment managers, realising the potential

profits that could be made by identifying market inefficiencies, are engaging in

the options market. Their aim is twofold: Establish solid hedges against

positions taken on the underlying assets but also make profits in the options

market when such opportunities arise (Korn, 1999). Hedgers might wish to

minimise risk close to zero, under ideal conditions, but they might also want to

resort to insurance to minimise future possible unfavourable outcomes (Sheedy,

1998). Fund managers engaging in active fund management could exploit

signals of market inefficiency even though transaction costs cause expected

profits to be reduced. However, according to recent studies, option strategies

are still profitable even after transaction costs are considered (Isakov, 2001).

The remainder of the paper is organised as follows. Section 2 describes

the methodology used and is followed throughout the rest of the paper. An

analogous to the implied volatility description is done for the historical

volatility to highlight differences in the two methods accuracy. In addition tests

are performed in order to emphasise the superiority of the implied variance as a

predictor of the future variance. The results of the tests for the implied and

historical variance are presented in section 3. Then the hedging strategy results

using both the implied variance and the historical volatility are outlined on a

5

monthly collective basis. Finally, a brief reference of this paper’s conclusions

and implications are discussed in section 4.

2. Volatility trading and market efficiency

2.1 The volatility trading strategy

Our analysis will attempt to test the efficiency of traded equity options in

LIFFE, by implementing a volatility trading strategy in order to exploit

potential deviations between theoretical and actual option prices. The

formulation of a trading strategy is based on the anticipation of the future

volatility of the security underlying the option. If one expects higher (lower)

future volatility this corresponds to forecasting higher (lower) option prices as

well. Hence a successful hedger will employ a buying (selling) strategy

respectively.

The first studies that examined the deviations between theoretical and

actual prices in option prices were conducted after the B-S model was

introduced on options trading on the newly established Chicago Board of

Options Exchange (CBOE). Their common result is that indeed evidence is

inconsistent with market efficiency (Black, 1972; Galai, 1977; Trippi, 1977;

Finnerty, 1978; Klemkosky, 1980). However, as Jensen (1978) indicates,

market efficiency implies that economic profits from trading are zero, where

economic profits are risk-adjusted returns net of all costs. Hence, in some of

6

these studies after trading costs are calculated profit opportunities vanish.

Phillips and Smith (1980) as well as Wilmott, Hoggard and Whalley (1994)

also address the transaction costs issue.

In more recent studies Harvey and Whaley (1992) testing the S&P 100

index option market find that, after trading costs, a trading strategy based upon

out-of-sample volatility changes does not generate economic profits while a

study by Tan and Dickinson (1992) tests the efficiency of the stock options

market of the European Options Market by use of a spreading strategy. Joo and

Dickinson (1993) on the other hand examine the efficiency of the European

Options Market developing a dynamic hedging strategy while taking into

account the bid-ask spread cost effect. Xu and Taylor (1995) test the efficiency

hypothesis in the currency options market and Cavallo and Mammola (2000)

examine the Italian index options market, but they find that no systematic profit

can be made by singling out potential mispricings.

2.2 The Merton formula

We use Merton’s formula, which adjusts the B-S model for the inclusion

of dividend payments,

})2/1()/ln({})2/1()/ln({22

tt

yRESNEet

tyRESNSC RtytCD σ

σσ

σ −−+−

+−+= −− (2.1)

7

where DC is the Merton pricing formula of the call price, y is the continuously

compounded dividend payment.

We calculate the implied standard deviation )(ISD of each option contract

by entering the current option price into the evaluation equation and using

numerical solution techniques to find which price of the standard deviation

equates the LHS and RHS of Merton’s formula. A trading strategy is formed

based on the following steps:

(a). The Implied Market Value )(IMV is calculated using the weighted

average of the implied standard deviations of its stock )(WISD in the pricing

formula.

(b). The )(IMV is compared to the actual market prices so as to form short

and long positions on the traded options.

(c). A risk-free hedge is created consisting of at least one short and long

position while the amount of each option included in the hedged position

depends on the hedge ratio. The hedge ratio is the reciprocal of the derivative

of (2.1) and is defined,

})2/1()/ln({/)(2

1

ttyRESNe

SC ytD

σσ+−+

=∂∂ − (2.2)

8

2.3 Data

The main body of the data consists of end of month data for LIFFE listed

options during the period January 1995 – December 1999 written on twenty

London Stock Exchange (LSE) listed options. The data were obtained from

LIFFE. The quoted call prices were approximately 7,200 and for each one a

corresponding fair value was calculated.

In order to achieve synchronisation of the transactions on the LSE and

LIFFE a complex and time-consuming procedure was carried out. From the list

of call and share prices we selected the call premium and share price at the

same time so as to bypass any estimation error. The share prices used are not

closing prices but transaction prices on the last trading day of the month that

coincide with the transactions made at the same time on LIFFE in the

underlying option contracts. During the 60 observation dates five stock splits

took place and the option data were modified to accommodate the changes.

The selected companies were divided into two groups of ten; one based on

the January, April, July and October cycle and the other on the February, May,

August and November cycle. Furthermore, the chosen listed shares have had

continuously traded option contracts. The above restrictions ensured the

accuracy of the ensuing results.

The risk-free interest rate was taken from the 3-month interbank deposit rate.

For the inclusion of the dividend component in the B-S formula the dividend

that the underlying stockholder is entitled to receive was used and was then

9

converted to an equivalent continuous rate. The above data were derived from

DataStream.

2.4 Volatility estimation

The dynamic strategy was implemented using historic and implied

estimates for future volatility. Historic volatility estimation is based on the

assumption that the volatility that prevailed over the recent past will continue to

hold in the future. Initially, we take a sample of returns on the stock over a

single period. These returns are then converted into continuously compounded

returns. Lastly, the standard deviation of the compounded returns is calculated.

Lets assume that we have i continuously compounded returns, where

each return is identified as tS which equals )ln(1

2

t

t

SS and t goes from 1 to i .

Alternatively if there was an ex-dividend day during the interval,

[ ]12 /)(ln ttt SDSS += where D is the dividend payment. Therefore the mean

return and variance are as follows:

iS

S ti

tΣ=

=1

(2.3)

1

/)()(

1

)(1 1

22

1

2

2

−

−=

−

−=

∑ ∑∑= ==

i

iSS

i

SSi

t

i

ttt

i

tt

σ (2.4)

10

Volatility is therefore Sσν = where S is the average stock price of all iS ’s, tS

is the weekly stock price, i is the number of observations, v is the volatility.

Following Chiras and Manaster (1978) the implied standard deviations are

weighted by the price elasticity of an option with respect to its implied standard

deviation. The formula used is:

∑

∑

=

=

∂

∂∂

∂

=N

j j

j

j

j

N

j j

j

j

jj

CC

CC

ISDWISD

1

1

σσ

σσ

(2.5)

where N is the number of option contracts on each stock on every particular

date, WISD is the weighted implied standard deviation for each stock on every

observation date, jISD is the calculated standard deviation of each recorded

option contract, jj

jj

CCσσ

∂

∂ is the price elasticity of option j relative to its implied

standard deviation.

The importance of WISDs is twofold. Firstly, WISDs are better indicators

of future volatility than historic volatility. Secondly, they render unnecessary

the collection of historical data. Nonetheless, Beckers (1981) concluded that

both historical and implied volatility provide valuable information for the user

of option models.

In order to determine the accuracy of the hypothesis that the standard

deviations deduced from option prices are a better predictor of a stock’s

volatility than the standard deviation inferred from historical data the following

regressions are tested:

11

tjPptj SHISTSFUT ,, βα += (2.6)

tjrrtj WISDSFUT ,, βα += (2.7)

tjstjsstj WISDSHISTSFUT ,,, γβα ++= (2.8)

where tjWISD , is the weighted implied standard deviation inferred from option

prices at time t , tjSHIST , is the historical standard deviation estimated using

data from time xt − to t , tjSFUT , is the standard deviation of option j from

time t to xt + , sssrrpp γβαβαβα ,,,, ,, are the estimated coefficients of the

regression parameters2.

There are 60 months (observation periods) during which our hypothesis

was tested. For each observation period data from 20 individual stocks were

used. The SHISTs and WISDs were tested against the SFUTs to determine

which predictor explains larger percentage of the future standard deviation. The

joint test of the WISDs and SHISTs tests the informational content of each

parameter, i.e. whether each one contains unique information and whether one

adds no additional information to the already known information from the other

parameter.

12

2.5 Methodology

For the calculation of the WISDs a numerical search routine is used that

solves for σ by equating the B-S model price to the observed market price.

This happens since it is impossible to solve the B-S option-pricing model for

σ . Approximately 5.6 option contracts on a monthly basis were used to

calculate the WISDs for each option. On some cases the market price of the call

is too low to allow convergence by a model price. Lastly, throughout the

sample period in only eight cases less than three standard deviation estimates

were used for the calculation of the WISDs .

The calculated WISDs are used as the volatility component in the B-S

formula in order to calculate the option model price )(IMV . Stock margin

prices are used as input in the B-S formula. The computed model price of each

option contract is then compared to the market price to identify possible short

or long positions. When the model price is lower (higher) than the market price

the option is undervalued (overvalued) and a long (short) position is taken in

the call with a corresponding short (long) position in the stock as long as their

difference is not less than ten percent. This threshold level for the difference

between calculated and effective prices was fixed at a high level (10%) in order

to account for potential inefficiencies of the model.

In order to create a risk-free hedge at least one short and one long position

are required. If for a particular stock more than one short and long position

2 For a detailed analysis for volatility estimation in option pricing see Christensen and Brabhala (1998).

13

exists the ones bearing the maximum percentage difference are chosen. The

hedge ratio is calculated so as to determine the amount of each option included

in the hedge. This follows the acknowledgement that a successful option

strategy involves not only a position in a mispriced option, but also an

appropriate hedge in the underlying stock. In this way each pair of options will

produce offsetting gains and losses for any immediate movement in the

underlying stock price.

The first step in the process is calculating the derivative of the B-S

formula adjusted for dividend payments with respect to the stock price:

Rtyt edNEdNSeC −− ∗−∗= )()( 21 (2.9)

)( 1dNeSC yt−=∂∂ (2.10)

Then the reciprocal of (2.10) is calculated:

)( 1

1

dNe

SC yt−−

=

∂∂ (2.11)

In order to identify the most profitable hedge ratio spread we maximize

the joint percentage deviation between the market and model prices using the

following:

)/()]()[( ''jijjii CCCCCC +−+− (2.12)

14

where 'iC is the fair value of an undervalued call, iC is the market value of the

undervalued call, 'jC is the fair value of the overvalued call, jC is the market

value of the overvalued call.

This rule has the effect of eliminating the low-priced, out of the money

options for which the model may not be a good predictor. The holding period

for each hedge is one-month (in the context of a five year period). The hedge

position is maintained over the one-month holding period and is closed out at

the opening stock and option transaction prices of the next trading day that is a

month later. During the holding period the hedge ratio may change which

would cause the characteristics of each hedge to change. This risk is diversified

away by selecting many hedge positions. The percent holding period returns

are aggregated across all hedges for the twenty stocks throughout the fifty-nine

holding periods. The sum of all these differences should give the total gain

from the hedging strategy.

3. Empirical results

3.1 Volatility estimation tests

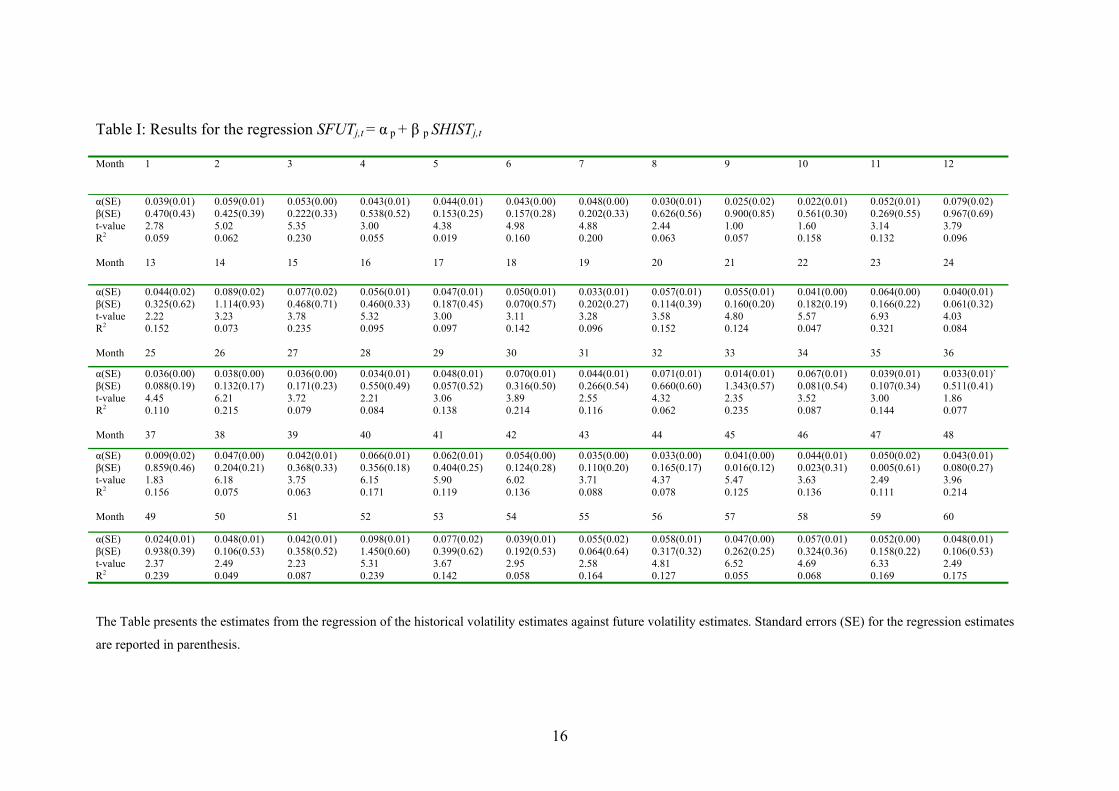

The regression estimates for equations 2.6, 2.7 and 2.8 are made using

Ordinary Least Squares method. By observing the data from Table I we note

that a very small part of the future standard deviation is explained by the

historical volatility. This feature is indicated by 2R which averages 14 percent.

15

Hence, the standard deviation of the historical volatility explained only 14

percent of the deviation of the future volatility. The 2R results do not indicate

any particular tendency towards diminishing or increasing over time.

″take in Table I″

The t values recorded are significant at the five percent significance level.

The higher the t values the lower is the probability that the sample used could

be obtained from a distribution with an actual price of β close to zero. No

negative values were recorded with mean t values approximately 4.20.

Negative t values could not be accepted because they contradict the theoretical

background.

16

Table I: Results for the regression SFUTj,t = α p + β p SHISTj,t

The Table presents the estimates from the regression of the historical volatility estimates against future volatility estimates. Standard errors (SE) for the regression estimates

are reported in parenthesis.

Month

1 2 3 4 5 6 7 8 9 10 11 12

α(SE) 0.039(0.01) 0.059(0.01) 0.053(0.00) 0.043(0.01) 0.044(0.01) 0.043(0.00) 0.048(0.00) 0.030(0.01) 0.025(0.02) 0.022(0.01) 0.052(0.01) 0.079(0.02) β(SE) 0.470(0.43) 0.425(0.39) 0.222(0.33) 0.538(0.52) 0.153(0.25) 0.157(0.28) 0.202(0.33) 0.626(0.56) 0.900(0.85) 0.561(0.30) 0.269(0.55) 0.967(0.69) t-value 2.78 5.02 5.35 3.00 4.38 4.98 4.88 2.44 1.00 1.60 3.14 3.79 R2 0.059 0.062 0.230 0.055 0.019 0.160 0.200 0.063 0.057 0.158 0.132 0.096 Month 13 14 15 16 17 18 19 20 21 22 23 24

α(SE) 0.044(0.02) 0.089(0.02) 0.077(0.02) 0.056(0.01) 0.047(0.01) 0.050(0.01) 0.033(0.01) 0.057(0.01) 0.055(0.01) 0.041(0.00) 0.064(0.00) 0.040(0.01) β(SE) 0.325(0.62) 1.114(0.93) 0.468(0.71) 0.460(0.33) 0.187(0.45) 0.070(0.57) 0.202(0.27) 0.114(0.39) 0.160(0.20) 0.182(0.19) 0.166(0.22) 0.061(0.32) t-value 2.22 3.23 3.78 5.32 3.00 3.11 3.28 3.58 4.80 5.57 6.93 4.03 R2 0.152 0.073 0.235 0.095 0.097 0.142 0.096 0.152 0.124 0.047 0.321 0.084 Month 25 26 27 28 29 30 31 32 33 34 35 36

α(SE) 0.036(0.00) 0.038(0.00) 0.036(0.00) 0.034(0.01) 0.048(0.01) 0.070(0.01) 0.044(0.01) 0.071(0.01) 0.014(0.01) 0.067(0.01) 0.039(0.01) 0.033(0.01)` β(SE) 0.088(0.19) 0.132(0.17) 0.171(0.23) 0.550(0.49) 0.057(0.52) 0.316(0.50) 0.266(0.54) 0.660(0.60) 1.343(0.57) 0.081(0.54) 0.107(0.34) 0.511(0.41) t-value 4.45 6.21 3.72 2.21 3.06 3.89 2.55 4.32 2.35 3.52 3.00 1.86 R2 0.110 0.215 0.079 0.084 0.138 0.214 0.116 0.062 0.235 0.087 0.144 0.077 Month 37 38 39 40 41 42 43 44 45 46 47 48

α(SE) 0.009(0.02) 0.047(0.00) 0.042(0.01) 0.066(0.01) 0.062(0.01) 0.054(0.00) 0.035(0.00) 0.033(0.00) 0.041(0.00) 0.044(0.01) 0.050(0.02) 0.043(0.01) β(SE) 0.859(0.46) 0.204(0.21) 0.368(0.33) 0.356(0.18) 0.404(0.25) 0.124(0.28) 0.110(0.20) 0.165(0.17) 0.016(0.12) 0.023(0.31) 0.005(0.61) 0.080(0.27) t-value 1.83 6.18 3.75 6.15 5.90 6.02 3.71 4.37 5.47 3.63 2.49 3.96 R2 0.156 0.075 0.063 0.171 0.119 0.136 0.088 0.078 0.125 0.136 0.111 0.214 Month 49 50 51 52 53 54 55 56 57 58 59 60

α(SE) 0.024(0.01) 0.048(0.01) 0.042(0.01) 0.098(0.01) 0.077(0.02) 0.039(0.01) 0.055(0.02) 0.058(0.01) 0.047(0.00) 0.057(0.01) 0.052(0.00) 0.048(0.01) β(SE) 0.938(0.39) 0.106(0.53) 0.358(0.52) 1.450(0.60) 0.399(0.62) 0.192(0.53) 0.064(0.64) 0.317(0.32) 0.262(0.25) 0.324(0.36) 0.158(0.22) 0.106(0.53) t-value 2.37 2.49 2.23 5.31 3.67 2.95 2.58 4.81 6.52 4.69 6.33 2.49 R2 0.239 0.049 0.087 0.239 0.142 0.058 0.164 0.127 0.055 0.068 0.169 0.175

17

The results for equation 2.7 (Table II) support the hypothesis that WISDs

provide better estimates of future volatility than SHISTs . 2R average value is

26 percent, almost double the SHISTs value, which can be interpreted as

WISDs having double the predictive ability of SHISTs . Nonetheless, there does

not seem to exist any particular trend on these results either, a fact which would

indicate a change in the predictive ability throughout the sample.

″take in Table II″

The majority of t values are significant at the five percent significance

level with five values bearing significance at the 0.01 level. Since t values are

still particularly high averaging 3.86 it could be stated that the null hypothesis

of β equalling zero is rejected for both regressions.

The coefficient standard errors appear to be higher for s'β rather than for

the constant in both regressions. From the results in table I the calculated mean

value for sa' is 0.0097 and for s'β 0.38. The mean constant value is 0.0234,

while the mean β is 0.0935.

In Table III the results from the joint regression are shown. The figures

partially support the conclusions drawn by the previous regressions. The t

values are significantly higher for the WISDs rather than for the SHISTs even

though in both negative values appear. The WISDs mean t value is 0.93

whereas the SHISTs mean value is 0.45. This notable difference in their

predictive power is not fully supported by the 2R results that are slightly higher

than regression (2.7) 2R results. The mean of 0.32 (compared to 0.26 in

regression 2.7) signals the existence of at least some informational content in

18

SHISTs that is not fully contained in the WISDs . In spite of this result WISDs

still appear to be better predictors of future standard deviations and to contain

the multitude of information required to make an accurate prediction of SFUTs .

These findings are consistent with Canina and Figlewski (1993) that also assert

that implied volatilities are better predictors of future volatility than those

obtained using historic data.

″take in Table III″

19

Table II: Results for the regression SFUTj,t = α r + β r WISDj,t

The estimates from the regression of implied volatility estimates against future volatility estimates are presented in this Table. Standard errors (SE) for the regression

estimates are reported in parenthesis.

Month 1 2 3 4 5 6 7 8 9 10 11 12

α(SE) 0.052(0.01) 0.062(0.01) 0.036(0.01) 0.076(0.01) 0.034(0.01) 0.055(0.01) 0.038(0.01) 0.052(0.01) 0.049(0.01) 0.062(0.01) 0.055(0.02) 0.029(0.02) β(SE) 0.003(0.05) 0.050(0.05) 0.037(0.04) 0.067(0.03) 0.017(0.05) 0.052(0.04) 0.015(0.03) 0.028(0.04) 0.004(0.07) 0.053(0.04) 0.015(0.07) 0.083(0.07) t-value 2.95 3.81 2.92 6.74 2.03 4.06 3.55 4.08 2.05 3.99 2.29 1.32 R2 0.125 0.087 0.242 0.148 0.215 0.076 0.187 0.129 0.254 0.198 0.238 0.161 Month 13 14 15 16 17 18 19 20 21 22 23 24

α(SE) 0.060(0.03) 0.041(0.05) 0.025(0.04) 0.047(0.03) 0.083(0.04) 0.071(0.04) 0.029(0.02) 0.101(0.03) 0.054(0.03) 0.018(0.02) 0.047(0.02) 0.001(0.02) β(SE) 0.025(0.15) 0.063(0.20) 0.166(0.19) 0.016(0.14) 0.123(0.16) 0.528(0.19) 0.308(0.12) 0.211(0.16) 0.030(0.12) 0.122(0.12) 0.043(0.08) 0.162(0.11) t-value 1.61 0.80 0.83 1.38 2.08 2.73 2.49 2.68 1.76 1.01 2.28 1.36 R2 0.208 0.224 0.187 0.149 0.182 0.292 0.256 0.183 0.263 0.175 0.149 0.203 Month 25 26 27 28 29 30 31 32 33 34 35 36

α(SE) 0.026(0.01) 0.030(0.01) 0.034(0.01) 0.014(0.02) 0.063(0.02) 0.046(0.03) 0.022(0.02) 0.073(0.02) 0.030(0.03) 0.051(0.01) 0.028(0.02) 0.034(0.02) β(SE) 0.057(0.06) 0.057(0.08) 0.041(0.07) 0.277(0.12) 0.074(0.09) 0.056(0.14) 0.126(0.110 0.082(0.11) 0.118(0.13) 0.061(0.07) 0.063(0.09) 0.083(0.10) t-value 1.74 1.60 1.95 2.30 2.96 1.41 1.05 2.79 0.99 2.84 1.33 1.39 R2 0.244 0.226 0.195 0.227 0.135 0.208 0.258 0.229 0.243 0.235 0.226 0.236 Month 37 38 39 40 41 42 43 44 45 46 47 48

α(SE) 0.028(0.02) 0.043(0.01) 0.048(0.02) 0.047(0.01) 0.033(0.01) 0.058(0.00) 0.018(0.01) 0.026(0.01) 0.035(0.01) 0.048(0.01) 0.048(0.02) 0.038(0.01) β(SE) 0.094(0.02) 0.012(0.05) 0.025(0.09) 0.001(0.08) 0.065(0.07) 0.004(0.00) 0.100(0.08) 0.068(0.07) 0.031(0.06) 0.025(0.07) 0.008(0.11) 0.042(0.09) t-value 1.42 3.39 2.23 2.53 2.04 3.64 1.15 1.78 2.57 3.21 2.03 1.99 R2 0.252 0.222 0.223 0.188 0.238 0.218 0.268 0.248 0.213 0.206 0.200 0.211 Month 49 50 51 52 53 54 55 56 57 58 59 60

α(SE) 0.061(0.03) 0.014(0.03) 0.057(0.04) 0.021(0.03) 0.002(0.04) 0.024(0.03) 0.071(0.03) 0.012(0.03) 0.019(0.02) 0.015(0.02) 0.050(0.02) 0.014(0.03) β(SE) 0.004(0.12) 0.223(0.12) 0.008(0.13) 0.121(0.12) 0.209(0.13) 0.065(0.10) 0.061(0.12) 0.121(0.12) 0.071(0.06) 0.109(0.09) 0.012(0.08) 0.223(0.12) t-value 1.67 1.77 1.40 0.94 1.56 0.81 1.90 0.99 1.03 1.20 1.95 1.77 R2 0.174 0.148 0.263 0.246 0.119 0.220 0.212 0.252 0.256 0.274 0.201 0.148

20

Table III: Results for the regression SFUTj,t = αs + βs SHISTj,t +γs WISD

The Table reports the estimates from the joint regression tests of implied volatility estimates and historical volatility estimates against future

volatility estimates. t-values are reported separately for each regressor.

Month 1 2 3 4 5 6 7 8 9 10 11 12

β 0.024 -0.040 0.036 -0.061 0.017 -0.049 0.015 -0.039 -0.027 0.074 0.014 0.105 γ 0.470 -0.365 -0.207 0.391 -0.153 0.063 -0.199 0.746 1.009 0.658 0.266 -1.137 t-value(β) 0.01 -0.74 0.84 -1057 0.31 -1.07 0.40 -0.97 -0.32 -1.62 0.18 1.41 t-value(γ) 1.03 -0.90 -0.607 0.76 0.58 0.21 -0.58 1.28 1.07 2.21 0.46 -1.65 R2 0.059 0.092 0.062 0.176 0.325 0.279 0.113 0.332 0.263 0.271 0.314 0.191 Month 13 14 15 16 17 18 19 20 21 22 23 24

β -0.008 0.008 0.167 0.030 -0.125 0.549 0.326 -0.224 -0.028 0.132 0.033 0.212 γ 0.318 -1.104 -0.475 -0.465 0.194 -0.305 -0.077 -0.189 -0.160 0.198 -0.152 0.235 t-value(β) -0.05 0.04 0.83 -0.22 -0.74 2.74 2.30 -1.30 -0.21 1.09 0.37 1.46 t-value(γ) 0.48 -1.12 -0.65 -1.35 0.42 -0.61 -0.28 -0.48 -0.76 1.03 -0.66 0.63 R2 0.315 0.373 0.261 0.297 0.240 0.308 0.260 0.295 0.336 0.209 0.338 0.214 Month 25 26 27 28 29 30 31 32 33 34 35 36

β 0.069 0.071 0.059 0.280 -0.085 0.052 0.126 -0.087 0.073 0.064 0.062 0.081 γ 0.137 0.155 0.216 0.572 -0.202 -0.308 0.266 -0.680 1.281 0.063 0.103 0.504 t-value(β) 1.01 0.80 0.74 2.37 -0.86 0.36 1.03 -0.78 0.60 0.78 0.67 0.80 t-value(γ) 0.68 0.89 0.88 1.30 -0.36 -0.59 0.48 -1.11 2.17 0.10 0.29 1.20 R2 0.368 0.285 0.259 0.297 0.242 0.328 0.371 0.295 0.251 0.336 0.331 0.211 Month 37 38 39 40 41 42 43 44 45 46 47 48

β 0.063 -0.016 -0.152 -0.041 0.041 -0.245 0.099 0.076 0.033 -0.025 0.018 0.044 γ 0.791 -0.208 0.368 -0.381 -0.371 0.081 0.104 0.182 -0.008 0.006 -0.006 0.091 t-value(β) 0.67 -0.27 -0.02 -0.49 0.53 -0.45 1.11 1.06 0.46 -0.31 0.07 0.47 t-value(γ) 1.62 -0.94 1.03 -1.94 -1.36 0.26 0.51 1.06 -0.05 0.02 -0.09 0.32 R2 0.178 0.351 0.363 0.182 0.233 0.322 0.383 0.107 0.313 0.306 0.300 0.317 Month 49 50 51 52 53 54 55 56 57 58 59 60

β -0.006 0.224 -0.005 0.059 0.201 0.092 -0.061 0.148 0.062 0.126 -0.011 0.224 γ 0.938 0.118 0.357 -1.370 -0.299 0.368 -0.002 -0.394 -0.228 0.402 -0.158 0.118 t-value(β) -0.05 1.72 -0.04 0.48 1.46 0.79 -0.45 1.22 0.89 1.37 -0.12 1.72 t-value(γ) 2.31 0.23 0.66 -2.14 -0.49 0.62 -0.03 -1.19 -0.88 -1.11 -0.69 0.23 R2 0.239 0.151 0.225 0.249 0.331 0.343 0.312 0.126 0.397 0.237 0.328 0.251

21

3.2 The hedging strategy results

After establishing the potential short and long positions hedges are

formed. There are 59 holding periods one less than the actual observation

period since each hedge is held for one month. Hedge positions were taken for

all months averaging 6.35 analogous positions every holding period. During

each of periods 3, 8 and 57 one hedge was held. Moreover, for periods 2, 7 and

51 two hedges were selected. For the rest of the holding periods more than

three hedges were selected. The maximum held positions were in period 27

when 11 pairs of short and long positions were assumed.

″take in Table IV″

During the first and last part of the sample period the number of option

contracts was smaller and profits through hedging relatively low. However, in

the middle of the examination period some significant profit opportunities

arose with profits from hedging reaching the 20-25 percent margin. This

phenomenon might be due to higher volatility during that period.

Among the 59 holding periods in six cases the hedges resulted in losses

that did not exceed the six percent boundary. Nevertheless, in the majority of

cases the observed inefficiencies in the options market resulted in profits being

made. The average profit for a trader during the holding period would have

been approximately 6.29 percent. The highest overall profit made on one

month’s hedge positions was 33.48 percent on the 4th month. On the contrary,

22

the highest overall loss made on a single month’s hedge was 5.74 percent on

the 58th month.

In addition of the 375 hedges 312 were profitable which constitutes 83

percent of the total number of hedges. The gain from the short and long

positions was 122 and minus 18 of the anticipated returns respectively.

Furthermore, 89 percent of the constructed portfolios were profitable, a

fact that verifies the correctness of the followed strategy. 37 out of the 71

options selected had opening prices that were considered favourable. Both the

favourable and unfavourable options categories indicated weekly profits of

about 10 percent. Results were modified accordingly to accommodate for the

presence of transaction costs. Commission varies depending on whether the

strategy is executed by a trader or an institutional investor (Nisbet, 1992). It is

assumed that if the simulated strategies were implemented by a professional

arbitrageur the tariffs would sum up to a 0.5 percent increase to the cost of the

formation of the hedge position.

A similar strategy was followed using the historical volatility for

underlying stocks using weekly return data for the period January 1990 –

December 1994. By examining the effects using historical volatility rather than

implied volatility it was attempted to identify discrepancies in our results. The

use of the historical volatility altered significantly our results without

nonetheless enabling us to identify whether it undervalued or overvalued option

23

contracts. Hence no definite conclusions can be made as to the nature that

historical volatility affects our results.

The results of the monthly hedge returns show that the overall profits

made by using the monthly hedges were 8.22 percent. During hedge periods 7,

16, 29 and 45 only one hedge was selected while the maximum number of

hedges was 16 in periods 3 and 52. Furthermore, 92 percent of the formed

hedges were profitable while only three monthly portfolios were negative. Out

of the total number of 395 hedges 323 were profitable while only one negative

hedge exceeded the 10 percent margin. The other three negative monthly

portfolios were minus 3.32, 4.89 and 1.03 percent respectively.

The maximum percentage gain from a monthly portfolio was 26.09 on the

31st holding period. In addition, the gain on the short positions is 141 percent of

the anticipated returns while the loss on the long positions was 9 percent of the

anticipated returns. Lastly, it should be emphasised that the pattern of higher

returns in the tails of the returns distribution that was seen using the implied

volatility is not observable in the historical volatility returns.

24

Table IV: Hedging strategy results using different volatility estimates

The hedging strategy results using WISDs and historical volatility estimates are presented above. The number of hedge positions formed during

each holding period are also reported.

Holding period 1 2 3 4 5 6 7 8 9 10 11 12

Return 11.06% -5.54% 7.25% 33.48% -4.11% 22.66% 3.85% 2.21% 1.53% 10.93% 14.57% 5.45% Number of Hedges 7 2 1 9 6 7 2 1 10 9 8 6 Return using Hist. volatility 6.54% 3.39% 12.21% 24.05% 4.35% -3.32% 7.59% 8.12% 2.25% 10.24% 9.95% -1.03% Number of Hedges 5 3 16 7 9 8 1 5 4 9 8 12 Holding period 13 14 15 16 17 18 19 20 21 22 23 24

Return -5.63% 10.59% 11.26% 43.21% 19.68% 11.03% 0.24% 17.44% 7.20% 42.58% 34.48% -4.60% Number of Hedges 5 10 9 8 9 4 6 9 3 8 5 7 Return using Hist. volatility 3.25% 9.55% 15.32% 17.21% 12.08% -4.89% 5.11% 9.92% 7.29% 18.95% 17.60% 6.69% Number of Hedges 6 9 5 1 6 4 8 9 4 6 8 9 Holding period 25 26 27 28 29 30 31 32 33 34 35 36

Return 30.27% 11.03% 2.27% 23.21% 11.20% 2.33% 8.86% 0.02% 7.73% 10.60% 27.31% 7.12% Number of Hedges 8 6 11 4 6 3 5 7 6 4 8 5 Return using Hist. volatility 7.21% 11.57% 9.54% 6.73% 3.54% 14.88% 26.09% 6.57% 5.11% 3.03% -10.01% 7.28% Number of Hedges 6 7 3 8 1 4 8 6 11 9 4 6 Holding period 37 38 39 40 41 42 43 44 45 46 47 48

Return 13.65% 3.16% -1.13% 11.85% 15.37% 23.60% 25.87% 8.88% 9.69% 5.65% 9.17% 23.30% Number of Hedges 9 4 9 8 10 5 3 8 8 7 9 6 Return using Hist. volatility 10.24% 4.45% 2.32% 1.17% 15.24% 8.64% 11.72% 10.05% 4.58% 7.11% 9.36% 14.68% Number of Hedges 7 10 6 8 7 4 6 5 1 4 9 7 Holding period 49 50 51 52 53 54 55 56 57 58 59

Return 2.47% 42.37% 12.84% 13.59% 6.17% 6.28% 9.33% 14.55% 0.47% -5.74% 2.00% Number of Hedges 4 8 2 8 9 6 8 7 1 9 3 Return using Hist. volatility 4.09% 16.74% 2.25% 11.08% 4.57% 8.99% 11.64% 8.57% 3.26% 12.89% 7.50% Number of Hedges 11 14 3 16 5 8 9 4 6 3 7

25

4. Conclusions

This paper has examined the ability of the Black-Scholes option pricing

formula adjusted for dividend payments to identify mispricing in the options

market for option contracts traded in the London Financial Futures and Options

Exchange. The model proved successful in identifying over and under valued

call options on an ex-post basis. Towards this goal a weighted implied standard

deviation is calculated for each underlying stock for the most accurate

calculation of each stock’s standard deviation.

Regression results proved that the implied standard deviation provides

superior to historical volatility estimates. These results suggested that only

small part of the future volatility was explained by the calculated standard

deviation based on past data. On the contrary, improved estimates of the future

volatility are obtained when the implied standard deviation was used.

Furthermore, the model displayed the previously observed pricing bias by

undervaluing, relative to the market price, out-of-the-money call options and

pricing fairly at and in-the-money call options.

The results of ex-ante performance tests did not support option market

efficiency. Therefore, a trading strategy in the options market would offer

above normal profits for an investor even after transaction costs were

considered. This outcome contradicting the majority of the recent literature in

derivatives exchanges could be attributed to equity options’ thin trading that

causes potential mispricings in the market.

26

In order to determine this result a hedging strategy was followed whereby

above a specified level undervalued option contracts were held as long

positions whereas overvalued option contracts were chosen as short positions.

Monthly hedge returns were mostly positive while the average profit from

trading in the options market during the observation period would have been

6.29 percent. Similar hedge positions were formed based on historical volatility

results. The average portfolio returns were 8.22 percent. However, the lack of

any particular pattern in the observed results prevented us from determining the

nature of influence that the historical volatility had in our results.

The implications of these results are twofold. First, the use of the Black-

Scholes formula is a practical and easy way to identify mispriced call options

that can provide above normal zero risk profits. Consequently, the options

market cannot only be used as a hedge against positions in the underlying

stocks market but also as an investment strategy itself. Secondly, the

transaction costs effect should always be considered as it causes expected

profits to be reduced, even though they do not vanish completely, and in the

context of how often positions should be revised.

References

Bakshi, G., Can, C., Chen, Z., 1997. Empirical Performance of Alternative

Option Pricing Models. Journal of Finance 52 (5).

27

Black, F., Scholes, M., 1972. The Valuation of Option Contracts and a Test of

Market Efficiency. Journal of Finance 27(2), 399-417.

Canina, L., Figlewski, S., 1993. The Information Content of Implied Volatility.

The Review of Financial Studies 6(3) 659-681.

Cavallo, L., Mammola, P., 2000. Empirical tests of efficiency of the Italian

index options market. Journal of Empirical Finance 7, 173-193.

Chiras, D., Manaster, S., 1978. The Information Content of Option Prices and a

Test of Market Efficiency. Journal of Financial Economics 6(2-3), 213-234.

Christensen, B., Prabhala, N., 1998. The Relation Between Implied and

Realized Volatility. Journal of Financial Economics 50(2), 125-150.

Finnerty, J., 1978. The Chicago Board Options Exchange and Market

Efficiency. Journal of Financial and Quantitative Analysis 13.

Galai, D., 1977. Tests of Market Efficiency of the Chicago Board Options

Exchange. Journal of Business 50(2), 167-197.

Harvey, C., Whaley, R., 1992. Market Volatility Prediction and the Efficiency

of the S&P 100 Index Option Market. Journal of Financial Economics 31

Isakov, D., Morard, B., 2001. Improving Portfolio Performance with Option

Strategies: Evidence from Switzerland. European Financial Management 7(1),

73-91.

Jensen, M. C., 1978. Some Anomalous Evidence Regarding Market Efficiency.

Journal of Financial Economics 6(2-3), 95-101.

Joo, T.H., Dickinson, J.P., 1993. A Test of the efficiency of the European

Options exchange. Applied Financial Economics 3.

28

Klemkosky, R., Resnick, B., 1980. An Ex Ante Analysis of Put-Call Parity.

Journal of Financial Economics 8(4), 363-378.

Korn, R., Trautmann, S., 1999. Optimal Control of Option Portfolios and

Applications. OR Spectrum 21.

Merton, R., 1976. Option Pricing when the Underlying Stock Returns are

Discontinuous. Journal of Financial Economics 3(1-2), 125-144.

Nisbet, M., 1992. Put-Call Parity Theory and an Empirical Test of the

Efficiency of the London Traded Options Market. Journal of Banking and

Finance 16, 381-403.

Phillips, S. M., Smith, C.W., 1980. Trading Costs for Listed Options: The

Implications for Market Efficiency. Journal of Financial Economics 8(2), 179-

201.

Sheedy, E., Trevor, R., 1998. Evaluating the Risk of Portfolios With Options.

Centre for Studies in Money, Banking and Finance, Macquarie University,

Working Paper.

Tan, H.J., Dickinson, J.P., 1992. Tests of Options Market Efficiency: A study

of the European Options Exchange. The Review of Futures Market 9, 552-570.

Trippi, R., 1977. A Test of Option Market Efficiency using a Random-Walk

Valuation Model. Journal of Economics and Business 29, 93-98.

Verbeek, M., 2000. A Guide to Modern Econometrics. John Wiley & Sons.

Wilmott, P., Hoggard, T., Whalley, A., 1994. Hedging Option Portfolios in the

Presence of Transaction Costs. Advances in Futures and Options Research 7.

29

Xu, X., Taylor, S.J., 1995. Conditional volatility and the informational

efficiency of the PHLX currency options market. Journal of Banking and

Finance 19(5), 803-821.

![WEP - NYSE Liffe US - Client Spec v1.7[1]](https://static.fdocuments.net/doc/165x107/577d376e1a28ab3a6b95abe2/wep-nyse-liffe-us-client-spec-v171.jpg)