Price volatility Overview of hedging instruments Hedging with futures Hedging with options Hedging...

49

• Price volatility • Overview of hedging instruments • Hedging with futures • Hedging with options • Hedging with swaps • Adapting the instrument & strategy to the market Class 3: Hedging commodity price risk

-

Upload

walter-mclaughlin -

Category

Documents

-

view

273 -

download

2

Transcript of Price volatility Overview of hedging instruments Hedging with futures Hedging with options Hedging...

• Price volatility• Overview of hedging instruments• Hedging with futures• Hedging with options• Hedging with swaps• Adapting the instrument &

strategy to the market

Class 3: Hedging commodity price risk

Cotton Futures High & Low Prices (1980-1997)

0

20

40

60

80

100

120

1980 82 84 86 88 90 92 94 96

Year

Cen

ts /

Lb.

Crude oil, WTI, May 1999 contract (NYMEX)

Risk managementFinance

Bought by institutional investors eager to take on risks

Traded among banksand large institutionalinvestors

Instruments are traded on exchanges, ina transparentmanner

Not traded - bankslay off risks throughvarious operations, including on futuresexchanges

In general,instruments are not traded

Marketing

Forwardcontracts

Futurescontracts

Optionscontracts

Swaps Commodityloans & bonds

Organizedexchanges

Over-thecounter

Commodity seller

Commodity buyer

Customized contractfor forward delivery,at fixed price (based on prices prevailing in the commodity market)

Commoditymarket

a. Forward marketContract

seller

Contract buyer

Standard contract forforward delivery,at fixed price

Liquidmarket

b. Brent oil forward market

Commodity buyer/seller

Bank

Contract for exchangeof financial flows, based on the differencebetween a fixed price and the (published) reference price

Referenceprices

c. Specialized swaps

Commodity buyer/seller

Bank

Commodityfutures & swaps

market

d. “Liquid” swaps

Information

Purchase of contracts to close out position

Sale of contracts to close out position

Active use of markets to lay off risks

Contract for exchangeof financial flows, based on the differencebetween a fixed price and the (futures market) reference price

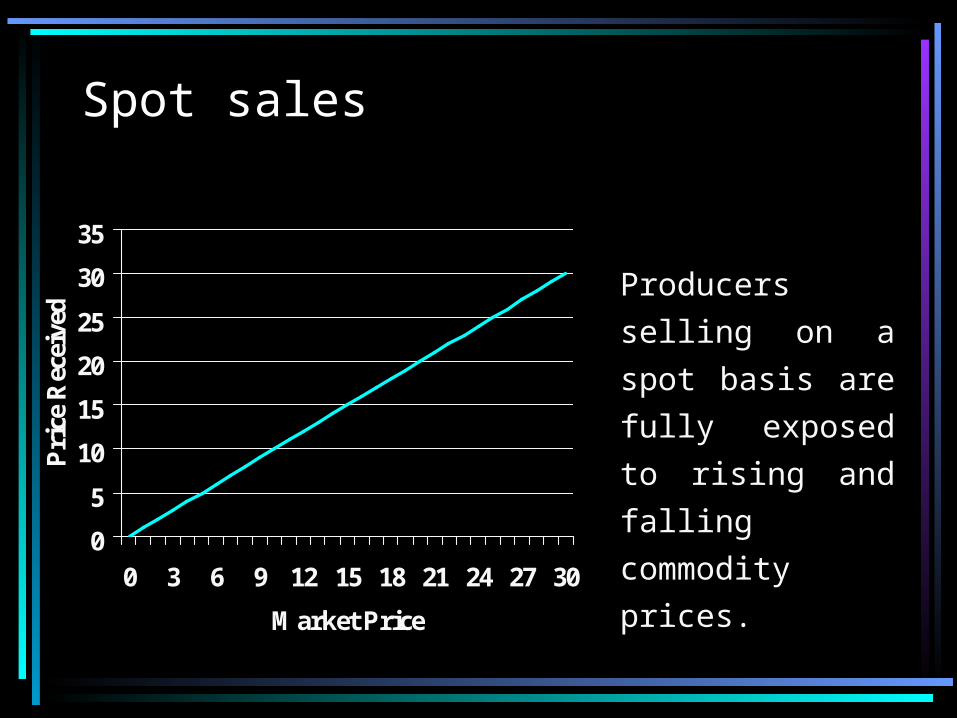

Spot sales

0

5

10

15

20

25

30

35

0 3 6 9 12 15 18 21 24 27 30

Market Price

Pri

ce R

ecei

ved

Producers selling

on a spot basis

are fully

exposed to rising

and falling

commodity

prices.

Spot sales and forwards

0

5

10

15

20

25

30

35

0 2 4 6 8 10 12 14 16 18 20 22 24 26 28 30

Market Price

Pri

ce R

ecei

ved

Spot SalesForwards

Adverse PriceDevelopments

Beneficial PriceDevelopments

Forward sales protectproducers from falling prices,

but remove exposure to beneficial price developments.

Spot sales leave producers fully exposed to price

variations, good and bad.

Futures contracts are standardized

1. Quantity: stated in an agreed unit of measure

2. Quality: Stated in accordance with international standards

3. Expiration months: specifies the duration of the contract

4. Delivery terms: details how delivery is to be executed

5. Delivery dates: a firm fixed future date

6. Minimum price fluctuation: the minimum band within which price fluctuation may be allowed

7. Daily price limits

8. Trading days and hours

Profit/loss

Price of the underlying

Underlying position (long)

Hedge (sale of futures)

Hedging with futures

Physical market price Futures price

1/1 100 110

sell futures <+ 110> (you don ’t get the money, but you have to pay a margin of say, 10)

1/3 90 100

sell physicals +90

close futures (buy) <-100>

profit on futures: +10

Total earnings 100

Hedging - the principle: use the fact that your physical market and the futures market move in parallel, and take a position on the futures market that offsets the risk

exposure that you have in the physical market. In this case, you plan to sell in March.

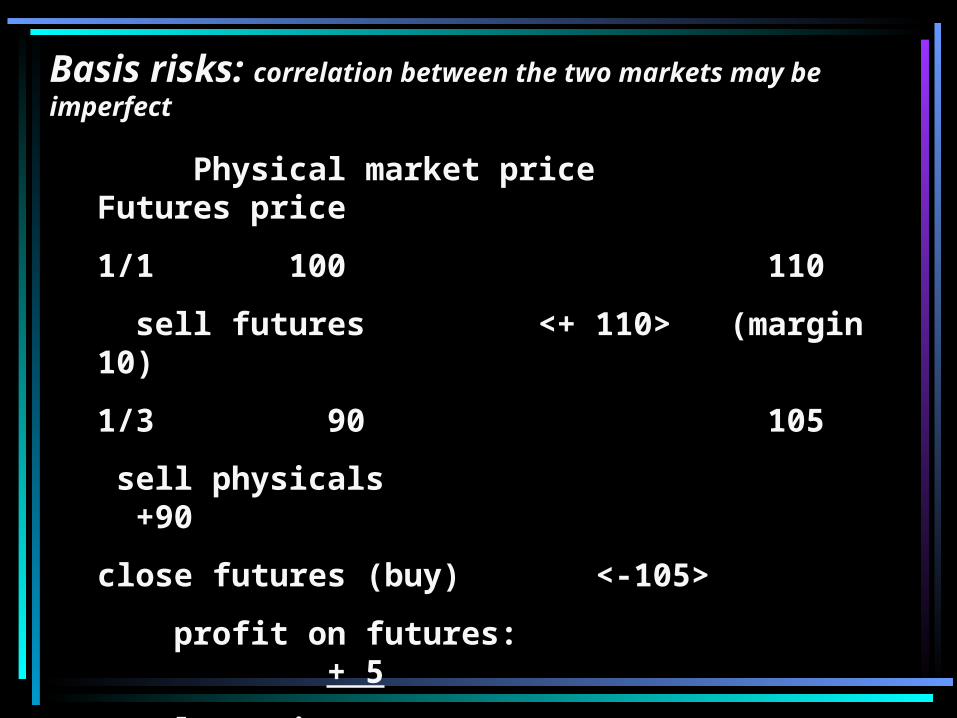

Physical market price Futures price

1/1 100 110

sell futures <+ 110> (margin 10)

1/3 90 105

sell physicals +90

close futures (buy) <-105>

profit on futures: + 5

Total earnings 95

Basis risks: correlation between the two markets may be imperfect

Before hedging

After hedging

Profit

Loss

You do not have to hedge your whole underlying position. You can also hedge part of it.

Futures contracts can be used: - to avoid the effects of fluctuations in prices for producers who, because of their limited production volume or seasonal factors, are not able to spread out their sales over the year; or for consumers, who because of their limited size cannot spread out their purchases; - to protect the value of inventories, or partly finance the cost of storage; - to secure a processing margin; - to "lock in" future prices at an attractive level; and - to improve marketing policies.

The main disadvantages of using futures contracts are that: - they freeze up working capital - although they may provide protection against unfavourable price changes, they do not permit profiting from favourable ones.

Hedging With OptionsHedging With Options

Using futures to cover price risks can provide price protection, but Using futures to cover price risks can provide price protection, but has one important disadvantage: while strongly reducing the has one important disadvantage: while strongly reducing the likelihood of losses, the possibility to benefit from price likelihood of losses, the possibility to benefit from price improvements is also lost. Options do not have this disadvantage.improvements is also lost. Options do not have this disadvantage.

By buying an option, protection can be obtained against By buying an option, protection can be obtained against unfavourable price movements, while the possibility to profit unfavourable price movements, while the possibility to profit from favourable ones remains.from favourable ones remains.

..

This is the basic reason for the use of options for hedging purposes.This is the basic reason for the use of options for hedging purposes.

To determine what option might be useful to protect against price To determine what option might be useful to protect against price risks, firstly the risks have to be identified: are price rises, or on the risks, firstly the risks have to be identified: are price rises, or on the contrary, price declines the risk? Then, to protect against the effects contrary, price declines the risk? Then, to protect against the effects of a price change, an option can be bought giving of a price change, an option can be bought giving profitsprofits when when prices move in the direction that the buyer wants to protect against. prices move in the direction that the buyer wants to protect against. Losses on the physical goods will then be compensated by profits on Losses on the physical goods will then be compensated by profits on

the options, just like is the case for futures contracts.the options, just like is the case for futures contracts.

In the case of futures contracts this kind of price protection is paid for In the case of futures contracts this kind of price protection is paid for by giving up the possibility of profiting from improved prices. In the by giving up the possibility of profiting from improved prices. In the case of options, a fixed price has to be paid: the premium.case of options, a fixed price has to be paid: the premium.

Spot price of the physical at the term period

Profit/loss

Max. loss equal to the premium paid

Unlimited profit

Strike price

Put optionPut optionAs can be seen in As can be seen in the chart of the put the chart of the put option, declining option, declining prices cause losses prices cause losses on the physical on the physical transactions, but transactions, but buying a put buying a put optionoption gives a gives a profit.profit.

For example, if money would be lost when prices decline (such as is For example, if money would be lost when prices decline (such as is the case for a producer who is to sell his production, or for a trader the case for a producer who is to sell his production, or for a trader who has unsold commodities in stock), an option that gives a profit who has unsold commodities in stock), an option that gives a profit when prices decline should be bought. This is called a when prices decline should be bought. This is called a put optionput option. . Graphically, this looks as follows:Graphically, this looks as follows:

If a price increase would involve a loss of money (such as is the case If a price increase would involve a loss of money (such as is the case for a consumer who still has to buy the commodities he needs, or for for a consumer who still has to buy the commodities he needs, or for a trader who has sold commodities for a fixed price, while he does a trader who has sold commodities for a fixed price, while he does not have these commodities in stock), an option can be bought not have these commodities in stock), an option can be bought which gives a profit when prices increase. Such an option is called a which gives a profit when prices increase. Such an option is called a call optioncall option..Graphically, this looks as followsGraphically, this looks as follows

Call optionCall option

Max. loss equal to the premium paid

Profit/loss

Unlimited profit

Strike price

When prices increase, When prices increase, losses are made on losses are made on the physical position, the physical position, but buying a but buying a call call optionoption will then give will then give profits. The result is: profits. The result is: protection against protection against price increases, but price increases, but with still the with still the possibility to profit possibility to profit from price declines. from price declines.

The option is like The option is like insurance: it provides insurance: it provides protection against price protection against price declines (put option) or declines (put option) or price increases (call price increases (call option), and option), and simultaneously the simultaneously the possibility to profit from possibility to profit from reverse price reverse price movements.movements.

moremore

Generally speaking, an option is a contract granting its buyer a Generally speaking, an option is a contract granting its buyer a right, but not the obligation to buy or sell a defined quantity of the right, but not the obligation to buy or sell a defined quantity of the underlying product (for example a futures contract) at a pre-fixed underlying product (for example a futures contract) at a pre-fixed price, and to do so during a period agreed beforehand or upon the price, and to do so during a period agreed beforehand or upon the contract's expiry. contract's expiry.

The option buyer, also called its holder, can choose to let the The option buyer, also called its holder, can choose to let the option expire or to exercise it. On the contrary, the writer or seller option expire or to exercise it. On the contrary, the writer or seller of an of an

Call

Put

Sell Buy

implies an obligation to sell the underlying at the set price, if the call is exercised

gives the right (not the obligation) to buy the underlying at the set price

implies an obligation to buy the underlying at the set price, if the put is exercised

gives the right (not the obligation) to sell the underlying at the set price

option has the option has the obligation to fulfil the obligation to fulfil the contract when the contract when the buyer decides to buyer decides to exercise. exercise.

So with these two So with these two options, four option options, four option positions can be positions can be taken:taken:

Spot price of the physical

Maximum loss equal to the premium paid

Profit/loss

Strike price

Unlimited profit potential

Pre

miu

m

Put optionPut option

Spot price of the physical

Maximum loss equal to the premium paid

Profit/loss

Strike price

Unlimited profit potential

Pre

miu

m

Call optionCall option

American-styleAmerican-style

European-styleEuropean-style

An option is An option is determined bydetermined by

the the stylestyle which d which determines etermines when the holder of an when the holder of an option can exercise his option can exercise his

right) right)

the the strike pricestrike price which is the which is the exercise priceexercise price

the the premiumpremium which is the price of which is the price of the option . It is composed bythe option . It is composed by Time valueTime value

Intrinsic valueIntrinsic value

European-style options may only be exercised at the date of expiration.

European-style options may only be exercised at the date of expiration.

American-styleAmerican-style

European-styleEuropean-style

An option is An option is determined bydetermined by

the the stylestyle which d which determines etermines when the holder of an when the holder of an option can exercise his option can exercise his

right) right)

the the strike pricestrike price which is the which is the exercise priceexercise price

the the premiumpremium which is the price of which is the price of the option . It is composed bythe option . It is composed by Time valueTime value

Intrinsic valueIntrinsic value

American-style options may be exercised at any time between the date of purchase and the date of expiration.

American-style options may be exercised at any time between the date of purchase and the date of expiration.

At the time of transaction, a price is set in terms of the option contract, specifying a price at which the underlying, for example a futures contract, may be bought or sold. This price is called the strike price, or the exercise price. The option buyer may take (call) or make (put) delivery of the contract against this price.

At the time of transaction, a price is set in terms of the option contract, specifying a price at which the underlying, for example a futures contract, may be bought or sold. This price is called the strike price, or the exercise price. The option buyer may take (call) or make (put) delivery of the contract against this price.

American-styleAmerican-style

European-styleEuropean-style

An option is An option is determined bydetermined by

the the stylestyle which d which determines etermines when the holder of an when the holder of an option can exercise his option can exercise his

right) right)

the the strike pricestrike price which is the which is the exercise priceexercise price

the the premiumpremium which is the price of which is the price of the option . It is composed bythe option . It is composed by Time valueTime value

Intrinsic valueIntrinsic value

Options traded on most exchanges are American options. Regardless of what option type is involved, beyond the expiration date, the buyer can no longer exercise his right.

Options traded on most exchanges are American options. Regardless of what option type is involved, beyond the expiration date, the buyer can no longer exercise his right.

When buying an option, a premium has to be paid to obtain the rights laid down in the contract. The premium is the price of the option. It is, like other prices, determined by market forces of supply and demand. As are other market-determined prices, premiums are subject to fluctuations.

When buying an option, a premium has to be paid to obtain the rights laid down in the contract. The premium is the price of the option. It is, like other prices, determined by market forces of supply and demand. As are other market-determined prices, premiums are subject to fluctuations.

It is either positive or zero and indicates the value of the option at any It is either positive or zero and indicates the value of the option at any time. For a call option, the intrinsic value is the price of the time. For a call option, the intrinsic value is the price of the underlying futures contract minus the strike price; the intrinsic value underlying futures contract minus the strike price; the intrinsic value of a put option is equal to the strike price less the futures price. So, a of a put option is equal to the strike price less the futures price. So, a US$ 17US$ 17

Intrinsic value price of the underlying futures Intrinsic value price of the underlying futures contract the strike pricecontract the strike price== --

DefinitionDefinition

crude oil option will have a positive crude oil option will have a positive intrinsic value for call options with a intrinsic value for call options with a strike price below US$ 17 and for put strike price below US$ 17 and for put options that have a strike price of options that have a strike price of above US$ 17.above US$ 17.

When the futures price rises compared to When the futures price rises compared to the strike price of a call option, its the strike price of a call option, its premium will probably increase because premium will probably increase because of increased intrinsic value (since it of increased intrinsic value (since it becomes more likely that exercising the becomes more likely that exercising the call will be profitable). The premium of a call will be profitable). The premium of a put decreases when the price of the put decreases when the price of the underlying future rises, since the intrinsic underlying future rises, since the intrinsic value diminishes; it will become less and value diminishes; it will become less and less interesting to exercise the rights less interesting to exercise the rights conveyed under the option contract. conveyed under the option contract. Following the same reasoning, for a Following the same reasoning, for a futures price decrease, the premium for a futures price decrease, the premium for a call option with a certain strike price gets call option with a certain strike price gets less since the chance of its exercise less since the chance of its exercise diminishes and the price for a put option diminishes and the price for a put option goes up.goes up.

The life-time of an option is one of the factors that determines the The life-time of an option is one of the factors that determines the time value. Suppose the other factors - the price of the underlying time value. Suppose the other factors - the price of the underlying futures, the strike price, volatility and short-term interest rates - futures, the strike price, volatility and short-term interest rates - remain the same. Then, the time value decreases when maturity remain the same. Then, the time value decreases when maturity approaches. The time value is highest when the strikeapproaches. The time value is highest when the strike

Time value Option’s Premium Intrinsic ValueTime value Option’s Premium Intrinsic Value== -- DefinitionDefinition

price equals the price of the price equals the price of the underlying asset. When these two underlying asset. When these two prices diverge, the time value prices diverge, the time value decreases. For then, the chances decreases. For then, the chances of exercise of a put as well as the of exercise of a put as well as the losses of an options seller will be losses of an options seller will be higher. The time value is, so to higher. The time value is, so to say, a time-related flexibility value say, a time-related flexibility value of an option.of an option.

e.g.e.g.

Imagine that all factors determining the time value remain stable and Imagine that all factors determining the time value remain stable and only the volatility of the price of the futures contract underlying the only the volatility of the price of the futures contract underlying the option increases. Bearing in mind that the option serves as an option increases. Bearing in mind that the option serves as an insurance against price changes of the futures contract, it is obvious insurance against price changes of the futures contract, it is obvious that the price that has to be paid to obtain this protection will rise. that the price that has to be paid to obtain this protection will rise. When the futures price is more volatile, there is a growing chance that When the futures price is more volatile, there is a growing chance that in its life the option may become worthwhile to exercise. This induces in its life the option may become worthwhile to exercise. This induces sellers to ask a higher premium, for the risks they run get higher.sellers to ask a higher premium, for the risks they run get higher.

e.g.e.g.

Regardless of the fact if the buyer of the option decides to exercise Regardless of the fact if the buyer of the option decides to exercise his right, the premium, once paid to the seller of an option, remains in his right, the premium, once paid to the seller of an option, remains in the hands of the seller. The maximum amount the options buyer can the hands of the seller. The maximum amount the options buyer can lose on his option position, is the premium paid for the option. His lose on his option position, is the premium paid for the option. His profit potential is virtually unlimited. A seller, on the other hand, can profit potential is virtually unlimited. A seller, on the other hand, can only have profits limited to the premium size; his loss can be only have profits limited to the premium size; his loss can be unlimited, since prices may move to unforeseen low or high levels. If unlimited, since prices may move to unforeseen low or high levels. If the price of the underlying asset drops below the strike price minus the price of the underlying asset drops below the strike price minus the premium paid, the buyer of a put will exercise his right and the the premium paid, the buyer of a put will exercise his right and the seller has to take delivery against payment of the, relatively high, seller has to take delivery against payment of the, relatively high, strike price.strike price.

If a call buyer decides to exercise his option when the strike price is If a call buyer decides to exercise his option when the strike price is below the price of the underlying, the seller is obliged to deliver the below the price of the underlying, the seller is obliged to deliver the underlying asset. If he does not possess it, he will have to buy the underlying asset. If he does not possess it, he will have to buy the asset on the market and suffer a loss equal to the difference between asset on the market and suffer a loss equal to the difference between the market price and the strike price (less the premium which he has the market price and the strike price (less the premium which he has collected), which can be enormous when supply is tight. The sale of a collected), which can be enormous when supply is tight. The sale of a call without the previous purchase of the underlying asset, is said to call without the previous purchase of the underlying asset, is said to be "naked". It is a position meant to collect the premium, a purely be "naked". It is a position meant to collect the premium, a purely speculative and very risky positionspeculative and very risky position..

An option trader who has a net selling position, in other words he has An option trader who has a net selling position, in other words he has sold more option contracts than he bought, is said to be short in sold more option contracts than he bought, is said to be short in options. If a market participant has bought more contracts than he options. If a market participant has bought more contracts than he sold, he is having a long position. sold, he is having a long position.

Following the same reasoning, a price decline is beneficial to Following the same reasoning, a price decline is beneficial to participants having a long put position, for they can sell the participants having a long put position, for they can sell the underlyingunderlyingat the strike price and will at the strike price and will be able to procure the be able to procure the underlying asset on the underlying asset on the market at a lower price. market at a lower price. And short call investors And short call investors will also benefit from a will also benefit from a price drop: the buyer of a price drop: the buyer of a call will not exercise his call will not exercise his right and the premium right and the premium paid remains at the seller's paid remains at the seller's account.account.

e.g.e.g.

Before option Before option contract contract expiresexpires

The buyer canThe buyer can

The seller canThe seller can

Let the contract Let the contract expireexpire

Exercise itExercise it

Close his positionClose his position

Wait for the Wait for the option to expireoption to expire

Close his positionClose his position

When closing out an When closing out an options position, options position, attention should be attention should be paid not only to the paid not only to the expiration date, the expiration date, the offsetting position, and offsetting position, and if course the if course the underlying asset, but underlying asset, but also to the strike price also to the strike price of the relevant option. of the relevant option. This means that a long This means that a long callcall

position can be closed out by selling calls with position can be closed out by selling calls with the same expiration date and the same the same expiration date and the same exercise price; similarly, when having the exercise price; similarly, when having the same expiration date and equal exercise same expiration date and equal exercise prices, a short call can be closed by a long call prices, a short call can be closed by a long call transaction, a long put can be offset by the transaction, a long put can be offset by the sale of a put, and a short put position can be sale of a put, and a short put position can be closed by the purchase of put options.closed by the purchase of put options.

Underlying Instrument: 1 NYMEX Sweet Crude Oil futures contract of 1,000 barrels (42,000 gallons)

Maturities: Twelve consecutive months plus three long-dated options at 18, 24, and 36 months out.

Strike prices: Multiples of US$ 0.50 per barrel for the first nine strike prices; the increments are US$ 1 for the next three strike prices and US$ 5 for the nearest higher or below the nearest lower existing strike price.

Last trading day: The Friday immediately preceding the expiration of the underling futures contract as long as there are three days left to the futures expiration. Otherwise, the option expires the second Friday prior to the futures expiration.

Expiration: 5.30 pm on the last trading day, or 45 minutes after the underlying futures settlement price is posted, is the last possible exercise time.

Tick Size: US$ 0.01 per barrel

The NYMEX Sweet Crude Oil option is traded from 9.45 am. to 3.10 pm. The NYMEX Sweet Crude Oil option is traded from 9.45 am. to 3.10 pm. (New York time). These are the same trading hours as for the (New York time). These are the same trading hours as for the underlying futures contract. As for the underlying futures, out-of-hours underlying futures contract. As for the underlying futures, out-of-hours trading is possible via the NYMEX Access trading system. trading is possible via the NYMEX Access trading system.

Option on NYMEX Sweet Crude Oil FuturesOption on NYMEX Sweet Crude Oil Futures

The use of average prices is one The use of average prices is one of the reason that users may of the reason that users may prefer OTC-rather than prefer OTC-rather than exchange-traded options. For exchange-traded options. For example, a shipping company’s example, a shipping company’s ships take on bunker fuel at ships take on bunker fuel at unpredictable moments, when unpredictable moments, when available at reasonable prices-an available at reasonable prices-an option which is fixed to one option which is fixed to one moment in time is thus difficult moment in time is thus difficult to use. Other reasons one may to use. Other reasons one may use OTC options is that they are use OTC options is that they are available on products not traded available on products not traded on the exchange, and are on the exchange, and are available in more complex forms.available in more complex forms.

Over-the-Counter OptionsOver-the-Counter Options

-2

0

2

4

6

8

10

89 90 91 92 93 94 95 96 97 98

$/b

bl.

Hedging with options allows you to lock in your minimum prices, while keeping full exposure to oil price increases. Below is a simulation for an oil exporter (in red, “loss” relative to market; in green, gain relative to market).

0

5

10

15

20

25

30

35

40

89 90 91 92 93 94 95 96 97 98

$/b

bl.

Market PriceProgram Revenue

Before hedging

After hedging

Profit

Loss

You can also hedge only part of your downside risks.

When buying option contracts, the right, but not the obligation, to buy or sell a futures contract at a given price is obtained. When prices move favourably, this right will not be exercised, and therefore, the purchase of options provides protection against unfavourable price movements, while permitting to profit from favourable ones.

Only the sellers of options have to pay margins. To buy an option, one has to pay a premium - when prices increase, this is the maximum loss from the option purchase. But, simplifying a bit, when prices decline, an options buyer will make a profit which is more or less commensurate with the extent of the price decline.

Options may be a better hedging vehicle than futures in the case of an uncertain supply - e.g. in the case of an oil company that can not be sure of the quantity it will be able to ship. They are often used to protect prices in deals with not fully reliable partners. If a fixed price deal with a seller has been concluded, and this position is covered with a futures contract, one may get stuck with a loss-making uncovered futures contract if the physical leg of the transaction disappears.

The sale of options also allows the generation some profits, but at a high risk, at least if those selling ("writing") are not properly protected by, for example, physical inventory.

SwapsA swap is a purely financial instrument under which specified cash-flows are A swap is a purely financial instrument under which specified cash-flows are exchanged at specified intervals. A swap can be described as a series of exchanged at specified intervals. A swap can be described as a series of forward contracts each with the same price but does not involve deliveries of forward contracts each with the same price but does not involve deliveries of physical commodities. In summary, physical commodities. In summary, swaps transactions are purely financial swaps transactions are purely financial instruments that are used to reduce price risks and to manage cash flowsinstruments that are used to reduce price risks and to manage cash flows..

Guarantee Guarantee income income streamsstreams

Obtain easier Obtain easier and cheaper and cheaper

access to access to capitalcapital

Lock in long-Lock in long-term pricesterm prices

From financial operations or new

investments

Tailor-made to cover the needs of the company

Long term instrument

Combination of price hedging and investment

securitization

No or less-strict margin calls

Low administrative costs once structured

Example of a straightforward swapAssume a trader who wants to protect himself against falling prices and therefore wants to lock in the price of his sales of 100 tons of white sugar annually, over a period of 5 years. A bank accepts to carry the price risks for these sales.

Assume a trader who wants to protect himself against falling prices and therefore wants to lock in the price of his sales of 100 tons of white sugar annually, over a period of 5 years. A bank accepts to carry the price risks for these sales.

Commodity: SugarAmount: The U.S. dollar equivalent of 100 tons of white sugar

every year.Payer of fixed price: Commercial bankPayer of floating price: TraderTenor: Five years, with annual paymentsFixed priced: 13.00 cts/lb (0.05 premium above the market price)Floating price: The average daily closing spot price of the white

sugar over the year preceding each payment date.Settlement: Netting-out

Commodity: SugarAmount: The U.S. dollar equivalent of 100 tons of white sugar

every year.Payer of fixed price: Commercial bankPayer of floating price: TraderTenor: Five years, with annual paymentsFixed priced: 13.00 cts/lb (0.05 premium above the market price)Floating price: The average daily closing spot price of the white

sugar over the year preceding each payment date.Settlement: Netting-out

The swap deal The swap deal can be described as follows:

1. The financial intermediary (i.e. the bank) undertakes to pay the trader an agreed fixed price (i.e. 13 cts/lb) times a specified tonnage of the product (100 tons of sugar), and in return the trader is obliged to pay the bank an average of the daily closing spot price of the white sugar over the year preceding each payment date.

2. At regular intervals (i.e. annually) and during the life of the swap (i.e. five years), the fixed and the moving prices are compared and the difference, netted out, is paid to the deserving party.If the average fluctuating (world) price is than the agreed fixed price, the bank has to pay the difference to the trader; orIf the average fluctuating (world) price is than the agreed fixed price, the trader has to pay the bank.

3. A fixed deposit in addition to the potential compensating payments have to be paid by the trader to the bank, as performance guarantee.

MarketMarket

Trading houseTrading house BankBank RefineryRefinery

Spot priceSpot price

Spot priceSpot price

Cts/lb 13.00 Cts/lb 13.35

The trader has fixed his selling price at 13 cts/lb

The refinery has fixed its buying price at 13.35 cts/lb

•Over the next five years, the trader will be selling white sugar at the spot price but will be effectively receiving fixed revenues at a price of 13 cts/lb from the bank.

•In order to lay off price risks, the bank will conclude a similar deal with a market participant (a refinery) that wishes to pay a fixed price in exchange for the market prices. The refinery thus fixes the price it will pay for its annual 100 tons of sugar input requirements that it buys on the spot market. If the bank cannot find a counterparty, it can layoff its risks on the futures market.

Swap sale

The sugar swap allows the trader to lock-in the selling price of his sugar to 13 cts/lb.

Trader Bank

Pays cash when sugar prices are

high

Pays cash when sugar prices are low

Sugar swap fixed price 13 cts/lb.

Market price.

The trader pays the bank

The bank pays the trader

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan

Pricects/lb

13

12

14

15

Benefits from the average-sugar price swap

The trader has hedged his cash flows from sugar trade. Even if the price of sugar declines to say, 10 cts/lb, the trader’s total revenues stay the same. The commodity swap allows the trader to lock-in the price of the 100 tons of sugar he will be selling annually for the next five years.

The trader will actually sell the sugar in the spot market but will receive 13 cts/lb from the bank; shifting away price risk fluctuations.

The trader will, therefore, receive a compensatory financial payments if the prices are indeed lower than 13 cts/lb but will have to give up its unexpected benefits if prices turns out to be higher than expected: thus the swap has more or less guaranteed “net price”.

The reduced risk would:

improve the trader’s credit rating

and thus,

enhance marketing offer,

lower the cost of financing

working capital or,

provide access to new lenders.

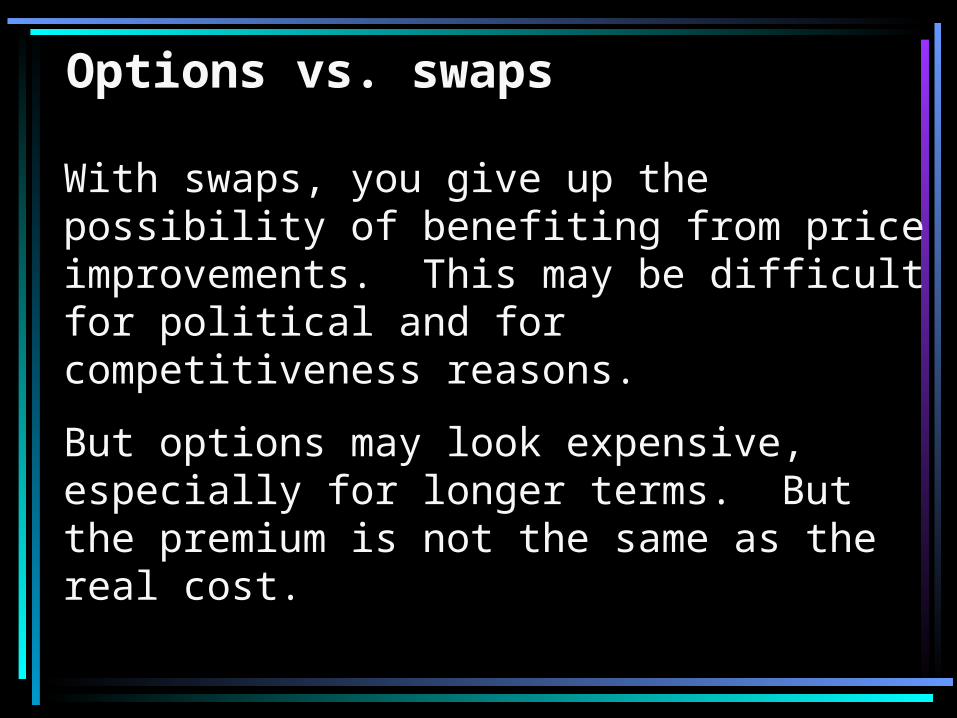

Options vs. swapsOptions vs. swaps

With swaps, you give up the possibility of benefiting from price improvements. This may be difficult for political and for competitiveness reasons.

But options may look expensive, especially for longer terms. But the premium is not the same as the real cost.

Premium of nearest white sugar futures contract over nearest raw sugar futures contract

cts/lb

0

Arbitrage. At times, you may have a choice of markets in which to hedge. E.g., a raw sugar producer could hedge in the New York No. 11 raw sugar contract, or in the London white sugar contract; an oil exporter/importer could hedge in Brent in London, or in light sweet crude in New York. The best choice depends on the price relation between the two. This relation normally moves within certain bands, and if it moves out “arbitrage” transactions by both hedgers and speculators are likely to bring it back within the “normal” range.

White sugar becomes relatively cheap. Good time for ……………………………… ……… to hedge in white, rather than raw sugar futures.

White sugar becomes relatively expensive. Good time for …………………… ………… to hedge in white, rather than raw sugar futures.

Backwardation. Common nowadays for many commodities, including crude oil, metals other than gold, and sugar

Time of contract expiration

price

price

Contango. Common nowadays only for precious metals, and often visible in markets for coffee, cocoa, and grains

March 99 May Sept Dec Mar 2000 May etc.

March 99 May Sept Dec Mar 2000 May etc. Time of contract expiration

forward pricing curve, copper

$1'000.00

$1'500.00

$2'000.00

$2'500.00

$3'000.00

$3'500.00

cash 3 months 15 months 27 months

US

$ p

er t

on

ne

31/12/93

30/12/94

29/12/95

31/12/96

31/12/97

31/12/98

30/12/99

Price volatility and hedging strategies

Rule of thumb: if volatility is high, hedge with futures. If low, hedge with options.

Dynamic versus static hedges

time

pricesell

You start with a long hedge

re-hedge

Downward trend: eliminate hedge

At first sign of trouble, put hedge on again

![Nail In The Coffin The Irony in the Variance Swaps...“Variance swaps are ideal instruments to bet on volatility: unlike vanilla op tions, [they] do not require any delta-hedging.”](https://static.fdocuments.net/doc/165x107/61290b8ab1c9ea19794324b3/nail-in-the-coffin-the-irony-in-the-variance-swaps-aoevariance-swaps-are-ideal.jpg)

![Hedging with a portfolio of Interest Rate Swaps 2_1_2.pdfHedging with a portfolio of Interest Rate Swaps ... working paper [2], ... A plain vanilla Interest Rate Swap (IRS) ...](https://static.fdocuments.net/doc/165x107/5aaeb2bc7f8b9a07498c7560/hedging-with-a-portfolio-of-interest-rate-212pdfhedging-with-a-portfolio-of-interest.jpg)