TIKEHAU SUBORDONNEES FINANCIERES - Tikehau …/media/Files/T/Tikehau-Capital/documents/... · -...

43

Open-ended Mutual Fund governed by French law TIKEHAU SUBORDONNEES FINANCIERES ANNUAL REPORT As at 30 December 2016 This English version is provided to you for information purposes only. Only the French version is binding and enforceable on the parties and the investors and, in case of discrepancy between the two versions, the French version will prevail. Management Company: Tikehau Investment Management Custodian: Caceis Bank Statutory Auditors: Ernst & Young Audit Tikehau Investment Management - 32 rue de Monceau - 75008 - Paris

Transcript of TIKEHAU SUBORDONNEES FINANCIERES - Tikehau …/media/Files/T/Tikehau-Capital/documents/... · -...

Open-ended Mutual Fund governed by French law

TIKEHAU SUBORDONNEES FINANCIERES

ANNUAL REPORT

As at 30 December 2016

This English version is provided to you for information purposes only. Only the French version is binding and enforceable on the parties and the investors and, in case of

discrepancy between the two versions, the French version will prevail.

Management Company: Tikehau Investment Management

Custodian: Caceis Bank

Statutory Auditors: Ernst & Young Audit

Tikehau Investment Management - 32 rue de Monceau - 75008 - Paris

2

1. CARACTERISTICS OF THE UCI

• Structure of the Fund Open-ended Mutual Fund (FCP). • Classification Bonds and other international debt securities. • Procedures for the determination and allocation of income: The income of the Fund is fully reinvested in the case of A, S, E and C units. It is distributed in the case of D units. • Investment objective: The Fund seeks to generate an annual performance that exceeds that of the EuroMTS 3-5 Index over an investment horizon of three years, minus the actual management fees for each unit class. • Benchmark index: Investors’ attention is drawn to the fact that the portfolio’s management style will never consist in tracking the composition of a benchmark index. However, the EuroMTS 3-5 Index may be used as an ex-post performance indicator. The level of the EuroMTS 3-5 Index can be viewed on the Internet, on www.euromtsindex.com, for instance.

• Investment strategy: a) Strategy used

The Fund is a fixed income fund that will primarily invest in subordinated debt securities (Tier 1, Upper or Lower Tier 2, or other) issued by European financial institutions (banks and insurance companies). A debt is said to be subordinated when its redemption depends on the other creditors (preferred and non-preferred creditors) being paid first. Thus, the subordinated creditors will be repaid after the ordinary creditors but before shareholders. The interest rate on this type of debt will be higher than on other receivables. Some Tier 1 bonds may not pay a coupon under certain conditions. Such non-payment may not be considered as a default. The Fund will also invest in derivatives for hedging and/or exposure purposes; such positions will be held with a medium to long-term view. The aim is to receive the income generated by the portfolio, and to optimise that income via an exposure that may amount to up to 130% of the net assets used for hedging and exposure purposes.

Modified duration range

Security issuers Security issuers’ geographical area

Corresponding exposure range

Between 0 and 6 Entities in the private and public sectors

Mainly in the euro zone. Other regions: OECD

Up to 130%

The aim is not to engage in any short-term arbitrage processes, except on an exceptional basis. The Fund's strategy is related to the intrinsic characteristics of the asset class in question. Debt securities in the "subordinated debt instruments" category carry a higher risk of default and offer a potentially high yield. The management company’s investment process seeks to capitalise on the major opportunities that exist in this bond market segment, primarily through selecting securities that have a high likelihood of being called. A call corresponds to the early redemption of a bond, and may therefore result in the potential revaluation of the security in question, thereby contributing to the Fund’s performance. As a result, the Fund’s investment strategy will be based on three main factors:

3

The level of the yield curve

o The average maturity of the portfolio will depend on expectations on changes in interest rates.

The general level of risk premiums, and their structure for borrowers

o The premium represents the return on risk for the asset class. The portfolio will have a minimum average rating of B+ (according to the Standard and Poor's/Fitch rating system B1 according to Moody's, or equivalent according to the analysis of the management company) with a modified duration of between 0 and 6. The Fund will constantly be involved in the fluctuations in this premium depending on the break-even points generated by the return on the portfolio.

o Each bond will have a minimum rating of CCC+ or equivalent according to the analysis of the management company when purchased (excluding the regulatory maximum of 10% of net assets (other eligible assets) where the bonds in which the Fund invests may be unlisted). In the event that the rating deteriorates, the asset management company will reserve the right to keep the bond, or not keep it in its portfolio.

The rating applied by the management company will be the highest obtained from the agencies Standard and Poor's, Fitch and Moody’s or equivalent according to the analysis of the management company. The management company leads its own analysis credit in the selection of the bonds to the acquisition and in the course of life.

Study of the different subordinated debt structures

o These structures have their own characteristics (repurchase option, option for deferred or non-payment of coupons or capital). The study and evaluation of these structures will be a major component of the investment strategy.

b) Financial instruments used The financial instruments likely to be used to implement the investment strategy are listed below: Assets used (excluding derivatives):

o Debt securities and money market instruments: up to 130% of net assets o The Fund will invest primarily in private debt securities (bonds or subordinated

bonds). The average issuer rating envisaged is B+ or equivalent according to the analysis of the management company.

o The average maturity of most of the bonds in the portfolio (regardless of whether they are perpetual) will be lower than 10 years on the date of the security’s next call; however, the Fund will invest in certain perpetual bonds.

o An increase in interest rates will result in a decrease in the value of the fixed-rate and potentially of the floating-rate bonds held by the Fund, along with the value of certain bond UCITS/funds held by the Fund. This means that upward or downward movements in interest rates will have an impact on the Fund’s net asset value. The risk is measured through sensitivity. For the Fund, sensitivity lies between 0 and 6. The occurrence of this risk may result in a decrease in the UCITS’ net asset value.

o The Fund can invest in bonds emitted by Debt Securitisation Funds respecting the provisions of the article R214-9 of the Monetary and financial Code (including Debt Securitisation Funds managed by Tikehau Investment Management and for whom the management company may impose structuring and management charges).

o This asset class will account for most of the capital investments.

o Units or shares of French or European UCITS and investment funds (FIA): up to 10% of net assets. For purposes of diversification, the Fund may invest up to 10% of its net assets in:

o units or shares of French or foreign UCITS

4

o or in units or shares of other French or foreign UCIs or foreign investment funds which meet the conditions laid down in Paragraphs 1 to 4 of Article R. 214-13 of the French Monetary and Financial Code.

o Listed Debt Securitisation Fund shares (or up to 10% of net assets if unlisted). The Fund may invest in units of Debt Securitisation Funds which meet the conditions laid down in article R214-9 of the French Monetary and Financial Code. This fund can be managed by Tikehau Investment Management and for which the management company may impose structuring and management charges.

The Fund may invest in units or shares of UCITS or FIA managed by Tikehau Investment Management or a company connected

o Exposure to the equity markets: up to 10% of net assets. The Fund may hold equities admitted to trading directly or when the debt securities held by the Fund are converted to or redeemed in equity capital. The Fund may invest in shares of companies of all market capitalisations and of all geographic regions. Moreover, the Fund may have exposure to the equity markets through investment in units or shares of UCITS.

o Securities with embedded derivatives: up to 100% of the net assets through bonds redeemable in shares. The Fund can invest in refundable bonds in shares, convertible bonds, including in the contingent convertible bonds (Cocos) and instruments likened until 100 % of its net asset,

Forward financial instruments: Types of markets: For purposes of hedging its assets and/or achieving its investment objective, the Fund may make use of financial contracts, traded on regulated markets (futures) or over the counter (options, swaps, etc.). In this respect, the portfolio manager may build an exposure to or a synthetic hedge on CDS indices, sectors of business activity or geographical regions. Accordingly, the Fund may initiate positions with a view to hedging the portfolio against certain risks (interest-rate, credit, or currency risk) or to gain exposure to interest-rate and credit risk. Risks in which the portfolio manager wishes to invest:

- Interest-rate risk - Currency risk: - Credit risk - Equity risk

Nature of investment:

- Hedging - Exposure

Types of instruments used:

- Interest rate options - Futures on interest rates and indices, on equities and equity indices - Options on bonds and indices, on equities and equity indices - Interest rate hedging instruments (swaps, swaptions) and CFD - Transactions in Credit Default Swaps (CDS) or via ITRAXX indices - Currency swaps: - Some of the liabilities of the Fund may be denominated in currencies other than the base

currency to benefit from a lower cost of carry or a devaluation of the currency (for example: a bond denominated in € may be financed in Swiss Francs).

- Similarly, assets may partially include exposure to currency for purposes of appreciation or for higher return (for example, part of the assets may be invested in £ without hedging the currency).

- Asset Swaps: contracts that enable the delivery of a (conventional or convertible) bond to the counterparty via swapping the physical security against its nominal value and via arranging an interest-rate and/or currency swap with a margin (known as an asset swap). The seller of the asset swap is hedged against credit risk.

5

- The Fund may use OTC (index) options on liquid underlying assets that do not pose any valuation issues (vanilla options). The managers are not planning to use over-the-counter financial instruments that are really very complex, and where the valuation may be uncertain or incomplete.

Strategy for using derivatives: Credit derivatives will be used in the context of the Fund’s management in cases where the Fund requires an active credit risk management policy. Their transaction market may be regulated, organised or over the counter. The use of credit derivatives will meet three fundamental requirements:

The implementation of long or short directional strategies Alongside positions in underlying cash assets, credit derivatives will primarily be used in the following cases: o There are no underlying cash assets for a given issuer; o There are no underlying cash assets for the desired length of exposure to a given issuer o The relative value of the underlying cash assets and the derivatives justifies the investment

Implementing spread strategies between issuers, and credit curves for the same issuer, or arbitrage strategies between the same issuer’s products (cash against derivatives).

The Fund will prioritise the use of listed instruments, although it may nonetheless use financial instruments traded over-the-counter. Authorized counterparties: Within the framework of the operations traded over-the-counter, the counterparties will be financial institutions specialized in this type of transactions. Additional information on the counterparties in the transactions will appear in the annual report of the Fund. These counterparties will have no discretionary power on the composition or of the management of the portfolio of the Fund. Management of the financial guarantees: Within the framework of operation on financial instruments traded over-the-counter, certain operations are covered by a policy of collateralization. This policy consists in making margin calls in cash in the currency of the fund to cover the latent result of the operation according to thresholds of releases. Deposits: The Fund may invest its excess cash in term deposit accounts. These deposits may amount to up to 100% of the Fund’s assets. Cash borrowing: The Fund may borrow up to 10% of its assets in cash on an exceptional basis. Temporary purchases and disposals of securities: The Fund may sell financial instruments on a temporary basis (security lending, and repos, etc.) up to an amount equivalent to 100% of its net assets. The Fund may purchase financial instruments on a temporary basis (borrowing securities, and reverse repos, etc.) up to an amount equivalent to 10% of its net assets. This limit will be raised to 100% in the event of reverse repos in exchange for cash, on condition that the financial instruments that are the subject of the repo are not included in any disposal transaction, including temporary transactions or the granting of guarantees. All revenues resulting from efficient portfolio management techniques, net of direct and indirect operating costs, are returned to the Fund. Authorized counterparties: Within the framework of the operations traded over-the-counter, the counterparties will be financial institutions specialized in this type of transactions. Additional information on the counterparties in the transactions will appear in the annual report of the Fund..

6

The selection of counterparties for over-the-counter transactions on derivatives and security loans complies with a “best selection” procedure. These counterparties will have no discretionary power on the composition or of the management of the portfolio of the Fund. Management of the financial guarantees: Within the framework of operation on financial instruments traded over-the-counter, certain operations are covered by a policy of collateralization. This policy consists in making margin calls in cash in the currency of the fund to cover the latent result of the operation according to thresholds of releases. In case of reception of the financial guarantee in cash, this one will be or:

- Placed in deposit with entities prescribed to the article 50, f), with the directive UCITS; - Invested in sovereign bonds of high quality; - Used for the purposes of transactions of reverse repurchase transactions, provided that these

transactions are concluded with credit institutions being the object of a prudent supervision and provided that the fund can call back at any time the total amount of liquid assets by taking into account accrued interest;

- Invested in short-term monetary collective investment undertakings (such as define in the orientations ESMA for a common definition of the European monetary collective investment undertakings).

Internal limits on benchmark entities and assets: The list of benchmark entities will be the same as that laid down in Article R. 214-14 3°) of the French Monetary and Financial Code for French UCITS. The investment strategy requires monitoring the financial structure of all issuers via an internal database, regardless of whether they are Investment Grade or Speculative Grade (below BBB-). Each position initiated on a particular issuer will moreover be subjected to a detailed financial analysis to assess the probability of default. For issuers whose credit is not covered by the rating agencies, it will be necessary to:

Perform a comparative study of the issuer and of their balance sheet structure compared with their main sector peers

Deduce a credit spread from the financial ratio analysis, using structural models. A comparison will need to be made between the spread obtained and the spread applied in the credit market (which can be observed based on the prices on credit derivatives such as CDS).

In the case of an unrated issuer, the credit spread level and degree of subordination will be used as criteria for determining the risk limits for each issuer. The use of derivative instruments may result in exposure amounting to up to 130% of net assets. Contracts amounting to financial collateral: The Fund will offer a Bank or Financial Institution granting it an overdraft facility a guarantee in the simplified form provided for by Article L. 431-7 et seqq. of the French Monetary and Financial Code. • Risk profile: Please Note: Your money will be invested primarily in financial instruments selected by the management company. These instruments will be subject to market trends and risk. Risk of capital loss: The capital is not guaranteed. Investors may not recover the value of their initial investment. Risk of release of the mechanism of the hybrid bonds: The Fund can know a direct or indirect equity risk or of rate / credit, linked to the possible investment in hybrid bonds (subordinated bonds, convertible bonds, refundable bonds in shares, …). The value of these instruments depends on several factors: level of the interest rates, the evolution of the equity price underlying, early refunds / delays or stop of the refunds on the subordinated bonds. These various elements can pull a reduction in the asset value of the fund.

7

Specific risks linked to the investment in the contingent convertible bonds:

Trigger level risk: trigger levels differ and determine exposure to conversion risk depending on the CET1 distance to the trigger level. Coupon cancellation: Coupon payments on AT1 instruments are entirely discretionary and may be cancelled by the issuer at any point, for any reason, and for any length of time. Capital structure inversion risk: contrary to classic capital hierarchy, CoCo investors may suffer a loss of capital when equity holders do not. Call extension risk: AT1 CoCos are issued as perpetual instruments, callable at pre-determined levels only with the approval of the competent authority. Yield/Valuation risk: investors have been drawn to the instrument as a result of the CoCos’ often attractive yield which may be viewed as a complexity premium.

Risk relating to investments in speculative high-yield securities: This UCITS must be considered as partially speculative, and is more specifically intended for investors who are aware of the inherent risks of investing in securities that have low credit ratings or are unrated, which may result in a decrease in the net asset value. Credit risk: the UCITS may be fully exposed to the credit risk on private and public issuers. In the event that their financial position deteriorates, or that they default, the value of the debt securities may fall and result in a decrease in the net asset value. Interest-rate risk: the Fund may be fully exposed to interest-rate risk at any time; sensitivity to interest rates may vary depending on the fixed-rate securities held, and may result in a reduction in the Fund’s net asset value. Discretionary risk: the discretionary management style is based on anticipating changes in the various markets (bonds). There is a risk that the Fund may not be invested in the best-performing markets at all times. Risk associated with futures commitments: as the Fund may invest in financial futures up to a maximum exposure equivalent to 130% of net assets, the Fund’s net asset value may therefore experience a steeper decline than the markets to which the Fund is exposed. Liquidity risk: liquidity may sometimes be low, particularly in over-the-counter markets. Especially in turbulent market conditions, the prices of portfolio securities may experience significant fluctuations. It can sometimes be difficult to unwind some positions on good terms for several consecutive days. There can be no assurance that the liquidity of financial instruments and assets will always be sufficient. Indeed, the Fund's assets may suffer from adverse market developments that may make it more difficult to adjust positions on good terms. The Fund is exposed to currency and counterparty risk on an ancillary basis. Equity risk: up to 10% of the Fund may be exposed to the equity market; the Fund’s net asset value will decrease in the event of a decline in the equity market. Currency risk: the Fund may be exposed to currency risk in proportion to the portion of net assets invested outside the euro zone that is not hedged against this risk, which may result in a decrease in its net asset value. Counterparty Risk: the Fund may be required to perform transactions with counterparties that hold currencies or assets during a certain period. Counterparty risk can be generated by the use of derivatives or securities lending and borrowing. The Fund therefore carries the risk that the counterparty does not carry out the transactions instructed by the Management Company due to insolvency, bankruptcy of the counterparty among others, which may cause a decline in the net asset value. Managing this risk entails the process of choosing counterparties both for brokerage and over-the-counter transactions. Risk of conflict of interests: the fund can be invested in OPC managed by Tikehau IM or company connected or securities issued by these OPC. This situation can be source of conflicts of interests.

8

• Guarantee and protection: The Fund offers no guarantee or protection. • Target investors and investor profile: The Fund's units are not open to investors with the status of "U.S. Person" as defined in Regulation S of the SEC (Part 230-17 CFR230.903). The Fund is not, and will not be, registered under the U.S. Investment Company Act of 1940. Any resale or transfer of units in the United States of America or to a "U.S. Person" may constitute a violation of U.S. law and requires the prior written consent of the management company of the Fund. Those wishing to acquire or subscribe for units must certify in writing that they are not "U.S. Persons". The Fund's management company is empowered to impose restrictions (i) on the holding of units by a "U.S. Person" and thus effect the compulsory redemption of units held; or (ii) on the transfer of units to a "U.S. Person". This power also extends to any person (a) who is shown to be directly or indirectly in contravention of the laws and regulations of any country or government authority, or (b) who could, in the opinion of the Fund's management company, cause the Fund to suffer harm that it would not otherwise have undergone or suffered. The offer of units has not been authorised or rejected by the SEC, by the specialist commission of a U.S. state or any other U.S. regulatory authority, nor have those authorities pronounced on or sanctioned the merits of such offer, or the accuracy or adequacy of documents relating to this offer. Any statement to this effect is contrary to law. Any unitholder must immediately inform the Fund's management company in the event that they become a "U.S. Person". Any unitholder who becomes a U.S. Person will not be allowed to acquire new units and may be requested to dispose of their units at any time to persons who do not have the status of "U.S. Person". The Fund's management company reserves the right compulsorily to redeem any units held directly or indirectly by a "U.S. Person", or if the holding of units by any person whatsoever is contrary to law or to the interests of the Fund. The definition of "U.S. Person(s)" as defined in Regulation S of the SEC (Part 230-17 CFR230.903) is available at the following address: http://www.sec.gov/laws/secrulesregs.htm Class A and S units are intended for institutional investors who wish to build an exposure to the credit market, a market that in general sees smaller fluctuations than the equity market. The minimum initial subscription amount is set at one (1) million euro (€) for Class A units and ten (10) million euro (€) for Class S units. For Class C and D units, this Fund is open to all investors, especially those who seek exposure to the credit market, a market that in general sees smaller fluctuations than the equity market. The minimum initial subscription amounts are set at 50,000 euro (€) for C and D units. Class E units are exclusively reserved for executive officers and employees (investing either directly, or through all companies under their control), shareholders, companies or invested funds under the control (i) of the portfolio management company or (ii) of any company directly or indirectly controlling the portfolio management company, the term "control" being used according to the meaning of Article L233-3 3-37 of the French Commercial Code. The minimum initial subscription amount is set at 1,000 euro (€) for E units. The recommended investment period is 3 years. The amount that is reasonable to invest in the Fund will depend on the personal circumstances of each unitholder. To determine this, each holder should take into account their personal wealth, the laws applicable to them, their current requirements over an investment horizon of at least 3 years, but also their willingness to take risks or opt instead for a prudent investment. It is also highly recommended that investors sufficiently diversify their investments so as not to be exposed solely to the risks of this Fund.

9

2. CHANGES DURING THE FISCAL YEAR OR FOR THE FISCAL YEAR TO COME

None.

10

3. INVESTMENT MANAGER’S REPORT

State of the financial markets on 2016

New the crisis of 2008, had we experienced such widespread risk aversion. All asset classes were in negative tendency at the beginning of 2016, with the exception of “safe investments” such as sovereigns or gold. Fears regarding Chinese growth, continuing economic slowdown, decrease in oil prices, mistrust in all the European banking industry as well as growing concerns about recession in the United States, have crystallized fears and led to a strong resurgence of volatility. In this extremely volatile conditions, we witnessed a strong increase in the correlation between risky assets, pacing with changes in oil prices. After a low point in mid-February, the trend reversed in March with a marked upturn on all asset classes. Unusually, the price of oil and actions by two major central banks have played a major role in the market sentiment reversal: a much more dovish comments from the FED and an extension of the European Central Bank asset purchase program to better rated companies. Then, even though in background, central banks PR began to become less important while macroeconomic data and geopolitical concerns have been dictating the tone on the financial markets.

“Brexit” was the first crisis shake. June 2016 will remain the date when United Kingdom voted in favour of leaving the European Union. The vote outcome took by surprise a substantial number of investors, which led to a downside movement for a majority of risky assets during the next two days. But this effect did not last long, as global central banks, proved willing to counter the uncertainties resulting from the vote, reassured the markets and assured a safe recovery.

This upward movement has continued during the summer until coming close to the US elections. Then, come the second geopolitical shake of the year with the election of Donald Trump as President of the United States. However, beyond the victory of populist theses, the markets were more focused on implications in purely economic terms, particularly regarding budget stimulus and tax cuts. A few hours later, the markets closed higher.

In parallel with the upward movement mentioned earlier, the continuing rebound in oil price, combined with more and more comforting macroeconomic releases, started a progressive increase of interest rates from their low point of mid-July. Deflation disappeared slowly in favour of an inflation coming back. The process accelerated after the U.S. elections. Indeed, on paper, it appears that Donald Trump writes a new page in terms of growth perspective and inflation. However, the question of how to finance such a plan in presence of a significant debt is raised. Even though details have not been disclosed, hopes are still high as shown by inflation expectations. This unshakeable increase in price for risky assets continued until the end of the year, in spite of the third and last geopolitical shake: the Italian referendum. Italians said “no” to Matteo Renzi. Although it enhances the mid-term risk of political instability in the euro area, particularly with the perspective of early elections in the second trimester of 2017 combined with the growth of the far right (Five star movement), this result was broadly expected. The hope of an ECB on the bedside of Italian economy and the absence of a negative surprise have led to an unwinding of hedging strategies and trade-offs favourable to risky assets, only two hours after the markets opening. Lastly, how could we not mention the central banks “dance” in December. The objective was simple: adjust their strategy to face a less and less deflationary environment. They did not disappoint. The ECB will reduce its monetary policy from next March until the end of 2017. The ECB has also softened its policy by integrating sovereign debts with a maturity of between one and two years as well as sovereign debts yielding the overnight rate (-0.40%). By acting this way, the ECB marks a slight inflation comeback but a weak growth that will probably be sufficiently sustained to trigger tension within the job market (wage increase) that will lead to an increase of entrenched inflation.

Across the Atlantic, it is the opposite. The FED benefits from sustainable upward price-dynamics in line with the growth of wages. Thus, it could raise its interest rates by 25bps while announcing three

11

consecutive increases next year. It also supported the idea that Trump’s recovery plan may be more inflationary if incorrectly set, possibly leading to a faster normalisation of its monetary policy than anticipated.

Finally, the Bank of Japan and the Bank of England have opted for a status quo in order to have a better visibility of their economy. If in Japan growth and inflation remain weak, the resilience of the British economy may not last long in a context of negotiations with the European Union which are to start in a few months. Comments on management on 2016

Remaining loyal to our flexible management of the fund, we greatly reduced the exposure of the fund at the beginning of the year, a decision motivated by the great stir caused by the change in the calculation method in MDA regulation. Thus, we cut in half our positioning in AT1 and substantially increased our source of liquidity, in order to protect the fund’s valuation at the strongest market low point. The uncertainties related to the Brexit led us to remain careful until June’s referendum, where we were positioned to capitalise on any shock on the valuations. As the shock did not last long, we limited our cash redeployment. Afterwards, we used the primary market to reinvest, but remained little active on the secondary market for technical reasons, as new issues seemed more attractive based on their elevated risk premia and low extension risk. Perspectives on 2017

We are ready to move into 2017 more invested than last year, as the market seems more favourable to subordinate bonds for many reasons. The regulatory environment seems more stable and pragmatic, more flexibility is given to banks on their distribution, the pressure on the markets seems to decrease (re-steepening of the curve of interests, less competition, volume of new loans increasing), and the asset quality continues to improve (stabilization or reduction of the doubtful loans stocks, a decrease in provisions). Although more invested, we keep our flexibility as the year will not be a smooth ride. The political risk is important in this election year (Holland, France, Germany, and possibly Italy if anticipated elections are planned), none of those countries seems to be safe from populist theses (increasing popularity of PVV in Holland, FN in France and Pediga in Germany), which can lead to bounces in the markets. Trump came to office at the beginning of the year in the United States, and the stock market euphoria since the election results can be reduced if his protectionist policy leads to geopolitical tensions, as the relations with China or Mexico are subject to great tensions. Lastly, the negotiation around the Brexit must begin in first trimester of 2017 with great uncertainties.

Two other risk factors must be monitored this year. The most important one concerns the shift in central banks strategy, the ECB in particular, which has recently announced its intention to reduce its asset purchase facility effective March 2017 (even though the program is extended to December 2017). If inflation is assessed earlier than anticipated, the markets may be surprised by a more aggressive reduction of the quantitative easing program. Lastly, certain banking sectors experience difficulties related to doubtful loans (in particular in Italy and Portugal). As the ECB, as the supervisor, fixed reducing the NPLs as its first objective, it is possible to assist to the resolution of the most risky banks, with an impact on the markets. AT1s loans remain for us the best couple benefits/risks for the sector at the moment. The risk on coupons decreases, valuations are still attractive, and the balance supply/demand is still in favour of the creditors. Tier 2 loans should experience less supply than expected, with the emergence of Tier 3 or “Non Preferred Senior”, however the risk premia are compressed. Lastly, on the segment of Tier 3, premiums are not generous enough to compensate investors from an important emission risk. Financial year’s performance:

Part C: 1.70%. Part A: 2.67%. Part E: 3.09%.

Part D: 0.54% (reinvested coupons).

12

Total asset as of 30/12/2016 is EUR 138 849 158.80 against EUR 163 856 799.63 as of 12/31/2015.

Shares Nbr of shares

31/12/2015

Nbr of shares

30/12/2016

Net asset 31/12/2015

Net asset 30/12/2016

A 442 194,8980 408 776,085 64 350 068,59 61 075 656,21

C 500 179,655 338 935,197 69 128 582,47 47 641 986,19

D 7 387,720 6 545,586 878 892,93 768 932,85

E 195 380,683 188 646,563 29 499 255,64 29 362 583,55

Past performance is not a reliable indicator of future results.

Main movements in the portfolio during the financial year:

Securities Movements ("Accounting currency")

Acquisitions Sales

AMUNDI CASH INSTITUTIONS SRI I

11 713 217.33

22 735 834.08

ELIS EXHOLDELIS ZCP 08-04-16

7 999 035.67

8 000 000.00

ELIS EXHOLDELIS ZCP 08-03-16

7 998 666.88

8 000 000.00

ABN AMRO 4.31%2016 TV PERP

7 033 531.76

7 500 000.00

VICAT ZCP 29-04-16

6 999 807.51

7 000 000.00

BRAK CAPI 7.125% 15-12-18

6 555 552.93

6 089 433.76

ELIS EXHOLDELIS ZCP 11-07-16

5 999 466.71

6 000 000.00

ELIS EXHOLDELIS ZCP 09-06-16

5 999 328.41

6 000 000.00

ELIS EXHOLDELIS ZCP 09-05-16

5 999 225.10

6 000 000.00

CASINO ZCP 06-04-16

5 399 785.51

5 400 000.00

Transparency of securities financing transactions and the re-using of financial instruments – (SFTR regulation) – in the accounting currency of the mutual fund (EUR)

During the financial year, the mutual fund have not been subject to transactions subject to SFTR regulation.

13

ESMA

• Information on Effective Portfolio Management Techniques

a) Exposure obtained through efficient portfolio management techniques and derivative

financial instruments

• Exposure obtained through efficient portfolio management techniques: 0.00

Loaned securities: 0.00

Borrowed securities: 0.00

Securities held under sell-back deals: 0.00

Securities sold under buy-back deals: 0.00

• Underlying exposures obtained through derivative financial instruments: 45 317 608.48

Forward currency transactions: 45 317 608.48

Futures: 0.00

Options: 0.00

Swaps: 0.00

b) Counterparty(s) in the techniques of efficient portfolio management and financial derivative instruments

Efficient portfolio management techniques Financial derivative instruments (*)

GOLDMAN SACHS INTERNATIONAL LTD

(*) Ex. contracts in regulated markets or similar.

14

c) Financial guarantees received by the UCITS to reduce the counterparty risk

Type of securities Value in accounting currency

Efficient portfolio management techniques

. Deposits

. Shares

. Bonds

. UCITS

. Cash (**)

Total

Financial derivative instruments

. Deposits

. Shares

. Bonds

. UCITS

. Cash (**)

Total

170 000.00

170 000.00

(**)The cash account also includes cash amounts resulting from repurchase transactions.

d) Operating income and operating expenses resulting of efficient portfolio management

techniques

Operating income and operating expenses Value in accounting currency

. Income (***)

. Other income

Total income

. Direct operating expenses

. Indirect operating expenses

. Other expenses

Total expenses

644.85

644.85

170.60

170.60

(***) Income resulting of loaned securities and securities held under sell-back deals

15

4. REGULATORY REQUIREMENTS

• DEONTOLOGY

Information relating to operations during the year and on the securities for which the

Management Company is informed that his group has a particular interest:

Net Asset Value in K EUR

Securities issued by the promoter group None Loans issued by the promoter group None UCITS issued by the promoter group None

• SELECTION AND EVALUATION OF MARKET INTERMEDIARIES The Brokers Committee Responsibilities of the Committee As part of the management of the relation with its market intermediaries and counterparties, Tikehau Investment Management equipped itself with a brokers Committee meeting, to be held as often as necessary, and at least once every year. The Broker Committee is responsible for:

Monitoring and updating the best selection policy;

Limiting or even terminating a relation with an intermediary or counterparty. Furthermore, the Committee takes note of newly developed relations since its last meeting. Decisions of the Committee are recorded on a synthesis document that will be archived for at least 5 years. Committee composition The Committee is formed with the following associates:

Directors of Tikehau Investment Management

Heads of management activities

Head of Middle Office

RCCI Anybody who is deemed necessary for the Committee to make a decision may be invited. In accordance with the applicable regulations, the execution policy defined by Tikehau Investment Management is aimed at obtaining the best possible results for its clients ("best execution" policy) considering the price, cost, speed, probability of execution and payment delivery, the nature of orders or any other consideration related to the execution. Tikehau Investment Management is not a market member and as such, does not by itself, execute the orders on the financial markets. It transmits them to authorized intermediaries for execution on the markets. Consequently, the management company has set up a policy of market intermediaries’ selection, called "best selection" policy. Tikehau Investment Management requests that its market intermediaries be categorized as professional clients in order for them to provide "the best execution" which the management company must in turn provide to its own clients.

16

New relationships Intermediaries’ selection criteria The main criteria taken for intermediaries and counterparties selection are:

Financial markets covered by the broker; o The offered price compared to the offered liquidity: o Fee percentage per transaction o Average size of orders to be placed, if required o Minimum fee per transaction, if required

Quality of research and broadcasted information;

Financial soundness of the structure;

Any other relevant criteria. The manager willing to work with a new counterparty will send to the Middle-Office (with copy to the RCCI) the "Request for new relationship with Counterparty / Broker form", filled with his part of the information. • REPORT ON INTERMEDIARY FEES When the order execution and investment decision support services and the intermediary fees for the prior financial year exceeded EUR 500,000, the Management Company draws up a document entitled “Report on intermediation fees”, updated each year. This document is available on the website of Tikehau Investment Management: www.tikehauim.com • VOTING POLICY The voting policy of the Management Company for all UCI it manages is available in the head office of the Management Company in accordance with Articles 314-100 to 314-102 of the “Règlement Général de l’Autorité des Marchés Financiers”. • ENVIRONMENTAL, SOCIAL AND GOVERNANCE QUALITY CRITERIA Pursuant to the provisions of Article L. 533-22-1 of the French Monetary and Financial Code, information regarding the procedures for including social, environmental and governance quality criteria is provided on the Tikehau Investment Management website at: www.tikehauim.com • RISK MEASUREMENT AND CALCULATION OF GLOBAL EXPOSURE AND COUNTERPARTY RISK The Management Company uses the commitment approach for the calculation of the Global Exposure of the UCI.

• OTHER INFORMATIONS The Fund’s regulations and the latest annual and periodic reports can be sent upon written request to: TIKEHAU INVESTMENT MANAGEMENT 32 rue de Monceau, 75008 PARIS, France E-mail: [email protected]

17

5. INDEPENDENT AUDITOR’S CERTIFICATION

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

BALANCE SHEET - ASSET ON 12/30/16 IN EUR

Fixed Assets, net 0.00 0.00

12/30/16 12/31/15

Deposits 0.00 0.00

Financial instruments 136,154,429.49 152,559,484.87

Equities and similar securities 0.00 0.00

Traded in a regulated market or equivalent 0.00 0.00

Not traded in a regulated market or equivalent 0.00 0.00

Bonds and similar securities 121,324,180.29 141,535,338.96

Traded in a regulated market or equivalent 121,324,180.29 141,535,338.96

Not traded in a regulated market or equivalent 0.00 0.00

Credit instruments 5,999,772.83 0.00

Traded in a regulated market or equivalent 5,999,772.83 0.00

Negotiable credit instruments (Notes) 5,999,772.83 0.00

Other credit instruments 0.00 0.00

Not traded in a regulated market or equivalent 0.00 0.00

Collective investment undertakings 8,830,476.37 11,024,145.91

General-purpose UCITS and alternative investment funds intended fornon-professionals and equivalents in other countries

8,830,476.37 11,024,145.91

Other Funds intended for non-professionals and equivalents in other EUMember States

0.00 0.00

General-purpose professional funds and equivalents in other EU MemberStates and listed securitisation entities

0.00 0.00

Other professional investment funds and equivalents in other EU MemberStates and listed securitisation agencies

0.00 0.00

Other non-European entities 0.00 0.00

Temporary transactions in securities 0.00 0.00

Credits for securities held under sell-back deals 0.00 0.00

Credits for loaned securities 0.00 0.00

Borrowed securities 0.00 0.00

Securities sold under buy-back deals 0.00 0.00

Other temporary transactions 0.00 0.00

Hedges 0.00 0.00

Hedges in a regulated market or equivalent 0.00 0.00

Other hedges 0.00 0.00

Other financial instruments 0.00 0.00

Receivables 45,438,847.91 52,488,065.89

Forward currency transactions 45,317,608.48 52,410,581.79

Other 121,239.43 77,484.10

Financial accounts 2,532,817.94 11,507,568.73

Cash and cash equivalents 2,532,817.94 11,507,568.73

Total assets 184,126,095.34 216,555,119.49

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

BALANCE SHEET - LIABILITIES ON 12/30/16 IN EUR

Shareholders' funds

12/30/16 12/31/15

Capital 160,521,643.17139,155,844.02

Allocation Report of distributed items (a) 0.000.00

Brought forward (a) 21.4340.89

Allocation Report of distributed items on Net Income (a,b) -2,210,763.44-5,712,010.22

Result (a,b) 5,545,898.475,405,284.11

Total net shareholders' funds (net assets) 163,856,799.63138,849,158.80

Financial instruments 0.000.00

Transfers of financial instruments 0.000.00

Temporary transactions in securities 0.000.00

Sums owed for securities sold under buy-back deals 0.000.00

Sums owed for borrowed securities 0.000.00

Other temporary transactions 0.000.00

Hedges 0.000.00

Hedges in a regulated market or equivalent 0.000.00

Other hedges 0.000.00

Payables 52,698,319.8645,276,936.54

Forward currency transactions 52,252,367.0844,905,625.72

Other 445,952.78371,310.82

Financial accounts 0.000.00

Short-term credit 0.000.00

Loans received 0.000.00

Total liabilities 216,555,119.49184,126,095.34

(a) Including adjusment(b) Decreased interim distribution paid during the business year

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

OFF-BALANCE SHEET ON 12/30/16 IN EUR

12/30/16 12/31/15

Hedges

Contracts in regulated markets or similar

OTC contracts

Other commitments

Other operations

Contracts in regulated markets or similar

OTC contracts

Other commitments

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

INCOME STATEMENT ON 12/30/16 IN EUR

12/30/16

Revenues from financial operations

12/31/15

689.38Revenues from deposits and financial accounts 0.00

0.00Revenues from equities and similar securities 0.00

7,105,811.52Revenues from bonds and similar securities 4,617,937.81

13,627.86Revenues from credit instruments 0.00

644.85Revenues from temporary acquisition and disposal of securities 0.00

0.00Revenues from hedges 0.00

0.00Other financial revenues 1,722.61

7,120,773.61Total (1) 4,619,660.42

Charges on financial operations

170.60Charges on temporary acquisition and disposal of securities 0.00

0.00Charges on hedges 0.00

2,513.70Charges on financial debts 888.74

0.00Other financial charges 0.00

2,684.30Total (2) 888.74

7,118,089.31Net income from financial operations (1 - 2) 4,618,771.68

0.00Other income (3) 0.00

1,290,823.54Management fees and depreciation provisions (4) 825,186.26

5,827,265.77Net income of the business year (L.214-17-1) (1-2+3-4) 3,793,585.42

-421,981.66Revenue adjustment (5) 1,752,313.05

0.00Interim Distribution on Net Income paid during the business year (6) 0.00

5,405,284.11Net profit (1 - 2 + 3 - 4 + 5 + 6) 5,545,898.47

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

NOTES TO THE ANNUAL ACCOUNTS

ACCOUNTING RULES AND METHODS The annual accounts are presented as provided by the ANC Regulation 2014-01 repealing Regulation CRC 2003-02 as amended.

General accounting principles apply, viz: - fair picture, comparability, ongoing business, - proper practice & trustworthiness, - prudence, - no unreported change in methods from one period to the next. Revenues from fixed-yield securities are recognized on the basis of interest actually received. Acquisitions and disposals of securities are recognized exclusiveof costs. The accounting currency of the portfolio is the EURO. The accounting period reported on is 12 months.

Asset valuation rules: Financial instruments are initially recognized at historic cost and carried on the Balance Sheet at their current value: this is their latest known market value or, in the absence of a market, is determined by any external means or by recourse to financial models. Differences between the securities’ current values determined as above and their original historic cost are recognized in the accounts as “differences on estimation”. Securities denominated in a currency other than that of the portfolio are valued in accordance with the above principle and then converted into the currency of the portfolio at the exchange rate obtained on the valuation date. Deposit: Deposits maturing in three months or sooner are valued according to the linear method. Equities, bonds and other securities traded in a regulated market or equivalent: When calculating the NAV, the equities and other securities traded in a regulated market or equivalent are valued based on the day’s closing market price. Bonds and similar securities are valued at the closing price notified by various financial service providers. Interest accrued on bonds and similar securities is calculated up to the date of asset valuation. Equities, bonds and other securities not traded in a regulated market or equivalent: Securities not traded in a regulated market are valued by the Fund Manager using methods based on net equity and yield, taking into account the prices retained in significant recent transactions.. Negotiable credit instruments (Notes): Negotiable credit instruments which are not actively traded in significant amounts are actuarially valued on the basis of a reference rate as specified below, plus any enhancement to represent the issuer’s intrinsic characteristics: Notes maturing in one year’s time or less: euro interbank offered rate (Euribor); Notes maturing in more than one year’s time: the prevailing rate on medium-term interest-bearing Treasury notes (BTAN) or, for the longest Notes, on near-term fungible Treasury bonds (OAT); Negotiable credit instruments maturing in three months or sooner may be valued according to the linear method. French Treasury notes are valued using the market rate published daily by the Banque de France. UCITS held: UCITS units or shares are valued at the latest known NAV. Temporary transactions in securities:

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

Securities held under sell-back deals are carried in Assets under “credits for securities held under sell-back deals” at the amount provided for in the contract, plus accrued interest receivable. Securities sold under buy-back deals are booked to the buying portfolio at their current value. The corresponding debt is booked to the selling portfolio at the value set in the contract plus accrued interest payable. Loaned securities are valued at their current value and carried in Assets under “credits for loaned securities” at their current value plus accrued interest receivable. Borrowed securities are carried in Assets under “borrowed securities” at the amount provided for in the contract, and in Liabilities under “debts for borrowed securities” at the amount provided for in the contract plus accrued interest payable. Hedges: Hedges traded in a regulated market or equivalent: Hedge instruments traded in regulated markets are valued at the day’s settlement price. Hedges not trades in a regulated market or equivalent: Swaps: Rate swaps and/or forward currency transactions are valued at their market value according to the price calculated by discounting future interest streams at market interest (and/or exchange) rates. This price is adjusted for default risk. Index swaps are valued actuarially on the basis of a reference rate provided by the counterparty. Other swaps are valued at their market value or are estimated as specified by the Fund Manager. Off-Balance Sheet Commitments: Firm hedging contracts are stated among “Off-Balance Sheet Commitments” at their market value at the rate used in the portfolio. Conditional hedges are converted into their underlying equivalents. Swap commitments are stated at their nominal value or at an equivalent amount, where there is no nominal value. Management fees: Management fees are calculated on the nominal capital on each valuation. These fees are imputed to the fund’s Income Statement. Management fees are paid in full to the Fund Manager, which bears all the fund’s operating costs. The management fees do not include dealing costs. The percentage of nominal capital charged is … % including taxes. Allocation of net profit: The net profit (loss) for the period is the total of interest, arrears, premiums, allotments and dividends, plus income on ready cash, minus management fees and financial dealing costs. Latent or realised capital gains or losses are not counted as revenue; nor are subscription/redemption fees. The amounts available for distribution are the net profit for the period, plus any sums brought forward, plus or minus the balance of any revenue adjustment accounts relating to the financial period in question. Gains and losses: The net realised gains (deducted from management fees and realised losses) from the financial year will increase the same type of net realized gains from earlier financial years, if the fund hasn’t distributed or accumulated its gains and will also increase or reduce the equalization accounts for realised gains. Appropriation methods for the distributable amounts:

Distributable amounts Unit: Allocation of the net income Accumulation and/ or distribution and / or carry forward a

decision taken by the management

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

Allocation of the net realized gains and losses Accumulation and/ or distribution and / or carry forward a decision taken by the management

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

CHANGES IN NET ASSETS 12/30/16 IN EUR

12/30/16

163,856,799.63Net assets in start of period 42,240,233.28

12/31/15

27,371,547.57Subscriptions (including subscription fees received by the fund) 155,688,922.55

-55,488,646.10Redemptions (net of redemption fees received by the fund) -34,460,231.19

1,532,571.80Capital gains realised on deposits and financial instruments 770,460.38

-6,210,173.30Capital losses realised on deposits and financial instruments -619,788.91

4,725,947.11Capital gains realised on hedges 2,323,123.00

-5,048,564.57Capital losses realised on hedges -4,600,014.11

-71,271.71Dealing costs -57,872.41

-1,099,289.76Exchange gains/losses 1,367,989.21

3,478,759.11Changes in difference on estimation (deposits and financial instruments) -2,564,739.74

2,042,041.77Difference on estimation, period N -1,436,717.34

1,436,717.34Difference on estimation, period N-1 -1,128,022.40

0.00Changes in difference on estimation (hedges) 0.00

0.00Difference on estimation, period N 0.00

0.00Difference on estimation, period N-1 0.00

0.00Net Capital gains and losses Accumulated from Previous business year 0.00

-25,786.75Distribution on Net Capital Gains and Losses from previous business year -24,867.85

5,827,265.77Net profit for the period, before adjustment prepayments 3,793,585.42

0.00Allocation Report of distributed items on Net Income 0.00

0.00Interim Distribution on Net Income paid during the business year 0.00

0.00Other items 0.00

138,849,158.80Net assets in end of period 163,856,799.63

2.

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

FURTHER DETAILS3.

BREAKDOWN OF FINANCIAL INSTRUMENTS BY LEGAL ORCOMMERCIAL TYPE

3.1.

Amount %

Assets

Bonds and similar securities

Convertible bonds traded on a regulated or similar market 334,225.83 0.24

Fixed-rate bonds traded on a regulated or similar market 117,695,056.03 84.76

Floating-rate bonds traded on regulated markets 3,294,898.43 2.37

Total bonds and similar securities 121,324,180.29 87.38

Credit instruments

Commercial Paper 5,999,772.83 4.32

Total credit instruments 5,999,772.83 4.32

Liabilities

Transactions involving transfer of financial instruments

Total transactions involving transfer of financial instruments 0.00 0.00

Off-balance sheet

Hedges

Total hedges 0.00 0.00

Other operations

Total other operations 0.00 0.00

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

BREAKDOWN OF ASSET, LIABILITY AND OFF-BALANCE SHEETITEMS, BY TYPE

3.2.

Fixed rate % Variable rate % Rate subject toreview % Other %

Assets

Deposits 0.00 0.00 0.000.00 0.00 0.00 0.000.00

Bonds and similar securities 0.00 3,629,124.26 0.0084.76 0.00 2.61 0.00117,695,056.03

Credit instruments 0.00 0.00 0.004.32 0.00 0.00 0.005,999,772.83

Temporary transactions in securities 0.00 0.00 0.000.00 0.00 0.00 0.000.00

Financial accounts 0.00 0.00 2,532,817.940.00 0.00 0.00 1.820.00

Liabilities

Temporary transactions in securities 0.00 0.00 0.000.00 0.00 0.00 0.000.00

Financial accounts 0.00 0.00 0.000.00 0.00 0.00 0.000.00

Off-balance sheet

Hedges 0.00 0.00 0.000.00 0.00 0.00 0.000.00

Other operations 0.00 0.00 0.000.00 0.00 0.00 0.000.00

BREAKDOWN OF ASSET, LIABILITY AND OFF-BALANCE SHEETITEMS, BY TIME TO MATURITY

3.3.

< 3 Months % ]3 Months - 1Year] % ]1 - 3 Years] % ]3 - 5 Years] % > 5 Years %

AssetsDeposits 0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00

Bonds and similar securities 0.00 0.00 0.00 7,640,974.22 113,683,206.070.00 0.00 0.00 5.50 81.88

Credit instruments 5,999,772.83 0.00 0.00 0.00 0.004.32 0.00 0.00 0.00 0.00Temporary transactions insecurities

0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00

Financial accounts 2,532,817.94 0.00 0.00 0.00 0.001.82 0.00 0.00 0.00 0.00

LiabilitiesTemporary transactions insecurities

0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00

Financial accounts 0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00

Off-balance sheetHedges 0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00

Other operations 0.00 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00 0.00

All hedges are shown in terms of time to maturity of the underlying securities.

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

BREAKDOWN OF ASSET, LIABILITY AND OFF-BALANCE SHEETITEMS, BY LISTING OR VALUATION CURRENCY

3.4.

USD

%

GBP

% %

Other currencies

%Amount Amount Amount Amount

Assets

Deposits 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00

Equities and similar securities 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00

Bonds and similar securities 37,717,640.36 7,413,296.19 0.00 0.0027.16 5.34 0.00 0.00

Credit instruments 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00

Mutual fund units 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00

Temporary transactions in securities 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00

Liabilities 20,443.23 0.00 0.00 0.000.01 0.00 0.00 0.00

Financial accounts 94,067.31 112,957.86 0.00 0.000.07 0.08 0.00 0.00

Liabilities

Transactions involving transfer of financial instruments 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00

Temporary transactions in securities 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00

Debts 37,500,611.66 7,405,014.06 0.00 0.0027.01 5.33 0.00 0.00

Financial accounts 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00

Off-balance sheet

Hedges 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00

Other operations 0.00 0.00 0.00 0.000.00 0.00 0.00 0.00

RECEIVABLES AND PAYABLES: BREAKDOWN BY TYPE3.5.

Funds to be accepted on urgent sale of currencies 45,317,608.48

12/30/16

Receivables

Coupons and dividends in cash 121,239.43Total receivables 45,438,847.91

Urgent sale of currency 44,905,625.72Payables

Redemptions to be paid 18,827.86Management fees 89,822.94Variable management fees 92,660.02Collateral 170,000.00

Total of Payables 45,276,936.54

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

SHAREHOLDERS’ FUNDS3.6.

Number of units issued or redeemed3.6.1.

Units subscribed during the period 25,026.696 3,355,040.95

Net Subscriptions / Redemptions -161,244.458 -21,833,699.49

Tikehau Subordonnées Financières C

Units redeemed during the period -186,271.154 -25,188,740.44

Units subscribed during the period 144,271.485 20,617,456.89

Net Subscriptions / Redemptions -33,418.805 -5,128,105.77

Tikehau Subordonnées Financières A

Units redeemed during the period -177,690.290 -25,745,562.66

Units subscribed during the period 22,212.000 3,380,644.90

Net Subscriptions / Redemptions -6,734.120 -1,057,958.10

Tikehau Subordonnées Financières E

Units redeemed during the period -28,946.120 -4,438,603.00

Units subscribed during the period 157.866 18,404.83

Net Subscriptions / Redemptions -842.134 -97,335.17

Tikehau Subordonnées Financières D

Units redeemed during the period -1,000.000 -115,740.00

Units Value

Subscription and/or redemption fees3.6.2.

Total of subscription fees received 0.00Total of redemption fees received 0.00

Tikehau Subordonnées Financières C

Total of subscription and/or redemption fees received 0.00

Total of subscription fees received 0.00Total of redemption fees received 0.00

Tikehau Subordonnées Financières A

Total of subscription and/or redemption fees received 0.00

Total of subscription fees received 0.00Total of redemption fees received 0.00

Tikehau Subordonnées Financières E

Total of subscription and/or redemption fees received 0.00

Total of subscription fees received 0.00Total of redemption fees received 0.00

Tikehau Subordonnées Financières D

Total of subscription and/or redemption fees received 0.00

Value

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

MANAGEMENT FEES3.7.

12/30/16

Tikehau Subordonnées Financières C

1.50Percentage of management charges812,280.10Fixed management fees

27,090.37Variable management fees0.00Trailer fees

0.00Underwriting commission

Tikehau Subordonnées Financières A

0.50Percentage of management charges315,506.62Fixed management fees

65,583.04Variable management fees0.00Trailer fees

0.00Underwriting commission

Tikehau Subordonnées Financières E

0.20Percentage of management charges57,902.28Fixed management fees

0.00Variable management fees0.00Trailer fees

0.00Underwriting commission

Tikehau Subordonnées Financières D

1.50Percentage of management charges12,461.13Fixed management fees

0.00Variable management fees0.00Trailer fees

0.00Underwriting commission

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

3.8. COMMITMENTS RECEIVED AND GIVEN

3.8.1. Guarantees received by the fund :

None

3.8.2. Other commitments received and/or given :

None

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

FURTHER DETAILS3.9.

Stock market values of temporarily acquired securities3.9.1.

Securities held under sell-back deals 0.00Borrowed securities 0.00

12/30/16

Stock market values of pledged securities3.9.2.

Financial instruments pledged but not reclassified 0.00Financial instruments received as pledges but not recognized in the Balance Sheet 0.00

12/30/16

Group financial instruments held by the Fund3.9.3.

12/30/16Name of securityIsin code

Equities 0.00

Bonds 0.00

Notes 0.00

UCITS 0.00

Hedges 0.00

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

3.10.TABLE OF ALLOCATION OF THE DISTRIBUTABLE

Table of allocation of the distributable share of the sums concerned to profit(loss)

Distribution 0.00 0.00

Brought forward 0.00 0.00

Allocation

Capitalized 1,536,473.36 1,908,592.76

Total 1,536,473.36 1,908,592.76

12/30/16 12/31/15

Sums not yet allocated

Brought forward 40.89 21.43

Profit (loss) 5,405,284.11 5,545,898.47

Total 5,405,325.00 5,545,919.90

12/30/16 12/31/15

C1 Tikehau Subordonnées Financières C

Distribution 0.00 0.00

Brought forward 0.00 0.00

Allocation

Capitalized 2,518,978.98 2,377,574.27

Total 2,518,978.98 2,377,574.27

12/30/16 12/31/15

C2 Tikehau Subordonnées Financières A

Distribution 0.00 0.00

Brought forward 0.00 0.00

Allocation

Capitalized 1,324,443.38 1,234,219.03

Total 1,324,443.38 1,234,219.03

12/30/16 12/31/15

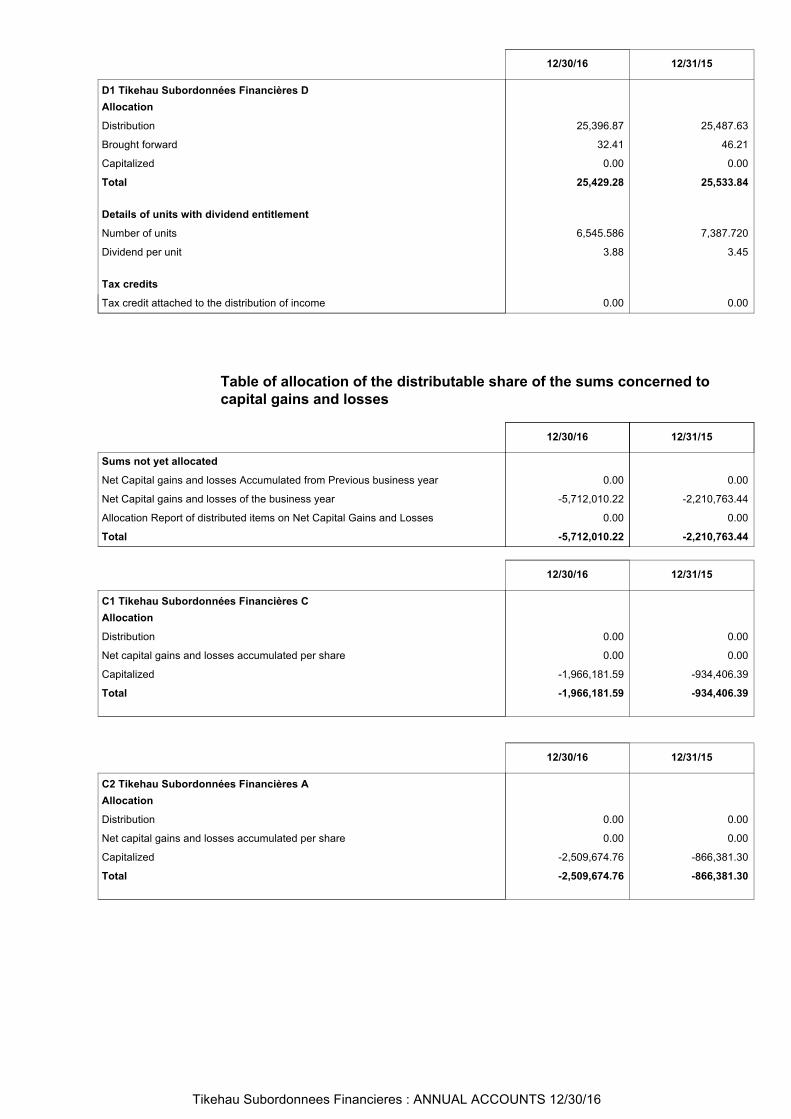

C3 Tikehau Subordonnées Financières E

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

Distribution 25,396.87 25,487.63

Brought forward 32.41 46.21

Allocation

Capitalized 0.00 0.00

Total 25,429.28 25,533.84

Details of units with dividend entitlement

Number of units 6,545.586 7,387.720

Dividend per unit 3.88 3.45

Tax credits

0.00 0.00Tax credit attached to the distribution of income

12/30/16 12/31/15

D1 Tikehau Subordonnées Financières D

Distribution 0.00 0.00

Allocation

Capitalized -1,966,181.59 -934,406.39

Total -1,966,181.59 -934,406.39

12/30/16 12/31/15

Sums not yet allocated

Net Capital gains and losses Accumulated from Previous business year 0.00 0.00

Total -5,712,010.22 -2,210,763.44

Net Capital gains and losses of the business year -5,712,010.22 -2,210,763.44

Allocation Report of distributed items on Net Capital Gains and Losses 0.00 0.00

12/30/16 12/31/15

C1 Tikehau Subordonnées Financières C

Net capital gains and losses accumulated per share 0.00 0.00

Table of allocation of the distributable share of the sums concerned tocapital gains and losses

Distribution 0.00 0.00

Allocation

Capitalized -2,509,674.76 -866,381.30

Total -2,509,674.76 -866,381.30

12/30/16 12/31/15

C2 Tikehau Subordonnées Financières A

Net capital gains and losses accumulated per share 0.00 0.00

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

Distribution 0.00 0.00

Allocation

Capitalized -1,204,122.97 -397,718.79

Total -1,204,122.97 -397,718.79

12/30/16 12/31/15

C3 Tikehau Subordonnées Financières E

Net capital gains and losses accumulated per share 0.00 0.00

Distribution 0.00 0.00

Allocation

Capitalized -32,030.90 -12,256.96

Total -32,030.90 -12,256.96

12/30/16 12/31/15

D1 Tikehau Subordonnées Financières D

Net capital gains and losses accumulated per share 0.00 0.00

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

TABLE OF PROFIT (LOSS) AND OTHER TYPICAL FEATURES OF THEFUND OVER THE PAST FIVE FINANCIAL PERIODS

3.11.

Tikehau Subordonnées Financières C

Net assets in EUR

Number of shares/units

NAV per share/unit in EUR in EUR

7,002,965.70

61,473.635

113.91

4.25

Net Capital Gains and Losses Accumulatedper share in EUR 0.00

Net income Accumulated per share in EUR

12,624,712.91

98,112.999

128.67

3.60

1.90

20,967,209.79

154,522.800

135.69

3.97

4.00

69,128,582.47

500,179.655

138.20

3.81

-1.86

47,641,986.19

338,935.197

140.56

4.53

-5.80

Tikehau Subordonnées Financières A

Net assets in EUR

Number of shares/units

NAV per share/unit in EUR in EUR

4,591,864.57

39,374.000

116.62

5.86

Net Capital Gains and Losses Accumulatedper share in EUR 0.00

Net income Accumulated per share in EUR

4,406,403.19

33,135.000

132.98

4.88

1.96

18,754,922.63

132,512.487

141.53

5.41

4.14

64,350,068.59

442,194.890

145.52

5.37

-1.95

61,075,656.21

408,776.085

149.41

6.16

-6.13

Tikehau Subordonnées Financières E

Net assets in EUR

Number of shares/units

NAV per share/unit in EUR in EUR

885,613.23

7,499.000

118.09

6.72

Net Capital Gains and Losses Accumulatedper share in EUR 0.00

Net income Accumulated per share in EUR

997,584.66

7,300.000

136.65

6.85

2.02

1,684,897.70

11,531.000

146.11

6.24

4.27

29,499,255.64

195,380.683

150.98

6.31

-2.03

29,362,583.55

188,646.563

155.64

7.02

-6.38

Tikehau Subordonnées Financières D

Net assets in EUR

Number of shares/units

NAV per share/unit in EUR in EUR

in EURTax credits per share/unit

775,824.00

7,000.000

107.97

4.68

0,35

Net Capital Gains and Losses Accumulatedper share in EUR 0.00

Unit brought forward in EUR on the result 0.00

Distribution on Net Income per share inEUR

670,901.14

5,733.676

117.01

3.31

0,00

1.73

0.00

833,203.16

6,938.296

120.08

3.54

0,00

3.65

0.00

878,892.93

7,387.720

118.96

3.45

0,00

-1.65

0.00

768,932.85

6,545.586

117.47

3.88

*

-4.89

0.00

12/31/12

Global Net Assets in EUR 13,237,333.04

12/31/13

18,699,601.95

12/31/14

42,240,233.28

12/31/15

163,856,799.63

12/30/16

138,849,158.80

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

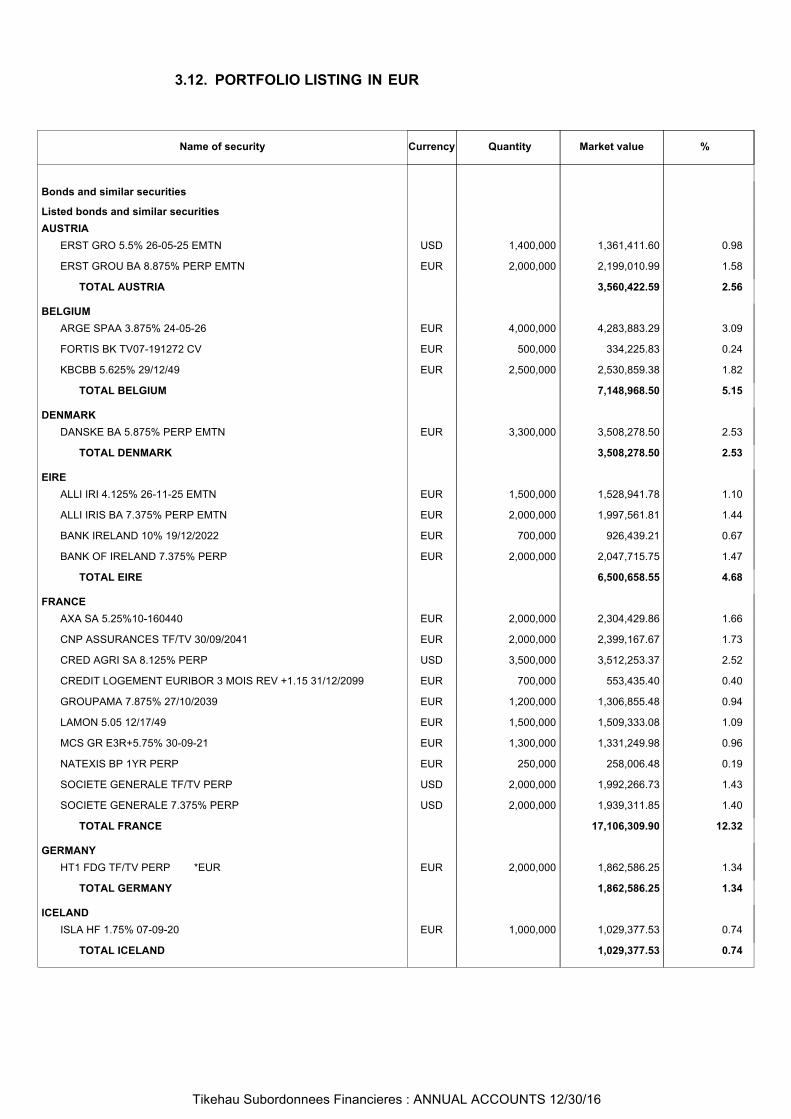

Bonds and similar securities

Listed bonds and similar securitiesAUSTRIA

ERST GRO 5.5% 26-05-25 EMTN USD 1,400,000 1,361,411.60 0.98

Currency Quantity Market value %Name of security

ERST GROU BA 8.875% PERP EMTN EUR 2,000,000 2,199,010.99 1.58

TOTAL AUSTRIA 3,560,422.59 2.56

BELGIUMARGE SPAA 3.875% 24-05-26 EUR 4,000,000 4,283,883.29 3.09

FORTIS BK TV07-191272 CV EUR 500,000 334,225.83 0.24

KBCBB 5.625% 29/12/49 EUR 2,500,000 2,530,859.38 1.82

TOTAL BELGIUM 7,148,968.50 5.15

DENMARKDANSKE BA 5.875% PERP EMTN EUR 3,300,000 3,508,278.50 2.53

TOTAL DENMARK 3,508,278.50 2.53

EIREALLI IRI 4.125% 26-11-25 EMTN EUR 1,500,000 1,528,941.78 1.10

ALLI IRIS BA 7.375% PERP EMTN EUR 2,000,000 1,997,561.81 1.44

BANK IRELAND 10% 19/12/2022 EUR 700,000 926,439.21 0.67

BANK OF IRELAND 7.375% PERP EUR 2,000,000 2,047,715.75 1.47

TOTAL EIRE 6,500,658.55 4.68

FRANCEAXA SA 5.25%10-160440 EUR 2,000,000 2,304,429.86 1.66

CNP ASSURANCES TF/TV 30/09/2041 EUR 2,000,000 2,399,167.67 1.73

CRED AGRI SA 8.125% PERP USD 3,500,000 3,512,253.37 2.52

CREDIT LOGEMENT EURIBOR 3 MOIS REV +1.15 31/12/2099 EUR 700,000 553,435.40 0.40

GROUPAMA 7.875% 27/10/2039 EUR 1,200,000 1,306,855.48 0.94

LAMON 5.05 12/17/49 EUR 1,500,000 1,509,333.08 1.09

MCS GR E3R+5.75% 30-09-21 EUR 1,300,000 1,331,249.98 0.96

NATEXIS BP 1YR PERP EUR 250,000 258,006.48 0.19

SOCIETE GENERALE TF/TV PERP USD 2,000,000 1,992,266.73 1.43

SOCIETE GENERALE 7.375% PERP USD 2,000,000 1,939,311.85 1.40

TOTAL FRANCE 17,106,309.90 12.32

GERMANYHT1 FDG TF/TV PERP *EUR EUR 2,000,000 1,862,586.25 1.34

TOTAL GERMANY 1,862,586.25 1.34

ICELANDISLA HF 1.75% 07-09-20 EUR 1,000,000 1,029,377.53 0.74

TOTAL ICELAND 1,029,377.53 0.74

PORTFOLIO LISTING IN EUR3.12.

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

ILIAC TRACTS CAIMANESMIZZEN BONDCO LTD 7.0% 01/05/2021 GBP 1,800,000 2,133,357.13 1.54

TOTAL ILIAC TRACTS CAIMANES 2,133,357.13 1.54

Currency Quantity Market value %Name of security

ITALYASSICURAZIONI GENERALI 7.75% 12/42 EUR 2,000,000 2,395,912.47 1.73

INTESA SAN TF/TV 20/06/2018 EUR 1,000,000 1,107,181.75 0.80

INTESA SANPAOLO 8.375% 09-PERP EUR 1,000,000 1,141,710.62 0.82

TOTAL ITALY 4,644,804.84 3.35

LUXEMBURGGARF HOLD 3 S 7.5% 01-08-22 EUR 2,000,000 2,167,083.33 1.56

TOTAL LUXEMBURG 2,167,083.33 1.56

NETHERLANDSABN AMRO BANK NV 5.75% PERP EUR 3,000,000 3,112,831.49 2.24

ACHMEA BV TF/TV 04/04/2043 EUR 2,000,000 2,268,782.19 1.63

ALLIANZ FINANCE BV 4.375%05-PERP. EUR 2,000,000 2,082,341.80 1.50

ATRA FINA BV 5.25% 23-09-44 EUR 2,300,000 2,168,431.34 1.56

ELM BV TF/TV PERP *EUR EUR 2,000,000 2,104,601.18 1.52

ING GROEP NV 6.875% PERP USD 3,000,000 2,880,301.02 2.07

RABO NEDE 6.625% PERP EUR 2,000,000 2,147,390.05 1.55

SNS BA 3.75% 05-11-25 EMTN EUR 3,550,000 3,744,581.34 2.70

STICH AK RABOBK 6,5%13-PERP. EUR 750,000 856,662.92 0.62

TOTAL NETHERLANDS 21,365,923.33 15.39

NORWAYDNB NOR BANK ASA 5.75% PERP USD 2,000,000 1,982,001.53 1.43

DNB NOR BANK ASA 6.5% PERP USD 400,000 392,599.83 0.28

TOTAL NORWAY 2,374,601.36 1.71

SPAINBANC BILB VIZC AR 8.875% PERP EUR 1,600,000 1,759,255.43 1.27

BANC DE 5.625% 06-05-26 EMTN EUR 1,000,000 1,113,281.25 0.80

BANCO BILBAO VIZCAYA ARGENTARIA SA 9% 29/05/2049 USD 1,400,000 1,404,977.48 1.01

BANKIA S.A. 4.0% 22/05/2024 EUR 2,000,000 2,084,534.25 1.51

BANKINTERSA 8.625% PERP EUR 1,000,000 1,107,656.25 0.80

BCO POP ESP 11.50% 12/49 EUR 2,000,000 2,073,027.78 1.49

IBERCAJA 5.0% 28-07-25 EUR 2,000,000 1,989,811.64 1.43

TOTAL SPAIN 11,532,544.08 8.31

STOCKING STITCHMERCURY BONDCO 8.25% 30-05-21 EUR 2,000,000 2,127,625.00 1.53

TOTAL STOCKING STITCH 2,127,625.00 1.53

SWEDENNORD BANK AB PUBL 5.5% PERP USD 1,500,000 1,438,223.11 1.04

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

NORD BANK AB 5.25% PERP EMTN USD 1,000,000 927,932.37 0.67

Currency Quantity Market value %Name of security

SEB 5 3/4 11/29/49 USD 3,180,000 3,041,090.33 2.18

SVEN HAND AB 5.25% PERP USD 1,500,000 1,468,992.65 1.06

SWEDBANK AB 6.0% PERP USD 1,800,000 1,723,056.65 1.24

TOTAL SWEDEN 8,599,295.11 6.19

SWITZERLANDAQUAIRUS + INV 6.375% 09/24 USD 1,500,000 1,525,099.55 1.10

CS 7 1/2 12/11/49 USD 2,000,000 1,998,015.33 1.44

UBS GROUP AG 5.75% PERP EUR 500,000 552,870.56 0.40

UBS GROUP AG 6.875% PERP USD 1,000,000 1,018,207.32 0.73

UBS GROUP AG 7.125% PERP USD 2,250,000 2,267,374.97 1.63

TOTAL SWITZERLAND 7,361,567.73 5.30

UNITED KINGDOMCOVE BUIL SOC 6.375% 31-12-99 GBP 1,000,000 1,147,896.68 0.83

HSBC HOLDINGS PLC 6.875% PERP USD 1,500,000 1,507,540.30 1.09

LBG CAPITAL 6.375%09-120520 EUR 1,000,000 1,019,364.58 0.73

LLOY BANK GROU PL 7.5% PERP USD 1,500,000 1,457,428.77 1.05

NWIDE 6.875% 29/12/2049 GBP 2,000,000 2,357,999.60 1.69

PRUDEN 4.375% PERP EMTN USD 2,000,000 1,757,016.41 1.27

RBS GROUP TF/TV PERP *EUR EUR 700,000 657,795.31 0.47

ROYA BK SCOT GROU TF/TV PERP USD 1,000,000 970,332.62 0.70

ROYAL BK SCOTLAND 5,5% PERP EUR 1,500,000 1,435,062.50 1.03

SANTANDER UK PLC 7.375% PERP GBP 1,500,000 1,774,042.78 1.28

STANDARD CHARTERED PLC L3RUSD+1.51% PERP USD 1,500,000 1,152,206.57 0.83

TOTAL UNITED KINGDOM 15,236,686.12 10.97

USAHYPO REAL INTL TRUST I TF/TV PERP EUR 3,000,000 3,064,090.44 2.21

Total listed bond and similar securities 121,324,180.29 87.38

Total bonds and similar securities 121,324,180.29 87.38

TOTAL USA 3,064,090.44 2.21

Credit instruments

Credit instruments traded in a regulated market or equivalentFRANCE

LISI ZCP 12-01-17 EUR 2,000,000 1,999,978.33 1.44

SFR GROUP ZCP 09-01-17 EUR 2,000,000 1,999,811.17 1.44

STEF ZCP 09-01-17 EUR 2,000,000 1,999,983.33 1.44

Total credit instruments traded on a regulated or similar market 5,999,772.83 4.32

Total credit instruments 5,999,772.83 4.32

TOTAL FRANCE 5,999,772.83 4.32

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

Collective investment undertakingsGeneral-purpose UCITS and alternative investment funds intended fornon-professionals and equivalents in other countriesFRANCE

AMUNDI CASH CORPORATE IC EUR 24.51 5,760,737.36 4.15

Currency Quantity Market value %Name of security

NATIXIS TRESORERIE PLUS Part IC EUR 1.332 138,543.53 0.10

SLF FRANCE MONEY MARKET EURO 3D EUR 116.74 2,931,195.48 2.11

TOTAL General-purpose UCITS and alternative investment fundsintended for non-professionals and equivalents in othercountries

8,830,476.37 6.36

Total collective investment undertakings 8,830,476.37 6.36

TOTAL FRANCE 8,830,476.37 6.36

Receivables 45,438,847.91 32.73

Debts -45,276,936.54 -32.61

Financial accounts 2,532,817.94 1.82

Net assets 138,849,158.80 100.00

Tikehau Subordonnées Financières C 338,935.197 140.56EURTikehau Subordonnées Financières A 408,776.085 149.41EURTikehau Subordonnées Financières E 188,646.563 155.64EURTikehau Subordonnées Financières D 6,545.586 117.47EUR

Tikehau Subordonnees Financieres : ANNUAL ACCOUNTS 12/30/16

ADDITIONAL INFORMATION CONCERNING THE FISCAL REGIME OF THE COUPON

UNIT NET INCOME CURRENCYCURRENCYTOTAL NET INCOME

3.88 EUREUR25,396.87TOTAL

3.88 EUREUR25,396.87Revenue qualifying for the withholding tax option

Shares entitling a deduction

Other revenue not entitling a deduction or withholding tax

BREAKDOWN OF THE COUPON

Non-distribuable and non-taxable income

Amount distributed on capital gains and losses

PORTFOLIO Tikehau Subordonnees Financieres