The Vulnerability of Pegged Exchange Rates: The British Pound … · 2019-10-10 · The...

16

41 Mathias Zurlinden Mathias Zurlinden, an economist with the Swiss National Bank, was a visiting scholar at the Federal Reserve Bank of St Louis when this paper was started. Thomas A. P01/mann provided research assistance. The Vulnerability of Pegged Exchange Rates: The British Pound in the ERM ETWEEN SEPTEMBER 1992 and August 1993, the European Monetary System (EMS) went through the most serious crisis since its start in 1979. Member countries cross-pegging their exchange rates in the framework of the Exchange Rate Mechanism (ERM) were confront- ed with a string of speculative currency attacks. Associated with these attacks were five realign- ments and the suspension of two major currencies—the Italian lira and the British pound—from the ERM. The situation eased off only when the fluctuation margins were widened considerably in August 1993. There are two reasons to review these events. First, there had been no genuine realignment in the EMS for more than five years. The EMS had widely come to be seen as a model for a viable pegged exchange rate system. Second, most of the recent cases of speculative currency attacks occurred in developing countries, where access to foreign exchange reserves is rather limited and capital controls usually play an important role in maintaining pegged exchange rates? Hence, the near-collapse of the ERM provides a useful example of a speculative attack under 1 See Edwards (1989) for a detailed analysis of devaluations in developing countries. 2 There is a vast literature on the EMS. Ungerer, et al. (1983, 1986, 1990) provide accessible reviews of EMS develop- ments. Also see Fratianni and von Hagen (1992), Giavazzi and Giovannini (1989), and Gros and Thygesen (1992) for more advanced discussions. conditions of easy access to foreign exchange reserves and free capital mobility. This article concentrates on the British epi- sode in the EMS crisis. Since the United King- dom’s participation in the ERM was suspended in September 1992, only the early phase of the crisis is covered. First, I describe a brief history of the pound in the EMS. Next, I have selected macroeconomic indicators on the eve of the cri- sis to provide a picture of the economic situa- tion and the credibility of the exchange rate band as perceived by the markets. Then, I dis- cuss the main features of the speculative attack on the pound against the background of the basic model of balance-of.payments crisis. To this end, I introduce the model originated by Krugman (1979), along with extensions motivated by the British situation. BRITAIN’S PARTICIPATION in the ERM 2 When the EMS started operating on March 8, 1979, Britain did not participate in the central ~cpTrL1ncRJnrTnnrn iooq

Transcript of The Vulnerability of Pegged Exchange Rates: The British Pound … · 2019-10-10 · The...

41

Mathias Zurlinden

Mathias Zurlinden, an economist with the Swiss NationalBank, was a visiting scholar at the Federal Reserve Bankof St Louis when this paper was started. Thomas A. P01/mannprovided research assistance.

The Vulnerability of PeggedExchange Rates: The BritishPound in the ERM

ETWEEN SEPTEMBER 1992 and August1993, the European Monetary System (EMS)went through the most serious crisis since itsstart in 1979. Member countries cross-peggingtheir exchange rates in the framework of theExchange Rate Mechanism (ERM) were confront-ed with a string of speculative currency attacks.Associated with these attacks were five realign-ments and the suspension of two majorcurrencies—the Italian lira and the Britishpound—from the ERM. The situation eased offonly when the fluctuation margins were widenedconsiderably in August 1993.

There are two reasons to review these events.First, there had been no genuine realignment inthe EMS for more than five years. The EMS hadwidely come to be seen as a model for a viablepegged exchange rate system. Second, most ofthe recent cases of speculative currency attacksoccurred in developing countries, where accessto foreign exchange reserves is rather limitedand capital controls usually play an importantrole in maintaining pegged exchange rates?Hence, the near-collapse of the ERM providesa useful example of a speculative attack under

1See Edwards (1989) for a detailed analysis of devaluationsin developing countries.

2There is a vast literature on the EMS. Ungerer, et al. (1983,1986, 1990) provide accessible reviews of EMS develop-ments. Also see Fratianni and von Hagen (1992), Giavazziand Giovannini (1989), and Gros and Thygesen (1992) formore advanced discussions.

conditions of easy access to foreign exchangereserves and free capital mobility.

This article concentrates on the British epi-sode in the EMS crisis. Since the United King-dom’s participation in the ERM was suspendedin September 1992, only the early phase of thecrisis is covered. First, I describe a brief historyof the pound in the EMS. Next, I have selectedmacroeconomic indicators on the eve of the cri-sis to provide a picture of the economic situa-tion and the credibility of the exchange rateband as perceived by the markets. Then, I dis-cuss the main features of the speculative attackon the pound against the background of thebasic model of balance-of.payments crisis. Tothis end, I introduce the model originated byKrugman (1979), along with extensions motivatedby the British situation.

BRITAIN’S PARTICIPATIONin the ERM2

When the EMS started operating on March 8,1979, Britain did not participate in the central

~cpTrL1ncRJnrTnnrn iooq

42

piece of the new system, the ERM? In the viewof British monetary authorities, the loss of roomfor maneuvering under a system of peggedexchange rates outweighed probable gains. Manyobservers did not give the ERM much crediteither. Some predicted an inflationary bias,while others expected the system to he drawnapart soon by the widely differing inflation ratesamong participating countries. In the event, theERM performed surprisingly well. Inflation ratesdecreased substantially (albeit not more than innon-ERM countries), and the variability of nomi-nal and real effective exchange rates fell a greatdeal.

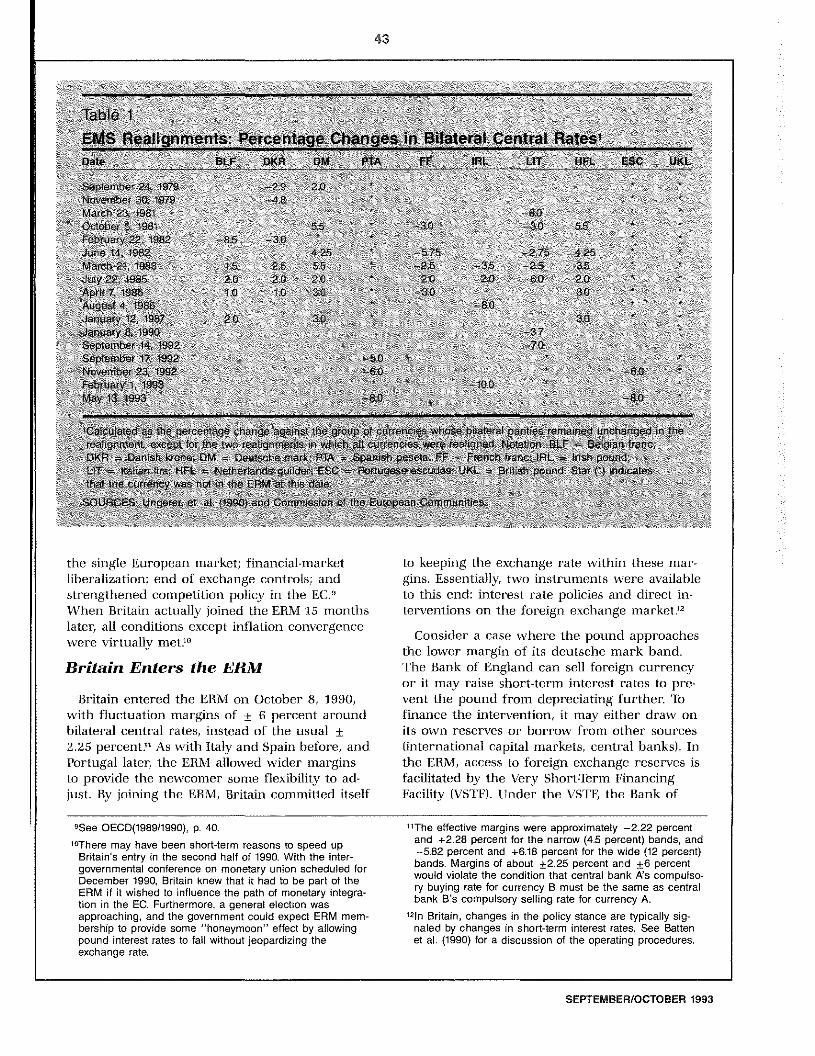

Certainly, many realignments were requiredfor the ERM to survive during its early years.The 17 realignments witnessed in the period1979-93 are summarized in Table 1.~‘fivo fea-tures stand out. First, the deutsche mark neverwas devalued against other ERM currencies.Second, realignments became less frequent until1992, reflecting the decline in intra-ERM infla-tion rate differentials.~

Capital controls also played a role in thesurvival of the ERM. They had intensified in thefinal years of the Bretton Woods System andmany European countries continued to use themafter that. It was not until 1988 that an ECdirective stipulated the complete liberalization ofcapital movements. For’ most member countries,this was accomplished by mid-1990 (extensionswere granted for Greece, Ireland, Portugal and

Spahi).

Britain chose a different way. Rather thanparticipate in the ERM when it began in 1979,Britain decided to pursue a deliberately tightmonetary policy based on a free float and

growth targets for monetary aggregates. Capitalcontrols were removed rapidly and fiscal policywas oriented toward balancing the budget.8 Thisstrategy resulted in a large reduction of inflation(from 18 percent in 1980 to less than 5 percentin 1983), albeit at the price of substantial outputlosses. A complicating factor was the increasinglyunstable relationship between the targetedmonetary aggregate (sterling M3) and nominalincome.’ This made sterling M3 a questionableindicator, which risked a reduction in the credi-bility of monetary policy. In response, monetaryauthorities tried several alternatives. First, sever-al aggregates were targeted simultaneously.Then, the emphasis shifted to narrow monetaryaggregates. Finally, in 1987-88, the free float wasreplaced by a managed exchange rate shadowingthe deutsche mark.

In retrospect, the mark exchange rate target-ing of 1987-88 was an ill-fated attempt at findinga stable nominal anchor. Initially, monetary poli-cy loosened due to the determination of thegovernment to stick with the unofficial targetexchange rate of 3 marks per pound. As aresult, the economy overheated and forcedmonetary authorities to tighten the policy stanceand to let the pound appreciate.8

Despite this troubled experience with anexchange-rate oriented policy, ERM membershipremained an option favored by the chancellor ofthe exchequer, Nigel Lawson, and supported byleading husinesspeople. Tn June 1989, at the EUsummit in Madrid, the government set theterms for Britain’s entry to the ERM. Theseterms were: British inflation close to the EUaverage; i-cal progress towards completion of

3The EMS includes all members of the European Communi-ty (EC). The ERM originally included only Belgium-Luxembourg, Denmark, Germany, France, Ireland, Italy andthe Netherlands. Portugal, Spain and the United Kingdomjoined in April 1992, January 1990, and October 1990,respectively. Italy and the United Kingdom suspended theirparticipation in the ERM in September 1992. Greece hasnever participated in the ERM.

~Itmay be argued that there were only 16 genuine realign-ments. On January 8, 1990, when the Italian lira switchedfrom ±6 percent to ±2.25 percent fluctuation margins,the central rate was devalued relative to the current marketrate. The new lower intervention margins were not belowthe old margins, however, except for the Spanish pesetaexchange rate of the lira.

5Giavazzi and Giovannmni, among many others, argue thatthe EMS became a greater deutsche mark area by 1983;Germany is the center country, and countries such as Italyand France peg their currencies to the mark. See Fratianniand von Hagen for qualifications of this view.

~Achronological account of British economic policy isprovided by the annual surveys on the United Kingdompublished by the Organization for Economic Cooperationand Development (OECD).

‘Sterling M3 is MS less residents’ deposits abroad.8See Belongia and Chrystal (1990) for a critical discussionof this episode.

FEDERAL RESERVE BANK OF St LOUIS

43

N

N

N ‘N

‘~ ~flbIs1 N “

~MSneanw,meêts~~ercent~à~angáin Bilateral centS fiatest\NDSt~~\ ~‘:N e~ \PJ~R ~rnK flA~~~P~‘~lRL’N~’NuTN:N~l*L> ~lsc~ Nu$L

\/\ \\/\\<$sptember 4197t ~ \~N N~

*Q~ \N /$ \ \“NN NN

is \\\\\N /N ‘N’N~ •

\ -~ -SD M‘k~$abttry ~!. \* 3ft, ~NN~ N

~4W*14l98?N N N & ‘N 278’N 42 NM*Is 983 6 fl N~t5 -4s -25 35

* 92 198$ tO 2,0 b 60 2flNA )‘19$6

TN Nj2$~ NN N tON N

NNJatw* 19W 2.0 // NN toJUt>409

9N N ~ N N N N \NN N

$set*ettaaaN N / ~NN N 7Ø,N

N/S~~St~ 19S N N NN ~ ‘-~W N N N N *

N

N’ N~~8 Nna~ ‘N \\N\ ~ N/// ,/,\ \N~, N

~‘G~9”t N’”’ N ,/,~//N//\/ / N

4* N~ N’N N NN /N~ ~ N / /N N NNNNN ~ N N N

t NNNNN:4

N:. NN N / “‘N N ~NN /

!t!~$~~~ ~ N

N N ~. ~ t~ssf tpSTtSJMatlwkS~’ ~ N’

//<~)4~a~ue “at øeSsa. py4~ / ~ ~ “~ N’~,

~ kjsN N ~“ N ~ ~N N’ / N

N C~/// N ~ N ;N ‘N/j 4” 44 N,’

the single European market; financial-marketliberalization; end of exchange controls; andstrengthened competition policy in the EC.9

When Britain actually joined the ERM 15 monthslater, all conditions except inflation convergencewere virtually met?”

Britain Enters the ERM

Britain entered the ERM on October 8, 1990,with fluctuation margins of ±6 percent aroundbilateral central rates, instead of the usual ±2.25 percent.” As with Italy and Spain before, andPortugal later, the ERM allowed wider marginsto provide the newcomer some flexibility to ad-just. By joining the ERM, Britain committed itself

to keeping the exchange rate within these mar-gins. Essentially, two instruments were availableto this end: interest rate policies and direct in-terventions on the foreign exchange market?2

Consider a case where the pound approachesthe lower margin of its deutsche mark band.The Bank of England can sell foreign currencyor it may raise short-term interest rates to pre-vent the pound from depreciating further. lbfinance the intervention, it may either draw onits own reserves or borrow from other sources(international capital markets, central banks). Inthe ERM, access to foreign exchange reserves isfacilitated by the Very Short-lerm FinancingFacility (VSTF). Under the VSTF, the Bank of

9See OECD(1989/1990), p. 40.‘°Theremay have been short-term reasons to speed up

Britain’s entry in the second half of 1990. With the inter-governmental conference on monetary union scheduled forDecember 1990, Britain knew that it had to be part of theERM if it wished to influence the path of monetary integra-tion in the EC. Furthermore, a general election wasapproaching, and the government could expect ERM mem-bership to provide some honeymoon” effect by allowingpound interest rates to fall without jeopardizing theexchange rate.

“The effective margins were approximately —2.22 percentand +2.28 percent for the narrow (4.5 percent) bands, and—5.82 percent and +6.18 percent for the wide (12 percent)bands. Margins of about ±2.25percent and ±6percentwould violate the condition that central bank A’s compulso-ry buying rate for currency B must be the same as centralbank B’s compulsory selling rate for currency A.

“In Britain, changes in the policy stance are typically sig-naled by changes in short-term interest rates. See Battenet al. (1990) for a discussion of the operating procedures.

SEPTEMBER/OCTOBER 1993

44

England is allowed to borrow marks from theBundesbank virtually without limits. TheBundesbank is obliged to grant such creditsupon request?3

After Britain joined the ERM, the poundmoved most of the time comfortably in the ±6percent band around its central rate. After atemporary appreciation, the pound stayed formore than one year in an implicit narrowerband in the neighborhood of ±2.25 percentaround central parity. Pressure on the poundusually was short-lived and quickly reversed byeither a slight increase in domestic interest ratesor modest interventions in the foreign exchangemarket. Interest rates were raised temporarilywhen Margaret Thatcher stepped down asprime minister in November 1990 and in theweeks before the general election of April 1992,when opinion polls pointed to a victory for theopposition Labour party. On the whole, however,interest rates (as well as inflation) decreasedsubstantially during the period Britain partici-pated in the ERM.

Tensions in the ERM

The tensions in the foreign exchange marketsthat finally led to the near-collapse of the ERMin September 1992 were triggered by doubtsabout the progress toward monetary union?~In June 1992, the Danes had voted no in areferendum on the Maastricht Tt1’eaty, whichincluded a chapter on European MonetaryUnion (EMU). Moreover, the outcome of theFrench referendum on the treaty in Septemberwas expected to be close. Since the prospect ofmonetary union had provided an anchor forexpectations, the outlook for the current paritiesin the ERM looked rather bleak if France reject-ed the treaty also. For reasons discussed below,pressure on the exchange rate became most

notable first in Italy, where the discount ratewas raised over the summer of 1992 in severalsteps, from 12 percent to 15 percent. The poundfelt some pressure too, and British monetaryauthorities began to step up interventions onthe foreign exchange market in late August.On September 3, 1992, Britain announced aprogram to borrow ECU 10 billion, about $14.3billion (U.S.) at the time, in the internationalmarket to increase foreign exchange reserves.

Ultimately, the rise in domestic interest ratesdid not save the Italian lira. On September 13,the lira’s central rate was devalued by 7 percent.TWo days later, Germany slightly eased monetarypolicy. The discount rate was lowered by 50basis points to 8.25 percent and the Lombardrate was lowered by 25 basis points to 9.5 per-cent. These adjustments—the first German in-terest rate cuts in nearly five years—wereperceived as unexpectedly small by the markets,and comments attributed to the Bundesbankpresident, who appeared to question the ade-quacy of the pound’s central rate (subsequentlydenied), raised tensions further?~

Britain Withdraws from the ERM

On September 16—Black Wednesday—the Bankof England intervened massively on the foreignexchange market to prevent the pound fromfalling below the lower margin of its Deutschemark band. Furthermore, it raised the baselending rate from 10 to 12 percent and an-nounced later in the day a further rise to 15percent, to be effective the following morning.These measures did not succeed in relieving thepressure on the pound. In the evening, Britishmonetary authorities announced the temporarysuspension of the pound from the ERM. Itseemed hardly feasible to fix a new parity less

‘3Even if access to the VSTF is said to be unlimited, this isnot literally true. The Bundesbank has two reasons tomake sure that the VSTF is not overburdened. First, itbears an exchange rate risk since the credits are denomi-nated in European Currency Unit (ECU), a basket currencydefined by fixed quantities of member currencies. So, if thepound depreciates relative to the mark, the Bundesbankwill be repaid the value of depreciated ECU. Second, theselling of the mark during interventions raises Germany’smonetary base and would jeopardize its inflation objectiveunless the Bundesbank is able to sterilize the intervention.Therefore, the Bundesbank insisted right from the start ofthe ERM on an opt-out clause. According to Central Bank-ing (1992; Robert Pringle, ed), this clause was confirmedin a letter to the German government by the then-presidentof the bank, Otmar Emminger.

‘4For a detailed account of the events prior to Britain’s with-drawal from the ERM, see Bank of England Quarterly Bulle-tin (November 1992).

‘5See Financial Times, September 15, 1992, and September16, 1992, respectively. As is now known, the Bundesbankactually did suggest a trade—with the size of German in-terest cuts depending on the size of the realignment—tothe chairman of the EC Monetary Committee. Since theItalian lira finally was the only currency devalued on Sep-tember 13, German interest rate cuts consequently weresmall; see Financial Times, December 11, 1992, for adetailed account.

FEDERAL RESERVE BANK OF ST. LOUIS

45

than a week before the French referendum onthe Maastricht ‘Theaty The next day, the baselending rate was moved back to 10 percent. Atthe same time, Italy announced the lira’s tem-porary withdrawal from the ERM, while Spaindevalued its currency by 5 percent and imposedtemporary capital controls.

The floating of the pound marks the end ofBritain’s ERM episode. In the following weeks,when the markets did not calm down after theFrench had narrowly approved the Maastricht‘meaty, it became clear thai Britain and Italywould not rejoin quickly ‘The ERM struggled onfor another 10 months. Then, on August 2,1993, EC member states decided to raise themargins of the exchange rate bands to ±15per-cent around the central parities, an action com-ing close to a suspension of the system. The oldmargins continued to be valid only for thedeutsche mark/Dutch guilder exchange rate.

In retrospect, the distinctive feature ofBritain’s defense of the pound was the almostcomplete lack of interest rate policies. Domesticinterest rates were raised only on the final dayof the crisis and the size of this rise was rathersmall. Most other weak-currency countries inthe 1992-93 crisis of the EMS raised their short-term interest rates more aggressively?6 As indi-cated above, however, this did not provide themdurable relief from speculative attacks.

ECONOMIC INDICATORS PRIORTO BRITAIN’S WITHDRAWALFROM THE ERM

When Britain participated in the ERM, Britishmonetary authorities regularly emphasized theircommitment to the established exchange rateparities. It is not enough to make such a pledge,however. The market has to be convinced thatmonetary authorities have no incentive to droptheir commitment and that they will takewhatever action is necessary to defend the pan-

ties. This, of course, turns out to be difficult.The market knows that pegging the exchangerate ultimately is a conditional commitment. Ex-pectations are formed that monetary authoritieswill realign if the perceived cost of defendingthe exchange rate is larger than the perceivedcost of a realignment. This section takes a lookat selected macroeconomic indicators and askswhether the exchange rate target bands wereperceived as credible by the markets.

General Economic Conditions

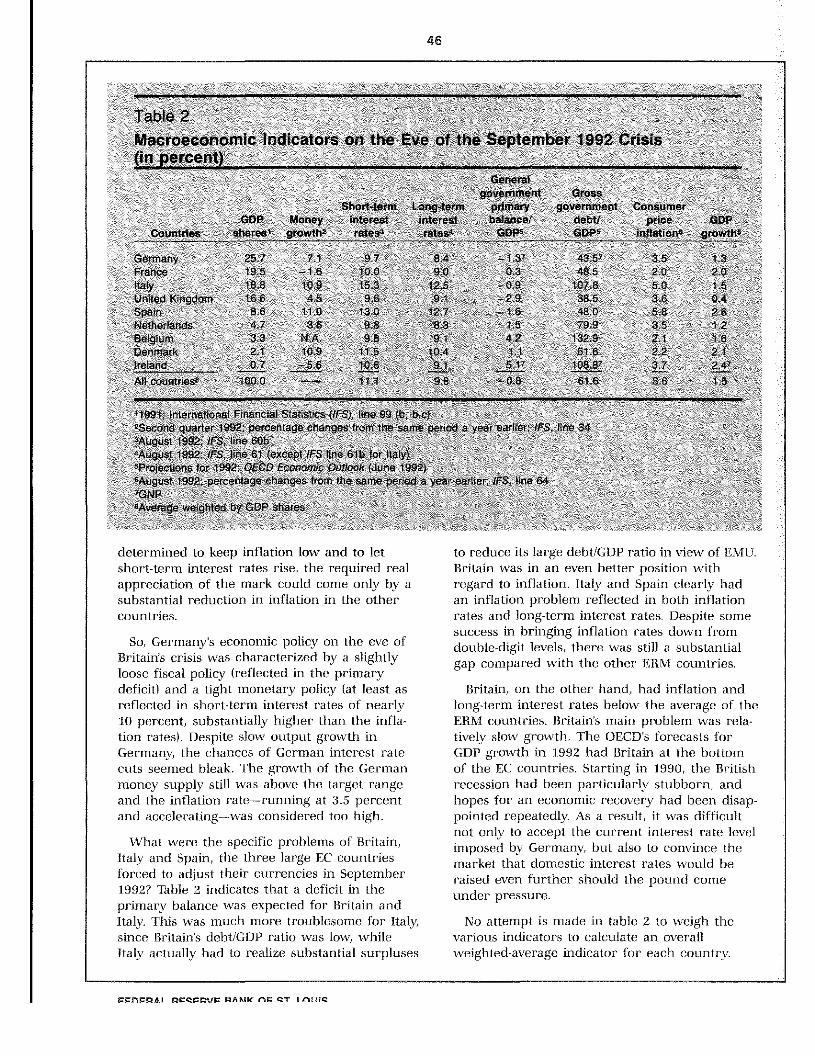

Table 2 shows macroeconomic indicators onthe eve of the crisis for all countries participat-ing in the ERM (except Portugal, because of datalimitations). The countries are ordered in termsof their relative size (measured by GDP). Indica-tors refer to August 1992 for monthly data andthe second quarter of 1992 for quarterly data.Annual figures are OECD forecasts for 1992,published in June of the same year. The indica-tors can roughly be divided into three groups:monetary indicators (money supply growth,short-term interest rate, long-term interest rate);fiscal indicators (primary deficit/GDP ratio,debt/GDP ratio); and indicators describing finalgoals (output growth, inflation)?~

These indicators shed some light on the diver-gent economic forces in the ERM. The most im-portant single event hitting the EC during recentyears has been German unification. Basic eco-nomic theory suggests that the German unifica-tion would lead to an increase in that country’saggregate demand and a real appreciation of themark (where tile real appreciation is equal tothe nominal appreciation adjusted by the infla-tion rate differential against foreign countries).These effects were heightened by the decisionto finance higher public spending by borrowingrather than by raising taxes?8 Under pegged ex-change rates, the real appreciation of the markis brought about by a positive inflation differen-tial between Germany and the other ERMmember countries. Since the Bundesbank was

‘°SeeGoldstein et al. (1993), Annex VI and the statisticalappendix in particular.

“Four out of the seven indicators closely correspond to themacroeconomic convergence criteria for EMU mentioned inthe Maastricht Treaty. These criteria are: (1) the inflationrate of the country under review must not exceed the aver-age of the three EC countries with the lowest inflation rateby more than 1.5 percent; (2) the interest rate on long-termgovernment securities must not be more than 2 percentagepoints higher than the average rate of the same threecountries; (3) the budget deficit must not exceed 3 percent

of GDP; and (4) the public debt/GDP ratio must not exceed60 percent. Note, however, that table 2 uses the primarydeficit (i.e. the budget deficit net of interest payments) toindicate whether the evolution of the fiscal indicators goesin the direction required by the EMU criteria.

‘8These are short-run effects. In the long run, an expansion-ary fiscal policy that permanently raises the debt/GDP ratiowill cause the real exchange rate to fall, since the countrymust export more to offset the effects of the decline in itsnet external asset position.

etnttliAatD,nrTnnco Inn.3

46

N N N N N N N NNN N N N \N N N‘N, N N’ N N N” ,NN NNNN,, NNN ,N N

N N N NN NNNNN N’ t~’~ N’ N N N N N N N

tablea N N N N N

Macroeconomic indicators on the, E~eof’ tt!e Septembé 1992 Crr~s NN (~npe~pent) N NN N NNNNN\ :,~ N\~ N N ,NN N\ :.N NN\

NNNNNNNNNNN

N N N N N N N N NN N ::NN N N N / gOVetflfl NN NGS N N NN N N N N N N N NNSh tetmN N~4fl94~tflt N::. Pr!mMt N gosern~nt Ctnsitrflet N N N

N N N NN N ~ NMOfl hIteSt N N N sn~test N N static.! ‘N debt/ N Npace NOOPN CaUñtnes. shares N grGwtht ~ N N N N GDfl N itlsonc ~towtM N

~

Gefatafty. 2S1TNNNI.t N~7NNNNs

4N12r 4$,57N NSSN it

Ft~fteeNNNNNN195 ~16NNt0*NN~N93~ NNfl N -485 N20 N~~22N:. NN

NIBSN N Q9 Nfl4 N j5NNN NN’~flN N NNtD7BN 50 0StedNKirtg4offi N N 4~ NNNfl NNNN S N Nfl N OAN N

NSNN SS ~i~: NtG NN NN N NNN~4RNN N N 4$,Q NNN~ 58 N *5 :NN

K~~NNN N47 $ØN 9~tNNNNN NN,~ NNNNNNN~ NN7fl S,SNNEeIjJfaN\ NNNa A NN*S ,UNNN4S NNNN$ZPN NN N[TtNNN

N95NN t0~ t4~ Nfl, N 1 816 22______ Nay -se iS N4 N 7

SQ tIN N NN 0’S SIS U N4 ~

‘‘N’ ,, , NNN, N N NNNNNNN,,NN ,,NN NN N, N N N

iast ‘Intetnanal N11a’ncla( Stattattes VP ‘WeStilt NN N N N

4s’Mfl scentaoe eM flflna $ S çser~ N

aAugust tQ9~$5 hne6Ob N N N

4Aug~ist1992 $5 tWa St (exc.~tIP& ltne Sm ot3W~N N, N N N

Pmfaehqns, S 1St DECO Eceh*$ic ONOc$jMteN199~ N,

!Mgust’Nta,* pSreS*9e 119* tv ba’ssØdØ year SWa JEt ‘West N

N N N N’> > ~~N,N N NNNNN

%&vel~WS9btS4~by GOP shates N N N N N> NN N NN>,N:NNNNN> N,NNN NN NN~:. N:: ~::~NN:> N N N N~ N NNNNNNN N N \NN NN NN4NNN NN. N

detertnined to keep inflation low and to letshort-term interest rates rise, the required realappreciation of the mark could come only by asubstantial reduction in inflation in the othercountries.

So, Germany’s economic policy on the eve ofBritain’s crisis was characterized by a slightlyloose fiscal policy (reflected in the primarydeficit) and a tight monetary policy (at least asreflected in short-term interest rates of nearly10 percent, substantially higher than the infla-tion rates). Despite slow output growth inGermany, the chances of German interest ratecuts seemed bleak. The growth of the Germanmoney supply still was above the target rangeand the inflation rate—running at 3.5 percentand accelerating—was considered too high.

What were the specific problems of Britain,Italy and Spain, the three large EC countriesforced to adjust their currencies in September1,992? Table 2 indicates that a deficit in theprimary balance was expected for Britain andItaly. This was much more trouhlesotne for Italy,since Britain’s debt/GOP ratio was low, whileItaly actually had to realize substantial surpluses

to reduce its large debt/GDP ratio in view of EMU.Britain was in an even better position withregard to inflation. Italy and Spain clearly hadan inflation problem reflected in both inflationrates and long-term interest rates. Despite somesuccess in bringing inflation rates down fromdouble-digit levels, there was still a substantialgap compared with the other ERM countries.

Britain, on the other hand, had inflation andlong-term interest rates below the average of theERM countries. Britain’s main problem was rela-tively slow growth. The (JECD’s forecasts forGDP growth in 1992 had Britain at the bottomof the EC countries. Starting in 1990, the Britishrecession had been particularly stubborn, andhopes for an economic recovery had been disap-pointed repeatedly. As a result, it was difficultnot only to accept the current interest rate levelimposed by Germany, hut also to convince themarket that domestic interest rates would beraised even further should the pound comeunder pressure.

No attempt is made in table 2 to weigh thevarious indicators to calculate an overallweighted-average indicator for each country.

rrflr~ftI QrQrn’tr QAMW flr QT flfl~C

47

A review of EMS realignments since 1979, how-evet~indicates that the chief cause for a devalu-ation was probably a persistent inflation differen-tial, leading to an overvaluation of the currency.Such an overvaluation often was built up overan extended period of tine. Therefore, a betterindicator than an annual performance measureis the cumulated rate of change of the real ex-change rate over the period starting with thedate when the current parities were established.

Movements in the RealExchange Rates

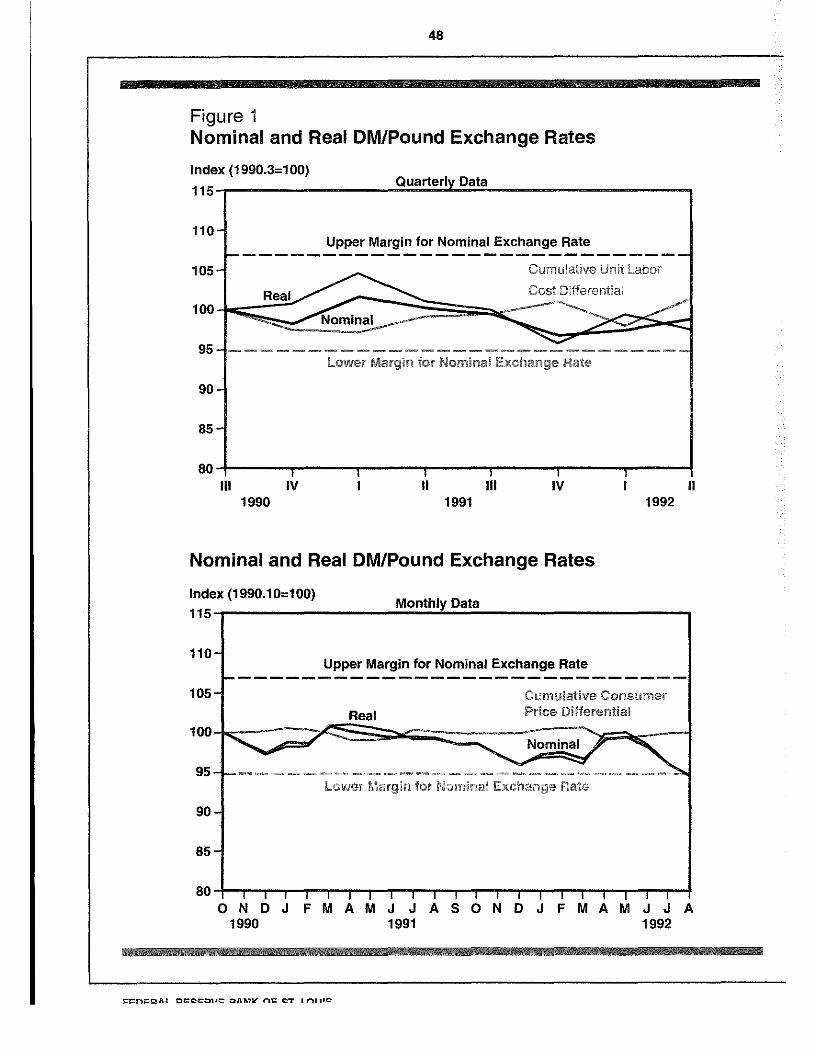

Figure 1 shows the real mark/pound exchangerate when Britain participated in the ERM.Nominal exchange rates, the margins of theexchange rate band, and cost or price differen-tials are given for convenience. There are vari-ous ways to calculate real exchange rates. Here,two indexes were calculated. The first is basedon unit labor cost, and the second on consumerprices?9 Note that unit labor cost data are quart-erly (ending in the second quarter of 1992),while consumer price data are monthly (endingin August 1992). Hence, the top graph of figure1 (quarterly data) does not have the pound fall-ing to the lower margin at the very end of theperiod. Both indexes show that cumulated infla-tion differentials were very small on the eve ofthe collapse (0.05 percent for consumer pricesand 1.4 percent for unit labor cost). Since thenominal exchange rate of the pound depreciatedinside the band, both measures of the realexchange rate indicate that the mark price ofthe pound was lower in real terms comparedto its entry level.

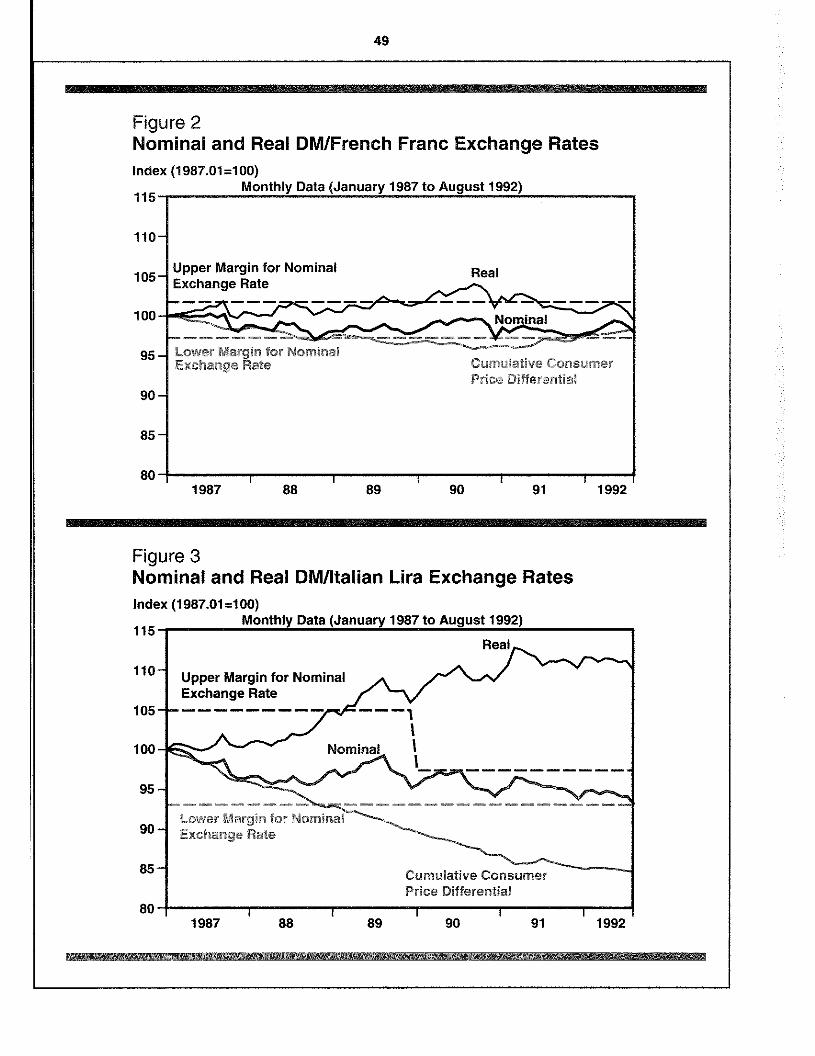

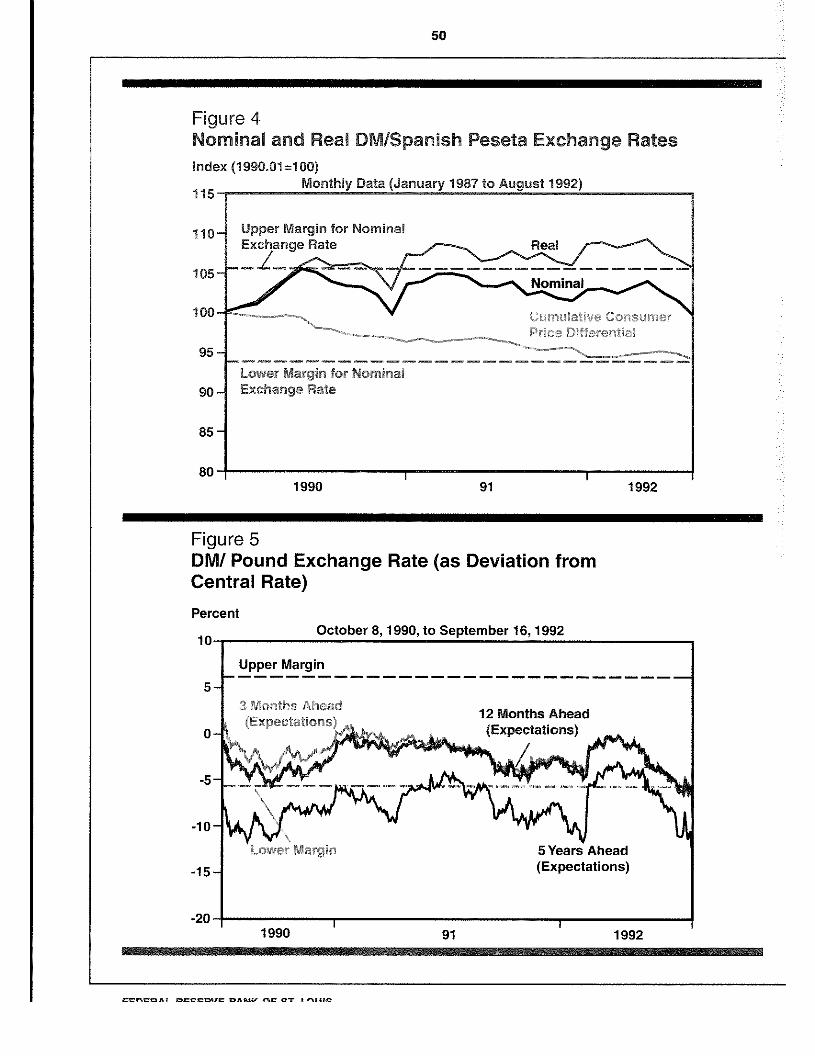

Figures 2-4 repeat this exercise for France,Italy and Spain, the three other, major, non-German countries participating in the ERM.Only the real exchange rates based on consumerprices are shown. The starting dates differ ac-cording to the preceding realignment (January

1987 for both the French franc and the Italianlira) or the entry to the ERM (January 1990 forSpain).20 The figures exhibit substantial real ap-preciation for both the Italian lira and (to a less-er extent) the Spanish peseta. The franc, whileappreciating in real terms during the first fewyears, largely retraced its rise by 1990 thanks tolow inflation.

Overall, the evolution of the real exchangerate does not point to the pound (or the franc)as a candidate for a devaluation.21 There wasnothing like the usual pattern of an increasingovervaluation due to a persistent inflation ratedifferential. Still, theme was the discrepancy be-tween the cyclical needs of the British economyand the high interest rates imposed on the ERMby Germany. The next section examines the per-ception of the exchange rate band’s credibilitybefore the speculative currency attacks actuallyforced the withdrawal of the pound (and thelira) from the ERM.

Perceptions of Britain’s Credibilityin the ERM

A simple way to assess an exchange rateband’s credibility is based on uncovered interestrate parity.zz Uncovered interest rate paritystates that under perfect international capitalmobility and risk-neutral speculation, thedifferential between nominal domestic and for-eign interest rates is equal to the anticipatedrate of depreciation of the domestic currency.So, given the current exchange rate and domes-tic and foreign interest rates for various maturi-ties, the expected exchange rate for thesematurities can be calculated. Then, the band issaid to be credible if the expected exchange rateis within the margins of the band.23

Figure 5 shows the results for the mark/poundexchange rate when Britain participated in theERM. The time horizons are three months, 12

~Consumerprices excluding mortgage rates are used forBritain in this calculation, but not in table 2. The formermeasure is widely seen as a better indicator of core infla-tion. If a tight monetary policy raises interest rates, includ-ing mortgage rates, the overall price index may actuallyshow an acceleration of inflation, while the brakes on infla-tion are already in place. Britain’s inflation would be lower(and the real depreciation of the pound even morepronounced) if the overall consumer price index weretaken, since interest rates were falling during much of theperiod under review.

20Again, the realignment of January 8, 1990, caused by theswitch of the Italian lira to a narrow band is ignored. Seefootnote 4 for explanations.

21There may have been real factors leading to a lower realmark/pound equilibrium rate, however. Also, the central par-ity may have been too ambitious from the beginning. Notethat the real Deutsche mark/pound exchange rate was low-er in October 1990 than during most of the 1980s.

22This test was originated by Svensson (1991).

2Slf the assumption of risk-neutrality is dropped, a term forrisk premia must be included in the interest rate paritycondition. Svensson (1992) showed that these premia arevery small for narrow exchange rate bands.

SEPTEMBER/OCTOBER 1993

48

Figure 1Nominal and Real DM/Pound Exchange RatesIndex (1990.3=100)

Nominal and Real DM/Pound Exchange Rates

Index (1990.10=100)Monthly Data

80— I I I I ION D J FM AM J JASON D J F MA M J J

19911990 1992

II

A

115

110’

105

100-

Upper Margin for Nominal Exchange Rate

Cumulative Unit Labor

Cost Differential

95

90

85

80

Lower Margin for Nominal Exchange Rate

Ill IV I II III IV I1990 1991 1992

115

110—

105-

100-

95-

90-

85-

Upper Margin for Nominal Exchange Rate

Cumulative Consumer

Real Price Differential

~nal

Lower Margin for Nominal Exchange Rate

~n~DAI Dretouc DAMIt flC I flflIO

49

Figure 2Nominal and Real DM/French Franc Exchange RatesIndex (1987.01=100)

Monthly Data (January 1987 to August 1992)

I I I

1987 88 89 90 91 1992

Nominal and Real DM/ltalian Lira Exchange RatesIndex (1987.01=100)

Monthly Data (January 1987 to August 1992)

Upper Margin for NominalExchange Rater

~r~nfoTomina~~

CumulatIve ConsumerPrice Differential

88 I 89 90I 91 1992

115-

110-

105-

100-

95 -

90-

85-

80-

Upper Margin for Nominal Real

Lower Margin for Nomtnal Cumulative ConsumerExchange Rate Price Differential

Figure 3

115—

110—

105-

100-

95

90-

85-

I

801987

50

Figure 4

Nominal and Real DM/Spanish Peseta Exchange RatesIndex (1 990.01 =1 00)

Monthly Data (January 1987 to August 1992)

Cumuiati.ve Consumer‘~¾. Puce Dtff*ranvat

Lower Margin for NominalExchange Rate

1990 91 1992

Figure 5DM1 Pound ExchangeCentral Rate)Percent

Rate (as Deviation from

115

110

105

100

95 -

Upper Margin for NominalExchange Rate

/

90-

85-

80

October 8, 1990, to September 16,1992

1990 91 1992

CflCO A OtOCO~IC C AMU flt 0T fl* HO

51

months and five years, hased on interest ratedifferentials. Interest rates for three and 12months are Euromarket rates, guaranteeing thatthe deposits are comparable in every respect ex-cept currency denomination. The interest ratesfor five years are based on government bondyields, since no Euromarket rates are readilyavailable for maturities of more than 12 months.The data are daily.

The results indicate that the expected exchangerate always moved within the margins of theband for maturities up to 12 months untilmid-August 1992. For maturities of five years,however, the expected exchange rate most of thetime was outside the margins. The latter resultimplies that there were some lingering doubtsabout the long-term credibility of the mark!pound exchange rate band. Nevertheless, a crisiswas not perceived as particularly likely. Doubtsabout the short- or medium-term credibility ofthe band arose only immediately before the par-ity actually was attacked.

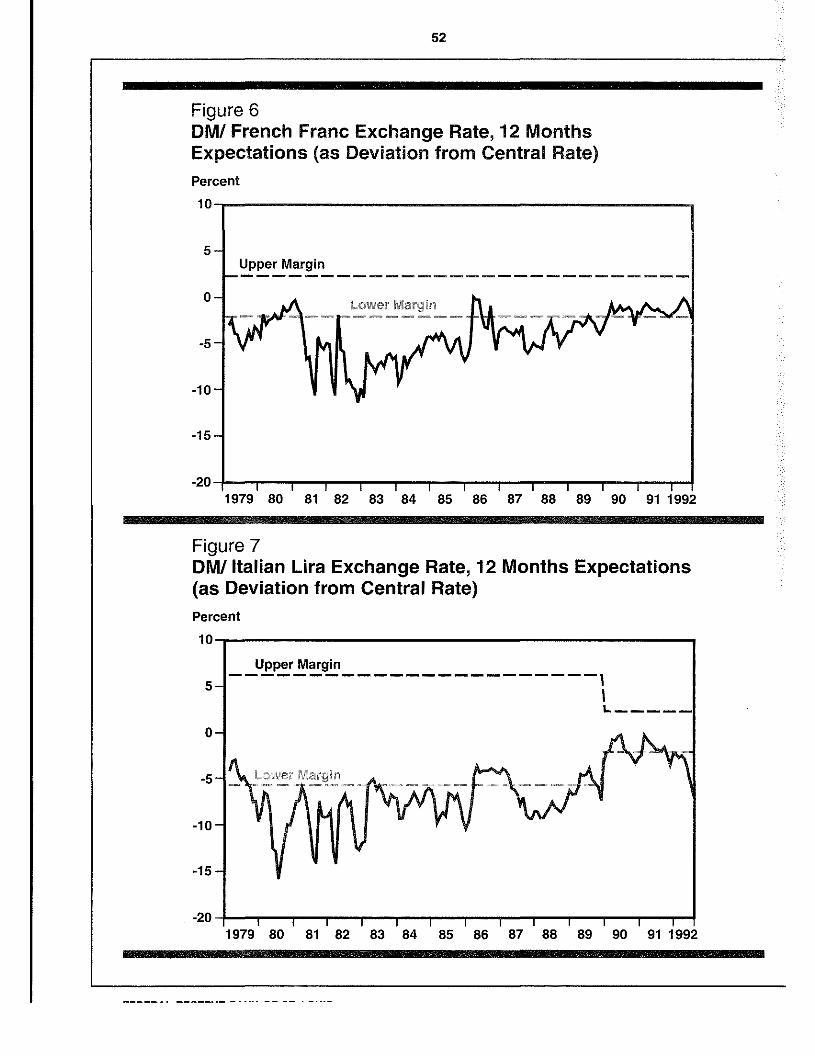

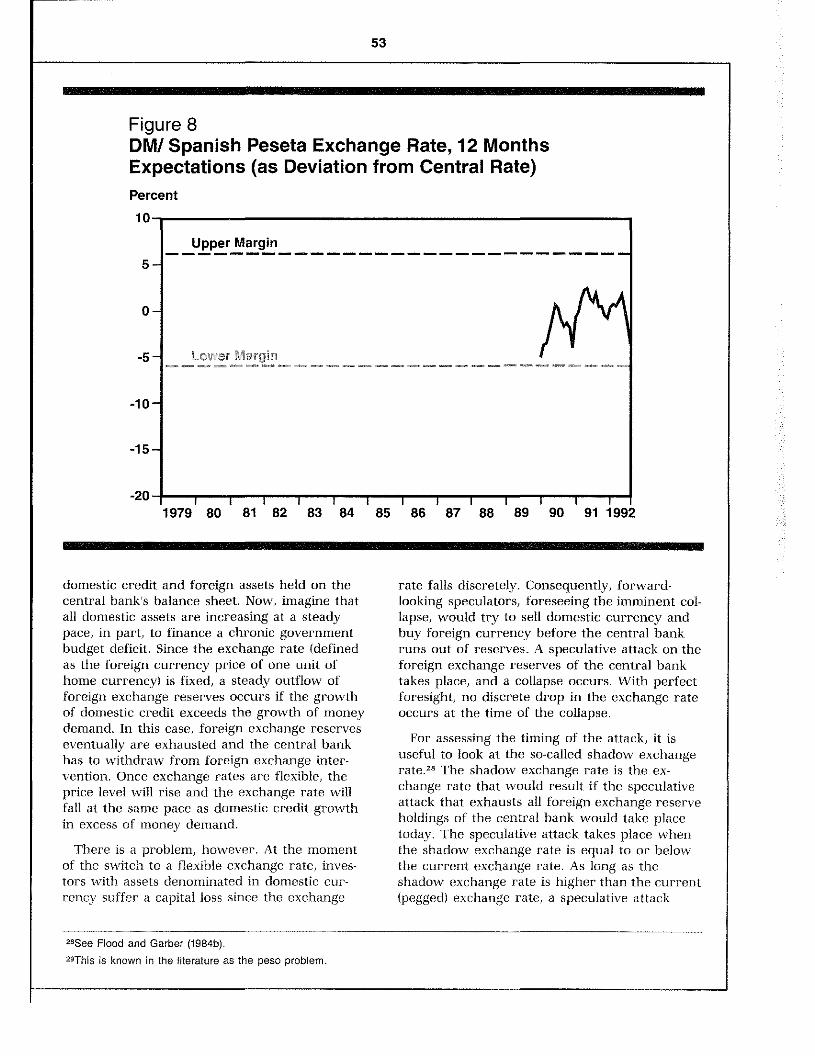

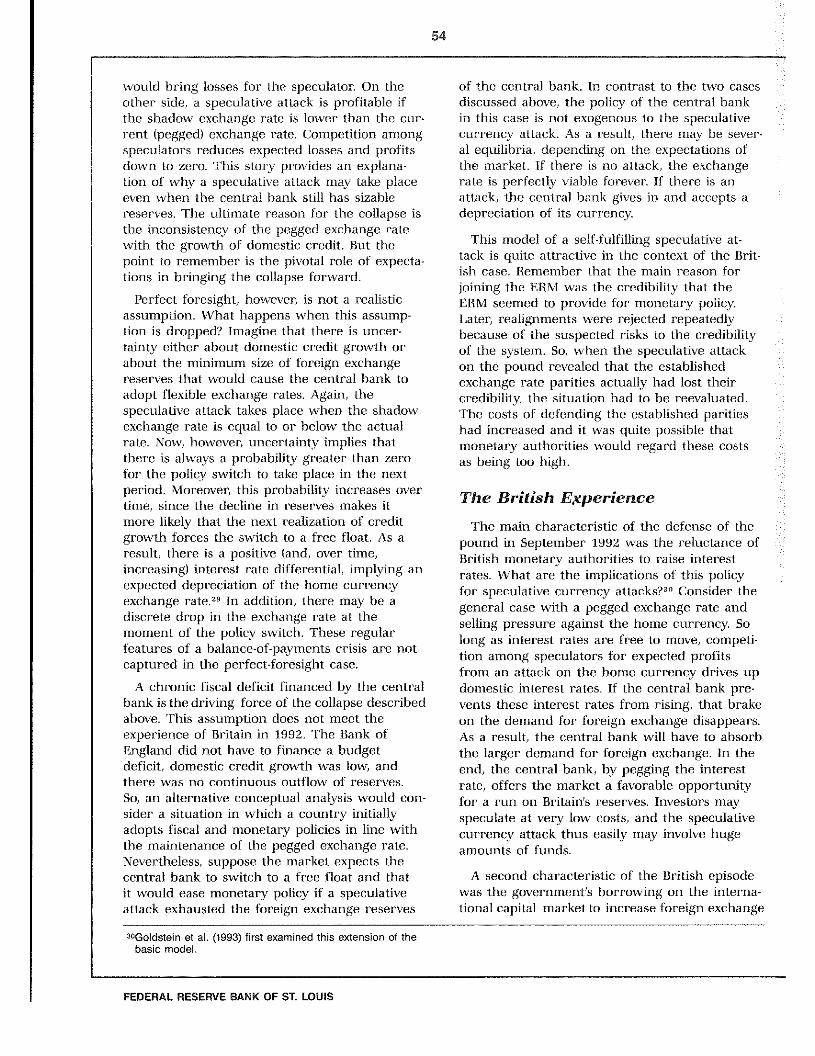

Using monthly data for 12 months, the sameexercise was applied to the franc, the lira andthe peseta during the periods these currencieswere participating in the ERM. The results,summarized in figures 6-8, show that thecredibility of the band derived for the poundcannot be generalized to apply to other EMScountries throughout the period of their par-ticipation. The expected future exchange ratesof both the franc and the lira mostly wereoutside the margins of the bands during 1979-89.Since 1989, the expected future exchange ratesof ERM currencies usually were within themargins.2~

Rose and Svensson (1991) proposed a slightlymore elaborate technique to assess the credibili-ty of exchange rate bands.25 They split the totalrate of depreciation implied by the interest ratedifferential into the expected rate of deprecia-tion within the band and the expected rate ofrealignment. The expected rate of depreciation

within the band (conditional upon no realign-ment) is estimated under the assumption ofrational expectations using realized exchangerate data. The result is deducted from the in-terest rate differential to get the expected rateof realignment.26 Rose (1993) recently used thismethod to calculate expected realignment ratesfor the mark!pound exchange rate. He showsthat expectations of a pound realignment werelow throughout most of 1992. The pound’scredibility was not in reasonable doubt untilmid-August 1992, at the earliest.

Overall, the credibility measures indicate thaithe successful speculative attack on the poundwas not anticipated well in advance. The diver-gent economic forces stemming from Germanunification—well known for quite some time—did not result in a prompt decline in the ex-change rate band’s credibility Signs of an ap-proaching crisis were strikingly rare. To gain abroader picture of the timing and the dynamicsof the speculative attack, the next section con-siders the basic model of a balance-of-paymentscrisis.

THE ECONOMIC ANALYSIS OF A

SPECULATIVE ATTACK

To clarify Britain’s problem in the ERM, anoutline of the basic model of speculative curren-cy attacks that has dominated the recent litera-ture follows. Also reviewed are some extensionsmotivated by the preceding discussion of theBritish episode. These extensions include theroles of interest rate pegging, borrowing andcapital controls.27

Some Theoretical Considerations

Consider a situation of a currency whosevalue is pegged to a foreign currency. Theforeign interest rate is assumed to be constant.There is no commercial banking sector, and thesupply of money is equal to the total of both

‘4See Frankel and Phillips (1991) for an investigation of credi-bility in the EMS using survey data on expected exchangerates in addition to interest rate differentials.

253ee Svensson (1993) for an application on EMS data.26lt is assumed that the position of the exchange rate inside

the band is the same before and after the realignment.While this makes it possible to interpret the result as theexpected rate of realignment, it is somewhat at odds withthe facts. After most realignments, the exchange ratelumped toward the upper margin of the band.

27The literature on speculative currency attacks starts withKrugman (1979) and Flood and Garber (1984b). Flood andGarber (1984a) and Obstfeld (1986) analyzed self-fulling at-tacks and multiple equilibria. Agënor et al. (1992) andBlackburn and Sola (1993) provide selective reviews of thefast-growing literature. For an excellent non-technicaldescription, see Goldstein et al. (1993), Annex V.

52

Figure 6DM1 French Franc Exchange Rate, 12 MonthsExpectations (as Deviation from Central Rate)Percent

10

5

0

-5

-10

-15

-20

Figure 7DM1 Italian Lira Exchange Rate, 12 Months Expectations(as Deviation from Central Rate)Percent

53

Figure 8DM1 Spanish Peseta Exchange Rate, 12 MonthsExpectations (as Deviation from Central Rate)Percent

•-15

I I I I I I I I I I I I I19798081828384858687888990911992

domestic credit and foreign assets held on thecentral bank’s balance sheet. Now, imagine thatall domestic assets are increasing at a steadypace, in part, to finance a chronic governmentbudget deficit. Since the exchange rate (definedas the foreign currency price of one unit ofhome currency) is fixed, a steady outflow offoreign exchange reserves occurs if the growthof domestic credit exceeds the growth of moneydemand. In this case, foreign exchange reserveseventually are exhausted and the central bankhas to withdraw from foreign exchange inter-vention. Once exchange rates at-c flexible, theprice level will rise and the exchange rate willfall at the same pace as domestic credit growthin excess of money demand.

There is a problem, however. At the momentof the switch to a flexible exchange rate, inves-tors with assets denominated in domestic cur-rency suffer a capital loss since the exchange

rate falls discretely. Consequently, forward-looking speculators, foreseeing the imminent col-lapse, would try to sell domestic currency andbuy foreign currency before the central bankruns out of reserves. A speculative attack on theforeign exchange reserves of the central banktakes place, and a collapse occurs. With perfectforesight, no discrete drop in the exchange rateoccurs at the time of the collapse.

For assessing the timing of the attack, it isuseful to look at the so-called shadow exchangerate.28 ‘i’he shadow exchange rate is the ex-change rate that would result if the speculativeattack that exhausts all foreign exchange reserveholdings of the central bank would take placetoday. The speculative attack takes place whenthe shadow exchange rate is equal to or belowthe current exchange rate. As long as theshadow exchange rate is higher than the current(pegged) exchange rate, a speculative attack

285ee Flood and Garber (1984b).

10-

Upper Margin5—

0-

-5- Lower Margin

-10-

-20

29This is known in the literature as the peso problem.

54

would bring losses for the speculator. On theother side, a speculative attack is profitable ifthe shadow exchange rate is lower than the cur-rent (pegged) exchange rate. Competition amongspeculators reduces expected losses and profitsdown to zero. This story provides an explana-tion of why a speculative attack may take placeeven when the central bank still has sizablereserves. The ultimate reason for the collapse isthe inconsistency of the pegged exchange ratewith the growth of domestic credit. But thepoint to remember is the pivotal role of expecta-tions in bringing the collapse forward.

Perfect foresight, however, is not a realisticassumption. What happens when this assump-tion is dropped? Imagine that there is uncer-tainty either about domestic credit growth orabout the minimum size of foreign exchangereserves that would cause the central bank toadopt flexible exchange rates. Again, thespeculative attack takes place when the shadowexchange rate is equal to or below the actualrate. Now, however, uncertainty implies thatthere is always a probability greater than zerofor the policy switch to take place in the nextperiod. Moreovet this probability increases overtime, since the decline in reserves makes itmore likely that the next realization of creditgrowth forces the switch to a free float. As aresult, there is a positive (and, over time,increasing) interest rate differential, implying anexpected depreciation of the home currencyexchange rate.29 In addition, there may be adiscrete drop in the exchange rate at themoment of the policy switch. These regularfeatures of a balance-of-payments crisis are notcaptured in the perfect-foresight case.

A chronic fiscal defIcit financed by the centralbank is the driving force of the collapse describedabove. This assumption does not meet theexperience of Britain in 1992. The Bank ofEngland did not have to finance a budgetdeficit, domestic credit growth was low, andthere was no continuous outflow of reserves.So, an alternative conceptual analysis would con-sider a situation in which a country initiallyadopts fiscal and monetary policies in line withthe maintenance of the pegged exchange rate.Nevertheless, suppose the market expects thecentral bank to switch to a free float and thatit would ease monetary policy if a speculativeattack exhausted the foreign exchange reserves

of the central bank. In contrast to the two casesdiscussed above, the policy of the central bankin this case is not exogenous to the speculativecurrency attack. As a result, there may he sever-al equilibria, depending on the expectations ofthe market. If there is no attack, the exchangerate is perfectly viable forever. If there is anattack, the central bank gives in and accepts adepreciation of its currency.

This model of a self-fulfilling speculative at-tack is quite attractive in the context of the Brit-ish case. Remember that the main reason forjoining the ERM was the credibility that theERM seemed to provide for monetary policyLater, realignments were rejected repeatedlybecause of the suspected risks to the credibilityof the system. So, when the speculative attackon the pound revealed that the establishedexchange rate parities actually had lost theircredibility, the situation had to be reevaluated.The costs of defending the established paritieshad increased and it was quite possible thatmonetary authorities would regard these costsas being too high.

The British Experience

The main characteristic of the defense of thepound in September 1992 was the reluctance ofBritish monetary authorities to raise interestrates. What are the implications of this policyfor speculative currency attacks?~°Consider thegeneral case with a pegged exchange rate andselling pressure against the home currency. Solong as interest rates are free to move, competi-tion among speculators for expected profitsfrom an attack on the home currency drives updomestic interest rates. If the central bank pre-vents these interest rates from rising, that brakeon the demand for foreign exchange disappears.As a result, the central hank will have to absorbthe larger demand for foreign exchange. In theend, the central bank, by pegging the interestrate, offers the market a favorable opportunityfor a run on Britain’s reserves. Investors mayspeculate at very low costs, and the speculativecurrency attack thus easily may involve hugeamounts of funds.

A second characteristic of the British episodewas the government’s borrowing on the interna-tional capital market to increase foreign exchange

30Goldstein et al. (1993) first examined this extension of thebasic model.

FEDERAL RESERVE BANK OF St LOUIS

55

change reserves. As emphasized above, aspeculative attack occurs when the shadowexchange rate is equal to or below the currentpegged exchange rate. The size of the fot-eignexchange reserves, in turn, has an effect on theshadow exchange rate. Since a run on foreignexchange reserves jeduces the domestic moneysupply (assuming the effect is not sterilized), themoney supply reduction associated with runningout of a larger stock of foreign reserves is alsolarger. The potentially larger reduction in thedomestic money supply, in turn, raises theshadow exchange rate.

Another device to postpone speculative cur-rency attacks is capital controls. While Britaindid not use them at all in 1992, the ERM crisisin September 1992 was the first, since virtuallyall capital controls in the EC had been removed.Thus, it may be useful to take a look at howcapital controls work in a speculative currencyattack. The simplest way to model capital con-troLs is to treat them like a tax on foreigninterest earnings. lb simplify the account, letthe starting point he a situation in which thefundamentals aie in order: i.e., no chronic fiscaldeficit or other influence is causing a gradualdepletion of the central bank’s foreign exchangereserves. The pre-tax foreign interest rate con-tinues to he assumed as constant throughoutthe analysis.

Since a speculative attack takes place whenthe shadow exchange rate is equal to or belowthe current pegged exchange i-ate, we direct ourattention again to the effects of the instrumenton the shadow exchange rate. A tax on foreigninterest earnings reduces the net return onforeign assets. As a result, an excess supply offoreign currency emerges at the current ex-change rate. Since the exchange rate is pegged,the excess supply must he absorbed by the cen-tral bank. This leads to highet- foreign exchangereserves, a higher money supply, and a reduc-tion in the domestic interest rate (reflecting thereduced level of the net return rate on foreignassets). The increase in foreign exchange

reserves, in turn, raises the shadow exchangerate in much the same way as in the example inwhich reserves are increased by borrowing. Atax on foreign interest earnings, by pushing upthe shadow exchange rate, may postpone aspeculative attack. To put it another way, theremoval of capital controls in the EC removed ashelter for weak ERM currencies.3’

Over’all, the distaste of British monetaryauthorities for allowing short-teim interest ratesto rise made the defense of the pound in Sep-tember 1992 more difficult. The effects onspeculation were particularly grave since therewere no restrictions on capital movements.Borrowing foreign exchange reserves by theauthorities—short of unliniited borrowing—was no serious substitute under these circum-stances.

CONCLUSIONSThe near collapse of the ERM in 1992-93

reflected the vulnerability of pegged exchangerate systems. This feature of pegged exchangerates is hardly new. Standard theory in interna-tional macroeconomics teaches that monetaryautonomy and pegged exchange m-ates are incom-patible in the absence of capital controls. Diver-gent econonuc forces or simple political eventsmay trigger a speculative attack, leading to thecollapse of the pegged exchange rate.

For policymakers, the possibility that specula-live currency attacks may be self-fulfilling isparticularly troublesome. In Europe, proponentsof pegged exchange rates have argued for yearsthat exchange rate pegging to the mark providesa way to import the reputation of the Bundes-hank and get a credible anchor for monetarypolicy. For obvious reasons, this approach had aspecial appeal to countries lacking a crediblemonetary policy. Yet the argument is less con-vincing if speculative attacks are self-fulfillingand the credibility of a country’s exchange ratecommitment can vanish as quickly and unex-pectedly as it did in September 1992.

310f course, capital controls are not as efficient as true taxeson foreign exchange. More importantly, capital controlstypically are not introduced when there is no pressure onforeign exchange reserves. Nevertheless, the analysis hereclarifies that capital controls can reduce the prevailing ex-cess demand for foreign currency, boosting foreign ex-change reserves and the shadow exchange rate. Thisanalysis ignores the reduction in incentives to invest in acountry that imposes capital controls as well, and this in-fluence coutd also bode ill for any actual boost in theshadow price.

56

A necessary condition for such an attack tooccur is that the markets expect the centralbank to shift policy as a result of the attack. Ifthe markets have reasons to believe that a coun-try will relax monetary policy once a specula-tive attack has exhausted the central bank’sreserves, an attack is more likely. In the case ofBritain, a persistent recession prepared the wayfor such beliefs. Uncertainties about the pros-pects for EMU and the reluctance of Britishauthorities to allow short-term interest rates torise in defense of the pound subsequently ac-celerated the attack and reinforced a realign-ment of the pound. In short, the United Kingdomcould not convince the markets of its commit-ment to a fixed exchange rate. This credibility isan essential factor in maintaining an effectiveexchange regime.

REFERENCESAgénor, Pierre-Richard, Jagdeep S. Bhandari and Robert

P. Flood. “Speculative Attacks and Models of Balance ofPayments Crises?’ IMF Staff Papers (June 1992),pp. 357—94.

Bank of England Quarterly Bulletin (various issues, 1992).Batten, Dallas S., Michael P Blackwell, ln-Su Kim, Simon E.

Nocera and Yuzuru Ozeki. “The Conduct of MonetaryPolicy in the Malor Industrial Countries: Instruments andOperating Procedures?’ Occasional Paper Na 70,International Monetary Fund (July 1990).

Belongia, Michael T., and K. Alec Chrystal. “The Pitfalls ofExchange Rate Targeting: A Case Study from the UnitedKingdom,” this Review (September/October 1990),pp. 15—24.

Blackburn, Keith, and Martin Sola. “Speculative CurrencyAttacks and Balance of Payments Crises?’ Journal ofEconomic Surveys (June 1993), pp. 119—44.

Edwards, Sebastian. Real Exchange Rates, Devaluation, andAdjustment (MIT Press, 1989).

Flood, Robert P., and Peter M. Garber. “Gold Monetizationand Gold Discipline?’ Journal of Political Economy (February1984a), pp. 90—107.

_______- “Collapsing Exchange-Rate Regimes: Some LinearExamples?’ Journal of International Economics (August1984b), pp. 1—13.

Frankel, Jeffrey, and Steven Phillips. “The EuropeanMonetary System: Credible at Last?” Working Paper Na3819, National Bureau of Economic Research (August 1991).

Fratianni, Michele, and JUrgen von Hagen. The EuropeanMonetary System and European Monetary Union (WestviewPress, 1992).

Giavazzi, Francesco, and Alberto Giovannini. LimitingExchange Rate Flexibility: The European Monetary System(MIT Press, 1989).

Goldstein, Morris, David Folkerts-Landau, Peter Garber,Liliana Rojas-Suárez and Michael Spencer. “InternationalCapital Markets: Part I. Exchange Rate Management andInternational Capital Flows?’ World Economic and FinancialSurveys, International Monetary Fund (April 1993).

Gros, Daniel, and Niels Thygesen. European MonetaryIntegration (Longman, 1992).

Krugman, Paul. “A Model of Balance-of-Payments Crisis?’Journal of Money, Credit, and Banking (August 1979),pp. 311-25.

Obstfeld, Maurice. “Rational and Self-Fulfilling Balance-of-Payments Crises?’ American Economic Review (March1986), pp. 72—81.

Organization for Economic Co-operation and Development.OECD Economic Surveys: United Kingdom (various issues).

Pringle, Robert, ed. “The Currency Crisis: A Seven PartSpecial Feature?’ Central Banking (Vol. 3, No. 2, autumn1992), pp. 12—21.

Rose, Andrew K. “European Exchange Rate CredibilityBefore the Fall: The Case of Sterling?’ Federal ReserveBank of San Francisco Weekly Letter (May 7, 1993).

_______ and Lars ED. Svensson. “Expected and PredictedRealignments: The FFIDM Exchange Rate During theEMS?’ Working Paper Na 3685, National Bureau ofEconomic Research (April 1991).

Svensson, Lars E. 0. “Assessing Target Zone Credibility:Mean Reversion and Devaluation Expectations in the ERM,1979—1992?’ European Economic Review (May 1993),pp. 763—94.

_______- “The Foreign Exchange Risk Premium in a TargetZone with Devaluation Risk,” Journal of InternationalEconomics (August 1992), pp. 21—40.

_______- “The Simplest Test of Target Zone Credibility?’ IMFStaff Papers (September 1991), pp. 655—65.

Ungerer, Horst, Owen Evans and Peter Nyberg. “TheEuropean Monetary System: The Experience, 1979-82,”Occasional Paper Na 19, International Monetary Fund(May 1983).

_______ Owen Evans, Thomas Mayer, and Philip Young.“The European Monetary System: Recent Developments?’Occasional Paper Na 48, International Monetary Fund(December 1986).

_______ Jouko J. Hauvonen, Augusto Lopez-Claros andThomas Mayer. “The European Monetary System:Developments and Perspectives?’ Occasional Paper Na 73,International Monetary Fund (November 1990).