BMGT428E Tax Avoidance, Tax Policy, and Tax Research - Course Recap

Upload

michael-welchCategory

view

214download

0

The Tax Policy Road Ahead

Jeff Kummer

Director of Tax Policy

Deloitte Tax LLP

March 23, 2010

2Copyright © 2009 Deloitte Development LLC. All rights reserved.

Agenda

Initial Observations

Healthcare Reform

“Must Do” Tax Legislation in 2009 2010

President’s FY2011 Tax Proposals

2010 and Beyond

3Copyright © 2009 Deloitte Development LLC. All rights reserved.

Initial Observations

– A changed tax policy environment in Washington

– Targeted tax increases at selected taxpayers will continue

– Healthcare reform status

– Industry fees focus

– Jobs and deficits driving agenda for 2010

Healthcare Reform

5Copyright © 2009 Deloitte Development LLC. All rights reserved.

Simple Math of Healthcare Reform

Concern about uninsured– Expected to increase from 45 to 54 million by 2019

Increasing health care costs– CBO predicts Medicare\Medicaid costs to rise from 4

percent of GDP to 12 percent by 2050

Capture cost savings through “efficiencies” to offset costs

6Copyright © 2009 Deloitte Development LLC. All rights reserved.

Key Healthcare Reform Tax ProposalsProposal House Senate White House

Surtax on upper income individuals

5.4 percent surtax on MAGIin excess of $1 million (jointfilers) and $500,000 (single)

No proposal No proposal

Excise tax on high value “Cadillac” plans

No proposal 40 percent excise tax on plans valued at $23,000 ($8,500 single) or higher beginning in 2013

40 percent excise tax on plans valued at $27,500 ($10,200 single) or higher beginning in 2018

HI wage tax increase

No proposal 0.9 percentage point HI wage tax increase for upper income individuals

Senate proposal plus 2.9 percent tax on unearned income

Codification of economic substance

40 percent strict liability penalty for transactions lacking economic substance

No proposal Includes House proposal

Corporate information reporting

File 1099s on payments exceeding $600

Same Same

7Copyright © 2009 Deloitte Development LLC. All rights reserved.

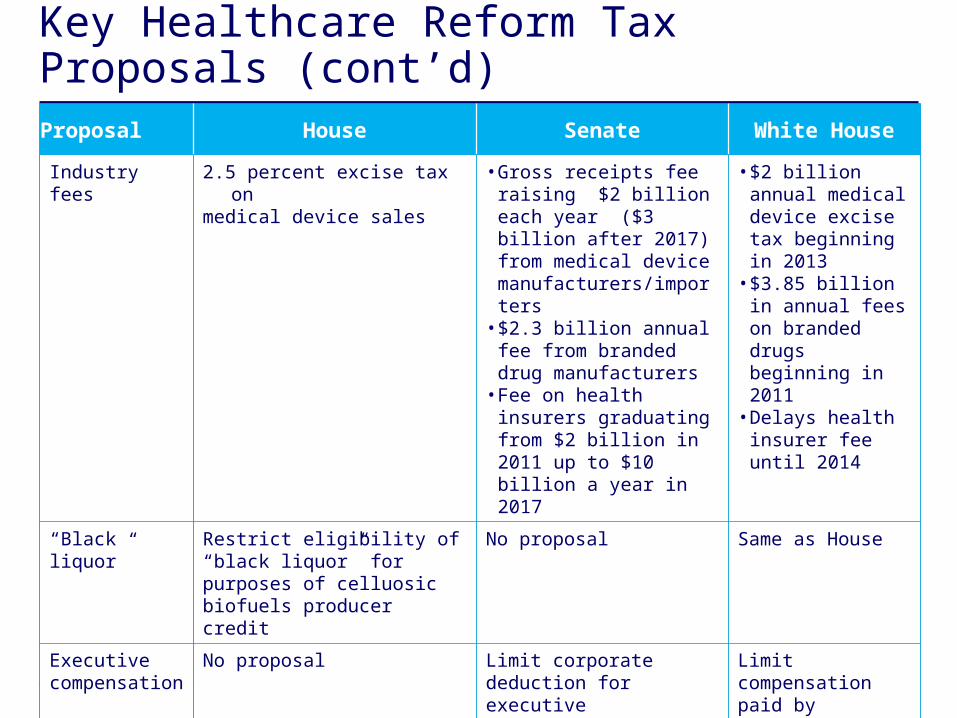

Key Healthcare Reform Tax Proposals (cont’d)Proposal House Senate White House

Industry fees 2.5 percent excise tax on medical device sales

• Gross receipts fee raising $2 billion each year ($3 billion after 2017) from medical device manufacturers/importers

• $2.3 billion annual fee from branded drug manufacturers

• Fee on health insurers graduating from $2 billion in 2011 up to $10 billion a year in 2017

• $2 billion annual medical device excise tax beginning in 2013

• $3.85 billion in annual fees on branded drugs beginning in 2011

• Delays health insurer fee until 2014

“Black liquor” Restrict eligibility of “black liquor” for purposes of celluosic biofuels producer credit

No proposal Same as House

Executive compensation

No proposal Limit corporate deduction for executive compensation to $500,000

Limit compensation paid by insurance companies

Other revenue raisers

Repeal worldwide interest allocationLimit treaty benefits

“Must Do” Tax Legislation in 2009 2010

9Copyright © 2009 Deloitte Development LLC. All rights reserved.

Tax Extenders

– Expired at end of 2009

• R&E tax credit

• Subpart F active financing exemption

• CFC look-through treatment

• 15 yr. recovery period for leasehold improvementsand restaurant property

• State sales tax deduction

• New Markets Tax Credit

– Senate and House have approved bills, but disagreement exists over revenue offsets

10Copyright © 2009 Deloitte Development LLC. All rights reserved.

Estate Tax

– Estate tax rate is now zero

– Political battle over rate and exemption level

– Taxwriters plan on retroactive reinstatement to January 1, 2010

– Possibility: freeze at 2009 levels

• Exemption: $3.5 million per person($7 million per couple)

• Rates: 18 to 45 percent

President’s FY 2011 Tax Proposals

12Copyright © 2009 Deloitte Development LLC. All rights reserved.

Tax Incentives

– Permanent R&E tax credit

– Extend certain other expiring tax provisions through 2011

– Bonus depreciation and small business expensing

– Remove cell phones from listed property

– Additional tax credits for advanced energy manufacturing projects

13Copyright © 2009 Deloitte Development LLC. All rights reserved.

General Business Tax Increases

– Repeal LIFO and LCM inventory accounting methods

– International tax reforms

– Reinstate Superfund taxes

– Repeal of fossil fuel tax incentives

– Worker classification

14Copyright © 2009 Deloitte Development LLC. All rights reserved.

Individual Income Taxes

– Ordinary income rates

• Reinstate pre-2001 rates above $200,000 single,$250,000 married

• Permanently extend other rates

• Reinstate hidden rates (PEP & Pease)

– Capital gains and qualified dividends rate

• 20 percent rate in brackets above $200,000 singleand $250,000 married

– Cap itemized deductions

– Estate tax changes

– AMT: extend and index the “patch”

15Copyright © 2009 Deloitte Development LLC. All rights reserved.

16Copyright © 2009 Deloitte Development LLC. All rights reserved.

Climate Change Legislation

– President has made climate change a priority

– House approved cap and trade system with roughly 85 percent free allowances and 15 percent auction

– Senate versions could go with cap and dividend

– EPA regulation of GHGs could drive action

– A number of tax issues could arise

• What is the character of the asset?

• When is income realized and recognized?

• Tax treatment of offsets

2010 and Beyond

18Copyright © 2009 Deloitte Development LLC. All rights reserved.

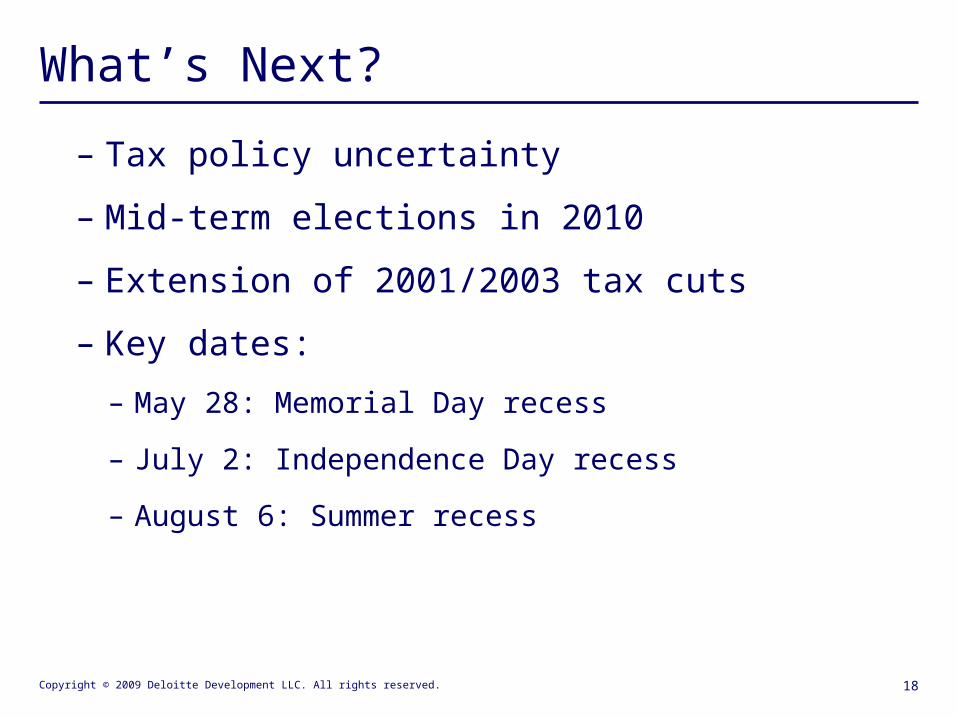

What’s Next?

– Tax policy uncertainty

– Mid-term elections in 2010

– Extension of 2001/2003 tax cuts

– Key dates:

– May 28: Memorial Day recess

– July 2: Independence Day recess

– August 6: Summer recess

19Copyright © 2009 Deloitte Development LLC. All rights reserved.

Outlook

– Individual taxes going up: not a matter of if, but when and how high

– PAYGO rules provide baseline relief for middle class taxpayers

– Focus on “anti abuse” and compliance revenue raisers

– President's tax reform panel and Deficit Commission

– Corporate tax reform?

– Nature of the tax code is unsustainable

20Copyright © 2008 Deloitte Development LLC. All rights reserved.

Questions?

Jeff Kummer

202.220.2148

21Copyright © 2008 Deloitte Development LLC. All rights reserved.

About DeloitteDeloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries.

Copyright © 2008 Deloitte Development LLC. All rights reserved.