The Status and Future of EVs - NCPA

15

The Status and Future of EVs Sandra Berg, Vice Chair, California Air Resources Board Daniel Sperling, CARB and UC Davis September 25, 2019 Squaw Valley, California 1

Transcript of The Status and Future of EVs - NCPA

The Status and Future of EVs

Sandra Berg, Vice Chair, California Air Resources Board

Daniel Sperling, CARB and UC Davis

September 25, 2019

Squaw Valley, California

1

Electric Utility Transportation Electrification

2

Mobile Source Emissions are Significant

3

Areawide4%

Stationary13%

Light-Duty Vehicles

18%

Heavy-Duty Vehicles

35%Other Mobile

Sources30%

South Coast Air Basin NOx Emissions (2017)

Recycling and Waste

3%

High GWP5%

Industrial21%

Electric Power16%

Residential & Commercial

10%

Agriculture9%

Light-Duty Vehicles

29%

All Other Transportation

7%

California GHG Emissions(2017)

Mobile

Sources

>80%

Mobile

Sources

~35%

Mobile sources represent ~50% of GHG inventory

when including emissions from fuel production

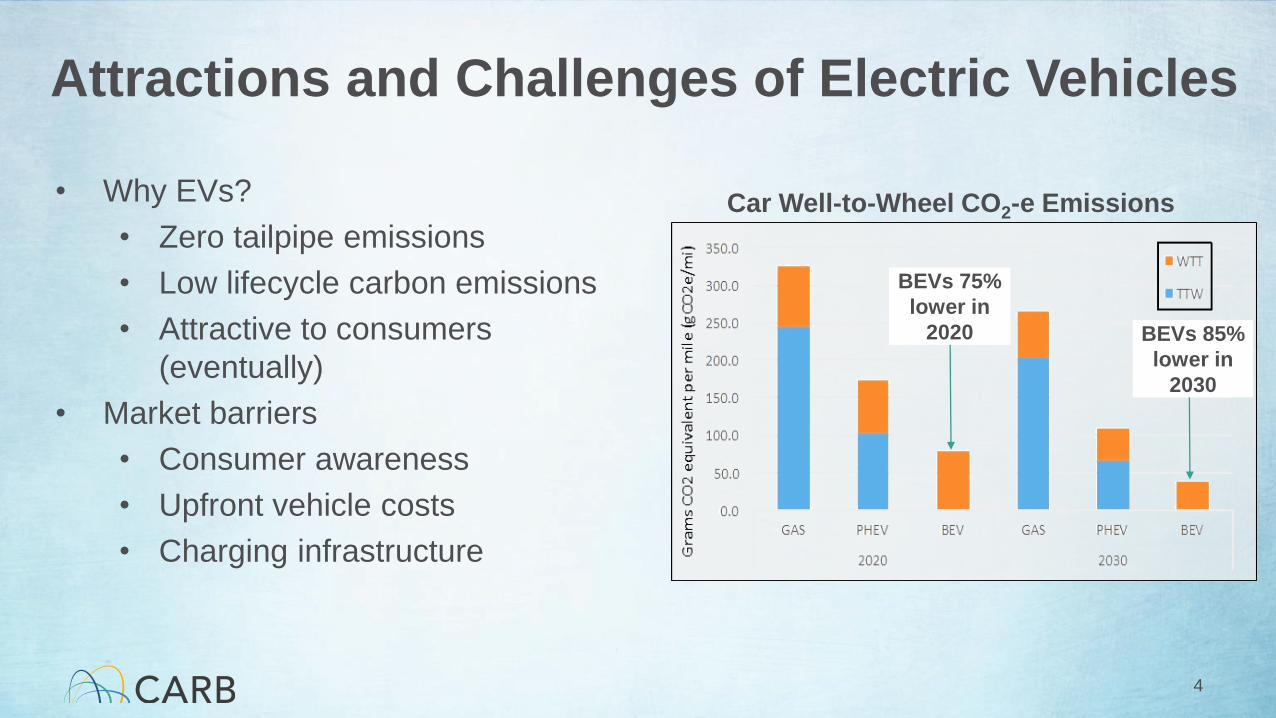

BEVs 75%

lower in

2020 BEVs 85%

lower in

2030

Car Well-to-Wheel CO2-e Emissions

Attractions and Challenges of Electric Vehicles

• Why EVs?

• Zero tailpipe emissions

• Low lifecycle carbon emissions

• Attractive to consumers

(eventually)

• Market barriers

• Consumer awareness

• Upfront vehicle costs

• Charging infrastructure

4

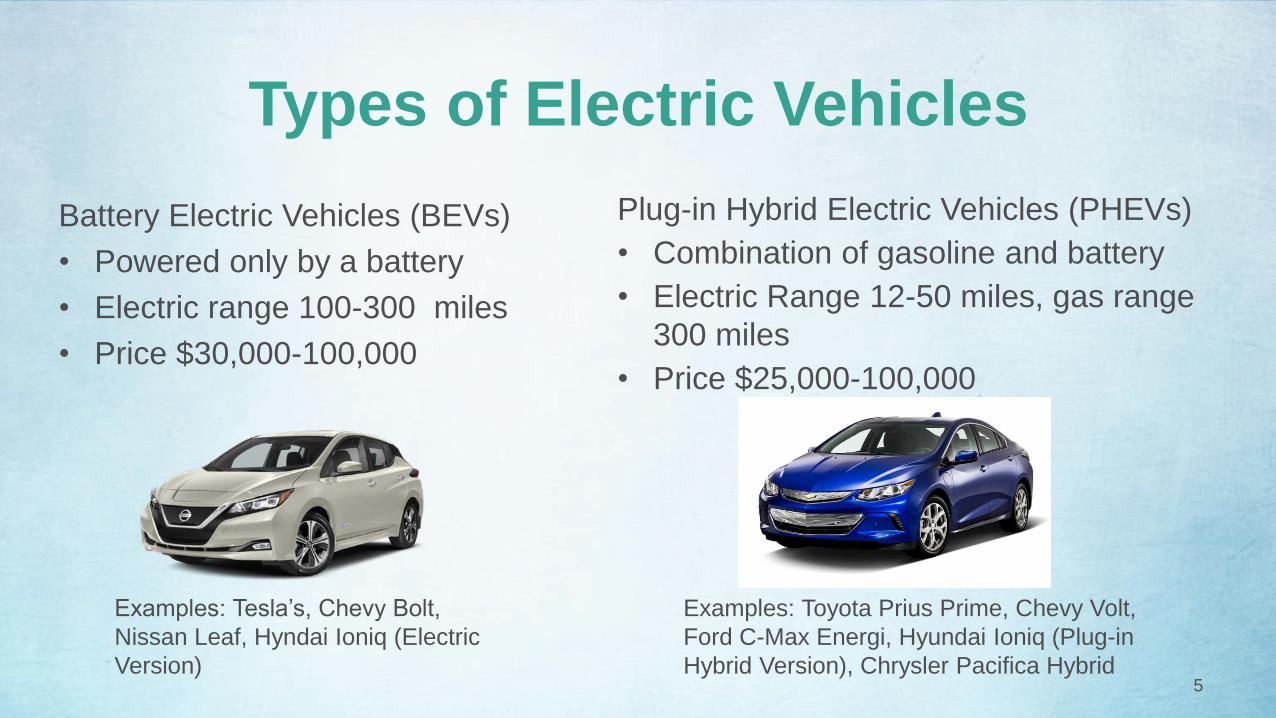

Types of Electric Vehicles

Battery Electric Vehicles (BEVs)

• Powered only by a battery

• Electric range 100-300 miles

• Price $30,000-100,000

Plug-in Hybrid Electric Vehicles (PHEVs)

• Combination of gasoline and battery

• Electric Range 12-50 miles, gas range

300 miles

• Price $25,000-100,000

5

Examples: Tesla’s, Chevy Bolt,

Nissan Leaf, Hyndai Ioniq (Electric

Version)

Examples: Toyota Prius Prime, Chevy Volt,

Ford C-Max Energi, Hyundai Ioniq (Plug-in

Hybrid Version), Chrysler Pacifica Hybrid

Model Availability

03 October 2019

6

0

100

200

300

400

500

600

Mo

dels

fo

r S

ale

Global

0

10

20

30

40

50

60

Mo

dels

fo

r S

ale

US

ZEVs Gaining Momentum & Market Share

8Source: Auto Alliance Sales Dashboard for 2011 through December 2018

0

1

2

3

4

5

6

7

8

9

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2011 2012 2013 2014 2015 2016 2017 2018

An

nu

al M

ark

et

Sh

are

(%

)

Ve

hic

le S

ale

s

Annual California Light-Duty ZEV and PHEV Sales

Total ZEV & PHEV Sales Market Share

Global Plug-in Electric Vehicle Sales

03 October 2019

9

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

An

nu

al

Sale

s

China USA Norway Germany UK

France Japan Canada Korea Sweden

Netherlands Belgium Spain Italy Other

ZEV Infrastructure is Critical

EV Charging

• AB 8 investments

• Electrify America Volkswagen investments

• Go-Biz and CEC support for local government planning

• Building standards for new construction

• Electric utility transportation electrification

10

ZEV Consumer Incentive Programs

• Federal ZEV $7,500

• CA State Rebate

• $5,000 – Fuel Cell

• $2,500 – BEV

• $1,500 – PHEV

• Clean Vehicle Assistance Program

• Clean Cars 4 All

• Regional Air District ZEV Grants

• Clean Fuel Reward (CFR) Program (2020)

11

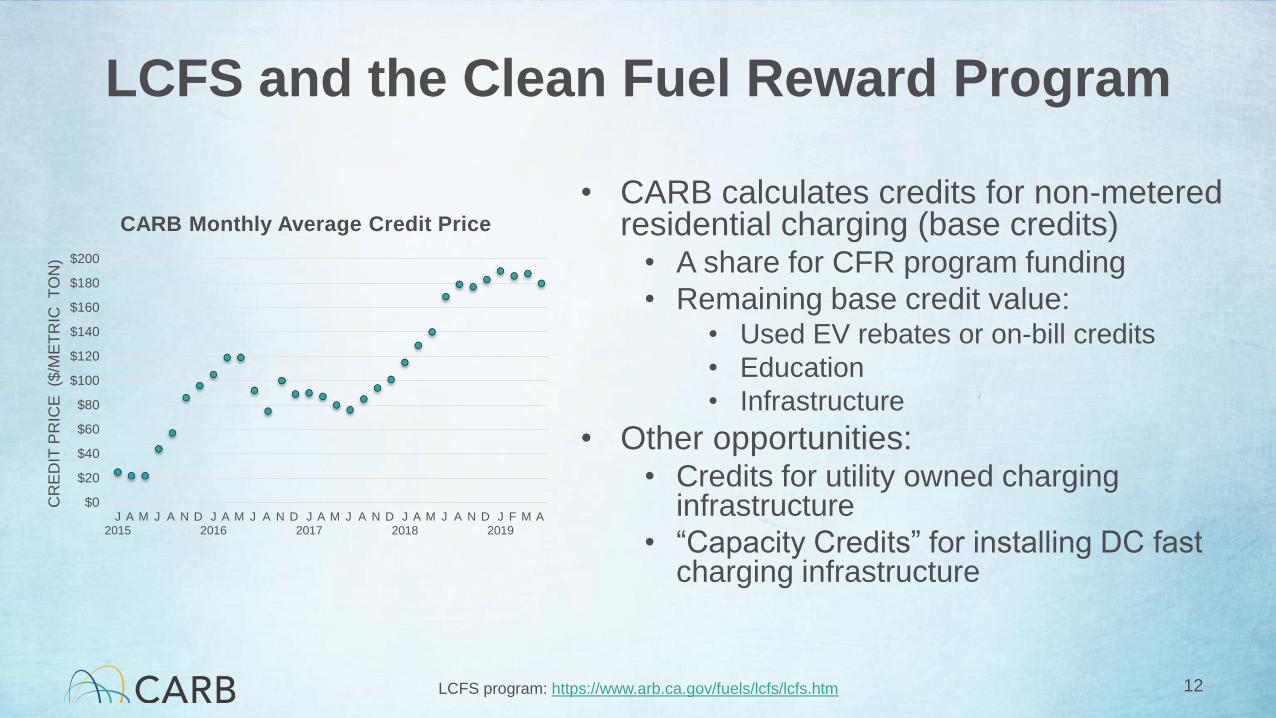

LCFS and the Clean Fuel Reward Program

• CARB calculates credits for non-metered residential charging (base credits)

• A share for CFR program funding

• Remaining base credit value: • Used EV rebates or on-bill credits

• Education

• Infrastructure

• Other opportunities: • Credits for utility owned charging

infrastructure

• “Capacity Credits” for installing DC fast charging infrastructure

12LCFS program: https://www.arb.ca.gov/fuels/lcfs/lcfs.htm

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

J2015

A M J A N D J2016

A M J A N D J2017

A M J A N D J2018

A M J A N D J2019

F M A

CR

ED

IT P

RIC

E ($

/ME

TR

IC T

ON

)

CARB Monthly Average Credit Price

And Trucks and Buses Too

• Buses

• Gradual transition to 100% ZEBs by

2040

• Zero Emission Airport Shuttle

• 100% zero emission by end of 2035

• Medium and Heavy Duty Trucks

next….

13

14

Regulations

Help ensure ZEVs are produced and that

fleets use them

Incentives

Help encourage consumers and fleets to purchase and test

ZEVs

Supporting Programs

Help provide fueling infrastructure,

education, and best practices

ZEV Programs