The State of Managed Services 2014 Final -...

15

The State of Managed Services 2014 By George Humphrey, Senior Director, Research, Managed Services, TSIA

Transcript of The State of Managed Services 2014 Final -...

The State of Managed Services2014

By George Humphrey, Senior Director, Research, Managed Services, TSIA

A TSIA Member Publication

The State of Managed Services: 2014 by George Humphrey

INTRODUCTION

At the end of 2013, TSIA published a book titled B4B: How Technology and Big Data Are Reinventing the Customer-Supplier Relationship.1 The book overviews several trends that are impacting the business models of technology companies.

• Growing importance of service revenues. As technology markets mature, the revenue streams become more service intensive. This naturally occurs as product margins compress and product revenues face pressure. Service revenues begin playing a greater role to drive both top-line and bottom-line growth of product companies.

• Changing economic engines. Technology companies have historically made their money by selling technology assets to customers and attaching traditional services like support contracts and technical training. With the advent of subscription-based consumption models, the traditional revenue streams of technology companies are now under increased pressure. As customers switch from buying to renting, product transactions disappear and traditional product support contracts designed to secure uptime are not attached. These changes are impacting the economic engines of product companies.

• Emergence of Level 3 and Level 4 service offerings. In the book B4B, we define four distinct levels of technology solution providers. For a comprehensive definition of these four levels, please refer to the book. Here is a shorthand definition for the four types of technology providers:

- Level 1: Sells products. - Level 2: Sells products plus classic product-attach services to implement and support

those products.

1 Wood, J.B., Todd Hewlin, and Thomas Lah. 2013. B4B: How Technology and Big Data Are Reinventing the Customer-Supplier Relationship. San Diego, CA: Point B, Inc.

EXECUTIVE INSIGHT

TSIA-EI-14-003

February 7, 2014

MANAGED SERVICES

2

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

- Level 3: Sells product, product-attach services, plus services designed to help customers operate and optimize the usage of technology solutions.

- Level 4: Sells business outcomes to customers that are enabled by technology capabilities.

TSIA is seeing more product companies that historically only offered traditional product-attach services (Level 2 offers) that are now experimenting with services that help customers accelerate their adoption of technology (Level 3 offers) or they commit to helping customers achieve specific business outcomes (Level 4 offers). This shift in the service portfolio is amplifying the shift in the economic engines of product companies.

• Commoditization of Level 2 offers. One of the reasons product companies are experimenting with Level 3 and Level 4 service offers is because the value proposition of traditional product-attach services is diminishing. Customers are less and less excited by services that are designed to implement and support a product as opposed to services that are designed to help achieve specific business outcomes.

• Changing role of services. Finally, all of the above trends are significantly changing the role of embedded service organizations. Instead of simply following the product sale, service organizations are being called upon to create service offerings that drive ongoing consumption and drive business outcomes for customers. Service organizations are also being called upon to drive account retention and expansion.

These general industry trends are clearly impacting the world of managed services.

WHY MANAGED SERVICES—TANGIBLE PROOF OF CONSUMPTION ECONOMICS

AND B4B

The Service 50 Index

Whenever we do a briefing for managed services, we feel it’s important to help set the context for what is happening in the market that is driving the growth and adoption of managed services. There are a number of factors, but suffice it to say it’s the perfect storm.

There is a disturbing trend in the overall tech market that we see as evidenced through the Service 50 Index. The Service 50 is a quarterly snapshot of the revenue and profitability performance of the technology industry. TSIA aggregates the financial performance of these 50 companies from the public record. We identify service revenue and profitability trends, and provide critical observations based on the current quarterly update of 50 of the largest global providers of technology services.

3

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

It is often said, “A picture paints a thousand words.” Figure 1 is a graphical depiction of what has been happening in the technology market since Q1 2011.

Figure 1: Service 50 Trend Since Q1 2011

There is a major trend of overall technology revenues declining. This is followed by two minor trends: The product revenues, hardware and software, are declining. The services revenues have been growing. The fastest growing service line among professional services, education services, support services, field services, and managed services is managed services. These trends support the overall theory of a shift in buying behaviors for technology solutions, with managed services being the most desired technology procurement model. These are the trends that we predicted in Consumption Economics: The New Rules of Tech2 and are the basis of the assertions in B4B.

The net result is that many companies are now starting to realize that a managed service play is no longer a “nice to have” part of the portfolio. It is a requirement and critical to the long-term health and evolution of a technology company.

MANAGED SERVICES: PROFITABLE GROWTH ENGINE

Many technology-centric companies resist investing in managed services mostly due to FUD (fear, uncertainty, and doubt). The reality is that most senior executives in technology companies don’t know what they don’t know about managed services. They have many reasons, or excuses, not to offer

2 Wood, J.B., Todd Hewlin, and Thomas Lah. 2011. Consumption Economics: The New Rules of Tech. San Di-ego: Point B, Inc.

4

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

Services Gross Margin

% of Rev from Svcs

Profitability (OI)

Revenue Growth Se

rvic

e 50

% of Rev from Svcs

Profitability (OI)

Revenue Growth

Services Gross Margin

Clo

ud 2

0

MS Rev Renewal Rate

Profitability (OI)

Revenue Growth

MS Gross Margin M

S B

ench

mar

k

managed services: we don’t have the investment dollars required, we don’t want to compete with our channel, it will be dilutive to the overall profits of the company, managed services bundled with product will cannibalize our revenues, and so on. Traditional tech, both hardware and software, is continuing to commoditize. Technology margins are continuing to shrink. Though there is evidence to support the concern of lower gross margins, today’s managed services companies are seeing both healthy growth and healthy gross margins, as illustrated in Figure 2.

Figure 2: Dashboard: Service 50 Index, Cloud 20 Index, Managed Services Index

ACCELERATING GROWTH

One of the most valuable elements of TSIA membership is the ability to benchmark the performance of your services business. For managed services members we do this by collecting data from all aspects of their company, including their corporate profile, services organization KPIs, managed services KPIs, and deep details on over 50 different key managed services practices. This not only allows us to take the pulse of the MS market, it also allows us to run hundreds of correlations between practices and KPIs to understand what processes, structures, and activities drive the best results from real companies. This allows members to learn from the success of others and to avoid costly and sometimes catastrophic mistakes.

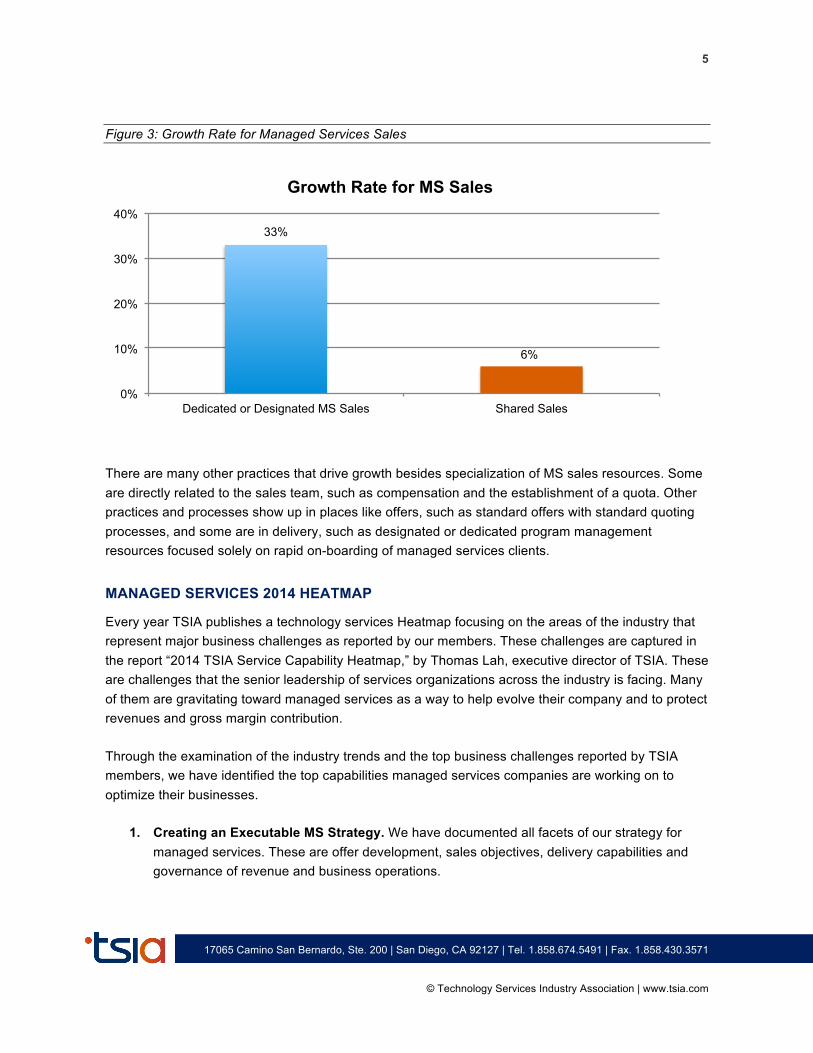

For example, should managed services be sold by the general sales team that sells products, or should a team of designated managed services sales resources be used? Through benchmark analysis, we can see that either a dedicated or a designated sales team has a dramatically positive effect on the growth rate of MS contracts, as shown in Figure 3.

5

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

33%

6%

0%

10%

20%

30%

40%

Dedicated or Designated MS Sales Shared Sales

Growth Rate for MS Sales

Figure 3: Growth Rate for Managed Services Sales

There are many other practices that drive growth besides specialization of MS sales resources. Some are directly related to the sales team, such as compensation and the establishment of a quota. Other practices and processes show up in places like offers, such as standard offers with standard quoting processes, and some are in delivery, such as designated or dedicated program management resources focused solely on rapid on-boarding of managed services clients.

MANAGED SERVICES 2014 HEATMAP

Every year TSIA publishes a technology services Heatmap focusing on the areas of the industry that represent major business challenges as reported by our members. These challenges are captured in the report “2014 TSIA Service Capability Heatmap,” by Thomas Lah, executive director of TSIA. These are challenges that the senior leadership of services organizations across the industry is facing. Many of them are gravitating toward managed services as a way to help evolve their company and to protect revenues and gross margin contribution.

Through the examination of the industry trends and the top business challenges reported by TSIA members, we have identified the top capabilities managed services companies are working on to optimize their businesses.

1. Creating an Executable MS Strategy. We have documented all facets of our strategy for managed services. These are offer development, sales objectives, delivery capabilities and governance of revenue and business operations.

6

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

2. MS Specific Financial Model. We have established a detailed financial plan in alignment with GAAP for the MS business.

3. MS Organization Structure. We have defined and documented an organizational structure that is optimized to obtain our strategic goals.

4. MS Sales Optimization. We have a strong understanding of what is required to sell managed services, including skills specialization and key compensation models.

5. MS Key Performance Metrics. We have established measurable and obtainable measurements to identify strong performance as well as areas requiring improvement.

6. Go-To-Market Model (Direct and Channel). We have established a go-to-market model that aligns with the corporate distribution strategy and is also conducive to successful attainment of our managed services objectives.

7. Standard MS Offers. Our managed services offers have been packaged in a way that is easy to consume for our clients and easy to sell for our sales representatives.

8. Scalable Delivery Operations. We are investing in process optimization and skills enhancement to continue to grow our MS business without impacting profitability or client satisfaction.

9. MS Specific Tools and Technologies. We are investing in tools and technologies to drive automation in fault isolation and resolution and to proactively and predictively prevent future incidents.

10. Governing and Growing Base Revenue. We are developing a client management team to monitor recurring MS revenues and to upsell new opportunities to our existing customers.

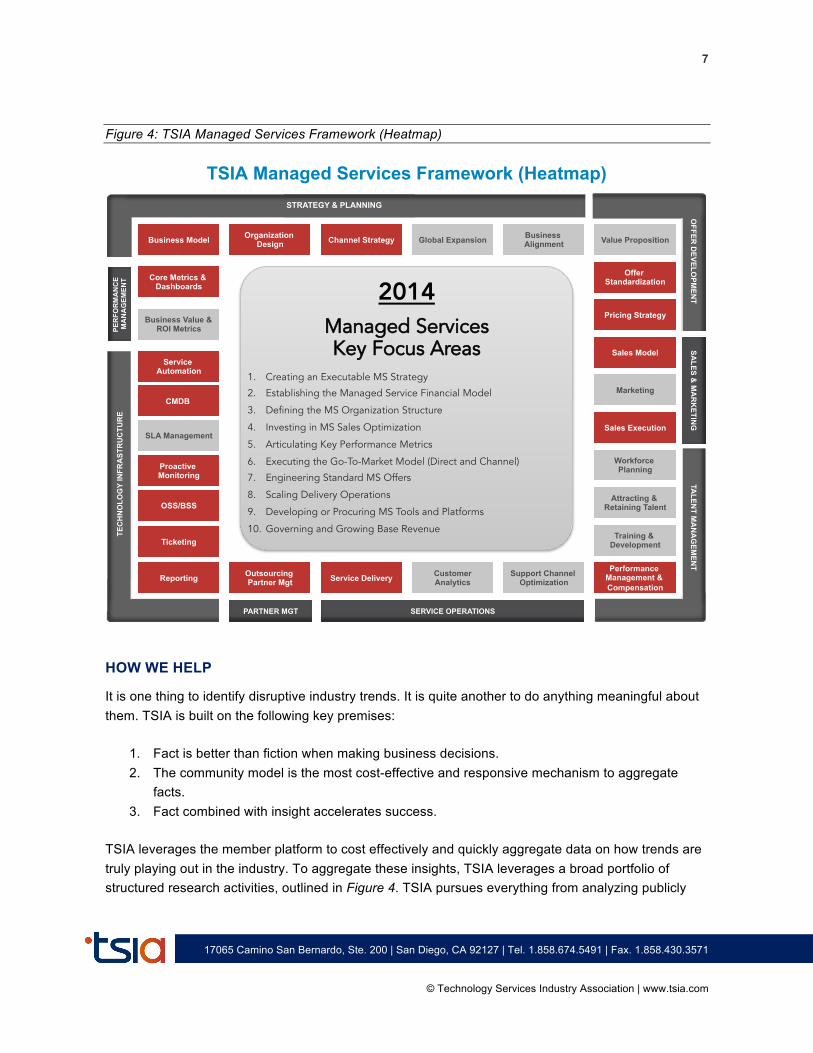

Figure 4 provides a graphical summary of these capabilities TSIA members are working to improve in 2014.

7

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

Managed Services Key Focus Areas

TSIA Managed Services Framework (Heatmap)

Business Model Organization Design Channel Strategy Global Expansion Business

Alignment Value Proposition

Core Metrics & Dashboards

Offer Standardization

Pricing Strategy

Sales Model

Business Value & ROI Metrics PE

RFO

RM

AN

CE

MA

NA

GEM

ENT

Service Automation

CMDB

SLA Management

Proactive Monitoring

OSS/BSS

Reporting

Marketing

Sales Execution

SALES &

MA

RK

ETING

Attracting & Retaining Talent

Training & Development

Performance Management & Compensation

Outsourcing Partner Mgt Service Delivery Customer

Analytics Support Channel

Optimization

SERVICE OPERATIONS

1. Creating an Executable MS Strategy

2. Establishing the Managed Service Financial Model

3. Defining the MS Organization Structure

4. Investing in MS Sales Optimization

5. Articulating Key Performance Metrics

6. Executing the Go-To-Market Model (Direct and Channel)

7. Engineering Standard MS Offers

8. Scaling Delivery Operations

9. Developing or Procuring MS Tools and Platforms

10. Governing and Growing Base Revenue

Workforce Planning

PARTNER MGT

OFFER

DEVELO

PMEN

T TA

LENT M

AN

AG

EMEN

T TE

CH

NO

LOG

Y IN

FRA

STR

UC

TUR

E

STRATEGY & PLANNING

Ticketing

2014

Figure 4: TSIA Managed Services Framework (Heatmap)

HOW WE HELP

It is one thing to identify disruptive industry trends. It is quite another to do anything meaningful about them. TSIA is built on the following key premises:

1. Fact is better than fiction when making business decisions. 2. The community model is the most cost-effective and responsive mechanism to aggregate

facts. 3. Fact combined with insight accelerates success.

TSIA leverages the member platform to cost effectively and quickly aggregate data on how trends are truly playing out in the industry. To aggregate these insights, TSIA leverages a broad portfolio of structured research activities, outlined in Figure 4. TSIA pursues everything from analyzing publicly

8

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

reported data to conducting in-depth service-line benchmarks, and conducting intimate focus groups to determine how service businesses are actually optimizing their business through industry disruptions.

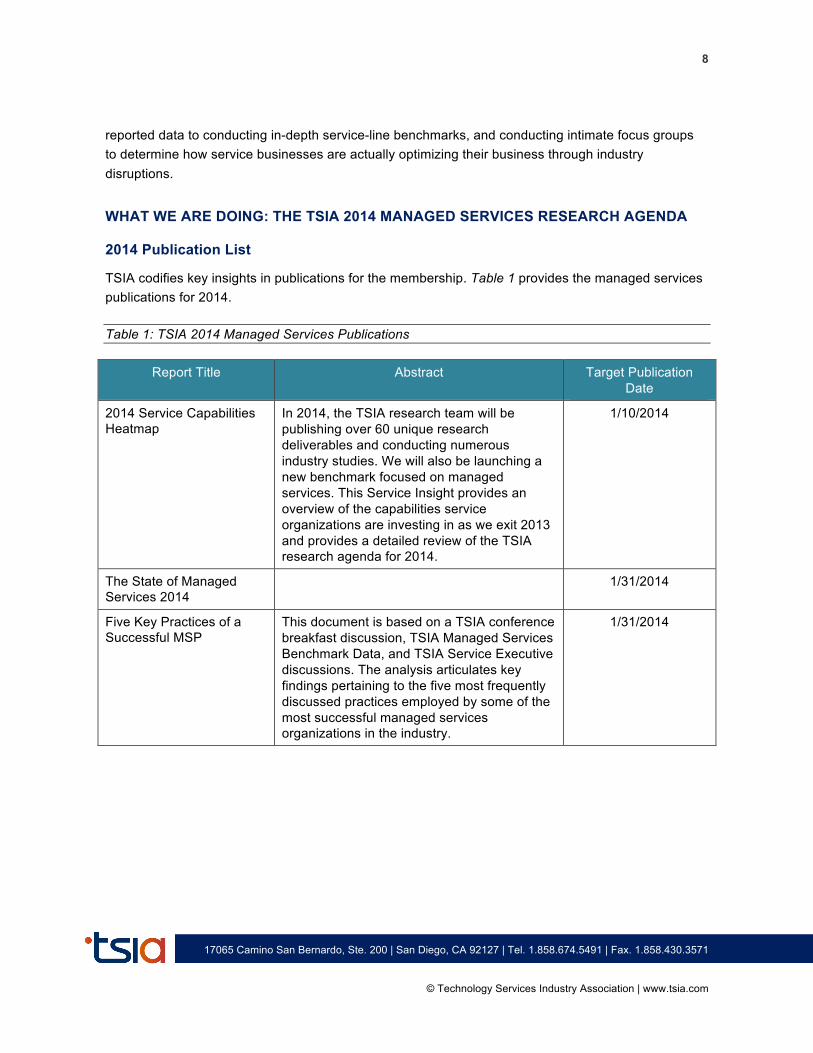

WHAT WE ARE DOING: THE TSIA 2014 MANAGED SERVICES RESEARCH AGENDA

2014 Publication List

TSIA codifies key insights in publications for the membership. Table 1 provides the managed services publications for 2014.

Table 1: TSIA 2014 Managed Services Publications

Report Title Abstract Target Publication Date

2014 Service Capabilities Heatmap

In 2014, the TSIA research team will be publishing over 60 unique research deliverables and conducting numerous industry studies. We will also be launching a new benchmark focused on managed services. This Service Insight provides an overview of the capabilities service organizations are investing in as we exit 2013 and provides a detailed review of the TSIA research agenda for 2014.

1/10/2014

The State of Managed Services 2014

1/31/2014

Five Key Practices of a Successful MSP

This document is based on a TSIA conference breakfast discussion, TSIA Managed Services Benchmark Data, and TSIA Service Executive discussions. The analysis articulates key findings pertaining to the five most frequently discussed practices employed by some of the most successful managed services organizations in the industry.

1/31/2014

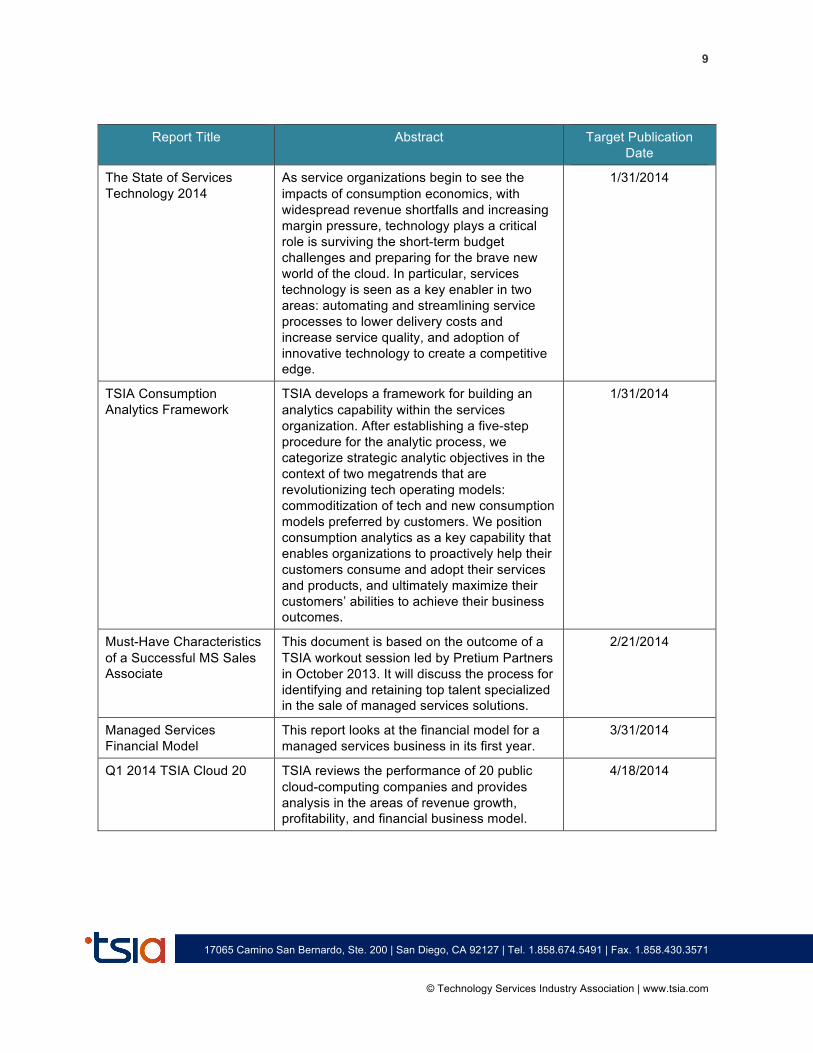

9

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

Report Title Abstract Target Publication Date

The State of Services Technology 2014

As service organizations begin to see the impacts of consumption economics, with widespread revenue shortfalls and increasing margin pressure, technology plays a critical role is surviving the short-term budget challenges and preparing for the brave new world of the cloud. In particular, services technology is seen as a key enabler in two areas: automating and streamlining service processes to lower delivery costs and increase service quality, and adoption of innovative technology to create a competitive edge.

1/31/2014

TSIA Consumption Analytics Framework

TSIA develops a framework for building an analytics capability within the services organization. After establishing a five-step procedure for the analytic process, we categorize strategic analytic objectives in the context of two megatrends that are revolutionizing tech operating models: commoditization of tech and new consumption models preferred by customers. We position consumption analytics as a key capability that enables organizations to proactively help their customers consume and adopt their services and products, and ultimately maximize their customers’ abilities to achieve their business outcomes.

1/31/2014

Must-Have Characteristics of a Successful MS Sales Associate

This document is based on the outcome of a TSIA workout session led by Pretium Partners in October 2013. It will discuss the process for identifying and retaining top talent specialized in the sale of managed services solutions.

2/21/2014

Managed Services Financial Model

This report looks at the financial model for a managed services business in its first year.

3/31/2014

Q1 2014 TSIA Cloud 20 TSIA reviews the performance of 20 public cloud-computing companies and provides analysis in the areas of revenue growth, profitability, and financial business model.

4/18/2014

10

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

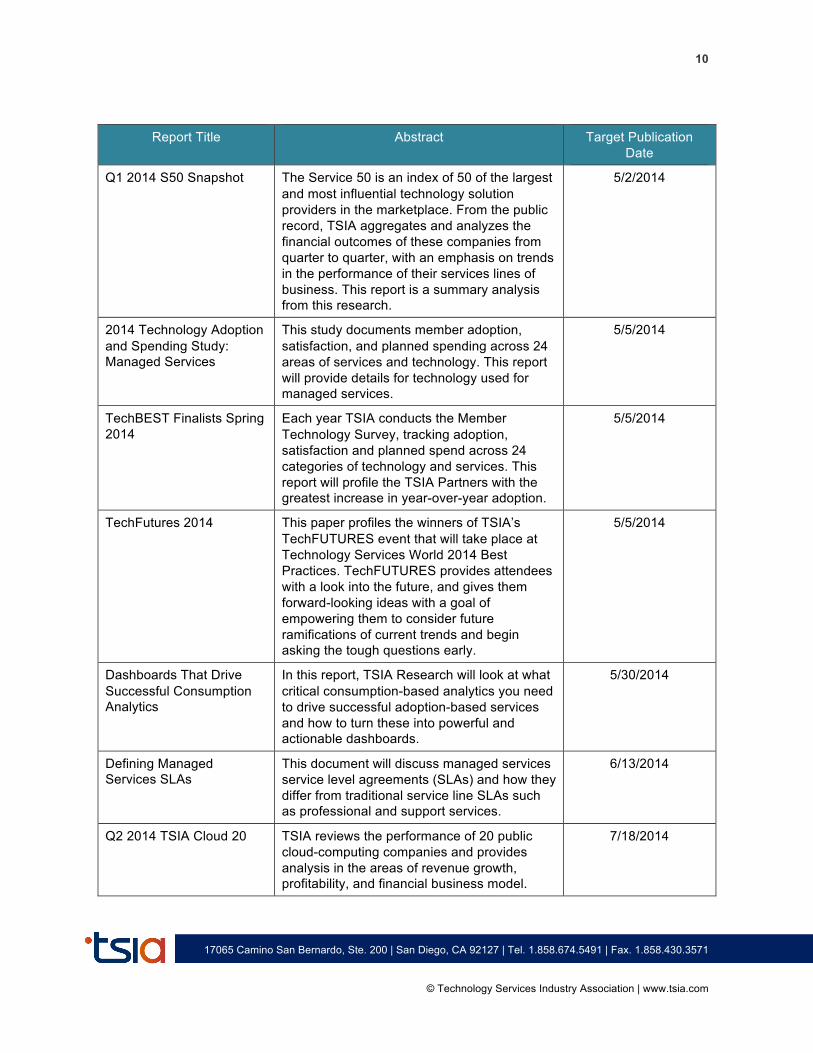

Report Title Abstract Target Publication Date

Q1 2014 S50 Snapshot The Service 50 is an index of 50 of the largest and most influential technology solution providers in the marketplace. From the public record, TSIA aggregates and analyzes the financial outcomes of these companies from quarter to quarter, with an emphasis on trends in the performance of their services lines of business. This report is a summary analysis from this research.

5/2/2014

2014 Technology Adoption and Spending Study: Managed Services

This study documents member adoption, satisfaction, and planned spending across 24 areas of services and technology. This report will provide details for technology used for managed services.

5/5/2014

TechBEST Finalists Spring 2014

Each year TSIA conducts the Member Technology Survey, tracking adoption, satisfaction and planned spend across 24 categories of technology and services. This report will profile the TSIA Partners with the greatest increase in year-over-year adoption.

5/5/2014

TechFutures 2014 This paper profiles the winners of TSIA’s TechFUTURES event that will take place at Technology Services World 2014 Best Practices. TechFUTURES provides attendees with a look into the future, and gives them forward-looking ideas with a goal of empowering them to consider future ramifications of current trends and begin asking the tough questions early.

5/5/2014

Dashboards That Drive Successful Consumption Analytics

In this report, TSIA Research will look at what critical consumption-based analytics you need to drive successful adoption-based services and how to turn these into powerful and actionable dashboards.

5/30/2014

Defining Managed Services SLAs

This document will discuss managed services service level agreements (SLAs) and how they differ from traditional service line SLAs such as professional and support services.

6/13/2014

Q2 2014 TSIA Cloud 20 TSIA reviews the performance of 20 public cloud-computing companies and provides analysis in the areas of revenue growth, profitability, and financial business model.

7/18/2014

11

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

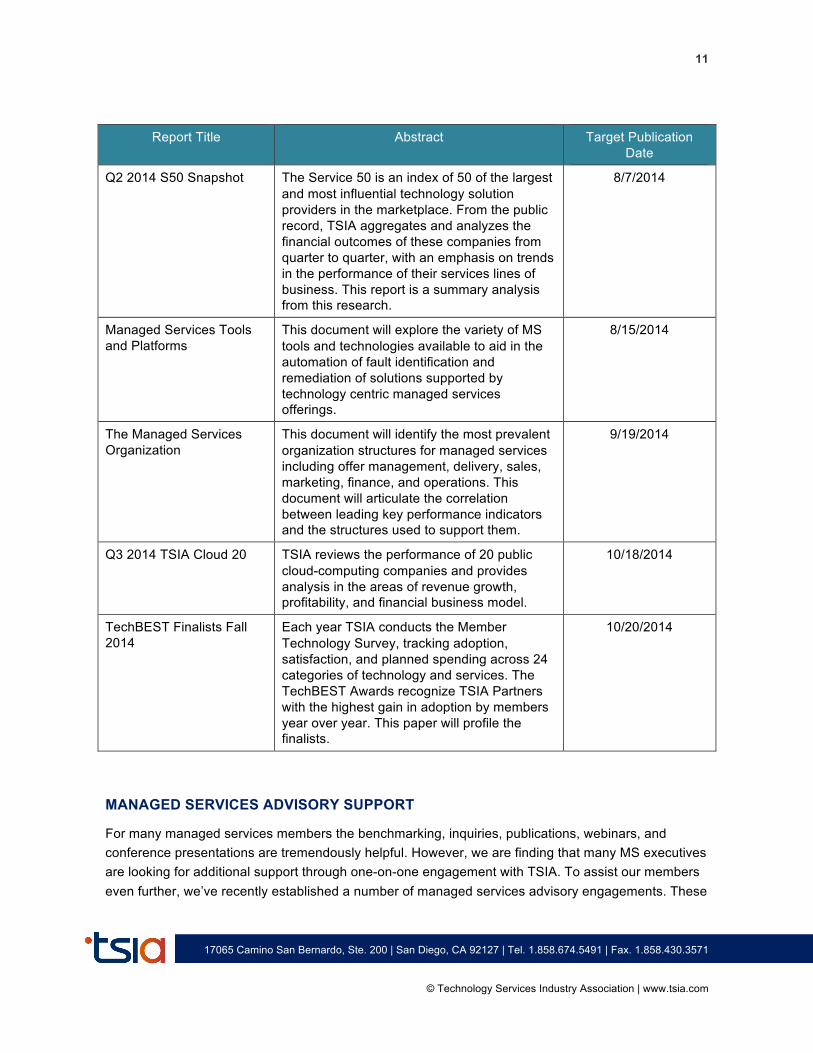

Report Title Abstract Target Publication Date

Q2 2014 S50 Snapshot The Service 50 is an index of 50 of the largest and most influential technology solution providers in the marketplace. From the public record, TSIA aggregates and analyzes the financial outcomes of these companies from quarter to quarter, with an emphasis on trends in the performance of their services lines of business. This report is a summary analysis from this research.

8/7/2014

Managed Services Tools and Platforms

This document will explore the variety of MS tools and technologies available to aid in the automation of fault identification and remediation of solutions supported by technology centric managed services offerings.

8/15/2014

The Managed Services Organization

This document will identify the most prevalent organization structures for managed services including offer management, delivery, sales, marketing, finance, and operations. This document will articulate the correlation between leading key performance indicators and the structures used to support them.

9/19/2014

Q3 2014 TSIA Cloud 20 TSIA reviews the performance of 20 public cloud-computing companies and provides analysis in the areas of revenue growth, profitability, and financial business model.

10/18/2014

TechBEST Finalists Fall 2014

Each year TSIA conducts the Member Technology Survey, tracking adoption, satisfaction, and planned spending across 24 categories of technology and services. The TechBEST Awards recognize TSIA Partners with the highest gain in adoption by members year over year. This paper will profile the finalists.

10/20/2014

MANAGED SERVICES ADVISORY SUPPORT

For many managed services members the benchmarking, inquiries, publications, webinars, and conference presentations are tremendously helpful. However, we are finding that many MS executives are looking for additional support through one-on-one engagement with TSIA. To assist our members even further, we’ve recently established a number of managed services advisory engagements. These

12

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

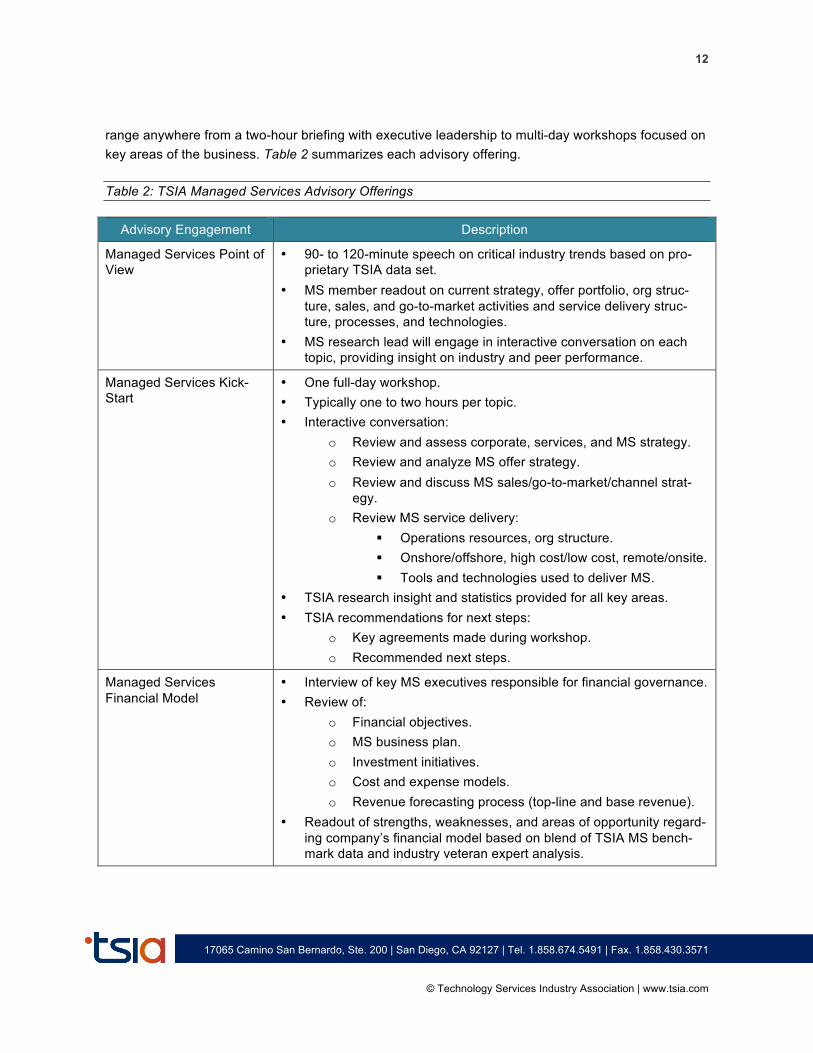

range anywhere from a two-hour briefing with executive leadership to multi-day workshops focused on key areas of the business. Table 2 summarizes each advisory offering.

Table 2: TSIA Managed Services Advisory Offerings

Advisory Engagement Description

Managed Services Point of View

• 90- to 120-minute speech on critical industry trends based on pro-prietary TSIA data set.

• MS member readout on current strategy, offer portfolio, org struc-ture, sales, and go-to-market activities and service delivery struc-ture, processes, and technologies.

• MS research lead will engage in interactive conversation on each topic, providing insight on industry and peer performance.

Managed Services Kick-Start

• One full-day workshop. • Typically one to two hours per topic. • Interactive conversation:

o Review and assess corporate, services, and MS strategy. o Review and analyze MS offer strategy. o Review and discuss MS sales/go-to-market/channel strat-

egy. o Review MS service delivery:

! Operations resources, org structure. ! Onshore/offshore, high cost/low cost, remote/onsite. ! Tools and technologies used to deliver MS.

• TSIA research insight and statistics provided for all key areas. • TSIA recommendations for next steps:

o Key agreements made during workshop. o Recommended next steps.

Managed Services Financial Model

• Interview of key MS executives responsible for financial governance. • Review of:

o Financial objectives. o MS business plan. o Investment initiatives. o Cost and expense models. o Revenue forecasting process (top-line and base revenue).

• Readout of strengths, weaknesses, and areas of opportunity regard-ing company’s financial model based on blend of TSIA MS bench-mark data and industry veteran expert analysis.

13

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

Advisory Engagement Description

Managed Services Offer Assessment

• Interview of key MS executives responsible for MS Strategy Exec, MS Sales Exec, and MS Product Line Management (offer) Exec. May also require review of additional service lines such as profes-sional services or support services.

• Review of: o Current offer portfolio and offer strategy/road map. o Sales objectives and sales offer requirements. o Review of offer realization and offer operations processes.

• Readout of strengths, weaknesses, and areas of opportunity regard-ing company’s offer strategy, portfolio, and processes based on blend of TSIA MS benchmark data and industry veteran expert analysis. Includes recommendation on current offer improvements as well as potential adjacent offer opportunity.

Managed Services Delivery Model

• Interview of key MS service delivery executives responsible for technical operations and customer support.

• Review of: o Current MS service delivery structure. o MS service delivery processes. o MS service delivery tools. o MS delivery cost and expense models. o Resource planning and optimization.

• Readout of strengths, weaknesses, and areas of opportunity regard-ing company’s MS service delivery model based on blend of TSIA MS benchmark data and industry veteran expert analysis.

MS Acquisition Assistance • Interview of key executive responsible for MS mergers and acquisi-tions.

• Review of acquisition targets (may include interviewing acquisition targets):

o Financial performance. o Client base, including likelihood of client retention. o Strategic road map. o Offer portfolio. o Service delivery capabilities (tools, processes, and re-

sources). • Readout of strengths and weaknesses of cited review areas for each

acquisition target.

14

17065 Camino San Bernardo, Ste. 200 | San Diego, CA 92127 | Tel. 1.858.674.5491 | Fax. 1.858.430.3571

© Technology Services Industry Association | www.tsia.com

CLOSING COMMENTS

As we enter the next generation of technology consumption, TSIA firmly believes that managed service organizations will find themselves at the epicenter of company success. Technology business models have become more services intensive over the last decade. None of the industry trends TSIA has identified change that general trajectory. Technology business models will continue to become more services intensive. The types of services may change from the traditional implementation, education, and support offerings currently in the comfort zone of product companies. But successful service transactions will clearly be at the heart of market success. Service organizations must develop new organizational capabilities that will help lead their companies to market success. The time to start developing those capabilities is now.