Avustajaeläin tulevaisuudessa/ Jussi Lehtonen, Turun Yliopisto

The State of Forestry Plantation Investments in Africa - Overview of Volumes and Investment Patterns

Working Conference Forests for the Future – New Forests for Africa Accra Ghana 16 to 17 March 2016Petri Lehtonen, Deputy Managing Director, Indufor Oy

Copyright © 2016 Indufor Oy

16 March 2016

Indufor and Timberland Investments

Copyright © 2016 Indufor Oy 2

Indufor was founded in 1980 Independent staff ownedAdvisory services in forest and forest industry developmentPrivate and public sector clientsLocated in:

Helsinki, Finland Auckland, New Zealand Melbourne, Australia Washington DC, USA

Copyright © 2016 Indufor Oy

Indufor in Africa

Due diligence and valuationsFeasibility studiesSustainability assessmentsStrategic advice in forest and wood processing investmentsHigh level reviews of government strategiesDevelopment of private forestry

Recent projects in:• Cameroon• Congo, DRC• Ethiopia

Ghana• Kenya• Liberia• Mozambique• Sierra Leone• South Africa• Tanzania• Uganda• Zambia• Mauritius• Cape Verde

3

Copyright © 2012 Indufor Oy 4

Photo: Mike May/EcofuturoParque das Neblinas, Brazil

Contents

Copyright © 2016 Indufor Oy 5

1. Investments in African Forestry 2. Role of Different Investors3. Barriers in Investing4. Solutions5. Take-home Messages

Copyright © 2016 Indufor Oy 6

Demand of forest products

Potential and suitable areas for forest plantations

Economic and social situation improving

Rationale to invest in forestry in Africa

Copyright © 2016 Indufor Oy 7

Africa has a huge population The working age population will be the largest in the world in a few decades

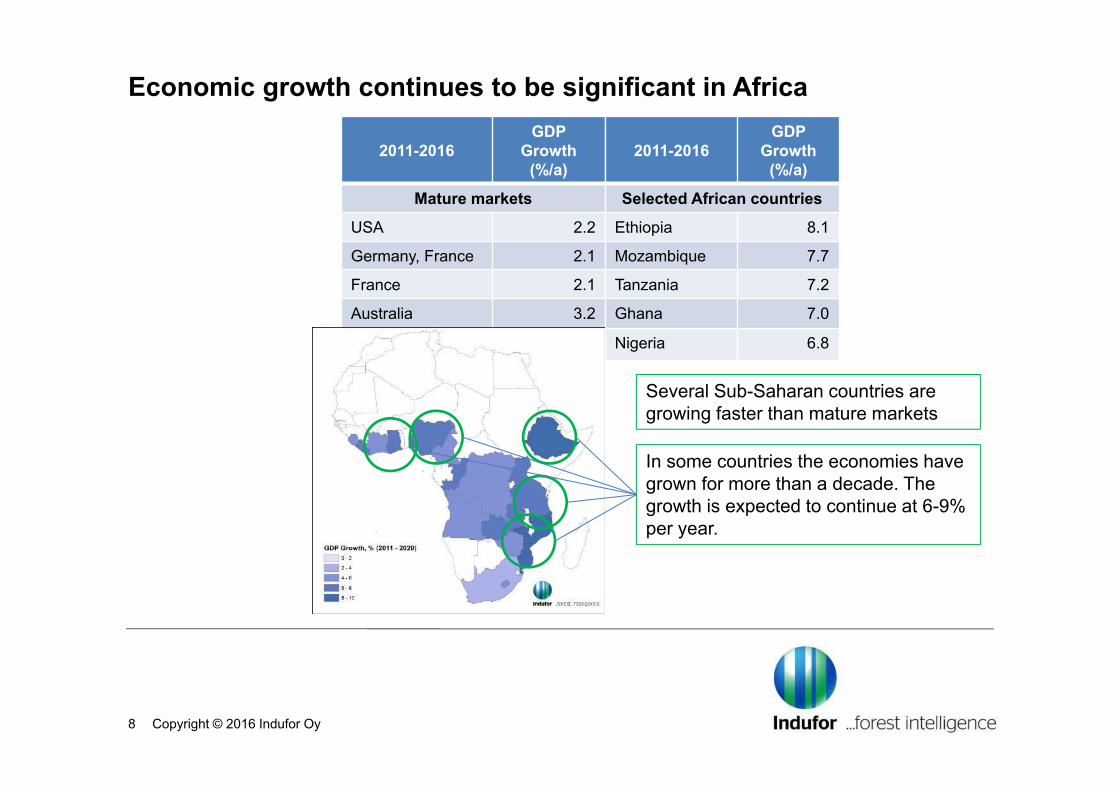

Economic growth continues to be significant in Africa

Copyright © 2016 Indufor Oy 8

2011-2016GDP

Growth(%/a)

Mature markets

USA 2.2

Germany, France 2.1

France 2.1

Australia 3.2

2011-2016GDP

Growth(%/a)

Selected African countries

Ethiopia 8.1

Mozambique 7.7

Tanzania 7.2

Ghana 7.0

Nigeria 6.8

Several Sub-Saharan countries are growing faster than mature markets

In some countries the economies have grown for more than a decade. The growth is expected to continue at 6-9% per year.

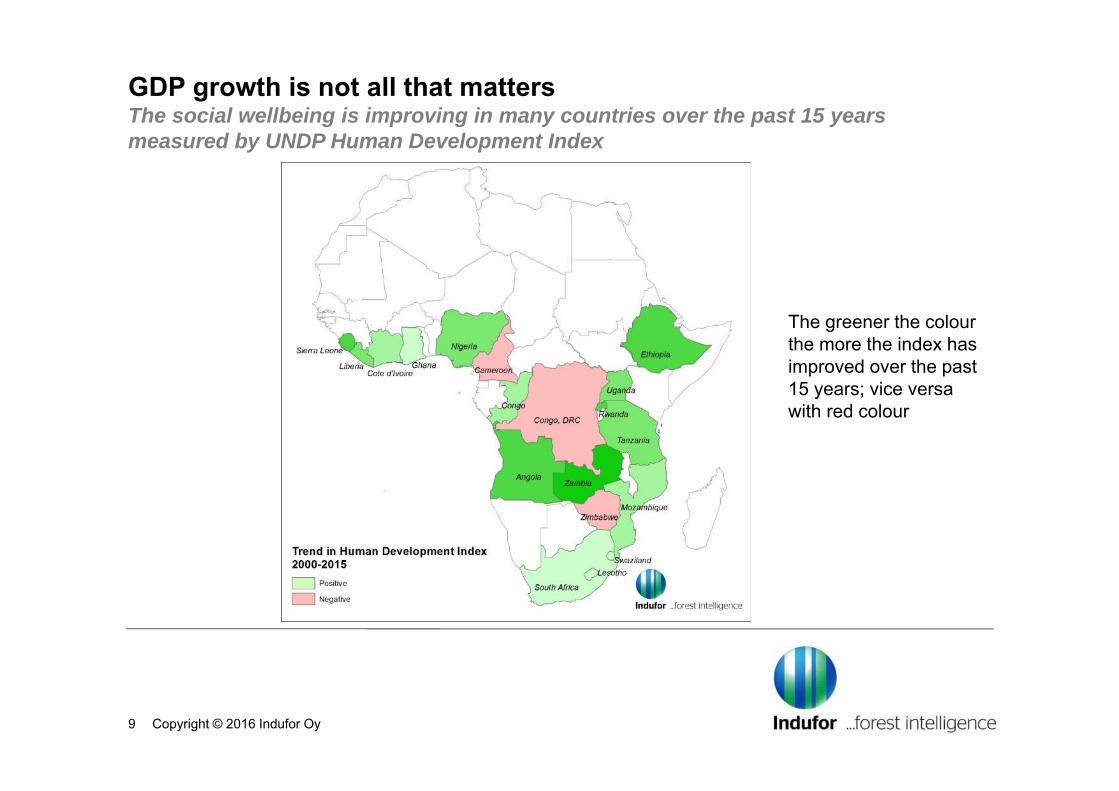

GDP growth is not all that matters The social wellbeing is improving in many countries over the past 15 years measured by UNDP Human Development Index

Copyright © 2016 Indufor Oy 9

The greener the colour the more the index has improved over the past 15 years; vice versa with red colour

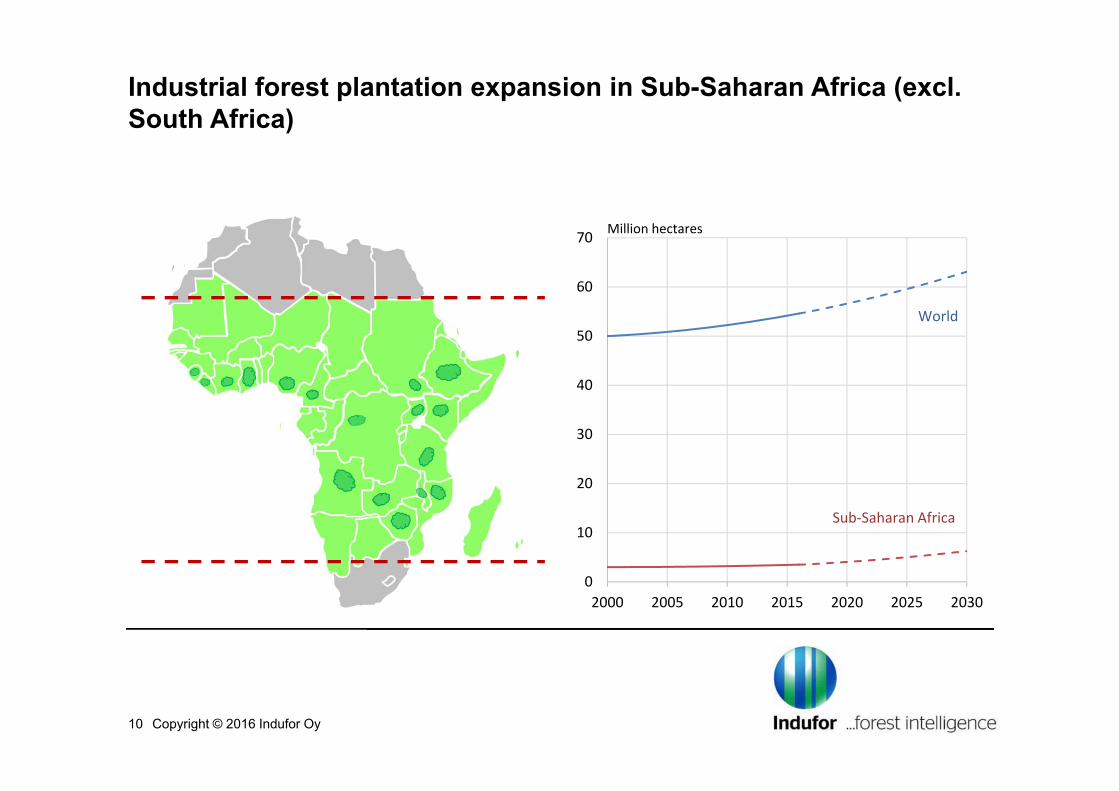

Industrial forest plantation expansion in Sub-Saharan Africa (excl. South Africa)

Copyright © 2016 Indufor Oy 10

World

Sub‐Saharan Africa

0

10

20

30

40

50

60

70

2000 2005 2010 2015 2020 2025 2030

Million hectares

The current wood supply is insufficientPlantation investments and overall development will be fundamental otherwise deforestation will inevitably continue

0

50

100

150

200

250

300

Wood supply and demand in Africa

Deficit

Natural forest/imports

Supply of plantationwood

Demand of industrialroundwood

Million m³

Copyright © 2016 Indufor Oy 11

Investing in Forestry

0

1

2

3

4

5

Greenfield investment intoprocessing

Plantation establishment Forestry ODA

Investing in forestry, 2010‐15 average per year

Latin America Asia‐pacific Africa

Billion USD

Copyright © 2016 Indufor Oy 12

Africa in the Universe of Timberland Investment

Copyright © 2016 Indufor Oy 13

African share of the value of timberland investments, %

Rest Africa0 2 4 6 8 10 12

Asia

Africa

Latin America

Oceania

Europe

North America

Million hectares

Global forest ownership by financial investors, 2015

REIT/Other

TIMO

Timberland Investment Universe: - area 25 million ha- value USD 80-100 billion

Copyright © 2016 Indufor Oy 14

1. Investments in African Forestry 2. Role of Different Investors3. Barriers in Investing4. Solutions5. Take-home Messages

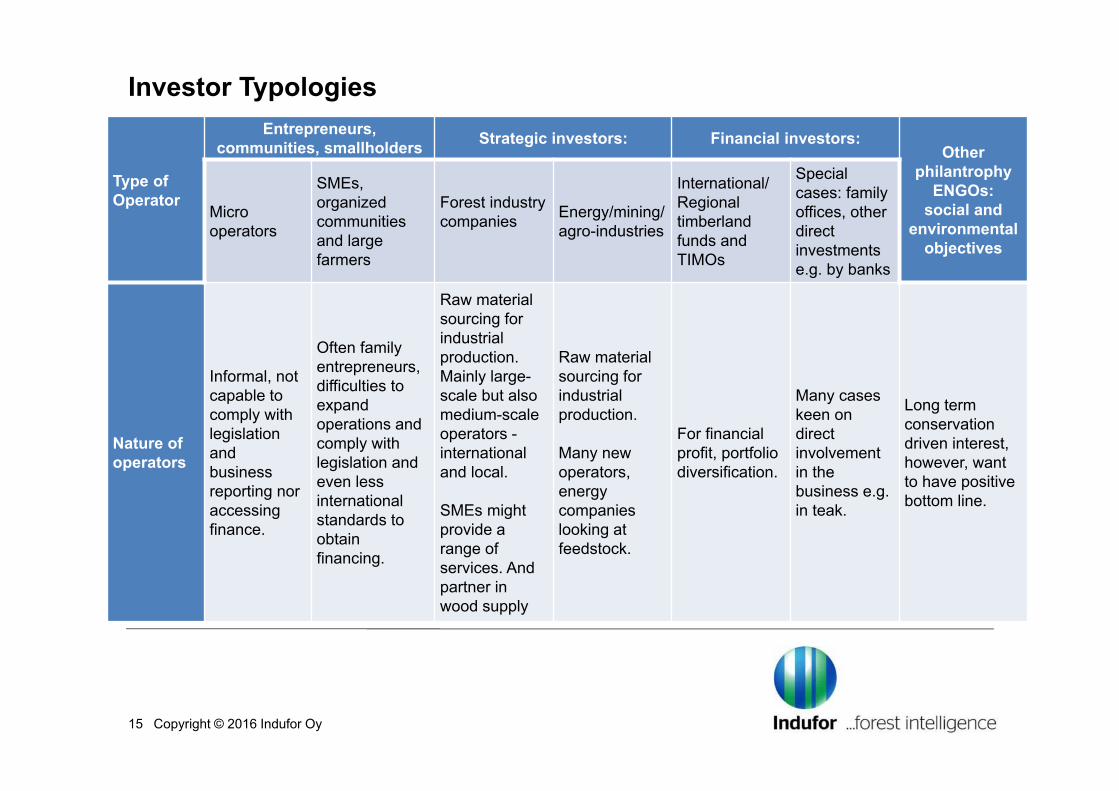

Investor Typologies

15

Type of Operator

Entrepreneurs, communities, smallholders Strategic investors: Financial investors:

Other philantrophy

ENGOs:social and

environmental objectives

Micro operators

SMEs, organized communities and large farmers

Forest industry companies Energy/mining/

agro-industries

International/Regional timberland funds and TIMOs

Special cases: family offices, other direct investments e.g. by banks

Nature of operators

Informal, not capable to comply with legislation and business reporting nor accessing finance.

Often family entrepreneurs, difficulties to expand operations and comply with legislation and even less international standards to obtain financing.

Raw material sourcing for industrial production. Mainly large-scale but also medium-scale operators -international and local.

SMEs might provide a range of services. And partner in wood supply

Raw material sourcing for industrial production.

Many new operators, energy companies looking at feedstock.

For financial profit, portfolio diversification.

Many cases keen on direct involvement in the business e.g. in teak.

Long term conservation driven interest, however, want to have positive bottom line.

Copyright © 2016 Indufor Oy

Vision for forest financing in Africa

Copyright © 2016 Indufor Oy 16

Today 5-10 years 10-15 years > 15 yearsPoor industrial infrastructureLimited existing planted forest assetsUnsecure land tenureLimited information

Private investments are more important than aidDevelopment driven by agricultural soft commodities and mineralsEmerging infrastructureUnsecure land tenureLimited information

Driven by private investmentsIndustrial infrastructure in placeExport of low value added wood productsDeveloped land tenure – still unbalanced landownership with social pressureDecent level of information

Developed infrastructure and logisticsBalance land ownershipNearly perfect information

Required development inputs in forestry / forest industry

Grants / subsidiesTechnical assistanceTechnologyPolicy changesInfra developmentAttract investments

Local loan instrumentsLocal service providersMarket accessGov. subsidies

Government subsidiesFace international competitiveness

Level of development HighLow

Risks and returns

Low

High

Role of Local Entrepreneurs, Governments and Donors

Frontier Market Emerging Market Developed Growing Market

Mature Market

Role of government, donors and development financingImproving the infrastructure and governance

Catalyse development with incentivesReduce need for development financing

Turning from developer to regulatorKey driver of sustainability

Regulator

Role of local entrepreneursTap local investment opportunitiesEstablish associations to promote sectoral interests

Establish partnerships with strategic investors in technologies and market access (including in small-scale plantations)

Growing position in supply chains

Important players in solid wood product industries

Copyright © 2016 Indufor17

Role of Strategic and Financial Investors as well as Impact Investors

Frontier Market Emerging Market Developed Growing Market

Mature Market

Role of Strategic investorsLimited access due to high risksPossibility to create long term unique position

Creating industrial infrastructure, providing technology and market access, HRD and R&D

Need to outsource assetsPartnerships with other forest ownersOrganic growth

Entering less mature marketsGrowth by acquisitions and structural rationalisation

Role of financial investorsFew possibilities without strategic investors and industrial infrastructure

Opportunities for high risk/returns assuming that strategic investors are entering

Increasing opportunities and transactions

Established presence/exits

Role of impact investorsFill the gap between development financingand private investments

Copyright © 2016 Indufor18

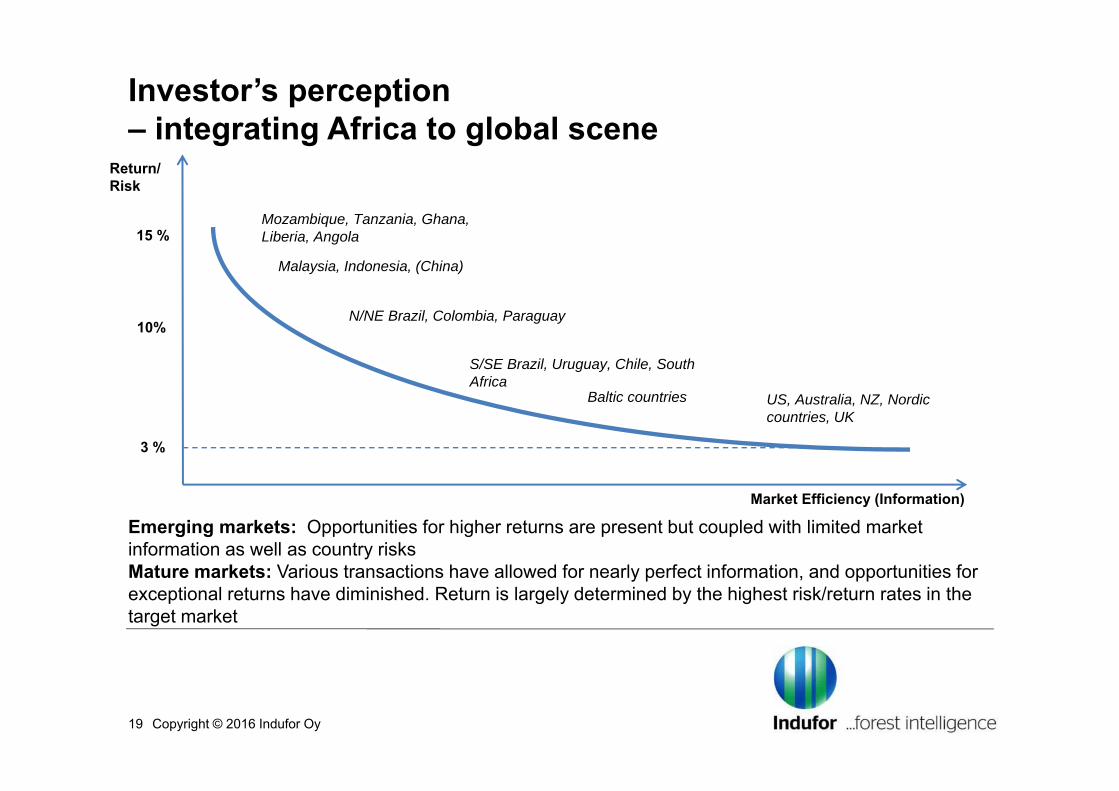

Investor’s perception – integrating Africa to global scene

Return/ Risk

Market Efficiency (Information)

Emerging markets: Opportunities for higher returns are present but coupled with limited market information as well as country risksMature markets: Various transactions have allowed for nearly perfect information, and opportunities for exceptional returns have diminished. Return is largely determined by the highest risk/return rates in the target market

Mozambique, Tanzania, Ghana, Liberia, Angola

N/NE Brazil, Colombia, Paraguay

S/SE Brazil, Uruguay, Chile, South Africa

US, Australia, NZ, Nordic countries, UK

Malaysia, Indonesia, (China)

Baltic countries

15 %

3 %

10%

Copyright © 2016 Indufor Oy 19

Copyright © 2016 Indufor Oy 20

1. Investments in African Forestry 2. Role of Different Investors3. Barriers in Investing4. Solutions5. Take-home Messages

Why investors are not investing and financiers not financing plantation development?

Copyright © 2016 Indufor Oy 21

LOCAL INVESTORS AND FINANCIERS are opportunistic

STRATEGIC INVESTORS are facing barriers to entry

FINANCIAL INVESTORS have demanding investment criteria

DEVELOPMENT FINANCING required to create enabling conditions

Major Obstacles

Copyright © 2016 Indufor Oy 22

Land Tenure and Land Use

Technology and Productivity

Industrial Infrastructure – Integration to Value Chain and Markets

Financing Gaps

Land Tenure – Underlying Issues

• Established formal land ownership is a major driver of economic development

• Lack of tenure security drives unsustainable and destructive use of land

• Land issues are sensitive and debates are characterized by– political myopia, – corporate interest, – international civil societies’ agenda, – critics on land grabbing, – and failed interventions to contribute to clarify issues by development

agents’

Copyright © 2016 Indufor Oy 23

Land Tenure – Who owns the land in Africa?

• Land ownership is a mixture of – customary rights, – traditional communal ownership (often with conflicts), – colonial and corporate estates, – government land, – and nobody’s land

• The land use is commonly with low productivity and often destructive• Unclear visions on how land tenure and related land uses can be developed• Local and national political interests reduce improvements• Formal property rights appear often less secure than customary rights

Copyright © 2016 Indufor Oy 24

0

2

4

6

8

10

12

14

Year

World

Agriculture Natural forest

Planted forest Other land

Billion hectares

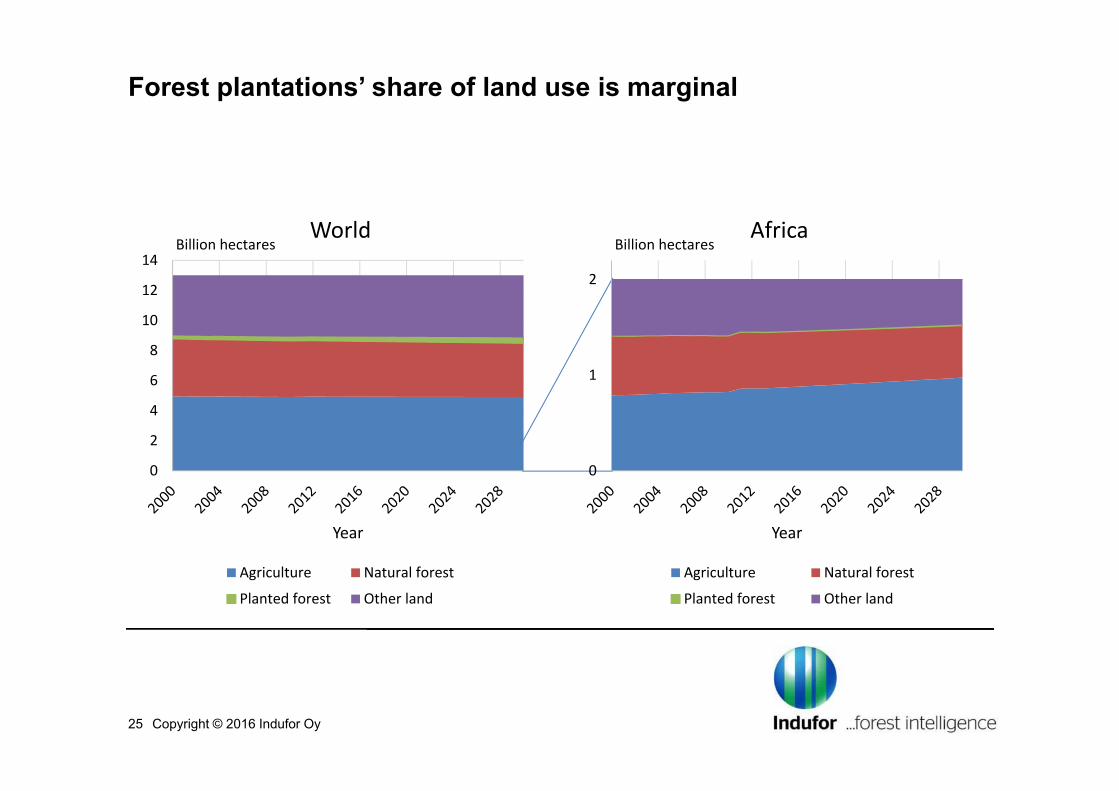

Forest plantations’ share of land use is marginal

Copyright © 2016 Indufor Oy 25

0

1

2

Year

Africa

Agriculture Natural forest

Planted forest Other land

Billion hectares

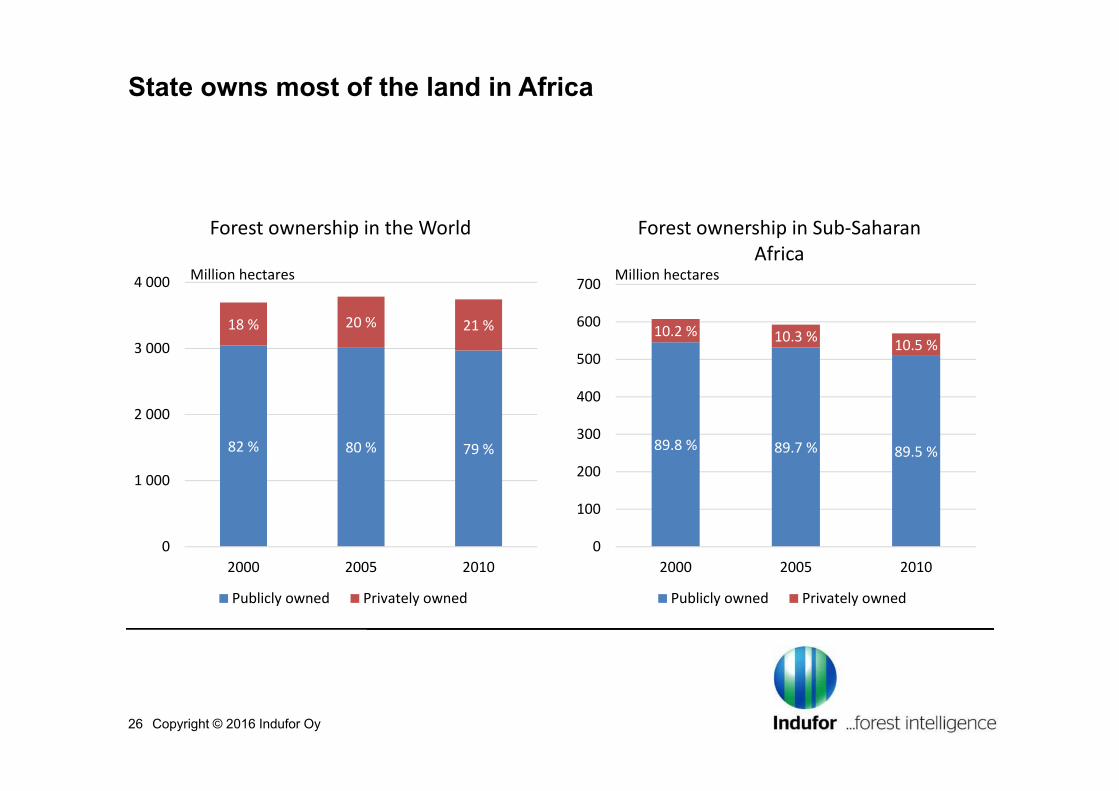

State owns most of the land in Africa

Copyright © 2016 Indufor Oy 26

89.8 % 89.7 % 89.5 %

10.2 % 10.3 % 10.5 %

0

100

200

300

400

500

600

700

2000 2005 2010

Forest ownership in Sub‐Saharan Africa

Publicly owned Privately owned

Million hectares

82 % 80 % 79 %

18 % 20 % 21 %

0

1 000

2 000

3 000

4 000

2000 2005 2010

Forest ownership in the World

Publicly owned Privately owned

Million hectares

Industrial Infrastructure – Integration to Value Chain and Markets

• Industrial infrastructure is mostly poor, however, developing in Sub-Saharan Africa

– Primary and secondary road infrastructure– Railways– Ports– Land border crossings

• Forest industry value chains are still largely disintegrated– Industrial scale plantations few and still limited access to markets– Value chains combining smallholders, small-scale industrial operators

and local urban markets are fragmented

Copyright © 2016 Indufor Oy 27

Copyright © 2016 Indufor Oy 28

CompanyPlantations

Govt.plantations

Large companies

SME´sPrivate tree growers

Bottlenecks:

Suboptimal mix of assortments

Lumber, poles

Lumber: poor quality

Veneer, plywood, furniture

None

Imports, scale of production

Paper, MDF (none currently)

Capital predictability of log markets

None

Capital, no free log markets/swaps

Premium for quality lumber

Traders play important role

Customers not sophisticated

End markets far, traders collect and

transport

Companies

High residues, poor technology

Lack of capital to buy logs

SME´s

Assets/Processing/End Markets are not integrated

Typical Forest Value Chains

Large-scale plantations – relatively new assets with initial downstream processing

Small-scale plantations – disintegrated value chain

Technology and Productivity

• Obsolete technology – opportunities to develop appropriate technologies• Productivity gap – opportunities for significant improvement

Copyright © 2016 Indufor Oy 30

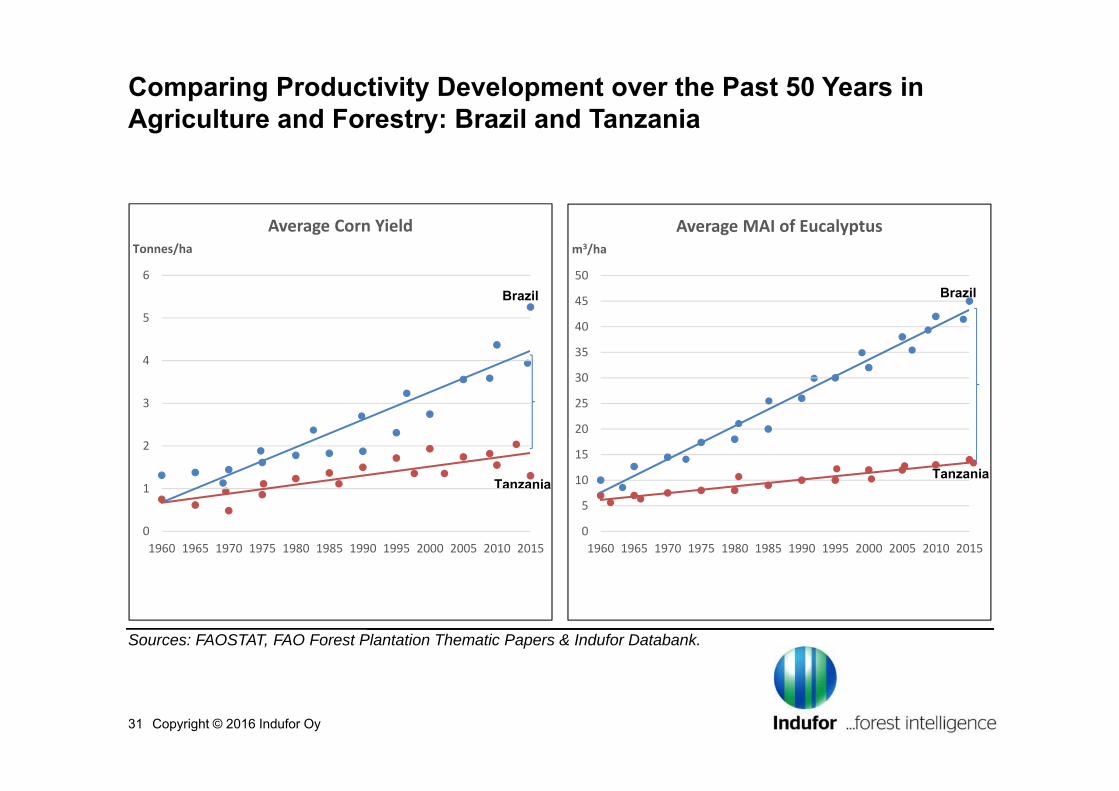

Comparing Productivity Development over the Past 50 Years in Agriculture and Forestry: Brazil and Tanzania

Copyright © 2016 Indufor Oy 31

Brazil

TanzaniaTanzania

Brazil

Sources: FAOSTAT, FAO Forest Plantation Thematic Papers & Indufor Databank.

0

1

2

3

4

5

6

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Tonnes/ha

Average Corn Yield

0

5

10

15

20

25

30

35

40

45

50

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

m3/ha

Average MAI of Eucalyptus

Financing Gaps

• Financing is available for business operations that can create positive cash flows in 3 to 5 years and have acceptable risk levels

• Companies have to be well established

• Financing gaps– New plantation establishment to develop assets (green field)– Small-scale industrial operations– Privatisation of state-owned plantations

Copyright © 2016 Indufor Oy 32

What kind of actions are expected to accelerate responsible investments?

• DFIs: WB or IFC, AfDB, EIB, Finnfund, FMO, Norfund, etc.– Financing to compensate the long exit periods and social risks

• Donors – Incentive schemes for local tree growers

• Governments – Innovative policies in leasing land for responsible investors

• Governments and donors together– Policy support, risk sharing, developing infrastructure that facilitate forest

investments, or provide complementary financing or guarantees• Strategic and financial investors

– Take seriously the opportunities in Africa and look for local partners

33 Copyright © 2016 Indufor

Contents

Copyright © 2016 Indufor Oy 34

1. Investments in African Forestry 2. Role of Different Investors3. Barriers in Investing4. Solutions5. Take-home Messages

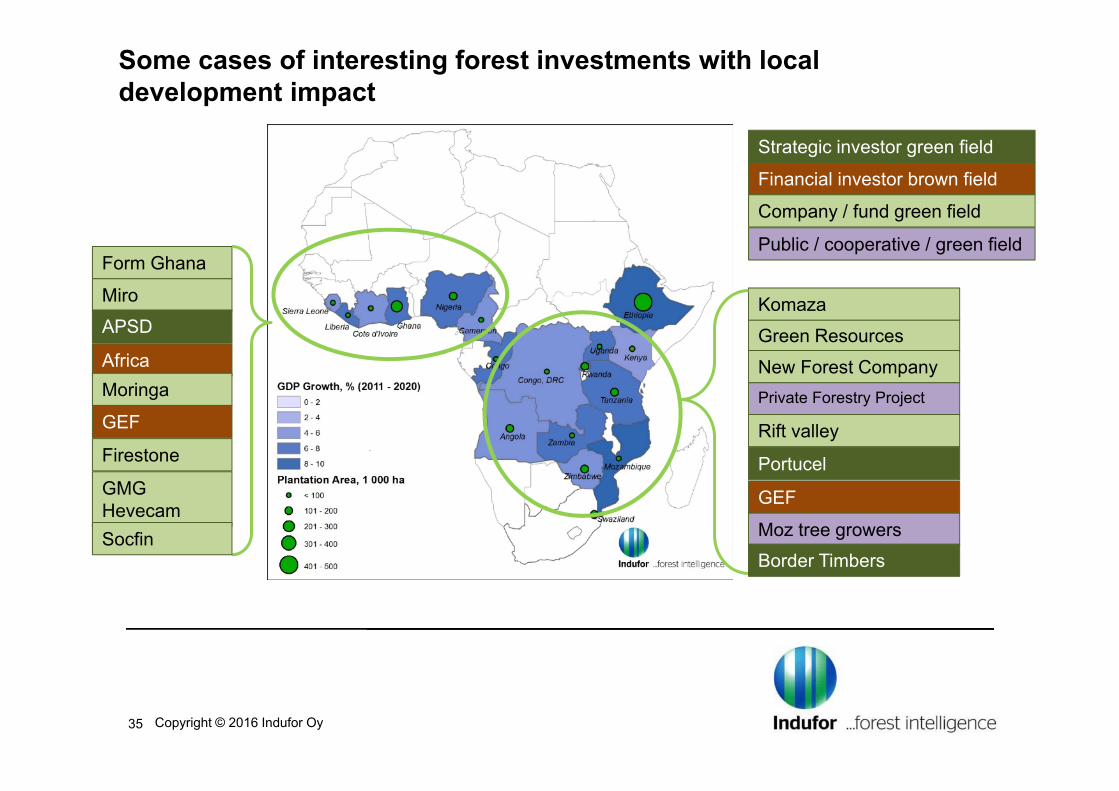

Some cases of interesting forest investments with local development impact

35 Copyright © 2016 Indufor Oy

Form Ghana

MiroAPSD Green Resources

New Forest Company

GEF

Africa Renewables

Komaza

Private Forestry Project

Rift valley

Portucel

Moringa

Strategic investor green field

Financial investor brown field

Company / fund green field

Public / cooperative / green field

Moz tree growers

GEF

Border Timbers

Firestone

GMG HevecamSocfin

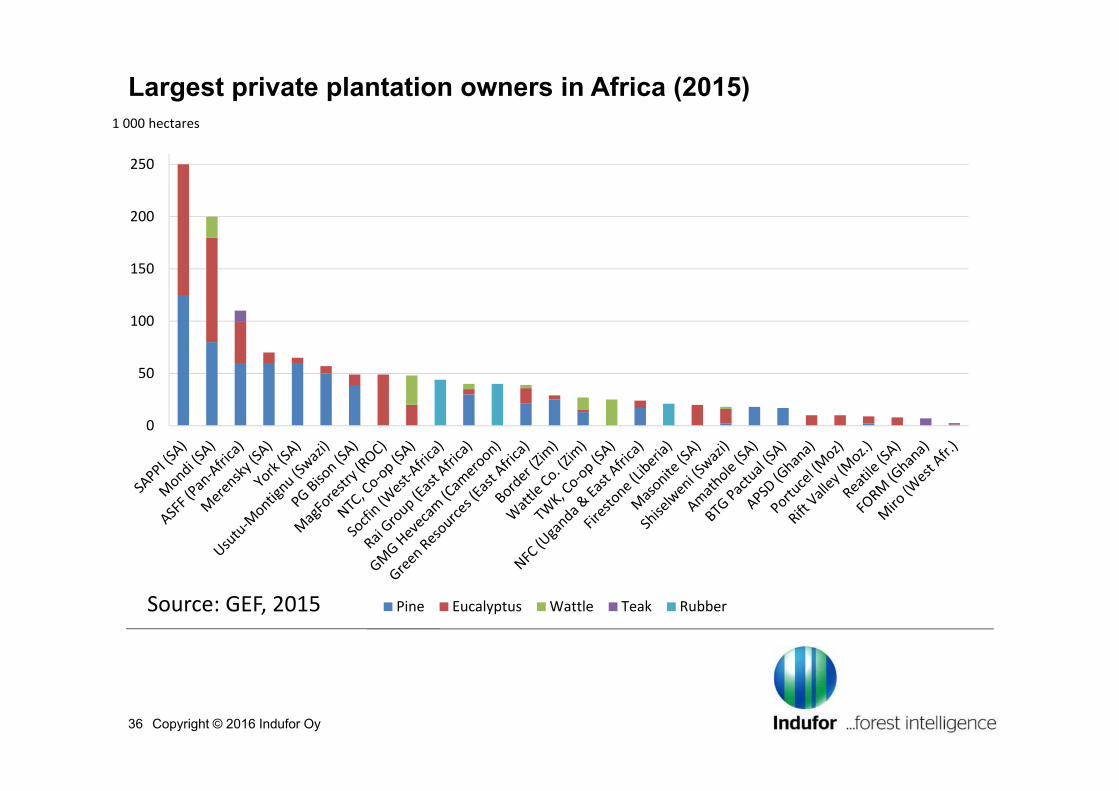

Largest private plantation owners in Africa (2015)

0

50

100

150

200

250

Pine Eucalyptus Wattle Teak Rubber

Copyright © 2016 Indufor Oy 36

1 000 hectares

Source: GEF, 2015

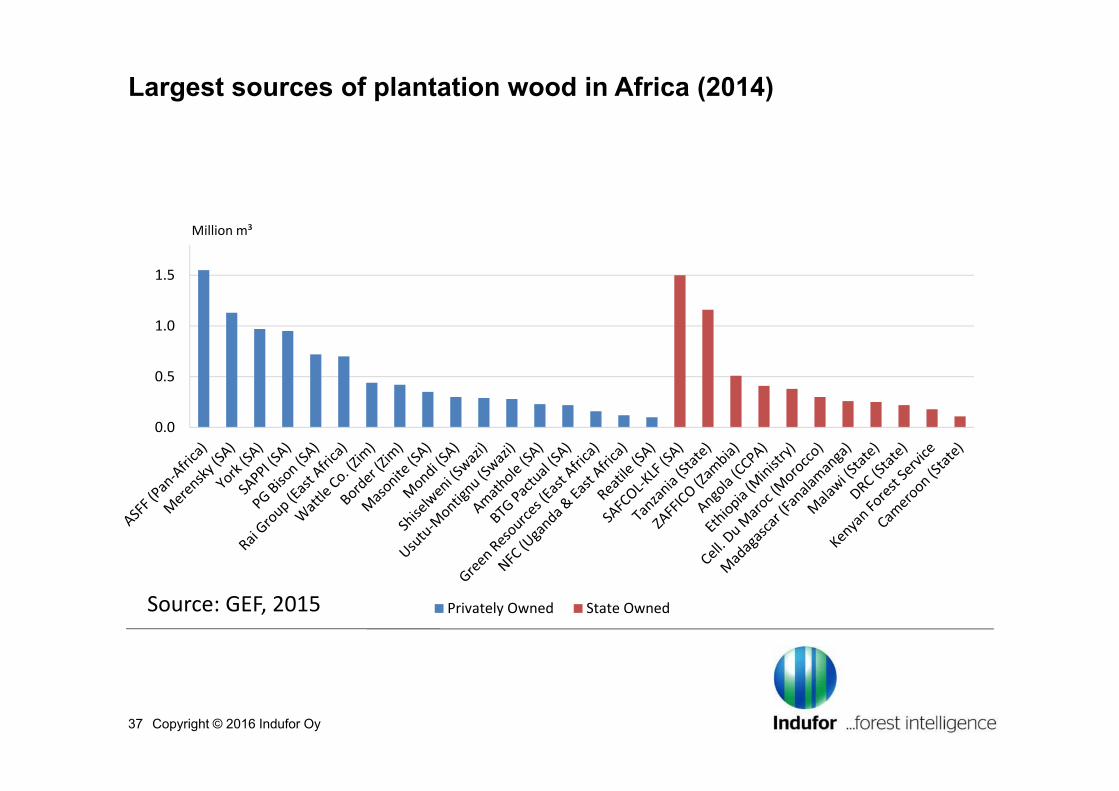

Largest sources of plantation wood in Africa (2014)

Copyright © 2016 Indufor Oy 37

0.0

0.5

1.0

1.5

Privately Owned State Owned

Million m³

Source: GEF, 2015

Contents

Copyright © 2016 Indufor Oy 38

1. Investments in African Forestry 2. Role of Different Investors3. Barriers in Investing4. Solutions5. Take-home Messages

Take-home Messages (1)

Global megatrends, regional demand and diminishing natural forests call for investments in forest plantations and wood processing industries in Africa

Forest plantations are an important vehicle to improve living standards create employment and reduce poverty

Operating environments are rapidly improving in many African countries

Stakeholders in forest investments have many reasons to follow Africa closely and take actions

Copyright © 2016 Indufor Oy 39

Take-home Messages (2)

The key question is to manage and mitigate the unique risks

Commitment required on national and local level

Appropriate technology, scale and logistics in place

Develop secure market channels

Proof of good performance in Africa

Copyright © 2016 Indufor Oy 40

Contact us

Indufor Oy, Töölönkatu 11 AFI-00100 Helsinki, FinlandTel. +358 9 684 0110 Email [email protected] www.indufor.fi

Copyright © 2016 Indufor Oy 41