The Impact of CEO Compensation on Nonprofit Donations

23

1 The Impact of CEO Compensation on Nonprofit Donations Steven Balsam Temple University Fox School of Business 1801 Liacorous Walk Philadelphia, PA 19122 [email protected] and Erica E. Harris Rutgers University School of Business Camden 227 Penn Street Camden, NJ 08102 [email protected] This version: October 13, 2011 Acknowledgements: We are grateful for comments from participants at the American Accounting Association (AAA) 2011 mid-year meeting in Baltimore, MD.

Transcript of The Impact of CEO Compensation on Nonprofit Donations

1

The Impact of CEO Compensation on Nonprofit Donations

Steven Balsam

Temple University

Fox School of Business

1801 Liacorous Walk

Philadelphia, PA 19122

and

Erica E. Harris

Rutgers University

School of Business Camden

227 Penn Street

Camden, NJ 08102

This version: October 13, 2011

Acknowledgements: We are grateful for comments from participants at the American

Accounting Association (AAA) 2011 mid-year meeting in Baltimore, MD.

2

The Impact of CEO Compensation on Nonprofit Donations

Abstract

Compensation in nonprofit organizations is controversial, with nonprofit organizations

trading off the need to attract and compensate employees against the wishes of donors that

contributions go to the core mission, e.g., helping those in need. This issue is particularly

controversial when top executives receive compensation rivaling those of for-profit

organizations. In this paper we look at the impact of nonprofit CEO compensation on nonprofit

donations, finding evidence that donors do in fact reduce their contributions to nonprofit

organizations with high CEO pay. Specifically, we find a negative relationship between direct

donor contributions and the ratio of CEO pay to total expenditures as well as other measures of

excessive CEO compensation. In additional analyses we find our results are robust over time and

across industries.

3

The Impact of CEO Compensation on Nonprofit Donations

I. Introduction

Recent media attention surrounding executive pay has not only increased scrutiny of for-

profit organizations, but the nonprofit sector as well (NY State Attorney General 2007; Boroff

2008; Banjo 2009; Wilhelm 2009; Gershman 2011).1 Concerns have been intensified by current

economic conditions, including shrinking endowments and the overall economic downturn. In

times of strained charity and personal budgets, donors are especially cautious of supporting

nonprofit organizations with high CEO pay (Charity Navigator 2010 CEO Compensation Study).

Donors have expressed this exact concern on CharityNavigator.org, America’s largest charity

evaluator, indicating that high salaries have made them “reconsider their donations” to certain

nonprofit organizations (Emerson 2010). The IRS has raised similar concerns in a recent report

of hospital executive compensation (IRS 2009). This comes in addition to several 2008 changes

to IRS Form 990 requiring detailed disclosure of executive compensation in an effort to increase

transparency and accountability. We examine whether donors have indeed “reconsidered their

donations” by reducing contributions to nonprofits who pay their CEOs well.

Using a sample drawn initially from Charity Navigator and augmented by hand collected

data from Form 990’s we find that donors react to high CEO pay. Specifically, we find a

negative relationship between direct donor contributions and CEO pay, a relationship that is

robust over time and across industries.

The remainder of this paper is organized as follows. In the next section, we discuss the

motivation and hypothesis. This is followed by section III which discusses sample selection,

1

4

section IV the model specification, and section V which discusses our empirical results. Tests of

robustness and paper conclusions are presented in sections VI and VII, respectively.

II. Motivation and hypothesis

There are about 1.4 million nonprofit organizations in the U.S. generating contributions

of over $260 billion (Nonprofit Almanac 2007). Given the magnitude of the contributions

involved, the ability to attract and maintain supporters is vital to the survival of these

organizations. Studies in the nonprofit sector find that donations are associated with three

primary accounting measures: efficiency, effectiveness, and the ability to continue operations

into the future (Parsons 2007). However, a fourth factor not examined in the literature (to the

best of our knowledge) is the impact of executive compensation on contributors’ willingness to

support nonprofit organizations.

Anecdotally we know that supporters of the United Way withheld contributions in the

wake of multiple scandals related to CEO compensation over the years. In 1992 uproar resulted

from the disclosure of United Way President William Aramony receiving an annual

compensation package worth $463,000. Even though Aramony resigned from his position

shortly after this disclosure, it was estimated that United Way collections would be down 10

percent in 1992 from the year earlier, with the implication that some, if not the entire drop was

caused by the scandal (Stodghill et al. 1992). In sum, “faithful donors to the organization

demanded change and greater accountability for the use of their charitable dollars” (Frumkin

2001), evidence that nonprofits do respond to pressure from stakeholders to control executive

pay.

5

Nonprofits compete with other organizations for employee and executive talent. While

they may attract individuals who are less driven by extrinsic rewards2, in most cases they need to

provide a pay package that is competitive with an individuals’ other alternatives. Consequently,

to attract and retain an individual capable of running a multi-million or billion dollar enterprise,

nonprofits need to provide a compensation package that is competitive with that of for-profit

entities. Emerson (2010) provides a list of the top 15 paid charity CEOs (outside of colleges and

universities) showing that each received in excess of $800,000 in 2008, with the highest Zarin

Mehta, of the New York Philharmonic topping $2.5 million. While these amounts are

substantially less than that paid to for-profit CEOs (see for example Balsam 2007), they come as

a shock to donors who, according to Emerson (2010), “assume that charity leaders work for free

or minimal pay and are shocked to see that they earn six figure salaries.”

The IRS stipulates that nonprofit organizations pay executive compensation that is “fair

and reasonable”. While there is no collective standard for what is fair and reasonable, balancing

the market value of executive talent and public trust is a critical component of charity success.

We argue that nonprofits perceived to pay their CEO excessively will suffer the political costs of

reduced donor support.3 Our research question is whether donors respond to high CEO pay by

cutting back on donations to these organizations.

H1: Nonprofit organizations with higher CEO pay have lower direct donations.

III. Sample selection

2 As an example, when Elizabeth Dole served as President of the American Red Cross from 1991-1999. Initially she

declined compensation. http://womenincongress.house.gov/member-profiles/profile.html?intID=59 3 There may also be actual penalties for excess compensation applied by the IRS. Penalties range from fines levied

on both executives and approving boards to revocation of tax exempt status (although rare). In a 2007 IRS

investigation, the service reported over $4 million in excess benefit transaction excise taxes arising from excessive

executive pay at charity organizations (IRS 2007).

6

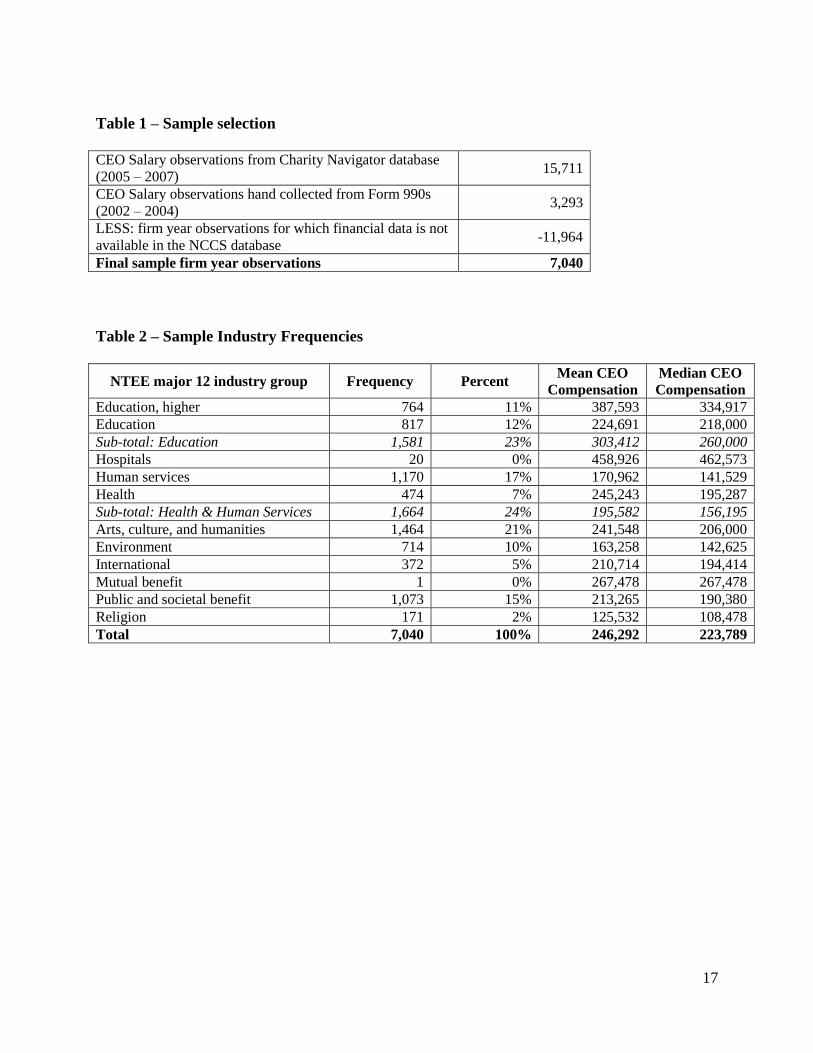

To test our hypothesis we analyze a sample of over 7,000 firm year observations across

six years and a broad array of industries. The majority of our CEO salary observations are drawn

from the CharityNavigator.org database. Charity Navigator is America’s largest charity

evaluator and the proprietor of financial and organizational data for over 5,500 mid to large size

US charities. Charity Navigator is the most frequently consulted website by individual givers,

with over 3 million unique hits in 2009 (charitynavigator.org). Further, Gordon et al. (2009) find

empirical evidence to support donor use of Charity Navigator ratings in their donation decisions.

In addition to providing ratings, Charity Navigator also highlights leadership salary information

for the nonprofits in their database. Each nonprofit organization listed has a section for

organizational leadership where the name, title, compensation, and percentage of compensation

to total expenses are presented.

Charity Navigator provided our initial sample of 15,711 CEO salary observations for

nonprofit organizations in their database from 2005 – 20074. We augmented this database with

hand collected salary information from IRS Form 990s5 for fiscal years 2002 – 2004 which

provided for an additional 3,293 CEO salary observations.6 We then merge our CEO salary

sample with financial information available from the National Council on Charitable Statistics

(NCCS) Statistics of Income (SOI) file. Unfortunately, not all the organizations in the Charity

Navigator database are included in the NCCS SOI file. We are forced to delete 11,964

4 We utilize CEO salary information through 2007 given that our model requires lagged CEO compensation and the

most recent data available for our dependent variable is for fiscal years ending 2008. 5 To verify that Charity Navigator salary data was extracted from the same source as our hand collected data, we

selected a random sample of 10 salary observations provided by Charity Navigator and traced them to the

organization’s Form 990. In all 10 cases the information presented on the organization’s Form 990 matched the

salary information supplied by Charity Navigator. 6 To minimize our data collection efforts we only collected salary data for nonprofits for which we had all other data

required for our empirical model. Consequently while it appears we have much less data for 2002 through 2004, the

number of usable observations is not significantly smaller in those years.

7

observations for which financial information is not available. This leaves a final sample of 7,040

observations. See Table 1 for a reconciliation of our sample.

IV. Model specification

Dependent variable

While nonprofits fund their operations from a variety of sources including government

grants and program service revenues, we focus on direct donations or public support. Direct

public support has been defined by the IRS as the “amounts of contributions, gifts, grants, and

bequests that the organization received directly from the public”. We focus on direct public

support as we believe that this source of funding, rather than government grants or program

service revenues, would be most sensitive to the political costs associated with high

compensation. Specifically, we test the response of direct donations to nonprofit CEO

compensation; given that direct donations are the most straight forward measure of donor

dissatisfaction.

Test variables

One of the issues we face is determining the appropriate form of the test variable. That

is, for example, do donors and potential donors react to the level of CEO compensation or do

they adjust for the scale of the nonprofit? Or do they react to some excess compensation

threshold? Unfortunately there is no prior literature to provide guidance. Our main analysis is

based on CEO salary as a percentage of total firm expenditures. We believe this may be the best

functional form for two reasons. First, information sites such as Charity Navigator present this

ratio to donors as a means of allowing for comparison between organizations. Second, because

scaling by total expenses controls for the size of the organization, and it is well know that size is

a major determinant of CEO compensation (Tosi et al. 2000). This is important in a sector, and

8

sample, where organizational size is so varied. However, because we are unsure of what donors

react to, we also present results for several alternative test variables. In particular we also define

CEO pay as: the level of CEO compensation, the change in CEO compensation, the percentage

change in CEO compensation,7 in addition to indicator variables taking the value of one if the

ratio of CEO pay to total expenses is in the top 10, 20, or 25 percent of our sample, and zero

otherwise. Whichever variable we use, we measure it as of year t-1 to allow for donors to

become aware of CEO pay and adjust their donations accordingly.8 Our expectation is that the

test variable, however it is operationalized, will be negatively associated with the dependent

variable, direct donations.

Control variables

Prior research (Weisbrod and Dominguez 1986; Posnett and Sandler 1989; Hyndman

1991; Callen 1994; Tinkelman 1998; Khumawala and Gordon 1997; Greenlee and Brown 1999;

Parsons 2003; Tinkelman and Mankaney 2007; Parsons and Trussel 2008; Tinkelman 2009)

confirms that organizational efficiency is associated with the ability to attract donations.

Following Baber et al. (2001), we utilize the ratio of program service expenses to total expenses,

or Program Ratio, to measure organizational efficiency. To illustrate consider a charity with

$1,000 in program service expenses and total expenses of $2,000. The Program Ratio equals .5

for this organization which is interpreted as for every $1.00 donated, $0.50 is used to provide

services related to the charity’s mission. Our expectation, based on prior research, is that a more

7 In the models where we use change in compensation or percentage change in compensation as our test variable, we

redefine the dependent and control variables in similar fashion (i.e., redefine them in change or percentage change

form). 8 This holds for our control variables as well. Given delays in filing however, sometime salary for year t-1 is not

disclosed until well into year t. If that is the case it is less likely that salary in year t-1 would affect direct donations

in year t. Consequently in untabulated analyses we also run our models using year t-2 data on the right hand side of

the equation finding comparable results.

9

efficient organization will be better able to attract donations; hence we expect a positive

coefficient on this variable.

The ability to continue operations has been described as the financial stability of a

nonprofit organization. Chang and Tuckman (1991) define a ratio similar to the for-profit gross

margin ratio, dubbed the operating margin, operationalized as the ratio of total revenues less

total expenses divided by total revenues. Operating margin is found to be positively related to

contributions (Chang and Tuckman 1991) and consequently we expect a positive coefficient.

Information quantity represents the amount of financial information displayed to potential

contributors typically in the form of advertising or other means of making the mission of a

nonprofit organization public. We use the fundraising expenses of an organization to proxy for

the amount of information made available to contributors. Weisbrod and Dominguez (1986) and

Tinkelman (1999) find fundraising expenses to be positively related to donations received by an

organization, thus we expect a positive coefficient on this variable.

Information quality is considered paramount in the decision to invest, as well as in the

choice to contribute to a nonprofit firm. Parsons and Trussel (2008) identify two variables which

are found to be related to the decision to donate: age and size. Weisbrod and Dominguez (1986)

suggest that a nonprofit’s reputation, proxied by age, plays a role in the volume of contributions

secured by an organization. Weisbrod and Dominguez operationalize reputation as the number of

years since the initial 501(c)3 filing for tax exempt status and predict that increased organization

age represents superior effectiveness. Organization size has been controlled for in related studies

(Tinkelman 1998; Krishnan and Schauer 2000) and will be proxied for by year-end total assets.

We expect both organization age and total assets to be positively associated with the level of

donations.

10

Several papers have included the notion of donors refraining from making donations to

organizations who receive high levels of government grants, program service revenue, or other

revenue all considered to “crowd out” donations (Weisbrod and Dominguez 1986; Posnett and

Sandler 1989; Callen 1994; Emanuele and Simmons 2004; Yetman and Yetman 2009). However,

other literature has also documented the “crowding-in” effect of these same variables (Okten and

Weisbrod 2000; Khanna and Sandler 2000; Petrovits et al. 2011). As such, these three revenue

sources have been included to control for the presence of income sources considered either to be

substitutes or compliments by the donor population. However, given the mixed results of prior

literature, we do not have predicted directions for these variables.

In sum, the ordinary least squares regression model to test our hypothesis may be

expressed as:

Direct Donationst = β0 + β1 Compensation test variablet-1 + β2 Program Ratiot-1 + β3 Operating

Margint-1 + β4 Fundraising Expensest-1 + β5 Total Assetst-1 + β6 Government Grantst-1

+ β7 Program Service Revenuet-1 + β8 Other Revenuet-1 + β9 Organization Aget-1 + ε

Where all variables are defined above.

V. Empirical results

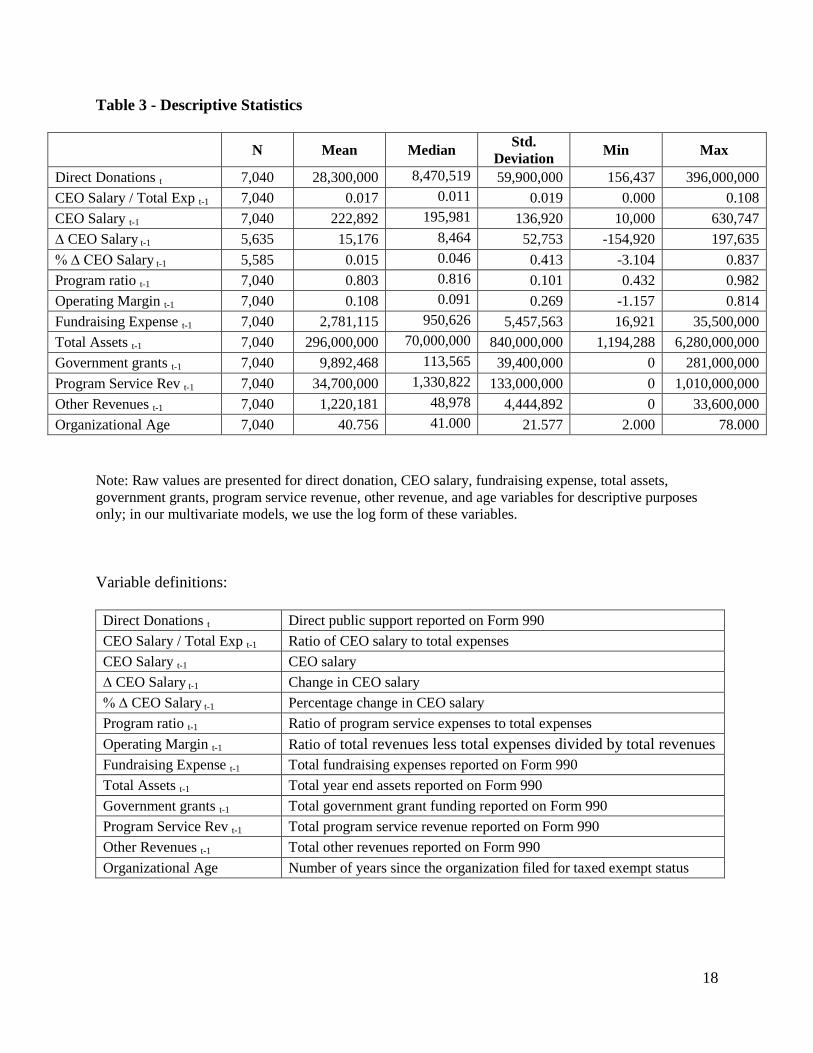

Descriptive Statistics

Table 3 provides descriptive statistics for the dependent and independent variables in our

model. The means and medians indicate a skewed distribution which is consistent with the need

for logged variables throughout our analyses. Additionally, all variables used in our empirical

analyses (Tables 5 – 8) are winsorized at the 1% level to mitigate the effect of extreme

observations. Table 4 presents Pearson and Spearman correlations for the variables included in

the model. Consistent with prior literature, age and size are significantly correlated with the

(1)

11

majority of the other control variables. For example, the highest (Pearson) correlation, 0.833, is

between total assets and program service revenue. However the Variance Inflation Factors are all

less than one, suggesting that multicollinearity is not a problem.

Empirical Results

Table 5 provides our first set of empirical results. Column one presents the model where

our test variable is lagged CEO compensation deflated by lagged total expenses, whereas in

column two the test variable is the log level of lagged compensation, column three the change in

compensation, and column four the percentage change in compensation9. In all cases the

coefficient on the test variable is negative and significantly different from zero, consistent with

our hypothesis that donors restrict contributions to organizations that pay their CEOs more.

Turning to our control variables, we generally find expected positive significant

relationships between direct donations and program ratio, operating margin, fundraising

expense, and total assets, however these results are not consistent across models. For example

when we use the change model, which incorporates the change in both the dependent and

independent variables, neither program ratio nor total assets are significantly related to direct

donations, while operating margin is negatively associated with direct donations. Related to the

crowding-in or out effects of government grants, program service revenues, or other revenues,

we find mixed results which differ across variable and model.

Table 6 provides our second set of empirical results, where the test variable is defined as

compensation relative to other nonprofit organizations. We define high compensation to be those

CEOs paid in the top 10 (column 1), 20 (column 2), and 25 (column 3) percent of our sample. In

all three columns we see the coefficient on the variable for high compensation is inversely

9 We lose a substantial number of firm year observations in our percentage change in CEO salary model because of

zero value variables which inhibit the ability to calculate a percentage change ration.

12

related to direct donations, once again supporting our hypothesis that donors restrict

contributions to organizations that pay their CEOs more.

VI. Robustness Tests

We explore two additional avenues as a means of testing the robustness of our results. In

the first we examine whether our findings are consistent across our sample period, while in the

second we examine whether our findings are consistent across our sample industries.

To rule out the possibility that any one year is driving our results, we analyze our model

by year. Table 7 presents the results of yearly regressions as well as the Fama MacBeth summary

statistics. Consistent with our hypothesis and our earlier results, we observe an inverse relation

between direct donations and the ratio of CEO salary to total expense in each year (2003 –

2008). The last column of Table 7 presents the Fama-MacBeth (1973) test which also confirms

the robustness of our findings.

To rule out the possibility that any one industry is driving our results, we analyze our

results by industry. Table 8 presents the results of industry regressions as well as the Fama

MacBeth (1973) summary statistics. In all seven industries we observe an inverse relation

between direct donations and the ratio of CEO salary to total expense.

VII. Conclusions

This paper examined the impact of nonprofit CEO compensation finding evidence which

suggests that donors take CEO compensation into account when they decide whether and how

much to contribute to a particular charity. This research extends and is incremental to prior work

showing that donors consider a charity’s success, efficiency, and stability in their donation

decision. It also builds on for-profit research that documents the political costs associated with

high CEO pay.

13

Using a fairly large sample of nonprofit organizations across a number of years and

industries, we find that donors do react to high CEO pay. Specifically, we find a robust negative

relationship between direct donor contributions and a variety of proxies for high or excessive

CEO compensation. These empirical results support the notion that donors have “reconsidered

their donations” and reduced their contributions to nonprofits that pay their CEO well.

14

References

Baber, W. R., A. A. Roberts, and G. Visvanathan. 2001. Charitable Organizations' Strategies and

Program-Spending Ratios. Accounting Horizons 15 (4): 329-343.

Balsam, S. 2007. Executive compensation: An introduction to practice and theory. WorldatWork.

Banjo, S. 2009. IRS Questions Pay of Charity Executives. Wall Street Journal February 18.

Boroff, P. 2008. Big Bucks for Theater Chiefs Draw Criticism as Sign of Excess. Bloomberg

October 28, 2008.

Callen, J., 1994. Money Donations, Volunteering and Organizational Efficiency. The Journal of

Productivity Analysis 5 (October): 215-228.

Chang, C., and H.P. Tuckman. 1991. Financial Vulnerability and Attrition as Measures of

Nonprofit Performance. Annals of Public & Cooperative Economics 62 (4): 655-672.

Charity Navigator. 2010. CEO Compensation Study.

(http://www.charitynavigator.org/index.cfm?bay=studies.ceo)

Emanuele, R., and W. Simmons. 2004. Does Government Spending Crowd Out Donations of

Time and Money? Public Finance Review 32 (5): 498-511.

Emerson, G. 2010. 15 Highest-Paid Charity CEOs. Smart Spending

(http://www.mainstreet.com/print/19173)

Fama, E., & J. MacBeth. 1973. Risk return and equilibrium: Empirical tests. Journal of Political

Economy 71: 607–636.

Frumkin, P. 2001. Are nonprofit CEOs overpaid? Public Interest (142):83.

Gershman, J., 2011. Charity Probe Questions. The Wall Street Journal September 9, 2011.

Gordon, T. P., C. L. Knock, and D. G. Neely. 2009. The role of rating agencies in the market for

charitable contributions: An empirical test. Journal of Accounting & Public Policy 28 (6):469-

484.

Greenlee, J.S. and K.L. Brown. 1999. The impact of accounting information on contributions to

charitable organizations. Research in Accounting Regulation 13: 111-125.

Hyndman, N. 1991. Contributions to charities – A comparison of their information needs and the

perceptions of such by the providers of information. Financial Accountability & Management 7

(2) (Summer): 69-82.

15

Nonprofit Almanac. 2007. The Nonprofit Sector in Brief, Facts and Figures from the Nonprofit

Almanac 2007. http://www.urban.org/UploadedPDF/311373_nonprofit_sector.pdf

IRS. 2007. Report on Exempt Organizations Executive Compensation Compliance Project –

Parts I and II. http://www.irs.gov/pub/irs-tege/exec._comp._final.pdf

IRS. 2009. IRS Nonprofit Hospital Project – Final Report. http://www.irs.gov/pub/irs-

tege/frepthospproj.pdf

Khanna, J., and T. Sandler. 2000. Partners in giving: The crowding-in effect of UK government

grants. European Economic Review 44 8: 1543–1556.

Khumawala, S. B. and T. P. Gordon. 1997. Bridging the credibility of GAAP: Individual donors

and the new accounting standards for nonprofit organizations. Accounting Horizons. 11 (3)

(September): 45-68.

Krishnan, J., and P.C. Schauer. 2000. The Differentiation of Quality Among Auditors: Evidence

from the Not-for-Profit Sector. Auditing: A Journal of Practice & Theory 19 (2): 9-25.

New York State Attorney General. 2007. Attorney General Cuomo Recovers $1,900,000 in

Excess Compensation from Morris Foundation. May 15, 2007.

Okten, C., and B. Weisbrod. 2000. Determinants of Donations in Private Nonprofit Markets.

Journal of Public Economics 75 (2): 255-272.

Parsons, L.M. 2003. Is accounting information from nonprofit organizations useful to donors? A

review of charitable giving and value-relevance. Journal of Accounting Literature. 22: 104-129.

Parsons, L. M. 2007. The Impact of Financial Information and Voluntary Disclosures on

Contributions to Not-For-Profit Organizations. Behavioral Research in Accounting 19:179-196.

Parsons, L. M., and J. M. Trussel. 2008. Financial reporting factors affecting donations to

charitable organizations. Advances in Accounting (23):263-285.

Petrovits, C., C. Shakespeare, and A. Shih. 2011. The Causes and Consequences of Internal

Control Problems in Nonprofit Organizations. Accounting Review 86 (1):325-357.

Posnett, J., and T. Sandler. 1989. Demand for Charity Donations in Private Non-Profit

Markets. Journal of Public Economics 40 (2): 187-200.

Stodghill, R., C. Del Valle, G. Sandler and L. Therrien. 1992. United They Stand. Business Week

Oct. 19: 40-41.

Tinkelman, D. 1998. Differences in Sensitivity of Financial Statement Users to Joint Cost

Allocations: The Case of Nonprofit Organizations. Journal of Accounting, Auditing & Finance

13 (4): 377-393.

16

Tinkelman, D. 1999. Factors Affecting the Relation Between Donations to Not-for-profit

Organizations and an Efficiency Ratio. Research in Governmental and Nonprofit Accounting 10:

135-161.

Tinkelman, D. 2009. Unintended consequences of expense ratio guidelines: The Avon breast

cancer walks. Journal of Accounting and Public Policy 28 (6):485-494.

Tinkelman, D., and K. Mankaney. 2007. When is Administrative Efficiency Associated With

Charitable Donations? Nonprofit and Voluntary Sector Quarterly 36 (1):41-64.

Tosi, H., S. Werner, J. P. Katz and L. R. Gomez-Mejia. 2000. How much does performance

matter? A meta-analysis of CEO pay studies. Journal of Management, 26(2): 301-339.

Weisbrod, B., and N. Dominguez. 1986. Demand for Collective Goods in Private Nonprofit

Markets: Can Fundraising Expenditures Help Overcome Free-Rider Behavior? Journal of Public

Economics 30 (1): 83-95.

Wilhelm, I. 2009. Executive Compensation at Charities Attracts New Scrutiny. The Chronicle of

Philanthropy February 18, 2009.

Yetman, M. H., and R. J. Yetman. 2009. Determinants of nonprofits' taxable activities. Journal

of Accounting and Public Policy 28 (6):495-509.

17

Table 1 – Sample selection

CEO Salary observations from Charity Navigator database

(2005 – 2007) 15,711

CEO Salary observations hand collected from Form 990s

(2002 – 2004) 3,293

LESS: firm year observations for which financial data is not

available in the NCCS database -11,964

Final sample firm year observations 7,040

Table 2 – Sample Industry Frequencies

NTEE major 12 industry group Frequency Percent Mean CEO

Compensation

Median CEO

Compensation

Education, higher 764 11% 387,593 334,917

Education 817 12% 224,691 218,000

Sub-total: Education 1,581 23% 303,412 260,000

Hospitals 20 0% 458,926 462,573

Human services 1,170 17% 170,962 141,529

Health 474 7% 245,243 195,287

Sub-total: Health & Human Services 1,664 24% 195,582 156,195

Arts, culture, and humanities 1,464 21% 241,548 206,000

Environment 714 10% 163,258 142,625

International 372 5% 210,714 194,414

Mutual benefit 1 0% 267,478 267,478

Public and societal benefit 1,073 15% 213,265 190,380

Religion 171 2% 125,532 108,478

Total 7,040 100% 246,292 223,789

18

Table 3 - Descriptive Statistics

N Mean Median

Std.

Deviation Min Max

Direct Donations t 7,040 28,300,000 8,470,519 59,900,000 156,437 396,000,000

CEO Salary / Total Exp t-1 7,040 0.017 0.011 0.019 0.000 0.108

CEO Salary t-1 7,040 222,892 195,981 136,920 10,000 630,747

∆ CEO Salary t-1 5,635 15,176 8,464 52,753 -154,920 197,635

% ∆ CEO Salary t-1 5,585 0.015 0.046 0.413 -3.104 0.837

Program ratio t-1 7,040 0.803 0.816 0.101 0.432 0.982

Operating Margin t-1 7,040 0.108 0.091 0.269 -1.157 0.814

Fundraising Expense t-1 7,040 2,781,115 950,626 5,457,563 16,921 35,500,000

Total Assets t-1 7,040 296,000,000 70,000,000 840,000,000 1,194,288 6,280,000,000

Government grants t-1 7,040 9,892,468 113,565 39,400,000 0 281,000,000

Program Service Rev t-1 7,040 34,700,000 1,330,822 133,000,000 0 1,010,000,000

Other Revenues t-1 7,040 1,220,181 48,978 4,444,892 0 33,600,000

Organizational Age 7,040 40.756 41.000 21.577 2.000 78.000

Note: Raw values are presented for direct donation, CEO salary, fundraising expense, total assets,

government grants, program service revenue, other revenue, and age variables for descriptive purposes

only; in our multivariate models, we use the log form of these variables.

Variable definitions:

Direct Donations t Direct public support reported on Form 990

CEO Salary / Total Exp t-1 Ratio of CEO salary to total expenses

CEO Salary t-1 CEO salary

∆ CEO Salary t-1 Change in CEO salary

% ∆ CEO Salary t-1 Percentage change in CEO salary

Program ratio t-1 Ratio of program service expenses to total expenses

Operating Margin t-1 Ratio of total revenues less total expenses divided by total revenues

Fundraising Expense t-1 Total fundraising expenses reported on Form 990

Total Assets t-1 Total year end assets reported on Form 990

Government grants t-1 Total government grant funding reported on Form 990

Program Service Rev t-1 Total program service revenue reported on Form 990

Other Revenues t-1 Total other revenues reported on Form 990

Organizational Age Number of years since the organization filed for taxed exempt status

19

Table 4 – Spearman (under) / Pearson (over) Correlations

Coefficients p-values (significant relationships are bolded)

C

EO

Sal

ary

to T

ota

l

Expen

ses

t-1

CE

O S

alar

y

t-1

Chan

ge

in

CE

O S

alar

y

t-1

% c

han

ge

CE

O S

alar

y

t-1

Pro

gra

m

rati

o t-

1

Oper

atin

g

Mar

gin

t-1

Fundra

isin

g

Expen

se t-

1

Tota

l A

sset

s

t-1

Gover

n-

men

t gra

nts

t-1

Pro

gra

m

Ser

vic

e

Rev

enue

t-1

Oth

er

Rev

enues

t-1

Org

aniz

a-

tional

Age

CEO Salary to Total

Expenses t-1

1.000 -0.277 0.010 0.098 -0.333 0.055 -0.314 -0.245 -0.192 -0.206 -0.197 -0.237

0.000 0.468 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000

CEO Salary t-1 -0.381 1.000 0.400 0.213 0.141 0.034 0.466 0.490 0.427 0.453 0.346 0.229

0.000 0.000 0.000 0.000 0.004 0.000 0.000 0.000 0.000 0.000 0.000

Change in CEO

Salary t-1

-0.057 0.406 1.000 0.726 0.043 0.045 0.109 0.133 0.103 0.127 0.104 0.041

0.000 0.000 0.000 0.001 0.001 0.000 0.000 0.000 0.000 0.000 0.002

Percentage change

CEO Salary t-1

0.042 0.195 0.950 1.000 0.010 0.037 0.003 0.001 -0.004 0.004 -0.006 -0.004

0.002 0.000 0.000 0.446 0.006 0.818 0.966 0.793 0.751 0.683 0.751

Program ratio t-1 -0.443 0.095 0.059 0.040 1.000 -0.082 0.094 0.206 0.189 0.205 0.123 -0.012

0.000 0.000 0.000 0.003 0.000 0.000 0.000 0.000 0.000 0.000 0.322

Operating Margin t-1 0.011 0.059 0.070 0.060 -0.039 1.000 0.013 0.085 0.022 0.020 0.032 -0.022

0.402 0.000 0.000 0.000 0.004 0.274 0.000 0.067 0.094 0.007 0.068

Fundraising Expense

t-1

-0.698 0.640 0.180 0.034 0.059 0.028 1.000 0.637 0.558 0.561 0.459 0.058

0.000 0.000 0.000 0.011 0.000 0.035 0.000 0.000 0.000 0.000 0.000

Total Assets t-1 -0.687 0.662 0.208 0.055 0.225 0.265 0.643 1.000 0.756 0.833 0.544 0.128

0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000

Government grants t-1 -0.370 0.348 0.090 0.006 0.151 -0.051 0.345 0.298 1.000 0.727 0.459 0.054

0.000 0.000 0.000 0.649 0.000 0.000 0.000 0.000 0.000 0.000 0.000

Program Service

Revenue t-1

-0.492 0.479 0.156 0.042 0.135 -0.005 0.417 0.516 0.348 1.000 0.501 0.131

0.000 0.000 0.000 0.002 0.000 0.718 0.000 0.000 0.000 0.000 0.000

Other Revenues t-1 -0.416 0.357 0.100 0.017 0.080 0.036 0.449 0.403 0.263 0.294 1.000 0.103

0.000 0.000 0.000 0.211 0.000 0.007 0.000 0.000 0.000 0.000 0.000

Organizational Age -0.203 0.261 0.048 -0.021 -0.026 0.023 0.246 0.327 0.100 0.371 0.160 1.000

0.000 0.000 0.000 0.115 0.048 0.083 0.000 0.000 0.000 0.000 0.000

20

Table 5 H1: Compensation regression results

Dependent Variable:

Direct Donations t

CEO Salary/Total

Expense t-1

CEOsalary t-1

Change in CEO

salary t-1†

Percentage change

in CEO salary t-1†

Coefficient Coefficient Coefficient Coefficient

p-value p-value p-value p-value

Constant 3.748*** 2.134*** 474,452.100** 0.221***

0.000 0.000 0.047 0.000

Test variable (Defined

in column heading) t-1

-10.062*** -0.019 -11.294*** -0.110***

0.000 0.311 0.006 0.002

Program ratio t-1

2.268*** 2.731*** -6,807,152.000 0.195

0.000 0.000 0.145 0.478

Operating Margin t-1 0.400*** 0.345*** -3,710,730.000*** -0.000

0.000 0.000 0.000 0.956

Fundraising Expense t-1 0.583*** 0.632*** 0.826** -0.101*

0.000 0.000 0.011 0.095

Total Assets t-1 0.201*** 0.231*** 0.005 -0.850***

0.000 0.000 0.193 0.000

Government Grants t-1 -0.001 -0.001 0.364*** 0.019**

0.430 0.617 0.000 0.011

Program Service

Revenue t-1

-0.030*** -0.028*** 0.095*** 0.005

0.000 0.000 0.001 0.884

Other Revenue t-1 0.006*** 0.007*** 0.331* -0.002

0.003 0.000 0.082 0.584

Organization Age t-1 -0.219*** -0.204*** n/a n/a

0.000 0.000

N 7,040 7,040 5,612 2,149

Adjusted R2 0.659 0.651 0.023 0.024

*significant at 10% level, **significant at 5% level, ***significant at 1% level.

See Table 2 for variable definitions.

21

Table 6 H2: Excess compensation regression results

Dependent Variable:

Direct Donations t

Top 10%

Salary Indicator t-1

Top 20%

Salary Indicator t-1

Top 25%

Salary Indicator t-1

Coefficient Coefficient Coefficient

p-value p-value p-value

Constant 2.427*** 2.965*** 3.078***

0.000 0.000 0.000

Test variable (Defined in

column heading) t-1

-0.250*** -0.343*** -0.328***

0.000 0.000 0.000

Program ratio t-1

2.615*** 2.460*** 2.425***

0.000 0.000 0.000

Operating Margin t-1 0.363*** 0.376*** 0.374***

0.000 0.000 0.000

Fundraising Expense t-1 0.618*** 0.602*** 0.600***

0.000 0.000 0.000

Total Assets t-1 0.222*** 0.215*** 0.212***

0.000 0.000 0.000

Government Grants t-1 -0.001 -0.001 -0.001

0.600 0.537 0.551

Program Service Revenue

t-1

-0.029*** -0.029*** -0.029***

0.000 0.000 0.000

Other Revenue t-1 0.007*** 0.006*** 0.006***

0.001 0.003 0.004

Organization Age t-1 -0.213*** -0.217*** -0.216***

0.000 0.000 0.000

N 7,040 7,040 7,040

Adjusted R2 0.653 0.657 0.657

*significant at 10% level, **significant at 5% level, ***significant at 1% level.

See Table 2 for variable definitions.

22

Table 7 Robustness: Yearly regressions and Fama MacBeth

Dependent

Variable: Direct

Donations t

2003 2004 2005 2006 2007 2008

Summary

(Fama

MacBeth)

Coefficient Coefficient Coefficient Coefficient Coefficient Coefficient Coefficient

p-value p-value p-value p-value p-value p-value p-value

Constant 4.521*** 3.736*** 3.180*** 3.853*** 2.910*** 3.148*** 3.558***

0.000 0.000 0.000 0.000 0.000 0.000 0.000

CEO Salary/Total

Expense t-1

-12.504*** -9.840*** -10.042*** -8.691*** -6.245*** -11.757*** -9.847***

0.000 0.000 0.000 0.000 0.010 0.000 0.000

Program ratio t-1

1.844*** 2.178*** 2.534*** 1.900*** 2.539*** 3.411*** 2.400***

0.000 0.000 0.000 0.000 0.000 0.000 0.000

Operating

Margin t-1

0.440*** 0.718*** 0.565*** 0.412*** 0.452*** 0.423*** 0.502***

0.000 0.000 0.000 0.000 0.002 0.000 0.000

Fundraising

Expense t-1

0.451*** 0.585*** 0.578*** 0.658*** 0.667*** 0.596*** 0.589***

0.000 0.000 0.000 0.000 0.000 0.000 0.000

Total Assets t-1 0.2994*** 0.215*** 0.235*** 0.133*** 0.151*** 0.182*** 0.202***

0.000 0.000 0.000 0.000 0.000 0.000 0.000

Government

Grants t-1

0.001 -0.006 -0.003 0.002 -0.001 -0.002 -0.001

0.716 0.113 0.326 0.480 0.827 0.526 0.309

Program Service

Revenue t-1

-0.042*** -0.037*** -0.036*** -0.018*** -0.022*** -0.030*** -0.031***

0.000 0.000 0.000 0.000 0.000 0.000 0.000

Other Revenue t-1 0.006 0.002 -0.001 0.007*** 0.011* 0.005 0.005**

0.213 0.656 0.911 0.000 0.060 0.228 0.025

Organization Age t-1 -0.216*** -0.227*** -0.214*** -0.173*** -0.218*** -0.283*** -0.222***

0.000 0.000 0.000 0.000 0.000 0.000 0.000

N 938 1,122 1,140 1,314 1,376 1,150 7,040

Adjusted R2 0.688 0.791 0.724 0.6914 0.546 0.716 0.680

*significant at 10% level, **significant at 5% level, ***significant at 1% level.

See Table 2 for variable definitions.

23

Table 8 Robustness: Industry regressions

Dependent Variable:

Direct Donations t

Education

(including

higher

education)

Health and

Human

Services

Arts, culture,

and

humanities

Environment International

Public and

societal

benefit

Religion

Coefficient Coefficient Coefficient Coefficient Coefficient Coefficient Coefficient

p-value p-value p-value p-value p-value p-value p-value

Constant 2.949*** 3.676*** 2.176*** 3.802*** -2.277** 5.597*** 9.664***

0.000 0.000 0.000 0.000 0.035 0.000 0.000

CEO Salary/Total

Expense t-1

-6.243*** -5.257*** -7.106*** -5.206*** -8.624** -21.122*** -16.381***

0.007 0.000 0.000 0.001 0.036 0.000 0.000

Program ratio t-1

0.953*** 2.651*** 0.895*** 1.459*** 6.881*** 2.833*** 0.298

0.000 0.000 0.000 0.000 0.000 0.000 0.759

Operating

Margin t-1

0.211** 0.300*** 0.576*** 0.287** 0.479** 0.209** 0.388

0.015 0.003 0.000 0.001 0.021 0.037 0.344

Fundraising Expense t-1 0.340*** 0.646*** 0.634*** 0.614*** 0.583*** 0.459*** 0.578***

0.000 0.000 0.000 0.000 0.000 0.000 0.000

Total Assets t-1 0.497*** 0.154*** 0.244*** 0.195*** 0.328*** 0.135*** 0.009

0.000 0.000 0.000 0.000 0.000 0.000 0.897

Government

Grants t-1

0.007** -0.004 -0.005 -0.004 -0.006 -0.004 0.023

0.018 0.227 0.217 0.299 0.361 0.387 0.442

Program Service Revenue

t-1

-0.054*** -0.020*** -0.014** -0.017*** 0.015* -0.001 -0.012

0.000 0.000 0.017 0.005 0.056 0.857 0.360

Other Revenue t-1 0.005 0.005 0.010*** 0.003 -0.035*** 0.006 0.040**

0.103 0.231 0.005 0.602 0.001 0.257 0.016

Organization Age t-1 -0.261*** -0.389*** 0.005 -0.208*** -0.089 -0.003 -0.575***

0.000 0.000 0.860 0.000 0.164 0.949 0.000

N 1,581 1,664 1,464 714 372 1,073 171

Adjusted R2 0.745 0.583 0.686 0.770 0.720 0.520 0.684

*significant at 10% level, **significant at 5% level, ***significant at 1% level.

See Table 2 for variable definitions.