The Hidden Cost of Financial Reform and Regulations on Banks and Their Clients The UNC Treasury...

70

The Hidden Cost of Financial Reform and Regulations on Banks and Their Clients The UNC Treasury Management Series October 1, 2012 Jeff Avers Group Vice President Treasury & Payment Solutions Liquidity Strategy & Consulting

-

Upload

sydney-scott -

Category

Documents

-

view

215 -

download

1

Transcript of The Hidden Cost of Financial Reform and Regulations on Banks and Their Clients The UNC Treasury...

The Hidden Cost of Financial Reform and Regulations on Banks and Their Clients

The UNC Treasury Management Series

October 1, 2012

Jeff Avers

Group Vice President

Treasury & Payment Solutions

Liquidity Strategy & Consulting

2

Financial Regulation and Your Business

Regulatory and Economic Environment

Corporate Governance

Working Capital Management

International

The Perfect Storm

Impact of Regulations

Reference Materials

Closing Remarks

3

Three Key Points for Today’s Financial Reform Discussion:

Financial Reform is complicated, widespread and painful

It will have a financial impact on both banks and their clients

It will have (and already has had) an impact on corporate and institutional liquidity management and payment practices

4

Regulatory Environment

5

Regulatory Environment

6

New regulatory entities created by Dodd-Frank

1. Consumer Financial Protection Bureau

2. Financial Stability Oversight Council

3. Office of Financial Research

4. Federal Insurance Office

5. Investor Advisory Committee

6. Office of Housing Counseling

7. Office of Minority and Women Inclusion

8. Office of Investor Advocate

9. Office of Credit Ratings

10.Office of Municipal Securities

11. Office of Whistleblower Protection

Entities eliminated by Dodd-Frank

1. Office of Thrift Supervision

Regulatory Environment

7

Regulatory Environment

8

Regulatory Environment

9

Regulatory Impact – A Sampling

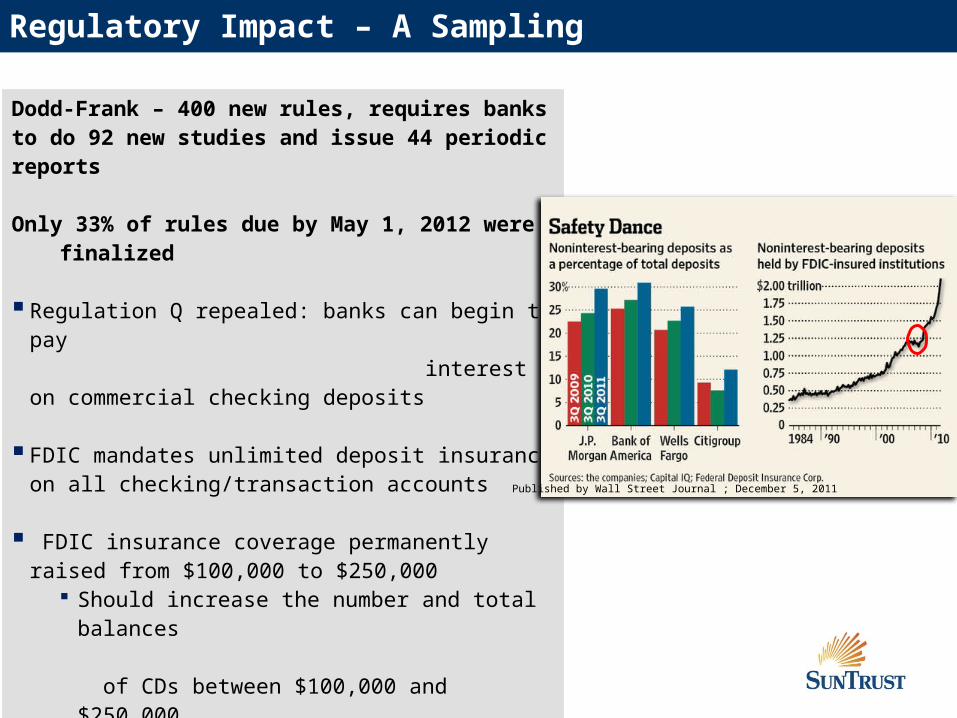

Dodd-Frank – 400 new rules, requires banks to do 92 new studies and issue 44 periodic reports

Only 33% of rules due by May 1, 2012 were finalized

Regulation Q repealed: banks can begin to pay interest on commercial checking deposits

FDIC mandates unlimited deposit insurance on all checking/transaction accounts

FDIC insurance coverage permanently raised from

$100,000 to $250,000 Should increase the number and total balances

of CDs between $100,000 and $250,000

FDIC deposit assessment changed from being based on quarterly ledger deposits to being based on consolidated assets minus average tangible equity

Published by Wall Street Journal ; December 5, 2011

10

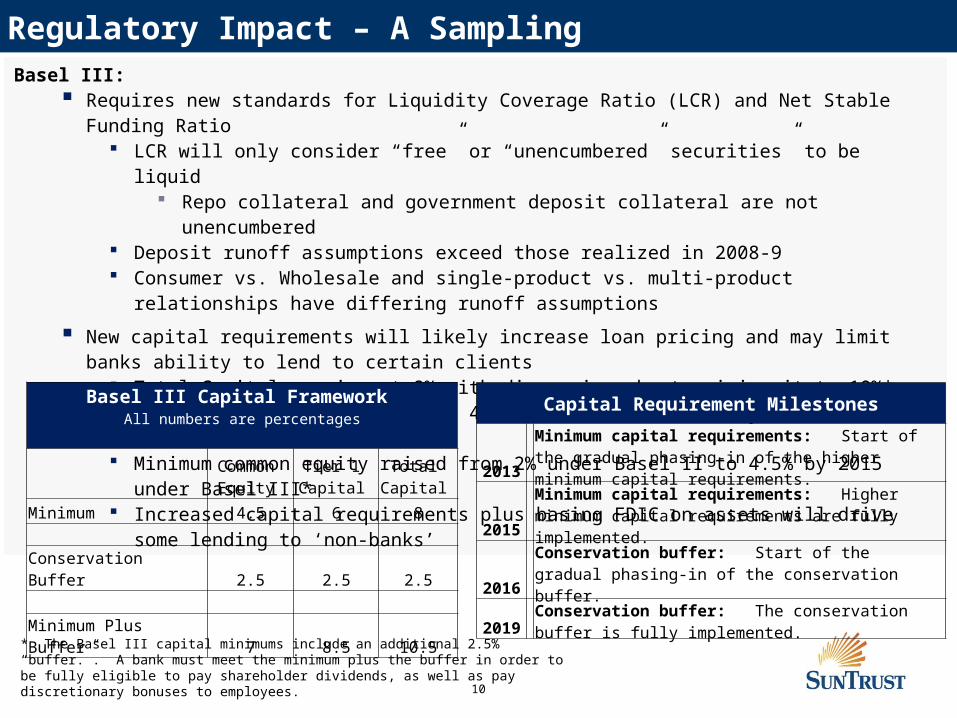

Regulatory Impact – A SamplingBasel III:

Requires new standards for Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio LCR will only consider “free” or “unencumbered” securities” to be liquid

Repo collateral and government deposit collateral are not unencumbered Deposit runoff assumptions exceed those realized in 2008-9 Consumer vs. Wholesale and single-product vs. multi-product relationships have differing runoff

assumptions

New capital requirements will likely increase loan pricing and may limit banks ability to lend to certain clients

Total Capital remains at 8% with discussion about raising it to 10%* Tier 1 Capital is raised from 4% under Basel II to 6% by 2015 under Basel III* Minimum common equity raised from 2% under Basel II to 4.5% by 2015 under Basel III* Increased capital requirements plus basing FDIC on assets will drive some lending to ‘non-

banks’

Basel III Capital Framework All numbers are percentages

Common

Equity Tier 1

Capital Total

Capital

Minimum 4.5 6 8

Conservation Buffer 2.5 2.5 2.5

Minimum Plus Buffer 7 8.5 10.5

* The Basel III capital minimums include an additional 2.5% “buffer.”. A bank must meet the minimum plus the buffer in order to be fully eligible to pay shareholder dividends, as well as pay discretionary bonuses to employees.

Capital Requirement Milestones

2013 Minimum capital requirements: Start of the gradual phasing-in of the higher minimum capital requirements.

2015 Minimum capital requirements: Higher minimum capital requirements are fully implemented.

2016 Conservation buffer: Start of the gradual phasing-in of the conservation buffer.

2019 Conservation buffer: The conservation buffer is fully implemented.

11

Impact of Money Fund Reform

Regulatory Changes Impact

2010 Changes

Maximum allowable weighted average maturity (WAM) was shortened from 90 days to 60 days

The overall credit quality of portfolios was improved, and A twofold liquidity requirement was added… with 30% of

assets maturing within a week and 10% required to mature overnight

Lessened investor risk, while also lowering the relative yield on a permanent basis

SEC Currently Proposed Changes

Maintain a capital buffer in order to serve as the first point of loss absorption to the extent required

Convert from $1.00 NAV to a Variable NAV, and Restrict redemptions so that up to 10% of a redemption is

held back for up to 30-days

SEC Recent Compromise Proposal

Rather than implement all proposed changes, each 2a-7 money fund must either:

Convert from $1.00 NAV to variable NAV, or Maintain $1.00 NAV and implement the capital buffer and

restrictions on redemptions described above

Likely Net Overall Effect Lessens investor risk Lowers the relative yield Reduces investor appetite leading to:

Decreased MMF investment assets Increased bank deposits Funding concerns for FI and Corporate issuers

SEC Money Market Fund Rule 2a-7 was changed in 2010 to reduce shareholder/investor investment risk

12

Financial Impact – A Sampling

Higher interest expense on deposits Reduced Revenue Streams Volcker Rule Potential divestitures

Reduced Fee Income NSF/Overdrafts (Regulation E) Debit Interchange (Durbin

Amendment)

Revamped marketing collateral

Increased Fees Uncollateralized daylight overdrafts FDIC

Client communication costs

Development costs for new products Employee training

Reduced value of deposits (“FTP”) Increased cost of compliance & oversight Human, Systems, tracking and reporting

Increased emphasis on eliminating marginally profitable and unprofitable relationships

Increased Bank Expenses Increased Customer Expenses

Discontinuation of “Free Checking”

13 13

Market Rates for Cash Investment Instruments

Alternative Cash Investment Options

• Rates obtained from (1) WSJ Money Rates, (2) Crane Data (money funds) and (3) State-specific LGIPs

SunTrust Sweep Yields

As of August 31, 2012

Master Note 35/20 bps

Repo 3 bps

Eurodollar 10 bps

Federated Prime Fund 4 bps

Federated Treasury

Fund

1 bps

Overall market rates have been cyclical over the last 2 years

Most money market instruments are currently in the top half of their 52 week High-Low range

While overnight rates are similar to those in the summer of 2010, with the exception of Libor, 30-day and 90-day rates bare more similarity to the summer of 2011

The “Greek situation” has caused a flight to safety, suppressing the yield on US Treasuries

Money Market Mutual Fund yields continue to be anemic

Short-term Investment Instrument Rate as of 7/19/2010*

Rate as of 7/13/2011*

Rates as of 9/14/2012*

52-Week*

Overnight Instruments Low High

Fed Funds 20 bps 6 bps 19 bps 6 bps 19 bps

Repo 25 bps 2 bps 33 bps 3 bps 33 bps

SunTrust ECR (Analyzed Business Checking) Ask Your SunTrust Treasury Management Representative

SunTrust ECR/Rate Paid (Analyzed Interest Checking) Ask Your SunTrust Treasury Management Representative

30-Day Instruments 9/14/2012* Low High

Treasuries 15 bps 2 bps 9 bps 0 bps 11 bps

Commercial Paper 29 bps 12 bps 7 bps 3 bps 13 bps

Eurodollars 25 bps 12 bps 12 bps 12 bps 23 bps

Libor 33.8 bps 18.7 bps 22 bps 20.5 bps 29.6 bps

SunTrust Money Market Account Rate Ask Your SunTrust Treasury Management Representative

90-Day Instruments 7/19/2010 7/13/2011 9/14/2012* Low High

Treasuries 15 bps 3 bps 10 bps 0.5 bps 11.5 bps

Commercial Paper 42 bps 15 bps 16 bps 12 bps 20 bps

Libor 51.25 bps 24.9 bps 38.5 bps 26.8 bps 58.25 bp

Eurodollars 45 bps 15 bps 20 bps 20 bps 28 bps

AAA-Rated Taxable Money Funds: 7-day Yield as of 6/30/2010 6/30/2011 8/31/2012 Low High

Crane Treasury Institutional MF Index 1 bps 1 bps 1 bps 1 bps 1 bps

Crane AAA Prime Institutional MF Index 12 bps 4 bps 8 bps 7 bps 10 bps

Local Government Investment Pools: Monthly Yield as of:

July 2010 June 2011 Aug 2012 Low High

Georgia Fund 1 LGIP (Monthly yield) 21 bps 13 bps 15 bps 9 bps 15 bps

Florida Prime LGIP (Monthly yield) 39 bps 23 bps 30 bps 21 bps 33 bps

14

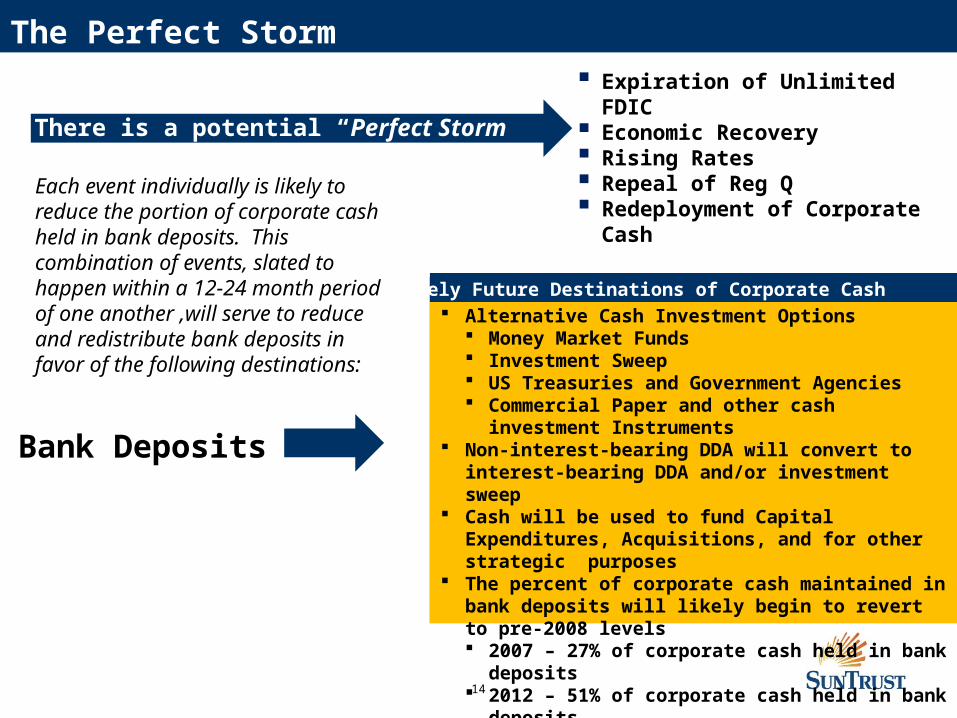

The Perfect Storm Expiration of Unlimited FDIC Economic Recovery Rising Rates Repeal of Reg Q Redeployment of Corporate Cash

There is a potential “Perfect Storm” brewing

Each event individually is likely to reduce the portion of corporate cash held in bank deposits. This combination of events, slated to happen within a 12-24 month period of one another ,will serve to reduce and redistribute bank deposits in favor of the following destinations:

Bank Deposits

Alternative Cash Investment Options Money Market Funds Investment Sweep US Treasuries and Government Agencies Commercial Paper and other cash investment

Instruments Non-interest-bearing DDA will convert to interest-

bearing DDA and/or investment sweep Cash will be used to fund Capital Expenditures,

Acquisitions, and for other strategic purposes The percent of corporate cash maintained in bank

deposits will likely begin to revert to pre-2008 levels 2007 – 27% of corporate cash held in bank deposits 2012 – 51% of corporate cash held in bank deposits

Likely Future Destinations of Corporate Cash Likely Future Destinations of Corporate Cash

15

Unlimited FDIC and the DDA Bubble

Destination* AllRev

< $1B

Rev >

$1B

Net Borrower

Net Investor

No Significant Change to DDA

59% 61% 58% 64% 53%

Prime MMF 17 11 24 20 16

Treasury MMF 16 14 19 16 17

Treasury/Agencies 14 21 10 9 23

Repo 6 9 4 7 5

Other 8 5 10 4 11

* Source: 2012 AFP Liquidity Survey

Possible Destinations of Non-Interest-Bearing DDA at End of 2012:

16

New Regulations Could Drive $1.5T onto Bank Balance Sheets

When interest rates rise, we could see an additional $1.5 trillion flow back onto bank balance sheets . In other post and non-Reg Q countries, companies hold as much as 50 - 70% of total liquidity in bank

deposits In addition to Reg Q repeal, two current regulations could potentially drive even more liquidity back into

the banking system - changes to 2a-7 regulations and collateral requirements for derivatives trading

In U.S., 25% of Corporate Liquidity = $1.3T

0%

10%

20%

30%

40%

50%

60%

70%

80%

U.S. France UK

Reg Q Post Reg Q No Reg Q

Percentage of Total Corporate Liquidity Held in Bank Deposits*

* Bank Deposits Defined as:DDA/Current Accounts, Offshore Deposits, Time Deposits/CDs, Savings/MMDAs and Sweep Accounts

This is a positive outcome for U.S. banks only if loan demand catches up to deposit growth

Impact of Reg Q Repeal

A Likely Unintended Consequence of Reg Q Repeal

For the typical treasury management bank, 60-70% of the revenue and 80-90% of profit comes from the spread on non-interest-bearing deposits

The Banking Industry will likely need to revise the pricing structure of the Treasury Management business in order to reflect the impact on revenue and profitability of the Repeal of Reg Q and the associated reduction or elimination of non-interest-bearing deposits

•Source: 2010 Treasury Strategies’ proprietary research; Commercial Deposit/Sweep Study & Global Corporate Liquidity Research

¹ Repealed in 2011, Regulation Q was a 1930s Depression Era regulation that disallowed banks from paying interest on commercial checking accounts

¹

17

The Economic Recovery May be Funded by Cash

Percent of Companies Self-Funding their 2010 and 2011 Capital Expenditures and Planning to Self-Fund in 2012

Redeploying Cash vs. Borrowing to Fund Capital Expenditures

Given the build-up of cash over the last 3-4 years, companies have been self-funding a major portion of their capital expenditures… and are likely to do so going forward

Banks usually benefit from an economic recovery through the expansion of their lending and/or underwriting activity… which may be slow in coming this time

Source: Greenwich Market Pulse, January 2012

18

Deposit Investment Allocations May Return to Pre-2008 Levels

18

Cash investors have been increasing their allocation to bank deposits over the last six years, while simultaneously decreasing their allocation to money market mutual funds

With more certainty around the future of money market funds, when rates begin to rise cash investors are likely to reallocate their portfolios to be weighted no more than 25-30% in bank deposits, which is consistent with pre-2009 levels

1

Source: 2012 AFP Liquidity Survey

19

Post Reg Q Repeal, the Primary Purpose of Sweep Has Changed

Primary Purpose of SweepOld Paradigm Post-Reg Q

Obtain yield on idle cash balances Diversify away from bank risk Obtain yield in excess of interest-bearing DDA

Predominant Sweep Vehicles

Money Funds Eurodollar Deposits Repo Bank Parent Commercial Paper

Repo (eliminate credit risk) Money Funds (diversify away from bank risk) Bank Parent CP (yield enhancement) Alternative ‘off balance sheet’ products

The Future of Sweep

Source: Treasury Strategies’ proprietary research; Commercial Deposit/Sweep Study & Global Corporate Liquidity Research

$-

$100

$200

$300

$400

$500

$600

$700

$800

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 YTD

Total U.S. Sweep Balances ($B)

20

Corporate Governance

2011 SEC Enforcement Activity

735 total enforcement actions

89 actions for financial fraud and issuer disclosure violations

57 actions filed for insider trading

Compare to total of 9 cases for 2010, and 3 cases for 2009

21

Working Capital Management: Payments

ACH Same-day Settlement

Mobile Payments

ISO 20022 – Wire Remittance

ACH Secure Vault/Credit Push

Post-Durbin/Dodd-Frank

Durbin Amendment

PPACA

Credit Card Act of 1990

22

Working Capital Management: Liquidity

FDIC Coverage and Expense

Repeal of Reg Q

Sweep Investment Disclosures

Money Fund Reform

Change in Allocation of Corporate Cash Investments

Counterparty Risk

Banks and Broker-Dealers

Corporate/Non-FI

The TED Spread

Liquidity: The Lifeblood of Business

23

Working Capital Management: Liquidity

December 1998 – December 2009

The Ted SpreadCalculated as the difference between three-month LIBOR and the three-month T-bill interest rate, the TED spread is an indicator of perceived credit risk in the general economy -- and in particular, the credit risk within the banking sector.

When the TED spread increases, lenders believe the risk of default on interbank loans (counterparty risk) is increasing

When the risk of bank defaults is considered to be decreasing, the TED spread decreases

The long term average of the TED has been 30 basis points with a maximum of 50 bps. During 2007 the TED Spread ballooned to 150-200 bps, in reaction to the subprime mortgage crisis On September 17, 2008, the TED spread exceeded 300 bps, breaking the previous record set after the

Black Monday crash of 1987 In the midst of the fall 2008 credit and liquidity crisis, On October 10, 2008, the TED spread reached

another all-time high of 457 basis points on October 10, 2008 The Ted Spread returned to normal levels in 2010 and has remained there since

September 2008 – June 2011

TED-Spread

24

International

Europe

BASEL III

Stability of European Union

SEPA - 2014

European Payments Council

SWIFT

25

Impact of Basel III

International

26

Eurozone

SWOT Analysis: SEPA

Strengths for Payers Weaknesses (Challenges) for Existing Providers

Opportunities for Global FIs Threats to Existing Providers

Economic, Payments & Liquidity Environment

0.710.715

0.720.725

0.730.735

0.740.745

0.750.755

0.76

07-N

ov-1

1

09-N

ov-1

1

11-N

ov-1

1

13-N

ov-1

1

15-N

ov-1

1

17-N

ov-1

1

19-N

ov-1

1

21-N

ov-1

1

23-N

ov-1

1

25-N

ov-1

1

27-N

ov-1

1

29-N

ov-1

1

01-D

ec-1

1

03-D

ec-1

1

05-D

ec-1

1

USD-EURO Exchange RateOverview of SEPA

The main objectives are:Standardization and straight-through processing of euro paymentsEliminate the distinction between domestic and cross-border international

payments within the SEPA Eurozone… creates a payment environment similar in concept to the domestic US

Improve efficiencies and provide cost reduction to payers Estimated to save payers €29 to €40 billion in transaction and

settlement costs, all of which is to the detriment of bank revenues Improved surveillance and transparency of payment flows at the expense

of money laundering and organized crime

SEPA has the potential to recast the payments competitive landscape in Europe

Lower cost of transacting business Operational efficiencies achieved Potential to consolidate payments/receipts with fewer

providers

Represents a significant hit to revenue Requires new investment in infrastructure Changes the economics of the payments business

Likely to alter the landscape of the payments business Volume and revenue is likely to shift away from small providers

in favor of large regional and global providers Will cause some providers to exit the payments business, and

others to limit their involvement as a full service provider Opens the door for non-European global banks to become

major players in the Eurozone payments business

Unique opportunity to gain market share in a major global region

Potential to become a primary provider for in-country MNCs Ability to leverage existing technology & innovation reputation Turmoil in Europe provides the opportunity to leverage

balance sheet strength as a key selling point concerning counter-party risk and future investment in technology

27

“These new regulations will fundamentally change the way we get around them.”

Closing Remarks

28

Summary of Today’s Discussions

Financial reform is complicated, widespread and painful

It will have a financial impact on both banks and their clients

Financial reform will have (and already has had) an impact on corporate and institutional liquidity management and payment practices

Closing Remarks

29

ResourcesPublications / epages

AFP Status Update of Current Issues (301.907.2862)

AFP Pulse & Membership (301.907.2862)

AFP’s Homepage: //www.AFPonline.org

Treasury Strategies (www.Treasurystrategies.com)

Federal Reserve Homepage: //www.federalreserve.gov

FDIC Homepage: //www.fdic.gov

NACHA: //www.nacha.org

American Banker (800.221.1809)

SWIFT: //www.swift.com

ISO: //

Wikipedia.com

Investopedia.comw

The Hidden Cost of Bank Regulations on Your Business

The UNC Treasury Management Series October 1, 2012

2:15-3:30 p.m.

Nick Alex

Senior Vice President, Director of Product Management

Treasury & Payment Solutions

SunTrust

The Hidden Cost of Bank Regulations on Your Business reviews the new world of rules and regulations that define how treasury managers must carry out their duties. This session covers a wide range of legal and regulatory issues, including corporate governance, IRS guidelines for business tax payments, HIPAA and SEC interventions. It concludes with an intermediate term outlook for what else may be coming.

31

32

33

34

Regulatory Environment

35

Only 110 of the 398 rule-making requirements mandated by Dodd-Frank have been finalized; 144 have not yet been proposed

Deadlines have been missed for 148

Regulatory Environment

36

37

38

NOTE: SOME RULEMAKINGS ARE ISSUED JOINTLY AND ARE COUNTED UNDER BOTH CATEGORIES

40

41

Regulatory EnvironmentCurrent Economic Context Uncertain regulatory environment

U.S. presidential election Dodd-Frank regulatory reform

Volker Rule

European economic stability

Sovereign debt

Austerity measures

Other recent legislative changes

Consumer Financial Protection Bureau (CFPB)

PPACA

42

43

Regulatory Environment

Current Economic Context Uncertain regulatory environment

Dodd-Frank Regulatory Reform Volker Rule Consumer Financial Protection Bureau

Other recent legislative changes

Durbin Rule PPACA Credit CARD Act of 2009 American Reinvestment and

Recovery Act of 2009

44

Regulatory EnvironmentCurrent Economic Context Uncertain regulatory environment

Dodd-Frank Regulatory Reform Volker Rule Consumer Financial Protection Bureau

Other recent legislative changes

Durbin Rule PPACA Credit CARD Act of 2009 American Reinvestment and

Recovery Act of 2009

45

Regulatory EnvironmentCurrent Economic Context Uncertain regulatory environment

Dodd-Frank Regulatory Reform Volker Rule effective July 21, 2012 Consumer Financial Protection Bureau

Other recent legislative changes

Durbin Rule PPACA Credit CARD Act of 2009 American Reinvestment and

Recovery Act of 2009

46

Dodd-Frank in Detail Reg Q was repealed, allowing banks to pay interest on Checking

Accounts (effective July 21, 2011)

$250k FDIC insured cap now permanent (up from $100k)

Regulatory Environment

Unlimited Insurance mandated on non-interest bearing checking accounts, set to expire December 31, 2012

The TED Spread, representing the rates banks charge each other to borrow money, appears to be settling into a pre-crisis pattern

47

2007 2008 2009 2010 2011 2012 JUL1000

1200

1400

1600

1800

2000

2200

2400

M1 Money Supply

Bil

lio

ns

of

Do

llar

sRegulatory Environment

Current Economic Context

The M1 Money Supply Line has shown a sharp increase since the credit crisis in 2008

48

49

Impact of Regulations

Dodd-FrankDurbin Amendment

FDIC Coverage

Revenue

Cost

50

51

Corporate Governance

2011 SEC Enforcement Activity

735 total enforcement actions

89 actions for financial fraud and issuer disclosure violations

57 actions filed for insider trading

Compare to total of 9 cases for 2010, and 3 cases for 2009

52

53

Privacy

Overlapping regulations including GLB, FCRA, FACTA, Bank Secrecy, USA PATRIOT Act, HIPAA, etc.

Overlapping regulators including the Federal Reserve, FDIC, OCC, SEC, FCC, various state agencies, etc.

800 breaches reported in 2011 (compared to 622 for all of 2010)

Remediation and recovery costs of over $200 per compromised record

54

55

PrivacyPCI-DSS and PA-DSS Compliance Worldwide security standards created and managed by the

Payment Card Industry Security Standards Council (PCI SSC)

Version 2.0

HIPAA and HITECH

Changes to HIPAA under the new healthcare reform law

HITECH provisions of ARRA

56

57

58

InternationalEurope

BASEL III

Stability of European Union

SEPA - 2014

European Payments Council

SWIFT

59

60

61

62

63

Impact of Basel III

64

65

InternationalCompetition and Cooperation

International Monetary Policy Coordination

Ongoing central bank support Legislative activity Liquidity support

International coordination to manage national funds rates

G20 Summits

66

“These new regulations will fundamentally change the way we get around them.”

67

Working Capital Management

Payments

ACH Same-day Settlement

Mobile Payments

ISO 20022 – Wire Remittance

ACH Secure Vault/Credit Push

Post-Durbin/Dodd-Frank

Durbin Amendment

PPACA

Credit Card Act of 1990

68

Working Capital Management

Liquidity

FDIC Coverage and Expense

Repeal of Reg Q

Sweep Investment Disclosures

Money Fund Reform

Change in Allocation of Corporate Cash Investments

69

71

Resources

Publications / Homepages

AFP Status Update of Current Issues (301.907.2862)

AFP Pulse & Membership (301.907.2862)

AFP’s Homepage: //www.AFPonline.org

Federal Reserve Homepage: //www.federalreserve.gov

FDIC Homepage: //www.fdic.gov

NACHA: //www.nacha.org

American Banker (800.221.1809)

SWIFT: //www.swift.com

ISO: //www.iso.or