The Energy Review - Contraction and Convergence … E XECUTIVE S UMMARY EXECUTIVE SUMMARY Key points...

218

A PERFORMANCE AND INNOVATION UNIT REPORT – FEBRUARY 2002 The Energy Review CABINET OFFICE

Transcript of The Energy Review - Contraction and Convergence … E XECUTIVE S UMMARY EXECUTIVE SUMMARY Key points...

A PERFORMANCE AND INNOVATION UNIT REPORT – FEBRUARY 2002

The Energy Review

Performance and Innovation UnitCabinet OfficeFourth FloorAdmiralty ArchThe MailLondon SW1A 2WHTelephone 020 7276 1416Fax 020 7276 1407E-mail [email protected]

© Crown copyright 2002

Publication date February 2002

This report is printed on Revive Matt material. It is made from 75% recycledde-inked post-consumer waste, is totally chlorine free and fully recyclable.

The text in this document may be reproduced free of charge in any format or media without requiring specific permission. This is subject to the materialnot being used in a derogatory manner or in a misleading context. The source of the material must be acknowledged as Crown copyright and the titleof the document must be included when being reproduced as part of another publication or service.

Th

e Energ

y Review

A PERFO

RMA

NC

E AN

D IN

NO

VATION

UN

IT REPORT – FEBRU

ARY 2002

CABINETOFFICE

CONTENTS

1

CONTENTS

Draft Foreword by the Prime Minister 3

Executive Summary 5

Chapter 1: Introduction 15

Chapter 2: The Challenge Ahead 19

Chapter 3: Framework 32

Chapter 4: Security in the Energy System 53

Chapter 5: Lessons from Scenarios 81

Chapter 6: Options for a Low Carbon Economy 93

Chapter 7: A Programme for a Low Carbon Future 109

Appendix to Chapter 7: Institutional Barriers 136

Chapter 8: Institutions 141

Chapter 9: Concluding Themes 155

Chapter 10: Implementing the Recommendations 161

Annexes

Annex 1: The Role of the Performance and Innovation Unit 168

Annex 2: Project Team, Sponsor Minister and Advisory Group 169

Annex 3: Organisations Consulted and Submissions Received 171

Annex 4: Impact of Energy Review Recommendations on Fuel Poverty 180

Annex 5: Energy Efficiency: The Basis for Intervention 182

Annex 6: The Potential for Cost Reductions and Technological Progress inLow Carbon Technologies 188

Annex 7: Timelines Affecting Decisions 200

Annex 8: Chief Scientific Adviser’s Energy Research Review:

Summary and Recommendations 206

Annex 9: Glossary 209

Annex 10: References 213

FOREWORD BY THE PRIME MINISTER

3

FOREWORD

Energy underpins our daily lives: it lights our streets, heats our homes,powers our industry, and fuels our vehicles. That’s why securing cheap,reliable and sustainable sources of energy supply has long been a majorconcern for governments.

However, the energy sector is constantly changing.

The last few decades have witnessed the development of North Sea oiland gas reserves; privatisation and liberalisation in the energy sector; ashift towards gas for electricity generation; and the emergence of newrenewable technologies. Electricity prices are now cheaper, and carbondioxide emissions are lower, than 10 years ago.

There is no reason to expect that the pace of change will slow. And thereare added challenges – climate change and, for the UK, resourcedepletion in particular – to which our energy policy needs to respond.That is why I asked the Performance and Innovation Unit to examine thelong-term challenges for energy policy in the UK, and to set out howenergy policy can ensure competitiveness, security and affordability in thefuture.

Their report looks to 2020 and beyond to 2050, sets out the key trends,and explains the choices that we face. It is difficult to predict thetechnological, economic and geopolitical changes that will take placeduring that time – and the report does not try to do so. But it makes clearhow important it is to keep our options open, so that we can respondpositively to changing circumstances.

Three issues stand out from the analysis:

● Diversity and security of supply are no longer only a matter of ensuringa balance of energy sources within the UK. Increased reliance onimports from Europe and elsewhere underlines the need to integrateour energy concerns into our foreign policy.

● Alongside low prices and secure supplies, climate change has become acentral aspect of energy policy. Achieving global emission reductionswill need major technological innovation, and I am convinced that theUK would benefit from being ahead of the game in moving to cleanand low carbon technologies and in sharply improving ourperformance on energy efficiency.

● It is striking that both security of supply and climate change issues aretruly international. The UK cannot therefore only act through domesticpolicies, but must address these issues via international policies and

4

agreement, particularly through EU market liberalisation and the Kyotoagreements.

This report is being published as a report to government, and as such isnot a statement of government policy. However, I believe the report raisesmany of the issues we need to discuss as we develop our energy policy.

I hope that this report will launch a thorough debate. The Governmentwill consult shortly on the issues raised in the report and will set out itsdetailed response in an Energy White Paper later in the year.

5

EXECUTIVESUMMARY

EXECUTIVE SUMMARY

Key pointsTrends in energy markets have been comparatively benign over the past 10–15 years: the UKhas been self-sufficient in energy; commercial decisions have resulted in changes in the fuel mixthat have reduced UK emissions of greenhouse gases; and trends in world markets anddomestic liberalisation have reduced most fuel prices.

The future context for energy policy will be different. The UK will be increasingly dependent onimported oil and gas. The Californian crisis has highlighted the importance of putting in placethe right incentives for investment in energy infrastructure. And the UK is likely to faceincreasingly demanding greenhouse gas reduction targets as a result of international action,which will not be achieved through commercial decisions alone.

The introduction of liberalised and competitive energy markets in the UK has been a success,and this should provide a cornerstone of future policy.

But new challenges require new policies. The policy framework should address all threeobjectives of sustainable development – economic, environmental and social – as well as energysecurity. Climate change objectives must largely be achieved through the energy system. Whereenergy policy decisions involve trade-offs between environmental and other objectives, thenenvironmental objectives will tend to take preference.

Key policy principles should be: to create and to keep open options to meet future challenges;to avoid locking prematurely into options that may prove costly; and to maintain flexibility inthe face of uncertainty. Increasingly policy towards energy security, technological innovationand climate change will be pursued in a global arena, as part of an international effort.

Within the UK, the overall aim should be the pursuit of secure and competitively priced meansof meeting our energy needs, subject to the achievement of an environmentally sustainableenergy system.

The UK’s future energy strategy should have the following elements:

(i) energy security should be addressed by a variety of means, including enhancedinternational activity and continued monitoring. However, there appear to be no pressingproblems connected with increased dependence on gas, including gas imported fromoverseas. The liberalisation of European gas markets will make an important contributionto security;

(ii) continued attention to long-term incentives is needed, though recent levels of investmentin the energy industries have been healthy;

(iii) there is a strong likelihood that the UK will need to make very large carbon emissionreductions over the next century. However, it would make no sense for the UK to incurlarge abatement costs, harming its international competitiveness, if other countries werenot doing the same;

Recent trends in energymarkets have been benign forpolicyIn recent decades, the context for energy policyin the UK has been remarkably benign. The UKis currently one of just two G7 countries whichis self-sufficient in energy. Energy prices havegenerally been falling in real terms, partlybecause world oil prices have fallen and partlybecause of the successful liberalisation of UKgas and electricity markets. UK industry andconsumers, including the fuel poor, havegained. And the UK has found it easier thanmany other countries to achieve greenhousegas reductions – the “dash for gas” in particular(which was driven by commercial decisions)reduced carbon emissions from electricitygeneration.

But the future context will bemuch more challengingThe future for energy policy seems likely to bemuch less benign for two reasons:

● issues of energy security are likely to becomemore important. The UK will becomeincreasingly dependent on imported oil andgas. And the Californian energy crisis hashighlighted the importance of gettingincentives for new investment in energyright;

● the UK is likely to face increasinglydemanding carbon reduction targets. A lowcarbon future, if it were to be adopted, couldnot be achieved on the basis of spontaneouschanges within the energy system, especiallywhen at present, one low carbon source,

6

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

(iv) keeping options open will require support and encouragement for innovation in a broadrange of energy technologies. The focus of UK policy should be to establish new sources ofenergy which are, or can be, low cost and low carbon;

(v) the immediate priorities of energy policy are likely to be most cost-effectively served bypromoting energy efficiency and expanding the role of renewables. However, the optionsof new investment in nuclear power and in clean coal (through carbon sequestration) needto be kept open, and practical measures taken to do this;

(vi) the Government should use economic instruments to bring home the cost of carbonemissions to all energy users and enable UK firms to participate in international carbontrading. Achieving deep cuts in carbon would require action well beyond the electricitysector where cuts have been concentrated in recent years;

(vii) step changes in energy efficiency and vehicle efficiency are needed, with new targets forboth. In the domestic sector, the Government should target a 20% improvement in energyefficiency by 2010 and a further 20% in the following decade;

(viii) the target for the proportion of electricity generated from renewable sources should beincreased to 20% by 2020;

(ix) institutional barriers to renewable and combined heat and power investments should beaddressed urgently; and

(x) the Government should create a new cross-cutting Sustainable Energy Policy Unit to drawtogether all dimensions of energy policy in the UK.

In the light of this review, the Government should initiate a national public debate aboutsustainable energy, including the roles of nuclear power and renewables.

nuclear power, faces a progressive run-downas existing plant reach the end of their livesand are decommissioned.

In addition, although good progress is beingmade towards the elimination of fuel poverty,many people continue to spend a substantialproportion of their income on fuel, largely as aresult of the age and energy inefficiency of thehousing stock.

New challenges require newpoliciesThe introduction of liberalised and competitiveenergy markets in the UK has been a success,and competitive markets should continue toform the cornerstone of energy policy. But newchallenges require new approaches. The futureframework for energy policy needs to addressall three objectives of sustainable development– environmental, economic and social – as wellas energy security. But climate changeobjectives must largely be achieved through theenergy system.

Consistent with this, the future aim of energypolicy should be the pursuit of secure andcompetitively priced means of meeting the UK’senergy needs, subject to the achievement of anenvironmentally sustainable energy system.

The strategy articulated in this review thus hasthree main dimensions:

● measures to address the security of theenergy system;

● measures to ensure the energy system isenvironmentally sustainable – these areintended in particular to create options toput the UK on a path to a low carboneconomy; and

● approaches which take full account of thepotential costs of achieving the objectives ofpolicy, in terms of higher energy bills.

Concerns about security needto be addressedThere are a number of reasons why security ison the agenda. These include:

● the Californian experience of electricityblackouts;

● concerns resulting from the terrorist attacksin the USA of September 11; and

● the sensitivity to the UK’s future need toimport gas, possibly across long pipelinesand from trading partners who seem to offerless security than we are used to.

There is general agreement that a diverseenergy system – both in terms of types ofenergy and their sources – can benefit security.Some people argue that self-sufficiency isneeded for security. But this is not necessarilyso. As in other markets, imports can be avaluable means of increasing diversity andreducing risks – most other G7 countriesalready rely substantially on imported energy.Some submissions to the review have suggestedthat the Government should decide the fuelmix to be used for electricity generation. Thisreview has rejected these proposals on thegrounds that they would seriously distort theefficient functioning of energy markets.

Instead, the approach taken is to view issues ofsecurity in risk management terms. Some risksare essentially international, others domestic.

There are three main ways to safeguard security:

● to make maximum use of competitivemarkets to meet customers’ needs. A keyconclusion of the review is that theliberalisation of EU gas and electricity marketsis important for energy security. Liberalisationwould add flexibility and depth to Europeanenergy markets, increasing substantially theresilience of the energy system;

● to create a more resilient and flexible energysystem. The review considers various optionsfor enhancing the resilience of the UK energy

7

EXECUTIVESUMMARY

system, including increased gas storage;greater use of liquid natural gas (LNG); andgreater ability to use coal than wouldotherwise be the case. In the first instance,these are matters for market participants toaddress. The role of government should beto monitor the actions of market participants;to remove any barriers due to policies, suchas the planning system; and to intervenedirectly, as a last resort, where there is clearevidence of market failure and where thebenefits of intervention are likely to outweighthe costs; and

● to use international action to address globalthreats to energy security. On just about anyscenario the UK will become moredependent on imports both for both its gasand its oil. There is little risk of there beinginsufficient gas available internationally: thereis plenty, and 70% of the world supplies canbe accessed from Europe. But the UK cannotbe sanguine about the path that the gas willtake from its source to the European marketand the risks it may encounter en route.Particular concerns are:

● the level of investment in the exportingcountries;

● investment in the transit countries; and

● facility failure overseas.

These risks need to be monitored. They areoutside the direct control of UK purchasers orthe UK Government. The key is to developstrong links with trading partners, so that theUK can ensure that the benefits associated withtrade are mutually recognised and delivered.

Making sure suppliers face theright investment incentives isessential The other main area of risk to energy security isthe set of issues which arise as a result of theCalifornian experience. Supplies of electricity

were interrupted because insufficientinvestment had been made both in the networkand in electricity generation. The Californianproblems were very specific to that state andwere due in considerable measure to failures inregulation, which have no parallels in the UK.

Present levels of capacity in the UK in bothelectricity and gas networks and in electricitygeneration are healthy. The processes ofprivatisation and liberalisation seem to havesucceeded well. Even so, the situation needs tobe monitored since future investment might beconstrained if the wrong signals and incentivescome through the regulatory structures. Butthere is no reason for immediate concern. Careis also needed to ensure that the anticipation ofpublic intervention does not lead the privatesector to hold back its own investment plans.

Moving to a low carboneconomy poses a majorpotential challengeLooking to the longer-term, the centralquestion for energy policy is the weight to begiven to environmental and other objectives.The strong likelihood of a stringent greenhousegas target being adopted in the future issufficient to justify giving the environmentalobjective a strong priority within future energypolicy – especially since the energy system isthe source of 80% of UK greenhouse gases and95% of CO2. Low carbon options also have themerit that, particularly where they are local anddispersed, they generally contribute to thesecurity of the energy system.

This review has not considered the scientificcase for carbon reductions – this was the task ofthe Royal Commission on EnvironmentalPollution (RCEP), and of bodies such as theIntergovernmental Panel on Climate Change(IPCC). Neither has the review conducted acost-benefit analysis of the different ways ofresponding to the challenge: this is a matter for

8

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

the international community as a whole. Thereis a lot of work on the possible overall costs tothe economy of meeting a substantial carbonreduction target. Most estimates suggest thatthe impacts on GDP are likely to be small –though precise costs will depend on themethods chosen to reduce carbon, the rate oftechnical progress, and the scope for tradingreductions elsewhere in the world.

Possible future energy worlds in 2020 and 2050have been analysed using scenarios. Crediblescenarios for 2050 can deliver a 60% cut in CO2

emissions, but large changes would be neededboth in the energy system and in society. Twoopportunities stand out. Substantialimprovements in domestic and business energyefficiency could be made, and there areprospects for significant improvements inenergy efficiency in the transport system. Yeteven if these improvements can be achieved,and even if the electricity system was toproduce no carbon whatsoever, a 60% cut inCO2 emissions could only be met if we werealso to go on to make very large reductions inthe use of fossil fuels as the main means ofpowering future vehicles. This shows the scaleof the challenge.

The Government will need to make decisionsabout its longer-term approach to carbonreducing policies in the light of the UK’sinternational commitments. The RCEP hasproposed that the UK should adopt a strategywhich puts the UK on a path to reducing CO2

emissions by 60% from current levels by 2050.This would be in line with a global agreementwhich set an upper limit for the CO2

concentration in the atmosphere of some 550ppmv. It would be unwise for the UK now totake a unilateral decision to meet the RCEPtarget, in advance of international negotiationson longer term targets. Greenhouse gases areglobal pollutants, and it would make no senseto incur abatement costs in the UK and therebyharm our international competitiveness, ifothers were not contributing.

Given the strong chance that future, legallybinding, international targets will become morestringent beyond 2012, a precautionaryapproach suggests that the UK should besetting about creating a range of future optionsby which low carbon futures could bedelivered, as, and when, the time comes. Thefocus of this review is on ways of creating newoptions, and building upon the options wealready have. Attention has been given to thecost-effectiveness of different options, bothimmediately and in the longer term.

There is a central role formarket-based instruments andfor support for innovation andR&DA centrepiece of any long-term carbon-reducingpolicy should be the use of market-basedinstruments to put a price on carbon emissionsand to help determine the most cost-effectiveopportunities. This need not happenimmediately, but decisions about long-termapproaches are needed soon, since earlycommitment will start to influence decisions inmany markets. A central aim should be toenable the UK to participate in internationalcarbon trading.

A vital means of increasing the range of optionsfor the future is innovation. This is a theme thatneeds to pervade all areas of energy policy anda range of policies should be directed towardsit. The encouragement of renewables is onemeans of increasing innovation and newtechnologies.

Central to that process will be a strongerresearch and development (R&D) base. A groupconvened by the Government’s Chief ScientificAdviser (CSA) has undertaken a review ofenergy research to inform this review. Thefindings of this group suggest there is a needfor much greater investment in R&D if thecutting-edge technologies for a low carbon

9

EXECUTIVESUMMARY

future are to be developed. R&D will not onlyfacilitate the achievement of environmentalgoals but should create valuable exportopportunities for British industry. A healthy R&Dbase is also necessary to attract and foster thescientific expertise needed by the newindustries which will arise from the innovation itstimulates. The CSA’s group suggested that anational Energy Research Centre should beestablished to provide the focus for suchscientific activity.

A step change in energyefficiency is neededIncreased energy efficiency is obviouslyworthwhile if it saves money. There is no pointin wasting energy that can easily be saved. Thescope for cost-effective energy efficiencyimprovement is large and new potential willcontinue to be created by innovation. Majorenergy users have the incentive to save energy,but where energy is a small part of anindividual’s or firm’s budget the opportunitiesare often ignored, partly because there are risksand bother involved in making the necessaryinvestments.

This review puts forward a programme toproduce a step change in the nation’s energyefficiency. At the centre would be a new target – to ensure that domestic consumers’energy efficiency improves by 20% betweennow and 2010, and again by a further 20%between 2010 and 2020. This wouldapproximately double the existing rate ofimprovement. It is a challenging proposition.The gains in terms of energy savings in a yearcould reach about 0.25% of GDP by 2020, overand above the cost of the investment needed tounlock these savings.

Combined Heat and Power (CHP) – which issometimes viewed as a form of energyefficiency – is a low cost option for carbonabatement, but not zero carbon. In the long

term, it will benefit from policies that put aprice on carbon. Industrial CHP is a maturetechnology. It does not need support toencourage “learning by doing” cost reduction,in the same way as new renewable technologiesdo. Yet it is important that current market andinstitutional barriers to CHP are removed –many of these barriers are similar to the onesconfronting renewable investments. The scopefor CHP will be increased substantially by micro-CHP suitable for use in homes.

An expanded role forrenewables should be a keyplank of future strategyRenewables are not just a single technology buta highly flexible set of options. Some of theseoptions will be developed under the existingRenewables Obligation. At the moment, the useof renewables nearly always costs more thanthe use of fossil fuels. Government support isjustified for two reasons:

● use of renewables will help the UK to obtaincarbon savings in the short term which helpsin meeting international obligations; and

● support for renewables will induceinnovation and “learning”, bringing downthe longer-term unit costs of the varioustechnologies as volumes increase andexperience is gained. In this way, today’sinvestment buys the option of a muchcheaper technology tomorrow. Althoughlearning will be international, some of thenew technologies – notably the marinetechnologies – may have particularly Britishapplications and require UK basedtechnological development.

In order to bring down the cost of newrenewables and to establish new options, anexpanded renewables target of 20% ofelectricity supplied should be set for 2020. Thereview estimates that meeting the whole of this20% target could produce domestic electricity

10

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

prices in 2020 around 5-6% higher thanotherwise. The longer-term assurance which anextended target would give to the industrycould, however, help to bring down the costs ofsupporting renewables over the next decade.The review has not come to a conclusion aboutthe means by which the 2020 target should bedelivered. This should wait upon the review ofthe working of the Renewables Obligation in2006/07.

Achieving the existing target that 10% ofelectricity should be supplied by renewableenergy by 2010 is by no means guaranteed.The renewables industry faces three institutionalbarriers that must be removed if it is tosucceed. These are:

● the excessive discount which, following theintroduction of the New Electricity TradingArrangements, is currently imposed on theprices paid to small and intermittentgenerators;

● the urgent need to change the way in whichlocal distribution networks are organised andfinanced; and

● the working of the planning system, which atpresent fails to place local concerns within awider framework of national and regionalneed.

Recommendations are made to address all ofthese barriers.

Measures are needed to keepthe nuclear option open . . .Nuclear power offers a zero carbon source ofelectricity on a scale, which, for each plant, islarger than that of any other option. If existingapproaches both to low carbon electricitygeneration and energy security prove difficult topursue cheaply, then the case for using nuclearwould be strengthened.

Nuclear power seems likely to remain moreexpensive than fossil fuelled generation, thoughcurrent development work could produce anew generation of reactors in 15–20 years thatare more competitive than those availabletoday. Because nuclear is a mature technologywithin a well established global industry, thereis no current case for further governmentsupport.

The decision whether to bring forwardproposals for new nuclear build is a matter forthe private sector. Nowhere in the world havenew nuclear stations yet been financed within aliberalised electricity market. But, given that theGovernment sets the framework within whichcommercial choices are made, it could, as withrenewables, make it more likely that a privatesector scheme would succeed.

The desire for flexibility points to a preferencefor supporting a range of possibilities, and not alarge and relatively inflexible programme ofinvestment such as would be implied by the10GW programme currently proposed by thenuclear industry. If the UK does not supportnuclear power today, the option will still beopen in later years, since the nuclear industry isan international one, using designs that havebeen developed to meet circumstances in manycountries. The desire for new options points tothe need to develop new, low waste, modulardesigns of nuclear reactors, and the UK shouldcontinue to participate in international researchaimed in this direction.

The nuclear skill base needs to be kept up-to-date. In particular the Government shouldensure that the regulators are adequatelystaffed to assess any new investment proposals.Action is also required to allow a shorter lead-time to commissioning, should new nuclearpower be chosen in future. Finally, within a newframework for encouraging a low carboneconomy, the Government should ensure that,as methods to value carbon in the market aredeveloped, additional nuclear output is able tobenefit from them.

11

EXECUTIVESUMMARY

The main focus of public concern about nuclearpower is on the unsolved problem of long-termnuclear waste disposal, coupled withperceptions about the vulnerability of nuclearpower plants to accidents and attack. Any moveby government to advance the use of nuclearpower as a means of providing a low carbonand indigenous source of electricity would needto carry widespread public acceptance, whichwould be more likely if progress could be madein dealing with the problem of waste.

. . . and to create futureoptions for coal by carbonsequestrationIn the medium-term, coal has a continuing roleto play in the energy mix. Its longer-termcontribution depends on there being a practicalway of handling the CO2 that it produces. CO2

capture and sequestration – whereby carbon istaken out of fossil fuels and stored:

● could be a means to preserve diversity of fuelsources, while meeting the need for deepcuts in CO2 emissions;

● has the potential to allow fossil fuels to be asource of hydrogen for transport and otherapplications without large-scale carbonrelease into the atmosphere; and

● seems to be well suited to UK circumstances,since the UK has potential repositories in theContinental Shelf, and the carbon couldpossibly be used to get more oil fromexisting wells.

At the moment uncertainties surrounding costs,safety, environmental impacts and public andinvestor acceptability are large. Steps should betaken to reduce these uncertainties – asdiscussed more fully in the DTI Clean CoalReview. As part of this work, the legal status ofdisposing of CO2 in sub-sea strata needs to beclarified, in the light of possible conflicts withthe London and OSPAR Conventions.

Increased vehicle efficiencyand investment in newoptions for transport fuels isrequired in the longer-termThe transport sector is likely to remain primarilyoil-based until at least 2020. Access to oilsupplies is not a current concern. Nevertheless,the economy’s dependence on transport,coupled with increased imports as UKCSproduction declines, reinforces the need toimprove the energy efficiency of oil-drivenvehicles. Prospective advances in vehicletechnology hold out the possibility of significantreductions in fuel use.

The potential long-term requirement forsignificant CO2 emissions reductions from thetransport sector combined with the possibilitythat oil will become scarcer, raise the need todevelop alternative fuels. There is the long-termprospect that the technology for poweringvehicles by fuel cells fed on hydrogen will fulfilits current promise, and so ultimately provide asubstitute for oil. Other options, such as liquidbiofuels may also have a role. Internationalefforts are needed to develop thesetechnologies.

Handling the projected growth in aviationenergy use and CO2 emissions must become apriority. Taxation and other measures tomanage aviation demand should be prioritisedfor discussion in EU and other internationalforums.

12

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

Institutional changes,including to the planningsystem, need to be made todeliver the strategy. The approach adopted in this review suggeststhat in the long-term the Government shouldbe aiming to bring together the threeinterlinked themes in this review – energypolicy, climate change policy and transportpolicy – in one department of state. In theshorter-term, consideration should be given tolocating responsibility for energy efficiency andCHP policy with other aspects of energy policy.

As an immediate response to the challenge, theGovernment should set up a Sustainable EnergyPolicy Unit. This would be a cross-cutting unitstaffed by civil servants from all thedepartments with an interest in sustainableenergy, as well as staff from the DevolvedAdministrations, external experts and peoplefrom the private sector. The Unit would focuson providing ministers with cross-cuttinganalytical capability to ensure that keydevelopments in energy use and supply weremonitored and assessed. It would lead on thedevelopment of strategic policy issues, adaptingquickly to changing circumstances.

The different responsibilities of the DTI and theregulators, most notably Ofgem, shouldcontinue. The DTI and DEFRA should do moreto set out their priorities in guidance to Ofgem,so that Ofgem can further consider the impactsof its proposals for non-economic objectives.But it is Ministers who should take responsibilityfor intervention in markets, if economicobjectives conflict with environmental andsocial goals.

In many parts of the energy industries, investorshave found that their projects have difficulty ingaining planning permission. The attitude oflocal communities to proposals for new energydevelopments is important. They must continueto have their say in the planning process, whichis one reason why it is important to engage the

public in the energy policy debate. But nationalplanning guidance needs to make it clear wherethere is a national case for new investment inenergy-related facilities by establishing therelevant national and regional context for eachtype of development.

Next steps: a national publicdebate is now neededThe review develops a radical agenda – toenable the UK to put itself on the path to a lowcarbon economy, while maintainingcompetitively priced and secure energy.Precautionary action is needed in advance offurther international agreement. Tasks thatshould be undertaken within the next five yearsinclude:

● Government should move towards a clearrationale for the balance of policyinstruments – taxes, permits and regulation –to create powerful incentives for long-termcarbon reduction; and

● immediate action is needed to assistinnovation and to create new options, andalso to manage risk.

But these are not matters for the UK alone.Increasingly, policy towards energy security,technological innovation and climate changewill be pursued in a global arena, as part of aninternational effort.

The implementation of an ambitious lowcarbon policy would be a demanding task.Change of this kind takes a long time. It wouldbe wrong to imagine that everything can be“win-win”: there will be some hard choices,and there will be losers as well as winners. Forthis reason the Government needs to take theissues to the public soon. During the review,proposals were made to the PIU for anextensive process of public involvement. Therewas insufficient time for this, but it shouldconstitute a central part of the implementationof the findings of the review.

13

EXECUTIVESUMMARY

The nation must not be lulled into inaction bythe focus of much of the expert debate on longtimescales and on energy systems in a futurewhich will belong mainly to our grandchildren:the time for action is now and all players in theenergy system have a role to play. Given thatthere is considerable inertia in the system, andthat the low carbon technologies are not partof the conventional energy system, a change ofdirection will be difficult to achieve. It willrequire clarity of purpose in all parts ofGovernment.

14

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

1

INTRODUCTION

Introduction1.1 Energy use is central to our lives, whetherto provide light or warmth, to drive our cars orto fuel our services and industries. Fortunately,the energy markets supplying UK consumersexhibit many signs of health and there is noenergy crisis in the UK. However, debate hasbeen increasing about the ways in whichenergy policy balances economic,environmental and social objectives. Blackoutsand price hikes in California in late 2000 andearly 2001 raised concerns about regulatoryframeworks and investment in energyinfrastructure. The fuel protests in October2000 illuminated how affordability andaccessibility of energy are vital to maintain asecure and equitable society. Human inducedclimate change is now being seen as a reality,with energy use being the major contributor,raising the question of how best to achieve asustainable future.

1.2 A number of countries and internationalorganisations have considered it timely toreview their approach to energy: for example,the USA1 and the European Commission2

published papers in 2001, and the Council ofAustralian Governments has set up a review toidentify strategic issues for Australian energymarkets.

1.3 A prudent government must be sure thatlong-term concerns have been addressed andvaried objectives are being balanced. In June2001 the Prime Minister, Tony Blair, asked thePerformance and Innovation Unit (PIU) to carry

out a review of the strategic issues surroundingenergy policy for Great Britain.

Review objectives and scope1.4 The review had three main objectives:

● to set out the objectives of energy policy,including the UK contribution to globalpolicy initiatives, to 2050;

● to develop a framework for reconciling thetrade-offs among the different objectives ofenergy policy; and

● to develop a vision and strategy for achievingthese objectives and to identify the practicalsteps that need to be taken in the short-andmedium-term, as well as the longer-term.

1.5 A further objective of the review was toinform the Government’s response to the RoyalCommission on Environmental Pollution’s(RCEP) report on Energy – The ChangingClimate3; and in particular the recommendationthat: “The Government should now adopt astrategy which puts the UK on a path toreducing carbon dioxide emission by some 60%from current levels by about 2050”.

1.6 The scope of the review was to coverenergy policy in Great Britain with a timehorizon of 2050. While the review analysed theimplications for fuel poverty of possible policychanges, the review did not cover policytowards fuel poverty. Fuel poverty has recentlybeen addressed by the consultation on, andfinal publication of, the UK Fuel PovertyStrategy.4 In addition, while the review covered

1. INTRODUCTION

1 US National Energy Policy Development Group (2001).2 Commission for the European Union (2001d). 3 Royal Commission on Environmental Pollution (2000).4 DTI, DEFRA (2001).

the role of the transport sector in futurescenarios and considered potential technicaldevelopments, the review did not covertransport policy instruments.

1.7 The review is being presented to theGovernment. It is a consultative document andnot a statement of Government policy.

1.8 Energy policy in England, Scotland andWales is the responsibility of UK Government,but responsibility is devolved in NorthernIreland. However, there are areas within energypolicy in Scotland and Wales that are devolved:these are detailed in Box 1.1 below. Thereview’s formal recommendations should beinterpreted as applying only to UK Governmentresponsibilities; it is for the devolvedadministrations to determine policy in relationto devolved matters. Given their range of

responsibilities, the Scottish Executive andNational Assembly for Wales must remain fullyinvolved in the development of energy policy.

Review process1.9 The review team, a multi-disciplinary mixof civil servants and secondees from outsideWhitehall, was assembled in June 2001. Annex2 lists the team members and their homeorganisations.

1.10 There were five phases to the review:

● posting scoping notes on various issues onthe PIU website to stimulate discussion;

● taking evidence from interested parties.Around 400 submissions were received, andmany were placed on the PIU website;

16

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

Box 1.1 Devolved powers and energy

While responsibility for energy policy in Great Britain is reserved to the DTI, anumber of areas relating to energy policy are devolved to Scotland and Wales.Listed below are the key areas that impact on energy policy that are devolved inScotland and Wales.

Devolved in Devolved inArea Scotland Wales

Environment policy ✓ ✓

Promotion of renewable energy ✓ ✘

Promotion of energy efficiency ✓ ✘ *

Support for innovation ✓ ✓

Housing ✓ ✓

Building Regulations ✓ ✘

Planning (apart from the energy consents listed below) ✓ ✓

Power station consents (over 50MW) ✓ ✘

Overhead electricity line and gas pipeline consents ✓ ✘

The National Assembly for Wales also has a cross-cutting duty under theGovernment of Wales Act to promote sustainable development across all of itsactivities. The Scottish Executive’s Ministerial Group on Sustainable Scotlandundertakes a similar role in Scotland.* The NAW controls the budget and/or funds certain energy efficiency schemes in Wales, e.g. the Home Energy Efficiency Scheme,the Energy Efficiency Best Practice Programme, and part of the activities of the Carbon Trust Wales.

● establishing important times and dateswithin the energy industry, and creatingscenarios for possible energy systems in 2020and 2050. These three sources of informationhighlight key issues for energy policy in theshort-, medium- and long-term;

● formulating a framework for Government onhow to make choices among differentpolicies and how to reconcile competingobjectives; and

● setting out key Government actions in theshort-term while exposing fundamentalpolicy decisions for the medium- and long-term.

1.11 In carrying out the review, the PIU teamhas drawn on the expertise of the review’sAdvisory Group, made up of representativesand stakeholders inside and outsideGovernment. (Annex 2 lists the membership ofthe Advisory Group.) Brian Wilson, the Ministerof State (Industry and Energy), Department ofTrade and Industry, acted as the review’sSponsor Minister and chair to the AdvisoryGroup. The input and assistance of the AdvisoryGroup was a crucial part of the review. Thegroup was, however, advisory; the report doesnot necessarily represent the views of all groupmembers.

1.12 In keeping with other PIU projects, thereview team adopted an open and consultativeapproach, involving discussions with a widerange of outside stakeholders. Severalworkshops were held in England, Scotland andWales and the team participated in severalconferences and undertook numerous bilateralmeetings. In addition, Whitehall departmentsprovided invaluable support and assistance. Weare grateful to all those who have spent timetalking to us, organising and taking part inworkshops, and referring us to relevantliterature and research findings.

Review outline1.13 The rest of the review is structured asfollows:

● Chapter 2 briefly describes the current stateof play in the energy system and challengesfaced;

● Chapter 3 sets out the objectives for energypolicy, a framework for future decisionmaking and a discussion of different policyinstruments;

● Chapter 4 considers the issue of security inthe energy system;

● Chapter 5 presents the lessons from fourscenarios created for 2050 and 2020;

● Chapter 6 discusses low carbon options;

● Chapter 7 presents policies and aprogramme for a low carbon future;

● Chapter 8 considers the institutional changesrequired to achieve a secure, low carbonfuture;

● Chapter 9 summarises the review’s mainconclusions and policy recommendations;and

● Chapter 10 looks at implementation of therecommendations.

1.14 Annexes then follow:

● Annex 1 sets out the role of the Performanceand Innovation Unit;

● Annex 2 gives details of the Project Team,Sponsor Minister and Advisory Group;

● Annex 3 lists the organisations consulted andsubmissions received;

● Annex 4 presents an analysis of the potentialimpact of recommendations on fuel poverty;

● Annex 5 presents the basis for governmentintervention in the improvement of energyefficiency;

● Annex 6 provides details of low carbontechnologies discussed in Chapter 6;

1

INTRODUCTION

● Annex 7 discusses key future events and setsout timelines affecting decisions;

● Annex 8 presents a summary andrecommendations from the Chief ScientificAdviser’s Energy Research Review;

● Annex 9 is a glossary; and

● Annex 10 lists references.

1.15 A series of working papers wascommissioned or prepared by the review teamto underpin the review’s analysis andconclusions. These are referred to in the textand listed in Annex 10.

18

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

19

THECHALLENGEAHEAD

Introduction2.1 The energy system would face a seriouschallenge if the UK were to try to achieve largecarbon reductions, while maintaining energysecurity and affordable and competitive energy

prices. The purpose of this chapter is tointroduce and explain those challenges, largelyby showing how the energy system hasdeveloped. Since this review has the task oflooking ahead for 50 years, this chapter takes

2. THE CHALLENGE AHEAD

Summary

The energy system would face a serious challenge if the UK were to try toachieve large carbon reductions, while maintaining energy security andaffordable and competitive energy prices.

● The UK is currently one of only two G7 countries that are netexporters of energy, but it will almost certainly be increasingly relianton imported energy over the next 10-20 years.

● Energy prices in the UK seem to be at, or even slightly below, theOECD average.

● There is the prospect of rapid technological change in the energyindustries. Substantial change may be in prospect, but it would needto be accommodated.

● UK carbon emissions have been falling steadily over the last 30 years.Future emission reductions will be harder to achieve than pastreductions.

● Energy use and emissions from transport have been growing broadlyin line with GDP, until recently.

● There is a continued need to protect the fuel poor from the impactof higher energy costs. Similarly concerns relating to industrialcompetitiveness need to be addressed.

some glances back over the past 50 or moreyears, but most of the information relates to thelast 30 years. After a brief historical review, thechapter gathers together some facts relating tothe major themes of this review: energysecurity, energy prices, fuel poverty, UKcompetitiveness and trends in carbon emissions.It finishes by looking at some of the optionsopened by recent change in energytechnologies.

2.2 An examination of past trends demonstratesthat huge changes in energy systems can bemade. The energy system is made up of a seriesof physical assets, for example power plants,gas and electricity network infrastructure, andoil refineries. These take time to build and, oncein place, last for years, often decades, into thefuture. It is therefore difficult to transfer out ofan energy system quickly without creatingstranded assets, and efficient policy should tryto minimise this waste. Annex 7 gives details ofsome of these “timelines”, whose importance isone of the themes of this review.

2.3 These long time horizons create a need totry to look into the future. Yet the history of

energy reviews is littered with failed attempts toproject or forecast the production and/or use ofenergy resources. This review is unlikely toprove an exception. The important thing is toreflect this uncertainty in policy-making, so thatit is flexible in the face of new information. Itwould be wrong to try to plan the energysystem, but equally, given the often long leadtimes within the energy system, a long-termvision is sometimes needed if we are to avoidcommitments which may be found wanting aspolicy needs change.

The UK Energy System in theTwentieth Century 2.4 The UK’s energy system has changeddramatically over the last century. Similarchanges in technologies, fuel supplies,infrastructure, management and operation ofthe industry and customer relationships can beexpected over the next century. In 1950, asFigure 2.1 shows, the energy system for bothindustry and domestic demand was fuelled bycoal. Fifty years later that energy system looks

20

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

Figure 2.1: Change in the UK primary fuel mix from 1950 to 2000 (%)

Source: Darmstadt et al (1971) and DTI (2001a).

1950 2000

Hydro0.1%Crude oil

10.4%

Coal89.5%

Renewables1%Nuclear

9%

Gas43%

Oil32%

Coal15%

very different. In 1965, it was not clear whetherthe UK would find natural gas in the NorthSea.1 Today domestic natural gas is our largestsource of energy.

2.5 A thumbnail sketch of the history is asfollows:

2.6 Before World War 2:

● coal was the dominant fuel in industry andelectricity power plants, and in houses andbusinesses;

● town-gas networks existed in larger towns,with the gas derived from coal; and

● vertically integrated, independent companiesdistributed electricity to customers viadistribution networks with limitedinterconnection between them.

2.7 The structure of the energy system and thediversity of energy supplies altered considerablyin the second half of the twentiethcentury:

● coal continued to be of central importancefor electricity generation, although itsimportance elsewhere fell substantially;

● nuclear power plants began to becommissioned from the mid-1950s;

● the electricity industry was combined intostate-owned monopolies, during the 1950s;

● the high voltage electricity transmissionnetwork was created in order to transportelectricity over long distances from bigpower plants;

● electricity distribution networks shrank inimportance and activity;

● during the 1960s and 1970s there was amove to an extensive natural gas network forheating (industry, commerce and domestic);

● demand for transport fuel increaseddramatically;

● gas fired central heating largely replacedopen coal fires in homes; and

● the use of electrical appliances in commerceand the domestic sector increased hugely.

2.8 During the 1990s, the GB energy sectorwas transformed by market liberalisation. Theprivatisation of the gas and electricity supplyindustries, combined with the introduction ofcompetitive markets, gave consumers choicebetween alternative providers of gas andelectricity. These changes, which were largelypioneered in GB, are now being adopted inmany other countries.

2.9 A longer-term shift from coal to gas wasalready underway but liberalisation acceleratedit, with beneficial environmental effects. Theswitch from coal to gas in electricity generationwas the result of:

● the availability of cheap gas;

● pressure on coal generators to reduce acidrain emissions;

● the wholesale electricity market; and

● the availability of combined cycle gas turbinetechnology.

2.10 The changes during the 1990s in theenergy system had a number of beneficialimpacts, both economic and environmental.Some of the environmental improvements inrespect of carbon were incidental, althoughthere were direct policy measures intended toimprove efficiency. The beneficial impacts were:

● privatisation and liberalisation helped toreduce the costs of production andtransportation;

● reductions in costs, partly also due to fallingworld fossil fuel prices, have been translatedinto retail fuel price reductions;

● falling real prices have helped to reduce fuelpoverty while maintaining thecompetitiveness of UK industry;

21

THECHALLENGEAHEAD

1 Ministry of Fuel and Power (1965) said that “… gas may be found under the British part of the Continental shelf”.

● the switch from coal to gas reducedenvironmental emissions, not only of acidgases, but also of greenhouse gases; and

● the switch from coal to gas increased thediversity and security of electricity generation– at the start of the 1990s, coal accountedfor about two-thirds of the fuel used forelectricity generation, but it now accountsfor only one-third.

Security2.11 Security of the energy system is a centralconcern and is examined in detail in Chapter 4.One facet of security has always been taken tobe the diversity of fuels in use in the energysystem. Countries vary widely in their energysupply mix. Figure 2.2 shows the different mixof primary fuels in the G7 countries. There areconsiderable differences among countries,especially in the shares of nuclear and coal. All

countries use roughly the same proportion ofoil, reflecting its dominance in transport usesand its phasing out in most other markets. Thedifferences in each country’s fuel mix largelyreflect historical circumstances, resourceendowments and different political and marketchoices. A variety of very different approacheshave been adopted.

2.12 In the UK, one aspect of security concernhas been the imminent peaking of oil and gasproduction from the UKCS. As Figure 2.3shows, the UK is one of only two G7 countriesthat is a net total exporter of energy. Table 2.1shows that the UK is projected still to be a netexporter of oil in 2010. But then total netexports are projected to fall rapidly, so that theUK becomes a net importer shortly after 2010.

2.13 The UK is expected to become a netimporter of gas sooner than for oil, indeed theUK already imports natural gas during periods

22

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

0

10

20

30

40

50

60

70

80

90

100

Other Nuclear Gas Oil Coal

Figure 2.2: Primary energy use in G7 countries and in the EU and OECD, 2000

Note: “Other” includes renewables and net imports of electricity. Electricity trade is less than 1% of total energy in all cases except France, which exports 2% and Italy, which imports 2%

Source: IEA (2001a).

UK Canada France Germany Italy Japan USA EUAverage

OECDAverage

of peak demand. Based on the current level ofreserves and prices, the Department of Tradeand Industry (DTI) forecasts that the UK willbecome a net importer of gas on an annualbasis from 2005.

2.14 Other changes which may impact onenergy security are expected by 2020:

● many of the existing nuclear power stationswill have ceased production; and

● coal is likely to play a smaller role in theenergy mix, and at least some UK coal mineswill have exhausted their reserves.

2.15 This means that the UK is heading towardsa situation where it becomes a net importer ofoil and gas and where the two leadingelectricity generating technologies of the pastcentury – nuclear and coal – are, on currentplans, running down. Whether this muchincreased import requirement represents aproblem is discussed in Chapter 4.

2.16 In the 1970s the energy problem waslargely defined in terms of potential world-wideshortages of resources. Energy policy was seenby some people as a process of finding newoptions to replace depleting reserves. Since the

23

THECHALLENGEAHEAD

Figure 2.3: Energy self-sufficiency in G7 countries and in the EU and OECD, 1999

Source: IEA (2001a).

UK Canada France Germany Italy Japan USA EUAverage

OECDAverage

0

20

40

60

80

100

120

140

160

% o

f en

erg

y us

e m

et f

rom

loca

l res

our

ces*

self-sufficient

*nuclear is treated as local

Table 2.1: UK oil production and trade, 1973-2010 (mtoe)

1973 1990 1998 2005 2010

Production 0.6 95.3 138.9 150.0 126.0

Exports 20.9 76.5 113.1 123.3 95.5

Imports 136.9 65.4 61.3 70.0 70.0

Bunker use 5.4 2.5 3.1 2.0 2.0

Net imports 110.6 –13.6 –54.9 –55.3 –27.5

Source: IEA (2000a).

1970s, views have changed and there is nolonger a sense of urgency about future world-wide energy resources. In large measure this isbecause there has been a more systematicsearch for major energy resources, and manyhave been found. While in the 1970s the worldreserve to production ratio for gas was around40 years; it is now close to 60 years, despitesubstantial and rising gas use in the meantime.2

World coal reserves now stand at 200 years ormore.3 The position for oil is slightly different.While world reserves have remained roughlyconstant at around 35 years, oil has beensearched for intensively for many years, and fewlarge new discoveries have been made for sometime.4 This means that for the 50-year period ofthe current energy review, it is possible to beconfident about world-wide coal reserves, andreasonably confident about gas availability, butoil might become scarcer by mid-century.

Energy Prices2.17 Table 2.2 shows that industrial energyprices have been on a downward trend sincethe early 1980s. The exception is the price ofheavy fuel oil which has fluctuated, and wherethe price in 2000 was above the price in 1990(and indeed 1970). This is a reflection ofchanges in oil prices. Table 2.3 shows that, withthe exception of petrol prices, domestic energyprices have fallen over the last decade: the fallsin gas and electricity prices have beenparticularly marked.

2.18 Figure 2.4 shows that if UK averageindustrial and domestic electricity prices arecompared with prices in other European andG7 countries, the UK is slightly below average.But average industrial prices conceal a widerange of terms, and it can be misleading toapply them to particular sectors. Figure 2.5

24

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

Table 2.2: Trends in real industrial energy prices by fuel, UK, 1970–2000

1970 1980 1990 2000

Coal 108.1 154.5 100.0 60.27

Heavy fuel oil 91.1 245.4 100.0 122.99

Gas 158.9 166.8 100.0 58.76

Electricity 117.1 127.0 100.0 67.95

Source: DTI (2001a).

Table 2.3: Trends in real domestic energy prices by fuel, UK, 1970–2000

1970 1980 1990 2000

Coal and smokeless fuels 89.2 109.0 100.0 94.9

Electricity 84.9 104.0 100.0 78.3

Gas 129.0 86.4 100.0 77.4

Petrol and oil 97.1 107.3 100.0 116.7

Source: DTI (2001a).

2 BP (2001).3 UNDP and WEC (2000).4 BP (2001).

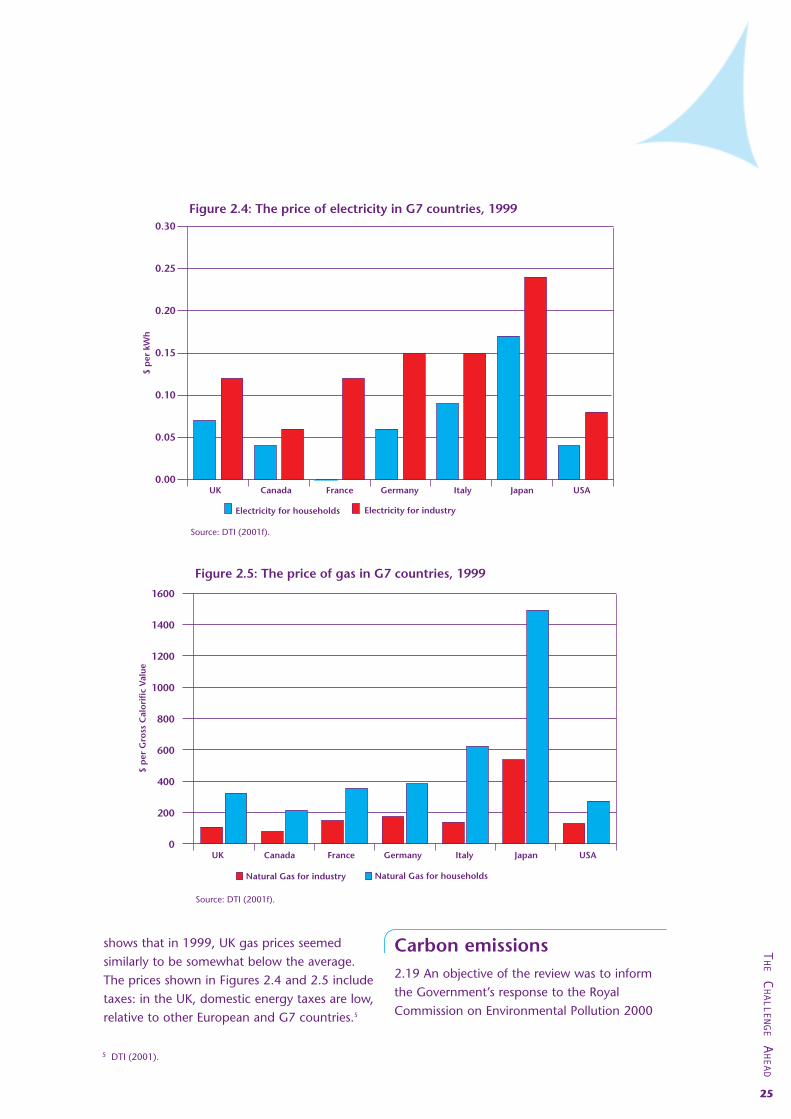

shows that in 1999, UK gas prices seemedsimilarly to be somewhat below the average.The prices shown in Figures 2.4 and 2.5 includetaxes: in the UK, domestic energy taxes are low,relative to other European and G7 countries.5

Carbon emissions2.19 An objective of the review was to informthe Government’s response to the RoyalCommission on Environmental Pollution 2000

25

THECHALLENGEAHEAD

Figure 2.4: The price of electricity in G7 countries, 1999

Source: DTI (2001f).

UK Canada France Germany Italy Japan USA0.00

0.05

0.10

0.15

0.20

0.25

0.30

Electricity for households Electricity for industry

$ p

er k

Wh

Figure 2.5: The price of gas in G7 countries, 1999

Source: DTI (2001f).

UK Canada France Germany Italy Japan USA0

200

400

600

800

1000

1200

1400

1600

$ p

er G

ross

Cal

ori

fic

Val

ue

Natural Gas for industry Natural Gas for households

5 DTI (2001).

report on Energy – The Changing Climate.6 Andin particular, the recommendation that: “TheGovernment should now adopt a strategywhich puts the UK on a path to reducingcarbon dioxide emission by some 60% fromcurrent levels by about 2050”.

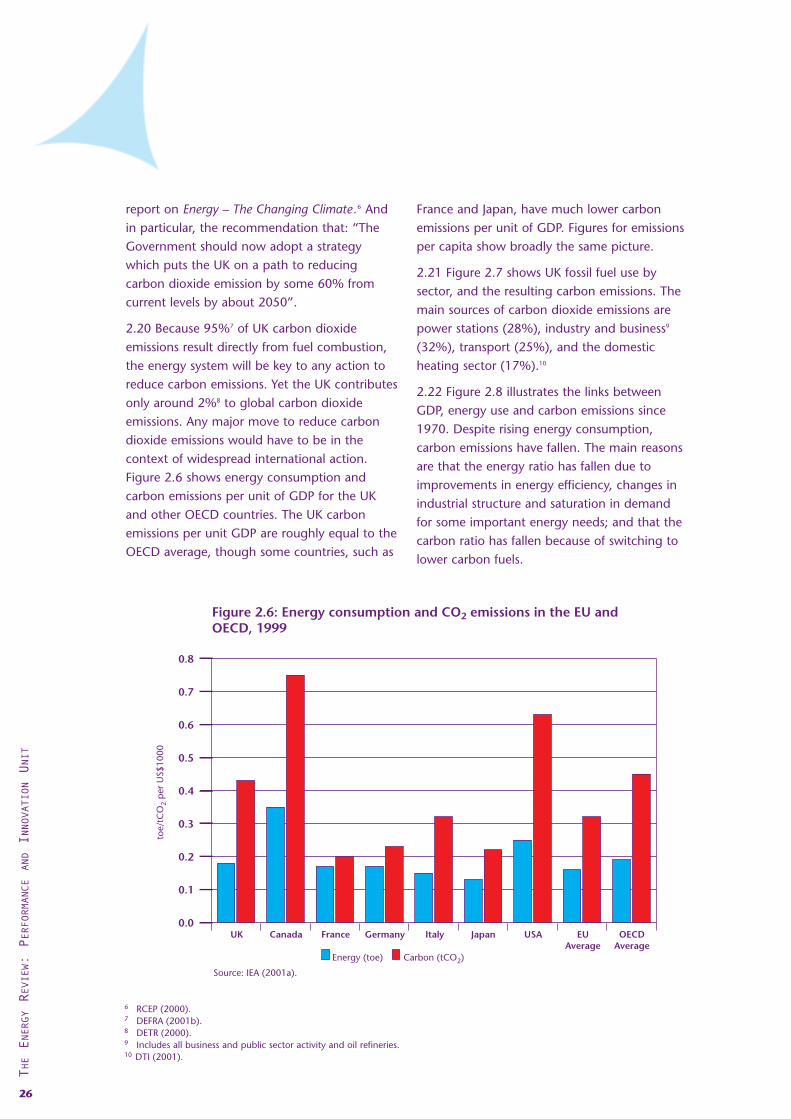

2.20 Because 95%7 of UK carbon dioxideemissions result directly from fuel combustion,the energy system will be key to any action toreduce carbon emissions. Yet the UK contributesonly around 2%8 to global carbon dioxideemissions. Any major move to reduce carbondioxide emissions would have to be in thecontext of widespread international action.Figure 2.6 shows energy consumption andcarbon emissions per unit of GDP for the UKand other OECD countries. The UK carbonemissions per unit GDP are roughly equal to theOECD average, though some countries, such as

France and Japan, have much lower carbonemissions per unit of GDP. Figures for emissionsper capita show broadly the same picture.

2.21 Figure 2.7 shows UK fossil fuel use bysector, and the resulting carbon emissions. Themain sources of carbon dioxide emissions arepower stations (28%), industry and business9

(32%), transport (25%), and the domesticheating sector (17%).10

2.22 Figure 2.8 illustrates the links betweenGDP, energy use and carbon emissions since1970. Despite rising energy consumption,carbon emissions have fallen. The main reasonsare that the energy ratio has fallen due toimprovements in energy efficiency, changes inindustrial structure and saturation in demandfor some important energy needs; and that thecarbon ratio has fallen because of switching tolower carbon fuels.

26

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

6 RCEP (2000).7 DEFRA (2001b).8 DETR (2000).9 Includes all business and public sector activity and oil refineries.10 DTI (2001).

Figure 2.6: Energy consumption and CO2 emissions in the EU and OECD, 1999

Source: IEA (2001a).

UK Canada France Germany Italy Japan USA EUAverage

OECDAverage

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

toe/

tCO

2 p

er U

S$10

00

Energy (toe) Carbon (tCO2)

2.23 Figure 2.9 illustrates how transportgrowth, measured in terms of both passengerkilometres and freight tonnes travelled, hasnearly doubled over the last thirty years. Unlike

Figure 2.8, which shows that GDP and carbondioxide emissions from energy use arediverging, Figure 2.9 shows that carbon dioxideemissions, transport growth and GDP continue

27

THECHALLENGEAHEAD

Figure 2.7: UK fossil use and CO2 emissions by sector, 2000(%)

Source: DTI (2001d).

Transport Domestic Industry* Electricity Non-energy**0

5

10

15

20

25

30

35

Fossil fuel CO2 emissions

Perc

enta

ge

shar

e

*Includes commerce, public sector and refineries**emissions from land use changes

Figure 2.8: UK GDP, energy consumption and CO2 emissions,1970-2000

Source: DTI (2001a), ONS (2001), DEFRA (2001b).

0

20

40

60

80

100

120

140

160

180

200

1970 1980 1985 1990 1995 20001975

CO2 emissions

GDP

Energy consumption

The carbon ratio (carbon output

divided by energy use) The energy ratio (energy use divided by GDP)

Inde

x (1

970

= 10

0)

to be in step with one another, except veryrecently when CO2 seems to have stabilised.

2.24 Figure 2.10 illustrates the variation amongthe amounts of carbon dioxide that are releasedthrough the use of different fuels. Natural gas

has lower emissions than coal or oil, whilenuclear and renewable energy have almost zeroemissions.

2.25 Different parts of the economy usedifferent types of energy: for example, the

28

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

Figure 2.9: UK GDP, transport growth and CO2 emissions, 1970-1999

Source: DTLR (2000), DEFRA (2001b).

1970

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1972

1994

1996

1998

40

60

80

100

120

140

160

180

200

Total passenger km Total freight tonne-km Real GDP Total CO2

Figure 2.10: The carbon content of fuels

Source: DTI (2000a).

0

5

10

15

20

25

30

CoalOilGasRenewablesNuclear

Kilo

gra

mm

es o

f ca

rbo

n p

er G

J

transport sector primarily uses oil, while thedomestic heating sector primarily uses naturalgas. There are obvious technological constraintson the extent to which each sector is able toswitch to a lower carbon fuel supply, in theshort term. The implication is that it is harder tomove those sectors towards a lower carbonratio than the sectors which use a lot ofelectricity.

2.26 Past trends in the carbon ratio should notlead us to be complacent about futureemissions from the energy system. As shown inFigure 2.8, between 1970 and 2000 theaverage rate of reduction in the carbon ratiowas 0.75% a year. To deliver 60% CO2 cuts, asenvisaged by the Royal Commission onEnvironmental Pollution, would require anaverage rate of reduction of 2% between 2000and 2050.

2.27 Moreover, the combination of favourablecircumstances that arose in the 1990s is unlikelyto be repeated:

● opportunities for carbon emissions reductionsthrough fossil fuel-switching by end-users arealmost over, with most heat demand alreadybeing met by gas; and

● the output from existing nuclear powerstations will start to decline as they reach theend of their commercial lives, puttingupward pressure on greenhouse gasemissions.

Fuel Poverty2.28 Any move towards a low-carbon futurewould need to take account of the impacts ofany changes in prices on those in fuel poverty.The most widely accepted definition of a fuel-poor household is that it is one which needs tospend more than 10% of its income on fuel useand to heat its home to an adequate standardof warmth. The number of households in fuelpoverty in the UK has fallen over the lastdecade (see Figure 2.11). The improvement has

29

THECHALLENGEAHEAD

Figure 2.11: Number of households in fuel poverty in the UK, 1996-2000

Source: DEFRA, DTI (2001).Note: chart based on definition of fuel poverty including housing benefit and income support for mortgage interest as income.

0

1

2

3

4

5

6

Northern IrelandWalesScotlandEngland

2000199919981996

Num

bers

(m

illio

ns)

largely been a result of reduced fuel prices,improved energy efficiency and increasedincomes. In more recent years, the new HomeEnergy Efficiency Scheme (HEES) and winterfuel payments, now standing at £200 perannum, have helped. Annex 4 gives moredetails.

New Opportunities2.29 The energy system in 2050 will be verydifferent from that in place today. It would bewrong to try to design a policy that appliedunchanged over the long term. Theuncertainties – both technological andcommercial – are too great. The guidingprinciple should be to design policy in such away that it allows maximum flexibility, if andwhen circumstances change.

2.30 Legislative requirements impose animportant set of boundaries or constraints. TheUK is bound by the provisions of relevant

European Directives11 and international treaties,for example the Kyoto Protocol, which establishcertain required outcomes by certain times.While the means of achieving those outcomesare left to individual governments, theoutcomes are legally binding.

2.31 The 1990s saw a number of developmentswhich opened up new options for future energysystems:

● a number of new renewable energytechnologies emerged on the world energyscene for the first time (some renewabletechnologies such as large-scale hydro havebeen established for many years). The UK isvery well endowed with renewable resources,yet it uses less renewable energy than mostEU countries (though many countries achievetheir higher ranking by extensive use of largehydro and conventional biomass plants,rather than by using new renewables).Looking at different countries’ plans for newinvestment in renewables to meet the EU

30

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

Figure 2.12: Increase in the share of renewable electricity required by 2010 to meet EU target

Source: Official Journal of the European Communities (2001).

0

5

10

15

20

25

UnitedKingdom

SwedenFinlandPortugalAustriaNetherlandsLuxembourgItalyIrelandFranceSpainGreeceGermanyDenmarkBelgium

Perc

enta

ge o

f ele

ctric

ity g

ener

ated

from

ren

ewab

le fu

els

11 For example, the Common Rules for the Internal Market in Electricity; the Common Rules for the Internal Market in Gas; thePromotion of Electricity Produced from Renewable Energy Sources in the Internal Electricity Market; a Community Strategy to LimitCarbon Dioxide Emissions by Improving Energy Efficiency; see http://europa.eu.int/eur.lex for full list.

renewable energy target, the increase towhich the UK is committed is broadly similarto that in many other countries (Figure 2.12);

● network information and controltechnologies, as well as meteringtechnologies, have opened up the possibilityof designing and operating energy networksin new ways;

● new demands, for example from Internetserver farms for high quality power secureagainst network disruptions, are drivingchanges to the energy system. As a resultthere will perhaps be more on-site power,different service offers or new networkquality standards;

● new technologies, such as fuel cells, microturbines, and new market structures haveopened up the possibility of energy systemsbased on clean and efficient, decentralisedunits;

● the major car makers have made progress inthe production of low emissions vehicles,such as hybrid electric engines. There havealso been major advances in research intogenuinely zero emission vehicles, based uponfuel cells.

Conclusions2.32 This brief survey suggests the followingthree main conclusions:

● UK carbon emissions have been fallingsteadily over the last 30 years, mainly as aresult of commercial decisions in the light ofgovernment policy. Future emissionreductions will be harder to achieve thanpast reductions. Until recently, emissionsfrom transport have been growing broadly inline with GDP;

● the UK is currently only one of two G7countries that are net exporters of energy,but it will be increasingly reliant on importedenergy over the next 10-20 years; and

● if instruments which raise energy prices areused to reduce carbon emissions, therewould be a continued need to protect thefuel poor from the impact. Similarly concernsrelating to industrial competitiveness willneed to be addressed.

31

THECHALLENGEAHEAD

32

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

3. FRAMEWORK

Summary

This Chapter looks at the justification for government involvement inenergy markets and proposes a framework on which future energy policyshould be based.

● Government intervention in energy markets may be justified wherethere are market failures or equity-related objectives, such as fuelpoverty, that market outcomes may not serve. But competitive energymarkets should continue to be encouraged.

● The guiding principle should be sustainable development, requiringachievement of economic, environmental and social objectives. It isalso vital to maintain adequate levels of energy security at all points intime.

There will be trade-offs and synergies between these objectives.

● Because greenhouse gas abatement can only be delivered through theenergy system, energy policy is likely to give preference to thisobjective.

● An overarching statement of energy policy could be “the pursuit ofsecure and competitively priced means of meeting our energy needs,subject to the achievement of an environnmentally sustainable energysystem”.

● We should prepare for the greater use of economic instruments thatenable the wider environmental costs of carbon to be incorporatedinto market prices. Such instruments are likely to be cost-effective andto be used in international carbon trading.

The rationale for having anenergy policy3.1 The general objective of Governmentenergy policy at present is “to ensure secure,diverse and sustainable supplies of energy atcompetitive prices”.1 The UK energy market isnow almost wholly in private ownership; thereis more competition than ever before and anindependent economic regulator is in place tocontrol the activities of the natural monopoliesin the energy sector – the gas pipelines andelectricity wires – and to police competition.Why then have a Government energy policy?

3.2 Government intervention in private marketsmay be justified on the following grounds

● market failures which lead to economicinefficiencies;

● equity issues, so that even where marketswork well, the outcomes are consideredsocially undesirable; and

● other reasons including strategic andpolitical ones.

It does not follow that the existence of potentialgrounds for government intervention meansthat actual intervention is necessarily justified.Governments do not have perfect knowledge,and interventions may be poorly structured andhave unanticipated consequences. Governmentintervention may sometimes make mattersworse.

33

FRAMEWORK

● This will tend to raise energy prices. If energy is used more efficientlyenergy bills will not necessarily rise. And action to reduce fuelpoverty will also help to remove constraints.

● Good policy will normally require a mix of different instrumentsincluding actions that directly tackle market failures. Targets can beuseful for signalling long-term Government intentions to the market,even if not backed up by specific measures from the outset.

● A unilateral commitment to large cuts in carbon emissions beyondthose already agreed would damage the competitiveness of UKindustry without corresponding global environmental gain.

● In the short- to medium-term, the key priorities of energy policy areto maintain energy security, to ensure compliance with existingcarbon abatement targets, and to develop a range of low carbonoptions to be used to meet possible post-Kyoto targets. The UKshould also be pursuing innovation to permit deep cuts in carbon inthe longer-term. The Government has an important role instimulating innovation.

1 DTI (2000c), page 4 paragraph 1.1.

Efficiency reasons3.3 There are four main market failuresassociated with the energy markets:

● there are market failures arising in part fromthe fact that electricity and gas networks arenatural monopolies. Even with regulationof those monopolies, their existence inhibitsthe ability of suppliers to tailor products tomeet the needs of individual consumers andfor consumers to communicate their wishesto suppliers. These issues are discussedfurther in Chapter 4;

● there are very large “environmentalexternalities” associated with energyproduction and use: the costs ofenvironmental damage are not visited onthose people who are responsible;externalities can be “internalised” bymeasures that enable the wider social costsof pollution to be factored into commercialdecision-making;

● there are information failures (or“asymmetries”), especially in the householdand small business sector, where consumershave much less information (for exampleabout energy saving possibilities) thansuppliers. Another way of looking at this is tosay that there are very substantial economiesof scale in making decisions about efficientenergy use; and

● there is the public good aspect ofinnovation which may result in the privatemarket tending to under-supply innovation,especially in a liberalised market, because itcannot privately capture all the benefits thatresult.

Equity reasons3.4 In the right conditions – such ascompetition among a large number of buyers

or sellers – markets will often provide the mostefficient outcome. But efficient markets are notnecessarily equitable. Governments andsocieties may have preferences for distributionsof incomes and products which are differentfrom those that markets produce, and in suchcases intervention for social reasons may bejustifiable.

3.5 Equity considerations are affected by thefact that energy is a necessity of life. Everyoneneeds warmth and light to survive. And in amodern society access to electricity is alsoessential in order to maintain a range ofhousehold needs. For example refrigerators andtelevisions and (increasingly) access to theInternet are no longer regarded as luxuries andtheir absence is liable to increase socialexclusion. The Government is concerned thatmany of the poorer and more vulnerablemembers of society cannot afford adequatesupplies of energy and for that reason has setout a strategy to tackle fuel poverty.2

3.6 It should also be recalled that equityconcerns can be addressed by means otherthan intervention in energy markets, forexample through special payments to thosethought to be in need through the socialsecurity system.

Other reasons3.7 But there are other reasons whygovernments tend to intervene in energymarkets which are essentially strategic andpolitical. Energy is essential, not only tohouseholds but also to businesses. The non-transport part of our energy system placesheavy reliance on two fuels, gas and electricity,for which energy storage is very difficult.Electricity cannot currently be stored insignificant quantities3 and gas is also difficultand costly to store except in large specialised

34

THEENERGYREVIEW: PERFORMANCE

ANDINNOVATIONUNIT

2 DTI, DEFRA (2001).3 Consumer could meet small needs using batteries and fuel-cell technologies are becoming developed for larger applications.

facilities.4 The difficulties with storing these fuelsmean that security of supply is extremelyimportant. Significant supply interruptions canvery quickly become a matter of major politicalconcern. This is reinforced historically: untilrecently Government owned the UK gas andelectricity industries. Consumers have becomeaccustomed to seeing Government playing amajor role in energy markets. The continuedexistence of “emergency arrangements” formost forms of energy, under whichGovernment can suspend market operations, isalso evidence of this continuingpolitical/strategic concern.

3.8 These are the reasons why Governmentmay choose to intervene, but what principlesshould govern its intervention? These must beestablished in relation to the Government’sobjectives.

Objectives of energy policy 3.9 Sustainable development is an overarchinggoal of Government policy. The notion ofsustainability originally stems fromenvironmental concerns, but sustainabledevelopment is now defined in terms of tryingto balance progress in high level economic,environmental and social objectives, rather thanjust environmental goals: