The Economics of the Belt and Road...

18

The Economics of the Belt and Road Initiative Michele Ruta Astana, Kazakhstan October 4, 2018

Transcript of The Economics of the Belt and Road...

The Economics of the Belt and Road Initiative

Michele Ruta

Astana, Kazakhstan

October 4, 2018

Roadmap

I. The Belt and Road Initiative (BRI)

II. Connectivity gaps in BRI economies

III. Assessing the economic effects of the BRI

IV. Conclusion

2

I. The Belt and Road Initiative

The Belt and Road Initiative: What is it?

4

• The BRI is an ambitious

effort to improve regional

cooperation and

connectivity on a trans-

continental scale

• The BRI consists primarily

of the Silk Road Economic

Belt and the New Maritime

Silk Road, with 6 economic

corridors being identified

• For this study, we focus on

71 economies located along

the Belt and Road• BRI economies account for

over 30% of global GDP,

60% of population, 40% of

world trade, and 75% of

known energy reserves

The Belt and Road Initiative: Challenges and Opportunities

5

Opportunities Challenges• Improving cross-border infrastructure and

their management;

• Reducing trade costs, improving trade rules,

boosting trade flows and GVC participation;

• Improving investment climate and boosting

cross-border investment;

• Improving growth, employment and

poverty reduction;

• Developing lagging and isolated regions.

• Ensuring that investment is efficient, in

the face of high uncertainty;

• Coordinating infrastructure investments,

lack of data and transparency;

• Managing environmental, social and

governance risks;

• Ensuring openness and transparency in

public procurement;

• Sustaining public debt.

II. Connectivity gaps in BRI economies

BRI Trade Landscape

7

The share of BRI exports in global exports increased from 21% in 1995 to

37% in 2015 driven by a surge in global value chains

Source: Boffa (2018)

But large disparities

persist across regions

and countries

A gravity model shows

that BRI economies

under-trade with each

other by 30%0 5 10 15 20 25

South Asia

Middle East and North Africa

Europe and Central Asia

East Asia and Pacific

Exports (% of World exports)

BRI share in global exports

2015 1995

Infrastructure Gaps

8

There are substantial transport and energy infrastructure gaps in

developing economies

- Mckinsey (2016) finds that the world needs $3.3 trillion in infrastructure annually; according

to ADB (2016), developing Asia only requires $1.7 trillion per year in infrastructure

BRI economies’ average score of

perceived quality of transport

infrastructure is 2.7 out of 5,

pointing to important gaps

But large differences:• 3 of the bottom 20 performers are

BRI (Afghanistan, Bhutan, Iraq)

• As are 3 of the top 20 performers

(Hong Kong SAR, Singapore, UAE)

Data Source: World Bank, Logistic Performance Indicator (LPI), 2018.

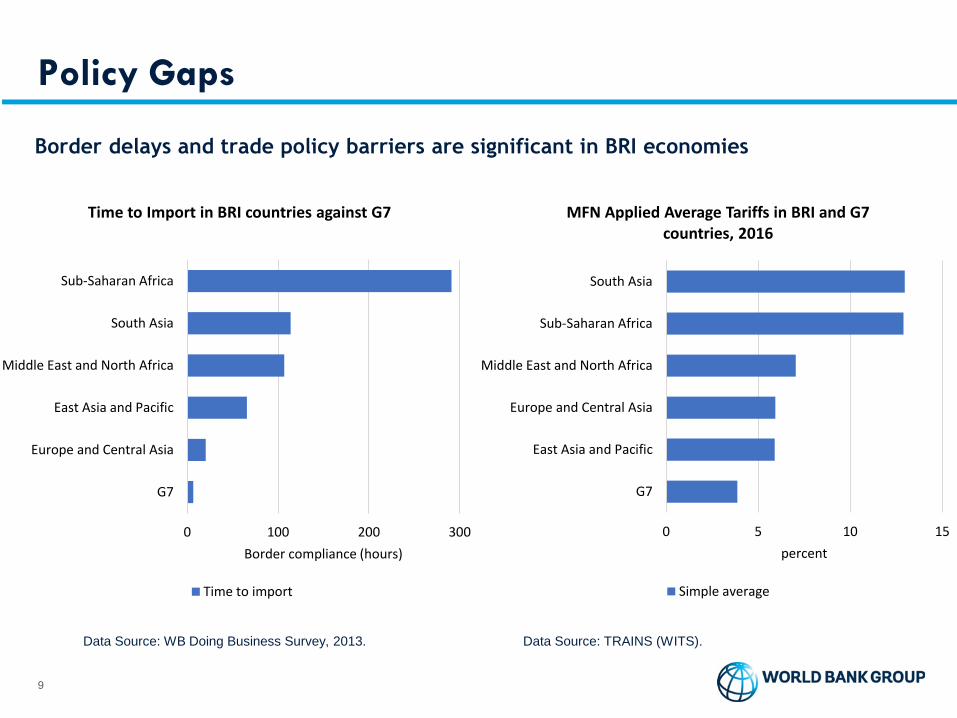

Policy Gaps

9

Border delays and trade policy barriers are significant in BRI economies

Data Source: WB Doing Business Survey, 2013.

0 5 10 15

G7

East Asia and Pacific

Europe and Central Asia

Middle East and North Africa

Sub-Saharan Africa

South Asia

percent

MFN Applied Average Tariffs in BRI and G7 countries, 2016

Simple average

Data Source: TRAINS (WITS).

0 100 200 300

G7

Europe and Central Asia

East Asia and Pacific

Middle East and North Africa

South Asia

Sub-Saharan Africa

Border compliance (hours)

Time to Import in BRI countries against G7

Time to import

III. Economic effects of the BRI:

opportunities and risks

11

BRI-related Transport Projects: A Database

Source: Reed and Trubetskoy (2018).

BRI and Time to Trade

12

BRI projects will reduce trade times by 2.5% for the world and

by 3.2% for BRI economies, thus reducing trade costs

Source: de Soyres, Mulabdic, Murray, Rocha and Ruta (2018).

Note: For each country, the aggregate proportional decrease is computed as the average of

proportional shipping time decrease with all other countries in the world.

Trade Effects: A Gravity Analysis

13

A gravity model predicts that BRI projects increase trade among BRI economies

by 4%. Industries that value time more experience the largest effect on trade

Source: Baniya, Rocha, Ruta (2018).

• Differences across countries reflect both the extent of improved connectivity and the export structure

of the country

• Sectoral effects reflect different time-sensitivity of products (direct effect) and time sensitivity of inputs

(indirect effect)

0%

2%

4%

6%

8%

10%

12%

14%

BT

N

BIH

LB

N

MK

D

NP

L

SV

K

HU

N

LV

A

SG

P

BG

R

ES

T

BL

R

EG

Y

ID

N

RU

S

AF

G

AR

M

IN

D

AZ

E

BR

N

IS

R

TJK

KA

Z

AR

E

KH

M

KW

T

TK

M

SA

U

YE

M

IR

Q

MM

R

OM

N

UZ

B

Percentage change in trade by country

0% 2% 4% 6% 8%

Grains, Seeds and Fibers

Extraction

Textile, Leather and Apparel

Machinery, parts and electronics

Processed food

Wood and mineral prods

Meat Products

Motor, parts and Transport

Vegetable, fruits, nuts, crops

Other Mnfcs (paper, metals, mnfcs nec)

Livestock

Chemical, ferrous metals, rubber, plastics

Percentage change in trade by sector

Direct effect Indirect effect

-1.0 0.0 1.0 2.0 3.0 4.0 5.0

World

BRI Area

percent

Impact of Infrastructure improvement on BRI economies on trade

Infrastructure improvement Reduced border delays

Reduced preferential tariffs

Welfare Effects: A General Equilibrium Analysis

14

Reduction in trade costs due to the BRI boost trade, increasing welfare by up

to 1.32% for BRI economies and 0.71% for the world

• Welfare gains are up to 10% in countries like Lao PDR and Cambodia

Source: Maliszewska and van der Mensbrugghe (2018).

-0.5 0.0 0.5 1.0 1.5

World

BRI Area

percent

Impact of Infrastructure improvement on BRI economies on welfare

Infrastructure improvement Reduced border delaysReduced preferential tariffs

Other Effects

Results from a structural trade model

15

And from analysis of growth through FDI

Source: Chen (2018).

Source: Chen (2018).

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5

Lower middle income

High income

Upper middle income

Low income

percent

BRI transport projects on GDP of BRI economies through trade

Estimated effect on GDP

-0.05 0 0.05 0.1 0.15 0.2 0.25 0.3 0.35 0.4

High income

Upper middle income

Lower middle income

Low income

percent

BRI transport projects on GDP growth of BRI economies through FDI

Estimated effect on GDP growth

Source: De Soyres, Mulabdic, Ruta (2018).

Effects of the BRI are larger when accounting for within country/region

efficiency gains and impact through increased FDI

Fiscal Risks

16

External debt from Non-Paris Club, including China, is historically small in BRI

economies. But it has increased in higher risk countries.

Source: World Bank and staff estimates.

BRI LICDs' Public and Publicly Guaranteed Debt of the General Government (in percent of GDP)

LIDCs –BRI: Composition of external public debt

(% of total)

LIDCs –BRI: External debt by risk of debt

distress (% of total)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2005 2010 2015 2016

Paris Club Bilateral Non-Paris Club Bilateral

Multilateral Bonds

Paris Club Commercial Non-Paris Club Commercial

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Low Moderate High

Paris Club bilateral Non-Paris Club

Multilateral Bonds

Paris Club commercial Non-Paris Club commercial

Conclusions

17

BRI will potentially have a large effect on trade and welfare for many

countries▪ All countries in the world experience a decrease in trade costs

▪ Not all sectors/countries will gain but potential aggregate effect is largely positive

But many policy barriers still remain in place. Potential gains of BRI

would be enlarged by complementary reforms▪ Need to reduce border delays, trade barriers and FDI restrictions

▪ But also boost investor protection, open public procurement, ensure private sector

participation

Economic and non-economic risks associated to BRI projects need to be

managed▪ Public debt sustainability, governance, environmental and social concerns

▪ Coordination problems, lack of data, poor transparency magnify these challenges

THANK YOU!

For more information, visit:

https://www.worldbank.org/en/topic/regional-integration

18