the dti Presentation on the Annual Report 2013/14

50

1 the dti Presentation on the Annual Report 2013/14 Mr Shabeer Khan Chief Financial Officer 29 October 2014 29 October 2014

-

Upload

maxine-lester -

Category

Documents

-

view

53 -

download

0

description

the dti Presentation on the Annual Report 2013/14. Mr Shabeer Khan Chief Financial Officer 29 October 2014. Presentation Outline. Economic Context Strategic Goals The structure of the dti’s work Annual Performance 2013/14 Key achievements Summary of achievement of targets - PowerPoint PPT Presentation

Transcript of the dti Presentation on the Annual Report 2013/14

1

the dti Presentation on the Annual Report 2013/14

Mr Shabeer Khan

Chief Financial Officer

29 October 201429 October 2014

2

Presentation OutlinePresentation Outline• Economic Context• Strategic Goals• The structure of the dti’s work • Annual Performance 2013/14

– Key achievements– Summary of achievement of targets – Financial Management

• Challenges

2

3

Economic contextEconomic context

3

4

Global EconomyGlobal EconomyJanuary – March 2014 (Q1 2014)

Global gross domestic product (GDP) growth slowed from an annualised quarter-on-quarter rate of 3.4% in the fourth quarter of 2013 to 2.1% in the first quarter of 2014.

This was primarily due to a 2.1% contraction of GDP in the United States (US) and slowing growth in China and the European Union (EU).

April – June 2014 (Q2 2014)

Global GDP growth likely recovered slightly in the second quarter as the US economy rebounded strongly and grew by 4% on an annualised quarter-on-quarter basis

Economic conditions in the EU worsened however with Germany surprisingly contracting

4

5

Global EconomyGlobal Economy

5

Source: International Monetary Fund IMF

6

Global EconomyGlobal Economy

International Monetary Fund (IMF) expects world output growth to rebound in the second quarter of 2014 and firmer in 2015 and 2016.

The IMF further projects that imports by advanced economies will increase from 1.4% per annum in 2013 to 4.6% per annum in 2015.

Overall, the economic growth outlook remains weak with significant downside risks.

6

7

Domestic Economy Domestic Economy Real GDP grew by an annualised quarter-on-quarter rate of 0.6% in

the second quarter of 2014.

South Africa’s growth performance was led by the tertiary sector, mainly:

o Government services,

o Finance, real estate and business services, and

o Transport, storage and communication services.

The Manufacturing sector contracted by 2.1% in the second quarter of 2014 due to low production in autos, chemical products, rubber and plastics, glass and non-metallic mineral products.

The contraction in Manufacturing was primarily due to the slow pick up in the mining sector after the prolonged strike in the platinum sector.

7

8

Domestic EconomyDomestic Economy

8

Source: Statssa

9

Domestic EconomyDomestic Economy SA exports and imports to the world declined in the second quarter of

2014.

Imports declined particularly significantly leading to an improvement in SA’s trade deficit.

SA exports to Africa increased from R70.2bn to R71.9 bn resulting in a trade surplus of R39.5 bn with the continent.

SA trade with the world and BRICS were affected by poor growth in the EU and the US.

Demand for commodities and commodity prices remain relatively flat as China’s policymakers attempt to re-balance the economy.

SA trade with Africa consequently remains a priority focus for the dti.

9

10

Domestic EconomyDomestic Economy

10

Source: the dti

Strategic GoalsStrategic Goalsthe dti’s strategic goals for the period under review were:Facilitate transformation of the economy to promote industrial development, investment, competitiveness and employment creation.Build mutually beneficial regional and global relations to advance South Africa’s trade, industrial policy and economic development objectives.Facilitate broad-based economic participation through targeted interventions to achieve more inclusive growth.Create a fair regulatory environment that enables investment, trade and enterprise development in an equitable and socially responsible manner. Promote a professional, ethical, dynamic, competitive and customer-focused working environment that ensures effective and efficient service delivery.

1212

The structure of the dti’s work The structure of the dti’s work

the dti’s work is organised in terms of the following clusters:

Industrial development; Trade, Investment and Exports; Broadening participation; Regulation, and Administration and co-ordination

Key achievements against Key achievements against planned targets for planned targets for

2013/14 Financial Year2013/14 Financial Year

1414

Key AchievementsKey Achievements

SG SG 1: Facilitate transformation of the economy to promote industrial development, investment, competitiveness and employment creationThe sixth iteration of the annual rolling Industrial Policy Action Plan (IPAP

2013/14-2015/16) was successfully launched in April 2013 and implementation reports were produced.

The new SABS Local Content Verification Office was officially launched in July 2013 together with a new technical instrument (SATS) 1286 in support of South Africa’s localisation strategy.

Revised National Industrial Participation Programme (NIPP) guidelines were approved, effectively closing existing loopholes with respect to multiplier calculations.

Concluded local content verification for all transversal contractors on clothing, textiles, leather and footwear (CTLF) tenders with contract value of R1 million or above in December 2013 to gauge compliance with designation instructions.

Industrial DevelopmentIndustrial Development

1515

Key AchievementsKey Achievements

SG SG 1: Facilitate transformation of the economy to promote industrial development, investment, competitiveness and employment creationTotal investment attracted into the Autos sector amounted to R16 billion.Since the designation of buses, 300 buses have been procured with

localisation requirements as set out in the Designation Instruction Note.

Major contracts included: • Mercedes-Benz SA’s successful tender to provide 134 buses for phase

1B of Johannesburg’s Rea Vaya Bus Rapid Transport (BRT) system; • Volvo SA’s successful tender to provide 40 new vehicles to the City of

Cape Town for its extended MyCiti bus routes, at a cost of R180 million; and

• MAN supplying 80 new commuter buses to Great North Transport, Limpopo’s largest public transit operator.

The Automotive Supply Chain Competitiveness Initiative (ASCCI), a partnership between government, labour and business was launched in October 2013.

Industrial DevelopmentIndustrial Development

1616

Key AchievementsKey Achievements

SG 1: Facilitate transformation of the economy to promote industrial development, investment, competitiveness and employment creation

Mercedes-Benz SA has escalated its total investment in South Africa to more than R5 billion, underpinning an increase in its local output to 100 000 units a year and creating 800 new jobs.

Production of the new C-Class has already started at the Mercedes’ East London plant, and will slowly ramp up from the current 250 units to full capacity of 420 units a day.

General Motors SA (GMSA), in partnership with component manufacturer Tenneco SA, had been awarded a R6 billion contract to export catalytic converters to North America.

Part of the 2013/14 Family Planning Tender (all SA-made contraceptives) worth an estimated R100 million has been designated.

Significant progress has been made in the Renewable Energy Independent Power Producer Procurement Programme (REIPPPP), with the Department of Energy (DOE) approving 19 bids in the second round of the solar photovoltaic, wind, small hydro and concentrated solar power sectors.

Industrial DevelopmentIndustrial Development

1717

Key AchievementsKey Achievements

SG 1: Facilitate transformation of the economy to promote industrial development, investment, competitiveness and employment creation

Transnet announced its intention to purchase more than 1 000 locomotives at an estimated value of R50 billion. The Transnet contract commits locomotive manufacturers to a target of 65% local content over time and these will create and preserve approximately 30 000 jobs.

Approximately 3 233 unemployed learners enrolled for training and 2 417 placed to increase the pool of agents suitable for middle management in the Monyetla Work Readiness Programme.

The film Long Walk to Freedom, was produced at a cost of R239 million, premiered and released countrywide in November 2013, earning more than R23 million at the box-office to become the highest-grossing film in the country

In agro-processing, the dti, in collaboration with Buhler, launched the innovative Isigayo plant in April 2013.

MCEP funding approved: 29.7% spent on Agro-processing, 15.7% spent on metals sector and the remainder was spread across other sectors

Industrial DevelopmentIndustrial Development

1818

Key AchievementsKey Achievements

SG 1: Facilitate transformation of the economy to promote industrial development, investment, competitiveness and employment creation

The Clothing and Textile Competitiveness Programme (CTCP) has stabilised the CTLF sector and much progress has been made since the launch of the programme:

• 44 applications were received to the value of R 645 million under the Competitiveness Improvement Programme (CIP), with R77.7 million already disbursed.

• 777 approvals have been made to date, under the Production Incentive Programme (PIP), to a total value of R2.2 billion. Since inception 63 311 jobs have been saved and 8 459 jobs created.

Two new regional footwear clusters have been established under the National Leather and Footwear Cluster Initiative – the Fast-Track Cluster (Eddels) in KwaZulu-Natal and the Southern Cape Regional Footwear Cluster (Watsons).

Industrial DevelopmentIndustrial Development

1919

Key AchievementsKey Achievements

SG 1: Facilitate transformation of the economy to promote industrial development, investment, competitiveness and employment creation

The SEZ Bill was passed by both the National Assembly and the National Council of Provinces (NCOP). The Bill (which has now become law since May 2014) will enable the creation of new industrial hubs and bring previously marginalised regions into the mainstream of the national economy.

A new IDZ was designated at Saldanha Bay in October 2013.

Pre-feasibility studies have been completed for Tubatse in Limpopo and Upington in Northern Cape, while others are being finalised for Bojanala (North West), Maluti-a-Phofung (Free State), Musina (Limpopo) and Nkomazi (Mpumalanga).

Applications for designation have been submitted to the Manufacturing Development Board in respect of Dube Trade Port (KwaZulu-Natal).

Industrial DevelopmentIndustrial Development

20

Overview of Incentive SchemesOverview of Incentive SchemesDescription Actual

Number of firms/projects supported

Potential jobs supported

Total disbursementR’000

Manufacturing Investment IncentivesEnterprise Investment Programme (EIP)- Manufacturing Investment Programme (MIP)

374 11 734 R1 137 620

EIP- Aquaculture Development and Enhancement Programme (ADEP)

20 574

Automotive Investment Scheme (AIS)

36 1 121 R 817 838

12I Tax Allowance Incentive 13 2 681Critical Infrastructure Programme (CIP)

08 4 262 R 139 968

Manufacturing Competitiveness Enhancement Programme (MCEP)

365 106 559 R 991 444

Services Investment IncentivesBusiness Process Services (BPS)

09 2 514 R 278 495

Film & Television 83 - R 276 505

21

Provincial Spread: Broadening Participation Incentives

North West:BBSDP: 32CIS: 10EIP: 12ISP: R 1

Northern Cape:BBSDP: 6CIS: 10EIP: 0ISP: R 3

Western Cape:BBSDP: 53CIS: 11EIP: 80ISP: 7

Eastern Cape:BBSDP: 130CIS: 62EIP: 38ISP: 0

Kwa Zulu Natal:BBSDP: 221CIS: 15EIP: 0ISP:1

Mpumalanga:BBSDP:54CIS: 6EIP: 12 ISP: 4

Limpopo:BBSDP: 208CIS: 74EIP: 20ISP: 3

Gauteng:BBSDP: 339CIS: 48EIP: 128ISP: 7

Free State:BBSDP: 23CIS: 7EIP: 8ISP: 2

22

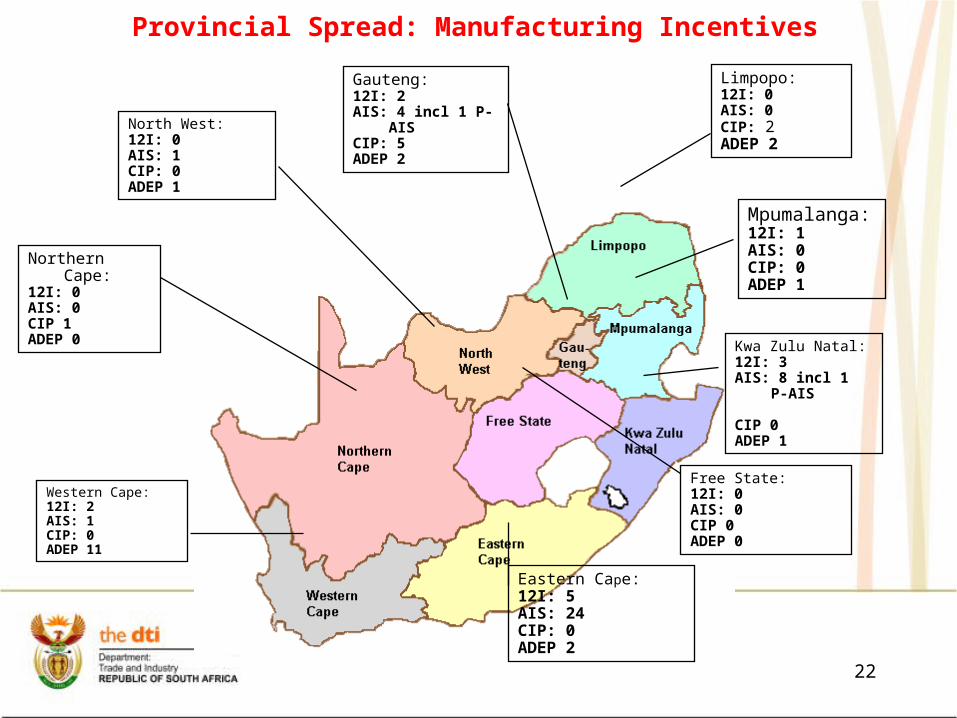

Provincial Spread: Manufacturing Incentives

North West:12I: 0AIS: 1CIP: 0ADEP 1

Northern Cape:12I: 0AIS: 0CIP 1ADEP 0

Western Cape:12I: 2AIS: 1CIP: 0ADEP 11

Eastern Cape:12I: 5AIS: 24CIP: 0ADEP 2

Kwa Zulu Natal:12I: 3AIS: 8 incl 1 P-AIS

CIP 0ADEP 1

Mpumalanga:12I: 1AIS: 0CIP: 0ADEP 1

Limpopo:12I: 0AIS: 0CIP: 2ADEP 2

Gauteng:12I: 2AIS: 4 incl 1 P-AISCIP: 5ADEP 2

Free State:12I: 0AIS: 0CIP 0ADEP 0

23

NORTH WEST2012/13:1 Approval (0.5%)R4.5 m (0.5%)2013/14:6 Approvals (1.6%)R35.3 m (1.3%)

LIMPOPO2012/13:3 Approvals (2%)R11.2 m (1%)2013/14:4 Approvals (1.1%)R 7.3 m (0.3%)

MPUMALANGA2012/13:5 Approvals (3%)R14.9 m (2%)2013/14:7 Approvals (2%)R25.9 m (0.9%)

KWAZULU-NATAL2012/13:29 Approvals (14%)R81.9 m (8%)2013/14:54 Approvals (14.8%)R301.7 m (10.6%)

FREE STATE2012/13:2 Approvals (1%) R1.6 m (1%)2013/14:15 Approvals (4.1%)R63.1 m (2.3%)

EASTERN CAPE2012/13:17 Approvals (8%)R70.6 m (7%)2013/14:32 Approvals (8.8%)R101.1 m (3.6%)

NORTHERN CAPE2012/13:1 Approval (0.5%)R 5.5 m (0.5%)2013/14:2 Approvals (0.5%)R5.7 m (0.2%)

WESTERN CAPE2012/13:66 Approvals (37%)R363 m (36%)2013/14:106 Approvals (29%)R497.8 m (17.5%)

GAUTENG2012/13:73 Approvals (37%)R431.5 m (44%)2013/14:139 Approvals (38.1%)R1.7 b (63.3%)

MCEP Provincial Performance: 2012/13 & 2013/14

24

Overview of Incentive Overview of Incentive SchemesSchemes

Description Actual Total disbursementNumber of firms/projects

supportedR’000

Broadening Participation

Co-operatives Incentive Scheme (CIS)

243 R 75 480

Black Business Supplier Development Programme (BBSDP)

1 066 R 291 493

New Incubation Support Programme (ISP)

28 Paid from EIP budget

Trade, Investment & Exports

Export, Marketing and Investment Assistance(EMIA)

1 835 R 273 818

BBSDP Applications Approved in 2013/14 per province

25

26

CIS Applications Approved In 2013/14

CPFP Assistance Across Countries For 2013-14

27

Senegal •Railway Development

Sierra Leone•Marampa Iron Ore Mine •Marampa Renewable energy

Ghana•Housing Development •Sugar Cane Fields Development

Angola •Development of the Hotel Chain

Namibia •Logistics Activity Precinct •Omitiomire Oxide Project

Zambia •Chingola Railway Line •Ndola Gold project•Solid waste to Energy project

Zimbabwe•Establishment of the Dark Fibre Infrastructure•Development of the Musami Dam project

Burundi •Mule Hydropower development •Jiji Hydropower Development

Madagascar•Molo Graphite Mine

Mozambique•Mineral Sand Deposits•Picoco III Housing Development•Alluvial Gold Mine

Tanzania•20 000 Housing Development •East Africa Dry Port

Ethiopia•Development of the Beef Abattoir

Guinea•Iron Ore Mine •Bel Air Bauxite Mine

Cameroon •Development of the Student Housing

Malawi •Solid Waste to Energy project

28

GAUTENG2012/13: 488 Approvals (47%)R35 630 177 (50%) 2013/14:526 Approvals (51%) R42 152 950 (54%)

LIMPOPO2012/13:6 Approvals (1%)R436 516 (1%) 2013/14; 6 Approvals (1%) R379 316 (1%)

MPUMALANGA2012/13:40 Approvals (4%)R3 275 095 (5%) 2013/14:50 Approvals (5%) R4 832 511 (6%)

KWAZULU-NATAL2012/2013:67 approvals (7%)R4 279 120 (6%) 2013/14:74 Approvals (7%) R5 011 653 (7%)

FREE STATE2012/2013:5 Approvals (1%)R192 142 (1%) 2013/14:6 Approvals (1%)R322 384 (1%)

EASTERN CAPE2012/2013:26 approvals (2%)R1 982 895 (3%) 2013/14:28 Approvals (3%) R2 004 402 (3%)

NORTH WEST2012/13:13 approvals (1%)R832 003 (1%) 2013/14:9 Approvals (1%) R829 654 (1%)

NORTHERN CAPE2012/13:0 approvals (0%)R0 (0%) 2013/14:0 Approvals (0%)R0 (0%)

WESTERN CAPE2012/13:373 approvals (37%)R23 253 853 (33%) 2013/14:318 Approvals (31%) R21 602 258 (27%)

EMIA Provincial Performance: 2012/13 & 2013/14

29

BPS & FILM Achievements 2013/14

Investment: R 325mIncentive: R 8,4mJobs: 750

Investment: R 66,723mIncentive: R 4,952mJobs: 788

Investment: R2,633mIncentive: R72,000Jobs: 285

Investment: R 13,2mIncentive: R 18,667Jobs: 93

Trade, Investment and ExportsTrade, Investment and ExportsSG SG 2: Build mutually beneficial regional & global relations to advance South Africa’s trade, industrial policy & economic development objective

Southern African Development Community (SADC)

•SADC Services negotiations: submitted South Africa’s initial offers on financial and communication services.

•Agreement reached at Cabinet’s International Cooperation, Trade and Security Cluster (ICTS) Director-General level to submit a cabinet memorandum to take steps to encourage compliance by certain SADC Members of their commitments under the SADC Trade Protocol.

30

Trade, Investment and ExportsTrade, Investment and ExportsSG SG 2: Build mutually beneficial regional & global relations to advance South Africa’s trade, industrial policy & economic development objective

Southern African Customs Union (SACU)

•Consensus reached on the need for high level bilateral engagement in SACU towards effective implementation of a development integration approach in SACU.

•Cabinet memorandum on options for South Africa in SACU was discussed at Cabinet.

•Unified engagement by SACU in its trade negotiations with third parties e.g. Economic Partnership Agreement (EPA), Tripartite Free Trade Agreement (T-FTA).

31

Trade, Investment and ExportsTrade, Investment and ExportsSG SG 2: Build mutually beneficial regional & global relations to advance South Africa’s trade, industrial policy & economic development objective

Tripartite Free Trade Agreement (T-FTA) negotiations•Agreement reached on the scope and coverage of the Phase 1 negotiations.

•Progress made in the tariff negotiations (Consultations within SACU on tariff offers to the East African Community (EAC) & Egypt at an advanced stage)

•Good progress made on the negotiations on the text:•successful conclusion of the non-tariff barrier (NTB) and technical barriers to trade (TBT) provisions that contain over 90% of South Africa’s inputs;•Agreement to re-open negotiation on trade facilitation related

annexes in light of the World Trade Organisation tripartite agreement

32

Trade, Investment and ExportsTrade, Investment and ExportsSG SG 2: Build mutually beneficial regional & global relations to advance South Africa’s trade, industrial policy & economic development objective

African Union (AU)/ New Partnership for Africa’s Development (NEPAD)

• Guidelines of Good Business Practice approved by the ICTS Directors-

General Cluster of Cabinet.

• Hosting of Africa-India Trade Ministerial Conference.

• Influenced Africa Partnerships to promote support for the development

integration agenda in Africa.

Tabled three memoranda of understanding (MoUs) on Economic Cooperation (Ghana, Benin and Nigeria) before Parliament.

Finalised draft MoU on Automotive Cooperation between SA and Nigeria. Draft text exchanged through diplomatic channels.

33

Trade, Investment and ExportsTrade, Investment and ExportsSG SG 2: Build mutually beneficial regional & global relations to advance SA’s trade, industrial policy & economic development objective

Engaged in 32 Business and/or Technical missions to promote economic cooperation.

Participated in 81 government to government platforms.

Conclusion and implementation of the South Africa- Cuba agreement on economic assistance.

Completion of the South Africa- Japan Joint Study on Economic Cooperation.

Continued lobbying for extension of South Africa’s inclusion in the African Growth Opportunity Act (AGOA).

Conclusion of the WTO Bali Package which included an agreement on Trade Facilitation

Drafted responses and made a presentation at a public hearing of

Australia’s safeguard investigation on canned fruits.34

Trade, Investment and ExportsTrade, Investment and ExportsSG SG 2: Build mutually beneficial regional & global relations to advance South Africa’s trade, industrial policy & economic development objective

Facilitated exports of R 3. 4 billion

1 000 companies were trained on the Global Exporter Passport Initiative to enhance their export readiness.

Obtained third position for the best stand in Mozambique (FACIM) in August 2013.

Made inputs to the review of International Trade Administration Commission’s (ITAC) Anti-Dumping and Countervailing Regulations.

Terminated the European Union (EU) bi-lateral investment treaty (BIT).

Published the draft Promotion and Protection of Investment Bill for public comment.

35

Trade, Investment and ExportsTrade, Investment and ExportsSG SG 2: Build mutually beneficial regional & global relations to advance South Africa’s trade, industrial policy & economic development objective

Investment Pipeline of R 60.5 bn with a potential of creating 34 560 jobs

Major projects in manufacturing, mining and green economy. Total investment attracted into the green industries sector amounted to approximately R10 billion.

Multinationals have affirmed South Africa as a hub and a Gateway into the continent with new investments and expansions in the manufacturing sector. These include Unilever, Proctor & Gamble, Nestle, Samsung, Hisense FAW, IVECO amongst others.

Domestic companies such as Aspen, MPACT, Amka, Gibela Rail have expanded or added new investment.

36

37

AIS & 12I achievements 2013/14

Investment: R 569mAllowance: R 202m

Investment: R1bAllowance: R 496mJobs: 1112

InvestmentL R5,4bnIncentive: R1,6bnJobs: 254

Mercedes Benz SA

Investment: R 301mIncentive: R 90,4mJobs: 73

Johnson Controls Automotive South Africa (Pty) Ltd - W205 C-Class Mercedes Interior Project

Investment: R257,6mIncentive: R64,4m

Jobs: 190

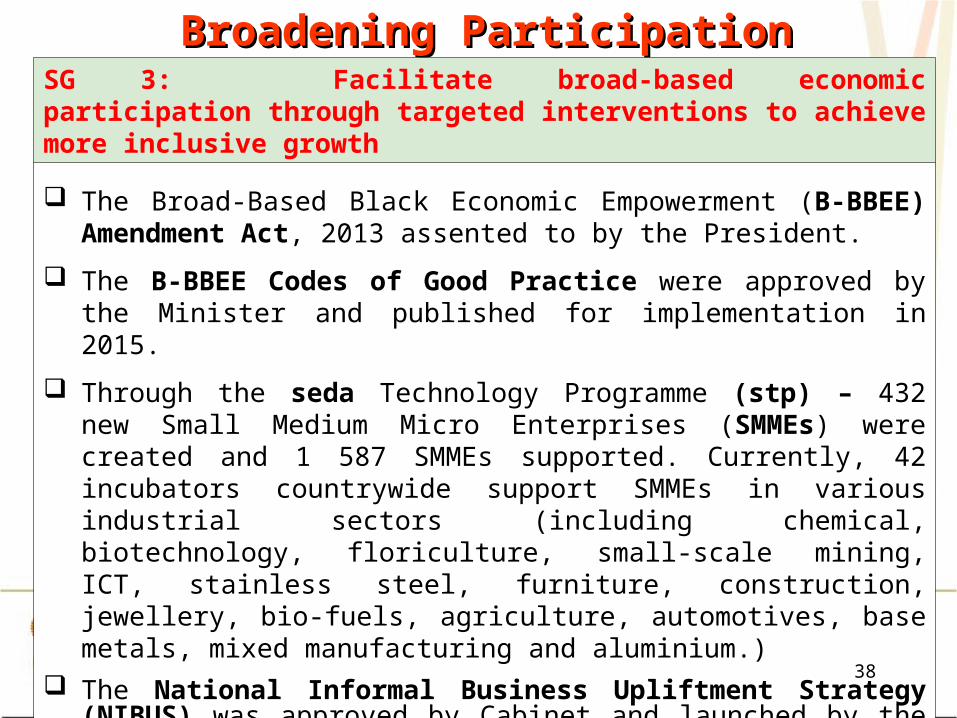

Broadening ParticipationBroadening ParticipationSG 3: Facilitate broad-based economic participation through targeted interventions to achieve more inclusive growth

The Broad-Based Black Economic Empowerment (B-BBEE) Amendment Act, 2013 assented to by the President.

The B-BBEE Codes of Good Practice were approved by the Minister and published for implementation in 2015.

Through the seda Technology Programme (stp) – 432 new Small Medium Micro Enterprises (SMMEs) were created and 1 587 SMMEs supported. Currently, 42 incubators countrywide support SMMEs in various industrial sectors (including chemical, biotechnology, floriculture, small-scale mining, ICT, stainless steel, furniture, construction, jewellery, bio-fuels, agriculture, automotives, base metals, mixed manufacturing and aluminium.)

The National Informal Business Upliftment Strategy (NIBUS) was approved by Cabinet and launched by the Minister in March 2014.

38

Broadening ParticipationBroadening ParticipationSG 3: Facilitate broad-based economic participation through targeted interventions to achieve more inclusive growth

The Co-operatives Amendment Act, 2013 was assented to by the President in August 2013 and provides for the Co-operative Development Agency (CDA), with its primary role being to provide support with the development and capacity building of co-operatives as well as the Co-operatives Tribunal to look at resolving disputes.

The Integrated SMMEs and Co-operative Development Framework and Action Plan have been approved by MinMec and the Minister. Phased implementation of the Action Plan is in progress.

The Isivande Women’s Fund (IWF) supported 16 projects. Supported 322 companies participating in the Workplace Challenge

Programme (WCP) Revised the draft National Strategic Framework on Gender and Women

Empowerment. Youth Enterprise Development Strategy (YEDS) approved and launched

by Minister in November 2013.

39

RegulationRegulationSG4: Create a fair regulatory environment that enables investment, trade and enterprise development in an equitable and socially responsible manner

The Lotteries Amendment Act and the Intellectual Laws Property Amendment Act for the Protection of Traditional Knowledge were assented to by the President.

The National Credit Amendment Bill was adopted by both Houses of Parliament.

Developed Draft Policy Frameworks on Intellectual Property and Gambling

Policy Framework and Bill for Licensing of Businesses developed and public consultations conducted.

An Impact Assessment Study on the Liquor Act, 2003 and draft Policy were developed and the results were incorporated in the draft liquor policy.

40

AdministrationAdministrationSG5: Promote a professional, ethical, dynamic and competitive and customer – focused working environment that ensures effective and efficient services delivery

The vacancy rate was at 9.4% with an employee retention rate of 93.2% (the cumulative turnover stood at 6.8% in respect of permanent employees).

The department recorded 44% of women employed in Senior Management Service (SMS) positions and 2.7% people with a disability.

Payment of all eligible creditors made well within 30 days.

Received an award in 2013 as the “Top performing government department” at the eleventh Annual National Business Awards organised by the private sector. Also received an acknowledgment as the second best functioning national department in 2012, according to the Management Performance Assessment Tool (MPAT) conducted by the Presidency’s DPME last year

41

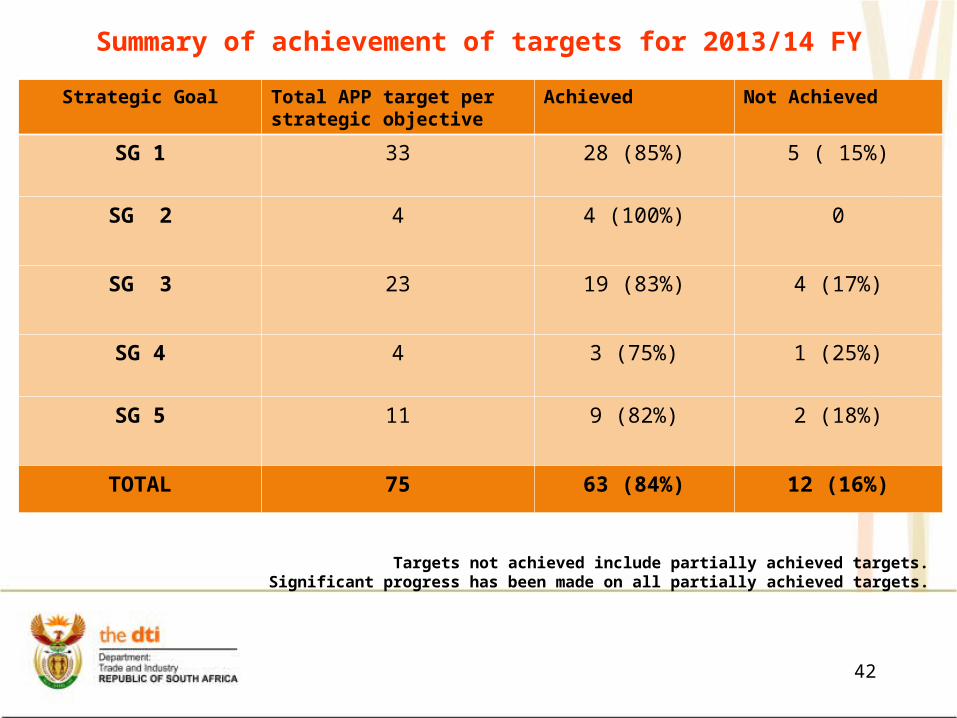

Summary of achievement of targets for 2013/14 FY

42

Strategic Goal Total APP target per strategic objective

Achieved Not Achieved

SG 1 33 28 (85%) 5 ( 15%)

SG 2 4 4 (100%) 0

SG 3 23 19 (83%) 4 (17%)

SG 4 4 3 (75%) 1 (25%)

SG 5 11 9 (82%) 2 (18%)

TOTAL 75 63 (84%) 12 (16%)

Targets not achieved include partially achieved targets.Significant progress has been made on all partially achieved targets.

43

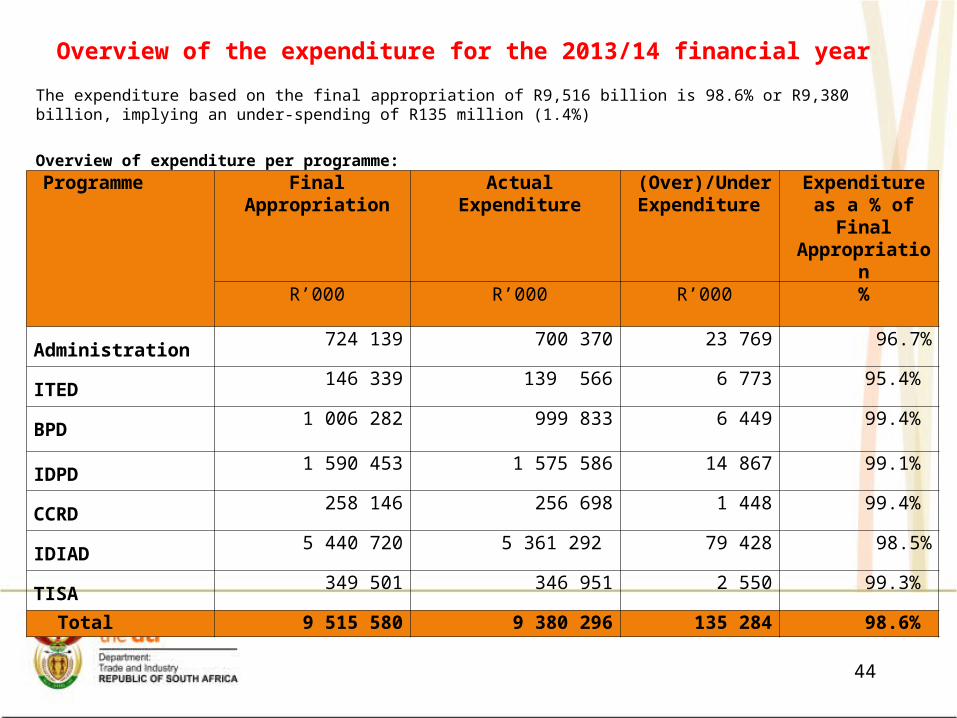

Financial Financial managementmanagement

44

Programme

FinalAppropriation

ActualExpenditure

(Over)/Under Expenditure

Expenditure as a % of Final

AppropriationR’000 R’000 R’000 %

Administration724 139 700 370 23 769 96.7%

ITED146 339 139 566 6 773 95.4%

BPD1 006 282 999 833 6 449 99.4%

IDPD1 590 453 1 575 586 14 867 99.1%

CCRD258 146 256 698 1 448 99.4%

IDIAD5 440 720 5 361 292 79 428 98.5%

TISA349 501 346 951 2 550 99.3%

Total 9 515 580 9 380 296 135 284 98.6%

Overview of the expenditure for the 2013/14 financial year

The expenditure based on the final appropriation of R9,516 billion is 98.6% or R9,380 billion, implying an under-spending of R135 million (1.4%)

Overview of expenditure per programme:

45

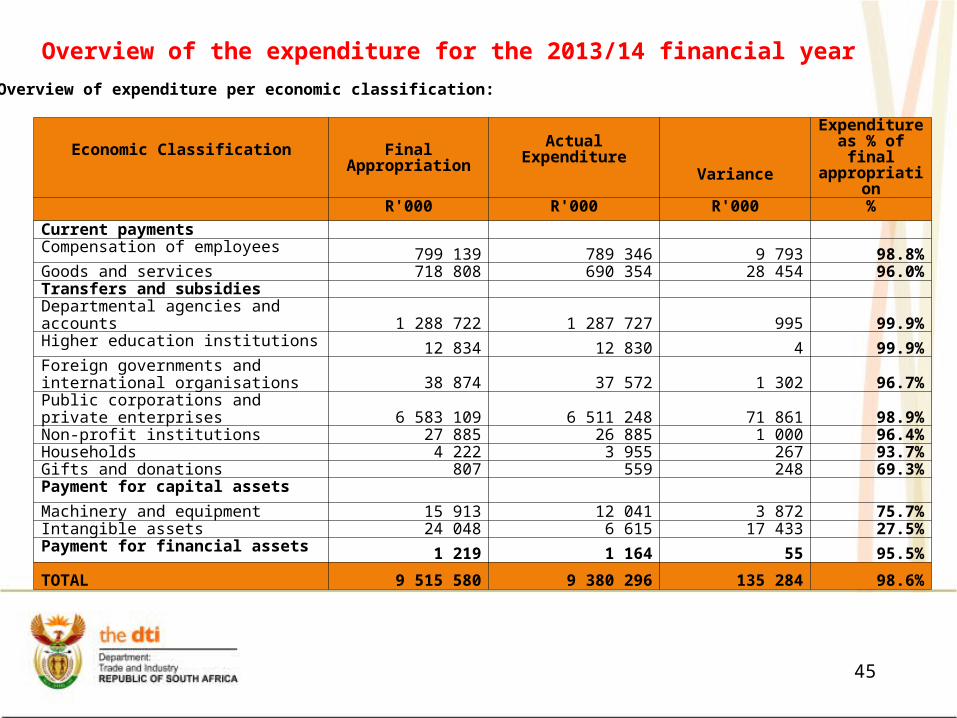

Economic Classification

FinalAppropriation

ActualExpenditure

Variance

Expenditureas % of final appropriation

R'000 R'000 R'000 %

Current payments Compensation of employees 799 139 789 346 9 793 98.8%Goods and services 718 808 690 354 28 454 96.0%Transfers and subsidies Departmental agencies and accounts 1 288 722 1 287 727 995 99.9%Higher education institutions 12 834 12 830 4 99.9%Foreign governments and international organisations 38 874 37 572 1 302 96.7%

Public corporations and private enterprises 6 583 109 6 511 248 71 861 98.9%Non-profit institutions 27 885 26 885 1 000 96.4%Households 4 222 3 955 267 93.7%Gifts and donations 807 559 248 69.3%Payment for capital assets Machinery and equipment 15 913 12 041 3 872 75.7%Intangible assets 24 048 6 615 17 433 27.5%Payment for financial assets 1 219 1 164 55 95.5%

TOTAL 9 515 580 9 380 296 135 284 98.6%

Overview of the expenditure for the 2013/14 financial year

Overview of expenditure per economic classification:

46

Audit outcome for 2013/14 Financial Year and

interventions to address the Auditor-General’s

findings

Audit outcomes

the dti has received a financially unqualified audit opinion from the Auditor-General South Africa (AGSA) for the 2013/14 financial year,

47

48

Finding Management interventionsThe accounting officer did not take steps to prevent irregular expenditure.

These relate to transactions where three quotations could not be obtained. The following additional measures was implemented:

•Clear communication via financial circulars on the procurement requirements of transactions less than R500,000 have been implemented.•Targeted training interventions with procurement staff and divisional advisors on the department’s procurement policies and procedures and SCM legislation was implemented.•An information session on irregular expenditure was presented by National Treasury on 28 October 2013•An easy to follow guide was also distributed during December 2013 to assist staff with the procurement procedure to be followed in order to prevent irregular expenditure•Irregular expenditure transactions are analysed per Division and memoranda were issued on a quarterly basis to the relevant managers to take appropriate action against staff that permits irregular expenditure. •Based on the implemented additional controls irregular expenditure reduced from R32 966 million in 2012/13 to R6 376 million in 2013/14.

Interventions to address AGSA’s Audit Findings

49

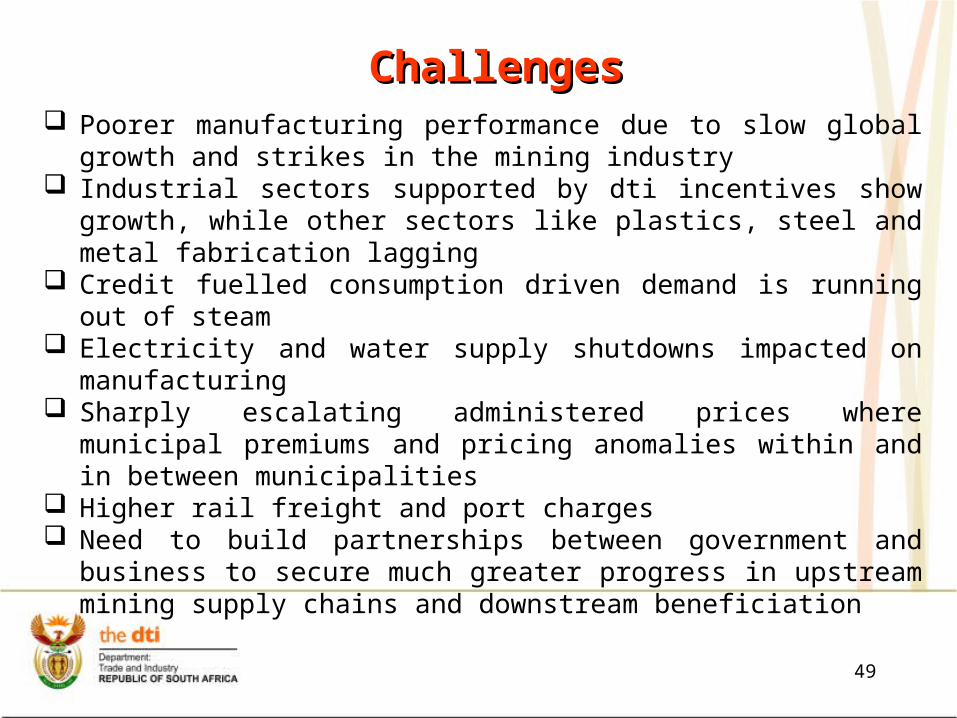

Poorer manufacturing performance due to slow global growth and strikes in the mining industry

Industrial sectors supported by dti incentives show growth, while other sectors like plastics, steel and metal fabrication lagging

Credit fuelled consumption driven demand is running out of steam Electricity and water supply shutdowns impacted on manufacturing Sharply escalating administered prices where municipal premiums and

pricing anomalies within and in between municipalities Higher rail freight and port charges Need to build partnerships between government and business to

secure much greater progress in upstream mining supply chains and downstream beneficiation

ChallengesChallenges

Ke ya lebogaKe a leboha

Ke a lebogaNgiyabonga

Ndiyabulela Ngiyathokoza

NgiyabongaInkomu

Ndi khou livhuhaDankie

Thank you

![2017 Full Year Results Presentation 29 August 2017 For personal use only DTI … · 2017-08-29 · DTI GROUP LTD 2017 Interim Results Presentation [_] February 2017 1 PETER TAZEWELL](https://static.fdocuments.net/doc/165x107/5f9e21b6f53076431645c599/2017-full-year-results-presentation-29-august-2017-for-personal-use-only-dti-2017-08-29.jpg)

![Downtown Presentation DTI Civic River2Rail River South ... · Microsoft PowerPoint - Downtown Presentation DTI Civic_River2Rail_River South [Read-Only] Author: kwagers Created Date:](https://static.fdocuments.net/doc/165x107/5fde234ae286745b1860198d/downtown-presentation-dti-civic-river2rail-river-south-microsoft-powerpoint.jpg)