The Daft.ie House Price Report analysis of recent trends in the Irish residential sales market for...

13

An analysis of recent trends in the Irish residential sales market for 2017 Q2 The Daft.ie House Price Report Introduction by Ronan Lyons, Assistant Professor of Economics at Trinity College Dublin and author of the Daft Report.

Transcript of The Daft.ie House Price Report analysis of recent trends in the Irish residential sales market for...

An analysis of recent trends in the Irish residential sales market for 2017 Q2

The Daft.ie HousePrice Report

Introduction by Ronan Lyons, Assistant Professor of Economics

at Trinity College Dublin and author of the Daft Report.

Sales market shows rule changes had expected effect.

The figures from this latest Daft.ie House Price Report show a sharp increase in prices around the country, for the second quarter in a row.

The national average list price in June was 8.8%

higher than in December. To put that in perspective,

prices rose by 8% in the whole of 2016 – and by

8.5% in 2015. If the first half of 2017 is anything to

go by, price increases are likely to match or exceed

those in 2014, when they rose by 14%.

That year, it was Dublin that drove those trends,

with prices in Dublin rising by 21% during 2014,

compared to 9% elsewhere in the country. And it

seems as though the same pattern is re-emerging

in the 2017 market. As shown in the graph

accompanying this article, annual inflation in the

Dublin market exceeds the rate elsewhere in the

country for the first time since early 2015.

-20%

-10%

0

10%

20%

30%

Elsewhere

Dublin

Q12015

Q12012

Q12010

Q12017

Q12016

Annual inflation in list prices, by region

Q12014

Q12011

Q12013

What took the steam out of the Dublin market

in early 2015 was the introduction of the Central

Bank’s mortgage rules. They were designed to

anchor housing prices to the real economy, in other

words to reflect supply and demand – especially

household incomes.

Before those rules were mooted, there was next

to nothing – other than collective memory of how

bad the last bubble was – to stop another credit-

fuelled bubble from happening. Expectations about

future house price increases are central to bubbles

and, as of late 2014, those expectations were high.

In Dublin, for example, survey respondents in late

2014 expected prices to increase by 12% in the

following year.

The Central Bank rules, though, by requiring a

minimum deposit in particular, took the sting out of

a potential housing bubble. Expectations of price

increases fell dramatically from 12% to just 3%. The

effect was obvious, especially in the Dublin market.

Price inflation fell from almost 25% to 1%.

What has changed? In terms of the underlying

market fundamentals of supply and demand, very

little. As outlined in my commentary to the January

report, the country still needs at least 40,000 and

probably closer to 50,000 homes of all types every

year. And still it gets just a small fraction of that –

with perhaps just 3,000 new homes added by the

professional construction sector in 2016.

All of this would point to prices rising as fast as is

consistent with the Central Bank rules. But what

happens when those rules change? This is what

happened late last year. The rules were changed in

quite a specific way: all first-time buyers now face a

Ronan Lyons, Economist at Trinity College Dublin and author of the Daft Report

The Daft.ie House Price Report – 2017 Q2 | 2

Market SurveyEach quarter, Daft.ie surveys over 1,000 property market participants, asking them about their sense of the market as a whole, and their own intentions. Below are some of the headline results.

Expected house price inflation over next five years reaches new high

The expected change in house prices over the coming 5 years currently stands at 13.6%, its highest on record since 2011. In Dublin, expected inflation over five years has risen from 8.4% in early 2016 to 19.1% in mid-2017.

Expected price change this year

Expected price-income ratio reaches new high in Dublin

Nationwide, the average expected price-income ratio is stable 4.4 - and outside Dublin is stable at 4.2. In the capital, however, the ratio has reached 4.8, the join highest on record (with 2015Q4).

Planned house price-to-income ratio

Perceptions of value at record low

Fewer than 10% of respondents believe property prices in Dublin represent good value currently, down from 43% in late 2012. Elsewhere in the country, the fraction believing prices represent good value has fallen from 49% to 26% since late 2015.

Perceptions of value

National Dublin Ex-Dublin National Dublin Ex-Dublin

0%

10%

20%

30%

40%

50%

60%

70%

80%

Q22017

Q12017

Q42016

Q32016

Q22016

Q12016

Q42015

Q42014

Q42013

Q42012

Q42011

Q22017

Q12017

Q42016

Q32016

Q22016

Q12016

Q42015

Q42014

-15%

-5%

0%

5%

10%

15%

-10%

Q42013

Q42012

Q42011

20%

-20%

National Dublin Ex-Dublin

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Q22017

Q12017

Q42016

Q32016

Q22016

Q12016

Q12015

Q12014

Q12013

Q12012

1.0

National Dublin Ex-Dublin National Dublin Ex-Dublin

0%

10%

20%

30%

40%

50%

60%

70%

80%

Q22017

Q12017

Q42016

Q32016

Q22016

Q12016

Q42015

Q42014

Q42013

Q42012

Q42011

Q22017

Q12017

Q42016

Q32016

Q22016

Q12016

Q42015

Q42014

-15%

-5%

0%

5%

10%

15%

-10%

Q42013

Q42012

Q42011

20%

-20%

National Dublin Ex-Dublin

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Q22017

Q12017

Q42016

Q32016

Q22016

Q12016

Q12015

Q12014

Q12013

Q12012

1.0

National Dublin Ex-Dublin National Dublin Ex-Dublin

0%

10%

20%

30%

40%

50%

60%

70%

80%

Q22017

Q12017

Q42016

Q32016

Q22016

Q12016

Q42015

Q42014

Q42013

Q42012

Q42011

Q22017

Q12017

Q42016

Q32016

Q22016

Q12016

Q42015

Q42014

-15%

-5%

0%

5%

10%

15%

-10%

Q42013

Q42012

Q42011

20%

-20%

National Dublin Ex-Dublin

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Q22017

Q12017

Q42016

Q32016

Q22016

Q12016

Q12015

Q12014

Q12013

Q12012

1.0

The Daft.ie House Price Report – 2017 Q2 | 4

10% deposit, rather than the 20% faced by the rest

of the market on anything over €220,000.

This means that first-time buyers buying expensive

homes have seen the biggest reduction in the

deposit required. To give an example, someone

buying a property in Dublin worth €250,000

has seen the required deposit fall by just over

10% (from €28,000 to €25,000). But someone

buying a property worth €660,000 has seen their

deposit requirement fall by 40% (from €110,000 to

€66,000).

Therefore, we would expect the change in the

Central Bank rules to have the largest effect on the

most expensive markets in the country. And, by

and large, this is what we have seen in the last six

months. Prices in Connacht and Ulster have risen

by 6% in the last six months. But prices in Dublin

have risen by 10% in just six months. In Dublin 2

and Dublin 8, two of the country’s most expensive

markets, prices are up by 16% since the start of the

year.

Some might argue that what we are seeing is the

effect not of the change in Central Bank rules, but

rather the almost contemporaneous Help-to-Buy

scheme brought in by the Government in the

last Budget. There have simply not been enough

new homes sold in the first half of 2016 for this to

explain such market-wide trends, however.

There have been about 1,200 sales of new homes

in Dublin in the first half of 2017, compared to

about 1,500 in the second half of 2016. This

represents about one fifth of the overall market in

the capital – which is probably too small a tail to

wag the dog that is the second-hand market. (In a

more health market, the new-home segment would

constitute close to half of all sales.)

More importantly, though, the Help-to-Buy scheme

would have had opposite effect across cheaper and

dearer markets. Its caps were such that its impact

would be greatest in the cheaper segments of the

market. Those buying new homes above €400,000

have a smaller percentage rebate, while those

buying above €600,000 have none at all.

Thus, we are left with the conclusion the changes

in the Central Bank rules had precisely the effect

predicted of them. There is some solace in that:

the Central Bank rules are perhaps the single most

important brake on housing prices. When those

rules are relaxed, prices rise, as supply is simply

not sufficient to meet demand. But if they are

maintained in their current form, the current spike

in house price inflation will prove to be just that.

The primary focus of policy efforts in the housing

market over the last 18 months has been to further

stimulate demand and prices. As I have written on

a number of occasions in the last year, what we

need is a focus on supply and quantities. When

obsolescence, falling household size, natural

increase and net migration are factored in, the

country needs 50,000 homes a year. It is not getting

that, and supply has not been meeting demand

since 2011, meaning we have also a backlog to

meet.

The principal reason why so few homes are being

built is the high cost of construction. Hopefully the

new Housing Minister will focus on reducing the

hard costs of construction. This will have beneficial

effects for both market and social housing.

Combined with a strategy for using vacant homes,

using land better and reform of housing subsidies,

it is entirely possible for this country to have a

healthy housing system.

3 | The Daft.ie House Price Report – 2017 Q2

Cork City€256,201 | 9.2%

Limerick City€177,199 | 15.1%

Galway City€268,535 | 13.4%

Waterford City€158,861 | 14.5%

NationwideAverage asking prices and Y-on-Y change

DublinAverage asking prices and Y-on-Y change

North County€302,457 | 12.7%

South County€563,442 | 8.8%

West County€297,070 | 7.0%

South City€387,266 | 11.7%

City Centre€299,635 | 18.2%

North City€323,550 | 13.0%

MN€160,55910.5%

CN€149,1328.3%

WH€184,02415.7%

LD€128,81623.5%

LH€210,08816.9%

MH€249,90312.5%

KE€253,68512.1%

WW€314,84011.2%

WX€197,53915.2%

CW€176,51018.0%

KK€210,17612.0%

LS€164,30711.8%

OY€170,56613.2%

G€182,3108.5%

MO€145,6187.0%

SO€133,88713.8%

DL€145,2175.0%

RN€129,6686.7%

LM€123,8844.5%

CE€165,4989.5%

T€162,9569.1%

L€170,8665.4%

C€206,68611.4%

KY€179,6836.4%

W€204,72911.9%

Prices up 46% from their lowest pointNationally, the average asking price reached its lowest point in

the third quarter of 2013 and has risen 46.2% - or just under

€76,000 - since then. In Dublin, however, the bottom was

reached in the second quarter of 2012 and prices have risen

by an average of 60% - or €132,500 - since that time. The last

part of the country to see prices level off was Limerick - in

both Limerick city and county, prices only reached their lowest

point in the final quarter of 2014 but prices have risen by 49%

in the city (and by 30% in the county) since then.

The Daft.ie House Price Report – 2017 Q2 | 65 | The Daft.ie House Price Report – 2017 Q2

4.3%Quarter-on-quarter change in average list price

Daft.ie List Price Index

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

January 185.3 213.8 212.9 184.5 151.6 128.2 105.6 96.8 99.9 112.8 122.1 134.1

February 200.2 215.8 212.3 180.9 150.3 128.1 104.5 96.1 99.3 117.6 122.9 135.6

March 198.1 214.8 209.6 177.4 146.7 125.3 102.9 96.6 103.3 119.1 125.7 135.8

April 203.2 216.5 208.1 174.7 146.6 121.8 101.7 96.6 104.5 118.7 125.0 140.9

May 205.3 217.5 205.7 171.0 145.0 120.1 102.2 97.0 107.2 119.4 126.0 141.9

June 207.1 217.1 203.4 167.7 141.8 116.1 99.5 97.5 107.9 118.2 127.8 140.9

July 209.3 219.2 202.3 165.1 138.0 115.4 97.8 96.5 109.9 120.3 128.9

August 210.4 217.5 199.6 161.2 137.6 113.1 98.9 97.0 111.2 120.4 130.1

September 213.8 215.8 198.1 159.2 136.5 113.3 97.1 96.7 112.9 121.5 130.9

October 214.7 214.8 193.7 156.4 134.0 108.7 97.9 97.2 110.5 120.6 128.7

November 212.8 212.4 188.2 152.3 130.9 106.0 95.8 96.9 110.0 119.5 129.0

December 214.9 213.5 186.3 150.9 129.8 106.0 96.0 96.2 111.1 119.8 131.0

Asking Prices, Residential Sales(2012 average = 100)

7 | The Daft.ie House Price Report – 2017 Q2

Strong rises in prices continueThe rise of 4.3% in the average list price seen in the second quarter of 2017 matches the rise in the first quarter, which was the largest since early 2015.

Inflation in Dublin now exceeds rate elsewhere

For the first time in over two years, the annual rate of inflation in Dublin (12.3%) exceeds the rate elsewhere in the country (11.3%).

Largest number of new listings since mid-2008

May 2017 saw over 6,000 properties listed for sale nationwide, the largest monthly total in almost 9 years.

Two in five properties sell within two months

40% of properties listed currently find a buyer within four months, up from 35% a year ago.

Stock of properties on Daft.ie (start of month) and flow of properties, 2007-2017

Stock (lhs) Inflow (rhs) Outflow (rhs)

0

2000

4000

6000

8000

10000

12000

14000

2009 2010 2011 2012 2013 2014 2015 2016 2008 2007

0

10000

20000

30000

40000

50000

60000

70000

2017

The Daft.ie House Price Report – 2017 Q2 | 8

The Daft.ie Asking Price Index is based on asking prices for properties posted for sale on Daft.ie. An index based on asking price, as opposed to closing price, is a measure of sellers’ expectations. Figures are calculated from econometric regressions, which calculate changes in price that are independent of changes in observable measures of quality, such as location, or bedroom number.

Daft.ie Snapshot ofAsking Prices Nationwide Average asking prices across Ireland (€000s), and annual change (%), 2017 Q2

The Daft.ie House Price Report – 2017 Q2 | 109 | The Daft.ie House Price Report – 2017 Q2

LEIN

STER

MU

NST

ERCO

NN

ACH

TU

LSTE

R

OTH

ER C

ITIE

S

1 bed apartment 2 bed terraced 3 bed semi-d 4 bed bungalow 5 bed detached

Dublin 1 €204 17.6% €306 19.3% €415 17.2% €579 11.4% €770 16.5%

Dublin 2 €275 19.0% €382 20.4% €526 14.8% €748 10.5% €871 12.8%

Dublin 3 €222 4.5% €332 13.5% €453 12.0% €668 3.0% €876 11.2%

Dublin 4 €320 14.4% €435 7.7% €648 8.7% €1,036 5.4% €1,299 7.7%

Dublin 5 €177 9.6% €254 17.3% €360 12.5% €565 9.6% €724 20.9%

Dublin 6 €293 10.6% €420 17.9% €595 13.1% €935 10.2% €1,197 21.6%

Dublin 6W €239 7.4% €342 14.9% €485 10.2% €762 7.4% €976 18.5%

Dublin 7 €186 13.0% €267 20.9% €378 15.9% €594 13.0% €761 24.6%

Dublin 8 €194 14.7% €278 22.7% €394 17.7% €618 14.7% €792 26.6%

Dublin 9 €181 7.2% €259 14.6% €367 10.0% €576 7.2% €738 18.2%

Dublin 10 €116 10.5% €166 18.3% €235 13.4% €369 10.5% €472 22.0%

Dublin 11 €141 11.9% €202 19.7% €286 14.8% €450 11.9% €576 23.5%

Dublin 12 €159 11.2% €228 19.0% €324 14.2% €509 11.2% €651 22.8%

Dublin 13 €182 6.2% €261 13.7% €370 9.0% €582 6.2% €745 17.2%

Dublin 14 €230 7.6% €329 15.1% €466 10.4% €733 7.6% €938 18.7%

Dublin 15 €144 10.6% €206 18.3% €292 13.5% €459 10.6% €588 22.1%

Dublin 16 €200 8.1% €287 15.6% €406 10.9% €638 8.1% €818 19.3%

Dublin 17 €122 6.5% €175 14.0% €248 9.3% €390 6.5% €499 17.6%

Dublin 18 €221 5.2% €317 12.6% €450 8.0% €707 5.2% €905 16.1%

Dublin 20 €166 9.6% €238 17.3% €338 12.5% €530 9.6% €679 21.0%

Dublin 22 €117 8.1% €168 15.6% €238 10.9% €374 8.1% €478 19.3%

Dublin 24 €125 7.5% €179 15.0% €254 10.3% €399 7.5% €510 18.6%

North Co Dublin €144 8.6% €207 16.2% €293 11.5% €460 8.6% €589 19.9%

South Co Dublin €259 4.7% €372 12.0% €527 7.4% €827 4.7% €1,060 15.5%

West Dublin €139 6.0% €200 13.4% €283 8.7% €444 6.0% €569 16.9%

Cork City €101 7.3% €145 16.0% €221 7.4% €383 7.2% €463 8.6%

Galway City €98 11.5% €141 20.5% €215 11.6% €372 11.4% €449 12.8%

Limerick City €73 12.5% €104 21.6% €159 12.6% €276 12.4% €333 13.8%

Waterford City €62 12.5% €89 21.6% €136 12.6% €237 12.4% €286 13.8%

1 bed apartment 2 bed terraced 3 bed semi-d 4 bed bungalow 5 bed detached

Meath €90 10.6% €128 20.1% €179 14.8% €346 14.9% €390 19.9%

Kildare €97 10.4% €137 19.8% €192 14.6% €372 14.7% €419 19.7%

Wicklow €119 9.5% €167 18.8% €235 13.7% €453 13.7% €511 18.7%

Louth €82 14.9% €116 24.8% €162 19.3% €313 19.4% €353 24.6%

Longford €44 21.9% €61 32.4% €86 26.6% €167 26.7% €188 32.2%

Offaly €61 11.6% €86 21.2% €121 15.9% €233 16.0% €263 21.0%

Westmeath €67 13.9% €94 23.6% €132 18.3% €255 18.3% €287 23.5%

Laois €61 10.2% €86 19.6% €121 14.4% €233 14.5% €263 19.5%

Carlow €63 16.5% €89 26.5% €125 21.0% €242 21.1% €273 26.3%

Kilkenny €73 10.3% €104 19.7% €145 14.5% €281 14.6% €317 19.6%

Wexford €66 13.5% €93 23.3% €131 17.9% €253 18.0% €286 23.1%

Waterford Co €74 16.6% €94 16.6% €138 14.4% €261 11.7% €295 14.0%

Kerry €63 11.4% €81 11.3% €119 9.2% €225 6.6% €254 8.9%

Cork Co €76 16.3% €97 16.2% €142 14.0% €268 11.3% €304 13.6%

Clare €61 13.6% €78 13.6% €115 11.4% €216 8.8% €244 11.0%

Limerick Co €59 17.2% €75 17.2% €110 15.0% €208 12.3% €235 14.6%

Tipperary €59 13.9% €76 13.8% €111 11.7% €209 9.0% €237 11.3%

Galway Co €55 5.8% €75 19.8% €109 17.4% €204 7.0% €245 15.6%

Mayo €50 4.1% €68 17.9% €99 15.5% €184 5.3% €221 13.7%

Roscommon €41 4.8% €56 18.6% €81 16.2% €152 5.9% €182 14.4%

Sligo €49 9.6% €67 24.1% €97 21.5% €182 10.8% €218 19.7%

Leitrim €42 1.9% €57 15.3% €83 13.0% €155 3.0% €185 11.2%

Donegal €47 1.9% €64 15.3% €93 13.0% €174 3.0% €208 11.2%

Cavan €47 4.8% €64 18.6% €93 16.2% €175 5.9% €209 14.4%

Monaghan €54 6.0% €73 20.0% €106 17.6% €199 7.2% €238 15.8%

DU

BLIN

DublinStrong price gains continue into second quarter

One year ago Previous quarter Current quarter

Proportion of properties marked as sale agreed and withdrawn, 2012-2017.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Within 6 months

Within 4 months

Within 2 months

How fast are properties in Dublin selling?

11 | The Daft.ie House Price Report – 2017 Q2

North CityAverage price: €323,550Qtr-on-qtr change: 4.4%Year-on-year change: 13.0%Change from trough: 64.1%

City CentreAverage price: €299,635Qtr-on-qtr change: 6.1%Year-on-year change: 18.2%Change from trough: 78.7%

South CityAverage price: €387,266Qtr-on-qtr change: 3.6%Year-on-year change: 11.7%Change from trough: 59.2%

North CountyAverage price: €302,457Qtr-on-qtr change: 3.3%

Year-on-year change: 12.7%Change from trough: 48.4%

West CountyAverage price: €297,070Qtr-on-qtr change: 3.2%

Year-on-year change: 9.7%Change from trough: 59.9%

South CountyAverage price: €563,442Qtr-on-qtr change: 2.8%

Year-on-year change: 8.8%Change from trough: 62.8%

Dublin City Centre North Dublin City South Dublin City North County Dublin South County Dublin West County Dublin

€650,000

€600,000

€550,000

€500,000

€450,000

€400,000

€350,000

€300,000

€250,000

€200,000

€150,000

Average rental price by area, 2006-2017.

€700,000

Q12006

Q12007

Q12008

Q12009

Q12010

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q22017

€750,000

How have house prices changed?

The Daft.ie House Price Report – 2017 Q2 | 12

Half sell within 2 months50% percent of Dublin properties find a buyer within

two months - up from 41% a year ago.

Transaction volumes reach new highThere were 3,550 transactions in Dublin between

January and March, the highest first-quarter total since

the start of the Price Register in 2010.

Stock on market down year-on-yearThere were 3,250 properties for sale in Dublin in June,

higher than three months previously (2,700) but lower

than a year ago (3,800).

Double-digit rises in most of cityTwenty of Dublin’s 25 markets saw prices increase by

at least 10% in the year to June - the highest number

since early 2015.

LeinsterSharp increase in prices in second quarter

One year ago Previous quarter Current quarter

Proportion of properties marked as sale agreed and withdrawn, 2012-2017.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Within 6 months

Within 4 months

Within 2 months

How fast are properties in Leinster selling?

13 | The Daft.ie House Price Report – 2017 Q2

LouthAverage price: €210,088Qtr-on-qtr change: 7.1%Year-on-year change: 16.9%Change from trough: 64.7%

MeathAverage price: €249,903Qtr-on-qtr change: 5.0%Year-on-year change: 12.5%Change from trough: 66.4%

KildareAverage price: €253,685Qtr-on-qtr change: 5.3%Year-on-year change: 12.1%Change from trough: 61.7%

WicklowAverage price: €314,840Qtr-on-qtr change: 6.6%Year-on-year change: 11.2%Change from trough: 54.9%

WexfordAverage price: €197,539Qtr-on-qtr change: 5.7%Year-on-year change: 15.2%Change from trough: 58.1%

LongfordAverage price: €128,816

Qtr-on-qtr change: 10.2%Year-on-year change: 23.5%Change from trough: 52.9%

WestmeathAverage price: €184,024Qtr-on-qtr change: 6.1%

Year-on-year change: 15.7%Change from trough: 55.8%

OffalyAverage price: €170,566Qtr-on-qtr change: 5.2%

Year-on-year change: 13.2%Change from trough: 41.2%

LaoisAverage price: €164,307Qtr-on-qtr change: 4.4%

Year-on-year change: 11.8%Change from trough: 58.4%

KilkennyAverage price: €210,176Qtr-on-qtr change: 4.3%

Year-on-year change: 12.0%Change from trough: 58.8%

CarlowAverage price: €176,510Qtr-on-qtr change: 7.1%

Year-on-year change: 18.0%From trough: 50.8%

Dublin Commuter Counties West Leinster South-East Leinster

€400,000

€350,000

€300,000

€250,000

€200,000

€150,000

€100,000

€50,000

Average house price by area, 2006-2017.

Q12006

Q12007

Q12008

Q12009

Q12010

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q22017

How have house prices changed?

The Daft.ie House Price Report – 2017 Q2 | 14

Two thirds sell within 4 months64% percent of Leinster properties find a buyer

within four months - up from 58% a year ago.

Transaction volumes reach new highThere were 2,800 transactions in Leinster (excluding

Dublin) between January and March, the highest

first-quarter total since the start of the Price Register

in 2010.

Double-digit rises across the provinceSharp increases in prices between March and June

across Leinster mean that prices are between 11%

(Wicklow) and 24% (Longford) higher than a year ago.

Stock on market down year-on-yearThere were almost 5,500 properties for sale in

Leinster in June, higher than three months previously

(5,000) but lower than a year ago (5,900).

MunsterMunster prices, outside cities, rise sharply in second quarter

One year ago Previous quarter Current quarter

Proportion of properties marked as sale agreed and withdrawn, 2012-2017.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Within 6 months

Within 4 months

Within 2 months

How fast are properties in Munster selling?

15 | The Daft.ie House Price Report – 2017 Q2

TipperaryAverage prices: €162,956Qtr-on-qtr change: 5.6%Year-on-year change: 9.1%Change from trough: 28.1%

Limerick CityAverage prices: €177,199Qtr-on-qtr change: 1.7%Year-on-year change: 15.1%Change from trough: 49.2%

Waterford CountyAverage prices: €204,729Qtr-on-qtr change: 5.7%Year-on-year change: 11.9%Change from trough: 42.4%

Waterford CityAverage prices: €158,861Qtr-on-qtr change: 3.5%Year-on-year change: 14.5%Change from trough: 51.6%

ClareAverage prices: €165,498Qtr-on-qtr change: 4.8%

Year-on-year change: 9.5%Change from trough: 38.4%

Limerick CountyAverage prices: €170,866Qtr-on-qtr change: 7.0%

Year-on-year change: 12.0%Change from trough: 29.9%

KerryAverage prices: €179,683Qtr-on-qtr change: 5.3%

Year-on-year change: 6.4%Change from trough: 27.9%

Cork CountyAverage prices: €206,686Qtr-on-qtr change: 5.4%

Year-on-year change: 11.4%Change from trough: 44.3%

Cork CityAverage prices: €256,201Qtr-on-qtr change: -0.3%

Year-on-year change: 9.2%Change from trough: 56.0%

Dublin Commuter Counties West Leinster South-East Leinster

€400,000

€350,000

€300,000

€250,000

€200,000

€150,000

€100,000

€50,000

Average house price by area, 2006-2017.

Q12006

Q12007

Q12008

Q12009

Q12010

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q22017

How have house prices changed?

The Daft.ie House Price Report – 2017 Q2 | 16

Over half sell in 4 monthsOver half (54%) of all properties in Munster find a

buyer within four months, up slightly from a year ago

(50%).

Transaction volumes steadyThere were 2,600 transactions in Munster in the first

quarter of 2017, similar to the total for the same three

months in both 2015 and 2016.

Urban-rural trend reversesUnlike in previous quarters, where Munster’s three

cities saw the strongest quarterly prices increases,

between March and June, it was the rural parts of the

province that saw the biggest increases.

Limited supply persistsThere were 7,650 properties on the market in

Munster in June, up roughly 500 from three months

previously - but a thousand fewer than a year

previously.

Connacht/UlsterPrice increases cool in the region

One year ago Previous quarter Current quarter

Proportion of properties marked as sale agreed and withdrawn, 2012-2017.

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Within 6 months

Within 4 months

Within 2 months

How fast are properties in Connacht/Ulster selling?

17 | The Daft.ie House Price Report – 2017 Q2

LeitrimAverage price: €123,884Qtr-on-qtr change: 2.3%Year-on-year change: 4.5%Change from trough: 44.2%

MonaghanAverage price: €160,559Qtr-on-qtr change: 3.5%Year-on-year change: 10.5%Change from trough: 40.7%

CavanAverage price: €149,132Qtr-on-qtr change: 4.6%Year-on-year change: 8.3%Change from trough: 45.2%

RoscommonAverage price: €129,668Qtr-on-qtr change: 1.2%Year-on-year change: 6.7%Change from trough: 41.5%

DonegalAverage price: €145,217Qtr-on-qtr change: 2.0%

Year-on-year change: 5.0%Change from trough: 27.8%

SligoAverage price: €133,887Qtr-on-qtr change: 5.8%

Year-on-year change: 13.8%Change from trough: 27.4%

MayoAverage price: €145,618Qtr-on-qtr change: 3.3%

Year-on-year change: 7.0%Change from trough: 30.9%

Galway CityAverage price: €268,535Qtr-on-qtr change: 1.2%

Year-on-year change: 13.4%Change from trough: 67.2%

Galway CountyAverage price: €182,310Qtr-on-qtr change: 4.5%

Year-on-year change: 8.5%Change from trough: 44.1%

Average house price by area, 2006-2017.

How have house prices changed?

Galway City Connacht Ulster

€50,000

€100,000

€150,000

€200,000

€250,000

€300,000

€350,000

€400,000

Q12006

Q12007

Q12008

Q12009

Q12010

Q12011

Q12012

Q12013

Q12014

Q12015

Q12016

Q22017

The Daft.ie House Price Report – 2017 Q2 | 18

Fewer than half sell in 4 monthsJust under half (48%) of all properties in Connacht-

Ulster find a buyer within four months, down

somewhat from a year ago (54%).

Recovery in transaction volumesThere were almost 1,750 transactions in Connacht-

Ulster in the first quarter of 2017, up from 1,670 in

the same period in 2016 - but still below the figure

for 2015 (1,900).

Limited supply persistsThere were just over 6,000 properties on the market

in Connacht-Ulster in June, up from 5,700 three

months previously - but well below the level a year

ago (6,900).

Return to single digit increasesIn late 2016, Connacht-Ulster had the fastest house

price growth in the country (12%, compared to 5%

in Dublin) - it now has the slowest (8%, and 12% in

Dublin).

Over the last number of years, Daft.ie has collected a vast amount of data on the Irish property market. Each year tens of thousands of properties for sale or rent are advertised on the site.

About the ReportThe goal of the Daft Report is to use this information to help all actors in the property market make informed decisions about buying and selling. In addition, because it is freely available, the Daft Report can help inform the media, the general public and policymakers about the latest developments in the property market.

This is the Daft.ie House Price Report, the partner to the Daft.ie Rental Report, which will be issuednext month. Together, they give house-hunters and investors more information to help them make their decisions. These twin reports mean that Daft is the only objective monitor of trends in both rental and sales markets on a quarterly basis, making the report an essential barometer for anyone with an interest in the Irish property market.

The Daft Report was first launched in 2005. It has already become the definitive barometer of the Irish rental market and is being used by the Central Bank, mortgage institutions, financial analysts and the general public alike. The Daft.ie House Price report is Ireland’s longest-running house price report, combining information from the Daft.ie archives with data from Ireland’s Residential Property Price Register.

Methodology and Sample SizeThe statistics are based on properties advertised on Daft.ie for a given period. The regressions used are hedonic price regressions, accounting for all available and measurable attributes of properties, with a Cooks Distance filter for outliers.

The average monthly sample size for sale properties is 5,000. Indices are based on standard methods, holding the mix of characteristics constant.

About Daft.ieDaft.ie is Ireland’s largest propertywebsite with over 2.5 million unique visitors generating over 228 million page impressions each month.

DisclaimerThe Daft.ie Report is prepared from information that we believe is collated with care, but we do not make any statement as to its accuracy or completeness. We reserve the right to vary our methodology and to edit or discontinue the indices, snapshots or analysis at any time for regulatory or other reasons. Persons seeking to place reliance on any information contained in this report for their own or third party commercial purposes do so at their own risk.

CreditsEconomic Analysis: Ronan LyonsMarketing and Communications: Martin ClancyLayout and Design: William Tector & Dara Gannon

19 | The Daft.ie House Price Report – 2017 Q2

Steal the Spotlight!The ultimate way to promote the launch of new builds

Stand out from the crowdwith unrivalled placement on Daft.ie’s homepage

Stay top of mindProminent agent brandingis guaranteed

Maximise interestin your property, drive more enquiries and instructions

Why you should build your brand on Daft.ie

• 85% of the property audience in Ireland are on Daft.ie

• 40% of people visiting Daft.ie would like to buy a property in the next 12 months

• 32% of people visiting Daft.ie already own a property

Source: Comscore and Sentiment Survey H2 2016.

For more information contact your account manager on: 01 421 8700

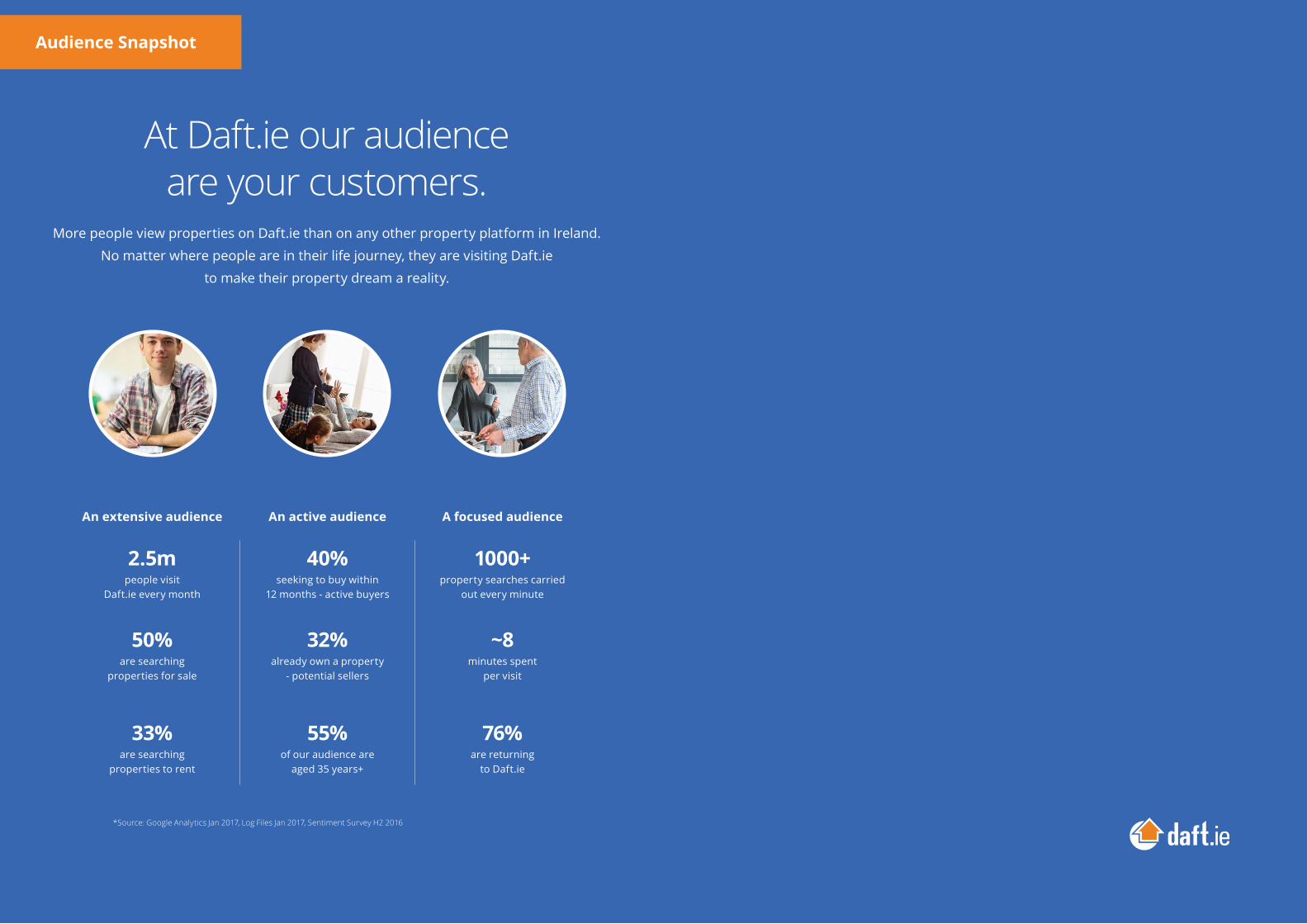

At Daft.ie our audienceare your customers.

More people view properties on Daft.ie than on any other property platform in Ireland.

No matter where people are in their life journey, they are visiting Daft.ie

to make their property dream a reality.

*Source: Google Analytics Jan 2017, Log Files Jan 2017, Sentiment Survey H2 2016

An extensive audience An active audience A focused audience

2.5mpeople visit

Daft.ie every month

40%seeking to buy within

12 months - active buyers

1000+property searches carried

out every minute

50%are searching

properties for sale

32%already own a property

- potential sellers

~8minutes spent

per visit

33%are searching

properties to rent

55%of our audience are

aged 35 years+

76%are returning

to Daft.ie

Audience Snapshot

Coming next:

The Daft.ie Rental Report ,2017 Q2.

The Daft.ie Rental Report will be published in August and will include a review of the performanceof Ireland’s rental market, plus all the usual indices, snapshots,trends and rental yield analysis, providing analysts, tenants, landlords, studentsand the public with the most up-to-date information on Ireland’s rental market.

All data is Copyright © Daft Media Limited. The information contained in this report may onlybe reproduced if the source is clearly credited. Please contact Daft.ie on 01-4218700 for further information.