Telecommunications - RHB TradeSmart

17

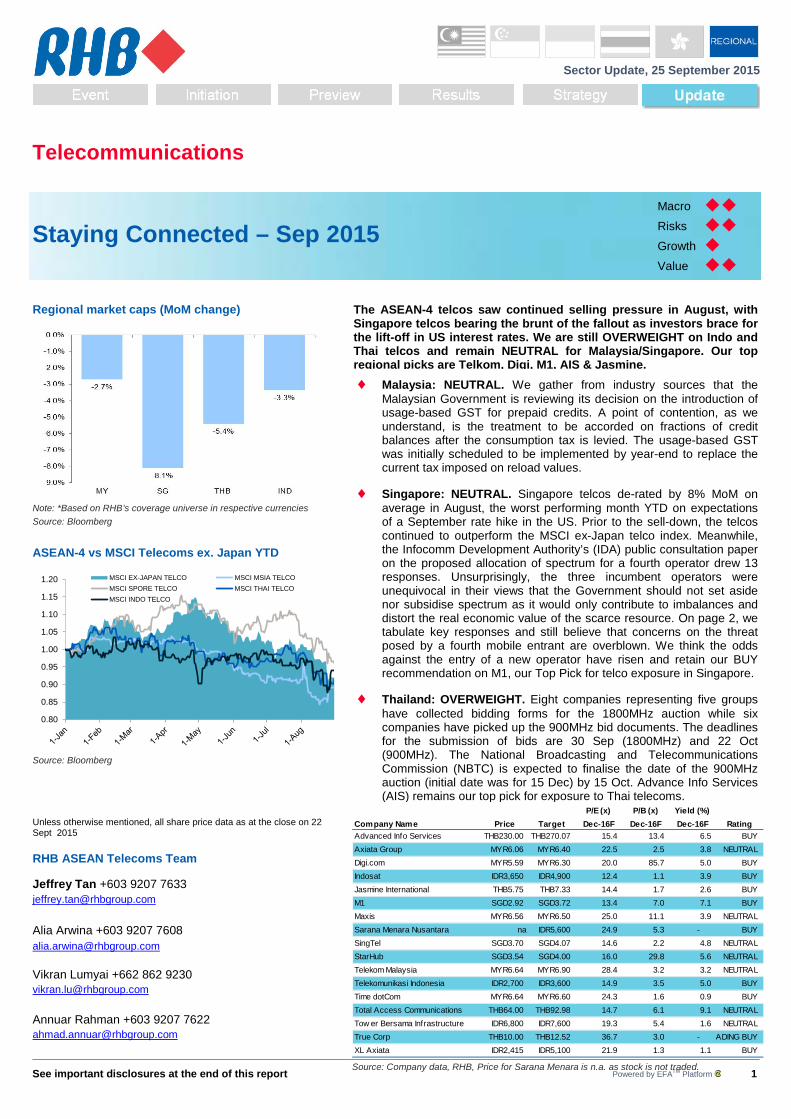

See important disclosures at the end of this report Powered by EFA TM Platform 1 Sector Update, 25 September 2015 Telecommunications Staying Connected – Sep 2015 Macro Risks Growth Value Regional market caps (MoM change) Note: *Based on RHB’s coverage universe in respective currencies Source: Bloomberg ASEAN-4 vs MSCI Telecoms ex. Japan YTD 0.80 0.85 0.90 0.95 1.00 1.05 1.10 1.15 1.20 MSCI EX-JAPAN TELCO MSCI MSIA TELCO MSCI SPORE TELCO MSCI THAI TELCO MSCI INDO TELCO Source: Bloomberg Unless otherwise mentioned, all share price data as at the close on 22 Sept 2015 RHB ASEAN Telecoms Team Jeffrey Tan +603 9207 7633 [email protected] Alia Arwina +603 9207 7608 [email protected] Vikran Lumyai +662 862 9230 [email protected] Annuar Rahman +603 9207 7622 [email protected] The ASEAN-4 telcos saw continued selling pressure in August, with Singapore telcos bearing the brunt of the fallout as investors brace for the lift-off in US interest rates. We are still OVERWEIGHT on Indo and Thai telcos and remain NEUTRAL for Malaysia/Singapore. Our top regional picks are Telkom, Digi, M1, AIS & Jasmine. ♦ Malaysia: NEUTRAL. We gather from industry sources that the Malaysian Government is reviewing its decision on the introduction of usage-based GST for prepaid credits. A point of contention, as we understand, is the treatment to be accorded on fractions of credit balances after the consumption tax is levied. The usage-based GST was initially scheduled to be implemented by year-end to replace the current tax imposed on reload values. ♦ Singapore: NEUTRAL. Singapore telcos de-rated by 8% MoM on average in August, the worst performing month YTD on expectations of a September rate hike in the US. Prior to the sell-down, the telcos continued to outperform the MSCI ex-Japan telco index. Meanwhile, the Infocomm Development Authority’s (IDA) public consultation paper on the proposed allocation of spectrum for a fourth operator drew 13 responses. Unsurprisingly, the three incumbent operators were unequivocal in their views that the Government should not set aside nor subsidise spectrum as it would only contribute to imbalances and distort the real economic value of the scarce resource. On page 2, we tabulate key responses and still believe that concerns on the threat posed by a fourth mobile entrant are overblown. We think the odds against the entry of a new operator have risen and retain our BUY recommendation on M1, our Top Pick for telco exposure in Singapore. ♦ Thailand: OVERWEIGHT. Eight companies representing five groups have collected bidding forms for the 1800MHz auction while six companies have picked up the 900MHz bid documents. The deadlines for the submission of bids are 30 Sep (1800MHz) and 22 Oct (900MHz). The National Broadcasting and Telecommunications Commission (NBTC) is expected to finalise the date of the 900MHz auction (initial date was for 15 Dec) by 15 Oct. Advance Info Services (AIS) remains our top pick for exposure to Thai telecoms. P/E (x) P/B (x) Yield (%) Dec-16F Dec-16F Dec-16F Advanced Info Services THB230.00 THB270.07 15.4 13.4 6.5 BUY Axiata Group MYR6.06 MYR6.40 22.5 2.5 3.8 NEUTRAL Digi.com MYR5.59 MYR6.30 20.0 85.7 5.0 BUY Indosat IDR3,650 IDR4,900 12.4 1.1 3.9 BUY Jasmine International THB5.75 THB7.33 14.4 1.7 2.6 BUY M1 SGD2.92 SGD3.72 13.4 7.0 7.1 BUY Maxis MYR6.56 MYR6.50 25.0 11.1 3.9 NEUTRAL Sarana Menara Nusantara na IDR5,600 24.9 5.3 - BUY SingTel SGD3.70 SGD4.07 14.6 2.2 4.8 NEUTRAL StarHub SGD3.54 SGD4.00 16.0 29.8 5.6 NEUTRAL Telekom Malaysia MYR6.64 MYR6.90 28.4 3.2 3.2 NEUTRAL Telekomunikasi Indonesia IDR2,700 IDR3,600 14.9 3.5 5.0 BUY Time dotCom MYR6.64 MYR6.60 24.3 1.6 0.9 BUY Total Access Communications THB64.00 THB92.98 14.7 6.1 9.1 NEUTRAL Tow er Bersama Infrastructure IDR6,800 IDR7,600 19.3 5.4 1.6 NEUTRAL True Corp THB10.00 THB12.52 36.7 3.0 - ADING BUY XL Axiata IDR2,415 IDR5,100 21.9 1.3 1.1 BUY Company Name Price Target Rating Source: Company data, RHB, Price for Sarana Menara is n.a. as stock is not traded.

Transcript of Telecommunications - RHB TradeSmart

See important disclosures at the end of this report Powered by EFATM Platform 1

Sector Update, 25 September 2015

Telecommunications

Staying Connected – Sep 2015 Macro

Risks

Growth

Value

Regional market caps (MoM change)

Note: *Based on RHB’s coverage universe in respective currencies Source: Bloomberg

ASEAN-4 vs MSCI Telecoms ex. Japan YTD

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20 MSCI EX-JAPAN TELCO MSCI MSIA TELCOMSCI SPORE TELCO MSCI THAI TELCOMSCI INDO TELCO

Source: Bloomberg

Unless otherwise mentioned, all share price data as at the close on 22 Sept 2015 RHB ASEAN Telecoms Team Jeffrey Tan +603 9207 7633 [email protected] Alia Arwina +603 9207 7608 [email protected] Vikran Lumyai +662 862 9230 [email protected] Annuar Rahman +603 9207 7622 [email protected]

The ASEAN-4 telcos saw continued selling pressure in August, with Singapore telcos bearing the brunt of the fallout as investors brace for the lift-off in US interest rates. We are still OVERWEIGHT on Indo and Thai telcos and remain NEUTRAL for Malaysia/Singapore. Our top regional picks are Telkom, Digi, M1, AIS & Jasmine. ♦ Malaysia: NEUTRAL. We gather from industry sources that the

Malaysian Government is reviewing its decision on the introduction of usage-based GST for prepaid credits. A point of contention, as we understand, is the treatment to be accorded on fractions of credit balances after the consumption tax is levied. The usage-based GST was initially scheduled to be implemented by year-end to replace the current tax imposed on reload values.

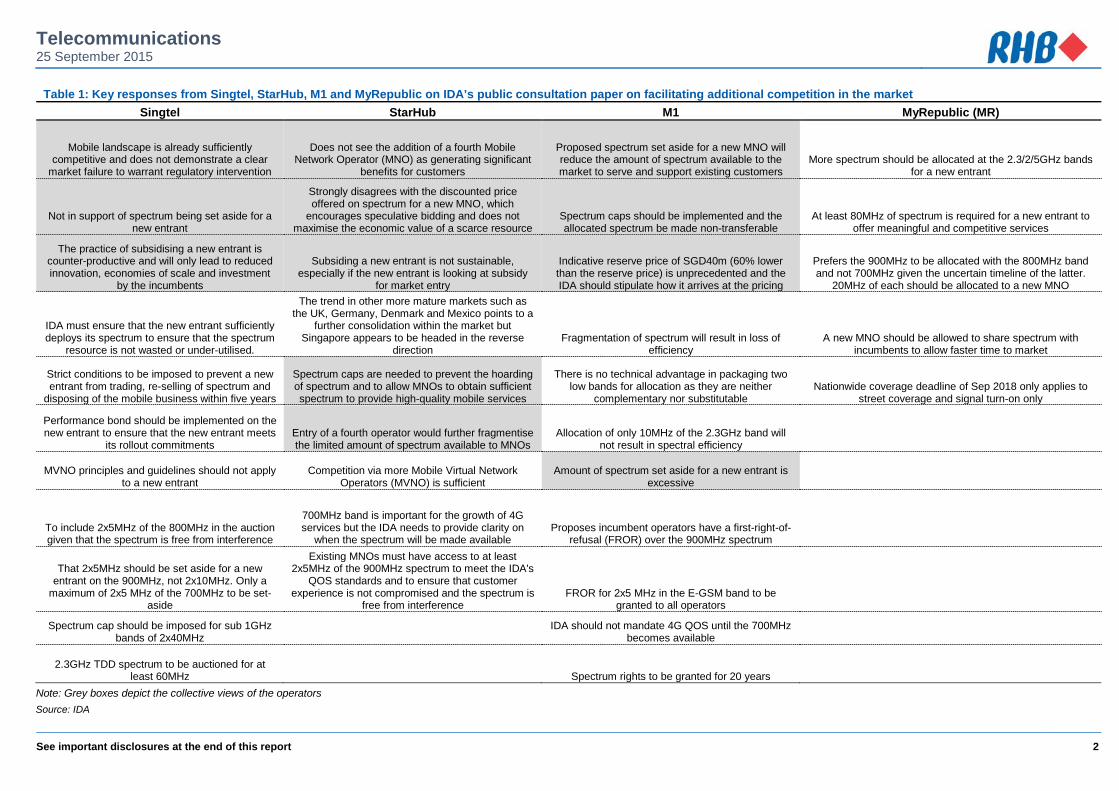

♦ Singapore: NEUTRAL. Singapore telcos de-rated by 8% MoM on average in August, the worst performing month YTD on expectations of a September rate hike in the US. Prior to the sell-down, the telcos continued to outperform the MSCI ex-Japan telco index. Meanwhile, the Infocomm Development Authority’s (IDA) public consultation paper on the proposed allocation of spectrum for a fourth operator drew 13 responses. Unsurprisingly, the three incumbent operators were unequivocal in their views that the Government should not set aside nor subsidise spectrum as it would only contribute to imbalances and distort the real economic value of the scarce resource. On page 2, we tabulate key responses and still believe that concerns on the threat posed by a fourth mobile entrant are overblown. We think the odds against the entry of a new operator have risen and retain our BUY recommendation on M1, our Top Pick for telco exposure in Singapore.

♦ Thailand: OVERWEIGHT. Eight companies representing five groups have collected bidding forms for the 1800MHz auction while six companies have picked up the 900MHz bid documents. The deadlines for the submission of bids are 30 Sep (1800MHz) and 22 Oct (900MHz). The National Broadcasting and Telecommunications Commission (NBTC) is expected to finalise the date of the 900MHz auction (initial date was for 15 Dec) by 15 Oct. Advance Info Services (AIS) remains our top pick for exposure to Thai telecoms.

P/E (x) P/B (x) Yield (%)Dec-16F Dec-16F Dec-16F

Advanced Info Services THB230.00 THB270.07 15.4 13.4 6.5 BUYAxiata Group MYR6.06 MYR6.40 22.5 2.5 3.8 NEUTRALDigi.com MYR5.59 MYR6.30 20.0 85.7 5.0 BUYIndosat IDR3,650 IDR4,900 12.4 1.1 3.9 BUYJasmine International THB5.75 THB7.33 14.4 1.7 2.6 BUYM1 SGD2.92 SGD3.72 13.4 7.0 7.1 BUYMaxis MYR6.56 MYR6.50 25.0 11.1 3.9 NEUTRALSarana Menara Nusantara na IDR5,600 24.9 5.3 - BUYSingTel SGD3.70 SGD4.07 14.6 2.2 4.8 NEUTRALStarHub SGD3.54 SGD4.00 16.0 29.8 5.6 NEUTRALTelekom Malaysia MYR6.64 MYR6.90 28.4 3.2 3.2 NEUTRALTelekomunikasi Indonesia IDR2,700 IDR3,600 14.9 3.5 5.0 BUYTime dotCom MYR6.64 MYR6.60 24.3 1.6 0.9 BUYTotal Access Communications THB64.00 THB92.98 14.7 6.1 9.1 NEUTRALTow er Bersama Infrastructure IDR6,800 IDR7,600 19.3 5.4 1.6 NEUTRALTrue Corp THB10.00 THB12.52 36.7 3.0 - ADING BUYXL Axiata IDR2,415 IDR5,100 21.9 1.3 1.1 BUY

Company Name Price Target Rating

Source: Company data, RHB, Price for Sarana Menara is n.a. as stock is not traded.

Telecommunications 25 September 2015

See important disclosures at the end of this report 2

Table 1: Key responses from Singtel, StarHub, M1 and MyRepublic on IDA’s public consultation paper on facilitating additional competition in the market Singtel StarHub M1 MyRepublic (MR)

Mobile landscape is already sufficiently competitive and does not demonstrate a clear

market failure to warrant regulatory intervention

Does not see the addition of a fourth Mobile Network Operator (MNO) as generating significant

benefits for customers

Proposed spectrum set aside for a new MNO will reduce the amount of spectrum available to the market to serve and support existing customers

More spectrum should be allocated at the 2.3/2/5GHz bands for a new entrant

Not in support of spectrum being set aside for a new entrant

Strongly disagrees with the discounted price offered on spectrum for a new MNO, which

encourages speculative bidding and does not maximise the economic value of a scarce resource

Spectrum caps should be implemented and the allocated spectrum be made non-transferable

At least 80MHz of spectrum is required for a new entrant to offer meaningful and competitive services

The practice of subsidising a new entrant is counter-productive and will only lead to reduced innovation, economies of scale and investment

by the incumbents

Subsiding a new entrant is not sustainable, especially if the new entrant is looking at subsidy

for market entry

Indicative reserve price of SGD40m (60% lower than the reserve price) is unprecedented and the IDA should stipulate how it arrives at the pricing

Prefers the 900MHz to be allocated with the 800MHz band and not 700MHz given the uncertain timeline of the latter.

20MHz of each should be allocated to a new MNO

IDA must ensure that the new entrant sufficiently deploys its spectrum to ensure that the spectrum

resource is not wasted or under-utilised.

The trend in other more mature markets such as the UK, Germany, Denmark and Mexico points to a

further consolidation within the market but Singapore appears to be headed in the reverse

direction Fragmentation of spectrum will result in loss of

efficiency A new MNO should be allowed to share spectrum with

incumbents to allow faster time to market

Strict conditions to be imposed to prevent a new entrant from trading, re-selling of spectrum and

disposing of the mobile business within five years

Spectrum caps are needed to prevent the hoarding of spectrum and to allow MNOs to obtain sufficient spectrum to provide high-quality mobile services

There is no technical advantage in packaging two low bands for allocation as they are neither

complementary nor substitutable Nationwide coverage deadline of Sep 2018 only applies to

street coverage and signal turn-on only

Performance bond should be implemented on the new entrant to ensure that the new entrant meets

its rollout commitments Entry of a fourth operator would further fragmentise the limited amount of spectrum available to MNOs

Allocation of only 10MHz of the 2.3GHz band will not result in spectral efficiency

MVNO principles and guidelines should not apply to a new entrant

Competition via more Mobile Virtual Network Operators (MVNO) is sufficient

Amount of spectrum set aside for a new entrant is excessive

To include 2x5MHz of the 800MHz in the auction given that the spectrum is free from interference

700MHz band is important for the growth of 4G services but the IDA needs to provide clarity on

when the spectrum will be made available Proposes incumbent operators have a first-right-of-

refusal (FROR) over the 900MHz spectrum

That 2x5MHz should be set aside for a new entrant on the 900MHz, not 2x10MHz. Only a

maximum of 2x5 MHz of the 700MHz to be set-aside

Existing MNOs must have access to at least 2x5MHz of the 900MHz spectrum to meet the IDA's

QOS standards and to ensure that customer experience is not compromised and the spectrum is

free from interference FROR for 2x5 MHz in the E-GSM band to be

granted to all operators

Spectrum cap should be imposed for sub 1GHz bands of 2x40MHz

IDA should not mandate 4G QOS until the 700MHz becomes available

2.3GHz TDD spectrum to be auctioned for at least 60MHz Spectrum rights to be granted for 20 years

Note: Grey boxes depict the collective views of the operators Source: IDA

Telecommunications 25 September 2015

See important disclosures at the end of this report 3

Malaysia (NEUTRAL) Alia Arwina +603 9207 7608 [email protected]

Jeffrey Tan +603 9207 7633 [email protected]

♦ Robi Axiata could be looking to merge with Airtel Bangladesh

Axiata (AXIATA MK, NEUTRAL, TP: MYR6.40) announced that it has entered into an exclusive discussion with India’s Bharti Airtel Ltd (BHARTI IN, NR) to explore the possibility of combining the business operations of their respective telco subsidiaries in Bangladesh – Robi Axiata Limited (98%-owned by Axiata) and Airtel Bangladesh Ltd. The discussions are still preliminary, with both parties indicating that there is no certainty that it would lead to the execution of a binding definitive agreement (Bursa Malaysia, 10 Sep)

Comment: Kindly refer to our report dated 10 Sept - Axiata Group: Robi To Merge With Airtel?

♦ U-Mobile launches 7GB postpaid plan U-Mobile, Malaysia’s fourth mobile player, has introduced its new Hero Postpaid P70 plan, which is bundled with 7GB of data for MYR70/month. This is one of the most attractively priced data bundled postpaid plans in the market and compares with the likes of Celcom’s First One Plan which offers 3GB of data for MYR48/month while Maxis’ One Plan offers 2GB of data for MYR98/month. (Company website, 1 Sep)

Comment: U-Mobile’s latest tactical campaign in dishing out excessive data to tempt users could well compromise network resources and looks to be untenable if the industry is vying to improve the economics of data. We note the competitive response by the bigger operators has been “selective”, with a certain level of pricing discipline instituted although it could take some time before the level of aggression normalises with a short to mid-term impact on industry revenue and EBITDA.

Singapore (NEUTRAL) Jeffrey Tan +603 9207 7633 [email protected]

♦ M1 introduces 10Gbps fibre broadband service

M1 (M1 SP, BUY, TP: SGD3.72) has announced the launch of its new “XGPON” fibre-optic broadband service, which supports downlink transmission speeds of up to 10Gbps. Offered over the city state’s next-generation national broadband network (Next Gen NBN), the new service is initially being made available to corporate customers only, but will be extended to residential users by year-end. The new service is priced at SGD1,088 (USD771) per month for a 2Gbps subscription, rising to SGD2,888 for a 10Gbps service (Telegeography, 3 Sep)

♦ Strong opposition to IDA’s public consultation on introducing further competition

The IDA has received 13 responses to its earlier Public Consultation on the Proposed Framework for the Allocation of Spectrum for International Mobile Telecommunications (“IMT”) And IMT-Advanced Services and for the Enhancement of Competition in the Mobile Market at the closing date for submission on 26 Aug (IDA, 26 Aug)

Comment: We tabulated the key views from the incumbent operators and MyRepublic (MR) (the leading contender for the fourth mobile license) on Page 2 of this report. Not surprisingly, IDA’s proposals on additional competition were met with heavy “criticism” from the incumbents. Most were of the view that the 60MHz spectrum to be set aside for a new operator at a 60% discount to the reserve price will only contribute to the inefficient use of a scarce resource and potentially hinder competition and further innovation. MR has called on the IDA to increase the amount of spectrum to be set aside and allow for spectrum sharing. Meanwhile, Singtel has cautioned the IDA against adopting an overly optimistic view of potential changes to the mobile landscape with the entry of a fourth operator. It also provided numerous examples of markets where spectrum that were set aside had led to negative implications on the industry.

Telecommunications 25 September 2015

See important disclosures at the end of this report 4

Indonesia (OVERWEIGHT) Jeffrey Tan +603 9207 7633 [email protected]

♦ XL Axiata aims to sign up 10% of its

subscriber base on LTE by year-end. XL Axiata (XL) (EXCL IJ, BUY, TP: IDR5,100) is aiming to sign up between 8m-10m 4G LTE mobile internet users by the end of 2016, up from the 1.2m subscribers it has today, out of a total base of over 46m. XL is currently working on a phased deployment of 4G LTE in the 1800MHz band, noting that in October it aims to add Surabaya and Denpasar to its footprint, while November will see the addition of coverage in Jakarta and Bandung. Indeed, to foster the expansion, XL is looking to raise up to IDR1.5trn (USD104.90m) by issuing Islamic bonds (or sukuk) this year, pending approval from the Financial Services Authority and the Indonesia Stock Exchange. The cellco is seeking to convert its USD-denominated liabilities to rupiah (IDR) and to extend the payment period – to account for the weakening rupiah and the rising burden that this is causing. It may also sell off some tower assets to trim debt levels arising from the acquisition of Axis Telekom Indonesia last year. (Telegeography, 15 Sep) Comment: XL recently repaid USD100m of its USD1.55bn debt in its books as part of its debt rationalisation exercise. The amount forms part of the USD400m or 38% of unhedged external debt.

♦ MNC Group targets to connect 10m homes with fibre

MNC Kabel Mediacom (MKM), a unit of Media Nusantara Citra (MNC Media), which is itself part of MNC Group, the largest and the only integrated media, broadcasting, entertainment and telecoms group in Indonesia, is looking to invest in its ongoing service expansion in the country with a view to signing up 50,000 fibre broadband users by end-2015. Ultimately, MKM is looking to build out a fibre optic network passing 10m homes and has allocated USD400m over three years and a total USD2bn-3bn over ten years to realise this. (Telegeography, 9 Sep)

Thailand (OVERWEIGHT) Vikran Lumyai +662 862 9230 [email protected]

Jeffrey Tan +603 9207 7633 [email protected]

♦ TOT may seek compensation from AIS over concession amendments

After the Telephone Organisation of Thailand (TOT) granted the concession to Advanced Info Services (AIS) (ADVANC TB, BUY, TP: THB270.07) in 1990, it amended the concession seven times, making changes such as extending the concession period to 25 years from 20 years and reducing the amount of prepaid revenue sharing. The most significant amendment came in 2001 when TOT changed revenue-sharing payments for prepaid services to a flat rate of 20% of service revenue, compared with original payments of 15% in 1991-1995, 20% in 1996-2000, 25% in 2001-2005 and 30% in 2006-2015. At present, the Cabinet has approved for the ICT Ministry to urge TOT to seek the compensation of THB60bn from AIS. (The Nation, 15 Sep)

Comment: Based on our estimates, the compensation amount is higher, at THB70bn, which includes an accumulated future loss of THB56bn and an outright loss of THB14bn. We believe the developments could be protracted as it involves all three operators. TOT also amended the concession contracts with Total Access Communication (DTAC) (DTAC TB, NEUTRAL, TP: THB92.98) and True Corp (TRUE TB, TRADING BUY, TP: THB12.52).In the worst case scenario that AIS needs to fork out the full compensation, it would translate to THB23.50/share. The issue has no bearing on the upcoming spectrum auction.

♦ CAT pulls out from 4G bid CAT Telecom (CAT) decided to pull out of the 4G spectrum auction in November as the state agency is not ready to compete in a bidding war after negotiations with foreign telecoms, NTT Docomo of Japan (9437 JP, NR) and SK Telecom (017670 KS, NR) of South Korea, failed. Furthermore, the requirement to declare its budget for the auction is a deterrent for CAT. Currently, CAT has the right to use the 1800MHz spectrum until 2025 despite its concession with DTAC expiring in 2018. (Bangkok Post, 1 Sep)

Comment: A total of eight bidding documents were collected from the regulator. This comprised one from AIS, two from DTAC, three from TRUE and one each from Hutchison Telecom (Thailand) and Jasmine International. Hutchison Telecom, a former CDMA operator, was acquired by True Corp in 2011.

Telecommunications 25 September 2015

See important disclosures at the end of this report 5

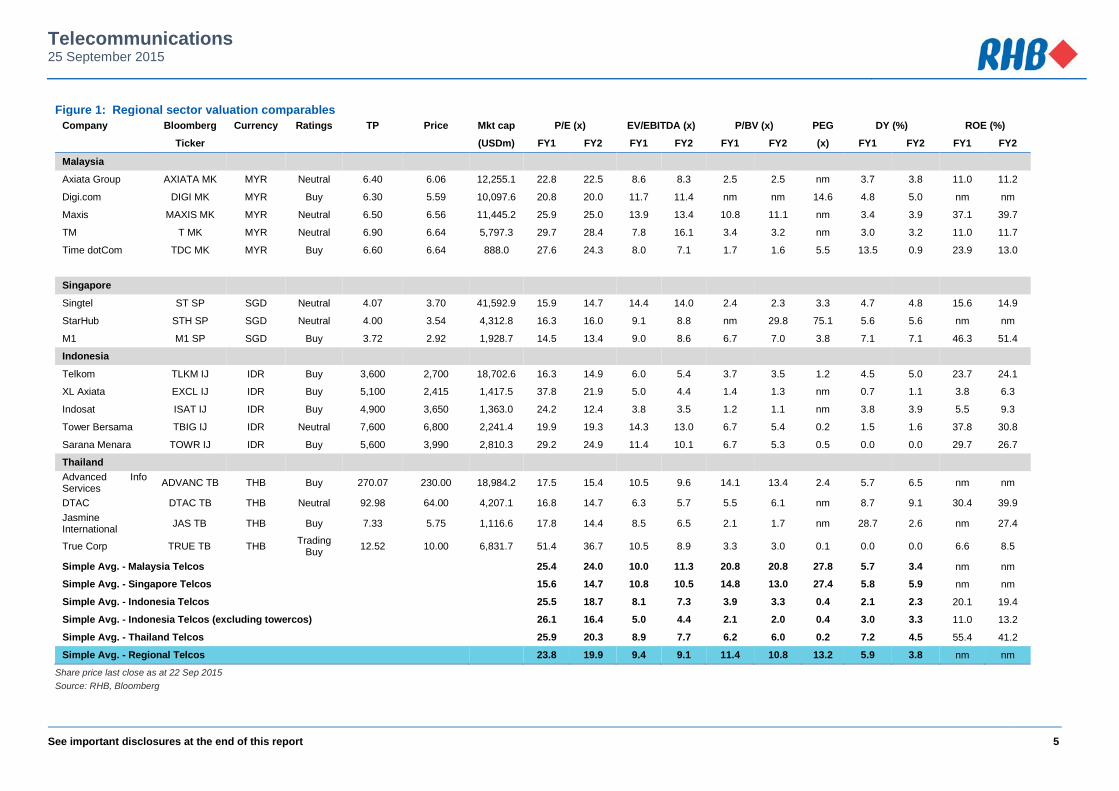

Figure 1: Regional sector valuation comparables Company Bloomberg Currency Ratings TP Price Mkt cap P/E (x) EV/EBITDA (x) P/BV (x) PEG DY (%) ROE (%)

Ticker (USDm) FY1 FY2 FY1 FY2 FY1 FY2 (x) FY1 FY2 FY1 FY2

Malaysia

Axiata Group AXIATA MK MYR Neutral 6.40 6.06 12,255.1 22.8 22.5 8.6 8.3 2.5 2.5 nm 3.7 3.8 11.0 11.2

Digi.com DIGI MK MYR Buy 6.30 5.59 10,097.6 20.8 20.0 11.7 11.4 nm nm 14.6 4.8 5.0 nm nm

Maxis MAXIS MK MYR Neutral 6.50 6.56 11,445.2 25.9 25.0 13.9 13.4 10.8 11.1 nm 3.4 3.9 37.1 39.7

TM T MK MYR Neutral 6.90 6.64 5,797.3 29.7 28.4 7.8 16.1 3.4 3.2 nm 3.0 3.2 11.0 11.7

Time dotCom TDC MK MYR Buy 6.60 6.64 888.0 27.6 24.3 8.0 7.1 1.7 1.6 5.5 13.5 0.9 23.9 13.0

Singapore

Singtel ST SP SGD Neutral 4.07 3.70 41,592.9 15.9 14.7 14.4 14.0 2.4 2.3 3.3 4.7 4.8 15.6 14.9

StarHub STH SP SGD Neutral 4.00 3.54 4,312.8 16.3 16.0 9.1 8.8 nm 29.8 75.1 5.6 5.6 nm nm

M1 M1 SP SGD Buy 3.72 2.92 1,928.7 14.5 13.4 9.0 8.6 6.7 7.0 3.8 7.1 7.1 46.3 51.4

Indonesia

Telkom TLKM IJ IDR Buy 3,600 2,700 18,702.6 16.3 14.9 6.0 5.4 3.7 3.5 1.2 4.5 5.0 23.7 24.1

XL Axiata EXCL IJ IDR Buy 5,100 2,415 1,417.5 37.8 21.9 5.0 4.4 1.4 1.3 nm 0.7 1.1 3.8 6.3

Indosat ISAT IJ IDR Buy 4,900 3,650 1,363.0 24.2 12.4 3.8 3.5 1.2 1.1 nm 3.8 3.9 5.5 9.3

Tower Bersama TBIG IJ IDR Neutral 7,600 6,800 2,241.4 19.9 19.3 14.3 13.0 6.7 5.4 0.2 1.5 1.6 37.8 30.8

Sarana Menara TOWR IJ IDR Buy 5,600 3,990 2,810.3 29.2 24.9 11.4 10.1 6.7 5.3 0.5 0.0 0.0 29.7 26.7

Thailand Advanced Info Services ADVANC TB THB Buy 270.07 230.00 18,984.2 17.5 15.4 10.5 9.6 14.1 13.4 2.4 5.7 6.5 nm nm

DTAC DTAC TB THB Neutral 92.98 64.00 4,207.1 16.8 14.7 6.3 5.7 5.5 6.1 nm 8.7 9.1 30.4 39.9 Jasmine International JAS TB THB Buy 7.33 5.75 1,116.6 17.8 14.4 8.5 6.5 2.1 1.7 nm 28.7 2.6 nm 27.4

True Corp TRUE TB THB Trading Buy 12.52 10.00 6,831.7 51.4 36.7 10.5 8.9 3.3 3.0 0.1 0.0 0.0 6.6 8.5

Simple Avg. - Malaysia Telcos 25.4 24.0 10.0 11.3 20.8 20.8 27.8 5.7 3.4 nm nm

Simple Avg. - Singapore Telcos 15.6 14.7 10.8 10.5 14.8 13.0 27.4 5.8 5.9 nm nm

Simple Avg. - Indonesia Telcos 25.5 18.7 8.1 7.3 3.9 3.3 0.4 2.1 2.3 20.1 19.4

Simple Avg. - Indonesia Telcos (excluding towercos) 26.1 16.4 5.0 4.4 2.1 2.0 0.4 3.0 3.3 11.0 13.2

Simple Avg. - Thailand Telcos 25.9 20.3 8.9 7.7 6.2 6.0 0.2 7.2 4.5 55.4 41.2

Simple Avg. - Regional Telcos 23.8 19.9 9.4 9.1 11.4 10.8 13.2 5.9 3.8 nm nm

Share price last close as at 22 Sep 2015 Source: RHB, Bloomberg

Telecommunications 25 September 2015

See important disclosures at the end of this report 6

Figure 2: MSCI Malaysia telecom index (YTD) Figure 3: MSCI Singapore telecom index (YTD)

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

MSCI MSIA TELCO MSCI EX-JAPAN TELCO FBMKLCI

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20MSCI SPORE TELCO MSCI EX-JAPAN TELCO Straits Times Index

Source: Bloomberg Source: Bloomberg

Figure 4: MSCI Indonesia telecom index (YTD) Figure 5: MSCI Thailand telecom index (YTD)

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

MSCI INDO TELCO MSCI EX-JAPAN TELCO Jakarta Composite Index

0.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20MSCI THAI TELCO MSCI EX-JAPAN TELCO

Stock Exchange of Thailand Index

Source: Bloomberg Source: Bloomberg

Telecommunications 25 September 2015

See important disclosures at the end of this report 7

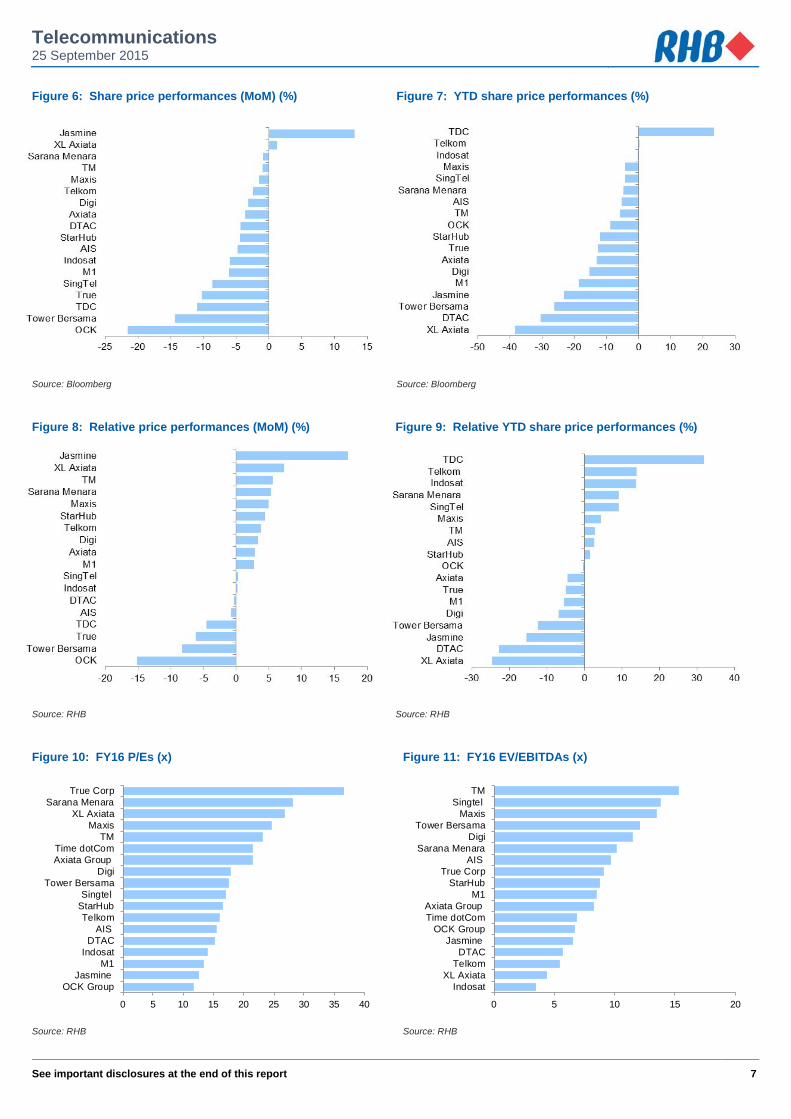

Figure 6: Share price performances (MoM) (%) Figure 7: YTD share price performances (%)

Source: Bloomberg Source: Bloomberg

Figure 8: Relative price performances (MoM) (%) Figure 9: Relative YTD share price performances (%)

Source: RHB Source: RHB

Figure 10: FY16 P/Es (x) Figure 11: FY16 EV/EBITDAs (x)

0 5 10 15 20 25 30 35 40

OCK GroupJasmine

M1Indosat

DTACAIS

TelkomStarHubSingtel

Tower BersamaDigi

Axiata GroupTime dotCom

TMMaxis

XL AxiataSarana Menara

True Corp

0 5 10 15 20

IndosatXL Axiata

TelkomDTAC

JasmineOCK Group

Time dotComAxiata Group

M1StarHub

True CorpAIS

Sarana MenaraDigi

Tower BersamaMaxis

SingtelTM

Source: RHB Source: RHB

Telecommunications 25 September 2015

See important disclosures at the end of this report 8

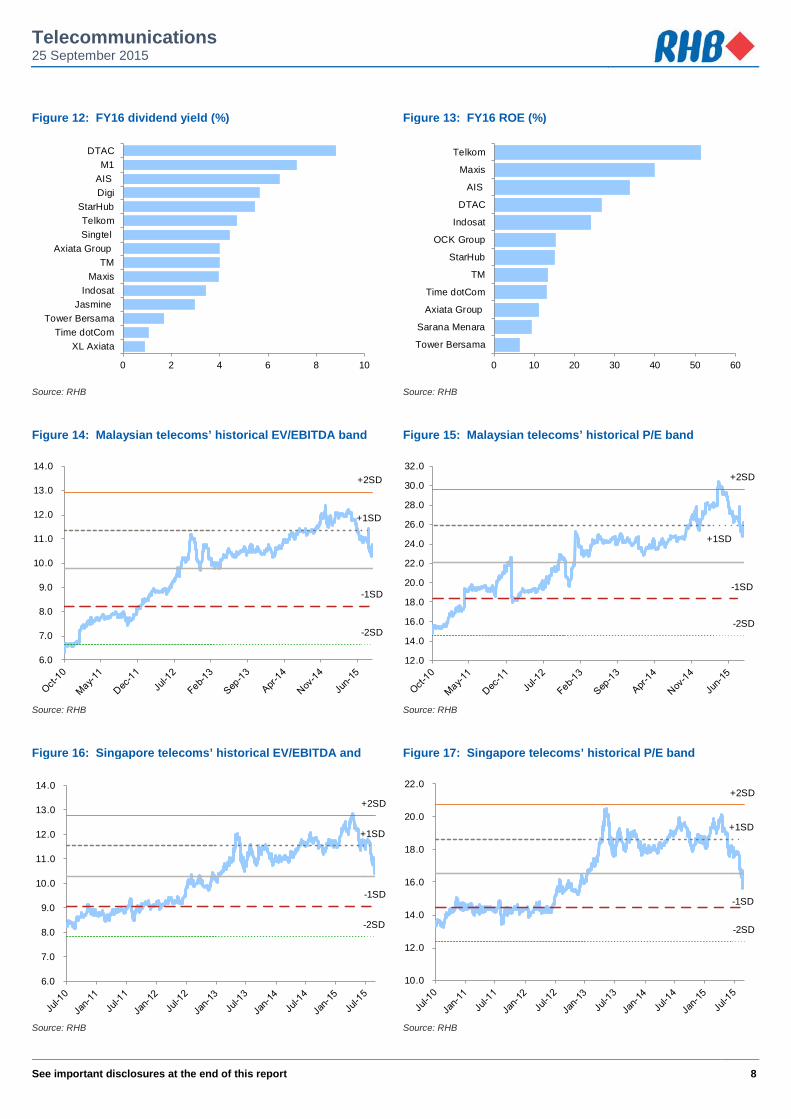

Figure 12: FY16 dividend yield (%) Figure 13: FY16 ROE (%)

0 2 4 6 8 10

XL AxiataTime dotCom

Tower BersamaJasmine

IndosatMaxis

TMAxiata Group

SingtelTelkom

StarHubDigiAISM1

DTAC

0 10 20 30 40 50 60

Tower Bersama

Sarana Menara

Axiata Group

Time dotCom

TM

StarHub

OCK Group

Indosat

DTAC

AIS

Maxis

Telkom

Source: RHB Source: RHB

Figure 14: Malaysian telecoms’ historical EV/EBITDA band Figure 15: Malaysian telecoms’ historical P/E band

+1SD

-1SD

+2SD

-2SD

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

+1SD

-1SD

+2SD

-2SD

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

30.0

32.0

Source: RHB Source: RHB

Figure 16: Singapore telecoms’ historical EV/EBITDA and Figure 17: Singapore telecoms’ historical P/E band

+2SD

+1SD

-1SD

-2SD

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

14.0

-2SD

-1SD

+1SD

+2SD

10.0

12.0

14.0

16.0

18.0

20.0

22.0

Source: RHB Source: RHB

Telecommunications 25 September 2015

See important disclosures at the end of this report 9

Figure 18: Indonesian telecoms’ historical EV/EBITDA band Figure 19: Indonesian telecoms’ historical P/E band

+2SD

+1SD

-1SD

-2SD

4.0

4.5

5.0

5.5

6.0

6.5

7.0

+2SD

+1SD

-1SD

-2SD

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

Source: RHB Source: RHB

Figure 20: Thai telecoms’ historical EV/EBITDA band Figure 21: Thai telecoms’ historical P/E band

-2SD

-1SD

+1SD

+2SD

2.0

4.0

6.0

8.0

10.0

12.0

14.0

+1SD

+2SD

-1SD

-2SD

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

28.0

Source: RHB Source: RHB

Telecommunications 25 September 2015

See important disclosures at the end of this report 10

Links To Recent Published Reports on the Sector Tower Bersama Infrastructure : Missing Estimates (1 Sep 2015) Sarana Menara Nusantara : Rebound In Tenancies (31 Aug 2015) Indosat : Striking Back (31 Aug 2015) Telekom Malaysia : Dialing a Strong 2Q15 (26 Aug 2015) Telecommunications : Staying Connected – Aug 2015 (25 Aug 2015) Time dotCom : A Silver Data Lining (25 Aug 2015) Time dotCom : Growing Steadily (24 Aug 2015) Axiata Group : Wading Through Rough Waters (21 Aug 2015) XL Axiata : Transforming Well (17 Aug 2015) Singtel : 1QFY16 Results Call Highlights (14 Aug 2015) SingTel : Currency Woes (13 Aug 2015) Telekomunikasi Indonesia : 2Q15 Results Call Takeaways (5 Aug 2015) Advanced Info Services : 2H Guidance Moderated (4 Aug 2015) Telekomunikasi Indonesia : Another Good Lift (3 Aug 2015) Jasmine International : 2Q15 Earnings Climbed 10% QoQ (29 Jul 2015) Time dotCom : Riding On The New Wave Of Data (28 Jul 2015) Total Access Communications : 49% YoY Earnings Drop (21 Jul 2015) M1 : A Weaker 1H15 Call (21 Jul 2015) Maxis : GST Boost To Margins (16 Jul 2015) Digi.com : Getting Inspired (14 Jul 2015) OCK Group : Making The Next (Big) Leap (9 Jul 2015) SG Telecommunications Sector: One Up For The Republic (8 Jul 2015) Total Access Communications : Another Missed Call? (26 Jun 2015) Telecommunications : Staying Connected – June 2015 (23 Jun 2015) Maxis : Issuing More Notes (18 Jun 2015) Digi.com : Time To Revisit The Yellow Man (16 Jun 2015) Telecommunications: The ASEAN-4 1Q15 Earnings Wrap (9 Jun 2015) Telekomunikasi Indonesia : Calling On Guam (2 Jun 2015) Telekom Malaysia : Waiting For More Data Packets (1 Jun 2015) Time dotCom : Toning Down Expectations (29 May 2015) OCK Group : Building Up Resources (28 May 2015) Time dotCom : Hitting The Right Note (28 May 2015) Indosat : A Stronger 2H In The Offing (27 May 2015) Tower Bersama Infrastructure : One-Offs Crimp 1Q15 Numbers (26 May 2015) Sarana Menara Nusantara : Holding On To Its Tenancies (25 May 2015) Telecommunications : Staying Connected – May 2015 (22 May 2015) Axiata Group : Errant Signals Over The Short Term (21 May 2015) Axiata Group : Slow Momentum Of Recovery (20 May 2015) StarHub : Falling Short on EBITDA (18 May 2015) Singtel : Catalysts Priced In (15 May 2015) SingTel : Higher Capex In Store for FY16 (14 May 2015) Telekomunikasi Indonesia : Not Distracted By Towerco Noises (8 May 2015) XL Axiata : From Volume To Value (7 May 2015) Jasmine International : Network Rental Cost a Burden (30 Apr 2015) Telecommunications : Status Quo For Now (30 Apr 2015) Telekomunikasi Indonesia : Mitratel Deal Gets The Boot? (29 Apr 2015) Advanced Info Services : Growing 2% YoY From Stronger Handset Sales (27 Apr 2015) Total Access Communications : Boosting Capex For 2015 (27 Apr 2015) Telecommunications : Staying Connected – Apr 2015 (22 Apr 2015) Jasmine International : A Tough Call on 4G (17 Apr 2015) Telekom Malaysia : Heeding The Clarion Call On Broadband (17 Apr 2015) M1 : A Softer Tone On Postpaid (14 Apr 2015) Time dotCom : Partial Disposal Of Digi Shares (13 Apr 2015) Telecommunications : The ASEAN-4 Earnings Wrap (10 Apr 2015) Axiata Group : Short-Term Pain But Long-Term Gain (10 Apr 2015) SingTel : Gaining Trust (9 Apr 2015) Telecommunications : Gearing Up For The 4G Auctions (8 Apr 2015) Telecommunications : The Key Answers To The Thai Telco Sector (8 Apr 2015) Telecommunications : Getting All Riled Up By The GST (3 Apr 2015) Indosat : Back Into the Game (31 Mar 2015)

11

RHB Guide to Investment Ratings Buy: Share price may exceed 10% over the next 12 months Trading Buy: Share price may exceed 15% over the next 3 months, however longer-term outlook remains uncertain Neutral: Share price may fall within the range of +/- 10% over the next 12 months Take Profit: Target price has been attained. Look to accumulate at lower levels Sell: Share price may fall by more than 10% over the next 12 months Not Rated: Stock is not within regular research coverage Investment Research Disclaimers RHB has issued this report for information purposes only. This report is intended for circulation amongst RHB and its affiliates’ clients generally or such persons as may be deemed eligible by RHB to receive this report and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. This report is not intended, and should not under any circumstances be construed as, an offer or a solicitation of an offer to buy or sell the securities referred to herein or any related financial instruments. This report may further consist of, whether in whole or in part, summaries, research, compilations, extracts or analysis that has been prepared by RHB’s strategic, joint venture and/or business partners. No representation or warranty (express or implied) is given as to the accuracy or completeness of such information and accordingly investors should make their own informed decisions before relying on the same. This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to the applicable laws or regulations. By accepting this report, the recipient hereof (i) represents and warrants that it is lawfully able to receive this document under the laws and regulations of the jurisdiction in which it is located or other applicable laws and (ii) acknowledges and agrees to be bound by the limitations contained herein. Any failure to comply with these limitations may constitute a violation of applicable laws. All the information contained herein is based upon publicly available information and has been obtained from sources that RHB believes to be reliable and correct at the time of issue of this report. However, such sources have not been independently verified by RHB and/or its affiliates and this report does not purport to contain all information that a prospective investor may require. The opinions expressed herein are RHB’s present opinions only and are subject to change without prior notice. RHB is not under any obligation to update or keep current the information and opinions expressed herein or to provide the recipient with access to any additional information. Consequently, RHB does not guarantee, represent or warrant, expressly or impliedly, as to the adequacy, accuracy, reliability, fairness or completeness of the information and opinion contained in this report. Neither RHB (including its officers, directors, associates, connected parties, and/or employees) nor does any of its agents accept any liability for any direct, indirect or consequential losses, loss of profits and/or damages that may arise from the use or reliance of this research report and/or further communications given in relation to this report. Any such responsibility or liability is hereby expressly disclaimed. Whilst every effort is made to ensure that statement of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable and must not be construed as a representation that the matters referred to therein will occur. Different assumptions by RHB or any other source may yield substantially different results and recommendations contained on one type of research product may differ from recommendations contained in other types of research. The performance of currencies may affect the value of, or income from, the securities or any other financial instruments referenced in this report. Holders of depositary receipts backed by the securities discussed in this report assume currency risk. Past performance is not a guide to future performance. Income from investments may fluctuate. The price or value of the investments to which this report relates, either directly or indirectly, may fall or rise against the interest of investors. This report does not purport to be comprehensive or to contain all the information that a prospective investor may need in order to make an investment decision. The recipient of this report is making its own independent assessment and decisions regarding any securities or financial instruments referenced herein. Any investment discussed or recommended in this report may be unsuitable for an investor depending on the investor’s specific investment objectives and financial position. The material in this report is general information intended for recipients who understand the risks of investing in financial instruments. This report does not take into account whether an investment or course of action and any associated risks are suitable for the recipient. Any recommendations contained in this report must therefore not be relied upon as investment advice based on the recipient's personal circumstances. Investors should make their own independent evaluation of the information contained herein, consider their own investment objective, financial situation and particular needs and seek their own financial, business, legal, tax and other advice regarding the appropriateness of investing in any securities or the investment strategies discussed or recommended in this report. This report may contain forward-looking statements which are often but not always identified by the use of words such as “believe”, “estimate”, “intend” and “expect” and statements that an event or result “may”, “will” or “might” occur or be achieved and other similar expressions. Such forward-looking statements are based on assumptions made and information currently available to RHB and are subject to known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievement to be materially different from any future results, performance or achievement, expressed or implied by such forward-looking statements. Caution should be taken with respect to such statements and recipients of this report should not place undue reliance on any such forward-looking statements. RHB expressly disclaims any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or circumstances after the date of this publication or to reflect the occurrence of unanticipated events.

12

The use of any website to access this report electronically is done at the recipient’s own risk, and it is the recipient’s sole responsibility to take precautions to ensure that it is free from viruses or other items of a destructive nature. This report may also provide the addresses of, or contain hyperlinks to, websites. RHB takes no responsibility for the content contained therein. Such addresses or hyperlinks (including addresses or hyperlinks to RHB own website material) are provided solely for the recipient’s convenience. The information and the content of the linked site do not in any way form part of this report. Accessing such website or following such link through the report or RHB website shall be at the recipient’s own risk. This report may contain information obtained from third parties. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. Third party content providers give no express or implied warranties, including, but not limited to, any warranties of merchantability or fitness for a particular purpose or use. Third party content providers shall not be liable for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including lost income or profits and opportunity costs) in connection with any use of their content. The research analysts responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. The research analysts that authored this report are precluded by RHB in all circumstances from trading in the securities or other financial instruments referenced in the report, or from having an interest in the company(ies) that they cover. RHB and/or its affiliates and/or their directors, officers, associates, connected parties and/or employees, may have, or have had, interests in the securities or qualified holdings, in subject company(ies) mentioned in this report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, RHB and/or its affiliates may have, or have had, business relationships with the subject company(ies) mentioned in this report and may from time to time seek to provide investment banking or other services to the subject company(ies) referred to in this research report. As a result, investors should be aware that a conflict of interest may exist. The contents of this report is strictly confidential and may not be copied, reproduced, published, distributed, transmitted or passed, in whole or in part, to any other person without the prior express written consent of RHB and/or its affiliates. This report has been delivered to RHB and its affiliates’ clients for information purposes only and upon the express understanding that such parties will use it only for the purposes set forth above. By electing to view or accepting a copy of this report, the recipients have agreed that they will not print, copy, videotape, record, hyperlink, download, or otherwise attempt to reproduce or re-transmit (in any form including hard copy or electronic distribution format) the contents of this report. RHB and/or its affiliates accepts no liability whatsoever for the actions of third parties in this respect. The contents of this report are subject to copyright. Please refer to Restrictions on Distribution below for information regarding the distributors of this report. Recipients must not reproduce or disseminate any content or findings of this report without the express permission of RHB and the distributors. The securities mentioned in this publication may not be eligible for sale in some states or countries or certain categories of investors. The recipient of this report should have regard to the laws of the recipient’s place of domicile when contemplating transactions in the securities or other financial instruments referred to herein. The securities discussed in this report may not have been registered in such jurisdiction. Without prejudice to the foregoing, the recipient is to note that additional disclaimers, warnings or qualifications may apply based on geographical location of the person or entity receiving this report. RESTRICTIONS ON DISTRIBUTION Malaysia This report is issued and distributed in Malaysia by RHB Research Institute Sdn Bhd. The views and opinions in this report are our own as of the date hereof and is subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Conduct Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. RHB Research Institute Sdn Bhd has no obligation to update its opinion or the information in this report. Thailand This report is issued and distributed in the Kingdom of Thailand by RHB OSK Securities (Thailand) PCL, a licensed securities company that is authorised by the Ministry of Finance, regulated by the Securities and Exchange Commission of Thailand and is a member of the Stock Exchange of Thailand. The Thai Institute of Directors Association has disclosed the Corporate Governance Report of Thai Listed Companies made pursuant to the policy of the Securities and Exchange Commission of Thailand. RHB OSK Securities (Thailand) PCL does not endorse, confirm nor certify the result of the Corporate Governance Report of Thai Listed Companies. Indonesia This report is issued and distributed in Indonesia by PT RHB OSK Securities Indonesia. This research does not constitute an offering document and it should not be construed as an offer of securities in Indonesia. Any securities offered or sold, directly or indirectly, in Indonesia or to any Indonesian citizen or corporation (wherever located) or to any Indonesian resident in a manner which constitutes a public offering under Indonesian laws and regulations must comply with the prevailing Indonesian laws and regulations.

13

Singapore This report is issued and distributed in Singapore by RHB Research Institute Singapore Pte Ltd and it may only be distributed in Singapore to accredited investors, expert investors and institutional investors as defined in the Financial Advisers Regulations and the Securities and Futures Act (Chapter 289), as amended from time to time. By virtue of distribution to these categories of investors, RHB Research Institute Singapore Pte Ltd and its representatives are not required to comply with Section 36 of the Financial Advisers Act (Chapter 110) (Section 36 relates to disclosure of RHB Research Institute Singapore Pte Ltd ’s interest and/or its representative's interest in securities). Recipients of this report in Singapore may contact RHB Research Institute Singapore Pte Ltd in respect of any matter arising from or in connection with the report. Hong Kong This report is issued and distributed in Hong Kong by RHB OSK Securities Hong Kong Limited (興業僑豐證券有限公司) (CE No.: ADU220) (“RHBSHK”) which is licensed in Hong Kong by the Securities and Futures Commission for Type 1 (dealing in securities) and Type 4 (advising on securities) regulated activities. Any investors wishing to purchase or otherwise deal in the securities covered in this report should contact RHB OSK Securities Hong Kong Limited. United States This report was prepared by RHB and is being distributed solely and directly to “major” U.S. institutional investors as defined under, and pursuant to, the requirements of Rule 15a-6 under the U.S. Securities and Exchange Act of 1934, as amended (the “Exchange Act”). RHB is not registered as a broker-dealer in the United States and does not offer brokerage services to U.S. persons. Any order for the purchase or sale of the securities discussed herein that are listed on Bursa Malaysia Securities Berhad must be placed with and through Auerbach Grayson (“AG”). Any order for the purchase or sale of all other securities discussed herein must be placed with and through such other registered U.S. broker-dealer as appointed by RHB from time to time as required by the Exchange Act Rule 15a-6. This report is confidential and not intended for distribution to, or use by, persons other than the recipient and its employees, agents and advisors, as applicable. Additionally, where research is distributed via Electronic Service Provider, the analysts whose names appear in this report are not registered or qualified as research analysts in the United States and are not associated persons of Auerbach Grayson AG or such other registered U.S. broker-dealer as appointed by RHB from time to time and therefore may not be subject to any applicable restrictions under Financial Industry Regulatory Authority (“FINRA”) rules on communications with a subject company, public appearances and personal trading. Investing in any non-U.S. securities or related financial instruments discussed in this research report may present certain risks. The securities of non-U.S. issuers may not be registered with, or be subject to the regulations of, the U.S. Securities and Exchange Commission. Information on non-U.S. securities or related financial instruments may be limited. Foreign companies may not be subject to audit and reporting standards and regulatory requirements comparable to those in the United States. The financial instruments discussed in this report may not be suitable for all investors. Transactions in foreign markets may be subject to regulations that differ from or offer less protection than those in the United States. OWNERSHIP AND MATERIAL CONFLICTS OF INTEREST Malaysia RHB does not have qualified shareholding (1% or more) in the subject company (ies) covered in this report except for: a) - RHB and/or its subsidiaries are not liquidity providers or market makers for the subject company (ies) covered in this report except for: a) - RHB and/or its subsidiaries have not participated as a syndicate member in share offerings and/or bond issues in securities covered in this report in the last 12 months except for: a) - RHB has not provided investment banking services to the company/companies covered in this report in the last 12 months except for: a) - Thailand RHB OSK Securities (Thailand) PCL and/or its directors, officers, associates, connected parties and/or employees, may have, or have had, interests and/or commitments in the securities in subject company(ies) mentioned in this report or any securities related thereto. Further, RHB OSK Securities (Thailand) PCL may have, or have had, business relationships with the subject company(ies) mentioned in this report. As a result, investors should exercise their own judgment carefully before making any investment decisions.

14

Indonesia PT RHB OSK Securities Indonesia is not affiliated with the subject company(ies) covered in this report both directly or indirectly as per the definitions of affiliation above. Pursuant to the Capital Market Law (Law Number 8 Year 1995) and the supporting regulations thereof, what constitutes as affiliated parties are as follows: 1. Familial relationship due to marriage or blood up to the second degree, both horizontally or vertically;

2. Affiliation between parties to the employees, Directors or Commissioners of the parties concerned;

3. Affiliation between 2 companies whereby one or more member of the Board of Directors or the Commissioners are the same;

4. Affiliation between the Company and the parties, both directly or indirectly, controlling or being controlled by the Company;

5. Affiliation between 2 companies which are controlled, directly or indirectly, by the same party; or

6. Affiliation between the Company and the main Shareholders.

PT RHB OSK Securities Indonesia is not an insider as defined in the Capital Market Law and the information contained in this report is not considered as insider information prohibited by law.

Insider means: a. a commissioner, director or employee of an Issuer or Public Company;

b. a substantial shareholder of an Issuer or Public Company;

c. an individual, who because of his position or profession, or because of a business relationship with an Issuer or Public Company, has access to inside information; and

d. an individual who within the last six months was a Person defined in letters a, b or c, above.

Singapore RHB Research Institute Singapore Pte Ltd and/or its subsidiaries and/or associated companies do not make a market in any securities covered in this report, except for: (a) - The staff of RHB Research Institute Singapore Pte Ltd and its subsidiaries and/or its associated companies do not serve on any board or trustee positions of any issuer whose securities are covered in this report, except for: (a) - RHB Research Institute Singapore Pte Ltd and/or its subsidiaries and/or its associated companies do not have and have not within the last 12 months had any corporate finance advisory relationship with the issuer of the securities covered in this report or any other relationship (including a shareholding of 1% or more in the securities covered in this report) that may create a potential conflict of interest, except for: (a) - Hong Kong RHBSHK or any of its group companies may have financial interests in in relation to an issuer or a new listing applicant (as the case may be) the securities in respect of which are reviewed in the report, and such interests aggregate to an amount equal to or more than (a) 1% of the subject company’s market capitalization (in the case of an issuer as defined under paragraph 16 of the Code of Conduct for Persons Licensed by or Registered with the Securities and Futures Commission (the “Code of Conduct”); and/or (b) an amount equal to or more than 1% of the subject company’s issued share capital, or issued units, as applicable (in the case of a new listing applicant as defined in the Code of Conduct). Further, the analysts named in this report or their associates may have financial interests in relation to an issuer or a new listing applicant (as the case may be) in the securities which are reviewed in the report. RHBSHK or any of its group companies may make a market in the securities covered by this report. RHBSHK or any of its group companies may have analysts or their associates, individual(s) employed by or associated with RHBSHK or any of its group companies serving as an officer of the company or any of the companies covered by this report. RHBSHK or any of its group companies may have received compensation or a mandate for investment banking services to the company or any of the companies covered by this report within the past 12 months. Note: The reference to “group companies” above refers to a group company of RHBSHK that carries on a business in Hong Kong in (a) investment banking; (b) proprietary trading or market making; or (c) agency broking, in relation to securities listed or traded on The Stock Exchange of Hong Kong Limited.

15

Kuala Lumpur Hong Kong Singapore

RHB Research Institute Sdn Bhd Level 11, Tower One, RHB Centre

Jalan Tun Razak Kuala Lumpur

Malaysia Tel : +(60) 3 9280 2185 Fax : +(60) 3 9284 8693

RHB OSK Securities Hong Kong Ltd.

12th Floor World-Wide House 19 Des Voeux Road Central, Hong Kong

Tel : +(852) 2525 1118 Fax : +(852) 2810 0908

RHB Research Institute Singapore

Pte Ltd (formerly known as DMG & Partners Research Pte Ltd)

10 Collyer Quay #09-08 Ocean Financial Centre

Singapore 049315 Tel : +(65) 6533 1818 Fax : +(65) 6532 6211

Jakarta Shanghai Phnom Penh

PT RHB OSK Securities Indonesia Wisma Mulia, 20th Floor

Jl. Jend. Gatot Subroto No. 42 Jakarta 12710, Indonesia Tel : +(6221) 2783 0888 Fax : +(6221) 2783 0777

RHB OSK (China) Investment Advisory Co. Ltd.

Suite 4005, CITIC Square 1168 Nanjing West Road

Shanghai 20041 China

Tel : +(8621) 6288 9611 Fax : +(8621) 6288 9633

RHB OSK Indochina Securities Limited

No. 1-3, Street 271 Sangkat Toeuk Thla, Khan Sen Sok

Phnom Penh Cambodia

Tel: +(855) 23 969 161 Fax: +(855) 23 969 171

Bangkok

RHB OSK Securities (Thailand) PCL

10th Floor, Sathorn Square Office Tower 98, North Sathorn Road, Silom

Bangrak, Bangkok 10500 Thailand

Tel: +(66) 2 862 9999 Fax : +(66) 2 862 9799

Thai Institute of Directors Association (IOD) – Corporate Governance Report Rating 2014

Excellent BAFS HANA KTB SAMART SIM BCP INTUCH MINT SAMTEL SPALI BTS IRPC PSL SAT TISCO CPN IVL PTT SC TMB EGCO KBANK PTTEP SCB TOP GRAMMY KKP PTTGC SE-ED

Very Good 2S BROOK DTAC HMPRO MACO OFM S&J SSSC THRE TSC ACAP BWG DTC HTC MAKRO OGC S&P STANLY TIC TSTH AF CENTEL ECL IFEC MBK OSIHI SABINA STEC TICON TTW AIT CFRESH EE INTUCH MBKET PAP SAMCO SUC TIW TUF AKR CGS EIC ITD MFC PDI SCCC SUSCO TK TVO AMATA CHOW ESSO IVL MFEC PE SCG SVI TLUXE UAC AP CIMBT FE JAS MINT PG SCSMG SYNTEC TMT UMI ASK CK FORTH KCE MODERN PHATRA*** SFP TASCO TNITY UP ASP CM GBX KGI MTI PJW SITHAI TCAP TNL UPOIC AYUD CPALL GC KSL NBC PM SMT TCP TOG UV BEC CPF GFPT L&E NCH PR SPALI TFD TPC VIBHA BFIT CSC GL LANNA NINE PRANDA SPCG TFI TRC VNT BH DCC GLOW LH NMG PRG SPI THANA TRT WACOAL BIGC DELTA GUNKUL LRH NSI PT SPPT THCOM TRU YUASA BJC DEMCO HANA LST OCC PYLON SSF THIP TRUE ZMICO *** PHATRA was voluntarily delisted from the Stock Exchange of Thailand effectively on September 25, 2012.

Good

AEONTS BGT CMO GENCO JTS LHBANK NC PTL SGP SWC TPAC UT AFC BLA CNS GFM JUBILE LHK NNCL Q-CON SIAM SYNEX TPCORP VARO AGE BNC CNT GLOBAL JUTHA LIVE NTV QLT SIMAT TBSP TPIPL WAVE AH BOL CPL GOLD KASET LOXLEY OSK QTC SINGER TCB TPP WG AHC BROCK CRANE HFT KBS MAJOR PAE RASA SIRI TEAM TR WIN AI BSBM CSP HTECH KC MATCH PATO RCL SKR TF TTCL WORK AJ BTNC CSR HYDRO KDH MATI PB RICH SMIT TGCI TWFP

ALUCON BUI CTW IFS KIAT MBAX PICO ROJNA SMK THANI TYCN AMANAH CCET DRACO IHL KKC M-CHAI PL RPC SOLAR TKS UBIS APCO CEN EASON ILINK KTC MDX POST SAM SPC TMD UEC APCS CHUO EMC INET KWC MJD PPM SCBLIF SPG TMI UIC APRINT CI EPCO IRC KWH MK PREB SCP SSC TNH UMS ARIP CIG FNS IRCP KYE MOONG PRECHA SEAFCO SST TNPC UOBKH AS CIMBI*** FOCUS IT LALIN MPIC PRIN SENA STA TOPP UPF ASIA CITY FSS JMART LEE MSC PSAAP SF SVOA TPA US *** CIMBI was voluntarily delisted from the Stock Exchange of Thailand effectively on September 25,

2012.

IOD (IOD Disclaimer)

การเปิดเผลผลการสํารวจของสมาคมสง่เสริมสถาบนักรรมการบริษัทไทย (IOD) ในเร่ืองการกํากบัดแูลกิจการ (Corporate Governance) นีเ้ป็นการ

ดําเนินการตามนโยบายของสํานกังานคณะกรรมการกํากบัหลกัทรัพย์และตลาดหลกัทรัพย์ โดยการสํารวจของ IOD เป็นการสํารวจและประเมินจากข้อมลูของบรษัทจด

ทะเบียนในตลาดหลกัทรัพย์แหง่ประเทศไทยและตลาดหลกัทรัพย์เอ็มเอไอ ที่มีการเปิดเผยตอ่สาธารณะและเป็นข้อมลูที่ผู้ลงทนุทัว่ไปสามารถเข้าถงึได้ ดงันัน้ผลสํารวจ

ดงักลา่วจงึเป็นการนําเสนอในมมุมองของบคุคลภายนอกโดยไมไ่ด้เป็นการประเมินการปฏิบตัิและมิได้มีการใช้ข้อมลูภายในในการประเมิน

อนึ่ง ผลการสาํรวจดงักลา่ว เป็นผลการสํารวจ ณ วนัที่ปรากฎในรายงานการกํากบัดแูละกิจการบริษัทจดทะเบียนไทยเทา่นัน้ ดงันัน้ผลการสํารวจจงึอาจ

เปลี่ยนแปลงได้ภายหลงัวนัดงักลา่ว ทัง้นีบ้ริษัทหลกัทรัพย์ อาร์เอสบี โอเอส เค จํากดั (มหาชน) มิได้ยืนยนัหรือรับรองถึงความถกูต้องของผลการสํารวจดงักลา่วแตอ่ยา่งใด

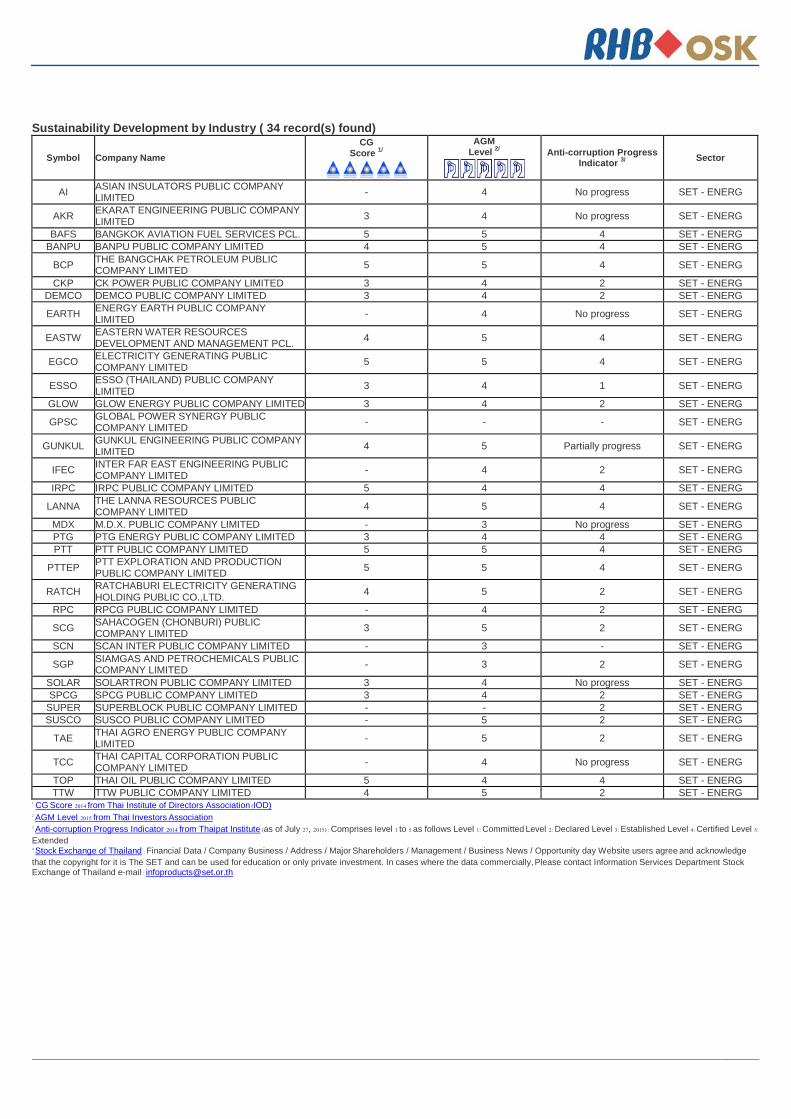

Sustainability Development by Industry ( 34 record(s) found)

Symbol Company Name CG

Score 1/

AGM Level 2/

Anti-corruption Progress Indicator 3/ Sector

AI ASIAN INSULATORS PUBLIC COMPANY LIMITED - 4 No progress SET - ENERG

AKR EKARAT ENGINEERING PUBLIC COMPANY LIMITED 3 4 No progress SET - ENERG

BAFS BANGKOK AVIATION FUEL SERVICES PCL. 5 5 4 SET - ENERG BANPU BANPU PUBLIC COMPANY LIMITED 4 5 4 SET - ENERG

BCP THE BANGCHAK PETROLEUM PUBLIC COMPANY LIMITED 5 5 4 SET - ENERG

CKP CK POWER PUBLIC COMPANY LIMITED 3 4 2 SET - ENERG DEMCO DEMCO PUBLIC COMPANY LIMITED 3 4 2 SET - ENERG

EARTH ENERGY EARTH PUBLIC COMPANY LIMITED - 4 No progress SET - ENERG

EASTW EASTERN WATER RESOURCES DEVELOPMENT AND MANAGEMENT PCL. 4 5 4 SET - ENERG

EGCO ELECTRICITY GENERATING PUBLIC COMPANY LIMITED 5 5 4 SET - ENERG

ESSO ESSO (THAILAND) PUBLIC COMPANY LIMITED 3 4 1 SET - ENERG

GLOW GLOW ENERGY PUBLIC COMPANY LIMITED 3 4 2 SET - ENERG

GPSC GLOBAL POWER SYNERGY PUBLIC COMPANY LIMITED - - - SET - ENERG

GUNKUL GUNKUL ENGINEERING PUBLIC COMPANY LIMITED 4 5 Partially progress SET - ENERG

IFEC INTER FAR EAST ENGINEERING PUBLIC COMPANY LIMITED - 4 2 SET - ENERG

IRPC IRPC PUBLIC COMPANY LIMITED 5 4 4 SET - ENERG

LANNA THE LANNA RESOURCES PUBLIC COMPANY LIMITED 4 5 4 SET - ENERG

MDX M.D.X. PUBLIC COMPANY LIMITED - 3 No progress SET - ENERG PTG PTG ENERGY PUBLIC COMPANY LIMITED 3 4 4 SET - ENERG PTT PTT PUBLIC COMPANY LIMITED 5 5 4 SET - ENERG

PTTEP PTT EXPLORATION AND PRODUCTION PUBLIC COMPANY LIMITED 5 5 4 SET - ENERG

RATCH RATCHABURI ELECTRICITY GENERATING HOLDING PUBLIC CO.,LTD. 4 5 2 SET - ENERG

RPC RPCG PUBLIC COMPANY LIMITED - 4 2 SET - ENERG

SCG SAHACOGEN (CHONBURI) PUBLIC COMPANY LIMITED 3 5 2 SET - ENERG

SCN SCAN INTER PUBLIC COMPANY LIMITED - 3 - SET - ENERG

SGP SIAMGAS AND PETROCHEMICALS PUBLIC COMPANY LIMITED - 3 2 SET - ENERG

SOLAR SOLARTRON PUBLIC COMPANY LIMITED 3 4 No progress SET - ENERG SPCG SPCG PUBLIC COMPANY LIMITED 3 4 2 SET - ENERG

SUPER SUPERBLOCK PUBLIC COMPANY LIMITED - - 2 SET - ENERG SUSCO SUSCO PUBLIC COMPANY LIMITED - 5 2 SET - ENERG

TAE THAI AGRO ENERGY PUBLIC COMPANY LIMITED - 5 2 SET - ENERG

TCC THAI CAPITAL CORPORATION PUBLIC COMPANY LIMITED - 4 No progress SET - ENERG

TOP THAI OIL PUBLIC COMPANY LIMITED 5 4 4 SET - ENERG TTW TTW PUBLIC COMPANY LIMITED 4 5 2 SET - ENERG

1 CG Score 2014 from Thai Institute of Directors Association (IOD) 2 AGM Level 2015 from Thai Investors Association 3 Anti-corruption Progress Indicator 2014 from Thaipat Institute (as of July 27, 2015) : Comprises level 1 to 5 as follows Level 1: Committed Level 2: Declared Level 3: Established Level 4: Certified Level 5:

Extended 4 Stock Exchange of Thailand : Financial Data / Company Business / Address / Major Shareholders / Management / Business News / Opportunity day Website users agree and acknowledge that the copyright for it is The SET and can be used for education or only private investment. In cases where the data commercially, Please contact Information Services Department Stock Exchange of Thailand e-mail : [email protected]