SuperChoice Superannuation Plan Pension Plan · SuperChoice Superannuation Plan Pension Plan ......

80

SuperChoice Superannuation Plan Pension Plan Supplementary Product Disclosure Statement (SPDS) Date Issued 19 December 2008 This Supplementary Product Disclosure Statement supplements the SuperChoice Superannuation and Pension Plan Product Disclosure Statement (PDS) dated 30 October 2008 issued by St Andrew’s Superannuation Services Pty Ltd (“St Andrew’s”, “we”, “us” and “our”). Trustee: St Andrew’s Superannuation Services Pty Ltd Fund: St Andrew’s Superannuation Services Fund Administrator: St Andrew’s Life Insurance Pty Ltd To invest in SuperChoice Superannuation and Pension Plan you should obtain and read the relevant PDS and this SPDS before making an investment decision. This SPDS is to be read together with the PDS. Terms defined in the PDS have the same meaning in this SPDS. The purpose of this SPDS is to inform you of changes to the ultimate owner of SuperChoice which are to take place on or about 19 December 2008.

Transcript of SuperChoice Superannuation Plan Pension Plan · SuperChoice Superannuation Plan Pension Plan ......

SuperChoice Superannuation PlanPension Plan Supplementary Product Disclosure Statement (SPDS)Date Issued 19 December 2008

This Supplementary Product Disclosure Statement supplements the SuperChoice Superannuation and Pension Plan Product Disclosure Statement (PDS) dated 30 October 2008 issued by St Andrew’s Superannuation Services Pty Ltd (“St Andrew’s”, “we”, “us” and “our”).

Trustee: St Andrew’s Superannuation Services Pty Ltd Fund: St Andrew’s Superannuation Services Fund Administrator: St Andrew’s Life Insurance Pty Ltd

To invest in SuperChoice Superannuation and Pension Plan you should obtain and read the relevant PDS and this SPDS before making an investment decision.

This SPDS is to be read together with the PDS.

Terms defined in the PDS have the same meaning in this SPDS.

The purpose of this SPDS is to inform you of changes to the ultimate owner of SuperChoice which are to take place on or about 19 December 2008.

The following text replaces the Relationships and Associations section:

Remove the text on this page relating to St Andrew’s Australia.

Replace all forms in the PDS with the forms attached to this document which are dated 19 December 2008.

Location: Inside Front Cover Section: Relationships and Associations

Location: Page 2 Section: St Andrew’s Australia

Location: Page 18 Section: Application Forms

There are a number of changes to our PDS

Relationships and associationsWe invest the assets of SuperChoice in a superannuation life insurance policy issued by the Administrator who is a registered life insurance company and an Australian Financial Services Licensee. The Administrator then invests the assets in the various portfolios described on pages 12 –15 of this PDS and administers SuperChoice. We pay the Administrator to administer SuperChoice on our behalf (pages 16 –18 of this PDS describes the administration fees charged).

Neither the Trustee nor the Administrator is an authorised deposit taking institution. Both the Trustee and the Administrator are wholly owned subsidiaries of St Andrew’s Australia Pty Ltd ABN 96 105 176 234 (‘SAA’). SAA is a related company of Bank of Western Australia Limited (‘BankWest’) ABN 22 050 494 454 AFSL 236872 and the Commonwealth Bank of Australia (‘CBA’) ABN 48 123 123 124 AFSL 234945 on or about 19 December 2008.

Investments in SuperChoice do not represent a deposit with or a liability of BankWest or CBA or any other member of the CBA group of companies in Australia or overseas (other than the Trustee). Your investment can be subject to investment risk, including possible delays in repayment and loss of income and principal. No member of the CBA group of companies in Australia (including BankWest) or overseas guarantees SuperChoice’s capital value or performance (apart from the guarantee given by the Trustee for the Simplicity – Capital Guaranteed Fund). None of these companies (other than the Trustee) is responsible for any statement contained in the PDS.

BankWest plays no role in the issue or administration of interests in SuperChoice and only distributes the SuperChoice PDS.

RACV plays no role in the issue or administration of interests in SuperChoice and only distributes the SuperChoice PDS.

25

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

MEM

bEr

ShIp ApplICATIon

– SupEr

Ann

uATIon

plAn

ImportantThis Application Form relates to the St Andrew’s SuperChoice Superannuation Plan and Pension Plan Product Disclosure Statement (‘PDS’).

please ensure you have read and understood the pDS before making a decision to invest in SuperChoice and completing this application form.

A person providing access to this application form (e.g. your Financial Adviser) must at the same time and by the same means provide access to the PDS and any document which updates the information contained in the PDS.

1. Applicant details

Mr Mrs Ms Miss Other

Surname

Given Names Sex: Male Female

Date of birth Employment status: Full time Part time Casual Not employed

/ / Residential address

Postal adress (if same as above, write ‘As Above’)

Home phone Work phone

Fax Mobile

2. For any rollover superannuation benefits, please complete the following

Fund Name Amount $ , . Fund Name Amount $ , . Fund Name Amount $ , . Fund Name Amount $ , . Fund Name Amount $ , . Fund Name Amount $ , .

This form must be accompanied by a Tax File Number (TFN) nomination form

Membership Application – Superannuation Plan19 December 2008

26

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

26

MEM

bEr

ShIp

App

lICA

TIon

– S

upE

rAn

nu

ATIo

n p

lAn

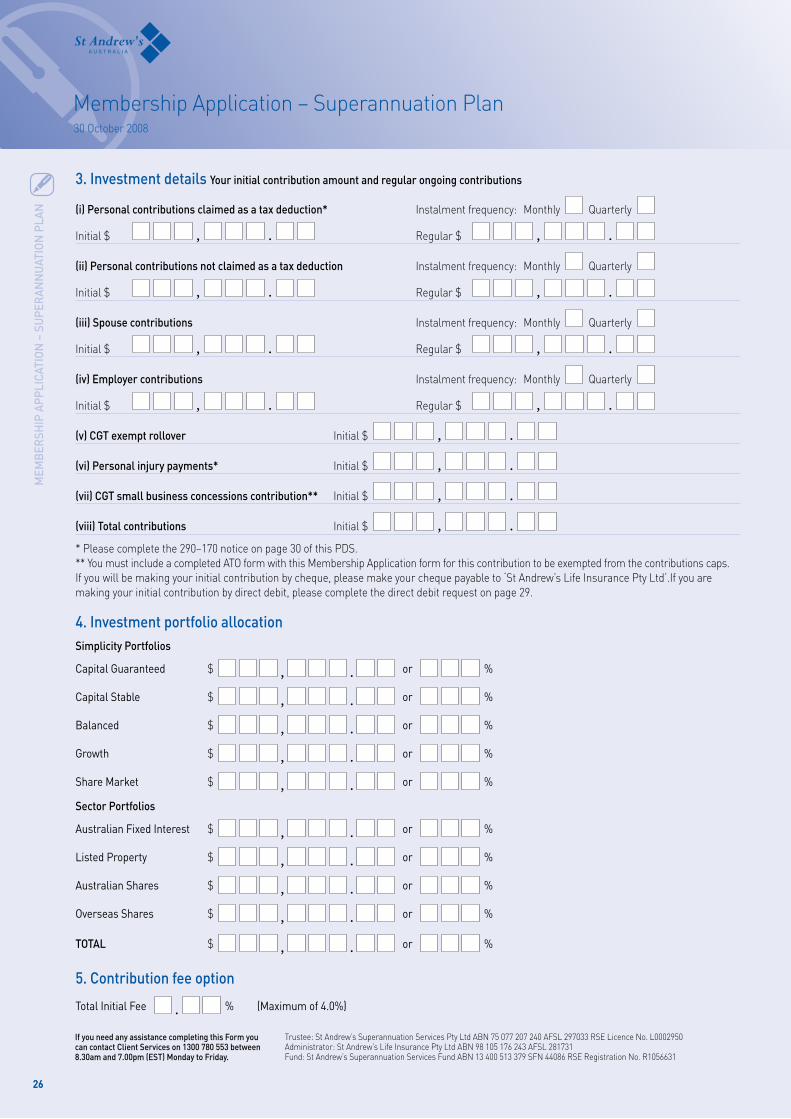

3. Investment details Your initial contribution amount and regular ongoing contributions

(i) personal contributions claimed as a tax deduction* Instalment frequency: Monthly Quarterly

Initial $ , . Regular $ , .

(ii) personal contributions not claimed as a tax deduction Instalment frequency: Monthly Quarterly

Initial $ , . Regular $ , .

(iii) Spouse contributions Instalment frequency: Monthly Quarterly

Initial $ , . Regular $ , .

(iv) Employer contributions Instalment frequency: Monthly Quarterly

Initial $ , . Regular $ , .

(v) CGT exempt rollover Initial $ , .

(vi) personal injury payments* Initial $ , .

(vii) CGT small business concessions contribution** Initial $ , .

(viii) Total contributions Initial $ , . * Please complete the 290–170 notice on page 30 of this PDS. ** You must include a completed ATO form with this Membership Application form for this contribution to be exempted from the contributions caps. If you will be making your initial contribution by cheque, please make your cheque payable to ‘St Andrew’s Life Insurance Pty Ltd’.If you are making your initial contribution by direct debit, please complete the direct debit request on page 29.

4. Investment portfolio allocationSimplicity portfolios

Capital Guaranteed $ , . or %

Capital Stable $ , . or %

Balanced $ , . or %

Growth $ , . or %

Share Market $ , . or %

Sector portfolios

Australian Fixed Interest $ , . or %

Listed Property $ , . or %

Australian Shares $ , . or %

Overseas Shares $ , . or %

ToTAl $ , . or %

5. Contribution fee option

Total Initial Fee . % (Maximum of 4.0%)

Membership Application – Superannuation Plan19 December 2008

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

27

MEM

bEr

ShIp ApplICATIon

– SupEr

Ann

uATIon

plAn

Membership Application – Superannuation Plan19 December 2008

6. Employer details Please complete this secton if your employer will be contributing to your SuperChoice account

Company

Contact name

Contact phone number Contact fax number

Website

7. Investor linkingName of the client with whom a link is to be established must be an immediate family member (as detailed on page 17)

Existing Client Signature

Date: / /

8. other offersWe may use and disclose (to your Financial Adviser and to service providers such as maybe related entities and business partners) your information so that they can forward to you, from time to time, details of other investment opportunities in which you may be interested. Please tick the box if you do not wish to be updated with such investment opportunities. If you do not mark the box we will assume that you want to hear about the investment opportunities we have described.

We will provide to anyone receiving an electronic copy of the PDS, a paper copy of the PDS, any document which updates it and the application form on request and without charge.

The law prohibits any person passing on to another person the application form unless it is attached to, or accompanied by, a complete and un-tampered electronic version of the PDS or a print out of it.

The law prohibits the Trustee from issuing an interest in SuperChoice unless this application form came with the current version of the SuperChoice PDS.

9. DeclarationI declare, acknowledge and agree that:

(i) I hereby apply for membership of SuperChoice and agree to be bound by its trust deed and rules as amended from time to time.

(ii) I understand that St Andrew’s Services Pty Ltd (St Andrew’s) acts as SuperChoice’s Trustee.

(iii) I acknowledge that I have received, read and understood the SuperChoice Superannuation Plan and Pension Plan Product Disclosure Statement (PDS) and that this application form is subject to the terms and conditions of the PDS.

(iv) If I have received the PDS in an electronic format, from the Internet or other electronic means, I acknowledge that I have received the PDS personally or a print out of it accompanied by or attached to this application form.

(v) My application, and the information provided in it, is true, correct and complete.

(vi) I will notify St Andrew’s in writing if at any time my personal details as disclosed in this membership Application Form have changed.

(vii) I understand that neither the repayment of capital nor the investment performance of the Funds (except the Capital Guaranteed portfolio) are guaranteed by St Andrew’s, the Administrator, BankWest, SAA, CBA or any other member of the CBA group in Australia or overseas.

(viii) At the date of this application: • Iwasagedbetween18and64;or • Iwasaged65to74andinthecurrentfinancialyearhave worked in gainful employment (including self employment) at least 40 hours in a period of not more than 30 consecutive days. I have provided the name, address and contact phone numberofmyemployerabove;or • Iamrollingover/transferringabenefittoSuperChoice.

7

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

28

MEM

bEr

ShIp

App

lICA

TIon

– S

upE

rAn

nu

ATIo

n p

lAn

To bE CoMplETED bY FInAnCIAl ADVISEr

Financial Adviser

Financial Adviser’s Signature

Date / / Branch State Adviser Code

office use only:

Client number Account number

7

Membership Application – Superannuation Plan19 December 2008

9. Declaration continued(ix) Iunderstandthatbenefitswillonlybepaidinaccordancewith

SuperChoice’s trust deed and rules as amended from time to time.

(x) I agree that this Membership Application Form and other relevant documents form the basis of the contract between St Andrew’s and me.

(xi) I acknowledge that I have read and understood the Privacy section headed ‘Your Privacy’ in the PDS and consent to the collection, use, maintenance and disclosure of my personal information as set out in that section.

(xii) IunderstandthatunitsinSuperChoicewillbeissuedwithinfivebusiness days after receipt of contributions and rollovers, and completed documentation by the Administrator using the buy unit price current at the date funds are converted into units.

(xiii) I understand that the Administrator guarantees that the unit price of the Capital Guaranteed portfolio will not fall in value. I understand that no other company, including St Andrew’s, the Administrator, St Andrew’s Australia Pty Ltd (‘SAA’), BankWest, CBA or any other member of the CBA group in Australia or overseas guarantee this investment portfolio.

(xiv) I acknowledge that investments in SuperChoice do not represent investments in St Andrew’s, SAA, the Administrator, BankWest, CBA or any other member of the CBA group in Australia or overseas or with any subsidiary of any of these companies and are subject to investment and other risks, including possible delays in repayment, loss of income and principal invested.

(xv) If investing in SuperChoice replaces other investments, I am aware that duplication of initial costs may be to my disadvantage.

(xv) We are bound by laws about the prevention of money laundering andthefinancingofterrorism,includingtheAnti-Money Laundering and Counter-Terrorism Financing Act2006(‘AML/ CTF Laws’). By completing the application form, you agree that: • youdonotsubscribetothefundunderanassumedname; • anymoneyusedbyyoutoinvestinthefundisnotderived fromorrelatedtoanycriminalactivities; • anyproceedsofyourinvestmentwillnotbeusedinrelation toanycriminalactivities; • ifweask,youwillprovideuswithadditionalinformationwe reasonablyrequireforthepurposesofAML/CTFLaws (includinginformationaboutyourself,anybeneficiary,orthe sourceoffundsusedtoinvest); • wemayobtaininformationaboutyouoranybeneficiaryfrom third parties if we believe this is necessary to comply with AML/CTFLaw;and • inordertocomplywithAML/CTFLawswemayberequiredto

take action, including: • delayingorrefusingtheprocessingofanyapplicationor

withdrawal, or • disclosinginformationthatweholdaboutyouorany

beneficiarytoourrelatedbodiescorporateorserviceproviders,orrelevantregulatorsofAML/CTFLaws(whether in or outside of Australia).

Applicant’s Signature

Date: / /

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

29

DIr

ECT DEb

IT rEqu

EST

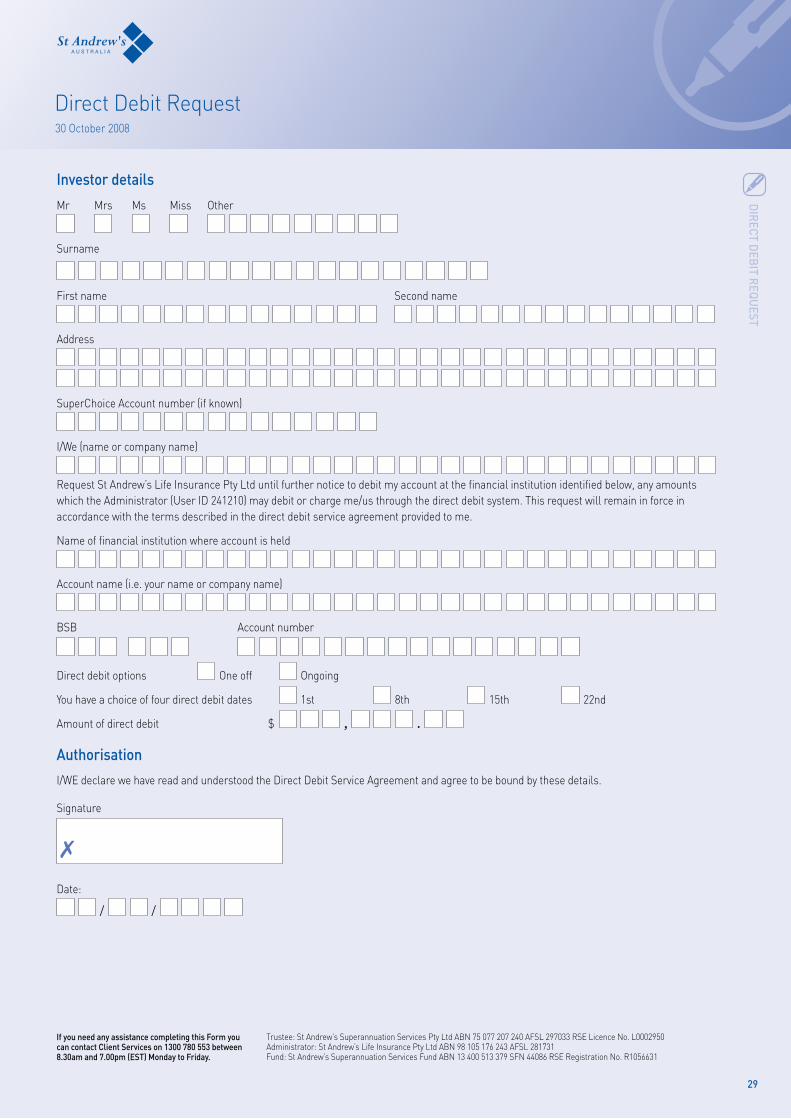

Direct Debit Request19 December 2008

Investor details

Mr Mrs Ms Miss Other

Surname

First name Second name

Address

SuperChoice Account number (if known)

I/We(nameorcompanyname)

RequestStAndrew’sLifeInsurancePtyLtduntilfurthernoticetodebitmyaccountatthefinancialinstitutionidentifiedbelow,anyamountswhichtheAdministrator(UserID241210)maydebitorchargeme/usthroughthedirectdebitsystem.Thisrequestwillremaininforceinaccordance with the terms described in the direct debit service agreement provided to me.

Nameoffinancialinstitutionwhereaccountisheld

Account name (i.e. your name or company name)

BSB Account number

Direct debit options One off Ongoing

You have a choice of four direct debit dates 1st 8th 15th 22nd

Amount of direct debit $ , .

Authorisation

I/WEdeclarewehavereadandunderstoodtheDirectDebitServiceAgreementandagreetobeboundbythesedetails.

Signature

Date:

/ /

7

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

30

SECT

Ion

290

-170

InTE

nTI

on T

o Cl

AIM

pEr

Son

Al C

onTr

Ibu

TIon

S AS

A T

Ax D

EDu

CTIo

n

office use only: Client number Account number Thisnotificationcanbevariedupuntilthetimeyoulodgeyourincometaxreturnortheendofthefollowingfinancialyearafterthecontributionwas made, whichever is earlier.

notice to SuperChoice Trustee under Section 290–170 of the Income Tax Assessment Act 1997This form should be completed if you are intending to claim a tax deduction for personal contributions.

Client name

If you are self-employed you can claim a tax deduction for personal contributions made to St Andrew’s Superannuation Services Pty Ltd (St Andrew’s) superannuation providing:

• lessthan10%ofyourassessableincomeisfromanemployer; • youhavecompletedthisform(Section290–170Notice)andreturnedittoStAndrew’s;and • youreceivealetterfromStAndrew’sadvisingreceiptofthisformstatingthatcontributionswillbetreatedastaxablecontributions by the Trustee.

In respect to the regular contributions you intend to make to SuperChoice, please complete the information below including the year to which the contributions will relate.

30 June 2 0 a) The total amount I intend to contribute to SuperChoice this year $ , . b) The amount of personal contributions to be claimed as a tax deduction $ , . c) Amount of personal contributions not to be claimed as a tax deduction $ , . NB: The total of (b) and (c) must equal (a)

A maximum applies to the amount that can be claimed as a tax deduction. Please contact Client Services or your Financial Adviser if you are unsure of these amounts.

Declaration:

IacknowledgethattheamountIhaveadvisedasbeingclaimedasataxdeductionwillbesubjecttocontributionstaxof15%.

Signature

Date: / / 7

Section 290–170 Intention to Claim Personal Contributions as a Tax Deduction19 December 2008

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

31

TAx FIlE nu

Mb

Er (TFn

) noTIFICATIon

ForM

TaxFileNumber(TFN)Notificationform19 December 2008

This form must be completed in conjunction with a SuperChoice application in all cases except where you are opening a Pension Plan and you are 60 years of age or older.

Asaresultoftheadversefinancialconsequencesyouwillincur,andtheaddedadministrativeburdenplacedonthetrusteeasaresultofanydecision by you not to provide your TFN.

The Trustee has elected not to open an account in SuperChoice where your TFN has not been provided.

Under the Superannuation Industry (Supervision) Act 1993, your superannuation fund is authorised to collect your TFN, which will only be used for lawful purposes.

These purposes may change in the future as a result of legislative change. The Trustee may disclose your TFN to another superannuation provider,whenyourbenefitsarebeingtransferred,unlessyourequestusinwritingthatyourTFNnotbedisclosedtoanyothersuperannuationprovider.

It is not an offence not to quote your TFN. However giving your TFN to us will have the following advantages (which may not otherwise apply):

• SuperChoicewillbeabletoacceptalltypesofcontributionstoyouraccount/s; • thetaxoncontributionstoyoursuperannuationaccount/swillnotincrease; • otherthanthetaxthatmayordinarilyapply,noadditionaltaxwillbedeductedwhenyoustartdrawingdownyoursuperannuationbenefits;and • itwillmakeitmucheasiertotracedifferentsuperannuationaccountsinyournamesothatyoureceiveallyoursuperannuationbenefits when you retire.

Please complete and sign the following and return it with your application for membership. All information provided will be treated in the strictestconfidence.

Name

IhavereadandunderstoodthisformandtheProductDisclosureStatementandconfirmthattothebestofmyknowledgeallinformationgiveninthis document is true and correct.

My Tax File Number is: MysignaturebelowconfirmsmyagreementfortheTrusteetotheuseofmyTFNforalllegallyauthorisedandpermissiblepurposes.

Applicant’s Signature

Date:

/ /

7

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

32

This page has been left blank intentionally.

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

33

MEM

bEr

ShIp ApplICATIon

– pEnSIon

plAn

Membership Application – Pension Plan19 December 2008

1. Are you tranferring from an existing SuperChoice Superannuation plan account?

no Yes – please provide your account number

2. Will the pension be a transition to retirement pension? Yes no

3. Applicant detailsMr Mrs Ms Miss Other

Surname

Given Names Sex: Male Female

Date of birth Australian resident? If No, country of residence

/ / Yes No Residential address

Postal adress (if same as above, write ‘As Above’)

Home phone Work phone

Fax Mobile

4. list the rollover superannuation benefits payments which form part of this pension plan

Fund Name Amount $ , . Fund Name Amount $ , . Fund Name Amount $ , .

ImportantThis Application Form relates to the St Andrew’s SuperChoice Superannuation Plan and Pension Plan Product Disclosure Statement (‘PDS’).

please ensure you have read and understood the pDS before making a decision to invest in SuperChoice and completing this application form.

A person providing access to this application form (e.g. your Financial Adviser) must at the same time and by the same means provide access to the PDS and any document which updates the information contained in the PDS.

This form must be accompanied by a Tax File Number (TFN) nomination form if under 60

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

34

5. reversionary pensionerIf you want to nominate a reversionary pensioner fill out this section.

Mr Mrs Ms Miss Other

Surname PLEASE PRINT

Given Names Sex: Male Female

Date of birth * Relationship to member

/ / Residential address

Postal adress (if same as above, write ‘As Above’)

Home phone Work phone

Fax Mobile

Client number if applicable * Under the law, you are only able to nominate a dependant – being a spouse, de facto spouse, child (including step-child, adopted child and ex-nuptialchild),apersonwhoisfinanciallydependantonyouorapersonwithwhomyouareinaninterdependentrelationship(whichgenerallyrequires a close personal relationship and cohabitation or a disability preventing cohabitation).

6. Income payments (please tick one box)

(A)Forpensionplanscommencingonorafter1June–wouldyouliketodeferpaymentuntilthestartofthenewfinancialyear?

Yes (complete C, D below)

No (complete the rest of the sections below)

(B)Isthepaymentspecifiedforthefirstyeartheannualpayment,orprorata Full year Pro rata

(C) Select amount client would like to recieve $ , . or Minimum Maximum (TTR pension only)

(D) Payment frequency Monthly Quarterly Half-yearly YearlyDateoffirstpayment / /

MEM

bEr

ShIp

App

lICA

TIon

– p

EnSI

on p

lAn

Membership Application – Pension Plan19 December 2008

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

35

MEM

bEr

ShIp ApplICATIon

– pEnSIon

plAn

Membership Application – Pension Plan19 December 2008

7. Investment portfolio allocation and pension payment allocationNB: If you do not nominate a sequence or payment composition, payments will be made on the asset allocation of your investments in the Fund.

Simplicity portfolios $ or % and pension payment Composition

or pension payment Sequence

Capital Guaranteed $ , . or % %Capital Stable $ , . or % %Balanced $ , . or % %Growth $ , . or % %Share Market $ , . or % %

Sector portfolios $ or %

Australian Fixed Interest $ , . or % %Listed Property $ , . or % %Australian Shares $ , . or % %Overseas Shares $ , . or % %

Total $ , . or % %

8. Contribution fee

Total Initial Fee . % (Maximum of 4.0%.)

9. payment details Please provide details of your nominated bank, building society or credit union account to which income payments will be paid:

Name of Institution

Branch address

Account name

Bank (BSB No.) Account number

10. Investor linkingName of the client with whom a link is to be established must be an immediate family member (as detailed on page 17)

Existing Client Signature

Date: / / 7

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

36

MEM

bEr

ShIp

App

lICA

TIon

– p

EnSI

on p

lAn

13. DeclarationI declare, acknowledge and agree that:

(i) I hereby apply for membership of SuperChoice and agree to be bound by its trust deed and rules as amended from time to time.

(ii) I understand that St Andrew’s Services Pty Ltd (St Andrew’s) acts as SuperChoice’s Trustee.

(iii) I acknowledge that I have received, read and understood the SuperChoice Superannuation Plan and Pension Plan Product Disclosure Statement (PDS) and that this application form is subject to the terms and conditions of the PDS.

(iv) If I have received the PDS in an electronic format, from the Internet or other electronic means, I acknowledge that I have received the PDS personally or a print out of it accompanied by or attached to this application form.

(v) My application, and the information provided in it, is true, correct and complete.

(vi) I will notify St Andrew’s in writing if at any time my personal details as disclosed in this membership Application Form have changed.

(vii) I understand that neither the repayment of capital nor the investment performance of the Funds (except the Capital Guaranteed portfolio) are guaranteed by St Andrew’s, the

Administrator, BankWest, SAA, CBA or any other member of the CBA group in Australia or overseas.

(viii) At the date of this application: • Iwasagedbetween18and64;or • Iwasaged65to74andinthecurrentfinancialyearhave worked in gainful employment (including self employment) at least 40 hours in a period of not more than 30 consecutive days. I have provided the name, address and contact phone numberofmyemployerabove;or • Iamrollingover/transferringabenefittoSuperChoice.

(ix) IunderstandthatbenefitswillonlybepaidinaccordancewithSuperChoice’s trust deed and rules as amended from time to time.

(x) I agree that this Membership Application Form and other relevant documents form the basis of the contract between St Andrew’s and me.

(xi) I acknowledge that I have read and understood the Privacy section headed ‘Your Privacy’ in the PDS and consent to the collection, use, maintenance and disclosure of my personal information as set out in that section.

(xii) IunderstandthatunitsinSuperChoicewillbeissuedwithinfivebusiness days after receipt of contributions and rollovers, and completed documentation by the Administrator using the buy unit price current at the date funds are converted into units.

11. Conditions of releaseThePensionPlan(otherthannon-commutablepensions)canonlybepurchasedwithunrestrictednon-preservedbenefits.

Ifanypartofyourbenefitcontainspreservedorrestrictednon-preservedbenefitsyouwillneedtocompletethefollowingdeclaration.

Ihaveattainedage65;or

Ihaveceasedgainfulemploymentsinceturningage60;or

I have attained age 55 but not yet reached age 65, have ceased gainful employment and do not intend to work again for more than 10hoursperweek;or

I have attained age 55 and am commencing a non-commutable transition to retirement pension.

Applicant’s Signature

Date: / /

12. other offers

7

We may use and disclose (to your Financial Adviser and to service providers such as posting services) your information so that they can forward to you, from time to time, details of other investment opportunities in which you may be interested. Please tick the box if you do not wish to be updated with such investment opportunities. If you do not mark the box we will assume that you want to hear about the investment opportunities we have described.

We will provide to anyone receiving an electronic copy of the PDS, a paper copy of the PDS, any document which updates it and the application form on request and without charge.

The law prohibits any person passing on to another person the application form unless it is attached to, or accompanied by, a complete and un-tampered electronic version of the PDS or a print out of it.

Membership Application – Pension Plan19 December 2008

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

37

MEM

bEr

ShIp ApplICATIon

– pEnSIon

plAn

Membership Application – Pension Plan19 December 2008

To bE CoMplETED bY Your FInAnCIAl ADVISEr

Financial Adviser

Financial Adviser’s Signature

Date

/ / Branch

Adviser Code

State

office use only

Client number

Account number

(xiii) I understand that the Administrator guarantees that the unit price of the Capital Guaranteed portfolio will not fall in value. I understand that no other company, including St Andrew’s, the Administrator, St Andrew’s Australia Pty Ltd (‘SAA’), BankWest, CBA or any other member of the CBA group in Australia or overseas guarantee this investment portfolio.

(xiv) I acknowledge that investments in SuperChoice do not represent investments in St Andrew’s, SAA, the Administrator, BankWest, CBA or any other member of the CBA group in Australia or overseas or with any subsidiary of any of these companies and are subject to investment and other risks, including possible delays in repayment, loss of income and principal invested.

(xv) If investing in SuperChoice replaces other investments, I am aware that duplication of initial costs may be to my disadvantage.

(xv) We are bound by laws about the prevention of money laundering andthefinancingofterrorism,includingtheAnti-Money Laundering and Counter-Terrorism Financing Act2006(‘AML/ CTF Laws’). By completing the application form, you agree that: • youdonotsubscribetothefundunderanassumedname; • anymoneyusedbyyoutoinvestinthefundisnotderived fromorrelatedtoanycriminalactivities; • anyproceedsofyourinvestmentwillnotbeusedinrelation toanycriminalactivities; • ifweask,youwillprovideuswithadditionalinformationwe reasonablyrequireforthepurposesofAML/CTFLaws (includinginformationaboutyourself,anybeneficiary,orthe sourceoffundsusedtoinvest); • wemayobtaininformationaboutyouoranybeneficiaryfrom third parties if we believe this is necessary to comply with AML/CTFLaw;and • inordertocomplywithAML/CTFLawswemayberequiredto

take action, including: • delayingorrefusingtheprocessingofanyapplicationor

withdrawal, or • disclosinginformationthatweholdaboutyouorany

beneficiarytoourrelatedbodiescorporateorserviceproviders,orrelevantregulatorsofAML/CTFLaws(whether in or outside of Australia).

Applicant’s Signature

Date: / /

7

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

38

This page has been left blank intentionally.

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

39

ApplICATIon To Tr

AnSFEr

SupEr

Ann

uATIon

bEn

EFITS

ApplicationtoTransferSuperannuationBenefits19 December 2008

This form should be completed if you would like to consolidate other superannuation funds you hold into SuperChoice. We can arrange to send this form to the paying institution on your behalf or alternatively you can arrange to post the form directly. You will need to complete a separate form for each fund. This form can be photocopied or you can ask your Financial Adviser or Client Services for multiple copies.

1. Investor detailsInvestor name

SuperChoice Account number

Postal address

2. Details of previous superannuation fundFund name

Fund account number

Fund address

Approximatevalueofbenefits $ , , . Amount of transfer

Total value

Partial rollover } Please tick one box only

Cheques to be made payable to: ‘St Andrew’s Life Insurance Pty Ltd’ GPO Box 2979 Melbourne VIC 3001.

Amount $ , . or

Units or

% %

3. Declaration

IrequestandauthorisetheTrusteetransfermybenefitsfrommypreviousfundasoutlinedabovetotheSuperChoicePersonalSuperannuationand Pension Plan. I acknowledge that I have received, read and understood the St Andrew’s SuperChoice Superannuation Plan and Pension Product Disclosure Statement (‘PDS’) and that this Membership Application Form is subject to the terms and conditions of the PDS. My application, and the information provided in it, is true, correct and complete. I understand exit fees may apply on leaving my previous fund. I understand both funds are complying Superannuation Funds. I understand the Trustee may be required under tax law to deduct tax from my transferred account. I authorise the Trustee and St Andrew’s Life Insurance Pty Ltd to act on my behalf in arranging and receiving information aboutthistransfer.IdischargetheSuperproviderofmypreviousfundofallliabilitiesinrespecttothebenefitstransferredtotheFund.

Signature

Date: / / 7

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

40

St Andrew’s Superannuation Services Pty Ltd

ABN 75 077 207 AFSL 297033

RSE Licence No L0002950

Superannuation Plan SPIN SAA002AU

Pension Plan SPIN SAA003AU

19 December 2008

Compliance Declaration

To whom it may concern

The St Andrew’s SuperChoice Superannuation Plan is the accumulation plan of the St Andrew’s Superannuation Services Fund (the Fund), ABN 13 400 513 379, SFN 440806, established by a Trust Deed dated 1 March 1962.

TheStAndrew’sSuperChoicePensionPlanisasuperannuationincomestreamasdefinedintheIncome Tax Assessment Act 1997 and is for thebenefitofthepensionertaxpayerorforhisorherdependantsintheeventofhisorherdeath.TheTrusteeoftheFundis St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240.

The Fund is a regulated superannuation fund within the meaning of the Superannuation Industry (Supervision) Act 1993 and is not subject to a direction by the Australian Prudential Regulation Authority not to accept contributions. It is the Trustee’s intention to maintain the Fund at all times as a complying superannuation fund within the meaning of s.42(1) of this Act.

TheTrustDeedoftheFundallowsbenefitsfromothersuperannuationfundstoberolledoverortransferredtotheFund.TheTrustDeedallowsemployerstomakecontributionsintotheFund.TherequirementsoftheFundforpreservationofbenefitssatisfythepreservationstandards set out in the Superannuation Industry (Supervision) Regulations.

For further information about making contributions to the Fund, contact Client Services on 1300 780 553 between 8.30am and 7.00pm EST Monday to Friday.

Sincerely

nadeeja Jayaratne Compliance Manager

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

41

bIn

DIn

G D

EATh n

oMIn

ATIon For

M

Binding Death Nomination Form19 December 2008

1. purpose of formI am using this form to (tick one):

Makeabindingdeathbenefitnomination(pleasecompletesections2,3,4and5below).

Changeabindingdeathbenefitnominationpreviouslymadebyme(pleasecompletesections2,3,4and5below).

When completing section 3 “Beneficiary Details”, please provide details of all beneficiaries you wish to nominate, including those you may have nominated when completing a previous binding death benefit nomination form.

Revokeabindingdeathbenefitnominationpreviouslymadebyme(pleasecompletesections2,4and5below).

Confirmabindingdeathbenefitnomination(pleasecompletesections2and4below).

2. Member detailsMr Mrs Ms Miss Other

Surname

First name(s)

Avalidbindingdeathbenefitnominationprovidesyouwithcertaintyinrespectofwhowillreceiveyourdeathbenefitintheeventofyourdeath. It is a legal instrument that requires the Trustee to pay your deathbenefittothepersonorpersonsnominatedintheBindingDeathNominationFormasyourbeneficiary/iesintheproportionsspecifiedbyyou.

For a binding nomination to be valid each of the following conditions mustbesatisfied.

• Itmustbeinwriting • Itmustbesignedanddatedbyyouinthepresenceoftwo witnesses (who are both at least 18 years of age and neither is a nominatedbeneficiary) • Itmustcontainadeclarationsignedanddatedbybothwitnesses stating that you signed the nomination in their presence • Itmustnotbemorethan3yearsafterthedateofsigningordate oflastbeingconfirmedoramended • Onlyyourdependantsand/oryourlegalpersonalrepresentative can be nominated • Theproportionofbenefitpayabletoeachnomineemustbeclearly indicatedandtheproportionsmustaddto100%

Youmay,atanytime,confirm,amendorrevokeyourbindingdeathbenefitnomination.Youcanconfirmyourexistingnominationbygiving us a written notice signed and dated by you. You can amend or revoke your existing nomination in the same way as you make your original nomination.

WewilladviseyouofyourcurrentnominationsinyourBenefitStatement sent to you each year. In addition, where three years has

passedandyournominationhasnotbeenconfirmedoramended,wewill advise you of the lapsing of your binding nomination.

If a nominated dependant dies or is no longer a dependant at the timeofyourdeathyourbindingdeathbenefitnominationwillbeinvalid.Intheeventthatyourbindingdeathbenefitnominationisinvalidandyoudiewewillpayyourdeathbenefittoyourlegalpersonalrepresentative.Ifwecannotpayyourdeathbenefittoyourlegalpersonalrepresentative,yourbenefitwillbepaidtoanyotherperson as permitted under the Fund’s Trust Deed (which is the document setting out the rules of the Fund).

If you have a superannuation account as well as a Pension account in the Fund any binding death nomination you provide to the Trustee will cover both accounts (except interests in Lite Super (if any)). All benefitspaidoutunderabindingdeathbenefitnominationwillbein the form a lump sum. If you have an income stream account and havenominateda‘reversionarybeneficiary’,thiswillbeappliedinplaceofavalidbindingdeathbenefitnomination.

The Trustee recommends that you should review any binding death nomination from time to time taking into account your Will and any change in your personal circumstances.

WheretheTrusteeholdsavalidbindingdeathbenefitnominationatthetimeofyourdeath,itwillpayyourdeathbenefitinaccordancewith your wishes. However, where the Trustee is subject to certain court orders, the Trustee is not required to comply with an otherwise valid nomination.

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

42

bIn

DIn

G D

EATh

noM

InAT

Ion

For

M

2. Member details continuedResidential address

Postal address (if same as above, write ‘AS ABOVE’)

Daytime contact number

Date of birth

/ / Account number(s)* Client number(s)*

* If you have more than two accounts within the St Andrew’s Superannuation Services Fund, or more than two client numbers, please provide all further details in an attachment to this Form.

3. beneficiary detailsPleaseprovideyourbeneficiary/iesdetailsbelow.Eachbeneficiaryyounominatedmustbeyourspouse(includingadefactospouse),child(includingadopted,step,ex-nuptialandadultchildren),financialdependant,interdependant,oryourlegalpersonalrepresentative(seetheinformationsheeton‘DeathBenefits’foranexplanationoftheseterms).The%ofbenefitcolumnmusttotal100%.

nominated beneficiary no. 1

Full name

Dateofbirth %ofbenefit(total100%)

/ / %Daytime contact number

Relationship to member

Binding Death Nomination Form19 December 2008

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

43

SIDE h

EADIn

G poSITIon

bIn

DIn

G D

EATh n

oMIn

ATIon For

M

Binding Death Nomination Form19 December 2008

nominated beneficiary no. 2

Full name

Dateofbirth %ofbenefit(total100%)

/ / %Daytime contact number

Relationship to member

nominated beneficiary no. 3

Full name

Dateofbirth %ofbenefit(total100%)

/ / %Daytime contact number

Relationship to member

nominated beneficiary no. 4

Full name

Dateofbirth %ofbenefit(total100%)

/ / %Daytime contact number

Relationship to member

nominated beneficiary no. 5

Full name

Dateofbirth %ofbenefit(total100%)

/ / %Daytime contact number

Relationship to member

Ifyouwanttonominatemorebeneficiariesthanwillfitonthisform,pleaseincludethesamedetailsforeachadditionalbeneficiaryinanattachment to this Form. Please ensure that the attachment includes your contact details and is signed, dated and witnessed in the same way and at the same time as this Form is witnessed.

If you need any assistance completing this Form you can contact Client Services on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday.

Trustee: St Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950 Administrator: St Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731 Fund: St Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 44086 RSE Registration No. R1056631

44

bIn

DIn

G D

EATh

noM

InAT

Ion

For

M

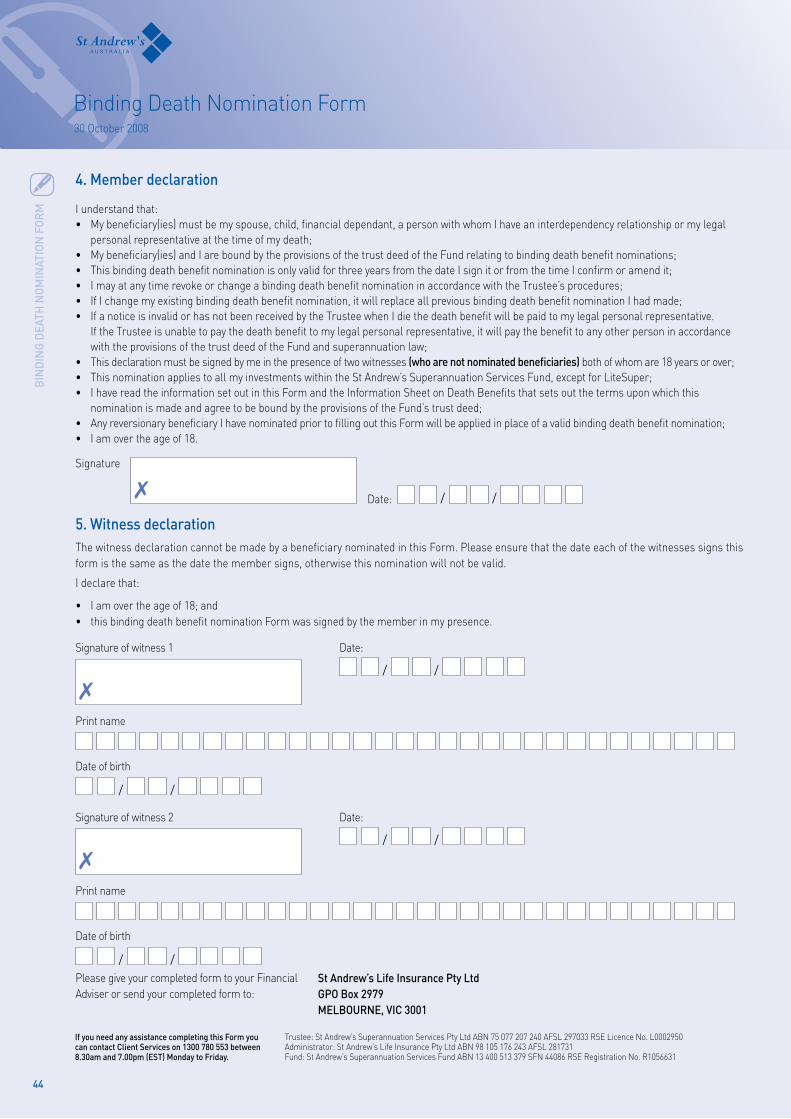

4. Member declaration

I understand that: • Mybeneficiary(ies)mustbemyspouse,child,financialdependant,apersonwithwhomIhaveaninterdependencyrelationshipormylegal personalrepresentativeatthetimeofmydeath; • Mybeneficiary(ies)andIareboundbytheprovisionsofthetrustdeedoftheFundrelatingtobindingdeathbenefitnominations; • ThisbindingdeathbenefitnominationisonlyvalidforthreeyearsfromthedateIsignitorfromthetimeIconfirmoramendit; • ImayatanytimerevokeorchangeabindingdeathbenefitnominationinaccordancewiththeTrustee’sprocedures; • IfIchangemyexistingbindingdeathbenefitnomination,itwillreplaceallpreviousbindingdeathbenefitnominationIhadmade; • IfanoticeisinvalidorhasnotbeenreceivedbytheTrusteewhenIdiethedeathbenefitwillbepaidtomylegalpersonalrepresentative. IftheTrusteeisunabletopaythedeathbenefittomylegalpersonalrepresentative,itwillpaythebenefittoanyotherpersoninaccordance withtheprovisionsofthetrustdeedoftheFundandsuperannuationlaw; • Thisdeclarationmustbesignedbymeinthepresenceoftwowitnesses(who are not nominated beneficiaries)bothofwhomare18yearsorover; • ThisnominationappliestoallmyinvestmentswithintheStAndrew’sSuperannuationServicesFund,exceptforLiteSuper; • IhavereadtheinformationsetoutinthisFormandtheInformationSheetonDeathBenefitsthatsetsoutthetermsuponwhichthis nominationismadeandagreetobeboundbytheprovisionsoftheFund’strustdeed; • AnyreversionarybeneficiaryIhavenominatedpriortofillingoutthisFormwillbeappliedinplaceofavalidbindingdeathbenefitnomination; • Iamovertheageof18.

Signature

Date: / / 5. Witness declarationThewitnessdeclarationcannotbemadebyabeneficiarynominatedinthisForm.Pleaseensurethatthedateeachofthewitnessessignsthisform is the same as the date the member signs, otherwise this nomination will not be valid.

I declare that:

• Iamovertheageof18;and • thisbindingdeathbenefitnominationFormwassignedbythememberinmypresence.

Signature of witness 1 Date:

/ /

Print name

Date of birth

/ / Signature of witness 2 Date:

/ /

Print name

Date of birth

/ / Please give your completed form to your Financial Adviser or send your completed form to:

St Andrew’s life Insurance pty ltd Gpo box 2979 MElbournE, VIC 3001

7

7

7

Binding Death Nomination Form19 December 2008

45

9 8

S T

L I F E

P T Y L T D

I N S U R A N C EC L I

G P O

M E L B O U R N E

V I C

B O X 2 9 7 9

E N T S E R V I C E S

1 3 0 0

3 0 0 1

7 8 0 5 5 3

A N D R E W ‘ S

1 0 5 1 7 6 2 4 3

4646

Tax File Number Declaration NotesThe Tax file number declaration is not an application form for a tax file number (TFN). If you have never had a TFN and want to provide your payer with your TFN you will need to complete a Tax file number application or enquiry for an individual (NAT 1432).

You will need to provide proof of identity documents as outlined on the application form. For further information about applying for a TFN, phonetheAustralianTaxationOffice(ATO)13 28 61, between 8.00am and 6.00pm, Monday to Friday.

Who ShoulD CoMplETE ThIS DEClArATIon?You should complete a new Tax file number declaration before you start to receive payments from a new payer, for example, when you start a new job or become entitled to a superannuation pension.

The entity making the payment is your ‘payer’ and you are the ‘payee’.

The information you provide in this declaration will help your payer work out how much tax to take out of payments to be made to you.

YourpayermustnotifytheTaxOfficewithin14daysofthestartofthe new arrangement.

This declaration covers payments for: •workandservices–paymentstoemployees,company directors,officeholders,aswellaspaymentsunderreturn-to-workschemes,labourhirearrangements,orpaymentsspecifiedby regulation•benefitandcompensationpayments,and•retirementpaymentsandannuitiesandeligibletermination

payments.

VArYInG Your CurrEnT rATE oF WIThholDInGYou also need to complete a Withholding declaration (NAT 3093) if at any time you wish to: •adviseachangetoyourtaxoffsetorfamilytaxbenefit

entitlement•claimthetax-freethresholdanddiscontinueclaimingthe

threshold with other payers•advisethatyouhavebecomeorceasedtobeanAustralianresi-

dent for tax purposes, or•adviseyourpayerofHigherEducationLoanProgram(HELP)or

Financial Supplement repayment obligations or changes.

If you qualify for a reduced rate of Medicare levy or are liable for the Medicare levy surcharge, you can vary the amount your payer withholds from your payments by completing a Medicare levy variation declaration (NAT 0929).

prIVACY oF InForMATIonThe Income Tax Assessment Act1936authorisestheTaxOfficetorequest information in this declaration. This information will help theTaxOfficeadministerthelawsrelatingtotaxation,andothergovernment agencies administering other legislation covering Commonwealthbenefitsandsuperannuation.Allinformation, includingpersonalinformation,collectedbytheTaxOfficeistreatedasconfidentialandisprotectedbytheIncome Tax Assessment Act 1936 and the Privacy Act 1988.

TheTaxOfficemaygivethisinformationtoothergovernmentagencies as authorised by taxation law, for example, Common-wealth agencies which administer laws relevant to your particular situation. Depending on your situation these agencies could include Centrelink, the Australian Federal Police, the Child Support Agency, the Department of Veterans’ Affairs, the

Department of Immigration and Multicultural and Indigenous Affairs, the Department of Family and Community Services and the Department of Education, Science and Training.

Only certain people and organisations can ask for your TFN. These include employers, some federal government agencies, trustees for superannuation funds, payers under the pay as you go (PAYG) system, higher education institutions, the Child Support Agency (CSA) and investment bodies such as banks. Section 202C of the Income Tax Assessment Act1936authorisestheTaxOfficetore-quest quotation of your TFN on this declaration for the purposes of administering taxation laws. It is not an offence not to quote your TFN but there may be consequences if you do not, for example, you may have more tax withheld than otherwise would occur.

If you need more information about how the tax laws protect your personal information, or have any concerns about how the Tax Officehashandledyourpersonalinformation,phone132861,between 8.00am and 6.00pm, Monday to Friday.

hoW To FIll In ThIS DEClArATIonThisTaxfilenumberdeclarationisnotanapplicationformforataxfilenumber(TFN).IfyouhaveneverhadaTFNandwanttoprovide your payer with your TFN you will need to complete a Tax file number application or enquiry for an individual (NAT 1432). You will need to provide proof of identity documents as outlined on the application form.

Please print neatly in BLOCK LETTERS, one character to a box, like this:

2 6 O ‘ C O N N O R S T

Please use a black or dark blue pen only.

For more information phone 13 28 61 between 8.00am and 6.00pm, Monday to Friday or visit www.ato.gov.au

4747

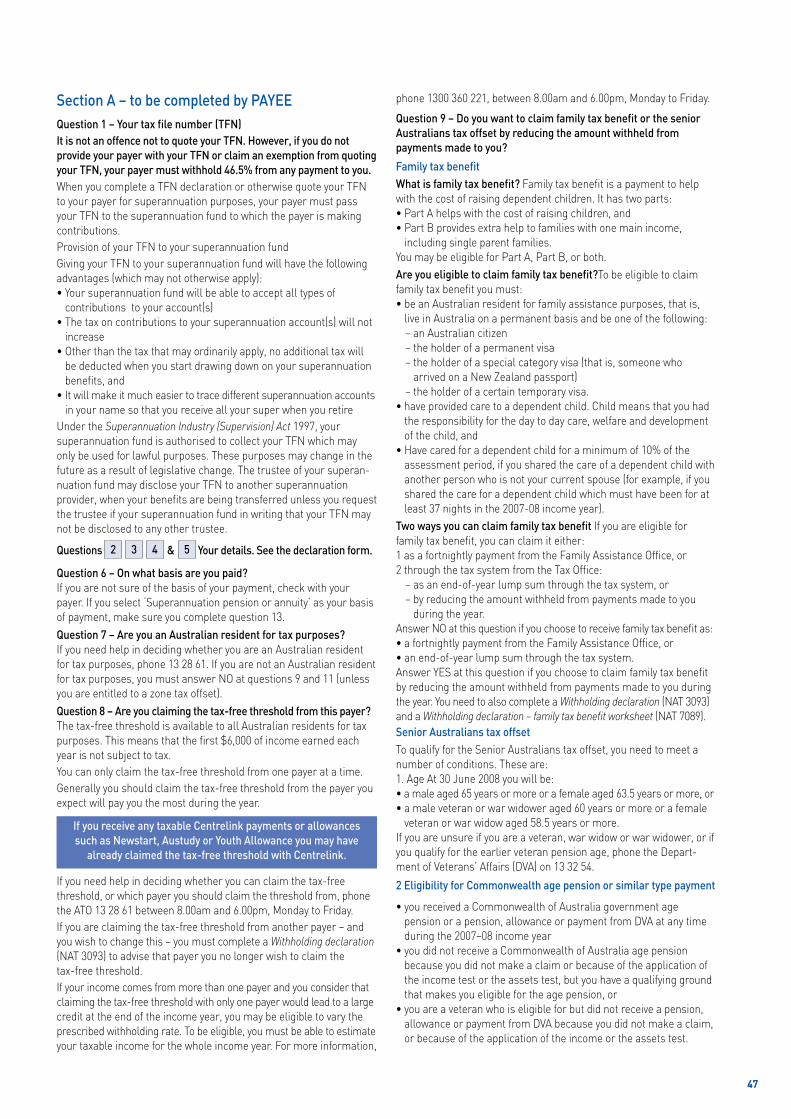

Section A – to be completed by pAYEEquestion 1 – Your tax file number (TFn)It is not an offence not to quote your TFn. however, if you do not provide your payer with your TFn or claim an exemption from quoting your TFn, your payer must withhold 46.5% from any payment to you.When you complete a TFN declaration or otherwise quote your TFN to your payer for superannuation purposes, your payer must pass your TFN to the superannuation fund to which the payer is making contributions.Provision of your TFN to your superannuation fundGiving your TFN to your superannuation fund will have the following advantages (which may not otherwise apply):•Yoursuperannuationfundwillbeabletoacceptalltypesof

contributions to your account(s)•Thetaxoncontributionstoyoursuperannuationaccount(s)willnot

increase•Otherthanthetaxthatmayordinarilyapply,noadditionaltaxwill

be deducted when you start drawing down on your superannuation benefits,and•Itwillmakeitmucheasiertotracedifferentsuperannuationaccounts

in your name so that you receive all your super when you retireUnder the Superannuation Industry (Supervision) Act 1997, your superannuation fund is authorised to collect your TFN which may only be used for lawful purposes. These purposes may change in the future as a result of legislative change. The trustee of your superan-nuation fund may disclose your TFN to another superannuation provider,whenyourbenefitsarebeingtransferredunlessyourequestthe trustee if your superannuation fund in writing that your TFN may not be disclosed to any other trustee.

questions 2 3 4 & 5 Your details. See the declaration form.

question 6 – on what basis are you paid?If you are not sure of the basis of your payment, check with your payer. If you select ‘Superannuation pension or annuity’ as your basis of payment, make sure you complete question 13.question 7 – Are you an Australian resident for tax purposes?If you need help in deciding whether you are an Australian resident for tax purposes, phone 13 28 61. If you are not an Australian resident for tax purposes, you must answer NO at questions 9 and 11 (unless you are entitled to a zone tax offset).question 8 – Are you claiming the tax-free threshold from this payer?The tax-free threshold is available to all Australian residents for tax purposes.Thismeansthatthefirst$6,000ofincomeearnedeachyear is not subject to tax.You can only claim the tax-free threshold from one payer at a time.Generally you should claim the tax-free threshold from the payer you expect will pay you the most during the year.

If you receive any taxable Centrelink payments or allowances such as newstart, Austudy or Youth Allowance you may have

already claimed the tax-free threshold with Centrelink.

If you need help in deciding whether you can claim the tax-free threshold, or which payer you should claim the threshold from, phone the ATO 13 28 61 between 8.00am and 6.00pm, Monday to Friday. If you are claiming the tax-free threshold from another payer – and you wish to change this – you must complete a Withholding declaration (NAT 3093) to advise that payer you no longer wish to claim the tax-free threshold.If your income comes from more than one payer and you consider that claiming the tax-free threshold with only one payer would lead to a large credit at the end of the income year, you may be eligible to vary the prescribed withholding rate. To be eligible, you must be able to estimate your taxable income for the whole income year. For more information,

phone 1300 360 221, between 8.00am and 6.00pm, Monday to Friday.

question 9 – Do you want to claim family tax benefit or the senior Australians tax offset by reducing the amount withheld from payments made to you?

Family tax benefit What is family tax benefit? Familytaxbenefitisapaymenttohelpwith the cost of raising dependent children. It has two parts:•PartAhelpswiththecostofraisingchildren,and•PartBprovidesextrahelptofamilieswithonemainincome,

including single parent families.You may be eligible for Part A, Part B, or both.Are you eligible to claim family tax benefit?To be eligible to claim familytaxbenefityoumust:•beanAustralianresidentforfamilyassistancepurposes,thatis,

live in Australia on a permanent basis and be one of the following: – an Australian citizen – the holder of a permanent visa – the holder of a special category visa (that is, someone who

arrived on a New Zealand passport) – the holder of a certain temporary visa.•haveprovidedcaretoadependentchild.Childmeansthatyouhad

the responsibility for the day to day care, welfare and development of the child, and•Havecaredforadependentchildforaminimumof10%ofthe

assessment period, if you shared the care of a dependent child with another person who is not your current spouse (for example, if you shared the care for a dependent child which must have been for at least 37 nights in the 2007-08 income year).

Two ways you can claim family tax benefit If you are eligible for familytaxbenefit,youcanclaimiteither:1asafortnightlypaymentfromtheFamilyAssistanceOffice,or2throughthetaxsystemfromtheTaxOffice: – as an end-of-year lump sum through the tax system, or – by reducing the amount withheld from payments made to you

during the year.AnswerNOatthisquestionifyouchoosetoreceivefamilytaxbenefitas:•afortnightlypaymentfromtheFamilyAssistanceOffice,or•anend-of-yearlumpsumthroughthetaxsystem.AnswerYESatthisquestionifyouchoosetoclaimfamilytaxbenefitby reducing the amount withheld from payments made to you during the year. You need to also complete a Withholding declaration (NAT 3093) and a Withholding declaration – family tax benefit worksheet (NAT 7089).Senior Australians tax offset To qualify for the Senior Australians tax offset, you need to meet a number of conditions. These are:1. Age At 30 June 2008 you will be:•amaleaged65yearsormoreorafemaleaged63.5yearsormore,or•amaleveteranorwarwidoweraged60yearsormoreorafemale

veteran or war widow aged 58.5 years or more.If you are unsure if you are a veteran, war widow or war widower, or if you qualify for the earlier veteran pension age, phone the Depart-ment of Veterans’ Affairs (DVA) on 13 32 54.

2 Eligibility for Commonwealth age pension or similar type payment

•youreceivedaCommonwealthofAustraliagovernmentagepension or a pension, allowance or payment from DVA at any time during the 2007–08 income year•youdidnotreceiveaCommonwealthofAustraliaagepension

because you did not make a claim or because of the application of the income test or the assets test, but you have a qualifying ground that makes you eligible for the age pension, or•youareaveteranwhoiseligibleforbutdidnotreceiveapension,

allowance or payment from DVA because you did not make a claim, or because of the application of the income or the assets test.

4848

3. Income threshold. You satisfy the income threshold that applies to you:•youdidnothaveaspouse(marriedordefacto)andyourtaxableincome was less than $43,707•youhadaspouse(marriedordefacto)andthecombinedtaxableincome of you and your spouse was less than $68,992, or•youhadaspouse(marriedordefacto)andthecombinedtaxableincome of you and your spouse, where you ‘had to live apart due to illness’ or either of you was in a nursing home at any time in 2004–05 income year, was less than $81,840.‘Had to live apart due to illness’ is a term used to describe a situation where the living expenses of you and your spouse (married or de facto) are increased because you are unable to live together in your homeduetotheindefinitelycontinuingillnessorinfirmityofeitherorboth of you.

4. not in jail. You were not in jail for the whole income year.If you qualify, the amount of tax offset available to you depends on your taxable income levels and whether you are single, married or a member of an illness-separated couple.Answer NO at this question if you wish to claim the entitlement to the tax offset as a lump sum in your end-of-year assessment.Answer YES at this question if you choose to receive the Senior Australians tax offset by having a reduced rate of tax deducted from your pay during the year. You will need to complete a Withholding dec laration (NAT 3093) (see ‘Varying your withholding rate’). Your payer will calculate your rate of withholding based on the information you provide.Your tax payable will be reduced to nil where you are entitled to the Senior Australians tax offset and your taxable income is equal to or below the relevant income threshold. A reduced tax offset will apply where your taxable income is above the income thresholds, but less than the cut-out threshold.You may not be required to lodge an income tax return if your income from all sources is less than or equal to the relevant income threshold.If your income comes from more than one source, do not comp lete this question for any of your payers. Phone 1300 360 221, between 8.00am and 6.00pm, Monday to Friday, for advice.

It is against the law to claim the Senior Australians tax offset from more than one payer at the same time.

question 10 – Are you claiming a zone, dependent spouse or special tax offset?You may be entitled to a:

•zonetaxoffsetifyouliveorworkincertainremoteorisolatedareasof Australia•dependentspouse(marriedordefacto)taxoffsetifyourspouse’s

separate net income is expected to be less than $8,682 for the income year ended June 2008, or•specialtaxoffsetforadependentinvalidrelative,dependentparent,

housekeeper caring for an invalid spouse or a dependent child housekeeper.

Answer NO at this question if you choose to receive any of these offsets as an end-of-year lump sum through the tax system.Answer YES at this question if you choose to receive these tax offsets by having a reduced rate of tax deducted from your pay during the year. You will need to complete a Withholding declaration (NAT 3093) (see ‘Varying your withholding rate’).You can phone us if you are not sure whether you are eligible for the zone, dependent spouse or special tax offset. See ‘More information for payees’ below.

It is against the law to claim tax offsets from more than one payer at the same time.

question 11a – Do you have an accumulated higher Education loan programme (hElp) debt?Answer YES if you have an accumulated HELP debt.Answer NO if you do not have an accumulated HELP debt, or you have repaid all your HELP debt.If you had a Higher Education Contribution Scheme (HECS) debt it became an accumulated HELP debt on 1 June 2006.HELP – The Higher Education Loan Programme (HELP) was introduced on1 January 2005, replacing the HECS. HELP consists of:•HECS-HELP–foreligiblestudentsenrolledinCommonwealth

supported places. A HECS-HELP loan will cover all or part of their student contribution.•FEE-HELP–foreligiblefee-payingstudentsenrolledataneligible

higher education provider. FEE-HELP provides students with a loan to cover up to the full amount of their tuition fees.•OS-HELP–foreligibleCommonwealthsupportedstudentswho

wish to study overseas. OS-HELP provides students with a loan to cover expenses such as accommodation and travel.

If the Australian Government lends you money under any of these schemes you will have a HELP debt.repaying your hElp debt You must start repaying your debt when your repayment income is above the minimum threshold. The minimum threshold for 2006–07 is $38,148 (or $728 a week). We will calculate your compulsory repayment for the year and include it in your income tax notice of assessment.If your annual income is likely to be above the minimum repayment threshold, your payer will regularly withhold additional amounts to cover any compulsory repayment that may be calculated.Do you have more than one job and a hElp debt? If your payments from all jobs add up to more than the repayment threshold for the income year, you will have a compulsory repayment included in your next income tax notice of assessment. You can ask one or more of your payers to withhold additional amounts to cover your compulsory repayment.question 11b – Do you have an accumulated Financial Supplement debt?Answer YES at (b) if you have an accumulated Financial Supplement debt.The Student Financial Supplement Scheme (SFSS) is a voluntary loan scheme for tertiary students to help cover their expenses while they study. Inthefifthyearaftertheloanistakenout,itbecomesanaccu-mulatedFinancialSupplementdebt,tobecollectedbytheTaxOffice.If your annual income is likely to be above the minimum repayment threshold, your payer will regularly withhold additional amounts to cover your anticipated compulsory repayment. The minimum Financial Supp lement repayment threshold for 2007–08 is $39,824 or $765 a week.When you have repaid all of your HELP or Financial Supplement debt, you must complete a Withholding declaration and answer NO at this question.

For more information about hElp and Financial Supplement debts, please contact us.

See “More information for payees’ below.

Make sure you have answered all the questions in section A and have signed and dated the declaration. Give your

completed declaration to your payer.

MorE InForMATIon For pAYEES

If you need more information about TFns or how to complete the Tax File number declaration, you can:

•visitourwebsiteatwww.ato.gov.au •phone132861between8.00am&6.00pm,Mon–Fri,or •obtainafaxbyphoning132860.

TrusteeSt Andrew’s Superannuation Services Pty LtdABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950

FundSt Andrew’s Superannuation Services FundABN13 400 513 379 SFN440806

AdministratorSt Andrew’s Life Insurance Pty LtdABN 98 105 176 243 AFSL 281731

Contact usTelephone 1300 780 553Facsimile 1300 780 573

GPO Box 2979 Melbourne, VIC 3001

19 D

EC 2

008

SuperChoiceSuperannuation Plan Pension Plan

Product Disclosure Statement Date Issued 30 October 2008 Trustee: St Andrew’s Superannuation Services Pty Ltd

SuperChoice Superannuation Plan and Pension Plan Product Disclosure Statement General InformationDate of issueThe SuperChoice Superannuation Plan and Pension Plan Product Disclosure Statement (PDS) was issued on 30 October 2008 by St Andrew’s Superannuation Services Pty Ltd, the SuperChoice trustee.

ContributionsDefinitionsThroughout this PDS, the Application Forms and other attached forms:

• ‘St Andrew’s Superannuation Services Fund’ SFN 440806 RSE Registration No. R1056631 is referred to as ‘SuperChoice’.

• ‘St Andrew’s Superannuation Services Pty Ltd’ ABN 75 077 207 240 AFSL 297033 RSE licence No. L0002950 is referred to as ‘St Andrew’s’, ‘we’, ‘us’, ‘our’, or ‘Trustee’.

• ‘St Andrew’s Life Insurance Pty Ltd’ ABN 98 105 176 243 AFSL 281731 is referred to as ‘the Administrator’.

• ‘I’, ‘you’, ‘me’ or ‘your’ refers to a potential member or member of SuperChoice.

• ‘SuperChoice – Superannuation Plan’ is referred to as ‘the Superannuation Plan’.

• ‘SuperChoice – Pension Plan’ – is referred to as ‘the Pension Plan’.

• ‘SuperChoice – Superannuation Plan’ and ‘SuperChoice – Pension Plan’ are jointly referred to as ‘SuperChoice’.

• St Andrew’s – SuperChoice Superannuation and Pension Product Disclosure Statement’ is referred to as ‘the PDS’.

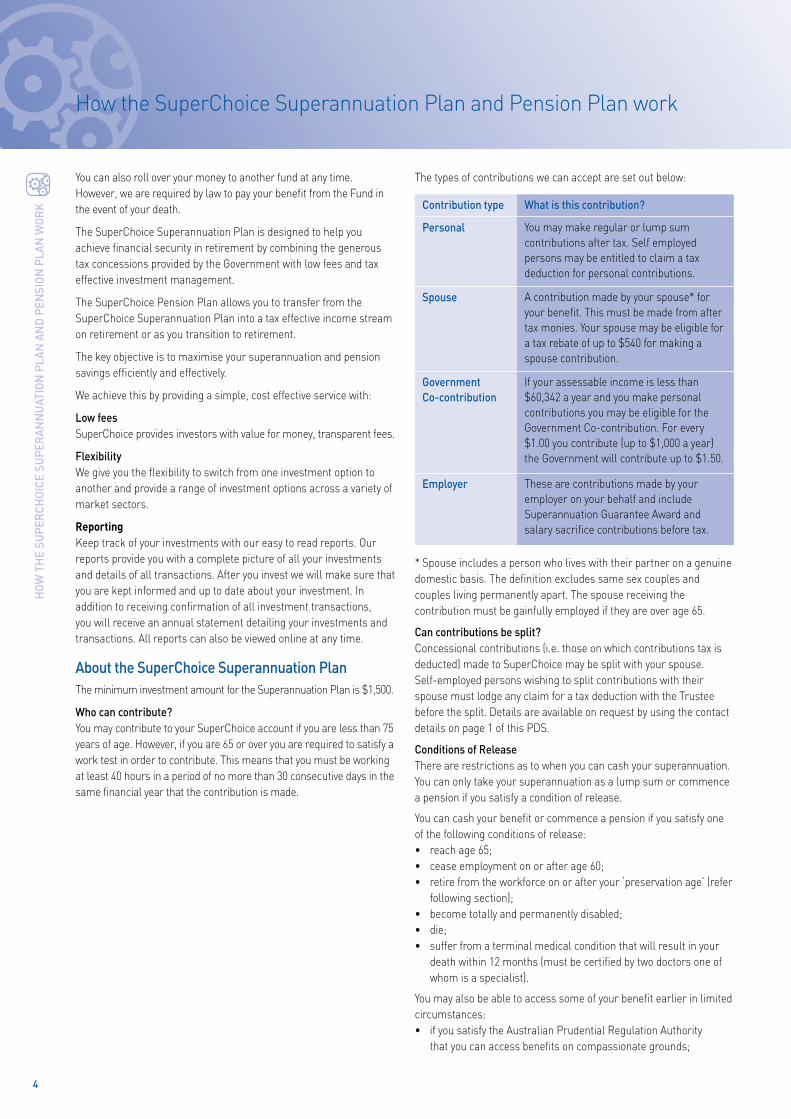

Information about SuperChoiceSuperChoice is a public offer superannuation fund. Residents of Australia are eligible to apply for the SuperChoice products in this PDS (subject to certain restrictions described on page 4 of this PDS).

TrusteeSt Andrew’s Superannuation Services Pty Ltd ABN 75 077 207 240 AFSL 297033 RSE Licence No. L0002950

FundSt Andrew’s Superannuation Services Fund ABN 13 400 513 379 SFN 440806 RSE Registration No. R1056631

AdministratorSt Andrew’s Life Insurance Pty Ltd ABN 98 105 176 243 AFSL 281731

Choosing a fundThe PDS explains the main features of SuperChoice, a regulated complying superannuation fund constituted by a trust deed as amended from time to time. The PDS will help you to compare SuperChoice with other superannuation funds to decide if it meets your needs. Please read the PDS carefully before making your decision. This PDS contains general information only. It does not take into account your individual objectives, financial situation or needs. You should not base your decision to invest in SuperChoice solely on the information in this PDS. You should consider SuperChoice’s suitability in view of your financial position, objectives and needs and you may want to seek advice before making an investment decision. You can ask your Financial Adviser to explain anything you don’t understand, or contact Client Services 1300 780 553.

The benefits and risks of SuperChoiceSuperChoice allows you to save for your retirement and/or receive a pension from a low cost, tax effective environment in a way that suits you. You can choose the investment portfolio that best suits your needs and attitude to risk. However, depending on the level of investment returns earned by SuperChoice and the charges, you may get back less than what you paid in, particularly if you exit SuperChoice within a few years of joining and or choose a high risk investment portfolio.

Investing in SuperChoice When you decide to invest in SuperChoice you must complete the application form and various other forms (attached to this PDS) to apply to become a member of SuperChoice. The offer to which this PDS relates is available to

persons receiving this PDS in Australia (either electronically or otherwise). The Trustee will notify you on acceptance of your application. We hold the investments on behalf of SuperChoice members and send information (including investment performance) and benefit statements to members annually. Members can request additional information that is reasonably necessary to understand SuperChoice’s financial condition and how it is being managed. A fee may be charged, depending on the type of information requested. All requests for information or assistance can be made by using the contact details shown on page 1 of this PDS.

Our responsibilities to youThe SuperChoice trust deed contains a number of provisions relating to the rights, terms, conditions and obligations imposed on both us, as the trustee, and you as a member. We can amend the trust deed, subject to limitations in it, superannuation law and trust law.

Is this PDS current?The information in this PDS is current at 30 October 2008. Information relating to SuperChoice that is not materially adverse may change from time to time. This information may be updated and made available to you on our website at www.standrewsaus.com.au or by contacting us on 1300 780 553. A paper copy of any updated information is available free of charge upon request.

Who looks after SuperChoice?The Trustee is responsible for the management and operation of SuperChoice in accordance with its trust deed and rules, the common law and the applicable Federal and State laws. In administering and investing the assets of SuperChoice, the Trustee uses other service providers including our related companies.

Relationships and associationsWe invest the assets of SuperChoice in a superannuation life insurance policy issued by the Administrator who is a registered life insurance company and an Australian Financial Services Licensee. The Administrator then invests the assets in the various portfolios described on pages 12–15 of this PDS and administers SuperChoice. We pay the Administrator to administer SuperChoice on our behalf (pages 16–18 of this PDS describes the administration fees charged).

Neither the Trustee nor the Administrator is an authorised deposit taking institution. Both the Trustee and the Administrator are wholly owned subsidiaries of St Andrew’s Australia Pty Ltd ABN 96 105 176 234 (‘SAA’) which is a subsidiary of HBOS Australia Pty Ltd ABN 50 070 002 587 (‘HBOSA’). Bank of Western Australia Limited (‘BankWest’) ABN 22 050 494 454 AFSL 236872 is a related company of SAA. All of these companies have the same ultimate owner HBOS plc.

On 18 September 2008, Lloyds TSB and HBOS plc announced that they have reached agreement on the terms of a recommended acquisition by Lloyds TSB of HBOS plc. The Boards of HBOS plc and Lloyds TSB believe that the acquisition is a compelling business combination which offers substantial benefits for shareholders and customers.

The Boards will now seek shareholder approval. The acquisition is subject to regulatory and shareholder approval which is expected to be completed by the end of 2008 to early 2009.

On 8 October 2008, The Commonwealth Bank of Australia (the Group) has acquired the Bank of Western Australia Limited (BankWest) and St Andrew’s Australia Pty Ltd (St Andrew’s) through the execution of a sale and purchase agreement with UK based HBOS plc.

The purchase is conditional on the receipt of all necessary competition, regulatory and government approvals – and will be completed following receipt of those approvals.

Investments in SuperChoice do not represent a deposit with or a liability of BankWest or any other member of the HBOSA group of companies in Australia or overseas (other than the Trustee). Your investment can be subject to investment risk, including possible delays in repayment and loss of income and principal. No member of the HBOSA group of companies in Australia (including BankWest) or overseas guarantees SuperChoice’s capital value or performance (apart from the guarantee given by the Trustee for the Simplicity – Capital Guaranteed Fund). None of these companies (other than the Trustee) is responsible for any statement contained in the PDS.

RACV plays no role in the issue or administration of interests in SuperChoice and only distributes the SuperChoice PDS.

1

Conten

ts and

ContaCt d

etails

talk to us 1

Welcome to st andrew’s australia 2

What superChoice can offer you – overview 3

How the superChoice superannuation Plan and Pension Plan work 4

investing in superChoice 9

superChoice investment options 12

Fees and other Costs 16

taxation 19

other information 22

application Forms 25

talk to usWe are happy to provide you with as much information as you need to fully understand how SuperChoice works. You can call our Client Services team on 1300 780 553 between 8.30am and 7.00pm (EST) Monday to Friday and we will be pleased to answer your questions and provide information.

Fax on 1300 780 573

Write to Client Services, St Andrew’s GPO Box 2979 Melbourne, VIC 3001

Log on to SuperChoice Online www.standrewsaus.com.au/super

Contents and Contact Details

2

Wel

Com

e to

st

and

reW

’s a

ust

ral

ia

st andrew’s australiaSt Andrew’s Australia Pty Ltd (“St Andrew’s Australia”) began trading in 1998 providing customer credit insurance to Australians via various business partners. In 2004, St Andrew’s Australia opened a new life insurance company, St Andrew’s Life Insurance Pty Ltd, to offer clients a range of insurance, superannuation and investment solutions.

St Andrew’s Australia, through its subsidiary companies, supports its clients on their journey to wealth, offers quality financial advice and delivers simple, value-for-money financial products and services.