Study Support Šárka Vilamová -...

49

VŠB – TECHNICAL UNIVERSITY OF OSTRAVA FACULTY OF METALLURGY AND MATERIAL ENGINEERING Strategic Management Study Support Šárka Vilamová Ostrava 2016

Transcript of Study Support Šárka Vilamová -...

VŠB – TECHNICAL UNIVERSITY OF OSTRAVA

FACULTY OF METALLURGY AND MATERIAL ENGINEERING

Strategic Management

Study Support

Šárka Vilamová

Ostrava 2016

1

Title: Strategic Management

Code:

Author: doc. Ing. Šárka Vilamová, Ph.D.

Edition: first, 2016

Number of pages:

Academic materials for the Economics and Management of Industrial Systems study

programme at the Faculty of Metallurgy and Materials Engineering.

Proofreading has not been performed.

Execution: VŠB - Technical University of Ostrava

2

TABLE OF CONTENTS

TABLE OF CONTENTS ...................................................................... 2

STUDY INSTRUCTIONS .................................................................... 4

1. THE PRINCIPLES OF STRATEGIC CORPORATE MANAGEMENT ...... 5

1.1 Introduction into the topic .......................................................................................................... 5

1.2 The essence of strategic corporate management ....................................................................... 5

1.3 Strategic management ................................................................................................................ 7

1.4 New trends in the development of strategic activities ............................................................... 8

2 MISSION AND STRATEGIC OBJECTIVES OF COMPANY ............... 13

2.1 Defining the company mission .................................................................................................. 13

2.2 Company Strategy ..................................................................................................................... 14

3 STRATEGIC ANALYSIS OF THE COMPANY SURROUNDING ENVIRONMENT ............................................................................ 20

3.1 Strategic analysis ....................................................................................................................... 20

3.2 Structure of company surrounding environment ..................................................................... 22

3.3 Pest analysis .............................................................................................................................. 23

4 ANALYSIS OF THE COMPETITIVE SURROUNDING ENVIRONMENT OF THE COMPANY ........................................................................ 27

4.1 Porter's five forces model ......................................................................................................... 27

4.2 Life cycle analysis of the field .................................................................................................... 29

4.3 Competing group analysis ......................................................................................................... 30

4.4. Future development Scenarios of the company surrounding environment ............................. 30

5 ANALYSIS OF THE COMPANY INTERNAL POTENTIAL ................. 34

5.1 Analysis of key competences ..................................................................................................... 34

5.2. Analysis of the value chain ........................................................................................................ 34

5.3. Benchmarking ............................................................................................................................ 36

6 DETERMINATION OF THE COMPANY STRATEGIC POSITION ...... 39

6.1 Determination of the company strategic position .................................................................... 39

6.2. Company Situation analysis ....................................................................................................... 40

6.3. SWOT analysis ........................................................................................................................... 40

7 STRATEGIC CONTROL AND STRATEGIC AUDIT .......................... 45

7.1 Strategic control ........................................................................................................................ 45

7.2 Strategic audit of the company ................................................................................................. 45

7.3 Controlling a strategic management ......................................................................................... 46

3

4

STUDY INSTRUCTIONS

Strategic management

You have received a study package for the course of Strategic Management containing the

integrated university mimeographed for the combined study, including the study instructions.

Course objective and learning outputs

The objective of this course is to become familiar with the principles of the creation,

execution and monitoring of the mission, strategic objectives and strategies at different levels of

strategic management. The graduates will be able to apply the main methods of strategic analysis

and strategic decision-making.

The course is focused on understanding the essence of strategic thinking, strategic behaviour

of entrepreneurial entities and on mastering selected methods and approaches of strategic analysis.

It introduces strategies at various levels of corporate management and establishes the foundation for

their successful formulation and implementation.

After studying the course, students should be able to:

characterize the basic corporate strategies and the principles of strategic corporate management

formulate the basic tools of strategic analysis of company

use their knowledge to decide on the appropriateness of using a specific analysis of the company

apply their theoretical knowledge to make suggestions to improve the strategic position of the company

Who is the course intended for

The course is included in the master's study of the fields of Economics and Management in

Industry and Quality Management of the program of study of Economics and Management of

Industrial Systems, but it can be studied by any other interested students from another field of study,

if they meet the required prerequisites.

The study support is divided into chapters that correspond to the logical structure of the

studied material, but they are not equally comprehensive. The estimated time to study the chapters

may vary considerably, because the large chapters are further divided into numbered sub-chapters

and they correspond to the structure described below.

Communication with the teacher

Students will be able to make use of consultations on selected areas of the discussed subject

matter beyond the lectures. Student will receive more information about the terms of consultations

at the beginning of the semester. If necessary, the teacher can be contacted at this phone no.: 596

994 400 or by email:[email protected].

5

1. THE PRINCIPLES OF STRATEGIC CORPORATE MANAGEMENT

Study time

The approximate total time recommended to study the following chapter is app. 3 hours.

Objective

After studying this chapter you will be able to:

define the principles of management and in particular the principles of strategic corporate management

understand the essence of strategic management, its importance and role in the company

describe the most important aspects and attributes of strategy and strategic management.

Explication

1.1 INTRODUCTION INTO THE TOPIC

At the beginning, it is necessary to become familiar with the terms to be used in this chapter.

The technical terms of "control" and "management" are often used interchangeably in practice.

While management is dealing exclusively with the control at the level of companies, institutions,

interest groups and individuals, the term "control" can be perceived in the broader sense (it can

mean controlling material systems, regulating mixed systems or influencing social systems) or in the

narrower sense, where the term "control" is semantically identical to the term of "management"

[36].

Strategic management is a kind of management and this is the right place to recall its

definition and the general principles of management. The purpose of management is to define and

achieve the objectives of management. The essence of success and of management and a manager is

based on how successful the manager is in the execution of both of these activities.

1.2 THE ESSENCE OF STRATEGIC CORPORATE MANAGEMENT

The dynamic development of strategic management dates back to the early 1980s, when the

idea that the future success of the company depends not only on the surrounding environment but

also on the quality of human resources, technologies and the key capabilities of the organization

began gaining ground. Keřkovský and Vykypěl define strategic management as: "Activities aimed at

maintaining long-term harmony between the mission of the company, its long-term objectives and

the available resources, as well as between the company and the environment in which it exists." [21]

6

Vacík and Šulák have presented the following definition of strategic management: "the art

and science of how to formulate, implement, and evaluate such decisions in all the functional areas of

the business entity that will ensure the achievement of the given objectives". [35]

According to this definition, the strategic management process is divided into the stages of

strategy formulation, strategy implementation, and the subsequent evaluation.

The strategic management process is a never-ending process, where the strategic goals of

the company are used to design, implement and evaluate the strategies, based on which the

strategic objectives and visions of the company are updated. [31]

Strategic management is associated with decision-making and long-term issues within the

company. It establishes a kind of framework for tactical and operational planning, which is inherently

of short-term nature. As a rule, the decisions or plans of short-term nature should not be in conflict

with the concept of strategic management. It is also focused on identifying the opportunities that the

company is able to use, while taking advantage of its resources, and to create a competitive

advantage. This is an advantage which allows the company to reach an exclusive position in certain

activity above its competitors.

Strategy is also defined with reference to the vision and mission of the organization (see

below). For example, Z. Souček states that the strategy of the organization expresses its mission and

vision (i.e. its future appearance), strategic objectives and strategic operations (i.e. activities ensuring

the mission, the vision and the strategic objectives are met). [33]

Similarly, M. Drdla and K. Rais state that strategy should be based on the company vision,

while the vision is understood as the ideas of the company owners. [3]

The interrelationship between vision and strategy is addressed by J. P. Kotter, see the

schemes. [25]

He also deals with vision in a more detailed way, and according to him, it "represents certain

image of the future with a more or less accurate commentary explaining why people should try to

create that future." [25]

He continues saying that a good vision serves three purposes. Firstly, according to him, it

clarifies the general direction and summarizes hundreds and thousands of more detailed decisions in

a simple way; secondly, it motivates people to step in the right direction, and thirdly, it helps to

coordinate the conduct of various (even many) people. [25]

7

Figure 1: Relationships among vision, strategies, plans and budgets [25, p. 77]

1.3 STRATEGIC MANAGEMENT

Strategic management itself is not a scientific branch or a discipline. It is rather an angle on

the organization, a possibility of thinking about the mission of the organization. It combines

conceptual and long-term management with the objective of winning over the others. From the

perspective of an enterprise, it is focused on getting a comparative advantage. [5]

The understanding of strategic management has changed over time. While in the 1970s and

1980s, strategic management was essentially equal to strategic planning1, later, there was a

significant qualitative shift in thinking, where strategic planning and decision-making have become

only the individual parts of strategic management. [39]

Strategic management can be defined in many different ways. One of the most frequently

used is the description of the process itself, i.e., what activities are included in strategic

management. According to J. Veber, for example, strategic management "represents a set of

activities that include a research of the market conditions, the needs and wishes of customers, an

identification of the strengths and weaknesses, a specification of the social, political and legislative

conditions, and a determination of the availability of resources that can create either opportunities

or threats, while their purpose is obtaining the information necessary for the formation of long-term

plans (objectives) with regards of the functioning of the organization." [37]

1 Even earlier, around the 1960s, it was associated with long-term planning

8

The second group of the possible definitions of strategic management is rather focused on

what the objective of strategic management should be, what is to be accomplished by using it. E.g.,

Z. Souček understands strategic management as "a process of the creation and implementation of

development projects that are crucial for the development of the company, they are intended to

develop specific strengths or future potential and to achieve global competitiveness." [33]

Another meaningful way how to define strategic management is a definition based on

contradictions. Strategic management is therefore compared with operational management. [21], [2]

A vast majority of authors uses a combination of these opinions to define strategic

management. E.g., Z. Souček also addresses the contradictions when stating that, while strategic

management is focused on creating a potential, the follow-up operational management uses only the

existing potential to ensure the operation and partly also the development of the organizational. [33]

1.4 NEW TRENDS IN THE DEVELOPMENT OF STRATEGIC ACTIVITIES

Although no new major approaches and methods have been introduced in relation to

strategic activities in recent years, the interest in these activities is relentless, and they are more and

more often associated with innovative activities.

The latest theoretical and practical concept of strategic activities is quite broad, and the topic

of strategic activities is viewed in very different ways. Their authors often deal with the relationships

between strategic management or the adopted strategy and various aspects related to the

organization and its surrounding environment. For example, V. Isoherranen and P. Kess study the

dependencies between the strategy focus and the gained market share. Using the example of the

international organization of Nokia, they show that the market share has increased due to the

transition from the technological and partly product orientation to customer orientation. [17]

Whether and how the adopted strategy influences the possibility of tax cuts is dealt with by

D.M. Higgins, T.C. Omer and J.D. Phillips, who divide organizations according to the adopted strategy

into "opportunity finders" ("prospectors"), "position defenders" ("defenders") and "analyzers" and

they state that the organizations with a strategy focused on minimizing and reducing costs are less

successful in evading taxes. [11]

M. A. Hitt, K. T. Haynes and R. Serpa are looking for an answer to the question of why more

than 50% of decisions lead to the failure of the organization. They especially emphasize the necessity

of strategy flexibility. According to the authors, it is necessary for organizations to be proactive, to

create effective human capital, but they also state that managers-strategists should be unselfish and

should stress ethics. [12]

R. S. Graber deals with the qualities of a manager-strategist, and he is looking for similarities

between the strategy while playing chess and the strategy of the organization. He believes that

playing chess can affect the performance of the player in the organization and his future career; it

teaches him to think in the longer horizon, learn from the mistakes, be patient, accept certain level of

risk, be able to give something up and still formulate an ongoing plan. [6]

9

The diversity of strategic activities is also affecting countries in which various surveys have

been carried out dealing specifically with the issue of strategic management, respectively strategy in

the organization. For example, S. Parthasarathy has applied Porter's five forces model in India, while

in Malaysia, it has been investigated what the strategy has been adopted by the most capable

organization focused on export. [29], [20]

Many authors deal with innovations in various ways. For example, K. Kyläheiko et al.

understand innovation as a development of new products, as one of the possible strategies leading

to the growth of the organization. [26]

Table 1: Strategic management development stages [27, p. 26]

Main idea

Objective

Methods

1960s Classical school

A manager who makes decisions is at the head

Creation of a SWOT analysis

Creation of a Ansoff matrix

1970s Process approach

Interconnection of the individual departments

and mutual cooperation

Product and geographic diversification

BCG matrix

1980s Evolution approach

Evolution approach related to the

competition (the market thinks instead

of the managers)

Get closer to the customer; improve the quality of production

Quality management models; Porter's five

forces model

1990s System approach

Extending strategic management by

including personal approach

Increase production efficiency

Creation of internal corporate cultures

Present time Modern approach

Unification of the concept of strategic management and

strategy

Increase the practical application of the

theoretical concept Strategic research

T Mallya presents a division of the development stages of strategic management. It is based

on a chronological distinction of the individual stages of strategic activities, and the first four stages

are always related to one decade, while the last one - present - includes more years. [27]

T. Mallya himself summarizes all the stages of the development in the above-presented

summary table 1. [27]

10

Summary of terms

Strategic management can be briefly defined as the activities necessary to meet the strategic

objectives of the company.

Strategic management process is divided into the stages of strategy formulation, strategy

implementation and its subsequent evaluation.

Strategic control process is a never ending process, in which the strategic objectives of the

company are used to design, implement and evaluate the strategies, based on which the strategic

objectives and visions of the company are updated.

Strategic management creates a framework for tactical and operational planning, which is

inherently of short-term nature.

Questions

1. What does the statement saying that the process of strategic management is a

never-ending process mean?

2. Define the meaning and the role of strategic management in a company.

3. Try to define the main differences between general and strategic management.

4. Describe the development stages of strategic management and identify the main

ideas, methods and objectives of each stage.

5. Try to define the new trends of the development of strategic activities of firms with

specific examples from practice.

Reference sources

[1] Crainer, S. Moderní management: základní myšlenkové směry. Praha: Management

Press, 2000.

[2] DEDOUCHOVÁ, M. Strategie podniku. 1. vydání. Praha: C. H. Beck, 2001. ISBN: 80-

7179-603-4.

[3] DRDLA, M., RAIS, K. Reengineering : Řízení změn ve firmě. 1. vydání. Praha: Computer

Press, 2001. ISBN 80-7226-411-7.

[4] FREEMAN, R. E. Strategic management: A stakeholder approach. Boston: Harper

Collins, 1984.

[5] GOLDSMITH, A. A. Making managers more effective : Application of strategic

management. [online]. 1995 [cit. 2013-02-02]. Dostupný na WWW:

<http://www.usaid.gov/our_work/democracy_and_governance/publications/ipc/wp

-9.pdf>

11

[6] GRABER, R. S. Business Lessons from Chess: A Discussion of Parallels between Chess

Strategy and Business Strategy, and How Chess Can Have Applications for Business

Education. Academy of Educational Leadership Journal. [online]. 2009, vol. 13, no. 1,

s. 79-85. ISSN 1095-6328. [cit. 2013-02-16]. Dostupný na WWW:

<http://search.proquest.com/docview/214231507/fulltext?source=fedsrch&accounti

d=16531>

[7] GRANT, R. M. Contemporary strategy analysis. 7th ed. Chichester: John Wiley & Sons,

2010. ISBN 978-0-470-74710-0.

[8] GRASSEOVÁ, M., DUBEC, R., ŘEHÁK, D. Analýza v rukou manažera. 33

nejpoužívanějších metod strategického řízení. Praha: Computer Press, 2010. ISBN

978-80-251-2621-9.

[9] HANZELKOVÁ, A., KEŘKOVSKÝ, M, ODEHNALOVÁ, D. a VYKYPĚL, O. Strategický

marketing, Teorie pro praxi, 1. vydání. Praha: C. H. Beck, 2009, ISBN 978-80-7400-

120-8.

[10] HARRISON, J. S., JOHN, C. H. Foundations in Strategic Management. South-Western

Thomson Corporation, 2004. ISBN 0-324-25917-4.

[11] HIGGINS, D. M., OMER, T. C., PHILLIPS, J. D. Does a Firm’s Business Strategy Influence

its Level of Tax Avoidance? SSRN Working Paper Series. [online]. Rochester: JATA

Conference. 2011, [cit. 2013-01-21]. Dostupný na WWW:

<http://search.proquest.com/docview/854451905/fulltext?source=fedsrch&accounti

d=16531>

[12] HITT, M. A., IRELAND, R. D., HOSKISSON, R. E. Strategic Management:

Competitiveness and Globalization (concepts and cases). Mason: Thomson Higher

Education, 2007. ISBN 978-0-324-31694-0.

[13] HOLMAN R. Ekonomie. 2. vydání. Praha: C. H. Beck. 2011. ISBN: 80-7179-387-6.

[14] HORÁKOVÁ, H. Strategický marketing. 2. rozš. a aktual. vyd. Praha: Grada Publishing,

2003. ISBN 80-247-0447-1.

[15] CHARVÁT, J. Firemní strategie pro praxi. Praha: Grada, 2006. ISBN 80-247-1389-6.

[16] ISOHERRANEN, V., KESS, P. Analysis of Strategy Focus vs. Market Share in the Mobile

Phone Case Business. Technology and Investment. [online]. 2011, vol. 2, no. 2, s. 134-

141. ISSN 2150-4059. [cit. 2012-12-20]. Dostupný na WWW:

<http://search.proquest.com/docview/874652761>

[17] JAKUBÍKOVÁ, D. Strategický marketing. Praha: Grada Publishing. 2005. ISBN 80-245-

0902-4.

[18] JOHNSON, G., SCHOLES, K. Exploring corporate strategy. 3rd edition. New York:

Prentice hall, 2008. ISBN 978-0-273-71192-6.

[19] KEŘKOVSKÝ, M., VYKYPĚL, O. Strategické řízení. Teorie pro praxi. 2. vydání. Praha: C.

H. Beck. 2006. ISBN: 80-7179-453-8.

[20] KIPLEY, D. Stakeholder Identification and Analysis using the Multi-Rater Metod. An

alternative metholodogy. Saarbrücken: VDM Verlag Dr. Müller Aktiengesellschaft &

Co KG, 2009. ISBN 978-3-639-17321-5.

[21] KOŠŤAN, P., ŠULEŘ, O. Firemní strategie: plánování a realizace. Praha: Computer

Press, 2002. ISBN 80-7226-657-8.

[22] KOTLER, P. a kol. Moderní marketing. Přel. J. Langerová a V. Nový. 1. vyd. Praha:

Grada Publishing, 2007. ISBN 978-80-247-1545-2.

12

[23] MALLYA, T. Základy strategického řízení a rozhodování. 1. vyd. Praha: Grada

Publishing, 2007. ISBN 978-80-247-1911-5.

[24] MEFFERT, H. Marketing Management. Přel. G. Tomek a V. Vávrová. Praha: Grada

Publishing, 1996. ISBN 80-7169-329-4.

[25] PARTHASARATHY, S. Business Strategy. Financial Management. [online]. 2011,

červen, s. 32-33. ISSN 1471-9185. [cit. 2013-02-03]. Dostupný na WWW:

<http://search.proquest.com/docview/522843459>

[26] SANDER, G., BAUER, E. Strategieentwicklung kurz und klar: Das Handbuch für Non-

Profit-Organisationen. Bern: Haupt, 2006. ISBN 978-3-258-07002-5.

[27] SEDLÁČKOVÁ, H., BUCHTA, K. Strategická analýza. Praha: C.H. Beck, 2006. ISBN 80-

7179-367-1.

[28] SIMON, W. Kursbuch Strategieentwicklung: Analyse – Planung – Umsetzung.

München: Redline Wirtschaft, 2008. ISBN 978-3-636-01542-6.

[29] SOUČEK, Z. Úspěšné zavádění strategického řízení firmy. Praha: Professional

Publishing, 2003. ISBN 80-86419-47-9.

[30] ŠMÍDA, F. Strategie v podnikové praxi. Praha: Professional Publishing, 2003. ISBN 80-

86419-41-X.

[31] VACÍK, E., ŠULÁK, M. Strategický management. Plzeň: Západočeská univerzita, 2001.

ISBN 80-7082-728- 9.

[32] VÁGNER, I. Systém managementu. Brno: Masarykova univerzita, 2006. ISBN 80-210-

3972-8.

[33] VEBER, J. Management: základy, prosperita, globalizace. Praha: Management Press,

2000. ISBN 8072610295.

[34] WIEBES, E., BAAIJ, M., KEIBEK, B., WITTEVEEN, P. The Craft of Strategy Formation :

Translating Business Issues into Actionable Strategies. 1. vyd. Chichester: John Wiley

& Sons, 2007. ISBN 978-0-470-51859-5.

[35] WRIGHT, G., NEMEC, J. Management veřejné správy: Teorie a praxe – zkušenosti

z transformace veřejné správy ze zemí střední a východní Evropy. Praha: Ekopress,

2003. ISBN 80-86119-70-X.

[36] ZELENÝ, M. Cesty k úspěchu: Trvalé hodnoty soustavy Baťa. Zlín: Čintámani, 2005.

ISBN 80-239-4969-1.

13

2 MISSION AND STRATEGIC OBJECTIVES OF

COMPANY

Study time

The approximate total time recommended to study the following chapter is app. 2 hours.

Objective

After studying this chapter you will be able to:

Define the mission and objectives of a company,

Describe the method used to determine the strategic objectives of organization,

Understand why the existence of a mission is important for every company.

Explication

2.1 DEFINING THE COMPANY MISSION

The mission of the company is the reason of existence of the company on the market.

Defining the company mission is a key task of the owners, respectively of the management of the

company. This mission usually defines the range of the company and clearly informs about the values

the company adheres to and respects.

A term similar to mission is the corporate vision, which usually affects certain development

direction of the company for the period of 10 to 20 years.

The purpose of the mission is to tell those who are involved in strategic decisions about the

general basic rules the organization has issued for itself. The mission should be broadly formulated

and should act as a permanent declaration of intent; it's basically a work document - and to be

effective, it has to be both brief and clear.

The mission is a public document. Its creation and subsequent publication should provide all

employees with a clear idea of the importance of the focus of the company business activities.

A well formulated mission of the company is inspiring. It must be sufficiently specific, and yet

also sufficiently general to leave room for people to exercise their own initiative.

The mission also plays an important role in case of the company image. By publishing the

mission, the management creates an impression of credibility of the company. It expresses how the

firm should be understood by the public.

Each company (organization, institution) has been established and exists to fulfil its specific

mission - production or provision of services to its customers. This mission of the company

14

corresponds to the basic ideas of the founders of the company with regards to the aspects of what

the subject of business will be, who the customers of the firm will be, what needs it will meet, and

what products and services the company will use to meet the customers' needs. This kind of mission

fulfils several functions at the same time:

It expresses the basic strategic intention of the company owners and the top management,

while the company strategy follows its mission and they specify it in concrete areas.

The mission has strong external information significance, because it declares the company

mission towards the public and, in this way, it exposes the company to public control. As a

result of that, the perception of the company among the public is usually improved. A

publicly declared mission provides the essential information necessary to form an opinion

about the company among: future shareholders, employees, suppliers, and customers. The

owners and the top management of the company formulate the mission to give the public

clear signals of its existence, position and its long-term business plans.

The company mission is the basic standard for the behaviour of the management as well as

the ordinary employees. In developed countries, it is quite common that employees are

informed about the company mission in a very detailed manner.

The mission actually expresses the widest and the highest level of the objectives of the

organization.

2.2 COMPANY STRATEGY

The strategy of the future conduct of the company answers the question of how to achieve

the defined objectives according to the vision specified by the company management. If the

management of the company focus their attention either exclusively or largely on operational

planning, it leads only to a short-term success. In the longer term, it will reveal the inadequate

concept and the performance of the company stagnates as a result of that. It was concisely stated by

Henry Mintzberg, who said: "If you do not have a vision but only formal plans, then during every

unexpected change of the environment it seems to you that everything is collapsing in your hands."

[19]

According to Dedouchová, strategy can be understood according to the traditional and

modern definition. [2]

1. The traditional definition understands strategy as: "A document in which the long-

term objectives of the company are determined, as well as the course of operations

and the allocation of the resources to meet these objectives."

2. The modern definition understands strategy as readiness for the future. "The strategy

defines the long-term objectives of the company, the course of the individual strategic

operations, and the deployment of the company resources necessary to meet the

objectives in such a way to make sure this strategy is based on the company needs,

15

taking into account the changes of its resources and capabilities, while responding to

the changes in the surrounding environment of the company." [ 2]

The above presented definitions clearly show that the latter one concisely and more

accurately describes strategy in such a way, in which it should be understood by companies in the

times of dynamic and turbulent changes.

Figure 2: Company strategy in its environment [16, s. 31]

The scheme illustrates the process of the creation of a strategic company plan. It is based on

an analysis of the factors having impact on the company. Taking into account these factors, the

management then defines the mission and objectives of the company (mostly in accordance with the

"SMART" criteria - see below) and subsequently the actual strategy, which is continuously updated

during the changes of the above mentioned factors.

The ultimate objectives of a vast majority of companies include profitability and market share

growth of the company. Other frequent objectives of organizations include, for example, increasing

efficiency, product quality, customer satisfaction, etc.

The principles of the correct determination of objectives

Entrepreneurial activity is associated with continuous definitions of the business objectives.

Priority is given to the long-term – strategic - ones, which determine the direction of the whole

company, and they also decide about the medium and short-term objectives. The definition of these

objectives is very important for communication, understanding and comprehension of all the people

affected by them. That is why the determination of any particular objectives (excluding the strategic

objectives, which are general) should adhere to the principles of SMART.

SMART is a set of rules that determine how the objectives should be expressed so as to make

it possible to assess whether they have been achieved or not. These objectives should typically be:

16

S – specific and concrete, which means that they should be accurately described. If we are able to answer the question of what the subject and the problem are, then we have met this criterion of specificity.

M – measurable, quantifiable, allowing us to accurately express, monitor and check the course and the degree of fulfilment. Here, we can, for example, ask a question of how we know that we have been successful.

A – acceptable for all who are affected by them in any way.

R – realistic and feasible, in terms of all the resources needed. Let us ask a question whether we can ever achieve this objective with the means we have.

T – time-bound, i.e. setting the required deadline.

The aforementioned main objectives can be developed into individual sub-objectives

according to the principles of SMART. For example, an objective from the economic area focused on

increasing the turnover can be developed into a sub-objective dealing with "increase in sales based

on the improved delivery and payment terms, higher offered guarantees and better and faster

handling of eventual complaints" or "increase in the effectiveness of the functioning of the company

logistics system (transportation, handling, storage, packaging) resulting in cost reductions based on a

rational solution".

Summary of terms

The mission of the company is understood as the reason why the company exists on the

market. The mission can be defined as a concise expression of why the company exists, what it wants

to achieve and in what ways and by what means.

The purpose of the mission is to introduce the general basic rules the organization has issued

for itself to those who are involved in the strategic decisions.

Defining the mission of the company is a key task of the owners, respectively of the

management.

Corporate vision usually affects certain development direction of the company for the period

of 10 to 20 years.

The strategies of the future conduct of the company answer the question of how to achieve

the defined objectives according to the vision defined by the company management.

The strategy involves long-term objectives of the company, development of the individual

strategic operations and allocation of the company resources necessary to meet the objectives in

such a way to make sure this strategy is based on the company needs, takes into account the

changes in its resources and capabilities, while responding to the changes in the surrounding

environment of the company.

To define the objectives of your organization, you have to follow the principles of SMART.

17

Questions

1. Why is the existence of a mission so important for each company and for its

surroundings?

2. What should the company mission be like to be effective?

3. What does the SMART principle mean and what is it used for?

4. How would you define "measurability" of the defined strategic objectives of the

organization?

Reference sources

[1] Crainer, S. Moderní management: základní myšlenkové směry. Praha: Management

Press, 2000.

[2] DEDOUCHOVÁ, M. Strategie podniku. 1. vydání. Praha: C. H. Beck, 2001. ISBN: 80-

7179-603-4.

[3] DRDLA, M., RAIS, K. Reengineering : Řízení změn ve firmě. 1. vydání. Praha: Computer

Press, 2001. ISBN 80-7226-411-7.

[4] FREEMAN, R. E. Strategic management: A stakeholder approach. Boston: Harper

Collins, 1984.

[5] GOLDSMITH, A. A. Making managers more effective : Application of strategic

management. [online]. 1995 [cit. 2013-02-02]. Dostupný na WWW:

<http://www.usaid.gov/our_work/democracy_and_governance/publications/ipc/wp

-9.pdf>

[6] GRABER, R. S. Business Lessons from Chess: A Discussion of Parallels between Chess

Strategy and Business Strategy, and How Chess Can Have Applications for Business

Education. Academy of Educational Leadership Journal. [online]. 2009, vol. 13, no. 1,

s. 79-85. ISSN 1095-6328. [cit. 2013-02-16]. Dostupný na WWW:

<http://search.proquest.com/docview/214231507/fulltext?source=fedsrch&accounti

d=16531>

[7] GRANT, R. M. Contemporary strategy analysis. 7th ed. Chichester: John Wiley & Sons,

2010. ISBN 978-0-470-74710-0.

[8] GRASSEOVÁ, M., DUBEC, R., ŘEHÁK, D. Analýza v rukou manažera. 33

nejpoužívanějších metod strategického řízení. Praha: Computer Press, 2010. ISBN

978-80-251-2621-9.

[9] HANZELKOVÁ, A., KEŘKOVSKÝ, M, ODEHNALOVÁ, D. a VYKYPĚL, O. Strategický

marketing, Teorie pro praxi, 1. vydání. Praha: C. H. Beck, 2009, ISBN 978-80-7400-

120-8.

[10] HARRISON, J. S., JOHN, C. H. Foundations in Strategic Management. South-Western

Thomson Corporation, 2004. ISBN 0-324-25917-4.

[11] HIGGINS, D. M., OMER, T. C., PHILLIPS, J. D. Does a Firm’s Business Strategy Influence

its Level of Tax Avoidance? SSRN Working Paper Series. [online]. Rochester: JATA

Conference. 2011, [cit. 2013-01-21]. Dostupný na WWW:

18

<http://search.proquest.com/docview/854451905/fulltext?source=fedsrch&accounti

d=16531>

[12] HITT, M. A., HAYNES, K. T., SERPA, R. Strategic leadership for the 21st century.

Business Horizons. [online]. 2010, vol. 53, no. 5, s. 437-444. ISSN 0007-6813. [cit.

2013-01-16]. Dostupný na WWW:

<http://www.sciencedirect.com/science/article/pii/ S0007681310000662

[13] HITT, M. A., IRELAND, R. D., HOSKISSON, R. E. Strategic Management:

Competitiveness and Globalization (concepts and cases). Mason: Thomson Higher

Education, 2007. ISBN 978-0-324-31694-0.

[14] HOLMAN R. Ekonomie. 2. vydání. Praha: C. H. Beck. 2011. ISBN: 80-7179-387-6.

[15] HORÁKOVÁ, H. Strategický marketing. 2. rozš. a aktual. vyd. Praha: Grada Publishing,

2003. ISBN 80-247-0447-1.

[16] CHARVÁT, J. Firemní strategie pro praxi. Praha: Grada, 2006. ISBN 80-247-1389-6.

[17] ISOHERRANEN, V., KESS, P. Analysis of Strategy Focus vs. Market Share in the Mobile

Phone Case Business. Technology and Investment. [online]. 2011, vol. 2, no. 2, s. 134-

141. ISSN 2150-4059. [cit. 2012-12-20]. Dostupný na WWW:

<http://search.proquest.com/docview/874652761>

[18] JAKUBÍKOVÁ, D. Strategický marketing. Praha: Grada Publishing. 2005. ISBN 80-245-

0902-4.

[19] JOHNSON, G., SCHOLES, K. Cesty k úspěšnému podniku. Praha: Computer Press,

2000. ISBN 8072262203.

[20] JOHNSON, G., SCHOLES, K. Exploring corporate strategy. 3rd edition. New York:

Prentice hall, 2008. ISBN 978-0-273-71192-6.

[21] KEŘKOVSKÝ, M., VYKYPĚL, O. Strategické řízení. Teorie pro praxi. 2. vydání. Praha: C.

H. Beck. 2006. ISBN: 80-7179-453-8.

[22] KIPLEY, D. Stakeholder Identification and Analysis using the Multi-Rater Metod. An

alternative metholodogy. Saarbrücken: VDM Verlag Dr. Müller Aktiengesellschaft &

Co KG, 2009. ISBN 978-3-639-17321-5.

[23] KOŠŤAN, P., ŠULEŘ, O. Firemní strategie: plánování a realizace. Praha: Computer

Press, 2002. ISBN 80-7226-657-8.

[24] KOTLER, P. a kol. Moderní marketing. Přel. J. Langerová a V. Nový. 1. vyd. Praha:

Grada Publishing, 2007. ISBN 978-80-247-1545-2.

[25] KOTTER, J. P. Vedení procesu změny: Osm kroků úspěšné transformace podniku

v turbulentní ekonomice. Přel. H. Škapová. Praha: Management Press, 2000. ISBN 80-

7261-015-5.

[26] MALLYA, T. Základy strategického řízení a rozhodování. 1. vyd. Praha: Grada

Publishing, 2007. ISBN 978-80-247-1911-5.

[27] MEFFERT, H. Marketing Management. Přel. G. Tomek a V. Vávrová. Praha: Grada

Publishing, 1996. ISBN 80-7169-329-4.

[28] PARTHASARATHY, S. Business Strategy. Financial Management. [online]. 2011,

červen, s. 32-33. ISSN 1471-9185. [cit. 2013-02-03]. Dostupný na WWW:

<http://search.proquest.com/docview/522843459>

[29] SANDER, G., BAUER, E. Strategieentwicklung kurz und klar: Das Handbuch für Non-

Profit-Organisationen. Bern: Haupt, 2006. ISBN 978-3-258-07002-5.

19

[30] SEDLÁČKOVÁ, H., BUCHTA, K. Strategická analýza. Praha: C.H. Beck, 2006. ISBN 80-

7179-367-1.

[31] SIMON, W. Kursbuch Strategieentwicklung: Analyse – Planung – Umsetzung.

München: Redline Wirtschaft, 2008. ISBN 978-3-636-01542-6.

20

3 STRATEGIC ANALYSIS OF THE COMPANY

SURROUNDING ENVIRONMENT

Study time

The approximate total time recommended to study the following chapter is app. 4 hours.

Objective

After studying this charter, you will be able to

define the elements of company surrounding environment

understand the essence of the performance of a strategic analysis of company surrounding environment

describe the most important aspects of the impact of the surrounding environment on the company and its strategic management

define the individual factors of PEST analysis

Explication

3.1 STRATEGIC ANALYSIS

Strategic analysis is an integral and very important part of the process of strategic

management. The preparation of a high-quality strategic analysis requires creative strategic thinking.

This is beneficial, because the strategic analysis will adequately prepare the company for

unpredictable changes that may occur in its surrounding environment in the future.

According to Sedláčková, the central objective of strategic analysis is: "to identify, analyze

and evaluate all the relevant the factors, which may be expected to affect the final choice of the

company objectives and strategy." [13]

However, it is not enough to simply identify the individual factors in isolation, but they must

be seen as an interrelated system of factors that affect the company.

It is also necessary to estimate the possible development trends, and to try to forecast

especially any eventual negative effects on the company in the future and to prepare for them.

Anticipating the future plays a crucial role in strategic management, and hence in strategic analysis –

it is not sufficient to analyze the past, we need to proactively look for new opportunities in an effort

to outrun the competitors.

21

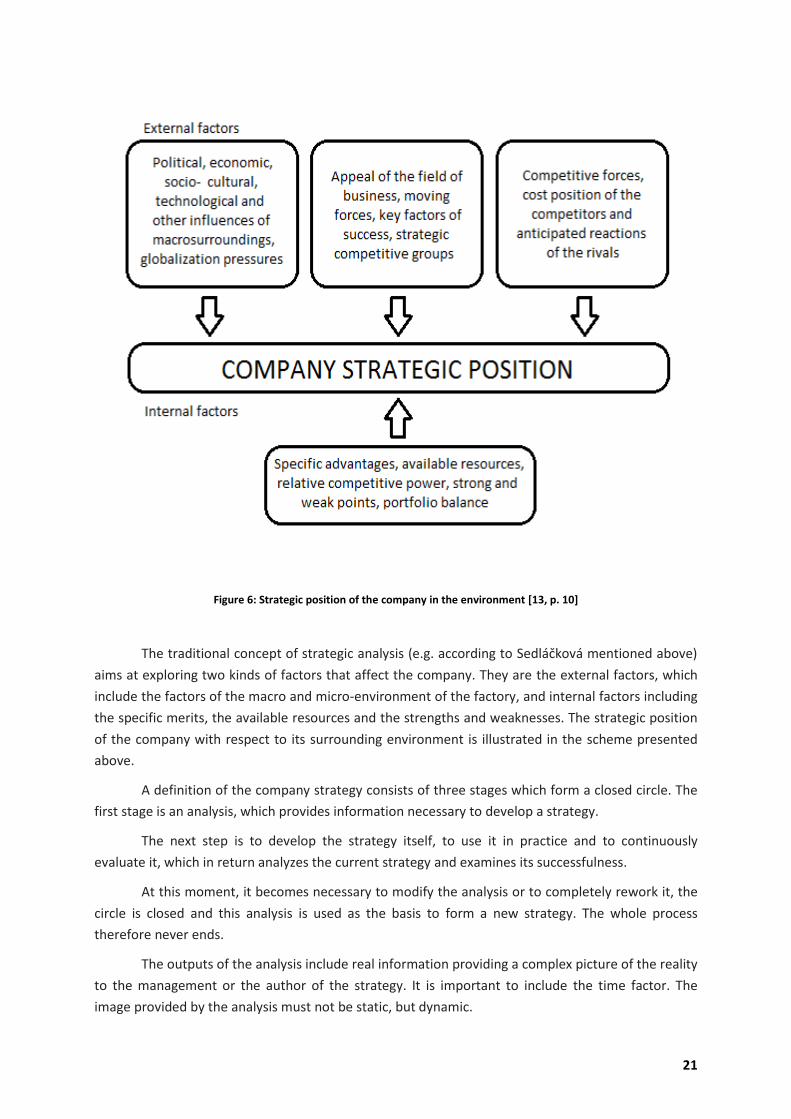

Figure 6: Strategic position of the company in the environment [13, p. 10]

The traditional concept of strategic analysis (e.g. according to Sedláčková mentioned above)

aims at exploring two kinds of factors that affect the company. They are the external factors, which

include the factors of the macro and micro-environment of the factory, and internal factors including

the specific merits, the available resources and the strengths and weaknesses. The strategic position

of the company with respect to its surrounding environment is illustrated in the scheme presented

above.

A definition of the company strategy consists of three stages which form a closed circle. The

first stage is an analysis, which provides information necessary to develop a strategy.

The next step is to develop the strategy itself, to use it in practice and to continuously

evaluate it, which in return analyzes the current strategy and examines its successfulness.

At this moment, it becomes necessary to modify the analysis or to completely rework it, the

circle is closed and this analysis is used as the basis to form a new strategy. The whole process

therefore never ends.

The outputs of the analysis include real information providing a complex picture of the reality

to the management or the author of the strategy. It is important to include the time factor. The

image provided by the analysis must not be static, but dynamic.

22

Monitoring data in time provides the authors of the strategy with the most powerful tool for

the prediction of the future development, which is essential for creating the analysis.

The attention when collecting data during the analysis is also focused on the opportunities

and threats. In principle, the objective is to find precisely the factors affecting the company on which

the subsequent strategy is built. A strategy is actually a way showing which situations should be

changed and how, in other words, positive information with a positive trend, no matter how pleasant

it is, cannot be used to build a new strategy, because there is nothing to change.

3.2 STRUCTURE OF COMPANY SURROUNDING ENVIRONMENT

An analysis of the company surrounding environment and a forecast of the future

development represent some of the basic starting points of strategy creation.

An analysis of the surrounding environment deals with the analysis and identification of the

factors in the company surrounding environment which influence and are likely to influence its

strategic position in the future, and create and will create potential opportunities and threats for its

activities.

A strategic analysis of the external environment is generally used to explore the environment

in which the company works, to identify the potential opportunities and threats arising from the

environment, and to obtain information important to forecast the subsequent developments in the

sector. [3]

The environment, or in other words the company surroundings, is further divided into

macro-environment and micro-environment, which is used, for example, by Sedláčková [13]

Grasseová [3] or Dedouchová [1], and also into general and sector surrounding environment, as it is

called by Keřkovský and Vykypěl [9 ], and these divisions are used to further identify the important

factors that affect the surrounding environment.

Macro-environment is defined as the surrounding environment which the company itself can

not influence but which has, more or less, influenced the demand. [1] These are the factors that are

common to all companies, not only in the market where the analyzed company operates, but in

other markets as well.

Macro-environment represents the overall economic, political, legal, social, technological,

demographic and international framework in which the company works. The basic property of

macro-environment is that the company (with some exceptions) is not able to change it.

The conditions of macro-environment are understood as the trends the company must be

aware of and predict, but it cannot influence them. The best-known analysis that examines the

macro-environment is the so-called PEST analysis.

Micro-environment (competitive surrounding environment) is defined by the sector or

sectors in which the company operates. The competitive surrounding environment includes all the

business entities that have direct ties with the company, both competitive and cooperative ones.

The most frequent groups that are subjected to the analysis are customers, suppliers and

competitors, both existing and potential.

23

The main characteristic of the competitive surrounding environment is the existence of

feedback – the business entities affect the company, but the company has the possibility of an active

response to these stimuli. The mutual ties may not only be studied and foreseen, but also created.

A traditional method used to analyze the competitive surrounding environment is the

Porter's five forces model. In the following parts of the text, we are also going to deal with the life-

cycle analysis and mapping of strategic groups in the sector. The analyses of the external

environment can take advantage of various methods and tools. In some cases, these tools and

methods overlap and it is therefore not necessary to use them all.

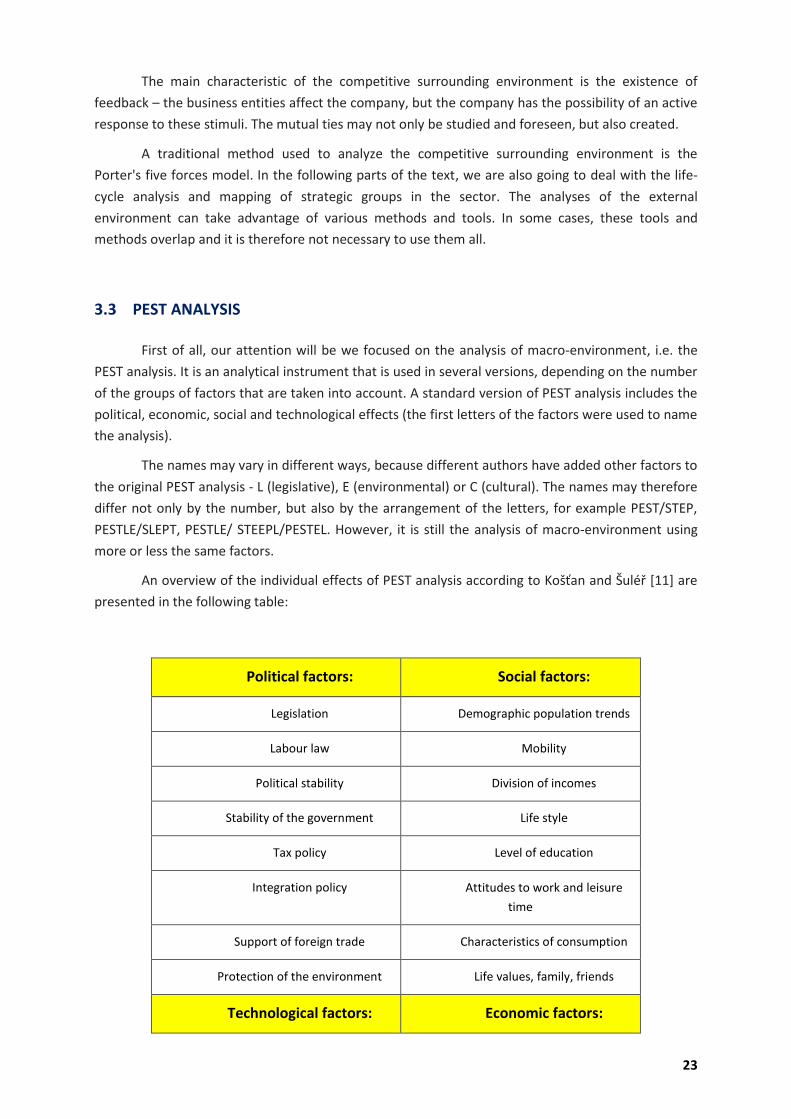

3.3 PEST ANALYSIS

First of all, our attention will be we focused on the analysis of macro-environment, i.e. the

PEST analysis. It is an analytical instrument that is used in several versions, depending on the number

of the groups of factors that are taken into account. A standard version of PEST analysis includes the

political, economic, social and technological effects (the first letters of the factors were used to name

the analysis).

The names may vary in different ways, because different authors have added other factors to

the original PEST analysis - L (legislative), E (environmental) or C (cultural). The names may therefore

differ not only by the number, but also by the arrangement of the letters, for example PEST/STEP,

PESTLE/SLEPT, PESTLE/ STEEPL/PESTEL. However, it is still the analysis of macro-environment using

more or less the same factors.

An overview of the individual effects of PEST analysis according to Košťan and Šuléř [11] are

presented in the following table:

Political factors: Social factors:

Legislation Demographic population trends

Labour law Mobility

Political stability Division of incomes

Stability of the government Life style

Tax policy Level of education

Integration policy Attitudes to work and leisure

time

Support of foreign trade Characteristics of consumption

Protection of the environment Life values, family, friends

Technological factors: Economic factors:

24

Level of expenditures on research GDP trend

Government support of research Interest rate

New technological activities and

their priority

Amount of money in circulation

General technological level Inflation

New discoveries and inventions Unemployment

Technological transfer rate Consumption

Rate of technological

obsolescence

Level of investments

Price and availability of energy

Tab. 2. Selected PEST analysis factors [11, p. 38]

The objective of PEST analysis is not an exhaustive list of the impacts from the macro-

environment of the company. It is important to distinguish the factors important for a concrete

company, i.e. to answer the following questions [8]:

What factors of the surrounding environment affect the organization?

Which of them are currently most important?

Which of them will be most important in the years to come?

After that, it is necessary to assess the impact of the key factors on the company and to try to take

them into consideration as much as you can when formulating the strategy.

Summary of terms

Strategic analysis of the external environment is generally used to explore the environment

in which the company operates, to identify the potential opportunities and threats arising from its

environment, and to obtain information relevant to forecasting the future development in the

sector.

The environment, or in other words the surroundings of the company is divided into its

macro-environment and micro-environment, while other experts divide environment into general

and sector.

Macro-environment represents the economic, political, legal, social, technological,

demographic and international framework in which the company operates.

25

The basic property of the macro-environment is that the company (with some exceptions) is

not able to change it. The conditions of the macro-environment are taken as trends which must be

known and predicted, but which cannot be affected. The best-known analysis that examines the

macro-environment is the so-called PEST analysis.

Micro-environment (competitive surroundings) is represented by the sector, respectively

sectors in which the company operates. The competitive surrounding environment therefore

includes all the business entities that have direct ties with the company, both competitive and

cooperative ones.

PEST analysis is an analytical tool that is used in several versions depending on the number

of the groups of factors that are involved.

Questions

1. Define the individual elements of the company surrounding environment.

2. Describe the most important aspects of the impact of the surrounding environment

on the company and try to determine how these aspects can affect the strategic

management of the company.

3. Explain what PEST analysis means.

Reference sources

[1] DEDOUCHOVÁ, M. Strategie podniku. 1. vydání. Praha: C. H. Beck, 2001. ISBN: 80-

7179-603-4.

[2] DVOŘÁČEK, J., SLUNČÍK, P. Podnik a jeho okolí. Jak přežít v konkurenčním prostředí?

1. vydání. Praha: C. H. Beck, 2012. ISBN 978-80-7400-224-3.

[3] GRASSEOVÁ, M., DUBEC, R., ŘEHÁK, D. Analýza v rukou manažera. 33

nejpoužívanějších metod strategického řízení. Praha: Computer Press, 2010. ISBN

978-80-251-2621-9.

[4] HORÁKOVÁ, H. Strategický marketing. 2. rozš. a aktual. vyd. Praha: Grada Publishing,

2003. ISBN 80-247-0447-1.

[5] CHARVÁT, J. Firemní strategie pro praxi. Praha: Grada, 2006. ISBN 80-247-1389-6.

[6] JAKUBÍKOVÁ, D. Strategický marketing. Praha: Grada Publishing. 2005. ISBN 80-245-

0902-4.

[7] JOHNSON, G., SCHOLES, K. Cesty k úspěšnému podniku. Praha: Computer Press,

2000. ISBN 8072262203.

[8] JOHNSON, G., SCHOLES, K. Exploring corporate strategy. 3rd edition. New York:

Prentice hall, 2008. ISBN 978-0-273-71192-6.

26

[9] KEŘKOVSKÝ, M., VYKYPĚL, O. Strategické řízení. Teorie pro praxi. 2. vydání. Praha: C.

H. Beck. 2006. ISBN: 80-7179-453-8.

[10] KONEČNÝ, M., MATUSIKOVÁ, L., LEDNICKÝ, V., WAGNEROVÁ, E. Strategický

management. Opava: Slezská univerzita v Opavě, Obchodně podnikatelská fakulta,

2007, ISBN 80-7248-049-9.

[11] KOŠŤAN, P., ŠULEŘ, O. Firemní strategie: plánování a realizace. Praha: Computer

Press, 2002. ISBN 80-7226-657-8.

[12] KOTLER, P. a kol. Moderní marketing. Přel. J. Langerová a V. Nový. 1. vyd. Praha:

Grada Publishing, 2007. ISBN 978-80-247-1545-2.

[13] SEDLÁČKOVÁ, H., BUCHTA, K. Strategická analýza. Praha: C.H. Beck, 2006. ISBN 80-

7179-367-1.

27

4 ANALYSIS OF THE COMPETITIVE SURROUNDING

ENVIRONMENT OF THE COMPANY

Study time

The approximate total time recommended to study the following chapter is app. 3.5 hours.

Objective

After studying this charter you will be able to:

define the elements of the competitive environment of the company choose a suitable strategy for analyzing the competitive environment of the

company analyze the market environment by means of Porter's five forces model use the method of competing group analysis clarify the use of the method of future development scenarios of the company

environment

Explication

4.1 PORTER'S FIVE FORCES MODEL

The five forces model was designed by M. E. Porter [10] as a tool used to examine the

competitive surrounding environment, which defines the conditions of the functioning and

development of the company in the given field. If the company is active in more fields, the analysis

should be performed for each field, i.e. for each strategic business unit.

The starting point for a competitive environment analysis is therefore a definition of the

field. According to Porter [10], a field is a sector of the industry involving the companies that

manufacture products or provide services of similar purpose and sell them in the market at the same

territory.

An official classification of the fields that are applied in the region can be used as a guide to

define the field. For example, there is the Standard Industrial Classification in the USA, in which every

field which has a four-digit code. A similar classification is used in the European Union. The Czech

Republic uses the so-called Classification of Economic Activities "CZ-NACE" which, with effect from 1

January 2008, replaced the Industrial Classification of Economic Activities (OKEČ).

28

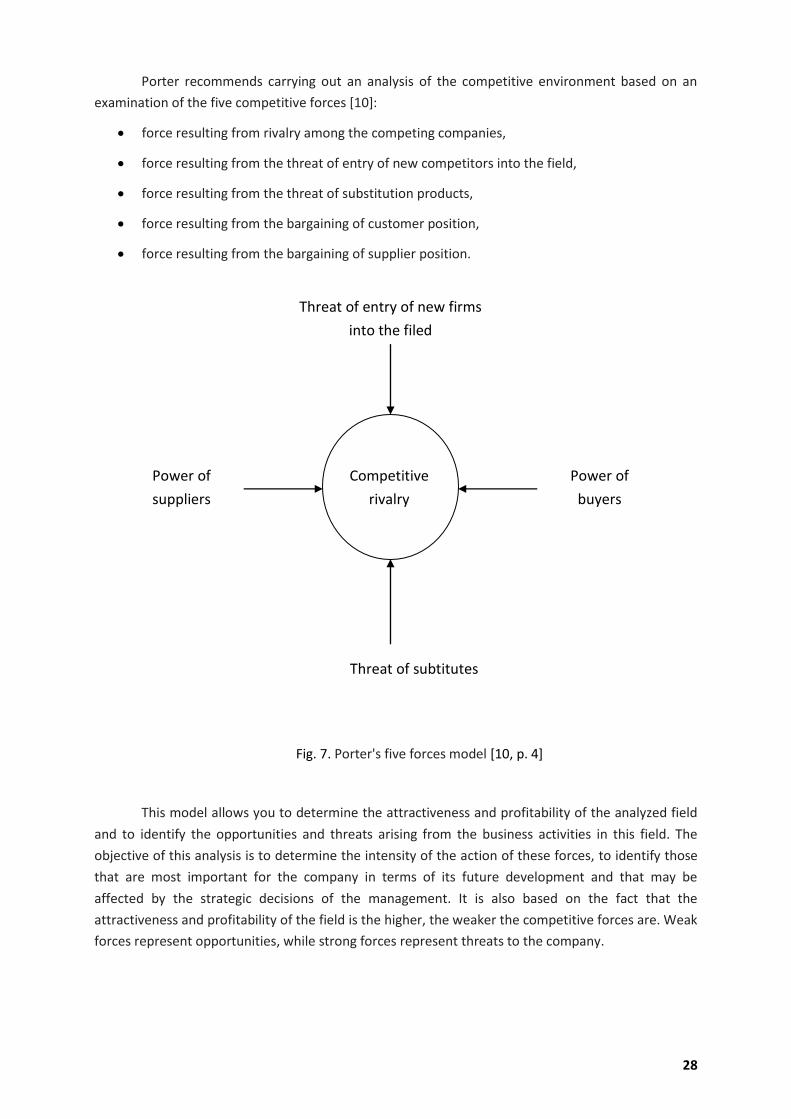

Porter recommends carrying out an analysis of the competitive environment based on an

examination of the five competitive forces [10]:

force resulting from rivalry among the competing companies,

force resulting from the threat of entry of new competitors into the field,

force resulting from the threat of substitution products,

force resulting from the bargaining of customer position,

force resulting from the bargaining of supplier position.

Fig. 7. Porter's five forces model [10, p. 4]

This model allows you to determine the attractiveness and profitability of the analyzed field

and to identify the opportunities and threats arising from the business activities in this field. The

objective of this analysis is to determine the intensity of the action of these forces, to identify those

that are most important for the company in terms of its future development and that may be

affected by the strategic decisions of the management. It is also based on the fact that the

attractiveness and profitability of the field is the higher, the weaker the competitive forces are. Weak

forces represent opportunities, while strong forces represent threats to the company.

Threat of entry of new firms

into the filed

Power of

buyers

Power of

suppliers

Threat of subtitutes

Competitive

rivalry

29

4.2 LIFE CYCLE ANALYSIS OF THE FIELD

A life cycle analysis of the field allows you to determine the future size of the examined field,

i.e. its prospects and the anticipated intensity of competitive rivalry.

This information is used by companies to select an appropriate strategy that will enable the

company to achieve the required level of profitability of its entrepreneurial activities.

A life cycle analysis of the field is based on the fact that the fields usually go through certain

evolutionary phases from its inception to its demise.

We usually distinguish four stages: introduction (birth), growth, maturity (adulthood) and

decline (aging):

Fig. 9 Life cycle of the field [7]

Each phase has different characteristics:

1. Introduction to the market - this stage is characterized by low profits or even losses. The

company is spending quite a lot on advertising and sales. The level of sales is low because the

products of this field are bought by a relatively small group of customers looking for "new

things".

2. Growth of sales - in this stage, the demand for the products in this field starts growing rapidly.

The rate of sales is high and continues to grow. Due to the increasing production, the fixed costs

are spread over a higher and higher number of units. Profits reach their highest values. However,

the number of competitors who are attracted by the attractive market is increasing. They invest

into further product innovation.

3. Maturity – the sales growth rate is lower and lower, the innovative customers begin to look for

new products. A typical feature in this stage is the occurrence of intense competition, which is

caused by the fact that there are many similar products on the market. Weaker competitors are

gradually edged out of the market. Costs at this stage tend to grow, which, in connection with

price pressure, leads to a profit decrease.

Sales

Profit

Č

as

Sales

Z

isk

Introduction

(birth)

Growth Maturity

(adulthood

)

Decline

(aging)

30

4. Decrease of sales - at this stage, sales are falling rapidly, thanks to market saturation and the

emergence of better products to meet the same need. The unit costs are rising due to production

cuts.

4.3 COMPETING GROUP ANALYSIS

A competing group analysis, designed by Porter [10], is a method analyzing the internal

structure of competition in the field. In its traditional form, competition in the market is based on the

rivalry of all companies with one another.

The concept of competing groups, however, is based on the assumption that competition

takes place only inside the so-called competing group. A competing group is defined by certain

characteristics that separate the individual companies from each other in the field. The commonly

used characteristics are:

assortment range,

quality of products,

price of products,

type of customers.

The outcome of this analysis is the determination of the competitors the company should

take into consideration most when formulating its strategy. On the other hand, the company can

establish cooperation with companies belonging to other competing groups in order to build

significant and long-term competitive advantages.

4.4. FUTURE DEVELOPMENT SCENARIOS OF THE COMPANY SURROUNDING

ENVIRONMENT

To create an effective strategy, it is necessary to predict the future development of the

company surrounding environment (business environment). At present, however, the company

surrounding environment has been changing very quickly.

There are also frequent events that are difficult to predict during the formulation of a

strategy.

In such a situation, it is not possible for the company to rely on one (most probable) forecast

of the future development of the environment. The starting point is the concept of the creation of

scenarios.

Scenarios are defined as descriptions of possible states of the future development of the

company surrounding environment. The concept of the creation of scenarios is based on the creation

of several scenarios of the surrounding environment development and a preparation of various

strategy options for each of them.

31

During the execution of the strategy, it is possible to flexibly switch between the prepared

strategy versions according to the actual development of the company surrounding environment.

The concept of the creation of scenarios is a way that can help companies to effectively protect the

company against unexpected changes in the business environment.

Summary of terms

The five forces model was designed by M. E. Porter as a tool for examining the competitive

surrounding environment, which defines the conditions for the functioning and development of the

company in the field.

The competing environment analysis, according to Porter, is performed on the basis of an

examination of five competitive forces:

force resulting from the rivalry among competing companies,

force resulting from the threat of entry of new competitors into the field,

force resulting from the threat of substitution products,

force resulting from the customer bargaining position,

force resulting from the supplier bargaining position.

Life cycle analysis of the field allows you to determine the future size of the examined field,

i.e. its prospects and the anticipated intensity of competitive rivalry.

The information is used by companies to select an appropriate strategy that will enable them

to achieve the required level of business profitability.

Life cycle analysis of the field is based on the fact that the fields usually go through certain

evolutionary phases from their inception to their demise, and we usually distinguish four phases:

introduction (birth), growth, maturity (adulthood) and decline (aging).

A competing group analysis, designed by Porter, is a method analyzing the internal

structure of the competition in the field. The concept of competing groups, however, is based on

the assumption that competition takes place only inside of the so-called competing group.

A competing group is defined by certain characteristics that separate the individual

companies from each other in the field:

assortment range,

quality of products,

price of products,

type of customers.

32

The scenarios of the future development of the company surrounding environment are

defined as descriptions of the possible states of the future development of the company surrounding

environment. This concept is based on the creation of several scenarios of the surrounding

environment development and a preparation of various strategy options for each of them.

During the execution of the strategy, it is possible to flexibly switch between the prepared

strategy versions, according to the actual development of the company surrounding environment.

The concept of the creation of scenarios is a way that can help companies to effectively protect the

company against unexpected changes in the business environment.

Questions

Explain why it is necessary to analyze the competing company environment and provide concrete practical examples.

Define the elements of competing environment of the company.

Explain what evidence a company can use to choose a suitable strategy to analyse the competing company environment.

Explain what factors the company must analyze if it decides to carry out an analysis of the company market environment by means of Porter's five forces model.

When is the method of the analysis of competing groups used in practice?

Explain what the method of future development scenarios of the company surrounding environment is used for and provide concrete practical examples.

Reference sources

[1] DEDOUCHOVÁ, M. Strategie podniku. Praha: C. H. Beck, 2001. ISBN 80-7179-603-4.

[2] FOTR, J., SOUČEK, I. Podnikatelský záměr a investiční rozhodování. Praha: Grada

Publishing, 2005. ISBN 80-247-0939-2.

[3] GIERSZEWSKA, G., ROMANOWSKA, M. Analiza strategiczna przedsiębiorstwa.

Warszawa: Polskie Wydawnictwo Ekonomiczne, 1997.

[4] GÜNTHER, H. O., TEMPELMEIER, H. Produktion und Logistik. Berlin: Springer Verlag,

1995.

[5] HANZELKOVÁ, A., KEŘKOVSKÝ, M, ODEHNALOVÁ, D. a VYKYPĚL, O. Strategický

marketing, Teorie pro praxi, 1. vydání. Praha: C. H. Beck, 2009, ISBN 978-80-7400-

120-8.

33

[6] HARRISON, J. S., JOHN, C. H. Foundations in Strategic Management. South-Western

Thomson Corporation, 2004. ISBN 0-324-25917-4.

[7] KEŘKOVSKÝ, M., VYKYPĚL, O. Strategické řízení. Teorie pro praxi. 2. vydání. Praha: C.

H. Beck. 2006. ISBN: 80-7179-453-8.

[8] MANKIW, N., SOJKA, M. Zásady ekonomie. Praha: Grada, 1999. ISBN 80-7169-891-

1.

[9] MEFFERT, H. Marketing Management. Přel. G. Tomek a V. Vávrová. Praha: Grada

Publishing, 1996. ISBN 80-7169-329-4.

[10] PORTER, M. Konkurenční strategie: Metody pro analýzu odvětví a konkurentů.

Praha: VICTORIA PUBLISHING, 1994. ISBN 80-95605-11-2.

[11] SEDLÁČKOVÁ, H., BUCHTA, K. Strategická analýza. Praha: C.H. Beck, 2006. ISBN 80-7179-367-1.

[12] ŠTRACH, P. Mezinárodní management. Praha: Grada Publishing, 2009. ISBN 978-80-247-2987-9.

[13] TOMEK G., VÁVROVÁ V. Jak zvýšit konkurenční schopnost firmy. 1. vyd. Praha: C. H. Beck, 2009. ISBN 978-80-7400-098-0.

[14] VEBER, J. Management: základy, prosperita, globalizace. Praha: Management Press, 2000. ISBN 8072610295.

[15] ZADRAŽILOVÁ, D. IN: PRAŽSKÁ, L., JINDRA, J. Obchodní podnikání. Management Press 1997. ISBN: 80-7261-059-7.

34

5 ANALYSIS OF THE COMPANY INTERNAL POTENTIAL

Study time

The approximate total time recommended to study the following chapter is app. 4.5 hours.

Objective

After studying this charter you will be able to:

define the individual analyses of the company internal potential describe and use the analysis of key competencies define the term benchmarking clarify the objective of benchmarking and divide it according to different criteria explain the essence of analysis of value chain

Explication

5.1 ANALYSIS OF KEY COMPETENCIES

An analysis of the key competencies is a method used to analyse the competitiveness

(competitive positions) of the company through an analysis of selected resources and skills of the

company. It is therefore based on the assumption that it is not necessary to examine the resources

and skills of the company in all its subsystems and functions. It is sufficient to limit it to those that

have a decisive impact on the competitiveness within the sector. Such resources and skills are

referred as the key competencies to by Hamel and Prahalad [4].

The key competencies are different in every field. For example, in the brewing industry, they

include the traditional brewing technologies, developed distribution network and effective

advertising [16]. It is important for the company to make the key skills its strengths. Then, it will be

competitive in the given field.

5.2. ANALYSIS OF THE VALUE CHAIN

Each company represents a set of activities whose purpose is to design, produce, sell in the

market, deliver and support its product. All these activities can be illustrated using the value chain.

Each organization has its own specific value chain. According to Porter [10, 11, 12], the

differences between the value chains of organizations and their performances are a key source of

competitive advantage.

35

Norton and Kaplan [6] highlight the value chain in their Balanced Scorecard concept as one

of the factors affecting the value for customers (BSC customer perspective) and the value for owners

(BSC financial perspective).

Tomek and Vávrová [19] say: ,,partnership relationship at every level of the value chain,

friendly relationship with customers, suppliers and other parties cooperating within the value chain is

a key element in improving the competitiveness in a production company".

The process view of the company expressed by its value chain is an important prerequisite

for performance management of the company. The knowledge of the value-creating processes, their

analyses and management lead to the identification of the factors affecting the company

performance.

Value chain characteristics

The process view of companies was first introduced by Michael Porter in 1985 in his book

Competitive Advantage, and it was in the form of the so-called value chain. Porter uses this chain to

analyse the sources of competitive advantages of individual companies and places them in a value

system that shows how the individual value chains concur, from supply chains to distribution ones

which enter into the value chains of the buyers.

Porter [10, 12] characterizes the value chain as a division of the company into its strategically

important activities in such a way to make it possible to understand the behaviour of costs and to

recognize the existing and potential sources of differentiation. Porter adds: ,,by doing these

strategically important activities cheaper and better than its competitors, the company will gain a

competitive advantage".

Robbins and Coulter [14] define the value chain as a set of working activities which add value

step by step, starting with the processing of materials and ending with the finished product in the

hands of the user.

According to Feller et al. [2], the concept of the value chain is based on the division of the

company (organization) into conceptually different activities according to the business plan. Feller

says: ,,Through the execution of these activities, the company creates a value the buyers are willing to

pay for. If the value exceeds the cost incurred by all of the executed activities, then the enterprise is

profitable".

According to Porter [10] Feller et al. [2], the value chain shows the total value and consists of

the value-creating activities and the margin. The value-creating activities of the organization create a

product or a service having certain value for the buyers. A margin is the difference between the total

value and the total costs incurred to carry out the necessary value-creating activities.

Tichá and Hron [17] highlight the focus of the value chain on perceived value, respectively

value defined by the customer. Such an approach offers a consistent way of evaluation of company

activities and shows that everything in the company can be controlled in order to increase the

company potential to create value.

The weakness of the concept of the value chain, as seen by the authors [17], is that the

model does not describe the interconnectedness of the individual activities and the consequences of

this mutual interconnectedness.

36

5.3. BENCHMARKING

A variety of new initiatives in the field of improvement and innovation, new business

philosophies, approaches and methodologies of management, whose main objective is to

ensure permanent competitiveness by means of effective satisfaction of the requirements of

the customers with the smallest possible consumption of resources, have been developed as

a result of intensifying competition. As shown by foreign experience and many researches,

the best tool based on sharing of knowledge and good practices is benchmarking.

The basic term of benchmarking is the English word "benchmark", which comes from

geographical research and means "measurement compared to a reference point". For the

area of quality improvement, the word "benchmark" means achieving the "best-in-class"

level, which makes it the "reference point" and the standard of excellence in comparison

with similar procedures or processes that are measured and compared. It can also be seen

as the measure or indicator of performance we would like to be inspired by. [8]

The basic objective of benchmarking is a comparison and subsequent

implementation of the improvements in processes, strategies, and performance. It is a

constantly ongoing process, whose objective is to identify the best practices within the

organization, and whose purpose is to achieve higher efficiency of the compared processes

in the organization. The outcome of this method is very closely linked to the quantity,

quality, and relevance of the current and historical available data.

Summary of terms

Analysis of key competencies is a method used to analyse the competitiveness (competitive

position) of the company through an analysis of selected resources and skills of the company.

Key competencies are different in every field. It is important for companies to make sure the

key skills are their strengths. Then, they will be competitive in the field.

Each enterprise is a set of activities whose purpose is to design, produce, sell in the market,

deliver and support its product. All these activities can be illustrated using a value chain.

Each organization has its own specific value chain. According to the Balanced Scorecard

concept, value chain is one of the factors influencing the value for customers (BSC customer

perspective) and the value for owners (BSC financial perspective).

Benchmarking is a technique in which the organizations measure their performances in

comparison with organizations that represent the world leaders, they learn how these organizations

have achieved the world performance, and they use the gathered information to improve their own

performances.

37

Benchmarking is a long continuous process of mutual monitoring and comparison of the

results of the company with the results of the competitors in terms of the quality and production

efficiency of certain product, or the execution of certain service, manufacturing processes, work

operations, marketing activities, ... it is based on the selection and comparison of suitable ideas,

methods or approaches that are applicable for the enterprise in question in order to improve its own

performance, efficiency or quality.

Questions

What analyses of the internal potential of the company do you know and what are these analyzes used for in practice?

Describe the essence of the analysis of key competencies. Where would you use it in practice?

Try to define the concept of benchmarking.

Explain what benchmarking is used for.

Divide the benchmarking process according to various criteria.

Explain the principle of value chain analysis.

Reference sources